Producer Prices Rise More Than Expected In August As Luxury Hotel Costs Soar

Both headline and core producer prices rose more than expected in August.

PPI +1.8% YoY (+1.7% exp)

PPI Core +2.3% (+2.2% exp)

Source: Bloomberg

With a major divergence continuing between goods and services pricing…

Source: Bloomberg

Under the hood shows a mixed message:

A major factor in the increase in prices for final demand services was the index for guestroom rental, which moved up 6.4 percent.

Source: Bloomberg

The indexes for fuels and lubricants retailing; apparel, footwear, and accessories retailing; chemicals and allied products wholesaling; gaming receipts (partial); and insurance also advanced. Conversely, margins for machinery and vehicle wholesaling declined 4.2 percent. The indexes for health, beauty, and optical goods retailing and for support activities for oil and gas operations also decreased.

Almost two-thirds of the August decline in the index for final demand goods can be traced to prices for gasoline, which dropped 6.6 percent. The indexes for fresh and dry vegetables, diesel fuel, corn, home heating oil, and ethanol also moved lower. In contrast, prices for meats advanced 3.0 percent.

People have been talking about a “debt bubble” for some years now. They’ve been right, of course, based on the combination of surging borrowing and plunging rates.

But the bubble hasn’t stopped inflating, and recently it entered what sure looks like a terminal blow-off stage. Some highlights:

Though July, China’s total debt rose by $2 trillion, a year-over-year increase of 26%. And this month the Chinese government cut bank reserve requirements in an attempt to further rev up lending.

A recent week of corporate bond issuance was “the biggest weekly volume to hit global markets on record,” according to Dealogic. US investment-grade companies raised $72 billion across 45 deals, equaling the total issued in all of August.

Numerous companies issued 30-year bonds with yields below 3%, which used to be the province of safe haven governments. Even Apple, which is sitting on an epic pile of cash, borrowed money.

At the other end of the spectrum, junk bond issuer Restaurant Brands, which owns the Popeyes and Burger King chains, sold 8.5-year bonds with a coupon under 4%, a record low yield for a US junk issuer.

In Europe sales of new bonds hit $1 trillion earlier than in any previous year. Fully a third of European investment-grade bonds (and some junk bonds) now trade with negative yields. And the ECB is expected to cut rates further at its upcoming meeting.

Why is all this happening? Three reasons:

1) Virtually all the world’s central banks are now easing, sending interest rates to record lows in most major markets. The lure of this ultra-cheap money is proving irresistible even to borrowers who don’t immediately need cash.

2) The world is looking increasingly scary, what with trade wars, military brinkmanship in Asia and the Middle East, and the hint of an incipient global recession. So a massive cash hoard is increasingly seen as a good thing to have.

3) Bubbles generally end this way, with everyone just giving up on self control and grabbing for one last piece of easy money.

All three of these rationales will probably turn out to be mistaken. But that’s just how it goes in financial manias. As Credit Bubble Bulletin’s Doug Noland notes, “It’s difficult to envisage a more manic bond market environment – at home or abroad.”

US Futures Drift, Global Markets Rally As China Takes Steps To Ease Trade War

S&P500 futures were perfectly unchanged in an oddly quiet session, failing to be inspired by a ramp in European and Asian stocks, after China announced exemptions from the 25% extra tariffs put in place last year in some product categories such as pharmaceuticals and lubricant oil, in a move that is being viewed as a good will concession by China to restart the trade negotiation on good terms in October. While this has lifted sentiment in Asia and Europe, combined with a technical rebound generally in equities…

… it failed to inspire a move in US futures, while US 10Y rates appear to have peaked at 1.74% overnight and with rate locks on a record $100 billion in investment grade issuance now in the rearview mirror, expect 10Y yields to resume their slide in the coming days.

Much of Europe’s gains came on the back of the tremendous momentum-to-value shift, which according to JPM’s Marko Kolanovic has “only occurred on two days in history“, with Europe’s Stoxx 600 Index benefiting from the strong rotation into cyclical sectors that had lagged behind this year, such as automaker and banking shares.

Leading the rally in equities was once again Japanese equities with Nikkei futures up 1.1% erasing the losses from the intermediate peak in July. The lift was broad based with Asian stocks gaining, led by financial firms and material producers, as investors assessed signs that China will move to lessen the trade war’s impact and awaited the European Central Bank’s policy decision on Thursday. Asian equities jumped in Japan and Hong Kong after the infamous twitter troll, Global Times editor Hu Xijin said in a Twitter post, that China will implement measures to ease the trade war’s impact on the world’s second-biggest economy. The moves planned by Beijing will benefit some companies from China and the U.S., Xijin said.

As a result, most markets in the region were up, with Japan and Singapore pacing gains. The Topix advanced 1.7% to a two-month high, as Japanese banks continued to rally following a rebound in U.S. Treasury yields. A weaker yen helped buoy shares of Japanese exporters. The Shanghai Composite Index dropped 0.4%, with Kweichow Moutai and Jiangsu Hengrui Medicine among the biggest drags. Haitong Securities led brokerages higher after China scrapped foreign investment limits in stock and bond markets. South Korean infrastructure shares outperformed after the departure of President Donald Trump’s national security adviser, spurring speculation the U.S. may show conciliatory gestures toward China and North Korea.

As Saxo Bank highlighted recently, economic surprises have become less and less negative with Citi’s Economic Surprise Index G10 turning almost positive. If we are right that central banks will deliver enough monetary stimulus, with ECB starting tomorrow, and macro data begin to surprise positively then the rally could continue.

Equities have rebounded sharply in September on hopes for fresh monetary stimulus from the ECB on Thursday (as long as there is bank tiering included in the package) and the Fed next week, while market-supportive measures by China helped lift sentiment.

“We are primed for a little bit of disappointment,” Investec’s Jeff Boswell told Bloomberg TV in Singapore. “On the QE front, whilst we’ve been expectant of something – certainly on the corporate bond-buying side that the market’s been expecting – it is unlikely to come tomorrow.”

In rates, treasury 10-year notes and similar German bunds drifted, after their yields earlier on Wednesday touched one-month highs. After hitting a session high of 1.74%, the 10Y Treasury dropped to session lows of 1.7057%, as rate locks on $100 billion of new investment grade issuance. Treasuries also halted a five-day decline as traders positioned before a pivotal eight-day period that includes meetings of the world’s three major central banks.

In FX, the yen fell for a third day after China announced measures to ease the negative impact of the trade war, reducing demand for haven assets. The pound rose, setting course for its third day of gains, as Prime Minister Boris Johnson was said to consider a fresh approach to the Irish border problem.

In commodities, oil futures climbed alongside gold.

The euro weakened, heading for its biggest drop in eight sessions.

Market Snapshot

S&P 500 futures little changed at 2,978.25

STOXX Europe 600 up 0.6% to 388.85

MXAP up 0.9% to 158.09

MXAPJ up 0.7% to 510.31

Nikkei up 1% to 21,597.76

Topix up 1.7% to 1,583.66

Hang Seng Index up 1.8% to 27,159.06

Shanghai Composite down 0.4% to 3,008.81

Sensex up 0.4% to 37,294.35

Australia S&P/ASX 200 up 0.4% to 6,638.04

Kospi up 0.8% to 2,049.20

Brent futures up 0.9% to $62.91/bbl

Gold spot up 0.4% to $1,490.99

U.S. Dollar Index up 0.2% to 98.52

German 10Y yield rose 1.0 bps to -0.537%

Euro down 0.2% to $1.1024

Italian 10Y yield rose 7.6 bps to 0.679%

Spanish 10Y yield rose 1.9 bps to 0.278%

Top Overnight News

China announced a range of U.S. goods to be exempted from 25% extra tariffs put in place last year, as the government seeks to ease the impact from the trade war without lifting charges on major agricultural items like soybeans and pork.

President Donald Trump said he fired his hawkish national security adviser, John Bolton, after disagreeing “strongly” with many of his positions, ending a tumultuous tenure marked by multiple setbacks in U.S. foreign policy.

Hong Kong Exchanges and Clearing Ltd. made a surprise $36.6 billion bid for London Stock Exchange Group Plc.

German Chancellor Angela Merkel said her government will work until the “last day” to ensure an orderly U.K. departure from the European Union but insisted Germany is ready for a no- deal Brexit.

The European Central Bank is about to turn the screws again on financial institutions by diving even deeper into negative interest rates. For holders of German and French government bonds, this week’s European Central Bank meeting is coming just in the nick of time.

President Donald Trump said he fired his hawkish national security adviser, John Bolton, after disagreeing “strongly” with many of his positions, ending a tumultuous tenure marked by multiple setbacks in U.S. foreign policy

Pound volatility is at emerging-market levels and U.K. assets are set for a substantial repricing once the Brexit outcome becomes known, according to Bank of England Governor Mark Carney

A cross-party group is seeking a way out of the Brexit “nightmare” by working together to find a deal that can secure a majority in Parliament, suggesting a Northern Ireland- only backstop may be one answer

Asian equity markets eventually traded mostly higher as the region shrugged-off the indecision from Wall St, which had been subdued by the continued global bond rout and tentativeness ahead of this week’s ECB. ASX 200 (+0.3%) and Nikkei 225 (+1.0%) were higher but with gains in Australia capped as the outperformance in mining names was counterbalanced by weakness in tech, while Tokyo exporters continued to reap the benefits of recent currency weakness and after source reports suggested BoJ policymakers could be open to additional easing measures. Advances were also seen across the Apple supply chain in Japan and Taiwan following the tech giant’s launch event where it announced a new streaming service and health app, as well as new iWatch, iPhone and iPad models. Hang Seng (+1.7%) and Shanghai Comp. (-0.4%) were mixed after a tepid PBoC liquidity effort in which the mainland failed to take impetus from China’s fresh efforts to further open its financial markets by dropping QFII and RQFII quota limits. Sources noted China is ready to sweeten a deal by buying US goods, however, the report added that a purchase agreement is no certainty and would be in exchange for a delay on tariffs as well as an easing of restrictions on Huawei. China’s Global Times Editor also later suggested China will introduce important measures to ease the impact from the trade war which would benefit some companies from both China and the US which briefly fuelled appetite for risk. Finally, 10yr JGBs were lower amid a continuation of the global bond rout which was partly attributed to this week’s supply and heavy corporate issuances, with weaker results across all metrics in today’s 5yr JGB auction adding to the pressure.

Top Asian News

Duterte Will Ignore South China Sea Ruling for China Oil Deal

BOJ’s Dilemma Spurs Speculation on Reverse ‘Operation Twist’

Hong Kong Stocks Climb to Six-Week High as Developers Jump

Asia Apple Suppliers Rise as MS Sees IPhone Price Driving Demand

Major European bourses are broadly in the green [Eurostoxx 50 +0.5%], following on from a similar APAC lead as sentiment is supported by China releasing a tariff exemption list for the US, effective from September 17th. Items on the list will not be subject to additional tariffs imposed by China on US goods as countermeasures to trade action taken by the US, however, the list does not include corn, soybean or pork. Spain’s IBEX (U/C) is the underperformer thus far amid disappointing earnings from heavyweight Inditex (-2.9%) whilst broad-based gains are seen across the region. Sectors are mixed with defensive sectors lagging, although the energy sector also feels some headwind from yesterday’s price decline in the oil complex. Turning to individual movers, LSE (+5.6%) shares spiked higher amid reports that Hong Kong Exchanges and Clearing have proposed a combination with LSE, terms of proposed deal would imply an enterprise value of GBP 31.6bln, and the transaction implies a value of GBP 83.61 for each LSE share. LSE said its board will consider the proposal. On the flip side, Suez (-1.3%) and Kone (-1.9%) opened lower amid downgrades, although the former saw some upside amid reports that the Co. won an approx. EUR 1bln treatment contract for the Dongying China chemical plant, contract is for 50 years.

Top European News

Merkel Answers IMF, Saying Lack of Money Not Germany’s Problem

British Airways Scraps Flights as Impact of Pilot Strike Lingers

Nordea’s Wholesale Banking Unit in Need of ‘Thorough Review’

Foreign Binge on European Bonds Is Ending Just in Time for ECB

In FX, the Euro is not quite the biggest G10 loser or underperformer, but the single currency has been a notable mover after topping out above 1.1050 against the Dollar and failing to close above key resistance just below yet again (1.1049 represents a 38.2% retracement of the decline from 1.1249 to 1.0926 ytd low). Eur/Gbp selling into the early 9 am fix may also have impacted, as the cross retests recent sub-0.8925 lows, but Eur/Usd is holding around the 10 DMA and bids said to be sitting just below (at 1.1022 and 1.1020 respectively) with one eye on Thursday’s ECB meeting and some form of easing/stimulus as German institutes continue to downgrade GDP estimates, while the other keeps tabs on higher global bond yields/spreads.

JPY/CHF – More safe-haven unwinding has nudged the Yen and Franc down to circa 107.85 and 0.9940 vs the Buck, and Usd/Jpy has breached a Fib, exporter offers plus a cloud top formation in the process, at 107.49, 107.50 and 107.71, with some fundamental/macro impetus stemming from another upturn in US Treasury yields and more curve steepening against the backdrop of positive-looking US-China trade headlines (such as Chinese tariff exemptions and buying US goods as a sweetener for upcoming talks).

GBP/AUD/NZD/CAD – All narrowly mixed vs the Greenback, with Cable forming multiple/lower peaks ahead of 1.2400 and reported stops at 1.2385+ and the Aussie fading into 0.6900 and the 100 DMA at 0.6907 following another downbeat sentiment survey overnight (Westpac consumer confidence turned negative). However, the Pound has not seen much angst in wake of an official ruling in Scotland against UK PM Johnson’s Parliament prorogation, while Aud/Usd is still outpacing Nzd/Usd as the latter remains heavy on the 0.6400 handle and the Kiwi struggles to stay above 1.0700 in cross terms ahead of NZ manufacturing PMI tomorrow and Westpac’s Q3 consumer survey on Friday. Elsewhere, the Loonie is maintaining its post-Canadian jobs momentum, but finding 1.3150 a tough hurdle to overcome convincingly.

NOK/SEK – Even though crude prices remain on a roll and the Norges Bank is still on course to take another step towards policy normalisation before the Riksbank (albeit not likely next week given yesterday’s soft inflation data), Eur/Nok is hovering around 9.8850 within a 9.9010-9.8765 range in contrast to Eur/Sek nearer the base of 10.6990-6595 parameters in wake of latest Riksbank comments reaffirming tightening guidance and dismissing weaker than expected Swedish CPI/CPIF metrics.

EM – The Rand’s bull run has been derailed around 14.6100 vs the Dollar and a deterioration in SA business confidence has hardly helped as Usd/Zar rebounds to 14.7000+, even though Moody’s indicated low risk of a ratings downgrade this year.

In commodities, WTI and Brent futures are holding onto most of its intra-day gains/consolidation following yesterday’s decline which was induced by the EIA cutting its 2019 and 2020 global oil demand forecasts by 100k BPD and 30k BPD, whilst downside was exacerbated after US President Trump fired the White House National Security Advisor/known policy-hawk Bolton. Prices have rebounded and remain on an upward trajectory thus far with WTI futures around the 58.00/bbl mark whilst its Brent counterpart trades just under 63.00/bbl (at time of writing). This morning also saw the release of the OPEC Monthly Oil Report in which its 2019 global oil demand growth forecast was revised lower by 80k BPD, in-fitting with the EIA STEO, next up IEA will release its report tomorrow at 0900BST. Ahead of tomorrow’s JMMC meeting, the Iraqi Oil Minister noted that the producers will have a discussion on whether or not there is the need for a deeper production cut with OPEC+, although this was rebuffed by the Russian Energy Minister who also expressed concern regarding global economy. Novak added that the slowing global demand for oil will also be discussed at the meeting tomorrow. Elsewhere, gold prices remain capped below the 1500/oz ahead of this week’s key risk events including US CPI and the ECB rate decision, whilst copper prices are little changed with little by way of immediate catalyst. Finally, Dalian iron ore prices rose for a third session amid a decline in shipments coupled with hopes of further Chinese stimulus.

US Event Calendar

8:30am: PPI Final Demand MoM, est. 0.0%, prior 0.2%; PPI Final Demand YoY, est. 1.7%, prior 1.7%

8:30am: PPI Ex Food and Energy MoM, est. 0.2%, prior -0.1%; PPI Ex Food and Energy YoY, est. 2.15%, prior 2.1%

10am: Wholesale Inventories MoM, est. 0.2%, prior 0.2%; Wholesale Trade Sales MoM, est. 0.5%, prior -0.3%

DB’s Jim Reid concludes the overnight wrap

Yesterday was the annual day in the diary when I wake up determined to take no notice of the new Apple product launch event and go to bed with a note in my diary to be the first in the online queue a few days later. It looks like I’ll be ordering a new phone due to the enhanced camera and a new watch due to the new fitness tracking improvements. I do believe they saw me coming.

To help me count down the hours until Friday’s pre-ordering, we have the small matter of tomorrow’s ECB meeting to look forward to. As we approach this main event, the relentless sell-off in global bond markets continues to show little sign of abating just yet. In fairness it took until the final couple of hours of the European session yesterday for yields to move notably higher on both sides of the Atlantic but the move carried on well into the US close with 10y UST yields finishing +9.1 bps at 1.735% – c.6bps occurred after Europe went home. That takes the 5-session move to 27.7bps, the steepest selloff since November 2016. The 2s10s curve didn’t do a lot though, holding steady at +5.1bps. Earlier 10y Bunds closed up +3.6bps. That now means that yields have closed higher in 4 out of the last 5 sessions with the move since the September 3rd intraday low now up to +19.5bps. The moves yesterday also meant 30y Bunds (+4.5bps) closed back in positive territory at 0.042% for the first time since August 2nd. Meanwhile BTPs sold off +7.8bps and Gilts +4.8bps.

There wasn’t actually a huge amount to report with regards to yields with the main talking point coming late in the European session with yet another pre-ECB MNI article, this time suggesting that we could see the ECB delay QE “possible contingent on further economic deterioration”. The headlines got the market excited but a closer read suggested that the base case from the main source in the article was that QE was still likely to be announced.

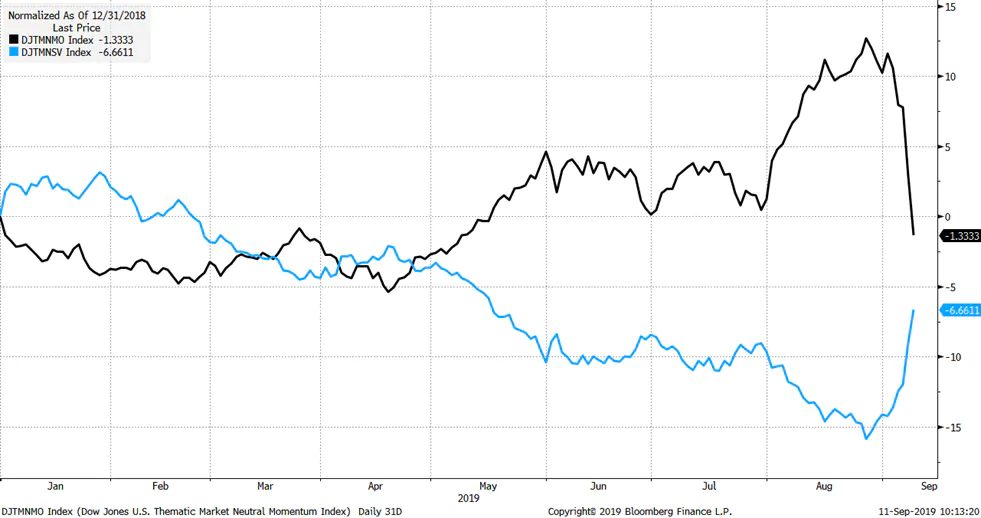

Equity markets have had an interesting couple of days where there’s been a big unwind in some popular trades. Several recent trends have reversed sharply, including momentum, growth versus value, and large versus small caps. Rising yields and steeper curves certainly contributed to the moves, but positioning had become stretched in recent months, as Binky highlighted in his report last week (link here ). To put the recent moves in context, the Bloomberg momentum index fell -1.26% to take its two-day loss to -2.51%, the worst since July 2008. Growth stocks have underperformed value by -4.09% over the last two days, the biggest shift since December 2016. Meanwhile, over the last seven sessions, growth stocks have underperformed -6.65%, the most since August 2009. Small caps have also underperformed versus large caps by 1.73% this week, the most in six weeks.

As for yesterday, the S&P 500, DOW and NASDAQ ended +0.03%, +0.28% and -0.04% respectively after a late rally but with tech names in particular struggling (-0.49%) again. Prior to this the STOXX 600 limped to a +0.10% gain thanks to a small bounce into the close although banks did rally another +1.83% owing to the rates move. This means that after bottoming out of August 15th, the rally off the intraday lows for European banks has been an impressive +14.52%. US banks are also up +11.89% over the same period. Elsewhere, in credit HY spreads were -8.7bps tighter in the US but +3.3bps wider in Europe. The talking point though has been primary and most notably for US IG where another 13 deals were announced yesterday. Amazingly we’ve seen deals from 80 borrowers since the Labour Day holiday.

Overnight in Asia markets are largely trading higher with the Nikkei (+0.88%), Hang Seng (+1.35%) and Kospi (+0.73%) all up. Chinese markets are trading lower after recovering from larger early losses – the Shanghai comp is trading flat while the CSI (-0.32%) and Shenzhen Comp (-0.25%) are trading down. 10y JGB yields are up +3.4bps this morning to -0.202% while US treasury yields are heading slightly lower across the curve after the recent run – 2y (-1.2bps), 5y (-1.3bps), 10y (-1.2bps) and 30y (-1.4bps). Elsewhere, futures on the S&P 500 are up +0.1% this morning while WTI is up +0.87% as a report from the American Petroleum Institute indicated that the US crude inventories fell by 7.23 mn barrels last week.

Sticking with Asia, China’s Global Times editor Hu Xijin said in a twitter post overnight that China will implement measures to ease the impact of the trade war while adding that the measures will benefit some companies from China and the US. Elsewhere South Korea’s trade minister said that the country will file a complaint today with the WTO against Japan’s export curbs on key materials used by the country’s chip and display makers.

Back to yesterday and in Germany Finance Minister Scholz confirmed that the budget proposed for next year (and up to 2023) is balanced. However Scholz also said that “it’s central that we’re in a position, with financial fundamentals we have, to respond with many, many billions, if indeed an economic crisis erupts”. It’s worth pointing out that the budget will likely not be passed until late November with the major political debate to take place around the ‘climate cabinet’ on the 20th of September. So there is still some chance that the budget adds new tax/spending measures to address the climate question.

As for the data, in the US the August NFIB small business optimism reading slid 1.6pts to 103.1 and a little worse than expectations for 103.5. For context though this index is still holding in relatively well compared to other surveys. Later on the JOLTS job data for July showed that job opening fell slightly for the second consecutive month, potentially signaling softer labour demand and reaching a five month low. Meanwhile, the report showed that hiring increased 0.1pp to 4.3%, which tends to be a strong leading indicator for wage inflation.

Here in the UK there was some decent wages data with basic earnings growth of +3.8% yoy (vs. +3.7% expected). The unemployment rate also edged down one-tenth to 3.8% after expectations were for no change. It’s worth noting that headline wages are now back in line with pre-crisis levels albeit boosted by historic revisions to the June data. Another puzzler for the BoE to square with the weaker demand data. Staying with the UK, Governor Carney sounded slightly hawkish yesterday, saying specifically that he doesn’t view negative rates as a tool in the UK. This backs up comments from Vlieghe on Monday.

To the day ahead now, which is another quiet one for data with little of note this morning while in the US the highlight is the August PPI report. Later on we’ll also get the final July wholesale inventories and trade sales prints. Away from that we get the Poland rate decision and OPEC monthly oil market report.

One day before the ECB is expected to cut rates further into negative territory and restart sovereign debt QE, moments ago president Trump resumed his feud with the Fed piling more pressure on Powell to cut rates “to ZERO or less” because the US apparently has “no inflation”, while also crashing the conversation over whether the US should issue ultra-long maturity debt (50, 100 years), saying the US “should then start to refinance our debt. INTEREST COST COULD BE BROUGHT WAY DOWN, while at the same time substantially lengthening the term.”

At least we now know who is urging Mnuchin to launch 50 and 100 year Treasuries. What we don’t know is just what school of monetary thought Trump belongs to – aside from Erdoganism of course – because while on one hand Trump claims that “we have the great currency, power, and balance sheet” on the other the US president also claims that “the USA should always be paying the lowest rate.” In a normal world, the strongest economy tends to pay the highest interest rate, but in this upside down world, who knows anymore, so maybe the Fed has just itself to blame.

Trump’s conclusion: “It is only the naïveté of Jay Powell and the Federal Reserve that doesn’t allow us to do what other countries are already doing. A once in a lifetime opportunity that we are missing because of “Boneheads.”

….The USA should always be paying the the lowest rate. No Inflation! It is only the naïveté of Jay Powell and the Federal Reserve that doesn’t allow us to do what other countries are already doing. A once in a lifetime opportunity that we are missing because of “Boneheads.”

One parting thought: if Bolton was fired for disagreeing with Trump over the Taliban, we wonder just how stable Powell’s job will be once the market actually drops.

Hong Kong Exchange Offers To Buy London Stock Exchange For $40 Billion

Hong Kong Exchanges and Clearing, the third-largest stock-exchange group in Asia, has offered to buy the London Stock Exchange for £20.45 a share in cash and 2.495 newly issued HKEX shares in a deal that would spoil LSE’s planned merger with data provider Refinitiv, according to the Financial Times.

HKEX’s offer values LSE at £83.61 a share, a 23% premium to LSE’s closing price on Tuesday. LSE shares climbed as much as 16% before paring gains to trade 5.9% higher after HKEX made its surprise $36.6 billion bid for the UK-based exchange group. LSE later said in a statement that it “remains committed to” its proposed acquisition of Refinitiv.

If the deal were to be completed, it would be by far the largest in the history of HKEX, which previously bought the London Metal Exchange for £1.4 billion in 2012.

“Bringing HKEX and the London Stock Exchange together will redefine global capital markets for decades to come,” said Charles Li, chief executive of HKEX. “Both businesses have great brands, financial strength and proven growth track records. Together, we will connect East and West, be more diversified and we will be able to offer customers greater innovation, risk management and trading opportunities.”

Per the FT, Li is trying to make HKEX into a “department store” for investors looking to increase their exposure to China just as Beijing is trying to open its markets to more foreign investment.

“LSEG and HKEX operate some of the most significant financial infrastructure in two of the world’s most important financial markets. Together, they will create a world-leading global exchange that spans Asia, Europe and the United States,” Li said. Li added that the move was “a vote of confidence in London and the UK’s future role as a global financial center [that] strengthens the City’s hand, ensures it will benefit from growth opportunities in Asia and that it plays a leading role in the RMB becoming a major global reserve currency in the future.”

But even with the weakened pound, Louis Capital’s Ben Kelly says the deal isn’t as opportunistic for HKEX than it might seem from the outset, especially when you look at LSE’s EV/Ebitda multiple, already at historically high levels.

Kelly doesn’t expect the deal to be consummated, given issues including likely political opposition in the UK to an exchange being taken over by a Hong Kong company that is 6% owned by the state. It’s likely that, if nothing else, national security concerns will almost certainly be raised to scuttle the deal.

House Democrats are battling congressional Republicans and the White House over the Pentagon’s budget. The question that divides them is whether the United States should spend too much on national defense, or way too much.

President Donald Trump has asked Congress for $750 billion, nearly $35 billion more than last year and enough to guarantee that the country remains atop the global leaderboard for military spending. Both Republicans and Democrats in the Senate are on board, passing a $750 billion bill, 86–8, in June. But this princely sum has hit a roadblock in the House, where the Democratic majority instead passed a bill allocating a mere $733 billion to the military.

In response, Republicans have rushed to the rhetorical ramparts.

“House Democrats are forcing our troops to pay the price for their political disputes with the president,” said Rep. Mac Thornberry (R–Texas), the ranking member on the House Armed Forces Committee, in a statement to Politico.“It is irresponsible in the midst of a war to tie the Pentagon’s hands by cutting these funds while we have Special Operators, as we speak today, in 72 countries,” said Rep. Michael Waltz (R–Fla.). A policy statement from the White House warned that spending only $733 billion would “not fully support critical national security priorities.” Were such a bill to make it to his desk, Trump said he would veto it.

The Republicans are making a lot of noise over nothing. Rep. Adam Smith (D–Wash.), chairman of the House Armed Services Committee, has stressed how little daylight there really is between these dueling spending proposals. “The amount of stuff that we disagree on is probably about 2 percent of the bill,” he said in June.

Regardless of which bill ends up becoming law, the United States will continue to have the most expensive military in the world, the Defense Department will continue to be the world’s largest employer, and U.S. power to interfere in the fates of nations around the globe will remain intact. But by squabbling over relatively small differences between two overgrown bills, representatives of both parties are selling out their constituents. An ever-growing military budget is yet another illustration of the GOP’s abandonment of small-government principles. Democrats, meanwhile, remain forcefully oblivious to the actual tradeoffs necessary to build, much less sustain, the broad government safety net they desire.

Every congressional budget standoff is a distraction from the actual problem: Left unchecked, government spending can swallow the American economy. While they may disagree over just how massive the Pentagon’s budget should be, both parties are on the same page about avoiding the real conversation.

from Latest – Reason.com https://ift.tt/2N7ODqI

via IFTTT

House Democrats are battling congressional Republicans and the White House over the Pentagon’s budget. The question that divides them is whether the United States should spend too much on national defense, or way too much.

President Donald Trump has asked Congress for $750 billion, nearly $35 billion more than last year and enough to guarantee that the country remains atop the global leaderboard for military spending. Both Republicans and Democrats in the Senate are on board, passing a $750 billion bill, 86–8, in June. But this princely sum has hit a roadblock in the House, where the Democratic majority instead passed a bill allocating a mere $733 billion to the military.

In response, Republicans have rushed to the rhetorical ramparts.

“House Democrats are forcing our troops to pay the price for their political disputes with the president,” said Rep. Mac Thornberry (R–Texas), the ranking member on the House Armed Forces Committee, in a statement to Politico.“It is irresponsible in the midst of a war to tie the Pentagon’s hands by cutting these funds while we have Special Operators, as we speak today, in 72 countries,” said Rep. Michael Waltz (R–Fla.). A policy statement from the White House warned that spending only $733 billion would “not fully support critical national security priorities.” Were such a bill to make it to his desk, Trump said he would veto it.

The Republicans are making a lot of noise over nothing. Rep. Adam Smith (D–Wash.), chairman of the House Armed Services Committee, has stressed how little daylight there really is between these dueling spending proposals. “The amount of stuff that we disagree on is probably about 2 percent of the bill,” he said in June.

Regardless of which bill ends up becoming law, the United States will continue to have the most expensive military in the world, the Defense Department will continue to be the world’s largest employer, and U.S. power to interfere in the fates of nations around the globe will remain intact. But by squabbling over relatively small differences between two overgrown bills, representatives of both parties are selling out their constituents. An ever-growing military budget is yet another illustration of the GOP’s abandonment of small-government principles. Democrats, meanwhile, remain forcefully oblivious to the actual tradeoffs necessary to build, much less sustain, the broad government safety net they desire.

Every congressional budget standoff is a distraction from the actual problem: Left unchecked, government spending can swallow the American economy. While they may disagree over just how massive the Pentagon’s budget should be, both parties are on the same page about avoiding the real conversation.

from Latest – Reason.com https://ift.tt/2N7ODqI

via IFTTT

China Waives Tariffs On 16 Types Of US Goods In Latest Attempt To ‘Sweeten’ Trade Deal

For the first time since the US-China trade war began, Beijing has waived import tariffs on more than a dozen US goods, FT reports.

Beginning Sept. 17, China will exclude tariffs on 16 types of US exported goods for one year – a sign of good will ahead of talks between US and Chinese trade delegations.

Cancer drugs, lubricant oils and a handful of chemicals which China either doesn’t produce itself or can’t easily replace by buying from other countries made it on the list.

No major US items, like soybeans or pork, were included in the list of excluded items, as Beijing has turned to other countries like Argentina and Brazil to source many of these products.

China’s State Council, which made the announcement, said it expects to release more lists of exempted goods in the near future, according to CNN.

Ahead of a trip to Washington by China’s top trade negotiators next month, lower-level Chinese delegates are expected to resume talks with their US counterparts this week or next.

Ultimately, the Chinese are hoping to see Washington roll back the ‘black-listing’ of Huawei.

“The Chinese are waiting to see what the US does on Huawei,” said one person briefed on the talks.

The next round of US tariff hikes is expected to take effect on Oct. 1, the same day that the CCP will celebrate its 70th anniversary of the founding of the People’s Republic of Chin in 1949.

Yesterday, US stocks pumped, then dumped, on the ‘old’ news that Beijing would try to “sweeten” the deal for the US by buying more agricultural products.

Russia is considering the notion that oil prices may be as low as $25 per barrel in 2020, the country’s central bank said in its new forecast published on Monday, as cited by Reuters.

Russia’s Central Bank has forecast in its macroeconomic forecast that oil could possibly hit that low due to falling demand for oil and oil products worldwide, as well as from disappointing global economic growth.

The doom and gloom scenario was just one proposed by the bank. If that risk scenario actually materializes, Russia’s inflation could increase to 7% or 8% next year, on the back of falling gross domestic product to 1.5%– 2%.

Russia is perhaps uniquely positioned to withstand low oil prices, although $25 per barrel is pretty bleak.

Source: Bloomberg

One of the reasons why Russia is more impervious to low oil prices compared to its competition is that its currency weakens when oil prices fall. This provides some type of a cushion – at least to some extent – for its lower oil revenues. Russian oil companies can pay their expenses in this weaker ruble, but still rakes in US dollars for its oil exports. Further allowing it to withstand lower prices, are that Russia’s oil company’s taxes are designed to be less as oil prices fall.

So much so is Russia’s ability to adapt to lower oil prices, that it actually struggles with higher oil prices, which dent demand for its oil. Russia’s budget for 2019 was based on $40 oil. Meanwhile, Saudi Arabia needs $80 – some say even $85 – per barrel.

In August, Russia said its 2019 budget breakeven was at a Urals price of $49.20 – the lowest breakeven in more than a decade. This has Russia and Saudi Arabia – colleagues in the current production quotas designed to rebalance the market—at odds, and likely working toward perhaps different goals.

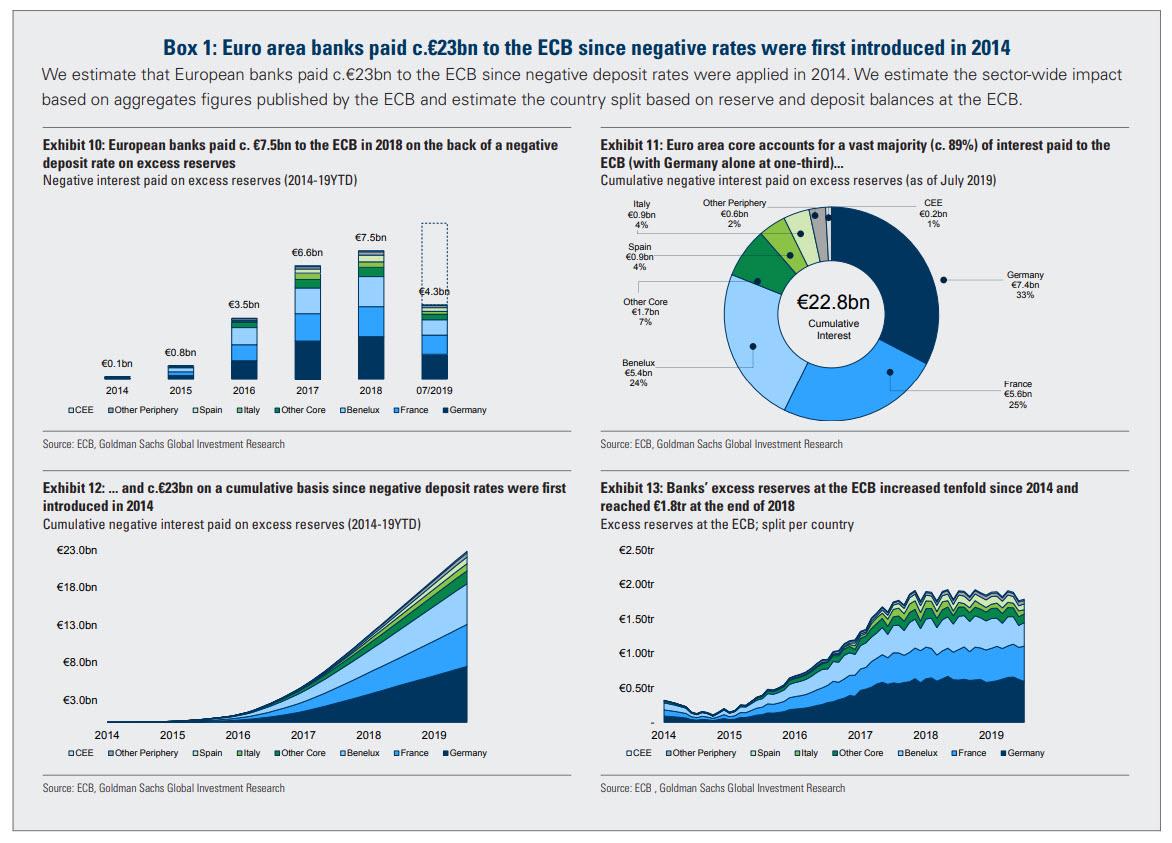

Since 2014, European Banks Have Paid €23 Billion To The ECB… And Now Face Disaster

Earlier this morning, there was an added wobble in European bond prices after an unconfirmed MNI report said the ECB could delay the launch of QE on Thursday and make it data dependent. While skeptics quickly slammed the story, saying it was just a clickbait by MarketNews…

About this MNI story on a possible delay in ECB QE announcement:

1) No substance, including from the ECB “sources”

2) Let’s hope the story is as accurate as the previous ones

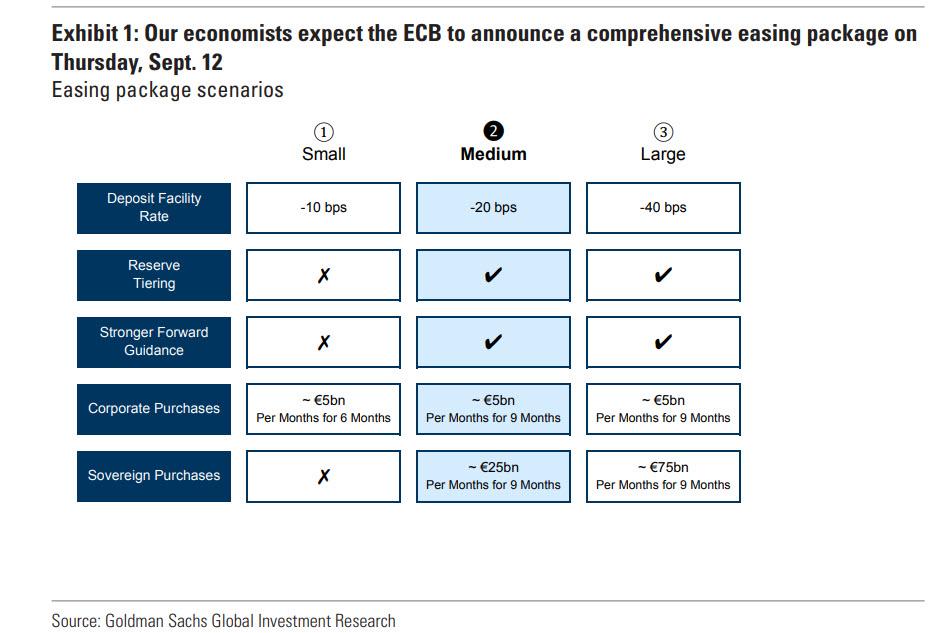

… it does highlight just how sensitive the bond market is to an announcement of aggressive easing by the ECB when it meets on Thursday, Sept 12, where consensus generally expects a significant easing package, including a -20bp rate cut (followed by -10bp cut later on), coupled with roughly €30 billion in sovereign debt QE for 9-12 months, coupled with enhanced forward guidance.

The three package expectations (small, medium, large) by Goldman analysts are laid out below:

There is just one problem: while it is unclear if any further easing by the ECB will do anything to stimulate the Eurozone economy, one thing is certain – further easing will only cripple Europe’s banks. In fact, as Goldman writes in its ECB preview, “further rate cuts are a very uncomfortable prospect for the [banking] sector” and estimates that a -20bp cut could lead to an aggregate €5.6bn (-6%) profit cut for 32 €-banks under the bank’s coverage; worse, a further -10bp cut, as per GS macro forecasts, increases the hit to -10% (-€8.3 bn). Overall, 19 banks in Goldman’s coverage face a >10% EPS cut, and 8 banks face as much as a 20% EPS hit.

Then there is Europe’s head on collision with a recession: the weakening rate outlook has been accompanied by >20% fall in €-bank shares (SX7E) since 2H18 and -4% cuts to their consensus Net Interest Incomes (for 2020E). According to Goldman, so far ~40% of the share price decline could be explained by NII cuts; the rest falls into the ‘other’ domain, “where political risk features notably.”

Here is the problem in one sentence, and chart: since negative rates were intorduced in 2014, European Banks have paid €23BN to the ECB!

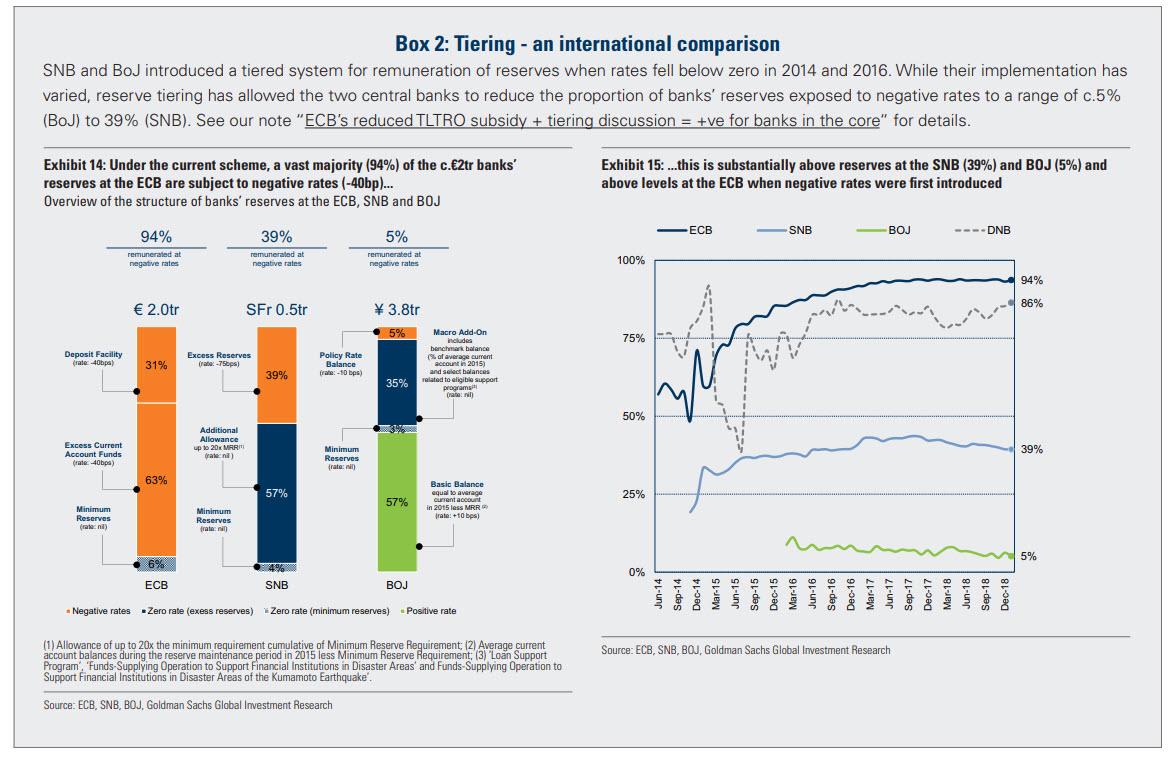

So to avoid a further banking sector, deterioration Goldman warns that “it’s critical that tiering accompanies further rate cuts if a large profit hit for the sector is to be avoided. A -20bp cut could lower €-banks EPS by ~6%. A tiering with efficiency on par with SNB scheme could offset ~30% of the hit.”

So the big question for Thursday is whether the ECB will also introduce rate tiering at the same time as it eases more.

On this topic, Goldman economists note that the implementation of the ECB’s new scheme is likely to be structured based on a multiple of minimum reserves held by individual banks (SNB model) or on a fraction of their actual excess reserve holdings (BOJ). Their baseline assumption is a two-tiered system, with one tier remunerated at the MRO (currently 0%), similar to minimum reserves, and a second tier charged at the prevailing DFR. They expect c. 50% of excess reserves to be priced at the DFR level.

In Goldman’s view, tiering is a critical part of any incremental easing package. As we have argued before, without it, an extremely challenging operating environment becomes worse, and may push an increased number of banks towards breakeven, or even loss-making territory. However, not all tiering is the same, and the schemes currently in use vary greatly in the extent of the offset/relief they provide to banks.

Key questions for bank investors ahead of the ECB meeting revolve around these following issues:

1. Could ECB’s tiering efficiency be on par with the Swiss or Japanese approach? The Swiss-like approach to tiering is Goldman’s baseline scenario (where c. 60% of deposit balances are exempt from negative rate), but it offers less relief for banks compared to the Japanese approach (>90%).

2. Would tiering be applied to the incremental cut (-20bp) only, or the full -60bp? In other words, would the tiered rate be set at the level of the MRO (0%) or lower. In our view, an offset for the entire -60bp is key. Goldman estimates that a scheme with efficiency on par with a ‘Swiss model’ with a relief applied retrospectively to a full negative rate (-60bps) has scope to shield ~⅓ of a fully-loaded impact of a 20bp rate cut for the Euro area banks under our coverage.

If rates on aggregate fall by -30bp, we calculate that the ‘tiering shield’ would be closer to 25-30% of the aggregate hit. It’s also important to note that even with tiering a 20-30bp rate cut is ultimately profit negative – when fully loaded. The relief it brings, however, is front-loaded leading to a near-term neutral impact for the aggregate.

In short: with the sellside analysts more focused on what the ECB will do to offset the adverse impact of its additional easing – as Europe inevitably careens to the reversal rate of roughly -1%, beyond which it’s game over for central banks – one wonders: just why is the ECB doing anything at all, if the biggest consideration is what it will do to offset the damage it creates by “fixing” things?