- China Pledges Greater Role for Market in Economy (WSJ), China vows ‘decisive’ role for markets, results by 2020 (Reuters)

- China expected to cut growth target to 7% (FT)

- World Trade Center Tower Debuts in Manhattan Leasing Test (BBG)

- Job Gap Widens in Uneven Recovery (WSJ)

- Khamenei’s conglomerate thrived as sanctions squeezed Iran (Reuters)

- Swiss referendum on wages of high earners stirs debate (FT)

- Obama to Nominate Massad to Head CFTC (WSJ)

- Japan readies additional $30 billion for Fukushima clean-up (Reuters)

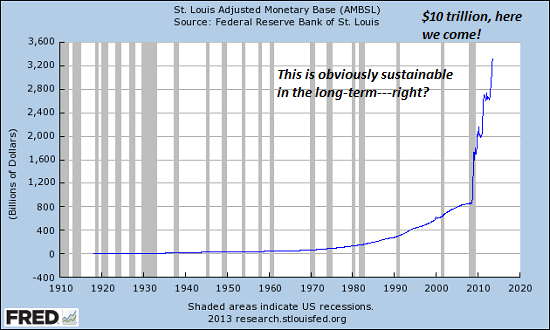

- Shadow banks reap Fed rate reward (FT)

- Airlines Run From Onboard Gabfests as Gadget Use Embraced (BBG)

- Target Fills Its Cart With Amazon Ideas (WSJ)

- Apple Said Developing Curved IPhone Screens, New Sensors (BBG)

- GE Printing Engine Fuel Nozzles Propels $6 Billion Market (BBG)

- Rolex Daytona Sells for Record $1.1 Million at Christie’s (BBG)

Overnight Media Digest

WSJ

* Initial reports suggest that fewer than 50,000 people successfully navigated the troubled federal health-care website to enroll in private health-insurance plans as of last week, two people familiar with the matter said.

* America’s jobs recovery is proceeding on two separate tracks – a pattern that is persisting far longer than after past economic rebounds and lately has been growing worse. Despite three years of steady job gains, and four years of economic growth, many Americans have yet to experience much that could be described as a recovery. That sort of pattern isn’t unusual in the aftermath of a recession, but it usually eases as growth picks up steam.

* Hedge funds are making a large bet on municipal debt, bringing aggressive tactics to a $3.7 trillion market long known as humdrum.

* Freddie Mac and Bank of America are in settlement talks to resolve disputes over more than $1.4 billion in faulty mortgages Freddie has said Bank of America should have to take back.

* Federal prosecutors and the SEC’s internal watchdog recently probed the personal financial holdings of some SEC employees in New York, a move that could again shine a spotlight on the agency’s internal compliance efforts.

* Just a handful of companies have taken goodwill write-downs this year on past acquisitions that have soured. Last year U.S. companies slashed the value of their past acquisitions by $51 billion because the deals didn’t pan out as expected, according to a study set for release Tuesday. That was the highest yearly total for such write-downs since the financial crisis.

* Sotheby’s said its third-quarter loss narrowed as the auction house logged an increase in private sale commissions and auction commission revenue.

* Target has come up with an answer to Amazon.com . Copy it. The discount chain’s latest online offerings have a distinct Amazon feel-from recurring deliveries for diapers to on-demand streaming video.

* Google said it will begin allowing Nielsen to measure audiences for ads on its YouTube website, a decision that could give ad buyers more confidence to shift dollars to online video.

FT

Industrial and Commercial Bank of China (ICBC), the world’s biggest bank by market capitalisation, has been added to the list of banks that must hold extra capital to counter the risk they pose to the financial system, the Financial Stability Board (FSB) said on Monday.

Rupert Murdoch’s News Corp reported a 3 percent decline in revenue in its first results since its separation from 21st Century Fox, blaming weakness in its Australian newspaper division.

Non-bank lenders, known as “shadow banks”, which often fall outside the remit of regulation, have emerged as among the biggest beneficiaries of the Federal Reserve’s ultra-low interest rates with three specialist categories increasing their assets by almost 60 percent since the height of the financial crisis.

Transocean Ltd said it reached an agreement with activist investor Carl Icahn that would see the offshore driller raise its dividend, step up its cost cuts and spin off some of its assets in a new partnership.

British retailer Marks & Spencer said on Monday it planned to make India its biggest foreign market, with “at least” 44 new outlets in the country by 2015, up from 36, as it seeks to stem a sales decline in parts of its UK business.

London-listed drugmaker Shire Plc said on Monday it had agreed to buy ViroPharma for $4.2 billion to strengthen its rare disease treatment business.

NYT

* Some major health insurers are so worried about the Obama administration’s ability to fix its troubled health care website that they are pushing the government to create a shortcut that would allow them to enroll people entitled to subsidies directly rather than through the federal system.

* The new video game consoles from Sony and Microsoft about to hit store shelves are almost certain to be hot holiday gifts this year. The uncertainty for the games business is: What happens after Santa leaves? Sales of a new generation of consoles could be dented by tablets, smartphones and Facebook, which offer games at lower prices.

* Sunday was a bad day for Fantex, the fledgling company promoting initial public offerings of National Football League stars, as its first two prospects were sidelined.

* Liquidators seeking to recover money for investors in two hedge funds filed a lawsuit on Monday against Standard & Poor’s, Fitch and Moody’s.

* A new trial expected to start this week will determine how much Samsung has to pay for an important suit it lost against Apple.

* Bitcoin’s emergence has brought a field of competitors. Already, dozens of ideas are jockeying for the market. The online payment system viewed by many insiders as having the best chance of supplanting bitcoin is Ripple. Ripple holds out the promise not just of a new currency, but also of a novel method to send money around the world.

* The Justice Department’s prosecution of SAC Capital Advisors raises the question of who the victims of a violation are.

* After several years of lackluster performa

nce, the hedge fund industry is increasingly turning to self-help programs, sometimes referred to as “mindware” products, to try to improve its game.

* Several ideas about using financial instruments and a for-profit approach in the world of non-profits are now taking hold.

Canada

THE GLOBE AND MAIL

* Fairfax Financial Holdings Chairman Prem Watsa, who recruited BlackBerry Ltd’s new interim chief executive, says he did not ask former CEO Thorsten Heins to leave.

* Manitoba is being criticized for making it easier to take polar bears from the icy shores of Hudson Bay and place them in captivity. The province – home to the polar bear capital of Churchill – has quietly lifted restrictions that had been in place for 30 years and which allowed only bears under the age of two to be put in zoos.

Reports in the business section:

* Betting that businesses are more interested in renting than buying software and online storage space, two of Canada’s biggest cloud computing companies, Mitel Networks Corp and Aastra Technologies Ltd, are joining forces to create a home-grown competitor to companies such as Oracle and Google.

* Canadian home renovation retailer Rona Inc is acquiring 49 percent of Groupe Coupal Inc for an undisclosed price from the Doucet family, which has run the 99-year-old business since 1971. Quebec-based Rona has held a majority stake in Coupal for nearly eight years.

NATIONAL POST

* Dating portal Ashley Madison has delivered a harsh legal counterattack to a former employee who is suing the company for $20 million for injuries sustained while typing up fake profiles of women for the adultery site, releasing pictures of the woman playing on a jet ski after her alleged injury.

* In the six months after the Canadian Senate began investigating the expense claims of some of its members, about two-thirds of senators claimed less than they had in the same six-month period before the Senate spending issue came to light.

FINANCIAL POST

* The last lifeline for Gabriel Resources Ltd’s controversial mining project in northwestern Romania went dead on Monday, after a parliamentary commission voted down a draft bill that would have allowed Europe’s largest open pit gold mine to move forward.

* Australia said it would allow Saputo Inc to bid for Warrnambool Cheese and Butter Factory Holdings Ltd, removing a key obstacle for the deal aimed at consolidating the country’s dairy industry as global demand surges.

China

CHINA SECURITIES JOURNAL

– China’s Ministry of Land and Resources said in recent meetings that it will restrict the use of land for industrial production to alleviate oversupply in certain industries. The areas of concern include iron and steel, cement, plate glass and shipping, among others.

– The Chinese central government provided 4.1 billion yuan ($673.1 million) in subsidies to cover the yearly costs of rural financial institutions in 2012, up by 74 percent from the year before, the finance ministry said. The funds supported the development of new types of rural financial institutions and strengthened basic financial services.

CHINA DAILY

– China will fine-tune its 30-year-old family planning policy, but changes will be made in a prudent and coordinated way, and serve to maintain a low birth rate, said Mao Qun’an, spokesman for the National Health and Family Planning Commission.

– China needs 75,000 executive managers with global experience in the next five to 10 years, but only 3,000-5,000 people in the local market meet necessary criteria, research by the Center for China and Globalisation shows.

SHANGHAI DAILY

– Shanghai’s Communist Party chief Han Zheng said the city could handle slower GDP growth, and looking ahead development would focus on reforms to make the economy more efficient, protect the environment, and improve the well-being of city residents. Shanghai’s GDP grew by 7.7 percent in the first nine months of the year. The government target for 2013 is 7.5 percent.

SECURITIES TIMES

– Guangdong will launch a pilot lending business that would allow domestic companies to obtain loans or credit from domestic financial institutions with a guarantee from external institutions or individuals, according to the People’s Bank of China Guangzhou Branch. This would help to expand the means of financing for private companies and small businesses.

Fly On The Wall 7:00 AM Market Snapshot

ANALYST RESEARCH

Upgrades

BioCryst (BCRX) upgraded to Neutral from Underperform at BofA/Merrill

Cinemark (CNK) upgraded to Buy from Neutral at Janney Capital

Comerica (CMA) upgraded to Market Perform from Underperform at Raymond James

Crosstex Energy LP (XTEX) upgraded to Outperform from Neutral at RW Baird

Crosstex Energy LP (XTEX) upgraded to Outperform from Sector Perform at RBC Capital

E-House (EJ) upgraded to Buy from Neutral at Goldman

EQT Corporation (EQT) upgraded to Buy from Hold at Stifel

Embraer (ERJ) upgraded to Neutral from Sell at Citigroup

Emulex (ELX) upgraded to Overweight from Neutral at Piper Jaffray

Heartland Express (HTLD) upgraded to Overweight from Neutral at JPMorgan

Kite Realty Trust (KRG) upgraded to Market Perform from Underperform at Wells Fargo

LeapFrog (LF) upgraded to Outperform from Market Perform at BMO Capital

MedAssets (MDAS) upgraded to Buy from Neutral at B. Riley

Regal Entertainment (RGC) upgraded to Buy from Neutral at Janney Capital

SeaWorld (SEAS) upgraded to Buy from Neutral at Citigroup

Downgrades

Clean Harbors (CLH) downgraded to Neutral from Outperform at Credit Suisse

Costco (COST) downgraded to Neutral from Buy at UBS

FARO Technologies (FARO) downgraded to Hold from Buy at Stifel

Gogo (GOGO) downgraded to Neutral from Buy at UBS

Heartland Payment (HPY) downgraded to Neutral from Outperform at RW Baird

Hologic (HOLX) downgraded to Hold from Buy at Canaccord

Hologic (HOLX) downgraded to Sector Perform from Outperform at RBC Capital

Innospec (IOSP) downgraded to Hold from Buy at KeyBanc

Randgold Resources (GOLD) downgraded to Sector Perform from Outperform at RBC Capital

Symantec (SYMC) downgraded to Neutral from Outperform at Macquarie

Initiations

Atmel (ATML) initiated with an Outperform at Oppenheimer

Container Store (TCS) initiated with a Buy at Stifel

Qualcomm (QCOM) initiated with a Buy at Jefferies

Star Bulk Carriers (SBLK) initiated with a Hold at Stifel

TriMas (TRS) initiated with a Buy at Deutsche Bank

Twitter (TWTR) initiated with a Neutral at Susquehanna

Voxeljet (VJET) initiated with a Neutral at Citigroup

Voxeljet (VJET) initiated with a Neutral at Piper Jaffray

HOT STOCKS

Baker Hughes (BHI) declared force majeure in Iraq

GlaxoSmithKline (GSK) said heart disease drug misses primary endpoint

Vale (VALE) selling Norsk Hydro shares

Heartland Express (HTLD) acquired Gordon Trucking for $300M

Assured Guaranty (AGO) approved $400M share repurchase authorization

EARNINGS

Companies that beat consensus earnings expectations last night and today include:

Achillion (ACHN), Third Point Reinsurance (TPRE), DISH (DISH), RDA Microelectronics (RDA), Assured Guaranty (AGO), Premier (PINC), TG Therapeutics (TGTX), Hologic (HOLX), Sotheby’s (BID), ESCO Technologies (ESE)

Companies that missed consensus earnings expectations include:

Dolan Co. (DM), Gran Tierra (GTE), Global Brass & Copper (BRSS), Northern Tier (NTI), Vocera (VCRA), Cray (CRAY), News Corp. (NWSA), BIOLASE (BIOL), Rackspace (RAX)

Companies that matched consensus earnings expectations include:

Fontegra Financial (FRF)

NEWSPAPERS/WEBSITES

- Target Corp. (TGT) has come up with an answer to Amazon.com (AMZN): Copy it. The discount chain’s latest online offerings have a distinct Amazon feel—from recurring deliveries for diapers to on-demand streaming video and free shipping and discounts for its members, the Wall Street Journal reports

- Hedge funds are making a large bet on municipal debt, bringing aggressive tactics to a $3.7T market. The strategies include demanding high interest rates in return for financing local governments, buying the debt of struggling municipalities on the cheap, and trying to profit on rising volatility, the Wall Street Journal reports

- Tyco International (TYC) is approaching global private-equity firms to sell its Korean security unit Caps Co. in entirety, sources say, the Wall Street Journal reports

- Russian crude oil producer Rosneft said its board approved deals to sell oil product cargoes to BP (BP) worth over $6B, in addition to a previous deal to sell oil worth $5.3B, Reuters reports

- John Malone’s Liberty Global (LBTYA), the European cable operator, is in talks to acquire Intel’s (INTC) online pay-TV service under development. Malone would use Intel’s system outside the U.S., sources say, Bloomberg reports

- UBS’s (UBS) China venture plans to offer more computerized-trading services as it bets on a surge in demand from institutional money managers in the biggest emerging market, Bloomberg reports

SYNDICATE

Allison Transmission (ALSN) announces sale of 15M common shares by holders

Booz Allen (BAH) files to sell 10M shares of Class A common stock for holders

Fiesta Restaurant (FRGI) files to sell $100M in common stock

Preferred Apartment (APTS) files to sell 3.23M shares of common stock

QuickLogic (QUIK) files to sell common stock

T-Mobile (TMUS) files to sell 66.15M shares of common stock

via Zero Hedge http://feedproxy.google.com/~r/zerohedge/feed/~3/fUlanwzDq2k/story01.htm Tyler Durden

{kind=link}