BET Founder Says 2020 Election Is “Trump’s To Lose”

Millions of Americans slept in on Friday morning after spending the early morning hours battling their way to the front of the line to take advantage of those sweet, sweet Black Friday deals.

Meanwhile, CNBC interrupted its coverage of the holiday sales madness to bring Robert Johnson, the founder of BET, on for an interview with Hadley Gamble. Johnson is no stranger to CNBC: He appears every few months, usually to discuss how the mainstream media distorts minorities and their view of President Trump.

Though he didn’t dwell on whether he voted for Trump, Johnson insisted that the media has the narrative wrong, and that plenty of minorities – the target audience for BET (Black Entertainment Television) – actually like Trump (despite the insistence of Wealthy White Liberals that he has no support among communities of color) because of the president’s abrasive style.

“I think the president has always been in a position where it’s his to lose, based on the fact that he’s bringing a disruptive force into what would be considered political norms, whether it’s the way he conducts foreign policy, the way he takes on the government agencies and the way he takes on immigration – he brings his style. And a lot of people who voted for him like this style.”

Looking ahead to the 2020 vote, Johnson warned the Dems who are still jousting for the nomination not to focus so much on Trump’s style (i.e. what he says and what he tweets) but instead to focus on his actual policy decisions (tax cuts for the wealthy, stepped-up deportations), which Johnson believes are far less popular.

“What Democrats need to be careful about is to not focus on stylistic Trump, but to focus on substantive Trump,” Johnson said.

But at the end of the day, Johnson wouldn’t be surprised to see Trump steamroll the Dems once again (though he lost the popular vote in 2016, he won the electoral college by a substantial margin) because Trump has a special ability to dominate a news cycle – something that no other politician can accomplish.

These skills apparently take time to develop, since Trump has been working the media to his advantage since the late 1970s.

Meanwhile, there’s one pitfall that Dems must avoid: Accusing Trump’s supporters of being racists and bigots.

“His ability to dominate the news cycle and get the narrative going about what he said to me has sort of a double effect on the Democrats. First they get all agitated about what he said, then they extend that to the voters.”

“What they’re doing is they simply adding to his support by saying ‘Trump is bad, and if you support Trump, then you’re bad’ – which is a really silly way to talk to the American people.”

It might seem like common sense to the rest of us, but labeling nearly half the country as a bunch of evil nazi bigots is clearly not the best strategy for winning over the hearts and minds. Yet, that’s what many on the far-left flank of the Democratic Party would like to see happen.

British banking giant HSBC plans to move $20 billion worth of assets to Digital Vault, a new blockchain-based custody platform by March 2020. By deploying the platform, the global investment bank aims to digitize paper-based records of private placements in order to increase standardization and speed up processes in the growing industry, Reuters reports Nov. 27.

HSBC reportedly expects the global volumes of private placements to surge 60% from 2017 to hit $7.7 trillion by 2022. The bank could not estimate how much the platform will save for the company or its clients, Reuters states.

HSBC to help investors track securities on private markets in real-time

Specifically, the Digital Vault platform will purportedly allow investors to track securities bought on private markets in real-time.

As private placements are usually conducted on paper, its processes are often associated with a lack of standardization, while access to documentation can be complicated and time-consuming. By deploying blockchain, the company hopes to reduce the time needed to make queries on holdings by investors.

No major savings in the first 18 months

While HSBC has not provided any estimations for the potential outcomes of adopting the platform, an independent blockchain expert suggested major savings would be unlikely during the first stages of the project.

Windsor Holden, an independent consultant who tracks blockchain and cryptocurrencies, told Reuters that he does not expect to see savings from increased efficiency in the first year to 18 months.

Private placement in the crypto and blockchain industries

Private placements are funding rounds of securities which are sold not through a public offering, but through a private offering. Private placement is considered to be an option to an initial public offering for a company looking to raise capital for expansion.

In July 2019, American digital asset management fund Grayscale Investments resumed private placement of Grayscale Bitcoin Trust shares, allowing investors to put money in Bitcoin (BTC) using a traditional investment structure.

The Trust private placement is offered on a periodic basis throughout the year to accredited investors for daily subscription. Previously, South Korea’s messaging app operator Kakao Corp. revealed its plans to offer a private placement to attract investors to develop their blockchain subsidiary.

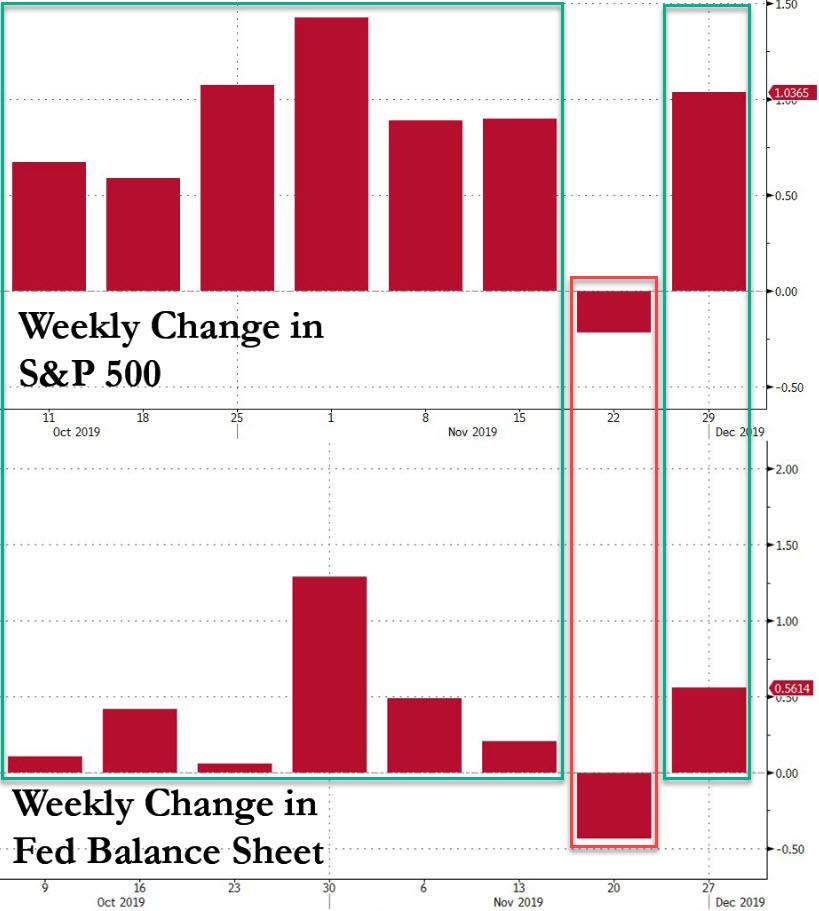

QE Or Not QE? Here Is The Market’s Answer In One Simple Chart

After a month of constant verbal gymnastics by the Fed – and its army of sycophants who can’t think creatively or originally and merely parrot their echo chamber in hopes of a blue checkmark and likes/retweets – that the recent launch of $60 billion in T-Bill purchases is anything but QE (whatever you do, don’t call it “QE 4”, just call it “NOT QE” please), two weeks ago one bank finally had the guts to say what was so obvious to anyone who isn’t challenged by simple logic: the Fed’s “NOT QE” is really “QE.”

As we reported on November 15, in a note warning that the Fed’s latest purchase program – whether one calls it QE, QE4, QE ∞ or NOT QE – will have big, potentially catastrophic costs, Bank of America’s Ralph Axel wrote that in the aftermath of the Fed’s new program of T-bill purchases to increase the amount of reserves in the banking system, the Fed made an effort to repeatedly inform markets that this is not a new round of quantitative easing, and yet as the BofA strategist notes, “in important ways it is similar.”

But was it QE? Well, in his October FOMC press conference, Fed Chair Powell said “our T-bill purchases should not be confused with the large-scale asset purchase program that we deployed after the financial crisis. In contrast, purchasing Tbills should not materially affect demand and supply for longer-term securities or financial conditions more broadly.” Chair Powell also gave a succinct definition of QE as having two basic elements: (1) supporting longer-term security prices, and (2) easing financial conditions.

Here’s the problem: as we have said since the beginning, and as Bank of America wrote, “the Fed’s T-bill purchase program delivers on both fronts and is therefore similar to QE,” with one exception – the element of forward guidance.

The upshot to this attempt to mislead the market what it is doing according to Bank of America, is that:

the Fed is continuing to “ease” even though rate cuts are now on hold, which is supportive of growth, higher interest rates and higher equities, and

the Fed is loosening financial conditions by increasing the availability of, and lowering the cost of, leverage, which broadly supports asset prices potentially at the cost of increasing systemic financial risk.

And while we have repeatedly argued why we think that, stripped of all its semantic veneer, the Fed’s latest asset purchase program is, in fact, QE, BofA effectively confirmed why we are right.

Which brings up a tangential, if just as important question: Why is the Fed so concerned about not signaling QE, and why are so many Fed fanboys desperate to parrot whatever Powell is saying day after day? Simply said, there are several reasons why the Fed is making a great effort to let the world know that its security purchases are not QE and are not reflective of any change in monetary policy stance.

The first is the obvious issue of signaling concern around the economic outlook which would run counter to its cautiously optimistic and often upbeat assessment. After all, why do QE if the economy has “never been stronger”, and the Fed was hiking rates as recently as a December. Included here are the concerns about running out of ammunition at the zero lower bound of rate policy. With negative rates increasingly off the table – until push comes to shove of course and the Fed is forced to join the ECB, BOJ and SNB in going subzero – QE is meant to be reserved as dry powder for a rainy day when conventional tools are exhausted (even if QE is in fact taking place this very instant).

A less obvious concern for the Fed is connecting monetary policy to bank demand for Fed liabilities, which as BofA admits, “is not something that fits neatly within its dual mandate”: last January, the Fed made a “momentous decision” to run an “abundant reserve regime” also known as a floor system, where the central bank decided not to return to its pre-crisis days of zero excess reserves. As such, the central bank now views the proper level of excess reserves (a Fed balance sheet liability) not in terms of its dual mandate for inflation and employment, but in terms of how banks prefer to meet regulatory liquidity requirements and how this preference impacts repo and other markets.

In short, the Fed’s dual mandate has been replaced by a single mandate of promoting financial stability (or as some may say, boosting JPMorgan’s stock price) similar to that of the ECB.

Here BofA ominously added that “by deciding to dynamically assess bank demand for reserves and reduce the risk of air pockets in repo markets, we believe the Fed has entered unchartered territory of monetary policy that may stretch beyond its dual mandate.” And the punchline: “By running balance-sheet policy to ensure overnight funding markets remain flush, the Fed is arguably circumventing the most important brake on excess leverage: the price.“

So if NOT QE is in fact, QE, and if the Fed is once again in the price manipulation business, what then?

According to BofA’s Axel, the most worrying part of the Fed’s current asset purchase program is the realization that an ongoing bank footprint in repo markets is required to maintain control of policy rates in the new floor system, or as we put it less politely, banks are now able to hijack the financial system by indicating that they have an overnight funding problem (as JPMorgan very clearly did) and force the Fed to do their (really JPMorgan’s) bidding.

While it is likely that beyond year-end, the additional tens of billions in reserves will have the required soothing effect, what is less clear is that the Fed can make sure the bank repo lending footprint is resilient to dips in the bank credit cycle.

And this is where BofA’s warning hits a crescendo, because while repo is fully collateralized and therefore contains negligible counterparty credit risk, “there may be a situation in which banks want to deleverage quickly, for example during a money run or a liquidation in some market caused by a sudden reassessment of value as in 2008.”

Got that? Going forward please refer to any market crash as a “sudden reassessment of value”, something which has become impossible in a world where “value” is whatever the Fed says it is… Well, the Fed or a bunch of self-serving venture capitalists, who pushed the “value” of WeWork to $47 billion just weeks before it was revealed that the company is effectively insolvent the punch bowl of endless free money is taken away.

To Bank of America, this new monetary policy regime actually increases systemic financial risk by making repo markets more vulnerable to bank cycles. This, as the bank ominously warns, “increases interconnectedness, which is something regulators widely recognize as making asset bubbles and entity failures more dangerous.“

Think of this as Europe’s infamous “doom loop”, only in the US and instead of linking bank equity values with the price of sovereign debt, it uses repo as a risk intermediary – one which is both used to grease the financial system, and which henceforth will also be an indicator of systemic bank stress.

In short, not only is the Fed pursuing QE without calling it QE, but by doing so it is implicitly raising the odds – more so than if it simply did another QE and rebuilt reserves to abour $4.5 trillion or more by purchasing coupon bonds – of another market crash.

It was, however, BofA’s conclusion that we found most alarming: as Axel writes, in his parting words:

“some have argued, including former NY Fed President William Dudley, that the last financial crisis was in part fueled by the Fed’s reluctance to tighten financial conditions as housing markets showed early signs of froth. It seems the Fed’s abundant-reserve regime may carry a new set of risks by supporting increased interconnectedness and overly easy policy (expanding balance sheet during an economic expansion) to maintain funding conditions that may short-circuit the market’s ability to accurately price the supply and demand for leverage as asset prices rise.“

In retrospect, we understand why the Fed is terrified of calling the latest QE by its true name: one mistake, and not only will it be the last QE the Fed will ever do, but it could also finally finish what the 2008 financial crisis failed to achieve, only this time the Fed will be powerless to do anything but sit and watch.

The reason we bring up this especially critical topic again today, is because we now have almost two full months of data since the start of NOT QE, which IS QE, and which conveniently gives us a snapshot of how the market – not we, not Bank of America, not pro or anti-Fed pundits – are responding to the expansion in the Fed’s balance sheet, which between repos, term repos, and permanent open market operations, has grown by $293 billion in just under the past three months.

The simple answer is the following: whether one wants to call it QE or not QE, ever since the Fed announced on Oct 11 that it would start purchasing $60 billion in T-Bills each month until “at least into the second quarter of 2020” – being careful to note that “these actions are purely technical measures to support the effective implementation of the FOMC’s monetary policy, and do not represent a change in the stance of monetary policy“, i.e., this is not QE, the Fed’s balance sheet has grown for 7 out of 8 weeks.

The market’s response? Just like during the POMO days of QE1, QE2, Operation Twist, and QE3, stocks have risen on every single week when the Fed’s balance sheet increased, following the three weeks of declines that led to the October 11 announcement. What about the one week when the Fed’s balance sheet shrank? That was the only week in the past two months since the launch of “NOT QE” when the S&P dropped.

So while Fed watchers, pundits, strategists, rank amateurs and virtually anyone else can debate whether or not what the Fed is doing is or is not QE, the market has made up its mind: if the balance sheet is rising, so are stocks, and vice versa. And since only POMO matters – so to speak – as it did back in the days of QE1 through QE3, we will do what we did back then, and list a schedule of all the upcoming days in which the Fed conducts liquidity injections – regardless of how one wants to call them (the latest schedule can always be found on the following page).

One final point for all those who despite the above, will still claim that just because the Fed is not purchasing coupon Treasuries, and thus is not changing either the duration of securities in the open market or investor risk preference, it is not, not, not QE, here is a snippet of what JPMorgan’s Nikolaos Panagirtzoglou wrote in his latest Flows and Liquidity newsletter:

… we see the Fed likely to conduct some of its balance sheet expansion next year via Treasuries.

Translation: some time in 2020, the Fed will stop pretending it is “NOT” QE.

Living on the opposite side of the world to the USA I am obliged to follow American politics as a stone thrown into the Washington swamp sends ripples that reach this far.

With less than a year to go until the next presidential election it is time to assess the current political landscape.

Trump of course is the focus of massive media noise. This must be ignored if a rational analysis is to be produced. 2016 proved that opinion polls must also be ignored.

As things stand today Trump holds the following chips in his stack:

He is the incumbent

The official employment numbers are in his favor

The official economic numbers are in his favor

His Republican approval is over 90%

His Hispanic/black approval ratings are at record levels for a Republican

He has made a dent in the illegal immigration problem

He has not started any new wars

Both Trump and the RNC are raking in record amounts of campaign cash

He will have the vote of most people with a 401(k) account

He will have the vote of most people in the military

He is in control of the social media narrative

He pushed the concept of the deep state and fake news into the mainstream

Democrat controlled cities are clearly in serious decline

He forced the DNC to defend their lunatic far left fringe and embrace their views

He forced the Democrats into the farcical impeachment process

The Democrats have little cash on hand

The Democrats do not have a viable policy platform

The Democrats do not currently have a viable contender for the nomination

Probably the most important fact we have learned since the election of Trump is that the deep state does exist in America and that it is a massively powerful hand on the tiller of American policy.

It has also become abundantly clear that this faction was strongly opposed to the policies Trump ran on in 2016 and that they have tried to impede him ever since he announced his candidacy. It is not unreasonable to conclude that this faction does not wish Trump to win re-election.

The question then becomes how far are they prepared to go in stopping him.

1. The most obvious way to stop Trump would be at the the ballot box. However, given the factors outlined above this is a long shot bet. None of the declared Democrat candidates can beat him. Hillary Clinton would fail again. A Republican cannot unseat him. Obama has been keeping a very low profile, it is possible that his wife Michelle could win, if she could be persuaded to run. Oprah?

2. What would turn the world of Trump upside down would be a financial crisis of a similar magnitude to 2008, or a major dollar collapse (Putin said last week the dollar would collapse soon). If there were a consensus among the deep state to take such action it would be incredibly easy for them to achieve given the highly unstable fabric of markets today.

The corporate credit markets could be pushed into panic by Jamie Dimon alone if he wished such an outcome and had the blessing of his buddies. Indeed, the cynic might argue that the groundwork has been laid since the start of the repo problem in mid September and the launching of QE4. Last time around the patsie was Lehman, has Deutsche Bank been singled out to take the fall this time? Time is running short for this to be an option, a crisis must be in play by spring next year to stymie the Orange Man.

3. The third way Trump could be stopped does not bear thinking about but it happened before to JFK 56 years ago.

Epstein did not kill himself.

* * *

The corrupt establishment will do anything to suppress sites like the Burning Platform from revealing the truth. The corporate media does this by demonetizing sites like mine by blackballing the site from advertising revenue. If you get value from this site, please keep it running with a donation. [Jim Quinn – PO Box 1520 Kulpsville, PA 19443] or Paypal

Newsweek Reporter Fired After Peddling Fake News That Trump Golfed On Thanksgiving

Newsweek has fired a reporter who penned a snarky, misleading article suggesting that President Trump spent Thanksgiving ‘tweeting and golfing,’ when he actually flew to Afghanistan for a surprise visit with US troops.

The fired journo, Jessica Kwong, wrote in an article entitled “How is Trump Spending Thanksgiving? Tweeting, Golfing and More,” that the president “has been spending his Thanksgiving holidays at his Mar-a-Lago resort in Palm Beach, Florida.”

The golfing claim comes later in the article, as Kwong notes that Trump played golf on Thanksgiving Eve “from mid-morning to mid-afternoon.” The headline, of course, suggests Trump golfed on Thanksgiving.

After Trump popped up in Afghanistan, Kwong and Newsweek took heat over Twitter for refusing to edit the article or delete the viral tweet promoting the lie.

This caught the attention of the Trump family, who promptly called out the beleaguered news outlet:

Eventually, Kwong caved by deleting her tweet, and Newsweek edited the article – at first with no mention of the edit, and then an editors note only after virtually the entire piece had been rewritten.

“This story has been substantially updated and edited at 6:17 pm EST to reflect the president’s surprise trip to Afghanistan. Additional reporting by James Crowley,” reads the update.

“Newsweek investigated the failures that led to the publication of the inaccurate report that President Trump spent Thanksgiving tweeting and golfing rather than visiting troops in Afghanistan,” a Newsweek spokesperson told TheNew York Post in an email. “The story has been corrected and the journalist responsible has been terminated. We will continue to review our processes and, if required, take further action.”

After Trump tweeted “I thought Newsweek was out of business?,” The Wrap reminds us that “The former owners of the publication and a faith-based online media company were accused of attempting to defraud lenders in an indictment filed in October 2018,” adding “High-ranking editorial staffers have been leaving the publication and three senior editorial staffers were fired in retaliation for a story about a legal investigation into the company in February 2018.”

Not quite out of business, but certainly not in a position to afford further reputational risk from obvious fake news.

Meanwhile, her fellow Democrats appear abysmally unconcerned about the human and financial toll…

The Democratic establishment is increasingly irritated.

Representative Tulsi Gabbard, long-shot candidate for president, is attacking her own party for promoting the “deeply destructive” policy of “regime change wars.” Gabbard has even called Hillary Clinton “the queen of warmongers, embodiment of corruption, and personification of the rot that has sickened the Democratic Party.”

Senator Chris Murphy complained:

“It’s a little hard to figure out what itch she’s trying to scratch in the Democratic Party right now.”

Some conservatives seem equally confused. The Washington Examiner’s Eddie Scarry asked:

“where is Tulsi distinguishing herself when it really matters?”

The answer is that foreign policy “really matters.”

Gabbard recognizes that George W. Bush is not the only simpleton warmonger who’s plunged the nation into conflict, causing enormous harm. In the last Democratic presidential debate, she explained that the issue was “personal to me” since she’d “served in a medical unit where every single day, I saw the terribly high, human costs of war.” Compare her perspective to that of the ivory tower warriors of Right and Left, ever ready to send others off to fight not so grand crusades.

The best estimate of the costs of the post-9/11 wars comes from the Watson Institute for International and Public Affairs at Brown University. The Institute says that $6.4 trillion will be spent through 2020. They estimate that our wars have killed 801,000 directly and resulted in a multiple of that number dead indirectly. More than 335,000 civilians have died—and that’s an extremely conservative guess. Some 21 million people have been forced from their homes. Yet the terrorism risk has only grown, with the U.S. military involved in counter-terrorism in 80 nations.

Obviously, without American involvement there would still be conflicts. Some counter-terrorism activities would be necessary even if the U.S. was not constantly swatting geopolitical wasps’ nests. Nevertheless, it was Washington that started or joined these unnecessary wars (e.g., Iraq, Libya, Syria, and Yemen) and expanded necessary wars well beyond their legitimate purposes (Afghanistan). As a result, American policymakers bear responsibility for much of the carnage.

The Department of Defense is responsible for close to half of the estimated expenditures. About $1.4 trillion goes to care for veterans. Homeland security and interest on security expenditures take roughly $1 trillion each. And $131 million goes to the State Department and the U.S. Agency for International Development, which have overspent on projects that have delivered little.

More than 7,000 American military personnel and nearly 8,000 American contractors have died. About 1,500 Western allied troops and 11,000 Syrians fighting ISIS have been killed. The Watson Institute figures that as many as 336,000 civilians have died, but that uses the very conservative numbers provided by the Iraq Body Count. The IBC counts 207,000 documented civilian deaths but admits that doubling the estimate would probably yield a more accurate figure. Two other respected surveys put the number of deaths in Iraq alone at nearly 700,000 and more than a million, though those figures have been contested.

More than a thousand aid workers and journalists have died, as well as up to 260,000 opposition fighters. Iraq is the costliest conflict overall, with as many as 308,000 dead (or 515,000 from doubling the IBC count). Syria cost 180,000 lives, Afghanistan 157,000, Yemen 90,000, and Pakistan 66,000.

Roughly 32,000 American military personnel have been wounded; some 300,000 suffer from PTSD or significant depression and even more have endured traumatic brain injuries. There are other human costs—4.5 million Iraqi refugees and millions more in other nations, as well as the destruction of Iraq’s indigenous Christian community and persecution of other religious minorities. There has been widespread rape and other sexual violence. Civilians, including children, suffer from PTSD.

Even stopping the wars won’t end the costs. Explained Nita Crawford of Boston University and co-director of Brown’s Cost of War Project: “the total budgetary burden of the post-9/11 wars will continue to rise as the U.S. pays the on-going costs of veterans’ care and for interest no borrowing to pay for the wars.”

People would continue to die. Unexploded shells and bombs still turn up in Europe from World Wars I and II. In Afghanistan, virtually the entire country is a battlefield, filled with landmines, shells, bombs, and improvised explosive devices. Between 2001 and 2018, 5,442 Afghans were killed and 14,693 were wounded from unexploded ordnance. Some of these explosives predate American involvement, but the U.S. has contributed plenty over the last 18 years.

Moreover, the number of indirect deaths often exceeds battle-related casualties. Journalist and activist David Swanson noted an “estimate that to 480,000 direct deaths in Afghanistan, Iraq, and Pakistan, one must add at least one million deaths in those countries indirectly caused by the recent and ongoing wars. This is because the wars have caused illnesses, injuries, malnutrition, homelessness, poverty, lack of social support, lack of healthcare, trauma, depression, suicide, refugee crises, disease epidemics, the poisoning of the environment, and the spread of small-scale violence.” Consider Yemen, ravaged by famine and cholera. Most civilian casualties have resulted not from Saudi and Emirati bombing, but from the consequences of the bombing.

Only a naif would imagine that these wars will disappear absent a dramatic change in national leadership. Wrote Crawford:

“The mission of the post-9/11 wars, as originally defined, was to defend the United States against future terrorist threats from al-Qaeda and affiliated organizations. Since 2001, the wars have expanded from the fighting in Afghanistan, to wars and smaller operations elsewhere, in more than 80 countries—becoming a truly ‘global war on terror’.”

Yet every expansion of conflict makes the American homeland more, not less, vulnerable. Contrary to the nonsensical claim that if we don’t occupy Afghanistan forever and overthrow Syria’s Bashar al-Assad, al-Qaeda and ISIS will turn Chicago and Omaha into terrorist abattoirs, intervening in more conflicts and killing more foreigners creates additional terrorists at home and abroad. In this regard, drone campaigns are little better than invasions and occupations.

For instance, when questioned by the presiding judge in his trial, the failed 2010 Times Square bomber, Faisal Shahzad, a U.S. citizen, cited the drone campaign in Pakistan. His colloquy with the judge was striking: “I’m going to plead guilty 100 times forward because until the hour the U.S. pulls its forces from Iraq and Afghanistan and stops the drone strikes in Somalia and Yemen and in Pakistan and stops the occupation of Muslim lands and stops Somalia and Yemen and in Pakistan, and stops the occupation of Muslim lands, and stops killing the Muslims.”

Ajani Marwat, with the New York City Police Department’s intelligence division, outlined Shahzad’s perspective to The Guardian:

“’It’s American policies in his country.’ …’We don’t have to do anything to attract them,’ a terrorist organizer in Lahore told me. ‘The Americans and the Pakistani government do our work for us. With the drone attacks targeting the innocents who live in Waziristan and the media broadcasting this news all the time, the sympathies of most of the nation are always with us. Then it’s simply a case of converting these sentiments into action’.”

Washington does make an effort to avoid civilian casualties, but war will never be pristine. Combatting insurgencies inevitably harms innocents. Air and drone strikes rely on often unreliable informants. The U.S. employs “signature” strikes based on supposedly suspicious behavior. And America’s allies, most notably the Saudis and Emiratis—supplied, armed, guided, and until recently refueled by Washington—make little if any effort to avoid killing noncombatants and destroying civilian infrastructure.

Thus will the cycle of terrorism and war continue. Yet which leading Democrats have expressed concern? Most complain that President Donald Trump is negotiating with North Korea, leaving Syria, and reducing force levels in Afghanistan. Congressional Democrats care about Yemen only because it has become Trump’s war; there were few complaints under President Barack Obama.

What has Washington achieved after years of combat? Even the capitals of its client states are unsafe. The State Department warns travelers to Iraq that kidnapping is a risk and urges businessmen to hire private security. In Kabul, embassy officials now travel to the airport via helicopter rather than car.

Tulsi Gabbard is talking about what really matters. The bipartisan War Party has done its best to wreck America and plenty of other nations too. Gabbard is courageously challenging the Democrats in this coalition, who have become complicit in Washington’s criminal wars.

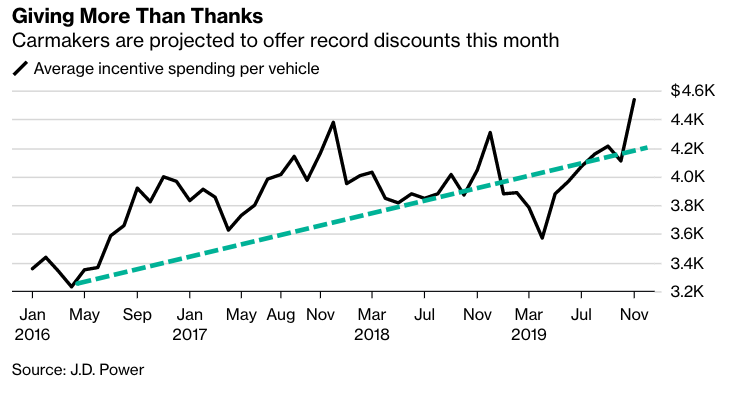

Automakers Offer Record Incentive Spending As Trillion Dollar Auto Bubble Becomes Unsustainable

Early last month, we outlined how automobile sales deteriorated in late summer and prophesized how “this would set the stage for increased incentive spending by carmakers, who will be desperate to clear inventory heading into the end of the year.”

It seems that we were right. Automakers are now offering the most discounts on record to entice deadbeat consumers in November, according to a new report from JD Power.

The average incentive spending per vehicle is $4,538, an increase of 12% YoY. The previous high for the industry was $4,378 in 4Q17.

Inventories for older model-year vehicles have soared in 2H19, forcing automakers to boost incentive spending to clear excess inventory.

With the average APR to finance a vehicle around 5.3% for the month, the average transaction price remained above $34,000, down from $179 from last month but up $622 over the year.

As a result of low rates and record-high incentives, consumers spent $40.3 billion on new vehicles in November. This figure is up $2.7 billion from 2018.

Thomas King, Senior Vice President of the Data and Analytics Division at JD Power, said, manufacturers will offer even greater incentives through December, and the trend could continue into early 2020.

“Incentive spending typically rises by 3-4% in December, which would continue to drive overall spending to unprecedented territory,” King said.

King warned: “This [incentive trend] is concerning for the health of the industry when combined with rising sub-prime sales, which are growing at the highest rate since August 2018.”

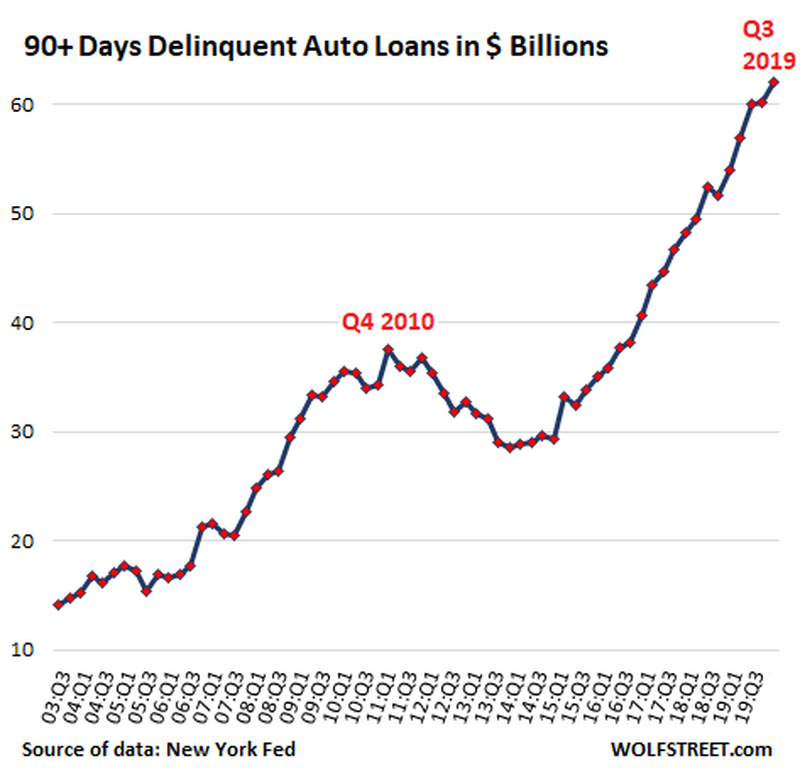

We recently noted serious auto-loan delinquencies (more than 90 days past due) in Q3 hit a historic high of $62 billion.

“This $62 billion of seriously delinquent loan balances are what auto lenders, particularly those that specialize in subprime auto loans, such as Santander Consumer USA, Credit Acceptance Corporation, and many smaller specialized lenders are now trying to deal with. If they cannot cure the delinquency, they’re hiring specialized companies that repossess the vehicles to be sold at auction. The difference between the loan balance and the proceeds from the auction, plus the costs involved, are what a lender loses on the deal,” wrote Wolf Richter via WolfStreet.com.

Automakers are recklessly blowing up a $1.32 trillion bubble, by ramping up subprime loans to deadbeat consumers. Recent incentive increases have taken the bubble blowing to an entirely new level that is not sustainable.

Coming up with ways to catch illegal immigrants bent on staying undetected in the United States is not an easy chore. There are only so many border patrol agents and a ton of territory to cover. U.S. Immigration and Customs Enforcement (ICE) has been suffering a lot of criticism for its determination to get a handle on the border crisis, especially since President Donald Trump took office. And now the federal agency is coming under fire again, this time for using a fake university to catch recruiters using the system to get money while aiding illegals and foreign students trying to remain in the U.S.

University of Farmington

Mainstream media is mostly reporting on how horrible it is that these students, who are only trying to better their lives, have been duped by the government. True, they were charged tuition fees for a school that didn’t even exist. But there’s much more to the story than that.

First, let’s start off with the fact that this was not a Trump administration program. Yes, you read that right.

The fake university “scheme” began during Barack Obama’s reign, but we all know the president will be the one criticized for it. One need only remember the detention facilities (set up before Trump) being compared to concentration camps and holding babies in cages to know how this one is going to turn out.

Of the 600 or so students “enrolled” in the fake Michigan-based University of Farmington, approximately 250 have been arrested since January. About 80% of those arrested were granted voluntary departure from the country and another 10% were given deportation notices. The other 10% are fighting the arrest and have either contested the deportation orders or have filed for relief. One student was even given permanent resident status by an immigration judge.

Students’ attorneys claim their clients were “trapped” or “preyed upon” by the government. They noted the website on which the Department of Homeland Security (DHS) stated that Farmington was legitimate and an accredited educational institution. But federal officials say the students should have known better since there were not even any physical classes to attend. Assistant U.S. Attorney Brandon Helms emphasized this in a sentencing memo for one of the eight recruiters arrested during the operation. In it, he said:

“Their true intent could not be clearer. While ‘enrolled’ at the University, one hundred percent of the foreign citizen students never spent a single second in a classroom. If it were truly about obtaining an education, the University would not have been able to attract anyone, because it had no teachers, classes, or educational services.”

The fake university program was designed to catch recruiters who take advantage of foreigners by charging them big bucks and recommending them to schools. Prosecutors say this is a form of visa fraud and jeopardizes the integrity of the student visa program, an initiative that allows immigrants to stay in the country as long as they are studying for a degree and are in good standing both academically and legally.

Some of the students caught in the sting effort were not trying to con the system and had transferred to the university because the school they had been attending lost its accreditation, which made their visas null and void. However, as DHS remarked, in most of these cases, the young academics remained enrolled even though they never attended a class or met a professor, which they should have realized was not appropriate. A very few did transfer to another facility after realizing something was not right, though.

Still, there is a lot of controversy over how ICE set up the operation using DHS to staff the fake facility and accepting tuition fees from the students. So far, no charges have been brought against the federal agency, but once the left has a chance to deflate from Thanksgiving dinner, we can be sure to see this latest issue laid squarely at the president’s feet, even though it was an Obama administration program to begin with.

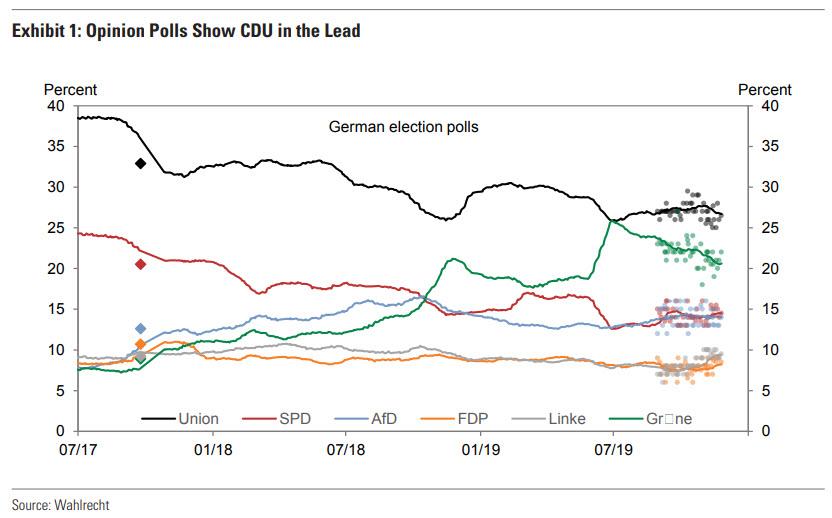

In Shocking Blow To Merkel, Germany’s SPD Elects Leftist Leaders, Risking Coalition Government Collapse

Merkel’s last term as German chancellor has been a series of relentless blows to her reputation and legacy, as the former leader of Europe finds herself trapped and increasingly powerless in a world that has grown hostile to her style of governing.

The latest shock came on Saturday, when the German Social Democratic Party (SPD) announced the winner of its leadership contest as both coalition partners of Germany’s Grand Coalition were transitioning their party leaderships after disappointing results in opinion polls and at regional elections.

Whereas consensus had widely expected finance minister Olaf Scholz and regional politician Klara Geywitz to preserve their control over the SPD after topping the first round of voting, the result announced just after 6pm CET showed that with a vote of 53% to 45%, SPD members elected Norbert Walter-Borjans, a former minister in the regional state of North Rhine-Westphalia, and Saskia Esken, an MP from Baden-Württemberg, as their new leaders.

The outcome was a blow to Merkel and her coalition government, as the duo of Walter-Borjans and Esken represent the left-leaning segment of the SPD and have been highly skeptical of the SPD’s role in the Grand Coalition government.

SPD’s new leaders, Norbert Walter-Borjans and Saskia Esken

The surprising swing to the left for Germany’s (formerly) centrist and fiscally prudent Grand coalition threatens to trigger a prolonged phase of political uncertainty in Germany, because as Bloomberg notes, “the victory of Walter-Borjans and Esken, who favor taxing the rich, boosting welfare spending and abandoning Germany’s long-standing policy of a balanced budget, will certainly weaken pro-government forces.”

Goldman Sachs agrees: in a Thursday note by the bank’s European strategist Sven Jari Stehn, he wrote that a victory by Walter-Borjans and Esken increases the risk that the SPD pulls out the coalition because under a left-leaning SPD “there would be a diminished consensus within the coalition” as the newly elected duo is demanding a re-negotiation of parts of the coalition agreement, and seeking to increase federal fiscal spending and investment.

Whereas this would be a virtually impossible concession for the CDU to make during its own leadership transition, Goldman does not expect “an immediate dissolution of the coalition”, even though the collapse of Germany’s current coalition is now just a matter of time.

“I never said we need to leave,” Walter-Borjans said after the results of the election were announced on Saturday evening. “We must improve the policies and perhaps loosen the black zero,” he said in reference to Merkel’s balanced budget policy, news that would be met over champagne and caviar everywhere from the ECB to Brussels, to the IMF, all of whom have been demanding that Germany boost its fiscal stimulus.

Ironically, it’s now only Angela Merkel who stands in the way of Germany doing away with its “black zero” balanced budget policy, and any deviation would almost surely mean the end of the Chancellor’s political career.

The fate of Germany’s fiscal stimulus has emerged as arguably the most important topic for Europe’s economic future.

While Germany avoided a technical recession by the narrowest of margins, growth continues to slow and will drop to an estimated 0.5% this year, one-fifth the rate of what it was in 2017, largely as a result of the global trade war and China’s collapsing credit impulse, although the ECB’s recent monetary boost has certainly helped delay the day of reckoning.

Ironically, after a tumultuous year in which the SPD and Merkel’s Christian Democrats both faced intense power struggles, Germany’s political and business elites had hoped for a period of calm and continuity; instead they are now looking at what appears to be an almost certain collapse of the ruling coalition.

As Bloomberg notes, in hopes of delaying political chaos, Merkel this week had made an unusual plea to see the alliance through to 2021, saying there was still much to be done. Finmin Scholz also argued that his party is achieving more of its objectives in government than it ever could in opposition, even if it needed to compromise. But Walter-Borjans managed to tap the dissatisfaction of many Social Democrats who feel their party has abandoned its working-class origins and should abandon an alliance with conservatives.

Meanwhile, as Goldman points out, the CDU/CSU coalition is not immune to internal tensions either. Since Annegret Kramp-Karrenbauer (AKK) took over the CDU leadership last year, both European and regional elections failed to show a turnaround in voter support that would have cemented her leadership of the party. While AKK’s critics refrained from a rival leadership bid at last week’s CDU party convention, her position remains uncertain. Absent a substantial improvement in her approval ratings, there will be an aggressive race for the CDU’s lead candidate for the next general election scheduled for the fall of 2021, with candidates from both the centre and the right of the party likely throwing their hats in the ring when the nomination process begins in late 2020. A more right-leaning candidate could also raise questions about the viability of the current coalition, especially with the SPD now turning a sharp left turn.

To be sure, Merkel may still fight to preserve the coalition, but that would come at a major cost: during the campaign Esken and Walter-Borjans said their price for staying includes billions of euros of government investment in climate and education, a 12 euro per hour minimum wage, and wage negotiations that should be made obligatory for employers. While such demands were seen as unacceptable by Merkel’s CDU and its leader, AKK, told delegates at a convention in Leipzig last week that she would refuse to renegotiate the coalition agreement that the two factions completed in March 2018, now that the numbers are in, Merkel may have no choice but to bend the knee.

In other words, while today was another major loss for Merkel, fans of MMT around the world are rejoicing as Germany is now one step closer to launching an ECB-monetized fiscal stimulus.

What happens next?

According to Goldman, notwithstanding the risks involved in the leadership transitions, the bank still expects the Grand Coalition to last through 2020 and, even in the event the coalition is dissolved, snap elections would not be triggered automatically as the hurdles to dissolving parliament are high. Neither coalition partner currently has a strong incentive to seek fresh elections as both are polling well below their 2017 election results, and the Greens continue to poll ahead of the SPD.

A CDU/CSU minority government is therefore the more likely option in the event of a breakup of the Grand Coalition, providing relative stability during Germany’s European Council Presidency in the second half of 2020.

As for Germany’s economy, Goldman expects the Esken/Walter-Borjans leadership to increase the chance that the fiscal space made available in the 2020 budget is fully exploited rather than under-delivering on the planned easing as in previous years seeing they have indicated to favor a looser fiscal stance. This could add stimulus worth 0.2% of GDP in 2020, but it would still fall significantly short of the easing space afforded by both national and EU rules. Should the Grand Coalition

break up, a CDU-led minority government would imply downside risks to Goldman’s ur baseline.

So while today’s result was a clear sign that at least one German party is turning sharply left, and thus more likely to endorse fiscal stimulus, Germany still faces an uphill climb before it concedes, a climb that may last well into 2021 by which point the global economic recession would make a German stimulus a moot point.

No doubt Los Angeles County’s VSAP (“Voting Solutions for All People”) rollout will not be covered as a debacle. The real question is: If there were a debacle — like, say, a case of election fraud — would we even know? Doubtful.

Just what we want in a voting system! In this post, I’ll give a brief overview of issues with electronic voting. Then I’ll look at VSAP as an institution. Next, I’ll show why the VSAP system is not only insecure, but likely to make money-in-politics even worse than it already is.

We’ve covered electronic voting before — see here, here, and here — and if you want to understand why hand-marked paper ballots, hand-counted in public (HMPBCP) is the world standard, you can read them, especially the first. In this overview, I’ll make a few high-level observations about electronic voting in general.

Digital systems can never be shown not to have bugs. As Computer Science Elder God Edgers Dijkstra wrote: “Program testing can be used to show the presence of bugs, but never to show their absence!” Many bugs in many important programs persist for years before they are discovered. A list would include Flash in IE6 (persisted 12 years), OpenSSL (15 years), LZO data compression (18 years), and bash (25 years). None of these examples are outlier programs or trivial; they are all used by millions, essential to enterprises, networks, etc. Each of these bug is an insecurity waiting to happen. And that’s before we get to Trojan Horses, which are bugs introduced deliberately by a developer for purposes of their own. In fact, I would go so far as to argue that any voting system decision maker who advocates electronic voting is doing so for reasons other than security, given that HMPBCP is available, which amounts to saying that such a decision maker regards a certain amount of exploited bugs — election fraud — as acceptable.

Now, of course we all use programs all the time: We have programs to turn on our lightbulbs, call cabs, download pr0n, etc. I’m using a program now to write this post! However, if we put voting machine software on the same plane as commercial software, we’re arguing that a central-to-mission function of democracy — the vote — is on the same plane as the very convenient ability to check the contents of our refrigerator from our cellphone. Lest I be thought curmudgeonly in this, recall the example of Bolivia, where one reason the vote was challenged was the use of an unauthorized server for data transmission of the count. Contrast that with the recent vote in Hong Kong, where there were many images of people marking paper ballots, and of people counting them, in public (in fact, of people demanding to be let in to observe). Imagine if electronic systems had been used: First, the Mainland would have had every incentive to have compromised the software, and might well have done so successfully; second, electronic systems, because they are always buggy, are always open to challenge. The fallout could have been extremely ugly at the geopolitical level. Nor would the people’s will have been respected.

With that, lets turn to Los Angeles County and VSAP. As with any software project, we need to understand the requirements. Here is what I can find on the extremely spiffy and well-budgeted VSAP site: “The Design Concepts“:

The final concept created for VSAP incorporates features driven by the project principles as well as focus group feedback, input and in-person testing.

The concept system features touch-screen technology with a simple user interface, both audio and visual output and a built-in scanner, printer and ballot box. The new voting system will provide voters with options to scan in QR coded ballots from their phone, enter their ballot choices in-person at the polling location or vote-by-mail with printed ballots.

(Note that the concept very explicitly does not say that hand-marked paper ballots will be available at polling locations; only vote by mail.) I note with alarm that the concept document includes no mention of security, or even that the voters vote be accurately recorded and tabulated. Let’s look elsewhere for that. From the aforementioned “Principles“:

TRUST The voting system must instill public trust and have the ability to produce a physical and tangible record of a voter’s ballot to verify the ballot was marked as intended before it is cast and to ensure auditability of the system. It must demonstrate to voters, candidates, and the general public that all votes are counted as cast.

(A little too much focus on PR for my taste: “instill,” “demonstrate.”) Note the fundamental equivocation, which I have underlined: The paper is not the ballot; the paper is only a record of the ballot, which is digital. More:

INTEGRITY The system must have integrity, be accountable to voters, and follow existing regulations. System features must protect against fraud and tampering. It should also be easy to audit and produce useful, accessible data to verify vote counts and monitor system performance.

“System features must protect against fraud and tampering.” See comments on bugs above. There is nothing insecure about counting ballots by hand in public. That’s why you count them in public. Finally:

TRANSPARENCY The processes and transactions associated with how the system is set up, run, and stored should be easy for the public to understand and verify. This should include making hardware components available for inspection, and source code to the extent that the manner of doing so would not jeopardize system security or availability

VSAP is being marketed as open source, but that underlined section is an awfully big qualifier. We’ll have to see how it works out in practice.

So, these design concepts and principles are the closest I can come to a requirements document (and I did look using several search tools, as well as doing an image search for diagrams). So, although VSAP uses “ballot marking devices,” we don’t know what requirements they are supposed to meet, and so have no way to judge the success of the VSAP system. If you, readers, can do better, please put your results in comments.

So, the VSA site reads like public relations to me. For completeness, here’s an image of the county-wide rollout:

Pop-up Demo center at LaCrescenta Library. You can interact and use the new ballot marking device!

2809 Foothill Blvd.

LaCrescenta, CA 91214

November 25th from 12-8pm

November 26th from 10am-6pm #VSAPpic.twitter.com/VElhLcPrkl

An innovative voter-centered election system will modernize the way Los Angeles County citizens will cast their ballots. In partnership with Smartmatic, who was awarded a contract to assist LA County in the design, construction, and deployment of the new voting solution, Votem will facilitate the development of the new system’s interactive ballot display.

“We are extremely pleased to be taking this important step forward in delivering on our commitment to modernize the voting experience in Los Angeles County and to lead in the development and implementation of a non-proprietary, publicly-owned voting system that is responsive to the needs and behavior of our electorate,” said Dean Logan, Registrar of Voters, following the awarding of the contract at the Board of Supervisors meeting on Tuesday.

Votem and its team will be responsible for the interactive ballot display and implementation, as designed by and for Los Angeles County, in partnership with IDEO, during prior phases of the VSAP initiative that focus on security, accessibility and usability. The interactive sample ballot display will allow for voters to mark their choices on their mobile device – anywhere, anytime – and then scan in their QR code in person for fast and easy voting at a vote center.

(Hold that thought on QR codes. As it will turn out, the QR code is the actual ballot.) Votem, eh? NC readers will be familiar with Votem, since Votem was involved in CalPERS corrupt election process (see here, here, and here). Of the Votem’s many problems, this one seems to be, well, the juiciest. Yves analyes a Votem “CalPERS Tabulation Incident Report” and concludes:

[T]he Incident reports starts with five Big Lies, which is quite impressive in such a short space:

The 2018 CalPERS Public Agency Member Election was conducted by the Everyone Counts/IVS Joint Venture. Everyone Counts has since been acquired by Votem, Corp. The election team and tabulation platform remained the same.

First, the election vendors admitted in 2017 (just the way CalPERS finally confessed that “CalPERS Direct” was not direct investing) that its election “joint venture” was no such thing. It was an operating agreement between K&H Printers-Lithographers, Incorporated, dba Integrity Voting Systems, and Everyone Counts, Inc.6 In keeping, the two parties signed the agreement as separate entities.

Second, the parties nevertheless attempted to depict the contract repeatedly as a joint venture, even stating in the operating agreement that the services were to be provided in the name of the “”IVS/Everyone Counts Joint Venture”. So Votem also misrepresented the name by putting “Everyone Counts” first, implying it is the more important player. We have the agreement embedded at the end of our second post. It makes very clear that K&H Printing, operating as IVS, was the dominant party.

Third, Votem falsely stated that the elections were conducted by the soi disant joint venture. That is false because Everyone Counts defaulted on the agreement by selling its assets to Votem before the election was over.

Fourth, Votem says it acquired “Everyone Counts”. It did not do so. It acquired only Everyone Counts’ assets, deliberately leaving the liabilities and the legal entity behind.

Finally, Votem claims that it acquired “Everyone Counts” after the election. This is false, since the sale of assets closed before the election was over and days before the tabulation took place.

So, underneath all the glossy PR, and the rollout, and the stakeholders, and the lavish website, we have a prime contractor that’s an extremely shady business entity. One, morever, in charge of the ballot!

The new VSAP system is a touchscreen Ballot Marking Device or BMD, which prints out a computer-marked paper ballot summary of votes selected via the touchscreen, before using another computer, an optical-scanner, to read the non-human readable QR Code that is also printed on the ballot summary. The QR Codes are used to tally votes. While the QR Code (a type of barcode) cannot be verified for accuracy by voters, it is also impossible with such systems to know if any voter has even verified the human-readable portion of the ballot summary at all, much less correctly, after an election. Studies reveal that most do not verify computer-marked ballots at all, and that of the minority who do, most don’t recall the details or selections on the ballot they voted just moments earlier. That’s just one of the many reasons why most cybersecurity and voting systems experts warn against the use of such systems which are now proliferating — and sometimes replacing verifiable hand-marked paper ballot systems — in many states and counties across the country before 2020. (The list of states where counties or the entire state are moving to BMD systems include a number of key battleground states. Such systems are planned for use next year, or are already being used, in OH, WI, PA, TX, WV, KY, NY, NJ, KS, TN, IN, SC, NC and, yes, CA, unless the public prevents these plans.)

(There’s much, much more; read the whole thing, especially Los Angeles residents.) For readers who think they have never seen a QR code, it’s like a bar-code in two dimensions, and it looks like this:

I wanted to find the requirements document and if possible some process flow diagrams, but I’ll take BradBlog at his word. The flow for a Ballot Marking Device would be something like: Voter makes selections on touch-screen (software, hence buggy and insecure), selections are stored (ditto) and printed out (ditto) on a page with a human-readable receipt reflecting the touchscreen selections, and the ballot itself, which is the QR code, which is not human-readable. The page is then scanned (ditto) and QR code is then tabulated (ditto). The sleight of hand is, of course, the ballot itself. A human may think that their reciept, which they can read to check that it matches what they selected on the touch screen, also matches the QR code, which they cannot. But there’s no reason on earth to think that! And the unreadable QR code, since that is what is tabulated, is the ballot! Take the matter out of the delusional digital realm. Suppose voting worked like this: You voted by hand-marking a yellow paper ballot. You then handed the yellow paper ballot to an official who, behind a screen so you could not see, then marked a blue ballot that you could not read, seaked it so you could not read it, and then handed the blue ballot back to you and told you to put it in the ballot box, that’s your vote. Does that make any sense? That is how a “Ballot Marking Device” works.

Worse, the QR code ballots reinforce the power of money in politics. Recall that “The new voting system will provide voters with options to scan in QR coded ballots from their phone.” Well, security aside, game that out. From Knock LA, “The Campaign Finance Problem is About to Get Worse“:

Voters who like to fill out their sample ballot in advance and bring it to the polls will be particularly interested in the new Interactive Sample Ballot (ISB) feature. This will allow them to store their choices to a “Poll Pass” containing a QR code and then reload it into the Ballot Marking Device. This is an option that will “help expedite the voting process” by negating the need to individually mark each line on the ballot while in the polling center. This will be particularly useful on a ballot that will be extraordinarily long now that local elections will be folded into the presidential ballot. Unfortunately, this convenience will come at a steep price for our democracy.

Instead of building in assurances that the Poll Pass could only be used by the person who created it, the designers left the system open so QRs can be created by third parties and then be distributed for use at the polls. This would significantly increase the effectiveness of the slate mailers that inundate mailboxes prior to an election[1].

While the casual voter may believe that the strategically named organizations that publish slate mailers have carefully screened candidates for inclusion, the truth is that most are nothing more than a pay to play form of political marketing. Inclusion on these ads has more to do with the ability to pay than the views of the included candidate. The ability to pre-fill a voter’s ballot will make inclusion on these mailers even more valuable and put candidates not funded by special interest groups at even more of a disadvantage.

Groups like the California Charter School Association (CCSA), which have already shown the willingness to throw ethics aside in order to win elections, will find the new system even more valuable. Their printed materials could highlight popular candidates without even mentioning their favored candidate while still embedding their choice within the QR code. The unsuspecting voter who does not check all the way down the ballot at the polling place would be casting a vote for a candidate they took no action in choosing and may, in fact, oppose. By creating different slates to cover multiple candidates in races that attract the most attention, groups like CCSA could magnify their effect on the election. They could even print one slate on their mailer and include a QR code that placed a completely different set of names on the ballot.

Given the role that liberal Democrats think the donor class should play in politics, this may not be an issue for VSAP.

Conclusion

G-a-a-a-a-a-h! All that design! All those principles! And at the end of the day we have a system where the voter doesn’t know the vote they cast, and that reinforces the power of big money. Some clever lawyer needs to bring suit on this and fight it all the way to the Supreme Court (who, I suppose, can choose to put the final nail in the democracy’s coffin, or not). Oh, and VSAP hopes a lot of other jurisdictions adopt its system. Swell.

{kind=link}