Top Republicans Urge FBI, DOJ To Investigate Hunter Biden’s $3.5 Million Moscow Payday Tyler Durden

Thu, 09/24/2020 – 15:00

Top Republicans are calling for the FBI and Justice Department to investigate a series of wire transfers from Russian and Chinese businesspeople to Hunter Biden, after Senate Republicans released a Wednesday report detailing the suspicious transactions – including a $3.5 million wire from a Russian billionaire whose late husband was the mayor of Moscow.

On Thursday, Rep. Jim Jordan (R-OH) sent a letter to FBI Director Christopher Wray inquiring whether the agency has investigated the wire transfers. The letter follows a Wednesday comment from Sen. Rand Paul (R-KY), who told Fox News that he would be submitting a criminal referral to the Justice Department over the payments, according to the Daily Caller.

A report that Senate Republicans released Wednesday detailed millions of dollars in transfers to and from accounts linked to Hunter Biden and various business associates, including his uncle James Biden.

The report, which cited confidential Treasury Department documents, said that the transactions had been “identified for potential financial criminal activity.” Republicans said that the payments raised “criminal financial, counterintelligence and extortion concerns.”

According to the report, Elena Baturina, a Russian billionaire whose late husband was mayor of Moscow, wired $3.5 million in February 2014 to a company co-founded by Biden. The report also said that Biden wired money to people linked to sex trafficking and prostitution in Eastern Europe. –Daily Caller

Russian Billionaire wired Hunter Biden 3 1/2 Million Dollars. This on top of all of the other money he received while Joe was V.P. Crooked as can be, but Fake Mainstream Media wants it to just go away!

Meanwhile, PLA-linked Chinese businessman Ye Jianming – chairman of Chinese energy conglomerate CEFC China Energy – wired hundreds of thousands of dollars to accounts linked to Biden in 2017, according to the GOP report. According to the Caller, Jianming was a top official during the mid-2000s for the China Association for International Friendly Contacts – a PLA front group which engages in “intelligence collection” for Beijing.

“The report…shows that the FBI has been aware of some misconduct for years,” wrote Jordan in the letter to Wray.

Of course, according to Joe Biden, there wasn’t “one single scintilla of evidence” that Hunter did anything wrong.

$3.5 million wire transfer to Hunter Biden from former Mayor of Moscow’s wife, that nobody knows what it was for, is apparently not “improper.” According to Rand Paul it’s criminal! – Supercut: Biden Insists There’s ‘Not One Single Scintilla of Evidence’ of Hunter Improprieties pic.twitter.com/a7f6sqlLzj

As sports were cancelled across the US, and the world, in the spring as the coronavirus pandemic spread, retail trading has effectively replaced sports gambling for millions of young Americans who followed Barstool Sports’ Dave Portnoy headlong into the market, prompting one Fidelity mutual fund manager to complain that Robinhood is going to supplant mutual funds as the investing vehicle of choice for Americans addicted to the adrenaline rush of markets.

As the FT reported Thursday, a similar pattern played out across China, prompting discount electronic brokerage apps to see a flood of new customers and orders. The bonanza of revenue has sent shares of some of these small firms soaring. Trading volume has surged to a staggering $129 billion in daily turnover. The subsequent surge in their publicly-traded shares pushed the valuation of some of these firms past Credit Suisse (though that’s not exactly saying much right now).

As one analyst told FT “the entire sector is going crazy”.

A surge in internet trading by China’s retail investors has boosted the country’s brokers, awarding some of them a valuation in line with the world’s best-known banks. Average daily turnover on China’s stock market has hit Rmb874bn ($129bn) this year, according to data from Goldman Sachs, up nearly 60 per cent from the average of the past five years, as the coronavirus crisis has driven interest in online equity trading. That has ignited shares in brokers, placing them among China’s best-performing stocks of the year. Shares in East Money, an internet trading group largely unknown outside China, have climbed by 84 per cent, giving the company a market capitalisation equivalent to $30.6bn — above that of Credit Suisse. “The entire sector is going crazy . . . all the most expensive brokerage companies are in China,” said Hao Hong, head of research and chief strategist at securities firm Bocom International. East Money shares trade at a price-to-earnings ratio of 69, compared with 14 times for US broker Charles Schwab.

Compared with the institution-dominated US market, China’s mom-and-pop traders comprise a much larger share of turnover, with the FT saying 80% of daily turnover by value is tied to retail trading.

Retail brokerages are run by a range of companies, from the relatively well known Citic Securities and CSC Financial, which have provided online services for mom and pop investors in China for several year, attracting customers with high-tech features such as facial recognition technology, to less established players.

East Money is the best-performing big financial stock in China this year. Though largely unknown outside China, its shares have climbed 84% this year, giving the company a market cap of $30.6 billion, making it more valuable than Credit Suisse.

It derives revenue from its brokerage business and commissions on mutual fund sales. The company’s revenue has increased by Rmb3.3 billion, up two-thirds, compared with last year.

Like their day-trading American counterparts, mom and pop traders in China derive so much enjoyment not just from trading, but from posting on message boards and discussing/debating their ideas with other traders. It’s this “game-ification” element that has made platforms like Robinhood, and its Chinese counterparts, so irresistible to many.

But the recent jump in turnover — prompted in part by coronavirus-related restrictions in the world’s second-biggest economy — comes with a new element: a parallel craze for mobile apps and financial platforms that allow investors to tap into market information and social networks. Liu Jianshun, a Beijing-based retail investor, said he found a “sense of belonging” from debating stock prices on East Money’s chat platform, known as Guba. He uses Guba to try to “talk up stock prices” as well as complain about poor share performance or corporate governance issues.

“East Money has created a virtual platform that replaced the physical brokerage outlets that were once the main gathering place for investors,” said a vice-chairman at one of the company’s rivals. Like elsewhere in the world — from the US to Russia — people in China have turned to the stock market at a time of rising uncertainty over other sources of income and employment due to Covid-19.

Chinese stock market turnover this year peaked in July when daily volumes exceeded Rmb1tn for 15 consecutive days, according to Goldman Sachs, as the CSI 300 index of Shanghai- and Shenzhen-listed shares reached its highest level for 2020. The benchmark is up 13.6 per cent this year.

A combination of idleness and low interest rates has helped to fuel the frenzy.

“If they still have the income, they have nowhere to spend” it, said Kinger Lau, chief China equity strategist at Goldman Sachs. “They spend more time buying stuff online and spend more time…just trading stocks at home.” Low interest rates, a problem faced by savers elsewhere in the world, have also fuelled appetite for stocks. Yu’ebao, a popular money market fund offered by Alibaba’s financial arm Ant Group, pays just over 1.6 per cent in interest. “If you look at Yu’ebao interest rates over the past few months, it’s been falling pretty steadily,” he said. “They [retail investors] are more incentivised to put money into stocks.”

Since mom-and-pop traders need companies to trade, the surge in retail trading has helped fuel a boom in Chinese IPOs, though a Trump Administration push to force Chinese companies to de-list from US exchanges unless they agree to more oversight has also contributed to this trend.

That same demand has charged China’s booming initial public offering markets. Shenzhen-listed shares of Contec Medical Systems closed up more than 1,000 per cent in its debut session last month after regulators relaxed rules on the city’s tech-focused ChiNext board.

Of course, Chinese traders are probably much more willing to throw cash at the market giving Beijing’s history of taking draconian steps like arresting short sellers if markets get turbulent. So buying stocks is like playing in casino where you really can’t lose.

via ZeroHedge News https://ift.tt/3hYyZsL Tyler Durden

We have been discussing the rising intolerance for conservative, libertarian, and Republican students and faculty on campuses across the country. Faculties rarely hire conservative or libertarian professors; journals rarely published studies from conservative authors. As the number of conservative faculty members diminish or disappear on faculties, schools appear to be carrying out the same bias in student admissions. The Harvard Crimson has finished its annual survey of the incoming class of students and found that the already small population of conservative and Republican students has been cut by as much as half.

The Crimson survey covered over 76 percent of the Harvard College Class of 2024 and found that the class contained 72.4 percent who self-identify as either “very liberal” or “somewhat liberal.” Only 7.4 percent self-identify as “very conservative” or “somewhat conservative.” Likewise, 88.9 percent view President Donald Trump as strongly or somewhat unfavorable with 80.7 percent falling in the “strongly unfavorable” category. Only 4.7 percent view Trump “somewhat” or “strongly” favorable.

Note that over 40 percent of this country view Trump favorably and the vast majority view themselves as holding either conservative or moderate views. It is demonstrably absurd to argue that this virtual absence of conservative students is somehow the result of accident and not design.

For years, faculty members pretended that there was not an ideological bias in faculty selection as the number of conservative and libertarian faculty members dropped to near zero on many faculties. Less than ten percent of faculty in all schools identify as conservative and Democrats outnumber Republicans by over ten times on faculties. In some schools this ratio goes up to roughly 30 to 1.

Liberal faculties routinely dismiss candidates who advance opposing views as intellectually unsound or simply not as intellectually “promising” as more liberal candidates. The bias is evident on every level. Faculty members tend to exclude conservatives from presentations, publications, and citations. The result is an echo chamber in academia that feeds upon itself.

Now we are seeing the same downward trend in admissions where conservative or libertarian students are being relegated to lower ranked schools. This bias has also become evident, not surprisingly, in classrooms. A Yale poll found that seventy percent of students said that they experienced political bias and the same poll said that the students only believe one percent of their faculty were conservative. A poll at Pomona found nine out of ten students said that “the campus climate prevents them from saying something others might find offensive.” Nearly two-thirds of faculty members felt the same. Seventy-five percent of conservative and moderate students strongly agree that the school climate hinders their free expression.

The impact of this bias is devastating for higher education. Faculty members are using their majority on faculties to exclude potential colleagues with opposing views, the very type of bias once used against not just liberals but minorities seeking entry to faculties. The result is that we are creating a bifurcated educational system where conservatives can only gain entry to top schools by heading their political views or espousing liberal positions. I was shocked when one of my kids (who is a moderate) was invited for an interview by one of the top colleges in the country. After sitting down, the interviewer proceeded immediately to go into a diatribe against Trump and to self-identify a liberal advocate. He felt that the interviewer wanted him to echo those views.

As shown in the Harvard survey, “diversity” at many schools now runs along a spectrum from extreme to mainstream liberal views with a statistically inconsequential number of conservatives or libertarians. This has been a uniform trend for many years in both the selection of faculty and students. It is a mockery to pretend that this is the result of anything other than systemic bias in academia.

via ZeroHedge News https://ift.tt/3i1Yb1o Tyler Durden

Week 2 Sunday Night Football Ratings Plunge 17% From Week 1’s Already “Steep Decline” Tyler Durden

Thu, 09/24/2020 – 14:25

We had already documented that Week 1 NFL ratings saw a “steep decline” from last year’s comparable ratings. In an article we published about a week ago, we questioned whether or not that could have something to do with the NFL focusing more on politics than – well, actually playing football.

Week 2 saw no respite for the NFL. Last Sunday’s Seahawks versus New England Patriots game – one of the premier matchups in all of the NFL – saw only 12.22 million viewers on NBC, according to the Daily Caller.

The numbers mark a 17% decline from Week 1, which saw roughly 7 million viewer plunge from Week 1 of the 2019 season.

As we noted, Week 1’s Sunday night’s game also featured popular teams: “America’s Team” – the Dallas Cowboys, and the newly moved Los Angeles Rams.

But the game posted a 4.7 among the key Adult 18-49 demographic with 14.81 million viewers. For comparison, last year’s Patriots vs. Steelers Sunday night opener had 22.2 million viewers. This total was generally in-line with the opener the year before, indicating that even with West Coast viewers factored in, this season’s ratings have been decimated.

The Daily Caller took their best shot at explaining what the issue could be: “It no longer feels like the NFL is about winning and losing games. It feels like it’s about lecturing fans around the clock. Average Americans don’t want to be lectured by millionaire athletes. They just don’t!”

And as we asked about 10 days ago: what could the NFL be doing wrong?

via ZeroHedge News https://ift.tt/2GbhpV5 Tyler Durden

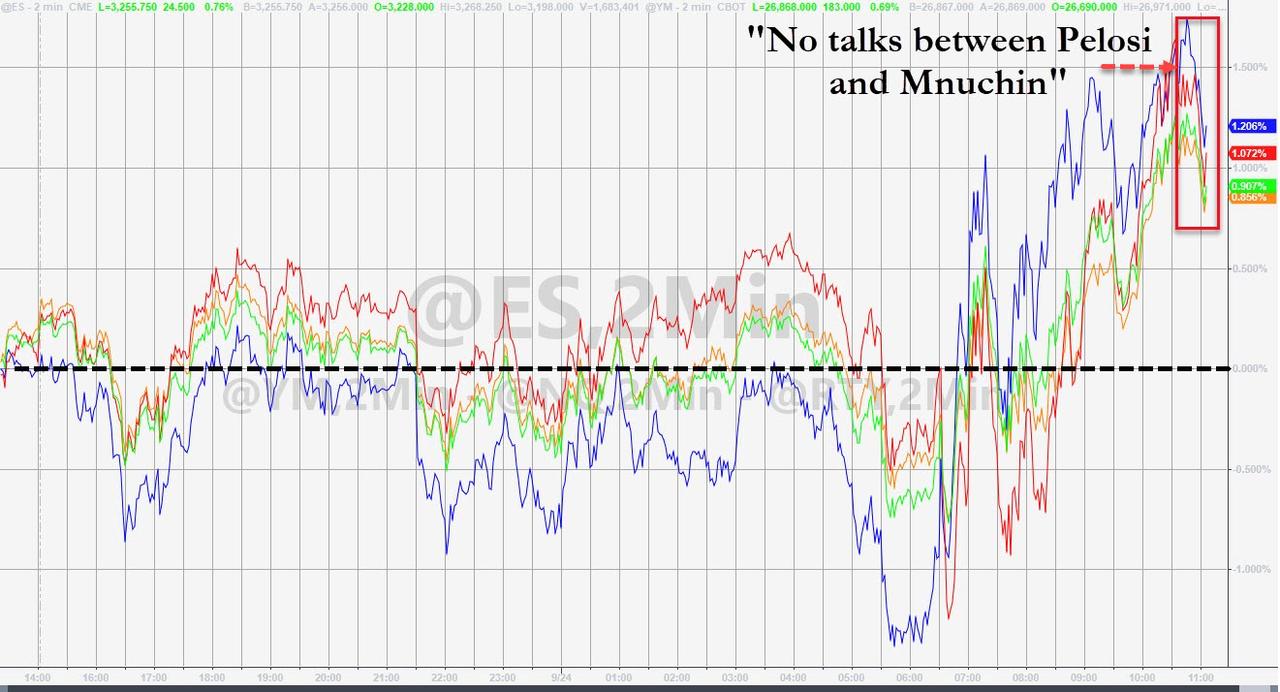

Stock Rally Reverses On Report There Are “No Talks” Scheduled Between Mnuchin, Pelosi Tyler Durden

Thu, 09/24/2020 – 14:15

With traders (and the Fed) desperate for some fiscal stimulus – now that Powell appears to have tapped out – earlier today stocks hit session highs on speculation that talks about a new round of economic stimulus will resume. As Bloomberg reported, the S&P 500 extended gains after House Speaker Pelosi said she spoke with Treasury Secretary Steven Mnuchin yesterday and expressed hope that there would be another round of negotiations.

This followed Congressional tesimotny from Mnuchin, who earlier on Thursday said that a targeted pandemic relief package is “still needed.”

However, today’s rally peaked the moment Politico’s Jake Sherman reported that “no covid relief talks are scheduled at this time” between Mnuchin and Pelosi…

… dousing excitement that another fiscal bill may be on deck.

In other words, no change, although with the dollar trading near session lows after it early rampage, it appears that downward momentum has for now been reversed.

Alas, that does not answer the $64 trillion question: who will blink first, Powell or Pelosi, and linked to that: what is the strike price of the Pelosi Put? In other words, does the S&P have to drop much more before the top House Democrat agrees to the republican bid of a $1.5 trillion stimulus, or will she hold out for the $2.2 trillion Democrat ask, no matter where the stock market is. That said, one would assume that Democrats would be delighted to see a stock market crash ahead of the election: after all, Trump has repeatedly confirmed that he views stocks as the only “objective” barometer of his administration, which is Democrats would be delighted if said barometer were to be much, much lower.

via ZeroHedge News https://ift.tt/2FPjBlH Tyler Durden

Wisconsin Authorities Investigate Absentee Ballots Found In Ditch, As FBI Probes Discarded Pro-Trump Ballots In PA Tyler Durden

Thu, 09/24/2020 – 14:11

Police in the swing-state of Wisconsin are investigating how three trays of mail which included absentee ballots ended up in a ditch, after the mail was found at 8 a.m. Tuesday morning near a highway before it was immediately turned over to the US Postal Service, according to Fox 11.

“The United States Postal Inspection Service immediately began investigating and we reserve further comment on this matter until that is complete,” said USPS spokesman Bob Sheehan in a statement.

The incident comes a mere five weeks before the presidential election, which has been steeped in partisan bickering over the system of mail-in and absentee ballots and wavering trust in the alternate system.

Due to the coronavirus pandemic, which marked a grim milestone this week of over 200,000 deaths in the U.S., voters are expected to cast ballots by mail in record numbers.

“We expect more than 3 million Wisconsin residents to vote in the November election, which means even more first-time absentee by mail voters,” Meagan Wolfe, the elections commission’s administrator, said in a statement earlier this month. –Fox News

Prior to the pandemic, just 6% of Wisconsin voters cast absentee ballots by mail – however during the state’s April primaries, that number jumped to 60%, when 1.1 million out of 1.55 million votes were conducted through the postal service. During the August partisan primary, Wolfe said that 82% of the 867,000 votes cast were via absentee ballot.

During said primaries, thousands of voters across the state complained that they never received the absentee ballots they requested. In one case, a Milwaukee postal worker said that three bins of absentee ballots had never been delivered.

Meanwhile in Pennsylvania, the FBI and the office of the United States Attorney found nine discarded mail-in ballots from members of the military, all cast for President Trump.

According to the DOJ:

Since Monday, FBI personnel working together with the Pennsylvania State Police have conducted numerous interviews and recovered and reviewed certain physical evidence. Election officials in Luzerne County have been cooperative. At this point we can confirm that a small number of military ballots were discarded. Investigators have recovered nine ballots at this time. Some of those ballots can be attributed to specific voters and some cannot. All nine ballots were cast for presidential candidate Donald Trump.

On Thursday, President Trump told Fox News’ Biran Kilmeade on his radio show that mail-in ballots are a “horror show” and that missing ballots are “emblematic of thousands of ballots” which could get lost this year.

Trump tells Brian Kilmeade on “Fox News Radio” that “these ballots are a horror show.” pic.twitter.com/6MppvzWvD4

ECB Pays European Banks 1% To Give Them €174 Billion Tyler Durden

Thu, 09/24/2020 – 13:40

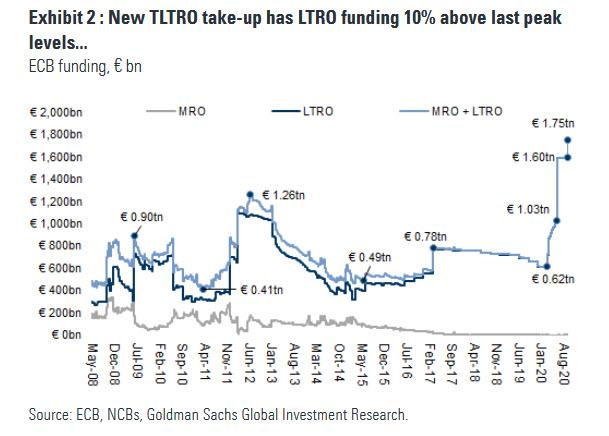

Today was one of those iconic days that defines the new centrally-planned paranormal, where as a result of such monetary abortions as negative rates, the ECB pays European banks to give them money. We are talking of course about TLTRO day, when the ECB lends to banks at rates as low as -1% to try to encourage them to lend to households which are about to be locked down again, and the last thing they want is more debt.

And so, after €1.3 trillion was the taken-up last time three months ago, today Euro-zone banks took up just €174.5 billion, or $203 billion, in the latest TLTRO even as the ECB gave banks every possible incentive to keep lending to the pandemic-stricken economy, including rates as low as -1%. In other words, the ECB is paying banks to take cash which they should then lend out, at least in theory. According to Bloomberg, this suggests that “most lenders now consider themselves well-financed.”

The latest facility brings the total TLTRO amount outstanding to €1.75 trillion…

… and was priced at -1% for Year 1, and -0.5% for Years 2-3. As such these loans fully compensate banks for the official policy rate of minus 0.5%, which works as a charge on their reserves and erodes their profitability. Without TLTROs as a counterbalance, that could eventually curb lending. Instead the ECB is effectively paying banks to lend. On the other hand, with the ECB almost fully offsetting the punitive effects of negative deposit rates, one wonders why the ECB still pretends to have NIRP?

The TLTRO3 bids came from 388 banks, and the takeup was at the high end of economists’ expectations, if well below the June TLTRO. The high participation and ample usage confirms that there is still no stigma associated with use of the facility (that may change).

A couple of observations from Goldman:

Overall, this is a moderate level of take-up, compared to the previous (June) auction of €1.3 tn by 742 banks, and total amount of ECB funding outstanding (€1.75 tn);

The net new addition of liquidity to the system is around €158 bn, as some €17 bn was repaid / rolled-off. This brings total ECB funding usage to a new record of €1.75 tn. By way of context, during the 2008/9 GFC usage was <€1 tn, while the 2011/12 sovereign crisis saw usage rise to €1.26 tn.

Further capacity exists. On current collateral terms, this facility could still be scaled up further over the coming auctions.

According to Bloomberg, the loans will likely push excess liquidity in the euro zone above 3 trillion euros for the first time on record.

According to Piet Christiansen, chief strategist at Danske Bank A/S in Copenhagen, excess liquidity will rise by another 600 billion euros to 800 billion euros by the summer of 2021.

To be sure, flooding the market with all this negative-yielding debt has adverse consequences besides merely blowing asset bubbles. According to Bloomberg, the ECB could undermine its own influence over short-term market rates. Three-month Euribor – the rate at which banks can theoretically borrow from one another – fell to a record low of minus 0.508% this week.

When it dropped below the ECB’s policy rate last week, that was a phenomenon that had happened only once before, in August 2019, shortly before the central bank cut its deposit rate. Euribor futures, which reflect the three-month benchmark rate held small gains following the announcement, a sign borrowing costs may fall further.

A record €3 trillion in excess liquidity however is probably not enough for Europe’s bank and more stimulus is coming. The ECB projects that the economy will contract 8% this year, and the inflation rate has fallen below zero for the first time in four years. Rising coronavirus infections could worsen the outlook. Economists predict the €1.35 trillion pandemic bond-buying program will be expanded again this year. Meanwhile, markets aren’t pricing another 10 basis-point rate cut until October 2021.

In any event, Goldman concludes that this auction was supportive of overall financial stability, “and on the margin supportive of bank revenue. The next auction, on the same terms, is on December 10, with subsequent auctions running quarterly until March 2021.” A more sarcastic take comes from Rabobank’s Michael Every, who writes:

The ECB will today meanwhile be carrying out another round of TLTRO’s, where it lends to banks at rates as low as -1% to try to encourage them to lend to households about to be locked down again and firms about to see the economy close again. EUR1.3 trillion was the take-up last time three months ago, but it is likely to be less this time round.

Every’s conclusion: “This is what central banking now looks like today.” But it’s not just the ECB. As Every adds:

The US is probably also on the verge of another huge fiscal stimulus package; and not making many mainstream headlines yet, the Fed’s Mester was yesterday muttering about the potential for Fed ‘digital dollars’ and depositing them directly into household accounts in the face of a downturn – so crypto helicopter money.

And in case it wasn’t clear the first time, a snarky Every doubles down that “this is what central banking also now looks like.”

via ZeroHedge News https://ift.tt/2G9B3Rj Tyler Durden

Since then, I have read many sarcastic comments on blogs or social media about the LPPLS model, and even econophysics as a scientific discipline.

How Nature Works

Somehow, the name “econophysics” can be misleading, as it is an interdisciplinary axis of research that was put forward by physicists like Per Bak or Didier Sornette. The study of complex systems has implications in almost every branch of science (e.g. seismology, cosmology, climatology, biology, anthropology, sociology, economics), and what is striking is the fact that so many systems exhibit very similar patterns also known as self-organized criticality. If humans are part of nature, then it seems legit to assume that their complex interactions obey to natural laws.

Thinking outside the box has always been essential, including for scientists or traders. While most economists postulate how the economy is supposed to work, and then built beautiful but meaningless theoretical frameworks on top of that, physicists like Bak argue that the right intellectual approach is to understand how nature works first, before trying to build any predictive model.

The LPPLS model is all about that. When a financial market is overwhelmingly dominated by a narrative, with all participants sharing the same opinion, then it tends toward a form of swarm intelligence, a singularity. But such a state is highly unstable and the system because vulnerable as there is no support since all investors have capitulated.

Researchers like Sornette have shown that such moments are characterized by typical patterns like an acceleration of fluctuations, as the fight between bulls and bears is getting fiercer.

What the Roller Coaster Is Telling Us

While one could argue that US stock market has been overvalued since 2015, the premise of the mania started in 2018. But, the stress provoked by the Fed balance sheet normalization and the fears of a trade war with China led to a severe correction during Fall 2018.

Since 2009, investors knew that the central banks could intervene if necessary. And this is what happened at the end of 2018. The Fed ended the normalization process, they started the “non-QE” REPO injections a few months later, and Donald Trump promised “a huge trade deal” with China. While many investors had turned bearish in December 2018, those actions led to a big short squeeze during the following months.

The aggressive rebound of 2019 was a massive positive feedback loops for participants as they got the confirmation that the Fed would do “whatever it takes” to support capital markets.

What happened during the first half of 2020 can be seen as a “bis repetita” event, but on a larger scale. Speculative behavior had started a few months before the end 2019, and things got worse in January and February with media talking about “the unstoppable tech bull run”.

The Covid-19 sell-off was a bigger test for the “Fed put” narrative (aka “stocks only go up”). However, despite a short but intense period of stress, many participants did not sell that much as they knew that central bankers might act quickly. And they were right, the trillion dollars stimulus and the infinite QE programs led to an even bigger bounce. In other words, another positive feedback loop.

As retail investors massively entered in the market after March, it seems legit to think that we had finally reached the final stage of a speculative mania that many people had expected for years. During August, the last bears capitulated, and everyone turned bullish on equities as it looked like “stocks would not go down again”.

Said differently, the dominant narrative has won the intersubjective war. However, this was not good news for bulls.

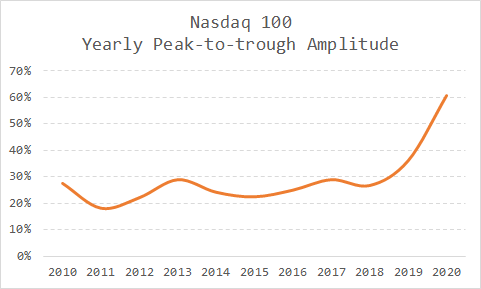

From a statistical perspective, long-term fluctuations have accelerated, as evidenced by the peak-to-trough log variation of the Nasdaq (see chart above). Somehow, it tells us that the market was exhibiting the patterns described by Sornette and other econophysicists.

Simulations and Results

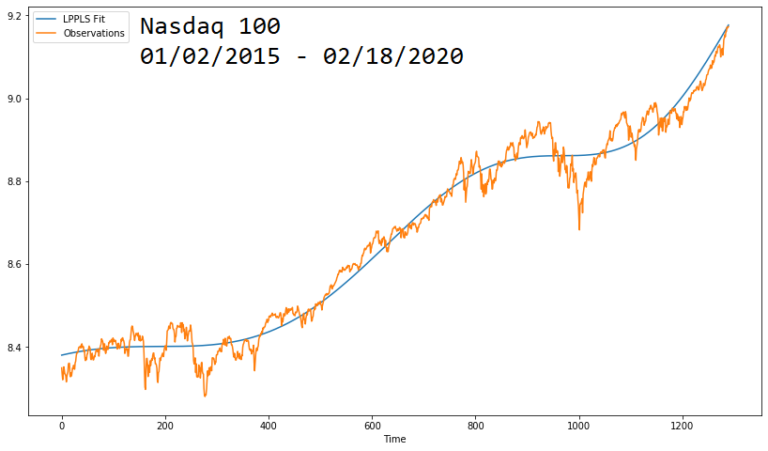

Even though tech valuations were already rising to the Moon at the beginning of 2020, it is interesting to note that the LPPLS model did not suggest the bubble had accelerated at a critical rate in February, and thus did not expected a near-term crash. The February-March sell-off was actually caused by an external factor: the pandemic and lockdowns in major countries all over the world.

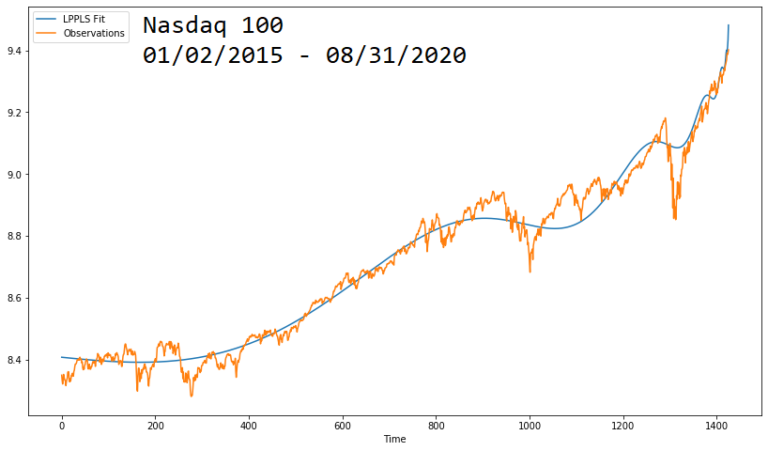

When I ran the LPPLS model in July, it suggested that the Nasdaq was driven by euphoria since March, expecting a crash “by the end of the summer” (i.e. mid-September). I decided to run it again at the end of August as I felt that the bull run had accelerated, and the conclusion was that the market could crash “any time”.

Therefore, the recent sell-off on tech that started on September 3 should not come as a surprise. This sudden move was not cause by any external event or any news, but by pure endogenous causes (i.e. large participants starting to sell). And this is what the LPPLS model told us.

What’s Next?

At this stage, the key question for everyone is, will the market crash more severely soon?

People might have noted that there is a strong support force on the market. This could be explained by the fact that the retail army seems to have regarded this correction as screaming-buy opportunity, opening new record positions on out-of-the-money short-term call options, and exacerbating the impact of the so-called gamma squeeze.

While some professional investors have turned more cautious, with CTAs exhibiting net short positions, the Fed has just decided to step in so as to try to stop the selling forces a few weeks before the election. If you are not convinced, then how do you explain the 17 media interventions of Fed speakers this week?

Even if the Fed put has always been the major pillar of the dominant narrative, other catalysts like “vaccine optimism”, “V-shaped recovery optimism”, or “trade deal optimism”, have significantly weakened. Thus, all that remain in this happy bull’s world is the intersubjective trust in the Federal Reserve ability to magically inflate equities.

One Flew Over the Cuckoo’s Nest

To conclude, I would like to remind that the prediction of the LPPLS was right, as the bull run ended at the beginning of September.

Has the trend been broken? I think it has, as the market is struggling to come back to all-time highs. More interestingly, the Nasdaq has made new lows almost every week since the end of August, suggesting that finally the powerful bullish trend was not invincible (Do you agree Dave Portnoy?).

Of course, the action of the Fed will be decisive for the evolution of the market until the end of the year (or at least until November 3).

But the thing is, it is a bubble. And like all bubbles in human history, it will pop. And there will be no happy ending.

No need to be a rock-star physicist to understand that.

via ZeroHedge News https://ift.tt/2Evukkt Tyler Durden

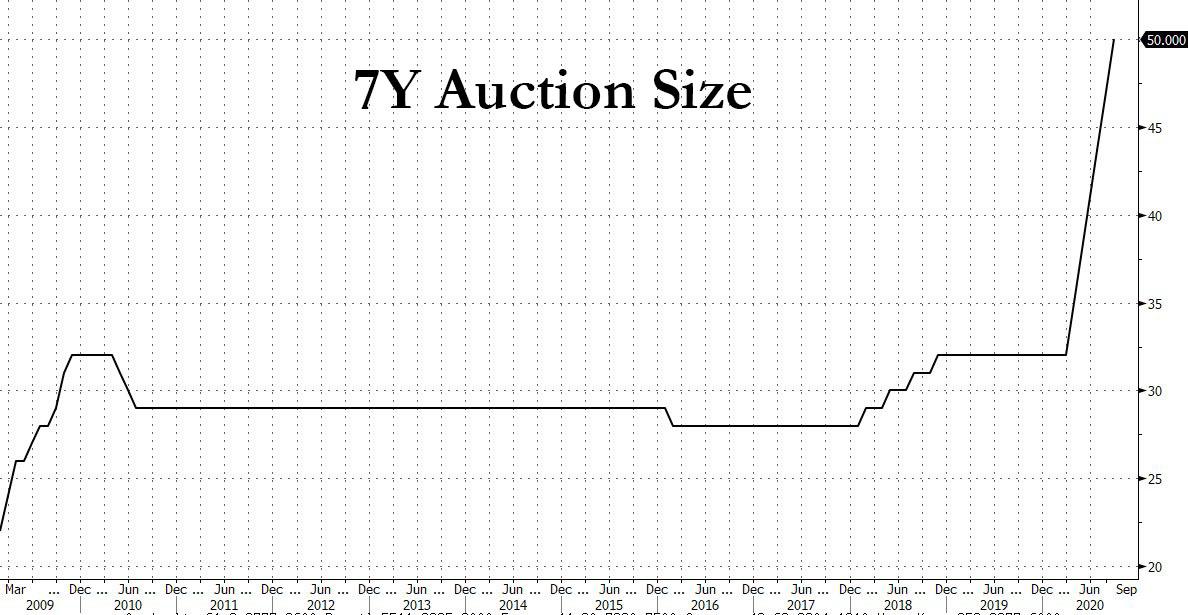

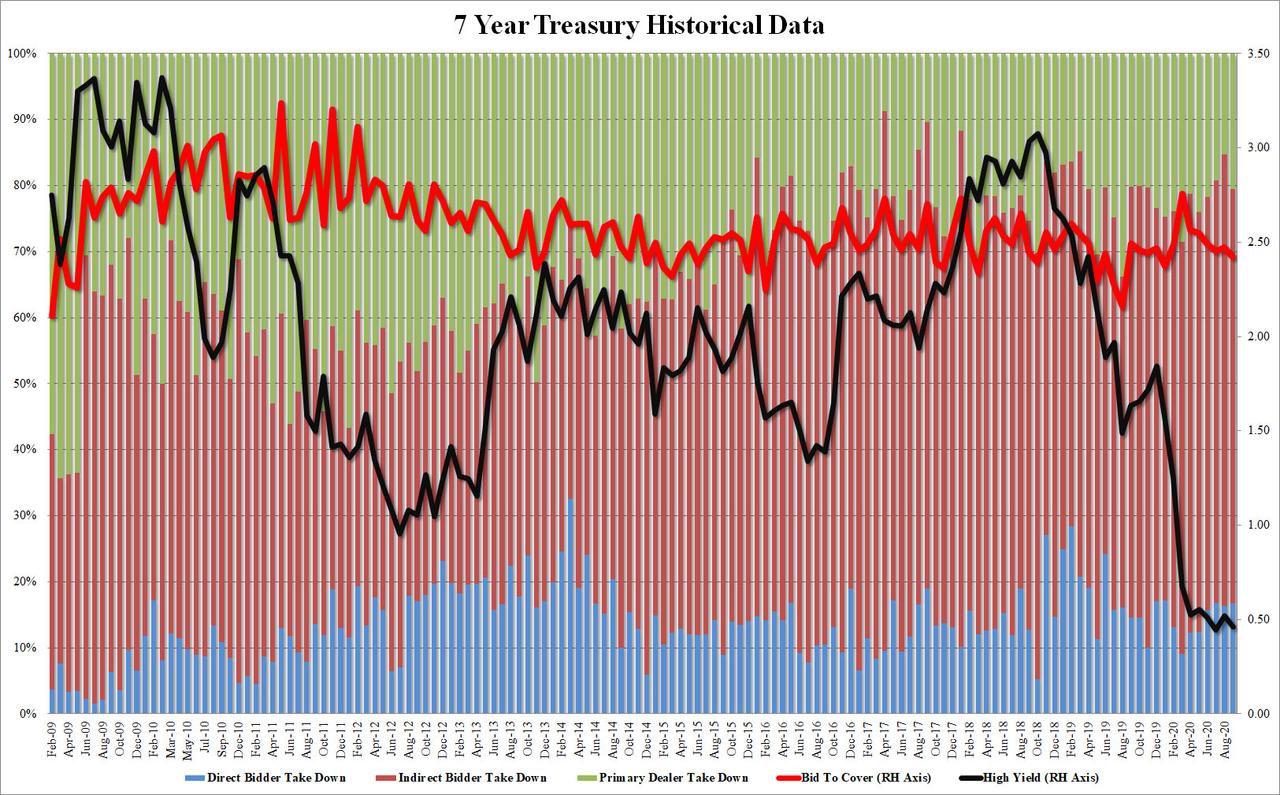

Another Record-Sized Auction As Treasury Sells $50BN in Tailing 7-Year Paper Tyler Durden

Thu, 09/24/2020 – 13:14

After two solid, stopping through auctions, moments ago the US Treasury completed the week’s coupon issuance with the auction of another record-sized treasury sale in the form of $50 billion in 7 year notes, up from $47 billion last month.

Unlike the week’s previous two auctions, the high yield of 0.462% was not the lowest on record: while it was below last month’s 0.591%, it was above the all time low hit in July when the auction printed 0.446%. And amid today’s listless Treasury activity, the auction tailed the When Issued 0.462% by 0.1bps.

The Bid to Cover was barely changed from last month, although at 2.42 it was the lowest since January, and well below the 2.55 six auction average.

The internals were also a bit on the weak side, with Indirects taking down 62.9%, below the 64.5% recent average. And with Directs taking down 16.7%, virtually unchanged from last month and higher than recent average, Dealers were left with 20.5%, the highest since June.

Altogether, another solid if not spectacular auction, with the most notable feature being that the bigger the auction size, the lower Treasury yields drop in a bond market that has now been fully taken over by the Fed.

via ZeroHedge News https://ift.tt/307LCf7 Tyler Durden

President Trump’s Niece Sues Family Claiming She Was “Defrauded” Of Inheritance Tyler Durden

Thu, 09/24/2020 – 12:55

With her uncle Robert now deceased, President Trump’s niece, Mary Trump, has committed to her scorched-earth campaign to embarrass her uncle, the president, in a way that – she probably hoped – might stir up legal action and possibly impact the election.

Various investigations into President Trump’s financial dealings continue, but apparently Mary Trump – who reported in her book that her uncle once complimenter “her figure” by exclaiming ‘Wow, Mary. You’re stacked’ after seeing her in a bathing suit – didn’t provoke the response she was hoping for.

Apparently unwilling to give up just yet, she and her legal team have decided to file a lawsuit against her uncle accusing him and his siblings of conspiring to keep her from receiving her share of her inheritance. Mary is the daughter of Trump’s deceased brother Freddy, the family’s purported black sheep, who died of alcoholism-related complications in his early 40s.

CNN, which got the scoop on the lawsuit filing, reports that in the filing, Mary Trump’s lawyers argue that she was defrauded by her relatives not out of spite but simply because that’s what they do.

In the lawsuit, filed in New York state court against the President, his sister Maryanne Trump Barry and the estate of their late brother Robert Trump, Mary Trump asserts that for the Trumps, “fraud was not just the family business—it was a way of life.”

The lawsuit accuses her two uncles and her aunt, a retired federal judge, of conspiring amongst themselves and with several other parties, including a trustee appointed to act on Mary’s behalf, to give her “a stack of fraudulent valuations” and force her to sign a settlement agreement that “fleeced her of tens of millions of dollars or more.”

“Rather than protect Mary’s interests, they designed and carried out a complex scheme to siphon funds away from her interests, conceal their grift, and deceive her about the true value of what she had inherited,” the lawsuit says.

Other accusations were initially detailed in Mary Trump’s book: “Too Much and Never Enough: How My Family Created the World’s Most Dangerous Man.” Unsurprisingly, it has been a best-seller.

CNN relitigates the allegations in detail in its report (you can find that here if you’re curious), but the gist is that her uncles Donald and Robert worked together with her aunt Maryanne Trump Barry to become the sole executors of their father’s estate. They then used all sorts of tricks and schemes, according to the lawsuit, to siphon money away from her late father Fred Trump Jr.’s estate, disguising some of the dealings as legitimate business.

Trump’s legal team has yet to comment on the news. We suspect a solid settlement and an NDA will soon be signed, and Mary Trump will go back to being the relatively anonymous niece of the president. Because if nothing else, this lawsuit shows why Trump started working with the media in the first place.

via ZeroHedge News https://ift.tt/2G380iC Tyler Durden