Roaring Twenties: What To Expect From Today’s 20Y Auction Tyler Durden

Wed, 05/20/2020 – 09:40

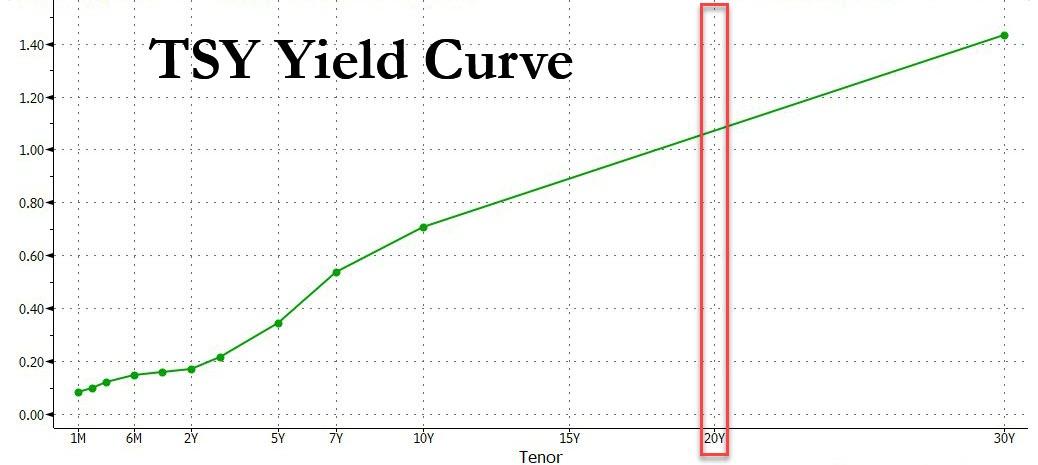

Today, May the 20th, marks the first auction of 20-Year Treasury bonds since 1986 with an inaugural auction size of $20 billion, and with the When Issued trading at 1.23%, there is a non-trivial chance the auction will price at 1.20%!

The auction will be closely followed with investors (and the Treasury Department) attempting to judge the degree of demand for duration in the sector. It will also be closely watched by the Fed, because as Bloomberg points out, the central bank already owns more than 70% of the two CUSIPs closest in maturity to the new 20-year.

“The Fed can purchase up to 70% of the outstanding amount of an issue, and has done so with all but two of the bonds closest in maturity to the new 20-year”

As BMO rates strategists Ian Lyngen and Jon Hill write, it’s likely to provide CTDs for the classic bond contract, therefore the perception is there will be a base of natural buyers. One might assume this factored into the initial size of $20 bn – above the estimates of many. An auction concession of some sort is warranted; although BMO anticipates the new issue will be well absorbed even if it comes at a modest discount. After all, there is no such thing as a bad bond; just a bad price. As such “aside from the reestablishment of a benchmark on the yield curve, today’s session offers very little to trigger a collective rethink of investors’ current interpretation of the macro landscape.”

The main event of the session and arguably week will be the first 20-year Treasury auction since 1986. There is ample reason to expect the inaugural offering will be met by a solid primary market bid. If the sponsorship to last week’s 10- and 30-years were any indication, despite the record large auction sizes and yields within striking distance of all-time lows there is still strong demand for dollar duration. Indeed, the largest stop through at a 10-year auction since March 2017 and a modest tail despite coming at the yield lows of the day for 30s hints of a long-end investor base that is eager to take advantage of the liquidity point supply provides. Especially as the 20-year sector of the curve becomes more established, it is not unreasonable to anticipate an incremental yield pick up in the early days of the new bond as a concession for what will initially be a comparably thinner volume profile.

In terms of valuation, the fact that we have seen 20s cheapen significantly on an interpolated 10s/20s/30s butterfly also bodes well for the takedown. To say nothing of the concession over the past several sessions as 10- and 30-year yields drift toward the top of their respective ranges while the curve steepens. Additionally encouraging is the return of favorable currency-hedged Treasury yields for Japanese investors, which should entice buying interest from an investor base who historically has been active in the long-end of the curve. While month-end is approaching, the fact that 20s will not settle until the calendar flips removes any rebalancing bid that will benefit the new bond at future auctions. All in all, we will look for a solid initial auction and expect a stop near 1pm WI levels.

And some more observations from the BMO rates strategists:

While equity futures suggest stocks are poised to open back near the post-crash highs, the initial euphoria surrounding a Covid-19 vaccine has quickly faded. Progress toward the slow and steady reopening of the global economy continues and results in Europe are encouraging; even if the lack of a resurgence thus far doesn’t imply the pandemic is behind us. In fact, given that the US has been lagging the Continent there is little doubt the coronavirus will remain top of mind for the balance of 2020. This backdrop leaves our range-trading thesis solidly intact as the lower and upper-bounds in 10-year yields that have been in place since late-March continue to hold.

In fact, the more habituated investors become to having 10s in the 54 bp to 78 bp zone, the greater the difficulty in anticipating a breakout. Sure, eventually the extremes will be challenged; rates will go up and rates will go down, just not necessarily in that order. Nonetheless, it will take a paradigm shift in the economic outlook to inspire a truly sustainable repricing. In part, this has driven our interest in determining exactly what the ‘consensus’ for the timing and pace of the recovery is at the moment. Setting aside the V, W, L, U, Swoosh name-calling, investors are resigned to a very deep recession which is followed by a difficult road to recovery. This isn’t new information per se, but as the market discourse on the timing of the rebound has slowly transitioned from months, to quarters and eventually settled on years – we’ll admit some surprise that neither the range in US rates has broken nor has the bullish trend in equities faltered.

The rise of zombie companies in the wake of the lockdowns represents another concern as the post-pandemic reality slowly takes shape. Firms which remain in existence, but only a shell of their pre-crisis business model intuitively need fewer employees and while government assistance has attempted to provide a bridge to make it through the lockdown, the risk has quickly become what companies will find on the other side. The secondary fallout for the labor market remains to be seen, even if expectations are for an elevated unemployment rate as the nation gets back to work. This will continue to edge wages lower and risks a durable period of disinflationary pressures. The Fed has taken dramatic steps to offset the acute downsides from the pandemic, though the longer the shutdowns linger, the more permanent much of the economic damage becomes.

Given all of the above is fairly consensus, anything which materially challenges this base case scenario will lead to an attempt at a repricing. Yesterday’s vaccine-inspired equity rally offers a prime example as such a decisive tool in combating Covid-19 would meaningfully shorten the path to recovery. Beyond greater success in slowing the progression of the coronavirus or limiting its impact, the incremental stimulus efforts on the part of the government and central banks will only serve to reinforce the lengthening timeline before the economy settles into a durable new normal. For the time being, the session ahead offers little to inspire revising investors’ core assumptions and as a result, the trading range is safe for the foreseeable future.

via ZeroHedge News https://ift.tt/2TmlmdB Tyler Durden

Ben Kenobi: How long before you make the jump to lightspeed?

Han Solo: It’ll take a few moments to get the coordinates from the navicomputer.

Luke Skywalker: Are you kidding??! At the rate they’re gaining…

Han Solo: Traveling through hyperspace ain’t like dusting crops, boy! – Star Wars, Episode IV

Light Speed

In the early Star Wars movies, Han Solo was the captain of the rusting Millennium Falcon spaceship. When making a daring escape, Solo would command the ship to jump to light speed. The surrounding stars would blur in streaks as they left their pursuers in stardust and suddenly ended up somewhere across the galaxy far, far away.

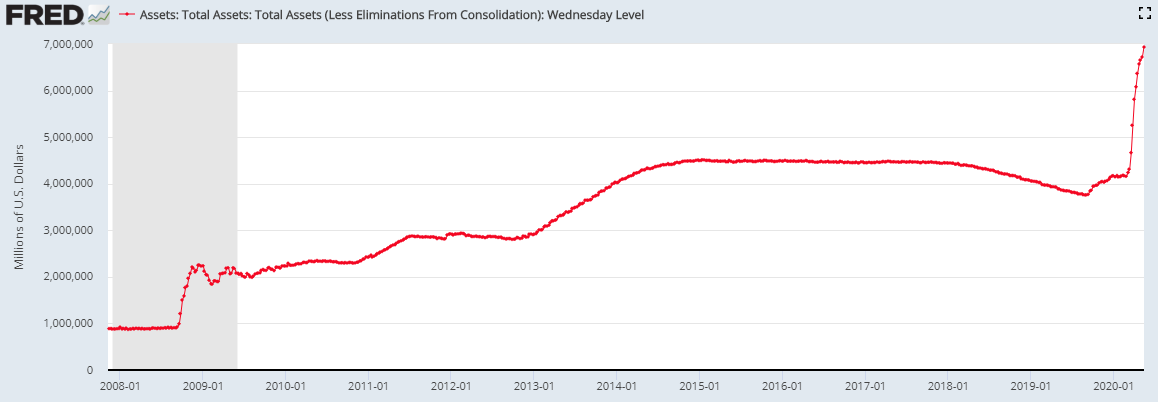

On April 9, 2020, the Fed made the jump to light speed with their announcements of even more remarkable stimulus packages. The new operations were in addition to the myriad of operations in March and prior months.

To define monetary light speed, the Fed’s balance sheet rose from $3.76 trillion at the end of August 2019 to $4.16 trillion at the end of February 2020 – a change of $400 billion. As of May 13, 2020 it was at $6.93 trillion. A shocking increase of $2.77 trillion in ten weeks, dwarfing anything seen during the financial crisis.

Having promised to purchase Treasuries, mortgages, and municipal bonds, in whatever amount necessary, they set off on a new path. Now they can buy investment grade corporate securities, high yield bonds (junk), and even certain Collateralized Loan Obligations (CLOs – the securitized form of high-risk leveraged loans). These operations will take place through the newly formed Secondary Market Corporate Credit Facility (SMCCF).

Per the Federal Reserve Act, the Fed can only purchase or lend against securities that have a government guarantee. So how can they purchase non-government guaranteed securities?

SPV Back Door

The simple answer is the Treasury is enabling the Fed to side-step the law, or to be more accurate, break the law.

As the Fed’s accomplice, the Treasury Department provides $75 billion of initial funding from the Exchange Stabilization Fund. The funds are deposited into a special purpose vehicle (SPV), and specifically aimed to purchase secondary market corporate bonds. Technically, the Treasury, not the Fed, is buying those securities on behalf of taxpayers.

Enter the co-conspirator. The Fed, acting as an intermediary and employing asset manager BlackRock, intends to leverage that amount ten times. This allows the Fed to buy an additional $675 billion in securities and select Exchange Traded Funds (ETFs).

Calling Out the Fed

As John Hussman described on April 20, 2020, Congress never granted that authority (the leverage) to the Fed, making such a maneuver illegal.

“… additional purchases to “leverage” that funding are neither secured by non-financial collateral, nor have security sufficient to protect taxpayers from losses. They are illegal, both under Section 13(3) of the Federal Reserve Act, and under Section 4003(c)(3)(B) of the CARES act, which “for the avoidance of doubt” specifically invokes 13(3) “requirements relating to loan collateralization, taxpayer protection, and borrower solvency.”

Given the leverage and speculative nature of the securities the Fed is acquiring in the SMCCF (SPV) scheme, a 10% drop or more in the value of the SPV assets would result in immediate insolvency and losses to taxpayers.

In simple terms:

The Treasury Department funds the SMCCF SPV with $75 billion (a legal action)

The Fed acting as the intermediary of the SPV, stated they may leverage those funds 10 times (an illegal action)

If at any point up to the $750 billion of investments made through the SPV, the value of held assets drops by more than the initial $75 billion funded by the Treasury, the loss is in breach of what Congress authorized.

The assets the Fed will buy do not meet the stated requirement of sufficient security intended “for the avoidance of doubt” about the potential for loss (to the taxpayer). It is an illegal structure.

If the economy and markets regroup, borrowing and consumption patterns return to pre-virus outbreak levels, and investors shed all fears of another leg down in markets, then maybe we can sound the all-clear.

Economic Reality

However, even Pollyanna would not subscribe to such an optimistic path. Unemployment in April was 14.8%, consumer spending, industrial production, and confidence are plummeting. Every industry and many individuals have their hands out for taxpayer-sponsored relief (bailout).

GDP is expected to drop by 12-15% in the second quarter and that may be optimistic. In a May 17th 60 Minutes interview, Fed Chairman Jerome Powell said it could be down as much as 30%.

Making matters worse, the economic carnage affects all industries and is global in nature. As if depression-like economic data were not enough, there is not yet a therapy or vaccine for the Coronavirus. Although there is little doubt one will be forthcoming, the timing is uncertain and appears to be, at best, months out in the future.

The probability of corporate losses on the Treasury’s balance sheet amounting to over $75 billion is not at all unrealistic. Plus, there is the continuing uncertainty in the economic outlook despite hopes for the economy to reopen gradually. Current valuations of the bonds in the Fed’s SPV do not adjust for the risk of a global economic outlook that is more constrained and restricted than at any time since the great depression.

Again, from John Hussman:

“As a result, the newly created SMCCF is either a Ponzi scheme at public expense (if the Fed plans to allow portfolio losses to exceed 10%) or a 1987-style portfolio insurance scheme (if the Fed plans to liquidate securities into a falling market in order to cap its losses at 10%).”

Pick your poison.

Fed Independence

The SPV scheme applies to several non-traditional lending facilities also used in the 2008 financial crisis and many new facilities. The collaboration merges the Fed and the Treasury into one organization. This plan follows a recommended script published as an Op-Ed by former Fed Governor Kevin Warsh in the Wall Street Journal on March 15, 2020.

Winners and Losers

The SPV scheme was used on a limited basis with much higher quality assets during the financial crisis but was quickly unwound as the economy recovered. Given the expansion of powers this time, we should assume these actions could reduce Jay Powell’s authority over monetary policy. Essentially he is indirectly ceding control of our “independent” central bank to the Treasury Department. The risk is that the executive branch may end up with dominant influence over certain important operations at the Fed. What this means is that the line between monetary and fiscal policy is even further blurred given the exposure taxpayers unknowingly assume for losses on risky SPV holdings.

Corporate executives reaped unwarranted multi-million-dollar rewards for short-term-oriented, profit-maximizing behavior over the past ten years. However, once again, the taxpayers, most of whom did not benefit from irresponsible corporate and fiscal actions are on the hook.

The SPV structure allows the Fed and Treasury to nationalize major segments of the financial markets. With that, the credibility of pricing signals is lost. The capital markets are not only crucial for raising capital but equally important in the way they offer traffic signals to businesses and individuals concerning true economic conditions. Without these signals, capital allocation becomes distorted, and productivity growth flounders. Based on observations over the past ten years, it is safe to say we are well past that point.

If Jay Powell and Steve Mnuchin were legislated to assume personal risk in their scheme, would they be willing to accept it?

No. Certainly, they would not accept it.

Summary

It is shameful to watch the blatant abuse of power where Constitutional order requires the Fed and other government officials to abide by proper laws intended to restrict such behavior.

As recently as January’s impeachment hearings, both sides of Congress were well-versed in quoting from the Constitution. Today, however, the laws of those guiding documents are largely ignored.

By most accounts, it seems very likely that the Fed will, sooner or later, buy equities in the ultimate act of expediency. Buying high yield bonds is but one very short step away from the next level down in the risk continuum – stocks.

With the Fed now engaged in light speed monetary policies, our future is likely to include:

Zero bound and potentially negative interest rates

A lower natural economic growth rate

An even larger wealth inequality gap

Loss of Fed independence from the Executive branch of government

Price instability (deflation then inflation)

Significant and damaging volatility

Nationalized financial markets

Irrelevant market signals

The Fed does not have the benefit of Star Wars technology or Hollywood special effects to avoid fostering ever new mutant forms of moral hazard. Quite the opposite, in fact. Their monetary “navicomputer” does not protect against the economic equivalent of slamming into a stray asteroid or planet.

Indeed, it seems more likely to steer the country into such a disaster.

Every crisis provides the latitude for an ever-greater power grab without regard for constitutional authority. The virus is inconvenient, but the policy actions taken with no regard of forethought are quite another matter.

No, the Fed is not “dusting crops” at this stage.

via ZeroHedge News https://ift.tt/2LIlFLg Tyler Durden

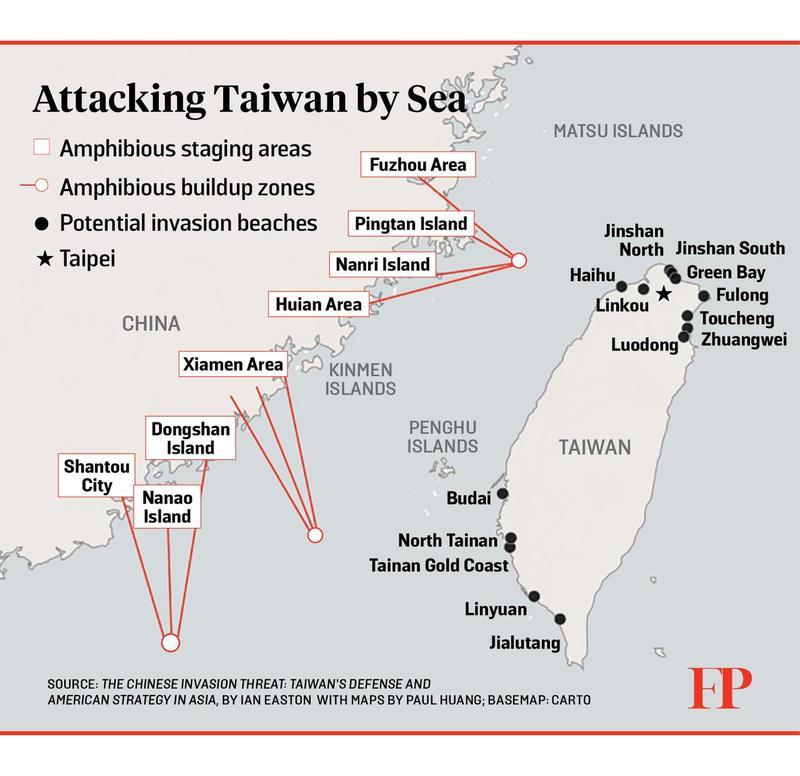

Pompeo’s Congratulations Tweet To Taiwan President Sparks Outrage With China Tyler Durden

Wed, 05/20/2020 – 09:11

Taiwan’s President Tsai Ing-wen was sworn in on Wednesday for a second presidential term amid worsening ties with China. US Secretary of State Michael Pompeo tweeted congratulations on Tuesday ahead of the ceremony, which led China to denounce Pompeo’s message as “wrong and very dangerous,” reported Bloomberg.

Taiwan cannot accept becoming part of China under its ‘one country, two systems’ offer of autonomy, President Tsai Ing-wen said as she was sworn in for her second and final term https://t.co/UqsIjltDpqpic.twitter.com/uAj1viKOxe

The Ministry of National Defense released a statement Wednesday that said the People’s Liberation Army (PLA) would “take all necessary measures to firmly safeguard” China’s sovereignty, while the Chinese Ministry of Foreign Affairs said Pompeo’s comments “seriously violated” the one-China principle.

“China urges the US side to immediately correct its mistakes,” the Ministry of Foreign Affairs said in a statement. “The Chinese side will take necessary countermeasures to respond to the above-mentioned erroneous actions by the US side. And the US side should bear the consequences arising therefrom.”

Washington has carefully refrained from recognizing Taipei’s government in the past. What triggered China into a fit of rage this week is Pompeo’s tweet that recognized Tsai as president and called Taiwan a “force for good in the world and a reliable partner.”

Congratulations to Dr. Tsai Ing-wen on the commencement of your second-term as Taiwan’s President. Taiwan’s vibrant democracy is an inspiration to the region and the world. With President Tsai at the helm, our partnership with Taiwan will continue to flourish.

Tsai told China to “find a way to co-exist” with Taiwan’s democratic government as her second term in Taipei will start on Wednesday. Tsai’s Democratic Progressive Party supports Taiwan’s independence from China and seeks additional measures to reduce reliance on China while increasing relations with the US.

With cross-strait relations and Sino-US diplomatic relations plunging to the lowest levels in quite some time, we recently noted how China’s “military leaders are pushing for a substantial increase in their budget to be announced at the National People’s Congress that starts on Friday, arguing that the world’s largest standing army needs more resources to cope with volatile challenges at home and overseas. And at the top of the list, according to the South China Morning Post, is the growing confrontation with the US.”

“With China-US relations sinking amid a trade war, spats over civil liberties and Taiwan, and conflicts over Beijing’s territorial claims in the South China Sea, recent months have added accusations between Washington and Beijing about the origins of the Covid-19 pandemic. From Beijing’s viewpoint, the military threats are surfacing on its doorstep with US bombers running about 40 flights over contested areas of the South China and East China seas so far this year, or more than three times the number in the same period of 2019. US Navy warships have sailed four “freedom of navigation operations” in the area in the same period, compared with eight in all of last year.”

To make matters worse, the Communist Party’s Global Times not only denounced Pompeo’s tweet but warned that PLA has the capability to “overwhelm the Taiwan military and deter the US military.”

“China is becoming more powerful, and our ability to claim sovereignty over Taiwan is certainly growing,” the Global Times said. “At this time, the US and Taiwan want to play petty tricks at a low cost, which is too naive. We will make them feel pain in some places that they can’t think of.”

“If the internal stability is a very serious issue, or economic slowdown has become a very serious issue for the top leaders to deal with, that is the occasion that we need to be very careful,” Taiwan’s Foreign Minister Joseph Wu said late last year.

“We need to prepare ourselves for the worst situation to come…military conflict,” Wu warned.

Because of a virus pandemic and crashed economies across the world, cross-Strait relations and increasing tensions in the South China Sea are likely to be seen in 2H20.

via ZeroHedge News https://ift.tt/36hZQMf Tyler Durden

So House Speaker Nancy Pelosi continues to prove the observation as true that the “Left Can’t Meme” by going on TV to decry President Trump prophylactic use of hydroxychloroquine and zinc to fend off COVID-19 by calling him “morbidly obese.”

What’s so sad about this exchange isn’t the obviously awkward set up by Anderson Cooper, the unctuous virtue signaling by Pelosi or the pathetic pandering to her base it is that Pelosi gets everything exactly wrong.

If Trump is morbidly obese, which would be a co-factor in falling to COVID-19, wouldn’t it make sense then for him TO be taking whatever precautions he and his doctors deemed helpful?

I guess Nancy would know all about morbid obesity because that’s the only kind of legislation she’s capable of sponsoring.

Her latest legislative fiasco was a new $3 trillion stimulus bill with precious little ‘stimulus’ in it whic was rejected by members of her own caucus (because truly who at this point could be stimulated to anything other than nausea by Pelosi).

Since the outset of the Coronapocalypse, I’ve been arguing that everything done to date has been the wrong approach. We should have been deregulating, allowing deflation to force debtors and debt-holders to figure things out themselves and put governments themselves on a massive diet.

My last article addressed this very issue.

The one single thing that would be of the most use to what’s left of the middle class, lowering payroll taxes, is the one thing they will not countenance.

Payroll taxes lowered, corporate taxes lowered, useless regulations cut, these are all good starts. But the real problem is the multi-trillion dollar elephant in the room, the cost of all levels of government that are a net drain on the real economy.

But all we have seen to this point is pointless theater from the pols in D.C. who still think the rules haven’t changed and anyone gives a rat’s ass about their schtick.

Treasury Secretary Steve Mnuchin and FOMC Chair Jerome Powell had to sit through grandstanding by Elizabeth Warren this morning to defend their actions during the worst of the crisis.

And that’s fine for what it is; blatant positioning by people who need a political win. Having Warren go after someone as odious as Mnuchin is like watching two rival teams you hate playing.

The best you can hope for is a tie and lots of injuries.

But what’s really surprising here is that Trump is stepping up the pace against his tormentors. He’s begun the attacks on Obama and his holdovers in the Justice Department through his acting Director of the ODNI, Richard Grenell.

BREAKING: New DNI instruction removes FBI from cordeword SIGINT briefings and products that contain sources/methods. They have been ordered to return to core LE/CT work

The orders have already gone out to the relevant IC commands, including INSCOM. Now FBI’s access will only be granted on a per-incident basis if matter is not directly related to terrorism or a criminal activity under active investigation

If Posobiec is correct about this and not over-stating the change, this is the biggest move to drain the swamp in decades. It makes it perfectly clear that Trump no longer trusts the FBI and that it is an agency that has far exceeded its mandate.

That it took them working overtime for years to bring down a sitting president and failing should be a huge wake up call to Americans of all political stripes.

The president said to his Cabinet members as he signed the order, “I want you to go to town and do it right. It gives you tremendous power to cut regulation.”

We don’t know the extent this will occur and what Trump’s really thinking at this point, but anything in this direction is welcome.

What’s important is that this kind of response never happens in D.C. but is exactly what the pols there are deathly afraid of. Because what happens when people get used to NOT having to comply with moronic rules.

The bureaucracy will find out that they aren’t needed. And that’s a real threat to them.

Removing bottlenecks even by temporarily not enforcing ridiculous mandates that are nothing more than barriers to commerce is enough to change the dynamic.

It is going to get harder and harder to justify big, bloated bureaucracies that just shuffle money around and waste people’s time. And Trump knows how to do this. This is a skill right in his wheelhouse as this is the greatest skill one has to have to get buildings built in the epicenter of corruption, New York City.

He knows that nothing will undercut the permanent bureaucracy more thoroughly then removing the rules which create the local fiefdoms that empower the petty and politically motivated in every city in the U.S.

And he also knows this is where the entrance into the hearts of those precious swing voters lies. I told you Trump would target the Tax Producers while Pelosi was still protecting the Tax Consumers.

He just doubled down on that and she has no answer but to call him fat.

Early in his response to COVID-19 Trump quietly got rid of barriers for doctors to practice across state lines and suspended prosecuting doctors for HIPAA violations that were not a result of gross negligence. He freed doctors up to mobilize them to lend expertise when and where it was needed.

Now he wants to do that for the entire economy by getting government out of the way of people trying to rebuild a society flattened by a draconian lock down which worsened an already terrible financial crisis.

I’m not surprised by this move at all. Trump understands what he’s up against this fall. Obama has entered the 2020 election in a way no former President ever has.

For the U.S. Deep State and the chattering class in D.C. the real existential crisis is the realization that a second Trump term means we figure out just how unnecessary they are.

We’re beginning to flex our muscles at the local level, disobeying brutal orders from Governors and local petty tyrants but it’s not enough. The swift moves to implement contact tracing via outsourcing to restaurants and business owners is a prelude of what comes next in the land of the not free, controlled by Karens.

Unpersoning those not willing to submit to will be in full flower by the end of the year if not sooner. And the quicker Trump moves to disempower the administrative state the better.

Because what truly needs to go on a diet is government. And those that need to be starved out are those that think that we work for them.

* * *

Join my Patreon if you want to join folks dedicated to starving the state. Install the Brave Browser if you want to be like Joe Rogan and starve the Google beast.

via ZeroHedge News https://ift.tt/2LGJa7J Tyler Durden

In Latest Escalation, President Trump Blames China For “Mass Worldwide Killing” Tyler Durden

Wed, 05/20/2020 – 08:42

A day after the WHA approved a resolution authorizing a WHO-led investigation to the origins of the coronavirus in China, President Trump just lashed out at China’s state-approved conspiracy-peddlers who are desperately trying to convince the Chinese people that the virus didn’t come from China – but actually originated in the US.

Some wacko in China just released a statement blaming everybody other than China for the Virus which has now killed hundreds of thousands of people. Please explain to this dope that it was the “incompetence of China”, and nothing else, that did this mass Worldwide killing!

The rhetorical tit-for-tat between the US and China has intensified in recent days, as the White House lambasted President Xi’s promise to share a vaccine “with the world” and pump $2 billion into the WHO’s effort to help the poorest countries as a “token” gesture to try and obviate China’s obvious culpability.

Trump and many members of his administration have bashed the WHO for uncritically accepting information provided by the CCP – despite having an office on the ground in Beijing – and writing glowing reports praising China’s early response while the government knowingly withheld information that could have inspired a more stringent response.

Instead, the organization hemmed and hawed, playing down the virus’s destructive potential, and celebrating China’s response as “a model” for other developing nations.

Twitter blue checks immediately pounced on the comment, reminding the world of the Trump Administration’s “failings”.

Some wacko in the White House is blaming everyone but himself for the disastrous spread of the COVID-19 coronavirus in America.

The original sin is China’s but the Trump administration had plenty of time to deal with the gathering storm. It’s not like it arrived unannounced. https://t.co/ZMltpmHhcB

Though the administration probably wishes it rolled out testing more quickly, most new information – including diagnoses of possible COVID-19 deaths and cases weeks or months earlier than previously believed – suggests that the reluctance of officials in Beijing and Wuhan to pounce on the virus was the initial “pandora’s box” moment, and that the virus was likely already spreading in the US in early January, before China had informed the world of evidence of human-to-human transmission.

via ZeroHedge News https://ift.tt/3cPCXST Tyler Durden

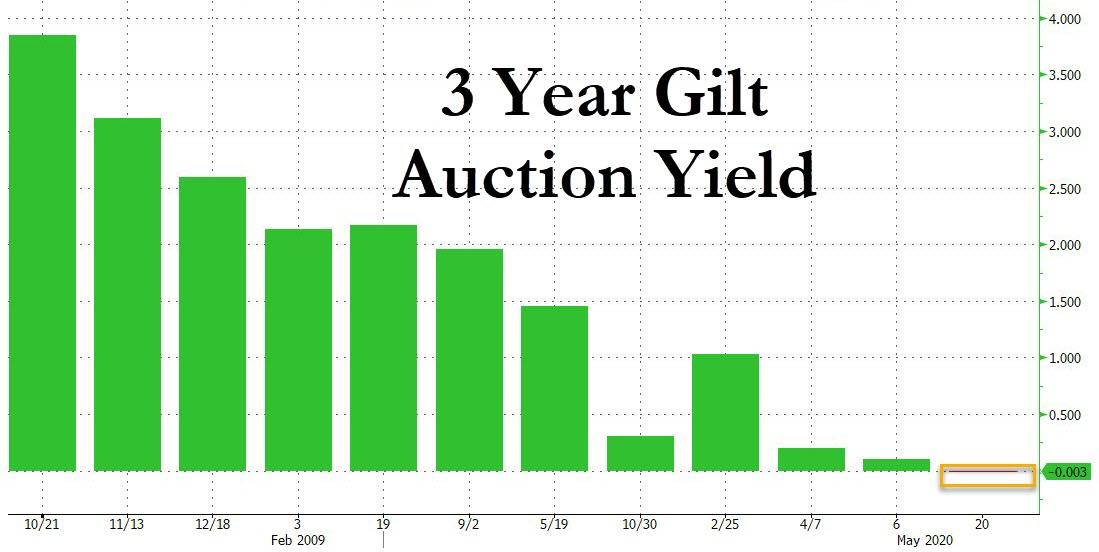

UK Sells Negative-Yielding Debt For The First Time Tyler Durden

Wed, 05/20/2020 – 08:30

Who would have thought that Brexit would result in a convergence of the European and UK bond markets.

With the UK swept by a debate whether it should follow Europe into negative interest rates, the bond market appears to have made the decision for it, when this morning the UK sold £3.75 billion in 2023 gilts at a negative yield of -0.003% for the first time, with a fall in inflation piling even more pressure on the fiscal and monetary policymakers to take new action to prop up the economy.

The UK drew orders of £8.1bn in Wednesday’s auction resulting in a 2.15 bid to cover to the amount the DMO was looking to sell. According to the FT, “the robust demand underscored the appeal of gilts, long considered to be a haven due to the UK’s strong creditworthiness. It also suggests any fears over the large increase in borrowing the UK has undertaken due to the Covid-19 pandemic has not yet weighed on investor appetite for the debt.”

The auction comes during the growing debate into whether the BoE will need to reduce its main interest rate from its already historic low into negative territory, as policymakers attempt to bring inflation back towards the 2% target. Whatever you do, don’t look at Japan.

The negative yield means investors who hold the debt to maturity will get fractionally less than they paid, and are paying for the privilege of lending to the UK government, reflecting growing investor expectations that the Bank of England may need to take additional steps to push inflation back to its 2 per cent target. The UK sold a one-month bill at a negative yield in 2016, but this represents the first time it has sold a conventional longer term bond at yield below zero.

Moyeen Islam, rates strategist at Barclays, said the auction was a “symbolic hurdle” noting that “given recent comments from monetary policy committee members, the question of negative policy rates is far from settled.”

While other central banks have already used negative rates they have faced stinging criticism, especially from bankers since it weighs heavily on the profitability of their traditional lending operations: “I can’t think of an economy where negative rates are a worse idea than the UK,” said SocGen FX strategist Kit Juckes. “The economic benefits are dubious but the power of a cocktail of negative rates and massive quantitative easing to weaken the currency seems clear and if the pound falls enough, it will make QE harder.”

Separately, also on Wednesday UK CPI inflation crashed below 1%, nearly halving to 0.8% last month from 1.5%, missing consensus expectations and the lowest level in almost four years.

According to Nomura, the most important reasons behind the fall were: 1) falling household energy bills, where the lower price cap in April led to a 3.6% m-o-m drop in gas bills versus a 9.2% m-o-m rise in April last year (as a result household energy took nearly 0.4pp off headline inflation between March and April), 2) the largest fall yet in petrol prices in response to lower oil prices since the start of the year (a fall of nearly 8% m-o-m versus a 2.6% m-o-m rise in April last year, taking 0.3pp off headline inflation) and 3) a regulatory-imposed reduction in household water bills (down 1.7% m-o-m compared with the April 2019 monthly rise of 2.7%). Taken together those three factors can account for pretty much the entirety of the 0.76pp decline in headline CPI inflation between March and April. Economists have warned the shock to demand caused by lockdowns could cause a wider disinflationary trend.

Against the backdrop of a protracted period of below-target inflation, and in order to preempt any liquidity disruption in bond markets associated with the exhaustion of the MPC’s existing asset purchase program, Goldman said it “continues to expect the Bank of England to announce an additional £100bn of quantitative easing at its next decision on 18 June.”

“With inflation now more than 1 percentage point below target, the governor of the Bank of England will . . . have to write a letter to the Chancellor explaining why inflation is so far below target and what he intends to do about it,” said Melanie Baker, senior economist at Royal London Asset Management. “The next step we expect to see is more asset purchases.”

via ZeroHedge News https://ift.tt/2LNkKJu Tyler Durden

“When things in life are rotten, there’s one thing you’ve forgotten…”

It’s fascinating to read US Online Brokerages have attracted record new punters, over 800,000 sign-ups – through the lockdown in March and April. Sport followers and racing gamblers have given up the lure of professional sports and now punting on the market – apparently fuelling the rally. They’re must feel like they are finally winning – backstopped by the rising market and the Golden Fed Put. Zac from Alabama is making $1000 a day trading, according to web sited promising to share the secrets Wall Street won’t!

I will share Blain’s Market Mantra No 1 with them for nothing: “The Market has but one objective: to inflict the maximum amount of pain on the maximum number of participants.”

Back in the real world…

The news remains unremittingly bad. Therefore… buy stocks would seem to be the obvious counter-intuitive recommendation…

Yesterday turned negative as the markets realised the Moderna trials showing “maybe” positive results in 8 of 37 patients isn’t quite the salvation we’re hoping for. Fear not.. Tomorrow, some other drug trial will announce the person its testing its virus on looks slightly happier, or a Central Banker will say something really market supportive like: “We’ve got lots of money and we want to give it to you so that markets don’t fall…”

The big risk is that people are going to tire of this B/S. Bank analysts and big investors trying to look past the vaccine/treatment noise, past the Central Bank puts, and focusing on fundamentals all say the same thing: Stocks are massively overvalued ahead of a looming recession. Corporate bond yields need to reflect rising default risk. Simple as.

As I predicted the global aerospace industry is in serious trouble. Rolls Royce are cutting 9000 jobs and preparing for years of disruption. That will have enormous cascading knock-on effects on specialist engineering and aerospace SMEs across the UK that subcontract for the aerospace giants. The Chancellor, Rishi Sunak is being open and honest about the economic crisis in terms of jobs and growth: “a severe recession, the likes of which we haven’t seen”. He’s crushed the Bank of England’s hopes for a V-Shaped recovery..

Someone should tell the BOE everyone else on the planet stopped taking about V-shapes weeks ago.

We can’t simply ignore the global reality – the recession is here, and that has profound implications for growth, supply and demand.

China is supposed to be great driver of global growth. Not anymore it’s not. Virus flare ups, rumours of mass lockdowns, and rising bankruptcies underly the hits we’ve seen in China GDP. Chinese consumers are resisting spending again – they are all in re-building/savings mode, expecting the picture to remain bad. While the economy has re-opened, news reports speak of empty shops, malls and streets. We’re likely to see the same phycological behaviours here in the west.

In the US we’ve even seen a decline in e-commerce sales, hinting at the demand shock from the 37 million Americans now on the dole queue are likely to create.

The latest BAML Survery is clear – A U or W shaped recovery. What is really interesting is the focus on what the new economic landscape will look like. Its clear we’re going face external pressures including challenges in addressing new supply chains and increased protectionism, and the prospect of higher taxes to pay for it all. Lots of folk now fear resurgent inflation will follow deflation!

The report also identifies three main risks – a second coronavirus wave triggering a repeat lockdown, sustained high employment and a European breakup.

I’m going to go out on a limb here, and say we can probably discount two of these.

A second Coronavirus wave is certainly a threat, but we will be better prepared logistically and in terms of therapies. We’ll know enough about how it infects and kills to manage a second partial lockdown better. Better contact tracing will make the response far more targeted and measured. The damage from subsequent waves could be contained – if we are prepared.

I also doubt the Euro and The EU will simply implode. It’s gone this far, and it will keep grinding on in a sub-optimal fashion for years yet. I’d bet the Euro eventually implodes or morphs into something more focused – but it’s a while down the road. What it does mean is years and years of continuing European underperformance.

The area that does worry me is Unemployment.

We may eventually find a vaccine for the virus, but not everyone can be saved from the coming recession. All around the globe corporates are looking at the recessionary outlook. Naturally, they are scaling back investment plans, rejigging targets and budgets, and looking to prepare for a number of lean years – which means cost savings and head count cuts. Let’s assume – as UK ministers admit – that 1 in 5 furloughed workers never return to work. Add that to the number of companies that will remain permanently closed – and its clear we’re in for potentially decades of trouble.

When the economy recovers, the lost jobs will have gone permanently.

I admit I am worried about my kids – one of them has already seen his salary cut and is working 14-hours a day for a company that has had to furlough 80% of staff. My daughter lost both her jobs (her main one in design, and the weekend job she was paying her rent with), but she’s now got a min-wage gig as a barrista – which she loves as it gets her meeting people. I am lucky they are so self reliant… but litterly millions of under 30 year olds in the UK working in hospitality, tourism and retail are going to struggle!

All round the global economy a whole generation of young adults and teenagers are going to find their roles on the bottom rungs of the corporate ladder to be stifled. That could play out badly.

Finally, but I have to take yet another pop at Bloomberg this morning.

I read a truly extraordinary “article” yesterday: “Merkel and Macron Conjure Hamilton Moment to Fight Euro Break-Up”. I am not hyperlinking it because it’s just a too embarrassingly silly opinion piece that is not news. The authors suggest the deal cobbled together by the EU, Germany and France is a brilliant diplomatic solution to save Europe and the Euro (which it is not), but also it’s a deal worthy of “Alexander Hamilton” – which is utterly irrelevant tosh.

Oh! these clever Americans. Apparently, all we need to save Europe is a better understanding of US financial history, and everything will be fine. Please. The travails of a half-baked political compromise between the unelected Brussels technocrats, France and Germany which will take at least a year to reach fruition, have zero to do with the first US treasury secretary who became of post-factual sensation because of a recent hip-hop musical fitting a story of “America then, as told by America now.” Its irrelevant to Europe.

Having read the book and not seen the musical, Hamilton is a fascinating character. I can confidently state the reality is the creation of a centralised US treasury and single currency shared by all the culturally aligned 13 states of the fledgling US in 1790 under Hamilton illustrates exactly why the Euro won’t work.

Or watch it when it comes out on Netflix next month and figure out the lessons…

For the record – the new Euro Recovery Fund has already run into to roadblocks from Austria, Sweden, Denmark and Holland. They don’t want the EU dishing out grants, they want it charging for loans. It also appears the fund won’t be up and running till 2021, which bodes ill for Southern European economies facing a 20% plus tourism hit this year, in addition to all the other economic damage the Virus is doing!

via ZeroHedge News https://ift.tt/2LPwrPT Tyler Durden

Futures Storm Higher, Reversing All Tuesday Losses Ahead Of FOMC Minutes, 20Y Auction Tyler Durden

Wed, 05/20/2020 – 08:03

US equity futures staged another remarkable overnight reversal, recovering all late Tuesday losses and rising right back to the 2950 resistance level observed in recent weeks, as investors clung to hopes of a recovery from the global recession amid signs of more central bank and government stimulus while eyeing fresh outbreaks of the coronavirus.

“Sustained central-bank support should prevent a new market correction,” wrote Xavier Chapard, global macro strategist at Credit Agricole. At the same time, “the main driver of asset prices should be the expectations regarding the timing, speed and extent of the economic recovery.”

Contracts on three main US inexes accelerated gains in the European morning, with traders looking beyond Tuesday’s report which raised doubts about progress in Moderna’s coronavirus vaccine as attention turned to a different company, Aldeyra Therapeutics, which said it would advance the investigational new HSP90 inhibitor ADX-1612 to clinical testing for COVID-19, sending its stock as much as 34% higher. Facebook climbed in the premarket after outlining steps for employees to return to work in July. Lowe’s Cos Inc jumped 8.4% in premarket trade after becoming the latest retailer to report an upbeat quarterly same-store sales; Target slumped after declining to provide FY guidance. The FAAMGs rose between 0.9% and 2.6% in early trading. Big Wall Street banks including Bank of America, Citigroup, JPMorgan gained about 2%.

“With headlines suggesting that more fiscal and monetary stimulus around the globe is under way and with the virus curve being much flatter than a couple of months ago, we would treat yesterday’s setback as a corrective move,” said Charalambos Pissouros, senior market analyst at JFD Group.

In Europe, bourses, and sentiment in general, have been choppy this morning but continues to drift higher ahead of the entrance stateside. The Stoxx Europe 600 Index erased an early decline, with Experian among the top advancers after the Irish credit-services firm weathered the pandemic better than analysts expected.

Asian stocks gained, led by health care and communications, after rising in the last session. Most markets in the region were up, with India’s S&P BSE Sensex Index gaining 0.9% and Thailand’s SET rising 0.8%, while Singapore’s Straits Times Index dropped 0.6%. The Topix gained 0.6%, with Tokyo Keiki and UACJ rising the most. Tokyo Stock Exchange was among stocks which surged amid speculation that it may be a contender to join the Nikkei 225 equity index.

The Shanghai Composite Index retreated 0.5%, with Yutong Bus and Nanjing Chervon Auto Precision posting the biggest slides. Overnight, China’s 5-year LPR was held at 4.65%. China has twin issues of weak external demand and elevated domestic debt, so the LPR will likely be trimmed over the coming months according to BMO’s Stephen Gallo. The upcoming third annual session of the thirteenth NPC will probably see a rethink of China’s GDP growth target.

Investors have been whipsawed by conflicting news regarding a possible vaccine for the virus, as many governments around the world ease lockdowns even as the pandemic continues to spread, with Brazil now the world’s hotspot for new infections.

In rates, Treasuries were steady with yields slightly cheaper across the curve ahead of Wednesday’s 20-year bond auction, broadly holding late-Tuesday advance spurred by closer examination of Moderna Inc.’s vaccine study. FRA/OIS continues tightening after latest drop in 3-month dollar Libor. Yields remain within 0.5bp of Tuesday closing levels, 10-year around 0.69%; bunds and gilts outperform by 1bp and 2bp. In the UK, the Debt Management Office sold 3.75 billion pounds($4.6 billion) of 2023 bonds at a negative yield of -0.003% for the first time.

In FX, the dollar slipped against most Group-of-10 peers, and the euro climbed toward a two-week high. The euro advanced for a fourth day against the dollar, yet failed to rise above Tuesday’s high. The euro’s gains coincide with progress on a 500 billion-euro fiscal-stimulus plan by the European Union, though critics say the package may be too little, too late to counter the devastating effect on the region’s economies and bolster the outlook for corporate profits.

The pound was among the worst G-10 performers after April U.K. inflation slowed to the weakest level since 2016; New Zealand’s dollar rose against most peers after central bank Governor Adrian Orr signaled that negative rates in the nation are still some way off. The yen hovered against the greenback while ultra-long Japanese government bonds climbed after an auction of 20-year debt drew the highest bid-to-cover ratio since July last year. The Norwegian krone gave up an earlier gain against the euro and the dollar amid profit taking and selling against its Swedish peer. South Africa’s rand soared as much as 2% against the dollar, with the country’s central bank seen slashing its policy rate to a record low on Thursday to bolster the economy.

In commodities, West Texas Intermediate crude climbed 1.4% to $32.41 a barrel. Gold strengthened 0.3% to $1,749.62 an ounce. Iron ore dipped 1.8% to $93.83 per metric ton. Platinum gained 2.7% to $914 an ounce.

To the day ahead now, and we’ll get the FOMC meeting minutes as well as April CPI readings from the UK and Canada, in addition to the final Euro Area CPI reading for April too. In terms of central bank speakers, there’s the BoE’s Governor Bailey, Deputy Governors Broadbent and Cunliffe, as well as the MPC’s Haskel, who’ll be giving evidence before the House of Commons’ Treasury Select Committee. Lastly, we’ll hear from the Fed’s Bostic and Bullard, while earnings releases today include Lowe’s and Target.

Market Snapshot

S&P 500 futures up 0.9% to 2,943.75

STOXX Europe 600 up 0.04% to 339.62

MXAP up 0.4% to 148.68

MXAPJ up 0.1% to 479.42

Nikkei up 0.8% to 20,595.15

Topix up 0.6% to 1,494.69

Hang Seng Index up 0.05% to 24,399.95

Shanghai Composite down 0.5% to 2,883.74

Sensex up 0.9% to 30,476.99

Australia S&P/ASX 200 up 0.2% to 5,573.05

Kospi up 0.5% to 1,989.64

German 10Y yield rose 0.7 bps to -0.457%

Euro up 0.2% to $1.0942

Italian 10Y yield fell 3.8 bps to 1.462%

Spanish 10Y yield rose 1.9 bps to 0.661%

Brent futures up 1.4% to $35.12/bbl

Gold spot up 0.3% to $1,749.43

U.S. Dollar Index little changed at 99.44

Top Overnight News from Bloomberg

Chinese doctors are seeing the coronavirus manifest differently among patients in its new cluster of cases in the northeast region compared to the original outbreak in Wuhan, suggesting that the pathogen may be changing in unknown ways and complicating efforts to stamp it out

China denounced U.S. Secretary of State Michael Pompeo for referring to Taiwan’s leader Tsai Ing-wen as “president,” vowing to “take necessary countermeasures” in response

In a challenge to the proposal set out by Germany and France on Monday to fund the economic recovery, Austria, the Netherlands, Denmark and Sweden expect to publish their framework some point after 3 p.m. Brussels time, according to two European officials familiar with their plans

Goldman Sachs is reopening offices including Frankfurt, Madrid and Milan as its European operations begin to re-emerge from shutdowns prompted by the coronavirus

If you’ve missed the rebound in European equities, it might be a little late to get in on the game now. Strategists only expect the Euro Stoxx 50 Index to rise another 3.8% from Monday’s closing level to 3,023 by the end of the year, according to the average response in a poll by Bloomberg News

Asian equity markets traded indecisively following the soured mood on Wall St amid ongoing US-China tensions and with the major indices pressured heading into the close as vaccine hopes were knocked by reports that Moderna’s COVID-19 vaccine did not produce data critical to its assessment. ASX 200 (+0.2%) was initially subdued by weakness in the utilities and energy sectors, while a record decline in preliminary retail sales and deteriorating relations with China added to the lacklustre tone, before a recovery in financials and strength in tech helped overturn the losses. Nikkei 225 (+0.8%) was underpinned by stimulus hopes after the BoJ announced to hold an off-schedule meeting this Friday to discuss a new loan scheme for firms impacted by the virus and with the Japanese government to set up a JPY 50bln fund with the private sector to inject capital into businesses. However, weakness was seen in Fujifilm on reports its Avigan drug was not showing apparent efficacy as a coronavirus treatment and earnings releases were also a catalyst for price action with both Sharp and Mitsubishi Motors suffering from weaker results in which the latter posted a full-year loss. Hang Seng (U/C) and Shanghai Comp. (-0.5%) mirrored the choppy trade after the PBoC kept its Loan Prime Rates unchanged as expected and following the verbal jousting between China and the US. Finally, 10yr JGBs attempted to nurse the prior day’s losses following the recent rebound in T-notes and following stronger results at the 20yr JGB auction although the gains were eventually reversed amid outperformance in Japanese stocks.

Top Asian News

Thailand Cuts Rate for Third Time as Economic Crisis Worsens

Turkey Turns to Gulf Ally Again With $15 Billion Qatar Swap Line; Lira-Averse Banks Fuel Turkish Fears of Another Dollar Rush

Debt Binge to Widen India’s Fiscal Gap to 13%, Says HSBC

A choppy and overall mixed session thus far in the European equity space [Eurostoxx 50 +0.3%], with little conviction amid light news flow and despite a mostly positive APAC handover. That being said, US equity futures grind higher and nurse the losses seen following yesterday’s Moderna disappointment. Sectors are mixed with clear outperformance seen in defensives vs. cyclicals ex-IT, reflecting more risk-aversion-heavy trade. The breakdown also paints a similar picture with Healthcare the outperformer whilst Autos, Banks, and Travel & Leisure all reside towards the bottom. In terms of individual movers, Fiat Chrysler (-3.2%) shares were halted amid doubts raised about the Co’s USD 6bln dividend following talks for a 3yr long EUR 6.3bln loan facility, with sources stating that Italy could look into Fiat Chrysler’s planned pay-out, with Peugeot (-3.4%) also lower in sympathy. On the flip-side Marks & Spencer (+4.5%) sees post-earnings gains after revenue printed in-line with forecasts. Fresenius SE (+3.9%) holds onto gains on the back of a broker upgrade at Morgan Stanley.

Top European News

U.K. Inflation Slows to Weakest Since 2016 Amid Virus Crisis

London Office Landlord Braces for Recessionary Hit to Rents

Cambridge University Moves All Lectures Online Until 2021

Norwegian Air Drops 60% as Reality Sinks In for Shareholders

In FX, hot on the heels of RBNZ Deputy Governor Bascand’s wait-and-see policy guidance on Tuesday, Governor Orr has echoed sentiments overnight by stating that negative rates are not on the current agenda, but an option for consideration much later. Hence, the Kiwi remains some distance ahead of the chasing G10 pack on the 0.6100 handle vs its US counterpart and closer to 1.0700 against the Aussie that is still hampered by deteriorating trade relations with China and a stark reality check on the retail side as sales slumped in April by more than double the magnitude of the prior month’s rise. In response, Aud/Usd has slipped back under 0.6550 after another test and rejection of recent highs around 0.6570 and now eyeing May PMIs for further direction.

CHF/EUR – The Franc and Euro are both holding gains relative to a broadly soft Dollar, as the DXY continues to pivot 99.500 ahead of FOMC minutes after little new from Fed chair Powell in testimony yesterday, but perhaps more impetus via his opening remarks at an event on Thursday. Eur/Usd is establishing a firm base above 1.0900 and decent option expiry interest between 109.30-35 (1 bn), while Usd/Chf straddles 0.9700 and Eur/Chf rotates either side of 1.0600 following its sharp spike from near 1.0500 multi-year lows in wake of Germany and France reaching agreement on a common EU debt funded COVID-19 rescue package.

CAD/JPY/GBP – All narrowly mixed vs the Greenback as the Loonie maintains momentum within 1.3960-16 parameters with ongoing assistance from firm crude prices awaiting Canadian CPI, while the Yen has pared more losses following a 3rd test of resistance just above 108.00, but crucially from a technical perspective no further approach towards the 200 DMA. Next up, Japanese trade data tomorrow before the BoJ’s bank lending inter-schedule policy meeting on Friday. In contrast, Sterling has succumbed to more ‘sell in May’ and chart-inspired downside pressure with stops, albeit light so far, tripped at 1.2225 in Cable that represents one side of in inverse head and shoulders formation, but the Pound has regained some poise post-soft UK inflation data and pre-BoE testimony to a TSC.

SCANDI/EM – Somewhat contrasting fortunes for the Scandinavian Crowns as Eur/Sek resumes its bearish tendencies towards 10.5500, but Eur/Nok rebounds from sub-10.9000 in wake of the Riksbank’s latest FSR and a Norges Bank economist survey both highlighting the adverse impact and risks related to the coronavirus. Meanwhile, the Turkish Lira looks apprehensive in the run up to tomorrow’s CBRT rate decision even though the Bank’s swap line to Qatar has been boosted by Usd10 bn to Usd15 bn, but the SA Rand is heading back down with more purpose after breaching a prior May peak ahead of retail sales and the SARB on Thursday with another 50 bp ease seemingly priced in.

In commodities, WTI and Brent front-month crude futures trade choppy and swing between gains and losses. WTI June expired yesterday whilst holding up above USD 30.0/bbl at USD 32.50/bbl, whilst June/July settled in backwardation – which some suggested show a clear significantly shift in sentiment MM. That being said, short-covering and low vol/open interest may have also influenced the June price action. Underlying fundamentals seem to be broadly improving, but “poor refinery margins suggest that this strength is unlikely to be sustainable in the near term.” ING says, “. We would need to see strength in refinery margins in order to persuade refiners to increase utilisation rates, but at current levels, there seems little incentive for them to do so.” On the geopolitical front, Iranian Navy said it will continue with its activities in the Persian Gulf despite US warnings, reported via ISNA, which follows remarks by the US navy that “Armed vessels approaching within 100 meters of a US naval vessel may be interpreted as a threat”. Private inventories yesterday printed a headline draw of 4.84mln barrels. Investors will be eyeing the DoEs for confirmation. Elsewhere in the States, North Dakota’s oil and gas regulators will be meeting today to discuss mandated cuts, albeit little is expected from the meeting and the State only pumps ~1.4mln BPD vs. Texas’ 5mln BPD. In terms of metals, spot gold trades modestly firmer around USD 1750/oz and seems to be deriving strength from a weaker Dollar amid light news flow in early European trade. Copper similarly remains little changed within a tight intraday band.

US Event Calendar

2pm: FOMC Meeting Minutes

DBs Jim Reid concludes the overnight wrap

I have decided that at the end of this week we’ll pause Corona Crisis Daily for now as new case growth and fatalities have been suppressed for now. I really hope it’s a permanent halt but we stand ready to bring it back if the virus has a second wave. Thanks for the numerous interactions and feedback on the report. It’s been a wild ride. In today’s edition we make some big assumptions as to what the fatality rate would be across all age buckets if the entire global population had been exposed to the virus. We use the latest England and Wales data (out yesterday), which splits the numbers by 5-year age buckets and estimate that if the global fatality rate was 0.75% – as many scientists think will end up being in the right ballpark – then our crude estimate is that the 20-64 year old ‘working age’ population fatality rate would be 0.1%. For over 70s, it could be 4.6% and 16.6% for over 90s. At the other end of the spectrum, based on this analysis we think 1 in every 298,000 under 14 year olds would die, again highlighting the hugely age discriminant nature of this virus. This analysis contains many big assumptions including over the end state fatality rate and the same proportionality across ages as current but you can see the theory in today’s CCD.

After around 9 weeks of working from home, being more productive, publishing more reports than ever before and conducting numerous video and audio meetings, at 4:30pm yesterday afternoon my internet finally went down for the first time. After 30 minutes of fighting it, I went into the garden put on my sunglasses and finished the work I had to do on my iPad using 4G. Just as I was finishing my iPad turned itself off and said it had to cool down before it could be used again. That’s how unseasonably hot it was yesterday here in the UK. Even the technology melted.

After a Monday session where there were no clouds to be seen for miles around, yesterday a few storm clouds appeared late in the New York session in the form of a report from health publication STAT saying that some vaccine experts may have doubts over the Moderna vaccine that saw markets rally universally the day before. The article found that ”based on the information made available by the Cambridge, Mass.-based company, there’s really no way to know how impressive — or not — the vaccine may be.” This caused a pullback in risk markets that were already a bit more mixed yesterday as we were reminded of the reality of the savage hit to the economy and to earnings. A reminder that our house global economic forecasts are based around a vaccine not being widely available over the next 18 months. Interestingly in our monthly survey published on Monday (link here) 75% thought that there would be a vaccine available within 18 months. This was obviously before any of the Moderna news this week.

The S&P 500 moved between gains and losses before the more negative Moderna news and ending the session -1.05%. While not especially deep given the sell-off of recent months, the pullback was broad based with all 24 industry groups trading lower by the end of the day and 80% of the index being down. Back in Europe, the story was similar even though they closed before the vaccine story, with equities closing lower after giving up morning gains, with the STOXX 600 down -0.61%. European auto stocks lagged behind as April EU vehicle registration fell 78% yoy with just over 290,000 cars sold, the lowest since the data started being tracked in 1990. Yesterday also saw short-selling bans end in a number of European countries and consequently benchmarks in those countries underperformed the broader index with Spain (IBEX -2.51%), Italy (FTSE MIB -2.11%), Belgium (BEL20 -1.69%), France (CAC -0.89%), Greece (ASE -1.37%), and Austria (ATX -4.30%) all declining.

In terms of earnings, Home Depot, the hardware giant, was down -2.90% after it announced that its virus-related costs surpassed the rise in sales, even as more people undertook home improvement projects while in lockdown. EPS for the company missed estimates at $2.08 (vs. $2.25), the first miss since 2014. Walmart was another giant member of the Consumer Staples sector that saw a large rise in sales as customers stockpiled into lockdowns. Sales ex-gas was up 10% in Q1, above the consensus +8.6%, while adj. EPS was reported at $1.18, beating the estimated $1.12. The shares were up +4% premarket, before trading lower on the day, finishing -2.11% as the company withdrew its 2020 guidance.

Oil had a less volatile day than seen recently, with WTI up just +2.14% as Brent actually fell back -0.46%, bringing its run of 3 successive advances to an end. It wasn’t all bad news for commodity prices though, as copper, which is often taken to be an industrial bellwether, rose a further +0.71% to reach a 2-month high.

Overnight, with little in the way of fresh news markets in Asia are trading more mixed with the Nikkei (+0.93%) and Kospi (+0.24%) up while the Hang Seng (-0.11%) and Shanghai Comp (-0.45%) are both down. Meanwhile, futures on the S&P 500 are trading up +0.59% while WTI oil is up a further +0.53%. Iron ore prices are also up +1.65% this morning bringing the gain since April 29th to 19.24%, a period, which also hasn’t seen a single daily decline.

Moving on. Fed Chair Powell appeared with Treasury Secretary Mnuchin before the Senate Banking Committee yesterday, where he said that the US was facing its biggest economic shock in living memory. The Fed Chair reiterated that more fiscal support may be needed but did shy away from taking a side in the current debate between Republican and Democratic lawmakers regarding the need for additional stimulus funding for state and local governments. Powell also talked up the ability of the Fed to make a difference, saying that “It’s all ahead of us. The amount that has gone out so far, in the context of the U.S. economy, is fairly modest.” The Main Street lending facilities, focusing on small business, should be up and running within 2 weeks. Lastly, Secretary Mnuchin, when asked about ultra-long US bonds, said that the Treasury did not find enough demand for that duration in studies undertaken prior to the current pandemic. Elsewhere, Minneapolis Fed President Kashkari said that it was “probably a year or two away before we really start seeing strong economic growth”.

Turning back to Europe, and on the recovery fund proposals from Merkel and Macron on Monday, the French finance minister Bruno Le Maire said yesterday that it “probably couldn’t be available before the start of 2021”. Furthermore, they’ll need to persuade all of the 27 member states to get it through, and some have already sounded notes of resistance, such as Austrian Chancellor Kurz the previous day who tweeted that they were willing to help with loans, whereas the proposal was for the fund to use grants instead. Also on European politics, it’s worth noting that French President Macron’s party lost its parliamentary majority yesterday after a number of MPs defected. See this piece here from Marc de-Muzion on the recent French political developments.

Against this backdrop, there was a further narrowing of peripheral spreads in Europe though, suggesting that investors continue to be reassured on balance by the prospects of an EU-wide recovery fund. By the end of the session, the spread of 10yr yields on Italian (-3.4bps), Spanish (-9.4bps), Greek (-13.3bps) and Portuguese (-9.2bps) debt over bunds had all narrowed even in a risk off equity session in Europe. In the US meanwhile, 10yr Treasuries also advanced, with yields down -3.7bps.

The downturn in risk market sentiment wasn’t helped by the economic data. Starting with the US, and housing starts in April fell to an annualised rate of 891k (vs. 900k expected), a -30.2% drop from the previous month’s reading. This now puts them at their lowest level since February 2015, and follows an -18.6% drop a month earlier. The building permits number was somewhat better than expected at 1.074m (vs. 1.000m expected), but that was also down -20.8% from the previous month. Here in the UK meanwhile, the number of jobless claims rose by 856.5k to 2.097m, which is their highest level since July 1996, while there was the largest quarterly decrease in vacancies (which fell to a 6-year low in the three months to April) since the current time series began back in 2001. In Germany, however, the ZEW survey’s expectations reading rose to 51.0 in May (vs. 30.0 expected), its highest level since April 2015. However, the current situation did fall to -93.5 (vs. -86.6 expected), the lowest since July 2003.

To the day ahead now, and we’ll get the FOMC meeting minutes tonight, but before then we’ll also get the Euro Area’s advance consumer confidence reading for May, as well as April CPI readings from the UK and Canada, in addition to the final Euro Area CPI reading for April too. In terms of central bank speakers, there’s the BoE’s Governor Bailey, Deputy Governors Broadbent and Cunliffe, as well as the MPC’s Haskel, who’ll be giving evidence before the House of Commons’ Treasury Select Committee. Lastly, we’ll hear from the Fed’s Bostic and Bullard, while earnings releases today include Lowe’s and Target.

via ZeroHedge News https://ift.tt/36dOPeU Tyler Durden

Global COVID-19 Infections Near 5 Million As Brazil Confirms Record Daily Jump Of 17k: Live Update Tyler Durden

Wed, 05/20/2020 – 07:09

Summary:

Russia outbreak tops 300k cases

Brazil reports 17k+ cases in latest record jump

Global COVID-19 case total nears 5 million

Rolls Royce cuts 9,000 jobs, largest layoffs in 30+ years

Afghanistan passes 8k cases

UN claims Africa largely ‘spared’ by coronavirus

Germany’s largest state reopens polls

German government bars foreign takeovers of German health-care firms

Spain makes mask wearing in enclosed spaces “compulsory”

UK still working out quarantine guidelines for travelers

Head of Japan’s virus advisory committee says 2nd wave possible before winter

* * *

For much of the last week, our coverage of the ongoing coronavirus pandemic has focused on two countries that have rapidly climbed the international rankings over the last 10 days, landing them in the top 5 worst-hit nations. They are: Russia and Brazil. After reporting ~15k cases for three straight days, Brazilian public health officials on Wednesday morning reported a staggering 17,408 new cases (case numbers are typically reported with a 24-hour delay, and don’t always reflect the true number of infections). The country has reported just below 300k cases, though some suspect the true number of infections might be as much as 4x the official number. The country has confirmed ~17,000 deaths as well.

Brazil’s outbreak has been exacerbated by President Jair Bolsonaro’s insistence that the virus is just “a little flu”, and that the only sensible approach is to simply let the disease run its course, Bolsonaro has said. Over the past 6 weeks, the Brazilian government has seen 2 health ministers resign. Meanwhile, across the country, businesses continue to reopen even as health-care systems in more-remote Amazonian states have been completely overwhelmed. Its Neighbors have closed their borders, fearing Brazilians might carry the illness across the border.

Meanwhile, the total number of coronavirus cases in Russia passed 300,000 as 8,764 new novel coronavirus infections were reported on Wednesday, taking the nationwide total to 308,705. Amazingly, this was the smallest jump in new cases in 3 weeks.

A Russian woman wears a mask

However, Russia’s leaders believe that their lockdowns and other measures are starting to work, Prime Minister Mikhail Mishustin – who took 3 weeks off to battle the virus after being infected himself – advised that restrictions should be lifted carefully in the 17 regions where lockdowns have been imposed over the coming weeks.

Dr Melita Vujnovich, the WHO’s Russia representative, claimed the outbreak in Russia had entered a “stabilization phase.” Others fear the outbreak is much larger than counted given the country’s surprisingly low death toll, which edged up to 2,972 on Wednesday, with 135 new fatalities reported in the past 24 hours.

As of ~7amET, Johns Hopkins University had counted more than 4.9 million cases of COVID-19, and more than 323,000 deaths. More than 1.7 million people have recovered.

The number of new cases reported on the day has moved higher recently thanks to Russia and Brazil, which combined now account for ~25% of new cases.

In corporate news, Rolls-Royce is cutting 1/5th of its workforce as it braces for the aviation industry disruptions caused by the coronavirus pandemic to endure for several years.

The aircraft engine maker said it would cut at least 9,000 of its 52,000 jobs in what would be its largest headcount reduction in 30 years.

As the US and Europe continue to reopen with minimal blowback, internationally, the focus has shifted toward the developing world – particularly countries in the Middle East and South America.

For example, the Guardian reported Wednesday that the number of confirmed coronavirus cases in Afghanistan had passed 8,000, as roughly 50% of tests done in a day come back positive for the 2nd straight day. The total numbers are: 8,145 cases and a death toll of 187.

So far 25,700 suspected patients have been tested. The country received 250 RNA extraction kits from the WHO on Tuesday. The northern province of Balkh exceeded Kabul in number of deaths, with three of the latest Covid-19 deaths reported in the province. Balkh has so far recorded 27 deaths and 622 cases. Four of the new deaths were reported in the eastern province of Nangarhar. The western province of Herat recorded 59 new confirmed cases. Afghanistan’s first case was recorded in Herat, where migrants from Iran are believed to have introduced the virus.

Fortunately, in Africa, the utter devastation that experts feared would hammer Africa as the world’s poorest governments confronted the virus has yet to emerge (sorry, Bill). This low (speaking relatively) case number has “raised hopes that African countries may be spared the worst of the pandemic,” said UN Secretary-General Antonio Guterres, as he praised the “swift” response of African governments.

As Germany continues to reopen, open-air swimming pools have reopened Wednesday as virologists say they are confident chlorine in the water could kill the virus. Authorities in North-Rhine Westphalia – Germany’s largest state by population – have granted the 340 lidos in the region permission to reopen – so long as they abide by the new hygiene rules. In Berlin, swimming pools won’t reopen until next week, while other regions won’t allow them to reopen until June.

In other news, the German government gave itself new powers to block hostile foreign takeover bids for prized German health-care and pharmaceutical companies, a measure intended to protect the country’s supplies of essential health-care equipment and drugs.

After reporting fewer than 100 deaths yesterday, the Spanish government has published new compulsory guidelines on mask-wearing making the wearing of a mask while in an “enclosed space” mandatory for all people over the age of six. It also calls for masks to be worn outdoors anywhere the 2-meter social distancing protocols can’t be followed.

The British government, meanwhile, is still working on the details of how it will implement quarantine measures for people arriving in the country, according to Interior Minister Priti Patel.

“We are still developing measures, so we are not in the position to say ‘this is how it’s going to work’,” Patel said during an interview with LBC radio. “In terms of how this will work, we will be announcing this shortly,” she said, confirming only that the duration of quarantine would be 14 days.

While China continues to carry out mass testing and reimposed lockdowns in Wuhan and the northeastern province of Jilin, Indonesia on Wednesday reported 693 new cases, its largest daily jump yet, bringing its total to 19,189 – though Indonesia’s outbreak is suspected of being much larger due to the government’s initial refusal to acknowledge it. 21 additional deaths reported, taking the total to 1,242, while 4,575 people have recovered.

In Japan, infection levels have returned to their lows from late March, but the deputy head of the Japanese government’s advisory panel on the coronavirus, Shigeru Omi, warned a parliamentary committee on Wednesday that it is still possible to see a new wave of infections before winter comes.

via ZeroHedge News https://ift.tt/2TnKKj2 Tyler Durden

One of the more flummoxing aspects about living in Puerto Rico is that the political leadership is never-ending parade of highly corrupted, certifiable idiots.

The latest Governoramus of Puerto Rico seems hellbent on destroying every remaining scrap of prosperity on this island, all in an effort to indulge her ego-maniacal God complex.

Puerto Rico was the first places in the US to order a full lockdown, and it may very well be the last place to open up; the governoramus ordered everyone to shelter in place starting March 15th, and the order is still in effect.

The rules have been completely ridiculous, too. Going to the beach was outlawed. But it’s perfectly acceptable to stand in a crowded line at the grocery store.

One of the great things about Puerto Rico, though, is that nobody cares. People here happily ignore their idiot politicians.

Puerto Ricans naturally distrust their government– local politicians and bureaucrats have been robbing and stealing longer than anyone can remember.

For example, the FBI recently came down here and arrested a number of top government officials for stealing federal aid that was supposed to have gone to Hurricane Maria recovery efforts.

Earlier this year when the island suffered a series of earthquakes, the US government sent emergency supplies. But as soon as those relief supplies ended up in the Puerto Rican government’s hands, they mysteriously disappeared.

Just last month, Puerto Rico’s government entered into a contract to buy faulty, overpriced Covid test kits from two companies that have personal and financial ties to the current administration.

Basically it was tens of millions of dollars (which is a lot of money for this place) of BS contracts that went into the pockets of friends of the ruling party.

The list is really never-ending. And people here know it. Puerto Ricans have no illusions that the government is on their side. They know that many of the people in charge are either incompetent, or criminals, or both.

And that’s why nobody here cares what the government says.

A friend of mine sent me a video from a local beach on Sunday showing thousands of people out enjoying the sun and sea in open defiance of the lockdown rules.

I really hope this attitude spreads worldwide.

And to me, that’s one of the many silver linings of this pandemic: more people may finally wake up.

At this point there are realistically two groups– the human beings, and the house cats.

The human beings are sick and tired of these lockdowns. They understand that the world is a scary place, that there are risks.

But they’re still willing to live their lives.

It’s not about taking unnecessary risks or being reckless; they just want to be treated like human beings who are free to make their own decisions without insane government overreach.

The other group just wants to be house cats.

House Cats love being locked down and want more of it. They like government intervention. They love endless money printing and free benefits. They love being taken care of and suckling from the maternal teet of government.

They love cowering in fear in their homes and being told what they can/cannot do.

The biggest difference, though, is that Team House Cat thinks everyone else should live by their rules… and their hysteria.

Team Human thinks that everyone should be free to make their own decisions. Anyone who wants to stay home can stay home, nothing wrong with that. Anyone who wants to go out and take a risk should be able to go out and take a risk.

But most governments are on the side of Team House Cat. And it’s probably going to stay that way for the foreseeable future.

China is experiencing a second wave of outbreaks and has reacted aggressively to lock down more than 100 million people already.

Sadly, nearly the rest of the world seems to want to copy the Chinese government.

(The Chinese central government has also told local housing officials that they will be ‘removed’ if there are Covid outbreaks in their sectors, though it’s unclear whether ‘removed’ means ‘fired’, or ‘disappeared.’)

But the silver lining here is that Team Human is growing by the day; tens of millions of people are starting to see first hand just how disgusting government overreach can be.