Authored by Charles Hugh Smith via OfTwoMinds blog,

Ironically, their ample compensation allows them to avoid the poor-quality services they’ve designed for everyone below them.

If we define middle class by the security of household income and what that income can buy rather than by an income level, what do we conclude? We have little choice but to conclude the middle class is decaying, both in the percentage of the workforce that qualifies as “middle class” according to traditional standards and in the quality of life of those who do qualify.

There’s a longstanding way to understand the middle class quality of life: it’s supposed to be superior to the indignities of being poor. If you’ve been poor (and I’ve been down to my last $100), even for short periods, you know the indignities and frictions of being poor (and by poor I don’t mean on welfare, I mean working poor, with unreliable incomes and low wages).

Being middle class meant being able to escape the hassles and indifferent services that await the poor. Fast-forward to today: what day-to-day tasks and interactions are easy and cost-free for the middle class? How many are nightmarish, complicated, frustrating, and costly?

Virtually all of them. Being “middle class” is no longer a buffer to the indignities and friction of a dysfunctional, costly status quo that only serves the wealthy with anything resembling what was once afforded the middle class.

No wonder what remains of the middle class is so anxious to qualify for “elite” airline miles programs and similar “special” service, because it approximates what every middle class person once expected as the norm.

In terms of the quality of life and of services, the bottom 95% is now poor. Can you really contest this, or is contesting a matter of hurt pride?

What qualifies as middle class? I’ve defined it by characteristics rather than income: starting with What Does It Take To Be Middle Class? (December 5, 2013), I’ve used 12 minimum standards of membership that were implicit characteristics of the conventional middle class a generation ago:

1. Meaningful healthcare insurance ($5,000 deductible plans don’t qualify, and neither does government-provided low-income coverage such as Medicaid.)

2. Significant equity (25%-50%) in a home or other real estate

3. Income/expenses that enable the household to save at least 6% of its income

4. Significant retirement funds: 401Ks, IRAs, etc.

5. The ability to service all debt and expenses over the medium-term if one of the primary household wage-earners lose their job

6. Reliable vehicles for each wage-earner

7. If a household requires government assistance to maintain the family lifestyle, their Middle Class status is in doubt.

8. A percentage of non-paper, non-real estate hard assets such as family heirlooms, precious metals, tools, etc. that can be transferred to the next generation, i.e. generational wealth.

9. Ability to invest in offspring (education, extracurricular clubs/training, etc.) without going into debt to pay for the extracurricular activities.

10. Leisure time devoted to the maintenance of physical/spiritual/mental fitness.

11. Continual accumulation of human and social capital (new skills, networks of collaborators, markets for one’s services, etc.)

12. Family ownership of income-producing assets such as savings bonds, etc.

To these core attributes we might add the host of services that are being cut back or eliminated en masse listed in yesterday’s guest post, ‘Workarounds’ Galore: How Real Americans Deal with ‘Real’ Inflation: attending sporting events, regular haircuts, dry-cleaning, membership in service clubs and country clubs, and dozens of other once-standard benefits of middle class life.

The decay of this standard of living is not just quantitative, it’s qualitative. The quality of life available to those with middle class incomes is decaying on two fronts: quantitatively, households can no longer afford services and activities, and what they can afford is of lower quality, both the goods and the services.

I touched on this in The Erosion of Everyday Life, but I only scratched the surface of the accelerating decay of the quality of services available to what remains of the middle class.

Do you get excellent service from automated Corporate America customer service? You must be joking if you answer “yes.”

The point here is the quality has been stripped out of Corporate America’s products and services to maximize quarterly profits. Whatever digital device that lasts more than a few years is obsoleted by some software “upgrade” that forces customers to buy a new device.

The quality of government services has also decayed, often to the point of dysfunction. Try getting a double-billing from a local government agency cleared up. Try getting the potholes on your local street that doubles as a bikeway (so the city can brag it’s bicycle-friendly) filled in less than a few years. And so on.

People in customer service and public service are doing their best, but they’re often hobbled by inefficient work rules, outdated equipment and software (or software that simply doesn’t function properly), poor training, overzealous compliance, staffing shortages, maxed-out managers and other hindrances to quality service.

As for the security of household income–at least one wage earner has to work for the government or a government-funded industry such as education, healthcare or defense to have even minimum security. Private-sector security simply doesn’t exist outside of the quasi-government sectors which are largely or completely funded by government.

Let’s not forget the insecurity of traditional middle class assets such as the family home and pensions. The family home has plenty of equity at the top of the bubble du jour, not so much when the bubble pops. The 401K retirement fund exudes security at the top of the bubble, not so much after it crashes. The pension is only as good as the pension fund and its annual growth rate, both of which are contingent on forces beyond the reach of the pension managers.

Stagnation Nation: Middle Class Wealth Is Locked Up in Housing and Retirement FundsOctober 25, 2017

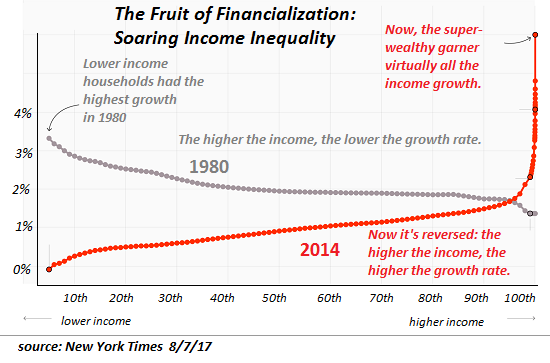

Yes, the super-wealthy have siphoned off most of the gains in income and wealth generated by financialization as shown on this chart. But that’s only part of the picture, as that only impacts income and capital–it doesn’t measure the decay of purchasing power and the quality of life available to everyone below the top of the wealth-power pyramid.

Many of the most richly compensated people in our economy are those who figure out ways to eliminate costs by degrading quality and service. Ironically, their ample compensation allows them to avoid the poor-quality services they’ve designed for everyone below them.

Of related interest:

Honey, I Shrunk the Middle Class: Perhaps 1/3 of Households Qualify December 28, 2015

What Does It take to Be Upper Middle Class? June 22, 2016

What’s Eroding the Middle Class? January 2016

What Killed the Middle Class? March 24, 2016

* * *

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

via ZeroHedge News http://bit.ly/2DEZBOf Tyler Durden