Wild, Rollercoaster Week Ends Where It Started After Blockbuster Jobs, Return Of “Deal Optimism”

It was a torrid week which started off ugly, with the S&P off to the worst start to a December since 2008 amid fears the trade deal with China would be pushed beyond the Nov 2020 election. However, “optimism” promptly returned after an “anonymous” Bloomberg article said that the trade deal remains on track, and subsequent comments by Trump and Larry Kudlow suggested that talks are progressing, restoring hope that the next round of tariffs, slated to begin on Dec 15, will be delayed.

And then there was today’s payrolls report, which blew away expectations with a 266K print, 29K above the highest Wall Street forecast, on the back of a surge in manufacturing jobs, which jumped by 54K, the biggest monthly increase since 1998, as striking GM workers returned to work.

As a result, after tumbling on the first two days of the week, the S&P staged a remarkable recovery and closed the week virtually unchanged, while 10Y yield mirrored every move in risk almost tick for tick.

A big reason for the continued impressive rally was Apple stock, which hit a new all time high above $270 as Tim Cook continues to repurchase every share he can find. The stock is now up more than 71% YTD.

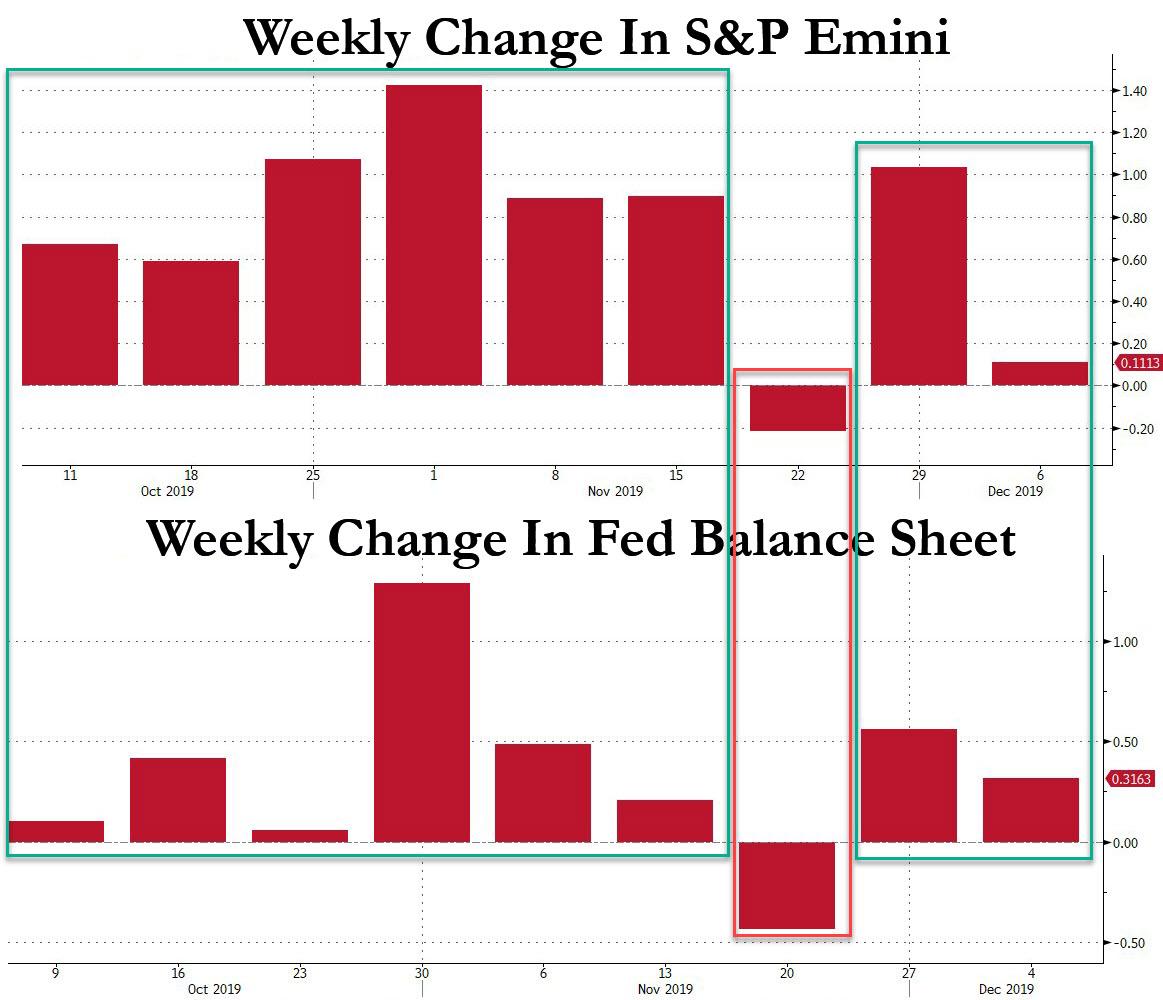

There was another reason for the return of the stock rally: this week the Fed’s balance sheet rose once again, and as we have shown, in the past 9 weeks ever since the Fed resumed repos and eventually POMO, the stock market is up every single week when the Fed’s balance sheet is higher; the only week the S&P was lower was when the Fed’s balance sheet also shrank. Surely, it’s just a coincidence…

As risk soared, safe havens pulled back, and after sliding as low as 1.70%, the 10Y yield was back in the mid 1.80% range.

Elsewhere, after surging from 12 to 18 at the start of the week, VIX was hammered as usual, and closed the week far below its Tuesday high of 18, if notably above where it started the week.

Those wondering if the brief volatility spike at the start of the week was enough to spark a short squeeze in the record VIX future net short, the answer is no, although for the second consecutive week, VIX net specs did shrink modestly.

The Dollar finally ended its 5-day losing streak, the longest since late October, with a bang, rising 0.15% on the day.

Brent jumped on Friday, after OPEC announced a surprise 500kb/d production cut, which however may be insufficient to prevent an increase in the oil glut. That said, Brent was almost unchanged from last Thursday following last Friday’s plunge amid fears Saudi Arabia may overproduce to punish those OPEC nations that violated the production quotas.

While the higher price of oil will be welcome by Saudi Arabia which eagerly awaits the first day of trading of Aramco following the company’s record IPO, it remains to be seen if Aramco’s $1.7 trillion valuation will be sustainable with Saudi Arabia needing a Brent price over $80 to fund all its budget obligations.

So after this week’s fireworks is it now safe to assume that stocks won’t deliver any more major surprises for the balance of 2019? Keep an eye on the Dec 15 tariff deadline: because today’s super strong job number merely assured that Trump now thinks he has even more leverage to demand concessions from China, while the Fed’s fears that trade war is hurting the economy and thus has to be vigilant to the downside, were blown away.

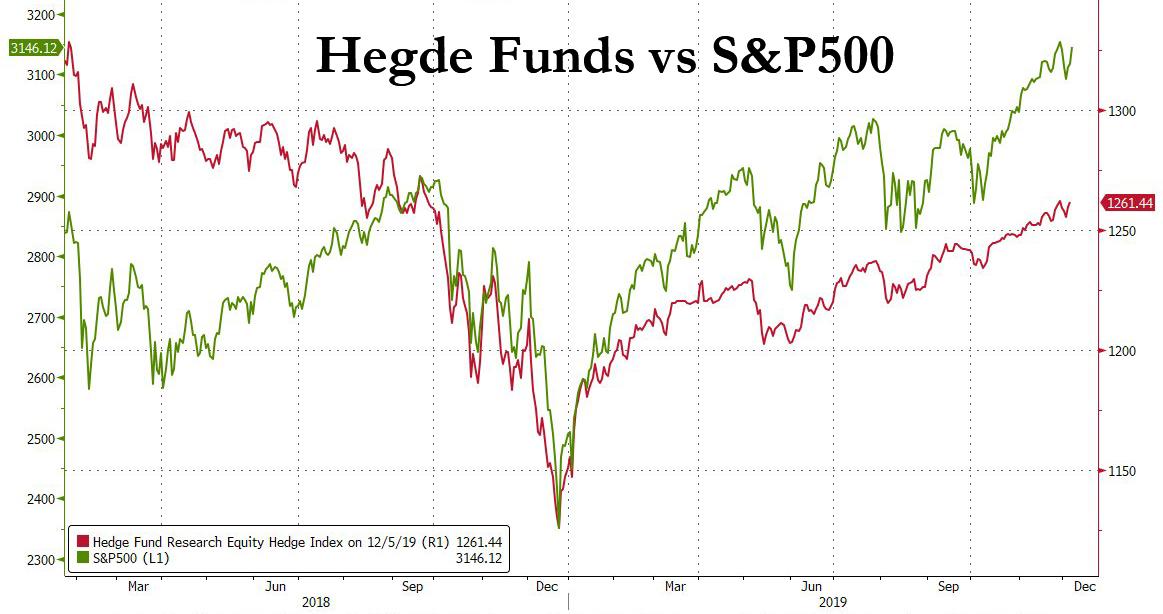

Ironically, while retail investors who bought the S&P are doing great, hedge funds are underperforming the S&P for yet another year, and many of them are facing a barrage of redemption requests.

Finally, this was and remains a market where one Trump tweet can mean the difference between a successful and catastrophic year for countless traders, and something tells us the coming three weeks, which see both the culmination of trade discussions and Trump’s impeachment, will be anything but quiet.

Tyler Durden

Fri, 12/06/2019 – 16:08

via ZeroHedge News https://ift.tt/2rcEP5F Tyler Durden