Following Iran’s provocative test firing last week of its medium-range ballistic missile the Shahab-3, which is capable of hitting Israel, Prime Minister Benjamin Netanyahu announced on Sunday the successful test firing of Israel’s own Arrow-3 ballistic missile shield over Alaska,tests previously considered secretive.

“The performance was perfect – every hit a bull’s eye,” Netanyahu, who doubles as defense minister, said in a statement following the three secret “live interception” tests held in coordination with the United States and the missile system’s maker, Boeing Co. The Arrow-3 is touted as being able to shoot downincoming missiles in space, or while a hostile missile is still outside the earth’s atmosphere, and is the “bottom tier” and longest range integration on top of the the short-range Iron Dome interceptor.

Specifically the Arrow-3 is designed to take out advanced ballistic missiles in Iran and Syria’s arsenal. The tests were held in Alaska due to Israel not being considered a capable hosting site given the system’s specifications, as well as likely the current soaring regional tensions with Iran.

“Today Israel has the capabilities to act against ballistic missiles launched at us from Iran and from anywhere else,” Netanyahu said on Sunday. “All our foes should know that we can best them, both defensively and offensively.”

“They were successful beyond any imagination. The Arrow 3 – with complete success – intercepted ballistic missiles beyond the atmosphere at unprecedented altitudes and speeds,” the Israeli PM added. However, no details regarding what altitudes were reached during the testing were given.

Wow, this is breathtaking. Actually pretty massive news!

The #Arrow3 🚀 is a real game changer! It allows #Israel to intercept long-range ballistic missile targets outside the atmosphere.

Simpler: Israel will be able to intercept Iranian nuclear missiles.

During the Alaska tests the Israeli Arrow-3 missiles were also integrated with the US’ long-range, very high-altitude active electronically scanned array surveillance radar which globally assists in early detection of hostile projectiles with a range up to 2,900 miles. As Reuters summarized:

Israel’s Ministry of Defense said that, as part of the Alaska tests, Arrow-3 was successfully synched up with the AN-TPY2 radar – also known as X-band – which provides the United States with extensive global coverage. Israel hosts an X-band battery.

“We are committed to assisting the government of Israel in upgrading its national missile defence capability to defend the state of Israel and deployed U.S. forces from emerging threats,” Vice Admiral John Hill, director of the Pentagon’s Missile Defence Agency, said in a statement.

The Arrow-3 system, once fully integrated with the Iron Dome and the medium-range ‘David’s Sling,’ will mark the highest level in Israel’s multi-tiered missile defense network.

No doubt, the publication of the weekend tests doubly serves asa strong message of warning to Iran amid soaring tensions and a US military build-up in the Persian Gulf after tit-for-tat drone shoot downs over the past month and ongoing “tanker war”.

via ZeroHedge News https://ift.tt/2ymym7S Tyler Durden

Last month, a BullionStar article titled “The Fifth Wave: A new Central Bank Gold Agreement?” brought your attention to the fact that the fourth and current round of the Central Bank Gold Agreement (CBGA) run by a cartel of heavyweight central banks in Europe was about to expire, and that these gold agreements, which have been running in rolling five year periods since September 1999, were not designed for the purposes they claimed to be.

That CBGA1 and CBGA2 from 1999 – 2008, were not intended to help the wider gold market by limiting central bank gold sales, but were really a cover by the central bank syndicate members to account for nearly 4000 tonnes of gold that had already been sold or leased in the 1990s. That CBGA3 was then used to distract the gold market about the secretive ‘gold sales’ that the IMF claimed to have undertaken in 2010, which were really another book squaring exercise for disposed IMF gold.

The heavyweight signatories to the central bank gold agreements (CBGAs) include Eurozone member banks such as the Bundesbank, the Banque de France, Banca Italia, De Nederlandsche Bank, National Bank of Belgium, the European Central Bank (ECB) itself, as well as the non-Eurozone Swedish Riksbank and the Swiss National Bank. In its composition, the consortium replicates the nexus of the 1960s London Gold Pool (Switzerland, Germany, France, Italy, Netherlands, Belgium) and the nexus of the central banks which met at the Bank of International Settlements (BIS) in 1979 and the early 1980s to plan a secretive new 1980s gold pool.

Last month’s article also pointed to the fact that this syndicate of European central banks had also been absent as buyers of monetary gold over the 1999 – 2019 period, when all around them central banks of nations such as Russia, China, India, Turkey, and Kazakhstan were busily doing the opposite and boosting their strategic monetary gold reserves.

The question then was, do these European central bank signatories to the CBGAs have an agreement among themselves not to buy any gold, that is contained in, for example, a non-public annex to the Agreement? If so:

“It would not be the first time that G10 and Switzerland central banks agreed among themselves not to purchase gold. They did so in the mid 1970s when in conjunction with the IMF, when “the countries in the Group of Ten and Switzerland also agreed that there be no action to peg the price of gold, and that the total stock of gold in the hands of the Fund and the monetary authorities of the Group of Ten and Switzerland would not be increased.”

European System of Central Banks

Open Season on Gold Buying

While waiting for word from the European Central Bank (ECB) about a fifth CBGA, the conclusion here last month was that:

“Given that the whole CBGA scheme was a cover whose main purpose has already been achieved, there is no compelling logic for a fifth CBGA, except of course unless there have been further physical gold flows out of western central banks which need to be squared off in the books.”

Well, we don’t have to wait any longer, since the ECB, Swiss National Bank, and Swedish Riksbank have all issued coordinated press releases dated 26th July, confirming that there will not be a fifth central bank gold agreement when the current agreement expires in September 2019.

This is because, according to the ECB press release, the signatory banks “conclude that a formal gold agreement is no longer necessary” because they say “the market has developed and matured”, more specifically that “since 1999 the global gold market has developed considerably in terms of maturity, liquidity and investor base.”

Given that the real reason for the CBGAs from 1999 onwards was to close out previously sold and leased gold while hiding the transactions, this excuse for non-renewal is irrelevant, but even in its wording about the changing shape of the global gold market it is misleading.

The ECB – SNB – Riksbank press releases also mislead with the ironic claim that “the Agreement contributed to balanced conditions in the gold market by providing transparency regarding the intentions of the signatories”, when in fact the Agreement was the complete opposite, i.e. a cover for gold that had already been disposed of.

However, this latest news about the non-renewal of the CBGA is important because it is the best evidence yet that there most likely is an unpublished agreement among the participating European central banks not to buy any gold, but that this private agreement not to buy gold is now being torn up. Which would mean that open season for central bank gold buying is about to begin.

The CBGA member press releases acknowledge the eagerness to buy gold, saying that “central banks and other official institutions in general have become net buyers of gold” and that “the signatories confirm that gold remains an important element of global monetary reserves, as it continues to provide asset diversification benefits.” The Swiss National Bank press release adds some flavor claiming that the “gold agreement [is] no longer necessary due to changes in market conditions and in central bank activities.”

As none of the CBGA cartel central banks “currently has plans to sell significant amounts of gold“, has it been a case of gold buying envy as Russia, China and the even Poland and Hungary have piled into the yellow metal? It would certainly seem so.

The press release from the ECB can be read in pdf format here, from the Swiss National Bank (SNB) in pdf format here, and from the Swedish Riksbank in pdf format here.

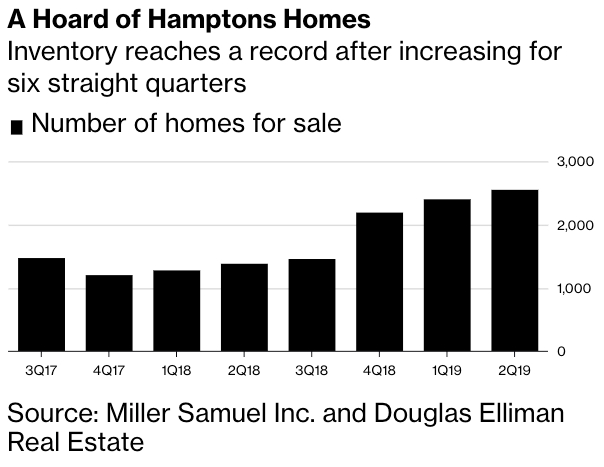

Hamptons, the beachfront playground for New York City’s financial elite, just recorded the worst second quarter for sales in eight years, according to a report from Douglas Elliman and Miller Samuel, and first reported by CNBC.

Real estates sales and prices in the Hamptons extended lower through 2Q19, indicating the luxury home market continues to stagnate for the last six quarters, the report said.

The weakness in the Hamptons was confusing for CNBC, considering they said real estate in the region should have been positive because the stock market is higher. But as Zerohedge readers know, the stock market has remained extremely disconnected from fundamentals this year, if not the last decade.

The Hamptons is experiencing the same pressures as many luxury markets across the country: an oversupply of mansions, dwindling demand from foreign buyers, changes to SALT deductions, and sellers who have become delusional that real estate prices can still hold 2014 values.

With no end in sight, the bust of the Hamptons real estate market could become more severe through 2020.

Miller Samuel said the number of homes listed in the region doubled in 2Q19, to 2,500. This is the highest level the research firm has recorded since it started gathering data in 2006.

According to the report, there is a 5-month supply of listings, with more than a three-year supply of luxury properties.

“I think it’s premature to talk about a turnaround until the inventory growth slows down,” said Jonathan Miller, CEO of Miller Samuel, the appraisal firm.

“There is just not a sense of urgency. The buyers are just waiting it out.”

Brokers told CNBC that demand is showing up for more affordable homes but not for +$5 million.

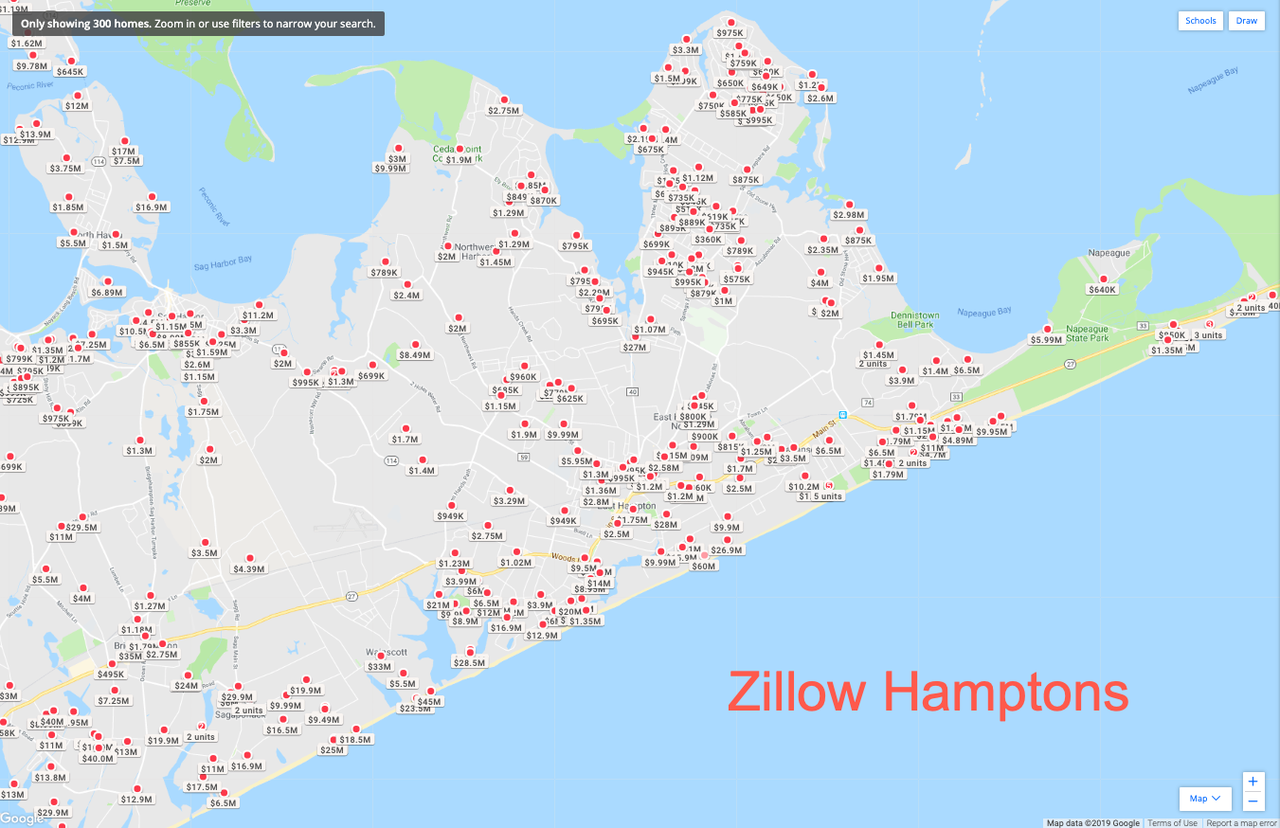

“You might look at Zillow and see nine properties on the oceanfront in Southampton, which looks like a lot,” said Cody Vichinsky of Bespoke Real Estate in the Hamptons.

“But then you dig into it, and you see that six of them are in places where you’d never want to live, with constant helicopter noise or a triple dune or encumbrances. And then the others, the price is ridiculous. When a property is priced decently, it goes.”

Glancing at Zillow Hamptons, hundreds of homes are for sale ranging from $625k to $60 million.

In a recent listing, the family of James Evans, the former chairman of the Union Pacific railroad empire, put their waterfront estate in East Hampton on the market for $60 million. The 5,500-square-foot home sits on 5.4 oceanfront acres, has an estimated mortgage payment of $362k per month.

A $49 million mansion on 4.5 acres with 430 feet of direct oceanfront has been on the market for 850 days.

The pullback in Hamptons real estate is a sobering reminder that inventory is building to levels that are making sellers uncomfortable, could unleash panic selling and metastasize into a full-blown market rout with implications beyond New York City.

via ZeroHedge News https://ift.tt/2SJbbOG Tyler Durden

A few Democrats get angry and all of America has to endure the hand-wringing…

Senator John Kennedy said the “four horsemen” of the Democratic party’s internal apocalypse were the “reason there are directions on a shampoo bottle”.

Rashida Tlaib whined about Trump being a “bully”. AOC called America a “story. Ayanna Pressley called the president “predictable” despite her and her colleagues constantly appearing surprised or taken aback by his actions. Ilhan Omar refused to retract her wildly anti-Semitic comments.

Gaslighting America into believing they’re the helpless victims of a pitchfork-wielding president.

Then there was Yahoo News basically calling actor Chris Pratt a white supremacist for wearing a t-shirt with a Gadsden Flag on it for a veteran’s charity.

It’s only been about 10 days since the Betsy Ross flag debacle. Megan Rapinoe’s U.S. flag would still be on the ground were it not for her lesbian teammate who picked it up. I mention her sexuality only because we were expected to be mad about that, for some reason. No one was.

They know they’ve gone nuts because they stealthily try to go un-nuts, having gone nuts already. Check the stealth edit on the Yahoo News article.

Originally: “Chris Pratt criticised for ‘white supremacist’ T-shirt’.

Later: “Chris Pratt criticised for T-shirt choice’.

You can’t go un-nuts once we’ve seen you go nuts.

That applies to Starbucks, Nike, Oreos, Yahoo, CNN, all of you.

…

For the right, it’s an example of how “everything is racist to the left”.

For the left it is an opportunity to shift the Overton window further. To create consternation about a flag that requires no consternation. To undermine the founding of America by undermining its symbols.

That’s all it took.

And that’s why all it takes to upset the political apple cart is those who John Kennedy referred to as the Democrats’ four horsemen: Alexandria Ocasio-Cortez, Ayanna Pressley, Rashida Tlaib, and Ilhan Omar.

One media company rattled the cage of another – for exposure, clicks, and profit – and America got sucked into a heated political war as a result.

The same reason Nike snubbed the Betsy Ross flag. For profit.

And that’s what the ‘Squad’ are doing to America.

Riling her up. Dividing her. Causing consternation and upheaval wherever they go, and through whatever they say.

For profit.

In their case, it’s not so much financial gain they’re after. It’s power. That’s what the whole internal fight they’re having with Nancy Pelosi is about. Power. The left craves power as the right craves autonomy.

But they’re forgetting those now “racist” words: Don’t Tread On Me.

And that’s why Trump continues to goad them. Because Americans don’t like being tread upon. And he knows elevating them provides his best hope of waking people up to the danger of a Democrat president, House, and Senate in 2020.

A Supreme Court decision to allow President Trump to redirect $2.5 billion in Pentagon funds towards his long promised border wall will “really accelerate” progress on the project, according to Acting DHS Secretary Kevin McAleenan in Sunday appearance on Fox News.

The 5-4 decision will allow for the construction of more than 100 miles of fencing – the most significant step yet, according to Bloomberg.

McAleenan said while the court’s ruling was “a big victory” to build more of the wall, “we do remain in the midst of a border security crisis” with migrants flooding the region and that Congress must take more action to deter crossings.

“We made very clear the targeted changes in law that we need,” McAleenan said. –Bloomberg

In Friday’s order, the Supreme Court said that the government made a “sufficient showing” that several groups challenging the decision had insufficient grounds to bring a lawsuit against President Trump’s Feb. 15 national emergency to fund the wall without congressional approval.

“Today’s decision to permit the diversion of military funds for border wall construction will wall off and destroy communities, public lands, and waters in California, New Mexico, and Arizona,” said Sierra Club attorney GLoria Smith.

Trump, meanwhile, took a victory lap – tweeting “Wow! Big VICTORY on the Wall,” adding “Big WIN for Border Security and the Rule of Law!”

Wow! Big VICTORY on the Wall. The United States Supreme Court overturns lower court injunction, allows Southern Border Wall to proceed. Big WIN for Border Security and the Rule of Law!

The wall segments in Arizona, New Mexico and California would give Trump a tangible achievement to tout in his re-election campaign. Until now, congressional and court resistance had thwarted significant progress toward a stronger barrier on the almost 2,000-mile frontier.

During his campaign, Trump said Mexico would pay for the wall. On Saturday he said the U.S. would be “fully reimbursed for this expenditure, over time, by other countries.” He didn’t say how. –Bloomberg

“This is not over,” said the ACLU’s lead lawyer, Dror Ladin. “We will be asking the federal appeals court to expedite the ongoing appeals proceeding to halt the irreversible and imminent damage from Trump’s border wall.”

That said, even Bloomberg has to admit: “the court’s unsigned order suggested the administration was likely to win the fight. The order said the administration “has made a sufficient showing at this stage” that the groups don’t have the legal right to challenge the Pentagon’s spending decisions.”

via ZeroHedge News https://ift.tt/2Mn1bcQ Tyler Durden

International Man: Economically, politically, and socially, the United States seems to be headed down a path that’s not only inconsistent with the founding principles of the country but accelerating quickly toward boundless decay.

The word “decadence” is often associated with the fall of the Roman Empire, which became morally corrupt—its people lazy, wasteful, and lacking discipline. Many observers have pointed out the US is similarly becoming decedent. How do you see it?

Doug Casey: There’s no question about it; the culture in the US is changing. Where to start? It’s a book-length subject. One thing that absolutely amazes me is that the term “cultural appropriation” has become a buzzword for a lot of people today. The concept is actually completely insane.

It’s bizarre—perverse, really—that the people doing the most whining about cultural appropriation by Americans don’t actually have worthwhile cultures themselves. The fact of the matter is that the only culture in the history of the world that amounts to anything is that of Western civilization. The West has given all of humanity concepts like freedom of speech, freedom of thought, freedom of the press, free markets, individualism, science, and rationality. In addition, the West has created almost all of the world’s great music, literature, architecture, and philosophy

People trying to make cultural appropriation on the part of Americans into a scandal are basically scam artists and race hustlers. I’m talking about blacks who are outraged about white women wearing African earrings. Or Hispanics picketing a couple of white girls who set up a taco stand after visiting Mexico.

I’ve spent a lot of time in the Spanish-speaking world south of the US border. Other than quaint sombreros, some local food, and some basically primitive handicrafts, they don’t have a culture that’s worth anything.

That’s absolutely true of Africa. Africans should be eternally grateful to the West if, when da Gama was rounding the Cape in the 15th century, he’d just thrown out a wheel. But he would have also had to throw out an instruction book. But nobody could read it, because the entire continent south of the Sahara was illiterate.

This is true of most of the primitive world. I hesitate to say “developing world” because development is solely due to imported capital and expertise. If that inflow stops, Africa could go back to the bush, with mass starvation.

The only cultures in the world that can compete with Western civilization are those in the Orient. But what do they have? Frankly, not much, apart from Taoism, Zen, yoga, martial arts, and some great cuisines. Some things of value but not much by comparison to the West.

The fact that Westerners are ashamed of their culture is a sign of the collapse of the West. Most Europeans and Americans are so intimidated by these people squalling about ridiculous things that they don’t even try to defend themselves.

Instead, they agree with their attackers, stick their tails between their legs, and wander off. I don’t doubt Americans will agree to pay “reparations” to blacks for slavery. It’s an absurd concept, about as ridiculous as the English paying me reparations because of what they did to my ancestors in Ireland 200 years ago.

In fact, the Africans exported to the New World were the lucky ones. Their descendants have a standard of living and opportunities 10 or 20 times greater than those still on the continent.

But the fact these things are even discussed is a definite sign of the collapse of the West. It’s very much like what happened in the late Roman Empire.

When Rome was in its ascendancy and at its height, the leaders of Rome were all native Romans or at least native Italians. If they were born in other parts of the Empire, they were of Roman culture and had Roman names and Roman values. They had a stake in their civilization.

But as time went on, all of this started changing.

By the time the barbarians invaded the Empire wholesale—starting with the battle of Adrianople in 378 AD—the handwriting was already on the wall. Within 30 years, the barbarians controlled the entire Empire.

The old political structure had completely collapsed. Native Romans were leaving the Empire, going to barbarian lands, to avoid onerous taxation. The currency was worthless. The economy was in a shambles. The military structure had completely collapsed. None of the soldiers were Italians; they were all barbarians hired as mercenaries. Likewise, here in the US, few Americans in the diminishing middle class want to join the military. The city of Rome itself was sacked in 410 AD and it never really recovered.

International Man: Economically, the US government continues to spend ever-increasing amounts of money. In 2018 alone, the federal deficit was $779 billion—a $113 billion increase from the year before. Politicians on both sides of the aisle are falling over themselves to offer new government freebies that could pay for college, medical care, and the list goes on.

How does this play into the theme of US decadence?

Doug Casey: Well, whether you’re an individual or a family or a country, when you live above your means, you’re almost by that very fact decadent. You’re not planning for the future.

But the US government’s debt and reported deficits represent only current cash outlays, not obligations in the form of future spending. If the deficits were represented with accrual accounting—which is what businesses have to do—the annual deficits would probably be more like $3 trillion.

Not to mention that interest rates are artificially suppressed to about 2% in the US. At more normal levels of, say, 6%, the annual deficit would be about $800 billion higher. So the financial situation is actually much, much worse than it seems.

On top of all this is the fact that these deficits come during a time of supposed recovery. But the “recovery” has been ramped up by creating trillions of new dollars and allowing people to borrow at effectively negative interest rates, certainly after inflation. This is all very decadent.

Eat, drink, and be merry, for tomorrow we die. That’s not the attitude of a rising civilization.

The opposite of “decadent” is to be constructive, disciplined, forward-thinking, and self-respecting. You produce more than you consume and save the difference.

That’s exactly the opposite of what Americans are doing today.

We’re completely decadent.

Small comfort that the Europeans are even worse off than we are.

International Man: On an individual level, Americans are living beyond their means. Many Americans have less than $1,000 in savings.

What does this say about a society?

Doug Casey: It augurs very poorly.

The average American is one paycheck from not being able to pay his rent. When the distortions that have been cranked into the economy over just the last 10 years unwind and the economy as a whole goes downhill again, there are going to be millions of people who can’t pay their rent. Many millions more are going join the 42 million Americans now living on food stamps.

The social repercussions of this are predictable.

The population will get angry; many will go into the streets and riot. They’re going to vote overwhelmingly for some politician who says that he—or quite possibly she—can cure all their problems by giving them free stuff stolen from rich people.

In a way it’s understandable, because the fact of the matter is the rich have indeed been getting richer at an accelerating rate.

Why?

Because they’re the ones that get to stand next to the firehose of money that’s coming out of Washington. They get it first; they get most of it. It’s another sign of a society in decline: the dominance of cronies. That creates a lot of class antagonism.

It’s going to explode and be really ugly. Perhaps one thing keeping a lid on the situation is the huge number of Americans on psychiatric drugs: Zoloft, Prozac, and a hundred others. Perhaps millions of others don’t care as long as their internet connection enables them to play video games.

International Man: Aside from the financial aspect of decadence, what is happening culturally and intellectually in the United States? For example, many Americans are rejecting biological facts in favor of the politically correct fad of the day. Is this a sign of decline?

Doug Casey: The PC types say there are supposed to be 30 or 40 or 50 different genders—it’s a fluid number. It shows that wide swathes of the country no longer have a grip on actual physical, scientific reality. That’s more than a sign of decline; it’s a sign of mass psychosis.

There’s no question that some males are wired to act like females and some females are wired to act like males. It’s certainly a psychological aberration but probably has some basis in biology.

The problem is when these people politicize their psychological peculiarities, try to turn it into law, and force the rest of the society to grant them specially protected status.

Thousands of people every year go to doctors to have themselves mutilated so that they can become something else. Today they can often get the government or insurers to pay for it.

If you want to self-mutilate, that’s fine; that’s your business even if it’s insane. To make other people pay for it is criminal. But it’s now accepted as normal by most of society.

The acceptance of politically correct values—“diversity,” “inclusiveness”—trigger warnings, safe spaces, gender fluidity, multiculturalism, and a whole suite of similar things that show how degraded society has become. Adversaries of Western civilization like the Mohammedan world and the Chinese justifiably see it as weak, even contemptible.

As with Rome, collapse really comes from internal rot.

Look at who people are voting for. It’s not that Americans elected Obama once—a mob can be swayed easily enough into making a mistake—but they reelected him. It’s not that New Yorkers elected Bill de Blasio once, but they reelected him by a landslide. All of the Democratic candidates out there are saying things that are actually clinically insane and are being applauded.

International Man: In fact, in the recent Democratic debate, candidate Julián Castro even mentioned giving government-funded abortions to transgender women—biological men. It received one of the loudest bouts of applause from the audience.

That’s not to mention that two other candidates spoke in broken Spanish when responding to the moderator’s questions.

Doug Casey: As you said, it got a lot of applause.

US presidential candidates speaking in Spanish would be very much like an ancient Roman addressing the Forum in Gothic, not Latin. It’s all over for a culture when it starts using the language of its conqueror. In a restaurant here in Aspen, the owners have a sign in Spanish that refers to the progress of the Reconquista—the recapture of the American Southwest from the Anglos. Perhaps someone will speak Arabic in the next debates.

I hate to sound defeatist, but it’s all over for what was once known as American civilization. The celebrity of AOC is indicative. How else could a 29-year-old Puerto Rican waitress, poorly educated and not very bright, set the political tone for the whole country?

International Man: Is America’s late-stage decadence a product of its political and economic decline or vice versa?

Doug Casey: The decadence we see all around us is arising from every source. Cultural, economic, and political. Cultural decline is the most basic area. Massive immigration of people with different cultures, languages, and religions guarantee it. Especially if they’re coming because of free benefits. Many actually despise traditional American culture, as well as holding the current culture in contempt.

Their views are then reflected in a corruption of the politics. We see that with the apparent acceptance of the Squad—although I prefer to call them the “Gang of Four.” Politics engenders economic distortions. Part of the problem is that politics completely dominates the economy today.

For Trumpers to think that building a wall is going to change things is naïve. A wall will be about as effective as a kid’s sandcastle on the beach to hold back the waves.

The barbarians are already within the gates.

* * *

As Doug Casey discussed, the late stage decadence in the US is contributing to a growing wave of misguided socialist ideas and politicians. All signs point to this trend accelerating until it reaches a crisis… one unlike anything we’ve seen before. That’s exactly why Doug and his team just released this urgent video. Click here to watch it now.

via ZeroHedge News https://ift.tt/2yhHryU Tyler Durden

A giant ‘city-killer’ asteroid that just whizzed past earth seemingly appeared “out of nowhere” has stunned astronomers after only being discovered last week, days before it flew within around 45,000 miles from earth – or less than 20% of the distance to the moon, according to the Washington Post.

“I was stunned,” said Alan Duffy – lead scientist at the Royal Institution of Australia. “This was a true shock.”

This asteroid wasn’t one that scientists had been tracking, and it had seemingly appeared from “out of nowhere,” Michael Brown, a Melbourne-based observational astronomer, told The Washington Post. According to data from NASA, the craggy rock was large, an estimated 57 to 130 meters wide (187 to 427 feet), and moving fast along a path that brought it within about 73,000 kilometers (45,000 miles) of Earth. That’s less than one-fifth of the distance to the moon and what Duffy considers “uncomfortably close.” –Washington Post

“It snuck up on us pretty quickly,” said Michael Brown, an associate professor at Australia’s Monash University School of Physics and Astronomy, adding later “People are only sort of realizing what happened pretty much after it’s already flung past us.”

The asteroid was discovered by separate astronomy teams in the United States and Brazil – while information on the ‘city-killer’ was announced only hours before it shot past Earth.

“It shook me out my morning complacency,” said Brown. “It’s probably the largest asteroid to pass this close to Earth in quite a number of years.”

How did we not see this coming?

For starters, while Asteroid 2019 OK (as it’s been named) is large enough to destroy a city, it’s nowhere near the half-mile-wide or larger asteroids which NASA and its international partners have scientists think they’ve identified 90% of.

“Nothing this size is easy to detect,” said Duffy. “You’re really relying on reflected sunlight, and even at closest approach it was barely visible with a pair of binoculars.”

Brown said the asteroid’s “eccentric orbit” and speed were also likely factors in what made spotting it ahead of time challenging. Its “very elliptical orbit” takes it “from beyond Mars to within the orbit of Venus,” which means the amount of time it spends near Earth where it is detectable isn’t long, he said. As it approached Earth, the asteroid was traveling at about 24 kilometers per second, he said, or nearly 54,000 mph. By contrast, other recent asteroids that flew by Earth clocked in between 4 and 19 kilometers per second (8,900 to 42,500 mph).

“It’s faint for a long time,” Brown said of Asteroid 2019 OK. “With a week or two to go, it’s getting bright enough to detect, but someone needs to look in the right spot. Once it’s finally recognized, then things happen quickly, but this thing’s approaching quickly so we only sort of knew about it very soon before the flyby.” –Washington Post

“It should worry us all, quite frankly,” Duffy added. “It’s not a Hollywood movie. It is a clear and present danger.“

The reason Asteroid 2019 OK is referred to as a ‘city-killer’ is because it’s large enough that if it struck earth, most of it would likely have reached the ground, resulting in catastrophic damage.

“It would have gone off like a very large nuclear weapon,” with enough energy to level a city,” said Duffy. “Many megatons, perhaps in the ballpark of 10 megatons of TNT, so something not to be messed with.”

In 2013, a much smaller meteor (around 65 feet across) broke up over the Russian city of Chelyabinsk – the shockwave from which shattered windows, collapsed roofs, caused car accidents, and provided some amazing footage to boot. Around 1200 people were injured.

According to the report, “The last space rock to strike Earth similar in size to Asteroid 2019 OK was more than a century ago, Brown said. That asteroid, known as the Tunguska event, caused an explosion that leveled 2,000 square kilometers (770 square miles) of forest land in Siberia.“

What to do?

Turning his attention to the topic of planetary defense, Duffy warns against trying to “blast it with a nuke” to avert disaster.

“It makes for a great Hollywood film,” he said. “The challenge with a nuke is that it may or may not work, but it would definitely make the asteroid radioactive.”

Instead, he recommends a ‘gravity tractor’ which would use the gravity of a spacecraft – something Duffy calls an “elegant solution.”

In light of Asteroid 2019 OK, Duffy stressed the importance of investing in a “global dedicated approach” to detecting asteroids because “sooner or later there will be one with our name on it. It’s just a matter of when, not if.”

“We don’t have to go the way of the dinosaurs,” he said. “We actually have the technology to find and deflect certainly these smaller asteroids if we commit to it now.”

Emily Lakdawalla, senior editor of the Planetary Society, which promotes space exploration, said the recent near miss is a reminder that “it’s an important activity to be watching the skies.” The more that can be learned about an asteroid, the better prepared people can be to prevent potential disasters, she told The Post. –Washington Post

“It’s the kind of thing where you learn about something that you didn’t know about, like things flying close by us, and your inclination is to be scared,” said Emily Lakdawalla. “But just like sharks in the ocean, they’re really not going to hurt you and they’re really fascinating to look at.”

Sure, until one lands on your house.

via ZeroHedge News https://ift.tt/30Zx9zM Tyler Durden

With the most important week for newsflow set to begin shortly, with the Fed expected to launch its first easing cycle in over a decade on July 31, the only question investors want answered is whether the Fed will cut rates by 25bps (while this is now fully priced in, many suggest it may be too little and lead to a sharp drop in risk assets) or by 50bps (which many see as overkill considering the relatively stable state of the US economy).

While the NY Fed recently and unceremoniously slapped down its president, John Williams, in an unprecedented example of the Fed’s failure to communicate, for suggesting it was now accepted that a 50bps rate cut is FOMC consensus, in effect sharply lowering the odds of a 50bps rate cut, the truth is that nobody knows what will Powell will announce on Wednesday. So, in order to give some further perspective on where the US economy is now, compared to September 2007 – when the Fed also started an easing cycle by cutting rates by 50bps to insure against uncertainty resulting from tighter financial conditions, and just two months before the last recession officially began in December 2007 – Morgan Stanley compared some of the key leading and market indicators now and back in September 2007.

As Morgan Stanley credit strategist Matthew Hornbach writes, one needs to look at the first cut in 2007 without the benefit of hindsight – meaning, the Fed’s decision to cut 50bp had nothing to do with the coming financial crisis. It was about lessening downside risks coming from tighter financial conditions. Fast forward to today when it’s about downside risks coming from global growth and trade uncertainty.

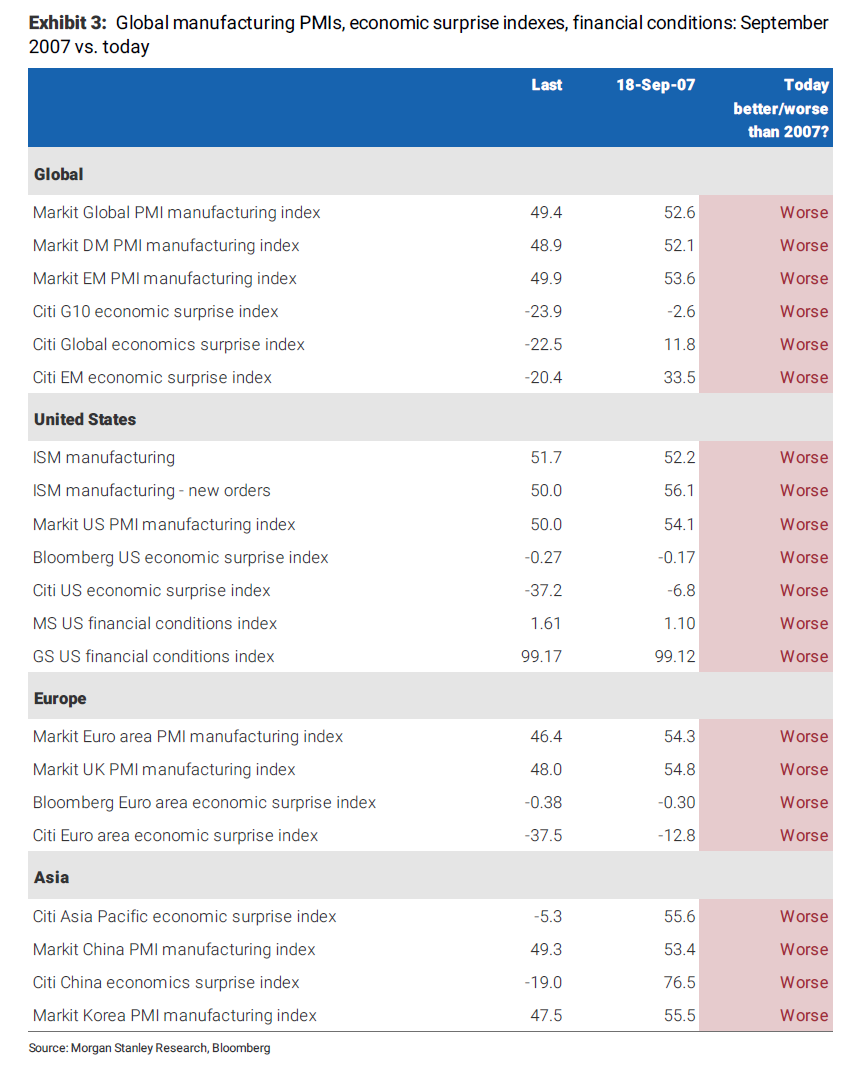

And here Hornbach makes a the stunning observation: as shown in the exhibit below, things look worse today than at the September 2007 meeting on every metric.

Of course, as MS admits, not everything looks worse than it did in September 2007, like some of the nonmanufacturing (services) PMI data (which the Fed isn’t focusing on when it comes to downside risks). The US labor market data also look better today than in late 2007. In particular, a very weak nonfarm payroll report occurred in early September 2007 (August NFP -4k vs. 100k expected; July revised down 125k to -33k.

On the other hand, developments in financial markets since the Committee’s last regular meeting have increased the uncertainty surrounding the economic outlook. The Committee will continue to assess the effects of these and other developments on economic prospects and will act as needed to foster price stability and sustainable economic growth.

Perhaps, MS is right, and the consensus is actually too hawkish at the moment, and Powell will indeed cut 50bps at 2pm on July 31. While we don’t know what the Fed’s ultimate decision will be, we have a nagging feeling it won’t matter much as we will simply remind readers of what happened back in Sept 2007 when the Fed did cut 50bps.

First, the S&P hit an all time high just after, in October 2007: that high would not be revisited until 6 years later, and at the cost of trillions in central bank QE.

Second, just three months after the Fed cut 50bps, the recession started in December 2007, which then promptly mutated into the greatest financial crisis since the Great Depression.

Third, after hitting a record – for the time high – the S&P then proceeded to plunge 60% lower by March 2009, and only the coordinated effort of all the world’s central banks managed to restore faith in the Western financial system.

It will be delightfully ironic if the Fed’s rate cut in three days unleashes a similar chain of catastrophic events.

via ZeroHedge News https://ift.tt/2YpXCov Tyler Durden

Most proponents of the nondelegation doctrine worry that Congress delegates too much decisionmaking authority to administrative agencies. The conventional critique of delegation thus emphasizes the breadth of discretion agencies are given to issue rules, define offenses, and set broad policy priorities. These sorts of choices are inherently legislative, the argument goes, and are thus of the sort that should be made by the people’s elected representatives.

A central concern about broad delegation is the resulting democratic deficit of agency decisionmaking. The specific concern is that the hand-off of broad policymaking authority transfers the power to enact normative preferences into positive law from the people’s elected representatives to unelected, and therefore less democratically accountable, administrators. Yet as some degree of delegation is inevitable (and has been with us since the earliest days of the Republic), the question inevitably becomes “how much is too much” – and this is a question the courts have seemed unwilling (if not unable) to answer.

The persistent focus on the scope of legislative delegations has caused commentators to overlook another relevant dimension of delegation: Time. Particularly in an era of legislative inaction, the delegation of authority to administrative agencies is not occurring in the present, but in the past. When agencies wield broad regulatory power, they often rely upon authority delegated to them in years past, by a prior Congress, and they regularly rely upon legislative measures that are increasingly obsolete.

That agencies routinely rely upon past delegations to administer, implement and enforce their programs exacerbates delegation’s democratic deficit. Were agencies exercising authority recently delegated authority, one could argue that such delegations reflect a contemporary judgment of the desirability of delegating broad authority to a particular agency to address a particular concern, perhaps due to the technical complexity of the underlying subject matter. As things stand today, however, agencies often rely upon age-old delegations of authority to address contemporary concerns.

Consider the Clean Air Act (CAA) and its application to greenhouse gas emissions. Congress enacted the CAA’s basic architecture in 1970, and made substantial revisions in 1977 and 1990. As originally constructed, the CAA focused most acutely on localized air pollution. What courts have identified as the “heart” of the Act are those provisions authorizing and enforcing ambient air quality standards in metropolitan areas. Relatively little of the CAA’s core architecture concerned interstate air pollutants. Global climate change, in particular, was not yet a serious concern within Congress when the CAA was passed and amended, and there are no CAA provisions drafted with concerns like global climate change in mind.

Nonetheless, seventeen years after Congress last revisited the CAA, in Massachusetts v. EPA, the Supreme Court concluded that the Act’s definition of “air pollutant” was broad enough to encompass greenhouse gases, thus conferring upon the EPA the authority to address climate change. Whether the Court was correct to interpret the CAA in this fashion, this decision set in motion a series of regulatory initiatives that Congress never contemplated, let alone endorsed, and forced the EPA to retrofit a twentieth-century statutory regime to address a twenty-first century problem. The resulting mismatch between the CAA’s architecture and the nature of both greenhouse gas emissions and resulting climate change has confounded the EPA and the courts since (see, e.g., UARG v. EPA).

The temporal lag between legislative delegation and the utilization of delegated authority raises distinct concerns about whether such delegation is consistent with democratic governance. When decades pass between the enactment of statutes delegating authority to agencies and the exercise of that authority, there is a risk that the delegated authority will be used for purposes and in ways that the enacting Congress never considered. This may lead to situations where Congress has not provided the proper tool for the problem the agency is addressing, or where agencies are left to try and force the square pegs of contemporary problems into the round hole of previously delegated authority, as has occurred with climate change.

This problem of time is largely overlooked in debates over delegation. Jurists, policymakers, and commentators have not considered how the passage of time accentuates the concerns motivating calls for a nondelegation revival and how the temporal dimension of the problem might require a different set of reforms – or so Chris Walker and I argue in our draft paper “Delegation and Time.”

It might be possible to craft a new nondelegation doctrine that is sensitive to the problem caused by broad delegations cemented within obsolete statutes, but courts have shown little awareness of this dimension of the nondelegation problem, let alone what a doctrine might look like that could address it. So perhaps courts are not the place to look for a solution.

In our paper we consider how Congress could create incentives for more regular revision of those statutes that delegate authority to regulatory agencies. Specifically, we suggest that Congress could force itself to engage in more regular reauthorization of relevant programs, summarize examples of where this has actually occurred, and consider the implications of more regulator reauthorization on existing administrative law doctrines. In effect, we suggest that one way to address delegation concerns – and, in particular, to address the problem of time – is to find ways to make Congress legislate again, and that is something that Congress itself should be able to do.

from Latest – Reason.com https://ift.tt/2ypvxmt

via IFTTT

On the same day the large British warship HMS Duncan arrived in the Persian Gulf to assist the MHS Montrose in providing safety escorts to UK-flagged ships against the threat of Iranian seizure in the vital oil transit waterway, Tehran has again slammed the UK-led initiative of a joint European fleet patrolling the region.

An Iranian government spokesman warned on Sunday that a joint European task force operating so close to Iran’s coast “sends a hostile message” and is “provocative and will increase tensions,” according to semi-official Fars News Agency. The rhetoric is nothing new; however what is new and poses immense danger for the prospect of stumbling toward major conflict is the frequency of US and UK warships’ movement in the increasingly “crowded” narrow Strait of Hormuz.

Britain’s controversial call for a “European-led maritime protection mission”quickly gained the support last week of keyEU nations France and Germany, with Denmark and The Netherlands also joining the initiative.

The BBC reports that the HMS Montrose has thus far escorted 35 vessels through the strait, according to the Ministry of Defence (MoD). The larger HMS Duncan frigate will further join what Britain has dubbed “freedom of navigation” operations not just for UK vessels but “also our international partners and allies,” according Defence Secretary Ben Wallace.

This as London has kept up pressure for the release of the still impounded Stena Impero, and after Iran’s leaders last week appeared to offer an “exchange” of vessels of sorts, demanding the release of the Grace 1, which had been seized by Royal Marines early this month off Gibraltar. Iranian Government Spokesman Ali Rabiyee said further on Sunday that Iran “welcomes” the mediation of certain countries, but that ultimately“seizure of the British tanker was based on legal principles but Britain should release our oil tanker as soon as possible.”

HMS Duncan, via UK MoD

Rabiyee added, “Iran believes that security of the region should be established by the regional states and we are the biggest guardian of security for customers in the Persian Gulf” — while addressing reports of the joint European patrol mission.

But considering that it appears the US and Europe stand ready to increase patrols close to Iranian waters, the potential for an explosive spark which ignites greater conflagration remains higher than ever.

via ZeroHedge News https://ift.tt/2SNZzdd Tyler Durden

{kind=link}