Watch Live: President Trump Enters Media Thunderdome For Ukraine-Biden Q&A

For the second time today, President Trump will stand behind a lectern outside the UN General Assembly and face down the Washington Press Corp and international press corp during a 4 pm news conference.

Unlike President Trump’s last-minute press conference with his Ukrainian counterpart Volodymyr Zelensky, where the Ukrainian leader backed up Trump’s narrative about a July phone call that is at the center of the latest impeachment furor in Washington, this one has been on the schedule for a while, and is ostensibly intended for Trump to offer some thoughts on the UNGA.

Trump is set to begin speaking at 4 pm ET, just as the acting DNI is supposed to turn over a copy of the whistleblower complaint that led to allegations that Trump threatened to withhold military aide to Ukraine unless Zelensky agreed to investigate the Bidens.

While the earlier presser was mostly Zelensky’s show, as he assiduously backed the president, expect that Trump will be entering the media thunderdome this time around, and will be peppered with questions about whether he tried to recruit the president of Ukraine into manipulating an American election – a narrative that the left is already running wild lift.

We wouldn’t be surprised if Trump is simply pelted by different versions of the same question: “did you coach Zelensky to back you?”

As many of you are aware, I am usually an equity bull. Let’s face it, over time, stocks often rise and it’s difficult to fight that tendency.

Yet the trader-in-me believes the time to lean against this propensity is upon us. I have abandoned my US long equity positions, and am leaning short on a trading basis.

Why the shift in tone? Let me sketch out the worries that have finally overwhelmed my desire to stick around for the last innings of this party.

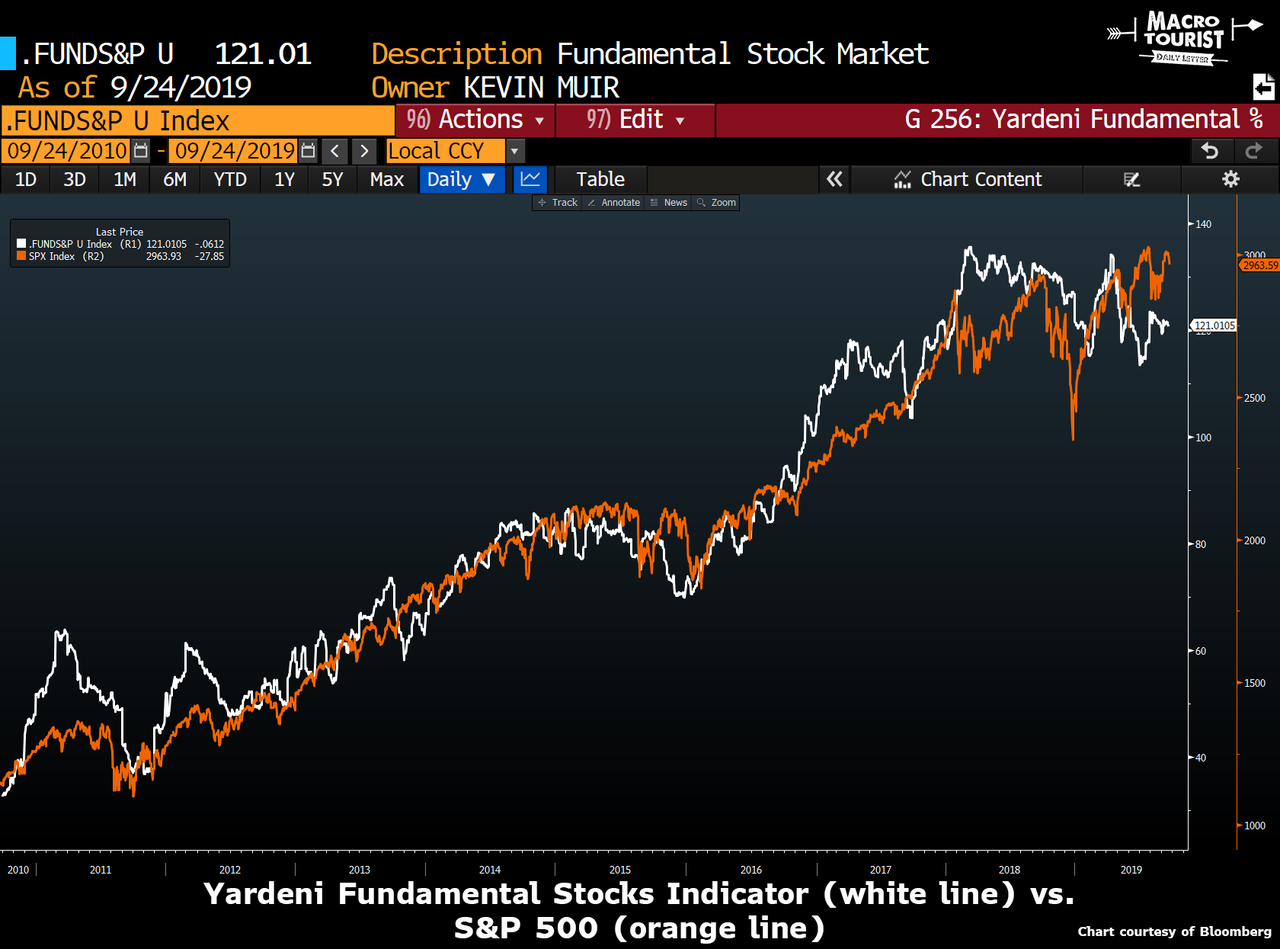

Yardeni’s hint

One of my favourite indicators is Ed Yardeni’s “Fundamental” Stock Indicator. I have written about it in The Best Unknown Indicator and Obi-Ed’s Magical Indicator so there is no need for me to rehash all the details. Needless to say, I have learned the hard way not to disregard this signal. When either series diverge, it seems like it’s only a matter of time before they converge again.

Even though the S&P has been pushing to new highs, Yardeni’s indicator refuses to join along. Why is that?

Well, the indicator has three main inputs – employment, consumer confidence and CRB Raw Industrial commodities.

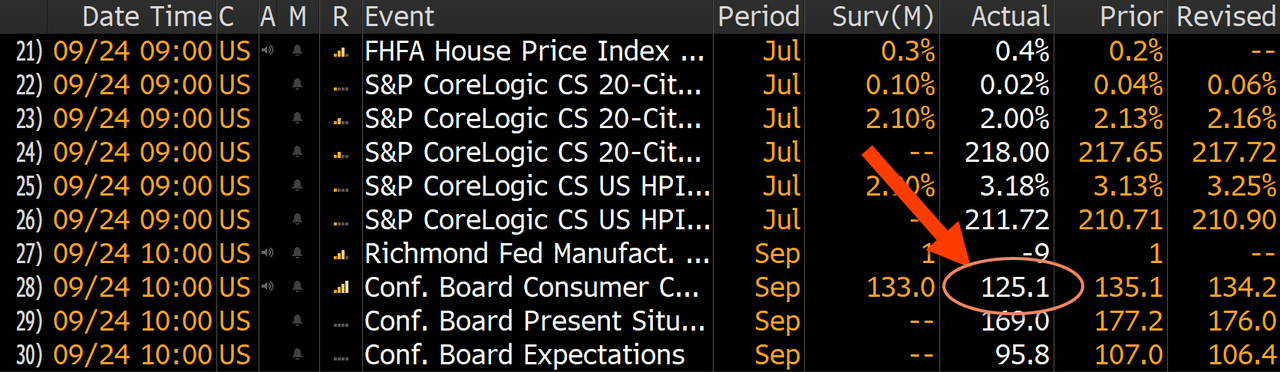

Initial jobless claims have been well behaved and show no signs of faltering. Consumer confidence had been resilient, but today’s release showed the first potential cracks.

But what has me most worried is the CRB Raw Industrial Commodity Index.

These commodities represent the building blocks of the global economy. It’s tough to get robust economic growth with the CRB Raw Industrial Commodities Index bumping along the lows.

Without a rally in this index, I don’t see how Yardeni’s indicator moves higher to close the gap, and therefore I worry that it resolves with the S&P 500 heading lower.

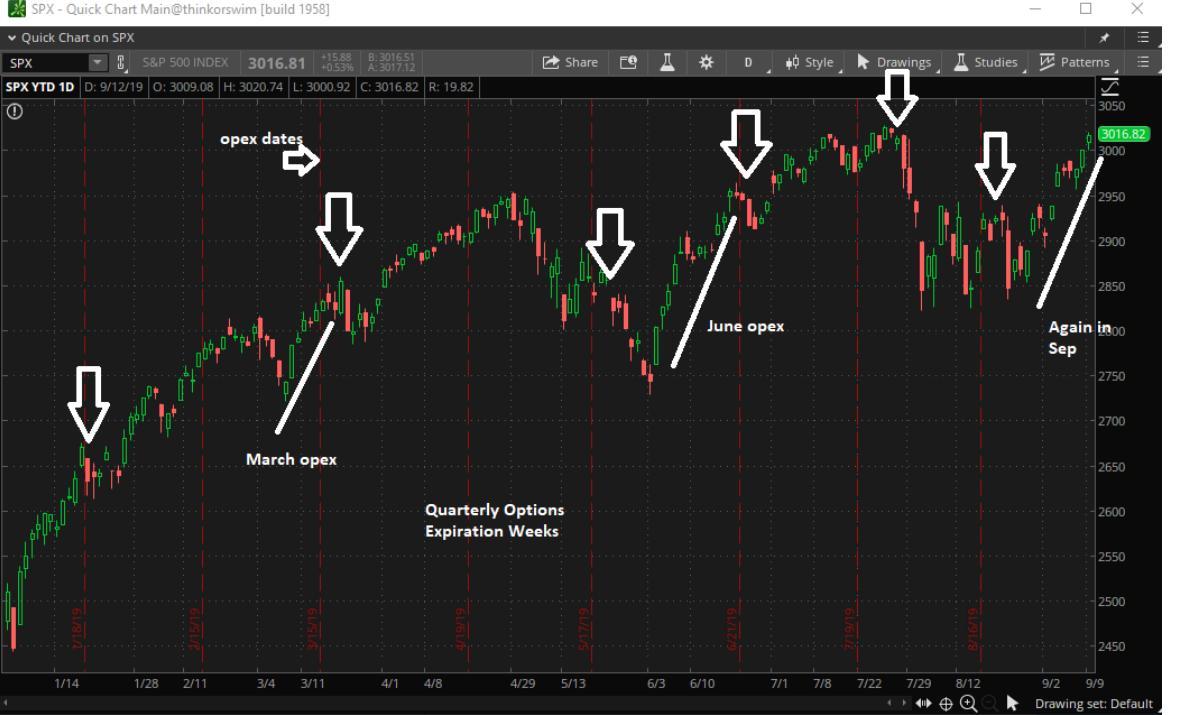

Seasonal triple-witching expiry weakness

Next up in my list of worries is the fact that we have just passed a triple-witching quarterly expiry – a point of time that has lately often been followed with stock market weakness. Here is a great chart by Scott Murray of @VolatilityWiz fame which highlights the S&P 500’s tendency to run up into expiry and then fade in the next week or two.

This September saw a near perfect setup. We rallied into expiry and are now threatening to roll over.

Repo-steria

Last week all sorts of shenanigans occurred in the repo funding markets. I will not bother giving you my opinion about the reasons for the stress. Yeah, I know the argument that it’s not a big deal as the Federal Reserve was able to provide the liquidity the market was needing.

But I worry about why they needed that liquidity. What changed in the financial system to cause that sudden need?

Sure, you can tell me about the big tax payment or the bombing in the Mideast, but we have had plenty of issues for the past nine years and there was no need for the Federal Reserve to do special repo operations. Now all of a sudden, they need to provide liquidity.

Could it be nothing? Of course. Heck it could even mean that liquidity is being used for more productive stuff. But I worry there is too much hubris on the Fed’s part. I worry that just like the recent yield curve inversion, they are busy coming up with reasons why this time is different.

This great picture was captured by Chris Whalen with the line about “we’ll see how this one ages.”

I worry that we will look back to this week’s funding stress and say that the signs were there, but we ignored them.

Geopolitical tensions

I am writing this in the aftermath of Trump’s speech at the United Nations. I am surprised the markets didn’t react even more violently to his comments. They were about as hawkish as I have ever seen. Whether it was the Chinese or the Iranians, I just don’t see the geopolitical situation getting better before it gets worse.

The market is underestimating the potential risks. The stock market has become numb to all the rhetoric, but I worry one of these days, it will turn into something more ominous than just words.

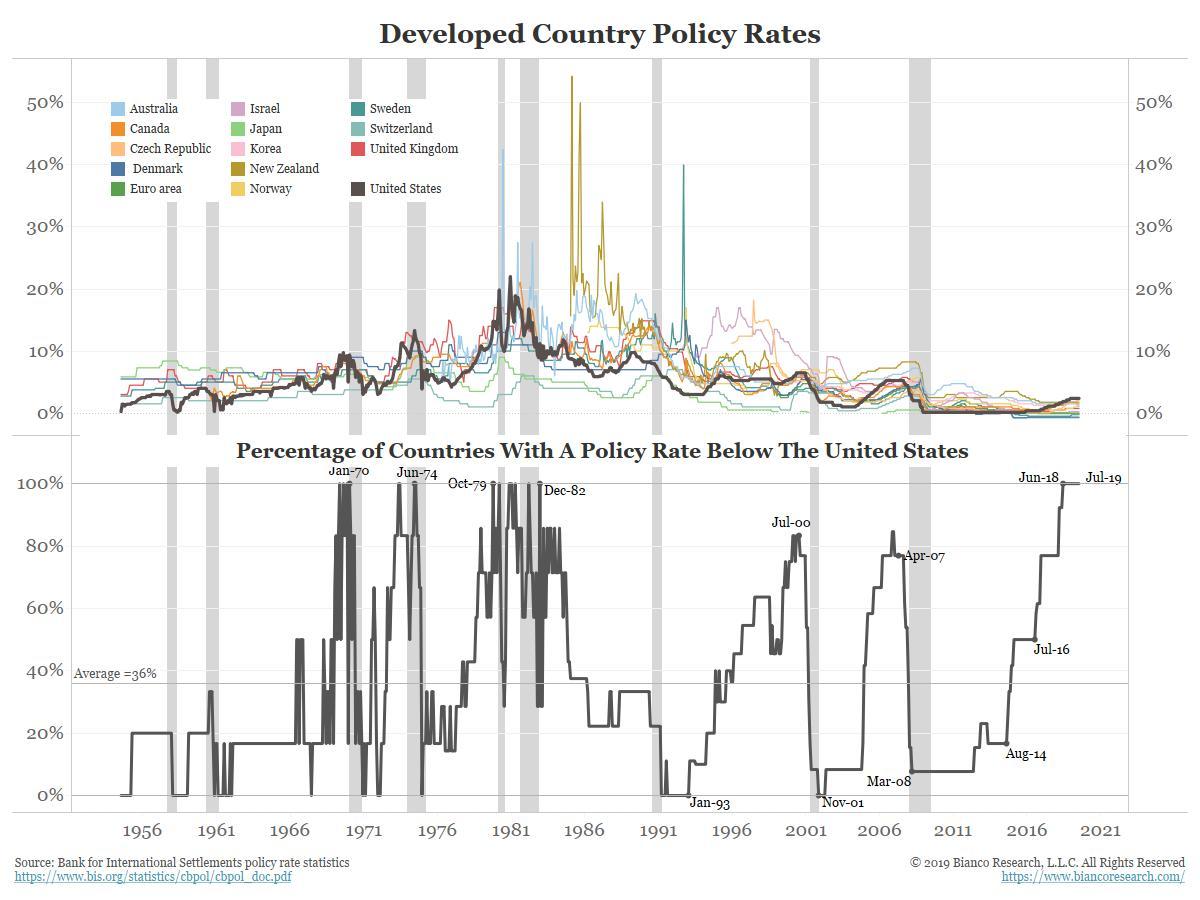

The biggest problem out there

And want to know my main worry? The country with the world’s reserve currency has the highest policy rate out there in the developed world. If we look back over time, this has often coincided with market crises.

I call this next graph, “The Most Important Chart in the Whole World”. It’s by the great Jim Bianco at Bianco Research and I have become a little bit of a zealot about it.

It sums up the main problem – the US is too tight for the world economy.

Now please don’t send me arguments how it’s the rest of the world’s fault for being too loose – I completely agree! Just like the United States, the rest of the world should implement fiscal stimulus and stop relying on monetary madness.

But our job is not to decide what should be, but calculate what is. And with the Fed so tight relative to the rest of the world, eventually it causes problems. Big ones.

Not turning into an uber-bear by any means

Don’t misunderstand me. I am not turning into one of those the end-of-the-world-is-upon us bears. Yet I think the time to be heavily long is past. The next 5-10% in the stock market is more likely to be down than higher.

Time to lighten up and look for spots to take stabs on the short side.

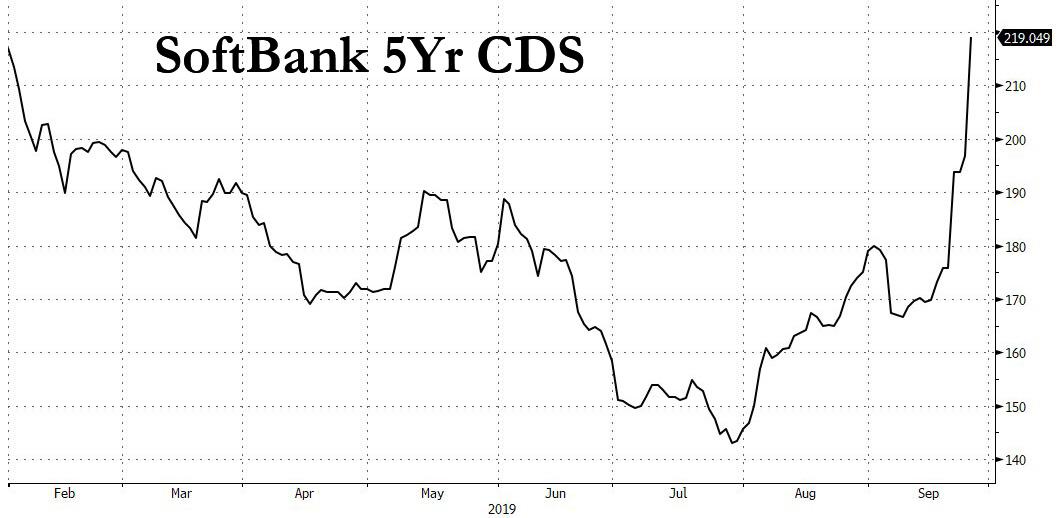

WeDone: Goldman Cuts Its Loan Exposure To SoftBank’s Vision Fund

In the aftermath of the WeWork IPO fiasco, which has not only sent the valuation of the glorified office subletter crashing from $47 billion to a number in the single digits but also cost the company’s messianic CEO, Adam Neumann, his ambition to become the world’s first immortal trillionaire, markets are increasingly shifting their attention over to the man that made this clownshow possible in the first place: Japan’s richest man, Masayoshi Son.

Caught in the crossfire is the increasingly amorphous entity controlled by Son, the venture capital giant SoftBank, whose Vision Fund over the past few years unleashed a furious investing spree, pumping tens of billions in dozens of startups whose valuations have been suddenly put into question.

And while the largest US bank, JPMorgan, now has its hands full cleaning up the mess resulting from its close relationship with Neumann and WeWork, Goldman Sachs is already anticipating the inevitable next step – which is a full-scale market revulsion to Softbank – and as Bloomberg reports is seeking to offload a portion of its stake in a $3.1 billion credit line it helped arrange for SoftBank Group Corp.’s Vision Fund.

According to the report, over the past few months, Goldman has been approaching other financial institutions “to take on some of its lending commitment to decrease its risk.” Needless to say, the key word in the previous sentence is “risk”, and suggests that at least according to Goldman, a shitstorm is about to hammer SoftBank all the way to its secured debt.

The bridge facility, which Goldman and Mizuho International began arranging last year, enables the behemoth investment vehicle to more quickly pounce on transactions. The loan was syndicated to other banks including Standard Chartered Plc, Citigroup Inc., Barclays Plc and Royal Bank of Canada, according to a SoftBank presentation in May.

As part of its stealthy liquidation of its SoftBank exposure, Goldman is selling the secured debt at prices slightly below par.

Also notable: while Goldman already reduced some of its exposure in May by bringing in additional lenders, the firm is now looking beyond the existing group, and at least one of the original 10 lenders isn’t interested in boosting its exposure, a Bloomberg source said. To entice interest, Goldman is offering to sell the credit line in pieces as small as $50 million, one of the people said; at this rate it will soon cut it down to $1,000 and open it up to clients on its retail, Marcus, platform.

Naturally, the fact that Goldman – which has deep ties to SoftBank and has been working with the company to raise a second Vision Fund and advising founder Masayoshi Son’s businesses on several deals in recent years – is seeking to trim its exposure can only be seen as bad news for both SoftBank, and the indicative value of its portfolio companies, which in addition to WeWork also include Uber where SoftBank is now said to be underwater following the company’s dismal post-IPO performance.

It’s not just Goldman though: in addition to sudden market concerns over its entire venture capital operation, SoftBank has also been plaued by doubts over the sale of its debt-laden mobile phone company, Sprint. But nowhere is the market’s growing skepticism to SoftBank’s future prospects more obvious than in the level of its CDS which has soared in recent weeks to 9 month highs.

What happens next? Here opinion is naturally divided: some think that the WeWork storm will quickly blow over, and things at SoftBank will quietly return to normal. Others, like outspoken unicorn critic, professor Scott Galloway,beliefe the SoftBank’s Vision Fund will shutter within 12 months.

Netanyahu Tapped By Israel’s President To Form Government After Deadlocked Election

It looks like he’s held on after last week’s deadlocked election, prior rumors of his political death notwithstanding. Longtime Prime Minister Benjamin Netanyahu has been tapped by Israeli President Reuven Rivlin on Wednesday to form a new government.

The longest serving prime minister in Israel’s history has now been given 42 days to form the country’s next government; and if he fails, the opportunity will fall to his rival – Blue and White Party centrist Benny Ganz. Rivlin said that Israel doesn’t want more elections, something which could theoretically happen for a third time in only a year should neither Netanyahu nor Ganz be successful.

Via The Times of Israel: President Reuven Rivlin meets with Prime Minister Benjamin Netanyahu and Blue and White party leader Benny Gantz at the President’s Residence in Jerusalem on September 23, 2019.

Facing three different allegations of corruption, Netanyahu is fighting for more than just his political future —but serious potential criminal charges which can go away only if he remains in the prime minister’s seat.

The president tapped the Likud leader after talks with Gantz to form a broad unity government broke down in the wake of the inconclusive election, and after both failed to agree on a power-sharing pact.

Netanyahu will have to cobble together 61 seats in order to form a majority government, even as he faces a pretrial hearing next week related to the attorney general’s bribery and fraud allegations.

The WSJ summarizes the newly published final results to last week’s elections as follows:

Israel’s Central Elections Committee on Wednesday released the final results of the Sept. 17 vote, in which Mr. Netanyahu’s Likud party won 32 seats and Mr. Gantz’s Blue and White party won 33 seats in the 120-member parliament, the Knesset. But Mr. Netanyahu won the pledges of 55 parliamentary members to be prime minister, while Mr. Gantz garnered 54.

The secular and nationalist politician, Avigdor Lieberman and his Yisrael Beiteinu party, remains kingmaker with eight seats; however, he’s consistently refused to back Netanyahu given the latter’s backing from religious parties.

Given Netanyahu’s failing to lure Lieberman also after the April vote, and with the major parties characteristically ensconced in their positions, Netanyahu’s new mandate to attempt a new government may just prove an act of kicking the can further down the road.

It’s hard to think of a time when political and cultural discourse has been more polarized. These days, it seems as if even casual conversation has become tougher to navigate than a World War II minefield. Everyone from prospective Saturday Night Livecast members to college professors teaching books on racism to social media folk heroes have been canceled for saying the wrong thing at the wrong time and holiday dinners occasion endless columns about surviving political discussions. In today’s world, “Can we all just get along?“—the phrase famously attributed to Rodney King after he was almost beaten to death by members of the Los Angeles Police Department in 1991—seems like it’s from a totally different universe.

Today’s guest, Peter Boghossian, hopes to remedy at least some of today’s toxic atmosphere. He’s an assistant professor of philosophy at Portland State University and the co-author, with James Lindsay, of the new book How To Have Impossible Conversations: A Very Practical Guide. Their aim is to give us all advice on how to have “effective, civil discussions about today’s most divisive issues.”

Boghossian talks with Nick Gillespie about strategies to bring people who disagree into useful, productive engagement with one another. They also discuss how Boghossian, Lindsay, and a third scholar, Helen Pluckrose, pulled off the “grievance studies” hoax, one of the biggest and most controversial academic controversies in recent memory. The trio authored 20 fake articles that they say exemplify how political correctness has trumped serious intellectual inquiry in many academic disciplines. These were not subtle satires: One talked about canine “rape culture” at dog parks and another appropriated aspects of Hitler’s Mein Kampf in the service of a feminist critique of patriarchy. They submitted the papers to academic journals, with seven being accepted for publication and four actually coming out when they were exposed by The Wall Street Journal.

Is there a contradiction between pulling off the hoax and writing a book about bringing ideological opponents together? And what punishment at Portland State does Boghossian still face as a result of his role in the hoax? Those are some of the questions raised in this wide-ranging conversation about politics, polarization, and intellectual inquiry.

Audio production by Ian Keyser.

from Latest – Reason.com https://ift.tt/2l6ivr6

via IFTTT

Earlier today, I wrote: “What is an impeachable offense? Turns out, it’s anything the Democrats can get enough votes for.” And I realize saying that gets rid of half my possible audience, but it’s still the impression I’ve gotten over the past -less than- 24 hours.

After 2+ years of her fellow party members and Congress(wo)men riding on the now-defunct Robert Mueller train and clamoring non-stop for impeachment of Donald Trump, the man who stole the 2016 election from their candidate, God’s own candidate Hillary, the one who deserved to win, after 2+ years Nancy Pelosi does a 180 and joins the chorus. So as not to end up as fish food.

And sure, if she’s finally spotted an impeachable offense, that would make sense. But she herself states she joined because of Trump’s phone call with Ukraine’s Zelensky, and we know Pelosi doesn’t know what was said in that call, nor what’s in the opaque whistleblower complaint linked to it, a complaint moreover that’s based solely on hearsay.

Making the contents of the call public would set a dangerous precedent, because no foreign leader would ever again speak freely to a US president. Even sharing it ‘only’ with Capitol Hill would make them cautious. In that regard, the White House reluctance to share both the call and the complaint makes a lot of sense.

We’re talking many decades of carefully crafted tradition, whose importance cannot be overestimated. Wars have been avoided by these calls. But then again, as Trump said, he’s sure everybody and their pet intelligence hamster is listening in the talks already, so what’s the use anymore?

Democratic Party members smell something, and they think they’re sure is blood, without ever contemplating it might be their own. They’ve all been thinking impeachment for a long time, and now more than ever, because they appear to realize it might be the only way to get rid of Trump and get their people in charge, that the ballot box may well not deliver that outcome.

Ryan Grim’s piece for the Intercept provides a a good picture of what is going on in Dem Camp, not because it’s so well written, it’s actually quite shaky, but because between the lines the despair seeps through. Do read the whole thing, it’s worth the while because it tells a story nobody really talks about.

That is, on various levels of the US political system, Democratic party candidates have become increasingly fearful of losing their seats, and impeachment must bring them ‘salvation’. You get the idea it’s not even so much about what Trump does, but squarely about him standing in their way, like he stood in Hillary’s.

[..] as Democrats prepped for a series of private meetings, it was clear that nerves had been frayed. August had been a challenge for the party’s rank-and-file, as activists and angry citizens back home browbeat them at town halls, grocery stores, and local events for the party’s unwillingness to impeach President Donald Trump.

“We spent all summer getting the shit kicked out of us back home,” said one Democrat who received such treatment. The day before, former Trump adviser Corey Lewandowski had made a mockery of the Judiciary Committee’s interview of him, betraying open contempt for the process and the people running it.

Swing district freshmen Democrats known as frontliners, meanwhile, had spent the last few weeks vocally decrying the pressure on them to call for impeachment, claiming it was putting them in a political jam. Democrats were debating publicly whether the hearings Rep. Jerry Nadler, D-N.Y., was running at his Judiciary Committee were or were not in fact the launch of impeachment proceedings.

I’m not sure to which extent to believe this. Do Democrat voters really pester their local politicians about impeaching Trump? Or are they making this up because they need something to blame for their own failures?

[..] The members without official primary challenges were by no means safe, either, as they might soon draw a challenge unless the trajectory of the politics changed. Freshman Lori Trahan from Massachusetts, for instance, came out for impeachment after Dan Koh, whom she beat in a primary by 147 votes in 2018, called on her to do so, with the clear threat that he may run again.

The seats of upward of 200 Democrats were being put at risk to protect a handful of loud frontliners, Raskin argued, and it wasn’t obvious that the strategy was actually protecting them from anything. Grassroots activists were demobilizing, Democrats across the board were facing primary challenges, and somehow, someway, Democrats seemed to be losing, again, to Trump. Something had to give.

“Democrats seemed to be losing, again, to Trump. Something had to give.” That sums it up. And we now know what it was that had to give. That doesn’t make it a winning strategy, though. And then came the Ukraine “news”. It was god-given. The “new” Kavanaugh story a few days before had seemed to, but it was false. Now, however….

[..] That something came later that night, in the form of a Washington Post scoop about a whistleblower complaint from a member of the U.S. intelligence community about a promise Trump had made to a foreign leader. Then, on Thursday evening, the Post reported that the country involved was Ukraine.

The news had landed like a bomb in a Democratic caucus that was already ready to explode. Calls to impeach Trump rained down from the party’s left flank and its presidential candidates. On Friday evening, Democrats were bracing for a backlash back home. “It’s going to be a brutal weekend for a lot of people, especially those who haven’t spoken for impeachment,” one Democrat predicted. Indeed it was.

Democrats, including frontliners, spent the weekend furiously texting and calling each other as they worked through how to respond to Trump’s latest lawlessness. “People are pissed,” said another Democrat over the weekend. “Frontliners are pissed! And not even the ‘progressive’ frontliners either.”

It’s a feeding frenzy inside an echo chamber. All quite rational, of course. And Pelosi had no choice but to join in, or she would have been fish food.

Pelosi didn’t seem to understand the shift that was taking place under her feet. Reporter John Harwood asked an aide to Pelosi over the weekend if the news changed her calculus on impeachment and got back the reply: “no. see any GOP votes for it?”

Jon Favreau, a speechwriter for President Barack Obama who now serves, from his perch at Pod Save America, as something of a tribune for the volunteer-resistance army that phone banked and door-knocked Democrats into the majority, was apoplectic. “This is insane,” he said. “This is pathetic. This is not what we worked so hard for in 2018.” By Tuesday afternoon, Pelosi was calling for impeachment proceedings to begin.

We want impeachment, and we’ll figure out later what for. There are Democrats right now, after recognizing nobody knows what is in either the call or the complaint, who say it’s about Trump’s entire body of work, about months and months of violating the constitution etc. I think they’ll have to be more specific than that for the inquiry, however.

“The actions taken to date by the president have seriously violated the constitution,” Pelosi said in a formal address in Washington on Tuesday evening.

“The president must be held accountable. No one is above the law.”

I swear, one of these days I’m going to lose it over the next person who says “No one is above the law.” That must be the emptiest statement in politics, ever, but certainly these days.

Now, of course, lest we forget, that plenty Democrats ‘support’ impeachment doesn’t mean much of anything. There’s about a zero Kelvin chance of getting it through the Senate. Plus, you need a specific reason for impeachment, and we’ve already seen the Ukraine isn’t it, because nobody even knows what was said.

Which makes me think Pelosi’s heart can’t be in it, and that makes her a weak advocate for the issue. So what other grounds for impeachment will they come up with? That can only be things that happened in the past, and things Pelosi never thought were impeachable, or at least wouldn’t get enough votes. Why should they now?

As an aside, the Democrat candidates and frontliners -and Nancy Pelosi as per last night- are throwing Joe Biden under the bus, who’s still their leading candidate. Because there’s no way Biden will survive a thorough investigation into Ukraine. That is so obvious I’m wondering if they meant to get rid of him all along.

And then there are the ‘technicalities’.

“In his response to the Democrats’ move, House Republican Leader Kevin McCarthy said: “Speaker Pelosi happens to be the Speaker of this House, but she does not speak for America when it comes to this issue.” “She cannot unilaterally decide we’re in an impeachment inquiry,” he added.”

And I absolutely love this bit:

“In her announcement Ms Pelosi said the six congressional committees already investigating Mr Trump would continue their work, but now under the umbrella of a formal impeachment inquiry.”. That says Heads of the Five Families to me, right there. You got your Tattaglia, your Barzoni etc.

There are 6 different active investigations into Trump. Well over two years after Robert Mueller started his $40 million utter failure of an investigation. Why? Impeachment. And they have all come up empty so far.

“Some argue that the timing could not be worse for President Zelensky, who is scheduled to meet Donald Trump in New York later on Wednesday. Public TV station Pershy describes the controversy as a “trap” for Ukraine. “It would be stupid to start playing into the hands of either Democrats or Republicans,” said one of the channel’s commentators. Others contend that the Ukrainian president has US politicians over the barrel. “Zelensky has two pistols in his hands: one pointing at Trump, and the other at Biden,” reports Pryamy TV.

She told “Fox & Friends” on Tuesday that she’ll remain consistent to her message that the road to 2020 can only be found in a clear victory and mandate, saying it’s for “the American people… making that decision” of who is in the White House, not impeachment.

“I believe that impeachment at this juncture would be terribly divisive for the country at a time when we are already extremely divided. The hyperpartisanship is one of the main things driving our country apart,” Gabbard told host Brian Kilmeade. “I think it’s important to beat Donald Trump, that’s why I’m running for president,” she said.

“But I think it’s the American people who need to make their voices heard making that decision.”

We need to get Tulsi her own party, right? Because right now, she’s not fighting Trump, she’s fighting the DNC and the rest of her ‘own’ party. What a waste of time and money, and conviction and talent.

It’s hard to think of a time when political and cultural discourse has been more polarized. These days, it seems as if even casual conversation has become tougher to navigate than a World War II minefield. Everyone from prospective Saturday Night Livecast members to college professors teaching books on racism to social media folk heroes have been canceled for saying the wrong thing at the wrong time and holiday dinners occasion endless columns about surviving political discussions. In today’s world, “Can we all just get along?“—the phrase famously attributed to Rodney King after he was almost beaten to death by members of the Los Angeles Police Department in 1991—seems like it’s from a totally different universe.

Today’s guest, Peter Boghossian, hopes to remedy at least some of today’s toxic atmosphere. He’s an assistant professor of philosophy at Portland State University and the co-author, with James Lindsay, of the new book How To Have Impossible Conversations: A Very Practical Guide. Their aim is to give us all advice on how to have “effective, civil discussions about today’s most divisive issues.”

Boghossian talks with Nick Gillespie about strategies to bring people who disagree into useful, productive engagement with one another. They also discuss how Boghossian, Lindsay, and a third scholar, Helen Pluckrose, pulled off the “grievance studies” hoax, one of the biggest and most controversial academic controversies in recent memory. The trio authored 20 fake articles that they say exemplify how political correctness has trumped serious intellectual inquiry in many academic disciplines. These were not subtle satires: One talked about canine “rape culture” at dog parks and another appropriated aspects of Hitler’s Mein Kampf in the service of a feminist critique of patriarchy. They submitted the papers to academic journals, with seven being accepted for publication and four actually coming out when they were exposed by The Wall Street Journal.

Is there a contradiction between pulling off the hoax and writing a book about bringing ideological opponents together? And what punishment at Portland State does Boghossian still face as a result of his role in the hoax? Those are some of the questions raised in this wide-ranging conversation about politics, polarization, and intellectual inquiry.

Audio production by Ian Keyser.

from Latest – Reason.com https://ift.tt/2l6ivr6

via IFTTT

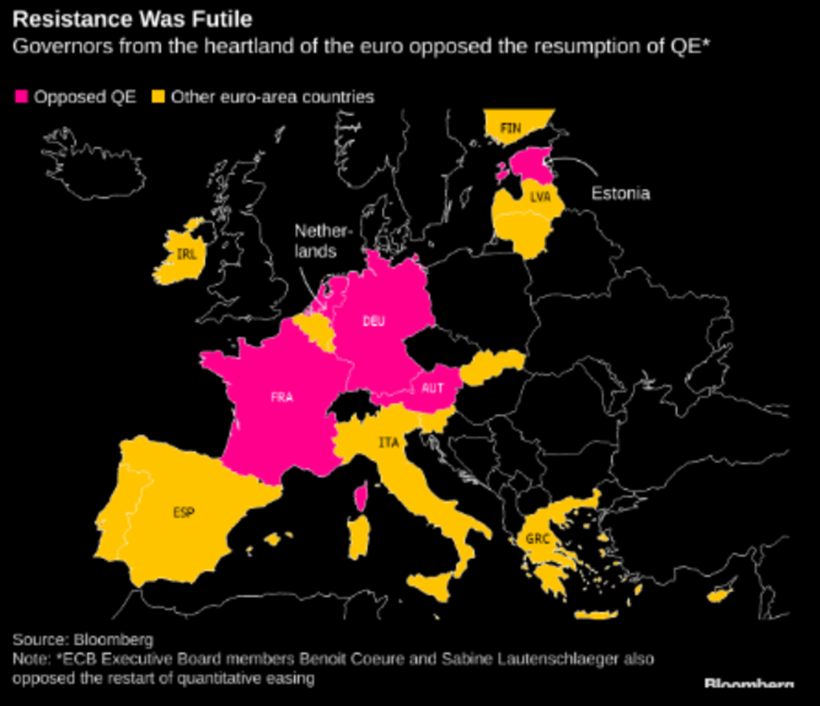

One Of The Biggest ECB Hawks Unexpectedly Resigns In Opposition To Draghi’s Massive Easing

One of the biggest hawks on the ECB executive board and governing counsel, Germany Sabine Lautenschlaeger, unexpectedly announced her resignation from the European Central Bank Executive Board more than two years before the official end of her term.

Sabine Lautenschläger

The German policymaker is stepping down on Oct. 31, the ECB said in a statement late on Wednesday. While the statement provided no reason for her decision, some – such as the WSJ – suspect that the departure of the outspoken hawk is in protest to outgoing ECB president Mario Draghi’s recent decision to launch massive easing, including cutting rates to -0.50%, and resuming open-ended QE, despite an “unprecedented revolt” from Europe’s core economies, including Germany, France, Austria and the Netherlands.

Lautenschlaeger was a board member since January 2014 and during her tenure served a full 5-year term as the vice-chair of the Supervisory Board of the Single Supervisory Mechanism.

“President Mario Draghi thanked her for her instrumental role in helping set up and steer Europe-wide banking supervision, a key pillar of banking union, as well as her unwavering commitment to Europe”, Draghi said in a brief statement published on the ECB’s website, republished below in its entirety.

Sabine Lautenschläger resigns from ECB Board

Today, Sabine Lautenschläger, Member of the Executive Board and Governing Council of the European Central Bank (ECB), informed President Mario Draghi that she will resign from her position on 31 October 2019, prior to the end of her term of office. Ms Lautenschläger has been a Member of the Executive Board and Governing Council since 27 January 2014 as well as serving a full term in office as the Vice-Chair of the Supervisory Board of the Single Supervisory Mechanism (SSM).

President Mario Draghi thanked her for her instrumental role in helping set up and steer Europe-wide banking supervision, a key pillar of banking union, as well as her unwavering commitment to Europe.

Yesterday, Massachusetts Gov. Charlie Baker (R) announced an “emergency” ban on the sale of all vaping products, including devices used to consume cannabis extracts, nicotine, or solutions with no psychoactive ingredients. Unlike the bans on flavored e-cigarettes in Michigan and New York or the similar ban planned by the Food and Drug Administration (FDA), which were presented as responses to underage consumption, the Massachusetts edict is based mainly on concerns about recent reports of severe respiratory illnesses associated with vaping. But the governor’s explanation is highly misleading in light of what we know about the causes of those illnesses, and his sweeping ban is apt to undermine public health instead of protecting it.

“The Centers for Disease Control and Prevention (CDC) and the Food and Drug Administration (FDA) are currently investigating a multi-state outbreak of lung disease that has been associated with the use of e-cigarettes or vaping products (devices, liquids, refill pods, and/or cartridges),” Baker’s press release says. “To date, the CDC has confirmed 530 cases of lung injury across 38 states. While many of the patients reported recent use of Tetrahydrocannabinol (THC)-containing products, some reported using both THC and nicotine products. No single product has been linked to all cases of lung disease.”

Baker is echoing the CDC’s framing, which obscures the fact that the overwhelming majority of lung disease cases (not just “many”) are associated with cannabis products, which remain illegal in most of the country (although not in Massachusetts, until now). In states where the products used have been reported, the share of patients who admitted vaping THC ranges from 83 percent to 100 percent. The actual rates in some of those states may be even higher, since patients might be reluctant to admit illegal drug use.

The most plausible explanation for the lung diseases is that vaping oil-based THC solutions is leading to lipoid pneumonia, a rare condition caused by fat particles in the lungs. A leading suspect is vitamin E acetate, which was detected in most of the THC fluids tested by the FDA and New York’s state lab. Legal nicotine e-cigarettes, by contrast, typically vaporize e-liquids containing propylene glycol and vegetable glycerin. Furthermore, such e-cigarettes have been in wide use for years in this country, while the respiratory illnesses have been reported only in the last few months, which suggests that relatively new additives or contaminants are to blame.

“These excipients [propylene glycol and vegetable glycerin] have been used in e-liquids for the past 12 years without a problem,” notes Boston University public health professor Michael Siegel, a physician and epidemiologist who supports e-cigarettes as a harm-reducing alternative to the conventional, combustible kind. “If PG/VG were the problem, then there would be a huge number of cases occurring among adults, much less of a differential by gender, and much less of an age gradient in the reported cases.”

Siegel faults the CDC for its muddled message about vaping-related lung disease. “Given the fact that close to 90% of cases and 100% of the deaths for which products have been reported are associated with marijuana vaping, it is inexcusable that the CDC fails to distinguish between the products being vaped,” he writes. “It is also inexcusable that CDC has failed to distinguish between the vaping of oil-based e-liquids (which are typically used in [THC cartridges]) and water/alcohol-based e-liquids (as are used in virtually all e-cigarettes).”

In this context, Baker’s comprehensive ban on all vaping products makes little sense. He is relying on his authority to declare an emergency “which is detrimental to the public health.” Based on Baker’s declaration, the commissioner of the Massachusetts Department of Health, with the approval of the state Public Health Council, has imposed a four-month ban covering a wide range of products that, so far as we know, have not been implicated in respiratory illnesses.

Implicitly conceding the inadequacy of his main justification, Baker also cites recent increases in e-cigarette use by minors as a rationale for the ban. “Vaping products are marketed and sold in nearly 8,000 flavors that make them easier to use and more appealing to youth,” says Lt. Gov. Karyn Polito. “Today’s actions include a ban on flavored products, inclusive of mint and menthol, which we know are widely used by young people.”

Baker’s action highlights the alarmingly broad authority that some governors are claiming to ban products they don’t like in the name of “public health.” Since the statutes on which they are relying do not define “public health,” they seemingly allow governors to declare any situation an “emergency” and impose bans without new legislation. Gregory Conley, president of the American Vaping Association, which seeks to preserve e-cigarettes as an option for smokers who want to quit, asks, “If a governor is permitted to just ban e-cigarettes for four months, what else could they ban?” That seems to be an open question, although litigation by vaping businesses may clarify the answer.

Baker’s defense of his ban lumps together several distinct issues: the outbreak of respiratory illnesses related to THC vaping, the surge in underage e-cigarette use, and the relative hazards of vaping and smoking. His take on that last issue is decidedly unscientific. “To further inform the public about the dangers of vaping and e-cigarette use,” his press release says, the Department of Public Health “is relaunching two public awareness campaigns aimed at educating parents and middle and high school-aged youth. ‘Different Products, Same Danger,’ originally launched in April 2019, links the dangers of vaping to cigarette smoking.”

Legal e-cigarettes, which deliver nicotine without tobacco or combustion, emphatically do not pose the “same danger” as conventional cigarettes. As David Abrams, a professor of social and behavioral sciences at NYU, explained in a recent interview with CBS News, studies of biomarkers in smokers who have switched to vaping find that they are exposed to far fewer hazardous substances, at far lower levels, than people who continue to smoke. “E-cigarettes are way less harmful than cigarettes,” he said, “and they can and do help smokers switch if they can’t quit.”

If every smoker in the United States switched to e-cigarettes, Abrams estimates, it would prevent as many as 7 million smoking-related deaths. Vaping “delivers nicotine in a very satisfying way without the major harms of burning tobacco,” he said. “If we lose this opportunity, I think we will have blown the single biggest public health opportunity we’ve ever had in 120 years to get rid of cigarettes and replace them with a much safer form of nicotine.”

The harm-reducing potential of e-cigarettes has been recognized by a wide range of public health agencies and organizations, including the FDA, the Royal College of Physicians, Public Health England, the American Cancer Society, and the National Academies of Sciences, Engineering, and Medicine. In 2015, Public Health England said “best estimates show e-cigarettes are 95% less harmful to your health than normal cigarettes.” Yet the Massachusetts Department of Public Health is telling people that e-cigarettes pose the “same danger” as combustible cigarettes, a false premise that seems to be part of the logic underlying its ban.

If you ignore the enormous difference between the health risks posed by smoking and the health risks posed by vaping, it is easier to rationalize a policy that will deprive current and former smokers of an alternative that could save their lives. Massachusetts Health and Human Services Secretary Marylou Sudders implicitly acknowledges the impact the vaping ban will have on smokers who have switched to e-cigarettes or might be interested in doing so. “As a result of the public health emergency,” she says, “the Commonwealth is implementing a statewide standing order for nicotine replacement products, like gum and patches, which will allow people to access these products as a covered benefit through their insurance without requiring an individual prescription.”

As David Abrams noted in his CBS News interview, research indicates that e-cigarettes are nearly twice as effective in smoking cessation as those “nicotine replacement products.” Many smokers who did not manage to quit with “gum and patches” were able to do so with e-cigarettes. By ignoring that reality, Massachusetts pretends that its vaping ban will improve public health when in fact it is apt to result in more smoking-related diseases and deaths as former smokers return to a much more hazardous habit and current smokers are deterred from quitting.

“Massachusetts has made significant progress over the past two decades in curbing youth and adult tobacco use,” the governor’s press release notes. “In 1996, the youth smoking rate was 36.7%. Today, the youth smoking rate is 6.4%. The adult smoking rate is also low, with just under 14% of adults using combustible tobacco products.” These downward trends not only continued as vaping became more common; they accelerated, suggesting that e-cigarettes are replacing a far more dangerous source of nicotine. But that consideration does not seem to have figured at all in Baker’s decision.

It should go without saying that the Massachusetts ban will not curtail vaping of mystery cartridges and e-liquids available on the black market, which pose the greatest risks. To the contrary, the ban will drive vapers toward those products. “Legal vapes while not safe are subject to regulation on manufacturing, sales, marketing, ingredients, warnings,” former FDA chief Scott Gottlieb noted last month. “If we outlaw all vapes, and pull legal products off the market, problems with illegal and counterfeit products will get worse.” Yet that’s exactly what Massachusetts is doing.

from Latest – Reason.com https://ift.tt/2l7uBAh

via IFTTT

Imagine approaching a friend that you think is very wealthy and asking her to borrow ten thousand dollars for just one night. To entice her, you offer as collateral the title to your 2019 Lexus parked in her driveway along with an interest rate that is 5% above that which she is earning in the bank. Shockingly, your friend says she can’t. Given the risk-free nature of the transaction and excellent one-day profit, we can assume that our friend may not be as wealthy as we thought.

On Monday, September 16th, 2019, a similar situation occurred in the overnight repurchase agreement (repo) funding market. On that day, banks were unwilling or unable to lend on a collateralized basis, even with the promise of large risk-free profits. This behavior reveals something very important about the banking system and points to the end of market stimulus that has been around for the past decade.

The Plumbing of the Banking System and Financial Markets

Interbank borrowing is the engine that allows the financial system to run smoothly. Banks routinely borrow and lend to each other on an overnight basis to ensure that all banks have ample funds to meet daily cash flow needs and that banks with excess funds can earn interest on them. Literally, years go by with no problems in the interbank markets and not a mention in the media.

Before proceeding, what follows is a definition of the funding instruments used in the interbank markets.

Fed Funds are uncollateralized interbank loans that are almost exclusively done on an overnight basis. Except for a few exceptions, only banks can trade Fed Funds.

Repo (repurchase agreements) are collateralized loans. These transactions occur between banks but often involve other non-bank financial institutions such as insurance companies. Repo can be negotiated on an overnight and longer-term basis. General collateral, or “GC,” is a term used to describe Treasury, agency, and mortgage collateral that backs certain repo loans. In a GC repo, the particular securities backing the loan are not determined until after the transaction is agreed upon by the counterparties. The securities delivered must meet certain pre-defined criteria.

On September 16th, overnight GC repo traded as high as 8%, almost 6% higher than the Fed Funds rate, which theoretically should keep repo and other money market rates closely tied to it. The billion-dollar question is, “Why did a firm willing to pay a hefty premium, with risk-free collateral, struggle to borrow money”? Before the 16th, a premium of 25 to 50 basis points versus Fed Funds would have enticed a mob of financial institutions to lend money via the repo markets. On the 16th, many multiples of that premium were not enticing enough.

Most likely, there was an unexpected cash crunch that left banks and/or financial institutions underfunded. The media has talked up the corporate tax date and a large Treasury bond settlement date as potential reasons. We are not convinced by either excuse as they were easily forecastable weeks in advance.

Regardless of what caused the liquidity crunch, we do know, that in aggregate, banks did not have the capacity to lend money. Given the capacity, they would have done so in a New York minute and at much lower rates.

To highlight the enormity of the aberration, consider the following:

Since 2006, the average daily difference between the overnight GC repo rate and the Fed Funds effective rate was .025%.

Three standard deviations or 99.5% of the observances should have a spread of .56% or less.

8% is a bewildering 42 standard deviations from the average, or simply impossible assuming a traditional bell curve.

What was revealed on the 16th?

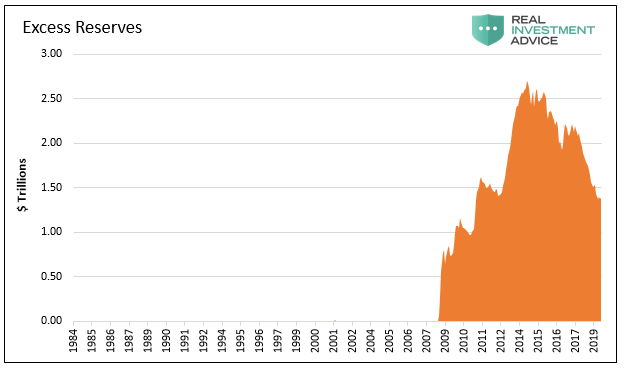

The U.S. and global banking systems revolve around fractional reserve banking. That means banks need only hold a fraction of the cash deposits that they hold in reserve accounts at the Fed. For example, if a bank has $1,000 in deposits (a liability to the bank), they may lend $900 of those funds and retain only 10% in reserves. This is meant to ensure they have enough funding on hand to make payments during the day and also as a buffer against unanticipated liquidity needs. Before 2008, banks held only just as many reserves as were required by the Fed. Holding anything more than the required minimum was a drag on earnings, as excess reserves were unremunerated at the time.

Quantitative Easing (QE) and the need for the Fed to pay interest on newly formed excess reserves changed that. When the Fed conducted QE, they bought U.S. Treasury, agency, and mortgage-backed securities and credited the selling bank’s reserve account. The purpose of QE1 was to ensure that the banking system was sufficiently liquid and equipped to deal with the ramifications of the ongoing financial crisis. Round one of QE was logical given the growing list of bank/financial institution failures. However, additional rounds of QE appear to have had a different motive and influence as banks were highly liquid after QE1 and had shored up their capital as well. That is a story for another day.

The graph below shows how “excess” reserves were close to zero before 2008 and soared by over $2.5 trillion after the three rounds of QE. Before QE, “excess” reserves were tiny, measured in the hundreds of millions. The amount is so small it is not visible on the graph below. The reserves produced by multiple rounds of quantitative easing may have been truly excess, meaning above required reserves, on day one of QE. However, on day two and beyond that is not necessarily true for any particular bank or the system as a whole, as we are about to explain.

Data courtesy: St. Louis Federal Reserve

The Fed, having pushed an enormous amount of reserves on the banks, created a potential problem. The Fed feared that once the smoke cleared from the financial crisis, banks would revert to their pre-crisis practice of keeping only the minimum amount of reserves required. This would leave them an unprecedented surplus of excess funds to buy financial assets and/or create loans which would vastly increase the money supply with inflationary consequences. To combat this problem, they incentivized the banks to keep the reserves locked down by paying them a rate of interest on the reserves that were higher than the Fed funds rates and other prevailing money market rates. This rate is called the IOER or the interest on excess reserves.

The Fed assumed banks would hold excess reserves because they could make risk free profits at no cost. This largely worked, but some reserves were leveraged by the banks and flowed into the financial markets. This was a big factor in driving stock prices higher, credit spreads tighter, and bond yields lower. This form of inflation the Fed seemed to desire as evidenced from their many speeches talking about generating household net worth.

From the banks’ perspective, the excess reserves supplied by the Fed during QE were preferential to traditional uses of excess reserves. Historically, excess bank reserves were invested in the Treasury market or lent on to other banks in the Fed Funds market. Purchasing Treasury securities had no credit risk, but banks are required to mark their Treasury holdings to market and therefore produce unexpected gains and losses. Lending reserves in the interbank market also incurred counterparty risk, as there was always the chance the borrowing bank would be unable to repay the loan, especially in the immediate post-crisis period. Additionally, as QE had produced trillions in excess reserves, there was not much demand from other banks. Therefore, the banks preferred use of excess reserves was leaving them on deposit with the Fed to earn IOER. This resulted in no counterparty risk and no mark to market risk.

Beginning in 2018, the Fed began reducing their balance sheet via QT and the amount of excess reserves held by banks began to decline appreciably.

Solving Our Mystery

It is nearly impossible for the public to figure out how much in excess reserves the banking system is truly carrying. Indeed, even the Fed seems uncertain. It is common knowledge that they have been declining, and over the last six months, clues emerged that the amount of “truly excess reserves,” meaning the amount banks could do without, was possibly approaching zero.

Clue one came on March 20th, 2019 when the Fed said QT would end in October 2019. Then, on July 31st, 2019, as small problems occurred in the funding markets, the Fed abruptly announced that they would halt the balance sheet reduction in August, two months earlier than originally planned. The QT effort, despite assurances from Bernanke, Yellen, and Powell that it would be uneventful, ended 22 months after it began. The Fed’s balance sheet declined only $800 billion as a result of QT, less than a quarter of what the Fed added to their balance sheet during QE.

Clue two was the declining spread between the IOER rate and the effective Fed Funds rate as the level of excess reserves was declining, as seen in the chart below. The spread between IOER and the Fed Funds rate was narrowing because the Fed was having trouble maintaining the Fed Funds rate within the targeted range. In March 2019, the spread became negative, which was counter to the Fed’s objectives. Not surprisingly, this is when the Fed first announced that QT would end.

Data courtesy: St. Louis Federal Reserve

The third and final clue emerged on September 16, 2019, when overnight repo traded at 7%-8%. If banks truly had excess reserves, they would have lent some of that excess into the repo market and rates would never have gotten close to 7-8%. It seems logical that banks would have been happy to lend on a collateralized basis at 3%, much less 7-8%, when their alternative, leaving excess reserves to the Fed, would have earned them 2.25%.

Further confirmation that something was amiss occurred on September 17th, 2019, when the Fed Funds effective rate was above the upper end of the Fed’s target range of 2-2.25% at the time. This marked the first time the Fed Funds rate traded above its target since 2008.

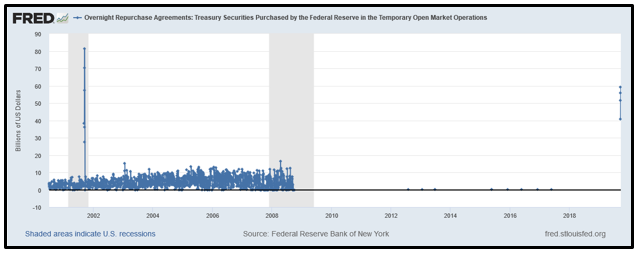

On September 17th, the Fed entered the repo markets with a $53 billion overnight repo operation, whereby banks could pledge Treasury collateral to the Fed and receive cash. The temporary liquidity injection worked and brought repo rates back to normal. The following day the Fed pumped $75 billion into the markets. These were the first repo transactions executed by the Fed since the Financial Crisis, as shown below.

These liquidity operations will likely continue as long as there is demand from banks. The Fed will also conduct longer-term repo operations to reduce the amount of daily liquidity they provide.

The Fed can continue to resort to the pre-QE era tactics and use temporary daily operations to help target overnight borrowing rates. They can also reduce the reserve requirements which would, at least for some time, provide the system with excess reserves. Lastly, they can permanently add reserves with QE. Recent rhetoric from Fed Chairman Powell and New York Fed President Williams suggests a resumption of QE in some form may be closer than we think.

Why should we care?

The QE-related excess reserves were used to invest in financial assets. While the investments were probably high-grade liquid assets, they essentially crowded out investors, pushing them into slightly riskier assets. This domino effect helped lift all asset prices from the most risk-free and liquid to those that are risky and illiquid. Keep in mind the Fed removed about $3.6 trillion of Treasury and mortgage securities from the market which had a similar effect.

The bottom line is that the role excess reserves played in stimulating the markets over the last decade is gone. There are many other factors driving asset prices higher such as passive investing, stock buybacks, and a broad-based, euphoric investment atmosphere, all of which are byproducts of extraordinary monetary policies. The new modus operandi is not necessarily a cause for concern, but it does present a new demand curve for the markets that is different from what we have become accustomed to.

Summary

Short-term funding is never sexy and rarely if ever, the most exciting part of the capital markets. A brief recollection of 2008 serves as a reminder that, when it is exciting, it is usually a harbinger of volatility and disruption.

In a Washington Post article from 2010, Bernanke stated, “We have made all necessary preparations, and we are confident that we have the tools to unwind these policies at the appropriate time.”

Much more recently, Jay Powell stated, “We’ve been operating in this regime for a full decade. It’s designed specifically so that we do not expect to be conducting frequent open market operations to keep fed fund [sic] rates in the target range.”

Today, a decade after the financial crisis, we see that Bernanke and Powell have little appreciation for the inner-workings of the financial system.

In the Wisdom of Peter Fisher, an RIA Pro article released in July, we discussed the insight of Peter Fisher, a former Treasury, and Federal Reserve official. Unlike most other Fed members and politicians, he discussed how hard getting back to normal will be. As we are learning, it turns out that Fisher’s wisdom from 2017 was visionary.

“As Fisher stated in his remarks, “The challenge of normalizing policy will be to undo bad habits that have developed in how monetary policy is explained and understood.” He continues, “…the Fed will have to walk back from their early assurances that the “exit would be easy.”

{kind=link}

{kind=link}