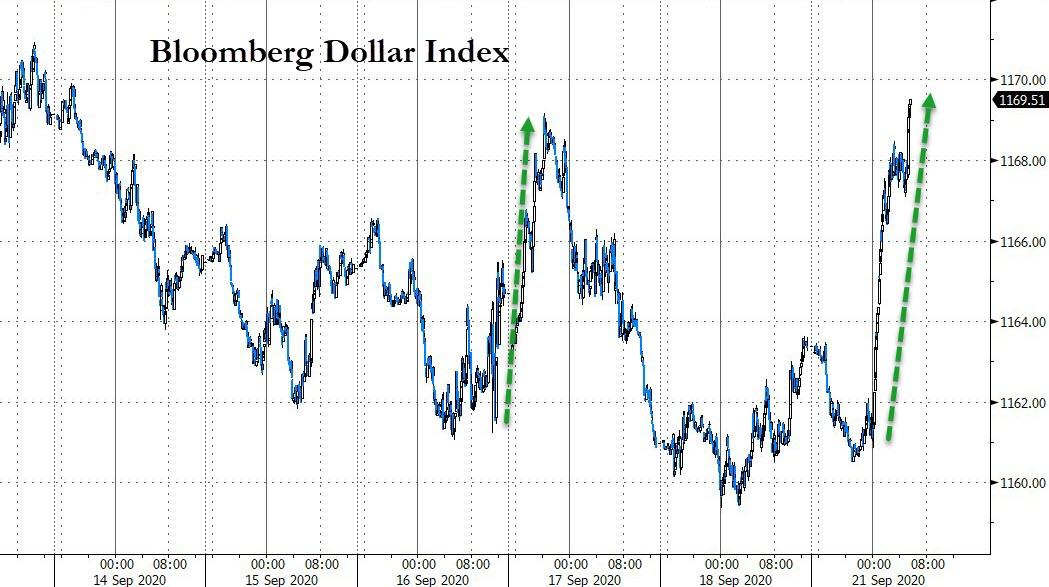

Stocks, Gold, & Crypto Crushed As Dollar Spikes Tyler Durden

Mon, 09/21/2020 – 08:45

Between bad banks behavior, COVID second-wave concerns, and political chaos; it appears markets (particularly stock markets) are waking up from their fiscal and monetary policy inspired dream-state.

Stocks are getting spanked…

The dollar is spiking…

Sending gold notably lower…

And Cryptos…

But bonds are bid…

Fed Chair Powell is on deck three times this week – seems like he needs to do so ‘splaining!

via ZeroHedge News https://ift.tt/361X7bs Tyler Durden

Rabobank: Is The Era Of American Global Hegemony Coming To An End Tyler Durden

Mon, 09/21/2020 – 08:36

By Michael Every of Rabobank

Friday saw the death of US Supreme Court justice Ruth Bader Ginsburg at 87. She was a true titan of the law, and leaves a critical (until now very liberal) Supreme Court seat vacant at a time when the US is bitterly divided on all issues. President Trump insists on pressing ahead with a hearing on a new appointment before the election – just as President Obama did before him when the (very conservative) justice Scalia died; Senate Republicans are saying they will proceed, which they wouldn’t in 2016; and the Democrats insist on not proceeding until after the election, which they didn’t in 2016. So business as usual.

However, this makes the US election even more important and heated than it already was – and harder to call. Listen to US commentators and all other topics are now secondary, including both the economy (bad for Trump) and Covid-19 (good for Trump). Republicans and Democrats are incredibly fired up given the outcome of the election could shift the balance of the court for a generation. Imagine if it shifted to 6-3 conservative; also imagine if no judge is appointed and it is then tied 4-4 when having to rule on a key element of what is widely expected to be a legally contested election; imagine the court being increased to 11 by Biden if he were to win; and imagine it going up to 15 or 17 if a Republican wins in 2024. This election was already seen as a potential risk event: arguably far more so now.

Meanwhile, on both Friday and Saturday, over a dozen Chinese fighter jets and bombers breached Taiwanese airspace, forcing defensive scrambles in response, and the Global Times has since threatened Taiwan’s president will be “wiped out” if she makes a misstep. That paper’s editor added on Weibo: “If we have no choice but war, we should avoid direct conflict with the US. We can (instead) severely beat up a US running dog that always crosses our bottom line….to send a warning.” It’s been a while since I’ve heard “running dog of US imperialism”: it isn’t very Davos.

As military strategists note, Taiwan must now allow Chinese military jets to fly unimpeded, not knowing if an attack might come; scramble its jets all the time, and see its far smaller forces become worn down; or respond militarily and provoke a terrible response. At which point the question of the US again enters the picture – unless it is too tied up in its own internal conflicts to focus on the outside world. However, legislation is currently being put forward forcing the US to defend Taiwan if it is attacked. Articles about TWD strength are justified on the macro level, but not so much at the meta level. Meanwhile, on the China-India border forces continue to build, and infrastructure building to allow rapid deployment continues apace even if the financial press has lost interest. The voluble Indian press, however, talk of fears of a surprise attack on US election day, or Xmas.

Against this backdrop, the US has reimposed full sanctions on Iran, which nobody else accepts the validity of – yet US secondary sanctions await anyone who breaks them;and the US reports Iran could have enough fissile material for a nuclear bomb by the end of the year; and that it is cooperating with North Korea to build an ICBM delivery system.

Echoing the hypothetical scenario we put forward in 2018, Iran is arguably happy to escalate this crisis because it believes with Russia, China, and even Europe and the UK unwilling to stand behind the US, the era of American global hegemony is close to a humiliating end, akin to the British at Suez. The bitterly divided US ‘will have to blink’.

And once it has blinked once, it will have to blink again and again, in Asia, in the Middle East, in Europe, etc., etc. One can imagine the kind of consequences that would flow: we might even talking about a new Potsdam and Yalta, even as we are would also be talking about whether the USD could remain top dog.

At the very least, Iran hope a change of president might see a new deal offered to them in January. [Ironically, as the hawkish US Foundation for the Defence of Democracy (FDD) notes, Iran is meantime relying on asset inflation until the US election is out of the way: despite “…recession, currency depreciation, and high inflation, [it is] showing all the signs of a state-initiated, state-sustained bubble.” Who knew the US and Iran had something in common?]

Relatedly, the latest financial scandal –where leaked documents show an alleged USD2 trillion of suspicious/illegal banking transactions– is news today. However, all previous scandals have had no market or political impact, and ‘the system is corrupt’ is hardly man bites dog, sadly. Perhaps the news can even be seen as bullish in that is shows some banks allegedly just ignore the kind of sanctions now back in place on Iran anyway.

Let’s be clear, however: US hegemony is extremely unlikely to go quietly into that good night. Like RBG, it is a fighter to the end. The US can still overcome internal divisions; its military prowess is still unmatched; and its financial architecture is the one in which we all work. True, the gloves may have to come off and sticks replace carrots, but a hegemon it is likely to remain. Such tail risks, the kind the likes of Bloomberg only refer to obliquely because it almost religiously inconvenient for them, are still very USD bullish should they transpire – which we all fervently hope they do not.

Yet we are proceeding down that same path at a more market-friendly pace anyway. TikTok might be saved, but as a de facto US entity, a mirror of how China’s critics say it treats Western tech firms there. However, a certain bank is reportedly going to be first on the newly defined China Unreliable Entity List, entry to which will mean loss of access to the Chinese market. The same bank is ironically also rumoured to be at risk of potential US sanctions for its actions supporting China. Moreover, Beijing is pressing ahead with reforms that mean Communist Party members must now enter into senior positions in all private companies, presumably including foreign firms. Again, this is likely to close off the current market ‘middle way’ of being in China but not ‘of China’, just as one could be in the US but not ‘of the US’ until TikTok.

As all this unfolds, Europe keeps on Europe-ing. The FT reports the EU wants new powers to break up tech giants, which means a head-on clash with the US unless the US comes to the same conclusion independently; the EU has to decide if it will follow US sanctions on Iran or not; it also has to try to decide today on its own sanctions on Belarus and for breaches of the Libyan arms embargo, including on Turkish firms; the EU is considering its own Magnitsky Act; and the ECB is considering reviewing its Covid-related bond buying program next month just as more and more countries see actions resembling a second lockdown more and more.

It’s hard work being a hegemon. Imagine if Europe were one again.

via ZeroHedge News https://ift.tt/2RJdzoH Tyler Durden

Joan Biskupic has published a lengthy profile of her twenty-year relationship with Justice Ginsburg. It is titled, “20 years of closed-door conversations with Ruth Bader Ginsburg.” Much of the material appears in Joan’s excellent books and articles. But there were a few bits I don’t remember seeing before. I will highlight them here.

First, Joan last met with RBG in January 2020:

In my last one-on-one session in her chambers, in January 2020 as a fire crackled, she had more pressing health concerns on her mind: “I’m cancer free. That’s good.” A year earlier she had undergone lung cancer surgery and, a few months after that, had endured a second pancreatic cancer scare.

Does this statement mean Biskupic and Ginsburg were out of touch after January? Most of Joan’s post-Term reporting concern events that happened after January. Most, but not all. And there may have been sessions that were not in chambers–especially after COVID shut down the Court. We’ll see next year if Biskupic continues to publish leaks, even without RBG.

Second, Joan addresses a common complaint: RBG used the press to speak to her colleagues.

On occasion, readers questioned whether Ginsburg was trying to send a message to the other justices through me. I brushed off that suggestion. Ginsburg was able to speak her mind and skilled at persuasion. And she never knew for certain when anything she told me would be published.

I’m not so sure about the last part. Media savvy people know what the money quote will be. When I speak to a reporter, I can usually get a feel for what will, and will not be published. Ginsburg’s “faker” line, for example, was bound for the front pages.

Third, Biskupic offers these remarks about Kagan. I don’t recall seeing these precise phrasings before:

She also enjoyed watching Kagan spar rhetorically with Chief Justice John Roberts in the behind-the-scenes drafting process. Kagan “is just a delight,” Ginsburg told me, “and very solid on substance.”

Over the years, I noticed RBG praised Justice Kagan fairly often. But I can’t recall seeing frequent praise of Justice Sotomayor. In big cases, Kagan would be assigned the dissent, and not Sotomayor. I’m sure this sleight was noticed.

Fourth, we learn that Justice Ginsburg broke her ribs a second time in 2013. (She broke them the year before, during the ACA deliberations):

The physical resilience of Ginsburg, then 79, continued to amaze me. When I went to see her at the close of the next year’s session, in 2013, I offhandedly asked whether she had again fallen. I did not expect the answer I received.

“Yes, I fell,” she said. “It was almost identical” to what had happened a year earlier. “I knew immediately what it was this time. They wanted to send me to … the emergency room, and I said, no, absolutely not. … There’s nothing you could do. You just live on painkillers for awhile.”

I don’t believe this injury was disclosed to the public. In 2012, she also delayed in telling the public about her broken ribs.

Fifth, Joan recounts an episode when President Obama invited RBG to lunch in 2014. Was he trying to nudge her to retire?

In 2014, I received a tip that Obama had privately invited Ginsburg to lunch a few months earlier. I could not help but wonder whether Obama was exploring the possibility that she might soon retire. I asked the justice how their time together had gone….

Ginsburg rejected my questions about whether he might have been fishing for any sign, as they dined alone, of her retirement plans.

“I don’t think he was fishing,” she said.

When I asked why she thought he had invited her, she said, “Maybe to talk about the court. Maybe because he likes me. I like him.”

In November 2014, the Democrats would lose the Senate. Perhaps this was a move in advance of that election, such that Ginsburg’s replacement could have been picked over the Summer of 2014. At the time, the Democrats had a slim, 53 seat majority.

Biskupic does relay a delightful anecdote:

“They’ve got a very good chef at the White House,” Ginsburg began. “The problem for me is the President eats very fast. And I eat very slowly. I barely finished my first course when they brought the second. Then the President was done, and I realized that he had important things to do with his time.”

Ruth loved food. She may have been 85 pounds soaking wet toward the end of her life, but she loved to eat. Slowly, very slowly. But God help you if you tried to take her plate way before she had eaten every last morsel of food on the plate.

Sixth, Biskupic relays some heart-felt comments from the wake of Justice Scalia’s passing.

“My first reaction was I was supposed to go first,” Ginsburg later told me. “I’m three years older. My second thought was, well, we all have to go sometimes.”

Referring to Scalia’s apparently dying in his sleep, she said, “It’s the best you can do.”

Apparently? Come on. Are we back to the Pillow Theory?

Seventh, RBG recounts a defeat from a 2011 CivPro case:

I told her that Scalia had once described her as “a tigress on civil procedure.”

“She has done more to shape the law in this field than any other justice on this court,” he had told me. “She will take a lawyer who is making a ridiculous argument and just shake him like a dog with a bone.”

“I wish he had listened to me more often,” Ginsburg responded during our January conversation.

She shuddered as she recounted a 2011 case in which, she said, Scalia and other conservatives had “picked up” enough votes to deprive her of a majority on a civil procedure issue. Before that case, she told me, “I was really on a roll.”

I scanned through the cases from OT 2010. My guess is J. McIntyre Machinery, Ltd. v. Nicastro. The court divided, sharply, about whether a consumer could sue a foreign manufacturer in state court over a product sold in the United States. Justice Kennedy wrote the plurality. Justice Ginsburg dissented, joined by Justices Sotomayor and Kagan.

from Latest – Reason.com https://ift.tt/35WuWem

via IFTTT

President Trump gave a series of interviews with Bob Woodward. Today, the Washington Post published some excerpts concerning the Supreme Court. Most of what Trump told Woodward is standard fare–he repeats the same points over and over again. There were a few new tidbits.

First, Woodward baits Trump by suggesting a statue of him should be built outside the Supreme Court:

Still, remaking the bench with conservatives is one of Trump’s key accomplishments, so much so that Woodward responded with a joke: “Maybe they’ll put a statue of you outside the Supreme Court.”

The president took to the suggestion instantly. “Oh, what a good idea,” Trump said. “I think I’ll have it erected tomorrow. What a great idea. I’ll think I’ll use it.”

But, Trump added, “I won’t say it came from me.”

Woodward is a good reporter. Woodward stroked Trump’s ego so Trump would say something outlandish. And nothing strokes his ego more than statues. Woodward succeeded. I recently watched All the President’s Men for the first time. (It is on HBO Max). Robert Redford captured Woodward well.

Second, Woodward asked Trump about the fact that President Carter had zero appointments. Trump relied, “He deserved none.” The Democrats had 61 seats during Carter’s first term and 59 seats during his second term. Imagine if White or Brennan or Marshall had retired early? Or if Douglas had stuck it out one more year?

It is remarkable how fickle life tenure is. In Trump’s first time, he will make three nominations. Obama had two in his first term, and zero in his second term. W. Bush had zero in his first term, and two back-to-back in his second year. Clinton had two in his first time, zero in his second term. H.W. Bush had two in his first term, and no second term. Reagan had one in his first term, and three in his second term. Carter had zero. Ford had one. Nixon had four in his first term. Had he served a full second term, in theory, he would have had the chance to replace William O. Douglas.

If Trump is able to confirm someone before inauguration day, he will have three appointments in his first term–second to only Nixon in the modern era. Of course, Presidents used to have many more. Eisenhower and Truman had five. FDR had nine. Harding had four. Taft had six. (Can you even name two of them?) Lincoln had five, but he was working with ten seats. (Too soon?). Jackson had six. And of course, GW, the OG, had eleven nominations (if you include John Rutledge’s recess appointment).

Third, Trump “keeps a list of judicial appointment orders displayed, prop-like, on the Resolute Desk — ‘kind of like he was cherishing it.'”

Fourth, Woodward tried to bait Trump on Bostock. Woodward was hoping Trump would criticize Justice Gorsuch, or say something homophobic. Nope:

Woodward also asked Trump about Gorsuch leading the court in a landmark decision on LGBT rights in June, when it ruled against the administration in offering sweeping protections for gay and transgender people against workplace discrimination.

When Woodward noted Gorsuch voted “against your administration’s position,” the president seemed to accept the decision, saying, “Yeah, but this is the way he felt. And, you know, I want people to go the way they feel.”

What a remarkable statement. After thousands of hours of vetting the short list, Trump says meh. “I want people to go the way they feel.” Forget textualism or originalism. Trump favors feelism.

Still, Trump lamented that the ruling “opens the spigots for a lot of litigation.”

He doesn’t say what those spigots are. Presumably, he is referring to the Title IX litigation. I doubt the Equal Rights Amendment litigation is on his radar. Keep an eye on those cases, post-Bostock.

Woodward asked whether Trump would have joined the Bostock majority. What a bizarre question. Again, Woodward was trying to bait Trump. Trump didn’t take the bait.

When Woodward said he believed that Trump might have joined the majority decision if he were on the court in favor of “more freedom,” the president considered the idea, before saying, “Well, I’ll never get that vote.”

Woodward tried to bait Trump one more time with flattery:

“Well, maybe you can appoint yourself,” Woodward joked.

“I am what’s good for the people,” Trump responded. “All people. So, you know, that’s where I am.”

After four years, I still cannot tell if Trump is toying with reporters, knowing they will blow up everything he says out of context.

from Latest – Reason.com https://ift.tt/2ZVa3w6

via IFTTT

President Trump gave a series of interviews with Bob Woodward. Today, the Washington Post published some excerpts concerning the Supreme Court. Most of what Trump told Woodward is standard fare–he repeats the same points over and over again. There were a few new tidbits.

First, Woodward baits Trump by suggesting a statue of him should be built outside the Supreme Court:

Still, remaking the bench with conservatives is one of Trump’s key accomplishments, so much so that Woodward responded with a joke: “Maybe they’ll put a statue of you outside the Supreme Court.”

The president took to the suggestion instantly. “Oh, what a good idea,” Trump said. “I think I’ll have it erected tomorrow. What a great idea. I’ll think I’ll use it.”

But, Trump added, “I won’t say it came from me.”

Woodward is a good reporter. Woodward stroked Trump’s ego so Trump would say something outlandish. And nothing strokes his ego more than statues. Woodward succeeded. I recently watched All the President’s Men for the first time. (It is on HBO Max). Robert Redford captured Woodward well.

Second, Woodward asked Trump about the fact that President Carter had zero appointments. Trump relied, “He deserved none.” The Democrats had 61 seats during Carter’s first term and 59 seats during his second term. Imagine if White or Brennan or Marshall had retired early? Or if Douglas had stuck it out one more year?

It is remarkable how fickle life tenure is. In Trump’s first time, he will make three nominations. Obama had two in his first term, and zero in his second term. W. Bush had zero in his first term, and two back-to-back in his second year. Clinton had two in his first time, zero in his second term. H.W. Bush had two in his first term, and no second term. Reagan had one in his first term, and three in his second term. Carter had zero. Ford had one. Nixon had four in his first term. Had he served a full second term, in theory, he would have had the chance to replace William O. Douglas.

If Trump is able to confirm someone before inauguration day, he will have three appointments in his first term–second to only Nixon in the modern era. Of course, Presidents used to have many more. Eisenhower and Truman had five. FDR had nine. Harding had four. Taft had six. (Can you even name two of them?) Lincoln had five, but he was working with ten seats. (Too soon?). Jackson had six. And of course, GW, the OG, had eleven nominations (if you include John Rutledge’s recess appointment).

Third, Trump “keeps a list of judicial appointment orders displayed, prop-like, on the Resolute Desk — ‘kind of like he was cherishing it.'”

Fourth, Woodward tried to bait Trump on Bostock. Woodward was hoping Trump would criticize Justice Gorsuch, or say something homophobic. Nope:

Woodward also asked Trump about Gorsuch leading the court in a landmark decision on LGBT rights in June, when it ruled against the administration in offering sweeping protections for gay and transgender people against workplace discrimination.

When Woodward noted Gorsuch voted “against your administration’s position,” the president seemed to accept the decision, saying, “Yeah, but this is the way he felt. And, you know, I want people to go the way they feel.”

What a remarkable statement. After thousands of hours of vetting the short list, Trump says meh. “I want people to go the way they feel.” Forget textualism or originalism. Trump favors feelism.

Still, Trump lamented that the ruling “opens the spigots for a lot of litigation.”

He doesn’t say what those spigots are. Presumably, he is referring to the Title IX litigation. I doubt the Equal Rights Amendment litigation is on his radar. Keep an eye on those cases, post-Bostock.

Woodward asked whether Trump would have joined the Bostock majority. What a bizarre question. Again, Woodward was trying to bait Trump. Trump didn’t take the bait.

When Woodward said he believed that Trump might have joined the majority decision if he were on the court in favor of “more freedom,” the president considered the idea, before saying, “Well, I’ll never get that vote.”

Woodward tried to bait Trump one more time with flattery:

“Well, maybe you can appoint yourself,” Woodward joked.

“I am what’s good for the people,” Trump responded. “All people. So, you know, that’s where I am.”

After four years, I still cannot tell if Trump is toying with reporters, knowing they will blow up everything he says out of context.

from Latest – Reason.com https://ift.tt/2ZVa3w6

via IFTTT

After remaining conspicuously silent during most of the negotiations, ByteDance spoke up Monday morning to declare that the TikTok-Oracle deal would result in an independent US-based company that would nevertheless be established as a ‘subsidiary’ of ByteDance.

However, according to Reuters, Oracle, Wal-Mart and other US investors are claiming that the deal would leave them with majority control.

Clearly, both can’t be true, especially with ByteDance claiming on Monday that it will own 80% of TikTok, and that reports to the contrary were merely “rumors”.

Accounts of the deal differ. ByteDance said on Monday that it will own 80% of TikTok Global, a newly created U.S. company that will own most of the app’s operations worldwide. Oracle and Walmart, which have agreed to take stakes in TikTok Global of 12.5% and 7.5% respectively, had said on Saturday that majority ownership of TikTok would be in American hands.

ByteDance in its statement on Monday said it was a “rumor” that U.S. investors would be TikTok Global’s majority owners and that ByteDance would lose control over TikTok. Oracle declined to comment on ByteDance’s statement, while Walmart did not respond to a request for comment.

Other sources tried to reconcile this discrepancy to Reuters, saying that 41% of ByteDance is owned by investors, including Sequoia, General Atlantic and other VC funds.

Some sources close to the deal have sought to reconcile the discrepancy by pointing out that 41% of ByteDance is owned by U.S. investors, so by counting this indirect ownership TikTok Global would be majority owned by U.S. parties. One of the sources said the deal with Oracle and Walmart values TikTok Global at more than $50 billion.

Not all of the deal details were contested. ByteDance also confirmed plans for an IPO next year – plans that were first reported last week. And also left the door open for TikTok’s reconstituted board to include a majority of Americans.

TikTok also confirmed plans for an initial public offering of TikTok Global. The Beijing-based firm said TikTok Global’s board of directors will include ByteDance founder Zhang Yiming as well as Walmart’s chief executive Doug McMillon and current directors of ByteDance. The company declined to further comment on who else would be among the directors.

But the most important details from the ByteDance announcement concerned the TikTok algorithm, and the app’s source code. Following reports yesterday that Trump had agreed to allow ByteDance to keep the algorithm, the company affirmed that the deal “does not involve any transfer of algorithms or technologies, and Oralce will be able to inspect TikTok US’s source code”. The division is “akin to US companies such as Microsoft Corp sharing their source code with Chinese technology experts”.

What’s more, after denying Trump’s claims about a plan to seed a $5 billion fund to finance the education of American children, ByteDance on Monday said that it would be paying $5 billion in taxes for TikTok global, which is based on “estimated income and other taxes the company will need to pay over the next few years and has nothing to do with the deal reached with Oracle and Walmart.”

China’s state-run newspaper the Global Times claimed that ByteDance retaining majority ownership of TikTok means it’s “not out of the game” and has “avoided the worst-case scenario” in the US. Another GT article cited a “concerted effort” between the Trump Administration, ByteDance and Beijing came together to hash out a deal that would work for all parties.

Shen Yi, a Fudan University professor, told the GT that if the Trump Administration tried to kill the deal, that it would “encounter direct checks and balances form interest groups of Wall Street”.

Anybody trying to follow the “head-spinning” deal terms could by forgiven for feeling lost. The New York Times pointed out in a story published last night that the TikTok deal has left investors and the general public wondering: What was that all for? Well, Oracle scored a major cloud computing contract, Wal-Mart scored a licensing deal and President Trump can still claim a “victory”, however meager. According to terms revealed yesterday, Oracle and Wal-Mart would own a 20% stake in the new company, which is expected to create 25,000 new US jobs, according to Trump.

TikTok US CEO greeted the news with a tweet proclaiming that TikTok was “here to stay”.

However, one cybersecurity expert quoted by the NYT claimed the deal raises new questions about security threats posed by the company.

Security experts said the national security threat posed by TikTok and other Chinese tech companies was certainly worthy of examination. Chinese law forces companies to cooperate with the government on national intelligence work, and officials from both parties in the United States said there was a risk that Beijing could access Americans’ sensitive data.

Yet the lack of specifics on how the new TikTok Global would handle national security concerns raised new questions on Sunday. “The premise was national security but where is the national security in this quote-unquote deal?” Professor Tobias said.

While the deal has averted what would have been a major crisis for millions of American teens and millennials (who would have been forced to make due with Instagram’s ripoff “reels” feature), the hectic negotiations have definitely taken a toll on the parties. In a humorous example of just how confusing the negotiations became, Wal-Mart published a news release on its website on Saturday that – according to the NYT – “perfectly captured the chaos”.

“This unique technology eliminates the risk of foreign governments spying on American users or trying to influence them with disinformation,” the company said. “Ekejechb ecehggedkrrnikldebgtkjkddhfdenbhbkuk.”

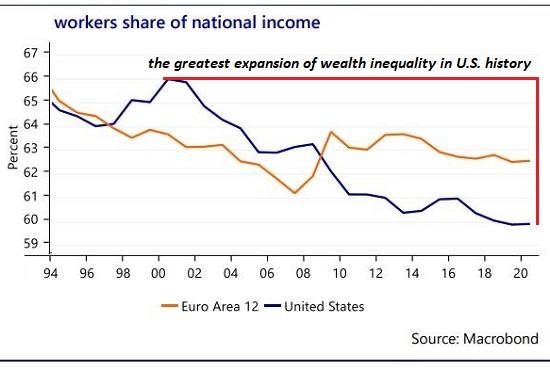

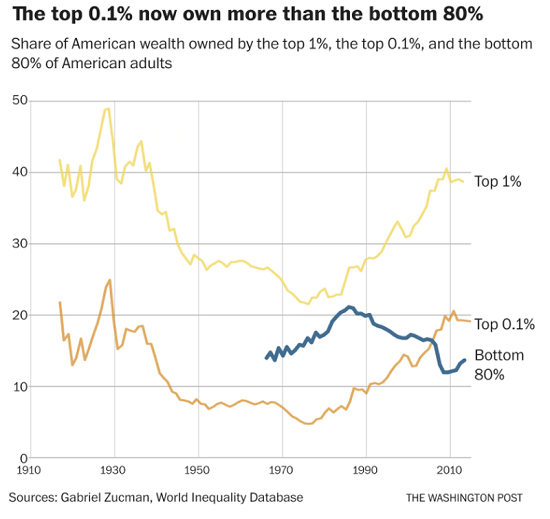

The battle to claw back a significant percentage of the $50 trillion is just beginning.

Do you hear the pathetic bleating of America’s billionaires and their army of toadies? If not, you soon will, for a remarkable report has been released that documents the $50 trillion in earnings that’s been transferred to the Financial Aristocracy from the bottom 90% of American households in the past 45 years.

The report was prepared by the RAND Corporation, and has a suitably neutral title: Trends in Income From 1975 to 2018. (The full report can be downloaded for free.)

Longtime readers know I’ve reported on the astounding increase in America’s economic inequality for the past 15 years, and addressed the eventual banquet of consequences this imbalanced, destabilizing state of affairs will serve up.

But with few exceptions, the corporate media has ignored this fundamental reality of American life, and blown off the consequences as easily ignored speculation by marginalized bloggers and commentators. (“Would somebody please shadow-ban these sites going on and on about soaring inequality? Thank you, Facebook, Google and Twitter–we’ll return the favor directly.”)

The extreme rarity of paragraphs like these in the corporate media cannot be over-emphasized. The corporate media has carried water for the billionaires and America’s Financial Aristocracy for decades. (No surprise, given that the vast majority of America’s media / social media is owned by the billionaires and Financial Aristocracy. Why bite the hand that feeds you, especially when the risk of losing your career is so high?)

Excerpted from the time.com article linked above:

There are some who blame the current plight of working Americans on structural changes in the underlying economy–on automation, and especially on globalization. According to this popular narrative, the lower wages of the past 40 years were the unfortunate but necessary price of keeping American businesses competitive in an increasingly cutthroat global market. But in fact, the $50 trillion transfer of wealth the RAND report documents has occurred entirely within the American economy, not between it and its trading partners. No, this upward redistribution of income, wealth, and power wasn’t inevitable; it was a choice–a direct result of the trickle-down policies we chose to implement since 1975.

We chose to cut taxes on billionaires and to deregulate the financial industry. We chose to allow CEOs to manipulate share prices through stock buybacks, and to lavishly reward themselves with the proceeds. We chose to permit giant corporations, through mergers and acquisitions, to accumulate the vast monopoly power necessary to dictate both prices charged and wages paid. We chose to erode the minimum wage and the overtime threshold and the bargaining power of labor. For four decades, we chose to elect political leaders who put the material interests of the rich and powerful above those of the American people.

That this level of incendiary outrage is now seeping into the mainstream media tells us that the bill for America’s $50 Trillion gluttony of inequality is long overdue and the pendulum of reckoning will swing to political, social and economic extremes equal to the extremes of wealth and income inequality engineered by America’s Financial Aristocracy and their toadies / lackeys in government, the Federal Reserve, Wall Street, Silicon Valley and the media.

The rallying cry to claw back a significant percentage of the $50 trillion is just beginning. The billionaires have the money and power, of course, and the best government that money can buy plus the loyalty of a vast army of well-paid toadies, lackeys, factotums and apparatchiks.

But once the citizens no longer accept their servitude, the pendulum will gather momentum. America’s Financial Aristocracy has reached extremes not just of wealth-income-power inequality, but extremes of hubris. Their faith in luxury bug-out estates / private islands is evidence that even if the way of the Tao is reversal, they’ll have their private bodyguards and stashes of fuel and other essentials.

The clawback might not be as easy to rebuff as they anticipate, nor will the pendulum swing that’s just starting necessarily arrive at the opposite extreme in the orderly, predictable fashion they’re accustomed to controlling.

Here’s a few of the many charts you’ve seen over the years here that illustrate rising inequality:

Global Stocks Plunge On Bank, Election, Virus Fears; Treasuries, Dollar Spike Tyler Durden

Mon, 09/21/2020 – 07:50

We said that futures trading ahead of the Monday open would be “fun“, and sure enough they did not disappoint.

Global markets tumbled on Monday, as S&P futures slid below 3,300 after failing to hold 50DMA support on Friday, and with European stocks falling the most since July as investors worried about renewed covid lockdowns across European countries and a report detailing suspicious transactions at international banks, with a lack of U.S. stimulus and concerns about how the death of Ruth Bader Ginsburg would impact what are already set to be extremely contested elections also hit sentiment.

U.S. stock index futures dropped 1.8% on Monday hit by bank stocks following media reports that several global banks moved sums of allegedly illicit funds over nearly two decades. Shares in JPMorgan Chase and Bank of New York Mellon Corp fell 4% and 3.3%, respectively, after a after a report by the International Consortium of Investigative Journalists that said lenders “kept profiting from powerful and dangerous players” in the past two decades even after the U.S. imposed penalties. HSBC Holdings Plc fell to the lowest since 1995 and European bank shares slumped (more here).

Shares of airlines, hotels and cruise operators led declines in premarket trading, tracking their European peers as the UK signaled the possibility of a second national lockdown. Marriott International, Hilton Worldwide and Hyatt Hotels Corp dropped between 1.5% and 3.6%, while casino operators Wynn Resorts, MGM Resorts International and Las Vegas Sands Corp shed between 2.7% and 6.0%. Tech giants including Apple, Facebook and Amazon.com which had dominated Wall Street’s rally since April, slid between 1.5% and 2.6% in early deals.

Nikola crashed 27.9% after its founder Trevor Milton stepped down as executive chairman, as the U.S. electric-truck maker battles allegations from a short-seller that it misled investors and automakers. General Motors which took an 11% stake in Nikola for about $2 billion earlier this month, slipped 3.7%.

Another round of business restrictions would also threaten a nascent recovery in the wider economy, analysts said, and could spark a flight from equities. The first round of lockdowns in March had led the benchmark S&P 500 to suffer its worst monthly decline since the global financial crisis.

“The market remains concerned about the broader risk emulating from the U.S: Covid, the Supreme Court fight and the upcoming presidential elections,” said Peter Rosenstreich, head of market strategy at Swissquote Bank SA. “With U.S. tech stocks looking weak, the need to jump right into U.S. assets feels less critical.”

The MSCI world equity index was down 0.5%. European indexes opened lower, with the pan-European STOXX 600 down 1.7% at its lowest in nearly two weeks. London’s FTSE 100 was at a two-week low, down 2.4% and Germany’s DAX fell 2%, led by banking shares which slid after a media report on how several global banks moved large sums of allegedly illicit funds over nearly two decades. HSBC shares tumbled to a 25-year low in Hong Kong.

Investors have also turned more cautious about Europe following a sharp uptick in new COVID-19 cases. European countries including Denmark, Greece and Spain have introduced new restrictions on activity. According to Reuters, Britain is considering a second national lockdown as new cases rise by at least 6,000 per day. Germany’s health minister said the rising new infections in countries like France, Austria and the Netherlands is worrying. Investors will be looking ahead to flash PMI data on Wednesday for the first hints of how economies have fared in September.

“Concerns are rising that the summer recovery is probably as good as it gets when it comes to the recent rebound in economic activity,” wrote Michael Hewson, chief market analyst at CMC Markets UK. “This reality combined with the growing realisation that a vaccine remains many months away, despite President (Donald) Trump’s claims to the contrary, has made investors increasingly nervous, as we head into an autumn that could see lockdowns reimposed.”

Earlier in the session, Asian stocks fell, led by materials and finance, after rising in the last session. The Hang Seng Index slid 1.5%, while equities in China and Australia also retreated. Taiwan’s dollar strengthened to a level not seen in seven years.The Shanghai Composite Index retreated 0.6%, with Sanxiang Advanced and Shandong Shida posting the biggest slides.

Emerging-market stocks and currencies headed for their biggest declines this month as surging coronavirus cases and uncertainty about additional US fiscal support dented demand for risky assets. The Mexican peso and South African rand led the retreat among peers as the U.S. political battle over who will be the next Supreme Court justice – following the death of Ruth Bader Ginsburg six weeks before Election Day – also weighed on sentiment. South Africa’s stock market was the worst performer, with the main benchmark headed for its longest losing streak since May 2019. The average spread on developing-nation dollar debt widened by 2 basis points.

Seven members of the Fed will speak this week – including chairman Jerome Powell appearing before Congressional committees – so investors will be looking for hints to determine the dollar’s direction. In a House Financial Services Committee hearing on Tuesday, Federal Reserve Chair Jerome Powell and Treasury Secretary Steven Mnuchin are expected to speak about the need for more stimulus.

“There’re too much expectations about U.S. economic resilience,” said Fabrizio Fiorini, chief investment officer at Pramerica SGR SpA. “There is more selloff to come. Election risk is underestimated.”

In FX, the Bloomberg Dollar Spot Index reversed early losses and extended Friday’s advance to rise against all Group-of-10 peers apart from the safe-haven Japanese yen which was in its sixth consecutive session of gains versus the dollar, up around 0.4% at 104.185. Japan has public holidays on Monday and Tuesday this week, meaning volumes are thin in Asian trading. The euro dipped against the dollar, sliding to $1.1791 while the safe Swiss franc rose against both the dollar and euro.

The yuan headed for a third straight daily drop, the longest slide since July, as the greenback advanced. The onshore yuan slipped 0.14% to 6.7793 a dollar as of 5:53 p.m. in Shanghai after earlier rising as much as 0.2%. A measure of the dollar’s strength rose in the afternoon as risk appetite took a hit on concern that the climbing number of virus cases across Europe could lead to travel restrictions and cripple an economic recovery. Despite the retreat over past few days, the onshore yuan has surged 4.3% in the third quarter, on pace for the best performance on record. The rally has come as the greenback is set for its weakest quarter in a decade and amid investor optimism over China economy.

The Turkish lira continued to plumb record lows with Moody’s adding more fuel to the fire warning that the country has almost depleted its buffers against a Balance of Payments crisis.

In rates, Treasuries jumped after risk sentiment deteriorated in global markets. Yields were lower by 5.5bp across long-end of the curve, flattening 2s10s, 5s30s by 3.1bp and 3.5bp; 10-year yields richer by 3.8bp at 0.655%. Treasuries bull flatten from London open after cash markets closed in Asia for Japan holiday. Risk-off backdrop supports long-end of the curve with S&P e-minis lower by 1.6% and Estoxx 50 dropping 3% over European morning session. U.S. 2-, 5-, 7-year sales due this week for comb. $155b, while Fed chair Powell is due to speak three times. In Europe, the benchmark 10-year German bund yield was down 2 basis points at -0.507% with most high-rated euro zone government bond yields down by a similar amount. The European Central Bank will review how long its emergency pandemic bond-purchase scheme should go on, the Financial Times reported. The European Council meets in a summit on Thursday and Friday this week.

Elsewhere, oil prices fell, with Brent crude down 1.8% at $42.39 a barrel while WTI was down 1.9% at $40.34 a barrel. Gold prices slumped, hit by the rising dollar, with spot gold down to $1,931 per ounce at 730am ET>

Data include the Chicago Fed National Activity Index. No major earnings are expected.

Market Snapshot

S&P 500 futures down 1.8% to 3,262.75

STOXX Europe 600 down 2.2% to 360.69

MXAP down 0.6% to 172.88

MXAPJ down 1% to 563.47

Nikkei up 0.2% to 23,360.30

Topix up 0.5% to 1,646.42

Hang Seng Index down 2.1% to 23,950.69

Shanghai Composite down 0.6% to 3,316.94

Sensex down 0.9% to 38,482.09

Australia S&P/ASX 200 down 0.7% to 5,822.62

Kospi down 1% to 2,389.39

Brent futures down 2% to $42.29/bbl

German 10Y yield fell 2.6 bps to -0.511%

Euro down 0.3% to $1.1807

Italian 10Y yield rose 0.7 bps to 0.756%

Spanish 10Y yield fell 0.2 bps to 0.283%

Gold spot down 0.5% to $1,940.89

U.S. Dollar Index up 0.3% to 93.19

Top Overnight News

U.S. deaths related to Covid-19 approached 200,000 and the nation’s new cases rose in line with a one-week average. Former FDA Commissioner Scott Gottlieb said he expects the U.S. to experience “at least one more cycle” of the virus in the fall and winter

The dollar’s weakest quarter in a decade may get even worse as investors respond to the effects that massive American equity-market gains have had on the composition of their portfolios

The European Union will unleash as many green bonds as the world issued last year, testing the level of investor interest in financing a shift toward cleaner economies

Democratic presidential nominee Joe Biden blasted Republican efforts to speed through a replacement for the late Justice Ruth Bader Ginsburg on the Supreme Court, warning that such a process would “inflict irreversible damage” on the country

Britain is at a “critical point” in the coronavirus pandemic, Prime Minister Boris Johnson will be told on Monday, as concern mounts that a second lockdown may be needed to stop the renewed spread of the disease.

The European Central Bank has launched a review of its pandemic bond-buying program to consider how long it should continue and whether its exceptional flexibility should be extended to older programs, the Financial Times reported, citing two Governing Council members that it didn’t identify

New Zealand cabinet has confirmed that gathering limits in Auckland will ease from Sept 23 while they will be lifted entirely for the rest of the country tonight, Prime Minister Jacinda Ardern said Monday

Oil steadied following its biggest weekly gain since June as a lack of clarity over the global energy demand recovery was balanced by the possibility that Saudi Arabia could press for more OPEC+ output cuts

A quick look at global markets courtesy of NewsSquawk:

Asian equity markets were subdued and US equity futures traded choppy after last Friday’s losses on Wall St amid quadruple witching and continued tech woes, with risk appetite also dampened by holiday conditions as Japanese participants observe a 4-day weekend. ASX 200 (-0.7%) was negative with losses in metal miners and financials underperforming in the broad weakness across its sectors aside from Health Care and Energy, while KOSPI (-1.0%) swung from gains and losses on varied COVID-19 headlines with South Korea to extend level 2 social distancing curbs by an additional week but will also be distributing emergency funds from the 4th extra budget within days. Hang Seng (-2.0%) and Shanghai Composite (-0.6%) were downbeat with HSBC shares slumping to a 25-year low in Hong Kong after a leaked document noted that the bank had permitted GBP 62mln to be moved to Hong Kong in suspicious transactions during 2013-2014 despite being warned by a regulator, while Standard Chartered also declined after being implicated by the ‘FinCEN’ leak, and other reports noted concerns HSBC and Standard Chartered could be frozen out of the US banking system in the event of a further escalation US-China tensions. Elsewhere, Tencent shares were pressured amid uncertainty regarding its US future despite a California judge halting President Trump’s ban on WeChat downloads, while weekend news that President Trump gave his blessing to the TikTok-Oracle-Walmart deal, also did little to spur risk appetite.

Top Asian News

Hedge Funds Raise Long Aussie Bets to 2018 High on China Rebound

Amundi Sanguine on Indonesian Bonds on Attractive Real Yields

China Tried to Dramatize Its Handling of the Virus. It Backfired

SCG Packaging Seeks to Raise Up to $1.27 Billion in Thai IPO

Stocks in Europe see deep losses across the board (Euro Stoxx 50 -3%) as the region coat-tailed on the downbeat APAC handover before extending on losses amid an intensifying risk averse tone and a number of sector-specific factors. Firstly, Travel & Leisure resides as the marked underperformer as the resurging cases across Europe trigger warning bells for the sector, with some of the region’s worst performers including the likes IAG (-12%), Tui (-8.6%), easyJet (-8.4%), Carnival (-8.0%), Lufthansa (-7.7%) and Ryanair (-7.1%). Secondly, the European banking sector plumbs the depths in light of a leaked US government document accused HSBC (-5%), Standard Chartered (-4.4%), Barclays (-6.2%), Deutsche Bank (-5.6%), JPM (-3.6% premkt) and BNY Mellon (-2.5% premkt) of moving large sums of illegal cash for shady characters and criminal networks. The documents center around the number of SAR’s (Suspicious Activity Reports) sent to US authorities between 1999 and 2017. The Basic Resources and Oil & Gas sectors are also among the laggards. As such, the UK’s FTSE 100 (-3.4%) underperforms the region despite a softer Sterling, given its heavy exposure to the aforementioned sectors. In terms of other movers and shakers, United Internet (-24%) and 1&1 Drillisch (-27%) reside as the biggest losers in Europe after cutting their respective FY EBTIDA guidance, whilst their spat with Telefonica (-3.6%) intensified over its subsidiary Telefonica Deutschland (-3.4) being accused of raising user costs significantly from July. Elsewhere, Rolls-Royce (-8.5%) holds onto its losses amid reports that the group is planning to raise as much as GBP 2.5bln to brace itself for another demand decline for aircraft engines. As such, Leonardo (-6.0%) continues falling despite an early halt, whilst Safran (-4.4%) is also pressured in sympathy. Finally, the Norwegian government has proposed that its Sovereign Wealth Fund should invest more within the US stock market and less within Europe.

Top European News

Unilever’s Dutch Investors Said to Approve Single Headquarters

European Stocks Drop Most Since July as HSBC Leads Bank Slump

Sweden Loosens Purse Strings With Virus Stimulus Budget

U.K. House Prices Up Most Since 2016 as Britons Seek More Space

In FX, although the Dollar has regained some poise amidst more pronounced risk aversion at the start of a new week, Usd/Jpy continues to decline alongside Yen crosses in the absence of Japanese market participants for ‘Old Age Day’. The headline pair has now breached another key chart if not major technical level in the form of July 31’s 104.20 low and there is little in the way of 104.00 to stop a 250+ pip cumulative fall from this month’s early peaks, especially given another holiday on Tuesday (Autumnal Equinox). However, it remains to be seen whether a 103.00 print provokes some verbal intervention from the MoF, and for now greater safe-haven demand for the Jpy is keeping the Usd index relatively capped beyond 93.000 within a 93.322-92.746 band.

AUD/CAD/CHF – All succumbing to the increasingly sour tone and deterioration in broad sentiment as the Aussie loses 0.7300+ status vs its US counterpart, the Loonie retreats through 1.3200 with added fuel from a reversal in crude prices and the Franc falls back below 0.9100, albeit holding above 1.0800 against the Euro following latest weekly Swiss bank sight deposit balances showing perhaps surprise declines ahead of the SNB. Question is, are these coincidental or significant in advance of a more official shift in policy to be revealed at Thursday’s quarterly review?

NZD/EUR/GBP – The Kiwi is back-pedalling further from Friday’s near 0.6800 peak vs its US peer and 1.0800+ apex on the Aud/Nzd cross even though NZ PM Adern scaled down the country’s COVID-19 alert level outside of Auckland again, while the Euro is retesting bids/support around 1.1800 and Sterling has recoiled over a big figure to sub-1.2850 on the ongoing rise of the pandemic across Europe.

SCANDI/EM – A sea of red as risk assets tumble, while the aforementioned downturn in oil takes a heavier toll on the Norwegian Crown compared to the Swedish Krona that seems to be deriving some traction from upbeat commentary by the nation’s Finance Minister. Similarly, the Yuan is drawing a degree of comfort from a steady PBoC Cny fixing, net liquidity injection and unchanged loan prime rates to offset other less favourable issues like the ongoing Sino-US spat and reports from China’s top infectious disease expert warning that a 2nd wave is inevitable. Conversely, diplomatic strains and the retracement in Brent are undermining the Lira and Rouble again, while the Rand has unwounded all and more of its post-SARB gains.

In commodities, WTI and Brent front month futures continue to decline with losses driven by the broader risk averse sentiment coupled with a firmer Dollar and the prospect of dwindling demand given the resurgence of COVID-19 prompting talks of renewed lockdown measures. Furthermore, on the supply side of the equation, Libya’s NOC said it will lift the force majeure at ports and facilities that were deemed safe, with the gradual return of Libyan oil raising questions in terms of an OPEC quota for the country. WTI Nov resides around USD 40.50/bbl, having declined from a high ~41.50/bbl, whilst Brent Nov hovers just under USD 42.50/bbl vs. a high of USD 43.30/bbl. Another thing to keep on the radar – unconfirmed twitter reports noted that Saudi King Salman is reportedly in a critical condition, albeit nothing has been seen since on this front, with participants likely to dwell on the future of the Kingdom’s oil policy should he be replaced. Elsewhere, precious metal prices succumb to the Dollar, with spot gold now losing ground below the USD 1950/oz mark having traded on either side of the level in APAC hours. Spot silver meanwhile extends losses below USD 26.50/oz after printing a high just shy of USD 27/oz earlier in the session. In terms of base metals, LME copper is pressured by the broader equity sell-off and the firmer Buck, whilst Dalian iron ore futures slipped over 2% amid the soured risk tone and sluggish downstream demand.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. 1.2, prior 1.2

12pm: Household Change in Net Worth, prior $6.55t deficit

DB’s Jim Reid concludes the overnight wrap

one of the reasons we have a widening bias for credit into year-end ( see our YE outlook here from a couple of weeks back) is that it seemed inevitable to us that we’d see a second wave causing confusion and chaos to many government’s strategies. Well as we sweltered in a pretty hot late September weekend here in the U.K. (and across much of Europe) the fact that the virus is already spreading quite rapidly is a big worry. It doesn’t feel like fatalities are going to be as big as an issue as they were in the first wave but it really is hard to understand what the strategies of governments are at the moment. They pretty much all don’t want a further wide scale lockdown but they also don’t want the virus to spread. Its not going to be easy to solve for both and as such It’s going to be a pretty difficult few months ahead if September is seeing numbers as high as they are already. I personally didn’t think these type of numbers would take place until well into October. Expect lots more restrictions over the days and weeks ahead, especially in Europe.

The latest on virus is that its spread has continued in the Europe with France reporting 37,282 new cases in the last 3 days, the highest since pandemic began. The 7 day average of new cases for France stands at 10,123,versus 8,161 a week ago. Over in the UK, the 3-day number stands at 12,661, the highest since May 9 with Health Secretary Matt Hancock not ruling out that London office employees might have to work from home again this week as Chief Medical Officer Chris Whitty is set to warn on today that the UK is at a “critical point.” Meanwhile, the LBC radio reported yesterday that London Mayor Sadiq Khan will recommend tightened rules for the capital today. Across the other side of world, South Korea reported 70 new cases yesterday, the lowest since the second wave began. However, the country is set to strengthen social distancing rules from September 28 to October 11, which will be designated as special quarantine period as the country celebrates Chuseok holidays from September 30 to October 4. So restrictions are tightening in even successful virus fighting places.

The weekend political press has also been full of news after US Supreme Court Justice Ruth Bader Ginsburg passed away late Friday night following a long battle with cancer. Afterwards, President Trump said that he would put forth a nominee to fill the seat and Senate Majority Leader McConnell said “President Trump’s nominee will receive a vote on the floor of the United States Senate,” indicating that Republican leadership will try to fill the seat ahead of the election.This represents a turn in the Majority leader’s thinking from 2016, where he did not allow a floor vote for then-President Obama’s nominee in an election year. The nomination and confirmation process will introduce a new element to an election not least because the court can hold sway over highly contentious issues like healthcare, abortion rights and gun law.

It brings lots of fascinating scenarios to the table. If Trump succeeds at getting his nomination through before the election there will be a 6-3 Republican bias to the Supreme Court which as discussed could have policy ramifications for the US for a generation. Democrats are up in arms that the Republicans won’t wait until after the election and are suggesting that may do extraordinary things to address the balance (like adding new judges to the bench) if they gain control of both the Senate and the White House. Congress altered the size of the bench seven times in the first eighty years of the republic (ranging from 5 to 10 justices) but this has not changed since the Judiciary Act of 1869. However getting the current Senate to confirm a nominee won’t be straight forward for Mr Trump as the GOP only hold a 53-47 majority in the Senate (with Vice President Pence serving as the tie-breaker) and a few members have already made noises that they don’t think a new judge should be added this close to the election. So even more drama added to an election campaign.

Another interesting weekend story is of China revealing how it will manage its “unreliable entity list” that aims to punish firms, organizations or individuals that pose a threat or potential threat to China’s sovereignty, national security, development and business interests; and those that discriminate against or harm Chinese businesses, organizations or individuals. According to details, penalties will include restrictions on trade, investment and visas of any company, country, group or person that appears on its “unreliable entity list.” The Global Times has carried an article that HSBC is a possible candidate and is down -2.91% to the lowest level it has traded since the 2008 financial crisis.

In overall trading, the Hang Seng (-0.95%) is leading the declines this morning not helped by this. Other Asian markets have also started the week on a weak footing with the Shanghai Comp (-0.41%), Kospi (-0.29%) and Asx (-0.54%) all down along with S&P 500 futures (-0.21%). In fx, all G-10 currencies are trading strong against the greenback with the US dollar index down -0.21%.

In other news, the FT reported that the ECB has launched a review of its pandemic bond-buying program to consider how long it should continue and whether its exceptional flexibility should be extended to older programs. The report added that the review is expected to be discussed by policy makers next month.

Looking to this week now, the flash PMIs on Wednesday will probably get the most attention due to it being one of the first glimpses of September economic performance around the world. Economic and social restrictions are mounting again in various places due to the virus but it may be a bit too early to see their impact in these numbers.

It’ll also be worth keeping an eye on Germany’s Ifo survey on Thursday, which has so far been rising each month since its April low, even as it remains below its pre-pandemic level. The consensus is looking for a further increase to 93.8, which would be just 2 points below its level in February.

Meanwhile Fed Chair Powell will be speaking three times before congressional committees. He’ll be appearing tomorrow before the House Financial Services Panel about the CARES Act. Then on Wednesday he’ll be appearing on the House Select Subcommittee on the Coronavirus Crisis, before Thursday sees him speak before the Senate Banking Committee on the CARES Act once again. Otherwise, there’ll be remarks from Fed Vice Chair Quarles on the economic outlook, while Bank of England Governor Bailey will be speaking twice next week.

There’ll also a special European Council summit on Thursday and Friday. As well as taking stock of the Covid-19 pandemic, the agenda includes a discussion of the single market, industrial policy and digital transformation, along with the EU’s external relations. Brexit may get a small mention as relationships between the EU and the U.K. are just about hanging by enough of a thread enough to merit it. The day by day calendar of the week ahead is at the end.

Recapping last week now and equity markets continued to feel the pullback in mega-cap tech stocks. The S&P 500 dropped -0.64% (-1.12% Friday) to six week lows, having declined for a third straight week for the first time since October 2019. The index is now down -7.30% from 2 Sept highs. The NASDAQ also fell a third week in a row itself, declining -0.56% (-1.07% Friday) and is now down -10.48% from recent highs. Meanwhile European equities edged higher for a second straight week with the Stoxx 600 ending the week +0.22% higher (-0.66% Friday). While the broader index rose on the week, many individual bourses across Europe finished lower with the DAX (-0.66%), FTSE 100 (-0.42%), FTSE MIB (-1.49%), CAC 40 (-1.11%) and IBEX (-0.19%) all posting losses as Covid-19 caseloads continue to rise throughout western Europe, prompting some restrictions to be reinstated. Asian equities were mixed with the CSI 300 up +2.37% on the week, while the Nikkei (-0.20%) and the Kospi (+0.66%) saw smaller weekly moves.

Similar to risk assets, core sovereign bonds were mixed on the week. US 10yr Treasury yields rose +2.8bps (+0.5bps Friday) to finish at 0.694%, while 10yr Bund yields were down -0.4bps (+0.6bps Friday) to -0.49% and gilts were largely unchanged (+0.1bps) at 0.18%. The dollar fell -0.44% on the week after rising in 3 of the previous 4 weeks. This in part supported gold’s +0.53% rise on the week, while copper gained +2.62%. However, the largest move in commodities was in oil. Brent (+8.34%) and WTI (+10.13%) rose in part on news that Russia and Saudi Arabia would push their fellow OPEC+ members on keeping to quotas.

On the data front from Friday, UK August retail sales rose more than expected and up +0.6% MoM (+0.4% expected) and +4.3% YoY (+4.2% expected). In Germany, August PPI was -1.2% YoY, up from last month’s -1.7% reading and slightly higher than expected (-1.4%). While in the US, the preliminary reading of the University of Michigan Sentiment survey showed an +4.9pt increase to 78.9 (75.0 expected), which is the highest since March.

via ZeroHedge News https://ift.tt/2FM9deg Tyler Durden