“He Needs Cash”: Ron Perelman’s Leveraged Empire Collapses In A Deluge Of Fire Sales Tyler Durden

Sun, 09/20/2020 – 20:25

For billionaire Ronald O. Perelman, the time to cash in his chips is now. And, of course, by “cash in his chips”, we mean liquidate everything in a panic after Covid sends your highly leveraged empire into ruins.

In what will likely wind up as a microcosm of the United States economy as a whole, Perelman is currently in the process of selling his Gulfstream 650, his 257 foot yacht and “crates” of his artwork, according to Bloomberg. According to the report, he has already sold his stake in AM General, sold a flavorings company he has owned for decades and has hired banks to sell stock he owns in other companies.

Among the art he is selling is Jasper Johns’s “0 Through 9,” worth about $70 million, Gerhard Richter’s “Zwei Kerzen (Two Candles),” worth about $50 million and Cy Twombly’s “Leaving Paphos Ringed with Waves,” which is worth about $20 million.

Art adviser Wendy Goldsmith said: “What he’s selling is as blue chip as it gets.”

Perelman, under pressure due to his crashing stake in Revlon, has seen his fortune drop from $19 billion to just $4.2 billion over the last two years, according to the Bloomberg Billionaire’s Index. His investment company, MacAndrews & Forbes, said it needed to “rework its holdings” back in July due to the pandemic.

That “reworking” looks more like a fire sale of – well – everything.

Perelman said publicly: “We quickly took significant steps to react to the unprecedented economic environment that we were facing. I have been very public about my intention to reduce leverage, streamline operations, sell some assets and convert those assets to cash in order to seek new investment opportunities and that is exactly what we are doing.”

He continued: “I realized that for far too long, I have been holding onto too many things that I don’t use or even want. I concluded that it’s time for me to clean house, simplify and give others the chance to enjoy some of the beautiful things that I’ve acquired just as I have for decades.”

A friend of Perelman’s, Graydon Carter, told Bloomberg: “Often when people say this sort of thing, it’s masking something else. In Ronald’s case, it’s true. He has learned to love and appreciate the bourgeois comforts of family and home.” He described Perelman as “crazy about spending time at home”.

Some of his sales will go to pay down loans from Citigroup, though Perelman’s spokesman says they are not “forced sales”. She also denied Perelman is selling his 57 acre estate in the Hamptons.

Perelman is best known being a fearless financial engineer in the 1980’s and 1990’s. Ken Moelis said of Perelman’s track record: “He was imaginative, aggressive and innovative in ways that changed the financial landscape.”

But the $1.74 billion valuation Revlon had back in the 1980’s when he purchased it has now fallen to just $365 million. Perelman loved the business and said it “defined him”. He had offered it several loans and had catalyzed several executive changes to try and keep the business afloat. Revlon is now losing to smaller cosmetic shops that advertise through social media – while dealing with the effects of Covid.

Some Revlon bonds trade at 14 cents on the dollar and the company has $3 billion in debt.

He used some of his massive stake in Revlon as collateral for debt in MacAndrews & Forbes. Revlon shares are down 68% this year, likely triggering the deluge of selling Perelman is doing.

All told, “at least nine banks” have claims against his assets, including his art collection, house in the Hamptons and “various aircraft”. There are $267 million in mortgages linked to his Upper East Side headquarters for MacAndrews & Forbes.

Currently, Perelman’s art collection makes up about a third of his fortune. And that can be tricky, for assets that have an illiquid market. Recently, one painting he tried to sell was pulled from auction at the last minute due to lack of interest.

MacAndrews & Forbes saw its general counsel, spokesman, head of capital markets and CFO all depart over the last few months.

And despite the spin on Perelman’s fire sales as being a way to spend more time with family, Perelman has his skeptics, including Richard Hack, who wrote a book about him in 1996.

Hack concluded: “If you want a simpler life, you go buy a farm in Oklahoma, not sell a painting out of your townhouse in Manhattan. If he’s selling his art, it’s because he needs cash.”

via ZeroHedge News https://ift.tt/3kxDo7I Tyler Durden

Fires, blackouts, high taxes, poverty, scarce housing, urban squalor, lousy schools – it’s a wonder anybody stays.

“California, folks, is America fast forward.” Thus Governor Gavin Newsom, hoarsely, amid brown smoke at the North Complex Fire on Sept. 11.

“What we’re experiencing right here is coming to a community all across the United States of America… unless we get our act together on climate change.”

I was with him all the way until he said the words “on climate change.”

As my Hoover Institution colleague Victor Davis Hanson put it last month, California is “the progressive model of the future: a once-innovative, rich state that is now a civilization in near ruins. The nation should watch us this election year and learn of its possible future.”

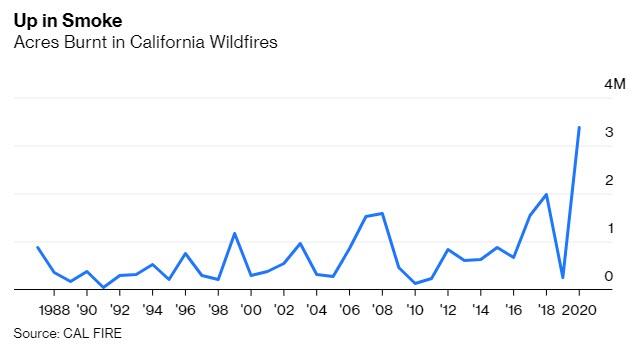

Let’s start with the fires. So far this year, they have torched more than five times as much land as the average of the previous 33 years, killing 25 people and forcing about 100,000 people from their homes. At one point, three of the largest fires in the state’s history were burning simultaneously in a ring around the San Francisco Bay Area. According to the California Department of Forestry and Fire Protection, or CAL FIRE, of the 10 largest fires since 1970, five broke out this year. Nine out of 10 have occurred since 2012.

No doubt high temperatures and unusual thunderstorms bear some of the responsibility for this year’s terrifying wildfires on the West Coast. It is deeply misleading to claim, as some diehard deniers still do, that temperatures aren’t rising and making wildfires more likely. But it is equally misleading to claim, as the New York Times did last week, that “scientists say” climate change “is the primary cause of the conflagration.”

In reality, as Stanford’s Rebecca Miller, Christopher Field and Katharine J. Mach argue in a recent article in Nature Sustainability, this crisis has at least as much to do with disastrous land mismanagement as with climate change, and perhaps more. Anyone who thinks solar panels, Teslas and a $3.3 billion white elephant of a high-speed rail line will avoid comparable or worse fires next year (and the year after and the year after) doesn’t understand what the scientists are really saying.

Most measures proposed by environmentalists to reduce carbon dioxide and other “greenhouse gas” emissions will pay off over 50 to 100 years, as the International Panel on Climate Change has long made clear. Even a best-case scenario of “stringent mitigation” (what the IPCC calls Representative Concentration Pathway 2.6) would not bring carbon dioxide emissions down to 1950 levels until around 2050. Nor would it lower global average temperatures; it would merely stop them rising.

And that’s only if the whole world — including China and India — takes action. California’s wildfire problem cannot be solved by the state’s citizens “getting their act together on climate change,” in Newsom’s words. The problem needs immediately effective action — and that means a return to sane forest management, if such a return is still possible. For decades, Democratic leaders in California have presided over a policy of leaving dead trees to rot, instead of the old and rational system of prescribed or controlled burns, not least because environmental and clear air regulations, as well as problems of legal liability, made controlled burns harder and harder to do.

In prehistoric California, according to a recent analysis in ProPublica, between 4.4 million and 11.8 million acres burned each year.

California’s land managers burned about 30,000 acres a year on average between 1982 and 1998. Over the next 18 years, that number dropped to an annual 13,000 acres. The result has been a huge accumulation of highly flammable kindling.

Miller, Field and Mach concluded that a total area of around 20 million acres – roughly one-fifth of the state’s territory – was in urgent need of “fuel treatment,” meaning prescribed burns, mechanical thinning and managed wildfire. It is hard to imagine anything remotely close to that happening under the current political dispensation. (The authors politely called for “fundamental shifts in prescribed-burn policies, beyond those currently under consideration.”) Or rather, it is going to happen, but at a time of Nature’s choosing, with catastrophic consequences.

A case in point: For a year and a half, red tape slowed down a forest-thinning project in Berry Creek, Butte County. The project covered just 54 acres but, thanks to the burdensome provisions of the California Environmental Quality Act, work had yet to start when the North Complex wildfire struck, devastating the town and killing 10 people.

I have some skin in this game.

Four years ago, I moved from Harvard University to Stanford University. My family traded a solid, century-old professorial residence in Cambridge for a wooden house in a wooded area that to our wooden heads seemed most idyllic. A few weeks ago, our neighborhood was on the edge of the evacuation zone.

However, I have less skin in the game than Victor Davis Hanson. He lives on the fruit and nut farm near Selma, in the Central Valley, that his family has owned since the 1870s. The air quality index in Stanford rose above 170 on three days in the last month. In Selma last week it was 460. (Anything above 301 qualifies as “emergency conditions.”)

I write these words over 1,000 miles from our California home, but it’s no good: in recent days the smoke has found us, too. Hotel parking lots full of vehicles with CA license plates confirm that we are not the only eastward migrants. It’s like Steinbeck’s “Grapes of Wrath” in reverse: Now that the Golden State is the Char-Grilled State, Californians have become the new Okies, though a good deal less impecunious.

Yet wildfires are only one of the reasons people are fleeing California.

In addition, the wrongheaded environmental policies of the sages of Sacramento have so undermined the power grid (for example, by shutting down gas-fired power plants and refusing to count hydroelectric energy as renewable) that residents have been subjected to rolling blackouts this year. The same policies have largely killed off the oil and gas industry. Newsom & Co. have failed to upgrade the water system to keep pace with the last half-century of population growth.

It’s not that California politicians don’t know how to spend money. Back in 2007, total state spending was $146 billion. Last year it was $215 billion. I know, I know: In real terms California’s GDP increased by nearly a third in the same period. And I know: If it were an independent nation it would be the fifth-largest economy in the world, ahead of India’s. But for how much longer will that be true?

California’s taxes aren’t the highest in the country — for the median household. But the tax system is one of the most progressive, with a 13.3% top tax rate on incomes above $1 million — and that’s no longer deductible from the federal tax bill as it used to be. The top 1% of taxpayers (those earning more than $500,000) now account for half of personal income-tax revenue. And there’s worse to come.

The latest brilliant ideas in Sacramento are to raise the top income rate up to 16.8% and to levy a wealth tax (0.4% on personal fortunes over $30 million) that you couldn’t even avoid paying if you left the state.

(The proposal envisages payment for up to 10 years after departure to a lower-tax state.)

It is a strange place that seeks to repel the rich while making itself a magnet for illegal immigrants by establishing no fewer than 20 “sanctuary” cities or counties.

And the results of all this progressive policy?

A poverty boom.

California now has 12% of the nation’s population, but over 30% of its welfare recipients. By the official measure, based mainly on income and family size, California’s 11.4% poverty rate in 2019 was close to the national average over the past three years. However, according to a new Census Bureau report, which takes housing and other costs into account, the real poverty rate in California is 17.2%, the highest of any state. (Newsom gets one thing right when he says, “We’re living in the wealthiest as well as the poorest state in America.”)

About a third of California’s poverty can be attributed to housing and other living costs such as clothing and utilities. As everyone who resides there knows, there’s a chronic housing shortage in the Bay Area (the median-priced home in San Francisco costs about $1.5 million), mainly because a plethora of regulations make the construction of affordable housing well-nigh impossible. In blithe disregard of all we know about rent controls — which discourage landlords from providing housing — that is, predictably, the solution the Democrats propose.

But that’s not all. The state’s public schools rank 37th in the country overall and have the highest pupil-teacher ratio.

“Only half of California students meet English standards and fewer meet math standards, test scores show,” was a headline in the Los Angeles Times last October.

Health care and pension costs are unsustainable. Oh, and they messed up on Covid-19, despite imposing the nation’s first shelter-in-place orders. Having prematurely claimed victory, California now leads New York in terms of cases, though not deaths.

Back in the 1960s, California was the world’s fantasy destination. “California Dreamin’,” “California Girls,” “Going to California” — you know the songs. But reputations have a way of outliving reality. Despite the economic miracle wrought in Silicon Valley, beginning with the genesis of the internet back in the 1970s, and despite the continuing strength of the state’s universities, the dream in terms of quality of life has slowly died.

When I first visited San Francisco in 1981, it was still one of the loveliest cities I had ever beheld. Now its streets are so filthy – human feces and syringe needles are the principal hazards – that I avoid it. (I was going to say “like the plague,” but that’s Lake Tahoe.)

Yet the Bay Area and its southern sister Los Angeles are only one of the two Californias.

As Hanson argued 10 years ago, the Central Valley is another country, more “Caribbean” or Latin American, where “countless inland communities … have become near-apartheid societies, where Spanish is the first language, the schools are not at all diverse, and the federal and state governments are either the main employers or at least the chief sources of income.”

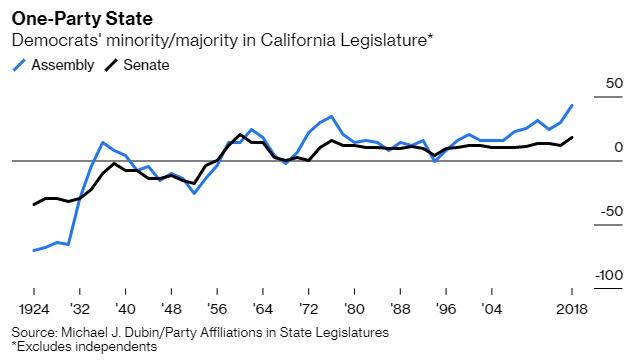

The principal reason for California’s decline is that the Golden State became a one-party state.

The Republican candidate won California in every election but one (1964) between 1952 and 1988. But the Democrat has won California in every election since, with the Democratic vote share rising from 46% in 1992 to 62% in 2016.

Democrats now have 61 out of 80 seats in the California State Assembly. The last time Republicans had a majority (of one) was in 1994, but that was an anomaly. The Democrats have essentially controlled the State Senate since 1958, with rising majorities since the 1990s. Apart from 1994, the only other year since 1958 when they did not win a majority of seats in the Assembly was 1968.

When regular voting has no effect, people eventually vote with their feet. From 2007 until 2016, about five million people moved to California but six million moved out to other states. For years before that, the newcomers were poorer than the leavers. This net exodus is surging in 2020. And businesses (for example, Charles Schwab Corp.) are leaving too. Silicon Valley is going virtual, with many big tech companies thinking of making work from home permanent for at least some employees. (One tech chief executive told me last week that his engineers were pleading not to return to the office.)

People are getting out of the Bay Area as much and perhaps more than they are getting out of New York City. Texas is only one of the favored alternatives. Realtors in Montana are reporting record demand from West Coast refugees. The hotels are full, which is unheard of at this time of year. I also know a number of eminent Californians who are now Hawaiians.

The conservative writer and broadcaster Ben Shapiro, born in L.A., just announced that he is heading to Nashville, Tennessee.

“I love the state, grew up in the state, married in the state and have had children in the state,” he told Laura Ingraham.

But California was “not a great place to raise children and not a great place to build a company.”

Now we know the true meaning of Calexit. It’s not secession. It’s exodus.

I cannot blame the leavers. When I moved West in 2016, it was in the naive belief that California was Massachusetts without snow and Stanford was Harvard with September weather all year round. How wrong I was.

But am I leaving? Well, maybe there’s no point. As Newsom’s predecessor Jerry Brown put it last week:

“There are going to be problems everywhere in the United States. This is the new normal. It’s been predicted and it’s happening … Tell me: Where are you going to go? What’s your alternative?”

Great question, but — as with Newsom’s prophecy — wrongly framed.

The big problem is not that climate change is coming to every state. It is, though most states will mitigate it better than California. The problem is that Democratic governance could be coming to the nation as a whole, starting on Jan. 20. And with the Democratic nominee, Joe Biden, turning 78 two weeks after election day, it is not a little troubling to me that his vice-presidential pick is a Californian, just as so many of his plans to spend, tax and regulate have “designed in California” all over them.

Yes, folks, California is America fast forward. Can someone please hit pause?

via ZeroHedge News https://ift.tt/2ZUL63O Tyler Durden

“Protesters” In Philadelphia Chase Down And Assault Random Citizens For Being “Nazis” Tyler Durden

Sun, 09/20/2020 – 19:35

Just when we thought we had seen peak boredom from America’s misinformed Marxists disguised as some kind of anti-fascist freedom fighters, three new videos out of Philadelphia have surfaced showing that now, more than ever, there’s too many art students and unemployed millennials that need to find hobbies.

The first video shows a group of several people chasing a man through a park.

“Holy shit you made a bad mistake,” one ‘protester’ says before another, cloaked in a hood of what appears to be a $500 REI jacket, tries to kick the man they’re chasing and then falls over.

The man then jogs in the other direction and appears to get away from his “bad mistake”, whatever it was, scot-free.

A second video out of Philadelphia shows a man that a mob reportedly chased to his car. And by “mob”, we naturally mean a group of what appears to be kids in their early 20s, replete with the full Antifa halloween costume of black hoods and masks.

“Fuck off Nazi scum,” the supposed “protesters” can be heard saying.

“Get the fuck out of here!” someone yells while other mob members kick and dent the person’s car repeatedly. When the car drives off, after being dented and damaged, someone throws a rock at its back window.

A third video shows a different angle of the assault, showing there was a dog in the back of the SUV at the time.

“F*ck you and your dog!”

Philadelphia: Antifa attacks a targeted individual, destroys his vehicle, and puts his dog’s (in the car) life in danger.

Record Numbers Of Companies Drown In Debt To Pay Dividends To Their Private Equity Owners Tyler Durden

Sun, 09/20/2020 – 19:10

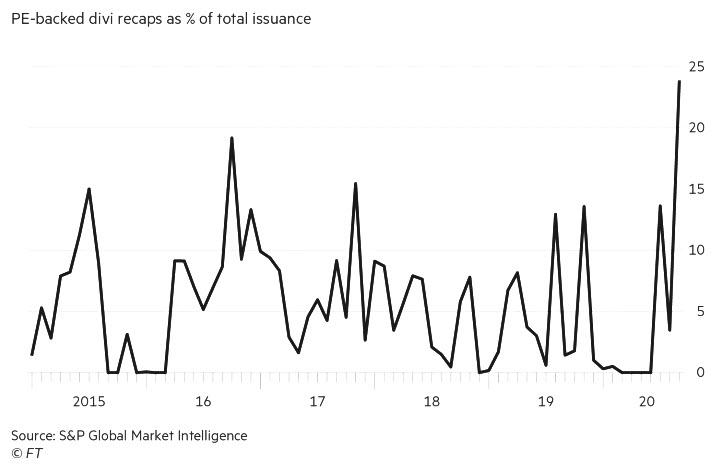

One week ago we used Bloomberg data to report that in the latest Fed-fuelled bubble to sweep the market, now with Powell buying corporate bonds and ETFs, private equity firms were instructing their junk-rated portfolio companies to get even deeper in debt and issue secured loans, using the proceeds to pay dividends to owners: the same private equity companies. Specifically, we focused on five deals marketed at the start of the month to fund shareholder dividends, which accounting for half of the week’s volume, and the most in a week since 2017, according to Bloomberg.

Now, a little over a week late, the FT is also looking at these dividend recap deals which have become all the rage in the loan market in recent weeks, among other reasons because they are “ringing alarm bells since they come on top of already high leverage and weak investor protections and against a backdrop of economic uncertainty.”

Having updated our calculation, the FT finds that in September a quarter (24% to be exact) of all new money raised in the US loan market has been used to fund dividends to private equity owners, up from an average of less than 4% over the past two years: that would be the highest proportion since the beginning of 2015, according to S&P Global Market Intelligence.

As we wrote a little over a week ago, while the loan market — where PE firms fund the companies they own by selling secured first, second, third and so on lien debt — had until recently not seen the same volume of issuance as other parts of the financial markets. That changed after the Fed stepped into the corporate bond market sending yields crashing to record lows, and forcing US investors into the last corner of the fixed income world to still offer some modest yields: leveraged loans. And since this is the domain of PE firms which desperately need to extract as much cash as they can from their melting ice cubes (another names for single-B and lower rated portfolio companies which will likely all be broke in the next 3-5 years), everyone is rushing to market with dividend recaps to pay as much to their equity sponsor as they can before the window is shut again.

According to Jessica Reiss who heads leveraged loan research at Covenant Review, investors have been accepting divi recaps because “there isn’t a ton going on” while “from the lender’s perspective they are looking for deals, so if sponsors and their companies can refinance and get a dividend up to their owners they will try it.”

In the latest example, cloud computing company ECi Software, which is owned by Apax Partners, will raise $740MM in new loans, of which $118MM will be used to pay for a dividend to its owner.

It follows a similar deal from snack foods maker Shearer’s Foods, which in turn is a portfolio company of Wind Point Partners and the Ontario Teachers’ Pension Plan, which raised over $1BN in the loan market on Tuesday and used more than a third, or $388MM, ro pay for a dividend to its owners. The news deal, which will help its PE sponsors maximize their IRR on their LBO investment, will also accelerate Shearer’s inevitable bankruptcy as its debt/EBITDA will surge from 5.1x to 6.6x. Meanwhile, at ECi, default is not a matter of if but when: leverage there is now almost 10x after the latest debt-funded check to the company’s sponsor.

Finally, broadband company Radiate Holdco was also in the market this week to fund a $500m payment to its owner TPG.

“If private equity sponsors can take money off the table then they are doing it” said John Gregory, head of leveraged finance capital markets at Wells Fargo Securities. “There’s going to be more coming for sure.”

He’s right: as long as the Fed manipulates corporate bond markets by picking winners and losers, deciding whose debt it will buy (and whose it won’t), Wall Street will find ways to maximize its profits and PE firms will make out like bandits even as their portfolio companies drown in so much debt that bankruptcies – and mass layoffs at the company level – are just a matter of time.

In total, a little over a quarter, or $4bn of the $15bn borrowed in the loan market this month, will be paid out in dividends; another $2 billion in divi recap deals are currently in the market and will price before the end of the month.

While the FT tries to mitigate the insanity, noting that “investors, bankers and analysts noted that the opportunity for private equity companies to pull cash out of the groups they control has been limited largely to higher-quality borrowers” we fail to see how a pro forma leverage of 10x is even remotely “higher-quality.”

“You have some very high leverage deals,” said Wells Fargo’s Gregory. “But if it’s a good company that people are familiar with and investors have money that they need to invest then transactions tend to go through. It’s a bull market trade for sure.”

Yes indeed, and all the billionaires currently in charge of private equity firms who are about to get even richer by milking zombies that would be long gone if it wasn’t for the Fed, thank Powell from the borrom of their heart.

However, investors express concern over loose documentation underpinning the loans, offering little protection to investors should a company end up in trouble.

Still, not everyone is acting like a 16-year-old Robinhood trader during a Softbank-fueled Tesla meltup: some are warning that this year’s market turmoil and subsequent debt-issuance euphoria is as a missed opportunity to improve lending standards after years of seeing them whittled away.

“It’s a shame,” said John Bell, a portfolio manager at Loomis Sayles. “I wished this pandemic could have reset the clock for a while but it doesn’t look like that is happening.”

No, it doesn’t, and in fact the opposite is happening as both sovereign and corporate debt is now at all time record highs…

… comfortable with the assumption that when the next crisis inevitably hits, far stronger than what took place in March, the Fed will eventually end up buying it all.

via ZeroHedge News https://ift.tt/2FRbCUO Tyler Durden

Massive FinCEN Leak Exposes How Biggest Western Banks Finance Drug Cartels, Terrorists & Mobsters Tyler Durden

Sun, 09/20/2020 – 18:45

In what looks like one of the biggest leaks of private banking records since the Panama Papers, Buzzfeed News has published a lengthy investigation into how the world’s biggest banks allow dirty money from organized criminals, drug cartels, and terror groups like Al Qaeda and the Taliban to flow through their networks.

The “FinCEN Files”, as Buzzfeed calls them, offer “a never-before-seen picture of corruption and complicity.” A lengthy investigation by Buzzfeed and the International Consortium of Investigative Journalists – the same group that handled the Mossack Fonseca leaks –

Instead of combating financial crime, the current system of requiring banks to report all suspicious transactions to FinCen simply allows money laundering to flourish, while ensuring that any enforcement will be of the ‘whack-a-mole’ variety.

These documents, compiled by banks, shared with the government, but kept from public view, expose the hollowness of banking safeguards, and the ease with which criminals have exploited them. Profits from deadly drug wars, fortunes embezzled from developing countries, and hard-earned savings stolen in a Ponzi scheme were all allowed to flow into and out of these financial institutions, despite warnings from the banks’ own employees.

Money laundering is a crime that makes other crimes possible. It can accelerate economic inequality, drain public funds, undermine democracy, and destabilize nations — and the banks play a key role. “Some of these people in those crisp white shirts in their sharp suits are feeding off the tragedy of people dying all over the world,” said Martin Woods, a former suspicious transactions investigator for Wachovia.

Laws that were meant to stop financial crime have instead allowed it to flourish. So long as a bank files a notice that it may be facilitating criminal activity, it all but immunizes itself and its executives from criminal prosecution. The suspicious activity alert effectively gives them a free pass to keep moving the money and collecting the fees.

The Financial Crimes Enforcement Network, or FinCEN, is the agency within the Treasury Department charged with combating money laundering, terrorist financing, and other financial crimes. It collects millions of these suspicious activity reports, known as SARs. It makes them available to US law enforcement agencies and other nations’ financial intelligence operations. It even compiles a report called “Kleptocracy Weekly” that summarizes the dealings of foreign leaders such as Russian President Vladimir Putin.

What it does not do is force the banks to shut the money laundering down.

In response to Buzzfeed‘s questions about the leaked trove of SARs, the Treasury Department warned that the company’s decision to publish information gleaned from the leaked SARs could make banks more hesitant to file them, because inevitably hundreds of thousands of reports are filed every year involving transactions that are legitimate. The program was first created in 1992, but it has changed substantially over the last 20 years.

Congress created the current SAR program in 1992 making banks the frontline in the fight against money laundering. But Michael German, a former FBI special agent who is a national security and privacy expert, said that after 9/11, “the SAR program became more about mass surveillance than identifying discrete transactions to disrupt money launderers.” Today, he said, “the data is used like the data from other mass surveillance programs. Find someone you want to get for whatever reason then sift through the vast troves of data collected to find anything you can hang them with.”

It also warned that leaking SARs is illegal, and that the Treasury Department’s inspector general would be looking into the leaks.

Since we must give credit where credit is due, Buzzfeed does point out that in addition to being a powerful law-enforcement tool, the SAR system is a “nightmare” of surveillance overreach. Particularly after 9/11, the system evolved into a tool of mass surveillance, creating a massive trove of data that could be weaponized against anybody, according to a former FBI special agent who spoke to Buzzfeed.

Congress created the current SAR program in 1992 making banks the frontline in the fight against money laundering. But Michael German, a former FBI special agent who is a national security and privacy expert, said that after 9/11, “the SAR program became more about mass surveillance than identifying discrete transactions to disrupt money launderers.”

Today, he said, “the data is used like the data from other mass surveillance programs. Find someone you want to get for whatever reason then sift through the vast troves of data collected to find anything you can hang them with.”

When it came time for Robert Mueller to investigate the Trump Campaign’s ties to Russia, and whether the president knowingly colluded with a foreign government – a narrative, we later learned, with zero basis in fact – Mueller was able to access reams of SARS filed on Manafort, Michael Cohen and other members of Trump’s circle.

What did any of this have to do with Russia? Nothing, apparently.

They requested SARs on Deutsche Bank, which had loaned Trump money; Christopher Steele, the former MI6 agent who wrote the so-called Trump dossier; an array of Russian oligarchs; Trump’s former campaign chairperson Paul Manafort; and even a small casino in the Pacific run by a former Trump employee. All told, they were looking for information on more than 200 entities.

Many of the 1,000-plus SARS received by Buzzfeed were apparently requested by the Mueller team. However, none of the SARS included any direct information on Trump or the Trump Organization.

FinCEN unearthed tens of thousands of pages of documents. Those documents, along with a few additional SARs requested by federal law enforcement authorities, make up the majority of the FinCEN Files. Some were never turned over to the committees that requested them.

A person familiar with the matter blew the whistle to multiple members of Congress. The collection does not include any SARs about Trump’s finances. (A source familiar with the matter told BuzzFeed News that FinCEN’s database did not contain SARs on either Trump or the Trump Organization.) And though the documents show suspicious payments to people in Trump’s orbit before and after key moments in the 2016 presidential campaign, they do not provide direct information on any election interference.

When banks settle AML violations with regulators, typically, they’re asked to improve their controls – and in most cases, that means filing more SARs. The way the system is set up, banks are required to detail transactions, but have no say in prosecuting them, and staff cuts at FinCEN mean only a very small percentage of notices every get read.

However, since all of this data is stored, prosecutors can bring it to bear whenever a particular person or organization catches their interest.

Buzzfeed saved the banks’ statements on their investigation for a separate article (one that most of its readers will probably never see). But in a series of statements, the banks explain that its not their place to investigate these types of crimes. Buzzfeed reports that banks’ compliance workers are often shunted away in backwater offices in places like Jacksonville Florida (where many of Deutsche Bank’s compliance employees are situated).

More than 2 million SARs were filed over the past year, a massive increase over the past decade, according to Buzzfeed. That’s because, as banks have been filing more reports to cover their own backsides, regulators have endured staff cuts that left far fewer people there to examine them.

But some of the most egregious financial frauds in recent memory never generated a single SAR, including Bernie Madoff’s Ponzi scheme. When the reckoning with authorities came, JPM got off with a slap on the wrist.

PMorgan Chase got a deferred prosecution deal of its own. For years, it was the primary bank of the world’s biggest Ponzi schemer, Bernie Madoff. Despite multiple warnings from its own employees, the bank never filed a suspicious activity report on him and allegedly collected $500 million in fees. For punishment, the bank was required to pay a $1.7 billion fine and promise to improve its money laundering defenses. But after it settled the Madoff case, the bank’s own investigators said they suspected it had opened its accounts to an alleged Russian organized crime figure who is known for drug trafficking and contract murders, as well as businesses tied to the repressive North Korean regime, which the US has placed off-limits.

Buzzfeed’s sources argue that the only way to fix the problem is to arrest the executives of banks that break laws.

“The bankers will never learn until you start putting silver bracelets on people…Think of the message you’re sending to repeat offenders.”

[…]

“These guys know what they’re doing,” said Thomas Nollner, a former regulator with the Office of the Comptroller of the Currency. “You break the law, you should go to jail, period.”

Of course, the report also pointed out why this hasn’t yet happened – and why it probably never will. Because thanks to the Fed and the Treasury, ‘too big to fail’ also means ‘too big to prosecute’.

In 2012, Standard Chartered and HSBC were facing criminal prosecution. George Osborne, at that time the UK’s chancellor of the exchequer, wrote to the chairperson of the US Federal Reserve, Ben Bernanke, and Treasury Secretary Timothy Geithner to discuss his “concerns” that a heavy-handed response could have “unintended consequences.” He warned of a “contagion.” The implication: Close one bank and the whole economy could suffer.

Because while money might come from unsavory places – Russian organized criminals, the Taliban, etc – it still contributes to economic growth, and puts dollars into the banking system.

One ex-federal agent told Buzzfeed there’s a “mosaic” of reasons why banks are rarely prosecuted for AML violations: “Even if it’s bad wealth, it buys buildings,” he said. “It puts money into bank accounts. It enriches the nation.”

via ZeroHedge News https://ift.tt/2FCkSfN Tyler Durden

– Donald J. Trump, U.S. President, September 17, 2020

“Now is not the time to worry about shrinking the deficit or shrinking the Fed balance sheet.”

– Steven Mnuchin, U.S. Secretary of the Treasury, September 14, 2020

Money for the People

The real viral contagion that has infected the American populace is not an illness of the body. It’s something far worse than COVID-19. The American populace is suffering from an illness of the mind.

The general malady, as we diagnose it, is the unwavering belief that the government has an endless supply of free money, and the expectation that everyone, except the stinking rich, has claim to it. Why pursue self-reliance and independence when a series of stimulus acts promises the more abundant life? This viral contagion’s really ripped through the population in 2020.

For example, just a year ago, the American populace thought they could all live off the forced philanthropy of their neighbors. That to pay Paul you had to first rob Peter. The CARES Act proved to Boobus americanus that, without a shadow of a doubt, there’s free ‘money for the people’ in Washington. Sí se puede!

This week the Congress did its part to further the greatest show on earth. The people want stimulus. Congress intends to get to them, in good time.

Of course, the need to sprinkle the Country with printing press money was already a foregone conclusion. There was no discussion of the wisdom of not having a stimulus bill. The debate at hand was centered on how much.

Crazy Nancy wants $3.4 trillion. Senate Republicans want $500 billion. Something called the House Problem Solvers Caucus wants $2 trillion.

President Trump wants Republicans to “go for the much higher numbers.” His rationale: “it all comes back to the USA anyway (one way or another!).”

Extreme Intervention

There are only 12 days left in the U.S. 2020 fiscal year. The budget deficit’s already well over $3 trillion – more than double the previous $1.4 trillion record deficit set in 2009. With a little luck, the March to Common Ground stimulus agreement will not be reached.

Fiscal year 2020 finances are a disaster. Why start FY 2021 with another massive stimulus bill? What good would it do? The longer Congress dithers the better.

In the meantime, the Federal Reserve’s fully committed to extreme intervention in financial markets. By this, the Fed promises to keep credit cheap and abundant forever.

On Wednesday, following a two day Federal Open Market Committee (FOMC) meeting, the Fed released new projections showing the federal funds rate would remain near zero through 2023. The Fed, via quantitative easing (QE) also promised to buy more Treasuries and mortgage-backed securities; at least $120 billion per month.

We’ll have to wait several weeks for the FOMC meeting minutes to confirm. But we presume there was no discussion of the wisdom of ending QE, reducing the Fed’s balance sheet, and raising the federal funds rate. Such contrary measures are off the table until at least 2024.

The unwritten objective of this now endless QE is to further inflate stock prices in the face of economic catastrophe. Once again, Wall Street and the big banks are being given an endless supply of cheap and abundant credit. Where does this all lead?

How to Tackle the Depression Head On

By and large, the challenges facing the economy have everything to do with central government. Over the last 40 years, as the Fed and the Treasury colluded to rig the financial system in totality, wealth has become ever more concentrated in fewer and fewer insider hands. The effect over the last decade has been a disparity that’s so magnified few can ignore it.

Obviously, something has gone horribly wrong. The main cause, as best we can explain, is the near total abandonment of the rules of common sense in the dealing of money and credit. Old standards, old principles, and honest thinking have given way to quack economists, shameless political swindlers, and a burgeoning citizenry of dependents.

Indeed, we live in a world of deception. A world that will only become more deceitful as policies of desperation are rolled out in earnest to keep the price of money cheap, the price of assets high, the government swindlers in Washington flush with printing press money, and the masses of dependents well supplied with bread and circuses. But make no mistake, deceit will lead to greater deceit.

More bread is needed. The masses have grown sick and tired of wealth being concentrated at the top of the wealth spectrum. Moreover, they’re sick and tired of having their noses rubbed in the mud.

To be clear, these are not failures of capitalism. They’re failures of America’s brand of a centrally planned economy. The tertiary impediments of fake money, regulatory insanity, and government dependency cannot be overcome.

However, there is another way. Steve Forbes, in a January 22, 2014 article, offered an alternative to the current paradigm:

“Vibrant economies, not central banks, create real money, and wealth is abundantly created when tax rates are low, money is stable and regulations are reasonable.”

Stop the deceit. Stop the stimulus. Stop the QE. Stabilize the money supply. Let markets determine the rate of interest.

No doubt, an epic depression would be immediately upon us. But the depression will come regardless. In fact, it’s already here. Better to tackle it head on, with honesty, than to attempt to shirk it with deceit and pretense.

via ZeroHedge News https://ift.tt/2RG40qO Tyler Durden

Portland Neighbors Frustrated After Police Take 90 Minutes Responding To Hostage Situation Involving 12-Year-Old Tyler Durden

Sun, 09/20/2020 – 17:55

Residents of a Southeast Portland neighborhood are furious after police took 90 minutes to respond to a bizarre hostage situation last week, when a man ran into an apartment with a 12-year-old boy inside, grabbed a knife, and eventually fled after a standoff with the boy’s father. Neighbors chased the man down and cornered him, but he ran off again before police arrived.

“I was so scared,” said Henry Kirim, who was searching for a missing bank card in his car when the man ran inside. After Kirim went back inside, the man charged at him with a knife and a 20-pound dumbbell he found in the apartment.

When Kirim sprinted back to the apartment and unlocked the door, he saw the man grab a large knife from his kitchen counter. Kirim’s son, trembling and crying, was behind the stranger.

…

More than a half-dozen calls had come into 911 over the course of the bizarre ordeal. But that apparently didn’t speed the response.

The wait confounded and angered Kirim and his neighbors. They wondered what it would take for police to respond if not an armed man placing a child in jeopardy.

“Every neighbor here was expecting the police to come. We called about a million times, and the police would not show up,” Kirim said. –Oregon Live

The police have acknowledged that the delay was unacceptable – however they cited a record number of retirements and fatigued officers who have been covering months of BLM protests.

“This is not the service our community expects, nor is it what we want to provide,” said Deputy Police Chief Cris Davis.

That said, 49 officers have retired and nine have resigned since July. According to Davis, other officers are injured or on vacation – leaving the bureau with around 310 officers on patrol divided between three precincts. 102 of those officers don’t have full training, Davis added.

In this case, officers were simultaneously responding to a tactical call in East Precinct which required a special team, as well as monitoring a violent clash between protesters downtown and preparing for chaos that evening.

The priority now is to respond to emergency calls “when there’s an active threat or a life safety issue,” he said, often leaving 80 to 100 lower priority calls holding during mass gatherings or what have been regular protests before historic wildfires gripped the state and hazardous air quality kept people inside in the last week. –Oregon Live

Kirim’s neighbor, Deja Sieles, was one of the people who called police during the knife incident – telling a dispatcher that several neighbors were holding the intruder down near her apartment.

“I told them what was going on, and the operator seemed to know because he had received so many other calls,” said Sieles. “I think it’s pretty sad because like anything could have happened to anybody here. It scares me because I can’t rely on the police to help us out.”

The first emergency call, presumably from a neighbor, came in at 12:41 p.m.: Intruder in the house. Has a knife. Boy still inside.

“They said police would be here,” Kirim said. “And no police came.”

Dispatch noted at 12:49 p.m.: “No units avail,” meaning no officers available to respond.

Over the next 15 minutes, the man with the knife ransacked the two-bedroom apartment. Then he suddenly ran out the back of the apartment, breaking down a screen door.

Neighbors and Kirim chased after him. They caught him less than a block away in a nearby driveway after he tried to enter another home.

“November To Remember” – Goldman Warns A Biden Win Will Accelerate Dollar Weakness Tyler Durden

Sun, 09/20/2020 – 17:30

In a Friday note from Goldman’s FX strategy team, strategist Zach Pandl previews what is sure to be a “November to Remember” (even more so now in the aftermath of RBG’s death and the SCOTUS vacancy which has profound implications for capital markets as discussed overnight), and frames in a generally optimistic note (similar to Morgan Stanley), expecting more cyclical upside despite possible near-term weakness through an eventful autumn, to wit: “despite recent risk obbles, we continue to see our central growth forecast as consistent with further strength in cyclical assets, including equities, and more depreciation for the US Dollar.” Pandl dismisses the recent – and still ongoing – tech-led sell-off, saying that the latest correction was more a position adjustment than a broader fundamental shift: “significant flows into cash and options helped drive the Nasdaq to a stellar August without much fresh news, outperformance that has now largely reversed.” Meanwhile, the announcement of the Fed’s framework review at Jackson Hole, though largely as expected, also resulted in an additional move in real rates and breakeven inflation whose reversal presaged the equity drops. Meanwhile, on the positive side, Pandl writes that the global growth recovery “while flattening out in places, has also been broadening.”

So, the Goldman strategists concludes, the “central case is that equity markets will revisit the September high over the next couple of months, but driven this time more by an upgrade to the market’s cyclical view” with the caveat that early vaccine approval remains central to the bank’s pro-cyclical outlook, while noting that “investors may be too pessimistic about risky assets under a Democratic election sweep, due to the prospect of substantial fiscal easing next year.”

Echoing Morgan Stanley’s latest thoughts (which we brought readers yesterday), while Goldman is optimistic, it does warn of a variety of potholes “from here to there”, most of which are identical to the list presented previously by MS:

First, with the school reopening season now properly underway across much of the northern hemisphere, it will be important to watch if new economy-wide lockdowns (as has been the case in Israel) can be avoided.

Second, investor expectations from the latest round of US fiscal negotiations are already low, but it will still be a negative surprise to markets if no agreement is reached, or if partisan tensions threaten a government shutdown at the end of September.

Third, after a surprisingly unified response to the pandemic in Europe, political risks are rearing their head again. The constitutional referendum and regional elections in Italy this weekend—which may result in some losses for the governing coalition—will be a test of political stability. That said, without a new election, which seems unlikely, it is hard to see a major shift in political direction or a major selloff in BTPs. More importantly, Brexit has thrust itself back on the screen of global investors. Despite provocative legislation that would “break international law”, we think it is too early to completely dismiss the possibility of a negotiated “thin deal.”

Which brings us to the election, where Goldman focuses on the potential impact to two asset classes: equities, volatility and currencies.

Starting with stocks, Pandl writes that a Democratic sweep “would present a complicated mix for headline US equity indices” with the potential increase in corporate taxes from a Democratic sweep would be the most direct consequence for equity markets. But the prospect of larger fiscal stimulus and of more predictability in trade policy in that outcome push, at least modestly, in the other direction. While the net effect for US equity indices is probably a modest negative, Goldman notes that the uncertainty around that judgment is high, particularly since it is still unclear which policies will emerge as priorities for the possible Biden Administrations and how much has already been priced (the relative performance of “high-tax” and “low-tax equities” suggest, unsurprisingly, that the market has already shifted to some degree to price a possible Biden win).

Meanwhile, with worries about an extended delay over election results, a swift resolution in either direction may also reduce risk premia although now that we also have a SCOTUS vacancy to fill an optimistic outcome here looks unlikely. At the same time, and as in 2016, shifts in perceptions of the race around the Presidential debates may serve as a helpful barometer for the market’s initial reactions. But 2016 is also a reminder that the initial reaction may quickly reverse as the market reassesses the winner’s policy priorities. The more obvious shifts may be in relative performance, where Goldman thinks expansionary Democratic fiscal policy could support the outperformance of cyclicals over defensives, while non-US cyclical indices may benefit too (albeit less directly) from a stronger US fiscal impulse, and without facing the drag from higher US taxes.

Next, the Goldman strategist looks at volatility, writing that while it remains sticky, it is “vulnerable beyond the big events” as the election and vaccine events have important implications for the pricing of volatility and options risk:

For a broad range of assets, it is true both that implied volatility is unusually high relative to realized volatility and the slope of implied volatility between 1 and 3 months is unusually steep (in part because of the election “bump”). Both of these features are potentially important. Because the distribution of potential outcomes around the mix of vaccine and elections remains quite wide, options markets need to reflect that even if the day-to-day volatility is lower. But the experience around prior elections of the last few years and events like the 2016 Brexit referendum illustrates that resolution in any direction often leads to stickiness in implied volatility until that point and a sharp drop in implied volatility as one or other path is confirmed.

If Goldman is right that we will know the outcomes of both the vaccine and the election by December – even assuming the “risk-negative” versions – there is a good chance that the VIX may be significantly lower than forward pricing assumes by year-end, according to Pandl: “Given the potential for both some vaccine news as Phase III trials progress and potential shifts in election views through the debates, we think that horizon presents potentially interesting opportunities to position for core themes.” (which likely means Goldman prop is buying long vol from its clients).

Which brings us to the punchline, especially since this report is written by Goldman’s FX team. According to them, a Biden win should accelerate Dollar weakness. As Pandl explains, Goldman continues to see “a good case for sustained US Dollar weakness, reflecting the greenback’s high valuation, deeply negative real interest rates in the US, and a recovering global economy (which tends to weigh on the currency’s because of its unique global role).” A Democrat sweep in the US elections would likely accelerate this trend:

First, Biden’s proposals to raise the US corporate tax rate would make domestic stocks less attractive compared to international markets, all else equal, which could result in Dollar selling if US equities underperform. Regulatory changes, especially anything targeting the technology sector, could have similar effects.

Second, a large fiscal stimulus would also likely weaken the Dollar, due to the Fed’s commitment to keep rates low. Normally currencies appreciate after fiscal stimulus, because it lifts rates, and higher rates in turn attract portfolio inflows from abroad. But academic research finds that currencies depreciate after fiscal expansions when unemployment is high and/or central bank policy rates are stuck at their effective lower bound.

Third, a more multilateral approach to foreign affairs should reduce risk premium in certain currencies, especially the Chinese Yuan. Goldman recently lowered its 12m target for USD/CNH to 6.50 for this reason: a Biden Administration would likely imply lower trade war risks, and therefore should allow the Chinese currency to gain alongside broad Dollar weakness.

That said, other election outcomes would likely imply less Dollar weakness and affect the performance of certain crosses, according to Goldman. For example, if Democrats were to take the White House but Republicans maintain control of the Senate, the US policy approach toward China would likely change, but fiscal stimulus would become much less likely. This could result in Yuan outperformance vs the more risk-sensitive EM and G10 currencies. Alternatively, a Trump win plus Republican control of the Senate would likely benefit the Dollar, especially vs the Euro and Yuan.

Finally, as discussed yesterday in Tug Of War Across Markets Hides “Trade Of A Lifetime“, Goldman agrees that “a potentially potent mix of vaccine approval and fiscal expansion” could lead to a rip-roaring value/cyclical/reflationary rally. Goldman explains:

Implied probabilities for early vaccine approval and a Biden win in the US election—e.g. probabilities provided by Good Judgment Inc and FiveThirtyEIght, respectively—have been hovering around the 65%-70% mark. As these probabilities have consolidated, there have already been some signs of markets moving to price the most likely outcomes: cyclical stocks have held onto most of their August outperformance even with the Nasdaq selloff and EM high-yielding currencies (with the telling exception of the Russian Ruble) have displayed remarkable resilience. In the event that such procyclical probabilities inch higher, “markets should move further towards pricing the modal outcomes: a move higher in cyclical exposures in equities, higher breakeven inflation, and a broadening in the outperformance versus a weaker Dollar to include EM.”

As Pandl concludes, “These remain our core cross-asset recommendations ahead of a very busy autumn. To state the obvious, the more the market moves to price either vaccine or election results with greater certainty, the worse risk/reward we would see in these expressions, and the greater the need to consider hedges.”

via ZeroHedge News https://ift.tt/33M5420 Tyler Durden

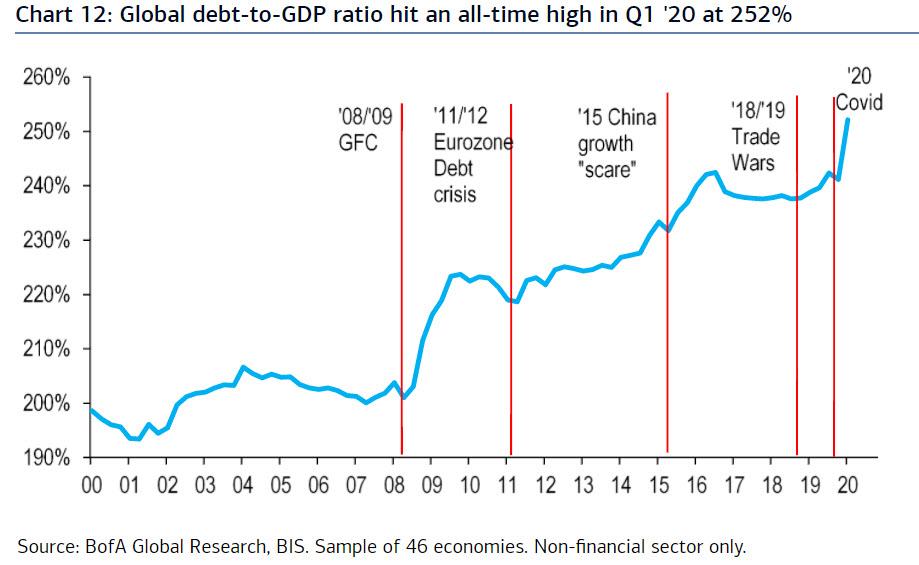

Global Debt Is Exploding At A Shocking Rate Tyler Durden

Sun, 09/20/2020 – 17:05

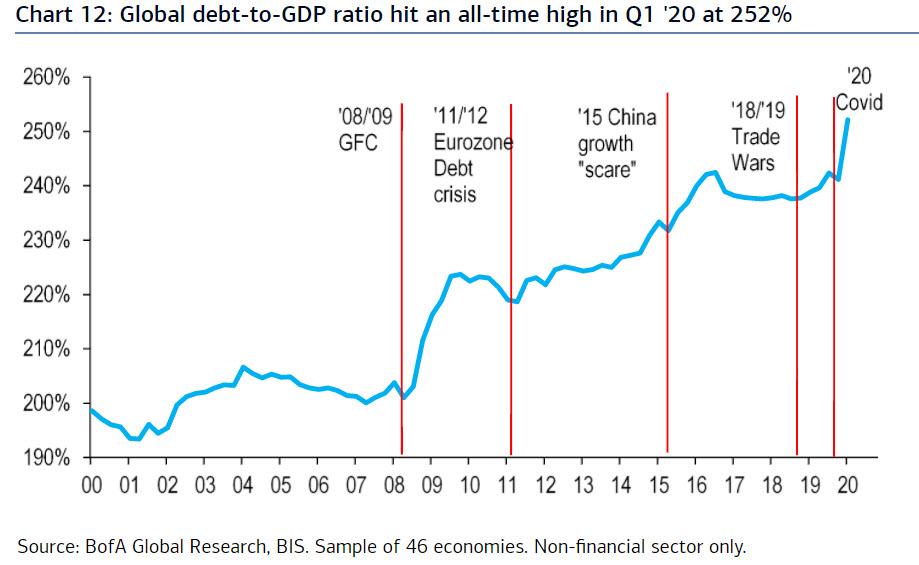

The primary reason why the global financial system is on the verge of daily collapse, and is only held together with monetary superglue and central bank prayers thanks to now constant intervention of central banks, is because of debt. And, as BofA’s Barnaby Martin succinctly puts it, much more debt is coming since “the legacy of the COVID shock is debt, debt and more debt.” In short: use even more debt to “fix” a debt probem.

So in this world of explosive credit expansion coupled with tumbling economic output where helicopter money has become the norm, central banks – and specifically the ECB – are scaling their QE policies to monetize and absorb much of this debt (relieving the pressure on private investors to buy bonds), more debt “hotspots” mean more vulnerabilities for the global economy.

We won’t preach about the consequences of this debt binge which has catastrophic consequences – we do enough of that already – but below we lay out some of the more stunning facts of global debt levels at the end of Q1 2020 as compiled by the BIS, courtesy of Martin:

Global debt/GDP surged to an all-time high in Q1 ’20, with overall debt for the non-financial sector now worth 252% of global GDP. This is up from 241% at the end of 2019, the biggest quarterly jump ever according to BIS data.

The chart also confirms that central bank inflation targets are higher, much higher than the “”official 2%: to erase this debt, central banks needs inflation to be in the 10%+ range. Anything below that would require debt defaults instead of inflation to wipe away the debt… and that is unacceptable.

This increase reflects the fallout from the first few weeks of the COVID crisis, with most advanced economies implementing total or partial lockdowns in March. Hence, the historical contraction in GDP growth observed worldwide in Q2 and the debt surge from both governments and non-financial corporations will translate into an even bigger rise in the global leverage ratio in Q2 ’20.

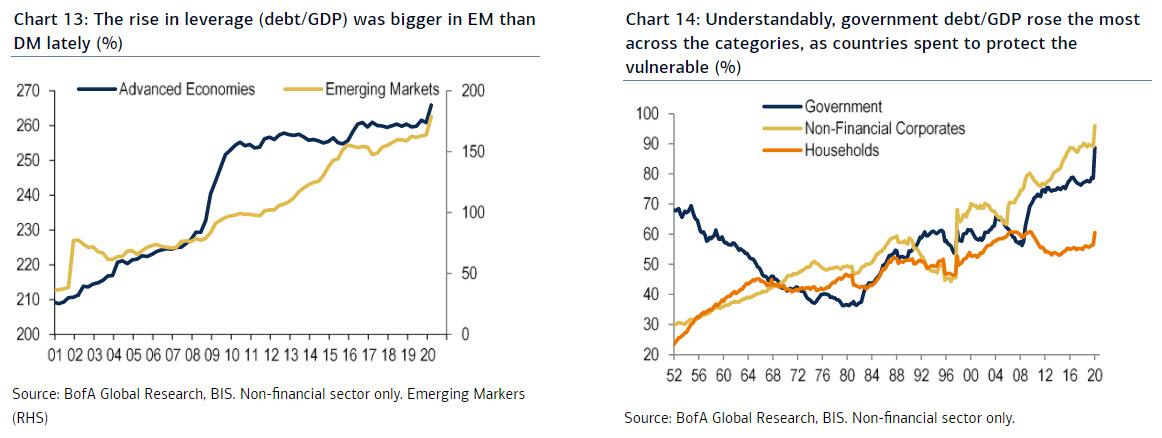

Pre-existing vulnerabilities have been laid bare by the nature of the COVID shock. While both advanced economies (DM) and emerging markets (EM) have seen their leverage ratios jump, the latter have observed a rapid increase since 2012 (Chart 13). The relatively deeper COVID recession expected for some EM economies – the OECD Sep ‘2020 Economic Outlook sees India and South Africa GDP falling by 10.2% and 11.5%, respectively – will likely magnify the jump in some EM’s leverage ratios.

By sectors, governments drove the big uptick in debt/GDP in Q1 ’20. The global sovereign debt-to-GDP ratio has reached 89%, up 10 percentage points, the largest quarterly rise on record.

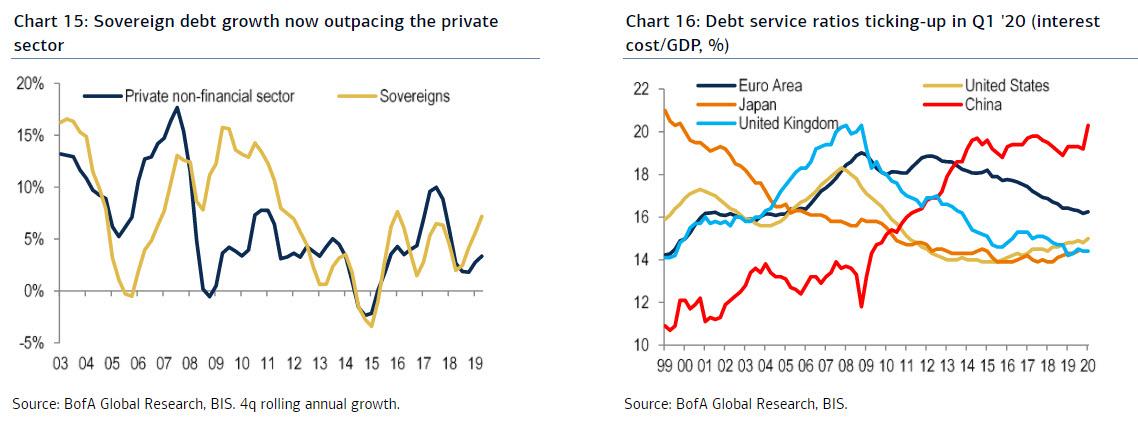

Debt service ratios ticked up, but only marginally, reflective of the tremendous QE support unleashed by central banks this year.

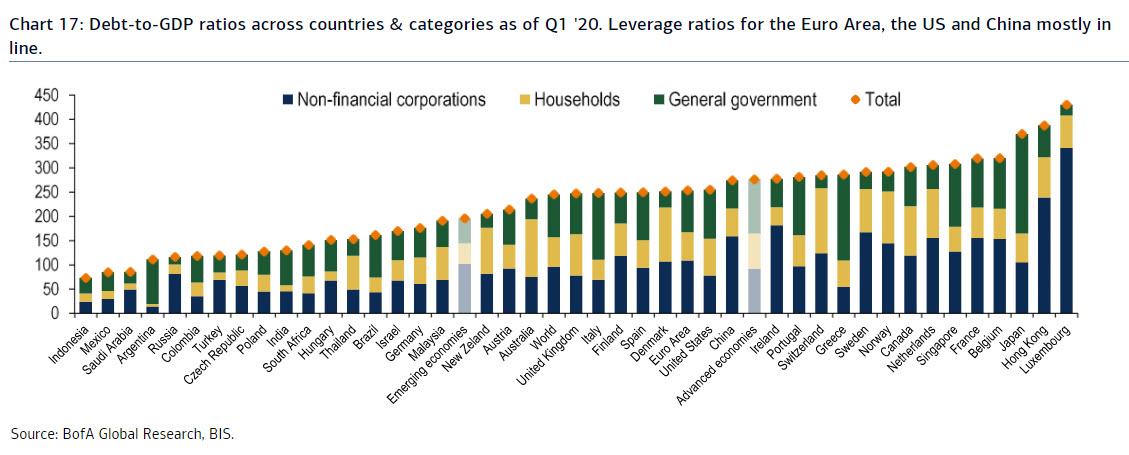

Total non-financial debt/GDP across countries and segments is shown in the BofA chart below; it shows that…

The total leverage ratio for Euro Area, China and the US are mostly in line now;

In Europe, a number of core countries (Belgium, Finland and Norway) saw a bigger increase in their total debt/GDP ratio than in the periphery in Q1 ’20;

While the rise in household debt has generally been more modest as consumers have moved into wait-and-see mode, China household debt/GDP rose 3.1% QoQ in Q1 ’20

Finally, the table below show global debt/GDP leverage ratio across the globe, broken down by countries and segments.

via ZeroHedge News https://ift.tt/3kAiKDS Tyler Durden

For all the infinite variations of time, personality and circumstance, U.S. presidential elections in their final three or four months fit remarkably clearly into one of two clear patterns:

There are those elections that are utter blow-outs where a decisive and usually landslide result was clear from the get go.

And there are those that are cliffhangers – in doubt up to the very last second.

Most U.S. elections surprisingly fit into the first category: Of the 10 presidential elections held over the past 40 years since 1980, no less than eight were blowouts where the loser had lost before the race had even begun:

Ronald Reagan in 1980 and 1984, George Herbert Walker Bush in 1988, Bill Clinton in 1992 and 1996, George W. Bush in his reelection race in 2004 and Barack Obama in his two sweeping victories of 2008 and 2012 were never seriously challenged. None of them had reason to doubt the outcome for a second.

Close calls are far rarer:

The only two in the past 44 years since 1976, were George W. Bush’s victory in 2000, which hinged on a highly dubious bungled vote in Florida stopped even more dubiously by a pro-Republican partisan majority on the Supreme Court stopping the recount by only a five to four margin.

The second was Donald Trump’s extraordinary victory in 2016 in which he won 30 out of the 50 states’ popular votes but lost the overall popular vote by almost 3 million.

This happened in large part because the Democratic governors and campaign managers in California and New York were witlessly obsessed with maximizing their own turn out including among illegal aliens.

Driving licenses were handed out to illegals in California in the months before November 2016 more freely than candy or crack cocaine for kids.

The other key pattern that usually emerges in U.S. presidential races is that the voting patterns and preferences harden after the two summer conventions and except for the most radical circumstances, major shifts are unlikely to occur until almost the end of the campaign. What is set by the end of August therefore usually remains unchanged until the beginning of November.

Then often key shifts do take place in the very last two weeks of the campaign when opinion polls are no longer taken.

That is what the decisive Heartland shift especially in the high population industrial states of Northeast and the Midwest to Donald Trump was completely missed by the pollsters four years ago.

Trump campaigned like a man inspired in those states recognizing their importance. His Democratic opponent Hillary Clinton chose to believe the meaningless reassurances of a computer algorithm called Ada – after the English peer Lord Byron’s hard-living and scandalous daughter – rather than the common sense warnings of her real flesh and blood campaign managers.

As Barack Obama, with all his many limitations, a master campaigner and election winner that only Ronald Reagan could match in the past 60 years, Clinton should not have been shocked by losing states that she never bothered to campaign in at all.

Joe Biden, even at age 77, has already proven that old as he is, he is an incomparably superior campaigner to Clinton. Unlike her, he knows people genuinely like him. He is Irish-American, and politics is to the Irish-Americans what whisky is to the Scots. And he is making sure he is seen and heard from Wisconsin to Florida.

But Biden is also reeling from a badly mismanaged convention season. Trump, at the Republican National Convention, presented a clear, coherent program of hope for beating the COVID-19 pandemic with new vaccines and restoring the great roaring bull economy he presided over for more than three years.

The Democrats instead repeated the same, ghastly mistake they made with Hillary Clinton in 2016: They made the convention the same mindless sugar for mentally deficient children that Clinton provided four years ago and contrary to all U.S. Mainstream Media predictions, Trump took effective advantage of it at his own convention.

Independent voters were manifestly unimpressed by the Democrats’ diet of sickly sweet sentimentality that even Walt Disney would have vomited over. Biden therefore got no bounce at all out his convention whereas Trump, previously far behind got a significant rise out in approval following his. By the end of August, Biden’s previous commanding lead over Trump had shrunk to within striking distance.

That process continues: As I write, a new poll commissioned by The Hill political newspaper in Washington with the HarrisX polling organization and released on September 15 gives Biden still a six-point lead over Trump. But Biden has lost two more points in less than two weeks according to the same pooling agency. If that kind of slippage continues un-reversed until November, Trump will win.

The race is currently too close to call.

via ZeroHedge News https://ift.tt/33KmH27 Tyler Durden