Google Says Apps No Longer Work On New Huawei Phones, Warns Users Not To “Sideload”

Last year, the U.S. government banned companies in the U.S. from working with Huawei – with Google being one of the notable names that would have to cease and desist, given its popular Android operating system and Google Play app store.

At the time, Trump had signed “executive order declaring a national emergency banning sales and use of telecom equipment that poses ‘unacceptable’ risks to national security, including critical infrastructure and the online economy,” according to Engadget. Huawei was obviously on that list. China was called the “primary target” of the order.

But there’s still confusion about what’s going on and which products are subject to the services ban, according to The Verge. This is mainly due to the fact that there are still updates and services available for older Huawei devices, but that newer phones like the Mate 30 Pro (below), don’t have access to its services.

To clarify, Google published a note on its Android forums on Friday, explaining its stance with Huawei phones and reminding its users not to try and “sideload” apps onto a phone where they shouldn’t be. The note from Google says that the company can only work with device models available to the public before May 16,2019:

“Our focus has been protecting the security of Google users on the millions of existing Huawei devices around the world. We have continued to work with Huawei, in compliance with government regulations, to provide security updates and updates to Google’s apps and services on existing devices, and we will continue to do so as long as it is permitted. To be clear: US law currently allows Google to only work with Huawei on device models available to the public on or before May 16, 2019.”

The note also makes it crystal clear that Google apps and services are simply not available “for preload or sideload” on Huawei’s new devices:

We have continued to receive a number of questions about new Huawei devices (e.g., new models launching now, or earlier models launched after May 16, 2019 but now becoming available in new regions of the world) and whether Google’s apps and services can be used on these devices. We wanted to provide clear guidance to those asking these important questions.

Due to government restrictions, Google’s apps and services are not available for preload or sideload on new Huawei devices.

The note says that sideloaded apps on newer devices, despite the warning, “will not work reliably because [Google] does not allow these services to run on uncertified devices where security may be compromised.”

“Sideloading Google’s apps also carries a high risk of installing an app that has been altered or tampered with in ways that can compromise user security,” the note says.

Google also offers users a way to check and verify whether or not their phone is certified for its apps:

To check if your device is certified, open the Google Play Store app on your Android phone, tap “Menu” and look for “Settings.” You will see if your device is certified under “Play Protect certification.” You can learn more on android.com/certified.

While it seems as though Google is trying to sidestep the political implications of these rule changes, it is also stern in reminding its users from using backdoor access to load Google apps onto to Huawei phones.

Meanwhile, China has much bigger problems than Huawei on their hands right now. And the U.S.? Perhaps they should consider quarantining not just Huawei, but anything that comes out of China at the moment.

Several outside groups are trying to slow the momentum of current Democratic presidential frontrunner Sen. Bernie Sanders’ (I-Vt.) by spending millions on ad buys, as he continues to dominate the polls.

The campaign against Sanders originated with hybrid PAC Democratic Majority for Israel, a pro-Israel moderate group, that spent over $1.4 million against Sanders. The group spent over $800,000 running ads against the frontrunning Democratic presidential candidate in Iowa and it’s spending $600,000 in Nevada, according to recent filings with the Federal Election Commission.

Sanders campaign file image via Der Spiegel

Most of the PAC’s contributors have a clear history of giving money to candidates on both sides of the aisle. Its biggest donor is Stacy Schusterman, CEO of Samson Resources, an oil and gas company, who donated $1 million to the group in 2019. Schusterman has a long history of donating to Democratic candidates, except in 2016 when she contributed almost $130,000 to 25 Republican lawmakers including $2,700 to House Speaker Paul Ryan (R-Wis.).

Venture capitalist Gary Mark Lauder was the second highest donor to the hybrid PAC giving $500,000. New York businessman Milton Cooper was the next highest at $150,000. Active in donating to various Democrats, he also contributed $4,000 to Sen. Lindsey Graham (R-S.C.) and $2,000 to Sen. Bill Cassidy (R-La.) in 2019.

Ron Zeff, founder and CEO of Carmel Partners, a real estate investment firm, gave the group $100,000. He previously contributed over $70,000 to the GOP. Zeff also donated to Republican presidential candidate Mitt Romney’s campaign in 2012 against President Barack Obama.

The Sanders campaign said it raised $1.3 million within a day of the super PAC ads airing. Of the non-billionaires in the race, Sanders is the only candidate to report substantial cash on hand through January.

Just turned on CNN town hall to see Bernie talking about the lsraeli siege on Gaza. This is why the Israel lobby sees him as a threat. pic.twitter.com/5gS4ieN0Mb

On Wednesday, Mark Mellman, president of Democratic Majority for Israel, announced the group will no longer be running any ads against Sanders or contribute in the presidential race after its ad buys in Nevada run out. The group will focus on Democratic congressional races instead, Jewish Insider reported.

“We will be involved in congressional races and in some cases those are Democrats running against Republican and in some case, those are pro-Israel champions running against anti-Israel challengers,” Mellman reportedly said.

While Mellman’s group will be taking a backseat, the committee has been running an anti-Sanders campaign through Facebook ads since last year. It recently came under scrutiny for accusing “radicals” in the Democratic Party of “pushing their anti-Semitic and anti-Israel policies down the throats of the American people.” The group later apologized for “the ad’s imprecise wording (that) distorted our message and offended many.”

Another group meant to boost moderates, The Big Tent Project, reportedly has a budget of $1 million to run ads against Sanders. Big Tent has spent $200,000 of the budget running two test ads in Nevada and South Carolina, as both states will hold upcoming primaries. Sanders is projected to win both states according to FiveThirtyEight’s average of polls.

While one ad accuses the frontrunner of dumping waste in Latino communities, the other criticizes his healthcare policy. “The cost? Another four years of Trump,” the ad says. Run by Jonathan Kott, a former top aide to Sen. Joe Manchin (D-W.Va.), Big Tent is classified as a 501(c)(4) and is not required to disclose its donors.

Sanders has long questioned American policy toward Israel and advocates an approach that addresses both Israeli security and a “pro-Palestinian” perspective. His criticism has made pro-Israel Democrats and supporters anxious, resulting in a surge of anti-Sanders ads.

As Sanders is projected to win the upcoming contests, big Democratic donors have concerns about him being the presidential candidate, Politico reported. The concern within democrats is that an anti-Sanders campaign could result in boosting his contributions from an already devoted support base. For others, it’s about Sanders’ possible inability to woo moderate and Republican voters.

Multiple news outlets are projecting that Sen. Bernie Sanders (I–Vt.) has won today’s Nevada caucus, making him the clear frontrunner for the Democratic presidential nomination.

NBC News has now projected Bernie Sanders the winner of the Nevada caucuses

Sanders hasn’t locked up the race yet, but he’s now in a position to do so. Democrats look very much like they’re about to nominate a self-described democratic socialist for president.

The basic takeaway here is that it's Bernie's nomination to lose. Exactly how big his margin is in Nevada, who finishes 2nd, etc., may tell us something about precisely how likely he is to lose it, and who is most likely to take it away from him. But it's his race to lose.

There are some hurdles Sanders will have to overcome first—namely the way the large primary field interacts with the complexities of the party’s nominating rules. A total of 3,979 “pledged” delegates are up for grabs in state primaries and caucuses; to win the nomination outright, a candidate must win a majority, or 1,991, of those delegates. But the unusually large field has made it difficult for any candidate to win an outright majority.

Currently, election odds site FiveThirtyEight projects that Sanders will win 1,676 of those delegates, with the projected second-place finisher, former New York Mayor Michael Bloomberg, winning 922 of those delegates. If that happens, Sanders will have the most votes—but not a majority. And then the party’s superdelegates will suddenly be a factor.

Superdelegates are part of state delegations to the Democratic nominating convention. But they’re unpledged, meaning they aren’t won by voting. Instead, they get included in the vote if no candidate wins a clear majority of pledged delegates, which the election model at FiveThirtyEight currently says is (just barely) the most likely outcome.

Currently, most superdelegates remain uncommitted. And as party insiders, it’s at least possible that they will not support an independent who failed to win a majority in the primary and caucus votes. An organized movement by the superdelegates to nominate a lower-placed finisher, combined with a consolidation of votes for other non-Sanders candidates, could keep Sanders from the top of the ticket.

Still, it’s hard to imagine that if Sanders won the most votes and the most pledged delegates in the primary/caucus process, the party’s superdelegates would vote to give the nomination to another candidate. After the 2016 election, the Democratic party changed the rules surrounding superdelegate votes in order to weaken their power, partly in response to frustrations and concerns from Sanders supporters, who viewed superdelegates as a mechanism used by the party establishment to thwart outsider candidates. For the superdelegates to step in and give someone else the nomination would be controversial at minimum, and could well spark something resembling a party-breaking revolt. (In addition, it would raise some eyebrows for the party that has spent the last several years complaining about subversions of democracy to give the nomination to a candidate who did not win the most primary/caucus votes.)

So even if Sanders isn’t on track to win a majority of pledged delegates, he is nevertheless on track to win the Democratic Party’s nomination. At a minimum, he has a clearer shot than any other candidate right now, since no rival appears poised to consolidate non-Sanders voters.

I've got news for the Republican establishment. I've got news for the Democratic establishment. They can't stop us.

Which means that as it faces off against Donald Trump in the 2020 election, the Democratic Party is probably going to be led by a cantankerous 78-year-old democratic socialist—not only someone who supports foolish and domestically unprecedented government programs such as single-payer health care and free tuition at public universities, but someone who honeymooned in the Soviet Union, proudly supported the brutal Sandinistas in Nicaragua, and who once spoke admiringly of the Cuban government. If they nominated Sanders, Democrats would own his entire radical agenda and history.

Should this happen, it would represent a tremendous gamble for the Democratic Party, which would be betting its future on a deeply polarizing figure who is disliked by many in his own party. And in a matchup against Donald Trump, it would represent a no-win scenario for anyone who values individual liberty, free markets, or even just basic executive competence.

Some Democrats appear to realize the predicament their party is in. But as former Jeb Bush adviser Tim Miller wrote for The Bulwark, with Super Tuesday, and its giant delegate haul, just days away, it may already be too late. Unless Democratic voters can consolidate around a non-Sanders candidate in a very short period of time, Sanders is set to win.

From his heart attack to his honeymoon in the USSR, nothing has stuck to Bernie Sanders. Now, with a burgeoning anti-Sanders effort underway, his Teflon shield face its biggest test. https://t.co/LTnsaiIuQY via @NYTimes

It’s possible, of course, that nominating Sanders could backfire on both the candidate and the party, and that Sanders could end up losing by a large margin in November. Some Republicans appear to believe that Sanders would be the easiest candidate to beat, and that he would have down-ticket effects on the rest of the party.

That scenario does not strike me as out of the range of possibility. Yet I wouldn’t be too sure. Because in many ways, the Democratic Party would be following in the footsteps of Republicans, who in 2016 similarly nominated a polarizing, populist, authoritarian-curious outsider who won just enough votes in an unusually crowded and competitive primary field despite broad opposition from the party establishment. Most knowledgable observers thought that nominee had little to no shot at winning the election. But Donald Trump is now our president.

It is still early, but Sanders is following in Trump’s footsteps. With Sanders’ win in Nevada, he’s one step closer to the presidential nomination. And America is one step closer to a socialist in the White House.

from Latest – Reason.com https://ift.tt/37TxOpo

via IFTTT

Multiple news outlets are projecting that Sen. Bernie Sanders (I–Vt.) has won today’s Nevada caucus, making him the clear frontrunner for the Democratic presidential nomination.

NBC News has now projected Bernie Sanders the winner of the Nevada caucuses

Sanders hasn’t locked up the race yet, but he’s now in a position to do so. Democrats look very much like they’re about to nominate a self-described democratic socialist for president.

The basic takeaway here is that it's Bernie's nomination to lose. Exactly how big his margin is in Nevada, who finishes 2nd, etc., may tell us something about precisely how likely he is to lose it, and who is most likely to take it away from him. But it's his race to lose.

There are some hurdles Sanders will have to overcome first—namely the way the large primary field interacts with the complexities of the party’s nominating rules. A total of 3,979 “pledged” delegates are up for grabs in state primaries and caucuses; to win the nomination outright, a candidate must win a majority, or 1,991, of those delegates. But the unusually large field has made it difficult for any candidate to win an outright majority.

Currently, election odds site FiveThirtyEight projects that Sanders will win 1,676 of those delegates, with the projected second-place finisher, former New York Mayor Michael Bloomberg, winning 922 of those delegates. If that happens, Sanders will have the most votes—but not a majority. And then the party’s superdelegates will suddenly be a factor.

Superdelegates are part of state delegations to the Democratic nominating convention. But they’re unpledged, meaning they aren’t won by voting. Instead, they get included in the vote if no candidate wins a clear majority of pledged delegates, which the election model at FiveThirtyEight currently says is (just barely) the most likely outcome.

Currently, most superdelegates remain uncommitted. And as party insiders, it’s at least possible that they will not support an independent who failed to win a majority in the primary and caucus votes. An organized movement by the superdelegates to nominate a lower-placed finisher, combined with a consolidation of votes for other non-Sanders candidates, could keep Sanders from the top of the ticket.

Still, it’s hard to imagine that if Sanders won the most votes and the most pledged delegates in the primary/caucus process, the party’s superdelegates would vote to give the nomination to another candidate. After the 2016 election, the Democratic party changed the rules surrounding superdelegate votes in order to weaken their power, partly in response to frustrations and concerns from Sanders supporters, who viewed superdelegates as a mechanism used by the party establishment to thwart outsider candidates. For the superdelegates to step in and give someone else the nomination would be controversial at minimum, and could well spark something resembling a party-breaking revolt. (In addition, it would raise some eyebrows for the party that has spent the last several years complaining about subversions of democracy to give the nomination to a candidate who did not win the most primary/caucus votes.)

So even if Sanders isn’t on track to win a majority of pledged delegates, he is nevertheless on track to win the Democratic Party’s nomination. At a minimum, he has a clearer shot than any other candidate right now, since no rival appears poised to consolidate non-Sanders voters.

I've got news for the Republican establishment. I've got news for the Democratic establishment. They can't stop us.

Which means that as it faces off against Donald Trump in the 2020 election, the Democratic Party is probably going to be led by a cantankerous 78-year-old democratic socialist—not only someone who supports foolish and domestically unprecedented government programs such as single-payer health care and free tuition at public universities, but someone who honeymooned in the Soviet Union, proudly supported the brutal Sandinistas in Nicaragua, and who once spoke admiringly of the Cuban government. If they nominated Sanders, Democrats would own his entire radical agenda and history.

Should this happen, it would represent a tremendous gamble for the Democratic Party, which would be betting its future on a deeply polarizing figure who is disliked by many in his own party. And in a matchup against Donald Trump, it would represent a no-win scenario for anyone who values individual liberty, free markets, or even just basic executive competence.

Some Democrats appear to realize the predicament their party is in. But as former Jeb Bush adviser Tim Miller wrote for The Bulwark, with Super Tuesday, and its giant delegate haul, just days away, it may already be too late. Unless Democratic voters can consolidate around a non-Sanders candidate in a very short period of time, Sanders is set to win.

From his heart attack to his honeymoon in the USSR, nothing has stuck to Bernie Sanders. Now, with a burgeoning anti-Sanders effort underway, his Teflon shield face its biggest test. https://t.co/LTnsaiIuQY via @NYTimes

It’s possible, of course, that nominating Sanders could backfire on both the candidate and the party, and that Sanders could end up losing by a large margin in November. Some Republicans appear to believe that Sanders would be the easiest candidate to beat, and that he would have down-ticket effects on the rest of the party.

That scenario does not strike me as out of the range of possibility. Yet I wouldn’t be too sure. Because in many ways, the Democratic Party would be following in the footsteps of Republicans, who in 2016 similarly nominated a polarizing, populist, authoritarian-curious outsider who won just enough votes in an unusually crowded and competitive primary field despite broad opposition from the party establishment. Most knowledgable observers thought that nominee had little to no shot at winning the election. But Donald Trump is now our president.

It is still early, but Sanders is following in Trump’s footsteps. With Sanders’ win in Nevada, he’s one step closer to the presidential nomination. And America is one step closer to a socialist in the White House.

from Latest – Reason.com https://ift.tt/37TxOpo

via IFTTT

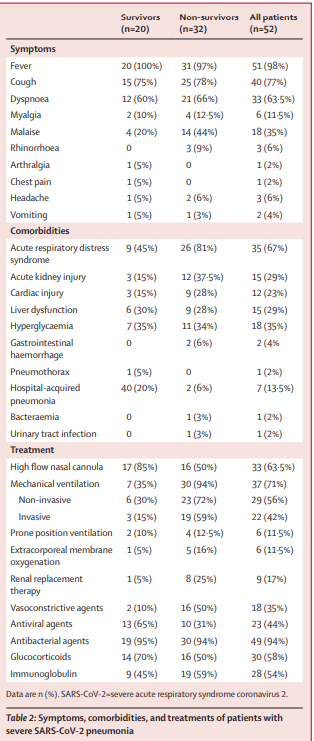

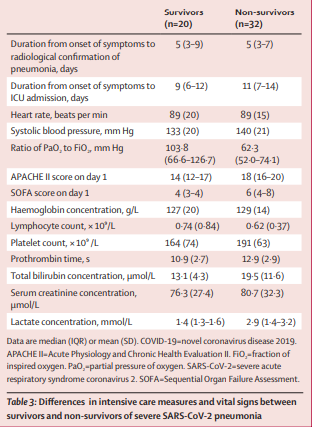

Researchers Find 61.5% Of Coronavirus Patients With Severe Pneumonia Won’t Survive

Since the Wuhan coronavirus first appeared late last year, researchers have been studying it, though for the first month or so, only Chinese scientists had access to the data.

But now that China has shared its data with the world, research has been appearing more quickly, with more opportunities for peer review.

According to a study published in the Lancet on Friday, patients who are especially vulnerable to severe COVID-19 infections – a group that includes the very old, very young and those with co-occurring conditions – die at a higher rate from COVID-19 than they did from SARS and MERS.

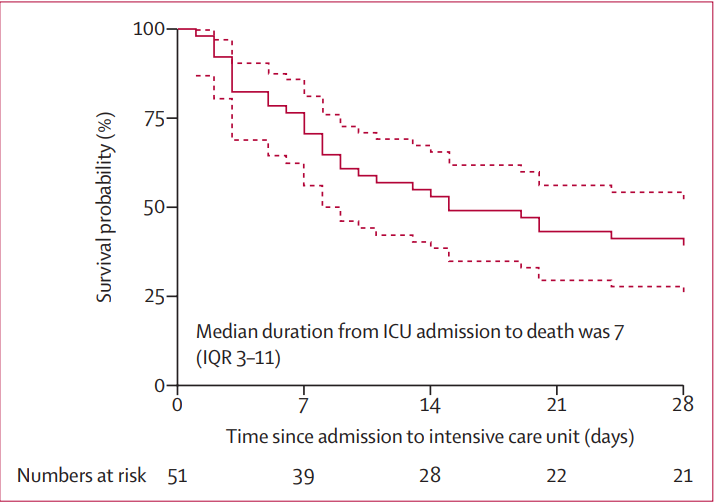

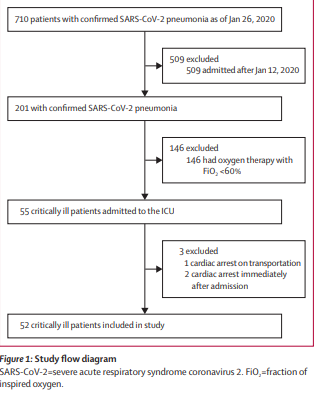

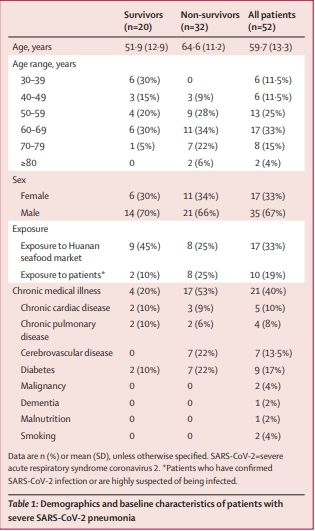

A study of 52 critically ill adults at Wuhan Jin Yin-tan hospital found that 61.5% of patients requiring hospitalization and intense monitoring ended up becoming “non-survivors”, to borrow some of the researchers’ terminology.

The researchers concluded that COVID-19 – or SARS-CoV-2, as they call it – is more lethal for vulnerable patients than SARS or MERS was.

Like SARS-CoV and Middle Eastern respiratory syndrome (MERS)-CoV, SARS-CoV-2 is a coronavirus that can be transmitted to humans, and these viruses are all related to high mortality in critically ill patients.12 However, the mortality rate in patients with SARS-CoV-2 infection in our cohort is higher than that previously seen in critically ill patients with SARS. In a cohort of 38 critically ill patients with SARS from 13 hospitals in Canada, 29 (76%) patients required mechanical ventilation, 13 (43%) patients had died at 28 days, and six (16%) patients remained on mechanical ventilation. 17 (38%) of 45 patients and 14 (26%) of 54 patients who were critically ill with SARS infection were also reported to have died at 28 days in a Singapore cohort13 and a Hong Kong cohort,14 respectively. The mortality rate in our cohort is likely to be higher than that seen in critically ill patients with MERS infection. In a cohort of 12 patients with MERS from two hospitals in Saudi Arabia, seven (58%) patients had died at 90 days.15 Since the follow-up time is shorter in our cohort, we postulate that the mortality rate would be higher after 28 days than that seen in patients with MERS-CoV.

Researchers presented their findings in a series of tables which clearly broke down each patient’s symptoms and path to recovery (or death).

The mean age of the 52 patients who participated in the study was 59 years old. 35 (67%) were men, 21 (40%) had been diagnosed with some kind of chronic illness, and 51 (98%)were found to have a fever.

A new video released on Friday showed the Turkish military and their allied militants attempting to hit a Russian aircraft with an anti-aircraft missile in the Idlib Governorate yesterday.

In the short video, the Turkish forces and their allies militants can be seen on the roof of a building, where they later attempted to shoot down the Russian aircraft in the skies of the Idlib Governorate.

NEW – Video footage from yesterday shows #Turkey soldiers firing a MANPADS at a #Russia jet flying over #Idlib.

As shown in the video, however, the anti-aircraft missile fails to hit the Russian aircraft that had just flown over their positions in what is presumably the eastern countryside of Idlib.

The Russian jet is seen deploying counter-measures seconds after the surface-to-air missile is fired.

Let’s break down how Turkish soldiers failed to shoot down the Su24 that wiped them out. pic.twitter.com/uwBv6Sr0yg

Prior to the release of this video, another film was released on Thursday that showed the militant forces in the Idlib Governorate trying to shoot down a Russian Su-24 aircraft that had just got done bombing their positions.

Below is the video that was released on Friday of the attempted downing of the Russian aircraft:

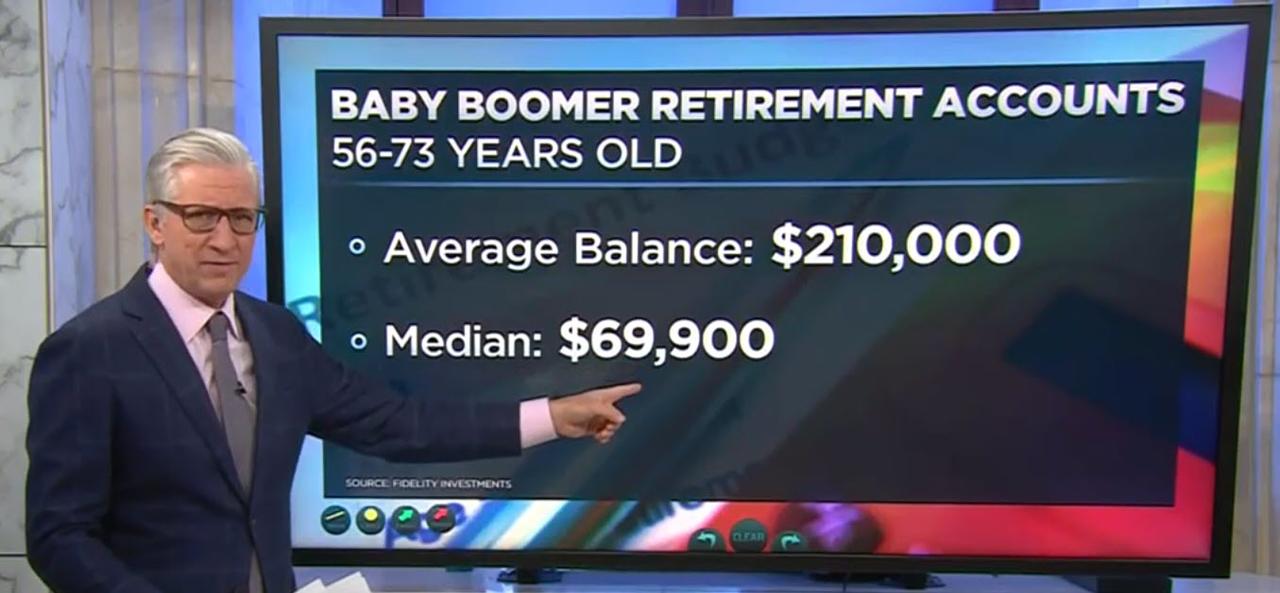

401(k) Millionaires Surge To Record Level Under Trump

A Fidelity Investments press release on Thursday said the number of customers with more than $1 million in their 409k 401k soared to record levels in 4Q19 fueled by higher savings rates and surging stock markets.

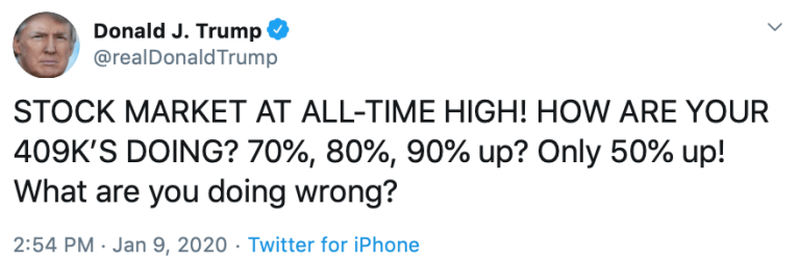

There’s a reason why President Trump touted 401k growth during his State of the Union address last week, because balances are increasing, and it will help him win the election.

Fidelity noted that 401k millionaires soared last quarter, reaching a record level. Customers with the brokerage house that have over one million dollars in their 401k hit 233,000, up from 200,000 in Q3, a 17% jump M/M.

The number of IRA millionaires increased to 208,000, also a record high and an increase from 182,400 in Q3.

All of these new 401k and IRA millionaires were created through President Trump’s pressure on the Federal Reserve to unleash easy money policies to boost the stock market.

And, of course, as we all know, JPM’s drain of liquidity via Money Markets and reserves parked at the Fed promoted a liquidity crisis that resulted in “Not QE,” which allowed even more liquidity to flow into the stock market starting last September, the same period when all of these investment accounts soared in value. Coincidence?

Kevin Barry, president of Workplace Investing at Fidelity Investments, noted in the release that “growth in savings levels over the last 10 years demonstrates the positive impact of taking a long-term approach to retirement, and recent Fidelity research demonstrates workers who do so have reason to feel increasingly confident about their retirement readiness.”

“However, as we enter a new decade and continue to see markets rise and fall, it’s more important than ever to remember some of the important elements of a successful retirement strategy – these include maintaining positive savings habits, ensuring your account has the right balance of stocks, bonds, and cash, and continuing to focus on your long-term savings goals,” Barry added.

Every chance Trump gets, he tweets or tells everyone that their 409k 401k is performing great.

Raoul Pal of Real Vision had a good take on it:

The irresponsiblity of this, telling the average person to take more risks this late in the cycle is simply staggering, regardless of what the markets do. To make them think a 50% return is low lacks any fiduciary responsibility. This is worse than the Greenspan housing comments. https://t.co/UqrFbYmoXM

It seems that the Fed’s easy money policies over the last year, juicing markets to all-time highs, could be a vote of confidence by the central bank to get Trump reelected.

The push for speech control escalates. There is now a concentration of stories concerning social media companies and their role in shaping political thought.

We are nine months from a pivotal presidential election in the U.S. and the push is on to ensure that the outcome goes the way those in power want it to.

Three times in as many weeks billionaire busybody George Soros has attacked Facebook CEO Mark Zuckerberg, demanding he be removed because he is working to re-elect Donald Trump.

Create a controversy that isn’t real to seed a narrative that there’s a problem in need of a solution. Facebook has been the center of this controversy to inflame passions on both sides of the political aisle to ensure the desired outcome.

They want regulation of all social media companies to create unscalable barriers to entry for new ones while curtailing free speech on the existing ones.

Warren Buffet would call that a moat. I call it tyranny.

Section 230 grants immunity to companies like Facebook and Google from prosecution for content hosted on their services as they argue they are not publishers but rather just pass-through entities or platforms of user-generated content.

Now, it’s pretty clear for the past few years the social media companies have been acting with open editorial bias to deplatform undesirables. They rewrite broadly defined terms of services and EULAs (End-User Licence Agreements) which they use to justify controlling what content they are willing to host.

And that’s where the Section 230 immunity comes into play. The big tech companies want to have it both ways, be a neutral platform legally but self-define ‘neutrality’ in such a way that benefits them politically, economically and socially while insulating themselves from breaching contracts with their customers.

What’s clear from Barr’s comments he’s approaching this from a law enforcement perspective.

“We are concerned that internet services, under the guise of Section 230, can not only block access to law enforcement — even when officials have secured a court-authorized warrant — but also prevent victims from civil recovery,” Barr said. “Giving broad immunity to platforms that purposefully blind themselves — and law enforcers — to illegal conduct on their services does not create incentives to make the online world safer for children.”

And this clearly doesn’t address the real issue. That’s your sign there’s something wrong here.

Both political parties are unhappy with the current situation and that should be your red flag that a great stitch-up is in progress. Because the end goal here is government oversight that has bipartisan support.

That support has to be manufactured from both sides. The left wants protection from ‘fake news’ and ‘Russian meddling’ while the right wants a level playing field to air ideas in the public square.

Didn’t you all notice how both of these things became issues right after the wrong person won the 2016 presidential election and the British people made the wrong decision about EU Membership?

I’m sure you noticed the blatant bias exhibited by Facebook, Google, YouTube, Twitter, Reddit and the rest of these protected platforms and wondered why they were allowed to act so egregiously with seemingly no recourse?

The big tech companies don’t want more government oversight, they simply want to continue to have their have their editorial take and enforce it too while taking your money and suppressing your voice.

Government intervention is not the solution here. In fact, it is the goal of the entire exercise.

I don’t want the government coming in and further defining the rules by which Facebook can deplatform everyone who tells inconvenient truths.

Because that’s all government does. And then it empowers a bureaucracy to enforce those rules.

I don’t need a Ministry of Truth to protect me from the bad people. I know where the bad people are and, in your heart, so do you.

So the question isn’t whether Barr should strip these companies of their Section 230 immunity. Of course he should if they exhibit any kind of editorial behavior.

But, in typical Swamp fashion, Barr isn’t concerned about that. He’s concerned with using Facebook to track down criminals; the implication being drug runners, murderers, etc.

That’s a sop to law and order conservatives to get their support politically.

But the real criminals are in the bowels of the compliance departments and algorithm factories of these social media companies pushing the bounds of indecency by trying to protect us from fake news to control the flow of information.

They’ve already done a great deal of this, altering search algorithms to ensure only approved news sources show up in the results.

We know they are all working in cahoots with the intelligence agencies here in the U.S. but no one will admit it publicly. The EU and China are more honest about their tyrannical impulses using their anti-democratic structure to create rules which they force onto these multi-national companies.

Now Twitter is testing new flagging abilities for verified accounts to act as community censors, creating the illusion of a user-controlled public space. It’ll only be for those that get blue check marks. And that’s a system clearly gamed to reflect a particular ideological bias as no one who dissents from the approved globalist message gets one of those anymore.

So, only journalists from official news outlets will have this ability to fact-check in real time the pronouncements of important influencers.

If you don’t think this is simply a means by which to make it seem fair to suppress the king of Twitter, Donald Trump, then you clearly haven’t had your morning coffee.

The Wire is simply a metaphor for the transmission of information. The Wire takes many forms. And if you aren’t sure whether something is The Wire just ask if you have control over it or not.

The Internet? The Wire.

Electricity? The Wire

Roads? The Wire.

Media? The Wire.

Money? The Wire.

In short, The Wire is the main conduit through which we communicate with each other. Money? Really? Yes, really. What are prices if not information about what we are willing to part with your money in exchange for?

Without The Wire modern society fails. So, government can’t shut it down but neither can it allow unrenstrained access to it.

Electricity, commerce, communications, everything, goes over The Wire.

Control of The Wire is everything. Soros is desperately trying to hold onto control over the social media companies he’s invested so heavily in to influence their influence.

And it’s clear we’ve entered the next phase of regaining control over it.

The solution to the Section 230 Immunity issue for these companies is to remove it and open them up to civil liabilities for their inconsistent enforcement of their own policies.

Because once you do that they have no protection under commercial contract law.

Those users that use these platforms for commercial purposes are materially harmed by the ever-changing rules of these platforms.

They entered into an agreement with YouTube or Facebook in good faith expectation of a certain level of service.

Facebook’s business is built on the implicit guarantee of that service. In turn, Facebook was built on the backs of those using the platform.

Unilaterally taking away that access without compensation simply because Facebook said so is a perversion of contract law. Why should Facebook be allowed to do that? Why hasn’t this clear inequity between parties to a contract been addressed by the courts?

And that’s what we should be addressing here.

And I’m not just talking about Facebook here. Remember when the social network Gab had its internet access revoked by GoDaddy? How does GoDaddy escape paying damages for unilaterally denying service?

There is clear opportunity for them to be sued into submission by the millions of users whose businesses and reputations have been destroyed due to arbitrary enforcement of company rules.

At the end of the day these companies create and use as excuses broad powers which have almost no precedent in contract law. Their EULAs are contracts the user signs which grants them no rights or guarantees of service in any way. They can be abrogated, updated and changed to suit the company’s whim with no redress for the breach of contract from the other party.

This is outrageous, unacceptable and flies in the face of hundreds of years of contract law.

If Facebook wants to ban Alex Jones from their platform fine. I have zero problem with that. If they want to act as a private business which is protected under the First Amendment’s protection of Freedom of Association, great!

I’m all for re-establishing that in this society.

Let’s open up that can of worms.

It would finally be an honest conversation. Because we are rapidly approaching the moment of reverse racism, whereby Facebook doesn’t want to host racist or sexist content.

And I’m fine with that. But I’m also fine then with restaurants not serving black people or people baking wedding cakes for gay couples.

Freedom OF association is also Freedom FROM association, folks.

The shit-libs and the oligarchs want it both ways. They want you to be forced to associate with others on their terms but deny you a place in society because you disagree with them.

That is, in a word, tyrannical.

So, in a just world, Facebook owes Alex Jones millions for lost revenue and damages to Jones’ business as well as, one could argue, a portion of Facebook’s revenue it generated during the time it hosted Jones’ content which brought the company users, revenue and market share.

Multiply that lawsuit by ten for the number of platforms Alex Jones has been banned from. Then multiply that number by the millions for everyone else these platforms have materially harmed.

And then we’ll see what the market cap of the NASDAQ 100 would truly be.

And that’s one way we should fight this, not by empowering more bureaucrats to police everyone’s speech on Twitter, but to sue Twitter for non-fulfillment of obligations under the reasonable expectation of service they are to provide as a party to a legal contract.

This is what I wanted to hear William Barr was focusing on in working on. But that is exactly what will not happen.

The other is to develop technology which resists the centralizing power of these companies to control our speech, democratizing it at the incentive level, through projects like Brave and other blockchain-based systems, which empower the user, not the platform to decide which content has value and which doesn’t.

* * *

Beware the deplatforming of Facebook, it’s just another brick in the wall. Join my Patreon if you believe in free and open exchange of ideas.

Libya Asks US To Establish Military Base To Combat Russian Presence

This is all we need: another American base located smack dab in the middle of yet another civil war we had a big hand in causing in the first place.

“Libya’s security chief called on the U.S. to set up a base in the North African country to counter Russia’s expanding influence in Africa,”Bloomberg reports.

It appears a desperate effort on the part of the Tripoli-based Government of National Accord (GNA) to gain Washington’s attention after Trump last year seemed to switch his preference to Gen. Khalifa Haftar.

File image, US Army/Air Force Magazine

The US president famously said last Spring that Haftar, who holds dual citizenship after living outside D.C. for two decades and is said to be close to the CIA, is “securing the oil”.

Haftar is being politically supported by Moscow, and it should be noted has Russian mercenaries in the ranks of his Libyan National Army, or LNA.

That’s just what we need — another indefensible American military base in a dangerous, remote, unwinnable, conflict where no side can claim moral purity. https://t.co/9kVkIsXCrE

The oil-rich nation across the Mediterranean from Europe has been one of the main stages for Russia’s push for influence over the past year. More than a thousand mercenaries deployed by a confidant of President Vladimir Putin have backed Haftar’s offensive to capture the capital from the internationally recognized government.

Bashagha warned that Russia’s backing of Haftar was part of a broader push for influence.

Pro-Haftar forces have been laying siege to the capital of Tripoli for months now, displacing tens of thousands of civilians, in what’s fast shaping up to be a major North African proxy war, given the UAE, Egypt and Russia have taken Haftar’s side, while Turkey and most major UN countries have stuck by Tripoli under Prime Minister Fayez al-Sarraj.

Khalifa Haftar is greeted on a 2017 trip to Russia, via AFP/Getty.

Though AFRICOM has been expanding rapidly over the past decade across the African continent, it doesn’t look as if the Trump administration is ready to commit any level of American troops to the Libyan War 2.0 any time soon.

Sanders Projected To Win Nevada Caucuses After Early Reporting Landslide

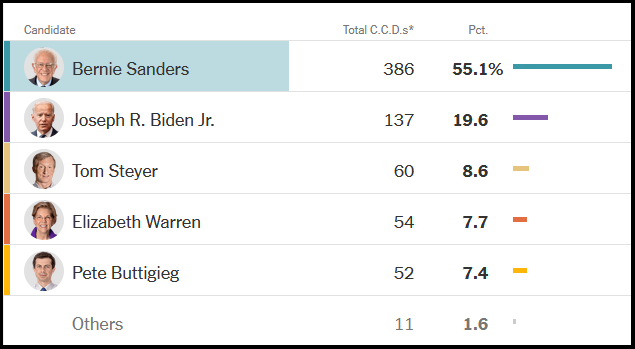

Sen. Bernie Sanders (I-VT) is projected to win the Nevada caucuses after early reports suggest a landslide victory, according to Fox News, which named Sanders the winner.

While just four percent of the results are in, Sanders has 56% of the delegates, followed by Biden at 18.8% and Warren at 8.5%.

The closely-watched process began with Nevada Democrats optimistic that they would avoid a repeat of the technical glitches that plagued the caucuses in Iowa. Those fears led the state Democratic Party to decide to rely on traditional reporting by phone, rather than an app made by the same developer that created the app blamed for the debacle in Iowa. It has also scrapped a plan to use a Google Forms app loaded onto iPads. –Fox News

“”Nevada Democrats have learned important lessons from Iowa, and we’re confident they’re implementing these best practices into their preparations,” said DNC spokeswoman Xochitl Hinojosa. “We’ve deployed staff to help them across the board, from technical assistance to volunteer recruitment.”

On Saturday, DNC Chairman Tom Perez told Fox News that the party is in “great shape,” adding “We have all of the early vote results distributed to the caucus sites. People are checking now…. I think it’s going to be a really exciting day.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}