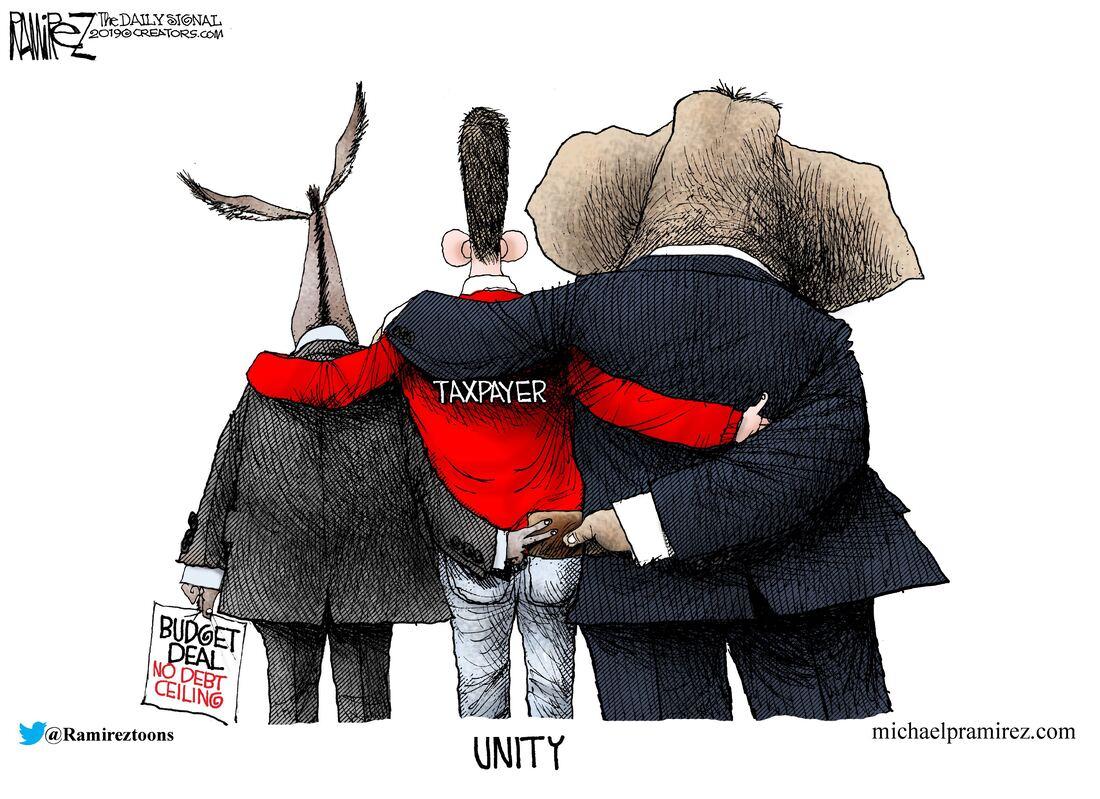

Poor Mick Mulvaney! Just kidding—the White House chief of staff (and director of the Office of Management and Budget) is, according to Nick Gillespie, a bald-faced and balding “liar.” And that was just within the first 10 minutes of today’s Editors Roundtable edition of the Reason Podcast.

Katherine Mangu-Ward, Peter Suderman, and Matt Welch take swings at bipartisan budget awfulness, Federal Reserve debt monetization, David Simon grumpiness, and—yes!—President Donald Trump’s swipes at Rep. Elijah Cummings (D–Md.), the City of Baltimore, and its residents. The editors also discuss what they learned on their summer vacations, tiptoe into the bi/trans wars, and even say nice things about you, the listening public!

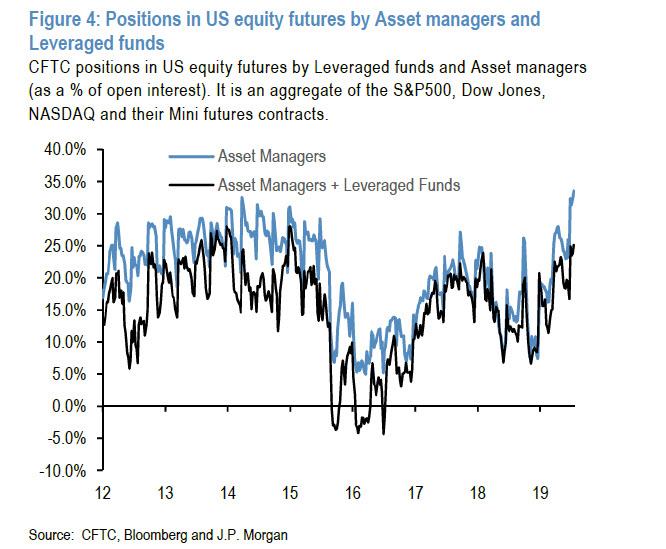

One of the constantly repeated mantras of this stock market, which keeps rising no matter how much bad news is lobbed at it, is that it is climbing a wall of worry as investors refuse to participate in the “most hated bull market of all time”. This has been, at its core, the primary reason why JPMorgan’s Marko Kolanovic has been bullish on stocks for the past several hundred points.

There is just one problem with this conventional wisdom: as often happens, it is dead wrong, and as JPMorgan’s “bad cop” strategist, and now chronic foil to Koalnovic’s unbridled permabullishness, Nick Panigirtzoglou wrote on Friday, not only are investors very much long risk, but most asset classes have now been massively “overbought”, with some positioning levels in record territory.

Case in point, the combined asset-manager and leverage fund positioning in U.S. equity futures the most extended in years this decade, if not ever.

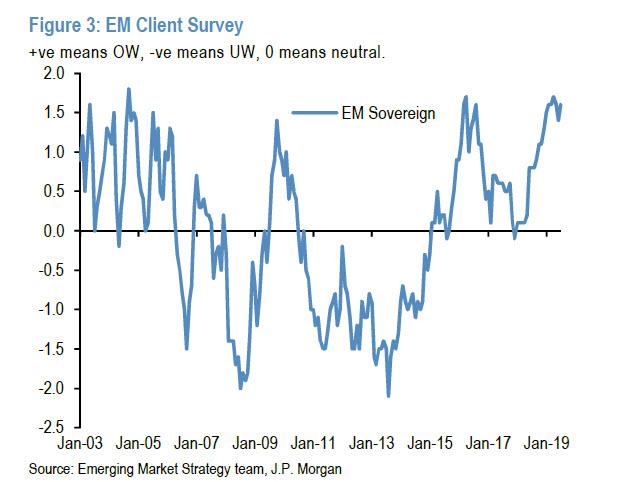

In the EM fixed income space, Panigirtzoglou shows the next chart, which shows that emerging market external debt overweights in JPM’s EM fixed income client survey are near levels last seen in 2005.

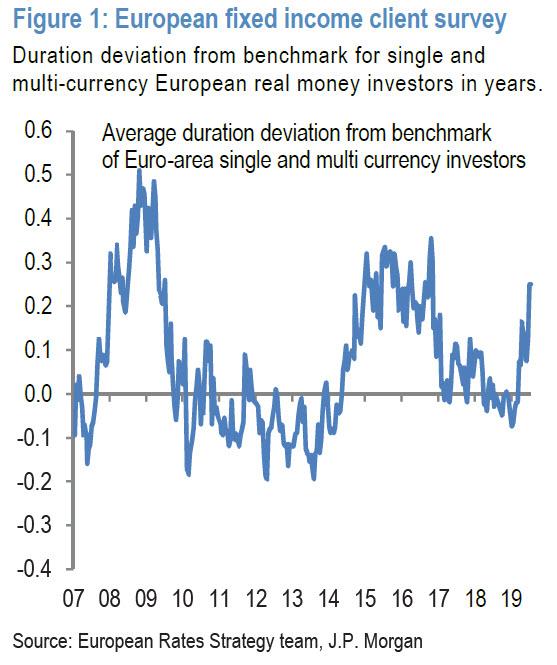

In the government bond space, while not at all time highs, the duration longs implied by European fixed income client survey, whose the most elevated duration longs in four years.

While longs are rushing into both risk and safe haven assets, and pretty much anything that isn’t nailed down, the shorts are getting crushed.

Consider first the chart below, which shows how low the short interest on the biggest US HY ETFs is at the moment, in contrast to the persistently high short interest observed for much of 2018. In other words, relative to last year, investors have closed their short exposure, and added significantly to their net HY exposures, something that is also consistent with the YTD reversal of last year’s HY ETF outflows.

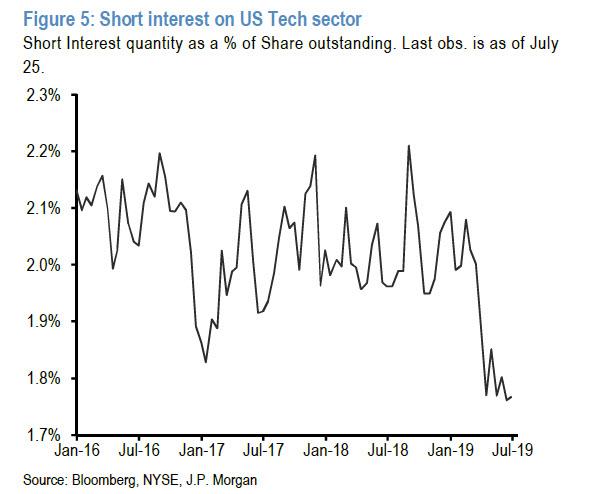

A similar observation can be made in the equity tech space, where shorts have similarly capitulated, “again pointing to overbought conditions for this sector.”

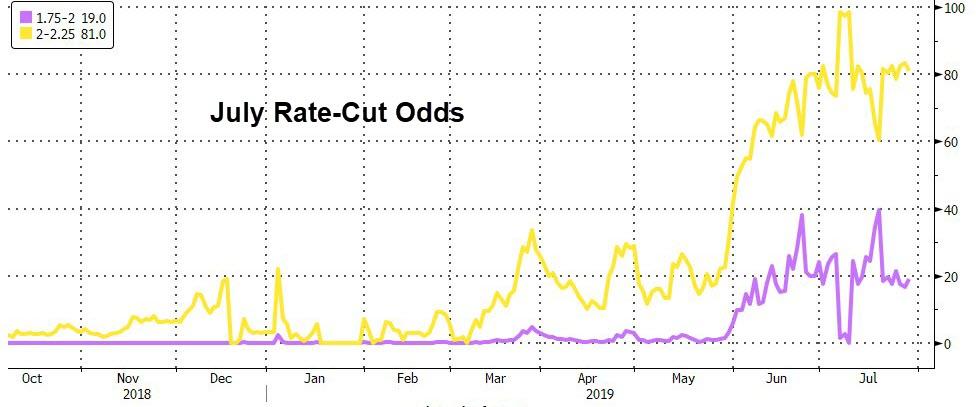

Why is the above relevant? Because as Bloomberg notes, “investors betting the U.S. Federal Reserve is set to extend the market bonanza with a rate cut may have overplayed their hand.”

One such investor is the multi-asset team at Aberdeen Standard Investments, which is preparing for disappointment as it lightens up on equity and emerging-market debt holdings ahead of the Fed’s meeting this week.

“This is an environment where there could be swings in sentiment, and we need to position ourselves for that,” said Ken Adams, head of tactical asset allocation at Aberdeen Standard Investments. “Maybe we won’t see the extent of monetary policy easing that’s now priced in. Investor expectations have become a bit too upbeat.”

Commenting on these observations, Panigirtzoglou writes that “the assets that have benefited from the low yield environment are vulnerable to retrenchment if central banks fail to validate market expectations of easing over the coming months.”

The JPM strategist also notes that whereas the so-called TINA, or There Is No Alternative, argument is often mentioned in client conversations as an argument to keep playing the asset reflation trade even if central banks fail to validate market expectations of easing, he disagrees, and believes that “There Is An Alternative (TIAA) which is dollar cash

which is yielding close to 2.25% (1m T-bills) at the moment well above the 1.4% yield of either the Global Agg bond index or the next high yielder in G10 (1m NZD bills), and above 10y UST yields without taking duration risk.”

And speaking of central bank disappointment, that’s precisely what Morgan Stanley believes will happen if the Fed cuts less than 50bps on Wednesday, something which the NY Fed hinted will not happen when it vocally corrected its president John Williams two weeks ago, when the latter hinted at a double 25bps rate cut on July 31.

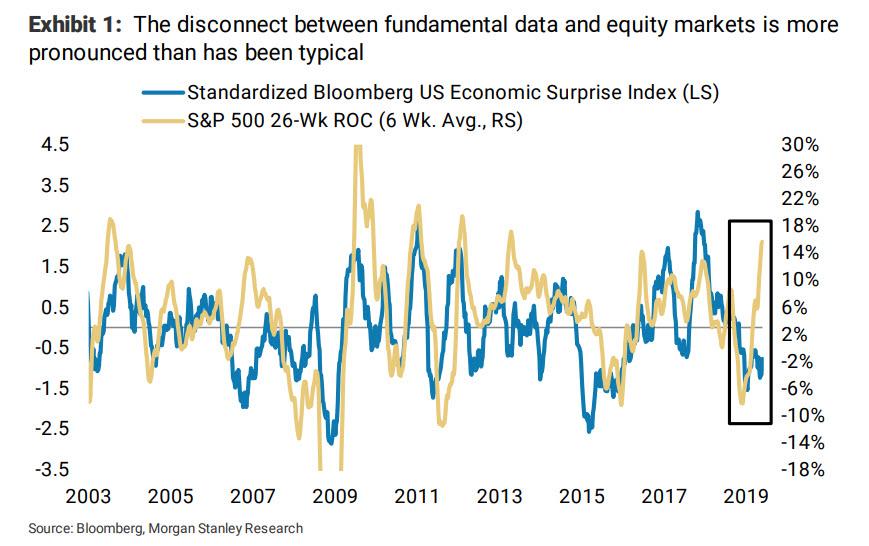

As a reminder, Morgan Stanley also cautioned that the disconnect between fundamental data and actual/promised future central bank easing has never been more pronounced in the equity market…

… and explained that “the growth and market impact of trend-following systematic strategies over the past decade may have driven this sharp divergence.” In this context, Morgan Stanley’s chief equity strategist, Michael Wilson, cautions that “any reversal in stock prices could lead to a faster and deeper drawdown than many are expecting.“

A reversal that would emerge once the Fed cuts by only 25bps, even as a still sizable portion of the market expects at least 50bps of cuts this week…

via ZeroHedge News https://ift.tt/2YqQF6t Tyler Durden

Poor Mick Mulvaney! Just kidding—the White House chief of staff (and director of the Office of Management and Budget) is, according to Nick Gillespie, a bald-faced and balding “liar.” And that was just within the first 10 minutes of today’s Editors Roundtable edition of the Reason Podcast.

Katherine Mangu-Ward, Peter Suderman, and Matt Welch take swings at bipartisan budget awfulness, Federal Reserve debt monetization, David Simon grumpiness, and—yes!—President Donald Trump’s swipes at Rep. Elijah Cummings (D–Md.), the City of Baltimore, and its residents. The editors also discuss what they learned on their summer vacations, tiptoe into the bi/trans wars, and even say nice things about you, the listening public!

As expected, increased ’dovishness’ by the Fed has gotten markets rallying. Both the S&P 500 and DJIA have touched new highs. From the perspective of late last year, such massive rallies seemed unlikely indeed. While some kind of a Fed pivot was to be expected, the response has been nothing short of “maniacal.”

In March, we noted that markets seemed completely oblivious to the fact that the ability of monetary and fiscal stimulus to uphold economic growth was declining fast and that the momentum of the global economy seemed to be eroding quite notably. But the “monetary drug” administered by the Fed apparently brushed all worries away. Unfortunately, such an artificial remedy only works until it doesn’t.

China on the way down

China has been active on our radar since September 2017, when we realized that it had—almost all by itself—supported the growth of the global (real) economy since early 2009. At that point we also warned that the effectiveness of Chinese debt stimulus was fading fast. During the first part of the current year this issue has grown even more pressing.

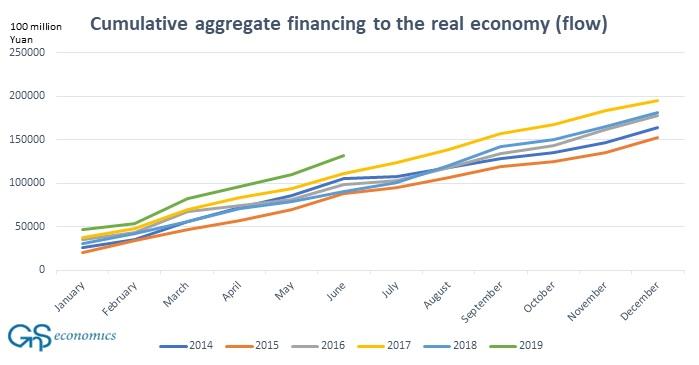

Despite record credit injections and fiscal stimulus (see our June 2019 forecasts for details), Chinese economic growth has remained at sub-par levels. In June, the aggregate social financing of the real economy, again, grew at record pace (see the Figure below), but the response of the Chinese economy was lacklustre, growing just 6.2 percent at an annualized rate. This was the slowest rate since 1992.

As shown in Figure below, the cumulative aggregate financing of the Chinese economy is at record levels with record monthly increases in January, March and June. Even when accounting for the deleveraging of the ‘shadow banking sector’ this is a troubling trend, especially as Beijing has signaled that more deleveraging may be on the way. The Chinese economy is simply not responding to stimulus as before. This implies that the most crucial engine of the global economy is stalling.

Figure. Cumulative aggregate financing to the real economy (flow) in China. Source: GnS Economics, PBoC

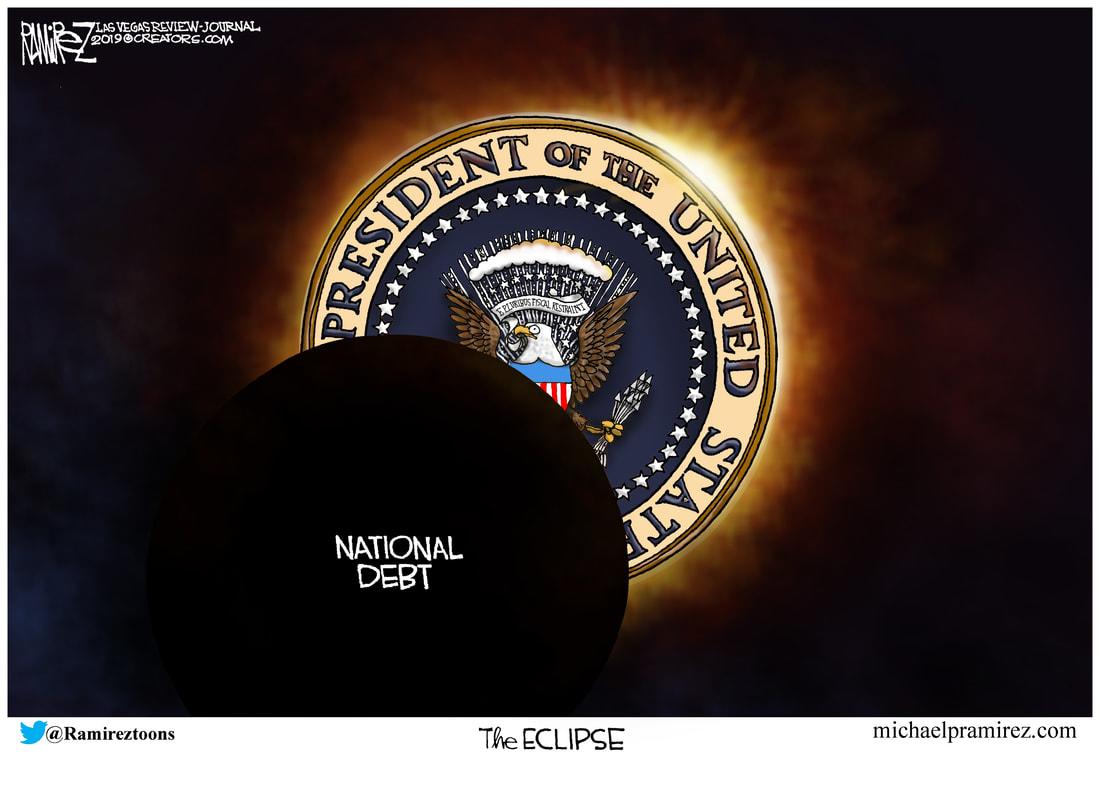

Desperation at the Fed

The tone of the Federal Reserve has turned more dovish basically throughout 2019. First, the FOMC panicked at the turn of the year due to rapid and steep deterioration in the stock and credit markets. After that, the Fed has basically turned into a market support machine, and for an obvious reason.

It’s quite clear that if the massively over-valued stock and credit markets crash, so does the economy, and the Fed will be left with little means to stimulate. This implies that even with the (comparatively) robust growth rates of the U.S. economy, the Fed is cutting rates just to support the markets. But this strategy, obviously, only subjects the markets and the economy to ever-greater risks when the economic downturn and market crash eventually arrives. Moreover, as we explained in March, the Fed is trapped. Manic markets go only up or down: there is no “soft landing” in sight.

Recently, a truly ominous “milestone” in market-meddling was reached when the yields of some Euro-junk bonds turned negative. Thus, now even the debt of companies that have a higher probability of default are giving out negative returns to investors! This yield-chasing madness is a direct result of incessant market interference by the Fed and other central banks (see Q-Review 1/2018).

The bailouts and timing

There have been at least three market bailout operations by the major central banks during the past two years. In November 2017, there was a run on the junk bond markets, which was halted by the liquidity injections and asset purchases of the BoJ and the PBoC. In March 2018, the European corporate bond markets froze over, which forced the ECB to step in clear the logjam by further purchases of corporate debt. In December 2018/January 2019, the PBoC and the Fed joined forces (figuratively) to stop the market rout.

As we explained in our June forecasts, the desperate efforts of China and the Fed to prolong the expansion, if continued, may postpone the day of reckoning for few quarters. But, it’s also impossible to estimate how long manic markets will respond positively to monetary stimulus when the real economy starts to crater.

Like manias, panics also start abruptly and often without a clear warning. With its relentless efforts to support the markets, the Fed is inadvertently increasing the likelihood of an abrupt market shock.

With the global economic downturn gathering steam—which will also likely become obvious in the U.S. during the fall—downward pressure on the markets will just keep growing from this point on. It is consequently not outside the realm of possibility that we may be heading toward a cataclysmic market event similar to what was experienced in October 1929.

The central bank fallacy

It remains to be seen whether we will see a supportive rate cut by the Fed next week and the eventual restarting of QE in the event of an unforeseen market event (or even beforehand). The truly worrying issue is that such actions do nothing to solve the underlying issues plaguing the world economy, but, rather, exacerbate them.

Evidence concerning the negative effects of monetary meddling on the drivers of long-run growth, investments and productivity is mounting (see, e.g., our blog on Japan and on the ‘zombification’ of the global economy as well as this, this and this). Further CB meddling, whether effective in supporting capital markets or not, will not just increase distortions, but will likely also cause the economy to weaken further—possibly to the point of collapse.

Central bankers, in their desperation, are playing a dangerous game.

via ZeroHedge News https://ift.tt/2Mmwvbu Tyler Durden

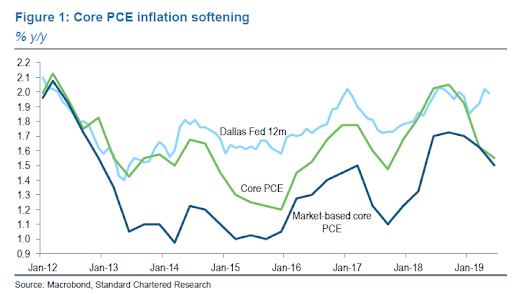

Inflation is only marginally below mandated levels.

And macro data has been surprising to the upside recently.

So, why the f**k are markets (and Fed speakers) so adamant that a 25bps (or 50) cut is required (or else)?

Is all of the above a lie and The Fed sees liquidity issues? Maybe, but in a somewhat stunning moment of clarity for the business channel, CNBC’s Steve Liesman just ever-so-quietly dropped a hint as to the real reason why The Fed is so keen to cut-cut-cut…

In a brief 45 seconds, Liesman drops the “existential” threat argument for why Powell will do whatever it takes to stay in Trump’s good graces…

“If The Fed gets this wrong, I think that they think if they make a mistake here, The Fed could be gone…”

Liesman expands on his ominous view:

“Think about what happens when a person gets up at a rally and starts railing against The Federal Reserve, and starts to create what could lead to Congressional pressure on The Fed, then you could imagine that their could be support for a different system.”

“I think they think there’s a lot of political downside risk to getting this wrong.”

This morning a Phoenix TV station aired a feel-good story about cops who are “rewarding people for good driving behavior” by pulling them over and giving them coupons for drinks at Circle K convenience stores. “If you see a Tempe police officer pulling you over,” chirped Colleen Sikora, a correspondent for the NBC affiliate KPNX, “it may not be a bad thing. If an officer sees someone following traffic laws correctly related to bicycles and pedestrians, they can pull you over, but instead of a citation, you’ll get a free drink coupon for either a cold drink or hot beverage…They’re kicking off the campaign this morning at 8 a.m., so if you see police lights in your rear view mirror, maybe hold off on the panic.”

For anyone who values the Fourth Amendment, which requires reasonable suspicion of a crime or traffic violation to justify forcibly detaining a motorist, the program described by Sikora is definitely “a bad thing.” That sentiment is clearly shared by viewers who reacted to the story on Twitter. “This is an insanely bad & illegal idea,” one commented. “This is actually illegal,” observed another.

To its credit, the Tempe Police Department seems to recognize that stopping motorists because they are not committing any traffic violations would be unconstitutional. According to the written version of the story on the KPNX website, bylined by Sikora herself, Tempe Det. Greg Bacon “said officers won’t be pulling over drivers, but officers will find opportunities to engage and educate citizens on traffic laws.”

Bacon explains the “Positive Ticketing Campaign” this way: “We will be having positive conversations with citizens. Say an officer happens to stop somewhere and see somebody, and says, ‘Hey, would you mind having a conversation with me?’ [to] educate them on bicycle laws and traffic laws.” KSAZ, the Fox station in Phoenix, likewise reports that “Tempe police report they will not be pulling anyone over to give them a free drink coupon.” In a tweet this afternoon, the Tempe Police Department reiterated that officers “will not be proactively stopping vehicles, bicycles, scooters or pedestrians.”

Given that police officers across the country have been less punctilious about following the Fourth Amendment when they perceive themselves as doing nice things for people, Sikora’s initial confusion may be understandable. But her insouciance in the face of blatant constitutional violations is harder to fathom.

[Thanks to Seth Mandel for the tip.]

from Latest – Reason.com https://ift.tt/2K3gaXO

via IFTTT

This morning a Phoenix TV station aired a feel-good story about cops who are “rewarding people for good driving behavior” by pulling them over and giving them coupons for drinks at Circle K convenience stores. “If you see a Tempe police officer pulling you over,” chirped Colleen Sikora, a correspondent for the NBC affiliate KPNX, “it may not be a bad thing. If an officer sees someone following traffic laws correctly related to bicycles and pedestrians, they can pull you over, but instead of a citation, you’ll get a free drink coupon for either a cold drink or hot beverage…They’re kicking off the campaign this morning at 8 a.m., so if you see police lights in your rear view mirror, maybe hold off on the panic.”

For anyone who values the Fourth Amendment, which requires reasonable suspicion of a crime or traffic violation to justify forcibly detaining a motorist, the program described by Sikora is definitely “a bad thing.” That sentiment is clearly shared by viewers who reacted to the story on Twitter. “This is an insanely bad & illegal idea,” one commented. “This is actually illegal,” observed another.

To its credit, the Tempe Police Department seems to recognize that stopping motorists because they are not committing any traffic violations would be unconstitutional. According to the written version of the story on the KPNX website, bylined by Sikora herself, Tempe Det. Greg Bacon “said officers won’t be pulling over drivers, but officers will find opportunities to engage and educate citizens on traffic laws.”

Bacon explains the “Positive Ticketing Campaign” this way: “We will be having positive conversations with citizens. Say an officer happens to stop somewhere and see somebody, and says, ‘Hey, would you mind having a conversation with me?’ [to] educate them on bicycle laws and traffic laws.” KSAZ, the Fox station in Phoenix, likewise reports that “Tempe police report they will not be pulling anyone over to give them a free drink coupon.” In a tweet this afternoon, the Tempe Police Department reiterated that officers “will not be proactively stopping vehicles, bicycles, scooters or pedestrians.”

Given that police officers across the country have been less punctilious about following the Fourth Amendment when they perceive themselves as doing nice things for people, Sikora’s initial confusion may be understandable. But her insouciance in the face of blatant constitutional violations is harder to fathom.

[Thanks to Seth Mandel for the tip.]

from Latest – Reason.com https://ift.tt/2K3gaXO

via IFTTT

One of the many virtues of markets is their ability to turn seemingly intractable conflicts into mutually beneficial trades. For evidence, look no further than a real estate deal in New York City that has managed to make peace between a housing developer and some would-be NIMBYs.

Last week, The New York Timespublished a story about the residents of a 12-story loft building in Manhattan’s Chelsea neighborhood who, faced with the prospect of a new condo building that would block their view of the Empire State Building, decided to bargain rather than litigate.

The building’s inhabitants offered to buy the air rights from their neighborhood developer for $11 million. Residents on the upper floors paid up to $1 million, people on the lower floors paid less, and those on the bottom floor paid nothing at all. People who didn’t have the cash to pay their full share relied on loans from their neighbors.

In return, developer Gary Barnett ceded his right to build anything other than a three- or four-story structure on his property.

“It’s not common,” Barnett told the Times. “Most of the time, they sue you and try and stop you somehow. These people stepped up to the plate and paid market value for the building rights.”

It’s true that conflicts over new developments are rarely worked out so harmoniously. Often, view-conscious property owners resort to legal or administrative action in order to either stop an unwanted project from going forward or delay things long enough to force a developer into making concessions.

One reason for this is that it’s often much cheaper to weaponize the planning process and the legal system than to work out a voluntary agreement. The stricter a city’s land-use regulations and the more discretion its planning process gives bureaucrats, the more appealing the former option becomes.

In San Francisco, for example, the planning process heavily favors community input over property rights, and planning officials have a lot of power to layer conditions on new developments beyond the city’s already exacting zoning code requires. In addition, California environmental laws make it possible to slow things down with administrative appeals and lawsuits that can take months, if not years, to recolve. With this setup, it’s no surprise that NIMBYs there rely on courts and bureaucracies rather than negotiating like the Chelsea residents.

Reason has covered a number of cases of NIMBY strong-arming in San Francisco, including when a totally zone-compliant single-family home was delayed for more than a year because neighbors resented the loss of a garden that the new house would replace. There have also been multiple cases where apartment projects were delayed because the new buildings would cast shadows.

In each case, project opponents could have tried to buy the land the offending project was to be built on. Or, like the Chelsea residents, they could have offered the developer cash compensation to build a smaller building that would cast fewer shadows.

One benefit of market arrangements like the one described in the Times story is that people have to actually put a price on these competing uses. The relative costs and benefits of building new housing over preserving a great view can be hashed out, and a mutually beneficial outcome can be reached. But when land use regulations stop these normal market mechanisms from functioning, competing interests are funneled into bureaucratic systems where the process is driven by politics and decisions have clear winners and losers. The result is an incessant conflict.

from Latest – Reason.com https://ift.tt/2KfhO7D

via IFTTT

Jon McNeill, Lyft’s Chief Operating Officer, has unexpectedly left the company, according to Bloomberg.

Lyft is having so much trouble retaining a COO that the company has said it won’t hire a replacement for McNeill. The company has struggled to keep top lieutenants in past years, with McNeill’s predecessor, former Amazon executive Rex Tibbens, lasting less than three years.

Prior to working at Lyft, McNeill spent two and half years working at Tesla, directly under Elon Musk. His title at Tesla was president of global sales and service. Upon his hiring at Lyft, the company touted his experience and welcomed him to the “Lyft family”. Since then, of course, the company has gone public and seen its stock trade about 10% lower than its IPO price.

Lyft founders Logan Green and John Zimmer said in a email that McNeill’s role and responsibilities will be reassigned to other employees, while crediting him with establishing new businesses, including car repair shops for Lyft drivers.

The e-mail stated: “As JMac moves on to his next chapter, we wish him the very best.”

Shares of Lyft fell nearly 4% in mid-day Monday trading on the news, before paring their losses.

via ZeroHedge News https://ift.tt/2K0qRKG Tyler Durden

“American exceptionalism has led to a country that is exceptionally un-self-aware.” – Peter Thiel

The economic contraction ahead will put this borderline psychotic country through some interesting ch-ch-ch-changes. Mr. Trump now fully owns the Potemkin status quo of record stock markets poised against a withering rot of human capital at the core of an industrial society in sunset mode. Leadership at every corner of American life – politics, business, media – expects an ever-higher tech magical updraft of fortune from an increasingly holographic economy of mere fugitive appearances in which everybody can get more of something for nothing. The disappointment over how all this works out will be epic.

Globalism is wobbling badly. It was never what it was cracked up to be: a permanent new plateau of exquisitely-tuned international economic cooperation engineered to perfection. It was just a set of provisional relations based on transient advantage. As it turned out, every move that advantaged US-based corporations blew back ferociously on the American public and the long-term integrity of the social order. Sinister as it seems, the process was simply emergent: a self-organizing evolution of forces previously set in motion. And, like a lot of things in history, it seemed like a good idea at the time.

“Off-shoring” US industry jacked up corporate profits while it decimated working class livelihoods. In return, that large demographic got “bargain shopping” at Walmart, a life of ever-upward revolving debt, and dead downtowns. The country got gigantic trade deficits and government debt loads. In effect, globalism compelled America to borrow as much as possible from the future to keep running things the way they were set up to run. Now, there is just suspicion that we’ve reached the limits of borrowing. Soon it will be a fact and that fact will upend everything we’ve been doing.

You can see how this is playing out in politics, especially the proposed government-enforced redistribution of whatever wealth is supposed to be left. Of course, much of that wealth is a figment, represented in abstract financial instruments pegged to “money” that may have a lot less value than presumed. The Democratic Party detects opportunity in the gross imbalances of this notional capital and so they are promising every conceivable form of grift to voters from a guaranteed basic income and free medical care and college education to reparations for the descendants of slaves.

They certainly might win the 2020 election on the basis of that proffer, but good luck scaring up the actual financial mojo to make it happen without destroying whatever value remains in the US dollar. The predicament may be aggravated by foreign capital seeking refuge in US financial markets as the banking systems in China and Euroland unwind, giving politicians the false impression that other people’s money belongs to Americans. And anyway, what will these foreigners actually be investing in here? Collateralized loan obligations based on seven-year used-car payment schemes?

The American Left just can’t grok the fact that we missed the window of opportunity for setting up a national health system. That was a mid-twentieth century thang: cheap oil and industrial growth. Please note: it was the Democratic Party under Mr. Obama that turned the college loan industry (and Higher Ed with it) into the appalling racket it’s become, because it fit the template of a society pretending to prosper by racking up debt. That demographic of debtors will be seeking magical debt relief. If they get it, it will be at the expense of the government that took on the guaranteed backing of all that debt, now well over a trillion dollars.

Industrial growth is over, and with it the expectation that all the old debts can be paid back. A few economic commentators are predicting “stag-flation.” We’d be lucky if that’s all it turned out to be. But we’re unlikely to get a re-play of the 1970s. That was an era of geo-financial disturbance that resolved for a while with new oil from Alaska and the North Sea. That’s not going to happen again this time. Stag-flation was just a matter of going nowhere for a decade. The contraction ahead will be brutal, not going nowhere but rather going down hard to a lower and harsher standard of living.

It’s also hard to calculate how disturbing and disruptive the prosecution of the RussiaGate perps will be. If the Democratic Party is acting batshit crazy about it now after the Mueller testimony fiasco, how will they react when dozens of their partisans are marched into court to face charges of sedition. That ugly business looks on-track to collide with the coming financial distress. The result will be much more severe political turbulence than the thinking class expects.

It’s easy to imagine circumstances in which normal institutions get suspended and the old major parties are superseded by “emergency” seizures of power by other parties as yet unknown.

via ZeroHedge News https://ift.tt/2ZjOh2O Tyler Durden