With all eyes focused on whether Jay Powell will go 25, 50, and/or end QT, Nomura’s Charlie McElligott notes that dealers are generally positioned aggressively long and additionally ‘long gamma’. However, given the potential for some serious volatility tomorrow, what levels should investors be watching for chaotic unwinds to begin.

Via Nomura,

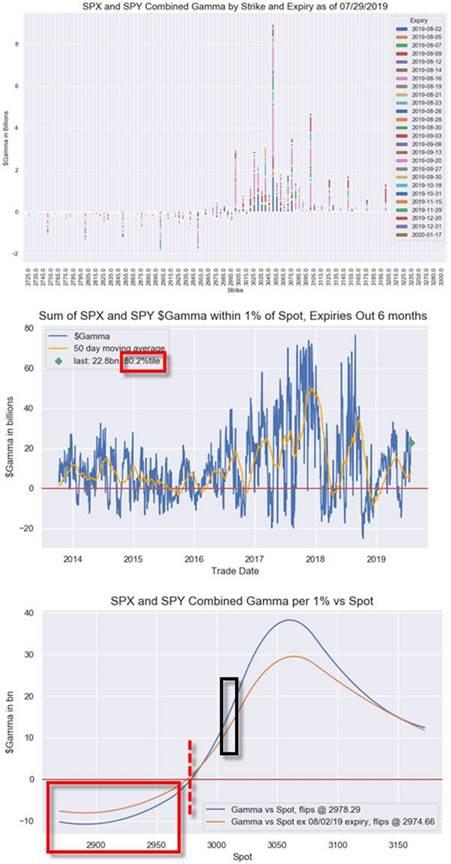

Our analysis shows that Dealers are currently “long Gamma” across combined SPX / SPY options, with $Gamma at 80th %Ile since 2013.

However, we would see that position “flip” to “Short Gamma” down at 2978, or 2974 ex the 8/2/19 expiry

Strikes that matter: 3050 ($9.375B), 3100 ($5.000B) and 3000 ($4.507B)

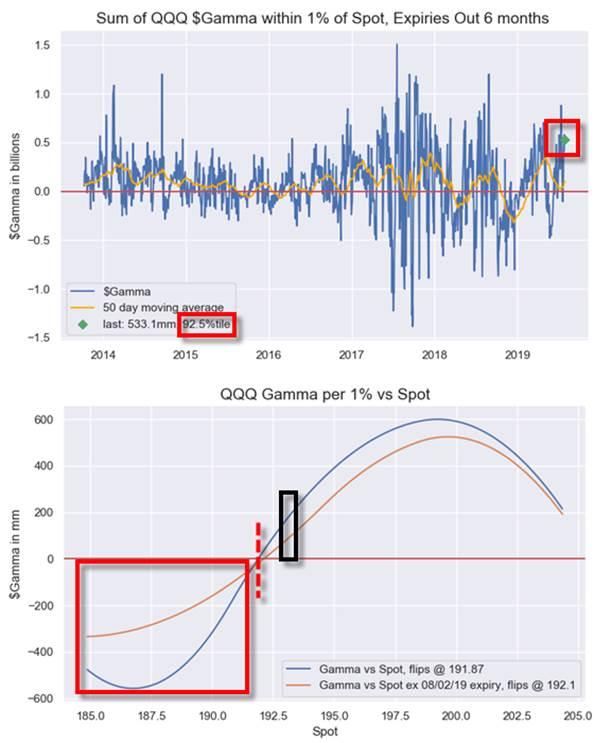

Also worth noting is the VERY long positioning in crowded Nasdaq.

This leaves QQQ too nearing a flip from current Dealer “Long Gamma” positioning to the “Short Gamma” flip-zone at 191.87 / 192.10 (ex 8/2/19 expiry)…

Particularly relevant at the $Gamma is currently extreme at 92.5 %ile since 2003.

Trade accordingly.

via ZeroHedge News https://ift.tt/2YcehAB Tyler Durden

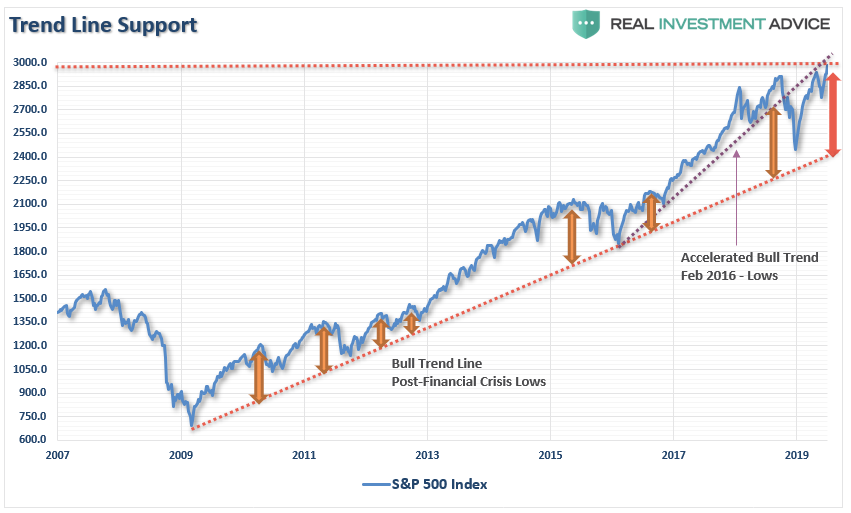

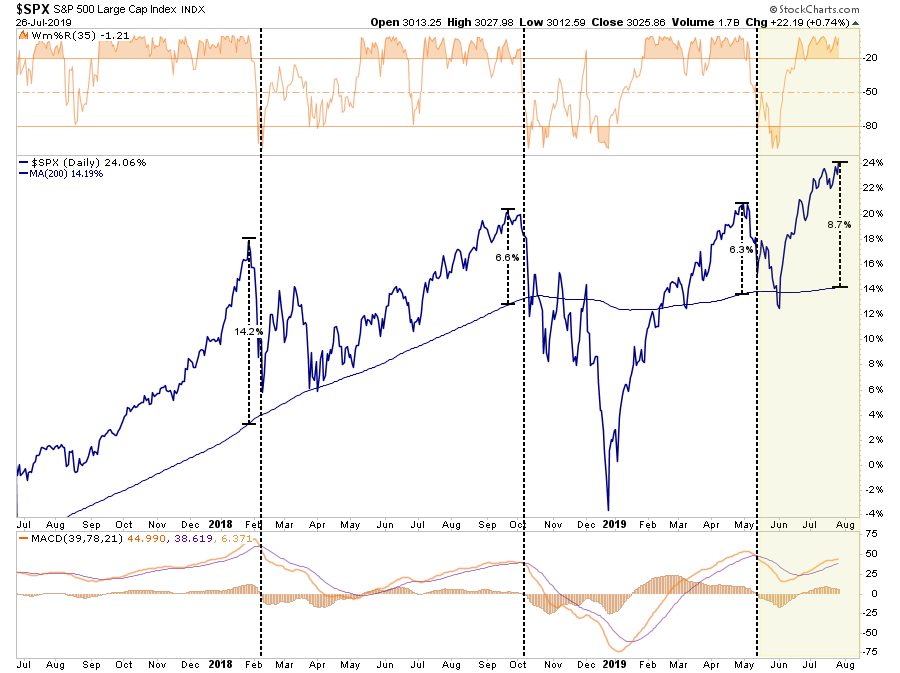

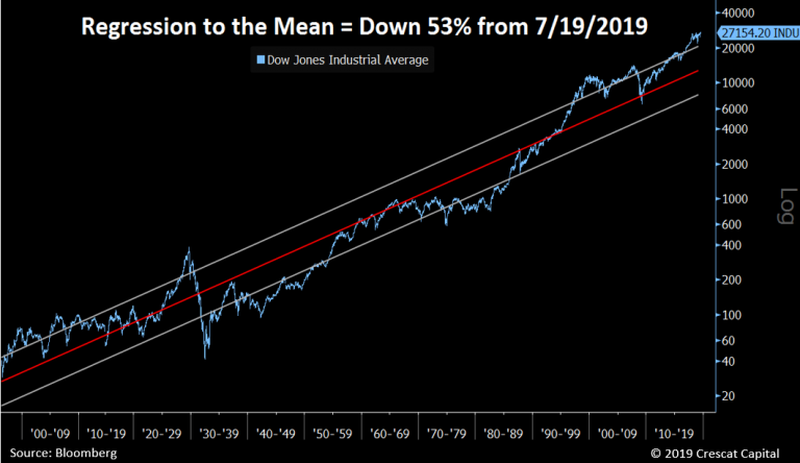

In this past weekend’s newsletter, I discussed the rather severe extensions of the market above both the longer-term bullish trend and the 200-dma. To wit:

There is also just the simple issue that markets are very extended above their long-term trends, as shown in the chart below. A geopolitical event, a shift in expectations, or an acceleration in economic weakness in the U.S. could spark a mean-reverting event which would be quite the norm of what we have seen in recent years.”

“As shown below, while the market is on a near-term “buy signal”(lower panel) the overbought condition, and near 9% extension above the 200-dma, suggests a pullback is in order.”

Of course, discussing the potential of a market correction is almost always perceived as being “bearish.” Therefore, by extension that must mean that I am either all in cash or shorting the market. In either case, it is assumed I “missed out” on previous advances.

If you have been reading our work for long, you already know we have remained primarily invested in the markets, but hedge our risk with fixed income and cash, despite our “bearish” views. I am reminded of something famed Morgan Stanley strategist Gerard Minack said once:

“The funny thing is there is a disconnect between what investors are saying and what they are doing. No one thinks all the problems the global financial crisis revealed have been healed. But when you have an equity rally like you’ve seen for the past four or five years, then everybody has had to participate to some extent.

What you’ve had are fully invested bears.”

While the mainstream media continues to misalign individuals expectations by chastising them for “not beating the market,” which is actually impossible to do, the job of a portfolio manager is to participate in the markets with a predilection toward capital preservation. This is an important point:

“It is the destruction of capital during market declines that have the greatest impact on long-term portfolio performance.”

It is from that view, as a portfolio manager, the idea of “fully invested bears” defines the reality of the markets that we live with today. Despite the understanding the markets are overly bullish, extended and overvalued, portfolio managers must stay invested or suffer potential “career risk” for underperformance.What the Federal Reserve’s ongoing interventions have done is push portfolio managers to chase performance despite concerns of potential capital loss.

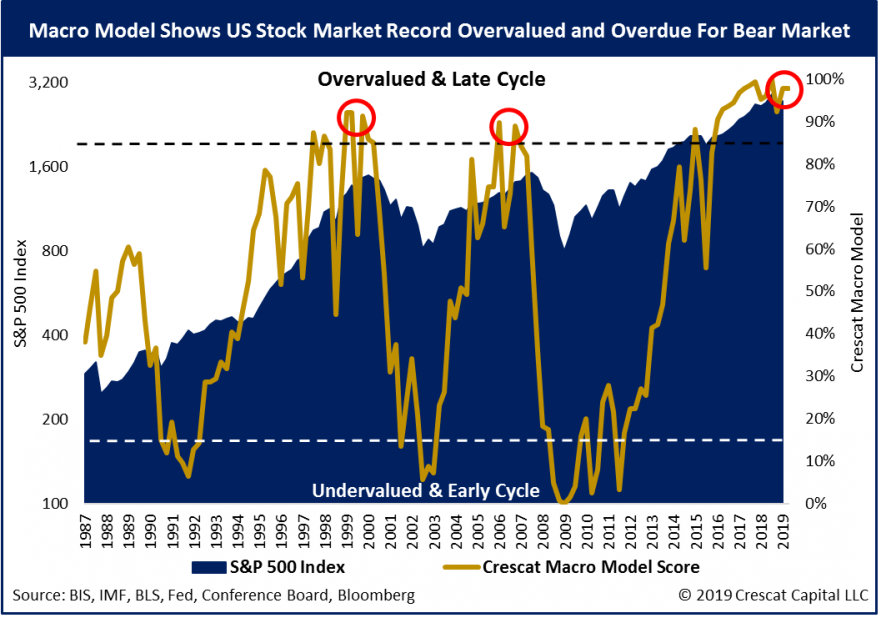

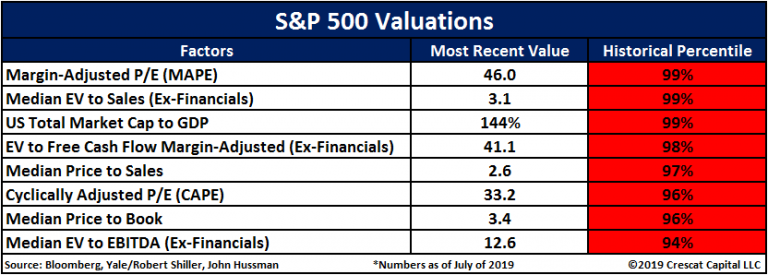

Managing portfolios for both risk adjusted returns while protecting capital is a delicate balance. Each week in the Real Investment Report(click here for free weekly e-delivery) we discuss the risks and challenges of the current market environment and report on how we are adjusting our exposures to the market over time. I wanted to share these charts from our friends at Crescat Capital which are all sending an important message. Currently, these are “risks” the market is ignoring, but eventually they will matter, and they will matter a lot.

Valuations

One of the consistent drivers behind the bull market over the last few years has been the idea of the “Fed Put.”As long as the Federal Reserve was there to “bailout” the markets if something went wrong, there was no reason NOT to be invested in equities. In turn, this has pushed investors to not only “chase yield,”due to artificially suppressed interest rates but to push valuations on stocks back to levels only seen prior to the turn of the century. As Crescat notes:

“ The reality is that stocks have never been this expensive for how low the 10-year Treasury yield is today. It’s true that all else equal, low interest rates justify higher valuations. However, the lowest interest rates historically haven’t corresponded to the highest P/E markets because extremely depressed yields also signal fundamental problems in the economy. Ultra-low rate environments are often marked by highly leveraged economies where future growth is likely to be weak.”

Given that valuations are all in the 90th percentile of historical values, it suggests that a reversion to the mean is increasingly likely.

Given these valuations are occurring against a backdrop of deteriorating economic growth and corporate profits, the risk to investor capital is high.

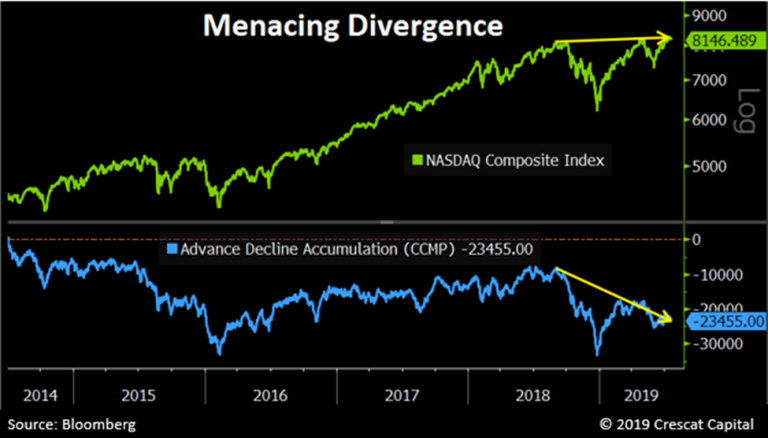

Divergences

I have previously addressed the narrowing of participation in the markets. Much of the advance in the markets this year alone can be solely accounted for by a handful of mega-capitalization stocks. Since those mega-cap reside in both the Nasdaq and the S&P 500 index, the lack of breadth is worth noting. As Crescat points out:

“While many US equity indices have marginally broken out to new highs recently, they have done so in the face of weakening market internals. Equity indices are being propped up by a narrowing group of leaders. The deteriorating breadth is most evident in the NASDAQ Composite, home to today’s leading growth stocks. While the overall index has reached record levels, the number of declining stocks has significantly outpaced the number of advancing stocks since last September. The collapsing internals point to an exhausted bull market.”

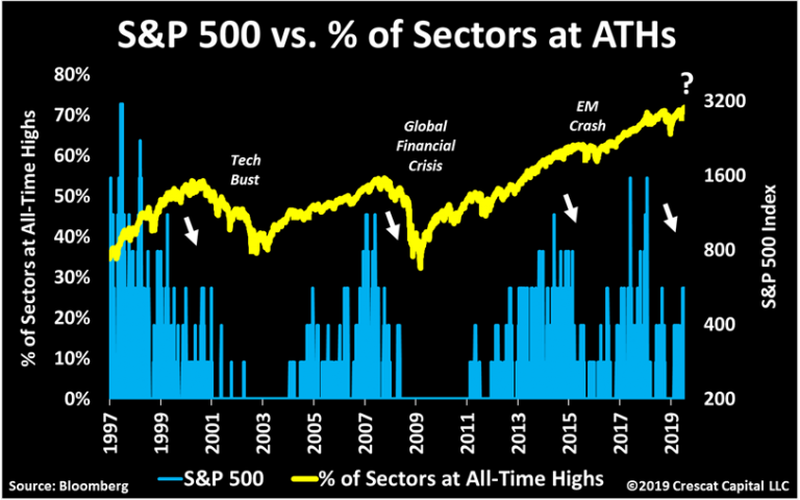

Volume & Participation

Another warning sign is that volume and participation have have also weakened markedly. These are all signs of a market advance nearing “exhaustion.” Back to Crescat:

“Stocks are also rising in defiance of extremely low volume. On July 16th, the SPDR S&P 500 ETF (SPY) had its lowest daily volume in almost 2 years. In a 15-daily average terms, volume is now as low as it was at the peak of the housing bubble and prior to the last two selloffs in 2018. Unusual calmness and breadth deterioration are not a good set up for record overvalued stocks.”

“The following chart is yet another illustration of how this recent rally in equities is running on empty, and again lacking substance. On July 15th, S&P 500 reached record levels, but only three sectors were at all-time highs. Market breadth today is faltering just as much as it did ahead of the last two recessions. In 2015, this was also the case, but back then only 20% of the yield curve was inverted. Now it’s close to 60%!”

Deviation

I have written many times in the past that the financial markets are not immune to the laws of physics. As I started out this missive, the deviation between the current market and long-term means is at some of the highest levels in market history.

There is a simple rule for markets:

“What goes up, must, and will, eventually come down.”

The example I use most often is the resemblance to “stretching a rubber-band.” Stock prices are tied to their long-term trend which acts as a gravitational pull. When prices deviate too far from the long-term trend they will eventually, and inevitably, “revert to the mean.”

As Crescat laid out, a “mean reverting” event would currently encompass a 53% decline from recent peaks.

Does this mean the current bull market is over?

No.

However, it does suggest the “risk” to investors is currently to the downside and some caution with respect to equity-based exposure should be considered.

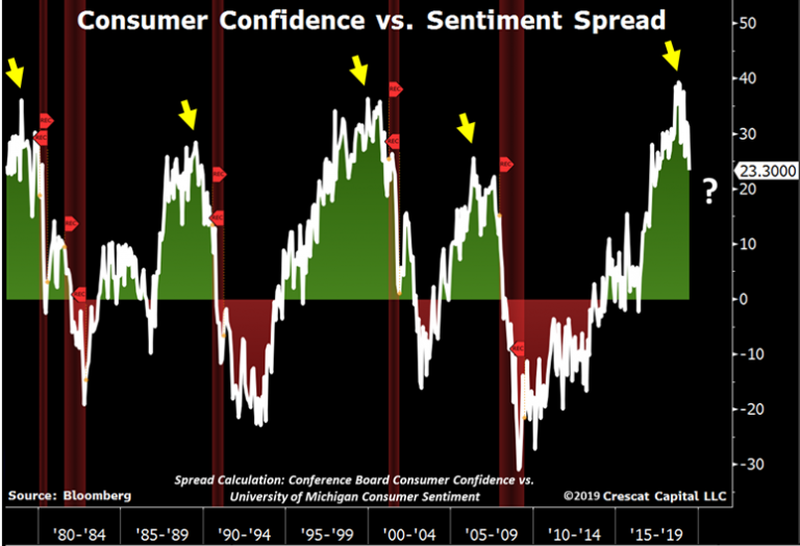

Sentiment

Lastly, is investor sentiment. When sentiment is heavily skewed toward those willing to “buy,” prices can rise rapidly and seemingly “climb a wall of worry.” However, the problem comes when that sentiment begins to change and those willing to “buy” disappear.

This “vacuum” of buyers leads to rapid reductions in prices as sellers are forced to lower their price to complete a transaction. The problem is magnified when prices decline rapidly. When sellers panic, and are willing to sell “at any price,” the buyers that remain gain almost absolute control over the price they will pay. This “lack of liquidity” for sellers leads to rapid and sharp declines in price, which further exacerbates the problem and escalates until “sellers” are exhausted.

With sentiment currently at very high levels, combined with low volatility and excess margin debt, all the ingredients necessary for a sharp market reversion are present. Am I sounding an “alarm bell” and calling for the end of the known world?

Of course, not.

However, I am suggesting that remaining fully invested in the financial markets without a thorough understanding of your “risk exposure” will likely not have the desirable end result you have been promised. All of the charts above have linkages to each other, and when one goes, they will all go.

So pay attention to the details.

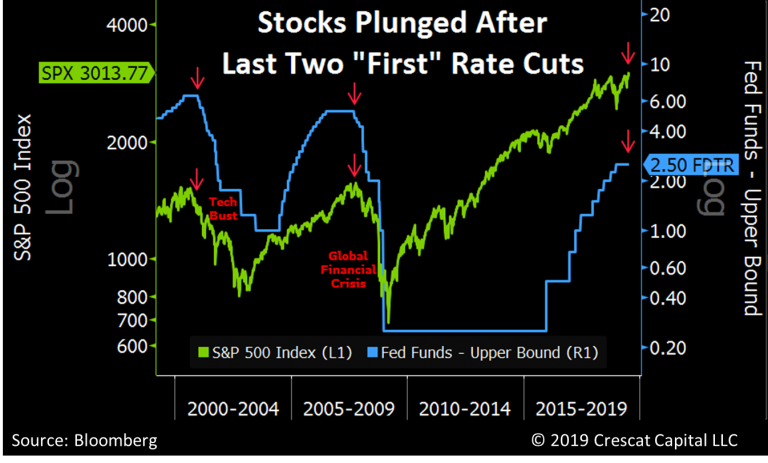

The markets currently believe that when the Fed cuts rates this week, the bull market will continue higher. Crescat, and history, suggest a different outcome.

As I stated above, my job, like every portfolio manager, is to participate when markets are rising. However, it is also my job to keep a measured approach to capital preservation.

Yes, I am bearish on the longer-term outlook of the markets for the reasons, and many more, stated above.

Just make sure you understand that I am an “almost fully invested bear.”

At least for now.

But that can, and will, rapidly change as the indicators I follow dictate.

What’s your strategy?

via ZeroHedge News https://ift.tt/2GEonPQ Tyler Durden

The U.S. Court of Appeals for the District of Columbia Circuit has ordered the Drug Enforcement Agency (DEA) to explain why it has yet to respond to nearly two dozen researchers around the U.S. who applied three years ago for a DEA license to grow research cannabis.

“Hopefully, DEA will finally explain, in a court-filing available for public inspection, the answer to this question that has frustrated everyone,” announced Sue Sisley, a physician and researcher at the Scottsdale Research Institute, a Phoenix-based clinical trial company that applied in 2016 for a DEA manufacturing license in order to grow its own cannabis for an ongoing study of medical marijuana as a treatment for veterans suffering from PTSD.

The Scottsdale Research Institute (SRI) sued the Justice Department and the DEA in June. It sought a “writ of mandamus” that would compel the DEA to respond to applicants seeking a license. SRI argued that the Improving Regulatory Transparency for New Medical Therapies Act, signed by President Obama in November 2015, requires “that the Attorney General, upon receiving an application to manufacture a Schedule I substance for use only in a clinical trial, publish a notice of application not later than 90 days after accepting the application for filing.” SRI and more than 20 other potential cannabis manufacturers applied for licenses from the DEA in 2016, but a notice of their applications has yet to appear in the Federal Register.

“Thus,” RSI’s suit argued, “agency action has been unlawfully withheld. And in view of an express directive to prioritize applications relating to clinical research, agency action has most certainly been unreasonably delayed.”

Despite congressional appeals to the DEA to complete the application review process, the applicants I’ve spoken to say they’ve received no substantive updates from the agency in over a year, and no applicant I spoke with has been contacted by their local DEA field office to schedule an inspection of their facilities, a crucial early step in the review process.

Sisley’s lawsuit and the court’s order are particularly newsworthy due to the lack of domestically grown cannabis suitable for research with human subjects. The University of Mississippi has the only DEA license for cannabis manufacturing in the U.S. and operates a 12-acre outdoor growing facility under a contract with the National Institutes for Drug Abuse, which is housed within the Department of Health and Human Services. Despite DEA claims to the contrary, researchers say that Mississippi’s cannabis is inadequate for testing in human subjects.

The Mississippi cannabis made available to Sisley and her team “arrived in powdered form, tainted with extraneous material like sticks and seeds, and many samples were moldy,” SRI’s lawsuit claimed. “Whatever reasons the government may have for sanctioning this cannabis and no other, considerations of quality are not among them. It is not suited for any clinical trials, let alone the ones SRI is doing.” What’s more, federal regulations prohibit the use of Mississippi’s cannabis in phase III clinical trials and thus make it practically impossible to develop pharmaceutical products using domestically grown cannabis.

Since August 11, 2016, when the DEA published an announcement in the Federal Register inviting applications for bulk cannabis manufacturers, Republican and Democratic members of both the House of Representatives and the Senate have sent multiple queries to the Justice Department requesting an update on the status of some two dozen applications.

In several appearances before Congress, then-Attorney General Jeff Sessions insisted that the Justice Department was limited by the United Nations Single Convention on Narcotic Drugs. However, many researchers in the U.S. legally import research cannabis from fellow convention signatories Israel and Canada, and the Food and Drug Administration last year approved Epidiolex, a drug developed using cannabis grown in the United Kingdom, another signatory of the narcotics treaty. In addition, the DEA regularly approves applications for the domestic manufacturing of other schedule I drugs, including synthetic cannabis.

The D.C. Circuit has instructed the DEA to respond to SRI’s suit by August 28, 2019. The lawsuit is available here.

from Latest – Reason.com https://ift.tt/2KcJppX

via IFTTT

The U.S. Court of Appeals for the District of Columbia Circuit has ordered the Drug Enforcement Agency (DEA) to explain why it has yet to respond to nearly two dozen researchers around the U.S. who applied three years ago for a DEA license to grow research cannabis.

“Hopefully, DEA will finally explain, in a court-filing available for public inspection, the answer to this question that has frustrated everyone,” announced Sue Sisley, a physician and researcher at the Scottsdale Research Institute, a Phoenix-based clinical trial company that applied in 2016 for a DEA manufacturing license in order to grow its own cannabis for an ongoing study of medical marijuana as a treatment for veterans suffering from PTSD.

The Scottsdale Research Institute (SRI) sued the Justice Department and the DEA in June. It sought a “writ of mandamus” that would compel the DEA to respond to applicants seeking a license. SRI argued that the Improving Regulatory Transparency for New Medical Therapies Act, signed by President Obama in November 2015, requires “that the Attorney General, upon receiving an application to manufacture a Schedule I substance for use only in a clinical trial, publish a notice of application not later than 90 days after accepting the application for filing.” SRI and more than 20 other potential cannabis manufacturers applied for licenses from the DEA in 2016, but a notice of their applications has yet to appear in the Federal Register.

“Thus,” RSI’s suit argued, “agency action has been unlawfully withheld. And in view of an express directive to prioritize applications relating to clinical research, agency action has most certainly been unreasonably delayed.”

Despite congressional appeals to the DEA to complete the application review process, the applicants I’ve spoken to say they’ve received no substantive updates from the agency in over a year, and no applicant I spoke with has been contacted by their local DEA field office to schedule an inspection of their facilities, a crucial early step in the review process.

Sisley’s lawsuit and the court’s order are particularly newsworthy due to the lack of domestically grown cannabis suitable for research with human subjects. The University of Mississippi has the only DEA license for cannabis manufacturing in the U.S. and operates a 12-acre outdoor growing facility under a contract with the National Institutes for Drug Abuse, which is housed within the Department of Health and Human Services. Despite DEA claims to the contrary, researchers say that Mississippi’s cannabis is inadequate for testing in human subjects.

The Mississippi cannabis made available to Sisley and her team “arrived in powdered form, tainted with extraneous material like sticks and seeds, and many samples were moldy,” SRI’s lawsuit claimed. “Whatever reasons the government may have for sanctioning this cannabis and no other, considerations of quality are not among them. It is not suited for any clinical trials, let alone the ones SRI is doing.” What’s more, federal regulations prohibit the use of Mississippi’s cannabis in phase III clinical trials and thus make it practically impossible to develop pharmaceutical products using domestically grown cannabis.

Since August 11, 2016, when the DEA published an announcement in the Federal Register inviting applications for bulk cannabis manufacturers, Republican and Democratic members of both the House of Representatives and the Senate have sent multiple queries to the Justice Department requesting an update on the status of some two dozen applications.

In several appearances before Congress, then-Attorney General Jeff Sessions insisted that the Justice Department was limited by the United Nations Single Convention on Narcotic Drugs. However, many researchers in the U.S. legally import research cannabis from fellow convention signatories Israel and Canada, and the Food and Drug Administration last year approved Epidiolex, a drug developed using cannabis grown in the United Kingdom, another signatory of the narcotics treaty. In addition, the DEA regularly approves applications for the domestic manufacturing of other schedule I drugs, including synthetic cannabis.

The D.C. Circuit has instructed the DEA to respond to SRI’s suit by August 28, 2019. The lawsuit is available here.

from Latest – Reason.com https://ift.tt/2KcJppX

via IFTTT

For a company that has already racked up a tab of over $1 billion in losses this year, what’s another $323 million amongst friends?

This was quite possibly the attitude the company took when agreeing to pay China 2.23 billion yuan – about $323 million – in taxes every single year as part of their deal with local authorities to build their factory on the outside of Shanghai, according to Bloomberg.

Tesla has also committed to drop about 14.08 billion yuan – or about $2 billion – in capex on the plant over the next five years, according to its lease. While the point of the Shanghai Gigafactory was to avoid tariffs and keep prices down, we’re not sure how an annual tax requirement of well over a quarter of a billion dollars is going to make things easier for Musk.

But, not unlike many of Musk’s other projects, we’re sure the motive was to get the factory set up for optics as quickly as humanly possible and (literally) at any cost so Tesla has something flashy to show the investment community; it would only worry about the expense side of the ledger much later.

Tesla will likely argue that the requirements are tame compared to their targets in China, where it aims to produce half a million cars at the site over the next 12 months, depending on how quickly output ramps up.

Tesla said in its 10-Q: “We believe the capital expenditure requirement and the tax revenue target will be attainable even if our actual vehicle production was far lower than the volumes we are forecasting.”

OK. We’ll hold you to that.

via ZeroHedge News https://ift.tt/2Kc1Wm8 Tyler Durden

A new round of attacks on our right to secure, hard-to-crack encryption has kicked off.

In separate speeches this month, Attorney General William Barr and FBI Director Christopher Wray each insisted that they understand encryption is a necessary tool—particularly as more and more information about us is digitized—to protect our personal data from anybody with ill intent. But both nevertheless believe that apps and tech platforms need to develop tools that let government officials bypass encryption to comply with warrants. Neither seems willing to accept the reality that a back door that lets the FBI in would by its very nature weaken encryption, making it subject to attacks by the very same predators we need to be protected from.

In an address at the International Conference on Cyber Security on July 23, Barr opined [emphasis added]:

At conferences like this, we talk about those costs in abstract terms. They are not abstract; they are real. The costs of irresponsible encryption that blocks legitimate law enforcement access is ultimately measured in a mounting number of victims—men, women, and children who are the victims of crimes—crimes that could have been prevented if law enforcement had been given lawful access to encrypted evidence.

Throughout the speech, Barr refers to “warrant-proof encryption” rather “end-to-end encryption” (which appears all of once in the whole speech) or “quantum cryptography” (which doesn’t appear at all). These are types of encryption designed to make it extremely difficult, if not impossible, for third parties or unintended recipients to access the information. This is an increasingly necessary tool for protecting our data privacy that also has a secondary effect of making it hard for law enforcement to access our private data and communications even with warrants.

This type of encryption also, incidentally, makes it hard for the governments of countries like Saudi Arabia, Iran, Russia, and China and others to access our private data. So it’s absurd but telling for Barr to dismiss it as “irresponsible” simply because his agencies can’t gain access. The costs of having your data accessed and copied by foreign governments are not abstract either.

Similarly, Wray gave a speech July 25 at the FBI International Cyber Security in which he insisted that he understands how important data security is, but also declared that government access to encrypted data is equally important:

I don’t want to think about a world in which we lose the ability to detect dangerous criminal activity because a technology provider decides to encrypt this traffic—data “in motion”—in such a way that the content is cloaked and no longer subject to our longstanding legal process. Our ability to do our jobs—law enforcement’s ability to protect the American people—will be degraded in a major way.

Later, he complains: “I get a little frustrated when people suggest that we’re trying to weaken encryption—or weaken cybersecurity more broadly. We’re doing no such thing.” There’s a reason that nearly everybody in the private sector tech security establishment is making that suggestion: because what Wray and Barr want cannot happen without weakening encryption. There is no such thing as a door that only the “good guys” (for whatever definition of good guys you choose) can enter.

Back in 2016, some hackers attempted to show the FBI exactly what would happen with encryption “back doors.” Microsoft had an encryption key to bypass part of its authentication process for its operating system. Developers used it to test new operating builds. The hackers managed to get their hands on this encryption key and publicized how it worked. Their intent was to show the FBI that anything that would allow law enforcement to bypass encryption would ultimately get into the “wild” somehow and that people with malicious plans, be they criminals or foreign governments, would also kick that door wide open. They begged the FBI to pay attention to their example.

Apparently, the FBI is still refusing to listen. We may end up trying to following Australia’s footsteps and making the world a more dangerous place for law-abiding citizens while clever criminals and predatory foreign governments both take advantage of these back doors and use a constantly shifting array of lesser-known, disposable encrypted communication apps that the feds will not be able to stay on top of. We’ll end up in the worst of all worlds.

from Latest – Reason.com https://ift.tt/2Msnv4C

via IFTTT

A new round of attacks on our right to secure, hard-to-crack encryption has kicked off.

In separate speeches this month, Attorney General William Barr and FBI Director Christopher Wray each insisted that they understand encryption is a necessary tool—particularly as more and more information about us is digitized—to protect our personal data from anybody with ill intent. But both nevertheless believe that apps and tech platforms need to develop tools that let government officials bypass encryption to comply with warrants. Neither seems willing to accept the reality that a back door that lets the FBI in would by its very nature weaken encryption, making it subject to attacks by the very same predators we need to be protected from.

In an address at the International Conference on Cyber Security on July 23, Barr opined [emphasis added]:

At conferences like this, we talk about those costs in abstract terms. They are not abstract; they are real. The costs of irresponsible encryption that blocks legitimate law enforcement access is ultimately measured in a mounting number of victims—men, women, and children who are the victims of crimes—crimes that could have been prevented if law enforcement had been given lawful access to encrypted evidence.

Throughout the speech, Barr refers to “warrant-proof encryption” rather “end-to-end encryption” (which appears all of once in the whole speech) or “quantum cryptography” (which doesn’t appear at all). These are types of encryption designed to make it extremely difficult, if not impossible, for third parties or unintended recipients to access the information. This is an increasingly necessary tool for protecting our data privacy that also has a secondary effect of making it hard for law enforcement to access our private data and communications even with warrants.

This type of encryption also, incidentally, makes it hard for the governments of countries like Saudi Arabia, Iran, Russia, and China and others to access our private data. So it’s absurd but telling for Barr to dismiss it as “irresponsible” simply because his agencies can’t gain access. The costs of having your data accessed and copied by foreign governments are not abstract either.

Similarly, Wray gave a speech July 25 at the FBI International Cyber Security in which he insisted that he understands how important data security is, but also declared that government access to encrypted data is equally important:

I don’t want to think about a world in which we lose the ability to detect dangerous criminal activity because a technology provider decides to encrypt this traffic—data “in motion”—in such a way that the content is cloaked and no longer subject to our longstanding legal process. Our ability to do our jobs—law enforcement’s ability to protect the American people—will be degraded in a major way.

Later, he complains: “I get a little frustrated when people suggest that we’re trying to weaken encryption—or weaken cybersecurity more broadly. We’re doing no such thing.” There’s a reason that nearly everybody in the private sector tech security establishment is making that suggestion: because what Wray and Barr want cannot happen without weakening encryption. There is no such thing as a door that only the “good guys” (for whatever definition of good guys you choose) can enter.

Back in 2016, some hackers attempted to show the FBI exactly what would happen with encryption “back doors.” Microsoft had an encryption key to bypass part of its authentication process for its operating system. Developers used it to test new operating builds. The hackers managed to get their hands on this encryption key and publicized how it worked. Their intent was to show the FBI that anything that would allow law enforcement to bypass encryption would ultimately get into the “wild” somehow and that people with malicious plans, be they criminals or foreign governments, would also kick that door wide open. They begged the FBI to pay attention to their example.

Apparently, the FBI is still refusing to listen. We may end up trying to following Australia’s footsteps and making the world a more dangerous place for law-abiding citizens while clever criminals and predatory foreign governments both take advantage of these back doors and use a constantly shifting array of lesser-known, disposable encrypted communication apps that the feds will not be able to stay on top of. We’ll end up in the worst of all worlds.

from Latest – Reason.com https://ift.tt/2Msnv4C

via IFTTT

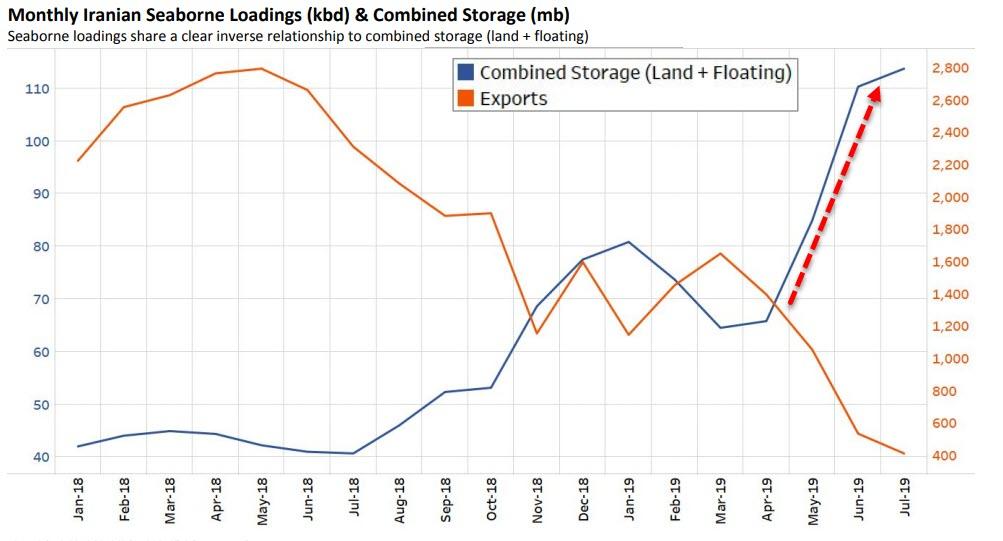

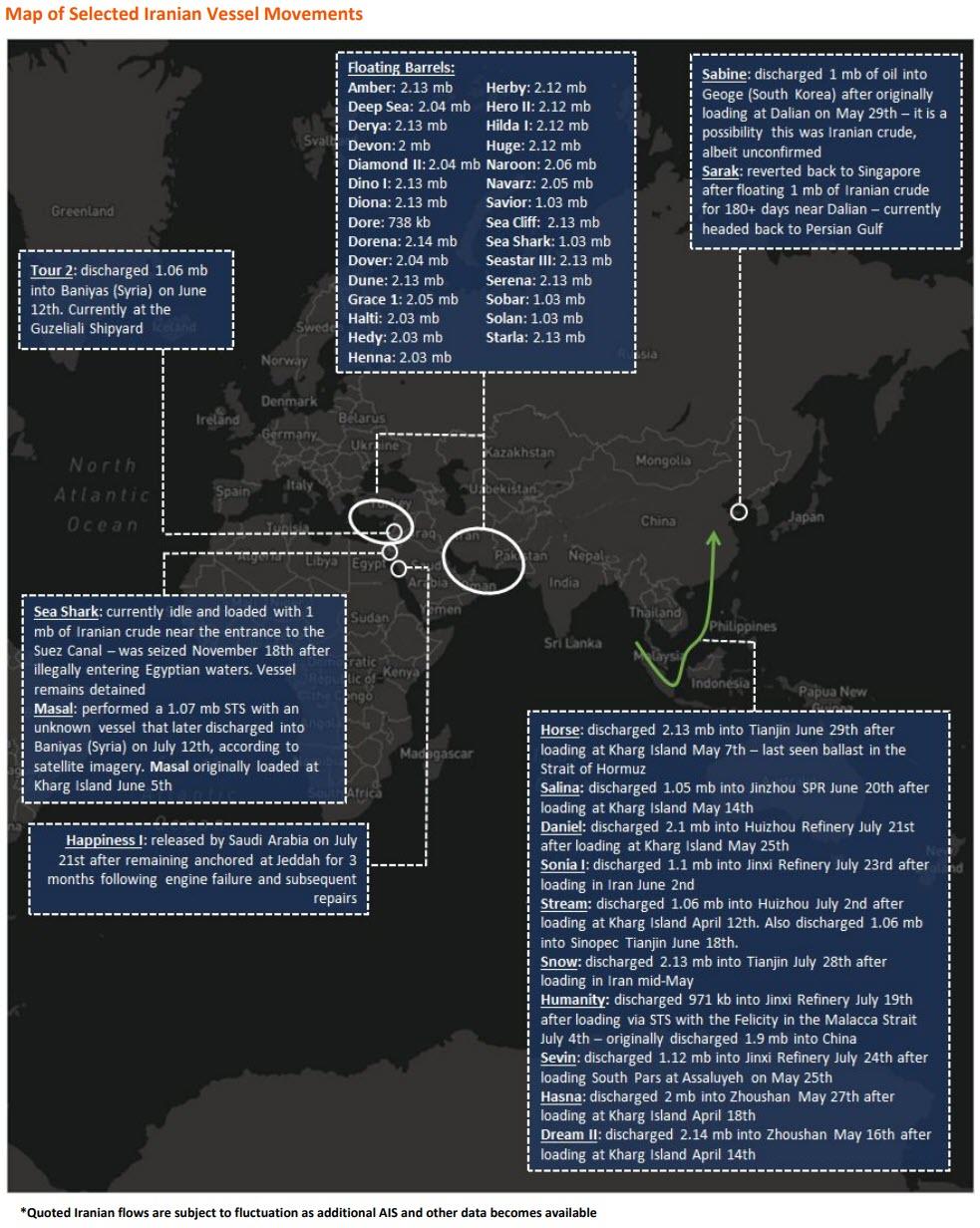

Crude oil in floating and onshore storage in Iran has exceeded 110 million barrels, French energy data analysts Kpler reported this week, noting the number of barrels in floating storage specifically had increased almost twofold over the last two months.

Oil in floating storage reached 56 million barrels, Kpler said, as exports continued to slide, falling to 417,000 bpd in July from 532,000 bpd in June. Oil in onshore storage stood at 55.5 million barrels at the start of this week. This is up by 11 million barrels since the middle of May, shortly before the expiration of the sanction waivers. Onshore inventories will likely continue to rise steadily as floating storage is running near capacity.

Meanwhile, Iranian oil is also pushing Chinese stockpiles higher. From 3.2 million barrels in mid-June, China’s strategic petroleum reserve in the northeastern province of Liaoning has reached 6 million barrels to date.

China has become Iran’s most important oil buyer following the removal of U.S. sanction waivers in May, Kpler also noted. In June, Iran exported oil and condensate to China at a rate of 174,000 bpd, of which two-thirds was loaded after the expiration of the sanction waivers. This month, shipments increased considerably to more than 360,000 bpd.

Turkey is also importing Iranian crude at a growing rate despite the risk of sanction violation action on the part of Washington and shipments to Syria are probably continuing although there is no full visibility on these, Kpler says, as Iranian tankers turn off their geolocation devices in the Mediterranean.

So, there’s more than 110 million barrels of crude in storage, ready to flow and push prices lower. Since the chance of the United States suddenly reconsidering its stance on Iran is non-existent, this amount will only continue to rise. The possibility of it turning into a ticking bomb for international prices at some point in the future may be negligible now, but does not have to stay negligible forever.

via ZeroHedge News https://ift.tt/2STr2Ky Tyler Durden

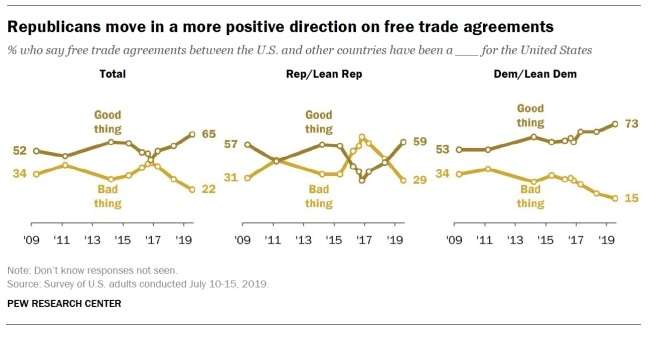

So it’s little surprise that Americans are increasingly unhappy with Trump’s anti-trade stance. What is surprising, perhaps, is that the Democrats vying to challenge Trump in next year’s presidential election seem mostly unwilling to take advantage of one of the incumbent’s most obvious weaknesses.

New polling data released Tuesday by the Pew Research Center shows that 56 percent of Americans now say the tariffs are “bad for the country.” That’s up from 53 percent in September of last year.

Even more interesting is that the number of Americans who say that signing free trade agreements is a good thing has increased to 65 percent—with majorities of both Democrats (73 percent) and Republicans (59 percent) favoring such deals. Among Democrats, that figure is the highest since Pew started asking about trade in 2009. Republicans’ views on free trade, meanwhile, have recovered to pre-2016 levels.

Other recent polls show similar results. A New York Times/Survey Monkey poll released earlier this month showed that 68 percent of respondents—including a majority of Republicans—said Trump’s trade policies will raise prices, while 53 percent said Trump’s Chinese tariffs will be “bad” for the United States.

Despite clear majorities that oppose Trump’s protectionism and favor more trade with more nations, both major parties seem to be moving in the opposite direction. There’s little hope that the GOP will rediscover the value of free trade as long as protectionist-in-chief Trump and his coterie of economic nationalists occupy the White House. Which gives the Democrats a clear opportunity to seize the high ground on trade.

Some of the 2020 candidates are tentatively trying to do so. The strongest rebukes of Trump’s trade policies, so far, have come from former vice president Joe Biden and from Pete Buttigieg, the mayor of South Bend, Indiana.

“Trump doesn’t get the basics,” Biden said during a speech in Iowa last month. “He thinks the tariffs are being paid by China. Any beginning econ student at Iowa or Iowa State could tell you the American people are paying his tariffs.” Trump thinks he’s being tough, Biden added, but that’s only because he’s forcing American farmers and manufacturers to “feel the pain.” Buttigieg has promised to lift Trump’s tariffs if elected, calling them a “counterproductive” policy unlikely to change China’s behavior while unnecessarily hurting Americans.

Generally speaking, however, the Democrats running for president have criticized Trump’s handling of the trade war and his use of tariffs, while tacitly acknowledging that they believe the problem is Trump, and not the policies themselves.

For example, Sen. Kamala Harris (D–Calif.) told CNN’s Jake Tapper in May that Trump’s habit of “conducting trade policy, economic policy, foreign policy by tweet” was “irresponsible.” But when pressed by Tapper she admitted that she largely agreed with Trump’s assessment that free trade is a scourge on American workers. This week, Sen. Elizabeth Warren (D–Mass.) unveiled a new trade policy paper that similarly criticized the style, but not the substance, of Trump’s tariffs. “While I think tariffs are an important tool, they are not by themselves a long-term solution to our failed trade agenda and must be part of a broader strategy that this Administration clearly lacks,” Warren wrote, clearly indicating that she would not rule out the use of tariffs if elected.

The subject of trade was raised only once by the moderators at last month’s Democratic presidential debates. “We need to crack down on Chinese malfeasance in the trade relationship, but the tariffs and the trade war are the wrong way to go,” offered Andrew Yang. “I think the president has been right to push back on China, but has done it in completely the wrong way,” said Sen. Michael Bennet (D–Colo.). “Tariffs are taxes,” Buttigieg said, before criticizing Trump for being “fixated on the China relationship as if all that mattered was the export balance on dishwashers.”

That was basically the extent of the discussion.

Will anything change this week? Partially, that will depend on the questions being asked. The first debate appeared intentionally structured to sideline the incumbent as much as possible, giving the 20-member Democratic field an opportunity to clash with one another, rather than simply teaming-up to attack Trump.

Breaking into the open on an issue like trade will also require some courage from the candidates. Even before Trump came along, Democrats had turned away from the bipartisan consensus that had helped usher in the North American Free Trade Agreement in the 1990s and that stood up to President George W. Bush in the 2000s when he flirted with steel protectionism. By the end of the Barack Obama administration, however, many Democrats (including Warren) were opposing a Democratic administration’s attempt to negotiate the Trans-Pacific Partnership, a multilateral trade deal meant as a bulwark against China.

What candidate might be willing to break with the party this week? Despite his previous comments, it probably won’t be Biden. As the clear frontrunner in a crowded field, the former Veep has little to gain from putting a target on his back. He is likely to keep playing it safe until after the primaries. Instead, look for a candidate like former congressman Beto O’Rourke to make the pro-trade play. O’Rourke is sinking in the polls and probably seeking a breakout moment—and since trade with Mexico is so critical for the Texas economy, it would make sense for the Texas candidate to embrace the issue.

If they are not going to follow the polls, the Democratic candidates should at least be willing to follow the economic data showing that voters are right to favor trade agreements. A 2017 analysis by the Peterson Institute for International Economics, a trade policy think tank, shows that international trade boosted American household incomes by about $18,000 per household since 1950—and that the gains flowed disproportionately to lower-income households. The Commerce Department says that more than 11 million American jobs are directly related to foreign investment or the export of American goods. And the mere existence of NAFTA boosts the U.S. economy by about 0.5 percent per year. There is no doubt that the past half-century of increasingly freer trade has made America better off.

Polls show that a majority of voters recognize the many benefits of trade. But in a campaign in which Democrats seem determined to outdo one another with offers of “free” healthcare and “free” college tuition, free trade may get ignored.

from Latest – Reason.com https://ift.tt/2OvZgVU

via IFTTT

So it’s little surprise that Americans are increasingly unhappy with Trump’s anti-trade stance. What is surprising, perhaps, is that the Democrats vying to challenge Trump in next year’s presidential election seem mostly unwilling to take advantage of one of the incumbent’s most obvious weaknesses.

New polling data released Tuesday by the Pew Research Center shows that 56 percent of Americans now say the tariffs are “bad for the country.” That’s up from 53 percent in September of last year.

Even more interesting is that the number of Americans who say that signing free trade agreements is a good thing has increased to 65 percent—with majorities of both Democrats (73 percent) and Republicans (59 percent) favoring such deals. Among Democrats, that figure is the highest since Pew started asking about trade in 2009. Republicans’ views on free trade, meanwhile, have recovered to pre-2016 levels.

Other recent polls show similar results. A New York Times/Survey Monkey poll released earlier this month showed that 68 percent of respondents—including a majority of Republicans—said Trump’s trade policies will raise prices, while 53 percent said Trump’s Chinese tariffs will be “bad” for the United States.

Despite clear majorities that oppose Trump’s protectionism and favor more trade with more nations, both major parties seem to be moving in the opposite direction. There’s little hope that the GOP will rediscover the value of free trade as long as protectionist-in-chief Trump and his coterie of economic nationalists occupy the White House. Which gives the Democrats a clear opportunity to seize the high ground on trade.

Some of the 2020 candidates are tentatively trying to do so. The strongest rebukes of Trump’s trade policies, so far, have come from former vice president Joe Biden and from Pete Buttigieg, the mayor of South Bend, Indiana.

“Trump doesn’t get the basics,” Biden said during a speech in Iowa last month. “He thinks the tariffs are being paid by China. Any beginning econ student at Iowa or Iowa State could tell you the American people are paying his tariffs.” Trump thinks he’s being tough, Biden added, but that’s only because he’s forcing American farmers and manufacturers to “feel the pain.” Buttigieg has promised to lift Trump’s tariffs if elected, calling them a “counterproductive” policy unlikely to change China’s behavior while unnecessarily hurting Americans.

Generally speaking, however, the Democrats running for president have criticized Trump’s handling of the trade war and his use of tariffs, while tacitly acknowledging that they believe the problem is Trump, and not the policies themselves.

For example, Sen. Kamala Harris (D–Calif.) told CNN’s Jake Tapper in May that Trump’s habit of “conducting trade policy, economic policy, foreign policy by tweet” was “irresponsible.” But when pressed by Tapper she admitted that she largely agreed with Trump’s assessment that free trade is a scourge on American workers. This week, Sen. Elizabeth Warren (D–Mass.) unveiled a new trade policy paper that similarly criticized the style, but not the substance, of Trump’s tariffs. “While I think tariffs are an important tool, they are not by themselves a long-term solution to our failed trade agenda and must be part of a broader strategy that this Administration clearly lacks,” Warren wrote, clearly indicating that she would not rule out the use of tariffs if elected.

The subject of trade was raised only once by the moderators at last month’s Democratic presidential debates. “We need to crack down on Chinese malfeasance in the trade relationship, but the tariffs and the trade war are the wrong way to go,” offered Andrew Yang. “I think the president has been right to push back on China, but has done it in completely the wrong way,” said Sen. Michael Bennet (D–Colo.). “Tariffs are taxes,” Buttigieg said, before criticizing Trump for being “fixated on the China relationship as if all that mattered was the export balance on dishwashers.”

That was basically the extent of the discussion.

Will anything change this week? Partially, that will depend on the questions being asked. The first debate appeared intentionally structured to sideline the incumbent as much as possible, giving the 20-member Democratic field an opportunity to clash with one another, rather than simply teaming-up to attack Trump.

Breaking into the open on an issue like trade will also require some courage from the candidates. Even before Trump came along, Democrats had turned away from the bipartisan consensus that had helped usher in the North American Free Trade Agreement in the 1990s and that stood up to President George W. Bush in the 2000s when he flirted with steel protectionism. By the end of the Barack Obama administration, however, many Democrats (including Warren) were opposing a Democratic administration’s attempt to negotiate the Trans-Pacific Partnership, a multilateral trade deal meant as a bulwark against China.

What candidate might be willing to break with the party this week? Despite his previous comments, it probably won’t be Biden. As the clear frontrunner in a crowded field, the former Veep has little to gain from putting a target on his back. He is likely to keep playing it safe until after the primaries. Instead, look for a candidate like former congressman Beto O’Rourke to make the pro-trade play. O’Rourke is sinking in the polls and probably seeking a breakout moment—and since trade with Mexico is so critical for the Texas economy, it would make sense for the Texas candidate to embrace the issue.

If they are not going to follow the polls, the Democratic candidates should at least be willing to follow the economic data showing that voters are right to favor trade agreements. A 2017 analysis by the Peterson Institute for International Economics, a trade policy think tank, shows that international trade boosted American household incomes by about $18,000 per household since 1950—and that the gains flowed disproportionately to lower-income households. The Commerce Department says that more than 11 million American jobs are directly related to foreign investment or the export of American goods. And the mere existence of NAFTA boosts the U.S. economy by about 0.5 percent per year. There is no doubt that the past half-century of increasingly freer trade has made America better off.

Polls show that a majority of voters recognize the many benefits of trade. But in a campaign in which Democrats seem determined to outdo one another with offers of “free” healthcare and “free” college tuition, free trade may get ignored.

from Latest – Reason.com https://ift.tt/2OvZgVU

via IFTTT