This weekend’s “truce” outcome may have been just as the market expected, and yet that did not prevent stocks from reacting as if what happened was the best possible – and unexpected – case. And, as we noted earlier, and as Nomura’s Charlie McElligott notes, global equities, risk FX and Asian Commodities-futures go “mongo” overnight in standard “relief rally euphoria” fashion.

At the same time, while equities are set to explode to new all time highs, Treasuries and rates remain well-bid despite the “feel-good” for risk-asset sentiment off the G20, as Monday brought another atrocious round of Global Mfg PMIs, with Germany at an eye-watering 45; Spain back “contracting” for the first time in more than 5.5 yrs; UK “back-to-back” contractions for first time in 6 yrs; China Caixin Mfg PMI at 49.4 lows since January, with 21 of 22 releases thus far declining vs the prior month and expectations for US to continue trend “lower” later today, all of which “capture the spectacular breadth of the global economic deterioration”, according to McElliogtt.

What is most surprising in the context of a positive US-China “truce”, Nomura observes that “we are seeing virtually no adjustments to the market’s already remarkable “Fed rate cut” expectations, still at approx. 100bps of easing looking-out over the next 1Y”, even though odds for a July 50bps cut now are down below 20% vs nearly 40% at the start of last week. Still, as McElligott adds…

… the market knows that “when the Fed goes, they go hard and fast” (i.e. of the last four easing cycles, 70% of the aggregate “easing” has occurred within the first six months of the initial cut), especially with the potential for negative “business investment” sentiment to remain high as legacy trade-tariffs stay “in-place.

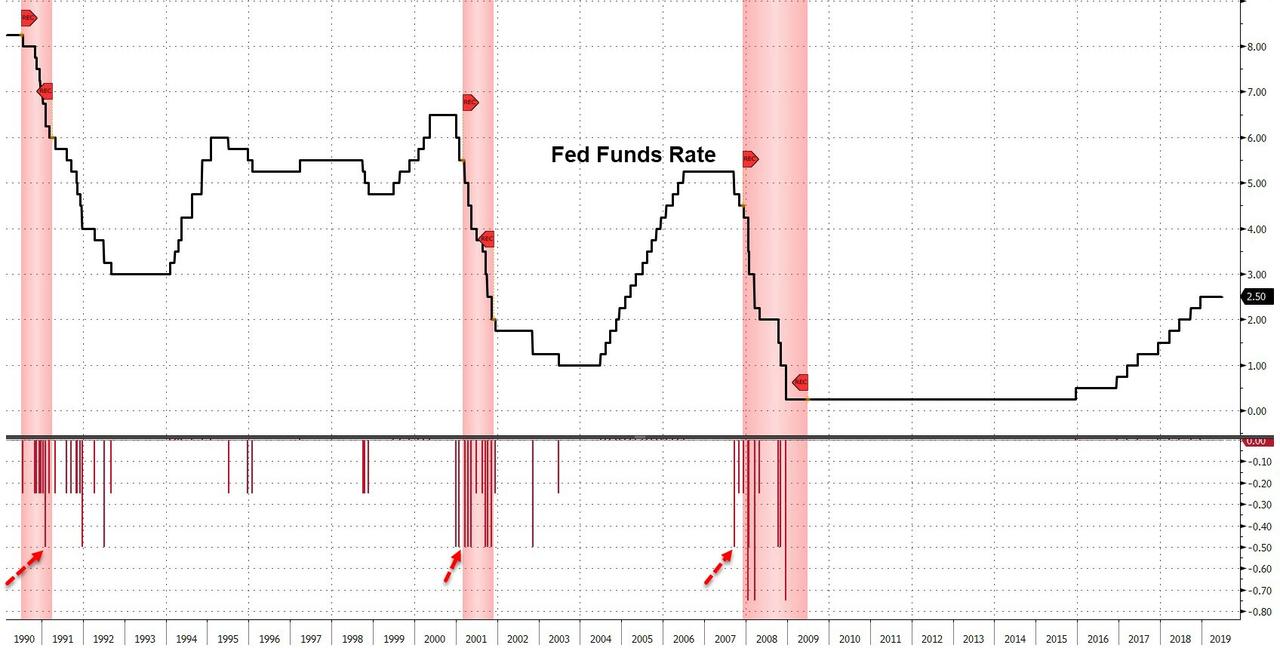

There is a negative flipside to that of course, because as we noted over the weekend, there are two signals which are pretty much fail safe coincident recessionary indicators:

- The Fed has never cut 100bp within a year in an easing cycle outside a recession.

- The Fed has never started an easing cycle with a 50bp cut outside a recession.

So while the US – and global economies – may be headed for a day of reckoning, traders have yet to extract some upside from the market and as McElligott observes, the US equities “Melt-Up” continues to be the most-likely early Summer scenario, for the same “under-positioning” dynamics he has been discussing over the past few months, which again are as follows:

- Street PB data showing median Equities HF “Net Exposures” at sub- 10th %ile ranks across 1-, 3-, 5- year ranks and since 2010 overall

- Not surprisingly then, we see “extreme” Leveraged Fund “Net Short” positioning in US Eq futures, shorting -$59.2B YTD and now -$36.2B overall across SPX-, NDX- and RTY- futures—a remarkable (“just”) 13th %ile since 2006

- Within the overall make-up of underlying portfolios, we continue to see a very “Slow-flation / end-of-cycle” lean from both Mutual- and Hedge- funds being heavily “Low Vol” (long / overweight the “Duration-Sensitives” of Defensives- and Secular Growers- vs short / underweight high-beta Cyclicals-):

- Long-Short “Beta to S&P 500” just 3rd %ile since ‘03

- Long-Short “Beta to Beta Factor” just 3rd %ile since ‘03

- Mutual Fund “Beta to Beta Factor” just 23rd %ile since ‘03

- Macro Fund “Beta to SPX” similarly “meh” at just 56th %ile since ’03, which is actually down vs 1m ago

- EPFR Global Fund Flow data now showing a -$138.4B redemption YTD from Global Equities funds, incl a “net outflow” of -$41.2B in US funds (-$83.0B from Active-, partially offset by +$41.8B inflow to Passive-)

- Conversely, there is significant “High Cash” component which then could act as “fodder” for a grab-in across both Risk-Assets (and further into Bonds), with Money Market funds experiencing a massive +$195.8B inflow YTD, which is 93rd %ile since 2000 (although last week saw a -$14.0B outflow as seemingly money was “put to work”)

- Still seeing some legacy “Net Short” positions in our Nomura QIS CTA Trend model which are incrementally nearing “buy to cover” levels in Russell 2000, Nikkei and KOSPI, while Hang Seng CH is within reach of triggering more re-leveraging / buying to get back to “+100% Long” signal as well

- Nomura QIS Risk-Parity model estimates the “gross exposure” across the aggregate position in Global Equities near 1.5 year lows, with the aggregate US Equities futures component near 28 month lows—the continued grind lower in trailing 2 year realized vol will gradually reverse last year’s “higher realized” environment and gradually see Equities exposure added back

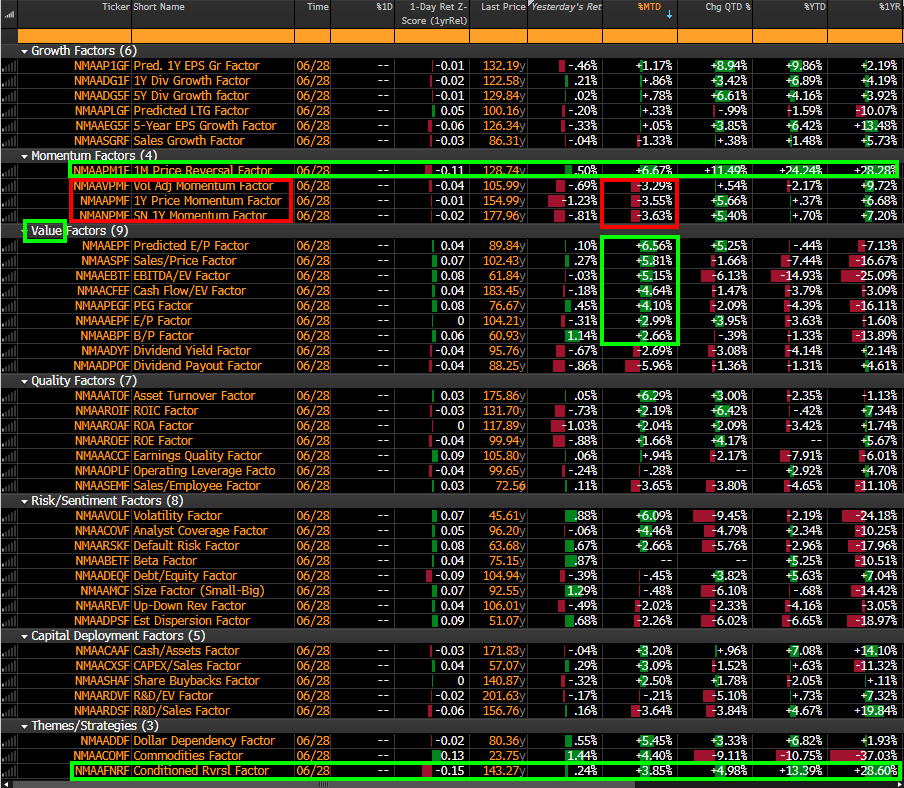

Meanwhile, looking back at June, which saw the S&P surge 7%, yet saw most hedge funds suffer losses, the Nomura derivatives expert attributed this to the positive impact of a steepening US yield curve on chronically under-owned “Value” (Predicted E/P factor +6.6% MTD; Sales / Price +5.8% MTD; EBITDA / EV+5.2% MTD; Cash Flow / EV +4.6% MTD; PEG +4.1% MTD) vs the NEGATIVE impacts of a steeper curve on “Momentum” (Sector Neutral 1Y Momentum -3.6% MTD; “Pure” 1Y Price Momentum -3.6% MTD; Vol Adjusted Momentum -3.3% MTD).

As shown below, the US “factor reversal” remains the story of June due to the positive “value”, negative “momentum” shift due to yield curve steepending (which itself should be negative for the market):

In conclusion, why has 2019 been so challenging within US Equities from a thematic / risk-premia perspective? As McElligott concludes, the above US Equities factor “unwind” phenomenon has been an almost monthly occurrence for the past year via said constant “end of cycle” macro regime-change across Volatility-, Financial Conditions- and US Rates- / Yield Curves- therein; the result: spectacular performance of Nomura-Instinet’s two “monthly reversal” factor market-neutral strategies of the past 1 year window: “1m Price Reversal” factor at +24.3% YTD / +28.3% past 1 year period; and “Conditioned Reversal” factor at +13.4% YTD and +28.6% past 1 year period.

via ZeroHedge News https://ift.tt/2Nn4iU4 Tyler Durden