California County To Remove COVID-19 Patients From Homes Based On ‘Living Situation’ — Will Place In ‘Other Kinds Of Housing’

Officials in Ventura County, California will be expanding coronavirus testing, tracking the infectedand those who they’ve been in contact with, and moving people out of their homes and into specialized housing for COVID-19 patients.

Discussing the need to hire contact tracers and manage active cases, Ventura County Public Health Director Dr. Robert Levin said during a May 4 press conference that people who live in homes where they could expose family members to COVID-19 would be moved into ‘other kinds of housing’ provided by the county.

“We also realize that as we find more contacts, some of the people we find are going to have trouble being isolated,” said Levin. “For instance, if they live in a home where there is only one bathroom and there are three or four other people living there, and those people don’t have COVID infection, we’re not going to be able to keep the person in that home.

Every person who we’re isolating, for instance, needs to have their own bathroom. And so we’ll be moving people like this into other kinds of housing that we have available.”

Watch:

The county walked back Levin’s comments on Facebook, responding that they “are not going to remove anyone from their home,” but that “If someone cannot isolate at their home because of their living situation we have alternative options available.”

Another Facebook user responded, “they can try — they will have a fight on their hands.“

Ventura county has had 595 COVID-19 cases, of which 416 have recovered, 22 are hospitalized, 11 of which are in the ICU, and 19 have died. Most cases are in those aged 45-64, while no data was provided on average age of death.

The Poseidon has been described as a “nuclear torpedo”, which is true in at least one sense, namely its propulsion. The Poseidon is, by all accounts, powered by a nuclear reactor which makes it a submersible equivalent of the Burevestnik nuclear-powered cruise missile, with an effectively global range. It is for all intents and purposes an unmanned miniature nuclear-powered submarine, with all the benefits that nuclear propulsion bestows on a submarine. The absence of a crew eliminates the need for heavy shielding and allows speeds considerably in excess of even the fastest submarines.

Its top speed is estimated at between 60 and 100 knots, with the upper end of the scale being comfortably in excess of all torpedoes except for the short-ranged, supercavitating rocket-propelled Shkval. And while conventional torpedoes can develop high speeds only at the expense of range, due to the limited propellant or battery charge, nuclear propulsion means high speeds can be sustained for longer periods of time, subject only to the design’s mechanical limitations.

Virtually all descriptions of the Poseidon describe it as a nuclear delivery vehicle, for use primarily against coastal targets such as cities and naval bases, and possibly also against mobile naval high-value targets such as aircraft carrier battlegroups. However, this application is too limited in usefulness to warrant the development of a costly system like the Poseidon and specialized submarines designed to carry it. Even an extremely powerful thermonuclear warhead would have to be brought quite close to the target in order for the underwater explosion to cause significant damage to the coastal site. In many cases, the high-value target may be considerably inland, like Washington, D.C., or shielded by natural coastal features, like New York City. In order to strike them, the large and heavy Poseidon would have to maneuver at slow speed in shallow coastal waters where it would be vulnerable to underwater defenses that would be surely developed to cope with it.

This points to the likelihood of the nuclear delivery mission being one, and possibly not even the most important, of missions that it will be called upon to carry out. A Poseidon diagram shown on Russian TV pointedly referred to it as a “multi-purpose oceanic system”, which rather strongly suggests that it is not only, or even primarily, a nuclear delivery system. Cruise and ballistic missiles, even with conventional and nuclear payloads, are not referred to as “multi-purpose systems”, either. Likewise the Burevestnik nuclear-powered cruise missile is also not referred to as a “multi-purpose” system.

In keeping with the general pattern of unmanned combat system development in Russia, which increasingly seeks to pair unmanned systems with manned ones to fully exploit the strengths and cover the weaknesses of each, it is entirely possible that Poseidon is intended to function not as an underwater Burevestnik, but rather as the equivalent of the stealthy Okhotnik combat drone developed as a “wingman” vehicle for the Su-57 fifth-generation fighter.

The peculiar qualities of deep ocean as a theater of war, particularly its opacity to sensors and limits on weapon speed mean that a combat underwater unmanned vehicle (UUV) would be of even greater use to a manned submarine than a combat crone accompanying a stealth fighter. But the support function would be essentially the same. The unmanned platform could enhance the lethality and survivability of the manned one by serving as a platform for sensors, weapons, and in extreme conditions even as a decoy.

The size of the Poseidon, specifically the 1.6m diameter and the length of 24m, suggest considerable internal volume suitable for a variety of configurable payloads, though it is unlikely these payloads could be changed once the Poseidon was loaded onto its carrier submarine. In addition to the already mentioned nuclear warheads, these payloads could include sensors, including sonar arrays, and even anti-submarine torpedoes. An early artist’s impression of the Poseidon actually depicted an underwater vehicle akin to a miniature submarine, complete with an array of torpedo tubes.

That the Poseidon has a broader range of intended capabilities than simply acting as a nuclear delivery vehicle is also suggested by the submarines being built to act as carriers for these torpedoes. There are currently two boats under construction that are intended for this role, the K-329 Belgorod, and the Khabarovsk.

The Belgorod, in particular, is interesting as a Poseidon launch platform because it is not a boat intended mainly for the “kinetic” combat role. Rather, this heavily modified Project 949A cruise missile submarine design is intended to act as a mother ship for the highly classified Losharik deep-diving research submarine, Shelf energo-capsules for the Harmoniya underwater sensor system network, and the Klavesin UUVs. While the diagrams crafted by the respected British undersea warfare analyst H I Sutton have the Belgorod carry Poseidons in forward-mounted horizontal torpedo tubes, the fact that the Belgorod is already extensively fitted for the external docking and internal recovery of manned and unmanned undersea vehicles could also mean that the Poseidon will be launched and recovered from launch bays. The original Project 949A design reserved extensive volume for a battery of 24 Granit anti-ship cruise missiles, whose launch tubes were arrayed on both sides of the hull in banks of 12. But if Sutton’s assessment of the Belgorod as being narrower than Project 949A, with a circular hull cross-section, then the Poseidon could still be carried in payload bays from which it could swim out and be recovered into.

Sutton’s analysis of photographs from the launch of the Belgorod led him to believe the boat is fitted with thrusters for precise undersea maneuvers, which would be required if the boat is to recover undersea vehicles. However, even if the Poseidon is carried in launch tubes and is not recoverable by the carrier submarine, the choice of Belgorod, a dedicated special-missions submarine, would be odd if Poseidon were intended only as a nuclear delivery vehicle.

Even less is known of the Khabarovsk, which is a purpose-designed boat whose main weapon system is supposed to be the Poseidon. Again, Sutton assumes that Poseidon torpedoes would be carried in torpedo tubes in the front of the hull, but the size of the Khabarovsk, a boat of estimated 10,000 ton displacement and 120m length, or only 40m shorter than the Borei SSBN, means there is ample volume for a swim-out launch and recovery bay. It is not yet clear what place Khabarovsk occupies in the Russian vision of undersea warfare. Perhaps it is intended as a mothership for an array of Poseidons with various payloads, to support operations of other submarines, including as escorts for ballistic missile submarines. It is also possible it is a prototype of a future class of attack submarines that will carry one or more Poseidons with conventional weapon and sensor payloads as a standard fit.

Being a world leader in nuclear technology, it is not surprising to see Russia leverage this advantage by creating novel aerial and naval platforms such as the Burevestnik and Poseidon. The coming years will no doubt provide additional information on their actual capabilities. It is already evident that Russia is not lagging behind in the development of novel applications for unmanned platforms.

‘We Have To Adjust To New Reality’ – Pandemic Leads To Surge In Americans Drinking At Home

Alcohol sales for home consumption jumped $2 billion more since the start of March than last year, while a top beer producer said the increase in sales at home would not offset lost ones seen at restaurants and bars.

A little more than half a month into lockdowns, around the first week of April, we mentioned how Americans were turning to beer, porn, pot, and chocolate, to cope with coronavirus pandemic stress. The Financial Times has now published alcohol sales data that shows drinking at home soared during lockdowns.

Data analytics firm IRI reported that by mid-April, retailers’ total alcohol sales hit $9 billion over the seven weeks. Sales of spirits increased, including tequila and gin surged 39% to $1.3 billion, and wine rose 28% to $2 billion. Beer also soared 20% to $5.5 billion.

Gavin Hattersley, CEO of Molson Coors, in an earnings call last week, spoke about the “challenging” environment for producers as supply chains disruptions are materializing:

“But obviously, there is no doubt that this is really a challenging time for us, not just for our business, but for everybody in our industry. And our focus, as I said, right now is mitigating the short-term business challenges and positioning our business to succeed in the long-term,” Hattersley said.

“From a sales to wholesalers point of view, the impact of the Milwaukee brewery tragedy as Tracey I think said was from a shipments point of view in February and early March and because of that our inventory levels at the end of March were lower than we would have liked.”

While drinking in quarantine did not offset the collapse in sales from restaurants and bars, Molson Coors reported net sales fell 8.7% in 1Q20 YoY.

The chief economist of the National Beer Wholesalers Association Lester Jones said: “I’m confident there will be plenty of beer, although I don’t know if it’s going to be in the right packages and the right formats that people expect.”

What Jones is describing is exactly what is happening to farmers at the moment. Since restaurants, hotels, resorts, cruise ships, cafeterias, etc., have shuttered operations during lockdowns, these establishments usually order bulk food – and for farmers to rework supply chains from bulk to individual packaging, well that takes time and money. Hence, this is one reason why food supply chains have become disrupted across the country.

Jones added: “Given that we all planned months ago to have a very different market, we have to quickly adjust to the new reality.”

Anheuser-Busch InBev is expected to share new data later this week on drinking habits during the pandemic.

To sum up, the pandemic is changing the way America drinks, lives, and how the economy functions. It has also allowed for people to save money in greater amounts as they have never done before. We noted last week the personal savings rate has exploded to decade highs.

It only took a pandemic for Americans to figure out that drinking at home is much cheaper than going out (which allows them to save money) because what’s ahead is an economic downturn that could last years.

Beijing May Dump US Treasuries In Response To US Hostility, Start Its Own QE: Chinese Media

In response to recent media speculation that as the blame game over the origins of the coronavirus pandemic escalates the US may cancel some of its $1.1 trillion debt owed to China, the South China Morning Post reported today that China may “move to reduce its vast holdings of US Treasury securities in the coming months” in response to a resurgence in trade tensions and a war of words between the world’s two largest economies.

While analysts have also said that the US was highly unlikely to take the “nuclear option” of cancelling Chinese-held debt, with Larry Kudlow himself refuting this suggestion on several occasions last week, the “mere fact that the idea has been discussed could well prompt Beijing to seek to insulate itself from the risk by reducing its US government debt holdings”, the SCMP writes.

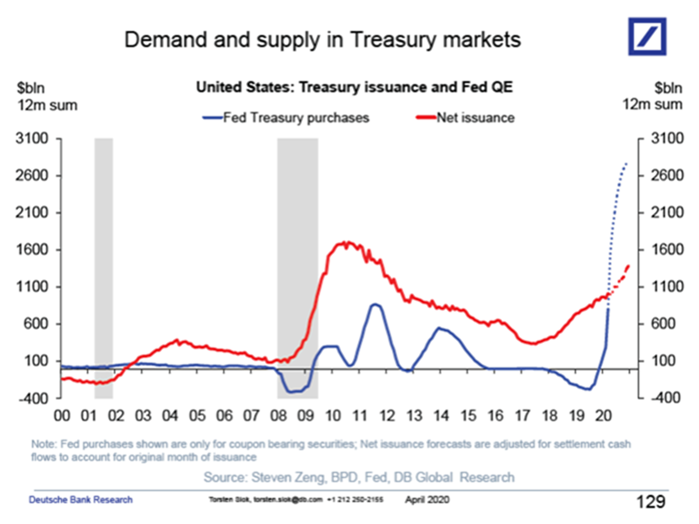

And while the SCMP then suggests that this “could spell trouble for the US government bond market at a time when Washington is significantly ramping up new issuance to pay for a series of programs to combat the pandemic and the economic damage it is causing”, nothing could be further from the truth: yes, the US Treasury will issue over $4 trillion in new debt this calendar year, but now that the US officially lives under central planning, courtesy of helicopter money, the Fed will monetize not just every dollar the Treasury issues, but will monetize double the net issuance.

Which means that not only does the US not need China to buy its debt ever again, the US in fact does not need anyone outside the Fed, now that open debt and deficit monetization is the endgame, with the only unknown is when this will lead to currency collapse.

Surprisingly, the Chinese still don’t get that any tactical advantage they may have had is now gone:

any move to cancel the debt owed to China – effectively defaulting on it – would be counterproductive to US interests because it would likely destroy investors’ faith in the trustworthiness of the US government to pay its bills, analysts warned.

This would send US interest rates soaring, making borrowing more costly for the government, as well US companies and consumers, and in turn strike a sharp blow to America’s already very weak economy.

Again: no. Maybe this idea had some validity when the Fed was pretending it wouldn’t do unlimited QE, but now that the Fed is purchasing hundreds of billions in US paper every month, what China may or may not do with its holdings of US debt is completely irrelevant.

“It’s such a crazy idea that anyone who has made it should really have their fitness for office reconsidered,” said Cliff Tan, East Asian head of global markets research at MUFG Bank. “We view this as largely a political ploy for [Donald Trump’s] re-election and a cynical one because it would destroy the financing of the US federal budget deficit.”

Uhm, Cliff, yes it is insane, but not because China has any leverage left: in case you missed it, the Fed purchased $2.5 trillion in debt in the past 6 weeks.

That’s more than double what China owns. So yes, if Beijing wants to dump its Treasuries, bring it on: it will cause yields to spike for an hour or two, at which point everyone will frontrun the Fed which will activate the turbo POMO and purchase every last penny that China had to sell.

China’s desperate fearmongering – as if it tries to convince itself that it has some leverage over the US continued:

China could trigger a crash in the US dollar and financial markets by flooding the market with US Treasuries for sale, which would push down US bond prices and cause yields to spike. But that would also ignite a global financial catastrophe, hurting China as well.

Two things: the financial catastrophe was already ignited when China allowed – accidentally or on purpose – a deadly pandemic escape from the Wuhan Institute of Virology. It doesn’t need the US. Second: a sale of a mere $1.1 trillion in Treasurys now that the total US debt just surpassed $25 trillion…

… of which the Fed owns $6.66 trillion, would have absolutely no impact on anything, besides long-end yields, and even there the spike would be brief as the market realizes that the Fed can and will buy everything China has to sell.

Oh, and a third thing: if China could actually crash the US dollar, both Powell and Trump would be giddy with happiness. In case someone still hasn’t figured it out, the Fed is desperate to crash the dollar because the longer it remains elevated (as a result of the infamous $12 trillion dollar margin call), the more likely it is that the coming global emerging markets collapse will crush the US as not even the Fed will have power to deflect that particular meteor.

Alas, none of this has registered with China which is dearly holding on to the myth that its sales of US paper could still have some impact:

“There’s a strong urge for countries like China, and Russia, to move away from US dollar settlements. This is simply because the US dollar can be weaponised by the US government,” said Xu Sitao, chief economist at Deloitte China, referring to the recent practise by the US government of cutting off foreign individuals, companies and governments from the global US dollar financial transaction settlement system, greatly complicating their ability to conduct business.

“ Clearly there’s more willingness for certain countries just to diversify and move away from US dollar settlements.”

Right, sure, and just what currency does China propose to exchange its dollar-denominated reserves, which account for some 58% of its total FX holdings, into?

Maybe China is just confused because it has yet to activate a full-blown QE of the type the Fed has perfected for the past decade. Which is apropos because in a follow up article, the same SCMP reports that China’s top economic policymakers have been “engaged in heated debate over whether the country’s central bank should directly buy special bonds issued by the finance ministry to help the government’s economic support measures.”

Which, of course, is preciely what the Fed has been doing on tilt for the past two months.

According to the report, the discord reflects the differing schools of thought in China over how best to help the world’s second largest economy recover from the coronavirus. The National People’s Congress which is due to meet in less than three weeks, is expected to provide clearer signals on Beijing’s economic policy. Liu Shangxi, president of the Chinese Academy of Fiscal Sciences, a finance ministry-affiliated think tank, kicked off the debate after he recently proposed issuing 5 trillion yuan (US$700.5 billion) in special Treasury bonds to help stabilise the economy

He called on the People’s Bank of China (PBOC) to buy them in tranches at an interest rate of zero.

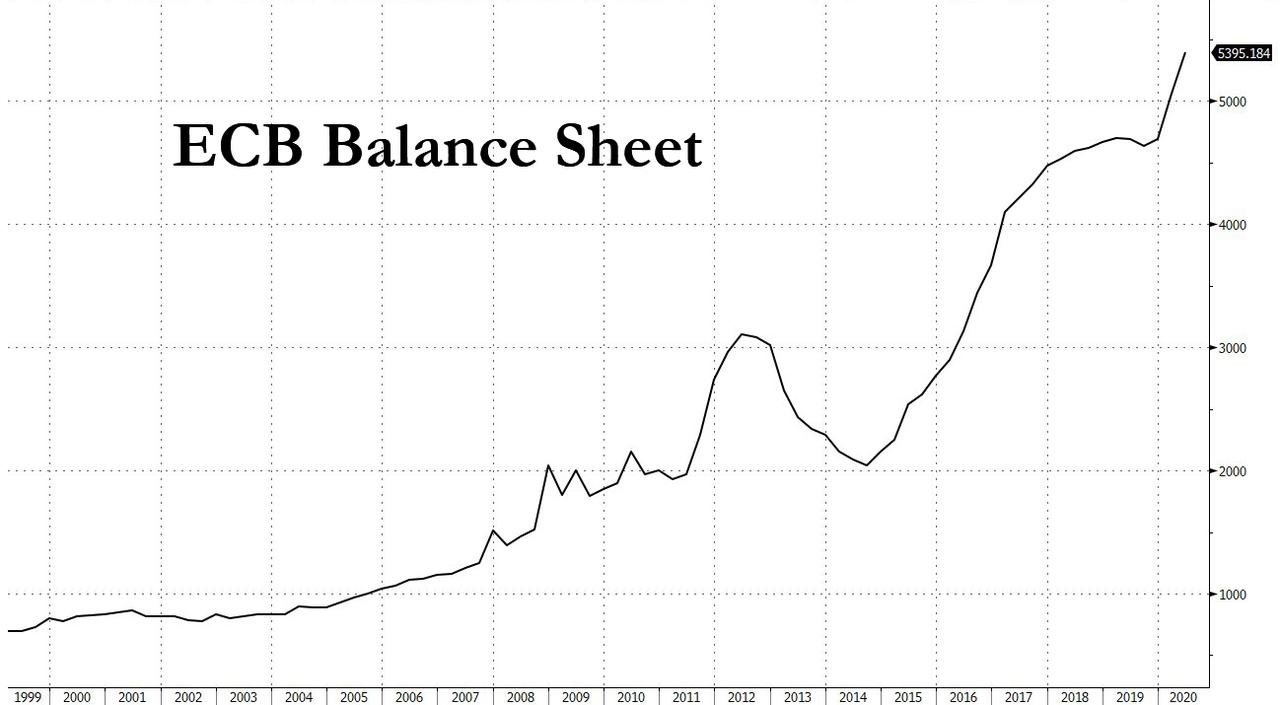

It gets funnier: in China purchases of bonds are technically taboo as central bank law forbids it from directly bankrolling government spending. Well, guess what: there is another central bank whose charter forbids it from engaging in state financing and debt/deficit monetization: the ECB. And here is its balance sheet.

And while for now China is stopped by the threat of soaring inflation once it too triggers monetary financing, it is only a matter of time before China realizes that the initial phase of the coming hyperinflation only affects asset prices, while sparking broader economic deflation (of course, eventually goes vertical as faith in the currency is extinguished). So once China realizes that by starting QE, it too can achieve all of its goals, it will do precisely that.

Which also gives us a glimpse of the endgame: the four biggest economies in the world: the US, Europe, China and Japan, all directly monetizing their own debt, all hoping to crush their own currency before their peers as the only remaining way to stimulate the global economy. Then one day, something will finally snap and the entire financial system will disintegrate overnight. Until them, however, just BTFD because when every central bank in the world is telling you that fiat paper in your hand will soon be worthless so best spend it now, well, you listen.

When some people become infected with the coronavirus, they only develop mild or undetectable cases of COVID-19. Others suffer severe symptoms, fighting to breathe on a ventilator for weeks, if they survive at all.

Could genetic differences explain the differences we see in symptoms and severity of COVID-19?

To test this, we used computer models to analyze known genetic variation within the human immune system. The results of our modeling suggest that there are in fact differences in people’s DNA that could influence their ability to respond to a SARS-CoV-2 infection.

What We Did

When a virus infects human cells, the body reacts by turning on what are essentially anti-virus alarm systems. These alarms identify viral invaders and tell the immune system to send cytotoxic T cells – a type of white blood cell – to destroy the infected cells and hopefully slow the infection.

To test whether different alleles of this alarm system could explain some of the range in immune responses to SARS-CoV-2, we first retrieved a list of all the proteins that make up the coronavirus from an online database.

We then took that list and used existing computer algorithms to predict how well different versions of the anti-viral alarm system detected these coronavirus proteins.

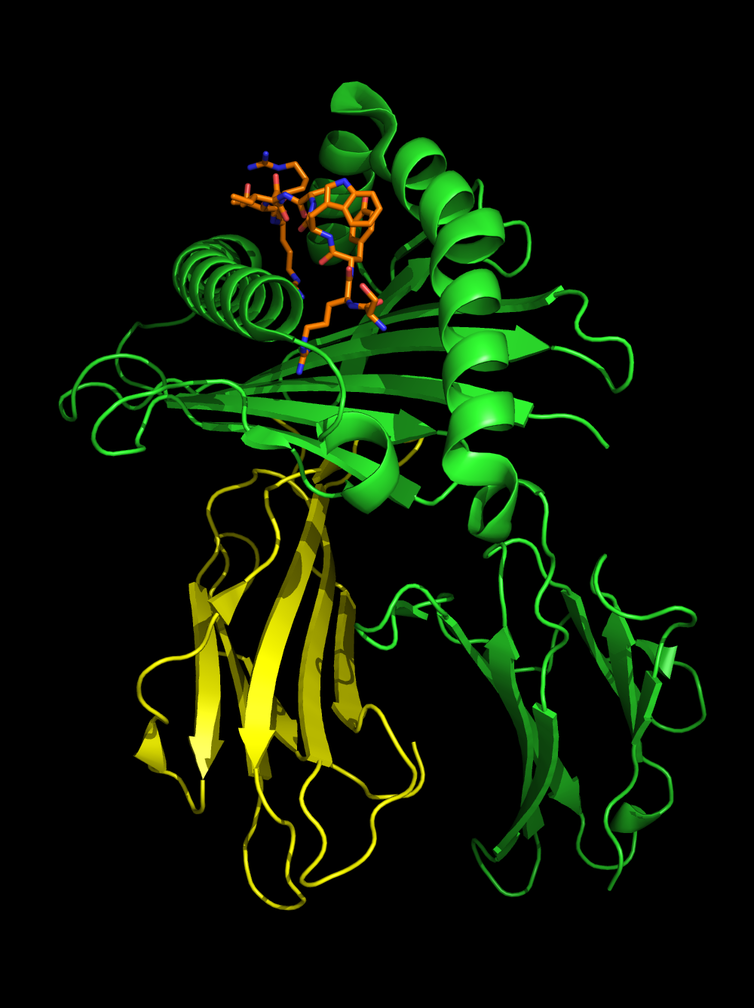

A model of an HLA protein (green and yellow) bound to a piece of a virus (orange and blue) – in this case, influenza. Prot reimage via Wikimedia Commons, CC BY-SA

Why It Matters

The part of the alarm system that we tested is called the human leukocyte antigen system, or HLA. Each person has multiple alleles of the genes that make up their HLA type. Each allele codes for a different HLA protein. These proteins are the sensors of the alarm system and find intruders by binding to various peptides – chains of amino acids that make up parts of the coronavirus – that are foreign to the body.

Once an HLA protein binds to a virus or piece of a virus, it transports the intruder to the cell surface. This “marks” the cell as infected and from there the immune system will kill the cell.

In general, the more peptides of a virus that a person’s HLAs can detect, the stronger the immune response. Think of it like a more sensitive sensor of the alarm system.

The results of our modeling predict that some HLA types bind to a large number of the SARS-CoV-2 peptides while others bind to very few. That is to say, some sensors may be better tailored to SARS-CoV-2 than others. If true, the specific HLA alleles a person has would likely be a factor in how effective their immune response is to COVID-19.

Because our study only used a computer model to make these predictions, we decided to test the results using clinical information from the 2002-2004 SARS outbreak.

We found similarities in how effective alleles were at identifying SARS and SARS-CoV-2. If an HLA allele appeared to be bad at recognizing SARS-CoV-2, it was also bad at recognizing SARS. Our analysis predicted that one allele, called B46:01, is particularly bad with regards to both SARS-CoV-2 and SARS-CoV. Sure enough, previous studies showed that people with this allele tended to have more severe SARS infections and higher viral loads than people with other versions of the HLA gene.

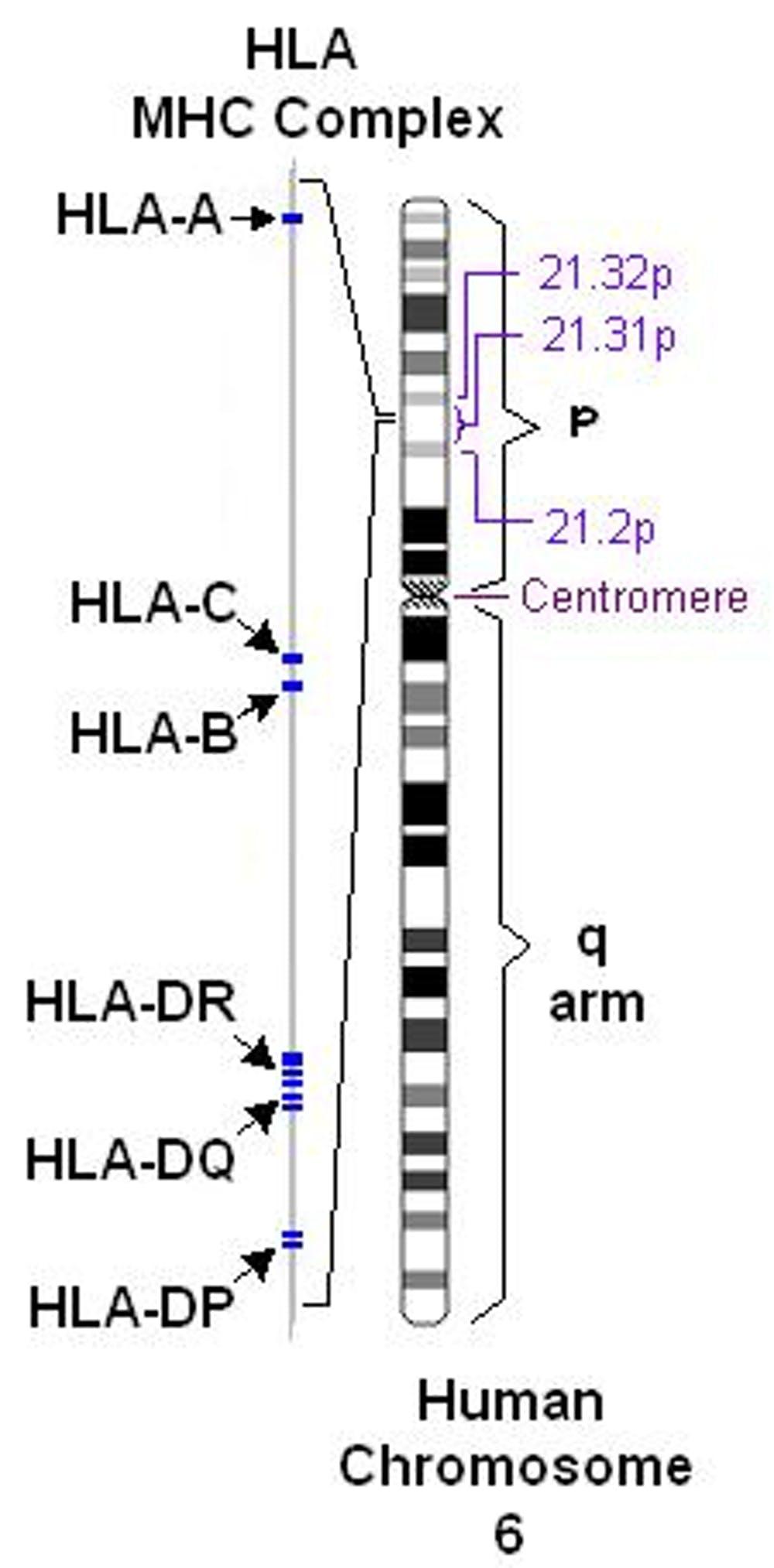

The section of DNA that codes for HLAs is on the sixth chromosome. Pdeitiker at English Wikipedia / Wikipedia, CC BY

What’s Next?

Based on our study, we think variation in HLA genes is part of the explanation for the huge differences in infection severity in many COVID-19 patients. These differences in the HLA genes are probably not the only genetic factor that affects severity of COVID-19, but they may be a significant piece of the puzzle. It is important to further study how HLA types can clinically affect COVID-19 severity and to test these predictions using real cases. Understanding how variation in HLA types may affect the clinical course of COVID-19 could help identify individuals at higher risk from the disease.

To the best of our knowledge, this is the first study to evaluate the relationship between viral proteins across a wide range of HLA alleles. Currently, we know very little about the relationship between many other viruses and HLA type. In theory, we could repeat this analysis to better understand the genetic risks of many viruses that currently or could potentially infect humans.

Putin’s Approval Rating Hits Historic Low As 3 Cabinet Members Infected

Over the past decade, poll after poll in Russia has found President Vladimir Putin to be by far the most popular leader in modern Russia’s relatively short history (since the collapse of the USSR). He’s also of course been the longest ruling, currently serving his fourth 6-year presidential term.

His popularity at home is commonly attributed to the general Russian public’s desire for continued stability and the weeding out of oligarchic control and corruption in society. However, like in other parts of the world, Russia’s ‘stability’ is now under threat by the explosive spread of coronavirus — now witnessing consecutive daily record rises in cases.

Via AP

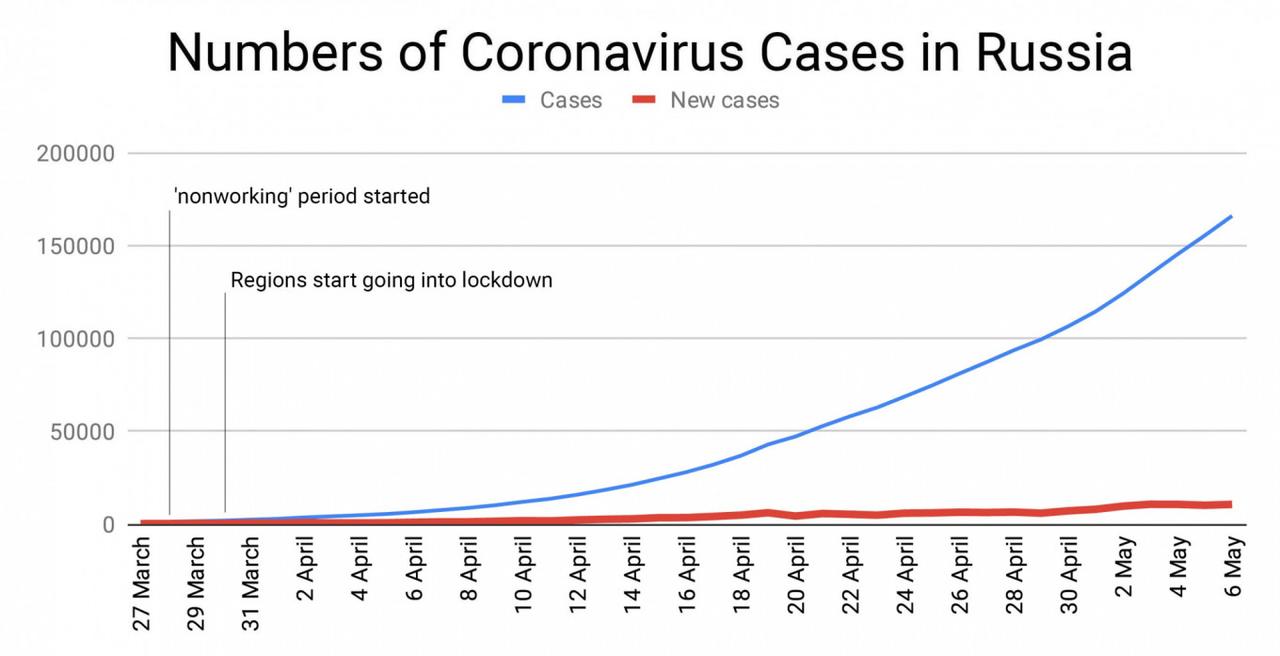

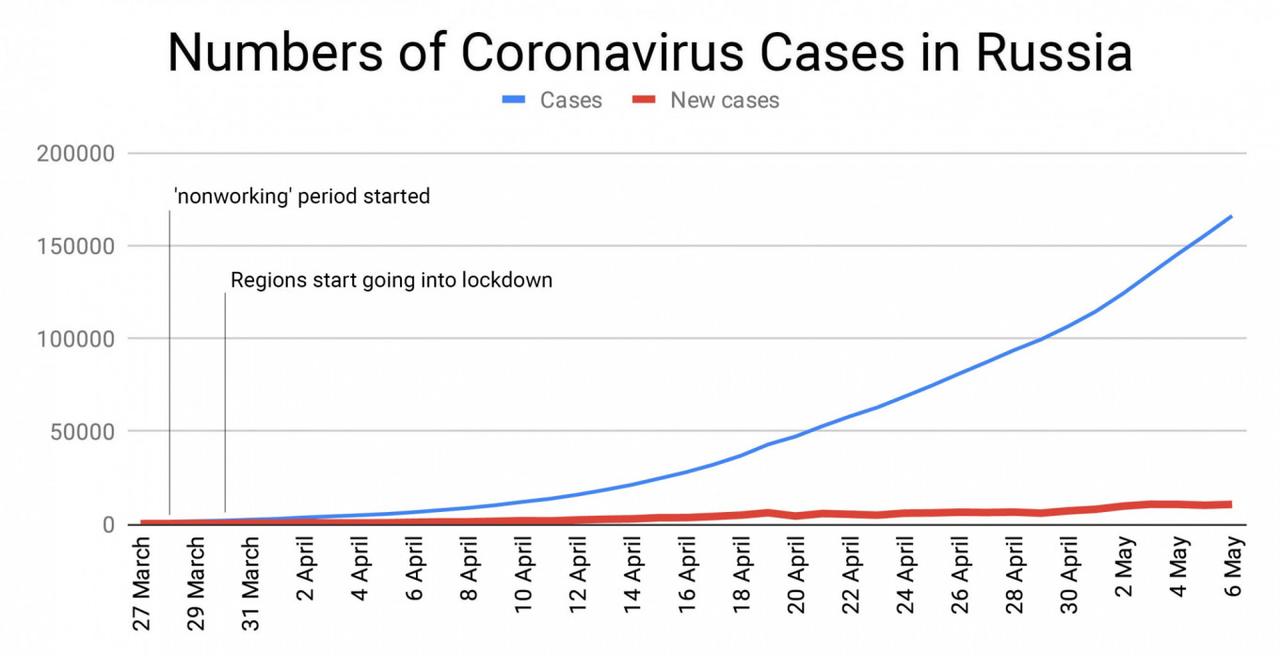

On Wednesday Russian health officials announced a whopping 10,559 new confirmed COVID-19 infections, bringing the national total to 165,929cases, including 1,537 deaths. This makes Russia the seventh most infected country, days ago surpassing Iran and China.

Following widespread criticism that Russia was slow in locking down the country, doing so at the very end of March significantly after European countries and the United States, a new poll from the Russian independent, non-governmental polling agency Levada Center finds that Putin’s popularity has plunged to a historic low.

This also amid fears not enough was done to insulate the economy amid a national lockdown and work “pause”.

President Vladimir Putin’s’s approval rating has hit a historic low of 59% as the country grapples with the coronavirus crisis, the independent Levada Center polling agency said Wednesday.

According to Levada’s results from a phone interview in late April, when most of the country was under enforced lockdown measures, 33% disapproved of Putin’s work.

Putin’s previous lowest approval rating since he first became president, 61%, was recorded in June 2000 and November 2013.

The latest results mark Putin’s lowest approval rating recorded by the Levada Center since September 1999, when he had a 53% approval rating shortly after being appointed prime minister.

The Kremlin downplayed the new Levada poll results, pointing to other research indicators which don’t paint as drastic a picture.

Russia’s culture minister, Olga Lyubimova, file image.

Meanwhile, things are looking to get worse, given days ago Russian Prime Minister Mikhail Mishustin announced he was confirmed for coronavirus.

And as of Wednesday a third cabinet minister has become infected (after also the Construction minister tested positive): Russia’s culture minister, Olga Lyubimova, has tested positive for the coronavirus, according to Reuters, citing state sources.

This Is What New Normal Looks Like After The Pandemic

Authored by Bloomberg macro commentator Ye Xie

The biggest market news Wednesday was the steepening of the Treasury yield curve as the government boosted planned sales of long-term debt to fund a $4 trillion deficit this year.

With short-term rates possibly staying near zero for the next few years, curve steepening seems to be a natural response to more debt sales. Still, it’s hard to see how much yields can back up when the Fed is gorging on debt. Bond vigilantes are nowhere to be seen, at least for the time being.

In the stock market, the Nasdaq Composite Index outperformed the S&P 500 again. It’s more evidence that the pandemic has accelerated the pre-existing trend: lower rates for longer and the secular rise of tech companies.

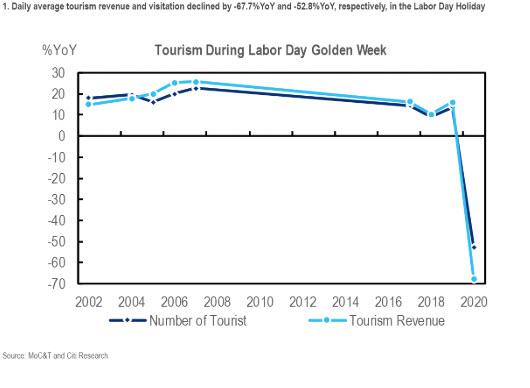

For those who are looking forward to the re-opening of economies, the past Golden Week holiday in China offered a sneak peek of reality: consumer spending remains sluggish, two months after the country cut its daily new confirmed virus cases to below 100.

During the five-day holiday, tourism revenue shrank 68% compared with last year. Among those operating restaurants, daily average revenues fell 46% below the levels at the beginning of the year, according to Nomura, citing a report from a catering industry information provider.

One silver lining is that e-commerce has flourished at the expense of brick-and-mortar shops. Sales of mobile phones, laptops and tablets at Tmall, one of China’s largest online shopping platforms, surged by 70%, 100% and 250% year-on-year, respectively, according to Nomura.

Debt, Digital and De-globalization. Welcome to the post-pandemic world.

Longtime correspondent Paul B. suggested I re-publish three essays that have renewed relevance. This is the first essay, from June 2008. Thank you, Paul, for the suggestion.

I’m not trying to be difficult, but I can’t help cutting against the grain on topics like surviving the coming bad times when my experience runs counter to the standard received wisdom.

A common thread within most discussions of surviving bad times–especially really bad times–runs more or less like this: stockpile a bunch of canned/dried food and other valuable accoutrements of civilized life (generators, tools, canned goods, firearms, etc.) in a remote area far from urban centers, and then wait out the bad times, all the while protecting your stash with an array of weaponry and technology (night vision binocs, etc.)

Now while I respect and admire the goal, I must respectfully disagree with just about every assumption behind this strategy.

Once again, this isn’t because I enjoy being ornery (please don’t check on that with my wife) but because everything in this strategy runs counter to my own experience in rural, remote settings.

You see, when I was a young teen my family lived in the mountains. To the urban sophisticates who came up as tourists, we were “hicks” (or worse), and to us they were “flatlanders” (derisive snort).

Now the first thing you have to realize is that we know the flatlanders, but they don’t know us.

They come up to their cabin, and since we live here year round, we soon recognize their vehicles and know about how often they come up, what they look like, if they own a boat, how many in their family, and just about everything else which can be learned by simple observation.

The second thing you have to consider is that after school and chores (remember there are lots of kids who are too young to have a legal job, and many older teens with no jobs, which are scarce), boys and girls have a lot of time on their hands.

We’re not taking piano lessons and all that urban busywork. And while there are plenty of pudgy kids spending all afternoon or summer in front of the TV or videogame console, not every kid is like that.

So we’re out riding around. On a scooter or motorcycle if we have one, (and if there’s gasoline, of course), but if not then on bicycles, or we’re hoofing it. Since we have time, and we’re wandering all over this valley or mountain or plain, one way or another, then somebody will spot that trail of dust rising behind your pickup when you go to your remote hideaway. Or we’ll run across the new road or driveway you cut, and wander up to see what’s going on. Not when you’re around, of course, but after you’ve gone back down to wherever you live. There’s plenty of time; since you picked a remote spot, nobody’s around.

Your hideaway isn’t remote to us; this is our valley, mountain, desert, etc., all 20 miles of it, or what have you. We’ve hiked around all the peaks, because there’s no reason not to and we have a lot of energy. Fences and gates are no big deal, (if you triple-padlock your gate, then we’ll just climb over it) and any dirt road, no matter how rough, is just an open invitation to see what’s up there. Remember, if you can drive to your hideaway, so can we. Even a small pickup truck can easily drive right through most gates (don’t ask how, but I can assure you this is true). If nobody’s around, we have all the time in the world to lift up or snip your barbed wire and sneak into your haven. Its remoteness makes it easy for us to poke around and explore without fear of being seen.

What flatlanders think of as remote, we think of as home. If you packed in everything on your back, and there was no road, then you’d have a very small hideaway–more a tent than a cabin. You’d think it was safely hidden, but we’d eventually find it anyway, because we wander all over this area, maybe hunting rabbits, or climbing rocks, or doing a little fishing if there are any creeks or lakes in the area. Or we’d spot the wisp of smoke rising from your fire one crisp morning, or hear your generator, and wonder who’s up there. We don’t need much of a reason to walk miles over rough country, or ride miles on our bikes.

When we were 13, my buddy J.E. and I tied sleeping bags and a few provisions on our bikes–mine was an old 3-speed, his a Schwinn 10-speed–and rode off into the next valley over bone-jarring dirt roads. We didn’t have fancy bikes with shocks, and we certainly didn’t have camp chairs, radios, big ice chests and all the other stuff people think is necessary to go camping; we had some matches, cans of beans and apple sauce and some smashed bread. (It didn’t start out smashed, but the roads were rough. Note: if you ever suffer from constipation, I recommend beans and apple sauce.)

We camped where others had camped before us, not in a campground but just off the road in a pretty little meadow with a ring of fire-blackened rocks and a flat spot among the pine needles. We didn’t have a tent, or air mattress, or any of those luxuries; but we had the smashed bread and the beans, and we made a little fire and ate and then went to sleep under the stars glittering in the dark sky.

There were a few bears in the area, but we weren’t afraid; we didn’t need a gun to feel safe. We weren’t dumb enough to sleep with our food; if some bear wandered by and wanted the smashed bread, he could take it without bothering us. The only animal which could bother us was the human kind, and since few people walk 10 or more miles over rough ground in the heat and dust, then we’d hear their truck or motorbike approaching long before they ever spotted us.

We explored old mines and anything else we spotted, and then we rode home, a long loop over rutted, dusty roads. In summer, we took countless hikes over the mountainous wilderness behind his family cabin.

All of which is to say that the locals will know where your hideaway is because they have lots of time to poke around. Any road, no matter how rough, might as well be lit with neon lights which read, “Come on up and check this out!” If a teen doesn’t spot your road, then somebody will: a county or utility employee out doing his/her job, a hunter, somebody. As I said, the only slim chance you have of being undetected is if you hump every item in your stash on your pack through trailess, roadless wilderness. But if you ever start a fire, or make much noise, then you’re sending a beacon somebody will eventually notice.

The Taoists developed their philosophy during an extended era of turmoil known as the Warring States period of Chinese history. One of their main principles runs something like this: if you’re tall and stout and strong, then you’ll call attention to yourself. And because you’re rigid–that is, what looks like strength at first glance–then when the wind rises, it snaps you right in half.

If you’re thin and ordinary and flexible, like a willow reed, then you’ll bend in the wind, and nobody will notice you. You’ll survive while the “strong” will be broken, either by unwanted attention or by being brittle.

Another thing to ponder is that the human animal is a much better predator than it is an elusive prey. Goats and wild turkeys and other animals have very keen senses of smell and hearing, and it’s tough to get close without them smelling you or hearing you. They’re well camouflaged, and since human sight is selected to detect movement and color, if they stay quite still we have a hard time spotting them.

In comparison, the human is a clumsy prey. It can’t smell or hear very well, and it’s large and not well camouflaged. Plus it’s usually distracted and unaware of its surroundings. It doesn’t take much to kill a human, either; a single-shot rifle and a single round of .22-long is plenty enough.

If the chips are down, and push comes to shove, then what we’re discussing is a sort of war, isn’t it? And if we’re talking about war, then we should think about the principles laid down in The Art Of War by Sun Tzu quite some time ago.

The flatlander protecting his valuable depot is on the defensive, and anyone seeking to take it away (by negotiation, threat or force) is on the offensive. The defense can select the site for proximity to water, clear fields of fire, or what have you, but one or two defenders have numerous disadvantages. Perhaps most importantly, they need to sleep. Secondly, just about anyone who’s plinked cans with a rifle and who’s done a little hunting can sneak up and put away an unwary human. Unless you remain in an underground bunker 24/7, at some point you’ll be vulnerable. And that’s really not much of a life–especially when your food supplies finally run out, which they eventually will. Or you run out of water, or your sewage system overflows, or some other situation requires you to emerge.

So let’s line it all up. Isn’t a flatlander who piles up a high-value stash in a remote area with no neighbors within earshot or line of sight kind of like a big, tall brittle tree? All those chains and locks and barbed-wire fencing and bolted doors just shout out that the flatlander has something valuable inside that cabin/bunker/RV etc.

Now if he doesn’t know any better, then the flatlander reckons his stash is safe. But what he’s not realizing if that we know about his stash and his vehicle and whatever else can be observed. If some locals want that stash, then they’ll wait for the flatlander to leave and then they’ll tow the RV off or break into the cabin, or if it’s small enough, disassemble it and haul it clean off. There’s plenty of time, and nobody’s around. That’s pretty much the ideal setting for leisurely thieving: a high-value stash of goodies in a remote area accessible by road is just about perfect.

Let’s say things have gotten bad, and the flatlander is burrowed into his cabin. Eventually some locals will come up to visit; in a truck if there’s gas, on foot if there isn’t. We won’t be armed; we’re not interested in taking the flatlander’s life or goodies. We just want to know what kind of person he is. So maybe we’ll ask to borrow his generator for a town dance, or tell him about the church food drive, or maybe ask if he’s seen so-and-so around.

Now what’s the flatlander going to do when several unarmed men approach? Gun them down? Once he’s faced with regular unarmed guys, he can’t very well conclude they’re a threat and warn them off. But if he does, then we’ll know he’s just another selfish flatlander. He won’t get any help later when he needs it; or it will be minimal and grudging. He just counted himself out.

Suppose some bad guys hear about the flatlander’s hideaway and stash. All it takes to stalk any prey is patience and observation; and no matter how heavily armed the flatlander is, he’ll become vulnerable at some point to a long-range shot. (Even body armor can’t stop a headshot or a hit to the femoral artery in the thigh.) Maybe he stays indoors for 6 days, or even 60. But at some point the windmill breaks or the dog needs walking or what have you, and he emerges–and then he’s vulnerable. The more visible and stringent the security, the more he’s advertising the high value of his depot.

And of course guarding a high-value stash alone is problematic for the simple reason that humans need to sleep.

So creating a high-value horde in a remote setting is looking like just about the worst possible strategy in the sense that the flatlander has provided a huge incentive to theft/robbery and also provided a setting advantageous to the thief or hunter.

If someone were to ask this “hick” for a less risky survival strategy, I would suggest moving into town and start showing a little generosity rather than a lot of hoarding. If not in town, then on the edge of town, where you can be seen and heard.

I’d suggest attending church, if you’ve a mind to, even if your faith isn’t as strong as others. Or join the Lions Club, Kiwanis or Rotary International, if you can get an invitation. I’d volunteer to help with the pancake breakfast fundraiser, and buy a couple tickets to other fundraisers in town. I’d mow the old lady’s lawn next door for free, and pony up a dollar if the elderly gentleman in line ahead of me at the grocery store finds himself a dollar light on his purchase.

If I had a parcel outside town that was suitable for an orchard or other crop, I’d plant it, and spend plenty of time in the local hardware store and farm supply, asking questions and spreading a little money around the local merchants. I’d invite my neighbors into my little plain house so they could see I don’t own diddly-squat except some second-hand furniture and an old TV. And I’d leave my door open so anyone could see for themselves I’ve got very little worth taking.

I’d have my tools, of course; but they’re scattered around and old and battered by use; they’re not shiny and new and expensive-looking, and they’re not stored all nice and clean in a box some thief could lift. They’re hung on old nails, or in the closet, and in the shed; a thief would have to spend a lot of time searching the entire place, and with my neighbors looking out for me, the thief is short of the most important advantage he has, which is time.

If somebody’s desperate enough or dumb enough to steal my old handsaw, I’ll buy another old one at a local swap meet. (Since I own three anyway, it’s unlikely anyone would steal all three because they’re not kept together.)

My valuable things, like the water filter, are kept hidden amidst all the low-value junk I keep around to send the message there’s nothing worth looking at. The safest things to own are those which are visibly low-value, surrounded by lots of other mostly worthless stuff.

I’d claim a spot in the community garden, or hire a neighbor to till up my back yard, and I’d plant chard and beans and whatever else my neighbors suggested grew well locally. I’d give away most of what I grew, or barter it, or maybe sell some at the farmer’s market. It wouldn’t matter how little I had to sell, or how much I sold; what mattered was meeting other like-minded souls and swapping tips and edibles.

If I didn’t have a practical skill, I’d devote myself to learning one. If anyone asked me, I’d suggest saw sharpening and beer-making. You’re legally entitled to make quite a bit of beer for yourself, and a decent homebrew is always welcome by those who drink beer. It’s tricky, and your first batches may blow up or go flat, but when you finally get a good batch you’ll be very popular and well-appreciated if you’re of the mind to share.

Saw-sharpening just takes patience and a simple jig; you don’t need to learn a lot, like a craftsman, but you’ll have a skill you can swap with craftsmen/women. As a carpenter, I need sharp saws, and while I can do it myself, I find it tedious and would rather rebuild your front porch handrail or a chicken coop in exchange for the saw-sharpening.

Pickles are always welcome in winter, or when rations get boring; the Germans and Japanese of old lived on black bread or brown rice and pickled vegetables, with an occasional piece of dried meat or fish. Learning how to pickle is a useful and easy-to-learn craft. There are many others. If you’re a techie, then volunteer to keep the network up at the local school; do it for free, and do a good job. Show you care.

Because the best protection isn’t owning 30 guns; it’s having 30 people who care about you. Since those 30 have other people who care about them, you actually have 300 people who are looking out for each other, including you. The second best protection isn’t a big stash of stuff others want to steal; it’s sharing what you have and owning little of value. That’s being flexible, and common, the very opposite of creating a big fat highly visible, high-value target and trying to defend it yourself in a remote setting.

I know this runs counter to just about everything that’s being recommended by others, but if you’re a “hick” like me, then you know it rings true. The flatlanders are scared because they’re alone and isolated; we’re not scared. We’ve endured bad times before, and we don’t need much to get by. We’re not saints, but we will reciprocate to those who extend their good spirit and generosity to the community in which they live and in which they produce something of value.

For security against robbers who snatch purses, rifle luggage, and crack safes,

One must fasten all property with ropes, lock it up with locks, bolt it with bolts.

This (for property owners) is elementary good sense.

But when a strong thief comes along he picks up the whole lot,

Puts it on his back, and goes on his way with only one fear:

That ropes, locks, and bolts may give way.

Thus what the world calls good business is only a way

To gather up the loot, pack it, make it secure

In one convenient load for the more enterprising thieves.

Who is there, among those called smart,

Who does not spend his time amassing loot

For a bigger robber than himself?

Captured US Mercenary Says In Video ‘Confession’ Trump Ordered Plot To “Abduct” Maduro

The nutty ‘Bay of Pigs invasion Venezuela edition’ which appears to have been an utter failure and half-baked scheme nearly from the start just took a few more bizarre turns.

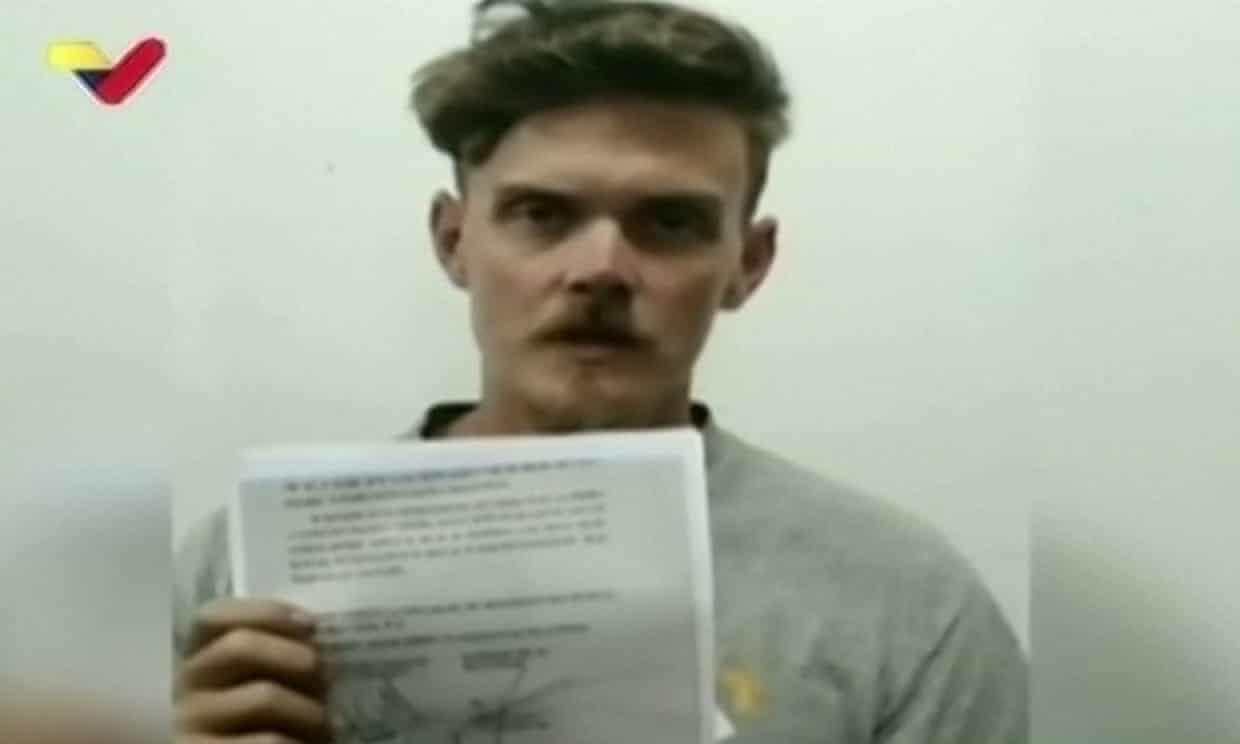

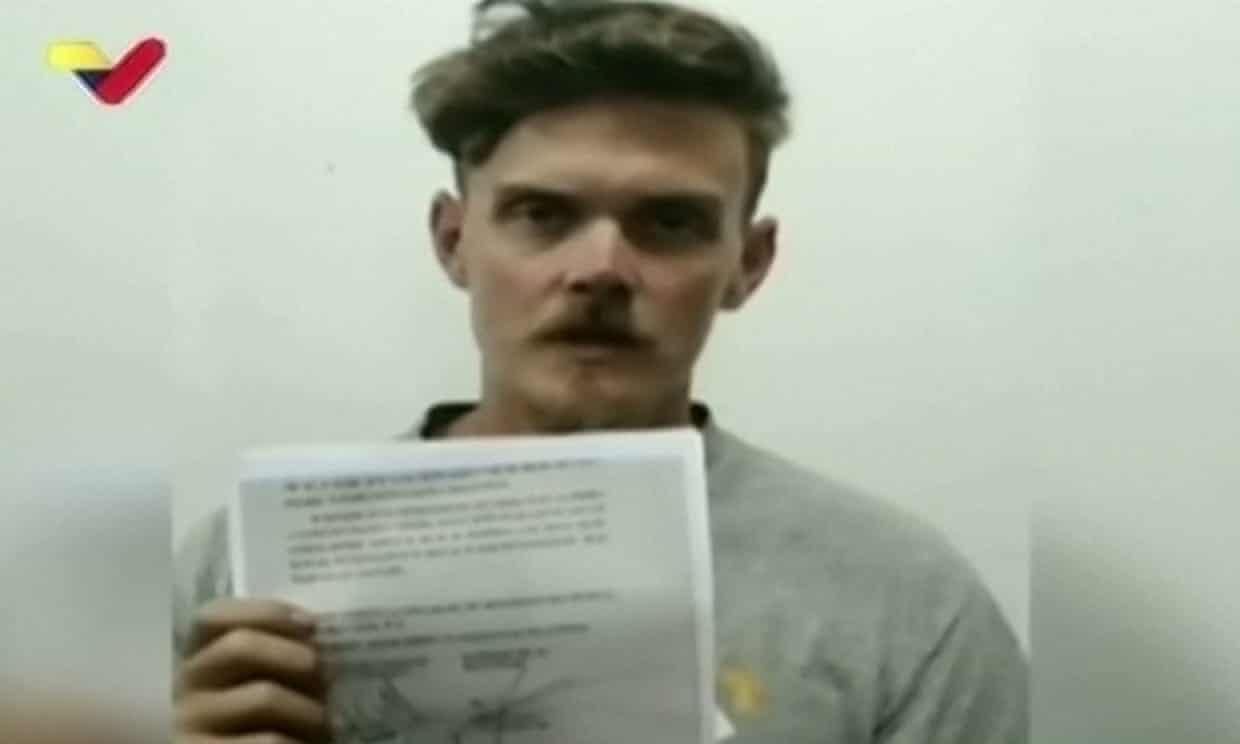

Two days after Venezuelan armed forces captured two US former special forces soldiers turned mercenaries along with others that made up a Venezuela ‘defector force’ allegedly trying to ‘invade’ the county to topple Nicolas Maduro, state TV has aired a “confession” video featuring 34-year old captured American Luke Denman.

Luke Denman shown on Venezuelan state TV after being arrested.

In the heavily edited and scripted “confession” Denman says the mission to orchestrate a coup in the socialist country went straight to the top – ordered by President Trump himself. There were also plans to “abduct” Maduro himself and fly him out of Venezuela and into US custody.

An American mercenary captured after a bungled attempt to topple Nicolás Maduro has claimed he was on a mission to seize control of Venezuela’s main airport in order to abduct its authoritarian leader – and he alleged that was acting under the command of Donald Trump.

…In a heavily edited video confession, broadcast on Wednesday by the state broadcaster, VTV, Denman said he had flown to Colombia in mid-January, where he was tasked with training Venezuelan combatants near Riohacha, a city 55 miles west from the Venezuelan border.

From there Denman – who said he had never previously set foot in either South American country – claimed the group planned to journey to Caracas to “secure” the city and the nearby Simón Bolívar international airport, before bringing down Maduro.

The group of a least a dozen men, who were trained by Florida-based private security firm Silvercorp, reportedly tried to sneak into Venezuela via fishing boats, but were caught soon after stepping foot on land.

BREAKING: Venezuela’s government releases the confession of Silvercorp mercenary Luke Alexander Denman.

Denman further describes in the video his task was to “secure the airport” to pave the way for a broader US military invasion force:

Denman said his mission had been to secure the airport, setup a perimeter, communicate with its tower and then “bring in planes” including “one to put Maduro on and take him back to the United States”.

“I thought I was helping Venezuelans take back control of their country,” Denman added.

There was no sign that any lawyers were present during Denman’s alleged confession or that he was not speaking under duress.

The Maduro government is hailing this as a major victory over Washington coup plotting, however on Tuesday President Trump formally denied that the US had anything to do with it.

“It has nothing to do with our government,” Trump told reporters at the White House.

Luke Denman, 34 (left) and Airan Berry, 41 (right), being paraded in front of Veneuzlean state TV cameras after their arrests Monday.

But Maduro and his top officials have alleged the mission came straight from both Trump and the Colombian president.

The Venezuelan president is further saying he’ll seek the extradition of the ex-Green Beret said to have overseen the mission, since back in the United States, Silvercorps founder Jordan Goudreau.

The fiasco prompted a formal denial of involvement or knowledge from US-backed Venezuelan opposition leader Juan Guaido.

The leader of this bungled assault, Jordan Goudreau, falsely claimed to his ragtag army that he had provided security to Trump. The closest he got was a brief relationship with Keith Schiller, who was Trump’s personal bodyguard. https://t.co/ItTktzYv3d

As we previously reported, Goudreau orchestrated the plot alongside a high ranking Venezuelan military defector, who hooked up with the mercenary firm Silvercorps in Colombia last year.

In the wake of the botched ‘invasion’ and ‘overthrow’ attempt, which many on social media are hilariously mocking under the #BayofPiglets hashtag, Goudreau has positively admitted to being behind it.

Goudreau reportedly ran the secret training camps in neighboring Colombia, with the aim to infiltrate the group into Venezuela in order to fuel momentum for a broader ‘armed popular uprising’ à la covert CIA-style Syria regime change ops.

After leaving the Army in 2016, Goudreau worked as a private security contractor in Puerto Rico and set up Silvercorp US in 2018. Image via SilvercorpsUSA/Daily Mail.

Secretary of State Mike Pompeo on Wednesday backed Trump’s denial of US military or intelligence involvement: “If we had been involved, it would have gone differently,” Pompeo said. “As for who bankrolled it, we’re not prepared to share any more information about what we know took place. We’ll unpack that at an appropriate time. We’ll share that information that makes good sense.”

And concerning the captured Americans: “We will start the process of trying to figure a way – if in fact these are Americans that are there – that we can figure a path forward. We want to get every American back. If the Maduro regime decides to hold them, we’ll use every tool that we have available to try and get them back. It’s our responsibility to do so,” the Secretary of State said.

Allegations in August 2017 scoping memo instructing special prosecutor to investigate Carter Page came from dossier that had already been discredited…

Then-Deputy Attorney General Rod Rosenstein instructed Special Counsel Robert Mueller in August 2017 to investigate allegations against former Trump campaign adviser Carter Page that originated with the Steele dossier and had already been discredited by the FBI, a newly declassified memo showed Wednesday night.

The Justice Department’s release of the unredacted version of Rosenstein’s so-called investigative scoping memo provided the first declarative evidence that Mueller was asked to investigate widely suspect allegations from Christopher Steele’s opposition research conducted for the Clinton campaign and Democratic Party back in 2016.

Specifically, Rosenstein’s memo instucted Mueller to investigate “allegations that Carter Page committed a crime or crimes by colluding with Russian government officials with respect to the Russian government’s efforts to interfere with the 2016 election for President of the United States, in violation of United States law.”

By the time that instruction was given, the FBI had fired Steele as an informant for leaking, interviewed Steele’s sub-source who disputed information attributed to him and had ascertain that allegations Steele had given the FBI specifically about Page were inaccurate and likely came from Russian intelligence sources as disinformation, recently declassified evidence showed.

In addition, the CIA had informed the FBI repeatedly that Page was not a Russian stooge but rather a cooperating intelligence asset for the United States government.

Former House Intelligence Committee Chairman Devin Nunes, who long called for the release of the unredacted scoping memo, said Wednesday’s development confirmed his worst suspicions. He accused prior officials of the Justice Department of unnecessarily hiding the evidence from Congress and the American people before Attorney General William Barr intervened.

“This information was redacted until now for one single reason – to hide the fact that false allegations from the Steele dossier were included in Mueller’s scoping memo,” Nunes told Just the News.

“In other words, a bunch of lies paid for by the Democrats were used to engineer the appointment of a Special Counsel to drag the Trump administration through the mud for years. The Russia collusion hoax was a disgrace, and we can’t let anything like it ever be repeated.”

The degree to which the FBI had discredited Steele’s intelligence reporting on Page — including allegations he colluded with Russia — only recently came into focus with the release of DOJ Inspector General Michael Horowitz’s report on FBI abuses of the FISA surveillance that targeted Page. In addition, just-declassified evidence showed the FBI had learned by February 2017 that Steele’s information on Page was likely disinformation from Russian intelligence planted with Steele.

“Most relevant to the Carter Page FISA applications, the specific substantive allegations contained in Reports 80, 94, 95, and 102, which were relied upon in all four FISA applications, remained uncorroborated and, in several instances, were inconsistent with information gathered by the team,” Horowitz wrote back in December in debunking key allegations against Page.

More recently, declassified footnotes made clear Steele’s claim he had met with a senior Russian back in 2016 named Igor Sechin and had been offered a lucrative finders fee had been debunked by the FBI by February 2017, or months before Mueller was appointed. In fact Steele’s own source challenged the veracity of the information attributed to him inside the dossier.

“The Primary Sub-source told the FBI that one of his/her sub-sources furnished information for that part of Report 134 through a text message, but said that the sub-source never stated that Sechin had offered a brokerage interest to Page,” Horowitz reported.

“The Primary Sub-Source also told the FBI at these interviews that the sub-source who provided the information about the Carter Page-Sechin meeting had connections to Russian Intelligence Services (RIS),” he added.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}