Fed’s Emergency Repo Operation Oversubscribed As Repo Rates Spike To December High

Ahead of today’s massive liquidity drain, which according to some calculations will be as much as $100 billion between $54BN in coupon settlements from last week’s Treasury auctions and an additional $50 billion or so in corporate income tax payments to the Treasury…

… which combined would be as large, if not bigger than the Sept 16 cash transfer to the Treasury which sparked the mid-September repo crisis, last Thursday the Fed announced a “kitchen sink” liquidity tsunami, throwing as much as $500 billion in liquidity backstops in the form of expanded and extended repo and term repo operations, while keeping the Fed’s “Not QE” T-Bill monetization chugging along.

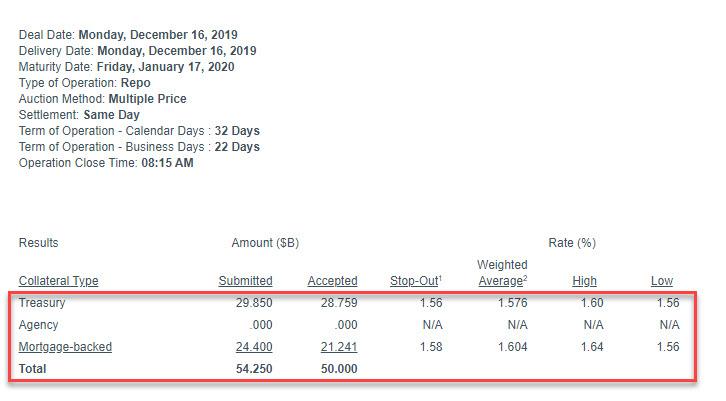

The first of these emergency repo operations was scheduled for this morning, ahead of the liquidity drain, in the form of a $50 billion, 32-day repo, which took place shortly after 8am, and was once again oversubscribed as there was more demand for liquidity, or $54.25 billion, than there was total supply.

Specifically, Dealers submitted $29.850BN in Treasury securities, and $24.4BN in MBS, at stop out rates of 1.56% and 1.58%, respectively, and which both came in more than fully subscribed relative to the $28.759BN in TSYs, and $21.241BN in MBS accepted.

This offering, which matures on January17, 2020, was the fourth “turn” repo providing funding past the year-end period.

The fact that the operation was oversubscribed was the first indication that banks are once again reserve-constrained and scrambling to procure as much year-end liquidity as they can get their hands on. Whether repo operations in the coming days are oversubscribed will indicate if the Fed’s roughly $500 billion in repo ops scheduled for the next 4 weeks will be enough to keep the Fed from losing control over overnight rates, as Credit Suisse repo expert Zoltan Pozsar predicted last week in his now infamous “Countdown to QE4” report.

One ominous sign: the overnight G/C repo rate spiked from 1.58% on Friday to 1.69% this morning, the highest print since the end of the November, and the clearest indication yet that despite throwing a kitchen sink of liquidity in the market, some dealers and banks are still having problems getting access to much needed liquidity.

Keep an eye on the repo rate over the next few hours for an indication if today’s $100 billion liquidity drain will overpower the Fed’s preemptive liquidity tsunami, in effect triggering Zoltan Pozsar’s worst-case scenario.

Obama Says Women Are “Indisputably Better” Than Men, And Should Lead Every Country

Are President Obama and his wife having some kind of lover’s quarrel?

Speaking at a private event in Singapore on Monday, President Obama said that if women ran every country, we would all live with significantly improved living standards and there would be less war and strife. When it comes to leadership, women are “indisputably better” than men, Obama said, according to the BBC, which was apparently invited to the event.

Most of the world’s problems, Obama said, stem from too many old men in positions of power, an obvious slight directed at President Donald Trump, though he wasn’t explicitly named.

Although they’re not perfect, women are so much more advanced and even-headed than men, that Obama believes if women were given two years running every country on earth, all of our problems would be fixed.

“Now women, I just want you to know; you are not perfect, but what I can say pretty indisputably is that you’re better than us [men].”

“I’m absolutely confident that for two years if every nation on earth was run by women, you would see a significant improvement across the board on just about everything…living standards and outcomes.”

When asked if he would ever consider going back into political leadership, he said he believed in leaders stepping aside when the time came.

“If you look at the world and look at the problems it’s usually old people, usually old men, not getting out of the way,” he said.

“It is important for political leaders to try and remind themselves that you are there to do a job, but you are not there for life, you are not there in order to prop up your own sense of self importance or your own power.”

For the record, there was no hint in the BBC story about Obama’s comments that he was joking.

Obama and his wife, Michelle, both traveled to Kuala Lumpur last week for an Obama Foundation event, and were apparently still in the region for Obama to appear at this event.

I am grateful for Orin Kerr’s response to my post on impeachment. Years ago, it was fairly common for law professors to respond to each other on legal blogs. In recent years, this sort of discourse has tended to wither away. I largely blame Twitter, which promotes instant, rapid-fire responses. These sorts of exchanges are seldom constructive, and quickly devolve into time-wasting flame wars. People reinforce those they agree with, and drag those they disagree with. We can do better. Orin does better. He disagrees with me, quite vigorously, but does so with reasoned discourse. Thanks Orin. Indeed, I sent Orin two drafts draft of this post in advance to hear his thoughts, and happily incorporated his feedback.

I think our positions are closer than they may appear. First, let me clear up a few points. I do not think an act must be criminal for it to be impeachable. I do not think the enumerated constitutional standards of criminal procedure extend to the impeachment process. There are some norms of due process that ought to be complied with but the strictures of the 5th and 6th Amendments are not controlling. I do not think that an article of impeachment based on “abuse of power” is void because that term is vague. Nor do I think that the term “abuse of power” is novel, or without precedent. Historically, there have been many articles of impeachment that use that phrase. In short, an article of impeachment premised on an “abuse of power” could be proper,as an original matter, even if the President was not on notice in advance of the precise contours of the offense. I also concur with co-blogger Jon Adler: the term “High Crimes and Misdemeanors” is not an inkblot. And, as far as my research suggests, the first article of impeachment is consistent with that original meaning.

I hesitate only slightly here because under the Framers’ design, the propriety of an article also turns, at least in part, on policy considerations. The decision to impeach does not depend solely on whether the President’s conduct rose to the level of a high crime or misdemeanor. The decision to impeach, like all decisions to prosecute, is premised on other factors beyond whether the specific elements of the offense were satisfied. In other words, not all impeachable offenses must lead to articles of impeachment (Several of the law professors who testified suggested that the word “shall” in the Impeachment Clause imposes a duty to impeach whenever the President commits such a high crime or misdemeanor. I do not think the word “shall” had such a mandatory meaning at the time of the framing.) Members of the Judiciary committee sued the President more than two years ago for violating the Foreign Emoluments Clause, but opted not to bring such an article of impeachment. Certain pragmatic considerations enter into any decision about whether to impeach.

Another important consideration concerns what precedent will be established. And precedent, not original meaning, was the focus on my earlier writing. I worry about the precedent that will be set by an article based on an “abuse of power.” There are several policy reasons to pause before proceeding down this route. First, an offense defined only after the act fails to provide the accused with any notice of possible wrongdoing. Second, the accused can then charge, perhaps rightfully, that this offense was synthesized with the purpose of simply getting him. Third, members of the public can believe, perhaps rightfully, that the impeachment proceeding is merely a political attack, rather than any process grounded in established law. This argument isn’t precisely premised on the prohibition of ex post facto laws or bills of attainder, but it has similar backing: the House determined that the President’s conduct was an “abuse of power” after he engaged in it. None of these concerns exist when impeachment is tied to a pre-existing, well understood offense. If the House managers wanted to follow that path, they could have included a free-standing bribery charge or a free-standing charge that he intentionally and unlawfully sought to withhold appropriated funds from Ukraine, or both.

These dynamics accordingly create additional burdens that the House must satisfy to substantiate an article based on an “abuse of power” standard, where there are no underlying criminal allegations. And this additional burden occasions certain risks to the process itself. Stephen Griffin articulated this premise on Balkinization:

The articles of impeachment submitted today are arguably the first in American history not to be grounded ultimately in allegations that the president committed a federal crime or other violation of law. This single fact creates unique opportunities and challenges for both parties going forward. For Democrats, it means they do not have to worry about whether the established facts satisfy the technicalities of a crime such as bribery or obstruction of justice. For Republicans, it creates the opportunity to respond by demanding clear criteria for the somewhat abstract offense of “abuse of power.” For example, haven’t all presidents abused their power to some extent? Democrats have the corresponding challenge of defending their criteria as specific and arguing that Trump is different from past presidents. They go some distance toward doing this in the first article by referring to “the integrity of the United States democratic process.”

The precise novelty of this claim might be nuanced, but the Johnson, Nixon, and Johnson articles all alleged specific violations of law. It is far easier to persuade the public that an article of impeachment is proper, if the claim is based on a well-worn criminal violation that is routinely prosecuted or which has supplied the basis for prior successful impeachments. That is, a crime that has elements and requirements that have been liquidated by judicial, as well as congressional precedent. The public is familiar with the elements of bribery and obstruction of justice. For example, the Mueller report spent considerable time developing each of the three elements of obstruction, when deciding whether the President ran afoul of the law. (Ultimately, Special Counsel Mueller did not make any recommendation.) This approach relies on established law and puts would-be wrongdoers on notice. Such precision is a long-standing feature, not a bug, of how the impeachment process has been carried out to date. In contrast, the House has launched an impeachment based on a newly crafted-political “crime.”

But here, we are left with an allegation of “abuse of power.” Persuading the public that these allegations rise to the standard of a high crime or misdemeanor, in theory at least, is more difficult than persuading the public that one of the two enumerated offenses (i.e., bribery and treason) is a high crime or a misdemeanor. I say in theory, because at this juncture, I doubt there are many minds that are not yet made up. But Griffin’s point stands: there are additional challenges, and risks by going down the road suggested by the House majority. And this sort of article departs from modern, if not all prior impeachment practice. The burden to justify this expansion rests with those advancing the articles, not those defending against them.

A recent article in the New York Timeshighlights how opponents of impeachment can view the “abuse of power” allegation as merely political:

Yet Republicans view the current episode through the opposite lens, saying that the Republican-led impeachment of Mr. Clinton was fully justified while the action against Mr. Trump is purely political and unsupported by the evidence.

“President Clinton committed a crime, perjury,” Representative Steve Chabot, an Ohio Republican who voted to impeach Mr. Clinton in 1998, said Thursday as the House Judiciary Committee drafted articles of impeachment against the president. “This president isn’t even accused of committing a crime.” . . . .

On Thursday, Representative Kelly Armstrong, Republican of North Dakota, recited a litany of past presidents of both parties who had drawn charges of abusing their power but were not impeached, and cautioned his colleagues that impeachment was becoming “the new normal.”

“In the history of our country, the party who is not in the White House has accused the White House of abuse of power,” Mr. Armstrong said. “It started 200 years ago, it will continue into the future, except now, congratulations, it will be impeachment every single time one party controls the House of Representatives and the other party is in the White House.”

The Senate is heading into uncharted territory. Once articles of impeachment are completely decoupled from any clearly articulated offenses, the burden of charging a president with “abuse of power” is significantly reduced. Moreover, any president who refuses to comply with what he sees as an improper investigation can be charged with “obstruction of Congress.” This one-two punch can be drafted with far greater ease than were the articles of impeachment presented against Presidents Andrew Johnson, Richard Nixon, or Bill Clinton. Without question, Congress can convict a president for conduct that is not criminal. This process is not bound by the strictures of the United States code. Moreover, Congress can begin impeachment proceedings for conduct that is inconsistent with the president’s duty to faithfully execute the laws. This inquiry, though subjective, is a necessary feature of the American constitutional order. But the predicates of the Trump articles will set a dangerous precedent, as impeachment might become—regrettably—a common, quadrennial feature of our polity.

I think the standards set by the House’s proposed articles will make impeachment far easier, even in cases where the allegations are far less severe.

Finally, a brief comment on the President’s alleged motives. The House report concluded that “Impeachable abuse of power can take two basic forms.” The articles have not alleged the first path: that the President’s exercise of authority “exceeds the President’s constitutional authority or violates legal limits on that authority.” The articles could have predicated conviction on Trump having violated either the statute authorizing military aid to the Ukraine or the Impoundment Control Act of 1974, but didn’t. The articles could have predicated conviction on Trump committing all of the traditional elements of bribery–an offense spelled out in the Constitution–but didn’t. The House impeachers have publicly framed the article as “abuse of power.”

I flag an issue that does give me some pause. Despite not leading with an article based on bribery, the article references bribery and unlawfully conditioning an appropriation. It is not clear to me, at least, whether the House intended to include a separate claim of bribery, or whether the allegation of bribery is offered as evidence that there is an abuse of power. It is also not clear to me whether the conditioning of an appropriation is unlawful, or if that act is offered as evidence of abuse of power. What exactly are the charges against the President? If the bribery charge or unlawful conditioning claims cannot be substantiated, independently, on what basis can the abuse of power claim be substantiated? In other words, if we are really talking about bribery or a statutory violation, why did the House use the framing of “abuse of power.” I think the House is trying to have their cake, and eat it too. That is, they’re trying to avoid charging the President with a specific crime that may be difficult to convict, but still accusing the President of committing those crimes. An acquittal in the Senate would not necessarily acquit the President of the alleged conduct, because it was never precisely charged.

In this first category–where the President’s exercise of authority “exceeds the President’s constitutional authority or violates legal limits on that authority”–the President’s motives are irrelevant. Additionally, these offenses are well-defined. The President, and everyone else, is on fair notice that such acts could give rise to impeachment. There can be no reasonable claim that the offense was only defined after the fact. For example, the general thrust of my criticism would not be relevant if the House included an article premised on bribery. I doubt the technical elements of the offense could be satisfied. But there is absence of notice; allegations about unfairness fade.

The House, however, chose the second path: the articles alleged that the President “engag[ed] in potentially permissible acts but for forbidden reasons (e.g., with the corrupt motive of obtaining a personal political benefit).” It is commonplace for Presidents to ask foreign governments to conduct investigations. What renders this request different, the articles contend, is that the object of that investigation was to injure the President’s political rival. And impeachment will turn on an assessment of the President’s motive. A corrupt motive would, according to the proponents of impeachment, transform a “permissible act” into an “abuse of power.” Effectively, they contend that otherwise legitimate presidential actions taken with a corrupt motive are, by definition, not faithful executions of the law. (I discussed that theory here.) The article now turns on what was in Trump’s head. If he had proper motivations, then there was no impeachable offense. Such an article sets an important, and risky new precedent: going forward, I fear that many presidential actions with potential consequences to the party not in the White House will be seen as corruptly motivated, and thus subject to impeachment.

There are some other areas of difference between Orin and me, but I will leave it here for now.

from Latest – Reason.com https://ift.tt/2EnrrOX

via IFTTT

Speech has never been freer than it was in this decade. But only if you take a broad view of what free speech means, and only if you look at the right parts of the decade.

There is an argument that says free speech isn’t just a matter of stopping direct government censorship, nor of keeping the state from indirectly chilling what we say. True freedom of expression, the theory goes, requires a broader culture of free speech—a society where art, information, and commentary face fewer restraints of all kinds, not just the restraints that have the government’s guns behind them.

Now, I’m not crazy about conflating the concept of free speech with those bigger, messier social questions. But they are undeniably linked—a culture hostile to open expression is surely more likely to pass legal limits on speech—and those big social questions are worth thinking about in their own right. So let’s roll with it. If by “free speech” you mean the capacity and willingness to speak, not just a shield from the institutions that could forcibly stop you from speaking, then the early to mid 2010s arguably saw the freest speech in history.

As the decade dawned, it was cheaper and easier than ever before to create and transmit a text, an image, or an audio or video recording. That transmission, in turn, had a bigger chance of reaching an audience. People didn’t waste that opportunity: Both the volume and the variety of widely available speech exploded. Whole new media ecosystems appeared. Budding musicians did an end run around the record labels, sketch comics did an end run around cable TV, and YouTube DIYers did an end run around licensed plumbers and repairmen. In the political world, the Overton window widened and a flood of oddball ideological tribes poured in—some of them rather unappealing, but that’s how it goes with unfettered expression.

That in turn provoked a backlash, and for the last several years we’ve seen a series of efforts to clamp down on all that uncontrolled chatter. There have been heightened calls for censorship from the left, right, and center, sometimes directed at new sorts of speech (bots, code for printing weaponry) but usually aimed at targets that feel familiar (sex-work talk, terrorist propaganda, hate speech, marchers wearing masks), sometimes so familiar that they’re moldy (pornography, Russian subversion). Beyond that, there was a broader feeling of brittleness around all that unfamiliar or unpleasant expression; even critics who would never call for censorship sometimes went overboard when attributing ill effects to speech they disliked. Meanwhile, the biggest conduit for all those emerging ecosystems of expression—the internet—seemed to be growing not just more censored but more centralized, more surveilled, more controlled. That was true not just in purely online spaces but in the dissident movements that at times use cyberspace to organize and communicate. Around the world, it became clear that it wasn’t just protesters who were imitating and adapting each other’s tactics; the regimes that they were protesting watched and learned from each other too.

All of that raises the question: Did we just witness Peak Free Speech? Will the first half of this decade be remembered not just as a time when speech was less fettered than ever before but as a time when it was less fettered than it will ever be again?

Freedom vs. Tolerance

I may have rushed too quickly past the question of what a “culture of free speech” is supposed to be. It’s not a term that everyone uses the same way. The people who throw around that phrase often claim, or at least assume, that certain sorts of speech are more conducive to open expression than others. Some of them suggest that speech should be more civil; others think it ought to be more oppositional. Most of them want the speech, or at least the speakers, to be tolerant of other points of view.

But freedom and tolerance simply aren’t the same thing. Both are valuable, but they’re often going to be in tension with each other.

Civil libertarians need to be clear-eyed about that. Speech has always included gossip, shaming, and other tools for enforcing conformity. In the past those sorts of speech may have been confined to a single village or middle school, but now they have a global reach. Some testy “free speech” debates of the last decade have really just been battles between different collections of culture warriors, each circulating misleading screenshots as they try to shout the other side down. That may look like illiberal intolerance, but it also looks like a lot of lively speech. It’s not a sort of speech that I like, but some form of it has always been a part of public life and it isn’t likely to go away anytime soon.

The more important issue, at least as far as the future of free speech is concerned, is whether the institutional environment makes it easier or harder for intolerant people to muffle the speech they don’t want to hear. And this is where the most significant change happened. From the ’70s through the ’00s, America’s electronic media grew ever more decentralized and participatory. Not so in the ’10s, as the social media services that made publishing so quick and easy also brought more of that publishing under consolidated corporate control. The result was the difference between getting kicked off an email list and getting kicked off a social media network: Both may be cases of a private association exercising its right not to give you a platform, but one has a much bigger impact than the other when it comes to whether your voice is heard.

This didn’t mean we reverted to the bad old days of just three big TV networks, or even to the 500-channel universe of the late cable era. It was still ludicrously easy by 1990s standards to get a homemade piece of media in front of a substantial audience. But it was also more likely that your homemade media would suddenly be obscured. That might be because you broke a platform’s rules; it might be because an algorithm mistook your photo of a nude sculpture for pornography and improperly assumed that you had broken a rule; it might be because you were mass-reported by the sorts of assholes that the rules were supposed to address. (Time and again, a social media company would create a system that was supposed to keep out the bigots and trolls who harass people, only to learn that the bigots and trolls had found a way to turn the system itself into a tool for harassment.) The result was more Brazil than 1984: a control apparatus full of leaks and loose wiring.

Governments encouraged the process, passing mandates that fostered both the proliferation of rules and a sloppy sort of enforcement. Germany, for example, started implementing a law last year that informed platforms that they had just 24 hours to take down “obviously unlawful” hate speech or face a steep fine. Inevitably, this combination of stiff penalties and narrow time windows prompted companies to suppress first and ask questions later, even if that meant excising speech that didn’t actually violate the law. (In one infamous example, the nominally anti-racist statute was used to remove some anti-racist satire.) That’s bad enough for the Germans, but in a global internet decisions made by the government of Germany—or any other wired nation, from Britain to China—can affect what people around the world can see.

Centralized platforms make the task that much easier. As Declan McCullagh wrote in Reason this year, they offer “a single convenient point of control for governments eager to experiment with censorship and surveillance.” A culture of freer speech might require a technology of freer speech—a more decentralized internet with fewer chokepoints, one built around protocols rather than platforms.

The Global Spring

All that said, there is one big reason to think the pendulum may already be swinging back in speech’s direction. This year saw an astonishing level of public protest around the globe, adding up to a revolutionary moment on par with 1968. Unrest has swelled everywhere from France to Hong Kong, from Chile to Indonesia, from Iran to Ecuador, from Haiti to Spain. Such movements have already brought down governments in Algeria, Iraq, Lebanon, and Sudan. In Bolivia, mass protests preceded the ousting of leftist president Evo Morales and then more mass protests greeted the new right-wing regime of Jeanine Áñez. Here in the U.S., last year saw the biggest strike wave in more than three decades, and we may be on track to top that in 2019.

These movements have been sparked by a wide variety of grievances. Their supporters come from a wide variety of ideologies. They use a wide variety of tactics, not all of them limited to nonviolent speech and assembly. It would probably be hard to find someone who backs every single one of them. But put together, they represent a surge in people’s willingness not just to speak out but to take risks to do so. That too represents a sort of culture of free speech, even though many of these regimes have reacted to the unrest with a repression that does not remotely resemble free speech in the legal sense.

Those movements are learning from each other, too: When one of them figures out a way to evade censorship, surveillance, or police assaults, the others take heed. (We live in an era when Hongkongers can be recorded neutralizing tear gas in the summer, videos of the technique immediately circulate on social media, and by October protesters in Chile are doing the same thing.) After a decade of authoritarian governments adjusting themselves to the ways protesters organize themselves on- and offline, the momentum is with the dissidents again as they find ways to adjust their tactics in return.

A decade that began with the rise and fall of the Arab Spring is concluding with a Global Spring. And while that could conceivably end with the most vicious clampdown of all, it’s also the best reason to hope that what looked like Peak Free Speech was really just a temporary speech recession.

from Latest – Reason.com https://ift.tt/2YX5eAS

via IFTTT

Speech has never been freer than it was in this decade. But only if you take a broad view of what free speech means, and only if you look at the right parts of the decade.

There is an argument that says free speech isn’t just a matter of stopping direct government censorship, nor of keeping the state from indirectly chilling what we say. True freedom of expression, the theory goes, requires a broader culture of free speech—a society where art, information, and commentary face fewer restraints of all kinds, not just the restraints that have the government’s guns behind them.

Now, I’m not crazy about conflating the concept of free speech with those bigger, messier social questions. But they are undeniably linked—a culture hostile to open expression is surely more likely to pass legal limits on speech—and those big social questions are worth thinking about in their own right. So let’s roll with it. If by “free speech” you mean the capacity and willingness to speak, not just a shield from the institutions that could forcibly stop you from speaking, then the early to mid 2010s arguably saw the freest speech in history.

As the decade dawned, it was cheaper and easier than ever before to create and transmit a text, an image, or an audio or video recording. That transmission, in turn, had a bigger chance of reaching an audience. People didn’t waste that opportunity: Both the volume and the variety of widely available speech exploded. Whole new media ecosystems appeared. Budding musicians did an end run around the record labels, sketch comics did an end run around cable TV, and YouTube DIYers did an end run around licensed plumbers and repairmen. In the political world, the Overton window widened and a flood of oddball ideological tribes poured in—some of them rather unappealing, but that’s how it goes with unfettered expression.

That in turn provoked a backlash, and for the last several years we’ve seen a series of efforts to clamp down on all that uncontrolled chatter. There have been heightened calls for censorship from the left, right, and center, sometimes directed at new sorts of speech (bots, code for printing weaponry) but usually aimed at targets that feel familiar (sex-work talk, terrorist propaganda, hate speech, marchers wearing masks), sometimes so familiar that they’re moldy (pornography, Russian subversion). Beyond that, there was a broader feeling of brittleness around all that unfamiliar or unpleasant expression; even critics who would never call for censorship sometimes went overboard when attributing ill effects to speech they disliked. Meanwhile, the biggest conduit for all those emerging ecosystems of expression—the internet—seemed to be growing not just more censored but more centralized, more surveilled, more controlled. That was true not just in purely online spaces but in the dissident movements that at times use cyberspace to organize and communicate. Around the world, it became clear that it wasn’t just protesters who were imitating and adapting each other’s tactics; the regimes that they were protesting watched and learned from each other too.

All of that raises the question: Did we just witness Peak Free Speech? Will the first half of this decade be remembered not just as a time when speech was less fettered than ever before but as a time when it was less fettered than it will ever be again?

Freedom vs. Tolerance

I may have rushed too quickly past the question of what a “culture of free speech” is supposed to be. It’s not a term that everyone uses the same way. The people who throw around that phrase often claim, or at least assume, that certain sorts of speech are more conducive to open expression than others. Some of them suggest that speech should be more civil; others think it ought to be more oppositional. Most of them want the speech, or at least the speakers, to be tolerant of other points of view.

But freedom and tolerance simply aren’t the same thing. Both are valuable, but they’re often going to be in tension with each other.

Civil libertarians need to be clear-eyed about that. Speech has always included gossip, shaming, and other tools for enforcing conformity. In the past those sorts of speech may have been confined to a single village or middle school, but now they have a global reach. Some testy “free speech” debates of the last decade have really just been battles between different collections of culture warriors, each circulating misleading screenshots as they try to shout the other side down. That may look like illiberal intolerance, but it also looks like a lot of lively speech. It’s not a sort of speech that I like, but some form of it has always been a part of public life and it isn’t likely to go away anytime soon.

The more important issue, at least as far as the future of free speech is concerned, is whether the institutional environment makes it easier or harder for intolerant people to muffle the speech they don’t want to hear. And this is where the most significant change happened. From the ’70s through the ’00s, America’s electronic media grew ever more decentralized and participatory. Not so in the ’10s, as the social media services that made publishing so quick and easy also brought more of that publishing under consolidated corporate control. The result was the difference between getting kicked off an email list and getting kicked off a social media network: Both may be cases of a private association exercising its right not to give you a platform, but one has a much bigger impact than the other when it comes to whether your voice is heard.

This didn’t mean we reverted to the bad old days of just three big TV networks, or even to the 500-channel universe of the late cable era. It was still ludicrously easy by 1990s standards to get a homemade piece of media in front of a substantial audience. But it was also more likely that your homemade media would suddenly be obscured. That might be because you broke a platform’s rules; it might be because an algorithm mistook your photo of a nude sculpture for pornography and improperly assumed that you had broken a rule; it might be because you were mass-reported by the sorts of assholes that the rules were supposed to address. (Time and again, a social media company would create a system that was supposed to keep out the bigots and trolls who harass people, only to learn that the bigots and trolls had found a way to turn the system itself into a tool for harassment.) The result was more Brazil than 1984: a control apparatus full of leaks and loose wiring.

Governments encouraged the process, passing mandates that fostered both the proliferation of rules and a sloppy sort of enforcement. Germany, for example, started implementing a law last year that informed platforms that they had just 24 hours to take down “obviously unlawful” hate speech or face a steep fine. Inevitably, this combination of stiff penalties and narrow time windows prompted companies to suppress first and ask questions later, even if that meant excising speech that didn’t actually violate the law. (In one infamous example, the nominally anti-racist statute was used to remove some anti-racist satire.) That’s bad enough for the Germans, but in a global internet decisions made by the government of Germany—or any other wired nation, from Britain to China—can affect what people around the world can see.

Centralized platforms make the task that much easier. As Declan McCullagh wrote in Reason this year, they offer “a single convenient point of control for governments eager to experiment with censorship and surveillance.” A culture of freer speech might require a technology of freer speech—a more decentralized internet with fewer chokepoints, one built around protocols rather than platforms.

The Global Spring

All that said, there is one big reason to think the pendulum may already be swinging back in speech’s direction. This year saw an astonishing level of public protest around the globe, adding up to a revolutionary moment on par with 1968. Unrest has swelled everywhere from France to Hong Kong, from Chile to Indonesia, from Iran to Ecuador, from Haiti to Spain. Such movements have already brought down governments in Algeria, Iraq, Lebanon, and Sudan. In Bolivia, mass protests preceded the ousting of leftist president Evo Morales and then more mass protests greeted the new right-wing regime of Jeanine Áñez. Here in the U.S., last year saw the biggest strike wave in more than three decades, and we may be on track to top that in 2019.

These movements have been sparked by a wide variety of grievances. Their supporters come from a wide variety of ideologies. They use a wide variety of tactics, not all of them limited to nonviolent speech and assembly. It would probably be hard to find someone who backs every single one of them. But put together, they represent a surge in people’s willingness not just to speak out but to take risks to do so. That too represents a sort of culture of free speech, even though many of these regimes have reacted to the unrest with a repression that does not remotely resemble free speech in the legal sense.

Those movements are learning from each other, too: When one of them figures out a way to evade censorship, surveillance, or police assaults, the others take heed. (We live in an era when Hongkongers can be recorded neutralizing tear gas in the summer, videos of the technique immediately circulate on social media, and by October protesters in Chile are doing the same thing.) After a decade of authoritarian governments adjusting themselves to the ways protesters organize themselves on- and offline, the momentum is with the dissidents again as they find ways to adjust their tactics in return.

A decade that began with the rise and fall of the Arab Spring is concluding with a Global Spring. And while that could conceivably end with the most vicious clampdown of all, it’s also the best reason to hope that what looked like Peak Free Speech was really just a temporary speech recession.

from Latest – Reason.com https://ift.tt/2YX5eAS

via IFTTT

It was all fun and games enriching the super-wealthy but now the karmic cost of the Fed’s manipulation and propaganda is about to come due.

A “market” that needs $1 trillion in panic-money-printing by the Fed to stave off a karmic-overdue implosion is not a market: a legitimate market enables price discovery. What is price discovery? The decisions and actions of buyers and sellers set the price of everything: assets, goods, services, risk and the price of borrowing money, i.e. interest rates and the availability of credit.

The U.S. has not had legitimate market in 12 years. What we call “the market” is a crude simulation that obscures the Federal Reserve’s Socialism for the Super-Wealthy: the vast majority of the income-producing assets are owned by the super-wealthy, and so all the Fed money-printing that’s been needed to inflate asset bubbles to new extremes only serves to further enrich the already-super-wealthy.

The apologists claim the bubbles must be inflated to “help” the average American, but that claim is absurdly specious. The majority of Americans “own” near-zero assets that earn income; at best they own rapidly-depreciating vehicles, a home that doesn’t generate any income and a life insurance policy that pays off only when they pass away.

The average American uses the family home for shelter, and so its currently inflated price does nothing to improve the household income: it’s paper wealth, and we’ve already seen how rapidly that paper wealth can vanish when Housing Bubble #1 popped. (Housing Bubble #2 is currently sliding toward the edge of the abyss.)

Were legitimate price discovery allowed, the asset bubbles would pop, and the real-world impact on the average household that owns essentially zero income-producing assets would be minimal. Their overvalued house would fall in half, but since it still functions as shelter, the actual economic impact is minimal. As for the life insurance company’s losses–where’s the benefit today of an “asset” that only pays out when you die?

Meanwhile, the super-wealthy own stocks, bonds, companies and commercial real estate, all of which generate income. The rich get richer in two ways: their assets generate small fortunes in income (unearned income is what separates “the rich” from everyone else) and thanks to the Fed’s constant goosing of asset prices, their paper wealth has multiplied.

The dirty little secret that nobody dares whisper lest the whisper trigger a self-reinforcing avalanche is that this Fed-manipulated “market” is illiquid: if any serious selling were to arise, there wouldn’t be enough buyers to stave off a complete implosion of the bubbles.

The Fed’s game is to create the illusion of liquidity by being the buyer of last resort, only now the Fed is the only buyer. This is the toxic consequence of the Fed’s 12 long years of Socialism for the Super-Wealthy: thanks to the Fed’s destruction of price discovery, the super-wealthy no longer worry about liquidity, so leverage is the name of the game.

The Super-Wealthy can gamble with hundreds of billions to stripmine the economy and not worry about whether a buyer will actually pay the overvalued price of the asset, because they can count on the Fed to step up and panic-money-print whatever sums are needed to maintain the illusion of liquidity.

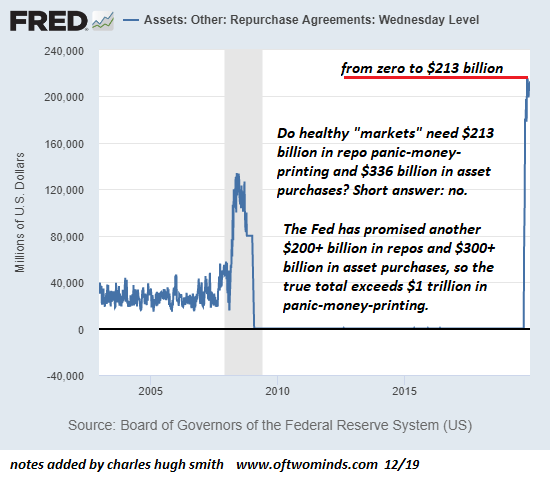

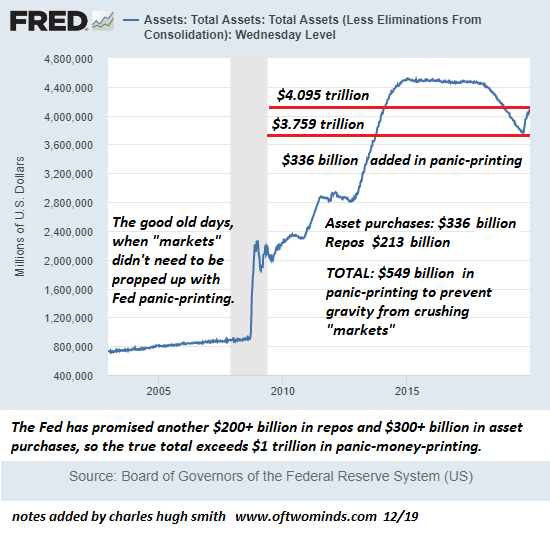

If the “market” is so healthy, why is the Fed panic-money-printing over $1 trillion in a few months? Please glance at the charts below: the Fed has printed $213 billion in repos and $336 billion for asset purchases in the blink of an eye, and the Fed has promised to panic-print another $200+ billion in repos and another $300+ billion in asset purchases, for a grand total of over $1 trillion in panic-money-printing.

Why has the Fed been forced to panic-money-print $1 trillion to stave off an implosion of their phony “market”?Moral hazard is coming home to roost, and the Fed is having a full-blown panic-attack because the Super-Wealthy (banks, corporations, financiers) have no fear that liquidity could dry up and markets go bidless, i.e. buyers disappear and there’s nobody left to buy their overvalued assets at bubble valuations.

If you want to understand how liquidity can dry up overnight and bids disappear, please read Mandelbrot’s bookThe Misbehavior of Markets: A Fractal View of Financial Turbulence. The point Mandelbrot makes here is that markets are intrinsically unstable and prone to sudden, chaotic turbulence. In a legitimate market with intact price discovery, buyers and sellers understand risk cannot be reduced to zero and so they trade accordingly.

But in our bogus Fed-controlled “market,” buyers and sellers are supremely confident the Fed will always buy assets regardless of price, and so they trade accordingly: There are no limits on leverage, derivative positions, credit lines, stock buy-backs or currency (FX) swaps: the Fed has been reassuring the legalized looters that the sky is the limit, go ahead and gamble hundreds of billions of dollars, we’ll buy your overvalued assets if things get dicey.

And so the tissue-thin “market” is fundamentally illiquid, and hence the Fed’s sudden panic-money-printing of $1 trillion, which is roughly equivalent to the entire GDP of Indonesia.

The Fed’s thorough destruction of price discovery and its elevation of moral hazard have created a monster that is about to devour the Fed’s phony facade of a “market”. It was all fun and games enriching the super-wealthy but now the karmic cost of the Fed’s manipulation and propaganda is about to come due, and few of the “market’s” supremely complacent and confident participants are prepared for the unraveling of the Fed’s illusion of liquidity.

If you want an analogy, try a population of rats that have proliferated on an island, and now the ravenous horde has consumed the last remaining bits of food. You can work out what happens next.

Global Markets Hit All Time High As Traders Brace For “Phase Two” Optimism

This is where we stand as we enter Monday morning:

European markets are firmer this morning, though the FTSE 100 significantly outperforms on a second-wave of UK election optimism.

China State Council stated it will continue to suspend additional tariffs on US vehicles and auto parts due to the Phase One deal.

China sources cited by CNBC’s Yoon note that the USD 40-50bln target on agricultural purchases is a “best case target”.

Boeing (BA) is mulling cutting or stopping its 737 MAX production, via WSJ – Co. shares are down 2% pre-market

USD remains subdued although Sterling and Euro were dented by the latest poor PMIs.

Now that “Phase one” of the US-China deal is in the history books, traders around the world are bracing for a full year of “Phase Two” optimism in continuation of the only thing that matters since the spring of 2018 (that, and central banks cutting like there’s a global crisis, of course). And after US cash markets hit a new all time high on Friday, world stock markets rudhes to catch up with the US on Monday, trading at fresh all time highs in what was another “sea of green” day.

Whether it was looking ahead to Phase Two optimism, or simply relishing the (non) deal that was China’s ridiculous promise to double US ag imports, Wall Street was quick to try and shape narratives as one of buying the rumor and then buying the news as well:

“We may have reached the point of ‘peak tariffs’ and this deal could be the start of a series of phased rollbacks, which could unlock further upside for equity markets, driven by an improvement in business confidence and a recovery in investment,” said Mark Haefele, CIO of UBS Global Wealth Management in a note to clients. We may have… but we haven’t, because as Morgan Stanley explained most supply chains are already in process of being moved while the “deal” will hardly inspire confidence among companies to spend more on CapEx.

For now, however, the optimism is working: European shares stormed out of the gate, and the pan-European STOXX 600 index was up by 1.1% hitting a new record high. Germany’s DAX rose as much as 0.5%, despite weakness in the Stoxx 600 Automobiles & Parts Index which underperformed the broader gauge. German auto stocks fell after China’s ambassador to Germany threatened retaliation if Germany excludes Huawei Technologies Co. as a supplier of 5G wireless equipment. Auto-parts stocks such as Valeo and Hella also underperformed after Morgan Stanley cut both stocks along with Schaeffler to underweight, saying that suppliers have failed to fully understand the size of structural changes ahead, which makes it tough to justify their re-rating against OEMs.

European markets also ignored the latest disappointing PMI print, indicating that Europe remains stuck in a manufacturing recession: German private sector activity shrank for the fourth month running in December as a downturn in manufacturing offset services sector growth in Europe’s largest economy. Across the boarder, French businesses grew at a steady pace in December despite a nationwide strike against pension reform, although activity in the manufacturing sector came unexpectedly close to stagnating. Overall, the Eurozone composite PMI was unchanged at 50.6, modestly missing the expectation of a rebound to 50.7, driven by continued manufacturing weakness which shrank from 46.9 to 45.9, well below the 46.9 expectation, while the Services PMI rose modestly from 51.9, to 52.4.

The weakness was largely due to another decline in both German and French mfg PMIs, both of which dropped, with the former now in contraction since March and the latter just one pension strike away from a sub-50 print.

Earlier in Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan to its highest level since April 18. It was last up 0.13%. Australia’s S&P/ASX 200 led the way as it jumped 1.63%, while shares in Taiwan added 0.22%. Japan’s Nikkei 225 succumbed to some profit-taking, falling 0.29% after surging 2.55% to a 14-month closing high on Friday.

While everyone was busy ignoring the latest European economic data, markets were positively giddy at the all too credible rebound in Chinese data unveiled late on Sunday night which saw most indicators post a sharp and orchestrated rebound.

Chinese investors initially had a more tepid reaction to the trade news, with the blue-chip CSI300 index struggling to rise further after trade hopes fanned a near 2% rise on Friday. But after a lackluster morning session, the CSI300 index turned higher in the afternoon and was last up 0.3%, helped by the latest industrial output and retail sales data.

And so, thanks to China’s latest data dump, positive sentiment helped push MSCI’s All Country World Index up 0.15%, after hitting an all-time high on Friday when the trade deal was agreed.

Looking at the latest trade development, on Sunday, China State Council stated it will continue to suspend additional tariffs on US vehicles and auto parts due to the Phase One deal, whilst also suspending the additional 5-10% tariffs on some US goods planned to take effect on December 15th, according to CNBC’s Yoon. Meanwhile, China’s Foreign Ministry said that more trade information will be released in due course and working-level officials from both sides remain in contact.

China sources cited by CNBC’s Yoon note that the USD 40-50bln target on agricultural purchases is a “best case target”, and that the US would likely allow ‘best endeavor’ purchases; adds that general feeling on tariff rollback is an issue of linguistics. Additionally CNBC’s Yoon adds, no Chinese confirmation regarding the hard targets for US agricultural purchases; although, China is likely to agree but cannot acknowledge this publicly due to a possible backlash.

In addition to the trade deal, markets were excited by the apparent end of the Brexit drama, if only for the time being. Ryan Felsman, senior economist at CommSec in Sydney, said the trade deal and the receding risk of a disorderly Brexit after the British election produced a strong Conservative majority provided support for sentiment in Australia. A lower-than-expected Australian budget surplus due to a sluggish economy has also “built expectations by markets for further easing from the Reserve Bank (of Australia),” he said. He added that investors wanted more details and the reduction in U.S. tariffs may have disappointed some looking for more aggressive action.

“Certainly there were expectations perhaps that the rollback would be more significant than just 50%.”

In the US, S&P futures were back to record highs hit last week. U.S. shares struck a cautious note on Friday, paring initial gains to end barely higher as weary investors awaited signs of a concrete deal.

However, the news of a deal was still enough to send the S&P 500 to a record closing high of 3,168.8, up just 0.01%. The Nasdaq Composite added 0.2% to end at 8,734.88, also a record, and the Dow Jones Industrial Average rose 0.01% to 28,135.38.

In rates, U.S. Treasury yields moved modestly higher on Monday, after the sharp reversal on Friday, reflecting the more positive mood. Benchmark 10-year Treasury notes rose to 1.8452% compared with their U.S. close of 1.821% on Friday, and the two-year yield touched 1.6304% compared with a U.S. close of 1.604%.

In FX, the Bloomberg Dollar Spot Index slipped and the euro held gains after data showed the euro-area economy is still struggling. EURUSD touched 1.1151 versus the dollar before paring gains after a slew of European PMIs. Treasuries halted their advance from Friday, while euro-area bonds were mostly higher. As noted above the latest Eurozone composite PMI stayed at 50.6 in December, slightly lower than the forecast of 50.7. The reading signals fourth-quarter output will be the weakest since the region exited a double-dip recession in the second half of 2013.

Sterling pared Asia session gains on profit taking and after a flash indicator for all business activity dropped to the lowest since the aftermath of the 2016 Brexit referendum; manufacturing activity slipped to 47.4, a sharper downturn than the 49.2 reading predicted by economists.

In commodities, oil prices which had risen on Friday following the deal, climbed further on Monday. Brent crude rose 0.1% to $65.28 per barrel, and U.S. West Texas Intermediate crude was down 0.05% at $60.11 per barrel. Spot gold prices were down 0.06% at $1,474.64 per ounce.

Looking at today’s US calendar we get the November Markit PMI data, December Empire State manufacturing survey, NAHB housing market index, October net long-term TIC flows, total net TIC flows.

Market Snapshot

S&P 500 futures up 0.3% to 3,181.25

STOXX Europe 600 up 1% to 416.15

MXAP down 0.1% to 168.88

MXAPJ up 0.06% to 542.89

Nikkei down 0.3% to 23,952.35

Topix down 0.2% to 1,736.87

Hang Seng Index down 0.7% to 27,508.09

Shanghai Composite up 0.6% to 2,984.39

Sensex down 0.1% to 40,950.83

Australia S&P/ASX 200 up 1.6% to 6,849.71

Kospi down 0.1% to 2,168.15

German 10Y yield fell 1.5 bps to -0.304%

Euro up 0.1% to $1.1133

Italian 10Y yield rose 20.4 bps to 1.09%

Spanish 10Y yield fell 0.7 bps to 0.406%

Brent Futures up 0.1% to $65.33/bbl

Gold spot up 0.1% to $1,477.23

U.S. Dollar Index down 0.1% to 97.08

Top Overnight News

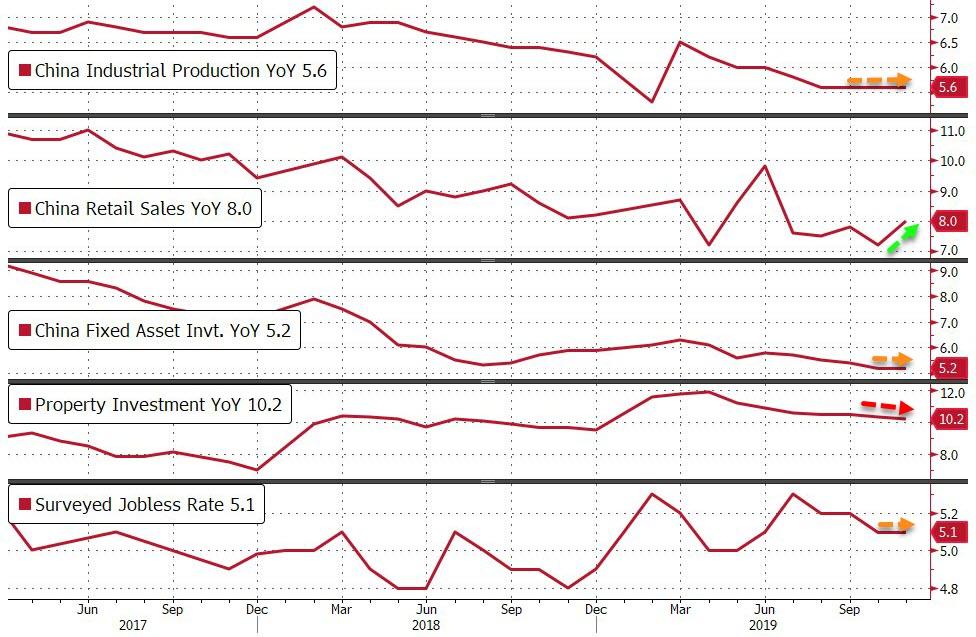

China’s economy showed signs of stabilizing and regaining growth momentum in November; industrial output rose 6.2% from a year earlier, versus a median estimate of 5.0%. Retail sales expanded 8.0%, compared to a projected 7.6% increase. Fixed-asset investment was unchanged at 5.2% in the first eleven months, the same as forecast

President Recep Tayyip Erdogan warned that Turkey could shut down two of the most critical NATO installations on its territory if the U.S. imposes sanctions over its purchase of an advanced Russian missile-defense system

Boris Johnson will appoint top ministers to his cabinet on Monday as he pushes ahead with Brexit, emboldened by the historic majority he won in last week’s British general election

China’s economy showed signs of stabilizing and regaining growth momentum in November, adding to the good news for the nation’s outlook after a preliminary trade deal with the U.S. was reached last week. China steps up talks with U.S. on opening its companies’ books

China’s ambassador to Germany threatened Berlin with retaliation if it excludes Huawei Technologies Co. as a supplier of 5G wireless equipment, citing the millions of vehicles German carmakers sell in China

Australia’s Treasury lowered its forecast surplus for the 12 months through June 2020 to A$5 billion ($3.4 billion) from April’s budget estimate of A$7.1 billion as it scaled back estimated tax revenues, according to the Mid-Year Economic and Fiscal Outlook released in Canberra Monday. It also predicted narrower surpluses for the following three fiscal years

Oil retreated from a three-month high as optimism the U.S.-China trade deal will spur demand for crude gave way to caution due to the agreement’s limited nature and lack of detail

Hong Kong’s demonstrators clashed with police late Sunday as Chief Executive Carrie Lam visited Beijing where she’s expected to update Chinese President Xi Jinping and other senior officials on the violent protests that have gripped the city for the past six months. Chinese Premier Li Keqiang gives Hong Kong leader fresh boost after protests

Asian equity markets traded mixed following relatively light newsflow over the weekend and last Friday’s flat performance on Wall St. where the major indices consolidated near record levels after the confirmation of a US-China Phase One deal which officials plan to sign in early January, although some noted the deal was only limited and questions arose over the feasibility of China committing to as much as USD 50bln of US agriculture goods. ASX 200 (+1.6%) was lifted by outperformance in defensives and the top-weighted financials sector with sentiment buoyed after the world’s 2 largest economies averted the December 15th tariffs, while Nikkei 225 (-0.3%) was subdued by the recent pullback in USD/JPY and as the latest Japanese Manufacturing PMI data remained in contraction territory. Hang Seng (-0.7%) and Shanghai Comp. (+0.6%) were constrained despite the phase one agreement confirmation and better than expected Chinese data in which Industrial Production and Retail Sales both topped estimates, as the stats bureau stated the economy still faces relatively big downward pressure and amid expectations for a reduced growth target for next year, while the mood in Hong Kong was also soured by a rise money market rates (Overnight HIBOR +57bps) and the resumption of violent protests over the weekend. Finally, 10yr JGBs were flat with prices hampered by last week’s resistance levels and with demand also subdued due to the absence of the BoJ in the market today.

Top Asian News

Top Turkish Bankers Say They Were Fired on Orders of Regulators

India Protests Spread as Anger Against Citizenship Law Grows

Masayoshi Son’s Bankers Are Worried About Their Favorite Client

Philippine Stocks Sink to Two-Month Low as Utilities Retreat

European equities kick-start the week on the front foot [Eurostoxx 50 +0.7%] following on from a relatively mixed APAC session, with traders citing an overall improvement in the trade environment as a reason for the advances. Cash Stoxx 600 (+1.1%) managed to notch intraday record highs, albeit the FTSE 100 (+2.1%) stands as the marked outperformer amid further post-election tailwinds on large-cap stocks, miners benefitting from rising copper prices and exporters taking advantage of a declining Sterling – Standard Chartered (+3.3%), RBS (+3.2%), Barclays (+3.5%), Glencore (+4.0%), BHP (+3.2%), Rio Tinto (+2.9%) and Antofagasta (+2.7%). DAX and other core European indices stalled gains amid disappointing December Flash PMIs. Sectors opened modestly in positive territory but have since gained traction, with cyclical Materials and Financials outperforming on the back of FTSE 100 gainers. In terms of other individual movers, Novartis (unch) opened lower after the Co. stated it will be dropping development of its asthma drug amid a string of disappointing trials. Meanwhile, Kerry Group (-3.5%) shares fell to the foot of the pan-European index after losing a USD 26bln deal to International Flavours and Fragrances for US-listed DuPont’s nutrition division (+1.9% pre-market). Last but not least, Sports Direct (+20%) soared on the back of a profit jump with group revenue increasing 14% YY which comes amid performance woes after the Co. acquired the troubled House of Fraser.

Top European News

Euro-Area Economy Ends 2019 Still Struggling as Momentum Stalls

Factory Woe Puts U.K. Economy on Brink of Contraction, PMI Shows

German Factory Slump Deepens Again as Recovery Seems Elusive

U.K. Rainmakers Eye Dealmaking Return Post Tory Election Win

In FX, Sterling’s post-UK election 2nd coming was already fading after a fleeting foray above 1.3400 vs the Dollar and test of resistance around the psychological 0.8300 level against the single currency when the preliminary PMIs for December confounded expectations for some improvement and missed consensus by quite a distance, especially in the manufacturing sector. Cable duly retreated towards 1.3325 and the cross rebounded to circa 0.8350 even though the earlier Eurozone flash surveys were also disappointing, and Germany’s manufacturing headline in particular. However, Eur/Usd remains depressed within a 1.1123-50 range and may struggle to pull away from decent option expiries between 1.1120-25 and 1.1100-10 (1.2 bn clips) rather than challenging slightly larger interest at 1.1150 (1.3 bn).

NZD/CAD/AUD – All firmer vs their US counterpart that continues to flounder (DXY anchored around 97.000), with the Kiwi keeping tabs on the 0.6600 handle, Aussie hovering just under 0.6900 and Loonie pivoting 1.3150 in wake of some upbeat Chinese data overnight (ip and retail sales) and further reserved reflection on US-China trade deal Phase 1. Nzd/Usd and Aud/Usd have both regrouped after losing some ground on independent impulses via growth forecast downgrades from the NZIER and government respectively, while the former also took note of Westpac rolling its RBNZ rate cut prediction to August next year from February.

NOK/SEK – The Scandi Crowns are both holding firm lines ahead of this week’s Norges Bank and Riksbank policy meetings, but Eur/Nok’s retreat is more technical after breaching the 100 DMA (10.0385) compared to Eur/Sek’s reversal through 10.4300 in anticipation of a 25 bp repo rate hike on Thursday.

CHF/JPY – The safe-haven Franc and Yen are narrowly mixed against the Buck, with Usd/Chf nearer the bottom of a 0.9825-45 band in contrast to Usd/Jpy hovering just below 109.50 compared to 109.25 at one stage and flanked by expiries between 109.00-05 and 109.50 in 1bn.

In commodities, little to report on the commodities front – with WTI and Brent futures largely unchanged on the day, albeit in positive territory after a relatively flat APAC session. WTI futures trade on either side of USD 60/bbl whilst its Brent counterpart topped USD 65/bbl in recent trade with little by way of fresh fundamental catalysts, and with participants somewhat cautious of the US-China Phase One deal amid a lack of details and a paucity on China’s commitments. Elsewhere, gold prices remain choppy within a tight USD 5/oz range thus far, as traders and investors await further Phase One details. Copper meanwhile has resumed its upwards trajectory with risk-sentiment a cited factor, although upside may be more due a receding USD and above-forecast China industrial production and retail sales. Finally, Dalian iron ore futures fell in excess of 1.5% after data showed weekly utilisation rates at 163 mills across China slumped almost 66 – thus casting fresh doubts on demand for the base metal.

US Event Calendar

8:30am: Empire Manufacturing, est. 4, prior 2.9

9:45am: Markit US Composite PMI, prior 52

Markit US Manufacturing PMI, est. 52.6, prior 52.6

Markit US Services PMI, est. 52, prior 51.6

10am: NAHB Housing Market Index, est. 70, prior 70

4pm: Net Long-term TIC Flows, prior $49.5b

DB’s Jim Reid concludes the overnight wrap

This is the last full week of the year and there are still a number of interesting events/data points to get through before the soporific Xmas week. I’m starting it a bit tired as for the second night in a row I fell asleep trying to finish “The Irishman” – the new Scorsese/De Niro et al film with de-ageing technology used. It’s very very good but 3hr 30mins is a little tough to watch in one (or even two) sitting(s) after a day running after atrociously behaved children. We’ll be trying to finish tonight.

As for this week, today’s global flash PMIs stand out, along with the German IFO (Wednesday) and the BoE/BoJ meetings (Thursday). We don’t often mention the Swedish central bank decision as a main highlight but on Thursday it’s expected that the Riksbank will end Sweden’s five year experiment with negative rates and take them back to zero even though they haven’t met their inflation target. As concerns over the side effects of negative rates rise around the world, especially in Europe, a lot of attention will be placed on how the Swedish economy and banking system deals with this in the months ahead.

More on the week ahead below but after a lot of drama we finally got a Phase One trade deal between the US and China, confirmed by both sides on Friday. The legal work, full details and signing (probably in January) is still to come but it appears that agreement has been made. The immediate consequence is that the tariffs scheduled to have come into effect yesterday have now been suspended. Meanwhile, tariffs on $120bn of Chinese imports by the US will be halved from 15% to 7.5%, although 25% on a remaining $250bn worth will remain, and the fact sheet released by the US Trade Representative’s office said that China has committed “to import various U.S. goods and services over the next two years in a total amount that exceeds China’s annual level of imports for those goods and services in 2017 by no less than $200 billion.” Looking forward, President Trump tweeted that discussions on the Phase Two deal would begin “immediately”, as opposed to after next year’s presidential election. There will clearly be relief that it looks like a deal has been done but there are fewer tariff rollbacks than some had thought likely and Mr Trump’s comments suggest phase two will be a live issue straight away. My base case was that this would wait until after next November’s election assuming he won. So it will be very interesting as to how much Trump keeps the negative China rhetoric alive in 2020 after the deal is eventually signed.

Staying with politics and as an additional word on the U.K. election result from the end of last week, I wonder if it marks a new chapter in populism. The victorious Conservative Party is traditionally a party of the better off with the Labour Party the party of the poorer and working class communities. The problem is that the working class is generally in favour of Brexit and the Conservatives ruthlessly exploited this and they subsequently voted for them in waves in areas that haven’t for a century in some cases. To maintain this support the Tories will have to shape policy to help those left behind by globalisation (mostly in the north of the country) and by definition reduce inequality. If you want to see a great graph look at the FT today where they show a scatter of the percentage of blue collar jobs in a constituency against the vote swing in this election in favour of the Tories. There was a big correlation. Although politics isn’t often rational, it would make perfect sense if this election heralded a spending bias towards the poorer parts of the U.K. that voted for Brexit. In terms of the read through to other countries, to arrest the rise of populism we’ve always thought mainstream parties will adopt more populist policies aimed at the so-called left behinds. No-one has done this better in terms of winning an election than Mr Trump in the US and Boris Johnson in the U.K. The confusing thing about the Trump presidency is that his tax cuts were biased towards the rich which is probably why the likes of Warren and Sanders remain in the Presidential race and populism is still alive there. As we said on Friday though, the U.K. election result may at the margin make Democratic voters conclude that a lurch too far to the left is dangerous in Anglo-Saxon countries. We will see. Nevertheless the concluding remark is that the U.K results show that populism is far from dead – it’s just that mainstream parties can morph into populist parties if the will is there. To me it seems that European mainstream parties have so far struggled with this. I wonder if lessons will be taken from this on the continent.

Overnight, we’ve seen a number of data releases from China that have surprised to the upside, something that will further boost sentiment after the reaching of a Phase One agreement with the US. November retail sales were up +8.0% yoy (vs. +7.6% expected), while industrial production was up +6.2% yoy (vs. +5.0% expected). That said, fixed-asset investment over the Jan-Nov period was only up +5.2% yoy, the joint weakest since at least 1998 where data became more readily available. Equity markets in Asia are treading water this morning though, with the Nikkei (+0.03%), the Shanghai Comp (+0.06%) and the Kospi (-0.05%) seeing little movement in either direction, though the Hang Seng is down -0.37%. S&P 500 futures are up +0.28% following another record high for the index on Friday.

In terms of a fuller rundown of the week ahead, for today’s PMIs, we’ll see manufacturing, services and composite PMI data for France, Germany, the Euro Area, UK and the US. So quite a collection to watch for, especially as the market expectation is that the global economy is steadily turning after recently bottoming out. In November, the PMIs showed some sign of this in the Euro Area with a 50.6 reading for the composite PMI, but which included both Germany (49.4) and Italy (49.6) in contractionary territory led by manufacturing.

With the Fed and the ECB having announced their policy decisions in the week just gone, attention will turn to central banks elsewhere over the week ahead. The major action takes place on Thursday, with the Bank of Japan, Bank of England, Riksbank, the Banco de Mexico and Bank Indonesia all announcing policy decisions that day. As we said at the top the Riksbank might be the most interesting longer-term as they are expected to end a 5-year dalliance with negative rates. The rest of the world will be watching to see if the sky falls in or whether this helps persuade people that negative rates are part of the problem. My guess is the latter when the history books are written.

In terms of central bank speakers next week, there’s a conference being held at the ECB on Wednesday in honour of Benoît Cœuré, whose 8-year tenure on the ECB Executive Board concludes at the end of the month. Cœuré himself, along with ECB President Lagarde and the Fed’s Brainard will all be making remarks there. In the US, we’ll also hear tomorrow from New York Fed President Williams, Boston Fed President Rosengren, and Dallas Fed President Kaplan. Chicago Fed President Evans will also be speaking on Wednesday.

Staying with Europe, Wednesday sees the publication of the latest Ifo survey from Germany. Last month, the business climate indicator rose to its highest level since July, so it’ll be interesting to see if recent momentum is sustained, with the consensus looking for a modest increase to 95.5. Separately, Wednesday also sees the final release of the CPI and core CPI readings for the Euro Area in November, and on Friday there’ll be the advance December reading of the European Commission’s consumer confidence reading for the Euro Area.

From the US, we also have a number of key readings out this week. Alongside the PMIs, Tuesday sees the release of November’s industrial production figures, as well as housing starts and building permits data. Last month, building permits rose to their highest level since May 2007, so it’ll be interesting to see if this strength in the recent data is sustained. Friday sees the final Q3 US GDP reading where the component breakdown will influence Q4 thinking.

Recapping Friday and last week now. Global markets were buoyed by the combination of a Phase One deal between the US and China, along with signs of a resolution to the immediate Brexit impasse from the UK election. The S&P 500 ended the week up +0.73% (+0.01% Friday) at a new record high, while in Europe the STOXX 600 was up +1.15% (+1.09% Friday) at its highest level since April 2015. Bond yields ended the week slightly lower after a sizeable trading range, with 10yr Treasury yields down -1.4bps (-7.0bps Friday), and 10yr bund yields -0.3bps (-2.0bps Friday). The removal of downside risks to the global economy saw investors move into other risk assets, with brent crude up +1.29% (+1.59% Friday) last week, while the spread of BTPs over bunds narrowed by -8.9bps.

Meanwhile, UK assets rallied on Friday as it emerged the Conservatives had won an 80-seat majority at the general election. Sterling ended the week up +1.45% (+1.29% Friday) at $1.3331, its highest level since March, while against the euro it was up +0.94% (+1.39% Friday) at its highest level since July 2016. UK equities also outperformed, with the FTSE 100 up +1.57% (+1.10% Friday), while the more domestically-focused FTSE 250 index was up +2.75% (+3.44% Friday). Banks in particular rose following the result, with Friday seeing big share price moves for Lloyds Banking Group (+5.25%), Barclays (+6.18%) and RBS (+8.39%). The other major rises were seen from the companies that had been floated as targets for nationalisation by Labour. Centrica, parent of British Gas, was up +10.51% on Friday, its best day since November 2008, while BT Group was up +6.54%, its best since November 2018.

Finally, in terms of data on Friday, US retail sales were weaker than expected, with a +0.2% (vs. +0.5% expected) increase in November, although the previous month was revised up a tenth to +0.4%. The year-on-year figure fell to +2.9%, its lowest since June. In spite of the figures, Fed Vice Chair Clarida said on Fox Business that “the U.S. consumer’s never been in better shape in my professional career.” Elsewhere, New York Fed President Williams also sounded a positive note on the outlook, saying that “we’ve got the economy on a very strong footing, sustainable footing, for good growth next year.”

The Constitution specifies that the “Senate shall have the sole Power to try all Impeachments,” and that when “sitting for that Purpose, they shall be on Oath or Affirmation.” The Senate rules have long specified the oath that the senators will take at the start of an impeachment trial. They will each have to affirm that “in all things appertaining to the trial of the impeachment of Donald J. Trump, now pending, I will do impartial justice according to the Constitution and laws.”

Things are about to get a little awkward. Lindsey Graham has apparently committed himself to being the most sycophantic senator in the Republican caucus. Thus, as the House prepares to impeach the president, Graham felt the need to publicly declare, “I am trying to give a pretty clear signal I have made up my mind. I’m not trying to pretend to be a fair juror here” and “I’ve clearly made up my mind, I’m not trying to hide the fact that I have disdain for the accusations and the process.”

But Graham is hardly alone. Republican senators have been badgered for months on the question of whether Trump should be impeached and removed—often by those hoping they would say, “yes.” Some have demurred. Some have clearly indicated that they expect to vote to acquit. Democratic senators are no different. Elizabeth Warrenhas been calling for the president’s impeachment and removal for months. Others have likewise found it to be politically expedient to show that they are card-carrying members of “the resistance” and want Trump to be ousted from office as soon as possible.

This has led to some silliness, such as the suggestion that Chief Justice John Roberts should refuse to allow Lindsey Graham to participate in the Senate trial or that the Democratic senators running for the presidency should recuse themselves. No one should hold their breath waiting for individual senators to recuse themselves or for the Senate as a whole to vote to recuse any senator. Each and every senator, from the most dedicated Trump loyalist to the most fierce Trump critic, will have the opportunity to vote on whether the president should be convicted of high crimes and misdemeanors.

We’ve seen worse conflicts of interest. When President Andrew Johnson was put on trial in the Senate in 1868, the senators who sat in judgment of him were not exactly disinterested parties. The Republican Congress had set up the impeachment by passing the Tenure of Office Act, over Johnson’s veto, barring him from removing Cabinet members without the consent of the Senate and including in its terms that any violation would be a “high misdemeanor.” Republican senators gave instructions to Johnson’s secretary of war as the president sought to fire him, and thus played a key role in the very event that was the basis of the president’s impeachment. Ohio senator Benjamin Wade would assume the office of the president if Johnson were convicted. Tennessee senator David Patterson was the president’s son-in-law. Both were allowed to participate in the trial. The right of their constituents to have their representatives in Congress participate in the impeachment and trial of the president was understood to be far more important than the right of the president or the House to exclude senators who might be less than impartial judges. Legislators have sometimes asked to be excused from voting in such proceedings, but they have never been disqualified from doing so.

The Senate impeachment trial is not like an ordinary judicial trial. Senators are understood to already be familiar with the case by the time it reaches their chamber. They are not shielded by the rules of evidence from hearing the kinds of testimony or seeing the kinds of documents that might be regarded as too prejudicial in an ordinary courtroom. They are not expected to be sequestered so as to avoid publicity regarding the case. They are not instructed to avoid discussing the case with others. Senators can expect to be relentlessly lobbied by their constituents, their colleagues, the media and others up until the moment that they cast their final vote. The Senate took a recess during Andrew Johnson’s trial so that the senators could attend the Republican national convention, which nominated Ulysses S. Grant for the presidency and debated whether to endorse the impeachment and whether to condemn the Republican senators who would not vote to convict.

The senators are not jurors in a legal trial. They are political actors charged with the task of inquiring into an officer’s alleged misconduct and taking whatever action might be necessary to secure the public interest (constrained by the constitutional limit of removal and disqualification from office—no beheadings allowed).

The senators have a duty to do impartial justice according to the Constitution in the impeachment trial of the president. That surely means, among other things, that they have a duty to vote to acquit if they believe that the president has not committed an impeachable offense under the Constitution. It means that they have a duty to conduct a trial that provides both sides an adequate opportunity to present their case. They have a duty to consider the evidence and the legal arguments that are relevant to determining whether the president has committed an impeachable offense. They have a duty to vote to convict if they believe that removal is constitutionally justified.