Futures Bounce After BOJ Jawbone; Traders Remain On Edge Ahead Of Payrolls

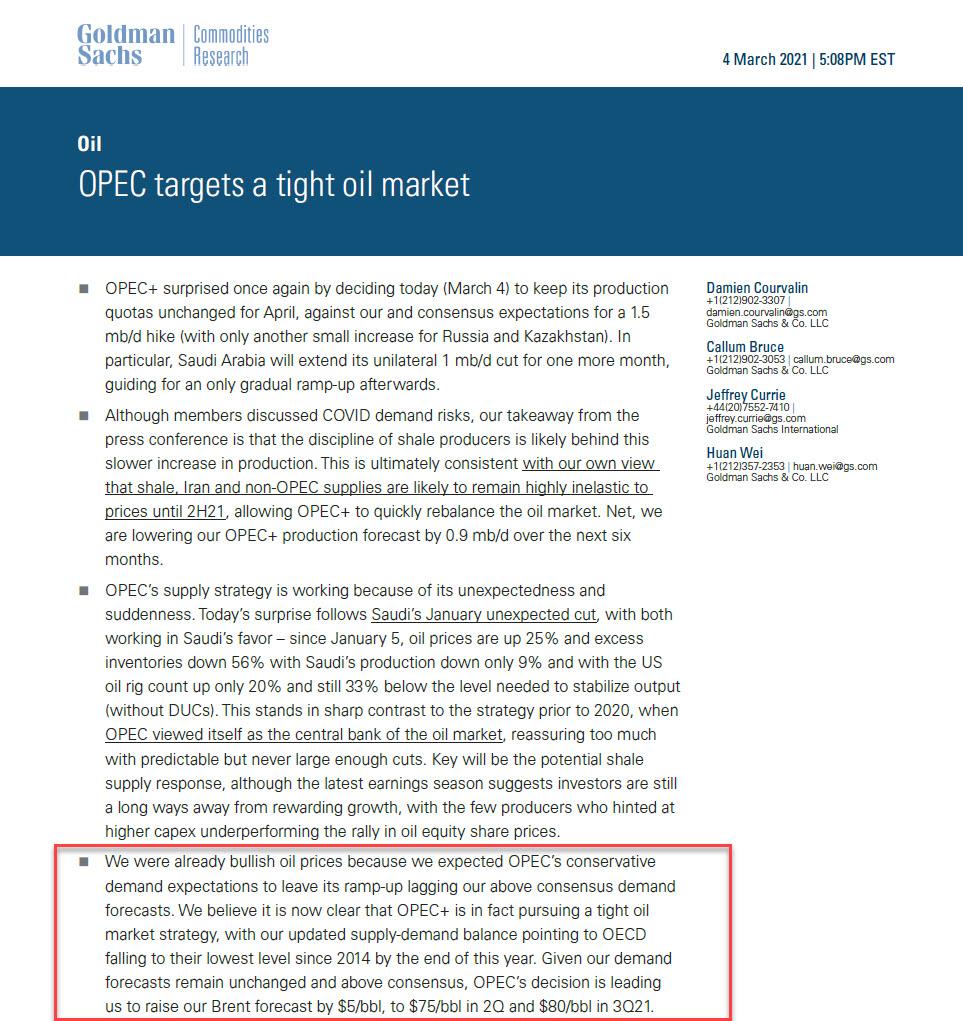

For the second day in a row US equity futures rebounded from an overnight rout that dragged spoos as low as 3,730 as investors kept a worried eye on US TSY yields ahead of key U.S. jobs data which better be crappy or else the reflationary panic may send the Nasdaq to 0 today. Treasuries also reversed an overnight loss, with their yields down one basis point to 1.55%; the dollar continued its advance. Oil surged more than 2% on Friday, hitting their highest in nearly 14 months after OPEC, with Brent rising above $68 after Goldman hiked it Q3 price target to $80.

At 730 a.m. ET, Dow E-minis were up 56 points, or 0.19%, S&P 500 E-minis were up 8.75 points, or 0.23% and Nasdaq 100 E-minis were up 14.50 points, or 0.14%. Contracts on the S&P 500 and Dow Jones Industrial Average turned higher along with those on the tech-heavy Nasdaq 100 after a three-day pullback for the S&P 500 and the Nasdaq, as investors looked to data that is likely to show accelerated jobs growth in February. On Thursday Jerome Powell maintained the central bank’s dovish stance to support maximum employment and said inflation was not a worry at the moment. But as markets made very clear, his comments disappointed investors who expected him to act on the recent spike in the U.S. 10-year Treasury yield that has set the S&P 500 and the Nasdaq on course for their third straight weekly decline, with the tech-heavy index not only sliding negative for the year, but briefly entering a 10% correction from its Feb. 12 intraday record.

Energy companies remained the only bright spot, with Chevron and Exxon firmed about 2% each as oil prices jumped to a near 14-month high. Shares of Broadcom fell about 2.6% after the company reported chip sales slightly below analysts’ estimates, joining a growing list of chip industry peers hit by a global semiconductor shortage. Costco dropped 1.6% after the warehouse club operator missed estimates for second-quarter profit.

Similar to US futures, Europe’s Stoxx 600 index pared a decline as shares of energy companies rallied. Ten-year Treasuries stabilized, with their yields down two basis points to 1.54%. The travel and leisure subgroup fell 2.5%, and was the worst performer in Europe’s Stoxx 600 Index, with airlines among the biggest decliner (IAG -3.7%, Ryanair -3.1%, Lufthansa -3%). “We’ve seen some solid gains in this sector over the past two to three weeks, so there could well be some froth getting blown off the top of the recent recovery,” Michael Hewson, chief market analyst at CMC Markets, says in written comments. Here are some of the biggest European movers today:

- ConvaTec shares climb as much as 4.8%, the most intraday since Nov. 10, after the company reported FY results, which Stifel described as a “nice beat” with an encouraging 2021 outlook.

- Norsk Hydro gains as much as 3.2% after the announced sale of its rolling business to KPS Capital Partners. Barclays says the business was sold for a good multiple.

- Corbion shares fall as much as 10%, the most in almost a year, after results from the Dutch supplier of lactic acid that ING describes as “bittersweet.”

- Argenx shares drop as much as 8.6%, the most since July 30, extending losses for a fourth consecutive day following worse than expected earnings on Thursday.

- London Stock Exchange Group shares drop as much as 7.8% as the exchange and data group’s cost guidance disappointed analysts. Morgan Stanley says cost outlook reflects investments to transform combined business and achieve synergies, along with recent small acquisitions by Refinitiv.

Asian stocks fell earlier, heading toward the lowest level in a month, after an overnight surge in U.S. bond yields and a slower-than-expected China growth target. Key gauges in China and Hong Kong declined after Beijing targeted GDP growth of 6% this year, below economist estimates, at the start of the nation’s National People’s Congress. Still, by the end of the day, both the CSI 300 and Hang Seng indexes pared drops of at least 2%. Regional benchmarks fell the most in Australia, India and South Korea. Japan’s government recommended extending its virus state of emergency for the Tokyo region by two weeks. Communication services and health care companies were the biggest drag on the MSCI Asia Pacific Index. Energy stocks outperformed across the Asia Pacific region, climbing with oil after the OPEC+ alliance decided to keep output unchanged.

Overnight, Chinese Premier Li delivered the government work report at the start of the NPC and announced that China targets GDP growth of above 6% this year, with CPI target at around 3% and a budget deficit target of around 3.2% of GDP. Some other highlights:

- Premier Li stated that China will keep liquidity reasonably ample and large commercial banks will increase SME loans more than 30% this year, while China is to further push loan rates lower and guides the financial system to sacrifice profit for the real economy.

- Furthermore, Li stated that China will further reduce the negative list for foreign investment and will not make a sharp turn in macro policies this year but will provide targeted support for enterprises and industries enduring a sustained impact from the pandemic, as well as expand effective investment and promote steady development in imports and exports.

- China announced it will keep economic operations within a reasonable range in 5 years and will keep liquidity reasonably ample, as well as keep growth in money supply and social financing basically in line with nominal GDP over next 5 years.

- China will step up breakthrough in tackling frontline technologies such as AI, quantum information, semiconductors, gene and biotech over next 5 years, as well as develop vaccines against major infectious diseases in its 5-year plan.

- China will reduce import tariffs and increase imports of consumer goods, advanced technologies and energy products, with the 5-year plan to also bolster the role of consumption in supporting economic development.

- Furthermore, China will resolutely deter any Taiwan separatist activity and a parliament official said China they will conduct changes to the number, composition and method of forming Hong Kong’s Election Committee which will continue to decide the Chief Executive and will participate in nominating all Legislative Council candidates.

Japan’s Topix reversed an earlier loss to finish higher as technology firms rebounded following the Bank of Japan governor’s remarks on yields. The benchmark gauge closed with a 0.6% gain, erasing a loss of as much as 1.3%. The Nikkei 225 Stock Average trimmed most of its 2.1% decline but finished slightly down as Fast Retailing fell on a UBS downgrade. BOJ Governor Haruhiko Kuroda made it clear a widening of the movement range around the central bank’s 10-year yield target is off the table for a policy review later this month, triggering a tumble in Japanese yields.

The plunge, which leaves Japanese investors with few yield options, means that it is only a matter of time before Japanese pension funds have to start buying US TSYs. Elsewhere, electronics stocks erased a loss to rise for the first time in four days. Chemicals, machinery and autos shares also reversed declines as the yen extended a steep loss against the dollar. Commodities-related stocks gained after oil jumped. “Because of the steep downward correction in stock prices, people were thinking they are at good levels to buy and they saw domestic long-term yields slipping, which spurred expectations that the easy monetary stance that has been backing share prices gains isn’t likely to change,” said Ikuo Mitsui, a fund manager at Aizawa Securities Co.

After another round of fireworks on Thursday, Treasuries were steady on Friday with yields slightly richer across the curve and futures off daily highs ahead of February jobs data. Yields richer by 1bp-2bp across long-end of the curve, slightly flattening spreads; 10-year near flat around 1.56% with gilts, bunds lagging by ~5bp and ~2bp. Markets were heavy during Asia session, focused on next week’s supply, comprising 3-, 10- and 30-year auctions. European bonds underperformed, catching up to the selloff in Treasuries during U.S. afternoon Thursday following Fed Chairman Powell’s comments.

Treasuries whipsawed Thursday on disappointment that Federal Reserve Chair Jerome Powell offered no specific course of action to rein in long-term rates, no mention of SLR treatment and no mention of turmoil in the repo market. Bond yields climbed in recent weeks on mounting expectations of stronger economic growth and price pressure, with erratic moves unsettling stocks as well. The February U.S. employment report on Friday will give a much-needed update on the speed and direction of the country’s labor-market recovery.

“It makes logical and intuitive sense that Treasury yields should move back up to 1.50% or 2%, but we are concerned with the rest of the market about the speed at which it’s getting there,” said Mona Mahajan, investment strategist at Allianz Global Investors LLC.

While most markets were generally unchanged, oil prices were not and crude soared after the OPEC+ alliance surprised traders with its decision to keep output unchanged. West Texas Intermediate crude rose above $65 a barrel for the first time since January 2020 and Brent was trading above $68…

… after Goldman raised its oil price target for Q2 and Q3 by $5.

Today’s crucial nonfarm payrolls report (previewed here) is expected to show a +200K increase in jobs as the U.S. economy benefited from falling new COVID-19 cases, quickening vaccination rates and additional pandemic relief money from the government. However, the report will also be a reminder that the recovery in the labor market is excruciatingly slow.

Investors are also keeping an eye on progress in President Joe Biden’s a $1.9 trillion coronavirus aid bill with a sharply divided U.S. Senate expected to begin a contentious debate on Friday on the legislature.

To the day ahead now, and the main highlight will likely be the aforementioned US jobs report for February, but other releases include German factory orders and Italian retail sales for January. Central bank speakers include the Fed’s Bostic and the BoE’s Haskel.

Market Snapshot

- S&P 500 futures down 0.5% to 3,746.00

- MXAP down 0.7% to 205.65

- MXAPJ down 1.0% to 690.66

- Nikkei down 0.2% to 28,864.32

- Topix up 0.6% to 1,896.18

- Hang Seng Index down 0.5% to 29,098.29

- Shanghai Composite little changed at 3,501.99

- Sensex down 1.1% to 50,306.48

- Australia S&P/ASX 200 down 0.7% to 6,710.85

- Kospi down 0.6% to 3,026.26

- Brent futures up 2.1% to $68.13/bbl

- Gold spot down 0.3% to $1,692.84

- U.S. Dollar Index up 0.39% to 91.99

- Euro down 0.4% to $1.1923

- Brent Futures up 2.1% to $68.14/bbl

Top Overnight News from Bloomberg

- China set a conservative economic growth target that signals more restrained monetary and fiscal policies this year, in contrast to other major nations still pumping in stimulus. The growth target was set at above 6%, well below economists forecasts, Premier Li Keqiang said Friday at the opening of the National People’s Congress

- Traders in the $21 trillion U.S. Treasury market are sending a clear signal that they intend to keep pushing yields higher until they upend financial conditions sufficiently to spark action from the Federal Reserve

- Corporate borrowing costs and gauges of credit risk rose around the world after Federal Reserve Chair Jerome Powell stopped short of detailing how he might tamp down a spike in rates. The Markit CDX North American Investment Grade Index, which investors use to hedge against losses on company notes, widened to a four- month high

- Surging ethical debt sales are helping to fuel the best-ever start to a year in Europe’s market for new bonds

- The U.K. Financial Conduct Authority confirmed Friday that the final readings for most Libor rates will take place at end of this year, with just a few set to linger for a further 18 months

Quick look at global markets courtesy of Newsquawk

Asia-Pac bourses extended on recent declines amid spillover selling from US where tech took the brunt again and the bond rout persisted after market participants were underwhelmed by the latest rhetoric from Fed Chair Powell who stuck to a dovish script and noted that that the current stance is appropriate which came as a disappointment for those awaiting commentary on SLR adjustments, YCC or operation twist. ASX 200 (-0.7%) was pressured by broad losses across its sectors and amid concerns of an impact to the ongoing vaccine rollout efforts after the EU blocked a shipment of AstraZeneca vaccines to Australia citing the drug maker’s failure to honour EU contracts, although there was notable outperformance in energy names after the OPEC+ decision to roll over current output curbs and with Saudi also maintaining its voluntary cuts for April. Nikkei 225 (-0.2%) was subdued in tandem with the global lacklustre risk appetite and as exporters suffered from a predominantly stronger currency, with participants looking towards PM Suga’s COVID announcement later after the government recommended a 2-week extension for the state of emergency in Tokyo. Hang Seng (-0.5%) and Shanghai Comp. (U/C) were initially negative after the PBoC continued with its tepid liquidity operations and with the US proposing to build an anti-China missile network to bolster its deterrence against China in islands including Taiwan, Okinawa and Philippines which China sees as its first line of defence. Chinese markets then gradually pared losses in the aftermath of Premier Li Keqiang opening speech at the NPC in which he delivered the government work report and announced an official growth target of above 6% for this year which also helped Hong Kong alleviate the pressure from the recent tech sector woes. However, pressure was seen as the session came to a close and European participants began entering the fray. Finally, 10yr JGBs were initially subdued and declined beneath the 151.00 level amid a resumption of the global bond rout but then prices surged on reopen of from the lunch break after comments from BoJ Governor Kuroda that he doesn’t think it is necessary and appropriate to widen the band around the BoJ’s long-term rate target, while he added that now is the time to keep the yield curve stably low.

Top Asian News

- Xi to Revamp Hong Kong Elections, Eliminate ‘Anti-China Forces’

- Hong Kong Arrests 12, Seizes $116 Million After Stock Scam

- China Sees Negative-Yielding Bonds in Burst of Friday Trading

- China to Pour More Money Into Chips, AI and 5G to Catch U.S.

European equities kicked off the last session of the week softer across the board (Euro Stoxx 50 -0.4%) following on from a similarly lacklustre APAC lead. US equity futures initially conformed to this tone but have experienced some mild support on the US’ entrance to market. Moreover, fundamental catalysts have remained light in this morning after Fed Powell’s speech underwhelmed equity markets in the run-up to the US jobs report. Back to Europe, all sectors opened in negative territory aside from Oil & Gas – which sees underlying support from the broader price action in the energy complex. However, since the market open Oil & Gas has been choppy but the energy (+1.5%) sub-sector remains firmer. To the downside, Travel & Leisure (-1.3%) is the notable laggard which may be due to the markets trying to pare back some of their recent “re-opening” gains, whilst Germany also warned of COVID variants spreading across Germany. Aside from this, Media (-1.0%) and Insurance (-1.3%) also see a downbeat performance in early morning trade. Alongside this and in terms of narratives, the broader sectors (ex-energy) portray more of a risk-off bias as defensives fare slightly better than cyclicals, but the Consumer Staple (-0.4%) sub-sectors remain in the red. In terms of individual movers, in-fitting with the price action seen this morning there are only a handful of companies within the Stoxx 600 that trade in the green. Unsurprisingly, energy names including Shell (+1.8%), BP (+2.4%), Total (+1.5%) and Tullow Oil (+9.0%) are firmer but off best levels. Moving on, LSE (-9.0%) is in the red despite a beat on FY Total Income, GBP 2.44bln vs exp. GBP 2.43bln, and the Co. stating it is nicely positioned for future growth despite an uncertain macro-economic & regulatory environment. Continuing on the earnings front, Dassault Aviation (-0.8%) reported a better-than-expected FY revenue EUR 5.49bln vs exp. EUR 5.16bln but remain hindered on broader price action and perhaps after outlining a lower than expected dividend distribution.

Top European News

- Aggreko Agrees to $3.2 Billion Takeover by TDR, I Squared

- London Stock Exchange Increases Dividend on Confident Outlook

- U.K. Government Defends Proposing 1% Pay Rise for Health Workers

- Surgical Glove Maker Catapults Into Poland’s Stock Benchmark

In FX, a quick look at the Dollar index and its latest exertions effectively tells the full story, as it extended gains beyond all remaining technical and psychological barriers on the way to topping 92.000, but the impetus behind the most recent rally came from another jump in UST yields following an address from Fed chair Powell that did not match considerable if not consensus expectations for some form of policy response. Explicitly, a significant proportion of the ‘market’ was looking for a QE twist, WAM or sign that expiring SLR exemptions might be extended, but were left disappointed and the Buck proceeded to breach upside chart levels that were proving tough to scale convincingly, like the 100 DMA. NFP looms next, but in the current environment only a real shocker and worse than the last payrolls miss is likely to stop bond bears and Buck bulls in their tracks, and even in that event the latter may benefit from heightened safe-haven demand if equities suffer on labour market concerns rather than long term rate angst.

- AUD/NZD – It seems almost churlish to single out a G10 loser as several currencies are contesting the race to the bottom vs the Greenback, but in percentage terms the high betas and cyclicals are naturally nursing heavier losses. The Kiwi is now under 0.7150 attempted to reclaim and sustain 0.7300+ status on Tuesday and Wednesday, while the Aussie has lost grip of the 0.7700 handle and is trying to keep its head above 0.7650 compared to consecutive peaks just shy of 0.7840 on March 2nd and 3rd.

- GBP/JPY – Sterling has surrendered another big figure to the resurgent Dollar, and Cable is now in danger of letting go of 1.3800 following a couple of forays beyond 1.4000, while the Pound has also retreated against the Euro after testing, but not breaking 0.8600 yesterday. Similarly, after defending 107.00 quite resolutely, the Yen has subsequently caved and put up relatively little fight through the 100 WMA (107.24), 107.50 or 108.00 on the way down to 108.50 and a fraction below in wake of somewhat mixed messages from BoJ Governor Kuroda. To recap, he expressed a desire to keep the JGB curve low and stable, but also stated that widening the 10 year yield target is likely to be up for debate.

- CHF/EUR/CAD – The Franc has pared some declines from sub-0.9300 vs the Buck and more against the Euro from circa 1.1150, but is still among the worst major performers over the week given its depreciation from 0.9075+ and 1.0970+ respectively. Nevertheless, the Euro has not gone unscathed as it hovers beneath 1.1950 and a key chart ‘support’ at 1.1945 vs 1.2110+ just 2 days ago, albeit holding above 1.1900 with some assistance from the aforementioned bounce in Eur/Gbp. Elsewhere, the Loonie is striving to contain losses between 1.2651-1.2711 parameters by virtue of crude prices that have rebounded further in relief post-OPEC+, and will look towards Canadian trade data for some independent direction or distraction from the US labour report.

In commodities, WTI and Brent front-month futures are both firmer on the session and continue to print fresh recovery highs in the aftermath of the OPEC+ confab. To recap, producers surprisingly decided to maintain production curbs – with Saudi unilaterally keeping its 1mln extra cut out of the market, whilst only Russia and Kazakhstan will be easing next month by a combined 150,000 BPD which is far inferior to the 1.5mln BPD cut the market was initially expecting. Due to the lack of easing and the tight supply, some suggest prices will continue to edge higher until the next meeting on April 1st. Furthermore, a number of banks have upgraded their forecasts in lieu of the surprise agreement. Goldman Sachs forecasts Brent to increase to USD 75/bbl in Q2 and USD 80/bbl in Q3 2021 and UBS upgraded its forecast for Brent to USD 75/bbl and WTI to USD 72/bbl for H2 2021 while JPMorgan raised its Brent crude price forecasts by between USD 2-3/bbl to USD 67/bbl this year and USD 74/bbl next year. Citi states the measures taken by OPEC are likely to quicken up the oil stock drawn down and increase prices more than OPEC+ already has. Moving away from OPEC, China announced its GDP growth target of above 6%. In turn, due to China being one of the biggest consumers and producers of commodities it may lead to higher economic activity which could support prices. However, the growth target was on the softer-side of analyst estimates for the figure. WTI resides around mid USD 65/bbl handle (vs low USD 63.84/bbl) and Brent trades near USD 68.50/bbl handle (vs low USD 66.69/bbl). Notable risk events on the table includes US non-farm payrolls and central bank speakers such as Bostic & Haskel. Elsewhere, spot gold fell to a near nine-month low and is set for a third straight weekly decline after Fed Chair Powell remarked that the rise in yields were not “disorderly”. As such, spot gold trades at USD 1695/oz (vs high 1,700/oz) and spot silver resides at USD 25.20/oz (vs low USD 25.04/oz); overall, the metals are relatively little changed on the session. Moving onto base metals, LME nickel is on course for its worse week since 2011 following on from the rising battery-grade supply outlook following the major supply deal in Shanghai. Conversely, LME copper nurses some of its recent losses, potentially deriving support from the China economic announcements.

US Event Calendar

- 8:30am: Feb. Change in Nonfarm Payrolls, est. 198,000, prior 49,000

- Feb. Change in Private Payrolls, est. 195,000, prior 6,000;

- Feb. Labor Force Participation Rate, est. 61.4%, prior 61.4%

- Feb. Average Weekly Hours All Emplo, est. 34.9, prior 35.0; Average Hourly Earnings YoY, est. 5.3%, prior 5.4%

- Feb. Change in Manufact. Payrolls, est. 15,000, prior -10,000; Average Hourly Earnings MoM, est. 0.2%, prior 0.2%

- Feb. Unemployment Rate, est. 6.3%, prior 6.3%

- 8:30am: Jan. Trade Balance, est. -$67.5b, prior -$66.6b

- 9am: Bloomberg March United States Economic Survey

- 3pm: Jan. Consumer Credit, est. $12b, prior $9.73b

DB’s Jim Reid concludes the overnight wrap

Well hopefully today is the last ever day of home schooling in my lifetime. All U.K. schools go back on Monday and to say my daughter can’t wait is an understatement. To say my wife can’t wait is a far bigger one. To say I can’t wait so that everyone is in a far better mood is an ever bigger one still. Fingers, toes and everything else crossed that this is the start of a steady journey towards normality. Next stop golf on March 29th!

This year in markets is going to be anything but steady as yesterday saw yet another episode in the great ongoing tug of war between risk assets and higher yields. This week was always going to be about whether Brainard or Powell pushed back on recent rates market moves. Expectations were high that they would. However the former stayed on message earlier in the week and Powell last night did something very similar. That disappointed markets that had expected more hints of intervention or at least a push back on recent Fed market pricing.

Echoing some of the Fed governors we heard from earlier this week he acknowledged the recent spike in bond yields “was notable and caught (his) attention,” and that he “would be concerned by disorderly conditions in markets or persistent tightening in financial conditions that threatens the achievement of our goals.” He repeatedly tried to assuage markets by making it clear that the Fed was not close to pulling back its bond-buying programs even though he did voice optimism that better economic times were ahead. While Powell was dovish in terms of overall tone, he did not provide any specific details on what the Fed was prepared to do if the committee wanted to pull down long-dated rates. He also emphasised the Fed’s intent on being patient in response to transitory increases in inflation.

In terms of market reaction, 10yr US Treasuries were slightly down (-0.5bps) at the start of Powell’s remarks, but sold off soon after he started speaking. 10yr yields rose +6bps in the half hour that Powell spoke and closed +8.3bps higher at 1.564%. That’s the highest closing level since 20th February last year. 30yr yields increased another +4.5bps to 2.32%. The move in the 10yr was driven by real yields (+9.5bps) as opposed to inflation expectations (-1.3bps) which is not good for risk. Real yields actually rose +13.4bps from their earlier intra-day lows. Yield curves resumed their steepening with the 2Y10Y curve +8.1bps higher at 142bps, the steepest level since November 2015. While we are discussing yields, a reminder of my piece from Wednesday looking at the long-term correlation between yields and credit (link here ). Real yields were key in our analysis so more days like yesterday would be bad. However more days like yesterday will lead to the Fed intervening.

In terms of risk, the S&P 500 was at its intraday high of +0.6% just prior to Powell speaking, the index then fell over -3% from this point before stabilising somewhat and finishing the day down -1.34%. The NASDAQ composite fell further as after being up +0.3% around midday, it lost as much as -3.7% from those intraday highs before finishing down -2.11% in total. The NASDAQ has now lost -6.37% over the last three days, its worst 3-day performance since the first week of September and means the index is now down -1.28% YTD. The S&P 500 was briefly negative on a YTD basis as well, but a late rally saw it close +0.33% YTD having been helped by stronger performances from cyclical industries such as banks, industrials and energy. In terms of the mega-cap tech names, the NYSE FANG index fell another -2.71% yesterday, making that 9 losses in the last 12 sessions. However, the index is still up +1.39% YTD. Elsewhere Tesla and Bitcoin fell -4.86% and -5.95% respectively.

Though Powell dominated the markets’ attention from the European close onwards, the other big story going on was the sharp move higher for oil prices, which surged after the OPEC+ group agreed to leave output unchanged. The decision by the group was well towards the most bullish end of expectations, and Brent Crude (+4.17%) climbed to its highest level in over a year in response, closing at $66.74/bbl. Meanwhile WTI oil prices (+4.16%) reached as an even bigger milestone, as they rose above their early-2020 peak to levels not seen since April 2019. Readers of our performance review will know that oil has been the best performing asset in our sample on a YTD basis thanks to tight supplies and a strong recovery in global economic demand, and this latest move leaves Brent and WTI up +28.8% and +31.6% since the start of the year respectively.

Given the moves in oil prices, it was no surprise that energy stocks outperformed on both sides of the Atlantic, with both Europe’s STOXX Oil & Gas index (+1.75%) and the S&P 500 Energy index (+2.47%) advancing to post-pandemic highs. Ahead of Powell’s remarks in Europe, sovereign bonds rallied yesterday, with yields on bunds (-2.3bps), OATs (-2.8bps) and BTPs (-3.2bps) all moving lower. Equities had a worse performance though, with the STOXX 600 (-0.37%) losing ground for the first time this week.

Overnight in Asia, markets are continuing to trade lower with the Nikkei (-0.99%), Hang Seng (-0.42%), Shanghai Comp (-0.56%) and Kospi (-0.59%) all down but off the lows for the session. Sentiment is likely getting weighed down a bit by news that China has set a conservative growth target of more than 6% for 2021. This signals that China will have more restrained monetary and fiscal policies this year. The growth target also comes short of expectations from our China chief economist, Yi Xiong, of 7-7.5% for 2021. In addition the Chinese government has also said that it will narrow the budget deficit to 3.2% in FY 2021 from 3.6% in 2020. The announcements came from the National People’s Congress in China which began today. To listen to expectations of the importance of this event hear our chief China economist’s podcast preview here.

Back to markets and futures on the S&P 500 (-0.27%) are pointing to another negative open today. Looking at yields, those on Australia (+6.1bps) and New Zealand’s (+7.5bps) 10 year sovereign bonds are up while those on 10yr JGBs are down -4bps after the BoJ Governor Kuroda said that a widening of the movement range around the Bank of Japan’s 10-year yield target is off the table for a policy review later this month. Yields on 10yr USTs are flattish.

Looking ahead, one of the main highlights today will be the US jobs report for February, which is also the first jobs report to entirely cover the Biden administration’s time in office. Recent months have seen a weakening in the pace of the labour market recovery, with the 3-month average change in nonfarm payrolls standing at just +29k, the slowest since the height of the pandemic last year. However, our US economists are forecasting a more positive picture for February, with growth of +200k in nonfarm payrolls, and a reduction in the unemployment rate to 6.2%. That said, as Fed officials have pointed out on numerous occasions, the unemployment rate underestimates broader slack in the labour market due to misclassification and people leaving the labour force altogether, so it’s worth keeping an eye on broader measures too like the U-6 unemployment rate, which at 11.1% last month is still more than 4pp above its pre-pandemic levels. Ahead of the jobs report, yesterday saw the initial jobless claims for the week through February 27 come in roughly as expected at 745k (vs. 750k expected), albeit this was a slight increase from the previous week’s revised 736k number. Furthermore, the continuing claims for the week through February 20 fell to a post-pandemic low of 4.295m (vs. 4.3m expected).

Turning to the pandemic, yesterday we found out that Italy had blocked a shipment of AstraZeneca vaccines to Australia, which would have included 250,000 doses. This follows the row between the EU and the company earlier in the year when AZ was criticised by the EU for not meeting their vaccine commitments. At the same time, yesterday also saw Germany recommend the AZ vaccine for use in adults aged 65 and over, having previously restricted it to those younger than that. In other news, Hungary increased their restrictions, including the closure of primary schools for a month until April 7 and most shops from March 8 to 22. However in better news, the 7-day average of cases here in the UK fell beneath 7,000 for the first time since October 2. Elsewhere France tightened restrictions and sped up the vaccine distribution to specific hard hit regions. The government is still trying to avoid a third national lockdown but the Pas-de-Calais region on the northern coast will be put under a weekend lockdown, with more measures to come if needed. Meanwhile, we have seen confirmation in Japan overnight that the government has recommended that the state of emergency for the Tokyo region be extended by two weeks beyond March 7.

Looking at yesterday’s economic data, the Euro Area unemployment rate remained at 8.1% in January (vs. 8.3% expected), though the same month’s retail sales fell by a much sharper-than-expected -5.9% (vs. -1.4% expected) as the pandemic restrictions took their toll. Meanwhile in the US, factory orders in January were up +2.6% (vs. +2.1% expected).

To the day ahead now, and the main highlight will likely be the aforementioned US jobs report for February, but other releases include German factory orders and Italian retail sales for January. Central bank speakers include the Fed’s Bostic and the BoE’s Haskel.

Tyler Durden

Fri, 03/05/2021 – 07:47

via ZeroHedge News https://ift.tt/3sWQ0tn Tyler Durden