Intervention… In Extremis

Authored by Sven Henrich via NorthmanTrader.com,

The Fed has gone into full intervention mode. Not only into full intervention mode, but accelerated intervention mode. Not just a little “mid cycle adjustment” but full bore daily interventions to the tune of dozens of billions of dollars every single day. What’s the crisis? After all we live in the age of trillion dollar market cap companies, unemployment at 50 year lows and yet the Fed is acting like the doomsday clock has melted as a result of a nuclear attack.

Think I’m in hyperbole mode here? Far from it.

Unless you think the biggest repo efforts ever by far surpassing the 2008 financial crisis actions are hyperbole:

What is the Fed not telling us?

I’m asking for a friend. pic.twitter.com/BZK0XuLloV— Sven Henrich (@NorthmanTrader) October 23, 2019

What indeed is the Fed not telling us?

Something’s off here. See it all started as a temporary fix in September when suddenly the overnight target rate jumped sky high and the Fed had to intervene to keep the wheels from coming off. Short term liquidity issues they said. Well those look to have become rather permanent:

And these liquidity injections are absolutely massive. Just yesterday the Fed injected $99.9 billion in temporary liquidity into the financial system and $7.5 billion in permanent reserves as part of its $60 billion per month in treasury bills buying program. The $99.9 billion coming from $64.90 billion in overnight repurchase agreements and $35 billion in repo operations.

All this action is surprising frankly. What stable financial system requires nearly $100B in overnight liquidity injections. The Fed did not see the need for these actions coming. They are reacting to a market that suddenly requires it. Funding issues Jay Powell called it in October. The Fed was totally caught off guard when the overnight financing rate suddenly jumped to over 5% and they’ve been reacting ever since which pretty much describes the Fed in all of 2019.

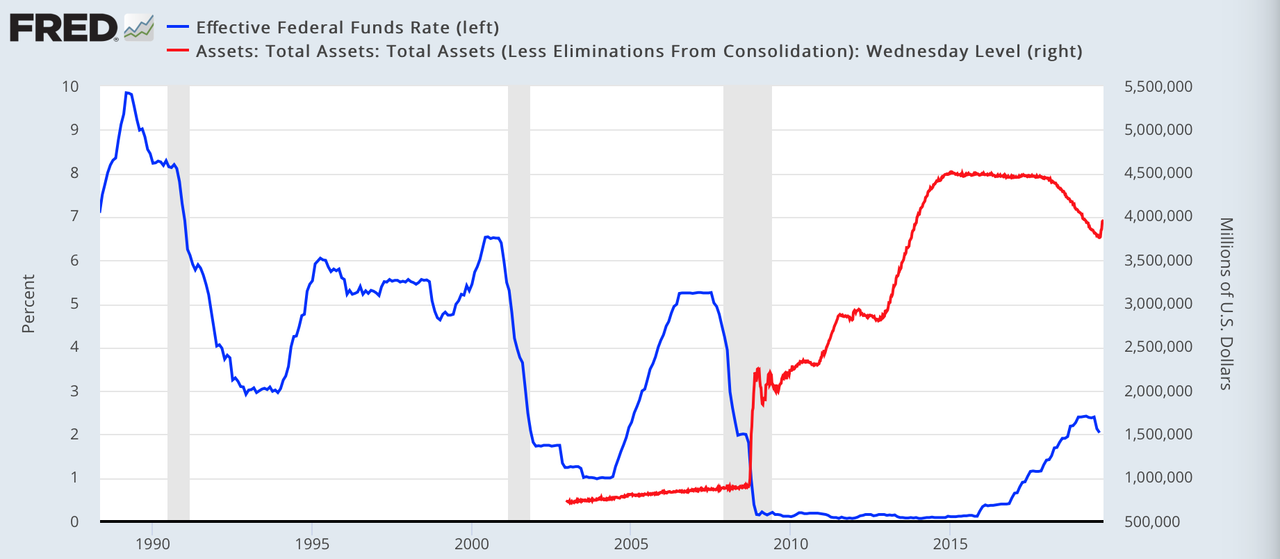

What started as a slow walk in policy reversion from last year’s rate hike cycle and balance sheet roll-off (QT) on autopilot has now turned into full blown ongoing rate cuts and balance sheet expansion:

And be clear: This is not a temporary jump in the balance sheet, this is the beginning of something big. The Fed’s balance sheet looks to expand to record highs once again.

Not a mid cycle adjustment.

I keep questioning the efficacy of all this and I have to question the honesty of the Fed. After all they keep chasing events and their policy actions are turning ever more aggressive while insisting on everything being fine. Their actions are saying things are not fine. Far from it. Otherwise they wouldn’t be forced into all these policy actions. But would the Fed cop to things not being fine? To do would be to sap confidence. Can’t have that.

What in fact would markets look like without all these policy interventions? One can only wonder. Well, we know the overnight financing rate would be much higher. This is after all why the Fed is forced to intervene, to keep the target rate low.

Many analysts now suggest a year end market rally to come primarily driven by the Fed as earnings growth remains lackluster and weak. If they print you must buy.

It may well be that our financial markets have permanently devolved into a Fed subsidized wealth inequality generation machine benefitting the few that own most stocks, but one has to wonder why all the rate cutting and liquidity injections have so far not been able to produce sustained new market highs.

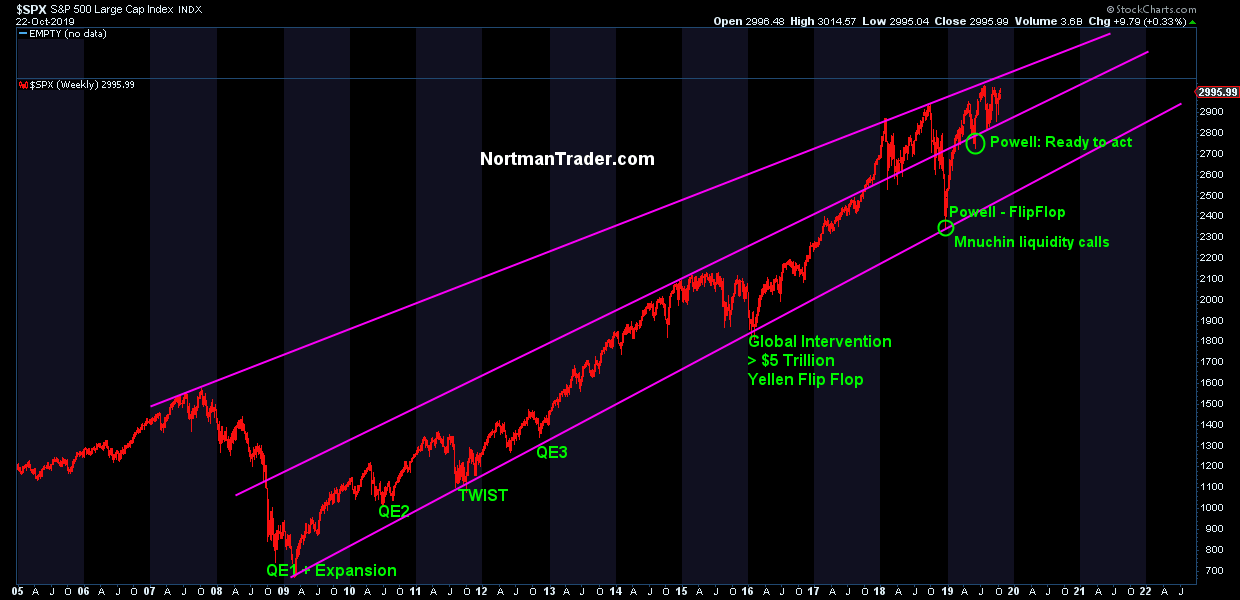

Consider the evolution of the Fed put in 2019 so far:

First came the hints in January. “Flexible on the balance sheet” Jay Powell suddenly was uttering following the Q4 2018 stock massacre producing a 3.5% market rally in one day on that pronouncement. Then we got treated to a multi month jawboning show of Fed speakers increasingly sending dovish messages and markets gladly jumped from Fed speech to Fed speech. Powell again rescued markets in early June after the May market rout. “Ready to act” was the rallying cry then and markets rallied dutifully into the July rate cut.

But then the dynamics changed. Rate cut 1 in July was sold. Rate cut 2 in September was sold. Then came repo operations also in September, now in October the $60 billion per month treasury bill buying program was announced and launched.

You note the accelerated pace of Fed actions here? We went from pausing rate hikes to ending balance sheet roll-off to multiple rate cuts and aggressive daily repos and balance sheet expansion. And all of this now since just July. And guess what? Another rate cut coming next week.

Why? Because markets want it. And what markets want markets shall receive. That’s the only data point that matters it appears.

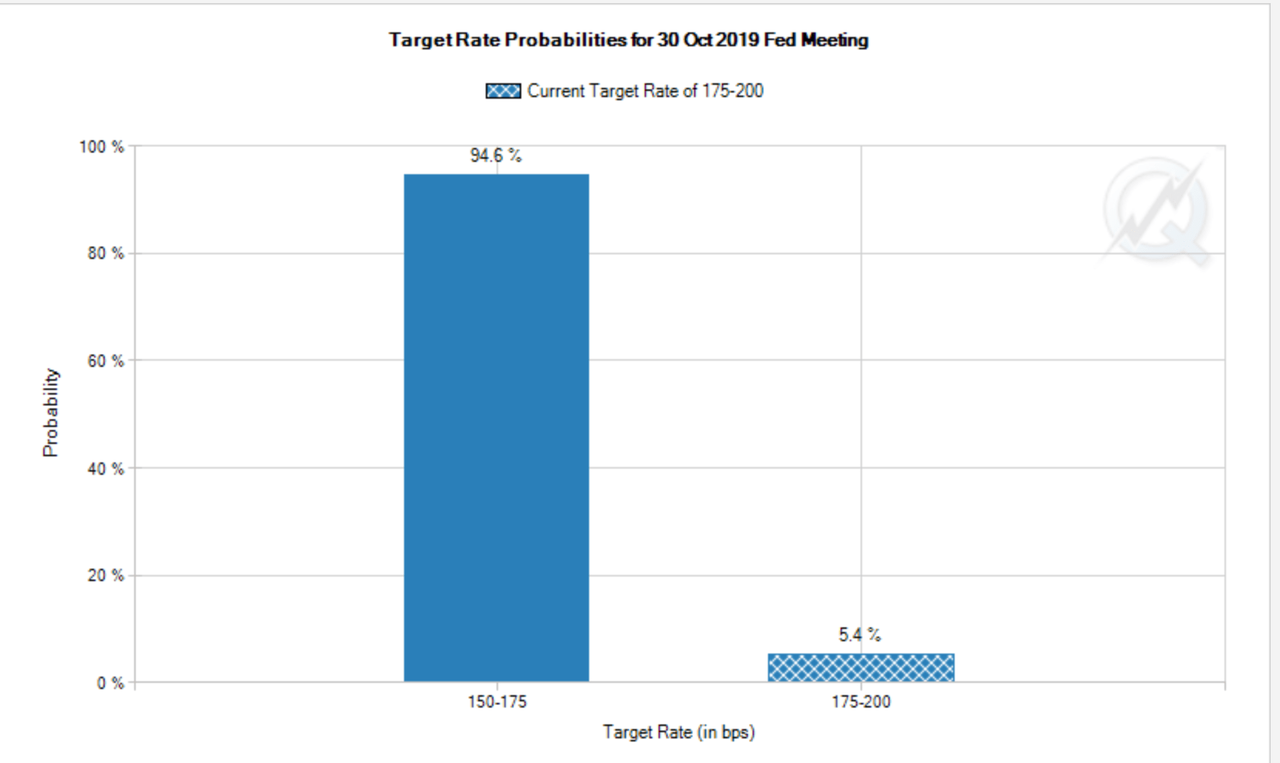

And markets really want that third rate cut next week:

94.6% probability of a rate cut. Think that a Fed that is intervening in markets daily by the dozens of billions of dollars will chance to disappoint markets by not cutting rates? Please.

Investors have been chasing the Fed into multiple expansion all year. But now that the Fed is forced to intervene ever more aggressively it has to prove something: Efficacy.

Are we seeing an improvement in growth? No. Are we seeing an improvement in earnings? No. From the looks of it they are barely keeping it together and are forced to do ever more to prevent markets from selling off as now the principle bull rationale for buying markets here is the Fed.

But, to be fair, the Fed has again succeeded in compressing volatility as price discovery has degraded to overnight action over any intraday price discovery. Markets are back to tight intra-ranges void of any actions and elevating indices near record highs.

Whether they can effect a move to sustained new highs remains to be seen and all eyes will be on the Fed next week to see whether they can achieve it.

If they can then investors can look for another run at the upper trend line on the $SPX chart:

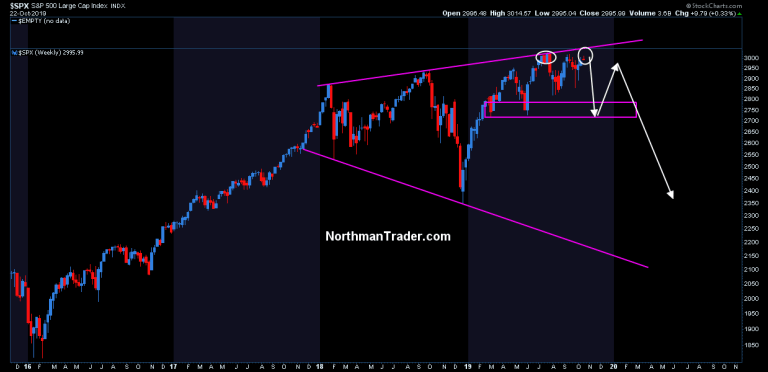

If they can’t, then things may turn out quite differently such as this speculative scenario:

What? You don’t think Fed is not all about markets? Where have you been? After all the Fed’s stated policy objective now is to extend the business cycle by any means necessary. And they can’t do that with falling stock prices.

And so they are in accelerated, daily, intervention mode. Because this is what it takes. The questions investors have to ask themselves is this:

-

What if it’s not enough?

-

And what is it they are not telling us?

-

Why are they are forced into these historic unexpected measures?

-

What happens if they lose control?

We may know more next week.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

Tyler Durden

Wed, 10/23/2019 – 15:30

via ZeroHedge News https://ift.tt/362mcAD Tyler Durden