“Right now, there’s no real inflation at play. But if we go further than we are currently, inflation is inevitably going to rise.” That’s from Alan Greenspan on CNBC this week. The “further” relates to US Federal deficit spending, the idea being that +$1 trillion annual budget shortfalls will eventually trigger price inflation.

It isn’t just Greenspan that is worried about rising US consumer price inflation; as we read through the most bearish market commentaries for 2020 this concern often has pride of place. Easy monetary and fiscal policy combined with a reaccelerating US/global economy late in a cycle is THE playbook for rising prices, so fair enough. The counterarguments are more structural (aging demographics, Internet price discovery, etc.), and while those work over the long term we can’t lean on them too hard in any given year. So do the inflation hawks have a case to make about 2020?

You know our methods for evaluating questions like this – a combination of market-based expectations and historical/real time data – so let’s get right to it:

Even during the period of Federal Reserve bond buying, TIPS spreads were reasonable proxies for market expectations about long-run future inflation. The lowest they ever got was 1.2% in early 2016 and they have often been +2.0% over the last decade, the Fed’s notional target (see chart below).

TIPS spreads were +2.0% for almost all of 2018, for example, only dropping in November along with US/global growth expectations.

Expected 10-year forward inflation as measured by the TIPS market hasn’t touched 2.0% in 2019 and currently sits at 1.73%.

Bottom line: after many years of holding out hope that US structural inflation could hold at 2.0%, TIPS spreads have thrown in the towel. The current TIPS spread of 1.73% is almost spot-on the 12 month average CPI of 1.82%. Even with the recently announced Phase 1 US-China trade deal and USMCA’s imminent passage, a late-year global equity rally, and a dovish Fed this market has resolutely refused to countenance the idea that US price inflation can make a comeback.

Here is the 10-year TIPS spread chart for the last decade:

Source: Bloomberg

#2: Core measures of inflation (PCE and CPI):

The Fed uses Personal Consumption Expenditures (PCE) data, while markets tend to look at the Consumer Price Index (CPI). Since 2000 core (ex-food and energy) PCE inflation has been lower than core CPI. We’ve included an explainer from the Cleveland Fed below if you want to learn more about why that’s the case.

The latest inflation readings for each: core PCE is at 1.6% as of October 2019 (latest data) but core CPI is higher at 2.3%.

Over the last 12 months core PCE has: 1) never hit 2.0% and 2) averaged 1.7%.

Over the last 12 months core CPI has: 1) always been 2.0% or greater and 2) averaged 2.2%.

Bottom line: inflation, like beauty, is in the eye of the index-focused beholder. By the Fed’s preferred measure (PCE) the US economy is still shy of their 2.0% inflation target. By the market’s primary metric (CPI), it is running slightly hot.

Since PCE is how the Fed makes policy, here is the 10-year chart for this measure’s core inflation rate for your review (and note how few times it breaches 2.0%):

Source: Bloomberg

#3: Owners’ Equivalent Rent (OER):

OER is how the BLS measures housing price inflation in the CPI calculation. It asks homeowners how much their house would rent for and tracks those responses over time.

OER is the single most important piece of core CPI, at 31% of the total. That makes it a more important contributor of measured inflation than any other single category by a wide margin.

OER inflation has not accelerated in over 4 years, trending consistently between 3.0% – 3.5% since mid 2015 (see chart below).

Bottom line: given that OER inflation shows no sign of acceleration (November’s 3.3% was the lowest since January’s 3.2%), this anchor in the CPI Index seems firmly set.

Here is the OER inflation chart:

Source: Bloomberg

Now, let’s wrap this up:

To believe in a 2020 inflation surge, one has to assume that the US economy is at a tipping point where marginal economic growth and/or fiscal and monetary stimulus has more of an effect on prices than any point in the last decade.

Bond markets do not see that happening. TIPS spreads say as much, and the Treasury market is among the most efficient in the world. In fact, this market is more worried about recession (witness the still paltry difference between 3 month and 10 year yields) and lower (not higher) price inflation.

Also worth noting: excluding the 1965-1970 experience when CPI inflation went from 1% to 6%, oil shocks are the proximate cause of every sudden ramp in core (ex-energy) consumer prices in the last 50 years. That was the case in 1974 (3% in 1973, 12% in 1975), 1979 (6% in 1978, 14% in 1980), and 1990 (4% in 1989, 6% at the start of 1991).

Our verdict: we simply cannot make a case for structurally higher inflation either in 2020 or the following several years. First, markets say it’s unlikely and investors already know about $1 trillion deficits, low unemployment, and positive catalysts like trade deals. Second, recent history (i.e. this year) exhibits little proof an inflection point is nigh. Lastly, the one thing that could shock the system into inflation – a sudden rise in oil prices – seems unlikely. That may not be a classic monetarist’s view of the world, but the data is clear enough.

Meltup Accelerates Into Christmas Break As Algos Run Wild In Illiquid Markets

After the decade’s last quad-witching came and went without any adverse incidents, and instead a massive short squeeze of the December Emini contract into its 930am Friday expiration repriced the entire market about 15 points higher…

… the relentless, QE4 inspired melt-up has only accelerated in today’s low volume session, as US equity futures pushed to fresh all time highs above 3,230…

… even as world stocks took a breather near record highs while currency and bond markets were little changed on Monday as trading volumes collapsed before the Christmas holiday.

On Friday, the S&P extended its record highs to seven straight sessions, its longest streak in more than two years, as all three major U.S. indexes – the S&P 500, Nasdaq and Dow – gained.

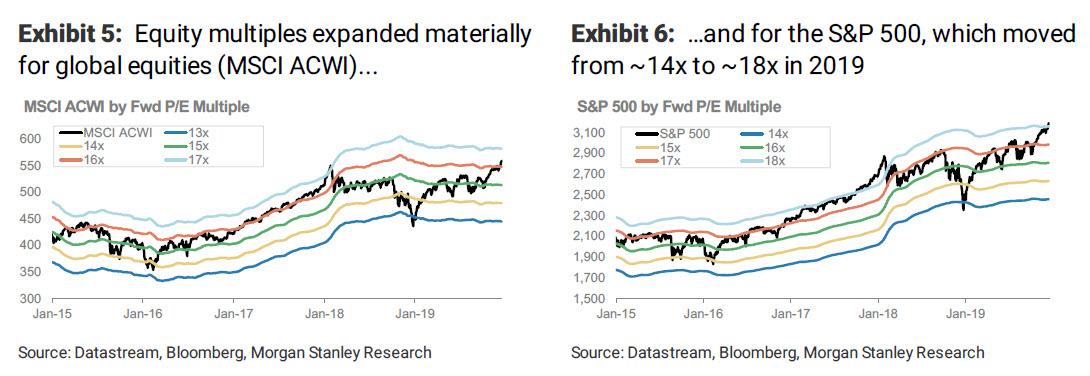

The MSCI ACWI index was flat, trading at Friday’s record high. It has risen nearly 3% this month as U.S.-China trade tensions eased and confidence grew that Britain would avoid a no deal exit from the European Union. The index is up 23% so far in 2019, set for its best year since 2009, with all of this upside thanks to multiple expansion as global earnings are down in 2019 compared to the prior year.

Trump did everything in his power to ensure a Monday spike after repeating – once again – on Saturday the United States and China would “very shortly” sign phase one a trade agreement, the same agreement he said in October would be signed in November. In response, China said on Monday it would lower tariffs on products ranging from frozen pork and avocado to some types of semiconductors next year.

“The Phase 1 (P1) agreement and UK elections have cleared up tail risks, but the market is now transcending that euphoria,” AxiTrader strategist Stephen Innes told Bloomberg. “While P1 is already reflected in stock prices, positioning is still relatively light, and with plenty of capital yet to be deployed, markets could even push significantly higher supported by the global growth rebound.”

The European Stoxx 600 index was flat, after starting off modestly lower before trading in positive territory. It hit a new record high in the Friday session.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan was near its highest since June 2018, up 0.05%, despite an unexpected hiccup in Chinese markets, where stocks posted their worst single-day drop in six weeks, weighed down by a correction in tech shares after a state fund announced plans to cut its stakes in some chip makers.

Asian shares were mixed with subdued volume ahead of the year-end holiday season. Health care stocks rose while material companies fell. The benchmark MSCI Asia Pacific Index was little changed, as gains in New Zealand stocks offset declines in China shares. The New Zealand Exchange 50 Gross Index jumped 0.6%, extending a new high on Monday, while China’s Shanghai Composite Index slumped 1.4% due to weak performance in financial shares. India’s S&P BSE Sensex Index dropped 0.3%. As we reported, on Monday the Chinese government said it will cut import tariffs for goods including frozen pork, pharmaceuticals, paper products and some high-tech components starting from Jan. 1, according to a statement from the Ministry of Finance.

As Bloomberg notes, all asset classes are on track for the best returns in a decade in 2019 after central banks around the world eased monetary policy.

“There is justification to say that the fundamentals are turning, but we haven’t seen confirmation in prices or data yet,” Kyle Rodda, an analyst at IG Markets Ltd., said on Bloomberg TV. “The risk is skewed to the upside, but I still think it’s a tentative picture at the moment.”

In FX markets, the euro was at $1.1083, up 0.05% after slipping 0.4% last week. Sterling tumbled again, sliding as low as 1,2930, a fresh 3 week low, extending its decline after seeing its worst week in more than two years. It remains on the back foot after U.K. Prime Minister Boris Johnson renewed hard-Brexit fears with an accelerated schedule for signing a trade deal with the European Union. It slid 2.6% last week for its worst weekly showing since October 2017. The safe-haven Japanese yen was down 0.08% at 109.35. And while the dollar was initially lower against most Group-of-10 peers in light holiday trading, it has since turned positive on the back of the pound’s latest mauling.

In commodities, Brent crude was down 23 cents to $65.95 a barrel. West Texas Intermediate crude slipped 24 cents to $60.2 a barrel, while gold rose to a 7 week high.

The U.S. personal consumption expenditure deflator for November, due on Friday, is the only major economic report this week.

Market Snapshot

S&P 500 futures little changed at 3,228.25

STOXX Europe 600 up 0.02% to 418.49

German 10Y yield fell 0.7 bps to -0.259%

Euro up 0.03% to $1.1082

Italian 10Y yield rose 2.4 bps to 1.237%

Spanish 10Y yield fell 0.7 bps to 0.436%

MXAP up 0.01% to 170.13

MXAPJ up 0.06% to 550.41

Nikkei up 0.02% to 23,821.11

Topix down 0.2% to 1,729.42

Hang Seng Index up 0.1% to 27,906.41

Shanghai Composite down 1.4% to 2,962.75

Sensex down 0.1% to 41,629.16

Australia S&P/ASX 200 down 0.5% to 6,785.14

Kospi down 0.02% to 2,203.71

Brent futures down 0.3% to $65.94/bbl

Gold spot up 0.4% to $1,484.27

U.S. Dollar Index little changed at 97.63

Top Overnight News from Bloomberg

China cut import tariffs on a wide range of goods including food, consumer items and parts for manufacturing smart-phones, continuing Beijing’s drive to lower trade barriers and spur domestic demand

Oil extended losses after the biggest decline in three weeks as Kuwait signaled a deal with Saudi Arabia to renew crude output along their border and as U.S. shale explorers increased drilling

One of Donald Trump’s top allies and his chief economic adversary are drifting closer, at least when it comes to trade

After money-laundering scandals involving hundreds of billions of euros rocked some of Europe’s biggest banks, the Baltic region has begun a fresh clampdown. This time, the target is payment-service providers

U.S. President Trump told Brazilian President Jair Bolsonaro he won’t reimpose tariffs on steel, aluminum from the Latin American nation, according to a person familiar

Satellite images show North Korea has added a structure to a factory linked to the production of intercontinental ballistic missiles, reports NBC News

Financial Times reports that traders at HSBC and JPMorgan Chase are among those who accessed a high-speed audio feed of Bank of England press conferences

Michel Barnier, European Commission chief negotiator for Brexit, says Britain must stick closely to Brussels’ standards on tax, state aid and environment to secure a trade deal with the bloc. Warns it will be “immensely challenging” to finish a deal by end of 2020 deadline, according to the Sunday Times

Asian equity markets traded somewhat mixed as the region once again failed to fully join in on the Christmas cheer which had propelled Wall Street to fresh record highs on Friday, with volumes light heading into the holidays. ASX 200 (-0.5%) and Nikkei 225 (+0.1%) were varied with Australia dragged by commodity-related losses and due to the adverse effects of its recent currency appreciation, while the Japanese benchmark remained afloat but with upside capped by an indecisive JPY and after Japanese Chief Cabinet Suga clarified that they have not eased export controls on South Korea. Hang Seng (+0.1%) and Shanghai Comp. (-1.4%) lacked conviction despite the announcement that China is to lower import tariffs for some products beginning January 1st and after the recent Trump-Xi call in which the leaders were said to have conducted a very good talk regarding the trade deal, although reports further noted that Chinese President Xi stated US interference is harming China’s interests and there were also downward revisions to November Chinese trade data including a wider contraction in Exports. Finally, 10yr JGBs languished firmly below the 152.00 level after the recent bear-flattening in USTs and with demand also dampened by the lack of BoJ presence in the market today.

Top Asian News

Warburg-Backed ESR Is Said to Mull REIT IPO of Korean Assets

SoftBank, Naver Hike Line Offer as Son Takes on Google, Amazon

Rescuers Sought for India Shadow Bank Altico as Crisis Deepens

India BJP Trails in State Poll Signaling More Woes for Modi

Tentative and mixed trade for European bourses in the final full session before Christmas [Euro Stoxx 50 -0.1%] following on from a similar APAC handover amid a lack of conviction and participants. In terms of YTD performance in Europe – FTSE MIB stands as the winner with YTD returns of just over 30% followed by the CAC 40 (+27.3%), DAX (+26.0%) and Euro Stoxx 50 (+25.7%) whilst IBEX 35 (+13.1%) and FTSE 100 (+12.8%) reside towards the bottom end of the spectrum. State-side, Nasdaq (+34.5%) leads the YTD gains followed by S&P 500 (+28.5%) and DJIA (+22.0%). Back to today’s session, FTSE 100 (+0.4%) outpaced peers as exporters benefit from a softer Sterling. Sectors also reflect an indecisive risk tone with no major standouts. In terms of individual movers: Bayer (+3.0%) rose to the top of the German index after the US government said the USD 25mln verdict on Co’s Roundup case should be reversed. Lufthansa (-1.3%) shares are pressured after talks with the German Union UFO fell through and strikes are imminent, albeit the union will refrain from strike action during the busy Christmas period. Meanwhile, GSK (-0.4%) drifted off lows but remains subdued after the US FDA declined to approve Co’s long acting HIV injections after the regulator questioned the treatment’s chemistry, manufacturing and controls process but not its safety. Finally, NMC Health (+28.5%) spiked higher at the open, and have continued to strengthen, after the Co. stated it will be commencing an independent third-party review to provide additional reassurances to shareholders after activist short-seller Muddy Waters questioned the integrity of NMC’s reports. Note: tomorrows session sees Eurex and all its derivatives closer whilst cash DAX will be shut all day – the rest of the cash bourses will see an early finish.

Top European News

Consilium Soars More than 200% on Unit Sale to Nordic Capital

Germany Expects Gas Pipeline Delay Before Completion in 2020

Neste Jumps on Reinstatement of U.S. Blender’s Tax Credit

Benettons’ Atlantia to Confront Italy Government on Road Reform

In FX, AUD/NZD – The Aussie and Kiwi are still outpacing their G10 rivals and jostling for top spot in the major stakes having made firmer breaches of big figures against their US counterpart, with Aud/Usd up to 0.6920 and Nzd/Usd reaching 0.6625. Both have benefited from a mixture of short covering and technical buying after recent relatively upbeat data that has reduced or rolled back RBA/RBNZ rate cut expectations. In terms of next bullish chart targets, 0.6939 looms as long as the pair holds/closes above the 200 DMA (circa 0.6905) and 0.6636 respectively.

CHF/GBP – The Franc is in bronze position and eyeing 0.9800 vs the Buck as latest weekly Swiss sight deposits suggest less active currency intervention and the Greenback drifts down from best levels generally (DXY dipping within a narrow 97.708-578 range) amidst even thinner seasonal volumes and a softer/flatter Treasury yield curve. Similarly, Sterling is trying to take advantage of the Dollar’s dip and attempting to keep hold or sight of the 1.3000 level even though no deal Brexit risks have risen with the passing of the 1st parliament vote on PM Johnson’s WAB that includes a no transition delay clause.

EUR//JPY/CAD – All more narrowly mixed against the Usd, with the single currency mired between 1.1074-88 parameters, Yen meandering from 109.35-53 and Loonie pivoting 1.3150 ahead of Canadian GDP for the month of October that is forecast to be flat, but could disappoint given a string of bleak data since this month’s BoC meeting. Back to Eur/Usd, some option expiry interest could impact in the absence of anything else and the aforementioned quiet pre-Xmas trade, as almost 1 bn rolls off at 1.1070 and from 1.1100-10.

SCANDI/EM – The Swedish Crown has slipped after another test of resistance near 10.4150 against the Euro failed to propel the Sek higher, but its Norwegian peer is extending gains through 10.0000 towards 9.9150 on the back of the Norges Bank’s gently inclined depo rate path. Elsewhere, EMs are largely going through the motions in tight bands vs the Dollar.

In commodities, the energy complex remains flat/subdued amid holiday-thinned conditions after a lacklustre Asia session in light of a number of bearish supply-side factors including Friday’s increase in active rigs reported via the Baker Hughes rig count coupled with reports of a Saudi-Kuwaiti agreement to renew oil output in the shared neutral zone by year-end. WTI futures hover just above the USD 60/bbl mark whilst its Brent counterpart retains USD 66/bbl+ status at time of writing. Russian Energy Minister Novak failed to provide the complex with much impetus in early EU trade despite noting that the OPEC+ could discuss deeper oil output cut quotas at its March meeting (5th/6th) in 2020. This follows this month’s policy revision in which the cartel agreed to deeper cuts of 496k BPD starting from Q1 2020, with an extraordinary meeting in March for a review. Elsewhere, gold trades on a firmer footing with the yellow metal hovering around current session highs of ~USD 1485/oz ahead of reported trend-line resistance at ~USD 1487/oz. Copper also garnered some support from the initially softer Dollar with prices re-eying USD 2.80/lb to the upside, although the red metal’s 100 WMA rests just below the round figure at USD 2.7988/lb. Finally, Dalian iron ore rose in excess of 1.0% after key steelmaking cities in Northern China issued pollution alerts as air quality in the region deteriorates.

UIS Event Calendar

8:30am: Durable Goods Orders, est. 1.5%, prior 0.5%; Durables Ex Transportation, est. 0.2%, prior 0.5%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.2%, prior 1.1%; Cap Goods Ship Nondef Ex Air, est. 0.0%, prior 0.8%

8:30am: Chicago Fed Nat Activity Index, est. -0.3, prior -0.7

10am: New Home Sales, est. 730,000, prior 733,000; New Home Sales MoM, est. -0.41%, prior -0.7%

5 Sentenced To Death For Murder Of Saudi Dissident Jamal Khashoggi; Royal Aids Go Free

The criminal trials of the 11 patsies men formally accused of participating in the killing and dismemberment of Saudi dissident Jamal Khashoggi are now over, and the end result was exactly what most expected.

That is, several royal aids implicated in the killing were let go without punishment, while five others who are probably only tangentially related to the case (if at all) have been sentenced to death.

And in Saudi Arabia, a sentence of death means only one thing: A very public beheading.

According to Bloomberg, the Saudi court said it didn’t have enough evidence to convict two top officials who are close to Crown Prince Mohammad bin Salman of any involvement in the crime.

Meanwhile, three of the 11 men were given a total of 24 years in prison, according to a statement from the Saudis that was read out loud at the public prosecutor’s office on Monday after the sentences had been handed down.

Jamal Khashoggi

Two senior figures who were fired from their posts in the wake of the scandal, which briefly strained Saudi Arabia’s relations with allies around the world, but particularly in the West (and prompted Wall Street and corporate America to skip MBS’s “Davos in the Desert” conference in 2018, though they returned the following year) were cleared of all wrongdoing.

Saud al-Qahtani, removed from his role as a top adviser to Prince Mohammed after the killing, was interrogated by Saudi investigators, but no evidence was ever found against him, according to Deputy Attorney General Shalaan Shalaan. Ahmed Alassiri, a top intelligence official, was also removed from his position. Both men were found not guilty by the court.

Most of those arrested in relation to Khashoggi’s murder inside the Saudi consulate in Istanbul will eventually go free, but most members of the global community expected that. Most doubted the process from the beginning, and figured the Saudis would allow the men truly responsible for masterminding Khashoggi’s murder walk free, while saddling a group of patsies with death sentences.

After all, the CIA is reportedly convinced that MbS himself ordered Khashoggi’s killing, and that members of the “death squad” who carried it out were hand-picked by some of the Crown Prince’s closest aids.

A UN special report even claimed that Saudi agents were recorded by Turkish intelligence discussing how to dismember Khashoggi’s body, and even referred to KHashoggi as a “sacrificial lamb” before he entered the consulate, undermining the kingdom’s claims that the murder wasn’t part of the original plan. Though most doubted that explanation from the beginning.

What did Khashoggi do to make MbS so angry? Other than writing his moderately critical op-eds, it’s not exactly clear.

Khashoggi was once a government insider, but he became a staunch critic of the royal family after leaving the country and settling in Virginia back in 2017, where he began occasionally writing columns for the Washington Post, where he was edited by Karen Attiah.

According to the FT, the trial began in January, and nine sessions were held before Monday’s sentencing. Representatives of the Turkish government, Saudi human rights groups and the five permanent members of the UN Security Council were allowed to attend the trial, which was otherwise closed to the public.

It’s not clear when the death sentences will be carried out.

China To Cut Tariffs On Pork, Tech And Many Global Imports It Desperately Needs

After a phase one trade deal with the US, China said on Monday that it would slash import tariffs on a wide range of goods from around the world to boost domestic consumption. As Bloomberg reported, the Ministry of Finance published a list outlining 859 products that will be subjected to lower tariffs, some of those items include food, consumer goods, and high-tech parts for electronics.

One of the most critical items on the list is pork, which will be imported in more significant amounts come early January to lower domestic spot prices that have hyperinflated in late 2019. Increasing pork imports will also allow the government to rebuild the pork cold storage inventory that was depleted thanks to the outbreak of African swine fever that decimated the country’s pig herds.

The list also includes pharmaceutical ingredients, avocados, orange juice, and seafood, as China’s middle-class, some of the wealthiest in the world, demand more expensive products.

Bloomberg notes that 2018 imports of the listed items were about $389 billion, or about 18% of China’s total imports of $2.14 trillion. And since tariffs are merely a tax on its consumers, what Beijing has just done is stimulate domestic consumption for an economy where GDP is set to hit a new sub 6% record soon.

That said, China will likely spin the tariff cuts as “generous concessions” to the US, but as we’ve explained before, China isn’t going to source from the US entirely. Chinese importers will gravitate to areas of the world where products are the most affordable. For example, Chinese importers of farm products ditched US farmers for ones in South America because of the exchange rate and lower spot prices on soybean and pork.

Translation: China cutting tariffs on stuff it desperately needs, will try to spin it as concession toward US https://t.co/dfcXgU7GRZ

“The move in lowering import tariffs reflects that the government wants to reaffirm its stance to the world on freer trade amid the trade war,” said Gary Ng, an economist at Natixis in Hong Kong. “Domestically, lowering import tariffs are helpful in reducing business and consumer costs.”

Monday’s tariff cuts hint that China’s economy continues to decelerate rapidly, and the government is scrambling to boost domestic consumption. And while China will try to use the tariff reduction as ammo to push the US for tariff cuts of its own, there’s little evidence that Chinese importers will source the new imports from the US.

We don’t normally associate Republican lawmakers with former Mexican leaders. But similar to the way many Latin American ex-presidentes suddenly discover an interest in legalizing marijuana once safely out of office, GOP members of Congress have an uncanny way of finding reasons to oppose Donald Trump right around the time they announce retirement.

Rep. Francis Rooney (R–Fla.) on October 19 became the 21st Republican member of the 116th Congress—compared to just seven Democrats at the time and nine as of press time—to announce that he will not seek that which politicians otherwise live for: re-election. The move came precisely one day after the southwest Floridian became the first current member of the House Republican caucus to declare openness to impeaching the president over the question of whether he made delivery of authorized aid money to Ukraine contingent on the newly elected president there announcing a possible investigation into 2020 Democratic presidential frontrunner Joe Biden.

“It’s painful to me to see this kind of amateur diplomacy, riding roughshod over our State Department apparatus,” Rooney, a member of the House Foreign Affairs Committee, told The New York Times. “I want to get the facts and do the right thing, because I’ll be looking at my children a lot longer than I’m looking to anybody in this building.”

Ten days later, Rep. Greg Walden (R–Ore.) became the 22nd Republican to announce retirement. The first Republican congressman to back an impeachment inquiry, self-described libertarian Rep. Justin Amash (I–Mich.), became a non-Republican within two months of that announcement, and at the end of October he was the only non-Democratic member of the House to back an impeachment investigation. Meanwhile, the growing number of premature retirees have been among the loudest in expressing alarm at the murky Ukraine-related behavior first made public by a CIA whistle-blower.

“There is a lot in the whistleblower complaint that is concerning,” Rep. Will Hurd (R–Texas), a former rising GOP star, tweeted September 26, seven weeks after announcing his own non-re-election. “We need to fully investigate all of the allegations addressed in the letter.”

It’s not just on substance that self-liberated Republicans dissent from a president who is often more popular among their constituents. They also tend to object much more bluntly than their remaining colleagues to Trump’s style, such as his statement that four House Democratic women of color should “go back” to their home countries, even though three of them were born in the United States.

“We’re here for a purpose—and it’s not this petty, childish bullshit,” Rep. Paul Mitchell (R–Mich.), prompted by the “go back” episode, told The Washington Post six weeks after his own surprise decision not to run again.

In one sense, the spike in Republican self-deportations—44 and counting in the House alone since Trump’s inauguration, compared to 25 Democrats during Barack Obama’s entire first term—is a boon to Trump, since it helps him shape the party more in his idiosyncratic image. Sen. Marsha Blackburn (R–Tenn.), the former vice chair of the president’s transition team, is a good deal more Trumpy than the man she replaced in the upper chamber, frequent presidential critic Bob Corker.

But retiring Republicans in swing districts and states also have a tendency to be replaced by Democrats, as happened in Arizona after Sen. Jeff Flake left Capitol Hill. And that might be the vulnerability most likely to sink this presidency. Trump’s fate seems likely to be in the hands of the Senate, presuming the Democrat-run House approves articles of impeachment. Support for the president in the 53-member Senate GOP caucus has been wide but not deep, with Sen. Mitt Romney (R–Utah) in particular criticizing Trump’s Ukraine gambits. And another three Republican senators will not be seeking re-election in 2020, freeing them up to speak openly if they choose.

Anyone who has bet on GOP lawmakers to meaningfully oppose the president has already lost a lot of money. And there is one anti-impeachment argument that may persuade even the most ardent anti-Trump Republicans: Removing a president in an election year seems much less politically wise than letting voters decide for themselves how his first term should be rewarded.

Republican senators may be damned either way. As of press time, public support for impeachment and disapproval of Trump’s presidency were reaching all-time highs. Sometimes the safest place to be in a firefight is far away from the front lines.

from Latest – Reason.com https://ift.tt/2ShQF9t

via IFTTT

We don’t normally associate Republican lawmakers with former Mexican leaders. But similar to the way many Latin American ex-presidentes suddenly discover an interest in legalizing marijuana once safely out of office, GOP members of Congress have an uncanny way of finding reasons to oppose Donald Trump right around the time they announce retirement.

Rep. Francis Rooney (R–Fla.) on October 19 became the 21st Republican member of the 116th Congress—compared to just seven Democrats at the time and nine as of press time—to announce that he will not seek that which politicians otherwise live for: re-election. The move came precisely one day after the southwest Floridian became the first current member of the House Republican caucus to declare openness to impeaching the president over the question of whether he made delivery of authorized aid money to Ukraine contingent on the newly elected president there announcing a possible investigation into 2020 Democratic presidential frontrunner Joe Biden.

“It’s painful to me to see this kind of amateur diplomacy, riding roughshod over our State Department apparatus,” Rooney, a member of the House Foreign Affairs Committee, told The New York Times. “I want to get the facts and do the right thing, because I’ll be looking at my children a lot longer than I’m looking to anybody in this building.”

Ten days later, Rep. Greg Walden (R–Ore.) became the 22nd Republican to announce retirement. The first Republican congressman to back an impeachment inquiry, self-described libertarian Rep. Justin Amash (I–Mich.), became a non-Republican within two months of that announcement, and at the end of October he was the only non-Democratic member of the House to back an impeachment investigation. Meanwhile, the growing number of premature retirees have been among the loudest in expressing alarm at the murky Ukraine-related behavior first made public by a CIA whistle-blower.

“There is a lot in the whistleblower complaint that is concerning,” Rep. Will Hurd (R–Texas), a former rising GOP star, tweeted September 26, seven weeks after announcing his own non-re-election. “We need to fully investigate all of the allegations addressed in the letter.”

It’s not just on substance that self-liberated Republicans dissent from a president who is often more popular among their constituents. They also tend to object much more bluntly than their remaining colleagues to Trump’s style, such as his statement that four House Democratic women of color should “go back” to their home countries, even though three of them were born in the United States.

“We’re here for a purpose—and it’s not this petty, childish bullshit,” Rep. Paul Mitchell (R–Mich.), prompted by the “go back” episode, told The Washington Post six weeks after his own surprise decision not to run again.

In one sense, the spike in Republican self-deportations—44 and counting in the House alone since Trump’s inauguration, compared to 25 Democrats during Barack Obama’s entire first term—is a boon to Trump, since it helps him shape the party more in his idiosyncratic image. Sen. Marsha Blackburn (R–Tenn.), the former vice chair of the president’s transition team, is a good deal more Trumpy than the man she replaced in the upper chamber, frequent presidential critic Bob Corker.

But retiring Republicans in swing districts and states also have a tendency to be replaced by Democrats, as happened in Arizona after Sen. Jeff Flake left Capitol Hill. And that might be the vulnerability most likely to sink this presidency. Trump’s fate seems likely to be in the hands of the Senate, presuming the Democrat-run House approves articles of impeachment. Support for the president in the 53-member Senate GOP caucus has been wide but not deep, with Sen. Mitt Romney (R–Utah) in particular criticizing Trump’s Ukraine gambits. And another three Republican senators will not be seeking re-election in 2020, freeing them up to speak openly if they choose.

Anyone who has bet on GOP lawmakers to meaningfully oppose the president has already lost a lot of money. And there is one anti-impeachment argument that may persuade even the most ardent anti-Trump Republicans: Removing a president in an election year seems much less politically wise than letting voters decide for themselves how his first term should be rewarded.

Republican senators may be damned either way. As of press time, public support for impeachment and disapproval of Trump’s presidency were reaching all-time highs. Sometimes the safest place to be in a firefight is far away from the front lines.

from Latest – Reason.com https://ift.tt/2ShQF9t

via IFTTT

Boris Johnson has only been back in Downing Street a few days following his stunning victory in Britain’s general election, but there are already early signs that his premiership will preside over a dramatic revival in transatlantic relations not seen since the heyday of Ronald Reagan and Margaret Thatcher.

First and foremost, the British prime minister has made it abundantly clear that his first priority will be to break the Brexit deadlock that has effectively paralysed British politics, and the country’s ability to make its voice heard on the international stage, at the earliest possible opportunity, thus opening the way for a trade deal with Washington.

As a start, Mr Johnson has committed his new government to fulfil its election pledge to complete Britain’s withdrawal from the European Union by the end of January. Furthermore, he will enshrine in law his promise that the complicated trade negotiations that are due to take place next year to finalise Britain’s future trading relationship with the EU bloc will be completed by the end of 2020.

Critics of Mr Johnson’s ambitious programme to free Britain from the EU’s shackles and negotiate a new network of global trade deals have argued that completing the process of establishing a new trading framework with the EU will take much longer than a year, especially in view of the EU’s notoriously slow approach to completing such transactions. The critics point out, for example, that the Canada-EU trade deal took seven years to negotiate and was 22 years in the making.

By enshrining Britain’s ultimate departure date in law, Mr Johnson has effectively silenced those critics, as well as sending a clear declaration of intent to Brussels that Britain aims to complete the withdrawal process by the end of next year, with or without a deal.

The fact, moreover, that Mr Johnson now enjoys a comfortable majority of 80 seats in the newly-constituted House of Commons means that he will no longer be subjected to procedural legislative obstructions from die-hard Remainers, as was very much in evidence during the death throes of the last parliament.

Thus Mr Johnson’s reinvigorated Conservative Party finds itself in a position to shape Britain’s destiny for the foreseeable future, with rebuilding relations between Washington and London seen as being one of Mr Johnson’s first priorities.

During the tenure of Theresa May, Mr Johnson’s hapless predecessor as prime minister, relations between Downing Street and the White House became strained, to say the least. As one senior former member of Donald Trump’s foreign policy team recently told me, “By the end of Mrs May’s premiership relations with the US had fallen to an all-time low”.

The first indication of a revival in relations between Washington and London came when Mr Trump was one of the first world leaders to congratulate Mr Johnson on his historic win — he secured the largest Conservative majority since Mrs Thatcher’s third election victory in 1987 — and immediately promised to strike a “massive” new trade deal with the UK post-Brexit. The US president said a future US-UK trade agreement has “the potential to be far bigger and more lucrative” than any deal that could have been made with the EU.

Indeed, with Mr Johnson assured of being Britain’s prime minister for the next five years, and Mr Trump well-placed to secure re-election in next year’s presidential election contest, there is every prospect that the two leaders could herald a new golden era of transatlantic relations not seen since the alliance of Mrs Thatcher and US President Ronald Reagan in the 1980s.

There will, of course, be numerous political obstacles that will have to be overcome regarding issues where the two men have opposing views, such as the controversial nuclear deal with Iran. While Mr Trump is determined to pressure Tehran with punitive economic sanctions, Mr Johnson still remains committed to working with other European powers, such as France and Germany, to save the nuclear deal.

Yet, compared with the calamitous impact a victory for Labour Party leader Jeremy Corbyn, whose politics is defined by his visceral anti-Americanism, would have had on transatlantic relations, Mr Johnson’s return to Downing Street will have been greeted with enormous relief in the White House, as it means Washington now has a firm ally in London, someone who is committed to breathing new life into the vital and long-standing partnership between Britain and America.

Chinese state TV pulled a scheduled broadcast of a Premier League soccer match between Arsenal and Manchester City after Arsenal midfielder Mesut Ozil tweeted criticism of China’s treatment of its Uighur Muslim minority and the silence of Muslims outside China. “Qurans are burned, mosques were closed down, Islamic theological schools, madrasas were banned, religious scholars were killed one by one. Despite all this, Muslims stay quiet,” he wrote.

from Latest – Reason.com https://ift.tt/2Q5E9XS

via IFTTT