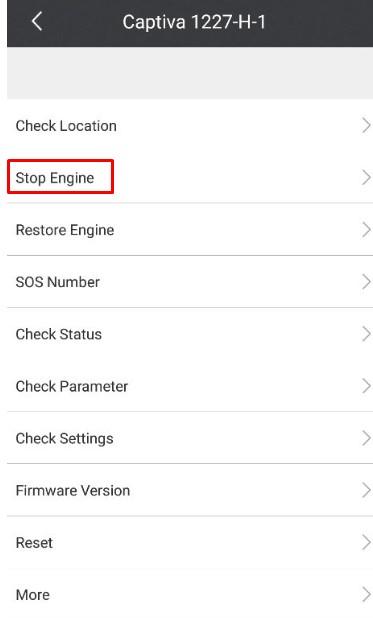

A hacker going by the name L&M says he has hacked into more than thousands of accounts belonging to users of GPS tracking apps, giving him the ability to monitor tens of thousands of vehicles – and even turn off the engines for some of them, while they’re in motion, according to Motherboard.

He has admitted to hacking into more than 7,000 iTrack accounts and more than 20,000 ProTrack accounts, two apps that companies use to monitor and manage fleets of vehicles through GPS tracking devices. He has tracked vehicles worldwide, even in countries like South Africa, Morocco, India, and the Philippines. The software on some cars can be used to turn off the engines of vehicles moving at 12 miles per hour or less.

Screenshot of one hacked account

L&M reverse engineered the ProTrack and iTrack Android apps to find out that all customers are given a default password of 123456 when they sign up. After finding “millions of usernames” the hacker then blasted them all with the default password. He wound up getting access to thousands of accounts as a result.

According to a sample of user data L&M shared, he has scraped information from ProTrack and iTrack customers, including: name and model of the GPS tracking devices they use, the devices’ unique ID numbers, usernames, real names, phone numbers, email addresses, and physical addresses. Four users included in the sample L&M shared confirmed the breach.

The hacker said: “My target was the company, not the customers. Customers are at risk because of the company. They need to make money, and don’t want to secure their customers.”

He continued: “I can absolutely make a big traffic problem all over the world. I have fully [sic] control hundred of thousands of vehicles, and by one touch, I can stop these vehicles engines.”

The apps have a feature to “stop engine,” according to a screenshot provided by the hacker – although he says he never has killed a car’s engine because it would “be too dangerous”. A representative for the makers of one of the hardware GPS tracking devices used by some of the users of ProTrack GPS and iTrack, confirmed that customers can turn off the engines remotely if the vehicles are going under 12 miles per hour.

Rahim Luqmaan, the owner of Probotik Systems, a South African company that uses ProTrack, said about the feature: “That makes it more dangerous. He can actually mess around with […] our clients and customers.”

ProTrack denied the data breach in an oddly worded email response to media inquiries: “Our system is working very well and change password is normal way for account security like other systems, any problem? What’s more, why you contact our customers for this thing which make them to receive this kind of boring mail. Why hacker contact you?”

That should instill their clients with confidence.

Meanwhile, L&M seems to have successfully held both companies for ransom. When he asked ProTrack for a “reward”, they responded: “If we pay you, you will give us the tool and will not hack our account again? How can we make sure about this? Sorry for too many questions, this is the first time we meet this disaster.”

The hacker said he “got what he wanted” from the company.

L&M concluded: “They warned after my attack [sic], and that was a success for me. To force them take care about security. They know now that their customers at risk, So they focused on how to secure their service, a little bit.”

via ZeroHedge News http://bit.ly/2DF6U8m Tyler Durden

Multiple reports say a military coup attempt is ongoing Tuesday morning in Venezuela as an anti-Guaido militia loyal to opposition leader and US-backed Juan Guaidó tries to establish military control of key points across the capital of Caracas and other major cities.

Information Minister Jorge Rodriguez confirmed via social media the government is in the midst of putting down what’s being described as a “small coup” by military “traitors” working with the right-wing opposition.

File photo of Venezuela soldier in Caracas, via AFP

The AP has confirmed ongoing clashes between coup supporters and police inside Caracas, including reports of tear gas being fired, moments after Guaido issued statements in a video calling for a military uprising. Guaido was shown in the video accompanied by detained activist Leopoldo Lopez and surrounded by well-armed soldiers.

Crucially, Lopez said he was liberated from captivity where Maduro had put him under house arrest for leading opposition unrest in 2014, and in the video called on all Venezuelans to peacefully take to streets.

En el marco de nuestra constitución. Y por el cese definitivo de la usurpación. https://t.co/3RD2bnQhxt

In the three-minute video shot early Tuesday, Guaido said soldiers who took to the streets would be acting to protect Venezuela’s constitution. He made the comments a day before a planned anti-government rally.

“The moment is now,” he said, as his political mentor Lopez and several heavily armed soldiers backed by a single armored vehicle looked on.

“Everyone should come to the streets, in peace,” Lopez said further. The past months have seen multiple failed attempts to generate some kind of mass military and civilian uprising against Maduro, but so far all attempts have failed to generate any significant momentum, size, or staying power.

BREAKING NEWS: Interim President of Venezuela Juan Guaido has started a military coup against Maduro. Heavily armed military forces are in various locations across the capital and other major cities pic.twitter.com/9jTC2BLQXR

So far Venezuela authorities have confirmed only coming up against a handful of armed militia members, which suggests Tuesday morning’s anti-Maduro action will likely be short-lived.

developing…

via ZeroHedge News http://bit.ly/2vvkM0J Tyler Durden

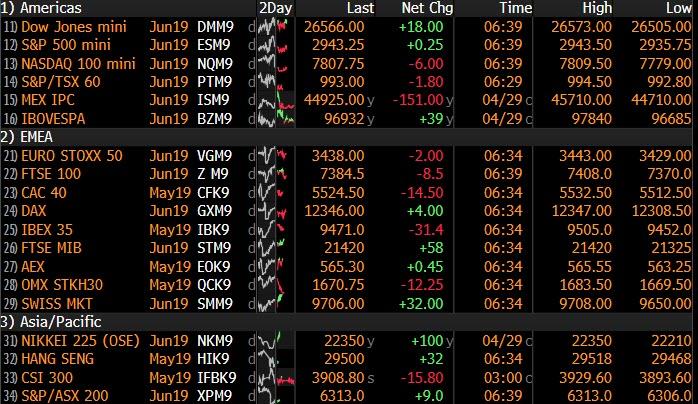

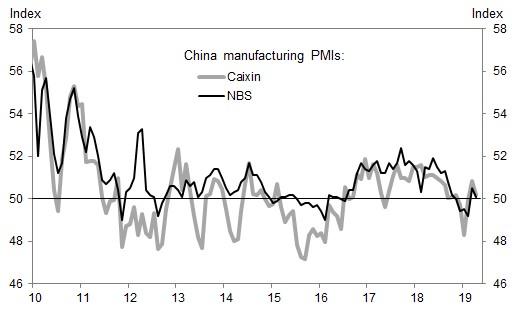

US futures were flat, while European equity markets and Asian stocks slipped on Tuesday as weak Chinese business surveys dampened appetite for risk, while a disappointing outlook and earnings at Samsung, the world’s biggest phone maker, and an ad revenue slowdown at Google sent tech stocks lower.

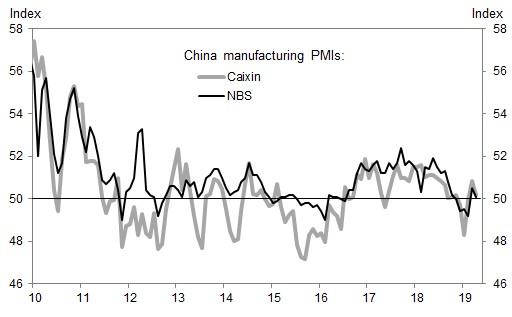

European shares followed Asian peers into the red after surveys on China manufacturing and services missed forecasts – another sign that Beijing’s efforts to spur growth n the world’s second biggest economy had yet to bear fruit, and that the rebound indicated by the spike in China’s PMI print last month was premature. As reported overnight, both official and private business surveys suggested slower Chinese factory growth this month, dashing hopes for a steady reading or even a faster expansion. Data also showed a slower expansion in its services sector. The full details again:

Chinese Manufacturing PMI (Apr) 50.1 vs. Exp. 50.5 (Prev. 50.5).

Chinese Non-Manufacturing PMI (Apr) 54.3 vs. Exp. 55.0 (Prev. 54.8)

Chinese Caixin Manufacturing PMI (Apr) 50.2 vs. Exp. 51.0 (Prev. 50.8)

And visually:

Asian markets fell after the poor Chinese data amid thin trading. MSCI’s index of Asia-Pacific shares outside Japan was off 0.5%. Bourses in South Korea and Hong Kong both fell. apan’s financial markets are closed throughout the week as Japanese Emperor Akihito prepares to abdicate in favor of his elder son, Crown Prince Naruhito.

The latest Chinese data underscored questions over prospects for the Chinese economy despite a record credit injections who impact appears to have fizzled early, while investors across the world are on edge over growing signs of a two-speed global economy where a robust United States outpaces its peers.

Adding to China’s economic disappointment were tech stocks, which slumped following Alphabet’s worse-than-expected results after the Monday close, and after Korean smartphone giant Samsung Electronics’s profit missed analysts’ recently reduced estimates and shared a worse than expected outlook. Equities in Hong Kong, South Korea and Australia all dropped, though trading was quieter than usual thanks to a holiday in Japan. As usual, bad news was good news, and shares rose in Shanghai despite poor Chinese manufacturing data.

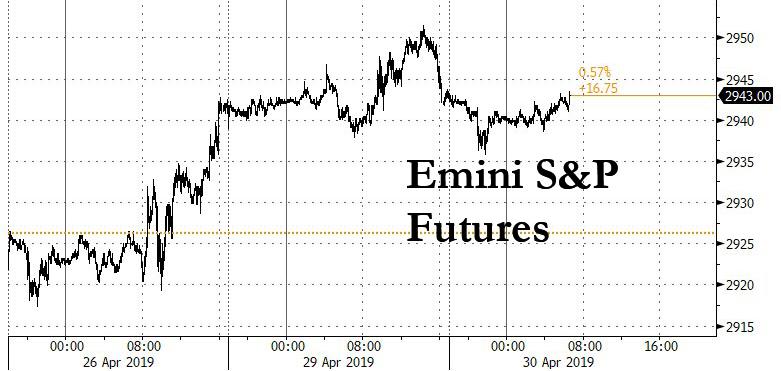

The Asian weakness initially spread to Europe, where the Stoxx 600 index was off 0.2%, with British shares down 0.2% and bourses in Germany and France down 0.1 and 0.4% respectively in early trading, while futures on the S&P 500 also pointed to a soft open in New York.

The Stoxx Europe 600 nudged into the red, led by declines in telecommunication and mining shares, as futures on the S&P 500 also pointed to a soft open in New York. France reported steady growth for the first quarter, while Spain’s economy also grew faster than expected. Chipmaker AMS jumped 16% after beating forecasts for first-quarter profit. AMS is a supplier to Apple, which is due to report its results later. Banks dragged heavily on the Stoxx 600. Danske Bank, hit by money-laundering scandals, fell more than 6 percent after lowering its outlook for 2019, while No. 1 euro zone bank Santander also slipped after first-quarter net profit. In contrast, Standard Chartered climbed after unveiling plans for share buybacks of up to $1 billion, its first in at least 20 years. The euro added to gains after regional GDP beat estimates and inflation in some of Germany’s regions accelerated in April.

Tech stocks were hit following Alphabet’s worse-than-expected results after the Monday close, and after Korean giant Samsung Electronics’s profit missed analysts’ recently reduced estimates. Equities in Hong Kong, South Korea and Australia all dropped, though trading was quieter than usual thanks to a holiday in Japan. Shares rose in Shanghai despite poor Chinese manufacturing data.

“It’s not a stellar reporting season — I don’t think anyone expected that,” said Nick Nelson, head of European equity strategy at UBS, on Bloomberg television. “But it’s certainly better than the fourth quarter. And that fits with some of the stabilization in the broader data in the euro zone, in emerging markets and in China.”

Emerging-market stocks and currencies were weaker Tuesday following the disappointing Chinese PMI data and as investors awaited further news on progress in trade talks between the U.S. and China. Still, MSCI’s gauge of developing-nation equities remained on track for a fourth successive monthly gain, the longest streak since January 2018. The currency index, however, is set for a third consecutive drop. Seasonal data complied by Bloomberg suggests both measures may retreat in May, as they have in seven of the past 10 years.

In FX, the euro strengthened for a third day as the euro-area economy expanded more than forecast in the first quarter. The pound shrugged off a report that said U.K. Prime Minister Theresa May faces a challenge from activists within her own party opposing her leadership, and GBPUSD rose above 1.30 for the first time in a week. AUDUSD swung to a loss after an official release showed Chinese manufacturing PMI missed.

Elsewhere, South Korea’s won led currency declines, falling to a two-year low after a weak earnings report from Samsung. The Philippine peso was firmer after the country’s credit score was lifted one step at S&P Global Ratings. Turkey’s lira fluctuated as investors pondered the latest statements by central-bank chief Murat Cetinkaya. The focus now turns to the Federal Reserve policy meeting on Wednesday.

In rates, Treasuries unexpectedly reversed direction around the time Europe opened, and reversed gains that came on the back of weaker-than-forecast China manufacturing growth.

In commodity markets, oil prices reversed losses after Saudi Arabia said a deal between producers to withhold output, in place since January, could be extended beyond June to cover all of 2019. Brent crude futures were last at $71.25 per barrel, down 0.4 percent.

In overnight geopol news, North Korea’s Vice Foreign Minister said that their resolve for denuclearisation is unresolved, adding that denuclearisation will be possible only if the US changes their current calculations. If the US fails to present new positions the US will then see unwanted consequences.

In the latest Brexit news, UK PM May is said to be facing a grassroots vote demanding her resignation with Conservative party local chairman and activists calling for an extraordinary meeting with PM to demand her resignation. May’s office thereafter downplayed the significance of the meeting, suggesting that it would not be legally-binding and the outcome of the meeting wouldn’t necessarily be passed. Furthermore, there will have to be a 28-day wait until such a meeting is held.

Looking ahead, traders will be looking for signals from economic data, a Fed policy meeting on Wednesday and earnings reports from the likes of Apple and McDonald’s. Meanwhile, the next round of trade talks between the U.S. and China will get under way this week with significant issues still unresolved. But enforcement mechanisms are “close to done,” according to Treasury Secretary Steven Mnuchin, although this has been said on countless times before.

Market Snapshot

S&P 500 futures down 0.07% to 2,941.00

STOXX Europe 600 down 0.2% to 390.65

MXAP down 0.1% to 162.36

MXAPJ down 0.5% to 538.26

Nikkei down 0.2% to 22,258.73

Topix down 0.2% to 1,617.93

Hang Seng Index down 0.7% to 29,699.11

Shanghai Composite up 0.5% to 3,078.34

Sensex down 0.6% to 38,840.30

Australia S&P/ASX 200 down 0.5% to 6,325.47

Kospi down 0.6% to 2,203.59

German 10Y yield rose 2.7 bps to 0.03%

Euro up 0.2% to $1.1203

Brent Futures up 0.3% to $72.27/bbl

Italian 10Y yield unchanged at 2.213%

Spanish 10Y yield rose 2.0 bps to 1.033%

Brent Futures up 0.3% to $72.27/bbl

Gold spot up 0.4% to $1,284.33

U.S. Dollar Index down 0.2% to 97.65

Top Overnight News from Bloomberg

Yield-starved investors outside the U.S. are abandoning their currency hedges on American assets, and that’s good news for dollar bulls.

Economic growth in the euro area strengthened more than expected in the first quarter, buoyed by resilience in France and Spain.

Markets aren’t adequately pricing in the risks from higher oil costs, according to Morgan Stanley Wealth Management. Rallies in stocks and Treasuries that have taken the S&P 500 Index to a record high and 10-year yields down to around 2.5 percent illustrate that investors are complacent about crude prices.

The first official gauge of China’s manufacturing sector fell in April, signaling that the economic stabilization seen in the first quarter remains fragile

President Donald Trump sued to block Deutsche Bank AG and Capital One Financial Corp. from complying with congressional subpoenas targeting his bank records, escalating the president’s showdown with Democratic lawmakers investigating his finances

U.K. Prime Minister Theresa May will face a challenge from activists in her Conservative Party after enough signed a petition opposing her leadership and Brexit strategy to force an emergency vote on her future

The U.K.’s opposition Labour Party’s ruling council will seek to thrash out a Brexit strategy Tuesday as leader Jeremy Corbyn tries to head off a split that threatens to derail his election plans

A week after the U.S. flagged tighter sanctions on Iranian crude and spurred oil higher, prices are back down to where they were before the announcement

U.K. traders are ignoring risk of a hawkish BOE, JPMorgan says

Asian equity markets traded mostly lower following weaker than expected Chinese PMI data and as the region digested a heavy slate of earnings. ASX 200 (-0.5%) was negative in which commodity names led the declines seen across a broad range of sectors due to its high exposure to China and the disappointing factory activity, while KOSPI (-0.6%) suffered amid losses in index heavyweight Samsung Electronics after the Co.’s final Q1 results showed operating profit fell around 60% Y/Y. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (+0.5%) diverged with Hong Kong dampened after Chinese Official Manufacturing, Non-Manufacturing and Caixin Manufacturing PMIs all fell short of estimates which overshadowed the earnings releases including the profit growth amongst the Big 4 banks, while the mainland remained afloat on month-end and pre-holiday position squaring as well as the increased hopes for more accommodative policy in the aftermath of the weak Chinese data.

Top Asian News

Jokowi Wants Indonesians to Have Say Picking New Capital City

Warning Signs Are Flashing in China Stock Market After Surge

China Triple Whammy Sees Stocks, Bonds, Yuan All Sink in April

Breaking Up: Asian Stocks Fall Out of Lockstep With U.S. Market

Major European bourses have drifted marginally lower since the EU open [Eurostoxx 50 -0.3%], following a mostly downbeat Asia-Pac lead and as the region digested a slew of pre-market earnings. Sectors are mixed with Telecom names lagging after France’s Orange (-3.5%) missed revenue forecasts and tumbled to the foot of the CAC 40. On the flip side, the energy sector is faring well amidst price action in the oil complex which aided BP (+0.4%), Shell (+0.2%) and Total (+0.1%) climb back into positive territory. Back to earnings, Standard Chartered (+5.7%) extended on opening gains after optimistic earnings coupled with a USD 1.0bln share buyback programme which is expected to reduce its CET1 ratio by around 35bps in Q2. Elsewhere, DSV (+6.8%), Beiersdorf (+2.3%), MTU Aero Engines (+2.2%), and Caixabank (-3.9%) are amongst the movers post-earnings. Finally, Danske Bank (-8.2%) shares fell to the foot of the Stoxx 600 after FT reported that Brussels vows to pursue a probe into the bank’s money laundering scandal.

Top European NEws

Greenpeace Norway Says Activists Have Left West Hercules Rig

Santander’s Bets on Latin America Pay off as Europe Stumbles

Biggest Nordic Banks Hit by Selloff After Bleak Results

Tria Says VAT Hike Could Be Inevitable Without Cuts: Il Fatto

In FX, the Dollar is softer across the board after Monday’s soft PCE inflation data and with rebalancing models for the last trading day of April flagging sells signals to varying degrees. Hence, the DXY has slipped back from 98.000+ levels again, and this time the index is probing somewhat deeper blow chart supports that were tested towards the end of last week, but not breached. If 97.544 (50% Fib) and 97.500 fail to hold, 97.460 is next on the radar before a stronger downside target and low from last week looms at 97.258.

GBP – The Pound is the best G10 performer and biggest beneficiary of month end Greenback weakness with one bank signalling especially strong Cable buying to balance portfolios. Subsequently, the pair has extended recovery gains from the low 1.2900 area to circa 1.2986 and through several DMAs including the 10, 100 and 200 levels (at 1.2940 and 1.2961 coincidentally).

EUR/JPY – Vying for 2nd place in the major ranks and both impacted by data, albeit diversely, as the single currency draws encouragement from firmer than forecast Eurozone GDP and inflation to reclaim the 1.1200 handle. However, the Jpy has now overcome strong resistance at 111.37 to peer above 111.30 in wake of disappointing Chinese PMIs overnight that spurred some risk-aversion and demand for the safe-haven Yen.

NZD/CHF/CAD – The next best G10s or gainers due to the more pronounced Usd downturn, with the Kiwi hovering near the top of a 0.6681-56 range and Franc back over 1.0200 within 1.0199-75 trading parameters, while the Loonie is pivoting 1.3350 ahead of Canadian data in the form of monthly GDP and PPI. Note also, BoC Governor Poloz and Wilkins are slated to speak later, and then NZ Q1 jobs and labour costs for Q1 are on tap before attention turns to Wednesday’s FOMC.

AUD – The Aussie is lagging on the aforementioned PMI misses from China and in particular the official and Caixin manufacturing reads that only just avoided stagnation. Aud/Usd is straddling 0.7050, as the Aud/Nzd cross slips a bit further below recent peaks of 1.0600+ towards 1.0565.

EM – The Try has been volatile again with further weakness vs the Usd in the run up and during the early part of the CBRT’s inflation presentation, but a partial recovery within a 5.9335-9835 band ultimately as Governor Cetinkaya clarified last week’s post-policy meet statement and guidance to maintain that tightening is still an option if upside inflation risks materialise.

In commodities, energy markets are trending higher, albeit remain relatively choppy in early EU trade following comments from Saudi Energy Minister Al-Falih who (in-fitting with reports) said that the Kingdom is ready to meet shortfalls caused by the expiry of Iranian oil waivers on May 2nd. However, with the upcoming JMMC meeting on May 19th (ahead of the OPEC+ meeting on June 26th) the Saudi Energy Minister also noted that a majority of the cartel’s oil ministers are tilting towards extending the global output deal. Analysts at BNP highlight that there is a “good chance” that OPEC countries and allies will decide to extent the supply curb deal in June, although some changes may be made to the current deal. The energy minister also noted that the nation’s oil output will be significantly lower than 10mln BPD (last recorded around 9.8mln BPD) until May-end, whilst exports will be below 7mln BPD (currently just under 7mln BPD). Meanwhile, IFX reported that Russia’s April oil output stood at 11.23mln BPD, slightly lower than March’s 11.3mln. This, coupled with a receding Dollar aided WTI and Brent futures to climb comfortably above USD 64.00/bbl and USD 72.50/bbl respectively. Elsewhere, precious metals are also benefitting from the weaker Greenback with spot Gold meandering just below its 100 and 200 DMAs at 1293.11 and 1297.40 respectively. Meanwhile, turning to base metals, downside seen from disappointing China Manufacturing data has been offset by the softer Dollar with copper now closer to intraday highs and just a whisker away from its 50 DMA at 2.9054.

US Event Calendar

8:30am: Employment Cost Index, est. 0.7%, prior 0.7%;

9am: S&P CoreLogic CS 20-City MoM SA, est. 0.2%, prior 0.11%; 20-City YoY NSA, est. 2.95%, prior 3.58%

9:45am: MNI Chicago PMI, est. 58.5, prior 58.7

10am: Pending Home Sales MoM, est. 1.45%, prior -1.0%

10am: Conf. Board Consumer Confidence, est. 126.8, prior 124.1; Pending Home Sales NSA YoY, est. -4.0%, prior -5.0%

The first couple of days of the week here in the UK have required a strict routine recently. Get through Monday avoiding all social media involving Game of Thrones until the evening when you can then rush home and watch it, and then speculate all day Tuesday with your colleagues about what happens next. As Jim was waiting for his house move to start series 8, we’ve had to remain tight-lipped but the flood gates have now opened since he’s been off, especially after last night’s blockbuster. We’ll politely refrain from saying any more and spoiling the plot for those who haven’t yet watched it.

Markets are stuck in a similarly welcome routine of their own at the moment as US equities continue to nudge higher to fresh record highs. Last night’s +0.11% close for the S&P 500 was the third new closing high for the index in the last week while the NASDAQ (+0.19%) likewise closed at a new high – though it is trading lower overnight after Google’s tepid earnings. The DOW (+0.04%) is still -1.02% off its own all-time high; however, it does feel more like when rather than if it’ll eclipse that level. The VIX ticked +0.38pts higher to 13.11, but remains near the bottom of its year-to-date channel. Remarkably, the VIX has traded in an intraday range of just 3.36pts for all of April. The last time we had a smaller range during a month was February 2017. One key market indicator that has snapped out of its recent range is the US 2s10s yield curve, which rose +1.9bps yesterday to 23.7bps. That’s its steepest level since November, and it was accompanied by a general rise in yields yesterday. Yields on Treasuries and Bunds rose +2.8bps and +2.5bps, respectively. This helped bank stocks, which powered equity gains on both sides of the Atlantic, with bank stock indexes equally gaining +1.32% in both the US and Europe.

Anyway, a soft PCE inflation report in the US yesterday – albeit one which was largely baked in post Friday’s data – got the ball rolling;however, the relatively muted price action likely better reflected what is still an exhausting week ahead of big macro events and earnings.

Indeed, this morning we’ve had China’s PMIs for April where both the official (50.1 vs. 50.5) and Caixin (50.2 vs. 50.9 expected) manufacturing readings have disappointed. They also dropped from 50.5 and 50.8, respectively, last month. The official non-manufacturing reading also declined half a point to 54.3 (vs. 54.9 expected) leaving the composite 0.6pts lower at 53.4. The good news is that the composite reading is still higher than the five months prior to March, while the manufacturing reading is above 50 for a second consecutive month, with underlying components including new orders looking healthy. So, consolidation following a big bounce in March is probably the most appropriate way to describe the data.

Equity markets in China are a little higher post that data with the Shanghai Comp up +0.43% and CSI 300 up +0.19%. Positive trade comments from Mnuchin appear to also be helping. He said on Fox News that the US has “made more progress than ever before” towards a real agreement. A reminder that Mnuchin and Lighthizer travel to Beijing today. Meanwhile, the rest of Asia is a little softer with the Hang Seng (-0.48%) and Kospi (-0.55%) down. The latter seems to be suffering following an earnings miss for Samsung. In FX, Sterling is little changed overnight after the Sun reported that more than 10% of chairmen and women of local parties had signed a petition calling for PM May to resign, thus meeting the threshold for an emergency meeting.

Meanwhile, after the close last night Alphabet’s results came in a bit soft, with revenues surprisingly missing expectations. The company reported overall sales of $29.5 billion, less than the $30.0 billion expected. Profits came in at $6.7 billion, down almost 30% versus the same period last year, but most of that was attributable to a $1.7 billion fine to the European Commission. The stock price, after closing at an all-time high in advance of the earnings report, fell as much as -7% in overnight trading, sending NASDAQ futures -0.25% lower this morning.

Turning back to yesterday, the USD was little changed; however, EM currencies including the Argentinian Peso (+3.50%) had a better day boosted by the announcement from Argentina’s central bank that it would start selling dollars to stabilize the currency. In Europe, the STOXX 600 (+0.08%) recovered from early losses to just about finish onside while the DAX rose +0.10%. Spain’s IBEX (+0.12%) erased losses from earlier in the day to close in line with the rest of Europe after the weekend election result, and 10y Spanish bond yields fell -1.2bps despite the broader bond selloff. Elsewhere WTI oil (+0.32%) rose after declining -4.52% over the preceding three sessions.

Just on the details of that inflation data in the US where the March core PCE deflator was confirmed at 0.0% mom in March compared with expectations for a +0.1% reading. The extra few decimals showed it was a more marginal miss at +0.046%; however, the annual rate, which nudged down from +1.7% to +1.6% yoy was +1.553% with the extra decimal places and so a whisker away from rounding down to an even lower +1.5%. Our US economists noted that the 3-month annualized change is now just +0.7% and the lowest since early 2015 too. Their full thoughts, parsing the various inflation measures and their associated implications for Fed policy, can be found here .

So clearly a soft set of data even if the market had priced much of it in post Friday’s Q1 details. That all being said, our US economists have noted that there are two reasons to expect core PCE to bounce back next month, however. The first is the read-through from the recent bounce in equities for financial services and portfolio management services following a plunge earlier this year, and the second is that core PCE has tended to outperform core CPI in April over recent years.

Other US data didn’t really move the needle. March personal spending rose +0.9% mom versus expectations for a +0.7% rise, but personal incomes rose only +0.1% versus +0.4% expected. Separately, the Richmond Fed manufacturing survey fell -4.9 points to 2.0, a notable decline but still above the negative levels seen in December-January.

Meanwhile, the European Commission’s April confidence indicators were hardly encouraging and underscored the problems facing the manufacturing sector, as the headline economic confidence reading fell -1pt to 104, its lowest level since September 2016. The industrial confidence reading dropped -2.5pts to -4.1, its lowest reading since September 2014. The consumer and services confidence readings were flat and above recent lows, but still a bit off their peaks from last year. Separately, March M1 money supply growth came in better than expected at +7.7%, up from +6.9% in February. Digging into the credit data, however, showed weak corporate loan flows, which pushed the credit impulse to -0.6pp of GDP, its fourth consecutive negative print.

In terms of the rest of the day ahead, all eyes this morning will be on the Q1 GDP reading for the Euro Area where the consensus is for a +0.3% qoq print. We’ll get the data for France prior to that while Italy is due out a little later. Also on the cards today are preliminary CPI data for France, Germany and Italy, while this afternoon we’ve got the Q1 ECI in the US along with the February S&P CoreLogic house price index data, Chicago PMI for April, March pending home sales and April consumer confidence. Away from that we’re due to get comments from the BoE’s Ramsden while Lighthizer and Mnuchin travel to Beijing for more trade talks. The big earnings highlight is Apple after the close tonight, while Pfzier, Merck, McDonalds, Airbus, General Electric and ConocoPhillips are also on the cards. So it should be a busy day.

via ZeroHedge News http://bit.ly/2IQC9lq Tyler Durden

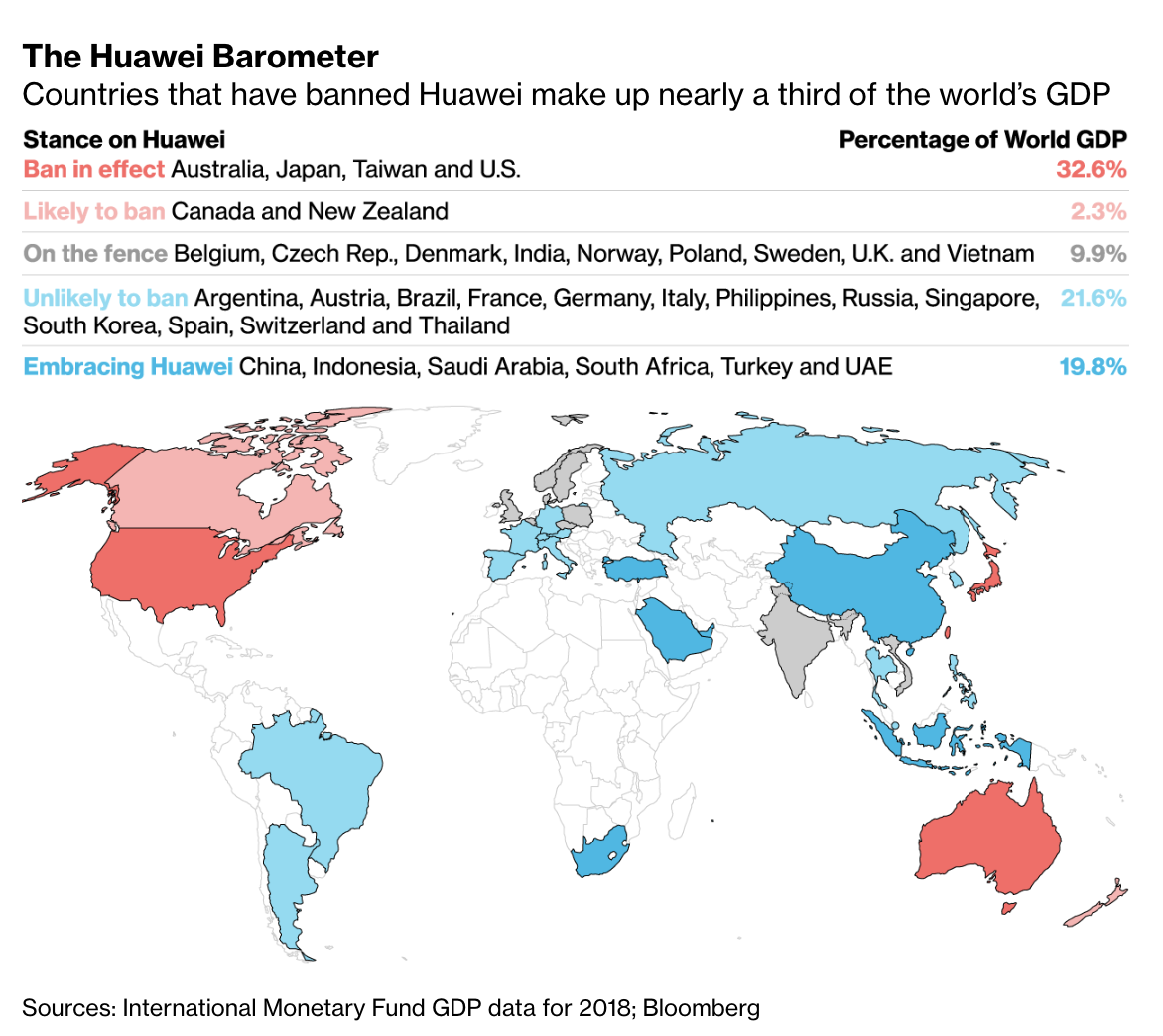

As Huawei denies Microsoft’s allegations that it discovered what appears to be a ‘backdoor’ built into the Matebook laptop series, Bloomberg on Tuesday reported on complaints from Vodafone, Europe’s largest wireless provider, about the discovery of what appear to be ‘backdoors’ discovered in Huawei equipment embedded in Vodafone’s Italian wireless network, potentially going back years.

Though Huawei has tried to cast these complaints, detailed in a series of emails obtained by Bloomberg, as innocuous glitches, but Vodafone’s acknowledgement of these concerns appears to support Washington’s warnings that Huawei equipment represents an international security risk – though the European Council and most individual states have done little to prevent Huawei equipment from being used in the Continent’s 5G wireless networks.

The vulnerabilities identified by Vodafone could grant Huawei access to the ‘fixed-line network’ in Italy, the system that provides Internet service to millions of homes and businesses, potentially exposing a large swath of the Italian population to spying by the Chinese.

After Vodafone approached Huawei in 2011 with its complaints, the Chinese telecoms giant offered assurances that the issues had been fixed; however, further testing revealed that Huawei had mislead Vodafone. What’s more, Vodafone also identified backdoors in its fiber-optic network, potentially exposing Internet traffic in Italy to Chinese spying.

Despite all of this, Vodafone did nothing after discovering backdoors throughout its Italian network and even catching Huawei in a lie when the company said it had fixed the issues, but Vodafone discovered that it hadn’t.

These concerns didn’t stop Vodafone for increasing its reliance on Huawei’s equipment, which underscores why European governments have been so reluctant to heed Washington’s warnings: Huawei is simply too important to Europe’s telecoms infrastructure. Spurning Huawei would put Europe at risk of falling behind the US and China in the race to build out 5G infrastructure.

Vodafone CEO Nick Read has joined peers in publicly opposing any restrictions on Huawei equipment in Vodafone’s 5G networks.

Most European countries are unlikely to crack down on Huawei over these security concerns.

And clearly, the issue didn’t sour the Italians on China, since Italy recently became the first G-7 country to join Beijing’s “Belt & Road Initiative”, which has been derided by critics as a “neocolonialist project.”

In addition to the security concerns in the core Italian network, Vodafone also complained about suspected vulnerabilities in routers shipped by the company. But both Huawei and Vodafone cautioned that these could have been the result of an unintentional flaw.

In a statement to Bloomberg, Vodafone said it found vulnerabilities with the routers in Italy in 2011 and worked with Huawei to resolve the issues that year. There was no evidence of any data being compromised, it said. The carrier also identified vulnerabilities with the Huawei-supplied broadband network gateways in Italy in 2012 and said those were resolved the same year. Vodafone also said it found records that showed vulnerabilities in several Huawei products related to optical service nodes. It didn’t provide specific dates and said the issues were resolved. It said it couldn’t find evidence of historical vulnerabilities in routers or broadband network gateways beyond Italy.

“In the telecoms industry it is not uncommon for vulnerabilities in equipment from suppliers to be identified by operators and other third parties,” the company said. “Vodafone takes security extremely seriously and that is why we independently test the equipment we deploy to detect whether any such vulnerabilities exist. If a vulnerability exists, Vodafone works with that supplier to resolve it quickly.”

In a statement, Huawei said it was made aware of historical vulnerabilities in 2011 and 2012 and they were addressed at the time.

But some of BBG’s other sources warned that backdoors were discovered in networks across Europe, and that Vodafone had sought to play down these discoveries.

However, Vodafone’s account of the issue was contested by people involved in the security discussions between the companies.

Vulnerabilities in both the routers and the fixed access network remained beyond 2012 and were also present in Vodafone’s businesses in the U.K., Germany, Spain and Portugal, said the people. Vodafone stuck with Huawei because the services were competitively priced, they said.

Emails obtained by BBG also revealed that some Vodafone executives were shocked by Huawei’s unwillingness to fix the backdoors, and its decision to lie about the issues being fixed.

“Unfortunately for Huawei the political background means that this event will make life even more difficult for them in trying to prove themselves an honest vendor,” Vodafone said in the April 2011 document authored by its chief information security officer at the time, Bryan Littlefair. He noted that Vodafone had made a recent security visit to Shenzhen and said he was surprised Huawei hadn’t given the matter a greater priority.

“What is of most concern here is that actions of Huawei in agreeing to remove the code, then trying to hide it, and now refusing to remove it as they need it to remain for ‘quality’ purposes,” Littlefair wrote.

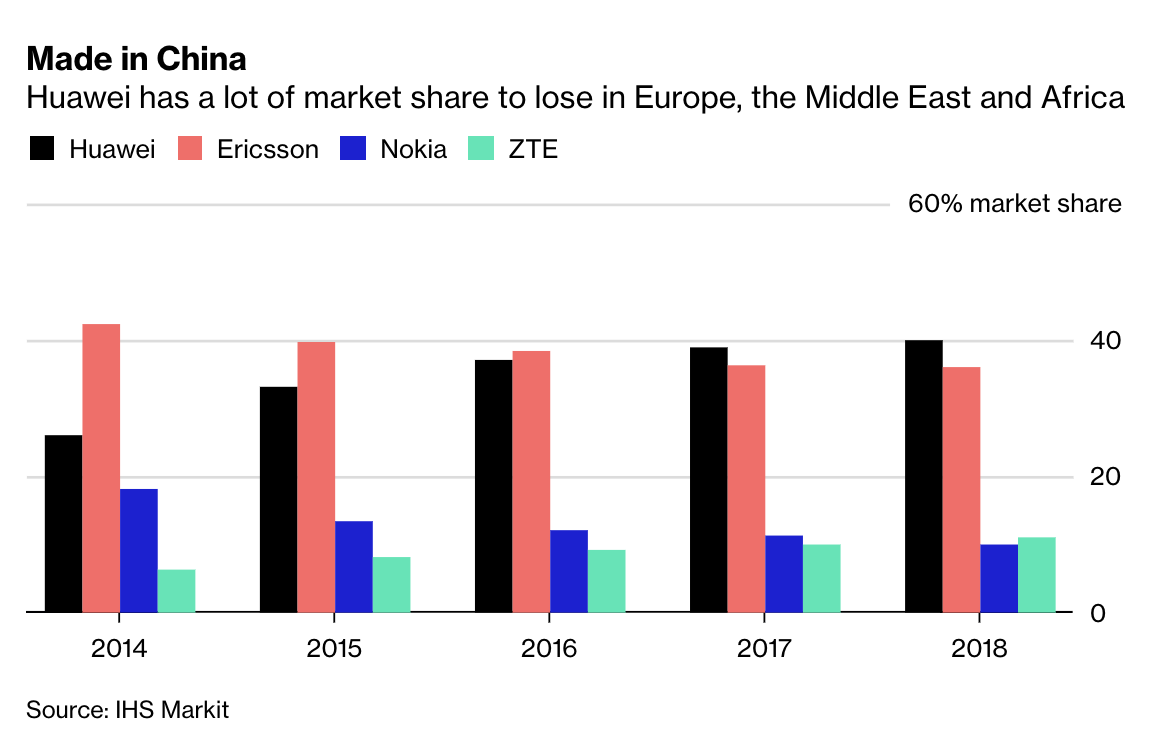

Of course, Huawei has a lot of market share to lose in Europe, and therefore it’s incumbent on the firm to keep its customers happy.

But then again, if telecoms companies in Europe continued to use Huawei equipment in such sensitive capacities after this incident, then apparently switching to Ericsson or Nokia technology isn’t really an option.

via ZeroHedge News http://bit.ly/2V3sa2E Tyler Durden

Authored by former Lehman trader and current Bloomberg macro commentator Mark Cudmore.

U.S. Equity Optimism Is Starting To Look Misplaced

It’s time to turn bearish on the S&P 500, at least for a few weeks. The benchmark U.S. equity index just made a fresh record high, but it’s unlikely to keep ignoring warning signs coming from elsewhere in markets.

After having been staunchly bullish global stocks this year, I turned bearish on Asia equities on Monday last week. That negative sentiment will now spread across the Pacific. Asia, and notably China, has led the 2019 global stocks rally, and similarly has the capacity to lead a correction.

There’s not one single looming catalyst that will send equities reeling. The problem is that almost every factor is starting to look like a marginal negative. The positives from Fed dovishness, a solid earnings season and hopes of a trade deal are all generously priced in. Where’s the good news going to come from going forward?

Companies’ guidance hasn’t been encouraging and earnings estimates for later in the year continue to slide. The S&P 500 has a blended 12-months forward price-to-equity ratio of 17 versus the 10-year average of 15. Such a substantial premium is ripe for disappointment.

The data out of Asia over the past week has been terrible. Tuesday’s PMIs out of China emphasize that the market may have got over- optimistic on how quickly the economy can accelerate: All the PMI prints disappointed — private and official, manufacturing and services.

Dollar strength is another marginal negative. As is the surge in oil prices. This week’s lengthy holidays in the world’s second- and third-largest economies, China and Japan, don’t help. And, of course, May is historically a tough month for emerging markets.

Once you get in this mindset, it’s easy to see further warnings signs from the sudden surge in exceptionally large IPOs, or Alphabet’s earnings miss that came after the close on a day its stock price reached a record.

How is this week’s Fed meeting going to help stocks? With dovishness already priced, it will either confirm a gloomy economic outlook or force yields to move higher.

It’s difficult to pinpoint what will be the exact trigger for risk-aversion, and it may seem unnecessarily contrarian to turn bearish upon a record high close, but the facts are lining up for a nasty correction in the S&P 500.

via ZeroHedge News http://bit.ly/2J3yr73 Tyler Durden

President Trump, his three eldest children, the Trump Organization and the family trust have jointly filed a lawsuit to try and stop Deutsche Bank and Capital One from turning over records of its financial dealings with the Trump Organization to the House Judiciary and Intelligence Committees, according to Bloomberg. In the lawsuit, the family’s lawyers contend that Congress is simply trying to “harass” their client with a “fishing expedition” (as Democrats cast about for a new narrative with which to bludgeon the president now that the Russia collusion narrative has fizzled with the publication of the Mueller report).

Trump’s lawsuit is similar to another he filed to block a subpoena sent by Elijah Cummings on behalf of the House Government Oversight and Accountability Committee to Mazar’s, the Trump Organization’s accounting firm.

Since winning control of the House in November, Democrats have warned about their plans to ‘let the subpeonaes fly’, and launch investigations into everything from Trump’s finances to any hint of interference from the White House in the DoJ’s decision to challenge the Time Warner-AT&T merger.

Leaks published earlier this year revealed how Deutsche Bank turned down a Trump Organization loan request made during the 2016 campaign. The company had been looking for money to finance renovations at its Turnberry golf club in Scotland. Documents showed the bank had been skittish about being associated with Trump due to his controversial rhetoric, and that senior executives at the bank weren’t aware of the extent of DB’s multi-decade lending relationship with the Trumps. Even after defaulting on a loan and suing the bank during the financial crisis, DB’s wealth management unit continued to do business with Trump.

DB has already started handing over documents to the New York State AG, who is carrying out a separate investigation.

The German lender has already begun the process of giving documents related to loans made to Trump or some of his businesses to the New York state attorney general, who is conducting her own probe, said a person familiar with the matter. The bank hasn’t yet handed over any client-related records to the House committees and will wait for the outcome of the legal proceedings, said the person, asking not to be identified in disclosing internal information.

“The subpoenas were issued to harass President Donald J. Trump, to rummage through every aspect of his personal finances, his businesses, and the private information of the President and his family, and to ferret about for any material that might be used to cause him political damage,” Trump’s lawyers wrote in the introduction to the 13-page complaint filed Monday in Manhattan federal court.

Though Deutsche Bank has been responsible for the bulk of the business lending to the Trump Org since the 1990s, Congress is seeking records from a total of nine financial institutions that have had financial dealings with the Trump Org.

House Democrats’ investigations into President Trump’s finances and potential money laundering tied to Russia have prompted them to demand documents from nine banking giants, according to people familiar with the matter. Deutsche Bank, which lent Trump some $340 million, has been a primary target of the House Financial Services Committee, led by Representative Maxine Waters.

But given Deutsche Bank’s reputation as the “biggest money laundering bank in the world”, as Maxine Waters once branded the bank, it has been the House’s highest-priority target.

Democrats vowed to push ahead with their subpeona, even as DB has decided to wait on complying with the House’s “friendly subpeona” until a judge rules on the Trump lawsuit.

Both Waters and House Intelligence Chairman Adam Schiff have been seeking information from Deutsche Bank since Democrats took over the House majority in January. Schiff said the Frankfurt-based bank has been cooperative with the investigations and their request was a “friendly subpoena.” Such a subpoena is typically submitted when a firm is willing to hand over documents but wants a formal request first.

“We remain committed to providing appropriate information to all authorized investigations and will abide by a court order regarding such investigations,” a Deutsche Bank spokesman said in a statement on Tuesday.

It’s unclear how Capital One plans to respond to the lawsuit.

via ZeroHedge News http://bit.ly/2LcTK95 Tyler Durden

European Central Bank’s President Mario Draghi recently announced that the ECB would be required to approve any management of gold reserves within the euro zone countries. The statement was specifically directed at two Italian members.

Why was Italy singled out? According to the Wall Street Journal, Italian citizens are preparing to take control of Italy’s gold reserves. During the past few years, a multitude of small investors lost billions of dollars due to the failure of several Italian banks. The Bank of Italy is seen as an elitist, inefficient entity indifferent to the needs of ordinary people. Deputy Prime Minister Luigi Di Maio is leading the attack against Italy’s central bank, along with the “5 Star Movement” and the nationalist “League,” all of whom blame the countries financial woes on the incompetence of the central bank.

The 5 Star Movement is asking Italy’s Parliament to approve measures that would allow private banks to sell their share in The Bank of Italy at 1930’s prices. Taking it a step further, they are also demanding that ownership of the Bank of Italy’s 2,451.8 tons of gold be taken over by the country’s citizens and spent on populist policies. The current value of these gold reserves is $102 billion.

If these laws are passed, investors would be able to sell gold and greatly deplete the central bank’s reserves. As Giorgia Meloni of the Brothers of Italy states, “The gold belongs to the Italians, not the bankers.”

Italy’s lawmakers hold a different view and are warning against any action that will upend the sovereignty of the central bank’s policies. Such expropriation of government gold would not be tolerated.

But the 5 Star Movement and the League are determined to return ownership of the country’s gold to the public. Approximately 60 percent of lawmakers support the movement, guarantying the law will be enacted. There is also rumbling about nationalizing the Central Bank of Italy entirely.

In the realm of global commerce, gold has become a most potent weapon.

Italy is not the only country embracing gold.

Romania has plans to repatriate gold reserves currently being held by the Bank of England. Romania currently has around 103.7 tons of gold, valued at $3.84 billion. Sixty-five percent of the yellow metal is being kept in storage at the Bank of England. According to a new law, only 5 percent of the country’s gold may be stored abroad. The rest will be repatriated. While the current leadership approves of the repatriation, the National Bank of Romania does not. Mugur Isarescu, director of the central bank, insists that the gold is for economic emergencies and should remain where it is.

Another European country, Germany, has quietly called back 674 tons of gold from France and the U.S. Federal Reserve to its central bank, the Bundesbank. Ninety-eight percent of Germany’s gold was stored abroad during the height of the Cold War to keep it out of the reach of Russia. With the weakening of the Euro, Germany wants the gold closer to home. The Bundesbank now has half of the country’s gold in safe storage.

Following the trend to keep gold close to home, the National Bank of Hungary will be recalling 100,000 ounces of gold from the Bank of England. Hungary has traditionally kept its gold reserves low, with only 50 tons being held in 1989. The global 2008 financial crisis had Hungary rethinking its approach to gold. Now, it wants its gold reserves home for safekeeping in the event of a geopolitical crisis.

Gold is seen by central banks as a way to maintain financial trust during economic upheaval. The move by global central banks to repatriate their gold may be a sign that an economic crisis could be looming in the near future.

via ZeroHedge News http://bit.ly/2V5y9Un Tyler Durden

In a move that many have interpreted as a shot across the bow of President Trump, Pope Francis has upped his globalist-leaning interventionism by donating $500,000 to help Central American migrants stranded in Mexico as they try to reach America.

The money is from church collections from around the world and is intended to help 75,000 people who arrived in Mexico to find passage to America.

RT reports that The Catholic Church’s Peter’s Pence Fund said in a statement that aid to migrants by governments and private individuals has dropped as global media coverage of the crisis decreased.

“All these people were stranded, unable to enter the United States, without a home or livelihood,” Peter’s Pence said.

“The Catholic Church hosts thousands of them in hotels within the dioceses or religious congregations, providing basic necessities, from housing to clothing.”

Many have interpreted this move as retaliation after Trump cut all aid to Guatemala, Honduras and El Salvador last month, accusing the Central American countries of not doing “a thing for us.”

‘Pope Francis donates $500G to migrants at U.S.-Mexico border’

But not everyone sees the Pope’s intervention that way…

POPE GIVING AWAY PARISHIONERS MONEY.

SHOULDN’T HE “ASK” IF THAT’S HOW THEY WOULD LIKE THEIR TYTHES SPENT?

WOULD HAVE. HELPED A LOT OF HOMELESS PEOPLE OR VETS.

Pope Francis recently spoke out against governments that build walls to keep out migrants, saying: “Those who build walls will become prisoners of the walls they put up.”

via ZeroHedge News http://bit.ly/2J3Su5q Tyler Durden

The US-NATO alliance is determined to encircle Russia more tightly, and Georgia wants to help it do so…

Britain’s Daily Express newspaper is a bizarre publication that specialises in sensationalist raving. Some of its reports are weird beyond imagination, and it went even further than usual into fogs of delusion on April 21 when one of its headlines announced “World War 3: UK CONFRONTS Russia by sending warship to Black Sea.”

The vessel despatched on a “freedom of navigation manoeuvre” by the UK’s Royal Navy is HMS Echo, which cannot be described as a warship. It is “designed to carry out a wide range of survey work, including support to submarine and amphibious operations” and it carries a few cannon and machine guns, but it is difficult to see how it could confront anything more deadly than a prawn-boat. It is, however, part of the grand plan of the US-NATO military alliance which on April 4 “agreed a package of measures to improve NATO’s situational awareness in the Black Sea region and strengthen support for partners Georgia and Ukraine.”

HQ NATO much regrets that its encirclement of Russia does not yet include Georgia or Ukraine. The Brussels sub-office of the Pentagon is trying hard to formally enlist both countries and announced on March 26 that “Georgia is one of the Alliance’s closest partners. It aspires to join the Alliance. The country actively contributes to NATO-led operations and cooperates with the Allies and other partner countries in many other areas. Over time, a broad range of practical cooperation has developed between NATO and Georgia, which supports Georgia’s reform efforts and its goal of Euro-Atlantic integration.”

The day before NATO’s declaration the globe-trotting head of the organisation, Jens Stoltenberg, was in Georgia to attend military exercises. At a meeting with Prime Minister Mamuka Bakhtadze he declared it had been “clearly stated that Georgia will become a member of NATO” and “We will continue working together to prepare for Georgia’s NATO membership,” which was first mooted in 2008 but somehow has never come about.

Non-US NATO military spending totals $264 billion a year, four times that of Russia, and the US will splurge $750 billion next year, so Georgia’s 37,000 military personnel, ten Su-25 combat aircraft and military budget of $380 million are not going to make much of a contribution to NATO, but that’s not the point. What the US-NATO grouping wants is to deploy its armed forces even closer to Russia than at present. When Georgia joins, there will be an opportunity to base tanks, aircraft and missiles right up against the Russian border, as in the Baltic states.

The most interesting observation about Georgia by Radio Free Europe in its account of the Stoltenberg visit was that “The country of some 3.7 million people fought a brief war with Russia in August 2008, and Moscow’s continued military presence on the country’s territory adds to tensions in the region.”

It is never mentioned by the Pentagon, Brussels or the Western media that the “brief war” was entirely the fault of Georgia. Nor is it admitted that if Russia had wished to do so, it could have swept through and occupied the whole of Georgia in a few days without interference by NATO or anyone else.

The European Union decided to conduct an inquiry into the conflict, and in 2009 produced a report which, deep down in its 1,000 pages, states that Georgia initiated the war. This was not at all what the Western world wanted to be told, and the paper is full of observations intended to disguise or excuse Georgia’s military antics. The UK’s Independent online newspaper reported that “The first authoritative study of the war over South Ossetia has concluded that Georgia started the conflict with Russia with an attack that was in violation of international law,” but there are very few people in the Western Establishment who will admit that Georgia was to blame, and they steadfastly support Georgia’s foolhardy aggression.

The EU noted that “There were reportedly more than a hundred US military advisers in the Georgian armed forces when the conflict erupted in August 2008, and an even larger number of US specialists and advisors are thought to have been active in different branches of the Georgian power structures and administration. Considerable military support in terms of equipment and to some extent training was provided by a number of other countries led by Ukraine, the Czech Republic and Israel.” In other words, Georgia was considered a prime ally because it opposed Russia, and the US and its allies helped it prepare for its futile attack.

This is not surprising, given the speech by President George W Bush in Georgia’s capital, Tbilisi, in May 2005. The man who ordered the invasions of Afghanistan in 2001 and Iraq in 2003 was eloquent about Georgia’s military contribution to these disastrous conflicts, and observed that “last year, when terrorist violence in Iraq was escalating, Georgia showed her courage. You increased your troop commitment in Iraq fivefold. The Iraqi people are grateful and so are your American and coalition allies.” Indeed Washington is so grateful to the Georgian government for contributing to its wars (which involved the needless deaths of 32 Georgian soldiers in Afghanistan and five in Iraq), it provides generous aid packages, both civil and military.

A US Congressional Research Service Report of April 2019 notes that in this financial year Congress approved $89 million in civil aid and that in 2018 military aid was $40 million. These amounts don’t seem much at first glance, especially when compared to the mega-billions doled out to Afghanistan, Israel and Iraq — but given that its population is only 3.7 million, Georgia is doing very nicely.

In June 2018, the US Assistant Secretary of State for European and Eurasian Affairs saidUS policy is to “check Russian aggression,” including by “building up the means of self-defence for those states most directly threatened by Russia militarily: Ukraine and Georgia,” which repay US financial patronage not only by sacrificing their soldiers in Washington’s wars (18 Ukrainian soldiers were killed in Iraq), but in more intriguing ways, including in UN forums.

For obvious reasons it has long been thought by most countries that there should be international agreement to ban weapons in space, and a Russian-Chinese draft treaty proposing such legislation was submitted to the UN in February 2008. Washington refused to consider it, and when an amended version was presented at the UN’s First Committee in 2015 it was voted against by the US — along with its well-paid puppets, Israel, Georgia and Ukraine.

The US-NATO alliance is determined to encircle Russia more tightly, and Georgia wants to help it do so. Such provocative cooperation in these endeavours heightens tension between Georgia and Russia, which in the eyes of the western media serves to justify yet more NATO expansion. It is reminiscent of the 1930 song whose last verse is “Whoa, Georgia, Georgia, No peace, no peace I find; Just this old sweet song, Keeps Georgia on my mind…”

via ZeroHedge News http://bit.ly/2GQXs3O Tyler Durden

Just about seven months have passed since Jamal Khashogggi, a former government insider-turned-critic of Saudi Crown Prince MbS, walked into the Saudi consulate in Istanbul and disappeared, sparking an international scandal that prompted several governments (though notably not the US) to suspend arm sales and spoiling MbS’s second ‘Davos in the Desert’ as dozens of CEOs and scheduled speakers pulled out.

Considering the intensity of the backlash to Khashoggi’s murder at the hands of a government death squad, something the Saudi kingdom begrudgingly admitted following weeks of denials (though it insisted that the team had only been sent to ‘talk’ to Khashoggi, and that his killing, dismemberment and the destruction of his remains were the work of rogue operatives) it’s a testament to the shoddy attention span of the global public (and their political and business leaders) that the scandal has been so quickly forgotten.

But as the public has moved on to criticize KSA’s mass executions and the brutal proxy war in Yemen, it appears at least one government involved in the Khashoggi affair might be taking advantage of the fact that the spotlight has moved away to seek some brutal retribution.

On Monday, WSJ reported that one of two suspected UAE spies under investigation by the Turkish government for playing some unspecified role in the Khashoggi’s killing – and who were helping Saudi and its allies spy on Arab critics living in Turkey – had been found hanged in his cell at a notorious Turkish prison.

The cause of death was quickly ruled a suicide.

Turkish prosecutors on Monday said wardens had found the suspect, identified as Zaki Y.M. Hassan, hanged inside his solitary cell in Istanbul’s Silivri prison and had ordered an investigation into his death. Turkish state media said Mr. Hassan had died by suicide.

U.A.E. officials couldn’t immediately be reached for comment.

Turkish authorities had said they were investigating the two men for a possible connection with the killing of Mr. Khashoggi in the Saudi consulate in Istanbul at the hands of Saudi Arabian operatives in October.

The alleged U.A.E. spies came to Turkey soon after the Oct. 2 killing, according to state media reports. They were detained on April 15 and have confessed to spying on behalf of the Gulf state, the reports have said.

Turkish state media has said authorities had tailed the two suspects for several months and had evidence that they were collecting intelligence on Arab nationals residing in Turkey and seeking to recruit other operatives to create a larger surveillance network.

it’s possible that Hassan’s death may have been a suicide. But the tensions between Turkey and members of the GCC who have kept up a shipping ban against Qatar (as the UAE has) have only intensified in the wake of Khashoggi’s murder. Turkey is a close ally of Qatar.

Meanwhile, the Saudi government has pressured the children of Khashoggi to grant clemency to 11 men who are potentially facing the death penalty for their alleged role in the killing (they were scapegoated as the kingdom continued to deny MbS’s involvement in the plot, despite a stream of leaks out of the US intelligence community pointing the finger at the Crown Prince). On another front, Erdogan’s government has continued to provoke the US by arresting yet another consular employee (all have been Turkish nationals).

If this was an act of retribution, does that mean there could be more to come? And what would that mean for Turkey’s increasingly shaky economy?

via ZeroHedge News http://bit.ly/2DELHvg Tyler Durden

{kind=link}

{kind=link}