Questioning Lagarde As Gross Interest Income In Germany Heads Towards Zero

Authored by Mike Shedlock via MishTalk,

Thanks to negative interest rates, Germans’ interest income has plunged towards zero.

Counterproductive Interest Rate Policy

Eric Dor, Director of Economic Studies at the IESEG School of Management in Paris emailed an article with some interesting charts regarding the Counterproductive Interest Rate Policy of the ECB.

What follows is a guest post by Dor, with my comments at the end. I added or changed some subtitles.

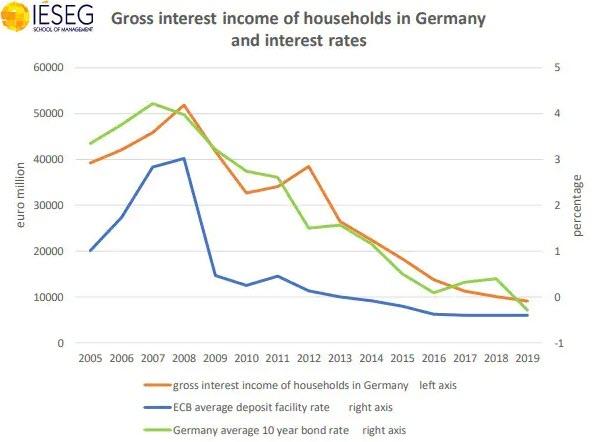

Collapse of Interest Income in Germany

The extremely accommodating monetary policy of the ECB has had huge redistributive consequences. The disposable income of savers has been hit by the collapse of the average return on their accumulated wealth invested in interest products. Low interest rates have benefited borrowers. By boosting asset prices, the decline of interest rates has also favoured the small segment of wealthy households who own securities, potentially increasing inequality.

ECB Monetary Policy

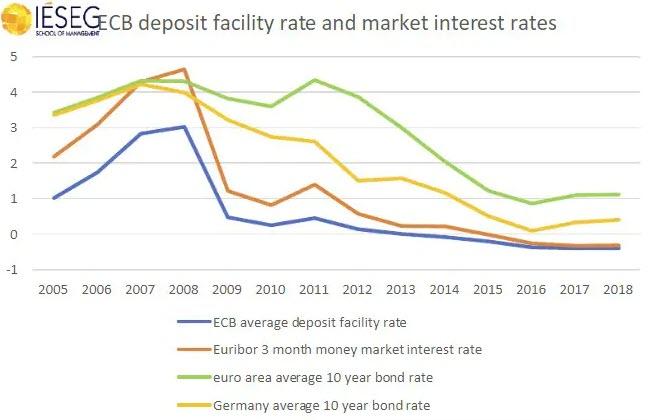

The ECB has used various instruments to push down market and bank interest rates in the euro area. The instruments used by the ECB are its traditional key interest rates, hereafter summarized by the deposit facility interest rate, recent unconventional tools like massive asset purchases known as QE, and forward guidance about the expected path of its policy. All these instruments have a decisive impact on market short term and long term interest rates, as shown on the following chart.

Money Lost and Gained

It is interesting to compute what German savers have lost by comparing their effective interest income to a hypothetical situation where they would have remained at their level of 2012. It is easily computed by adding up the difference between effective gross interest income and their level of 2012.

The monetary policy conducted after 2012 has implied a cumulative loss of gross interest income of euro 158 billion for German households until 2019.

Of course, the monetary policy has benefited German borrowing households. After 2012 and until 2019, German borrowing households “saved” a cumulative 99 billion of interest expenses. It is computed by adding up, for all the years after 2012, the difference between effective interest expenses and their initial level.

The net result is a loss of euro 58 billion to German households.

Counterproductive Policy

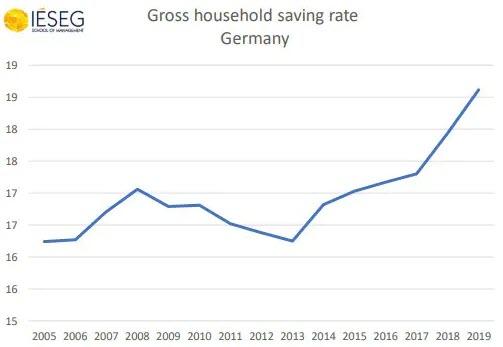

The ECB has been engineering an overall decrease of interest rates hoping that cheap credit opportunities would lead households and companies to increase their spending. The problem is that this policy may lead to the opposite result, if households decide to offset declining returns on savings by saving more.

Evidence shows that it is what happens in Germany. The saving rate of households has been continuously increasing since 2014.

German Savings Rate

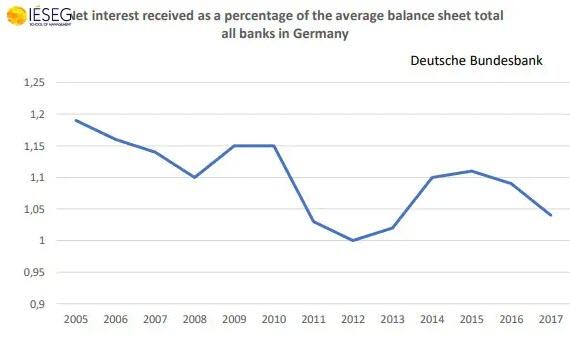

Banks Harmed

Low or negative interest rates are also decreasing the net interest income of banks. It threatens their profitability perhaps decreasing their supply of loans to the private sector.

End Dor Article

On August 30, I commented Lagarde Praises Negative Rates, Study Shows They Reduce Lending

This common-sense report by Dor also strongly disputes Lagarde’s view.

Twilight Zone

There is something about this statement that strikes me as Twilight Zone material

“10y yields jump to -0.59%” https://t.co/OLTgLSbaNj

— Mike Mish Shedlock (@MishGEA) September 10, 2019

Fed vs ECB

Whereas the Fed bailed out US banks by paying interest on excess reserves, the ECB charged banks interest on excess reserves draining bank profits.

Negative interest rates unquestionably hurt EU banks and there is no evidence of Lagarde’s proposed counter-benefits.

A European banking crisis awaits.

Tyler Durden

Thu, 09/12/2019 – 03:30

via ZeroHedge News https://ift.tt/2LRzsz8 Tyler Durden