NASA is already beginning preparations for the arrival of the asteroid called “The God of Chaos.” The asteroid is said to be approaching Earth and will come close to our planet in 2029.

The asteroid’s official name is 99942 Apophis. It is a 1,110-foot-wide asteroid named after the Egyptian god of chaos. It will fly as close to the Earth as some of the orbiting spacecraft panicking scientists.

99942 Apophis will come within 19,000 miles of Earth on April 13, a decade from now, but scientists at the Planetary Defense Conference are already preparing for the encounter, Newsweek reported. They plan to discuss the asteroid’s effects on Earth’s gravity, potential research opportunities and even how to deflect an incoming asteroid in a theoretical scenario.

The asteroid will be visible to the naked eye and will look like a moving star point of light, according to NASA. It will pass over the United States in the early evening, according toWUSA 9. 99942 Apophis was discovered in 2004 and, after tracking it for 15 years, scientists say the asteroid has a 1 in 100,000 chance of striking Earth decades in the future. But in the fairly distant future: after 2060, Newsweekreported.

NASA is going to be using a simulation of an “asteroid apocalypse” in order to help the space agency prepare for the cataclysmic event. And they are taking it seriously, as disaster planners from FEMA will join NASA for a dress rehearsal of doomsday.

International partners, including the European Space Agency (ESA), will also be a part of the simulation. The drill is said to be a “tabletop exercise” that will simulate just how a planetary asteroid emergency would play out in real time. Although an emergency on this scale has never happened, and factors such as the location of impact will have a massive effect on the response to such a globally catastrophic event.

According to the Metro UK, disaster planners from Federal Emergency Management Agency (FEMA) will join with NASA to hold a “make-believe apocalypse” intended to “inform involved players of important aspects of a possible disaster and identify issues for accomplishing a successful response.” The scenario will begin with the fictional premise that on March 26, astronomers “discovered” a near-Earth object (a comet or asteroid which comes within 30 million miles of Earth and one they consider potentially hazardous to Earth), NASA wrote. -SHTFPlan

This recent simulation was for a different asteroid named 2019 PDC.

via ZeroHedge News http://bit.ly/2Jg3BrZ Tyler Durden

New York Times White House correspondent Peter Baker has published an updated edition of his book “Obama: The Call of History”, and it includes several embarrassing details about President Obama’s reaction to Donald Trump’s historic electoral triumph, as well as Obama’s complaints about Hillary Clinton’s “scripted, soulless” campaign strategy.

According to the Daily Mail, which published some of the excerpts on Friday, Obama interpreted Trump’s victory as a “personal insult”, and whined to his aides and family that the loss “stings” and that the American people had “turned on him” while bashing Clinton for “bringing her many troubles on herself.”

As Baker wrote, as Obama saw it, the “real blame” for Clinton’s loss “lay squarely with Clinton” – despite her many well-documented attempts to make every conceivable excuse, from blaming Bernie Sanders and his misogynistic “Bernie Bros” to misogynistic Trump supporters.

But as Obama vented, nobody forced Clinton to take money from Goldman Sachs, or set up an illicit private email server at her house in Chappaqua.

In a stinging passage Baker writes: ‘To Obama and his team, however, the real blame lay squarely with Clinton.

‘She was the one who could not translate his strong record and healthy economy into a winning message.

‘Never mind that Trump essentially ran the same playbook against Clinton that Obama did eight years earlier, portraying her as a corrupt exemplar of the status quo.

‘She brought many of her troubles on herself. No one forced her to underestimate the danger in the Midwest states of Wisconsin and Michigan.

‘No one forced her to set up a private email server that would come back to haunt her.

‘No one forced her to take hundreds of thousands of dollars from Goldman Sachs and other pillars of Wall Street for speeches.

‘No one forced her to run a scripted, soulless campaign that tested eighty-five slogans before coming up with ‘Stronger Together’.

Feeling secure in Clinton’s impending victory, Obama and his top aide Valerie Jarrett retreated to the White House movie theater to watch the Marvel Movie Dr. Strange. Michelle Obama went to bed early that night, but later in the evening, as results from Florida started coming in, Obama checked the results, and was suddenly struck by a sinking feeling.

He watched in abject horror as Trump won Michigan, Wisconsin and Pennsylvania – formerly Democratic strongholds.

In the weeks after Trump’s victory, Obama vacillated from philosophical contemplation to rage, and complained to his speech writer Ben Rhodes that he was about to hand the nuclear codes over to a “cartoon character” and a “huckster straight out of Huckleberry Finn”.

Obama tried to keep his cool in the weeks afterwards and texted his speechwriter Ben Rhodes: ‘There are more stars in the sky than sand on the earth’.

But soon he was unable to contain his rage which escalated after he met Trump in the Oval Office.

Baker writes that despite being cordial in public he afterwards summoned Rhodes who told him that Trump ‘peddles in b*******’

Rhodes said: ‘That character has always been part of the American story. You can see it right back to some of the characters in Huckleberry Finn’.

Obama replied: ‘Maybe that’s the best we can hope for’.

As the weeks went by Obama went through ‘multiple emotional stages’, at times being philosophical and other times he ‘flashed anger’.

He also showed a rare self-doubt and wondered if ‘maybe this is what people want’, Baker writes.

Obama told one aide: ‘I’ve got the economy set up well for him. No facts. No consequences. They can just have a cartoon’.

Of particular interest considering the Mueller report’s findings, which have been endlessly relitigated since the redacted report was released last month, Baker explains Obama’s decision not to come out harder against Russia during the campaign, after US intelligence warned about the Kremlin’s attempts to ‘interfere’ in the US election.

As Baker tells it, Obama’s “don’t-do-stupid-shit” instincts made him reluctant to bash Russia over the meddling, as did his confidence that Clinton would surely prevail. As Obama saw it, if he made a big deal about Russian interference, Trump would simply complain to his voters that the whole election was rigged.

Baker’s book also gives new insight into why Obama was so hesitant about criticizing Russia for meddling in the 2016 election before vote took place.

Obama was led by his ‘cautious don’t-do-stupid-s**t instincts’ and feared that a forceful response would make Russia ‘escalate’ its operation.

Then there was the question of how Trump would react and Obama admitted that ‘if I speak out more, he’ll just say it’s rigged’.

Obama wrongly assumed that Clinton would win the election and Obama said in one meeting that Russian President Vladimir Putin ‘backed the wrong horse’.

When it came time to meet his successor and start planning the transition, Obama was cordial. But he never could get past the unshakeable feeling that the American people had rejected his legacy.

President Trump on Friday spoke with Russian President Vladimir Putin for the first time since the release of the Mueller report.

The two spoke on the phone for more than an hour, discussing the Mueller report, Venezuela, Noth Korea and other matters, according to White House Press Secretary Sarah Sanders.

.@PressSec Sarah Sanders: “Earlier this morning the president spoke with President Putin. They had a very good discussion. Spoke for a little over an hour.” pic.twitter.com/ywIlX11Sy4

On the Mueller report, Sanders said “both leaders knew there was no collusion,” adding that their discussion on the matter was brief, according to CNBC.

The two world leaders have spoken via phone over six times, according to official readouts from the White House. Putin said last year that the two spoke “regularly,” according to the report.

The discussion between the two leaders comes amid a tense political standoff in Venezuela. Opposition leader Juan Guaido has escalated his calls in recent days for a mass uprising, with the backing of the United States, against Russian-supported leader Nicolas Maduro.

The two countries have warned each other against intervention –CNBC

“This is our hemisphere,” said National Security Adviser John Bolton on Wednesday. “It’s not where the Russians ought to be interfering.”

Meanwhile, Russian Foreign Minister Sergei Lavrov issued a warning to US Secretary of State Mike Pompeo that US intervention in Venezuela would violate international law and could lead to grave consequences, according to Reuters.

via ZeroHedge News http://bit.ly/2WnNwUL Tyler Durden

There’s some good news for employees of Tesla that haven’t yet been laid off, and are burning the midnight oil working tirelessly for their visionary leader Tony Stark Elon Musk: the company is now offering them personal loans that can be paid back directly from their paychecks, according to CNBC.

As if going into the insurance business (please clap) wasn’t enough of a pivot for Tesla of late, the company is now also apparently going to try its hand in loansharking… to its own employees. The loans will be facilitated through London-based fintech start-up Salary Finance, and funded via its partner Axos Bank.

The plan is being pitched as a way for employees to “borrow money at relatively affordable rates”, where the key word, of course, is relatively.

Salary Finance is in the business of letting workers borrow up to 20% of their salary and pay it back at rates under 5%, although the “under” tends to be loose. Tesla is referring to this plan as a “financial well being” benefit, as if charging employees 5% interest is somehow a convenience. Though, it doesn’t surprise us entirely that a company with over $11 billion in debt is following this line of logic.

Tesla says that the plan is a way for employees to “handle their debt and expenses without turning to higher-cost alternatives like a 401k loan, credit cards with a high annual percentage rate, or traditional payday loans.” Cynics have seen right through these explanations, and believe this is a way for the company to avoid its employees being “forced” to liquidate their TSLA stock, especially as it drops ever lower, and subjects an increase number of them to margin calls.

Current employees, however, don’t seem to excited about the idea.

CNBC spoke to three employees who said that they view employee loans as a “band-aid”. Maybe Tesla should promote these three employees to their accounting department for a couple days – sounds like they may be able to clean up some of the company’s finances. Instead, employees are only asking for the basics: “more predictable income from a set, 40 hour work week” as Tesla is notorious for asking its employees to change hours, change departments and change schedules on the fly:

In recent weeks, for example, Tesla sent workers home early from their shifts after glitches at the Fremont car plant. In the production line under the tent at the site, conveyors have broken down at the point where cars are carried forward for “battery marriage,” where workers install heavy battery packs into the Model 3 sedans and join two halves of the cars together. Inside the main building, there have been troubles with camera calibration, where employees test the in-vehicle cameras on a Model 3 to make sure they are working properly in concert with sensors to enable Tesla’s semi-autonomous-driving features.

Tesla also told some workers not to come in to work at the Gigafactory during what employees described as unexpected maintenance and cleaning.

Six additional employees said that raises and bonuses typically “don’t cover cost-of-living increases.” Other employees said that the company caps raises at about 2%, even for those with the best performance ratings by their managers. One employee recalled getting an annual raise of less than 1% and three shares of stock as a bonus after a year of “good, but not spectacular” performance.

Social media seems to be enjoying the news:

I haven’t read details yet but I surmise it is loans against your shares so you don’t need to add more selling pressure to the markets. $tsla

After Jerome Powell sent stocks into a downward spiral on Wednesday with his view that low inflation is expected to be ‘transitory’, surprising the market with its hawkish overtones, Fed Vice Chairman Richard Clarida has once again been brought in to offer a safely dovish counterpoint.

Adding his voice to a chorus of dovish Fed officials speaking on Friday, Clarida reassured markets that inflation expectations are “stable” and that there is “no need” for the Fed to change its policy stance at the moment.

On the face of it, Clarida’s comments don’t offer much new:

CLARIDA: WE’LL WEIGH `WHAT, IF ANY, FURTHER ADJUSTMENTS’ NEEDED

CLARIDA: FED FUNDS RATE NOW IN RANGE OF NEUTRAL ESTIMATES

CLARIDA SAYS FED CAN AFFORD TO BE DATA DEPENDENT

FED’S CLARIDA SAYS U.S. ECONOMY IS IN A `VERY GOOD PLACE’

With stocks already in rally mode, Clarida’s comments didn’t elicit much of a reaction.

Though at least where rate-expectations are concerned, it appears the dovish offensive is having the desired effect.

On another note, analysts pointed out that New York Fed President John Williams released a paper that sounded ‘pretty darn dovish’:

This paper uses a standard New Keynesian model to analyze the effects and implementation of various monetary policy frameworks in the presence of a low natural rate of interest and a lower bound on interest rates. Under a standard inflation-targeting approach, inflation expectations will be anchored at a level below the inflation target, which in turn exacerbates the deleterious effects of the lower bound on the economy. Two key themes emerge from our analysis. First, the central bank can eliminate this problem of a downward bias in inflation expectations by following an average-inflation targeting framework that aims for above-target inflation during periods when policy is unconstrained. Second, dynamic strategies that raise inflation expectations by keeping interest rates “lower for longer” after periods of low inflation can both anchor expectations at the target level and further reduce the effects of the lower bound on the economy. Both of those “key themes” appear to argue for low interest rates, which probably explains the bid to fixed income.

via ZeroHedge News http://bit.ly/2LkXQfp Tyler Durden

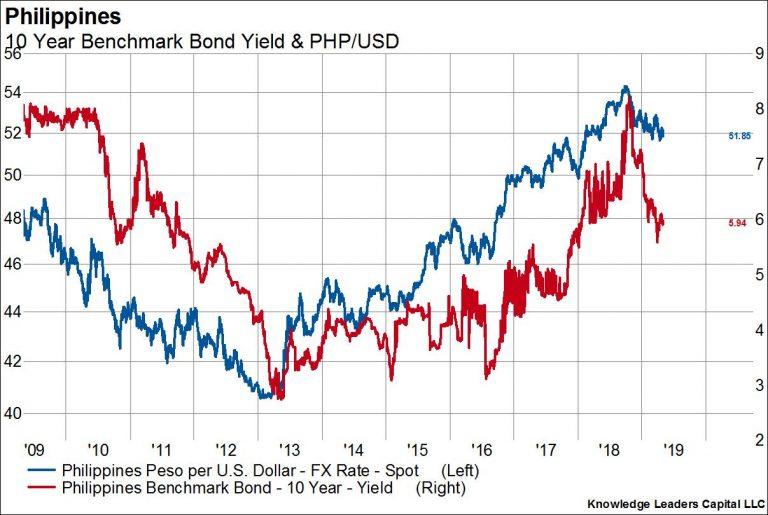

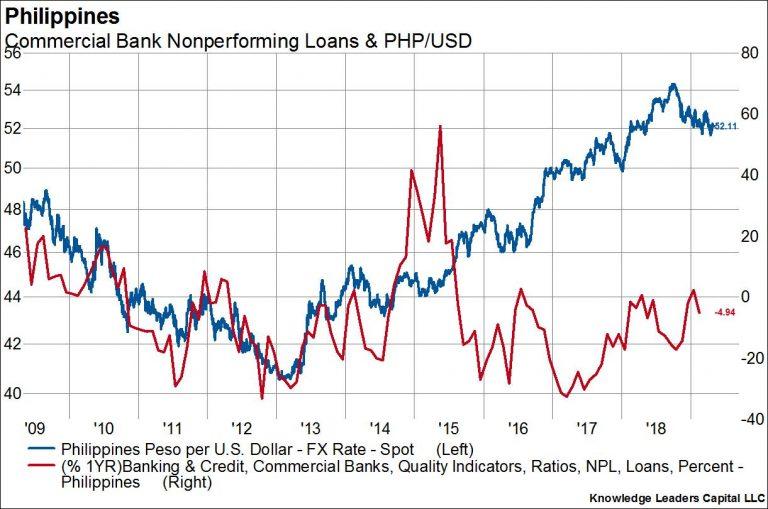

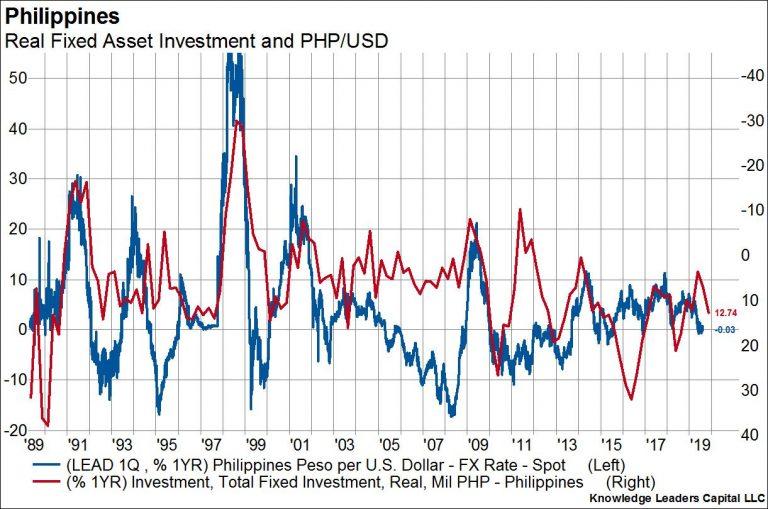

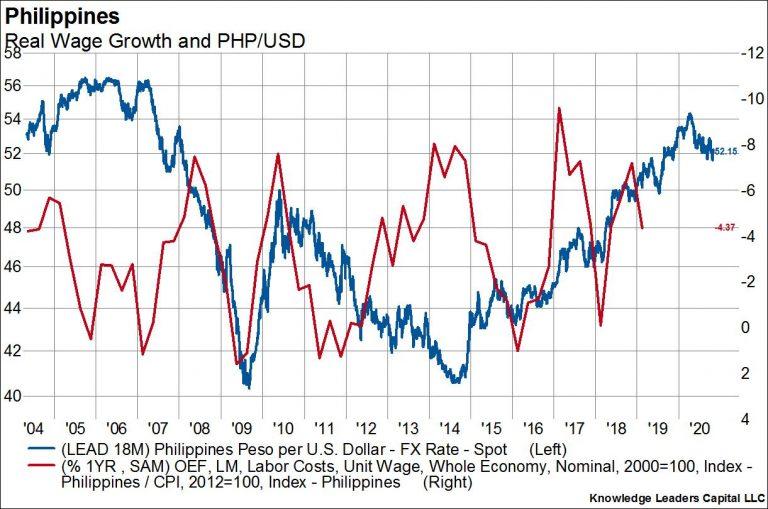

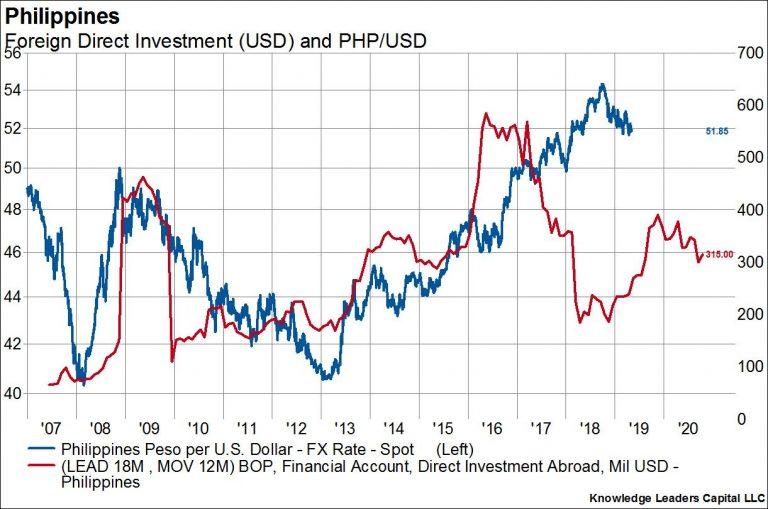

The relationship between the performance of emerging market stocks and the US dollar is one of the tightest macro relationships that exists in investing. As we can see in the first chart, the relative performance of EM stocks vs the S&P 500 is highly negatively correlated with the level of the dollar. That is, when the dollar goes up, EMs underperform US large caps and when the dollar goes down they outperform. It’s like clockwork really. But that observation is nothing new. Indeed, given the recent strength of the dollar we’ve written about it twice in the last two weeks here and here. But it’s also a good time to not just remind readers of the relationship, but also to describe the mechanics of it. That’s what I’ll do here, using the Philippines as our case study. I have no particular bias one way or the other with the Philippines, it’s just one example of many in the EM world for which dollar strength equals trouble, and vice versa.

The reason EM stocks and economies tend to struggle in the face of dollar strength is largely due to the quantity of US dollar denominated debt those countries tend to carry as a share of total debt. Why would they carry USD denominated debt instead of local currency denominated debt? The answer is lower interest rates and the ability to place larger amounts of debt. Of course, there are consequences to issuing debt in a currency a country’s central bank cannot print, one of which is that it makes the economy of the issuing country extremely procyclical. That is, economic outcomes are amplified both to the upside and to the downside. This is opposed to many developed market countries which tend to have built in mechanisms in the economy and financial markets that taper cyclicality in both directions.

For example, in the case of a developed market country, when growth and inflation are strong and rising the central bank may raise short-term rates and the bond market will experience higher longer-term rates. With a lag and all else equal, this will tend slow down the economy. When growth and inflation are low and slowing, a developed market central bank may lower short rates or take other measures to boost demand while longer-term rates will naturally fall. With a lag and all else equal, this will provide a cyclical boost to the economy.

However, when a country’s debt is denominated in a different currency all that changes. Economic booms cause the currency to strengthen and inflation to fall, which allows the central bank to lower policy rates. Because rates are falling and the currency is strengthening, interest and principle payments on foreign currency denominated debt go down, making economic agents feel richer. The government budget balance improves, often moving to surplus and bringing the current account with it. Long-term rates fall in sympathy with short rates, which lower default risks and provides further stimulus. Investment increases, wages rise, growth picks up even more and the currency continues to strengthen. It’s a self reinforcing loop of strength begetting strength.

It’s ugly when it happens in reverse. Weakness in growth causes the currency to fall, which then causes inflation to rise. Higher inflation means the central bank must tighten policy despite the economy turning down. The government surplus turns to deficit, and the need for imported capital causes the current account to turn negative too. The rising short rates and a lower currency causes foreign currency denominated debt payments to increase rapidly. There is a cash flow squeeze, and especially a shortage of US dollars with which to make debt payments. Non-performing loans rise, growth slows more, investment is cut, wages fall, and the currency weakens even more. It’s a self reinforcing loop of weakness begetting weakness. With that, let’s dig into the Philippines example.

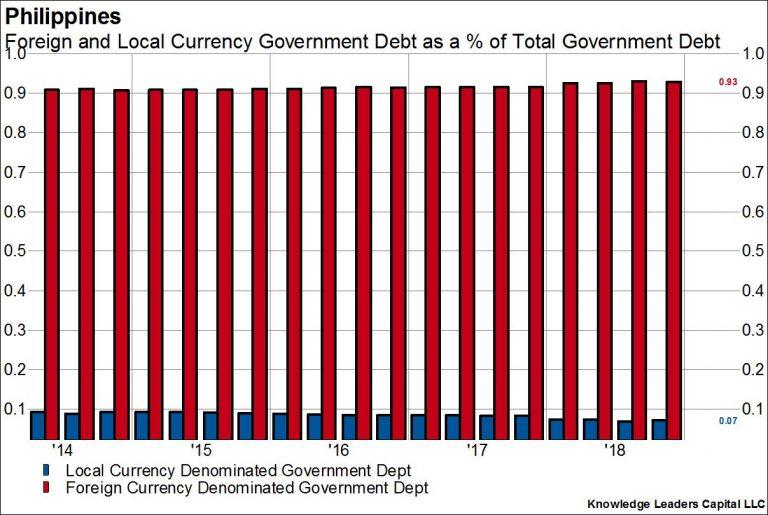

This first chart breaks down the local currency and foreign currency denominate government debt as a percent of the total. Local currency debt accounts for only 7% of total debt issuance in the Philippines. The remainder is largely USD denominated debt.

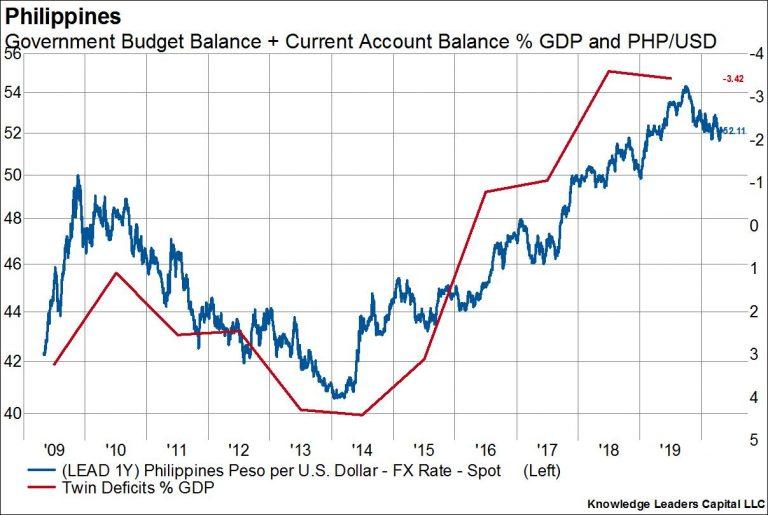

Here we show the twin deficit as a percent of GDP (right axis, inverted) overlaid on the Philippine peso per USD exchange rate (left axis). The exchange rate leads by one year. As the currency rises (blue line going down), the twin deficits improve materially, as they did from 2009-2014. When the currency falls the twin deficits deteriorate as USD debt payments become more onerous.

Currency rises and falls bring inflation with it. When the currency strengthens (blue line going down) inflation tends to fall, and vice versa.

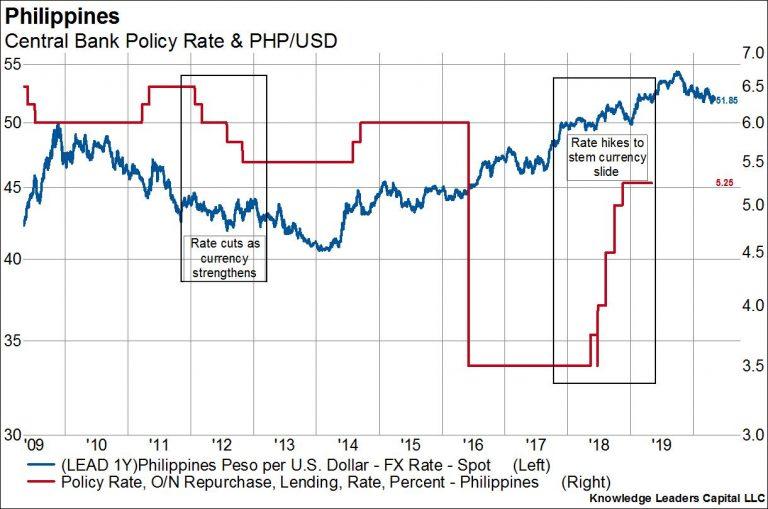

The inflationary dynamics cause the central bank to act. In the case of the Philippines, this meant rate cuts from 2011-2012 as the currency was strengthening and rate hikes in 2018 as the currency was falling precipitously. In this case, currency moves led central bank action by about a year.

Of course, economic strength caused by the rising currency pushes down long-term bond rates credit risk abates. The opposite is true when the currency weakens.

When the currency is falling, debt service gets harder. The government and companies must come up with US dollars with which to pay the lenders. The way they earn those US dollars is through exports. As the currency falls, a larger and larger portion of the US dollars the country earns through exports get used in debt repayment. In other words, US dollar liquidity tightens dramatically, which only reinforces the currency weakness. Of course, the opposite is also true when the currency is strong.

Non-performing loans are highly correlated to changes in the exchange rate. A rising local currency means debt payments are easier to meet and NPLs fall. A falling currency means debt payments are much more difficult to meet and NPLs rise.

If companies are flush because their debt obligations are lower, they are more inclined to invest, and vice versa. Dramatic currency strength or weakness feeds right into the real economy through investment.

While unemployment may or may not be affected by the currency, real wages (wage growth after inflation) do tend to be highly correlated to the currency, with a lag of 18-24 months. Higher wages obviously raise consumption and reinforce the growth while falling wages reinforce the downturn.

The cycle ends when the currency gets to such extreme levels that foreigners add to or subtract from foreign direct investment. When the currency is so low that the future ROIC of foreign direct investment is exceedingly high, dollars will start to flow back into the country. This was 2009 and 2016 in the case of the Philippines. Foreign investors were rather tepid from 2010-2013 and then again in 2018, but may be coming back in. Foreign direct investment flows lead currency moves by 12-24 months.

As readers can see, there happen to be logical, almost mechanical, relationships between EM currencies and the economy that reinforce either growth or a slowdown. In the end, it all comes back to debt, and the propensity of EMs to issue debt denominated in currency other than the one they print. The result for investors is a very predictable EM relative performance pattern that is directly tied to the US dollar.

via ZeroHedge News http://bit.ly/2DXPLav Tyler Durden

After the New York Times revealed that the FBI sent a second spy to infiltrate the Trump campaign during the 2016 US election – a ‘honeypot’ who went by the name of Azra Turk who posed as a research assistant to the first spy they sent in, Stefan Halper – the rest of the MSM has been virtually silent.

Both the Washington Post and CNN – which breathlessly reported on their peers’ anonymously-sourced anti-Trump propaganda for two years – have somehow failed to write a single article mentioning Azra Turk.

It’s been 24 hours since the New York Times reported that the FBI sent a honeypot with a fake name and job to entrap a Trump campaign advisor overseas, and the Washington Post is still refusing to report on it. Any thoughts, @ErikWemple? pic.twitter.com/Alpc8XmEWU

Rather than admit they were wrong and that Barr was right about the Obama administration sending spies overseas to entrap Trump campaign advisors, the Collusion Truthers have apparently decided to just ignore the news entirely. pic.twitter.com/GnMVqxkS5B

As the Times revealed on Thursday, the FBI operative who went by the name Azra Turk repeatedly flirted with Trump aide George Papadopoulos during their encounters as well as in email exchanges according to an October, 2018 Daily Callerreport, confirmed by the Times.

While in London in 2016, Ms. Turk exchanged emails with Mr. Papadopoulos, saying meeting him had been the “highlight of my trip,” according to messages provided by Mr. Papadopoulos.

“I am excited about what the future holds for us :),” she wrote. –New York Times

And as the Times makes clear, “the FBI sent her to London as part of the counterintelligence inquiry opened that summer” to investigate the Trump campaign.

In his House testimony, George Papadopoulos described undercover FBI informant Stefan Halper introducing him to undercover FBI informant ‘Azra Turk.’ pic.twitter.com/8jO4lK6Ldt

CNN has made mention of the report on-air, yet they haven’t written a single article mentioning “Azra Turk.”

One of the NYT reporters who wrote the FBI honeypot story was asked on CNN whether honeypot “Azra Turk” worked for the FBI.

His response: “I’m just going to leave it right now as a ‘government investigator.’ I use that wording for a reason, and I’m going to leave it at that.” pic.twitter.com/yVwezWnUWf

Meanwhile, a Russian-born academic falsely accused of being a Kremlin ‘honeypot’ operative against Mike Flynn, Svetlana Lokhova, has an interesting theory as to why the Times published the ‘2nd spy’ revalation in the first place.

2/ You might remember that McCabe picked Goldman of all people to interview him about the use of ‘Confidential Human Sources’ in Operation Crossfire Hurricane – funny that! https://t.co/87Qp4sM3Fr

4/ Goldman’s (McCabe’s) argument is that the President was a national security risk because he fired Comey. “Counterintelligence investigators had to consider whether the president’s own actions constituted a possible threat to national security.” https://t.co/1Myo2IbnDo

6/ Goldman is the go-to guy whenever the heat about the FBI spying on the campaign gets too much. Trump smokes Halper out in May 2018: pic.twitter.com/DQHP58npdR

8/ What was it that prompted Goldman (ie McCabe) to publish his latest article on the FBI Russia investigation? Answer: Barr’s criticism’s of the FBI. pic.twitter.com/SqLlwB56v6

10/ The main message is that the Russia investigation was legally predicated, started on 31 July 2016, and was conducted properly. if only it were true..

12/ The reason why spying by Halper on Gen Flynn is absent from the latest FBI propaganda piece by NYT is because it predates the official timeline by many months and was not legally predicated.

CNN law enforcement analyst and retired FBI agent James A. Gagliano opined on Twitter that perhaps the Times was helping the intelligence community get out in front of the upcoming Inspector General report on the FBI’s conduct during the 2016 election.

Unless it was foreign intelligence service supplying the “honey trap.” Papadopoulos argued *Azra Turk* had thick accent — which wouldn’t preclude her from FBI service, if US citizen. Some argue Agency employee. Surmise, absent heavy redaction, pending IG report lays this bare.

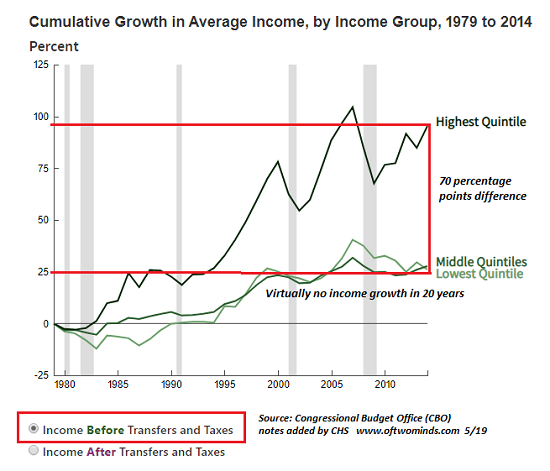

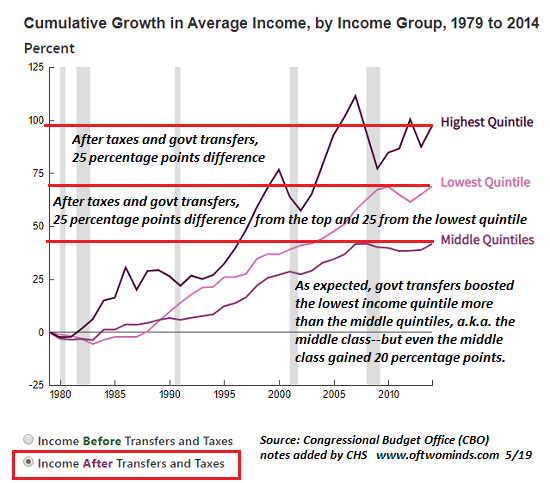

Now look at the middle quintiles–the middle class: their income has gone nowhere in the past decade.

These two charts of average incomes of U.S. households by quintile (bottom 20%, middle 60% (20%+20%+20%) and top 20%) have both good news and bad news. (Charts are from the non-partisan Congressional Budget Office — CBO).

These charts depict 1) household income before transfers (means-tested government benefits) and taxes, in other words, pre-tax earned income, income from capital gains and interest, unemployment insurance, etc., and 2) income after federal transfers and taxes.

This is a much more accurate view of household income, as this is what gets deposited in households’ accounts.

The typical chart of average incomes doesn’t include government transfers, so it under-reports the actual income of households receiving means-tested government benefits. (Note that the CBO methodology may not include all government transfers, as not all transfers are means-tested, i.e. based on income and other qualifying factors.)

The CBO reports periodically on the Distribution of Household Income and Federal Taxes, but it doesn’t generate these charts every year. (Go to Congressional Budget Office reports and scroll down to Distribution of Household Income and Federal Taxes).

Here’s the CBO’s summary of what the charts depict:

Means-tested transfers and federal taxes cause household incomes to be more evenly distributed. Those transfers and taxes:

Increased income among households in the lowest quintile by $12,000 (or more than 60 percent), on average, to $31,000.

Decreased income among households in the highest quintile by $74,000 (or more than 25 percent), on average, to $207,000.

While the gap between $31,000 and $207,000 is the core issue in rising income inequality, taxes and means-tested programs do make a big difference:a 60% gain in household income is significant.

Note that the charts depict cumulative income growth as percentages, with zero being set in 1979.

Let’s call this the good news: yes, income inequality is soaring, but America’s progressive tax system (the wealthy pay higher rates) and government programs transfer income from the top households to the bottom households–pretty much in line with the political mandate of the majority of Americans.

The bad news is the middle class has received no real income gains in the past 20 years, and they don’t qualify for many means-tested transfers. I’ve marked the charts up to highlight this.

In the income before transfers and taxes chart, the lowest and the middle quintiles are about where they were in 1999. Both gained ground in the 2005-08 housing bubble, but as with all bubbles, the effects only lasted as along as the bubble itself.

Since the top quintile’s income accelerated away from the bottom 80% in the early 1990s, there is a 70 percentage point gap between the top 20% and the bottom 80%. I’ve addressed the reasons for soaring income-wealth inequality here many times, but the key takeaway is the enormous gains reaped by the top 20% during asset bubbles, which are the consequence of financialization and central bank-fueled speculation.

In the income after transfers and taxes chart, the gap between lowest and top quintiles drops from 70 to 25 percentage points: a big reduction. After transfers, the lowest quintile income has gained steadily since the late 1980s. If we eliminate the asset bubble peaks, the gap between the top and bottom quintiles hasn’t grown that much.

Now look at the middle quintiles–the middle class: their income has gone nowhere in the past decade. Both the top and bottom quintiles have notched percentage gains in income while middle class income has stagnated.

And there you have it: financialization, central bank-fueled speculation and globalization greatly boosted the incomes of the top 20%, while government transfers have significantly increased the incomes of the bottom 20% of households.

The middle 60%, who did not benefit from the credit-fueled orgies of speculative bubbles (financialization) or globalization, and who do not qualify for many means tested transfers, have experienced near-zero income growth in the past decade of “recovery” and soaring asset bubbles.

We all know this from real-life experience in America: it pays to be either wealthy or low-income (especially if the household getting means-tested benefits also works in the black-market informal economy for cash). As for the middle 60%: you get nothing.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

via ZeroHedge News http://bit.ly/2V9BPoa Tyler Durden

Attorney General William Barr told the Senate Judiciary Panel this week that he has assembled a team at the Justice Department to probe whether the spying conducted by the FBI against the Trump campaign in 2016 was improper, reports Bloomberg.

Barr suggested that he would focus on former senior leaders at the FBI and Justice Department.

“To the extent there was overreach, what we have to be concerned about is a few people at the top getting it into their heads that they know better than the American people,” said Barr.

Barr will also review whether the infamous Steele dossier – a collection of salacious and unverified claims against Donald Trump, assembled by a former British spy and paid for by the Clinton campaign – was fabricated by the Russian government to trick the FBI and other US agencies. (Will Barr investigate whether Steele made the whole thing up for his client, Fusion GPS?)

“We now know that he was being falsely accused,” Barr said of Trump. “We have to stop using the criminal justice process as a political weapon.”

Mueller’s report didn’t say there were false accusations against Trump. It said the evidence of cooperation between the campaign and Russia “was not sufficient to support criminal charges.” Investigators were unable to get a complete picture of the activities of some relevant people, the special counsel found.

Although Barr’s review has only begun, it’s helping to fuel a narrative long embraced by Trump and some of his Republican supporters: that the Russia investigation was politically motivated and concocted from false allegations in order to spy on Trump’s campaign and ultimately undermine his presidency. –Bloomberg

As Bloomberg notes, Barr’s review could receive a boost by a Thursday New York Times article acknowledging that the FBI sent a ‘honeypot’ spy to London in 2016 to pose as a research assistant and gather intelligence from Trump foreign policy adviser George Papadopoulos over possible Trump campaign links to Russia.

The Trump re-election campaign immediately seized on the Times report as evidence that improper spying did occur. “As President Trump has said, it is high time to investigate the investigators,” said Trump campaign manager, Brad Parscale in a statement.

During Barr’s Wednesday testimony, Senator John Cornyn (R-TX) told Barr “It appears to me that the Obama administration, Justice Department and FBI decided to place their bets on Hillary Clinton and focus their efforts” when it came to investigating the Trump campaign.

Depending on what Barr finds, his review of the Russia probe could give Trump ammunition to defend himself in continuing congressional inquiries — and in a potential impeachment for obstructing justice. Barr told senators that Trump’s actions can’t be seen as obstruction if he was exercising his constitutional authority as president to put an end to an illegitimate investigation.

Barr’s efforts follow two years of work by a group of House Republicans who have been conducting dozens of interviews regarding the FBI’s and Justice Department’s conduct in the early stages of investigation of Trump and his campaign. –Bloomberg

On Thursday, Rep. Mark Meadows (R-NC) issued a criminal referral for Nellie Ohr – a former Fusion GPS contractor who passed anti-Trump research to her husband, then the #4 official at the DOJ.

On Thursday, Meadows said that Barr’s “willingness to investigate the origins of the Russia investigation is the first step in putting the questionable practices of the past behind us,” and that the AG’s “tenacity is sure to be rewarded.”

The FBI opened its counterintelligence investigation against the Trump campaign after a self-professed member of the Clinton Foundation, Joseph Mifsud, fed Papadopoulos the rumor that Russia had “dirt” on Clinton. That rumor would be coaxed out of the former Trump aide by another Clinton-connected individual – Australian diplomat Alexander Downer, who would notify authorities of Papadopoulos’ admission, officially launching the investigation.

Barr says he wants to get to the bottom of it.

His review will examine the above chain of events that set the investigation into motion, and whether any US agencies were engaged in spying on or investigating the Trump campaign before the probe was officially launched.

Barr said he’s working with FBI Director Christopher Wray “to reconstruct exactly what went down.” He said he has “people in the department helping me review the activities over the summer of 2016.”

Notably, Barr said his aides will be “working very closely” with the Justice Department’s inspector general, Michael Horowitz.

Horowitz is conducting his own investigation into the origins of the Russia investigation and whether there were abuses when the FBI obtained a secret warrant from the Foreign Intelligence Surveillance Court in October 2016 to spy on another foreign policy adviser to the campaign, Carter Page. –Bloomberg

Barr will also investigate when the DOJ and FBI knew that the Democratic Party and Clinton was Steele.

More subterfuge, or is this really happening?

via ZeroHedge News http://bit.ly/2LhoHZx Tyler Durden

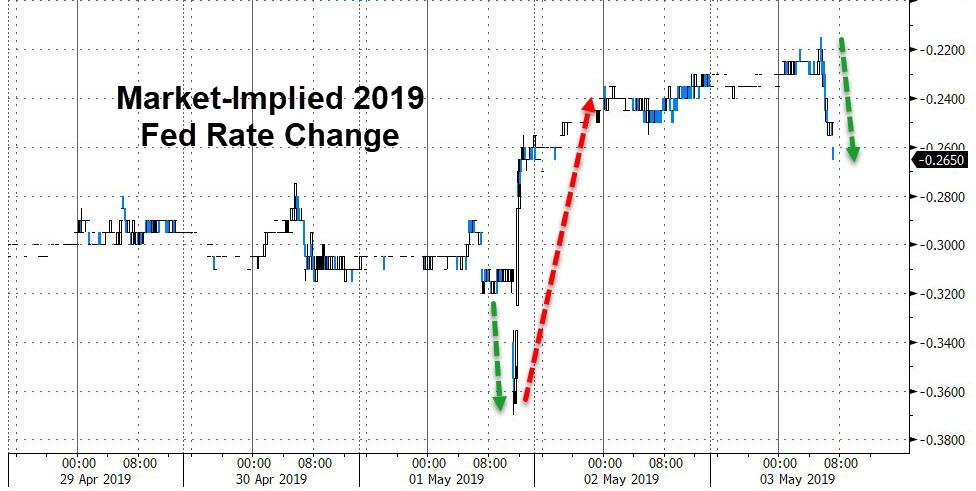

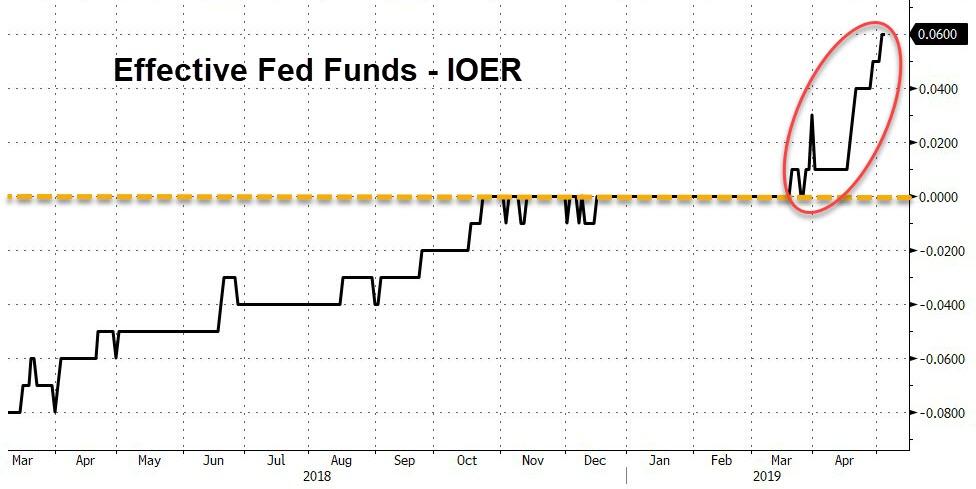

While the rest of the world is distracted by the plummeting unemployment rates and trade deal hype, a funny (well not so funny) thing happened in the short-term funding markets in the world’s reserve currency.

As we noted previously, something unexpected has been going on in overnight funding markets: ever since March 20, the Effective Fed Funds rate has been trading above the IOER. This is not supposed to happen.

As a reminder, ever since the financial crisis, in order to push the effective fed funds rate above zero at a time of trillions in excess reserves, the Fed was compelled to create a corridor system for the fed funds rate which was bound on the bottom and top by two specific rates controlled by the Federal Reserve: the “floor” for the corridor was the overnight reverse repurchase rate (ON-RRP) which usually coincides with the lower bound of the fed funds rate, while on top, the effective fed funds rate is bound by the rate the Fed pays on Excess Reserves (IOER), which served as the corridor “ceiling.”

Or at least that’s the theory. In practice, the effective FF tends to occasionally diverge from this corridor, and when it does, it prompts fears that the Fed is losing control over the most important instrument available to it: the price of money, which is set via the fed funds rate.

This week, The Fed tried to do something about it by cutting the IOER.

It has failed!

The effective fed funds rate fell to 2.41% on Thursday from 2.45%, according to New York Fed data. With the Federal Reserve’s 5bp cut to the interest on excess reserves (IOER) rate to 2.35%…

Fed effective rate on March 20 surpassed IOER for the first time since 2008, and it’s stayed above most days since.

This is a 6bps failure – worse than the 5bps spread BEFORE the Fed “tweaked”.

In other words, as one veteran funding market trader exclaimed, “it’s getting worse!”

Simply put, this is front and center a dollar liquidity shortage signal that The Fed is unable to solve… for now.

As Barclays’ Joseph Abate recently ominously concluded:

the large move also suggests that the banking sector is “nearing the steeply sloping part of the reserve demand curve” which means that “bank reserves are now significantly closer to what individual banks consider their ‘least comfortable level of reserves’ and thus banks are more willing to pay higher rates to retain these balances.”

In other words, some $1.5 trillion in excess liquidity created by the Fed is no longer enough for banks which are starting to scramble to obtain additional liquidity, which needless to say, is very troubling for a banking system which is supposedly “fortress” and “much more stable” than it was before the financial crisis. If anything, this means that even a modest liquidity draining crisis at any point in the future could have vastly more dire consequences than even the pessimists believe.

So what can the Fed do to regain control over interest rates?

According to Barclays to address the expected increase in fed funds volatility, the Fed could either end the balance sheet runoff this summer instead of waiting until September, create a standing repo facility – something which has been rumored for months – or conduct standard open market operations, injecting even more liquidity into the system.

Is Larry Kudlow right? Is The Fed preparing to cut rates, despite Powell’s dismissal of directional bias? The market still thinks so…

Note, the market is shifting dovishly today despite the big beats in jobs, suggesting something else (cough liquidity cough) is affecting policy expectations.

via ZeroHedge News http://bit.ly/2VIk135 Tyler Durden