Syria & Russia Thwart US Oil Blockade With Massive Fuel Convoy To Northeast Syria Tyler Durden

Sat, 06/13/2020 – 17:15

To the consternation of the West, Iran and Russia have increasingly turned from assisting Assad’s military effort to aiding Syria as it struggles to survive sanctions and a collapsing economy.

At a moment US special forces still occupy the bulk of oil and gas fields in northeast Syria, also in support of the Kurdish-led SDF, Damascus has ramped up efforts at busting past US lines with Russia’s help. It should be underscored that this is all happening within UN-recognized Syrian sovereign territory.

“On Saturday, more than two thousand oil tanks coming from the Syrian coast, arrived in Al-Qamishli to help the citizens in northeastern Syria,” Beirut-based war monitor al-Masdar News reports.

Iranian oil has been supplying the country via the second largest port city of Tartous, after last year a national fuel shortage resulted in sometimes miles-long lines at gas stations, amid the broader economic crisis, which is currently witnessing runaway inflation.

RT Arabic published footage of a large oil convoy as it traveled along the M-4 Highway to make deliveries from a coastal refinery to al-Qamishli, very near US-occupied territory where American and Russian troops have squared off lately.

RT Arabic reported drivers in the convoy as saying: “the U.S. Caesar sanctions have not been imposed on the oil and gas sector yet,” according to a translation.

Another added that “the results will be disastrous for the Syrian people if these sanctions are applied to the energy sector.”

Over the past months there’s been multiple incidents at checkpoints in northeast Syria involving US and Russian/Syrian convoys in direct stand-offs.

The Caesar sanctions are expected to go into effect later this month, tightening the noose further on Syria’s already war-ravaged and sanctioned population, made worse by the ongoing economic crisis in neighboring Lebanon.

via ZeroHedge News https://ift.tt/2MX9ACM Tyler Durden

Sometimes it seems life can’t get any worse in this country. Already in terror of a pandemic, Americans have lately been bombarded with images of grotesque state-sponsored violence, from the murder of George Floyd to countless scenes of police clubbing and brutalizing protesters.

Our president, Donald Trump, is a clown who makes a great reality-show villain but is uniquely toolless as the leader of a superpower nation. Watching him try to think through two society-imperiling crises is like waiting for a gerbil to solve Fermat’s theorem. Calls to “dominate” marchers and ad-libbed speculations about Floyd’s “great day” looking down from heaven at Trump’s crisis management and new unemployment numbers (“only” 21 million out of work!) were pure gasoline at a tinderbox moment. The man seems determined to talk us into civil war.

But police violence, and Trump’s daily assaults on the presidential competence standard, are only part of the disaster. On the other side of the political aisle, among self-described liberals, we’re watching an intellectual revolution. It feels liberating to say after years of tiptoeing around the fact, but the American left has lost its mind. It’s become a cowardly mob of upper-class social media addicts, Twitter Robespierres who move from discipline to discipline torching reputations and jobs with breathtaking casualness.

The leaders of this new movement are replacing traditional liberal beliefs about tolerance, free inquiry, and even racial harmony with ideas so toxic and unattractive that they eschew debate, moving straight to shaming, threats, and intimidation. They are counting on the guilt-ridden, self-flagellating nature of traditional American progressives, who will not stand up for themselves, and will walk to the Razor voluntarily.

Now, this madness is coming for journalism. Beginning on Friday, June 5th, a series of controversies rocked the media. By my count, at least eight news organizations dealt with internal uprisings (it was likely more). Most involved groups of reporters and staffers demanding the firing or reprimand of colleagues who’d made politically “problematic” editorial or social media decisions.

The New York Times, the Intercept, Vox, the Philadelphia Inquirer, Variety,and others saw challenges to management.

Probably the most disturbing story involved Intercept writer Lee Fang, one of a fast-shrinking number of young reporters actually skilled in investigative journalism. Fang’s work in the area of campaign finance especially has led to concrete impact, including a record fine to a conservative Super PAC: few young reporters have done more to combat corruption.

Yet Fang found himself denounced online as a racist, then hauled before H.R. His crime? During protests, he tweeted this interview with an African-American man named Maximum Fr, who described having two cousins murdered in the East Oakland neighborhood where he grew up. Saying his aunt is still not over those killings, Max asked:

I always question, why does a Black life matter only when a white man takes it?… Like, if a white man takes my life tonight, it’s going to be national news, but if a Black man takes my life, it might not even be spoken of… It’s stuff just like that that I just want in the mix.

Shortly after, a co-worker of Fang’s, Akela Lacy, wrote, “Tired of being made to deal continually with my co-worker @lhfang continuing to push black on black crime narratives after being repeatedly asked not to. This isn’t about me and him, it’s about institutional racism and using free speech to couch anti-blackness. I am so fucking tired.” She followed with, “Stop being racist Lee.”

Like many reporters, Fang has always viewed it as part of his job to ask questions in all directions. He’s written critically of political figures on the center-left, the left, and “obviously on the right,” and his reporting has inspired serious threats in the past. None of those past experiences were as terrifying as this blitz by would-be colleagues, which he described as “jarring,” “deeply isolating,” and “unique in my professional experience.”

To save his career, Fang had to craft a public apology for “insensitivity to the lived experience of others.” According to one friend of his, it’s been communicated to Fang that his continued employment at The Intercept is contingent upon avoiding comments that may upset colleagues. Lacy to her credit publicly thanked Fang for his statement and expressed willingness to have a conversation; unfortunately, the throng of Intercept co-workers who piled on her initial accusation did not join her in this.

I first met Lee Fang in 2014 and have never known him to be anything but kind, gracious, and easygoing. He also appears earnestly committed to making the world a better place through his work. It’s stunning that so many colleagues are comfortable using a word as extreme and villainous as racist to describe him.

Though he describes his upbringing as “solidly middle-class,” Fang grew up in up in a diverse community in Prince George’s County, Maryland, and attended public schools where he was frequently among the few non-African Americans in his class. As a teenager, he was witness to the murder of a young man outside his home by police who were never prosecuted, and also volunteered at a shelter for trafficked women, two of whom were murdered. If there’s an edge to Fang at all, it seems geared toward people in our business who grew up in affluent circumstances and might intellectualize topics that have personal meaning for him.

In the tweets that got him in trouble with Lacy and other co-workers, he questioned the logic of protesters attacking immigrant-owned businesses “with no connection to police brutality at all.” He also offered his opinion on Martin Luther King’s attitude toward violent protest (Fang’s take was that King did not support it; Lacy responded, “you know they killed him too right”). These are issues around which there is still considerable disagreement among self-described liberals, even among self-described leftists. Fang also commented, presciently as it turns out, that many reporters were “terrified of openly challenging the lefty conventional wisdom around riots.”

Lacy says she never intended for Fang to be “fired, ‘canceled,’ or deplatformed,” but appeared irritated by questions on the subject, which she says suggest, “there is more concern about naming racism than letting it persist.”

Max himself was stunned to find out that his comments on all this had created a Twitter firestorm. “I couldn’t believe they were coming for the man’s job over something I said,” he recounts. “It was not Lee’s opinion. It was my opinion.”

By phone, Max spoke of a responsibility he feels Black people have to speak out against all forms of violence, “precisely because we experience it the most.” He described being affected by the Floyd story, but also by the story of retired African-American police captain David Dorn, shot to death in recent protests in St. Louis. He also mentioned Tony Timpa, a white man whose 2016 asphyxiation by police was only uncovered last year. In body-camera footage, police are heard joking after Timpa passed out and stopped moving, “I don’t want to go to school! Five more minutes, Mom!”

“If it happens to anyone, it has to be called out,” Max says.

Max described discussions in which it was argued to him that bringing up these other incidents now is not helpful to the causes being articulated at the protests. He understands that point of view. He just disagrees.

“They say, there has to be the right time and a place to talk about that,” he says. “But my point is, when? I want to speak out now.” He pauses. “We’ve taken the narrative, and instead of being inclusive with it, we’ve become exclusive with it. Why?”

There were other incidents.

The editors of Bon Apetit and Refinery29both resigned amid accusations of toxic workplace culture. The editor of Variety, Claudia Eller, was placed on leave after calling a South Asian freelance writer “bitter” in a Twitter exchange about minority hiring at her company. The self-abasing apology (“I have tried to diversify our newsroom over the past seven years, but I HAVE NOT DONE ENOUGH”) was insufficient. Meanwhile, the Philadelphia Inquirer’s editor, Stan Wischowski, was forced out after approving a headline, “Buildings matter, too.”

In the most discussed incident, Times editorial page editor James Bennet was ousted for green-lighting an anti-protest editorial by Arkansas Republican Senator Tom Cotton entitled, “Send in the troops.”

I’m no fan of Cotton, but as was the case with Michael Moore’s documentary and many other controversial speech episodes, it’s not clear that many of the people angriest about the piece in question even read it. In classic Times fashion, the paper has already scrubbed a mistake they made misreporting what their own editorial said, in an article about Bennet’s ouster. Here’s how the piece by Marc Tracy read originally (emphasis mine):

James Bennet, the editorial page editor of The New York Times, has resigned after a controversy over an Op-Ed by a senator calling for military force against protesters in American cities.

James Bennet resigned on Sunday from his job as the editorial page editor of The New York Times, days after the newspaper’s opinion section, which he oversaw, published a much-criticized Op-Ed by a United States senator calling for a military response to civic unrest in American cities.

Cotton did not call for “military force against protesters in American cities.” He spoke of a “show of force,” to rectify a situation a significant portion of the country saw as spiraling out of control. It’s an important distinction. Cotton was presenting one side of the most important question on the most important issue of a critically important day in American history.

As Cotton points out in the piece, he was advancing a view arguably held by a majority of the country. A Morning Consult poll showed 58% of Americans either strongly or somewhat supported the idea of “calling in the U.S. military to supplement city police forces.” That survey included 40% of self-described “liberals” and 37% of African-Americans. To declare a point of view held by that many people not only not worthy of discussion, but so toxic that publication of it without even necessarily agreeing requires dismissal, is a dramatic reversal for a newspaper that long cast itself as the national paper of record.

Incidentally, that same poll cited by Cotton showed that 73% of Americans described protecting property as “very important,” while an additional 16% considered it “somewhat important.” This means the Philadelphia Inquirer editor was fired for running a headline – “Buildings matter, too” – that the poll said expressed a view held by 89% of the population, including 64% of African-Americans.

(Would I have run the Inquirer headline? No. In the context of the moment, the use of the word “matter” especially sounds like the paper is equating “Black lives” and “buildings,” an odious and indefensible comparison. But why not just make this case in a rebuttal editorial? Make it a teaching moment? How can any editor operate knowing that airing opinions shared by a majority of readers might cost his or her job?)

The main thing accomplished by removing those types of editorials from newspapers — apart from scaring the hell out of editors — is to shield readers from knowledge of what a major segment of American society is thinking.

It also guarantees that opinion writers and editors alike will shape views to avoid upsetting colleagues, which means that instead of hearing what our differences are and how we might address those issues, newspaper readers will instead be presented with page after page of people professing to agree with one another. That’s not agitation, that’s misinformation.

The instinct to shield audiences from views or facts deemed politically uncomfortable has been in evidence since Trump became a national phenomenon. We saw it when reporters told audiences Hillary Clinton’s small crowds were a “wholly intentional” campaign decision. I listened to colleagues that summer of 2016 talk about ignoring poll results, or anecdotes about Hillary’s troubled campaign, on the grounds that doing otherwise might “help Trump” (or, worse, be perceived that way).

Even if you embrace a wholly politically utilitarian vision of the news media – I don’t, but let’s say – non-reporting of that “enthusiasm” story, or ignoring adverse poll results, didn’t help Hillary’s campaign. I’d argue it more likely accomplished the opposite, contributing to voter apathy by conveying the false impression that her victory was secure.

After the 2016 election, we began to see staff uprisings. In one case, publishers at the Nation faced a revolt – from the Editor on down – after articles by Aaron Mate and Patrick Lawrence questioning the evidentiary basis for Russiagate claims was run. Subsequent events, including the recent declassification of congressional testimony, revealed that Mate especially was right to point out that officials had no evidence for a Trump-Russia collusion case. It’s precisely because such unpopular views often turn out to be valid that we stress publishing and debating them in the press.

In a related incident, the New Yorker ran an article about Glenn Greenwald’s Russiagate skepticism that quoted that same Nation editor, Joan Walsh, who had edited Greenwald at Salon. She suggested to the New Yorker that Greenwald’s reservations were rooted in “disdain” for the Democratic Party, in part because of its closeness to Wall Street, but also because of the “ascendance of women and people of color.” The message was clear: even if you win a Pulitzer Prize, you can be accused of racism for deviating from approved narratives, even on questions that have nothing to do with race (the New Yorker piece also implied Greenwald’s intransigence on Russia was pathological and grounded in trauma from childhood).

In the case of Cotton, Times staffers protested on the grounds that “Running this puts Black @NYTimes staff in danger.” Bennet’s editorial decision was not merely ill-considered, but literally life-threatening (note pundits in the space of a few weeks have told us that protesting during lockdowns and not protestingduring lockdowns are both literally lethal). The Times first attempted to rectify the situation by apologizing, adding a long Editor’s note to Cotton’s piece that read, as so many recent “apologies” have, like a note written by a hostage.

Editors begged forgiveness for not being more involved, for not thinking to urge Cotton to sound less like Cotton (“Editors should have offered suggestions”), and for allowing rhetoric that was “needlessly harsh and falls short of the thoughtful approach that advances useful debate.” That last line is sadly funny, in the context of an episode in which reporters were seeking to pre-empt a debate rather than have one at all; of course, no one got the joke, since a primary characteristic of the current political climate is a total absence of a sense of humor in any direction.

As many guessed, the “apology” was not enough, and Bennet was whacked a day later in a terse announcement.

His replacement, Kathleen Kingsbury, issued a staff directive essentially telling employees they now had a veto over anything that made them uncomfortable:

“Anyone who sees any piece of Opinion journalism, headlines, social posts, photos—you name it—that gives you the slightest pause, please call or text me immediately.”

All these episodes sent a signal to everyone in a business already shedding jobs at an extraordinary rate that failure to toe certain editorial lines can and will result in the loss of your job. Perhaps additionally, you could face a public shaming campaign in which you will be denounced as a racist and rendered unemployable.

These tensions led to amazing contradictions in coverage. For all the extraordinary/inexplicable scenes of police viciousness in recent weeks — and there was a ton of it, ranging from police slashing tires in Minneapolis, to Buffalo officers knocking over an elderly man, to Philadelphia police attacking protesters — there were also 12 deaths in the first nine days of protests, only one at the hands of a police officer (involving a man who may or may not have been aiming a gun at police).

Looting in some communities has been so bad that people have been left without banks to cash checks, or pharmacies to fill prescriptions; business owners have been wiped out (“My life is gone,” commented one Philly store owner); a car dealership in San Leandro, California saw 74 cars stolen in a single night. It isn’t the whole story, but it’s demonstrably true that violence, arson, and rioting are occurring.

However, because it is politically untenable to discuss this in ways that do not suggest support, reporters have been twisting themselves into knots.

Even people who try to keep up with protest goals find themselves denounced the moment they fail to submit to some new tenet of ever-evolving doctrine, via a surprisingly consistent stream of retorts: fuck you, shut up, send money, do better, check yourself, I’m tired and racist.

Minneapolis mayor Jacob Frey, who argued for police reform and attempted to show solidarity with protesters in his city, was shouted down after he refused to commit to defunding the police. Protesters shouted “Get the fuck out!” at him, then chanted “Shame!” and threw refuse, Game of Thrones-style, as he skulked out of the gathering. Frey’s “shame” was refusing to endorse a position polls show 65% of Americans oppose, including 62% of Democrats, with just 15% of all people, and only 33% of African-Americans, in support.

Each passing day sees more scenes that recall something closer to cult religion than politics. White protesters in Floyd’s Houston hometown kneeling and praying to black residents for “forgiveness… for years and years of racism” are one thing, but what are we to make of white police in Cary, North Carolina, kneeling and washing the feetof Black pastors? What about Nancy Pelosi and Chuck Schumer kneeling while dressed in “African kente cloth scarves”?

There is symbolism here that goes beyond frustration with police or even with racism: these are orgiastic, quasi-religious, and most of all, deeply weird scenes, and the press is too paralyzed to wonder at it. In a business where the first job requirement was once the willingness to ask tough questions, we’ve become afraid to ask obvious ones.

On CNN, Minneapolis City Council President Lisa Bender was asked a hypothetical question about a future without police: “What if in the middle of the night, my home is broken into? Who do I call?” When Bender, who is white, answered, “I know that comes from a place of privilege,” questions popped to mind. Does privilege mean one should let someone break into one’s home, or that one shouldn’t ask that hypothetical question? (I was genuinely confused). In any other situation, a media person pounces on a provocative response to dig out its meaning, but an increasingly long list of words and topics are deemed too dangerous to discuss.

The media in the last four years has devolved into a succession of moral manias. We are told the Most Important Thing Ever is happening for days or weeks at a time, until subjects are abruptly dropped and forgotten, but the tone of warlike emergency remains: from James Comey’s firing, to the deification of Robert Mueller, to the Brett Kavanaugh nomination, to the democracy-imperiling threat to intelligence “whistleblowers,” all those interminable months of Ukrainegate hearings (while Covid-19 advanced), to fury at the death wish of lockdown violators, to the sudden reversal on that same issue, etc.

It’s been learned in these episodes we may freely misreport reality, so long as the political goal is righteous.

It was okay to publish the now-discredited Steele dossier, because Trump is scum. MSNBC could put Michael Avenatti on live TV to air a gang rape allegation without vetting, because who cared about Brett Kavanaugh – except press airing of that wild story ended up being a crucial factor in convincing key swing voter Maine Senator Susan Collins the anti-Kavanaugh campaign was a political hit job (the allegation illustrated, “why the presumption of innocence is so important,” she said). Reporters who were anxious to prevent Kavanaugh’s appointment, in other words, ended up helping it happen through overzealousness.

There were no press calls for self-audits after those episodes, just as there won’t be a few weeks from now if Covid-19 cases spike, or a few months from now if Donald Trump wins re-election successfully painting the Democrats as supporters of violent protest who want to abolish police. No: press activism is limited to denouncing and shaming colleagues for insufficient fealty to the cheap knockoff of bullying campus Marxism that passes for leftist thought these days.

The traditional view of the press was never based on some contrived, mathematical notion of “balance,” i.e. five paragraphs of Republicans for every five paragraphs of Democrats. The ideal instead was that we showed you everything we could see, good and bad, ugly and not, trusting that a better-informed public would make better decisions. This vision of media stressed accuracy, truth, and trust in the reader’s judgment as the routes to positive social change.

For all our infamous failings, journalists once had some toughness to them. We were supposed to be willing to go to jail for sources we might not even like, and fly off to war zones or disaster areas without question when editors asked. It was also once considered a virtue to flout the disapproval of colleagues to fight for stories we believed in (Watergate, for instance).

Today no one with a salary will stand up for colleagues like Lee Fang. Our brave truth-tellers make great shows of shaking fists at our parody president, but not one of them will talk honestly about the fear running through their own newsrooms. People depend on us to tell them what we see, not what we think. What good are we if we’re afraid to do it?

via ZeroHedge News https://ift.tt/3fjLsX4 Tyler Durden

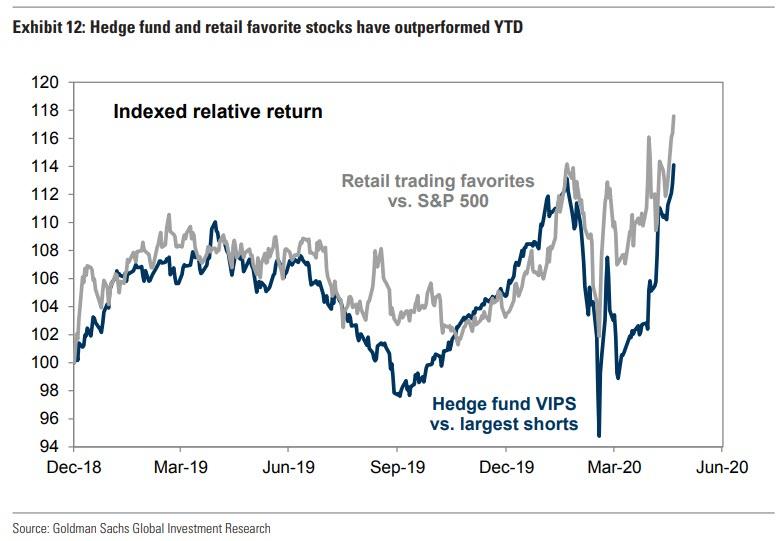

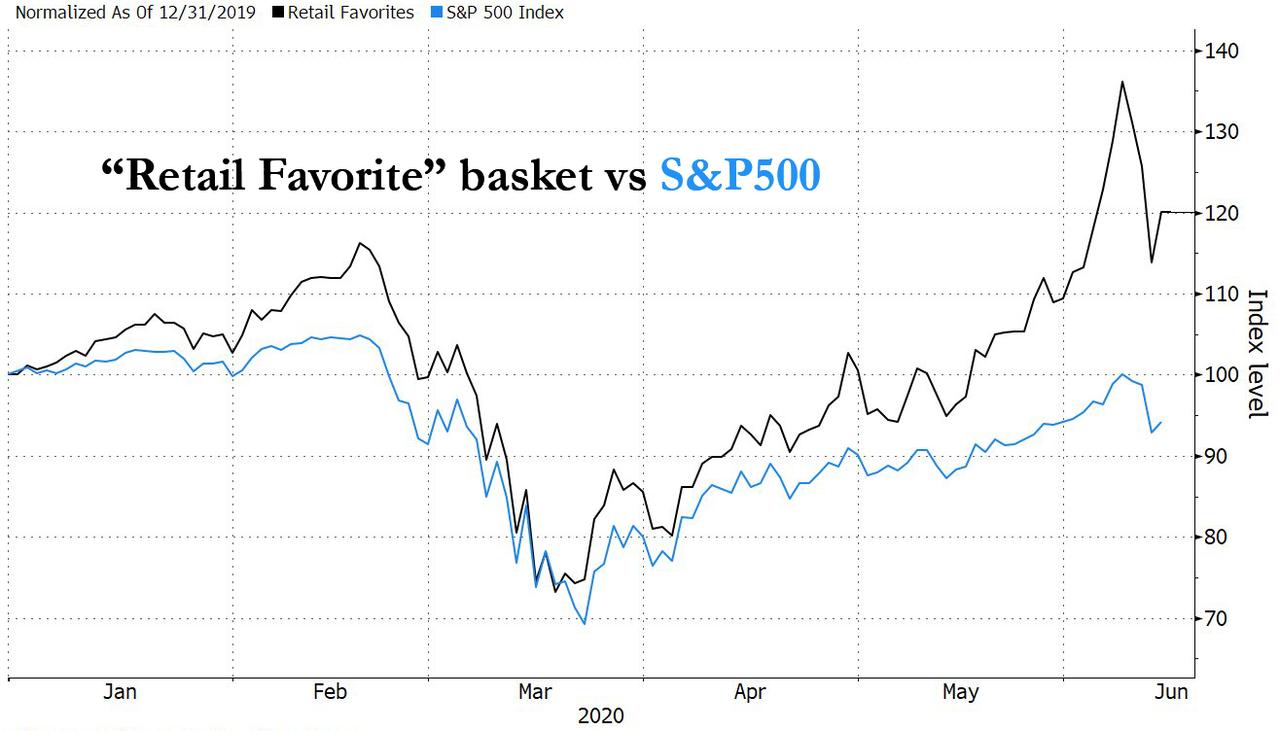

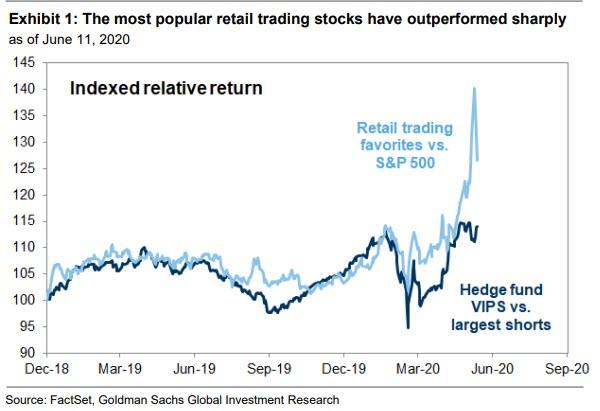

… we reported that something unprecedented has happened: a basket of Goldman “retail favorite” stocks had outperformed not only the broader S&P500, but also Goldman’s basket of most popular hedge fund stocks.

Indeed, as Goldman highlighted at the end of May, as a result of free government money, zero cost online trades and millions of bored “unemployed from home” Gen-Zers, there has been nearly a tripling in retail user activity this year, with the number of distinct user-positions in S&P 500 stocks rising from 4 million at the start of 2020 to 5 million at the market peak in February, 7 million at the S&P 500 trough in March, and 12 million as of the end of May (since then this number has exploded even higher). This sharp increase in retail trading amid still muted hedge fund bullishness in a very illiquid market, helped a basket of popular retail stocks (which for those who have access can track it using Goldman’s Marquee platform under the GSXURFAV ticker) outperform the S&P 500 by 13 percentage points YTD.

Or maybe unprecedented is too strong a word: after the last time retail outperformed hedge funds was in late February – just two days after the S&P hit an all time high – when we posted the exact same observation, and concluded by saying that “while it is certainly a novelty to see retail investors outperform hedge funds, we doubt this divergence will last long.”

It did not, and the market crashed just days later.

However, what has happened since is truly unprecedented because if retail had merely smacked “smart money” returns at the end of February, it has positively crucified both the smart money – and all the money in the face of the S&P500 as of right now, when the basket of most popular retail stocks is up 20% YTD compared to the S&P which after Thursday’s rout ended down 5% for the year…

… and the Hedge Fund VIP basket which is roughly unchanged YTD. Even on a hedged basis (retail favorites/S&P500 vs hedge fund VIPs/largest short pair trades), the retail army is up almost 30% despite last week’s rout, massively outperforming virtually everyone else, and as the Goldman chart below shows, since the start of 2019, retail is outperforming hedge funds roughly 3 to 1.

To be sure, retail outperformance was somewhat hobbled after last Thursday’s rout but not nearly enough to catch down to the broad market, which experienced its sharpest decline since bottoming on March 23, which shockingly took place one day after arguably the most dovish Fed statement ever, one in which the central bank announced its intention to keep the funds rate at 0-25 bp through 2022, while formalizing open-ended QE. (that said, the S&P is still 36% above its March low largely thanks to the trillions in Fed stimulus).

This disconnect between retail and hedge fund performance has not gone unnoticed by Goldman’s clients – who pay Goldman handsomely to outperform – or be told how to outperform – the market.

As David Kostin writes in his latest Weekly Kickstart, unlike the past three months, when many of the bank’s client discussions centered on the disconnect between financial assets and the economy, as “most institutional investors have been stunned by the juxtaposition of the sharpest GDP contraction on record with a 36% market rally”, in recent weeks, (increasingly angry) investors have focused on a different type of disconnect between Wall Street and Main Street: The relative performance of institutional and retail investors.

Since the March 23 low, our Hedge Fund VIP (GSTHHVIP) and Mutual Fund Overweight (GSTHMFOW) baskets have each returned 45%, outpacing the 36% S&P 500 rally by 900 bp. However, a basket of the most popular retail trading stocks (GSXURFAV) has returned an incredible 61%. As we highlighted in May, broker data reveal a tripling of retail trading activity as the market declined.

Why are Goldman’s clients angry?

Because instead of listening to Dave “Stool President” Portnoy, the self-proclaimed king of the Robinhood daytrading army, something they can do for free by just following his twitter account, they are instead paying Goldman a 2-3% commission for what? To underperform by as much as 1600 bps. And those that are not getting angry, they should be, because the conditions that have allowed Portnoy to take the other side of Warren Buffett’s airline trade but to also outperform all of the “smartest guys in the room”, are the same that are allowing bankrupt Hertz to issue up to $1 billion in worthless stock to Robinhooders: it’s the Fed’s green light to go crazy and just buy everything, which is the only obvious trade in a market in which the Fed has made failure impossible – something we have been pounding the table on ever since 2013 when we said that the best performing strategy is to go long the most shorted names, a trade that has generated tens of thousands of bps in alphaas BofA “discovered” last year (but sure, call us bears).

So in an attempt to win back some goodwill from its clients, Goldman’s Kostin lays out several observations on whether it no longer makes sense to pay for a professional financial advisor (such as Goldman), when the Fed has assured that this is a market where 10-year-olds (i.e., the e-trade baby all grown up) can make money hand over fist:

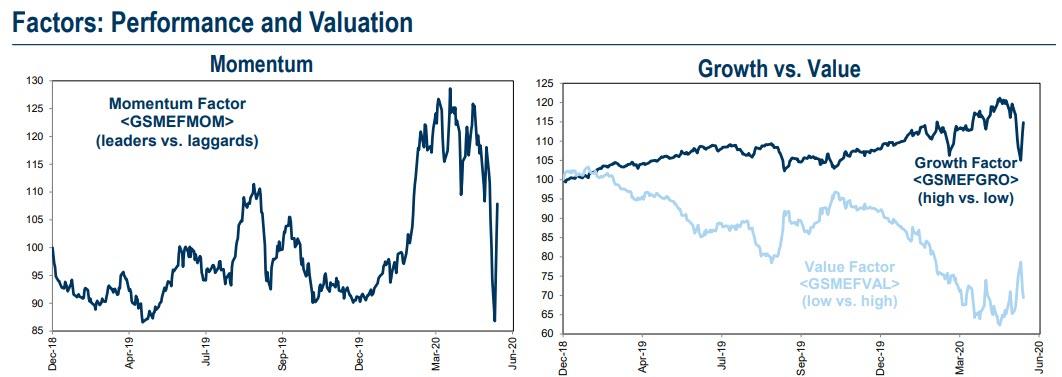

The surge in retail trading activity has amplified the market rotation toward cyclicals and value stocks. High quality growth stocks outperformed during the market drawdown and continued to lead in the first weeks of the rebound, narrowing market breadth and contrasting with past bear market recoveries. Between March 23 and the middle of May, our long/short Growth factor returned 9% and our Momentum factor rose by 2%. This dynamic benefited institutional investors, who had shifted toward growth stocks as the market declined. Since mid-May, however, our Momentum factor has declined by 19% as improving virus and activity data pushed investors toward cyclicals, small-caps, and other economically-sensitive, low- multiple stocks. Stocks with these qualities which were quickly embraced by value-seeking retail investors, and now make up a large portion of our retail basket.

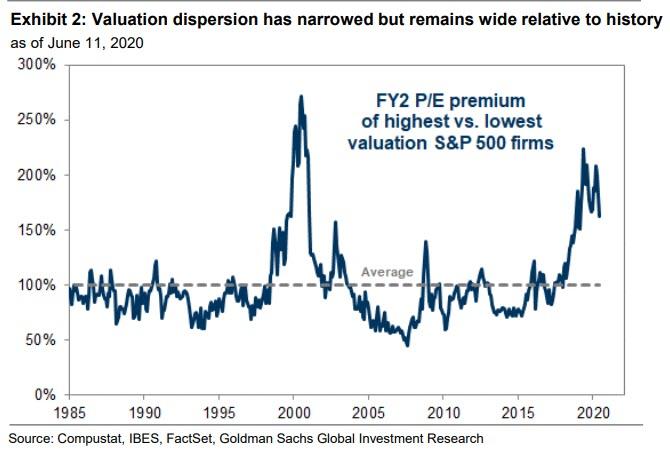

Despite the recent Value rally, the dispersion of stock multiples is still extremely wide relative to history. Last month, the gap in valuations between the highest and lowest valuation stocks registered the widest on record outside of the Tech Bubble peak. During the last few weeks that spread has narrowed, but it still ranks in the 93rd percentile since 1980. Wide valuation dispersion signals long-term opportunity for value investors. However, the volatile rotations in recent weeks underscore just how difficult timing that opportunity can be. We believe most investors should include some value exposure in their portfolios, although the degree will depend on time horizon and risk tolerance, among other factors. In the medium-term, the challenge is determining which laggards are value opportunities and which leaders will experience fundamental growth that justifies current elevated valuations.

Yes David, we know the challenge, the problem for you – as you try to earn your pay and provide the solution – is that as the market continues to trade increasingly insane based on the whims of 10-year-olds, not even the most spot on accurate analysis based on fundamentals will matter one bit when the marginal price setters are traders who are still not legal to drink and maybe drive.

Which is why the Goldman strategist cops out and takes the easy way out: just keep buying what has worked for the past decade, namely tech, resulting in even narrower market breadth even though it was Kostin himself two months ago warning that “narrow market breadth is always resolved the same way: narrow rallies lead to large drawdowns as the handful of market leaders ultimately fail to generate enough fundamental earnings strength to justify elevated valuations and investor crowding. In these cases, the market leaders “catch down” to weaker peers.” Maybe amid the shock of his clients, Kostin is hoping they don’t recall what he said less than two months ago:

The unrivaled market leader this year has been Tech, and we expect it will continue to outperform [ZH: really? that;s not what you said on April 27]. The Information Technology sector has returned +7% YTD, and even following this week’s decline the NASDAQ 100 trades within 1% of its pre-crisis peak. As the market was falling, the sector was supported by its quality attributes, including strong balance sheets and high profit margins, as well as the resilience of its earnings. This year analysts have revised down Tech 2021 EPS by just 5%, compared with a 20% cut for the remainder of the S&P 500. In addition, low interest rates increase the value of the sector’s long-term growth prospects that, in cases like ecommerce and cloud usage, have been accelerated by the impact of the pandemic on consumer and business activity. Major risks to the sector include its popularity, which could cause underperformance in the event of a sharp investor derisking, as well as the possibilities of government regulation and tax reform. While Health Care EPS estimates have been similarly resilient, political risk has suppressed the sector’s multiples, as is often the case prior to presidential elections.

And so on. Meanwhile as Kostin, and his very generous clients contemplate the tea leaves and analyze such meaningless “data” as cash flows, growth projections, technical reversal patterns and what not, the rabid army of millennial daytraders rushes from one stock to the next, sending it soaring then plunging with no regard for underlying data, in one truly unprecedented pump and dump scheme, where all those who jump in first make a killing, while the laggards are crushed.

As we noted recently, until Powell does something to stop this catastrophic mockery of efficient markets, which are now juiced to the gills with the Fed’s trillions in newly printed money, nothing will change. And judging by what Powell just said last week, nothing will change for a long, long time:

“The Fed doesn’t believe, and shouldn’t believe, that it can forecast the stock market, and therefore recognize a bubble in real time,” said Princeton University economist Alan Blinder, a former Fed vice chairman, in a Bloomberg Television interview. “They’re pretty easy to recognize after the fact, after they burst. But, in real time, in a predictive way, pretty much impossible.”

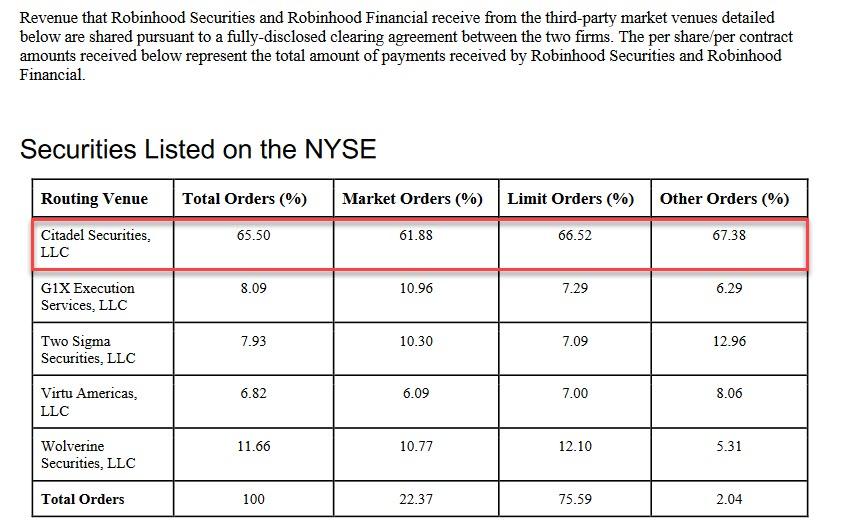

Really? Impossible? How about one look at the chart of bankrupt Hertz…

… whose market cap almost hit $1 billion last week and prompted the company to do the unthinkable: try to sell stock to the hordes of Robinhood daytraders, whose tiny trades are being frontrun all day long by HFT algos which are accentuating the momentum and allowing a handful of small investors to have an outsized impact on the market (below is Robinhood’s latest 606 Report: 65.5% of all orders are sold to Citadel).

Or how about Chesapeake? Or maybe Fangdd, you worthless career economist.

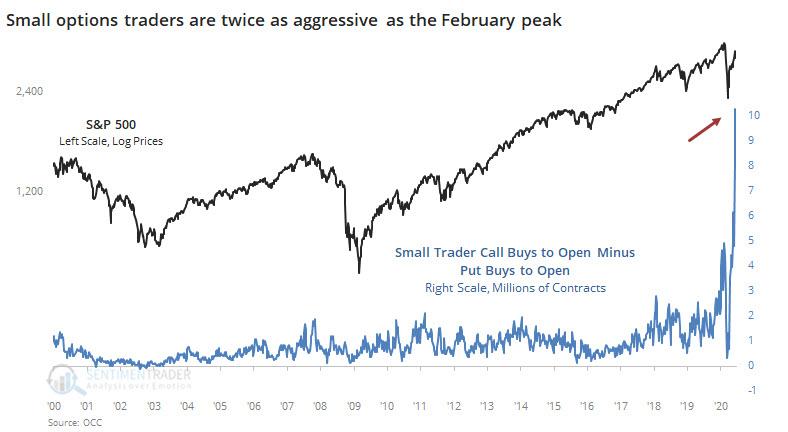

Meanwhile, retail investors – confident they can never lose – and certainly their returns to date justify it, are betting more and more aggressively on the market, in the form of the ever more levered upside bets such as tiny, short duration calls. According to SentimentTrader, one-contract transactions have surged to 13% from roughly 9%. The smallest of traders bought more than 14 million speculative call options in the week ended June 5, an all time high.

“We have Instagram influencers and now we have Reddit influencers,” QVR’s Benn Eifert told Bloomberg. “They post a trade idea in an option, in a single name, and within an hour you see hundreds of thousands of call options placed, which is totally insane.”

Insane? Yes, but it’s working, and who can blame them: the Fed chairman himself said he will do nothing to pop the bubble (which he can’t see) with tens of millions of Americans out of work. That means that, all else equal, when it comes to market insanity you ain’t seen nothing yet. Jim Bianco, president and founder of Bianco Research LLC, agrees, and says that it all comes down to the Fed’s only mandate: never again allow a drop in stocks.

“That’s why we’re seeing a giant rush of small retail investors and everybody else into the market,” Bianco told Bloomberg Television Wednesday. “When you go into the market, you go to the riskiest end of the market, so you buy bankrupt companies, you buy beaten down airlines, you buy cruise ships, you buy retailers because they will benefit the most from a support system where everything is targeted, and the markets will always go up.”

And as they do, and as “retail investors” retire at the old age of 11, Goldman’s clients will get angrier by the day until one day, who knows, we may just see riots in the streets with chants of “millionaires’ lives matter.“

via ZeroHedge News https://ift.tt/2BWSYsq Tyler Durden

A new study has found that Sars-Cov-2, the virus linked to Covid19, maybe five times more widespread than previously thought, and therefore five times less deadly.

The authors infer from this that antibodies are inexplicably absent from the majority of mild cases of covid19. But, given the known inaccuracy of the diagnostic tests and the well-documented tendencies to over-diagnose by clinical observation, another potential explanation would appear to be that the absent antibodies were due to the fact the subjects had never actually been infected with SARS-COV-2 in the first place, and their ‘mild’ cold-like symptoms were due to some other pathogen, like…the common cold.

However, if the authors are indeed correct in their estimation, this might mean SARS-COV-2’s infection rate (IFR) would need to be revised downward yet again. If 80% of those infected really do not produce antibodies then there is a live possibility the virus is present in many more people than usually supposed. Which would in turn potentially reduce the IFR, possibly considerably.

In the early stages, the World Health Organization (WHO) estimated the virus’ IFR to be as high as 3.4%. The models based on those numbers have, however, been shown to be wildly inaccurate.

Another study from last month meanwhile has found evidence up to 60% of people may be partially resistant to SARS-COV-2 without ever being exposed to it.

Importantly, we detected SARS-CoV-2-reactive CD4+ T cells in ∼40%–60% of unexposed individuals, suggesting cross-reactive T cell recognition between circulating “common cold” coronaviruses and SARS-CoV-2.

In other words, large numbers of people may be immune or resistant to this virus because they have already been infected by other coronaviruses.

This may not be surprising, given the close relationship between most coronaviruses, but it is a further indicator that this virus, known to be harmless in the vast majority of cases, is neither especially unique nor especially dangerous.

The evidence continues to mount that the original estimates of the danger posed by this virus were massively exaggerated.

NAACP Demands Atlanta Chief Resign Over Latest Police Killing Of Unarmed Black Man Tyler Durden

Sat, 06/13/2020 – 15:35

The latest police killing of an “unarmed” black man unfolded Friday night in Atlanta, and footage released Saturday afternoon is already causing a major uproar in the city. Activists are demanding that Atlanta’s police chief Erika Shields, whose statements to the press and willingness to push deescalation tactics made her a media darling during the unrest that followed the killing of George Floyd.

Though the only details of the incident so far involve grainy cellphone camera footage, it’s clear in the video that one of the two APD officers involved in the incident shot a suspect in the back as he was running away after wresting one of the officer’s tasers away from him.

The Georgia NAACP claimed the APD needs “a serious overhaul” and argued that the deceased suspect, later identified as Rayshard Brooks, 27, was killed for “sleeping” (not for attacking two officers and stealing one of their weapons)>

@KeishaBottoms, @Atlanta_Police needs a serious overhaul. The continuation of these kinds of actions require immediate resolution. Instead of seeing an improvement, it continues to happen day after day.

The footage posted to twitter earlier shows Brooks successfully wrestle both officers to the ground before running off with the taser. At the end of the video, several gunshots ring out, though the shooting of Brooks isn’t shown.

Meanwhile, protesters showed up Saturday to Washington DC’s “Black Lives Matter” plaza where smaller protests have been ongoing every day. Saturday marked the 16th day of demonstrations.

Here’s what happened according to the Washington Post: the ADP received a call and was dispatched to a local Wendy’s Friday night following a complaint about a man parked and asleep in the drive-through, according to a preliminary report from the Georgia Bureau of Investigation. The situation escalated when the two officers tried taking Brooks, 27, into custody. He resisted, and the situation quickly became violent.

Shields

Atlanta activists wrote Saturday that “ADP shot another unarmed black man in South Atlanta. Details are still coming and our rage continues.”

The GBI’s preliminary report told a different story.

“During the arrest, the male subject resisted and a struggle ensued,” GBI said. “The officer deployed a Taser. Witnesses report that during the struggle the male subject grabbed and was in possession of the Taser. It has also been reported that the male subject was shot by an officer in the struggle over the Taser.”

Brooks died Saturday morning at a local hospital after emergency surgery.

Brooks’s death marks the 48th officer-involved shooting the GBI has been asked to investigate since the start of 2020. Ahmaud Arbery was also shot and killed in Georgia, though his assailants – who will all stand trial for murder – weren’t cops.

Once the GBI completes its independent investigation, the case will be turned over to the Fulton County District Attorney’s Office for review. Later on Saturday, the Fulton County DA’s office said it had already launched “an intense, independent investigation of the incident” and that personnel were dispatched to the scene immediately after the shooting. One local outlet said both officers involved have been removed from duty pending an investigation.

via ZeroHedge News https://ift.tt/3fiQRh9 Tyler Durden

The New York Times has run an opinion column by Mariame Kaba denouncing efforts by Democratic leaders and the media to try to spin the call for defunding the police as just a reallocation of funds and a new set of priorities and a new structure for policing. Kaba wrote “Yes, we mean literally abolish the police.”

Kaba states what people in the streets has been saying (including rallies chanting “no more cops”) even as some in the media has mocked those who claimed that “defund the police” could actually mean defunding the police or that “dismantle the police” could actually means dismantling the police. Indeed, recently Minneapolis City Council President Lisa Bender told CNN’s Alisyn Camerota that people who are concerned about their personal safety after defunding police are simply speaking “from a place of privilege.”

Kaba rejects “liberal reforms” from congressional Democrats and Joe Biden including calls for cracking down on police misconduct or ordering reforms:

“Enough. We can’t reform the police. The only way to diminish police violence is to reduce contact between the public and the police.”

She states that police have always been a “force of violence against black people” dating back to slavery. At a minimum, Kaba wants police cut “in half” because “fewer police officers equals fewer opportunities for them to brutalize and kill people.” For this reason, Kaba explains “We don’t want to just close police departments. We want to make them obsolete.”

“At the same time we have to hold the establishments in various cities accountable. This violence against the peaceful protest movement on Capitol Hill was carried out by Mayor Jenny Durkan. And that’s why it’s no surprise that tens of thousands of people in Seattle are calling for her resignation because they reject police violence, they reject police brutality and we want a society that is based on equality and cooperation

….as far as things going awry, I can tell you the only thing that went awry day after day after day since the first protest on May 30th was the police under orders by the Democratic Party establishment and the Mayor Durkan, it was the police making things going awry.”

The disconnect is widening between what actual activists are saying and what the media is reporting and Democratic leaders are hearing. For example, Atlanta Mayor Keisha Bottoms assured people that the slogan is simply a “simplified message. . . but I think the overarching thing is that people want to see a reallocation of resources into community development and alternatives to just criminalizing.” That sounds a bit different from “no more cops” and demands to “dismantle the police” heard in these rallies:

As discussed earlier, Democratic leaders have been trying to tap into the energy and numbers of the antifascist movement for years despite its anti-free speech and sometimes violent record. It is now struggling to control this careening movement by simply refashioning its demands in a more a new image. The establishment is dealing with another sharp disconnect. While the media has attempted to re-make the movement to defund into a more mainstream image, polls show 64% of the public oppose the call. It is a dangerous pivot to make in the middle mad rush to the extremes. This is why, during the French Revolution, the journalist Jacques Mallet Pan warned, “Like Saturn, the revolution devours its children.”

via ZeroHedge News https://ift.tt/2YudCb2 Tyler Durden

Brawl At Thrift Store Breaks Out Over One Way Social Distancing Arrows Tyler Durden

Sat, 06/13/2020 – 14:45

By now, you’ve all seen them: the arrows that are placed on the floors at stores to try and help customers keep up with social distancing rules. And while you may have even had a friendly engagement with other shoppers about somebody going the wrong way down a “one way” aisle, it was probably nothing like what took place in a Tampa, Florida Goodwill last week.

Two shoppers wound up under arrest for battery after 29 year old Jenna Sims and 50 year old Paul Turner wound up in a confrontation in a Tampa store “over the floor directions due to COVID-19,” according to The Smoking Gun. Goodwill, like many other stores, had established one-way aisles for customers to walk down.

Sims apparently became upset after noticing Turner going the wrong way down an aisle, which led to an argument.

Sims wound up striking Turner (who, from the mugshots looks like he got the worst of it) “about his body, head, and face.” Turner shoved Sims in response. The police report says that Turner “did not suffer any injuries” from the battery, which doesn’t exactly look to be the truth:

Sims, who is 5’ 4”, 125-pounds, seemed to have gotten the better of the 6’3″ 220-pound Turner in the altercation. Police say the incident was recorded by security cameras and both parties were arrested for battery, which is a misdemeanor.

via ZeroHedge News https://ift.tt/2Y08492 Tyler Durden

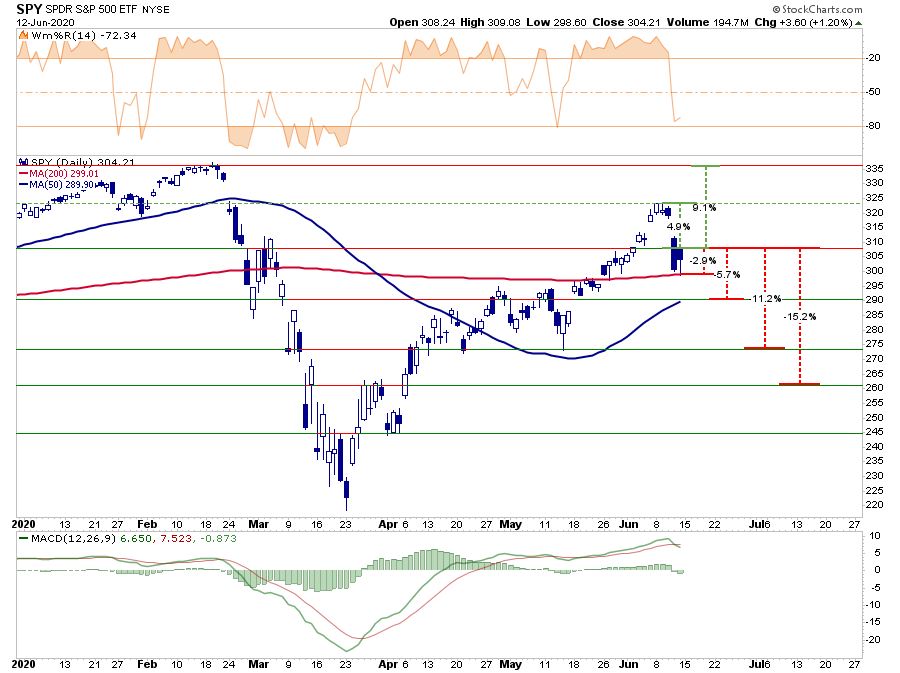

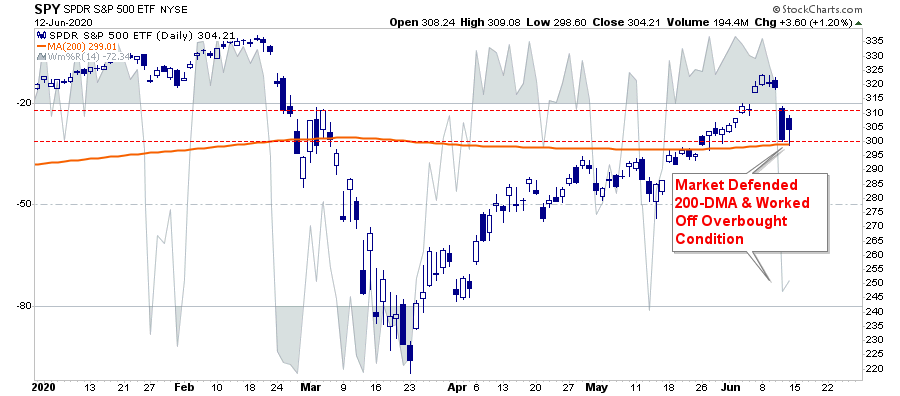

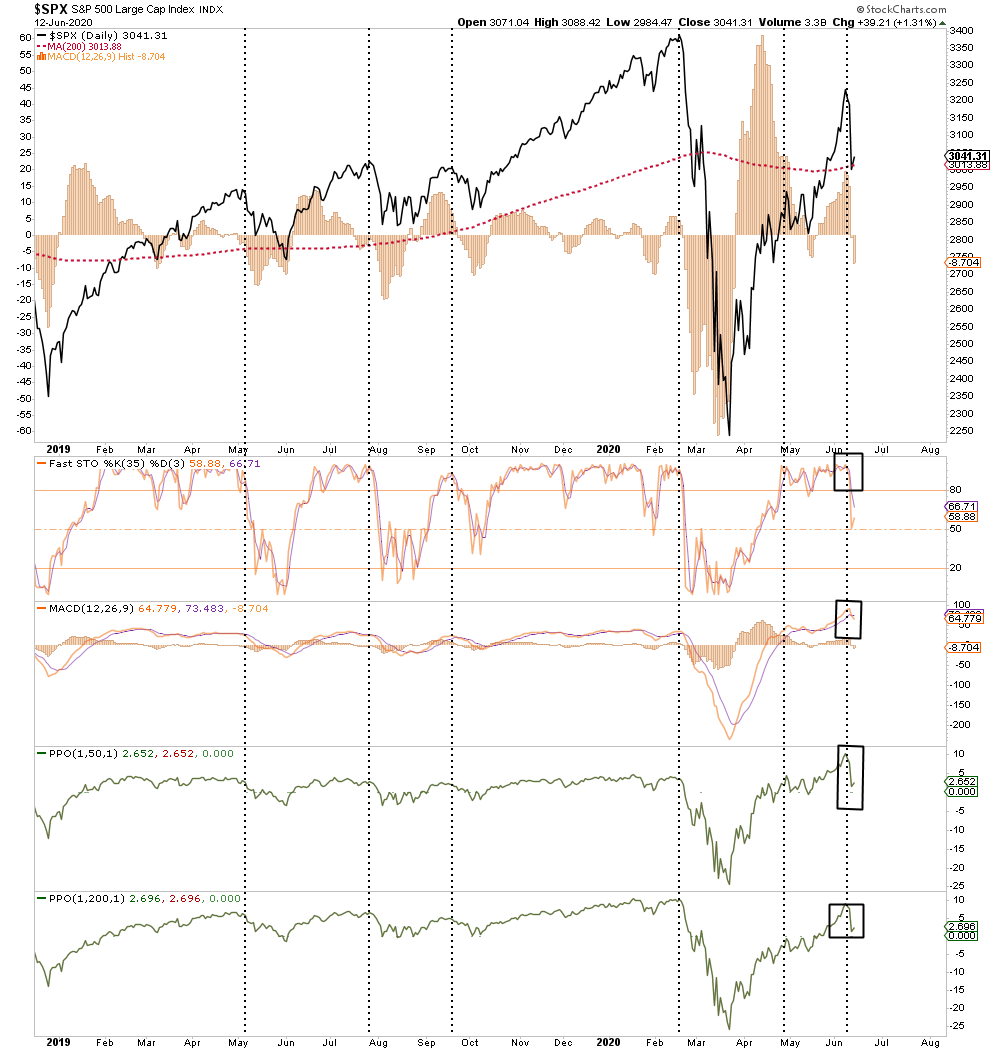

As I wrote previously, the break above the 200-dma had changed the complexion of the market.

“If the markets can break above the 200-dma, and maintain that level, it would suggest the bull market is back in play.“

However, in our Tuesday follow up, we discussed how the market rally had gotten to an extreme. As such, we noted the need to become more defensive in the short-term. To wit:

“Regardless, the markets are bullish biased, and we must be respectful of that reality. No matter how you slice the data, the markets are back to more extreme overbought conditions on a short-term basis.

The break above the 200-dma triggered a parabolic advance in the market over the last week. The market is making a 3-standard deviation move to the upside. With indicators very overbought, short-term corrective action is likely. (Note the market was just 3-standard deviations BELOW the 50-dma in March.)”

That correction came swiftly on Thursday. The surge in COVID-19 cases in the U.S. undermined the “V-Shaped” economic recovery meme. As we noted, the market had rallied into overhead resistance, and the correction found support at the 200-dma.

We can now update the risk/reward parameters from last week.

-2.9% to the 200-dma vs. +4.9% to previous high. (Positive)

-2.9% to the 200-dma vs. +9.1% to all-time highs. (Positive)

-5.6% to 50-dma vs. +4.9% to previous high. (Neutral)

-11.21% to consolidation lows vs +9.1% to all-time highs (Negative)

-15.2% to March bounce peak vs. +9.1% to all-time highs. (Negative)

The market achieved the retracement to the 200-dma support on Thursday during the most intense sell-off since March. Importantly, it was a good reminder of just how brutal markets can be when there is a complete lack of liquidity.

Correction Reduces Short-Term Excesses

Previously we discussed the more extreme levels of optimism in the markets. These indicators have historically corresponded with short-term market peaks and corrections.

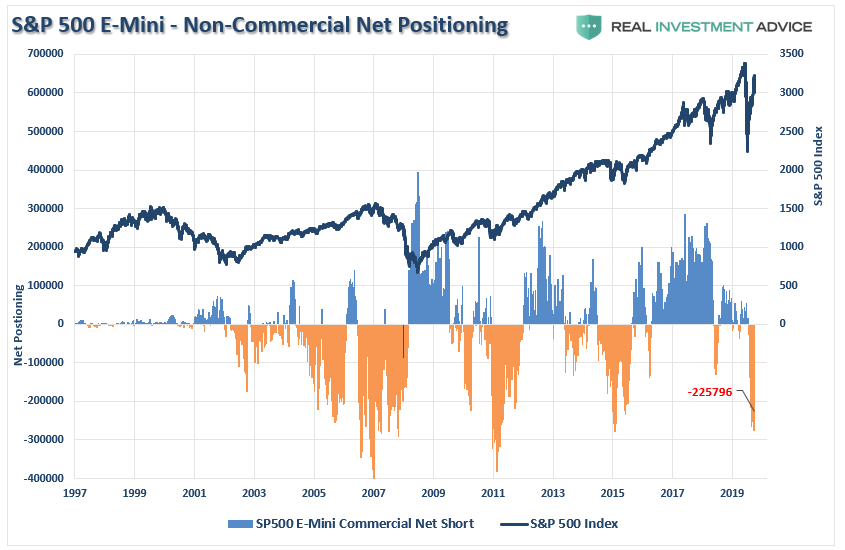

The first was the large level of short-positions non-commercial speculators were carrying on the S&P 500. (These are contracts on the S&P 500 in the futures market used for hedging long market positioning.) Net-short positioning had reached a more extreme level, which historically aligns with short-term peaks and bear markets. The correction last week reduced some of that excess.

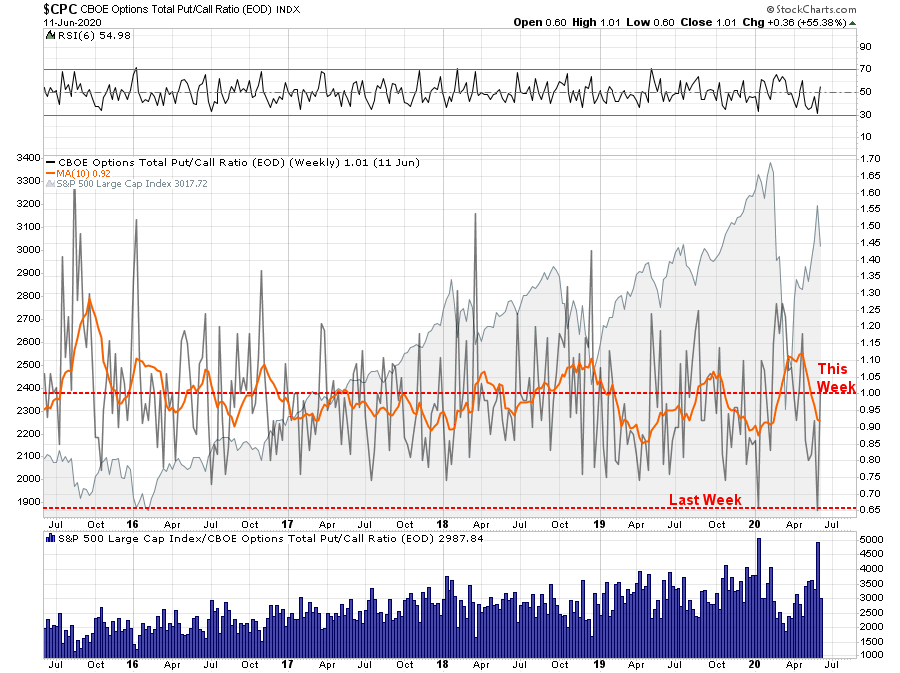

The same goes for the total put-call ratio, This ratio measures the total of option contract buying. Investors had gotten extremely aggressive in buying call options betting the market would only go higher. At extremes, retail “call option” buyers generally wind up on the wrong side of the trade. The quick rout on Thursday reduced some of those excesses.

Note, however, the 10-day moving average of the put-call ratio remains in more “bearish” territory, suggesting we may not be done with the correction just yet.

The issue remains that the markets have priced in a “V-shaped” recovery, which is well ahead of what the economic data suggests.

A Note About The Fed

There were two catalysts that ignited the sell-off on Thursday. The first, as stated above, were headlines of a surge in COVID-19 cases. (As discussed in this week’s #MacroView below)

The second, and probably more important reason, was what the Fed didn’t say following this week’s Fed meeting. While the markets were hopeful for announcements for more stimulus to support the markets, the Fed simply reiterated their current stance.

More importantly, the Fed stated that QE would remain at $40 billion per week or $120 billion per month. This is substantially less than the current level of Treasury issuance. As Tavi Costa of Crescat Capital noted this week:

Jay Powell better not be printing “only” $120B per month…

The government just borrowed $760B in May alone!

Second largest net issuance of Treasuries in history.

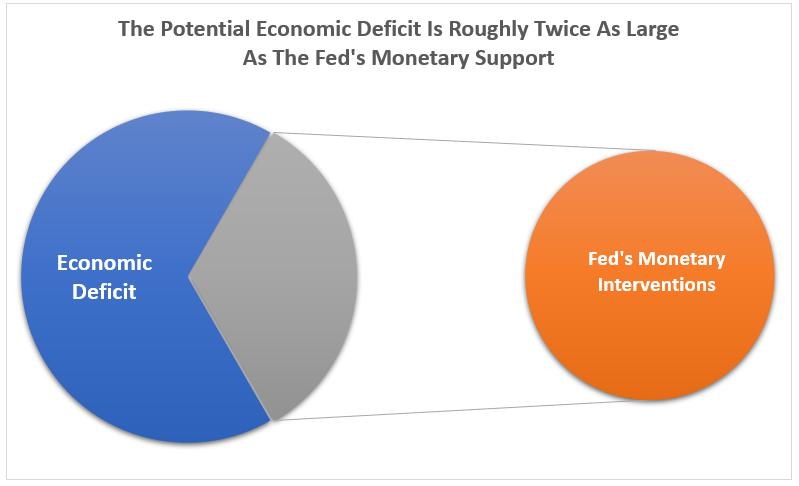

As noted previously,while the Fed is doing a massive amount of QE, the “hole” they are trying to fill is substantially larger. In what I call the “PacMan” chart below, the “economic deficit” will consume more than the Fed has currently committed. (Economic deficit is the estimated loss due to ongoing unemployment, reduced growth, and impact of debt and deficits.)

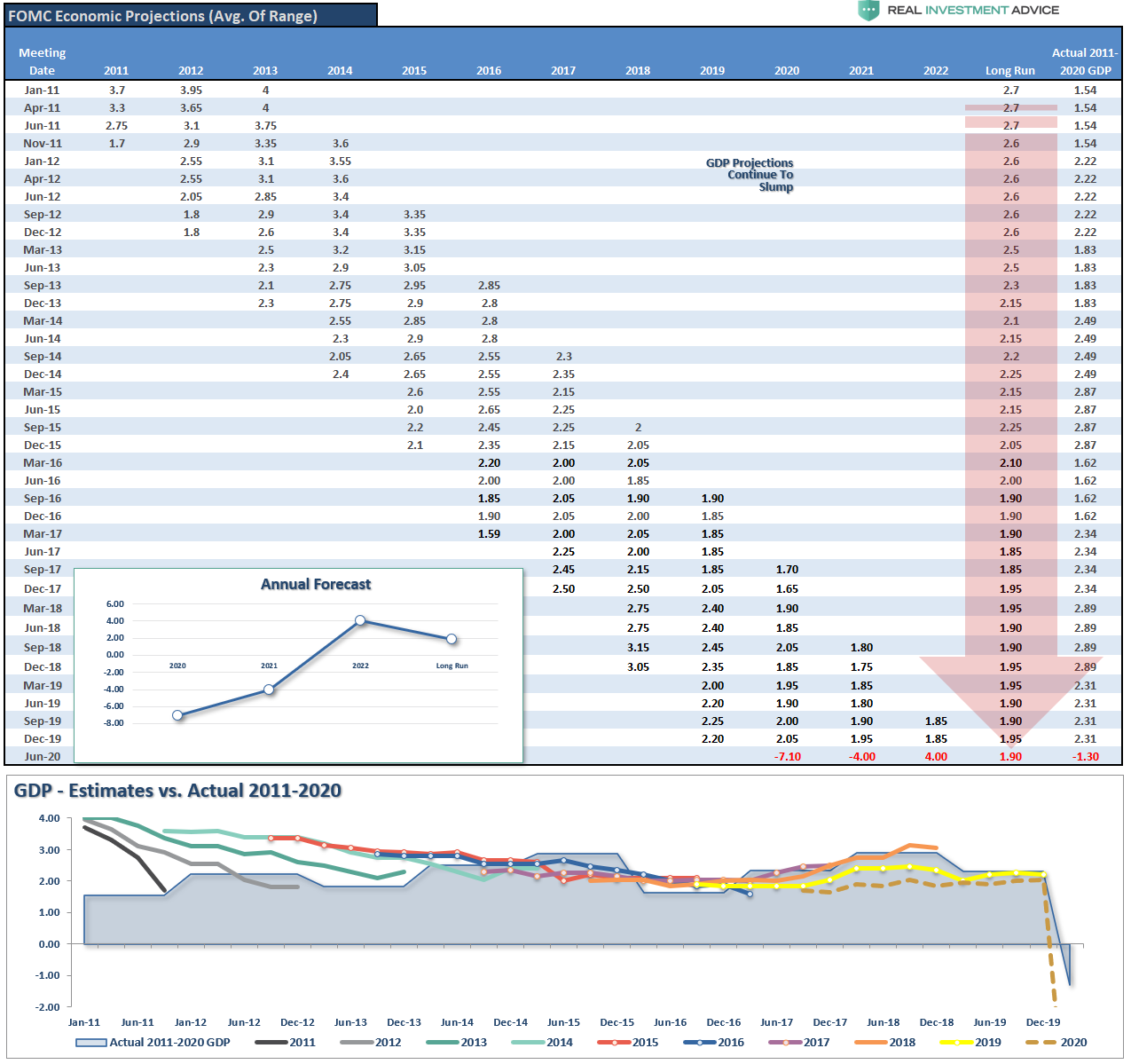

The Worst Economic Forecasters Ever

The Federal Reserve must qualify as the worst economic forecasters ever. Despite annual promises of stronger economic growth, such has yet to be the case. Ever.

While the economy will indeed recover in 2021 and 2022, the Fed is likely overestimating the outcome. However, in the short-term, they have little choice.

“Unwittingly, the Fed has now become co-dependent on the markets. If they acknowledge the risk of weaker economic growth, the subsequent market sell-off would dampen consumer confidence and push economic growth rates lower. Therefore, they have to be overly optimistic.”

As discussed Friday, the surging levels of debts and deficits, combined with demographics, will suppress economic growth below 2%. Such leaves very little room for the Fed to make a policy mistake.

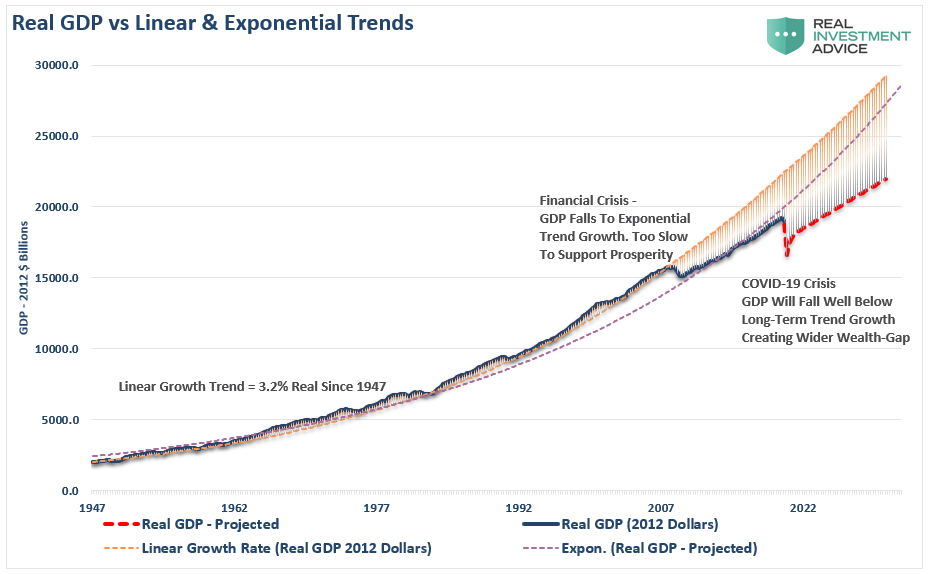

“Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt, and leverage increased.”

While the Fed had an opportunity to disconnect monetary policy from the market, they failed to do so. Instead, they once again opted to bail out financial markets at the expense of economic prosperity longer-term.

By voting to avoid short-term pain, the Federal Reserve has locked the economy into a long-term economic malaise. Like a “frog in boiling water,” the vast majority of Americans will see their economic prosperity slowly fade.

The stock market is not the economy. It is a distortion of economics.

The Bear Case Is Still Valid

As my colleague Doug Kass pointed out on Friday:

Yesterday provided at least five reasons for the markets to decline:

Federal Reserve Chairman Powell delivered a cautionary economic message for not only this year but for several years to come. To me, this renders the rosy EPS projections of the consensus, and many high-profile strategists (like my friends Dave Kostin and Thomas Lee) are unrealistic.

There was mounting evidence that Covid-19 is still not tamed.

Wells Fargo CFO John Shrewsberry said second-quarter loan loss reserves would be higher than in 1Q-2020.

The Robinhood traders’ objects of affection, stocks of bankrupt companies, took a sudden dive. Silly speculation is almost always evidence of a maturing bull market.

Technical signposts are flashing red: Investor sentiment has increased as stock prices rose as a bull market in complacency has quickly unfolded from the depths of March. Market breadth has started to wane.

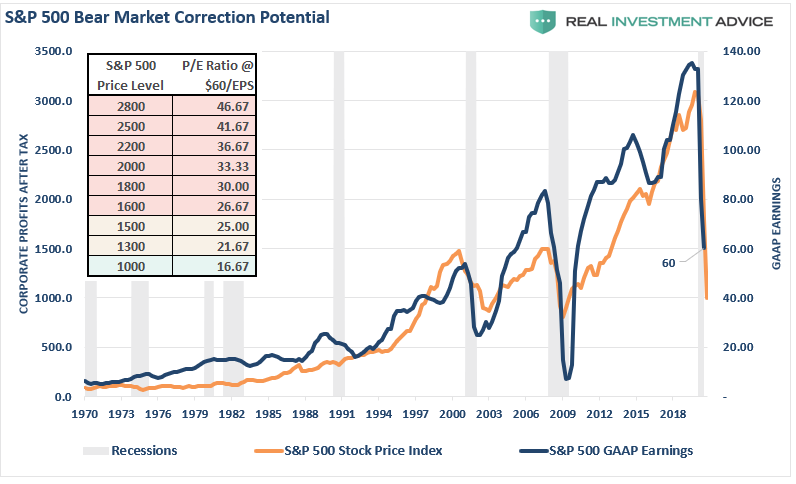

I agree with Doug and have been well ahead of the media in lowering forecasts. As noted previously:

“Given the horrific data we now have coming in, we already know our previous estimates of $100/share were too high. A more realistic, and still overly optimistic 50-60% decline in earnings, makes current valuations even more challenging to support. (Using the chart and table below, you can pick your price and valuation level.) “

What is essential to understand is that while Fed liquidity is currently fueling a “bull market,” the “bear case” still has teeth.

Eventually, the market will fill the gap between “fantasy” and “reality.”

Technical Review Remains Bullish

In the short-term, however, the technical backdrop of the market remains bullish. The market had gotten overheated over the last couple of weeks, but the correction successfully retested the 200-dma. Such establishes important support. Concurrently, the correction reversed most of the more extreme overbought conditions.

However, if we slow our analysis down a bit, we find that the current sell signal remains intact. Such suggests the market could still experience further corrective or consolidative actions over the next couple of weeks or months.

The short-term technical structure remains bullish and overbought currently. However, the longer-term fundamentals remain worrisome in light of the economic devastation. While the Fed’s monetary policies mitigated much of the downside risk, it can not be removed entirely.

As experienced on Thursday, “reversions happen fast.”

Portfolio Positioning For An Overbought Market

As I noted last week:

“With ‘coronavirus cases’ likely to rise sharply following Memorial Day celebrations and recent crowded protests, the risk of disappointment has risen. Such has been an exceptionally rally. All of our equity positions are now extremely stretched and overbought. Conversely, all of our hedges VERY oversold.”

That reversion happened this past week, with our hedges of Treasury bonds and the U.S. dollar offsetting the decline in our longs on Thursday.

This is a very risky market. Caution is advised.

via ZeroHedge News https://ift.tt/30Dwyqt Tyler Durden

‘Expect Something Big’: Kim Jong-Un’s Powerful Sister Threatens Military Action Against South Tyler Durden

Sat, 06/13/2020 – 13:55

Earlier this week North Korea announced it would cut off all government and military communications with the South, also as its foreign ministry declared Pyongyang would “never again” allow President Trump to use ’empty’ dialogue to score political points, suggesting the whole prior year long Trump-Kim bromance is now effectively dead.

And now the increasingly visible and powerful sister of Kim Jong Un has further gone on the offensive by threatening military action against South Korea Saturday.

Kim Yo Jong vowed “We will soon take a next action.” Referencing her brother, she described, “By exercising my power authorized by the Supreme Leader, our Party and the state, I gave an instruction to the arms of the department in charge of the affairs with enemy to decisively carry out the next action,” according to KCNA news agency.

Kim Yo-jong, now increasingly in the spotlight, is the most powerful woman in North Korea, increasingly speaking on behalf of her brother, the Supreme Leader. AFP/Getty Images

“The right to taking the next action against the enemy will be entrusted to the General Staff of our army. Before long, a tragic scene of the useless north-south joint liaison office completely collapsed would be seen,” Kim Yo Jong added.

The widely reported “reason” behind the sudden jingoistic stance is related to activists apparently continuing to defy the north in floating anti-Pyongyang leaflets across the border.

Such activism has been particularly sensitive to the north because it’s driven in many cases by defectors. Lately Pyongyang’s angry rhetoric against South Korea welcoming and hosting such defectors and their political activism has intensified.

But there’s also rising tensions given Seoul’s failed to materialize assurances that Washington would ease sanctions as part of denuclearization talks. This further appears an opportunity for Kim’s increasingly visible and powerful sister to flex her authority over the military and next in line to rule.

THREAD: Kim Yo Jong’s warning this evening is v. worrying.

On Monday I wrote that the DPRK wants to create an inter-Korean crisis.

Well, in two days it’s June 15, the 20th anniversary of the first inter-Korean summit.

I strongly suspect something is being timed to coincide.

Some analysts also believe Kim Jong Un is looking to rapidly manufacture an inter-Korean crisis for much bigger leverage amid stalled and effectively dead talks with the US. Importantly June 15, a mere two days away, will mark the 20th anniversary of the first inter-Korean summit.

Thus we are likely to see some big provocative fireworks in the form of some drastic action or weapon test, sure to re-trigger soaring tensions by Monday.

via ZeroHedge News https://ift.tt/3e48zEQ Tyler Durden

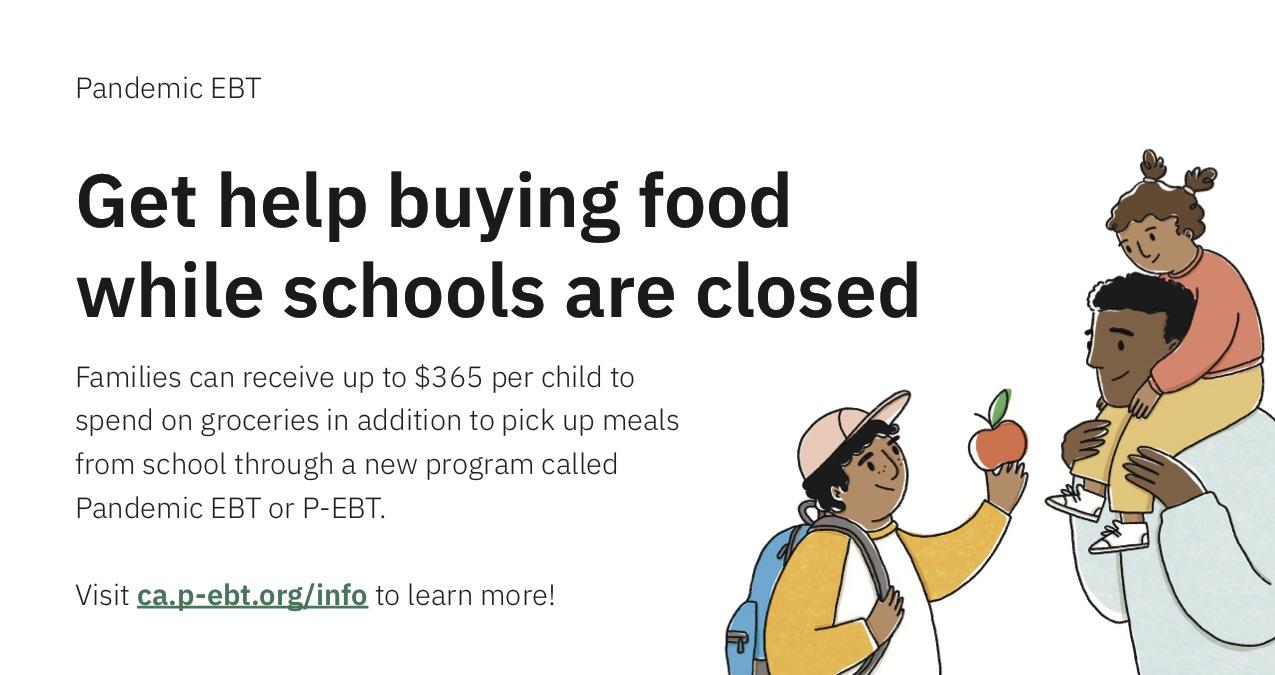

Across America, kids are receiving Electronic Benefit Transfer, or EBT, cards in their names. Each card will be loaded with around $365. This is meant to provide these young people who would otherwise have access to free or reduced-price meals when schools are open with a “free lunch.” The school system here where I live in Indiana and the School District of Philadelphia are just two of the districts busy reminding parents that help with summertime meals is on the way to their mailboxes.

In many school districts, all students will be receiving a card. This is being done so they will have access to meals during the summer. These are going out to both young children and high school students. If a child in Pre-K happens to be in a grade school participating in the federal free and reduced lunch program the child is included in this program and will be eligible to receive this benefit. Both the children and parents can thank the wisdom of lawmakers for this benefit while those concerned about the exploding national deficit are left to pray it will be properly used.

Families can use the P-EBT benefit to purchase food items at EBT authorized retailers, including most major grocery stores. Many gas stations also accept EBT, but you can only use your benefits to pay for specific items. If you receive Supplemental Nutrition Assistance Program (SNAP) benefits, you can purchase food items such as cereal, dairy products, snacks, and candy, but you can’t buy prepared foods, toiletries, over-the-counter medicine, alcohol, or tobacco. Unused benefits will rollover month-to-month and must be used within 365 days. The theory is that families that don’t need the benefit can simply return it.

A lot of questions may arise concerning who will get these cards and how they will be used.Such as, if a child’s issued P-EBT card has their other parent’s name on it but you have custody of the child and that is the child’s address of record with the school, you can use it for the child? The answer is yes. As to the ID requirement for using the P-EBT card at the grocery store, the Grocery Retailers Association is aware of the process for P-EBT and have been informed of the card design as well as benefit projections. By federal statute, retailers cannot ask for ID for EBT purchases if they do not request ID on regular debit card purchases.

This leaves many of us wondering how many kids are really sitting at home with nothing to eat. At times it seems the government is bending over backward to spend money where it does not need to be spent. The quality of what some may think is a free lunch has yet to be determined. When all is said and done it is easy to see this program is ripe for abuse. These cards are good as gold and could even be sold at a discount for cash. Considering how many children in this country are obese, it is likely a great deal of soda pop, chips, candy, and cookies will be bought with EBT cards.

via ZeroHedge News https://ift.tt/2MUirF9 Tyler Durden

{kind=link}