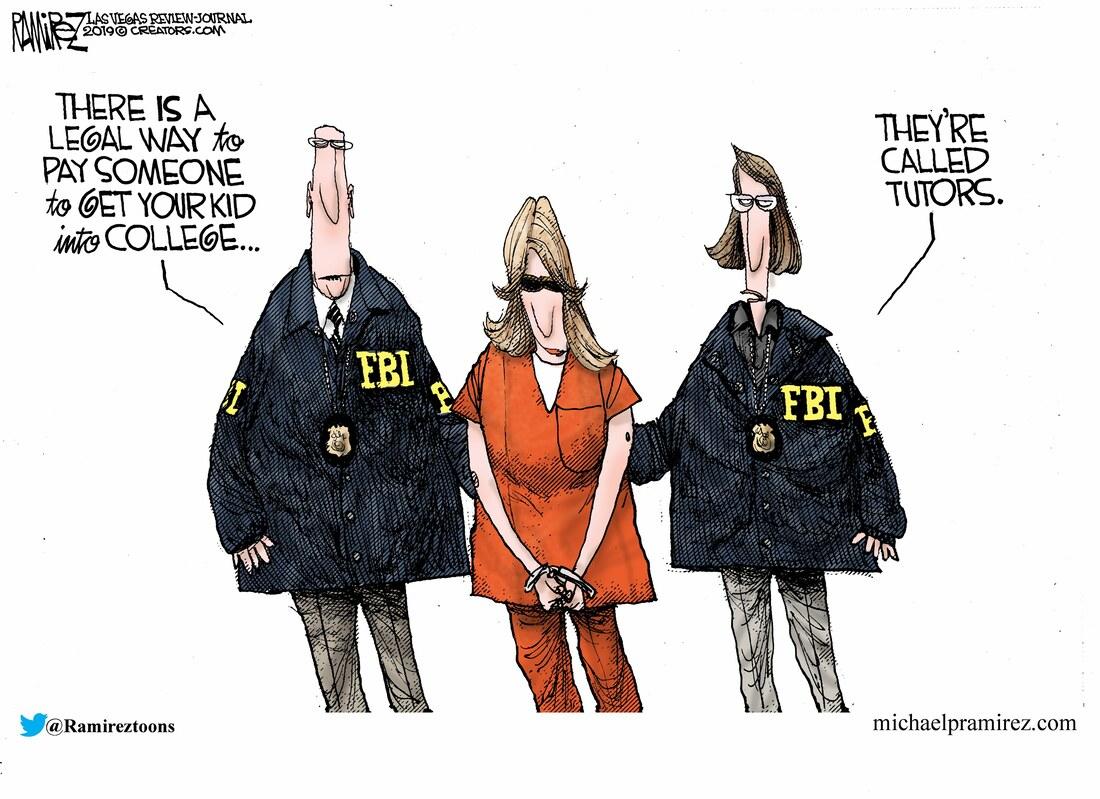

Is there anything left in this country that has not been deeply tainted by corruption?

By now you have probably heard that dozens of people have been arrested for participating in a multi-million dollar college admissions scam. Enormous amounts of money were paid out in order to ensure that children from very wealthy families were able to get into top schools such as Yale University, Stanford University, the University of Texas and the University of Southern California. We should certainly be disgusted by these revelations, but we shouldn’t be surprised. Such corruption happens every single day on every single level of society in America. At this point our nation is so far gone that it is shocking when you run into someone that actually still has some integrity.

The “mastermind” behind this college admissions scam was a con man named William Rick Singer. He had been successfully getting the kids of wealthy people into top colleges for years using “side doors”, and he probably thought that he would never get caught.

But he did.

There were four basic methods that Singer used to get children from wealthy families into elite schools. The first two methods involved bribes…

Bribing college entrance exam administrators to allow a third party to facilitate cheating on college entrance exams, in some cases by posing as actual students,’ is the first.

Bribing university athletic coaches and administrators to designate applicants as purported athletic recruits – regardless of their athletic abilities, and in some cases, even though they did not play the sport,’ is the second.

Because many of these kids didn’t even play the sports they were being “recruited” for, in some cases Photoshop was used to paste their faces on to the bodies of real athletes…

In order to get non-athletic kids admitted to college as athletes, Singer often had to create fake profiles for them. Sometimes this involved fabricating resumes that listed them having played on elite club teams, but to finish the illusion Singer and his team would also use Photoshop to combine photos of the kids with actual athletes in the sport.

A number of college coaches became exceedingly wealthy from taking bribes to “recruit” kids that would never play once they got to school, but now a lot of those same coaches are probably going to prison.

‘Having a third party take classes in place of the actual students, with the understanding that the grades earned in those classes would be submitted as part of the students’ application,’ is the third.

The fourth was ‘submitting falsified applications for admission to universities … that, among other things, included the fraudulently obtained exam scores and class grades, and often listed fake awards and athletic activities.’

Of course the main thing that the media is focusing on is the fact that some celebrities are among those being charged in this case, and that includes Lori Loughlin from “Full House”…

It was important to “Full House” star Lori Loughlin that her kids have “the college experience” that she missed out on, she said back in 2016.

Loughlin, along with “Desperate Housewives” actress Felicity Huffman, is among those charged in a scheme in which parents allegedly bribed college coaches and insiders at testing centers to help get their children into some of the most elite schools in the country, federal prosecutors said Tuesday.

Despite how cynical I have become lately, I never would have guessed that Lori Loughlin was capable of such corruption.

After all, she seems like such a nice lady on television.

But apparently she was extremely determined to make sure that her daughters had “the college experience”, and so Loughlin and her husband shelled out half a million dollars in bribes…

Loughlin and Giannulli ‘agreed to pay bribes totaling $500,000 in exchange for having their two daughters designated as recruits to the USC crew team – despite the fact that they did not participate in crew – thereby facilitating their admission to USC,’ according to the documents.

As bad as this scandal is, can we really say that it is much worse than what is going on around the rest of the country every single day?

Of course not.

We are a very sick nation, and we are getting sicker by the day.

William Rick Singer had a good con going, and he should have stopped while he was ahead…

“This book is full of secrets,” he said in Chapter 1 before dispensing advice on personal branding, test-taking and college essays.

But Singer had even bigger secrets, and those would cost up to $1.2 million.

But like most con men, Singer just had to keep pushing the envelope, and in the end it is going to cost him everything.

The ironic thing is that our colleges and universities are pulling an even bigger con. They have convinced all of us that a college education is the key to a bright future, but meanwhile the quality of the “education” that they are providing has deteriorated dramatically. I spent eight years in school getting three degrees, and so I know what I am talking about. For much more on all this, please see my recent article entitled “50 Actual College Course Titles That Prove That America’s Universities Are Training Our College Students To Be Socialists”.

I know that it is not fashionable to talk about “morality” and “values” these days, but the truth is that history has shown us that any nation that is deeply corrupt is not likely to survive for very long.

Avarice, ambition, revenge and licentiousness would break the strongest cords of our Constitution, as a whale goes through a net. Our Constitution was made only for a moral and religious people. It is wholly inadequate to the government of any other.

Today, we are neither moral or religious.

What we are is deeply corrupt, and America will not survive if we keep going down this path.

via ZeroHedge News https://ift.tt/2Cmnolc Tyler Durden

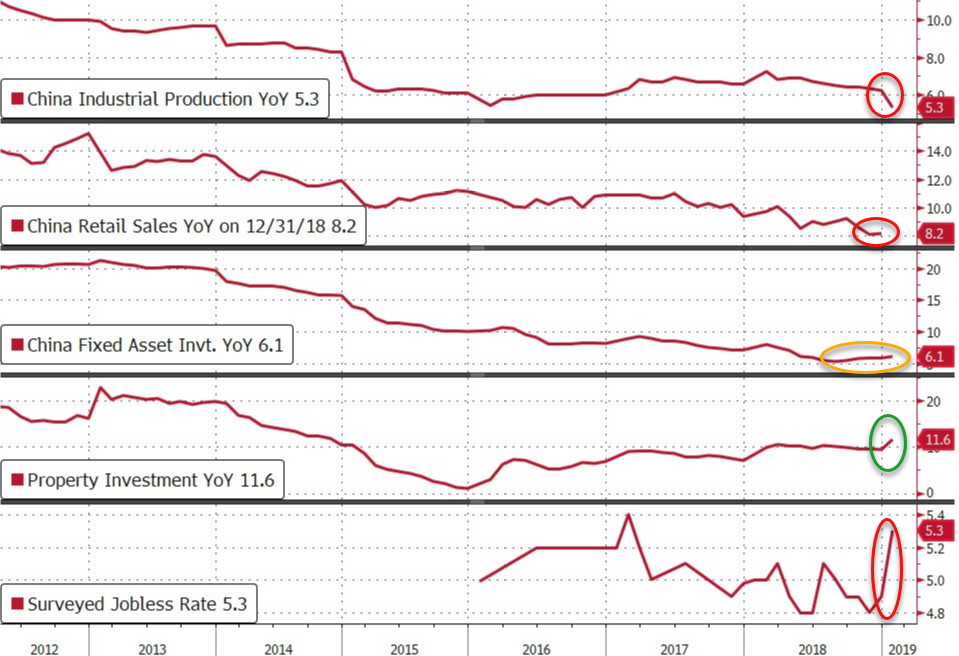

Having risen to session highs on the back of fresh global optimism over trade, a delay in Brexit and fresh hopes for a “goldilocks” economy (while ignoring China’s worst Industrial Production print on record), US equity futures slumped on Thursday as America and China were reportedly set to push back a key meeting on trade. European stocks trimmed an advance on the news, but remained higher while the pound fell as the Brexit saga rumbled on.

Following the meeting delay report, S&P futures tumbled from a loss to a gain while Treasuries pared a drop, the dollar gained and the yuan dropped.

Major European indices remained in positive territory, initially following the positive sentiment on Wall Street where the S&P 500 finished at a 5-month high and above the key 2800 level, although indices have since fallen off sharply from session highs following the previously noted report that the meeting between US President Trump and Chinese Premier Xi is delayed to at least April. European miners fell with the Stoxx Europe 600 basic resources index sliding as much as 0.8%, as metals slide on the weak Chinese industrial data reported overnight, and after the U.S. and China were said to push back a key meeting on trade. Chinese economic data published this morning are “putting the brakes on the rise in metals prices,” Commerzbank analysts wrote: “China’s industrial production has lost momentum more significantly than expected. Although fixed-asset investments increased slightly, they remain at a low level.”

Earlier, Asian stocks were initially higher across the as the region took early impetus from the US, where sentiment was underpinned by favorable data and a pre-quad witching surge, although the risk tone was eventually clouded as participants digested another round of disappointing Chinese data.

As noted last night, this is how China’s February’s data dump looked like:

China Industrial Production YoY MISS +5.3% vs +5.6% exp and +6.2% prior

China Retail Sales YoY MEET +8.2% vs +8.2% exp and +9.0% prior

China Fixed Asset Investment YoY MEET +6.1% vs +6.1% exp and +5.9% prior

China Property Investment YoY BEAT +11.6% vs +9.5% prior

China Surveyed Jobless Rate WEAKER 5.3% vs 4.9% prior

This was the weakest Industrial Production growth since March 2009 and Retail Sales growth was hovering near its weakest since May 2003. But perhaps the most worrisome for Chinese officials is the surge in the surveyed jobless rate to 5.3%, the highest since Feb 2017. Elsewhere, the ASX 200 and Nikkei 225 was unchanged with energy the outperformer in Australia after oil prices hit their best levels since November, while SoftBank shares were among the top gainers in the Japanese benchmark after reports it is in discussions regarding a USD 1bln investment into Uber’s self-driving unit. Chinese markets instigated a turnaround but with the downside in the Hang Seng (+0.1%) limited by notable strength seen in China’s oil majors and as China Unicom rallied post-earnings, while Shanghai Comp. (-1.2%) underperformed and fell below the 3000 level following mixed data with Retail Sales inline with expectations and Industrial Production at a 17-year low.

Emerging-market currencies and shares edged lower.

Summarizing recent price action, Bloomberg notes that investors have a lot to grapple with just now. U.S. stocks have extended gains this week as economic data comes in neither too hot nor too cold, while traders in Europe on Thursday seemed to be shrugging off more warning signs from the region – perhaps because of hopes Brexit can be delayed or derailed. Figures suggesting China’s slowdown deepened in the first two months of the year added to reasons for caution following this quarter’s rebound in Asian shares.

In geopolitical news, the US announced plans to test-launch missiles later this year after President Trump recently pulled out of the Nuclear Force Treaty. Separately, the US Senate voted 54-46 to end US support for the Saudi-led war in Yemen.

In FX, the Bloomberg Dollar Spot Index snapped four days of declines as Treasury yields edged higher. The pound fell ahead of another vote in the U.K. House of Commons where lawmakers will decide on whether to delay Brexit. The yen fell the most in two weeks and, falling against all G-10 peers, as traders positioned themselves ahead of the Bank of Japan’s policy decision on Friday, with some speculation that the central bank may turn slightly more dovish. Australian and New Zealand dollars slid after downbeat China data combined with falling short-end rates weighing on sentiment.

European sovereign debt was mixed as Germany said the economy likely to grow moderately in first quarter.

Elsewhere, oil prices slipped after touching a four-month high following reports that a Trump-Xi summit may be delayed until April vs. prior expectations of an end-March summit. As such WTI and Brent futures fell back into their respective one-month long range of around USD 3.50/bbl. This summit push-back has however been touted for a while as USTR Lighthizer recently noted that sticking points remain in talks

Expected data include jobless claims and new home sales. Dollar General, Adobe, Broadcom and Oracle are among companies reporting earnings.

Market Snapshot

S&P 500 futures up 0.1% to 2,822.75

STOXX Europe 600 up 0.4% to 377.02

MXAP down 0.3% to 157.79

MXAPJ down 0.2% to 521.60

Nikkei down 0.02% to 21,287.02

Topix down 0.2% to 1,588.29

Hang Seng Index up 0.2% to 28,851.39

Shanghai Composite down 1.2% to 2,990.69

Sensex down 0.06% to 37,731.10

Australia S&P/ASX 200 up 0.3% to 6,179.59

Kospi up 0.3% to 2,155.68

German 10Y yield rose 2.3 bps to 0.088%

Euro up 0.01% to $1.1328

Italian 10Y yield rose 1.2 bps to 2.197%

Spanish 10Y yield fell 0.2 bps to 1.186%

Brent futures up 0.8% to $68.09/bbl

Gold spot down 0.5% to $1,302.26

U.S. Dollar Index up 0.1% to 96.65

Top Overnight News from Bloomberg

The pound climbed to its highest level since June after Parliament on Wednesday evening rejected leaving the EU after 46 years without an agreement in place to keep trade flowing. Legislators will now vote on a postponement to the current March 29 deadline

A gauge of trader positioning from Citigroup Inc. shows short bets on sterling at their highest levels since December and the bearish wagers are set to rise even further, according to market participants

China’s economic slowdown deepened in the first two months of the year as industrial output rose 5.3 percent from a year earlier, versus 5.6 percent forecast by economists

Gary Cohn, the former head of President Donald Trump’s National Economic Council, said the U.S. is “desperate right now” for a trade pact with China as negotiators from both countries seek to reach a deal

U.K. derivatives clearing houses would face tighter post-Brexit scrutiny from European Union regulators if they want to keep doing business in the bloc under an agreement announced by EU negotiators on Wednesday

Royal Institution of Chartered Surveyors said its headline price index fell for a fifth month in February, dropping to the lowest level since 2011, as uncertainty caused both buyers and sellers to hold off on property deals in the U.K.

Oil held its advance to the highest level this year as a decline in U.S. crude and fuel stockpiles added to evidence of a tightening market

A delay to Brexit this week may be better than the alternatives, but that’s cold comfort for the U.K. economy. While a vote Thursday is likely to buy time for an orderly divorce, that would hurt, too, by prolonging the uncertainty for businesses and consumers

Data showed that China’s economic slowdown deepened with industrial output having its worst start to a year since 2009 and retail sales expanding at the slowest pace since 2012; the unemployment rate jumped to 5.3% in February from 4.9% in December, the highest level in two years. On the upside, fixed-asset investment accelerated and property investment jumped

Asian stocks were initially higher across the as the region took early impetus from the US, where sentiment was underpinned by favourable data. This saw all US major indices finish positive with the S&P 500 at a 4-month high and in turn spurred the momentum in Asia, although the risk tone was eventually clouded as participants digested Chinese data. ASX 200 (+0.3%) and Nikkei 225 (U/C) both gained at the open with energy the outperformer in Australia after oil prices hit their best levels since November, while SoftBank shares were among the top gainers in the Japanese benchmark after reports it is in discussions regarding a USD 1bln investment into Uber’s self-driving unit. Chinese markets instigated a turnaround but with the downside in the Hang Seng (+0.1%) limited by notable strength seen in China’s oil majors and as China Unicom rallied post-earnings, while Shanghai Comp. (-1.2%) underperformed and fell below the 3000 level following mixed data with Retail Sales inline with expectations and Industrial Production at a 17-year low. Finally, 10yr JGBs were lacklustre amid upside in Tokyo stocks and as the BoJ began its 2-day policy meeting, although there was a different picture in the longer-end as both 20yr and 30yr JGB yields fell to November 2016 lows.

Top Asian News

China Insiders Are Selling Stakes After Mammoth Equity Rally

Hedge Fund Sees China’s Distressed Debt Generating Juicy Returns

UBS Said Fined About $48 Million Over Work on Hong Kong IPOs

StanChart Loses Two Top India Bankers Amid Turn-Around Efforts

Major European indices are in positive territory [Euro Stoxx 50 +0.2%] initially following the positive sentiment on Wall Street where the S&P 500 finished at a 5-month high and above the key 2800 level; although indices have fallen off sharply off of session highs following reports that the meeting between US President Trump and Chinese Premier Xi is delayed to at least April. While this has been seen as a potential outcome for a while markets were still taken by surprise hence the significant drop from session high. Sectors have strengthened throughout the session to all being firmly in the green, after a somewhat mixed start to the session for sectors; with IT names the initial notable laggard. Notable movers include K+S Group (+7.3%) at the top of the Stoxx 600 after their FY18 EBITDA beat on expectations, alongside the Co. presenting strong EBITDA guidance for 2019. At the bottom of the Stoxx 600 are Lufthansa (-5.3%) after the Co. cut its growth plans as higher fuel costs weighed on earnings. Elsewhere, RWE (+0.3%) shares have been volatile since opening lower by around 2% after the Co. posted earnings below expectations, the turnaround in shares may be due to the Co. stating that they are confident the timetable for a E.ON (-0.1%) deal can be adhered to, after highlighting a potential delay to it in the event of a hard Brexit.

Top European News

Keep Hedging for U.K. Downside Risks, UBS Wealth Says

Short Bets on Pound Jump to Most This Year on Brexit Chaos

Brexit Impasse Sees U.K. Property Price Index Drop to 7-Year Low

Ifo Institute Slashes Forecast for German 2019 Growth to 0.6%

In FX, there was some respite for the Dollar and index after Wednesday’s relatively sharp sell-off, as the steeper reversal from recent 97.000+ highs stopped at the 96.371 level that coincides with technical support on some charts. However, the rebound was at least partly if not mainly due to external factors with several major counterparts undermined bearish impulses or running out of bullish momentum in the case of Sterling. The DXY is just shy of a recovery high inches above 96.750, and the 30 DMA at 96.602 could be key in terms of a firmer rebound or fade before another leg down towards the next downside technical level ahead of 96.000, which comes in at 96.283.

AUD/NZD/GBP/JPY – It’s a 4-horse race to avoid being last G10 currency to Thursday’s (EU session) finishing post, as the Aussie is undermined by data again, albeit Chinese this time rather than domestic, and fresh reports about a delay to the eagerly awaited Trump-Xi Summit to sign off a trade pact. Aud/Usd has slipped back further from near 0.7100 at one stage to 0.7050 and the Kiwi in sympathy with Nzd/Usd now around 0.6817 vs 0.6865 at best. Meanwhile, the Pound has pulled back following another Brexit-related spurt that catapulted Cable to circa 1.3340 before a retreat through 1.3300 to 1.3250. Sterling got an extra boost from the 2nd UK Parliamentary vote this week that saw a no deal in any guise rejected by MPs, in principle at least. Attention now turns to an extension of the March 29 Article deadline, and the strong prospect of that being approved has prompted PM May to tentatively schedule a 3rd MV sometime before next week’s EU Summit. Elsewhere, Usd/Jpy has backed off from circa 111.73 overnight peaks on the aforementioned breaking US-China news, but the headline pair remains above a key chart level in the form of the 200 DMA (111.43) and could be prone to further upside if the BoJ is as dovish as expected tomorrow, or even more. Note, for a full preview of the impending policy meeting please refer to the Ransquawk Research Suite.

CHF/EUR/CAD – All holding up better against the Buck revival, as the Franc hovers close to the top of a 1.0050-30 range and perhaps finds some traction from firmer than forecast Swiss import/producer prices (albeit still deflationary in y/y terms). Meanwhile, the single currency is keeping its head above 1.1300, marginally, but shy of Fib resistance (1.1327 represents a 38.2% retracement of this year’s 1.1570-1.1177 move) after another hefty 2019 German GDP forecast downgrade (0.6% from 1.1% per Ifo) and the Loonie is back below 1.3300 vs its US rival against the backdrop of toppy oil prices and ahead of Canadian house price data then a speech from BoC’s Wilkins.

In commodities, WTI (-0.2%) and Brent (-0.1%) futures have slipped following reports that a Trump-Xi summit may be delayed until April vs. prior expectations of an end-March summit. As such WTI and Brent futures fell back into their respective one-month long range of around USD 3.50/bbl. This summit push-back has however been touted for a while as USTR Lighthizer recently noted that sticking points remain in talks. Elsewhere, Iraqi Energy Minister emerged on the wires stating that the nation will decrease crude exports to average 3.5mln BPD from USD 3.62mln BPD in order to comply with OPEC’s output curbs. The metals market is largely on the backfoot amid a pick-up in the USD wherein the yellow metal breached USD 1300/oz to the downside. Gold is now back below its 50 DMA at 1303/oz ahead of its 100 DMA at 1271/oz. Elsewhere, copper erased its three-day gains amidst a firmer Buck couple with a turnaround in risk sentiment after the Trump-Xi meeting. US is seeking to reduce Iran oil sales by about 20% to below 1mln bpd from May and is likely to renew sanctions waivers to Iranian oil buyers but could deny waivers to countries not using them, according to sources. CME lowered COMEX 5000 silver futures margins by 8.4% to USD 3300 per contract and lowered COMEX copper futures margins by 11.1% to USD 2400 per contract.

US Event Calendar

8:30am: Import Price Index MoM, est. 0.3%, prior -0.5%;

8:30am: Export Price Index MoM, est. 0.1%, prior -0.6%

8:30am: Initial Jobless Claims, est. 225,000, prior 223,000, Continuing Claims, est. 1.76m, prior 1.76m

9:45am: Bloomberg Consumer Comfort, prior 62.1

10am: New Home Sales MoM, est. 0.16%, prior 3.7%; New Home Sales, est. 622,000, prior 621,000

DB’s Jim Reid concludes the overnight wrap

Maybe the next piece should be “How to fix Brexit… and why it matters”. The first part might be more difficult to write then the second. Last night’s Parliament voted 321-278 to reject a no-deal Brexit under all circumstances. This was an amended motion that was stronger than the government wanted and hence they instructed MPs to vote against it. So in effect they lost again with the government’s authority is some disarray. I would note that this is the same government who are 10pp ahead in the latest opinion polls though. In response, Mrs. May has tabled a motion for today that effectively says that if Parliament can agree a deal by March 20th (next Wednesday and on the eve of the EU summit) she’ll ask for an extension to June 30th. If no deal is agreed she suggested an extension could be much longer as the EU will insist on it (assuming they allow one at all). So the stakes are raised and the likelihood of MV3 coming back next week is high. I’m not sure there is any time or consensus for an alternative plan to be ready by then but watch out for attempts and watch out for any amendments today that could complicate this timeline.

Sterling rallied ahead of, during, and after the vote, gaining +2.01% versus the dollar (-0.7% this morning but still up 3 cents from this week’s lows) to reach its highest level since last June. The chances appears to have increased materially for a more positive outcome. Either May’s deal or an even softer version will eventually pass, or Article 50 will be extended for a long period. The threat of the latter scenario, where Brexit might be deferred indefinitely, could be enough of a discouragement to entice the hard Brexit wing of the Conservative party to support May’s deal. However it’s fair to say that they are angry at the moment and their next steps are unpredictable.

In what feels like another planet, the rally for risk this week continues. Anyone that remembers the 1990s band Chumbawamba’s big hit will know of a good soundtrack to the recent resilience. The S&P 500 (+0.70%) rose for a third consecutive day yesterday and has now wiped out last week’s losses and is back above the 2,800 level for the first time since March 1st and to the highest close since 7 November. 2,800 has proven to be a level that the S&P has failed to hold above in recent months, but the index is back to within 4.5% of those September all-time highs now. The index did dip -0.36% off its intraday high late in the session however, after President Trump said that he is in no rush to complete a trade deal with China. Elsewhere even the DOW (+0.58%) climbed yesterday as Boeing shares finished slightly higher – notwithstanding a +/-4.83% intraday range after the US and Canada joined Europe in grounding the 737 Max plane – following two heavy day declines on Monday and Tuesday. The NASDAQ was +0.69% while in Europe the STOXX 600 ended +0.63% and is back above the levels seen before the ECB last week and just about level with its YTD high. European Banks also closed +1.59% (still below ECB meeting levels) with bond yields up 1-2bps in Europe and +0.7bps for Treasuries. Oil rose +1.50% after US data showed another larger-than-expected drawdown in crude inventories. Usually, inventories build during the winter and are reduced during the summer, but they fell by -3.86mn barrels last week.

In Asia this morning markets are trading lower with China’s bourses leading declines due to mixed economic data releases. The Shanghai Comp (-1.09%), CSI (-0.48%) and Shenzhen Comp (-2.39%) are all lower along with the Hang Seng (-0.14%) and Kospi (-0.28%) while the Nikkei (+0.24%) is up. Elsewhere, futures on the S&P 500 are down -0.12% and all G-10 currencies are trading weak (-0.1% to -0.7%) this morning. Overnight, we saw China’s February economic data dump which presented a mixed bag for the economy with YtD industrial output (at +5.3% yoy vs. +5.6% yoy expected) marking the slowest start to the year since 2009. The unemployment rate (at 5.3% vs. 4.9% in December) rose to the highest since February 2017 and YtD retail sales came in line with expectations at +8.2% yoy, marking the slowest pace of growth since 2003. On the other hand, China’s YtD fixed asset investment came in line with consensus at +6.1% yoy (vs. 5.9% in last month) and YtD property investment jumped to 11.6% (vs. 9.5% in last month).

So China data is taking a shine off things but US data seems to be bouncing back with more evidence yesterday. Most notably, the January durable and capital goods orders data beat and painted a reasonable picture for Q1 capex so far. Core capex orders were up a lot more than expected (+0.8% mom vs. +0.2% expected), as were shipments (+0.8% mom vs. -0.2% expected). We should note that the data tends to be a bit volatile however and subject to big swings so best to look across months. Also, the January construction spending print was up a better than expected +1.3% mom (vs. +0.5% expected).

In contrast, albeit helping the carry trade, the February PPI print disappointed coming in at +0.1% mom for the core (vs. +0.2% expected). That said the healthcare component printed at a solid +0.25% which therefore helps the healthcare component of the PCE, although it was somewhat offset by other components which feed into the PCE, such as a -3.5% drop in airfares. So a mixed report.

In the UK yesterday we had the Spring Statement. Unsurprisingly it played second fiddle to all things Brexit related with the highlights being a £3bn improvement in the public sector net borrowing for the 2018-19 fiscal year. Stronger revenues from corporate and income taxes have been the key driver so far, though lower interest rates have also reduced borrowing costs. In a vacuum, this would reduce gilt issuance forecasts and would be bullish, but of course the outlook and price action is going to be mostly swamped by Brexit dynamics.

To the day ahead now, where the non-Brexit events this morning include final February CPI revisions in Germany and France, followed this afternoon by the February import price index print, latest weekly initial jobless claims, January trade balance and January new home sales. The ECB’s Coeure is due to speak in Milan and EU ambassadors meet.

via ZeroHedge News https://ift.tt/2UCurxg Tyler Durden

With the U.K. in limbo and Parliament deadlocked, MPs will vote today on whether to delay Brexit after they rejected a no-deal split from the EU (in a non-binding vote that does not legally remove it from the table).

Prime Minister Theresa May has called a meeting of her political Cabinet at 1:30 p.m. ahead of tonight’s vote (expected after 12ET beginning with amendments), two people familiar with the matter said.

Key Developments:

Theresa May says if deal approved by March 20, she’ll ask for short delay; if deal isn’t approved, it will have to be a longer one

European Council President Donald Tusk said he will push for a long extension.

Cabinet Minister Andrea Leadsom to announce next week’s parliamentary business; another vote on Brexit deal expected

Chancellor Hammond repeats call for MPs to choose way forward

But most notably, Bloomberg reports that Theresa May would put her Brexit deal back to Parliament for a third vote if she thought it would win support, her spokesman told reporters.

“If it were felt it would be worthwhile to bring the deal back for a new vote then that is something we would do,” James Slack, her spokesman said.

Cable has erased much of the rally from the non-binding no-no-deal brexit vote…

If you’re confused at the non-binding nature of the vote against a no-deal Brexit; the DUP and GRE; the EU’s attitude; May’s indignance; and broad-based project fear from the establishment; here is MEP Daniel Hannan to explain, “now what”, in under four minutes,,,

It isn’t clear that the EU will agree to an extension regardless. We pointed out that a natural ally of the UK, the Netherlands, was tasked to and accepted delivering a tough message on an extension. Readers reported that another UK ally, Denmark, has given up on the UK. May trying to get yet another vote on her Withdrawal Agreement next week means the odds are high that the Government will deliver its extension request right before the EU summit, which is yet another display of UK disregard for protocol and competent decision-making. If you want to let pique play a role, this is just the way do it, and too many EU leaders have been having to work too hard to maintain a veneer of politeness as it is.

More generally, too many people are not thinking straight, particularly those who believe the no deal bomb has been disarmed. And I would not trust the self-appointed sappers in Parliament.

Confirming the warnings from last week, GE has issued a 2019 guidance statement that the company expects industrial free cash flow as low as negative $2 billion.

On March 5th, CEO Larry Culp warned that cash flow from GE’s industrial operations will be negative this year as GE grapples with further challenges in its power business and other operational pressures.

Today’s guidance confirms that.

Looking ahead to 2020 and 2021, GE expects adjusted Industrial free cash flows to be positive in 2020, with the pace of improvement accelerating in 2021.

Sees year adj. EPS 50c to 60c, vs. estimate 67c.

Expects power unit free cash flows down in 2019.

Sees GE Capital net income breakeven by 2021.

“GE’s challenges in 2019 are complex but clear,” says CEO Lawrence Culp, adding

“We have work to do in 2019, but we expect 2020 and 2021 performance to be significantly better with positive Industrial free cash flow as headwinds diminish and our operational improvements yield financial results.”

The reaction was not positive, as it seems the final short-squeeze two weeks ago exhausted the ammo and downside risk is back:

“We will continue to take thoughtful actions to reduce downside risk and increase upside optionality to create long-term value for our shareholders,” Culp added.

via ZeroHedge News https://ift.tt/2Uz48bi Tyler Durden

The democratic presidential hopeful field expanded by one on Thursday morning, when Beto O’Rourke, the 46-year-old former Texas congressman, who surged to prominence by nearly unseating Republican Senator Ted Cruz in last year’s midterm congressional elections, formally announced his candidacy for president on Thursday.

O’Rourke told US media that he would run as a Democratic candidate for president. He had first suggested that he was running in an article for Vanity Fair magazine published on Wednesday.

“This is a defining moment of truth for this country and for every single one of us,” O’Rourke said in a video announcing his candidacy sent to US media.

“The challenges that we face right now, the interconnected crises in our economy, our democracy and our climate have never been greater. They will either consume us, or they will afford us the greatest opportunity to unleash the genius of the United States of America.”

As Axios notes, Beto was unknown outside of Texas until his race against Ted Cruz put him on the national stage. If he ends up winning, AP writes that he “would be the first U.S. politician to do so since Abraham Lincoln lost his Senate bid to Stephen Douglas in Illinois in 1858, then was elected president two years later.”

The fluent Spanish speaker created a grassroots phenomenon by driving to all 254 counties in Texas and posting images of his travels on social media. He raised a record $38m in the quarter before the election from small donors, easily outpacing Mr Cruz despite not taking money from special interests. Donald Trump and the Republican establishment became so concerned that Mr O’Rourke might beat Mr Cruz that the president flew to Texas to campaign for the man he once mocked as “Lyin’ Ted” Cruz.

“He’s not ‘Lyin’ Ted’ any more. He’s Beautiful Ted’,” Mr Trump said two weeks before the election, as he slammed Mr O’Rourke who was attracting big crowds at his rallies across the second-biggest US state.

O’Rourke, who is starting a three-day swing through eastern Iowa on Thursday, said he will hold a kick-off rally for his campaign in El Paso, Texas, on March 30: “You can probably tell that I want to run. I do. I think I’d be good at it,” Mr O’Rourke told Vanity Fair for a cover story illustrated with an image taken by the renowned portrait photographer Annie Leibovitz.

The 46-year-old Irish-American had been mulling a presidential bid since his unexpectedly strong challenge to Cruz. While he lost 51-48 per cent, his performance was seen as remarkable in a conservative state that has not elected a Democrat to the Senate for three decades and not voted for a Democrat candidate for president since Jimmy Carter in 1976.

Donald Trump and the Republican establishment became so concerned that Mr O’Rourke might beat Mr Cruz that the president flew to Texas to campaign for the man he once mocked as “Lyin’ Ted” Cruz.

“He’s not ‘Lyin’ Ted’ any more. He’s Beautiful Ted’,” Mr Trump said two weeks before the election, as he slammed Mr O’Rourke who was attracting big crowds at his rallies across the second-biggest US state.

O’Rourke previewed his candidacy with an Annie Leibovitz cover and 17-page Vanity Fair spread.

Joe Hagan, who wrote the cover story, tweets that he spent two months reporting this story before ever meeting Beto, starting last December:

I spent 2 months reporting this story before ever meeting Beto, starting last December. He wasn’t doing any media at the time but I figured it was an interesting story whether he talked or not, whether he ran or not.

“I convinced Beto O’Rourke to do this cover story after walking up to his house and introducing myself one Sunday afternoon. He was lounging on the front veranda, barefoot in blue jeans and T-shirt, talking on his cell phone.”

Hagan captures O’Rourke’s “radical openness”:

Beto O’Rourke seems like a cliff diver trying to psych himself into the jump. And after playing coy all afternoon about whether he’ll run, he finally can’t deny the pull of his own gifts. “You can probably tell that I want to run,” he finally confides, smiling. “I do. I think I’d be good at it.” …

The more he talks, the more he likes the sound of what he’s saying. “I want to be in it,” he says, now leaning forward. “Man, I’m just born to be in it, and want to do everything I humanly can for this country at this moment.”

O’Rourke enters the crowded Democratic field as moderately progressive candidate who wants to reform the immigration system and opposes the wall that Trump wants to build on the US-Mexico border. During the Senate race, he also made criminal justice reform a central issue, which helped generate strong support from African-Americans.

Larry Sabato, a University of Virginia politics professor, said Mr O’Rourke was “terrific on the trail” but one question was whether he could “capture lightning in a bottle a second time”, given that his opponent will not be Cruz.

At rallies from Dallas to Amarillo in west Texas before the midterms, some supporters told the Financial Times the Mr O’Rourke reminded them of former president Barack Obama or of Robert Kennedy, the former attorney-general and brother of president John F Kennedy who was also assassinated as he ran for president in 1968.

Democratic critics say Mr O’Rourke has no discernible record from his time in Congress. But his fans point to his optimistic vision for the US, his anti-Trump message on immigration and his ability to draw large, excited crowds as evidence that he has the ability to turn out enough voters to beat the president.

O’Rourke faces a very crowded and diverse field of opponents, who include two African-Americans and a record number of women, including senators Kamala Harris and Elizabeth Warren. He also will face Bernie Sanders who, despite his age, was able to electrify younger voters in 2016 when he challenged Hillary Clinton for the nomination.

His campaign launch also comes as Joe Biden, the former vice-president and moderate Democrat, is expected to launch his own candidacy.

via ZeroHedge News https://ift.tt/2O3gIxb Tyler Durden

The Trump administration just delivered a massive budget to Congress. And as Veronique de Rugy explains, a look at the numbers and the talking points drafted to defend it confirms that budgets favor politics over policy. This also confirms that it really doesn’t really matter who is in the White House. Big spenders will spend and then dissemble to cover up their fiscal irresponsibility.

With S&P futures trading at session highs, at precisely 6am EDT the Eminis tumbled, rapidly approaching session lows following a Bloomberg report that trade negotiations may not be going quite as well as represented, as a meeting between President Donald Trump and President Xi Jinping to sign an agreement to end the ongoing US-China trade war won’t occur this month and is more likely to happen in April at the earliest.

The market reaction is shown below.

As Bloomberg adds, despite repeated claims of progress in talks by both sides, a hoped-for summit at Trump’s Mar-a-Lago resort will now take place at the end of April “if it happens at all.” China is pressing for a formal state visit rather than a lower-key appearance just to sign a trade deal, the person said.

Confirming prior reports, a Bloomberg source said that Xi Jinping’s staff have scrapped planning for a potential flight to the U.S. following a trip to Europe later this month.

The hints that not all is well were there, even if the market chose to ignore them: earlier this week, U.S. Trade Representative Robert Lighthizer pointed to “major issues” still unresolved in the talks, with few signs of a breakthrough on the most difficult subjects including treatment of intellectual property. Chinese officials have also prickled at the appearance of the deal being one-sided, and are wary of the risk of Trump walking away even if Xi were to travel to the U.S.

Trump himself has shifted tone in recent days, walking back from a more urgent approach to getting a deal signed as early as March. He acknowledged concerns in Beijing about the possibility of him walking away from a trade deal, offering to push back a summit with Xi until a final deal is reached.

“We could do it either way,” Trump told reporters Wednesday at the White House. “We can have the deal completed and come and sign or we can get the deal almost completed and negotiate some of the final points. I would prefer that. But it doesn’t matter that much.”

Considering that much of the 500 or so S&P point rally from December 24 has been built on market “optimism” that a US-China deal is now a done deal, any potential failure to secure an outcome that has already been priced in risks sending the S&P sharply lower, and certainly once again below 2,800 a level which algos just seem powerless to break out decisively above.

via ZeroHedge News https://ift.tt/2HxJ9St Tyler Durden

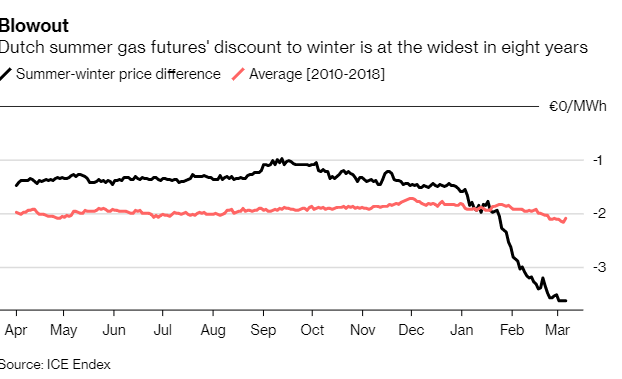

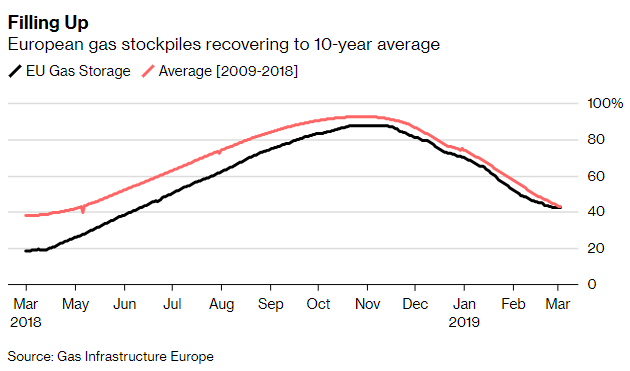

At the end of last winter’s heating season, it was an unusually cold spell that upended European natural gas markets, with storage levels falling below average and prices firming up as demand shot up.

At the end of this winter’s heating season, it is the unusually mild weather in most of Western Europe for most of the winter that has driven natural gas prices down and left supplies higher than the seasonal average.

The summer gas futures at the Dutch TTF hub have declined by 16 percent so far this year and have been trading lately around the lowest in 10 months. The winter gas futures contract, however, has dropped by just one third of the decline in the summer contract, according to data from ICE Endex compiled by Bloomberg.

So the discount of the Dutch summer natural gas futures to the winter contract widened to the biggest since 2011 as of early March. Typically, such a wide spread would mean that one of the most common European gas trades—buying cheaper gas futures in the summer to sell in the winter—would be the most profitable in eight years.

However, traders are unable to take full advantage of the wide winter-summer spread because several factors have combined this winter season to create a perfect storm in the European natural gas markets. These factors are higher stockpiles than usual, limited available storage capacity as most of it is booked out amid declining overall capacity, and increased liquefied natural gas (LNG) shipments to Europe as Asian LNG spot prices continue to tumble.

First, unlike last year’s winter, this winter has been unusually mild in many parts in Western Europe. This has led to lower natural gas demand and lower withdrawal from storage—a stark contrast compared to the 2018 winter.

The cold spell in Europe at the end of February and early March of 2018 led to record withdrawals in the first quarter of 2018, and storage levels dropped to 18 percent of capacity—well below the five-year range—the European Commission (EC) said in its Q1 Quarterly Reporton European gas markets. By the end of the winter season, natural gas stock levels dropped below 10 percent of capacity in countries such as Belgium, France, and the Netherlands, where high gas demand from the UK contributed to strong withdrawals.

Before the 2019 winter season began, the European market was tight amid higher demand in the summer’s heat wave, while natural gas stockpiles were still lower than usual after the winter of 2018, one of the coldest winters in the past decade.

Natural gas prices in the UK surged to the highest for a summer season, with Europe’s natural gas market the most bullish in years, as higher-than-expected summer demand and a tighter market drove natural gas price futures to levels last seen during the winter’s supply crunch.

But the 2019 winter has been quite a different story. The UK, for example, registered its warmest February on record, with daily maximum temperatures the highest on record dating back to 1910, according to the UK’s Met Office.

Due to the warmer winter, natural gas stockpiles across Europe are now higher than the typical levels for this time of the year. What’s left of the storage capacity is nearly “sold out”, according to analysts who spoke to Bloomberg.

“We are going into this summer with full storage, among the highest in years,” Wayne Bryan, a trader and analyst at Alfa Energy in London, told Bloomberg, noting that he wasn’t buying anything at the moment.

In addition, Europe’s total storage capacity has declined by more than 4 percent since 2016, according to data from gas industry trade association Gas Infrastructure Europe, cited by Bloomberg.

As a result, higher-than-usual gas stocks in European storage and almost fully booked storage space have been preventing natural gas traders from profiting from the most profitable price differential between winter and summer gas futures contracts in years.

via ZeroHedge News https://ift.tt/2TPFzK4 Tyler Durden

Benjamin de Rothschild’s family plans to take Swiss Bank Edmond de Rothschild (Suisse) S.A. private as it consolidates and simplifies the bank’s legal structure.

According to Bloomberg, Edmond de Rothschild Holding SA will acquire all publicly held Edmond de Rothschild (Suisse) bearer shares at 17,945 francs per share, a 6.7% premium to Tuesday’s closing price, in a deal worth about $100 million. The Swiss bank, which has long been linked with managing the wealth of countless uber-wealthy families, offers a variety of wealth management service for private and institutional clients, is expected to be delisted from the Zurich exchange. The stock, which traded on Wednesday around 17,500 francs, jumped by more than 8% to 17,800 before trimming gains to trade up 6.7%.

“My role has been to simplify the group’s structure, which was very complicated and lacked transparency, and to ensure the group’s longevity and stability,” Ariane de Rothschild, president of the group’s executive committee, said in an interview at the bank’s headquarters in Geneva. “I am passing the torch on to Vincent and to the teams with full confidence. The group has been cleaned up and is in working order now.”

Founded in the early 1950s, the Edmond de Rothschild Group has 170 billion francs in assets under management and 1.1 billion francs in revenue. The Edmond de Rothschild (Suisse) banking unit had client assets of 128 billion francs at the end of 2018, down 7% from the prior year. It saw an outflow of 2.5 billion francs in assets under management last year.

The buyout offers closure to a dispute among the Rothschild family over the use of the banking dynasty’s historic family name.

The deal involves liquidating cross-holdings and buying back shares in a transaction worth 100 million francs to give complete control of the bank to the family.

By taking it private, “we are demonstrating our commitment to our banking group and our ambitions for growth, both organic and through acquisitions,” Benjamin de Rothschild, chairman of Edmond de Rothschild Holding’s board of directors, said in the statement.

via ZeroHedge News https://ift.tt/2XR1ksh Tyler Durden

The Martin County, Florida, sheriff’s office is investigating whether a school bus aide committed a crime when she yanked a “Make American Great Again” hat off a student’s head. The boy’s mother filed a report with the sheriff’s office after school officials told her they would not let her see security video of the incident until the school system had completed an investigation. That video shows the aide confront the boy seconds after he boards the bus and demand he take the hat off. When he refused, she pulled the hat off.

The Trump administration just delivered a massive budget to Congress. And as Veronique de Rugy explains, a look at the numbers and the talking points drafted to defend it confirms that budgets favor politics over policy. This also confirms that it really doesn’t really matter who is in the White House. Big spenders will spend and then dissemble to cover up their fiscal irresponsibility.

The Trump administration just delivered a massive budget to Congress. And as Veronique de Rugy explains, a look at the numbers and the talking points drafted to defend it confirms that budgets favor politics over policy. This also confirms that it really doesn’t really matter who is in the White House. Big spenders will spend and then dissemble to cover up their fiscal irresponsibility.

The Martin County, Florida, sheriff’s office is investigating whether a school bus aide committed a crime when she

The Martin County, Florida, sheriff’s office is investigating whether a school bus aide committed a crime when she