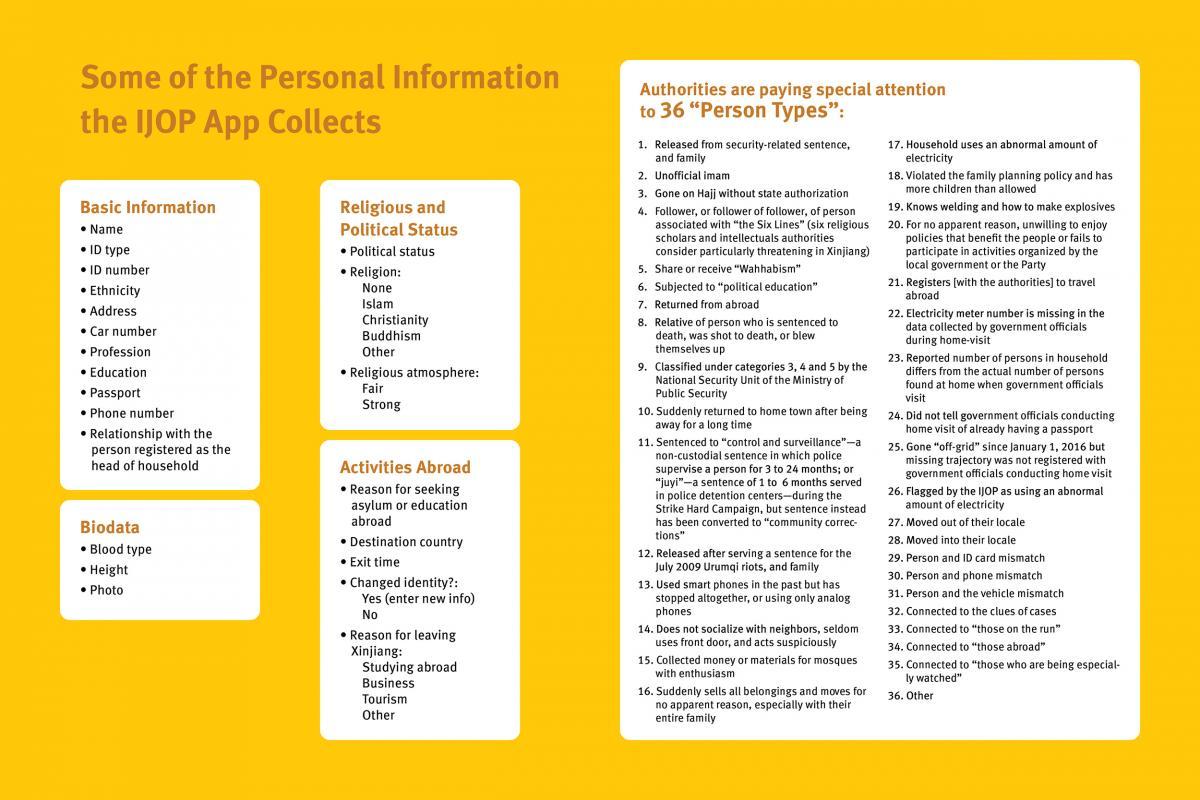

Human Rights Watch got their hands on an app used by Chinese authorities in the western Xinjiang region to surveil, track and categorize the entire local population – particularly the 13 million or so Turkic Muslims subject to heightened scrutiny, of which around one million are thought to live in ‘reeducation’ camps.

By “reverse engineering” the code in the “Integrated Joint Operations Platform” (IJOP) app, HRW was able to identify the exact criteria authorities rely on to ‘maintain social order.’ Of note, IJOP is “central to a larger ecosystem of social monitoring and control in the region,” and similar to systems being deployed throughout the entire country.

The platform targets 36 types of people for data collection, from those who have “collected money or materials for mosques with enthusiasm,” to people who stop using smartphones.

[A]uthorities are collecting massive amounts of personal information—from the color of a person’s car to their height down to the precise centimeter—and feeding it into the IJOP central system, linking that data to the person’s national identification card number. Our analysis also shows that Xinjiang authorities consider many forms of lawful, everyday, non-violent behavior—such as “not socializing with neighbors, often avoiding using the front door”—as suspicious. The app also labels the use of 51 network tools as suspicious, including many Virtual Private Networks (VPNs) and encrypted communication tools, such as WhatsApp and Viber. –Human Rights Watch

Another method of tracking is the “Four Associations”

The IJOP app suggests Xinjiang authorities track people’s personal relationships and consider broad categories of relationship problematic. One category of problematic relationships is called “Four Associations” (四关联), which the source code suggests refers to people who are “linked to the clues of cases” (关联案件线索), people “linked to those on the run” (关联在逃人员), people “linked to those abroad” (关联境外人员), and people “linked to those who are being especially watched” (关联关注人员). –HRW

*An extremely detailed look at the data collected and how the app works can be found in the actual report.

HRW notes that “Many—perhaps all—of the mass surveillance practices described in this report appear to be contrary to Chinese law, and also violate internationally guaranteed rights to privacy, the presumption of innocence, and freedom of association and movement. “Their impact on other rights, such as freedom of expression and religion, is profound,” according to the report.

Here’s what happens when ‘irregularities’ are detected:

When IJOP detects a deviation from normal parameters, such as when a person uses a phone not registered to them, or when they use more electricity than what would be considered “normal,” or when they travel to an unauthorized area without police permission, the system flags them as “micro-clues” which authorities use to gauge the level of suspicion a citizen should fall under.

IJOPalso monitors personal relationships – some of which are deemed inherently suspicious, such as relatives who have obtained new phone numbers or who maintain foreign links.

Chinese authorities justify the surveillance as a means to fight terrorism. To that end, IJOP checks for terrorist content and “violent audio-viusual content” when surveilling phones and software. It also flags “adherents of Wahhabism,” the ultra-conservative form of Islam accused of being a “source of global terrorism.”

A former Xinjiang resident told Human Rights Watch a week after he was released from arbitrary detention: “I was entering a mall, and an orange alarm went off.” The police came and took him to a police station. “I said to them, ‘I was in a detention center and you guys released me because I was innocent.’… The police told me, ‘Just don’t go to any public places.’… I said, ‘What do I do now? Just stay home?’ He said, ‘Yes, that’s better than this, right?’” –Human Rights Watch

The IJOP system was developed by a major-state owned military contractor – the China Electronics Technology Group Corporation (CETC). The app itself was developed by Hebei Far East Communication System Engineering Company (HBFEC), a company that, at the time of the app’s development, was fully owned by CETC.

CETC’s “three-dimensional portrait and integrated data doors” – special machines that are used in some of Xinjiang’s checkpoints to vacuum up people’s identifying information from their electronic devices. This is placed at the entrance to the Aq Mosque, in Urumqi, 2018.

Credit: Joanne Smith Finley

Meanwhile, under the broader “Strike Hard Campaign,“ authorities in Xinjiang are also collecting “biometrics, including DNA samples, fingerprints, iris scans, and blood types of all residents in the region ages 12 to 65,” according to the report, which adds that “the authorities require residents to give voice samples when they apply for passports.“

The Strike Hard Campaign has shown complete disregard for the rights of Turkic Muslims to be presumed innocent until proven guilty. In Xinjiang, authorities have created a system that considers individuals suspicious based on broad and dubious criteria, and then generates lists of people to be evaluated by officials for detention. Official documents state that individuals “who ought to be taken, should be taken,” suggesting the goal is to maximize the number of people they find “untrustworthy” in detention. Such people are then subjected to police interrogation without basic procedural protections. They have no right to legal counsel, and some are subjected to torture and mistreatment, for which they have no effective redress, as we have documented in our September 2018 report. The result is Chinese authorities, bolstered by technology, arbitrarily and indefinitely detaining Turkic Muslims in Xinjiang en masse for actions and behavior that are not crimes under Chinese law.

Read the entire report from Human Rights Watch here.

via ZeroHedge News http://bit.ly/2Jfw9BV Tyler Durden

“Who would be free themselves must strike the blow…

By their right arms the conquest must be wrought.”

So wrote Lord Byron of Greece’s war of independence against the Turks, though the famed British poet would ignore his own counsel and die just days after arriving in Greece to join the struggle.

Yet Byron’s advice is the wise course for the United States, and for the people of Venezuela who seek to free their country of the grip of the incompetent and dictatorial regime of Nicolas Maduro.

Let the Venezuelans decide their own destiny, as did we.

As of today, Caracas seems to be in something of a standoff.

Opposition leader Juan Guaido, recognized by the U.S. and 50 other nations as president, has failed to persuade the army to abandon Maduro.

Yet he can still muster larger crowds in the streets of Caracas to demand the ouster of Maduro than Maduro can call out to stand by his regime.

Tuesday and Wednesday, Guaido announced that the regime’s final hour was at hand. But by midweek, the army’s leaders, including the minister of defense, still stood with Maduro.

Guaido’s opportunity seems to have passed by, at least for the moment. Maduro remains in power, though his generals, weighing the odds, have apparently been negotiating in secret with Guaido.

The Trump administration has backed Guaido, only to see him fail twice now at taking power.

The White House backed the plan in February to breach Venezuela’s borders with truckloads of food and medicine, counting on the army not to use force to block the trucks.

Vice President Mike Pence traveled to the border.

But Guaido and the Americans miscalculated. The army stood by Maduro. The trucks were kept out.

This week, when Guaido called out the crowds again to bring the strongman down, the White House went all in. President Donald Trump, Pence, Secretary of State Mike Pompeo and John Bolton all tweeted support for the uprising.

But by Thursday, it was again clear that no matter what Washington had been told and anticipated, the army remained loyal to Maduro.

Frustrated, exasperated, appearing at once bellicose and impotent, Washington has now begun to bluster about military intervention.

“All options are on the table,” says Joint Chiefs of Staff Chairman Gen. Joseph Dunford. Presumably that includes the 82nd Airborne.

“While a peaceful solution is desirable, military action is possible,” said Pompeo. “If that’s what required, that’s what the United States will do.”

“All options are open,” says Bolton. “We want a peaceful transfer of power. But we are not going to see Guaido mistreated by this regime.”

Clearly, Juan Guaido is our man in Caracas.

Bolton also had strong words for Vladimir Putin:

“(T)his is our hemisphere. It’s not where the Russians should be interfering. This was a mistake on their part.”

“The brutal repression of the Venezuelan people must end, and it must end soon,” said Trump.

“People are starving. They have no food; they have no water. And this was once one of the wealthiest countries in the world.”

Yet Trump is reportedly reluctant to intervene. Let us hope that his anti-interventionist impulses guide his decisions. Venezuela’s future is not ours to decide.

This civil conflict is not our war. We have not been attacked. Not only is there no justification for U.S. military intervention, but also any arrival of U.S. troops on Venezuelan soil could turn into yet another 21st-century strategic debacle.

There could be again Americans killing and dying in a country where no vital interest was imperiled, no matter how obnoxious the regime.

There is no Tiananmen Square slaughter, no massive human rights violations going on in Venezuela to justify military intervention. Indeed, there appears to be a conscious effort on the part of Maduro to minimize casualties and bloodshed, and the consequences they could bring.

Troops are not firing indiscriminately on protestors, though rock-throwers in the streets are provoking the soldiers. Planeloads of Russian or Cuban troops are not pouring into the country.

U.S. intervention in a nation of 30 million people, with an army of scores of thousands of troops, would enable Maduro to cast himself in the role of martyr of Yankee imperialism.

Finally, time is on our side, not Maduro’s.

The Venezuelan economy, one of the richest in the hemisphere owing to the world’s largest oil resources, is now in shambles. Some 3 million people, 1 in every 10 Venezuelans, have fled the disaster that Maduro and his mentor Hugo Chavez created.

The currency is sinking to Weimar levels. Oil exports are falling. Shortages of food and medicine are spreading. Power blackouts have been reported. It is difficult to foresee any turnaround the Maduro regime can execute to revive the economy or prevent the continued exodus of its people. Most of the nations of Latin America are with us and against Maduro.

Venezuela’s situation is not sustainable. Let the fate of the Marxist Socialist regime of Nicolas Maduro be decided by the people of Venezuela.

via ZeroHedge News http://bit.ly/2GZONfx Tyler Durden

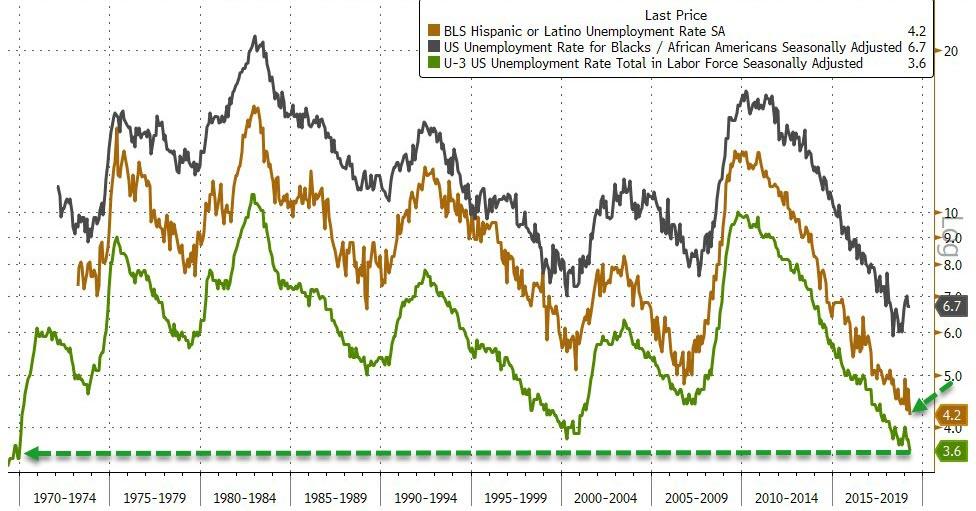

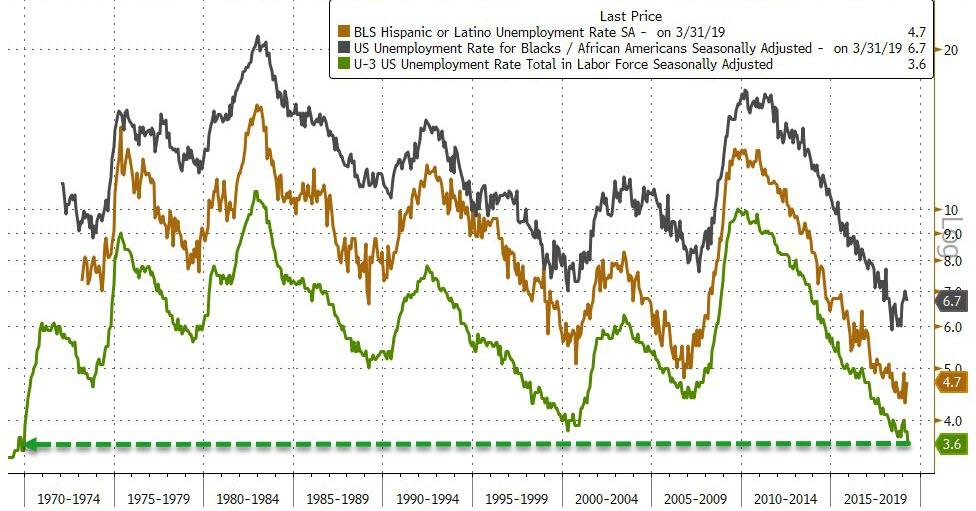

While the aggregate U-3 US unemployment rate fell to its lowest since Dec 1969 (matching the initial jobless claims records), we suspect President Trump will be more glowingly positive about another data item that dropped this morning.

Hispanic unemployment has never been lower than right now…

We look forward to Nancy Pelosi’s explanation of why this is a bad thing, or fake news (perhaps she will use the fact that black unemployment was unchanged in April?).

via ZeroHedge News http://bit.ly/2LlxcDc Tyler Durden

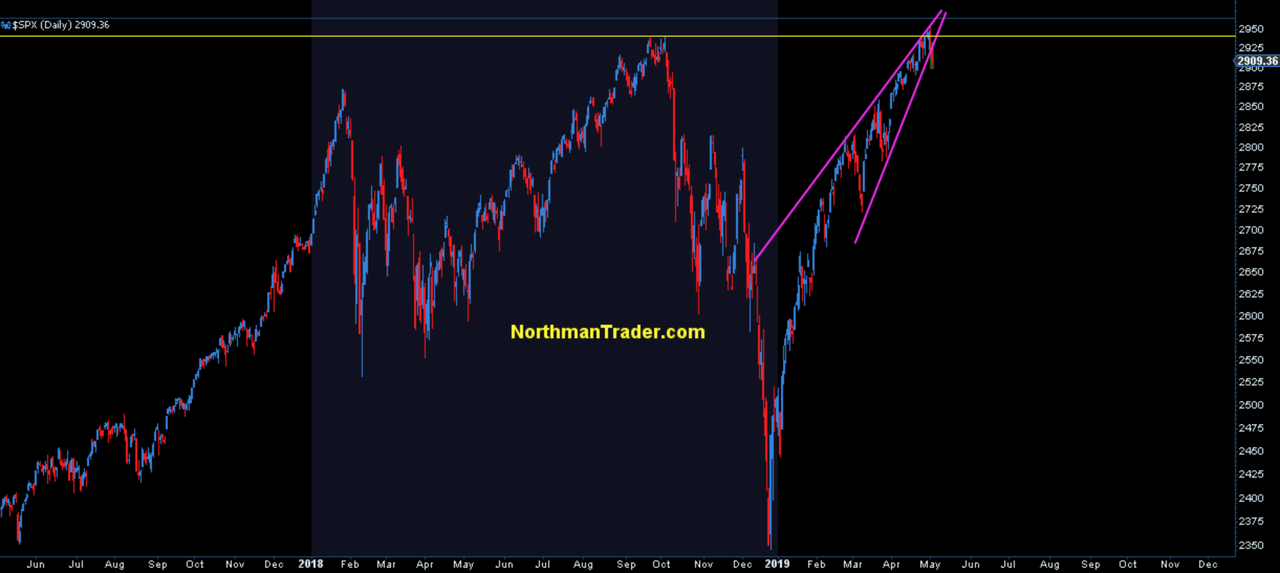

Pay attention here, we just witnessed trend breaks on some index charts and these breaks are coming at a key time and could spell more trouble to come.

Speaking of key time, who says twitter trolls are good for nothing. If anything, they sometime can serve as contrarian sentiment checks. I sensed markets were reaching a potential turning point over the last few days as I got my usual “perma bear” hate trolling on twitter. I tend to get this a lot near key market pivot points.

I got the obsessive perma bear hate labels last year in the run-up to Lying Highs. Oddly enough I didn’t get any of the perma bear hate in December when markets were plunging 20%. And ironically I didn’t get perma bear hate when I was bullish in December. But once $SPX reached 2940 and they came back.

Yes trolls on twitter are rather selective and like to distort for their own reasons. It’s silly of course as objective readers actually know me not to be a perma bear. I can’t speak to the psychology and motivation of trolls on the internet. Perhaps they secretly love me lol, after all some have been dedicating years of their lives to trolling me. Look, I don’t have time for nonsense and hate by people who don’t know me and have never even met me.

Yes, I’m posting analyses that are critical of market structures, central banks, and macro structural issues. And I stand by my criticisms. I outline my rationale with facts and figures.

But if that makes me a perma bear I must be a terrible perma bear. I mean what kind of perma bear has any sort of bullish technical outlooks? (For examples see here, here, here, here, and here).

I put out some of my analytical work publicly. When I favor the short side I outline the rationale for that. When I favor the long side I outline my rationale for that. I outline risk levels, I share some of what I see in charts. Don’t like my rationale? Don’t read it. Don’t like me? Don’t follow me. Simple.

And yes there will be times when I’m wrong or I’m early. And there are lessons on being wrong and I’ve outlined them.

Indeed my philosophy on my work:

I may not always be right, nobody is, but my analysis is always backed up with data, facts and a thought out rationale that strives to balance technicals & macro.

Above all: Keeping it real. Always.

That’s my commitment to my follows, our clients & myself.

Take April. April has not been a great month for me. Had a great January, an ok February and March, but April has been a paint drying watching exercise. So what? Nobody ever experienced a drawdown?

Let the traders who’ve never had a challenging time in markets raise their hands and step forward.

Currently I’m on the record for not liking the bullish side while recognizing the upside risk and I’ve outlined my rationale for that.

Some of the charts I’ve posted pertain to wedge patterns. I’ve outlined that they can keep going and going until something breaks, then it gets interesting. And it may be getting interesting now.

Take $NDX:

That’s a clean break. Does that mean no more new highs? Not necessarily as we saw in August/September new highs were still squeezed out, but it’s a warning sign especially since this rally remains technically uncorrected. But without larger confirmations the Combustion case is not off the table yet.

$DJIA:

Uptrend broken, 2 failed attempts to get back above the January 2018 highs. One of the lower gaps filled today. That’s now the third rejection from this price zone and risks a major topping pattern.

$WLSH:

Another wedge break in context of a notable uncorrected chart with a failure to make new highs at this stage.

$SPX:

What a pattern. Also seeing a wedge break and a failure to sustain new highs. I’ve questioned the sustainability of new highs just this weekend in Get Real.

I guess that made me perma bear worthy. Oh it’s easy to criticize and hate on twitter. Especially when you don’t put out any analytical work of your own in front of tens of thousands of people. It’s easy to distort and be selective.

And it’s easy to hate on social media from the safety and comfort of your own home. A behavior most people wouldn’t engage in in real life for there would be consequences.

Khloe Kardashian actually had a good point on that the other day:

“Social media has made many of you comfortable with disrespecting people and not getting punched in the mouth for it”.

We live in a complex diverse world. We have all to decide how we want to spend our limited time.

I have no time, desire or interest in engaging in perma narratives or hate. My focus is on quality work. That’s what motivates me. Let others be motivated by hate.

Remember:

Don’t be a perma bull or perma bear, rather just be perma smart

While overall expectations for the April payrolls number were generally in line, the “whisper” was for some weakness below the 190K consensus as a result of delayed census hiring (as discussed earlier). However, it was just not meant to be as the US job market juggernaut continues to accelerate, and moments ago the BLS reported that in April the US economy added another 263K, smashing expectations of a 190K print, and well above both the March (189K) and February (56K) prints.

The change in total nonfarm payroll employment for February was revised up from +33,000 to +56,000, and the change for March was revised down from +196,000 to +189,000. With these revisions, employment gains in February and March combined were 16,000 more than previously reported. After revisions, job gains have averaged 169,000 per month over the last 3 months.

While overall payrolls were scorching, the goldilocks picture continued, as Average hourly earnings rose “only” 0.2% from the prior month, and 3.2% from a year earlier – once again these figures were below forecasts and the same as March’s readings, however it is worth noting that wages for production and nonsupervisory workers accelerated to a 3.4% gain from 3.3%, signaling gains for lower-paid employees.

While of secondary importance, the jobless rate fell to a new 49-year low of 3.6%, though that was partly due to another drop in the size of the labor force; the household survey showed the employed fell by 103,000, the unemployed fell by 387,000, and the overall labor force shrank by 490K to 162.47 million.

Also of note, and a key point that Trump will be making shortly is that Hispanic unemployment dropped to a record low.

via ZeroHedge News http://bit.ly/2VLFbgw Tyler Durden

Iran has warned that OPEC might “collapse” due to the “unilateral actions” by some of its members, in a clear jab at Saudi Arabia.

“Iran is a member of OPEC because of its interests, and if other members of OPEC seek to threaten Iran or endanger its interests, Iran will not remain silent,” Oil Minister Bijan Zanganeh said on Thursday, as quoted by the ministry’s official news agency, SHANA.

OPEC headquarters, image via WSJ

Following the US declaring its “maximum pressure” campaign to take Iran crude exports down to zero, and ending the waiver program, Saudi Arabia and its close ally UAE pledged they will maintain appropriate supply for the markets to compensate for the shortfall — in accordance with President Trump’s demands that OPEC do more to curb rising oil prices.

Zanganeh had issued the statements warning of the oil cartel’s collapse on the occasion OPEC Secretary-General Mohammad Barkindo visit to an oil and gas exhibition in the Iranian capital. Barkindo had sought to assure the Iranians that “OPEC tries to depoliticize oil” by saying at the exhibition, “I have told my colleagues at OPEC that you must leave your passports home when coming to this organization,” according to Reuters.

Iran last month also accused Saudi Arabia and its allies of exaggerating their surplus oil capacity, to which the oil minister followed this week by saying “any threat from member states won’t go unanswered.”

Meanwhile the OPEC Secretary-General, in a further attempt to calm fears of an unraveling OPEC, told reporters, “It is impossible to eliminate Iranian oil from the market.” He added, “We have faced troubles in the OPEC in the last 60 years, but we have resolved them by unity.”

Iran oil minister Bijan Zanganeh. Image source: Iran’s SHANA

And referencing global geopolitical hot spots in which conflict and tensions have been clearly linked to the oil factor, Secretary-General Barkindo observed, “What is happening in Iran, Venezuela or Libya has an impact on all the market and the energy sector.”

Meanwhile the latest Washington The decision to end the waivers will impact recipients in different ways: Three of the eight countries that were granted the 180-day waivers back in November – Greece, Italy and Taiwan – have already reduced their Iranian oil imports to zero.

The other countries that will need to cut off imports or face serious repercussions include China, India, Turkey, Japan and South Korea. As of now, China and India are the largest importers of Iranian oil, and if they don’t swiftly act to cut down on their imports, bilateral relations with the US could suffer.

via ZeroHedge News http://bit.ly/2VF20CS Tyler Durden

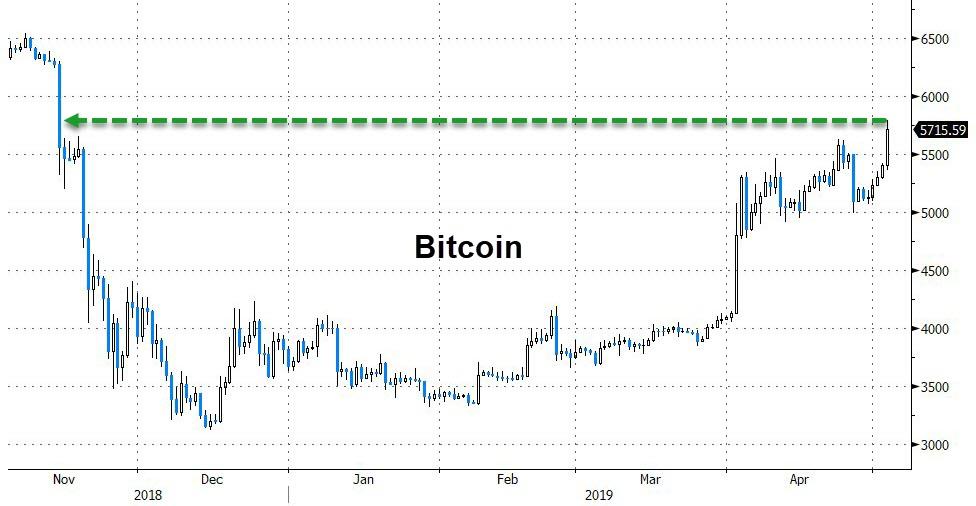

Having erased, the dip from the BitFinex scandal, Bitcoin has pushed up to almost $5800 this morning – its highest since 11/14/18 – helped by reports that social media giant Facebook is seeking investments worth $1 billion for its rumored cryptocurrencystablecoin, according to the Wall Street Journal.

As CoinTelegraph.com reports, citing people familiar with the plans, WSJ revealed Facebook was currently talking to major payment networks Visa and MasterCard about potential support, along with payment processor First Data Corp.

The cryptocurrency project, dubbed “FB Coin,” has fuelled rumors for around a year that Facebook wants to provide in-house payments to users.

As more information trickles down to the outside, it appears various options are under consideration by executives, including payments via a user’s Facebook profile.

“Facebook is also talking to e-commerce companies and apps about accepting the coin, and would seek smaller financial investments from those partners, one of the people said,” the WSJ added.

As Cointelegraph reported, interest in a fiat-centric FB Coin has already reportedly come from within cryptocurrency circles, specifically in the form of VC investment mogul Tim Draper.

Last month, plans surfaced that Draper, who is a well-known bitcoin (BTC) bull and supporter of altcoin Tezos (XTZ), would meet with Facebook to discuss investment options.

According to the WSJ sources, however, the huge fiat backing is further deliberately designed to remove perceived doubts about FB Coin versus bitcoin and other cryptocurrencies. Volatility, they said, should be avoided in order to boost uptake.

via ZeroHedge News http://bit.ly/2WnHRy7 Tyler Durden

After establishing its Vision Fund as the world’s preeminent marginal investor in Silicon Valley’s most overhyped (and overvalued) startups, SoftBank, its CEO Masayoshi Son and its Middle Eastern backers have settled on a time-tested strategy for locking in profits even if the startups they’ve backed never realize profits, as some have warned might be the case.

That strategy? Dumping their shares on unsuspecting retail investors.

That’s right. According to the Wall Street Journal, in what would be an unprecedented move for a venture fund with an international reach, SoftBank is reportedly considering an IPO for its $100 billion Vision Fund. The Japanese telecoms conglomerate with a massive VC arm is also reportedly in talks with the Sultanate of Oman to secure an additional investment in its existing fund. Masayoshi Son also recently visited China to discuss potential investments in the Vision Fund worth several billion dollars.

And, if the offering goes through, the firm is already drawing up plans to launch a second ‘Vision Fund’ after the original allocated all of its capital in private investment deals involving Uber, WeWork and others in under two years.

SoftBank is considering audacious fundraising plans, including a public offering of its $100 billion investment fund and the launch of a second fund of at least that size, as it looks to seize on an exploding startup scene, people familiar with the matter said.

More immediately, SoftBank is negotiating with the sultanate of Oman for an investment of several billion dollars in its existing $100 billion Vision Fund, which raised nearly all its cash from Saudi Arabia and Abu Dhabi, the people said.

The fund’s staff is hustling to keep up with the frantic pace of deal making by SoftBank founder and Chief Executive Masayoshi Son, who has invested nearly all the money that the Vision Fund took in just two years ago.

Highlighting the need for new funds: Mr. Son recently returned from China, where he negotiated informal deals worth several billion dollars that the Vision Fund doesn’t yet have, one of the people said.

It’s difficult to imagine that the IPO would be anything other than a desperate exit strategy for SoftBank, considering recent reports that the firm’s backers in Saudi Arabia and Abu Dhabi have reportedly expressed reservations about Masayoshi Son’s investment strategy, complaining that he had made reckless investments at valuations that many felt were too high. And Uber, one of the fund’s most visible investments, has already cut its planned valuation at IPO twice.

The news comes just weeks after WSJ reported that Masayoshi Son lost $130 million of his personal fortune after buying into bitcoin at the top of the 2017 bubble, then selling while prices were crashing.

But in a sign that some will interpret a Vision Fund as a sign that the rally is only just getting started, let’s look at the recent trend: Tesla shares climbed after the company returned to the market to plug a massive hole in its balance sheet (which will still leave it incapable of investing more in capex), and Beyond Meat, a company with no profits to speak of, soared 150% during its trading debut.

In other words: If SoftBank wins regulatory approval for the deal, retail traders will likely be more than happy to supply an escape hatch.

via ZeroHedge News http://bit.ly/2J2QZW7 Tyler Durden

Global stocks were higher, with European markets and US equity futures a sea of green on the last day of the week, as China and Japan remained closed for holidays, as world stocks battled to avoid their first weekly fall in six weeks on Friday while investors waited to see if April US jobs data would give the Federal Reserve another reason to dismiss rate cut calls.

While Asian stocks were broadly flat, mostly due to subdued volumes as China and Japan remain closed, and the MSCI Index of Asian stocks closing just 0.02% higher, it appears that Asia once again was instrumental in pushing US futures higher as the Emini rebounded as Hong Kong shares rose 0.4 percent, while Australia gained 0.1%, while Korea’s KOSPI dipped 0.5 percent.

There was more action in Europe, whose bourses were higher across the board as earnings from banks HSBC and Societe Generale cheered traders and encouraging Adidas profits sent the German sportswear firm’s shares surging 7% to a record high.

On Thursday, the S&P dropped on concerns about the US-China trade deal, giving up an initial attempt to regain their record highs and closed in the red, weighed down by energy shares. Oil prices had plunged again after U.S. crude production output set a new record, though the losses were capped by the intensifying political crisis in Venezuela and the stopping of Iranian oil sanction waivers by Washington.

Yet while stocks were broadly higher, bond and commodity markets remained firmly on the backfoot with most benchmark government bond yields up and Brent sliding back toward $70 a barrel again for what will be its worst week in over two months.

Quoted by Reuters, UBP strategist Koon Chow said it all pointed to a little bit of the steam coming out of the markets after a flying start to the year: “For the last four months it has been the unwinding the extreme pessimism that had built up (last year)” he said, referring to trade war nerves and the slowdown in many of the world’s largest economies. “So here we are now in search of the next big thing, and I think today, and for the last few weeks, it is a views and portfolio repositioning exercise.”

Some of the overnight bullishness was attributed to trader expectations for today’s jobs report. The only problem is that nobody knows if it’s better for the report to show bad or good news: since the recent surge in markets has been due to a dovish Fed, any unexpected overheating in job or wage gains, will likely further pressure risk. April payrolls, due at 830am ET, are forecast to show 185,000 net new jobs were added in April and the unemployment rate at a steady 3.8%. Average hourly earnings are expected to rise 3.3%, just shy of the post-crisis highs.

Over in the UK, the latest local council elections results show Labour Party councillors dropped by 53 councillors to 601 and Conservative party councillors dropped by 117 to 512 in England. Instead, voters turned to alternative parties which saw a significant swell in support for the Liberal Democrats, the Greens and independent candidates.

In the currency markets, the dollar strengthened, and the BBDXY rose to session highs ahead of the payrolls report although it may dip soon as an army of Fed doves hits the microphones: there are no less than eight Federal Reserve policymakers due to speak on Friday. The euro stayed lower even as inflation data beat estimates. The pound led G-10 losses but was still set for its biggest weekly gain in almost two months amid optimism a compromise Brexit deal may be struck next week. Australian and New Zealand dollars both fell as speculators wagered both countries could see interest cuts next week. The Aussie slipped below psychological support of $0.7000 overnight to the lowest since early January while the kiwi dollar drifted closer to a recent five-month trough of $0.6581. The weakness in the antipodean currencies also came as the U.S. dollar gained on remarks by U.S. Federal Reserve Chair Jerome Powell earlier this week that a recent weakness in inflation owed to “transitory” factors. That led traders to start paring expectations for a Fed rate cut. Futures now imply about a 49 percent probability of an easing at year-end, down from 61 percent late on Wednesday, according to CME Group’s FedWatch program.

In commodities, West Texas crude steadied, but was in the red in early London trade down 0.3% at $61.65 a barrel, while Brent slipped 0.5 percent to $70.42. Copper fluctuated, still on course for the biggest weekly drop since August. Bitcoin climbed to its highest level since November, advancing toward $6,000.

Other economic releases include wholesale inventories, Markit services PMI. American Tower, Dominion Energy are among companies reporting earnings. There is an avalanche of Fed speakers today including Williams, Bowman, Bullard, Daly, Kaplan and Mester.

Market Snapshot

S&P 500 futures up 0.4% to 2,928.00

STOXX Europe 600 up 0.3% to 390.15

MXAP up 0.02% to 162.61

MXAPJ up 0.02% to 540.03

Nikkei down 0.2% to 22,258.73

Topix down 0.2% to 1,617.93

Hang Seng Index up 0.5% to 30,081.55

Shanghai Composite up 0.5% to 3,078.34

Sensex up 0.4% to 39,153.64

Australia S&P/ASX 200 down 0.04% to 6,335.80

Kospi down 0.7% to 2,196.32

German 10Y yield rose 1.3 bps to 0.043%

Euro down 0.07% to $1.1164

Brent Futures down 1% to $70.06/bbl

Italian 10Y yield fell 0.3 bps to 2.181%

Spanish 10Y yield rose 0.2 bps to 0.999%

Brent Futures down 1% to $70.06/bbl

Gold spot down 0.05% to $1,270.07

U.S. Dollar Index up 0.06% to 97.89

Top Headline News from Bloomberg

Temporary federal government hiring for the U.S. Census Bureau’s 2020 count may give nonfarm payrolls a boost starting with the April jobs report due Friday, economists say

A Brexit backlash hit both main parties in U.K. local elections, with smaller parties gaining seats. The news increases hopes that a compromise Brexit deal could be struck next week as both Labour and the Conservatives attempt to bring an end to the divisive issue

ECB’s Weidmann sees signs of pickup in Germany economy, with the current weak phase only “temporary”. Urges the ECB to press ahead with its exit from unconventional monetary policy if inflation allows

ECB’s Rehn also sees evidence of a recovery, but warns not to ‘jump the gun’ on first green shoots

Oil tumbled as much as 4% in New York, lowest levels in a month, as American crude inventories hit highest level in two years and Russia missed targets for production cuts in April

PIMCO Chief U.S. Economist Tiffany Wilding says many on the Fed may favor preemptively cutting rates if they see risks as to the downside, even if a recession is not expected

European Commission president Jean-Claude Juncker is reported to have said that Bundesbank chief Jens Weidmann is a suitable candidate to take over from Mario Draghi as ECB president

Global Times said in analysis that many observers are wondering if China-U.S. trade talks have hit an impasse as there were few details revealed after the latest meetings on Wednesday

Billionaire investor Warren Buffett told CNBC in an interview that Berkshire Hathaway Inc. has been buying Amazon.com Inc. shares and the purchases will show up in a regulatory filing later this month

Inflation in the euro area accelerated more than expected and a core measure jumped the most in nearly a year, capping a week of encouraging data for the European Central Bank

Donald Trump doesn’t want anyone to see his tax returns. Not the public. Not Congress. But at least one group has peered into the carefully guarded trove and could provide some insight — a team from Deutsche Bank AG

Asian equity markets were mixed with the region cautious ahead of the looming US NFP data and after losses on Wall St where the fallout from the FOMC disappointment persisted and the energy sector underperformed on weaker oil prices. ASX 200 (U/C) swung between gains and losses with notable weakness seen in energy names after WTI crude declined by more than 3% and with financials subdued after Macquarie’s full-year results which improved from the prior year although it flagged a decline for FY20. KOSPI (-0.7%) and Hang Seng (+0.4%%) were negative with South Korea heavily focused on earnings and with risk appetite in Hong Kong sapped by poor GDP data which showed its economy grew at the slowest pace in nearly a decade. However, the Hang Seng is well off intraday lows as trade related news provided a glimmer of optimism with Chinese Foreign Minister Wang to travel to the US on Tuesday and is expected to close the trade deal next week, while US Commerce Secretary Ross suggested they are in the end-game of trade negotiations. As a reminder, mainland China and Japan remained closed for holidays.

Top Asian News

Chip Makers Lead Asia Gains on Hope of Better Earnings, Orders

Foreign Fund Inflows Into Indonesian Bonds Surpass 2018 Level

Major European indices have been gradually grinding higher throughout the session [Euro Stoxx 50 +0.3%], diverging from the cautious trade seen overnight where sentiment was somewhat deterred by the upcoming US jobs report and mixed US-China trade reports. There is no real standout European bourse this morning with gains relatively broad based; although, the SMI (+0.2%) while positive is underperforming its peers, with the index weighed on by Swiss Re (-2.6%) after the Co. posted a miss on Q1 net. In a similar fashion sectors are predominantly in the green with the exception of the Technology sector which is weighed on by heavyweight Sap (-0.4%) in the red following on from reports yesterday that up to 50k companies which are using the Co’s software are at risk of a security breach; the Co. state that guidance on resolving these issues was published in both 2009 and 2013. Other notable movers this morning include banking giant HSBC (+2.4%) who are firmer post-earnings where they beat on both Q1 revenue and pre-tax profit. Separately, but also boosted by earnings are Adidas (+6.1%) with the Co. also topping the Dax (+0.3%) after confirming FY guidance and reporting strong net income & operating figures. Elsewhere, and at the other end of the Stoxx 600 are Intu Properties (-6.4%), after stating that they see FY19 LFL retail income falling by 4-6% and forecast the remainder of the year as being challenging.

Top European News

Norway’s Wealth Fund Surges $84 Billion After Snapping Up Stocks

Merkel Weighs German Carbon Prices to Speed Pollution Cuts

U.K. Economy Seen Stagnating in April as Services Eek Out Growth

Societe Generale Shares Gain on Surprise Strong Capital Beat

In FX, the Greenback remains on a firmer footing ahead of the monthly BLS jobs report, and the index has just notched a new post-FOMC peak at 97.971 amidst expectations that payrolls will post another solid gain, with average earnings forecast to tick up in m/m and y/y terms. The DXY has eclipsed Fib resistance at 97.881 in the process and is now eyeing another retracement level just above 98.000 at 98.059.

CHF/EUR/GBP/JPY/AUD – All weaker, albeit marginally vs the Usd, with the Franc straddling 1.0200 after a further deterioration in Swiss consumer sentiment and in line/steady y/y CPI, but still well shy of the SNB’s 2% target. Meanwhile, the single currency is grinding down further having relinquished the 1.1200 handle on Thursday with Fibs marking out support and resistance at 1.1147 and 1.1186 respectively, and hefty option expiry interest also likely to influence trade/direction ahead of NFP if not the NY cut. Note, firmer than forecast Eurozone inflation has been largely shrugged off given national numbers indicating an upside bias vs consensus. Similarly, Cable failed to glean and positive momentum from confirmation that the UK services sector joined its construction counterpart back into expansion from contraction, with the pair having dipped below the 1.3000 level to circa 1.2990 (just shy of the 100DMA at 1.2983) while Usd/Jpy is pivoting 111.50 and the 30 DMA (111.47) in advance of the aforementioned US labour data and a 111.70 Fib. Last, but by no means least, the Aussie is trying to keep sight of the psychological 0.7000 mark following extended losses to a fractional 2019 low (0.6985) where decent expiry interest (877 mn) resides, but still wary about a potential RBA rate cut next week.

CAD/NZD – Marginal G10 outperformers, or at least holding their own as the Loonie meanders between 1.3458-75 and Kiwi hovers above 0.6600, albeit also conscious that the RBNZ could ease policy at the May meet.

EM – The Lira remains in the spotlight and under pressure in wake of weaker than anticipated Turkish CPI on perceived less hawkish CBRT policy implications, with Usd/Try at the upper end of 5.5800-9595 trading parameters.

In commodities, Brent (-0.5%) and WTI (-0.2%) prices are subdued this morning, as the general uptick in risk appetite this morning has not been able to outweigh the bearish pressure from the stronger dollar. WTI prices are still relatively secure above the USD 61/bbl level, currently trading around the USD 61.40 figure; however, the session lows for Brent did briefly breach the USD 70/bbl level. UBS note that of central concern for oil on the upside are the recent reports that US-China trade talks may have reached an impasse, ahead of next week’s negotiations in Washington. News flow this morning includes sources commenting that Saudi Arabia’s production may increase in June but will still be below the 10.3mln BPD quota under the OPEC+ agreement. For reference, surveys indicate that Saudi Arabia’s output as of April 30th is 9.85mln BPD. Gold (U/C) is relatively lacklustre this morning with the yellow metal torn between the firmer dollar, mixed US-China trade reports and the general improvement in risk sentiment; as such the metal is left pivoting the USD 1270/oz level. Elsewhere, copper is still suffering from the absence of China, although industrial metals in general have strengthened somewhat with some attributing this to recent comments from Tesla, stating that they foresee shortages of minerals which are used in electric vehicles.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. 190,000, prior 196,000

Unemployment Rate, est. 3.8%, prior 3.8%

Average Hourly Earnings MoM, est. 0.3%, prior 0.1%

Average Hourly Earnings YoY, est. 3.3%, prior 3.2%

Underemployment Rate, prior 7.3%

Wholesale Inventories MoM, est. 0.2%, prior 0.2%; Retail Inventories MoM, est. 0.1%, prior 0.3%

9:45am: Markit US Services PMI, est. 52.9, prior 52.9; Markit US Composite PMI, prior 52.8

10am: ISM Non-Manufacturing Index, est. 57, prior 56.1

10:15am: Fed’s Evans Speaks at NABE International Forum in Stockholm

11:30am: Fed’s Clarida Speaks at Hoover Institute Policy Conference

1:45pm: Fed’s Williams Speaks at Hoover Institute Policy Conference

3pm: Fed’s Bowman Speaks at Hoover Institute Policy Conference

7:45pm: Fed’s Bullard, Daly, Kaplan and Mester Speak at Hoover Event

DB’s Craig Nicol concludes the overnight wrap

The last 24 hours was always going to be a little bit of a no man’s land for markets given that it fell in-between the Fed meeting and a payrolls Friday. That said, the Fed-inspired plunge for equities continued, albeit at a much more moderate pace, with the S&P 500 ending -0.21% lower by the time the closing bell rung last night. That was admittedly 0.59% off the intraday lows, with the NASDAQ also bouncing off its low of -0.91% to end the session only -0.16% lower. The DOW fell -0.46%, dragged lower by poor earnings from Dow Chemicals, whose management said they see “discrete” headwinds in the second quarter, and by Caterpillar after investors were unimpressed with its latest dividend announcement.

In Europe we had the PMIs to focus on – more on that below – however equities were playing catch up to the US moves from the day prior with the STOXX 600 ending -0.58%. Cash HY spreads widened by +4bps in Europe but tightened -1bp in the US. It was at least a bit more exciting in the rates market where 2y and 10y Treasury yields rose +4.0bps and +4.1bps respectively, and thus extending Wednesday’s move, while Bunds ended +1.7bps. Those moves were completely driven by real yields, as inflation expectations fell notably. That move was in turn driven by lower oil prices, as investors noted rising US stockpiles unconfirmed reports about increases to Russian and Saudi output. WTI ended -2.81% lower. The USD rose +0.15% which weighed on EM FX once again, as a basket of currencies retreated -0.40%. Oil exporting countries saw bigger falls, led by the Russian Ruble’s -1.24% retreat. In other commodities, Gold and Silver fell -0.48% and -0.32% to fresh year-to-date lows.

So before we can finally take a breather from what has felt like a fairly non-stop week, there’s the small matter of getting through this US employment report in about seven hours’ time. Our US economists expect nonfarm payrolls to slow to 160k versus 196k in March, while the consensus is for 190k. Our colleagues do note though that their forecast should be enough to keep the unemployment rate at 3.8%, while for earnings they forecast +0.2% mom, a tenth below what the market expects. That should still be enough to see the annual rate nudge up to +3.3% yoy though and just shy of its post-recession high.

It’s worth noting that as well as payrolls today we’ve got a number of Fed speakers due up this afternoon. Evans, speaking at 3.15pm BST, should be interesting given that Monday’s inflation data nudged closer to the 1.5% level that Evans said would make him “extremely nervous”. As you’ll see in the day ahead at the end we’ve also got Clarida, Williams, and Bowman speaking at the Hoover Institution Conference this afternoon.

This morning in Asia there isn’t a huge amount to report with markets fairly directionless. Thin trading volumes are still a factor however with Japan and China closed. The Hang Seng (-0.02%) is little changed while the Kospi (-0.69%) has struggled, in contrast to the ASX which is up +0.18%.

In other news, yesterday Stephen Moore withdraw his name from consideration for a Fed governorship, though he gave an interview 2 hours before that decision in which he said he was still “all in.” In China trade talks reportedly concluded positively between the US and China, though subsequent reporting in the Chinese press suggested that officials “may have hit an impasse” which seemed to be the trigger behind the mid-afternoon plunge for equities. The details were less negative than the headline suggested, but the story could nevertheless be a signal from Chinese officials about their willingness to walk away from talks if a satisfactory deal isn’t soon completed.

Meanwhile, the CBO released its latest budget forecasts which turned out to be uneventful. There were no major changes to the forecast for deficits to average -4.3% of GDP over the next 10 years, taking the public debt from its current 78% of GDP level to 92%. Roughly half of that rise is due to the CBO’s projections for higher interest rates, which are above DB’s and consensus forecasts, which suggests the rise will be less severe, but on the other hand the forecasts only include ‘current law’ so there is plenty of scope for things to get worse as tax cuts are renewed and spending caps are lifted moving forward.

Here in the UK it was the turn of the BoE to take the spotlight. As expected there were no policy surprises and the message was fairly neutral at best with growth projections revised up and inflation forecasts down. Our UK economists summarised that the overall communication from the BoE yesterday confirmed that policy remains almost exclusively conditional on a Brexit resolution. And with the ongoing tension between the Bank’s inflation projections and market pricing, Governor Carney reiterated the need for more hikes (than currently priced in) to keep inflation in check. Indeed, Carney’s push back against more dovish pricing at the front end of the UK rate curve was consistent with the MPC’s hawkish bias for gradual and limited tightening over the Bank’s forecast horizon. And given that our colleagues’ base case is for a Brexit resolution in May, they retain their call for an August rate hike. Sterling faded from the highs yesterday to close down -0.14% while the Gilt curve was a touch weaker with 10y yields ending +3.5bps.

As for the details of those PMIs in Europe, the manufacturing reading for the Euro Area was revised up 0.1pts to 47.9. That included better than expected readings for Italy (49.1 vs. 47.8 expected) and Spain (51.8 vs. 51.2 expected) and a +0.4pt upward revision for France to 50.0. The winner? Greece at 56.6 and the highest since 2000. Imagine thinking that four years ago. More significant for Europe, Germany was revised down 0.1pts to 44.4 which puts the increase over March at just +0.3pts. However, the good news was that new orders were up +1.4pts. As our economists noted, the improvement in the southern periphery is welcome and confirms that German contagion is more limited to its cyclical neighbours with falls in the manufacturing PMIs for Switzerland, Sweden, and the Czech Republic, possibly as collateral damage from Germany’s slide. The services readings are due on Monday so that’s the next focal point. Despite some green shoots of optimism then, the reality is that the manufacturing reading for the Euro Area is still the second lowest level in the current cycle and well into contractionary territory.

Over in the US, jobless claims stayed steady at 230k and the final print for March core capital goods orders were revised up +0.2pp to 0% mom. Factory orders rose +1.9% mom, better than the +1.6% expected, and the prior month was revised higher as well. This is likely to present upside risks for the first revision to Q1 US GDP growth later this month. Separately, Q1 productivity rose by +3.6% qoq, the fastest pace since 2014. On a yoy basis, that was the fastest pace since the financial crisis. Our US economists have published research previously showing that productivity tends to lag wage growth, as companies respond to wage pressures by finding new ways to boost output per hour. That underlies DB’s house view for US growth to remain strong over the next several quarters and years, as opposed to the consensus which envisions a gradual slowing.

Finally, the day ahead is unsurprisingly headlined by the April employment report in the US this afternoon, however prior to that we’ll get April CPI data out of Turkey this morning which will be worth a close eye, followed by the April services and composite PMIs in the UK and the April CPI report for the Euro Area. The core reading is expected to rise two-tenths to +1.0% yoy. The other data due in the US today includes the March advance goods trade balance, March wholesale inventories, the April services and composite PMIs and April ISM non-manufacturing. As mentioned earlier the other potentially interesting event to watch is the raft of Fedspeak this afternoon. It starts with Evans who is speaking at an event in Stockholm at 3.15pm BST, before Clarida (4.30pm BST), Williams (6.45pm BST) and Bowman (8pm BST) speak at the Hoover Institute Policy Conference. The Bundesbank’s Weidmann is also due to speak this morning.

via ZeroHedge News http://bit.ly/2PMVJiT Tyler Durden

More cracks are forming in the White House’s carefully-constructed narrative that trade talks could be headed for a resolution next Friday following the 11th round of talks between US and Chinese trade negotiations in Washington. After Beijing floated a report on Thursday suggesting that talks had been an impasse, sending stocks hurtling toward session lows early Thursday afternoon, they have followed up on Friday with a statement casting doubt on Washington’s assertion that a deal is imminent.

According to the South China Morning Post, the Communist Party has published what appears to be a warning to Washington and the investing public. The Communist Party warned in a post on Taoran Notes, a venue for publishing trade-talk updates for the Chinese public, that reports about a deal being reached next Friday were part of a pressure campaign to get Beijing to acquiesce to a deal, adding that this “smoke and mirrors” ploy wouldn’t work.

“Taoran Notes, a social media account used by Beijing to release trade talk information and to manage domestic expectations, said the hints from the US side that next week’s 11th round of talks are a deadline is merely a trick “to increase tensions and generate pressure on the other side.”

“It’s the same tactic as the US threatening to raise tariffs, it is merely smoke and mirrors to exert extreme pressure [on China],” the post said. “You don’t have to take it seriously.”

Of even greater concern for stock market bulls: Beijing warned that “an unhappy departure” is still possible if the US fails to compromise.

It warned that there is still a possibility that the two sides will end up in “an unhappy departure” if one side wants the other to make compromises and neglects “fairness in negotiation.”

Exact details of the talks are shrouded in secrecy, although Beijing and Washington have hailed “progress” after every round of talks over the last five months, with Mnuchin calling this week’s talks in Beijing “productive.”

Which is surprising because over the past week, media reports have suggested that the US has done nothing but compromise. Not only have Mnuchin, Lighthizer & Co. reportedly backed down on US demands for a stable enforcement mechanism and – even more embarrassingly – demands that China promise to end its cyberespionage campaign, and the US Chamber of Commerce said Thursday that a final deal could fall short on addressing state industrial subsidies – another one of the Trump Administration’s key demands.

During a speech at the BRI Forum last week, President Xi spoke about promises to increase agricultural purchases, increase market access for foreign companies and prohibit forced technology transfers. Though Xi didn’t explicitly mention talks with the US, it’s looking increasingly likely that these concessions represent a ‘final offer’ from Beijing.

Whether the White House decides to take it, or leave it, next week could decide whether a deal is reached, or China walks away.

via ZeroHedge News http://bit.ly/2IZc6IK Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}