“We Have Hours Left”: Turkish Ceasefire On Edge Of Collapse As Erdogan Gives Kurds Hours To Flee Territory

The Turkish lira has started to slide again…

.. as last week’s ceasefire between Turkey, northern Syria and its Kurdish inhabitants – which has just over 24 hours to go – now appears in jeopardy.

On Monday, Turkey gave Kurdish fighters until Tuesday night to leave a narrow strip of territory in northeastern Syria or face becoming targets, setting aside its demand for the militia to withdraw from a much larger “safe zone.”

“We have hours left,” Turkey’s Foreign Minister Mevlut Cavusoglu told a forum organized by state-run TRTWorld television in Istanbul on Monday. “If they don’t withdraw, our operation will start. This is our agreement with the U.S.”

As Bloomberg notes, citing a senior Turkish military official said, the Kurdish-led Syrian Democratic Forces must exit the 120-kilometer (75-mile) area between the Syrian border towns of Tal Abyad and Ras al-Ayn by 10 p.m. local time on Tuesday. While Turkey still wants the Kurds to withdraw from a swath of frontier territory more than 440 km long and 32 km deep, it recognizes that won’t happen before the expiry of a 120-hour truce negotiated by the U.S. last week, said the official who also ruled out any extension of the deadline for withdrawal from a 120-kilometer long frontier.

The clarification over the parameters of the truce on Monday followed threats by President Recep Tayyip Erdogan to restart the offensive if the militants do not pull back from the area.

Turkey’s immediate goal is to clear the 120-kilometer strip and so far 125 vehicles have left the area and that the effort to implement the deal was closely coordinated with the U.S., the official said, adding that Turkey plans to set up observation points, including combat units, in the area; he also said that control over the 120- kilometer strip would belong to the Turkish Air Force but that it would take time to fully make sure that the area is cleared from the militants.

Separately, Turkish president Erdogan is due to travel to Sochi on Tuesday for talks with Russian president Vladimir Putin that will likely dictate what happens next. With the departure of US forces, Russia has become the sole major influencer in Syria since its military intervened to help win the civil war in favor of Bashar al-Assad’s regime.

As Bloomberg notes, Russia has been favoring direct contacts between Turkey and Syria based on a 1998 security accord, though there are no plans for such talks during Erdogan’s visit to Sochi on Tuesday, Russian Foreign Minister Sergei Lavrov tells reporters at news conference with Bulgarian counterpart Ekaterina Zaharieva.

* * *

Meanwhile, as the US withdraws from northern Syria, the WSJ reports that civilians in Kurdish areas hurled rotten fruit and insults at a convoy of U.S. military vehicles that crossed from northern Syria into Iraq early Monday, marking “a dramatic drawdown to an American presence there to combat Islamic State.”

A Wall Street Journal reporter saw around a dozen armored vehicles on the road near Sheikhan in northern Iraq flying American flags. Stony-faced U.S. soldiers flashed victory signs for the camera. They appeared to be part of a larger convoy that passed through the town of Duhok about 37 miles from the Syrian border earlier Monday. A witness there heard onlookers in the predominantly Kurdish city curse the soldiers. One man called them “sons of bitches” and shouted at them to get out, he said.

A convoy of U.S. vehicles at the Iraqi-Syrian border crossing on the outskirts of Duhok, Iraq

The US withdrawal has been seen as a historic betrayal by the Kurds, who partnered with U.S. troops in Syria to fight Islamic State. The U.S. presence had served as a buffer against Turkey, which regards the Kurdish fighters as terrorists.

Fear not though: instead of withdrawing, it now appears that US troops are merely relocating to neighbor Iraq, where the US already has around 5,000 troops in Iraq, many of whom are based in the western province of Anbar.

U.S. Defense Secretary Mark Esper said late Saturday that all of the roughly 1,000 U.S. troops ordered to leave northeastern Syria would be redeployed to western Iraq and conduct operations against the Islamic State extremist group from there.

American troops are leaving Syria via helicopters, planes and ground convoys, a process that will be completed within weeks, Esper said. He didn’t say where precisely those troops would go.

Four Drug Companies Reach 11th Hour Settlement In Opioid Litigation

Four large drug companies have reached a last-minute settlement with two Ohio counties to avoid trials blaming them for their part in fueling the ongoing opioid crisis, according to the Wall Street Journal. A fifth defendant, Walgreens Boots Alliance (WBA), has yet to agree to a deal.

The details of the agreement with McKesson Corp. , Cardinal Health Inc., AmerisourceBergen Corp. and Teva Pharmaceutical Industries Ltd. will be announced later Monday morning. It is unclear whether trial will proceed against just WBA.

AmerisourceBergen CEO Steven Collis testified before Congress on May 8, 2018, alongside other drug company executives. Photo: Alex Brandon/Associated Press

While the deal with the Ohio counties will avoid a federal jury trial with the two counties, it falls short of a more sweeping deal currently under negotiation to resolve thousands of opioid lawsuits across the country.

The cases of Ohio’s Cuyahoga and Summit counties had been selected to go to trial first from more than 2,300 opioid lawsuits brought in federal court by local municipalities, hospitals, Native American tribes and others that are consolidated before U.S. District Judge Dan Polster in Cleveland.

The lawsuits broadly allege the pharmaceutical industry pushed opioid painkillers for widespread use without adequately warning of the risks of addiction and allowed high volumes of pills to flood into communities.

The Ohio cases will likely serve as a benchmark for how the more comprehensive opioid litigation may be resolved, as virtually every state – and thousands of local governments, have sought to recover money from pharmaceutical companies involved in the manufacture, marketing and distribution of opioids.

Over 400,000 people in the US have died from overdoses of opioids – both legal and illegal, since 1999 according to the report.

The Ohio cases would have provided a rare insight into how drug distributors contributed to the crisis, as documents and witnesses would be under a public microscope. According to the Journal, the companies are middlemen who fulfill drug orders placed by hospitals, pharmacies and others.

An earlier opioid-crisis trial, in Oklahoma, had only drugmaker Johnson & Johnson as a defendant, limiting the scope of the narrative unspooled in court.

McKesson, Cardinal and AmerisourceBergen collectively controlled 95% of the U.S. drug distribution market in 2018, according to Drug Channels Institute, which provides research on the drug-supply chain. The three companies are among the largest in the U.S., all ranking in the top 25 of the Fortune 500.

The distributors have argued that their role is to ensure medicines prescribed by licensed doctors are delivered to patients who need them. They say they must balance their mission to deliver medicine against efforts to prevent and detect illegal diversion of those drugs.

Walgreens, widely known as a pharmacy, has been included in the trial for its role as a drug distributor to its own stores.

Israel-based Teva and its subsidiaries make generic opioid painkillers and two branded drugs used for cancer pain. The company has argued that it doesn’t market its generic opioids. –Wall Street Journal

According to some accounts, the comprehensive deal between the industry and a coalition of state attorneys could be worth as much as $48 billion – a number which has been rejected by lawyers for cities and counties. It includes $18 billion to be paid over 18 years by AmerisourceBergen, Cardinal and McKesson; $4 billion from Johnson & Johnson over a shorter time frame; and the donation of drugs from Teva and distribution services valued at as high as $28 billion according to the report.

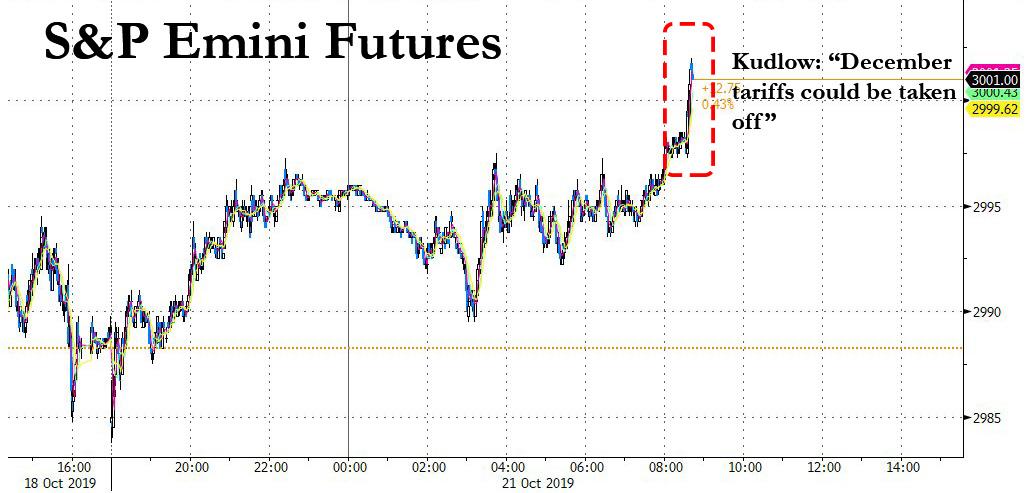

Kudlow Spikes Spoos Above 3,000, Says “December Tariffs” Could Be Taken If China Talks Go Well

With Trump eager to put last week’s turbulence in the readview mirror and start off the new week on a high note, he dispatched his best headline generator, economic advisor Larry Kudlow to Fox Business, to boost risk sentiment with a few strategically phrased quotes meant to bolster US-China trade talk optimism which as we noted earlier helped push risk sentiment higher overnight, and which is all the headline scanning algos were looking for:

WHITE HOUSE ADVISER KUDLOW SAYS IF PHASE ONE CHINA TRADE TALKS GO WELL, DECEMBER TARIFFS COULD BE TAKEN OFF

KUDLOW SAYS THINGS LOOK PRETTY GOOD AS U.S., CHINA TRADE TALKS CONTINUE KUDLOW SAYS THINGS LOOK PRETTY GOOD AS U.S., CHINA TRADE TALKS CONTINUE

Kudlow’s comments were all it took to spark a buying frenzy from the all too predictable algos, which quickly pushed the S&P above 3,000.

And so, with all due respect to William Cowan and his lengthy conspiracy theory article in Vantiy Fair, this is all it takes to send futures surging, and no, one doesn’t have to be an inside trader to expect that Trump (and Kudlow) will be doing this each and every day just to preserve the illusion that all is well.

Mike Dorf offers a welcome suggestion: the Supreme Court should eliminate the requirement that amici have to seek leave of the parties.

The Court should simply abolish the requirement of consent with the backstop of leave and allow anyone and everyone who wants to file an amicus brief to do so. The fact that many parties give blanket consent shows that the world will not end if parties no longer play a gatekeeping role. And it’s a waste of the Court’s time to have to decide whether an amicus brief should be allowed. It’s easier just to start reading and put down a brief that proves unhelpful.

Generally, after certiorari is granted, blanket consent is provided. At this juncture, the parties are usually represented by frequent participants before the Supreme Court. They understand the game, and recognize that withholding consent is futile. However, at the cert stage, parties are often represented by counsel who do not frequently participate before the Supreme Court. At this juncture, consent is often denied; counsel think there is some advantage for doing so. (There is no advantage.) Thus, amici have to seek leave of the Supreme Court. So long as the brief meets all of the formalities, the Court will grant leave.

But why bother with this additional step? Dorf explains:

Requiring consent of the parties seems rooted in the fiction that the Supreme Court sits to resolve disputes between parties. That’s a formal limitation on its jurisdiction per the case-or-controversy requirement, but given the discretionary nature of Supreme Court review and its use in cases that present important questions, the Court is not a court of error.

I emphatically agree. The Court should dispense with this requirement, and permit amici to submit briefs without seeking leave.

Indeed, this rule should be extended to the lower courts. I’ve found that in the Circuit Courts, and especially the District Courts, parties routinely withhold consent. Even the federal government. The Solicitor General’s office will usually grants blanket consent at the Supreme Court. In my experiences, DOJ Civil Appellate does grant consent, though they may inquire about the contents of the brief. A slight burden, but a reasonable request.

However, in the District Court, DOJ Federal Programs “takes no position” on amici requests. That posture still requires seeking leave of court. This process is a waste of time. The motion will be granted. There is no reason to force amici (often working pro bono) to prepare an additional motion, which the court then needs to rule on. And, in almost every case, the lower court will grant the motion.

There is another obstacle to filing amicus briefs in the District Courts: Pro Hac Vice fees. In the Southern District of New York, for example, that fee is $200. Attorneys who represent paying amici can easily be reimbursed for this fee. However, attorneys who represent amici pro bono cannot be reimbursed for this fee. In some cases, law firms may eat the fee. But for academic amici, law schools may not have the budget for such expenditures. (Mine does not.) Moreover, when several professors sign the brief, each attorney must pay the fee.

My proposal: create a fee waiver for attorneys who represent amici pro bono. Alternatively, so long as one attorney on the brief is admitted to the district, pro hac vice fees should be waived for other attorneys who represent the amicus pro bono. Courts should incentivize, not discourage amici filings from parties who are not financially interested.

from Latest – Reason.com https://ift.tt/31zZ7Ss

via IFTTT

Mike Dorf offers a welcome suggestion: the Supreme Court should eliminate the requirement that amici have to seek leave of the parties.

The Court should simply abolish the requirement of consent with the backstop of leave and allow anyone and everyone who wants to file an amicus brief to do so. The fact that many parties give blanket consent shows that the world will not end if parties no longer play a gatekeeping role. And it’s a waste of the Court’s time to have to decide whether an amicus brief should be allowed. It’s easier just to start reading and put down a brief that proves unhelpful.

Generally, after certiorari is granted, blanket consent is provided. At this juncture, the parties are usually represented by frequent participants before the Supreme Court. They understand the game, and recognize that withholding consent is futile. However, at the cert stage, parties are often represented by counsel who do not frequently participate before the Supreme Court. At this juncture, consent is often denied; counsel think there is some advantage for doing so. (There is no advantage.) Thus, amici have to seek leave of the Supreme Court. So long as the brief meets all of the formalities, the Court will grant leave.

But why bother with this additional step? Dorf explains:

Requiring consent of the parties seems rooted in the fiction that the Supreme Court sits to resolve disputes between parties. That’s a formal limitation on its jurisdiction per the case-or-controversy requirement, but given the discretionary nature of Supreme Court review and its use in cases that present important questions, the Court is not a court of error.

I emphatically agree. The Court should dispense with this requirement, and permit amici to submit briefs without seeking leave.

Indeed, this rule should be extended to the lower courts. I’ve found that in the Circuit Courts, and especially the District Courts, parties routinely withhold consent. Even the federal government. The Solicitor General’s office will usually grants blanket consent at the Supreme Court. In my experiences, DOJ Civil Appellate does grant consent, though they may inquire about the contents of the brief. A slight burden, but a reasonable request.

However, in the District Court, DOJ Federal Programs “takes no position” on amici requests. That posture still requires seeking leave of court. This process is a waste of time. The motion will be granted. There is no reason to force amici (often working pro bono) to prepare an additional motion, which the court then needs to rule on. And, in almost every case, the lower court will grant the motion.

There is another obstacle to filing amicus briefs in the District Courts: Pro Hac Vice fees. In the Southern District of New York, for example, that fee is $200. Attorneys who represent paying amici can easily be reimbursed for this fee. However, attorneys who represent amici pro bono cannot be reimbursed for this fee. In some cases, law firms may eat the fee. But for academic amici, law schools may not have the budget for such expenditures. (Mine does not.) Moreover, when several professors sign the brief, each attorney must pay the fee.

My proposal: create a fee waiver for attorneys who represent amici pro bono. Alternatively, so long as one attorney on the brief is admitted to the district, pro hac vice fees should be waived for other attorneys who represent the amicus pro bono. Courts should incentivize, not discourage amici filings from parties who are not financially interested.

from Latest – Reason.com https://ift.tt/31zZ7Ss

via IFTTT

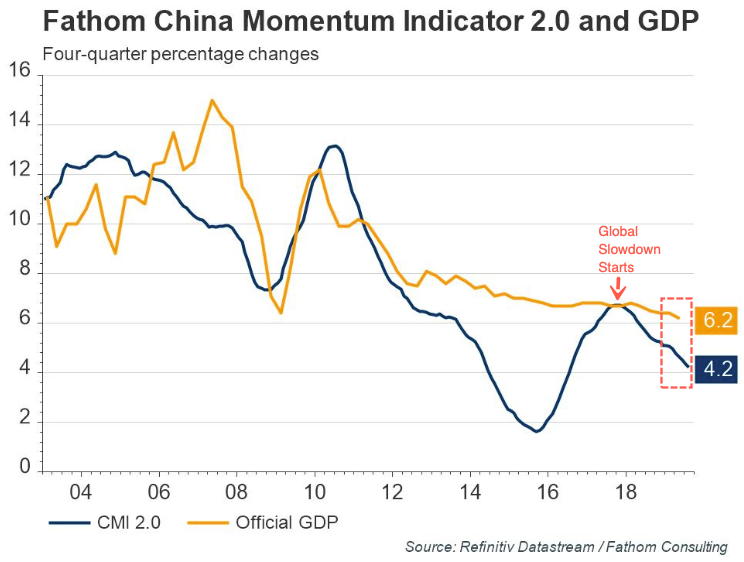

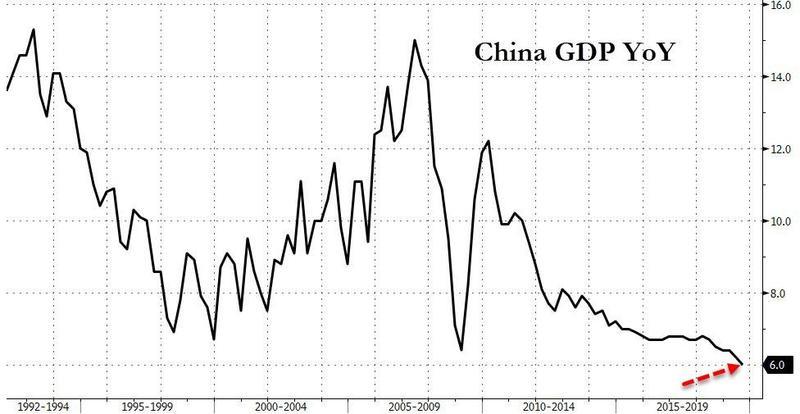

China Braces To Unveil 5%-GDP Growth At Two Key Meetings In Coming Weeks

Earlier this month, Beijing marked the 70th anniversary of the People’s Republic of China with huge military parades, showing off its hypersonic weapons and weaponized drones. But behind the scene’s China’s economy is quickly decelerating, and fresh evidence last week shows GDP could slip under 6%. China’s GDP, published last Friday, showed 6% growth for 3Q, the weakest quarterly prints since 1992 and down from 6.2% in 2Q.

“Trade tension with the US is the key factor weighing on business sentiment and investment activities, although domestic stimulus policies are providing some buffer from the downside,” said Chaoping Zhu, a global market strategist for JP Morgan.

The latest growth (and trade) figures suggest China’s economy is slowing even more as we enter 4Q. In fact, according to Lipper Alpha Insight’s China Momentum Indicator (CMI) 2.0, the latest China GDP was likely at 4.2%, a third below the official print.

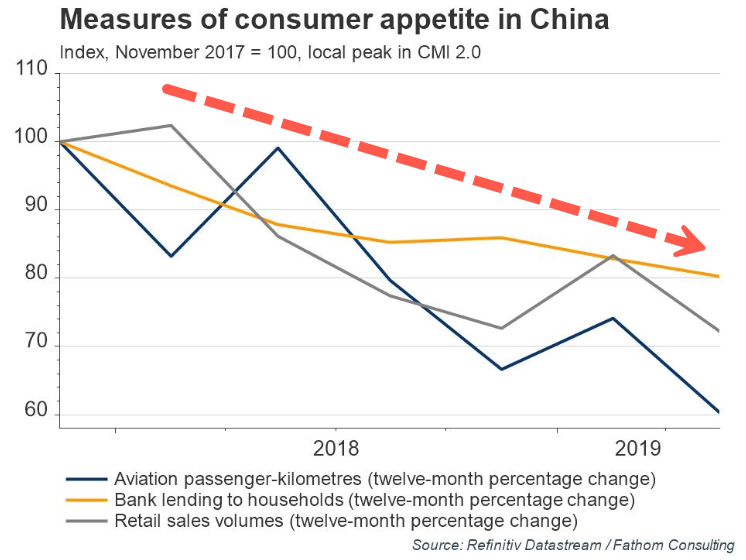

Lipper Alpha Insight told their clients that the slowdown in China’s economy isn’t a “consequence of rebalancing; China abandoned its half-hearted attempt to reform the economy in a bid to cushion the slowdown last year. Recent measures of consumer appetite have reinforced this message. Retail sales, bank lending to households and aviation passenger numbers have all slowed since the end of 2017 (when our CMI last peaked), despite being key indicators of a more consumer-led economy.”

Lipper Alpha Insight adds that while the “pursuit of growth at the expense of reform is the wrong medicine; it will work for a time, but allocative inefficiencies and diminishing returns mean that unless something changes China is destined for perennially lower economic growth. This idea is reflected in our forecast, with the path into the future expected to be one that winds to and fro, with key events likely to intensify China’s prioritization of growth, regardless of the long-term cost.”

To be sure, this is something we have flagged repeatedly in recent weeks, when we pointed out that despite its best efforts, China is no longer able to reflate its all too critical credit impulse, which can barely stage a rebound from multi-year lows and appears to already be fading lower.

With that in mind, it is hardly a surprise that as Bloomberg reports, China’s policymakers are preparing for two key meetings in the coming weeks with fresh evidence that sooner rather than later, the GDP number will start with a 5-handle.

The People’s Bank of China Governor Yi Gang responded over the weekend to the deterioration in 3Q GDP data. Gang didn’t hint at more stimulus but said China would keep its debt situation under control. As seen in the chart below, China’s attempt to clean up imbalances and financial risk in the economy is being done through an increase in social credit by reducing off-balance-sheet risks.

Yi’s comments are setting the scene for a meeting of the Politburo, the Communist Party’s top leaders, and the ensuing Fourth Plenum of the Party’s Central Committee, a broader gathering that may mull longer-term questions of economic policy. While those events could produce a shift away from the current targeted, moderate stimulus regime, there have been few signals to date of any change.

Yao Wei, the chief China economist at Societe Generale in Paris, told reporters at the IMF meetings last week that Chinese leaders are “looking at a very long horizon,” and the intermediate fluctuations above or below 6% aren’t important at the moment.

“They measure the policy scope by looking at the overall debt, by looking at how much risk there is in shadow banking, in the housing sector and in inflation,” Yao said. “Looking at all these things, they judge they actually don’t have much scope from a long-term perspective. So they’re very careful about how to use it and when to use it.”

With growth estimates in China missing the mark in 3Q, it’s likely slippage below 6% could be seen in 4Q, as there is no indication that China, nor the global economy is turning up at the moment. There are some positive factors when it comes to the recent trade truce, or at least that’s what the market believes. Still, as we have repeatedly discussed, the global slowdown didn’t start because of the trade war but due to residual problems within China’s massively overlevered economy, so any resolution will likely only boost global growth for a brief period.

Bloomberg data shows China’s full-year expansion for 2019 to come in around 6.2% and will slow to 5.9% in 2020.

China can cut interest rates and unleash higher doses of monetary policy. But the problem China is running into today, as explained in our report Sunday night, is that monetary stimulus is becoming less effective than ever before.

As the world awaits the upcoming Politburo meeting for economic clarity and a medium-term outlook from Chinese leaders, China’s economy is rapidly deteriorating and will likely fall underneath 6% in the quarters ahead, and could even register full-year growth rates for 2020 under 6%.

The world, led by China, has already entered a new phase of below-trend growth, it’s just that equity markets haven’t yet figured this one out.

Blain: “I Am Convinced The Debt Markets Are About To Blow Up”

Blain’s Morning Porridge, submitted by Bill Blain of Shard Capital

“If you wake up on a Casper mattress, work out with a Peloton before breakfast, Uber to your desk at a WeWork, order DoorDash for lunch, take a Lyft home, and get dinner through Postmates, you’ve interacted with seven companies that will collectively lose nearly $14 billion this year.”

It’s a big week for markets with the ECB meeting, some critical Q3 stock numbers and a host of things to worry about in terms of economic releases and the continuing slowing of the Chinese economy. Its all critical stuff for the bond market – which I reckon is a ticking time-bomb. But more about that later… For stock markets, the quote this morning sums it up – the mood is changing: forget the disruptive tech unicorns and focus on fundamentals. But, first up we really can’t ignore the Brexit mess in the UK. Saturday’s SNAFU gives investors another chance to load up on Sterling. At some point Brexit will be fixed. It might be messy.

Brexxxxxxiiiiitttt…..

I am sure foreign readers are wondering how the Mother of All Parliaments is making such a Horlicks of the Brexit negotiations. It really doesn’t look good does it? On the other hand, it does show the vibrancy of our political process, and the fact individuals can force it to change. It’s just a shame so many of these individuals seen to be self-seeking egotistical numpties of the worst kind – but even Oliver Letwin has a mother that probably loves him.

The reason Brexit is so messy is simple. It boils down to weak government – which is a recent thing here in the UK. As soon as the Tories lost their working majority in Theresa May’s ill-advised and badly conceived 2017 general election, the process fell hostage to individuals thinking they could save the country from its misguided referendum decision, and political calculators cynically working out how best to way-lay and embarrass the May and now Johnson Government. (Easy for the Labour party to chop/change policies and promise Brexit one-day and a referendum the next – why? Because nobody cares about them..)

As parliament tends to attract political types who sincerely believe the Public desperately needs to know their opinions (in detail), the egotistical pond life than inhabits the green benches has taken every opportunity to frustrate, delay, push-their-own-agenda, and conflabulate the process. That’s how an idiot-savant like Oliver Letwin was able to hi-jack the vote and kill it on Saturday. The result is the massive uncertainty of Brexit – which is the real issue damaging the economy, making voters apoplectic, management uncertain and peeving everyone.

Relax – long-term it does not matter.

In a few years time, after Brexit finally happens (because even if the Remoaners get their second vote, Europe wants us out), then the effect on the UK economy will be a minor plus or minus. We will not notice. The UK and Europe will not be riven for eternity. We will adjust, we will still trade between each other. We will still scream at dirty French play in the Six Nations rugby, (yes, I am thinking of Vahaamahina on Sunday.) We will still drink German beer, eat French cheese and take holidays in Spain.

From the rhetoric, you’d think Brexit was the End of the World. It’s not. It’s political process. They do say: “Democracy is the worst form of government, except for any of the alternatives”. So get over it, get set to buy sterling and UK domestic stocks on the likelihood that speaker John Bercow will frustrate the vote today and cause sterling to tumble. Buy the dip. Boris may lose every battle, but in the long-term the Tories will win an election, and the UK will get a Brexit which will ultimately change the World by a tiny infinitesimal fraction..

We are fortunate to have a vibrant political system that questions, objects and demands answers. Would you rather be part of something more somnambulant? (As one Brexiteer explained to me: We joined a simple trade agreement with open borders to the world, but that mission-crept into a closed economy heading towards an unlikely political union bound together in common currency that shackles most countries to perpetual penury, in a system designed and promoted by the French to pursue their 400 year historical goal of European hegemony?)

Brexit is a change in our foreign relations – which happens all the time across the globe. Politicians throwing numbers plucked from no-where about how much damage it will do are just guesses. Nothing more. Lets move on..

The Ticking Time Bomb in the Debt Markets

I am more and more convinced the Debt Markets are about to blow up. It will start with a small wobble. Perhaps a small hint that anticipated global recession isn’t/won’t be so bad, or further acknowledgement Central Bank experimental monetary policy hasn’t worked and they won’t continue to slash rates and institute QE on every chill economic wind. Or maybe it will start with a trickle of investors looking to sell corporate debt, discovering just how illiquid the market is and panicking, causing a massive avalanche of bond misery.

If/when any of these happen, then bond market holders will be left holding massive losses on low yielding assets. Will it trigger crisis? Most of the risk that caused the 2008 crisis was held by banks. Over the past 10-years the bulk of that risk has been transferred out the banks into fund management – real money insurance and pension savings.

How willing will central banks be to bail the system when an immediate banking crisis, (except in Europe, because there is bound to be a banking crisis in Europe, because that’s just how it is..), is not such a threat?

And, although investors will take losses, these will largely be mark-to-market and income rather than default – meaning investors get hosed, lose money but don’t lose everything. It will hurt and it will cause retail investor fury… if they understand why! (Clue – blame central banks!)

Stocks

The big stock to watch this week will be Boeing. The moment to buy will be when they sack the management. The negative thesis that Boeing had effectively “captured” the Federal Aviation Authority and pushed thru an unsafe B-737 Max has been in the market for months. Now it looks like there is truth in the rumors – with a smoking email from a test pilot about “Jedi-mind tricks on regulators”. Boeing has already demoted Dennis Muilenberg from Chair/CEO to CEO. When he’s out the door, put your buying boots on.

US Futures Rally As Trade Deal, Brexit Optimism Return Despite Prevailing Chaos

One day after US stocks ended last week on the back foot amid growing uncertainty over Brexit, the ongoing trade talks on “Phase one” deal between the US and China and signals of a global slowdown, world stocks and US futures have rebounded, with risk sentiment boosted as the “ole’ faithful” – optimism in trade talks – made a return, with the added kicker of resurgent hopes that Britain will avoid a disorderly exit from the European Union gave cause for riskier bets, even though Saturday’s events in the UK showed that BoJo is anything if in control of the process.

Global markets started off the new week, the second busiest in Q3 earnings season, on the front foot, with MSCI’s world equity index rising 0.2%, with the broad Euro STOXX 50 adding 0.4%, led by mining and banking shares. Major European bourses are modestly firmer after risk sentiment turned more constructive following AsiaPac indecisiveness, during which the latest developments (or lack thereof) on the Brexit front and the PBoC’s decision not to cut Loan Prime Rates contributed to the cautious tone. The FTSE 100 (+0.1%) lags amid a stronger Pound on hopes that the worst possible Brexit outcomes are off the table and that PM Johnson may have enough backing for his Brexit deal. Sectors are mostly in the green, apart from defensives, with Consumer Staples (-0.6%), Health Care (-0.5%) and Utilities (-0.2%) all lagging on improved risk appetite.

The positive mood mirrored gains for Asian stocks earlier in the session. MSCI’s broadest index of Asia-Pacific shares ex-Japan rose 0.3%, with Chinese shares gaining 0.3%. The Asian advance was led by financial and industrial firms, as traders awaited quarterly earnings and a Brexit deal that’s still up in the air. Markets in the region were mixed, with Japan advancing and Australia retreating. The Topix rose 0.4%, supported by services, telecommunications and banking shares. The Shanghai Composite Index erased earlier losses to close 0.1% higher, with large lenders and insurers among the biggest boosts. China’s economy may be ready to stabilize despite recent warning signs, according to some economists.

In the US, S&P500 futures nudged up, pointing to a firm open that would keep American stocks still within sight of a fresh all-time high.

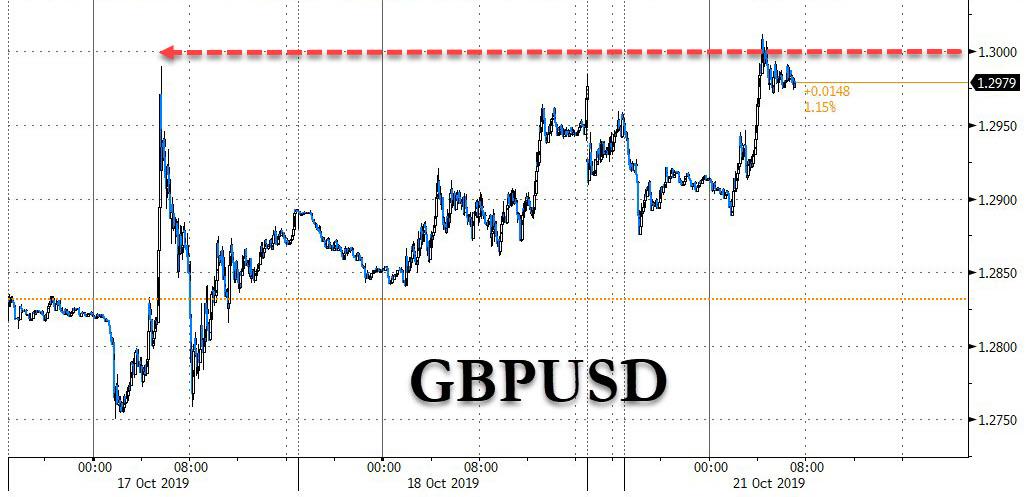

Appetite for riskier assets was supported as markets judged the chances of a disruptive “no deal” Brexit as lowering, even after Britain’s parliament delayed a vote on Prime Minister Boris Johnson’s deal to exit the EU. As reported earlier, BoJo will seek to put his Brexit deal to a vote on Monday, with the government proposing a debate on the agreement. Parliament was due to open at 1330 GMT. It was unclear, though, whether parliament’s speaker would allow a vote to go ahead; for now however traders bought the pound first and would ask questions later, with cable rising as high as 1.30 before, the highest level since May, a long-term resistance level, before paring back some of the move.

As a reminder, on Saturday, the UK Parliament vote on a Brexit deal was postponed after lawmakers voted (322-306) in favor of passing the Letwin amendment which withholds approval of the Brexit deal until legislation to ratify it is passed and which effectively forced PM Johnson to request a Brexit extension to January 31st under the Benn Act. Following this, PM Johnson stated that the legislation will be tabled in the upcoming week and sent a letter to the EU requesting a Brexit extension which he did not sign, while he sent 2 other letters where he stated that the extension request was from Parliament and urged the EU not to grant the extension. UK PM Johnson could be held in contempt by Scottish Court for urging EU leaders to ignore a letter asking for an extension to Brexit. Scotland’s most senior judge, Carloway, alongside two other judges will hear the allegations today. UK de facto Deputy Gove has triggered official contingency plans for a no-deal Brexit in an attempt to pressure MPs into backing PM Johnson’s Brexit deal. Elsewhere, the UK Government are reportedly drawing up plans for an election as soon as November 28th.

Daily Telegraph’s Political Correspondent Yorke tweeted that a senior DUP figure said the party could back a customs union amendment to the WAB in order to ensure whole of the UK leaves EU under the same customs arrangements and that the party will discuss issue over next 24-48 hours, while he added that another DUP figure said they’ll unleash guerrilla warfare in Parliament to block the Brexit deal unless Boris Johnson goes back to Brussels and addresses their concerns with the party said to be looking at multiple options this week.

Earlier in Asia, investors were boosted by Chinese vice premier Liu He’s comments on Friday that Beijing will collaborate with the United States to address mutual concerns on the trade war. President Trump on Friday also struck an optimistic tone, saying he thought a trade deal would be signed before an Asia-Pacific Economic Cooperation meeting in Chile next month.

“They seem to making progress,” said Jeremy Gatto, an investment manager at Unigestion in Geneva. “But we have seen in past that everything seems to look great and then a couple of days later seems to deteriorate again.” The 2020 U.S. presidential election was also influencing the talks, investors said, with Trump looking to avoid the possibility of tariffs imposed by China impacting his voting base. “Trump realizes that some of the tariffs that potentially could be implemented towards the end of the year could affect the consumer, which would be bad for the U.S. economy – and obviously bad for him,” Gatto said.

“It would be significant if they can get a phase one deal signed before Thanksgiving — the probability of that is probably a little bit over 60% right now,” Brett Ewing, chief market strategist at First Franklin Financial Services, told Bloomberg TV. “This is a very important issue, and I think it could remove a lot of uncertainty.”

Markets are also gearing up for high-profile earnings reports this week. Earnings season continues with a large number of releases taking place next week. On Tuesday, there’ll be Procter & Gamble, Novartis, McDonald’s, Texas Instruments, United Technologies and UBS Group. Wednesday will see Microsoft, Boeing, PayPal, Caterpillar and Ford announce results. On Thursday, there’s Amazon, Visa, Intel, Comcast, AstraZeneca, Royal Bank of Scotland, Nordea Bank and Twitter. And on Friday, announcements come from Verizon Communications, Anheuser-Busch InBev, Charter Communications and Barclays.

As noted above, in FX it was all about the pound, which had surged to $1.3015, recovering earlier losses of half a percent against the dollar. Sterling had by Friday risen by up to 6.5% in seven trading days to a five-month high, as a furious short squeeze underscored market expectations that either a deal or delay was most likely. As we reported on Sunday, Goldman Sachs said it now sees the chance of a no-deal Brexit reduced to 5%, from 10% previously.

Still, some investors said that sterling’s medium-term prospects were limited, even if no deal is avoided.

“I wouldn’t be too bullish because there is still going to be a huge amount of uncertainty going forward, even if the current deal is agreed,” said Tim Drayson, head of economics at Legal & General Investment Management. “If this deal does go through, ultimately it is still a relatively hard Brexit – we are out of the customs union – and it is still a deterioration in the UK terms of trade.”

Elsewhere, the dollar weakened against most G-10 peers as the week started with a pickup in risk sentiment.

In rates, Treasuries and euro-area bonds dropped as disagreements surfaced over next year’s budget, while gilts fall amid growing optimism that a Brexit breakthrough is possible. BTPs bear steepened, 10-year yields rising 5bps to 0.98%, reaching the highest since Sept. 12 ahead of a coalition meeting in Rome Monday. At the same time, Gilts slumped as U.K. PM Johnson attempts to put his Brexit deal to a vote in Parliament, with the U.K. 10-year yield climbing as much as 7bps to 0.78%.

In commodities, oil prices largely held steady on Monday, recouping some early losses as investors took stock of global economic pressures that could impact oil demand. Global benchmark Brent crude oil futures were down 12 cents to $59.35 a barrel.

There are no major economic announcements today; Halliburton, Lennox, and Celanese are reporting earnings today.

Market Snapshot

S&P 500 futures up 0.2% to 2,995.00

STOXX Europe 600 up 0.3% to 393.07

MXAP up 0.3% to 160.04

MXAPJ up 0.4% to 514.63

Nikkei up 0.3% to 22,548.90

Topix up 0.4% to 1,628.60

Hang Seng Index up 0.02% to 26,725.68

Shanghai Composite up 0.05% to 2,939.62

Sensex up 0.6% to 39,298.38

Australia S&P/ASX 200 up 0.04% to 6,652.51

Kospi up 0.2% to 2,064.84

German 10Y yield rose 4.2 bps to -0.34%

Euro up 0.09% to $1.1177

Italian 10Y yield rose 3.6 bps to 0.586%

Spanish 10Y yield rose 4.2 bps to 0.287%

Brent futures down 1.2% to $58.71/bbl

Gold spot little changed at $1,490.40

U.S. Dollar Index little changed at 97.23

Top Market News from Bloomberg

Asian equity markets began the week with a cautious tone following last Friday’s lacklustre close on Wall St and amid continued Brexit uncertainty. ASX 200 (Unch) and Nikkei 225 (+0.3%) were mixed with Australia dragged by underperformance in the tech sector. However, resilience in the property and mining sectors has limited the losses in Sydney, while Tokyo sentiment was kept afloat by mild JPY weakness as a larger than expected contraction in exports ata added to the pressure for the BoJ to act. Hang Seng (Unch) and Shanghai Comp. (+0.1%) conformed to the indecision after the PBoC injected liquidity via open market operations but refrained from anticipated cuts to its Loan Prime Rates, with Hong Kong also mildly underpinned after China revised rules to permit mainland investors to trade Hong Kong-listed dual class shares through the Stock Connect. Finally, 10yr JGBs are lower in which prices retested prior support around the 154.00 level and with demand subdued as Japanese stocks remained afloat, although downside was stemmed amid the BoJ presence in the market for JPY 1.16tln of JGBs in up to 10yr maturities.

Top Asian News

China Braces for Sub-6% Economic Growth in Key Policy Meetings

Temasek Offers to Buy Control of Keppel for About $3 Billion

Xiaomi’s Long Suffering Shareholders to Get Mainland Boost

China Banks Unexpectedly Keep Loan Prime Rate Steady in October

ESR Seeks $1.45 Billion in Year’s Second-Biggest H.K. IPO

Major European Bourses (Euro Stoxx 50 +0.4%) are modestly firmer after risk sentiment turned more constructive following AsiaPac indecisiveness, during which the latest developments (or lack thereof) on the Brexit front and the PBoC’s decision not to cut Loan Prime Rates contributed to the cautious tone. The FTSE 100 (+0.1%) lags amid a stronger Pound on hopes that the worst possible Brexit outcomes are off the table and that PM Johnson may have enough backing for his Brexit deal. Sectors are mostly in the green, apart from defensives, with Consumer Staples (-0.6%), Health Care (-0.5%) and Utilities (-0.2%) all lagging on improved risk appetite. In terms of individual movers; Wirecard (+8.2%) shares spiked higher on the news that the Co. had decided to commission an independent audit relating to the recent allegations made by the FT. Smith and Nephew (-8.0%) sunk after the Co.’s CEO stepped down. Micro Focus (-5.6%) fell on after Open Text confirmed that it is not considering a potential acquisition. Meanwhile, strong earnings saw SAP (+1.7%) move higher, while weak earnings saw Just Eat (-6.5%) head lower. Prudential (-8.2%) shares took a dive on the news that the Co. is to split its UK business (M&G Business) from its Asia operations today. Finally, Osram (-0.4%) shares were initially supported by an upgrade to buy at Commerzbank and after AMS (+4.9%) confirmed its offer for the Co. whilst lowering its minimum accepted threshold, whilst Pearsons (+0.1%) was upgraded to hold from sell at Deutsche Bank.

Top European News

Wirecard Shares Jump After Hiring KPMG for Independent Audit

Swiss Greens Surge at the Expense of the Anti-Immigrant Right

Berlin Freezes Rents in Landmark Plan to Tackle Cost Spiral

M&G Starts Trading in London at Low End of Analyst Estimates

In FX, sterling has staged a strong comeback from post-super Saturday lows amidst increasingly bullish calls for the Pound and more bouts of short covering on the premise that the risk of a hard Brexit is declining with every move by UK Parliament to assume control of proceedings and/or force another Article 50 extension. Cable snuffed out stops around 1.3000 after eclipsing last week’s 1.2990 peak, but topped out around 1.3012 and Eur/Gbp retreated through 0.8600, though the cross held above last Thursday’s 0.8575 base as the single currency climbed alongside its UK counterpart.

NZD/AUD – Although Sterling’s resilience awaiting PM Johnson’s next move and attempt to put his WA to the HoC is noteworthy, the Antipodean Dollars are outperforming and extending their recovery gains vs the Greenback as the Kiwi climbs above 0.6400 and Aussie nudged over 0.6875. The improvement in US-China trade relations and less dovish on balance near term RBNZ and RBA policy outlooks have underpinned the Nzd and Aud, while the YUAN is also maintaining momentum with the aid of steady PBoC mid-point fixes.

CAD/EUR/CHF/JPY – The Loonie is benefiting from broad Buck weakness, as Usd/Cad eyes 1.3100 and support residing just ahead of the big figure, while the DXY has declined through 97.280 Fib support to fresh sub-97.200 lows and closer to the next downside chart target before 97.000 even (97.033 lows from August). Not much sign of Canadian election jitters or pressure via the ongoing retracement in crude prices, with Tuesday’s retail sales data expected to reveal stronger consumption. Elsewhere, Eur/Usd has been tracking Cable as noted above, but also buoyed by higher Eurozone debt yields on its way up towards 1.1180 and conscious of decent layered option expiry interest from 1.1120-30 (1 bn) through 1.1150-60 (1 bn) to 1.1200 (1.1 bn), while the 200 DMA is also in close proximity (1.1209). Conversely, the Franc and Yen are lagging on mild risk-on trade and safe-haven unwinding, as Usd/Jpy and Usd/Chf pivot 108.50 and 0.9850 respectively after weaker than forecast Japanese trade data overnight and a decline in weekly Swiss sight deposits.

NOK/SEK/TRY – The Scandi Crowns are both clawing back losses amidst the aforementioned risk positive tone, and also consolidating ahead of Thursday’s Riksbank and Norges Bank meetings that preface the ECB convene and could see the former retain guidance for tightening around the turn of the year. Eur/Nok has retreated from new record highs around 10.2440 to sub-10.1900 and Eur/Sek has pulled back further from peaks over 10.9300 to just under 10.7300 at one stage. However, geopolitical jitters have resurfaced to blight Turkey’s Lira after initial relief in wake of the 5-day ceasefire in Syria, with Usd/Try back above 5.8200 in advance of this week’s CBRT rate decision (also on Thursday and contributing to a Central Bank fest) and weighing up whether 1-week repo will be cut again, and if so by how much.

In commodities, crude markets are lower, but choppy, after risk sentiment seemingly took a turn for the better in early trade, although some downside was seen later in the session with no immediate fundamental catalysts of note. The recent downside took WTI Dec’ 19 futures back below the 54/bbl mark whilst its Brent counterpart lost the 59/bbl handle after initially consolidating around USD 59.50/bbl region during APAC/early EU trade. In terms of supply news, media reports alleged that Saudi Arabia and Kuwait are expected to sign an agreement within 45 days which would see oil production resumed at the neutral zone; and see production at the jointly run fields of Khafji and Wafra reopen following four years of closure amid an ongoing dispute between the two countries. Around 500mln BPD could be brought back online, however, ING note that given that both Iraq and Kuwait are part of the OPEC+ production cut deal, it should not have an impact on overall oil supply for the time being. On the geopolitical front, US Defence Secretary Esper noted that US troops in Syria are with SDF to deny access of oilfields to ISIS and others, but no decision has yet been made about keeping the troops there. Moving on to metals; Gold is slightly lower, but sits well within recent ranges, after the precious metal failed an early bid to get substantially above its 10DMA at 1493/oz. Copper, meanwhile, remains a beneficiary of the mostly weaker buck, despite a lack of decisive PBoC action overnight.

US Event Calendar

Nothing scheduled

DB’s Jim Reid concludes the overnight wrap

The next 36 hours will be absolutely crucial in the whole Brexit saga…. hang on… I’m sure we’ve said that about 12 times in the last year. Perhaps this time it’s true but don’t hold all of your breath. There’s little point going through the whole twists and turns of Saturday other than to say that the Government’s Brexit deal vote was blindsided by an amendment that said they could not attempt to pass the deal until all the legislation had gone through Parliament. This was meant to shore up the defences against no-deal and forced PM Johnson to write an (unsigned) letter to the EU asking for an extension. He sent this with another letter saying that in reality he doesn’t want one and doesn’t think the U.K. needs it or is best served by it. If we take a step back the situation is actually more positive for the government than it was on say Thursday/Friday of last week but they have lost some momentum. Back then it was slowly swinging towards the PM’s deal but it still looked like it would fall slightly short whereas it actually probably would have passed had the main vote been held on Saturday.

Although the PM lost the amended vote by 322 to 306 that essentially means that only 8-9 need to now vote for the deal for it to go through. Given that a few of those that voted against the government on Saturday have already publicly stated that they will now vote for the deal given they now feel more certain that a no-deal is off the table, there is a decent chance the deal can still pass through Parliament. There are a few massive caveats below however.

It seems the government will try to have another meaningful vote today but there seems to be a high probability that the speaker won’t allow it as it would be essentially the same bill as Saturday’s which is not technically allowed. If so we will likely move onto Tuesday where first the government is expected to put the program motion with the timetable of events to try to pass the deal. This could be the first obstacle. Then when they try to bring the legislation through, the amendments will come thick and fast with the main ones likely being a confirmatory referendum on the deal and one on membership of the customs union. It’s not clear that the numbers are there for either but the second one is more likely, might get momentum, and would be something the current government is highly unlikely to accept which in turn might encourage more to vote for it. As such if this goes through expect the bill to be withdrawn and we’ll be back at square one – albeit with a no-deal Brexit being much less likely than it was two weeks ago

It’s possible that the lure of customs union membership may sway those who were going to vote for the PM’s bill out of there being no alternative. It may also attract those who have no interest in that but see it as the best way of stopping the PM’s bill going through. So it could be a lightning rod. So it’s possible that the Government’s deal loses a little of the momentum it had last week when MPs felt that they had to agree to it for lack of alternatives. We also have to take into account any response from the EU to the request for a delay. The most likely scenario is that the EU stays fairly quiet until they see what Parliament does and hoping that no response might encourage some MPs to go for the deal in case an extension isn’t offered. Ultimately it probably will be though. It’s also not impossible that there’ll be a vote of no confidence finally now that no deal has been ruled out (assuming the EU are onside). However the government (and ex Tories) are unlikely to support that if there’s a deal on the edge of passing. Confused? You’re not alone.

We still think most scenarios point towards a deal, a softer Brexit, an election or a second referendum (with a deal on the table) and as such any dips in Sterling should be a buying opportunity. However strange unexpected things continue to happen and what we’ll be talking about in tomorrow or Wednesday’s EMR is very much up for grabs.

This morning in Asia, Sterling is down around -0.6% and is relatively calm for now. Elsewhere markets are making modest advances in thin trading with the Nikkei (+0.37%), Hang Seng (-0.32%), CSI (+0.31%) and Kospi (+0.11%) all up. Futures on the S&P 500 are up +0.25% while oil prices are down c. -0.30%. As for overnight data releases, China’s October 1 year and 5 year loan prime rates both came higher than consensus at 4.20% (vs. 4.15%) and 4.85% (4.83%) respectively. Meanwhile, Japan’s September trade balance stood at JPY -123.0bn (vs. JPY -54.0bn expected) with imports declining by -1.5% yoy (vs. -2.8% yoy expected) while exports declined -5.2% yoy (vs. -3.7% yoy expected).

In other weekend/ overnight news, China’s Vice Premier Liu He said that “China and the U.S. have made substantial progress in many aspects, and laid an important foundation for a phase one agreement,” while reiterating that China is “willing to work in concert with the U.S. to address each other’s core concerns on the basis of equality and mutual respect.” Staying with China, the National Development and Reform Commission’s spokesman Yuan Da said overnight that growth volatility is acceptable if other targets on new jobs, residential income and environment protection could be met while adding that the statement that China’s economy is going through severe slowdown is “unfounded”. Elsewhere, the Greens overtook the Christian Democrats in Switzerland elections to become the fourth-strongest party in parliament’s 200-member lower house, and the Green Liberal Party (GLP) also increased its share of the vote, meaning that the two now control about a quarter of the chamber (44 seats). Meanwhile, the euro-skeptic Swiss People’s Party (SVP) is set to lose 11 seats, according to state broadcaster SRF, as voters got swayed by environmental concerns. This is a trend that looks set to continue in the years ahead.

Outside of Brexit there’s a lot going on this week including the release of the crucial preliminary PMI readings for October (Thursday), Mario Draghi’s final ECB meeting as President (also Thursday), and earnings season gathering momentum with a large number of releases due.

Given how poor the PMIs have been over the last two months (with services catching down) the preliminary PMIs on Thursday will be potentially pivotal. Manufacturing has been doing particularly poorly, with the German PMI falling to 41.7 in September, its lowest reading since June 2009, while the Eurozone manufacturing PMI was also deep in contractionary territory in September at 45.7, the lowest reading since October 2012. The consensus expectation is for a modest rise in both the manufacturing and the services PMIs for the Euro Area, with the consensus expecting a 46.0 reading in manufacturing and a 52.0 reading in services. The US equivalent numbers will also be scrutinised for any signs that the “phase one” US/China handshake has made any very early impact.

The main central bank event next week comes from the ECB, who’ll be deciding policy on Thursday with a quiet one expected on Draghi’s last outing. The press conference will be his last opportunity to push the direction of the debate and it’ll be interesting to see the word count for the word “fiscal”. In terms of Fed speakers, it’s a light week as we enter a blackout period ahead of the next FOMC meeting on October 30th.

Other data releases to look out for include Thursday’s US preliminary durable goods orders for September along with September’s new home sales reading. Finally, Friday will see the release of the University of Michigan’s final consumer sentiment index for October, along with the current conditions and expectations readings. The preliminary release saw consumer sentiment rise more than expected to 96.0 (vs. 92.0 expected).

Earnings season continues with a large number of releases taking place next week. On Tuesday, there’ll be Procter & Gamble, Novartis, McDonald’s, Texas Instruments, United Technologies and UBS Group. Wednesday will see Microsoft, Boeing, PayPal, Caterpillar and Ford announce results. On Thursday, there’s Amazon, Visa, Intel, Comcast, AstraZeneca, Royal Bank of Scotland, Nordea Bank and Twitter. And on Friday, announcements come from Verizon Communications, Anheuser-Busch InBev, Charter Communications and Barclays.

Reviewing last week now, the “positive” Brexit news dominated attention last week, helping most global equities to rally. The S&P 500 and STOXX 600 gained +0.54% and +0.06% (-0.39% and -0.32% Friday), respectively, and the moves had a distinct cyclical tilt. Bank stocks gained +2.69% and +2.67% in the US and Europe (+0.43% and +0.12% Friday), while an index of utilities shares dropped -0.14% (+0.37% Friday). The moves retraced a bit on Friday, as some trade pessimism resurfaced when the White House announced the Vice President Pence will give a speech about China on Thursday. Will this be his long anticipated hawkish speech that’s been postponed previously? Semiconductor shares fell -0.06% on the week (-1.06% Friday), as some indeed expect him to be confrontational. The DOW fell -0.17% (-0.95% on Friday), dragged down by Boeing’s -8.19% fall (-6.73% Friday) as reports indicated that company employees had concerns about the 737 MAX plane as early as 2016.

Government bonds sold off again last week, with 10-year yields up +2.5bps and +6.0bps in the US and Germany (+0.2bps and +2.6bps Friday). The front-end treasury curve rallied -1.8bps, however (-2.6bps Friday), on firmer expectations for Fed rate cuts. Vice Chair Clarida gave the final Fed comments before their pre-meeting blackout period, and he continued to emphasize “evident risks” to the outlook, saying nothing to push back on market pricing. The market is now just about fully priced for a cut at the October meeting, plus around a 40% chance for another cut in December. That helped the dollar to weaken -1.18% (-0.48% Friday), which came despite euro and pound strength. Those currencies gained +1.13% and +2.49% (+0.38% and +0.72% Friday) amid the positive Brexit news.

{kind=link}

{kind=link}