Fed Overnight Repos Continue To Rise As QE Shrinks Tyler Durden

Mon, 06/08/2020 – 10:09

After barely seeing any utilization for much of April and May after the Fed launched Unlimited QE, in the past three weeks there has been a clear rising trend in usage of the Fed’s overnight (and term) repo operations, which on Friday rose to the highest since the March crisis, hitting $106.25BN alongside a $53.2BN in 20 day repos, and earlier on Monday saw another $67.05BN in overnight repo (across both TSYs and MBS). While there is some debate about the cause for this apparent tightening in financial conditions, the simplest explanation is that as the Fed continues to shrink its daily POMO, which this week averages just $4.5 BN per day, dealers have to find other means to extract liquidity and are increasingly turning to the Fed’s repo operations.

The question here is whether the Fed has shrunk its QE to a point that is unsustainable in light of surging treasury supply, which as a reminder, should amount to trillions more in the near term. One place where this theory has validation is in long-term yields, which spiked late last week, and sharply steepened the yield curve.

Commenting on this, JPM’s Nikolaos Panigirtzoglou said that “steepening of the U.S. Treasury curve reflects to a significant extent high (bond) supply versus QE.” He then echoed a warning we posted some time ago, namely that “the Fed at $4-5 billion QE a day is not doing enough to offset supply. It would become more challenging for the Fed if the 10-year…yield approaches 1%.“

Of course, at that point the Fed can simply launch Yield Curve Control to make sure the Fed does not lose control, although according to a WSJ article over the weekend from the Fed’s current “whisperer” Nick Timiraos, “Fed officials aren’t prepared to announce any decision on so-called yield caps when their two-day policy meeting concludes Wednesday.” Perhaps, but that may change fast should the blow out in yields accelerate and the 10Y rise above 1%.

Meanwhile, as Wrightson ICAP economist Lou Crandall writes, when the Federal Reserve announces the next repo operations schedule this week, it’s unlikely it will make “any significant changes,” as Powell has repeatedly said that the Fed is in no hurry to “normalize” its operations, and the April minutes put the market on notice that the terms of the Desk’s repo funding would probably become less generous over time.

According to Crandall, it’s also unlikely the Fed sees any near-term need to push repo rates higher as the cumulative effect of the Treasury’s bill issuance in April and May has begun to push overnight rates higher this month and the “prospect of large seasonal outflows” from money funds during the delayed tax season in July could create additional pressures next month. Also of note, the ICAP strategist notes that the Fed has been “quietly” scaling back its repo market footprint by shortening tenors and reducing the frequency of its term operations.

Putting all this together, between the shrinking amount of weekly QE and the Fed’s scaling back of the repo market, it is distinctly possible that we may soon get a rate tantrum as bond traders realize that there is not enough organic demand to prefund the trillions in budget deficits over the horizon, and that another market “intervention” will be needed by the Fed to restore the generous liquidity conditions from March/April with the US continuing to spend like a drunken sailor.

via ZeroHedge News https://ift.tt/30nKdSq Tyler Durden

“I’ve Been Far Too Cautious”: Druckenmiller Admits He’s “Humbled” By Fed-Enabled V-Shaped Market Recovery Tyler Durden

Mon, 06/08/2020 – 09:55

Stanley Druckenmiller took to CNBC Monday morning to admit that he “underestimated” the power of the Federal Reserve and that he had been “humbled” by the market’s V-shaped recovery.

Of course, what he meant is the Federal Reserve’s “power” to completely and totally rig markets, but, nonetheless, the longtime hedge fund manager offered up a mea culpa of sorts – seemingly surrendering any concerns he had about monetary policy as unwarranted.

“Well I’ve been humbled many times in my career, and I’m sure I’ll be many times in the future. And the last three weeks certainly fits that category,” he said.

Druckenmiller continued:

“I had long-term concerns for the last few years that because of easy money, too much debt was being built up in the corporate sector. When Covid hit, I was pretty much of the view that there was a good chance that the credit bubble had finally burst and the unwinding of that leverage would take years.”

“The risk-reward for equity is maybe as bad as I’ve seen it in my career,” Druckemiller said back in May.

The Fed promptly made a fool of Druckenmiller, as stocks rallied more than 11% since those comments. The Fed also seemed to demoralize Druckenmiller, who admitted Monday morning he had been “far too cautious” about things.

“I would say since that time, a couple things have happened technically. I would also say I underestimated how many red lines, and how far, the Fed would go.

I’ve been far too cautious. I was up 2% the day of the bottom and I’ve made all of 3% during the [market’s] 40% rally,”

“What is clearly happening is the excitement of reopening is allowing a lot of these companies that have been casualties of Covid to come back and come back in force. With a combination of the Fed money and, in particular, a vaccine where the news has been very, very good,” Druckenmiller concluded.

While the market has rallied over the last 2 weeks due to vaccine hopes and businesses re-opening, they’re also being helped along by massive tailwinds like 0% rates, unlimited QE and the Fed buying corporate junk bonds.

via ZeroHedge News https://ift.tt/2A5RSu9 Tyler Durden

Trump Uses ‘Defund The Police’ Movement Against Biden As Minneapolis Faces Uphill Battle Tyler Durden

Mon, 06/08/2020 – 09:40

President Trump has been linking Joe Biden with a Democrat-led movement to “defund the police,” as the city of Minneapolis City Council pledged to “begin the process” of dismantling its police force, according to Bloomberg.

“The ‘Defund the Police’ movement is growing in Joe Biden’s party and he is forced to own it,” said Trump campaign communications director Tim Murtaugh. “Police organizations have noticed that Biden has abandoned them as he moved far to the left to appease the most radical elements in his party.”

Biden notably hasn’t endorsed the movement – though as another new Democrat slogan goes, “silence equals consent.”

The movement to defund the police comes after the murder of George Floyd, a black man who died after a Minnesota police officer knelt on his neck for over eight minutes. Activists supporting the idea have taken a range of positions – including shifting money towards ‘economic and social ills that disproportionately affect blacks and other people of color,’ according to the report.

“When we talk about defunding the police, what we’re saying is invest in the resources that our communities need,” said Black Lives Matter co-founder Alicia Garza in an appearance on NBC‘s “Meet the Press.”

Uphill battle

While Minneapolis has a veto-proof majority with 9 out of the council’s 13 members supporting the measure, actually defunding the police won’t be that easy according to local TV station Fox9.

According to the city charter, the council is responsible for the funding of the department — and is required to maintain a minimum force determined by the city’s population — about 723 officers based on recent population estimates.

The mayor’s office is given “complete power” over the department under the charter as well. Currently, the city’s budget allows for about 888 sworn officers.

In order to change, the charter, an amendment would require a public vote or full approval of the entire city council along with the mayor. –Fox9

“We might have to take it to the people to have a vote on it, but I think there are a lot of ways in which the council can move forward with the plan even if the mayor isn’t on board,” said Councilmember Jeremiah Ellison, who is in support of the effort.

BREAKING: Minneapolis City Council President says having police is a sign of ‘privilege’ pic.twitter.com/NPVON4cseJ

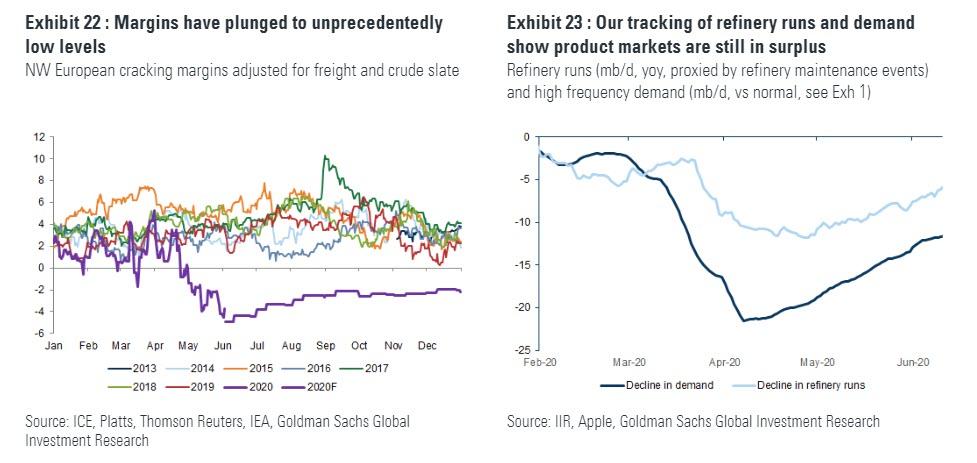

Goldman Turns Bearish On Oil Again, See Brent Dropping Back To $35/bbl Tyler Durden

Mon, 06/08/2020 – 09:12

Yesterday, when commenting on the latest developments in the oil market, including the OPEC+ agreement to extend supply cuts by one month and the Aramco decision to boost oil export prices by the most on record, we said that “the problem for OPEC+ is that after the February/March supply glut turned into a shortage as demand rebounded, the biggest risk for oil prices is back, with the WSJ reporting that as oil prices continue to rise, American oil producers are reopening the spigots, and companies including Parsley Energy and WPX Energy are starting to turn some of those wells back on, even as they continue to put off most new drilling. The result will be a surge in new output which will reverse the benefit from the OPEC+ output cuts, and once again shift the equilibrium in the global oil market to one of oversupply.”

Well, just 24 hours or so later, Goldman’s energy analyst Damien Courvalin, who on May 1 turned bullish on oil (after being one of the first in mid-March to correctly warn that negative oil prices are coming) expecting a jump in prices from record lows due to a sharp reversal in supply/demand dynamics in the oil market, has agreed with us, and in a note discussing the latest fundamental drivers in the oil market, says it has turned “short-term bearish” on oil, for the following four reasons: i) the unprecedented collapse in oil margins to unprecedented lows (which is reflective of both over-valued crude prices as well as a more moderate demand recovery); ii) demand expectations are running ahead of a more gradual and still highly uncertain recovery; iii) shale and Libyan shut-in production are coming back online, and iv) prices are at levels where OPEC supply cuts should ease and Chinese purchases slow.

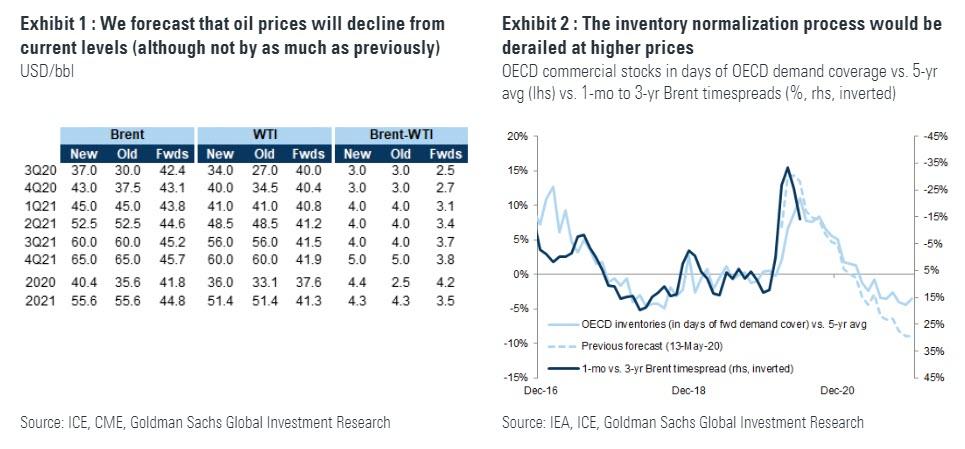

As a result, Goldman now sees a tactical “pull-back in prices in coming weeks with our short-term forecast of $35/bbl vs. Brent spot prices of $43/bbl.”

Below are the key excerpts from Courvalin’s note:

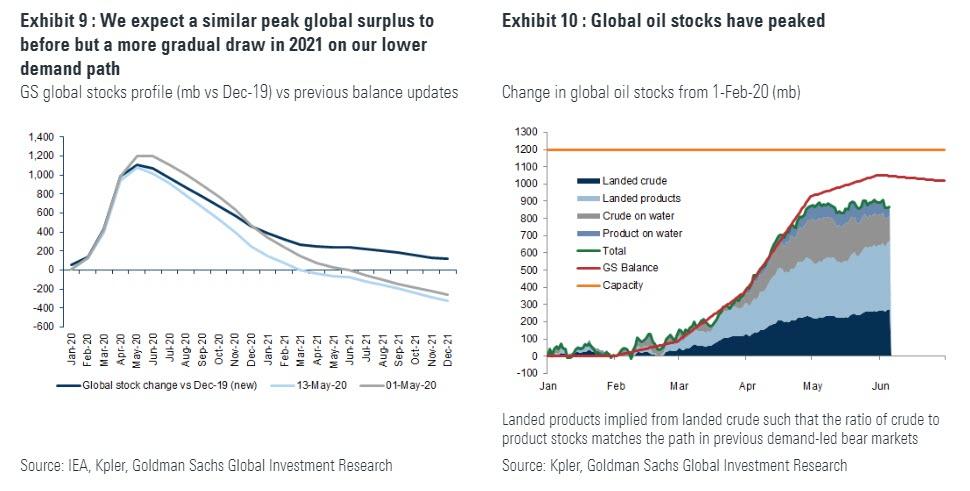

The oil market only moved into deficit late May and still faces the daunting challenge of normalizing a billion barrels of excess inventories. Yet, the oil relief rally remains unfazed, with prices doubling and exceeding our year-end price target just six weeks after the likely cycles lows.

This rebound has been fueled by a macro risk-on backdrop and a policy induced Chinese crude import binge yet fundamentals are turning bearish: demand expectations are running ahead of a more gradual and still highly uncertain recovery, shale and Libyan shut-in production are coming back online, and prices are at levels where OPEC supply cuts should ease and Chinese purchases slow.

With OPEC’s latest cut already more than priced in, we now forecast a pull-back in prices in coming weeks with our short-term Brent forecast of $35/bbl vs. spot prices of $43/bbl. Just as strengthening physical oil prices led us to turn constructive on the oil market on May 1, very poor refining margins and the recent sharp decline in US crude bases now comfort us in our sequentially bearish outlook.

When we turned constructive on the oil outlook last month, we argued that after the initial relief rally, the second stage of the oil market recovery – the cyclical tightening – would be gradual as the inventory normalization takes time and requires patience. We reiterate this view as it is rooted in the binding reality of excess inventories for a physical asset like oil, with the overhang set to break the recent high correlation with anticipatory financial assets.

The oil market rebalancing continues, with our latest fundamental update pointing to supply and demand improvements likely to have brought the global market into deficit late-May. Despite this notable inflection, the inventory overhang remains significant and uncertainty remains high for the forward supply and demand outlooks.

The oil rally remains unfazed, however, with Brent prices doubling and exceeding our year-end price target just six weeks after the likely cycles lows. We see three reasons behind this rebound: (1) a macro risk-on backdrop with oil rallying with equities and dollar depreciation, (2) a policy induced Chinese crude import binge, and (3) frictions in releasing crude from storage as the deficit starts.

While positioning leaves room for this rally to continue, we see four reasons why fundamentals are likely to set the stage for a pull-back in coming weeks:

(1) demand expectations are running ahead of a more gradual and still uncertain rebound,

(2) both shale and Libyan shut-in production are currently restarting,

(3) prices are nearing levels where OPEC supply cuts should ease and Chinese purchases slow, and

(4) the inventory overhang remains daunting with our latest deep dive still pointing to 1 bn in excess stocks.

The scale of the rally and the size of the inventory overhang are two challenges for OPEC+, threatening the higher prices, volumes and market-share targeted through 2021. While large cuts are needed to normalize excess inventories, too long a cut instead benefits competing high-cost producers, with US E&P HY debt issuance restarting. As we have argued, this should point to OPEC soon targeting higher output before shale activity inflects. If successfully carried-out, such a strategy should weigh on long-dated prices, helping achieve the backwardation that benefits low-cost producers.

Our modeling suggests, in fact, that OPEC’s latest cut is already more than priced in, especially with Libyan production restarting. With the oil relief-rally set to run out of steam and the expected volatility normalization playing out, our tactical market views are now for a pull-back in WTI and Brent prices in coming weeks. As previously, physical oil prices will be key to signaling the inflection lower, as they typically offer the best insight in periods of high fundamental uncertainty. To that end, very poor refining margins globally and the recent sharp decline in US crude bases comfort us in our sequentially bearish outlook.

Our updated supply and demand forecasts as well as the macro repricing of the positive start of the reopening nonetheless point to less downside to current Brent spot prices of $43/bbl than our prior $30/bbl June spot forecast. Our updated short-term Brent price forecast is now $35/bbl with our year-end spot forecast now of $45/bbl, with a similar $6/bbl average forecast increase through 2H20 for WTI.

Although our global inventory path is nearly unchanged, our accounting points to a smaller accumulation in OECD countries, with instead higher EM (especially China) stocks, which are once again helping smooth global oil shocks. On our quantitative pricing model which links the level of OECD inventories to the shape of the Brent forward curve[1], this points to a shallower Brent contango, leading us to raise our spot price forecast from $30/bbl to $35/bbl. Our OECD inventory path – and hence Brent curve shape forecasts – remains unchanged for 2H20, although we now expect higher long-dated prices than previously.

The positive start to reopening does not resolve the uncertainties about a potential second wave of infections or of a more difficult recovery beyond the easier gains of the first few months. However, it does increase the probability of our economists forecasts materializing, which are based on a relatively optimistic view of both of these issues. This has reduced the bearish biases reflected in market forwards, with dollar weakness further raising the marginal cost of non-US production and hence long-dated prices. Accounting for these improvements, we are also raising our forecast for long-dated (3-year forward) Brent prices by c. $6/bbl in 2H20 to $45/bbl – although still below current market forwards.

After their recent rally, we estimate that long-dated prices have, however, more than fully priced in this good news, reaching levels where US producers will re-start shut-in production and contemplate bringing online drilled but uncompleted wells, helped by the collapse in oil service costs. We believe such an activity restart is premature given the exceptional level of OPEC spare capacity and with the inventory overhang barely dented.

When we turned constructive on the oil outlook on May 1, we argued that the second stage of the oil market recovery – the cyclical tightening – would be gradual as the inventory normalization takes time and requires patience, leaving oil to lag other risky assets. We reiterate this view as it is rooted in the binding reality of excess inventories for a physical asset like oil, with the overhang set to break the recent high correlation with anticipatory financial assets. The path of oil prices remains important – lower oil prices need to clear today’s inventory overhang and, as a physical asset, cannot price the expected tightening in fundamentals that we forecast through 2021, where our price forecasts remain unchanged, above market forwards and consensus expectations.

via ZeroHedge News https://ift.tt/2MDVEgL Tyler Durden

“Today Is A New Day” – NYC Begins Lifting Lockdown, New Zealand Declared “Coronavirus Free”: Live Updates Tyler Durden

Mon, 06/08/2020 – 09:00

Following nearly 2 weeks of peaceful protests pockmarked by violence and looting – killings and shootings skyrocketed across NYC last week as the summer ‘killing season’ begins – America’s biggest “hot zone” kicked off “Phase 1” of its plan to reopen its economy on Monday, exactly 100 days after the first case of the virus was confirmed.

Since the outbreak began, more than 205,000 New Yorkers who have tested positive for the virus, while another 22,000 succumbed to the virus.

Exactly 100 days since its first case of coronavirus was confirmed, New York City, which weathered extensive hardship as an epicenter of the worldwide outbreak, is set to take the first tentative steps toward reopening its doors on Monday.

According to the NYT, as many as 400,000 workers will return to construction jobs, manufacturing sites and retail stores in the city’s first phase of reopening as the number of COVID-19 deaths recorded across the US continues to fall, with fewer than 1,000 deaths reported each day (remember when the NYT claimed that deaths would be north of 3,000/day by June 1?).

It’s a far cry from the ‘peak’ of the outbreak, when 800 NYC residents were dying from the virus every day.

The city ran more than 60k tests a day over the weekend, Gov Cuomo claimed.

That is low enough for New York City’s corps of contract tracers, who began work last week, to try to track every close interaction and, officials hope, stop a resurgence of the virus.

“You want to talk about a turnaround — this one, my friends, is going to go in the history books,” Gov. Andrew M. Cuomo said on Saturday.

Of course, it could be months before office workers return en masse, as the world waits to see how the city’s public transit will handle social distancing concerns. And for many retailers in the city, the conditions in ‘Phase 1’ are still too restrictive. Simply reopening doesn’t mean customers will return, and curbside pickup doesn’t make a lot of sense for many retailers either, according to the NYT. Business groups in the city say many retailers are waiting for the next phase to venture out, when outdoor dining is allowed, office workers are permitted to return and shoppers are allowed to take their time and browse. The earliest these shops might be able to reopen would be later this month.

Some employers have developed new technological solutions to this problem. When more than 100 workers return to Newlab, a “technology hub” in the Brooklyn Navy Yard, they will be offered a device that buzzes whenever they get too close to another worker. The essential workers that have remained in the office this entire time have already been wearing the devices.

The city’s army of thousands of contact tracers officially started their work last week, and will continue aiding in efforts to quash a rebound in infections. Meanwhile, city officials will be closely monitoring a suite of metrics, from emergency room admission data to new case numbers, for signs of a potentially crippling resurgence.

On the other side of the world, New Zealand lifted all social and economic restrictions except for its border controls on Monday after declaring that the small island nation is “coronavirus free”, making it one of the first nations to return to normalcy after the outbreak. Prime Minister Jacinda Ardern said she “danced for joy”. Restaurants, retailers, transit and virtually everywhere else reopened without mandatory social distancing. It has been 17 days since the country recorded a new case of the virus.

“While the job is not done, there is no denying this is a milestone … Thank you, New Zealand,” Prime Minister Jacinda Ardern told a news conference, saying she had danced for joy at the news.

“We are confident we have eliminated transmission of the virus in New Zealand for now, but elimination is not a point in time, it is a sustained effort.”

Globally, the total case count topped 7 million late last night, while the number of deaths passed 400k over the weekend, as Brazil, Mexico, Russia and possibly India struggle to bring the outbreak to heel. In the US, the number of confirmed cases have surpassed 1.9 million, and the 2 million mark draws ever-nearer, with ~1.94 million as of Monday morning. At the current rate of ~20k cases a day, the US is on track to pass its next grim pandemic milestone by Thursday.

via ZeroHedge News https://ift.tt/3h4wqWQ Tyler Durden

Rabobank: “There Is A LOT Of Anger Out There, And The Post-War Architecture Is Clearly Collapsing” Tyler Durden

Mon, 06/08/2020 – 08:48

Submitted by Michael Every of Rabobank

Keep on Rockin’ in the Free World

It was already going to be easier to have a “What is happening in markets” section and then a separate “What is happening in reality” in this Daily. Things are now complicated by the ‘reality’ no longer being the reality, as the US version of Goskomstat provides jobs data they admit are wrong (counting millions of unemployed as employed, and let’s not even start on how the business births/deaths model ‘works’ when everything is shut down). In short, Friday’s payrolls report was legendary. It was supposed to be down 7.5m and was actually up 2.5m, the largest and most significant ‘beat’ ever.

Goskomstat were wrong, as they say themselves. The economists’ forecasts were also wrong: does that surprise anybody? And the markets are wrong too. They seem to think Trump was right when, with no sense of irony, he almost sang “Keep on Rockin’ in the Free World” about the data. What we have is a not a V-shape but a reverse tick shape: down huge and up a little (and even less than shown). Yes, at least it’s not still down. Yes, some more jobs will come back as reopening begins. But many sectors won’t, and once government payroll support schemes end we will see just how ugly things really are. Oh, and Forbes today underlines that US-Europe air fares are about to double to cover the cost of a nearly empty plane.

Nonetheless, dollar down big, bonds down big, and equities up big: because bad news is good news for stocks and good news is also good news, apparently. On which note, when does the Fed have to do something about longer-dated yields? Because if the market keeps pricing in recovery like this then we aren’t going to have one: that’s the corner we have brilliantly been painted into over the past 40 years by our central banks. Moreover, market bullishness ignores word from Mitch McConnell that any further stimulus likely won’t now get past the Republicans in Congress. Friday saw the president talk about a payroll tax cut and a separate report saying the White House might introduce tax reforms to accelerate the on-shoring of US supply chains from China, with lower taxes floated in areas with higher minority representation and/or business ownership. Keep on Rockin’ in the Free Market, eh?

Meanwhile, back in the real world Chinese May trade data showed their exports -3.3% y/y and yet imports slumping 16.7% y/y: this shows both domestic weakness AND mercantilism that pushes us towards global trade war; and the US is threatening tariffs on the EU and China if they don’t buy more lobster. How emblematic of our times: “Eat more luxury food now – or else!”

Trump is already to remove 10,000 troops from Germany (and the same number of National Guard from Washington DC) as a shot across the bows of peacenik Angela Merkel. Poland will get some of them, and many others could just leave Europe – if this goes through. Not to worry: the EU are ready, willing, and able to fill that gap in vital national security in increasingly uncertain times. Just let them sort out the budget and the economy and the banking system and Brexit and North/South and East/West splits and then build up their own defence industries up first, please, cruel world.

China is meanwhile threatening Australia by saying no more tourists or students should go there (though with the borders shut it is all talk for now); threatening the UK with walking away from building its nuclear power stations if Boris drops Huawei (“Please do!” say the British press); and there are whispers from Beijing of threats that Hong Kongers who claim a British National Overseas passport and then become UK citizens would directly lose Chinese citizenship and right of abode in Hong Kong.

Linking Hong Kong and the US/West are major street protests. There were social-media reports of “Mazel Tov cocktails” being thrown at police in the US over the weekend: I don’t think that happened. Yet in sharp contrast to Hong Kong, the US has already seen a major street in DC renamed “Black Lives Matter Plaza”; New York and LA have sharply reduced their municipal police budgets and raised community funding; and Minneapolis, where the George Floyd protest started, has voted to defund the police department entirely and move towards community-based schemes. Meanwhile, in the UK police allowed protestors to topple a statue of a former slaver (and local philanthropist) in scenes similar to Baghdad when Saddam’s statue fell. Indeed, the British government, which has seen its support drop by 20 percentage points over its poor virus handling, is trying to signal that it supports the protestors in spirit. In the US, Trump is clearly going for a more Nixon-style ‘Law and Order’ approach in 2020, which will at least will leave voters a clear choice.

Removing police departments in one of the world’s most heavily-policed (and violent) societies and tearing down public statues in a traditionally conservative country – those are radical overnight changes.

Should markets take heart that Western democracies are capable of rapid reinvention, mirroring the flexibility that markets themselves once offered? Or should less-flexible markets take heed of these revolutionary headwinds and fear where they might lead next? After all, there is still a LOT of anger out there, and the post-War and post-Cold War architecture is clearly collapsing. Or will markets just shrug and rally exactly as they did after Saddam’s statute fell (regardless of what loomed for Iraq itself)? Note Bloomberg’s top headline today was “AstraZeneca Proposes Gilead Deal Talks” – which is surely tied to hopes of maximizing profit over a potential Covid-19 vaccine. What was the Global Daily saying on Friday about the communist Morning Star’s headline on the day the Berlin Wall fell?

Finally, Brazil has decided to stop reporting Coronavirus death data; one could say markets are doing the same.

Keep on Rockin’ in the Free World.

via ZeroHedge News https://ift.tt/3dVfK1S Tyler Durden

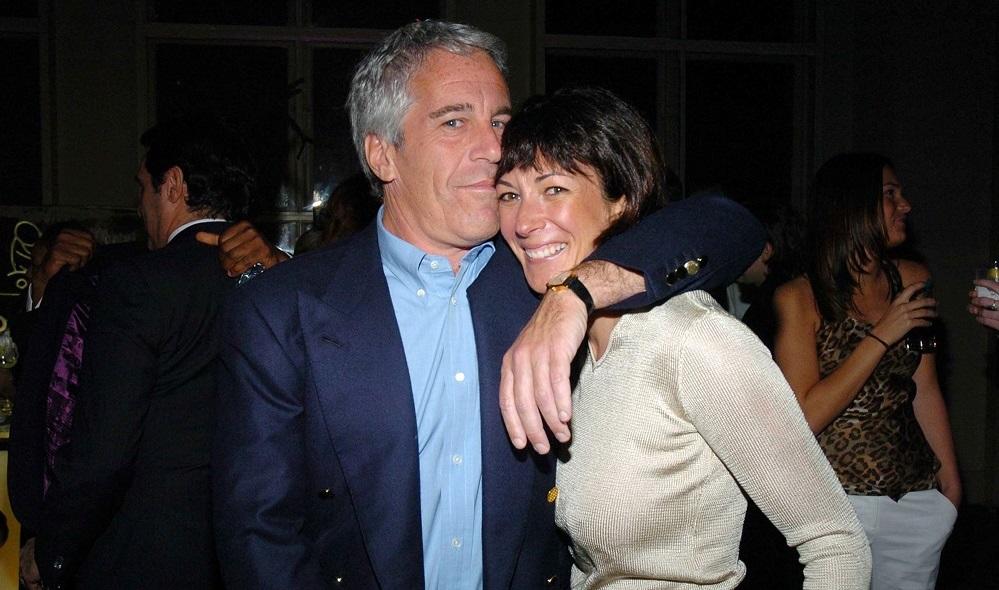

DOJ Demands Prince Andrew Testify In Criminal Investigation Of Jeffrey Epstein Accomplices Tyler Durden

Mon, 06/08/2020 – 08:29

The Justice Department has made a formal request that the British government hand over Prince Andrew for questioning over his relationship with deceased pedophile Jeffrey Epstein, according to The Sun and confirmed by ABC News.

The request, made on behalf of prosecutors for the Southern District of New York would force the 60-year-old Andrew to help prosecutors investigate Epstein’s accomplices – despite his previous empty offer to cooperate. The DOJ filed for “mutual legal assistance” (MLA) directly with Britain’s Home Office, bypassing Buckingham Palace.

As The Sun notes, MLA requests are only used in criminal cases under a legal treaty with the UK, which if granted would formally request Andrew’s attendance at the London City of Westminster Magistrates’ Court for oral or written evidence under oath while DOJ lawyers question him. If he refuses, the Duke could be forced to attend by summons. That said, the evidence session could be held privately “in camera” without the public or press present.

And unlike the Queen Andrew does not enjoy sovereign immunity from prosecution. He could, however, “plead the Fifth” to avoid self-incrimination according to the report.

Last month former federal prosecutor Evan T Barr told Law.com “While the Prince would retain the right to decline to testify under the Fifth Amendment to the United States Constitution, the impact on his already diminished reputation would be considerable and an adverse inference could be drawn against him in the related civil litigations, leading to a possible default judgment.”

Until now, it was thought that Andrew would at most have to answer to Epstein’s victims in US civil courts – not the US government.

Accuser attorney Lisa Bloom said Andrew had been an “enabler” of Epstein’s crimes. He has been accused of having sex with Virginia Roberts Giuffre in 2001, when she was 17 – however the Prince has claimed in an interview that he was at a Pizza restaurant in Woking during one of the alleged encounters.

Alleged victim Virgina Roberts Giuffre says she was trafficked by Epstein to have sex with Andrew in London in 2001.

She described Andrew as “sweating profusely” at Tramp nightclub before having sex at Ghislaine’s Mayfair flat.

Was this the night he Andrew claims he was indulging in Pizza?

According to The Sun, the request – which has yet to be addressed by British officials – is likely to cause a diplomatic row with the US.

“It’s a huge statement of intent from the US and it moves Andrew into the realms of a criminal investigation,” said one source, adding “It’s also frankly a diplomatic nightmare.“

Andrew admitted to being friends with Epstein since 1999 following an introduction through socialite and Epstein’s so-called ‘madam’ Ghislaine Maxwell. Epstein and Andrew got together on at least ten occasions – with the Duke staying at the pedophile’s New York mansion, his Palm Beach home and his private ‘pedo’ island in the US Virgin Islands.

via ZeroHedge News https://ift.tt/3dMKRwS Tyler Durden

Before he knelt on Floyd’s neck, Chauvin was the subject of 18 prior complaints filed against him with the Minneapolis Police Department’s Internal Affairs.

Only two of the 18 complaints were “closed with discipline,” according to a MPD internal affairs public summary. In both cases, Chauvin received a letter of reprimand.

We do not know whether any of the other complaints were valid or not.

But 18 seems like quite a bit and it is certain that most valid charges are swept under the rug.

Already, the Minneapolis union signaled it wants to protect the other three officers complicit in the death of George Floyd.

Prosecutors Charge Police Inspector

On Friday, Philadelphia Inspector Joseph Bologna smashed a student on the back of the head.

Staff Inspector Joseph Bologna faces charges of aggravated assault, simple assault, possession of an instrument of crime and recklessly endangering another person, Philadelphia District Attorney Larry Krasner announced Friday.

Prosecutors say Bologna was captured on cell phone video striking a Temple University student in the back of his head while he was participating in a mass demonstration on Monday.

The unidentified student suffered “serious bodily injury, including a large head wound that required treatment in a hospital while under arrest, including approximately 10 staples and approximately 10 sutures,” Krasner’s office said.

Philadelphia police arrested the student protester and detained him for more than 24 hours and referred him to the district attorney for prosecution. But after prosecutors reviewed the video and other evidence, Krasner declined to charge the student and charged Inspector Bologna instead.

Police Unions Defend Nearly Anything

The Philadelphia Fraternal Order of Police vowed in a statement to “vigorously defend Bologna against these baseless allegations and charges.”

The police union said they were “disgusted” to learn about the charges. Bologna, a police officer for more than 30 years, was “engaged in a volatile and chaotic situation with only milliseconds to make a decision,” the union said.

Public Unions are the Problem

It is nearly impossible to get rid of bad cops and bad teachers.

It takes outright murder caught on video before police unions don’t look the other way. Even then, the union tries to protect the others involved.

The same happens with teachers who abuse kids, Bad teachers cannot be dismissed.

Matthew Lang was a band director at O’Fallon Township High School in Illinois in 2007 when administrators learned he was having a sexual relationship with a 17-year-old female student. But instead of being fired, Lang was able to resign, and the relationship was kept out of his file so he could seek another teaching job.

“… we are asking that all information concerning the request for his resignation not be placed in his file,” read a letter from the teacher’s union rep to the O’Fallon school board that was originally obtained by education news site EAGnews.

The district complied and even provided a letter of recommendation that called Lang “an outstanding instructor.” Lang landed a job with Alton High School near the Mississippi River and about 15 miles north of St. Louis, Mo.He worked at the school until 2010, when he was convicted of molesting another female student and sentenced to six years in prison, according to the St. Louis Post-Dispatch.

Jon White was sentenced to 48 years in prison in 2008 for abusing ten students at schools in the Illinois towns of Urbana and Normal. But those victims might have been spared their ordeals if White’s past had been revealed.

He had previously worked in McLean’s school district, where he was twice suspended for viewing pornography on a school computer and for making sexually suggestive comments to a fifth-grader. Instead of being fired, the union-protected teacher was allowed to resign – with a letter of recommendation that made no mention of the incidents.

There are 10 more stories like that in the one article above.

The police officer who killed George Floyd had been the subject of more than a dozen complaints about his conduct. In two previous incidents, Derek Chauvin had been disciplined with letters of reprimand. Tou Thao, who stood by as Floyd died, previously had a lawsuit brought against him over excessive use of force. The lawsuit was settled for $25,000. How can such men be allowed to “serve and protect”? Unions.

Public-sector unions, including police unions, will do almost anything to protect their members. These unions create a culture of impunity. Even police officers who are terminated can be reinstated, “often via secretive appeals geared to protect labor rights rather than public safety” as a 2014 piece in the Atlantic put it.

All Government employees should realize that the process of collective bargaining, as usually understood, cannot be transplanted into the public service. It has its distinct and insurmountable limitations when applied to public personnel management. The very nature and purposes of Government make it impossible for administrative officials to represent fully or to bind the employer in mutual discussions with Government employee organizations.

Particularly, I want to emphasize my conviction that militant tactics have no place in the functions of any organization of Government employees. Upon employees in the Federal service rests the obligation to serve the whole people, whose interests and welfare require orderliness and continuity in the conduct of Government activities. This obligation is paramount. Since their own services have to do with the functioning of the Government, a strike of public employees manifests nothing less than an intent on their part to prevent or obstruct the operations of Government until their demands are satisfied. Such action, looking toward the paralysis of Government by those who have sworn to support it, is unthinkable and intolerable. It is, therefore, with a feeling of gratification that I have noted in the constitution of the National Federation of Federal Employees the provision that “under no circumstances shall this Federation engage in or support strikes against the United States Government.”

Roosevelt was discussing strikes, but public unions threaten them all the times, especially teachers’ unions. They demand money “for the kids”. The school boards are padded with teachers demanding more money “for the kids”.

Collective bargaining cannot possibly exist in such circumstances. Unions can and have shut down schools. The unions do not give a damn about the kids.

Notice I said “unions” do not give a damn. Many, if not most, teachers do care for the kids, but the union does not. The unions can, and do, protect teachers guilty of abusing kids. It is nearly impossible to get rid of a bad tenured teacher or a bad cop.

Unions also threaten to shut down mass transportation.

None of this is in the public interest.

Abolish Public Unions Entirely

Union leaders have a mandated goal of protecting bad cops, bad teachers, and corrupt politicians. Unions blackmail politicians and threaten the public they are supposed to serve.

Union leaders will do anything to stay in power, the kids and the public be damned.

The only way to deal with the situation is to “effectively” abolish public unions entirely.

The key word is effectively. What do I mean by that? Take away 100% of their power as opposed to ending their right of association.

Recommended Steps

National right-to-work laws

Abolishment of all prevailing wage laws

Ending public unions ability to strike

Ending collective bargaining by public unions

Consider Illinois’ prevailing wage laws: Prevailing wages are union wages. Municipalities and businesses have to pay prevailing wages. If they do not hire union workers, they get picketed.

Why bother hiring non-union workers if you have to pay union wages in the first place?

As a direct result, municipalities and businesses must overpay for services in Illinois.

Illinois is Bankrupt

Not only do public unions protect bad cops, bad teachers, and bad employees in general, Illinois is bankrupt after giving in repeatedly to union contract demands and pension spiking.

Fundamental Problem

Lost in the wake of the death of George Floyd is the simple fact that officers like Chauvin may have long ago been weeded out had corrupt union not protected bad cops.

President Trump had two years with a Republican Congress to pass legislation on right-to-work, collective bargaining, national bankruptcy reform and other related items.

His scorecard is a perfect zero.

It will be interesting to see if he cowers to the unions in the next 5 months in an attempt to get re-elected.

Police Unions Love Uprisings

The unions love these uprisings. They will use it to demand more cops, higher pay, and more prisons.

Public Unions Have No Business Existing: Even FDR Admitted That

The unions are willing to hold the public hostage without police service, without fire service and without schools to get what they want.

“So tell me Mish. How do you reconcile your admission with the Police unions being at the heart of the problem with your support for the Democratic party which fully supports public unions.”

My Reply

How the hell do you conclude I support the Democratic Party?

I speak out against what is wrong.

Speaking out against Trump does not make me a Democrat. Speaking out against Obama as I frequently did does me me “Radical Right” and yes, I was accused of that.

I am tired of idiots who support people and parties instead of ideas.

via ZeroHedge News https://ift.tt/2YaeS2U Tyler Durden

Global Stocks Rise, S&P Futures Above 3,200 As Melt-Up Continues Tyler Durden

Mon, 06/08/2020 – 07:59

One day after a record surge in Nasdaq trading volumes on Friday, which was coupled with a record spike in call option activity as both retail and hedge fund investors rush into stocks, global stocks inched higher again on Monday, adding to a 42% surge from their March lows, as the unexpectedly strong US jobs report data fuelled hopes of a quicker global economic recovery from the coronavirus pandemic. Emini futures jumped in early trading overnight then drifted in a range between 3,185 and 3,210.

In stock-specific news, Bloomberg over the weekend reported that AstraZeneca approached Gilead regarding a potential merger which would mark the largest healthcare deal on record. However, sources via The Times downplayed the prospect of any AstraZeneca interest, stating that it has abandoned a tentative interest, while Wall Street analysts puked on the prospects of the deal. Gilead was 3.3% higher in pre-market.

The MSCI all-country world stocks index was 0.1% higher and just 7% away from a fresh record high, while the benchmark S&P 500 is within striking distance of turning positive for the year.

In Europe, a surge in travel and leisure stocks helped cap losses on the pan-regional index, which traded 0.2% lower after poor German and Chinese economic data. The Eurostoxx 50 was weighed down by tech and healthcare names while the FTSE MIB and IBEX bucked the trend, rising over 0.5% supported by banks and autos.

Europe’s fundamentals remain dismal with German industrial output slumping a record 17.9% in April and firms now expect a bumpy road ahead despite a massive stimulus package.

“European stocks are probably under pressure following weak China data overnight. However, we do not think this marks the end of the rally,” said Marija Vertimane, senior strategist at State Street Global Markets. “We are beginning to see evidence of economic data improving gradually and thankfully no major secondary spikes in infections. We expect that to encourage investors to come back to the market.”

Asia shares rose in a catch-up rally following Friday’s U.S. jobs data but were again capped by the Chinese data, published on Sunday, which showed exports contracted in May although an even bigger drop in imports resulted in a record trade surplus. All markets in the region were up, with Jakarta Composite gaining 2.5% and Singapore’s Straits Times Index rising 1.4%. Trading volume for MSCI Asia Pacific Index members was 25% above the monthly average for this time of the day. The Topix gained 1.1%, with Asahi Broadcasting Group and Gumi rising the most. The Shanghai Composite Index rose 0.2%, with Fujian Start Group and Changshu Fengfan Power Equipment posting the biggest advances.

In rates, the payrolls report pushed the 10-year Treasury yield as high as 0.959% on Friday, a level not seen since mid-March. It last stood just below 0.91%. The rise in U.S. yields has put more focus on the Fed which will hold a two-day policy meeting ending on Wednesday.

“Steepening of the U.S. Treasury curve reflects to a significant extent high (bond) supply versus QE (quantitative easing),” Nikolaos Panigirtzoglou, strategist at JPMorgan, said. “The Fed at $4-5 billion QE a day is not doing enough to offset supply. It would become more challenging for the Fed if the 10-year…yield approaches 1%.”

Pointing to the spread between U.S. two- and 10-year Treasury yields widening above 70 basis points to its highest since February 2018, Panigirtzoglou believes there is scope for Fed to introduce yield curve control measures.

In Europe, Bunds and peripheral spreads were quiet ahead of ECB President Lagarde’s appearance at a European Parliament hearing later Monday.

In FX, the dollar fell against a basket of its peers and headed for the longest losing streak since 2011. The broad improvement in sentiment weighed on the safe-haven Japanese yen, which stood at 109.5 to the dollar, near Friday’s 10-week low of 109.85. The pound continued its long rally against the dollar on hopes that the U.K.’s coronavirus lockdown restrictions will be lifted more quickly. Australian dollar climbed as iron ore futures surged above $100 a ton after Brazil’s Vale SA was ordered to suspend operations that account for about a 10th of its output after workers contracted Covid-19, boosting concerns surging cases will disrupt its output

In commodities, Brent crude initially climbed above $43 per barrel, but faded some gains after Saudi Arabia said an extra month of production cuts is voluntary and will be self-policed. Over the weekend, OPEC+ unanimously agreed to extend current cuts for one month through July and will review if a longer extension is needed this month, while Saudi and Russia emphasised they want stronger compliance from other nations and both Iraq and Nigeria agreed to slightly deeper cuts. Saudi Arabia set July Arab light crude oil OSP to Asia at Oman/Dubai +USD 0.20 and to north-west Europe at ICE Brent + USD 0.30, while reports noted that the July pricing for all grades to Asia was higher by between USD 5.60-7.30 and the largest hike in prices in 2 decades.

Iron ore jumped after a Brazil mine hit with Covid-19 infections suspended operations.

There is nothing on the US economic calendar for Monday; Thor Industries and Coupa Software are among companies reporting earnings.

Market Snapshot

S&P 500 futures up 0.5% to 3,202.75

STOXX Europe 600 down 0.4% to 373.69

MXAP up 0.7% to 159.96

MXAPJ up 0.4% to 515.34

Nikkei up 1.4% to 23,178.10

Topix up 1.1% to 1,630.72

Seng Index up 0.03% to 24,776.77

Shanghai Composite up 0.2% to 2,937.77

Sensex up 0.5% to 34,463.87

Australia S&P/ASX 200 up 0.1% to 5,998.72

Kospi up 0.1% to 2,184.29

German 10Y yield fell 0.2 bps to -0.279%

Euro up 0.1% to $1.1305

Italian 10Y yield fell 0.9 bps to 1.241%

Spanish 10Y yield rose 1.1 bps to 0.569%

Brent futures up 1% to $42.72/bbl

Gold spot up 0.6% to $1,695.49

U.S. Dollar Index down 0.1% to 96.84

Top Overnight News from Bloomberg

China’s trade surplus surged to a record in May as exports fell less than expected, helped by an increase in medical-related sales, and imports slumped along with commodity prices, data over the weekend showed

Car sales in China rose for the first time in almost a year last month, evidence that the world’s largest auto market is rebounding from the coronavirus crisis and the trade war with the U.S

Saudi Arabia increased prices for some crude exports by the most in at least two decades, doubling down on a strategy to bolster the oil market after OPEC+ producers extended historic output cuts over the weekend

New Zealand will remove social distancing requirements after reporting zero active cases of Covid-19, indicating it has achieved its aim of eliminating the virus

Qatar’s peg against the dollar has been the only one in the region that hasn’t come under pressure even as local economies succumb to what may be their worst recession ever. The nation’s bonds have also outperformed those of the other five members of the Gulf Cooperation Council this year

Asian equity markets began the week relatively upbeat as the region took its first opportunity to react to the strong US jobs data which firmly lifted all major indices on Wall St last Friday and the Nasdaq to a fresh all-time high, with mostly encouraging Chinese trade data and early strength in oil prices following the OPEC+ extension agreement, adding to the constructive risk tone. As such, Nikkei 225 (+1.4%) gapped above the 23k level but with some of the gains later reversed after Final Q1 GDP missed expectations despite showing a significant improvement from the preliminary release, and the KOSPI (+0.1%) outperformed shortly after the open before it briefly wiped out all its gains amid a cooling of inter-Korean relations, as well as weakness in index heavyweight Samsung Electronics as de facto chief and Samsung Group heir Jay Y. Lee attended a court hearing on the arrest warrant related to accounting fraud. Elsewhere, Hang Seng (U/C) and Shanghai Comp. (+0.2%) were kept afloat after the PBoC injected CNY 120bln of liquidity and announced to conduct an MLF operation in around a week’s time, while the latest trade figures from China over the weekend mostly topped estimates which included a record trade surplus in USD terms and a surprise expansion in CNY-denominated Exports. Finally, ASX 200 remained closed for the Queen’s Birthday Holiday and 10yr JGBs were higher despite the gains in stocks as prices reversed Friday’s selling pressure, in which the rebound in JGBs also followed the weaker than expected Japanese GDP data.

Top Asian News

New Zealand to End Social Distancing After Eliminating Covid-19

JD’s $4.1 Billion Hong Kong Listing Is Said to Be Oversubscribed

China’s Monthly Car Sales Rise for First Time in Almost a Year

Hong Kong’s Most Vocal Activist Investor Says He Has Cancer

European equities attempted to nurse earlier losses [Euro Stoxx 50 -0.5%] following on from firm APAC trade as the region had the first chance to react to the blockbuster US jobs data. Europe kicked the session off with broad losses of over 1%, but thereafter recouped amid a lack of fresh catalysts and with investors focusing on reopening economies alongside Central Bank support. Major bourses now see a more mixed performance, as is the case for broader sectors which started trade mostly in the red; stateside, futures remain modestly in positive territory. Energy remains the top gainer, but overall sectors do not reflect a clear risk tone. The sectoral breakdown sees banks and oil & gas topping the charts whilst financial services and IT. In terms of individual movers – the story in focus: AstraZeneca (-2.2%) reportedly approached Gilead (+3% pre-mkt) regarding a potential merger, which would mark the largest healthcare deal on record. However, sources via The Times downplayed the prospect of any AstraZeneca interest, stating that it has abandoned a tentative interest. Meanwhile, Intesa Sanpaolo (+3.4%) and UBI Banca (+4.1%) are higher after the ECB authorised the former’s takeover of the latter. Wirecard (-1.6%) opened lower by over 7% amid reports late-doors Friday that Munich prosecutors said Co’s premises have been searched as part of a market manipulation probe initiated by Bafin; prosecutors have opened a probe against the Co, including the whole management board. Co. said it is cooperating with authorities and reaffirmed guidance. Elsewhere, IAG (+7.8%) extend on gains after British Airways has threatened to dismiss all its 4.3k pilots and rehire them on individual contracts unless it can reach a new employment agreement with the Balpa union. Finally, Danske Bank (+8.9%) has extended on initial gains after the group agreed to sell its troublesome Estonian business in a EUR 312mln deal.

Top European News

German Industrial Slump Hits Bottom With Record Output Drop

Johnson Seeks Path to U.K. Revival as Poll Ratings Slip Away

Private Equity Comes Back With Bridgepoint Reviving Agro Deal

Airbus’s Global Footprint Becomes a Burden as Sector Shrinks

In FX, although risk sentiment has stalled somewhat after Friday’s unexpected rise in US employment, the Greenback remains shy of best levels amidst doubts about the validity and accuracy of the data due to misrepresentation or reporting irregularities. Hence, the DXY has not been able to maintain momentum or revisit post-NFP peaks just above the 97.000 level with the index meandering between 96.985-741 as attention turns to the FOMC and the prospect that the Fed may edge a bit closer to enhancing forward guidance via a more targeted approach yield control.

AUD/NZD/NOK – In contrast to the Buck, bullish impetus is keeping the Aussie, Kiwi and Norwegian Krona elevated as the former hovers a fraction below 0.7000 in holiday-thinned trade, but underpinned alongside the YUAN (Usd/Cnh and Usd/Cny either side of 7.0700) in wake of significantly wider than forecast Chinese trade surpluses forged on above consensus exports even though relations between the 2 countries continue to deteriorate. Note, Aud/Usd has essentially carved out a double top, while the Kiwi is building a firm base on the 0.6500 handle and Aud/Nzd is straddling 1.0700 ahead of NZ fully reopening from COVID-19 lockdown due to no further cases and an impending shift to Alert Level 1. Elsewhere, Eur/Nok has now breached 10.5000 and eyeing the 200 DMA beyond technical support at 10.4387 (March 2 high) against the backdrop of firmer oil prices on the back of OPEC+ reaching agreement to extend the reduced output pact by a further month to the end of July.

GBP/EUR/CAD – Sterling has also retained its upward trajectory and sights on the 1.2700 marker in terms of Cable following a retest of Friday’s circa 1.2730 peak as UK PM Johnson comes under pressure to press ahead with the next stages of lifting coronavirus restrictions, with Eur/Gbp pivoting 0.8900 even though the Euro is keeping tabs on 1.1300 against the US Dollar after last week’s impressive gains and despite more weaker than anticipated Eurozone macro releases in the form of German ip and Sentix sentiment. Meanwhile, the Loonie is gleaning more crude traction around 1.3400 in advance of Canadian housing starts and the aforementioned Fed policy meeting.

JPY/CHF – Both narrowly mixed vs the Greenback and relatively rangebound between 109.69-39 and 0.9639-13 parameters with the Yen noting downward tweaks to final Japanese Q1 GDP and Franc paring some declines against the Euro from sub-1.0900 irrespective of mixed weekly Swiss bank sight deposit balances.

EM – Regional currencies have largely picked up where they left off las week, with the oil and commodity focused Rub, Zar and Mxn all on the front foot as oil remains buoyant, but the Try underperforming as an importer.

In commodities, WTI and Brent futures hold onto modest gains amid the fallout from the OPEC+ meeting – which saw an extension of 9.6mln BPD cuts (barring Mexico’s 100k BPD) by an extra month to the end of July as anticipated. Focus meanwhile has now turned to compliance and how the heads of the group plan to enforce full/over-compliance – namely among the known laggards Iraq and Nigeria – who reaffirmed commitment to the pact over the weekend. On that front, Iraq has already hinted at possible problems regarding making up for its shortfall. In terms of over-compliance, Gulf OPEC producers (Saudi, UAE, Kuwait) are not planning to continue with their voluntary deeper oil cut of 1.18mln BPD beyond June, according to sources. Eyes will now be on the June 18th JMMC meeting where the committee will review secondary source data alongside current market fundamentals before proposing policy recommendations. Note: sources last week said that OPEC+ is to move cautiously to rebalance the market amid easing lockdowns, while possible Shale resumptions could also weigh on eastern producers’ minds. Thereafter, Saudi Aramco also released its July Official Selling Prices (OSPs) which showed steep increases for all crude grades to all regions. Furthermore, Libya’s El Sharara oilfield (300k BPD) has restarted output at 30k BPD and is expected to reach capacity within 90 days after 142 days of inactivity. Reports also note that the El Feel field (70k bpd) has restarted operations. Meanwhile, Cristobel made landfall over the weekend but has since weakened to a Tropical Storm as it moves further inland. Heavy Rainfall and storm surges continue along the gulf coast from Southeastern Louisiana eastward to the Florida Panhandle. It was reported that energy firms evacuated 195 Gulf of Mexico production platforms and 3 rigs ahead of Storm Cristobal on Sunday and that producers had cut 34% of offshore oil and 32% of nat gas output as of mid-Sunday. WTI July trades on either side of USD 40/bbl (vs high. 40.44/bbl) and Brent August dipped back below USD 43/bbl (vs. high 43.41/bbl). Spot gold trades on the firmer side of a USD 1678-97/oz range with little specific for the metal, whilst copper prices extend gains above USD 2.50/lb amid falls in stocks at exchange warehouses – falling to 139k tons which is the lowest since Jan 17th. Meanwhile, around 90% of the large Peruvian mines have received the green light at resuming operations following a pandemic-related disruption. Libya’s El Sharara oilfield (300k bpd) has restarted output and is expected to reach capacity within 90 days. Reports also note that the El Feel field (70k bpd) has restarted operations.

US Event Calendar

Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

As far as I can see the two most ruinous financial decisions you can make are either to short US equities or buy an old house. Fortunately I’ve never done the former but I’ve done the latter twice over the last decade and would have been better off setting aside a big pile of cash and burning it. A year after finishing renovations on our dream home the latest saga arrived at 2:30am on Saturday night when I get a poke in the ribs from my wife. “Wake up. Wake up! Something terrible has happened downstairs and we need to go and investigate”. I take this pretty badly having woken out of a deep sleep and dismiss her claims that there was a very loud bang as nothing more than her having a bad dream. I begrudgingly get my dressing gown on and trudge downstairs. Half way down the stairs, dust starts rising everywhere and as the fog got more intense we reached the downstairs hallway to find rubble and debris everywhere and half our ceiling collapsed onto the floor. My wife and I were both in shock, especially once we realised how heavy the fallen plaster was and how dangerous it could have been. When we renovated we had to unwillingly replace virtually all of the ceilings as they progressively fell down during the heavy works but not this one. I’ll find out early this week what this latest problem is going to cost us!!! However at least no one got hurt.

The week after payrolls is normally light on activity and to be honest it might take me a week to get over the shock of a collapsed ceiling and a week for all economists to work out how the data missed their payrolls forecasts on Friday by probably the biggest amount ever for an economic data release (more later). Having said that it’s likely to be quiet the market highlight is undoubtedly the Federal Reserve’s monetary policy decision on Wednesday. Elsewhere ECB President Lagarde appears today at a European Parliament Committee but don’t expect too much given the close timing to the ECB meeting last week. We also have another Eurogroup meeting on Thursday where the recovery fund will be the main interest, as well as the release of US CPI data for May on Wednesday.

For the Fed on Wednesday, our economists expect the meeting to mark a first step away from a complete focus on crisis prevention towards more traditional goals of providing accommodation to support the recovery. In particular, they expect the Fed to announce an open-ended QE program consistent with monthly Treasury purchases of between $65bn and $85bn. In addition, the meeting statement should slightly enhance the commitment to keep rates lower for longer. An updated SEP should reflect a cautious outlook where elevated unemployment and below-target inflation should result in the median dots signalling that officials expect to keep rates unchanged at least through end-2022. See here for their preview.

The meeting comes after a remarkable payrolls report on Friday. To recap, headline nonfarm payrolls rose by 2.509 million with private payrolls increasing by 3.094 million versus consensus of -7.5m and -6.75m respectively. In addition, the main U-3 unemployment rate fell by 1.4ppts to 13.3% versus 19% expected. While the BLS noted that the U-3 rate was likely boosted by ongoing classification issues, and should likely have been three percentage points higher, the U-6 unemployment rate also fell to 21.2%, down 1.6% from its April all-time high. Just as three sectors of the labour market (food service & accommodation, health care & social assistance and retail) accounted for 55% of the February to April decline in private payrolls, the same sectors comprised 64% of the May gain, recovering between 15.5% and 17.5% of their declines over the previous two months. Hiring though was broad-based, with the payroll diffusion index surging to 64.0%, its highest since December 2018 (64.9%). In our economists view, the unexpected bounce in employment may reflect rehiring ahead of planned re-openings within states that was not quite captured in the initial jobless claims data. In short, the May payroll figure was what they would have expected for June. Overall there’s little doubt that this was a very positive print but it will take time to work out whether this was more of a bringing forward of re-hirings or something more structural.

As we’ll see in the weekly recap at the end, the payrolls report helped drive another bumper day in equities (S&P +2.62%). Looking deeper at US equities, DB’s Binky Chadha, in a report late on Friday, suggested positioning is still as low as the 8th percentile for the US helped in part by new retail money coming into the market. He also argues that there is a cash mountain in money markets after $1.2 trillion went in since March with almost none moving out so far. This now amounts to $5 trillion (25% of GDP) and is still at financial crisis highs and any re-allocation away should be beneficial across risk assets. However positioning in the mega cap growth stocks (MCGs) we discussed at length last week now look stretched so there is still room for a catch-up for the rest where positioning is very light. See Binky’s full report here.

On a similar vein Craig in my team has looked more at the bifurcation in US HY credit. If we look at a bucket of what we perceive to be the most defensive BB sectors, making up 28% of the BB and single-B market (ex-financials), this group now has a cash price higher than what it was pre-covid. Spreads have also repriced to the point where they rank in the 61st percentile (100% equals tightest). The other segment of the market is simply the rest of the BB and single-B market. This bucket has a current cash price which is 5pts lower than it was pre-covid. The repricing in spreads is also less significant, with spreads now ranking in the 20th percentile. However, like the equity market, these less favoured names have started to ‘catch up’ to the BB defensive bucket in recent days. As investors continue to search for dislocations, assuming this move towards less favoured sectors continues, opportunities within this segment of the market are likely to be far greater. See Craig’s note here for more on this.

In terms of weekend news OPEC+ agreed to a one-month extension in its recent output cuts and suggested a stricter compliance approach to those who breech this. Oil is up around +1% so far this morning after six weeks of gains and another good week last week as we’ll see in the weekly recap below. Elsewhere, China’s trade surplus came in at record $62.9bn (vs. $41.4bn expected and $45.3bn in April) in May with exports sliding to -3.3% yoy in USD terms (vs. -6.5% yoy expected and +3.5% yoy last month) while imports tumbled to -16.7% yoy (vs. -7.9% yoy expected and -14.2% in April).

Nevertheless, markets in Asia have kicked off the week on the front foot with the Nikkei (+1.23%), Hang Seng (+0.17%), Shanghai Comp (+0.28%) and Kospi (+0.16%) all up. Futures on the S&P 500 are also up +0.24% as we type. Overnight, Japan’s final Q1 GDP came in at -0.6% qoq (vs. -0.5% qoq expected).

Looking back to last week now. Global equities continued to rally to new post-shutdown highs as economic data improved throughout the week, accentuated by the US payroll data on Friday, and further promised stimulus in Europe. Equities that lagged the most throughout the pandemic, such as retailers, cruises and airlines were some of the best performers on the week with hopes for a faster than expected economic recovery taking hold. The S&P 500 rose +4.91%, with the largest one-day gain coming on Friday after the jobs report (+2.62%). The index is now +42.75% off the March lows and is down just -5.68% from all-time highs and ‘only’ -1.14% YTD. Equity markets both in the US and Europe continued to see a rotation into value-oriented stocks with US banks up +17.11% (+4.86% Friday) on the week, while European Banks rose +20.18% (+7.55% Friday). The tech-focused NASDAQ underperformed the S&P for a second week in a row, up “just” +3.42% (+2.06% Friday). However, the index has outperformed throughout the crisis and on Friday closed just -0.03% below February’s all-time high having briefly traded above it in the session.

European equities rallied even further on the week as the ECB announced an increase to the size of their PEPP by a further €600bn, the German government agreed additional fiscal stimulus, and virus case counts remained contained even as economies are slowly reopened. The Stoxx 600 rallied +7.12% (+2.48% Friday) over the five days with the core continental ones up around +9-11% on the week. Asian indices rose alongside their European and American counterparts. The Nikkei was up +4.51% over the week (+0.74% Friday) while the CSI 300 was up +3.47% (+0.48% Friday), and the Kospi rose +7.50% (+1.43% Friday).

Oil rallied further on the week as demand expectations rose with economic data improving. Prices were also helped by hopes that OPEC+ would extend production cuts as has been confirmed over the weekend. WTI futures rose +11.44% (+5.72% Friday) to $39.55/barrel and Brent crude rose +19.73% on the week (+5.78% Friday) to over $40/barrel for the first time since the first week of March.

Credit spreads on both sides of the Atlantic tightened on the week with risk sentiment continuing to drastically improve. European HY cash spreads were -83bps tighter on the week (-30bps Friday), while European IG spreads tightened -35bps (-13bps Friday). US HY cash spreads were -121bps tighter (-33bps Friday), while IG tightened -25bps on the week (-10bps Friday).

Peripheral debt tightened as well, with Spanish 10yr yields -17.5bps tighter to German bunds over the 5 days, while Italian BTPs were -23.5bps tighter, Greek 10yr yields tightened -33.8bps, and Portuguese bonds tightened -13.6bps. With risk assets rallying, core sovereign bonds sold off as US 10yr Treasury yields rose +24.3bps (+7.2bps Friday) to finish at 0.895%, while 10yr Bund yields rose +17.0bps over the course of the week (+4.3bps Friday) to -0.28%.

Also on Friday, the EU’s chief Brexit negotiator, Michel Barnier, said that “the truth is that there was no substantial progress” following the latest round of talks with the UK on their future relationship after Brexit. He also said that a full legal text would need to be ready by the end of October given the time needed for ratification. Nevertheless, the pound strengthened further against other major currencies, reaching its highest level against the US dollar in nearly three months (+0.56% Friday and +2.63% on the week).

via ZeroHedge News https://ift.tt/2XJQaY0 Tyler Durden

Seattle Motorist Shoots Protester, Police Violate ‘Tear Gas Ban’ During Another Night Of “Peaceful” Demonstrations Tyler Durden

Mon, 06/08/2020 – 07:25

The media has taken great pains to protect the legitimacy of the protest movement by pushing the narrative that demonstrations were ‘largely peaceful’ even as protesters in the US defaced the Lincoln Memorial, and attacked a children’s hospital, among other transgressions. On Sunday evening, the Minneapolis City Council sided with the radical left by voting in a veto-proof to dismantle the city’s police department and replace it with a “holistic” public-safety department.

As NYPD officers in some parts of NYC smoked cigars and enjoyed ice cream while taking pictures with some marchers and motorists in a gesture of “deescalation”, an armed driver in Seattle barreled into a crowd of protesters, shooting one person who reportedly tried to stop him, before surrendering to police.

At least, that was the description of the incident provided by the media: Video shows the motorist driving into a “barricade” in the middle of the street, then whipping out his gun after a protester reached his hand inside the man’s vehicle. The shooter is in custody, and the protester who was shot is in stable condition.

A man drove through 11th and hit a barricade. He exited his car and flashed a gun. The police say they have the man in custody and have the gun. They asked for anybody who is hurt to come to the barricade. A man was on the ground on 11th and Pine. He’s up now. pic.twitter.com/47eZZOvG59

Sunday marked the 10th consecutive day of protests in the city. After “banning” the use of teargas on Friday, Seattle police used gas, smokebombs and flash-bang grenades to bring the crowd of protesters under control early Monday morning.

Overwhelmed by this footage right now. @SeattlePD@MayorJenny y’all are a disgrace. So much for that tear gas ban, huh? Imagine what this city could look like if you spent all that $$$ giving people homes & healthcare instead of brutalizing your own people. @cmkshama@JayInsleehttps://t.co/5Kc89LksM9

Over in the UK, one of the dozens of countries that saw “solidarity” protests spring up over the weekend, statues of Winston Churchill and Edward Colston (a philanthropist who earned most of his money in the slave trade) were defaced or destroyed. When a group of British conservatives showed up to protect a Churchill statue along one of the march’s routes, Metropolitan Police asked them to move.

Some guys have turned up to protect the Winston Churchill statue themselves – as the #BlackLivesMattter crowd pass Parliament Square and head up to Downing Street again @LBCpic.twitter.com/L5u5OLmtJ3

— Rachael Venables (@rachaelvenables) June 7, 2020

Looking ahead, there are two important events on the calendar: Mourners will be able to view George Floyd’s casket Monday in Houston, a city widely identified as Floyd’s “hometown”. It’s the final stop in a series of memorials in Floyd’s honor.The six-hour viewing will be held Monday at The Fountain of Praise church in southwest Houston. The viewing is open to the public, though visitors will be required to wear a mask and gloves.

The funeral is set for Tuesday in Houston. Floyd will be buried at the Houston Memorial Gardens cemetery in suburban Pearland, where he will be laid to rest next to his mother, Larcenia Floyd.

Democratic contender Joe Biden plans to travel to Houston to meet with Floyd’s family and will provide a video message for Floyd’s funeral service, the AP reports. Though Biden won’t be attending the service.

Monday also marks the first court appearance of Derek Chauvin, the Minneapolis Police Officer charged with 2nd degree murder in Floyd’s killing.