Is The Fed Trying To Inflate A 4th Bubble To Fix The Third?

Authored by Lance Roberts via RealInvestmentAdvice.com,

Over the last couple of years, we have often discussed the impact of the Federal Reserve’s ongoing liquidity injections, which was causing distortions in financial markets, mal-investment, and the expansion of the “wealth gap.”

Our concerns were readily dismissed as bearish as asset prices were rising. The excuse:

“Don’t fight the Fed”

However, after years of zero interest rates, never-ending support of accommodative monetary policy, and a lack of regulatory oversight, the consequences of excess have come home to roost.

This is not an “I Told You So,” but rather the realization of the inevitable outcome to which investors turned a blind-eye too in the quest for “easy money” in the stock market.

It’s a reminder of the consequences of “greed.”

The Liquidity Trap

We previously discussed the “liquidity trap” the Fed has gotten themselves into, along with Japan, which will plague economic growth in the future. To wit:

“The signature characteristics of a liquidity trap are short-term interest rates that are near zero and fluctuations in the monetary base that fail to translate into fluctuations in general price levels.”

Our “economic composite” indicator is comprised of 10-year rates, inflation (CPI), wages, and the dollar index. Importantly, downturns in the composite index leads GDP. (I have estimated the impact to GDP for the first quarter at -2% growth, but my numbers may be optimistic)

The Fed’s problem is not only are they caught in an “economic liquidity trap,” where monetary policy has become ineffective in stimulating economic growth, but are also captive to a “market liquidity trap.”

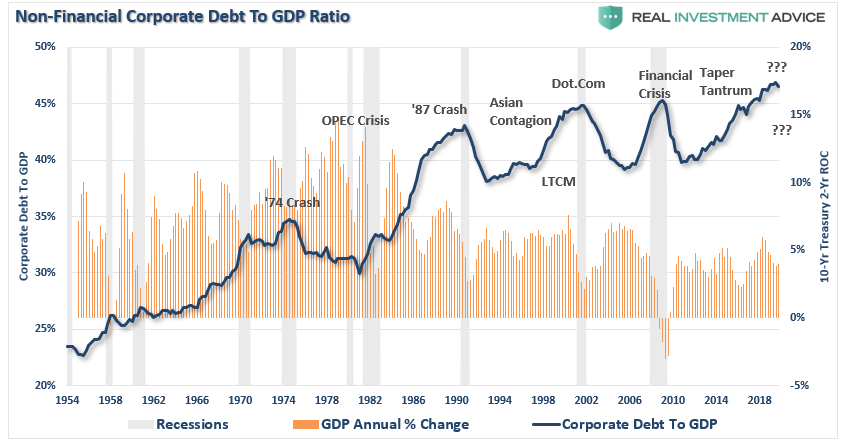

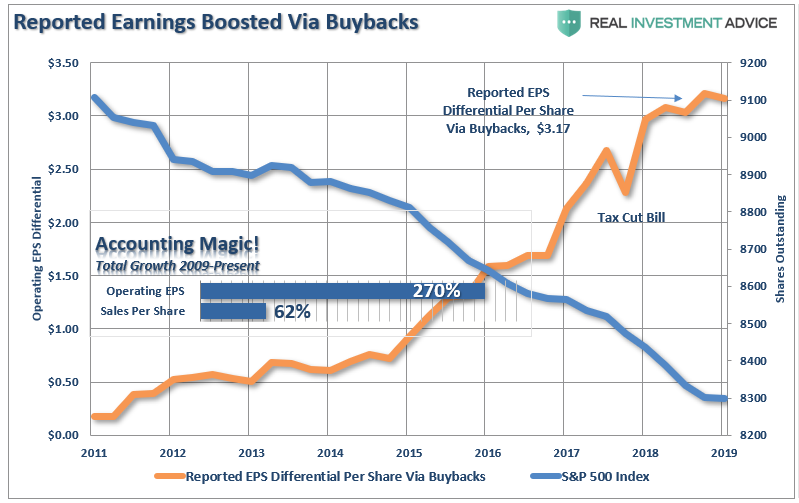

Whenever the Fed, or other Global Central Banks, have engaged in “accommodative monetary policy,” such as QE and rate cuts, asset prices have risen. However, general economic activity has not, which has led to a widening of the “wealth gap” between the top 10% and the bottom 90%. At the same time, corporations levered up their balance sheets, and used cheap debt to aggressively buy back shares providing the illusion of increased profitability while revenue growth remained weak.

As I have shown previously, while earnings have risen sharply since 2009, it was from the constant reduction in shares outstanding rather than a marked increase in revenue from a strongly growing economy.

Now, the Fed is engaged in the fight of its life trying to counteract a “credit-event” which is larger, and more insidious, than what was seen during the 2008 “financial crisis.”

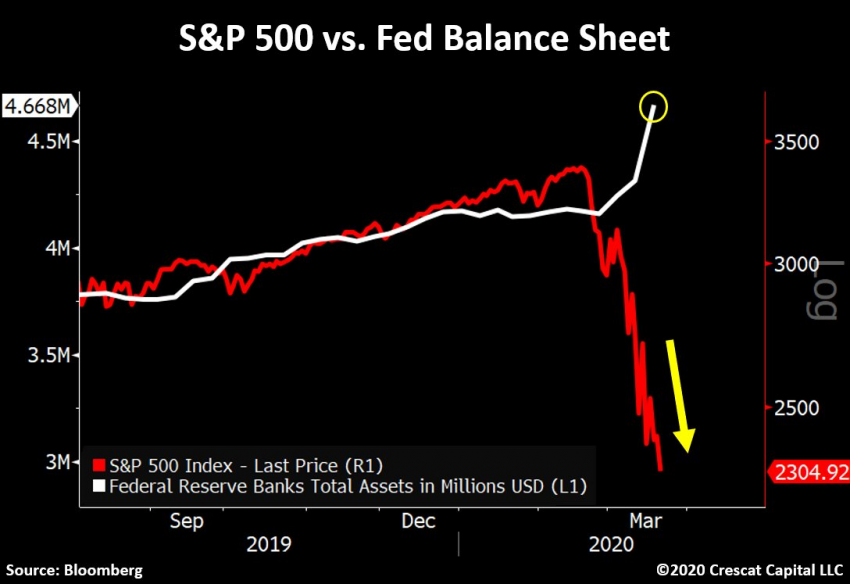

Over the course of the next several months, the Federal Reserve will increase its balance sheet towards $10 Trillion in an attempt to stop the implosion of the credit markets. The liquidity being provided may, or may not be enough, to offset the risk of a global economy which is levered roughly 3-to-1 according to CFO.com:

“The global debt-to-GDP ratio hit a new all-time high in the third quarter of 2019, raising concerns about the financing of infrastructure projects.

The Institute of International Finance reported Monday that debt-to-GDP rose to 322%, with total debt reaching close to $253 trillion and total debt across the household, government, financial and non-financial corporate sectors surging by some $9 trillion in the first three quarters of 2019.”

Read that last part again.

In 2019, debt surged by some $9 Trillion while the Fed is injecting roughly $6 Trillion to offset the collapse. In other words, it is likely going to require all of the Fed’s liquidity just to stabilize the debt and credit markets.

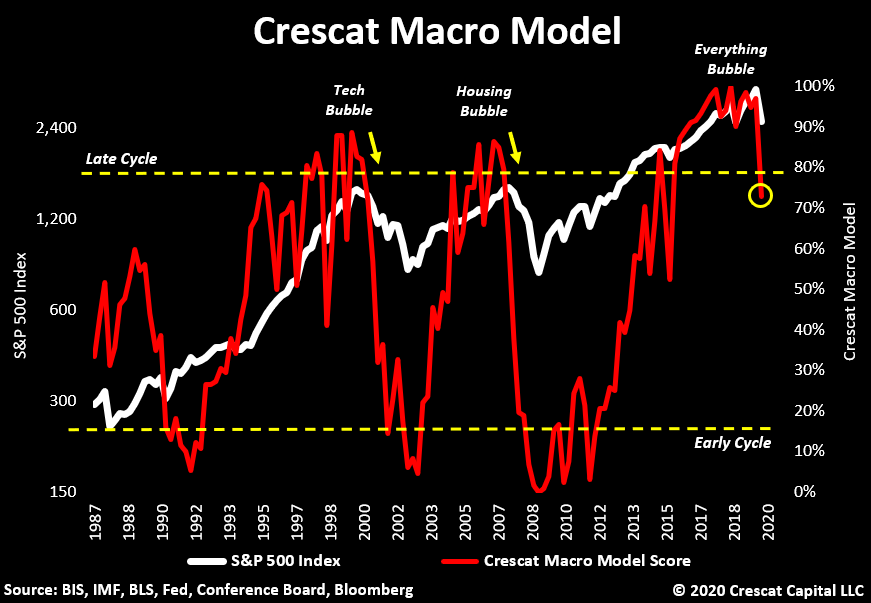

Bubbles, Bubbles, Bubbles

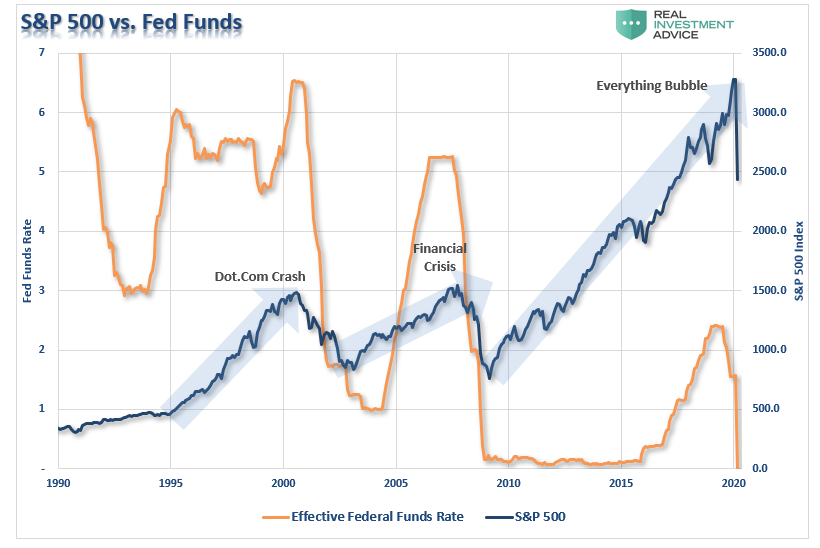

Jerome Powell clearly understands that after a decade of monetary infusions and low interest rates, he has created an asset bubble larger than any other in history. However, they were trapped by their own policies, and any reversal led to almost immediate catastrophe as seen in 2018.

“In the U.S., the Federal Reserve has been the catalyst behind every preceding financial event since they became ‘active,’ monetarily policy-wise, in the late 70’s.”

For quite some time now, we have warned investors against the belief that no matter what happens, the Fed can bail out the markets, and keep the bull market. Nevertheless, it was widely believed by the financial media that, to quote Dr. Irving Fisher:

“Stocks have reached a permanently high plateau.”

What is important to understand is that it was imperative for the Fed that market participants, and consumers, believed in this idea. With the entirety of the financial ecosystem more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the “instability of stability” was the most significant risk.

“The ‘stability/instability paradox’ assumes that all players are rational, and such rationality implies avoidance of complete destruction. In other words, all players will act rationally, and no one will push ‘the big red button.’”

The Fed had hoped they would have time, and the “room” needed, after more than 10-years of the most unprecedented monetary policy program in U.S. history, to try and navigate the risks that had built up in the system.

Unfortunately, they ran out of time, and the markets stopped “acting rationally.”

This is the predicament the Federal Reserve currently finds itself in.

Following each market crisis, the Fed has lowered interest rates, and instituted policies to “support markets.” However, these actions led to unintended consequences which have led to repeated “booms and busts” in the financial markets.

While the market has currently corrected nearly 25% year-to-date, it is hard to suggest that such a small correction will reset markets from the liquidity-fueled advance over the last decade.

To understand why the Fed is trapped, we have to go back to what Ben Bernanke said in 2010 as he launched the second round of QE:

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.”

I highlight the last sentence because it is the most important. Consumer spending makes up roughly 70% of GDP; therefore increased consumer confidence is critical to keeping consumers in action. The problem is the economy is no longer a “productive” economy, but rather a “financial” one. A point made by Ellen Brown previously:

“The financialized economy – including stocks, corporate bonds and real estate – is now booming. Meanwhile, the bulk of the population struggles to meet daily expenses. The world’s 500 richest people got $12 trillion richer in 2019, while 45% of Americans have no savings, and nearly 70% could not come up with $1,000 in an emergency without borrowing.

Central bank policies intended to boost the real economy have had the effect only of boosting the financial economy. The policies’ stated purpose is to increase spending by increasing lending by banks, which are supposed to be the vehicles for liquidity to flow from the financial to the real economy. But this transmission mechanism isn’t working, because consumers are tapped out.”

This was shown in a recent set of studies:

The “Stock Market” Is NOT The “Economy.”

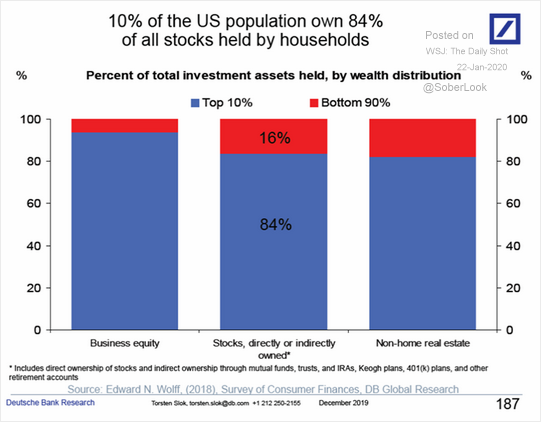

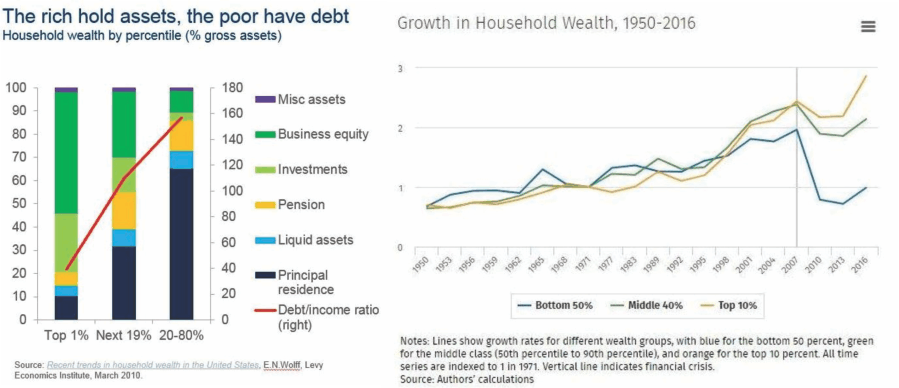

Roughly 90% of the population gets little, or no, direct benefit from the rise in stock market prices.

Another way to view this issue is by looking at household net worth growth between the top 10% to everyone else.

Since 2007, the ONLY group that has seen an increase in net worth is the top 10% of the population.

“This is not economic prosperity. This is a distortion of economics.”

As I stated previously:

“If consumption retrenches, so does the economy.

When this happens debt defaults rise, the financial system reverts, and bad things happen economically.”

That is where we are today.

The Federal Reserve is desperate to “bail out” the financial and credit markets, which it may be successful in doing, however, the real economy may not recover for a very long-time.

With 70% of employment driven by small to mid-size businesses, the shutdown of the economy for an extended period of time may eliminate a substantial number of businesses entirely. Corporations are going to retrench on employment, cut back on capital expenditures, and close ranks.

While the Government is working on a fiscal relief package, it will fall well short of what is needed by the overall economy and a couple of months of “helicopter money,” will do little to revive an already over leveraged, undersaved, consumer.

The 4th-Bubble

“The current belief is that QE will be implemented at the first hint of a more protracted downturn in the market. However, as suggested by the Fed, QE will likely only be employed when rate reductions aren’t enough.”

The implosion of the credit markets made rate reductions completely ineffective and has pushed the Fed into the most extreme monetary policy bailout in the history of the world.

The Fed is hopeful they can inflate another asset bubble to restore consumer confidence and stabilize the functioning of the credit markets. The problem is that since the Fed never unwound their previous policies, current policies are having a much more muted effect.

However, even if the Fed is able to inflate another bubble to offset the damage from the deflation of the last bubble, there is little evidence it is doing much to support economic growth, a broader increase in consumer wealth, or create a more stable financial environment.

It has taken a massive amount of interventions by Central Banks to keep economies afloat globally over the last decade, and there is little evidence that growth will recover following this crisis to the degree many anticipate.

There are numerous problems which the Fed’s current policies can not fix:

-

A decline in savings rates

-

An aging demographic

-

A heavily indebted economy

-

A decline in exports

-

Slowing domestic economic growth rates.

-

An underemployed younger demographic.

-

An inelastic supply-demand curve

-

Weak industrial production

-

Dependence on productivity increases

The lynchpin in the U.S., remains demographics, and interest rates. As the aging population grows, they are becoming a net drag on “savings,” the dependency on the “social welfare net” will explode as employment and economic stability plummets, and the “pension problem” has yet to be realized.

While the current surge in QE may indeed be successful in inflating another bubble, there is a limit to the ability to continue pulling forward future consumption to stimulate economic activity. In other words, there are only so many autos, houses, etc., which can be purchased within a given cycle.

There is evidence the cycle peak has already been reached.

One thing is for certain, the Federal Reserve will never be able to raise rates, or reduce monetary policy ever again.

Welcome to United States of Japan.

Tyler Durden

Thu, 03/26/2020 – 13:25

via ZeroHedge News https://ift.tt/39npH5j Tyler Durden

{kind=link}