During his appearance on the Joe Rogan podcast, Elon Musk said he sympathized with the anti-globalization movement because “we don’t ever want everywhere to be the same.”

The context of the conversation was how civilizations rise and fall and are negatively affected by hive mind thinking, a concept Musk referred to as the “mind virus.”

“I do think that the globalization that we have at the memesphere – there’s not enough isolation between countries or regions. If there’s a mind virus, that mind virus can infect too much of the world,” said Musk.

“I actually sort of sympathize with the anti-globalization people because we don’t ever want everywhere to be the same for sure and we need some kind of mind viral immunity,” he remarked, adding, “That’s a bit concerning.”

The Tesla founder clarified that he was talking about a concept that “happens right now” and not in the future, suggesting he may have been referring to the coronavirus panic.

“When I’m talking about the mind virus, I’m talking about a concept that infects people’s minds,” said Musk, describing it as a “wrongheaded idea that goes viral in an idea sense.”

As we previously highlighted, Musk has become a target of the establishment after he called for the coronavirus lockdown to be lifted.

The Tesla founder asserted at the beginning of March that the panic behind COVID-19 was “dumb.”

He briefly discussed the issue elsewhere in the Rogan interview, asserting that the mortality rate of coronavirus turned out to be vastly lower than health authorities initially claimed.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

US Has ‘Limited’ Ability To Manufacture Coronavirus Treatments, Vaccines

A pharmaceutical company CEO says that while the United States may have the capability to deliver coronavirus treatments – if and when available – that the US has limited capacity to manufacture said treatments.

“Our distribution capabilities work. I’m not worried about that,” said Leonard Schleifer, CEO of pharmaceutical company Regeneron, which is working on a coronavirus treatment. “Our manufacturing capacity, on the other hand…I think our capacity is limited,” he added.

The United States’ manufacturing capacity is “limited” in terms of producing coronavirus related treatments and vaccines says Dr. Leonard Schleifer, CEO of Regeneron. #CNNSOTUpic.twitter.com/hU78ZbUY79

“If there’s something we have to learn from this pandemic so that when COVID-21 or 25 or 32 comes along, we need a little bit more capacity already in place so that we can get it to everybody,” said Schleifer, whose company is developing a method of treating COVID-19 using antibodies.

This, of course, is nothing new – considering that at least 80% of the active ingredients found in all of America’s medicines come from abroad – primarily China, according to the Senate Finance Committee.

“Imagine if China turned off that spigot,” author Rosemary Gibson told Fox News last year. Gibson’s book “China RX: The Risks of America’s Dependence on China for Medicine” reveals the threat posed by such a high level of dependence on a foreign adversary for critical medical items.

“China’s aim is to become the global pharmacy to the world — it says that. It wants to disrupt, to dominate, and displace American and other Western companies,” Gibson added.

And with the US and China currently in a narrative war over how the Wuhan coronavirus began, Americans’ access to vital treatments may be held hostage or used as leverage.

Population Densities per Square Kilometer – Countries

Singapore: 8,337

South Korea: 515

Japan: 334

UK: 267

Italy: 206

China 144

Spain: 98

United States: 33

Sweden: 22

Population Densities per Square Kilometer – US Cities

New York City: 10,431

San Francisco: 6,659

Boston: 5.143

Chicago: 4,582

Philadelphia: 4,337

Miami: 4,324

Population Densities of Cities Japan

Tokyo, Japan: 6,158

Yokohama, Japan: 8,534

Osaka, Japan: 5,200

Population Density of South Korea

South Korea is one of the planet’s most densely populated countries with a density of 503 people per square kilometer, or 1,302 people per square mile. Nearly 70% of South Korea’s land area is mostly uninhabitable due to it being mountainous and the population is established in lowland areas, contributing to a density that is higher than average. In 1975, an estimate was made that South Korea’s population density in its cities, each containing at least 50,000 people, was nearly 4,000 on average. As a result of the continued following of the practice to migrate to urban areas, the figure was much higher in the 1980s.

Seoul’s population density was estimated around 17,000 average persons in 1988, an increase of over 3000 when compared with 1980’s population density of nearly 14,000 people every square kilometer. The current density of Seoul is almost twice that of New York City. The density of Busan, the second largest city in the country, was just over 8,500 persons for every square kilometer in 1988, while this figure stood at a little over 7,000 people back in 1980.

Population Density of Singapore

With a population of around 5.7 million people in 2019 and a land area of approximately 720 square kilometers, Singapore was the second most densely populated country in the world, after Monaco.

High Population Density Does Not Necessitate High Covid-19 Deaths

That is the bottom line.

Of course, there is a tradeoff.

Singapore , South Korea, and Japan all did three things that the US did not do and many in the US still do not want to do.

Aggressive Early Testing

Cooperative Society on Social Distancing Rules

Contact Tracing

1: The US did not do aggressive early testing and it’s too late for that now.

2: The US was late in social distancing and some want to fight it

3: The US did not do contact tracing and may still view that as violation of personal privacy.

Too Late for Early Testing, But Not Overall Testing

Most do want aggressive testing, but despite Trump’s claims, the US is not where we need to be.

However, the number of tests is finally ramping up.

Coupled with spotty social distancing (compared to other countries) Is that enough?

Around the world, the number of new cases reported dropped for the second day in a row, according to data from Johns Hopkins.

However, the number of new cases in Germany accelerated again just days after the federal government loosened restrictions once again, acting in concert with state leaders.

The Robert Koch Institute for disease control said in a daily bulletin released Sunday morning that the number of people each sick person now infects (known as the reproduction rate, or R) has risen to 1.1.

Meanwhile, in the US, the reopening has been going more or less as well as can be expected in Georgia, Texas and the dozens of other states that have already started the process.

Any reading above 1 means the number of new cases is growing, not slowing. And the German government had previously promised to slow down, or even reverse, its reopening policies should ‘R’ linger above 1 for too long.

The institute claimed the number of new coronavirus cases had increased by 667 yesterday, bringing Germany’s total to 169,218, while the daily death toll had risen by 26 to 7,395.

Germany wasn’t the only country to report a slight acceleration in cases Sunday. Iran warned of a resurgence of its own as it reported 51 new deaths. Iran started relaxing virus-related a month ago (around the same time that Turkey surpassed it as the worst outbreak in the Muslim world) and has been reporting steady declines in new cases and deaths ever since.

While Germany considers how to respond to these troubling new data, Spain’s federal government continues to clash with several of the country’s regions over PM Pedro Sanchez’s decision to restrict the scope of the relaxation of its Spain’s extremely harsh 2-month-old lockdown.

On Sunday, as Sánchez held his weekly teleconference with the heads of the country’s regions, several local officials complained about the government’s decision to reject requests by certain, mostly urban, territories (including Madrid but also parts of Valencia and Andalusia).

“It is obvious that Madrid needs to take a step forward,” said Isabel Díaz Ayuso, the head of the region worst hit by the pandemic, citing the capital’s role as the heart of Spain’s economy. As stage one of the reopening begins tomorrow, 51% of Spain will be allowed to gather in groups of up to ten, non-essential shops will be allowed to reopen without appointment, and restaurants and bars may serve people in outside seating.

“It is important to keep everything we’ve gained up to now,” responded María Jesús Montero, government spokeswoman, who said the government’s decision was based on technical criteria.

Meanwhile, Pope Francis on Sunday called on the leaders of the EU to work together to deal with the social and economic consequences of the coronavirus pandemic. The pope noted in his Sunday blessing that 75 years have passed since Europe began the challenging process of reconciliation after World War II. He said the process spurred both European integration and “the long period of stability and peace which we benefit from today.”

In Asia, the Philippines’ health ministry reported 184 new coronavirus cases, taking the Southeast Asian nation’s total reported infections to 10,794, while 15 more deaths related to COVID-19 were recorded, bringing the toll to 719, while 82 patients have recovered to bring total recoveries to 1,924, it said in a bulletin.

In the US, local media reported that at least 75 protestors tested positive for COVID-19 after attending a large rally against the stay-at-home order in Wisconsin.

In the UK, as BoJo prepares to lay out his plan for reopening the British economy, Housing Minister Robert Jenrick said said the economy would restart slowly and cautiously.

“The message … of staying at home now does need to be updated, we need to have a broader message because we want to slowly and cautiously restart the economy and the country,” Jenrick told Sky News.

Jenrick added that easing the lockdown would be conditional on keeping the spread of the virus under control, and if the rate of infection begins to increase in some areas, more stringent measures could be re-introduced. Elsewhere in the UK, a trial of a controversial government test-and-trace app carried out on the Isle of Wight has yielded positive results, much to the chagrin of privacy advocates.

“The trial in the Isle of Wight of that tracking app, the NHSX app designed to help assist people, is going well. People have been downloading it enthusiastically and I know that the plan is later in the month to make it more widely available as well,” a local official told the FT.

In Turkey, which is – as we mentioned above – the worst-hit country in the Muslim world by number of infections, senior citizens have been allowed to leave their homes for the first time in seven weeks Sunday under relaxed coronavirus restrictions. Those aged 65 and over, deemed most at risk from the virus, had been subjected to a curfew since March 21, but they were permitted outside Sunday for four hours as part of a rolling program of reduced controls being pushed by Ankara.

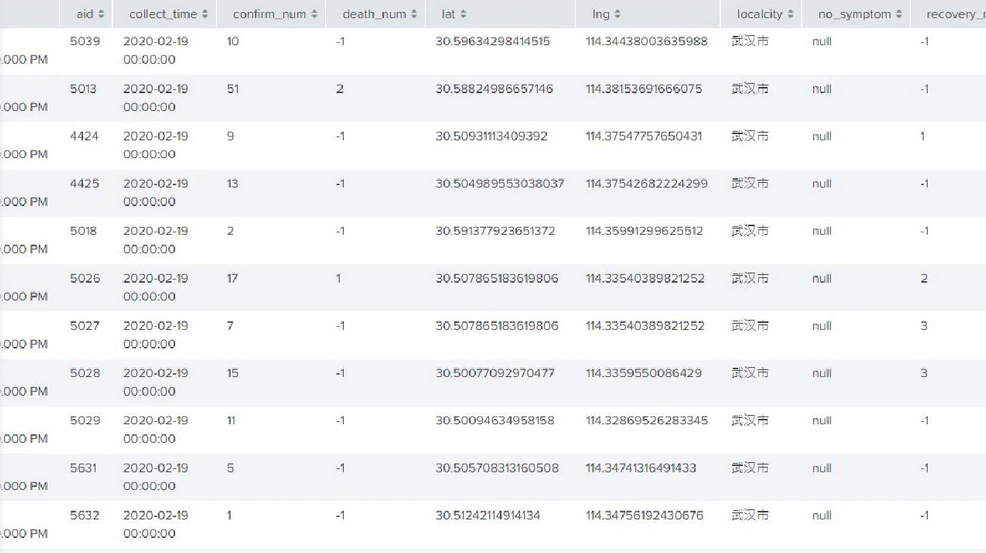

Wuhan Lab Hack Reveals Unreported COVID-19 Cases, Evidence Records Were Deleted

Nearly three weeks ago, a cache of approximately 25,000 email addresses and records of organizations involved with COVID-19 were leaked, including the Wuhan Institute of Virology (WIV), the WHO, the US National Institute of Health, and the Gates Foundation.

Today, The Weekend Australian reports that a dataset obtained from the WIV using the hacked credentials suggests that cases in China have been under-reported.

The dataset, seen by The Weekend Australian, contains empty records for the period February 2-18, indicating records were not kept for that period or that data was deleted. The Australian reported on April 23 that data from the Wuhan Institute of Virology had been hacked. –The Weekend Australian

“I’ve had credible sources tell me that people have used the credentials that were leaked on Twitter and Facebook to access the lab,” said Robert Potter, CEO and founder of online security firm Internet 2.0 – who added that he has “high confidence” in the records, and that it was “highly unlikely that the data had been fabricated.”

“They appear to showcase tracking from what I think is probably a research project within the Wuhan lab working on coronavirus data.

“It’s not data of individual cases, it’s tracking buildings where there are confirmed or suspected (cases) or recoveries or people have died from coronavirus in those buildings. The metadata tab translated to English shows areas (that) correspond to apartment blocks a lot of the time.

But I would also say that the data doesn’t appear to cover every case in China, but it covers different cases to what have been publicly reported.”

The dataset includes an ID, collection time, number of deaths and recoveries, and geolocation information for buildings with infected people.

He said the records included cities that hadn’t appeared among publicly revealed cases. He found more cases from the northern city of Harbin than reported. There were cases in Inner Mongolia and Shanxi Province not found in public data. He had done comparisons with recently released information in China.

He said there were two possibilities for the blank records in early February, one being that data was uploaded in late February or data had been deleted because there “appears to be logs for those days … but they have no entries”.

So it appears that there could be data from before that period that may have been deleted.

There seems to be a high sensitivity around data from that period: –The Weekend Australian

We’ve long known that the data coming out of China is bogus. In March, Chinese investigative outlet Caixin revealed that when mortuaries opened back up this week, photos revealed a far greater number of urns than reported deaths. In one, a truck loaded with 2,500 urns can be seen arriving to the Hankou Mortuary. According to the report, the driver said he had delivered the same amount the previous day.

In another photo, seven 500-urn stacks can be seen inside the mortuary, adding up to 3,500 deaths.

This adds up to more than double the amount of reported deaths in the region – for which grievingfamily members waited in line for as long as five hours to collect, according to Shanghaiist.

And according to Radio Free Asia (funded by the US State Department, so take with a grain of salt), there were around 46,800 deaths in Wuhan, vs. the 4,633 reported.

Reminder to all of the journalists that took China at face value when they claimed they had no more cases https://t.co/mlS0t9HvRo

Larry McDonald, publisher of the investment research service The Bear Traps Report, warns that this crisis is far from over. He spots growing tensions in the credit markets and thinks that large public borrowers like Italy and New York State are in need of massive bailouts.

Stocks have staged an impressive comeback. Since the lows of March, the S&P 500 has gained almost 30%. Despite that, Larry McDonald would not be surprised if new turmoil soon arose.

«In March 2008 for instance, after the failure of Bear Stearns, the Fed acted aggressively and we had a big relief rally. But then came Lehman,» says the renowned investment strategist.

Mr. McDonald knows what he’s talking about. As a former vice-president of distressed debt trading at Lehman Brothers he witnessed the meltdown of the global financial system first hand. Today, he runs the The Bear Traps Report, an independent investment research service for institutional investors.

In this in-depth interview with The Market/NZZ, Mr. McDonald warns of rising defaults in the credit markets and points out that large public borrowers such as Italy and New York State are going to need bailouts of historic proportions. However, he spots opportunities in the metals and mining sector.

Mr. McDonald, despite a grim economic picture, investors are getting confident that the worst of the pandemic is behind us. What’s your take on the financial markets?

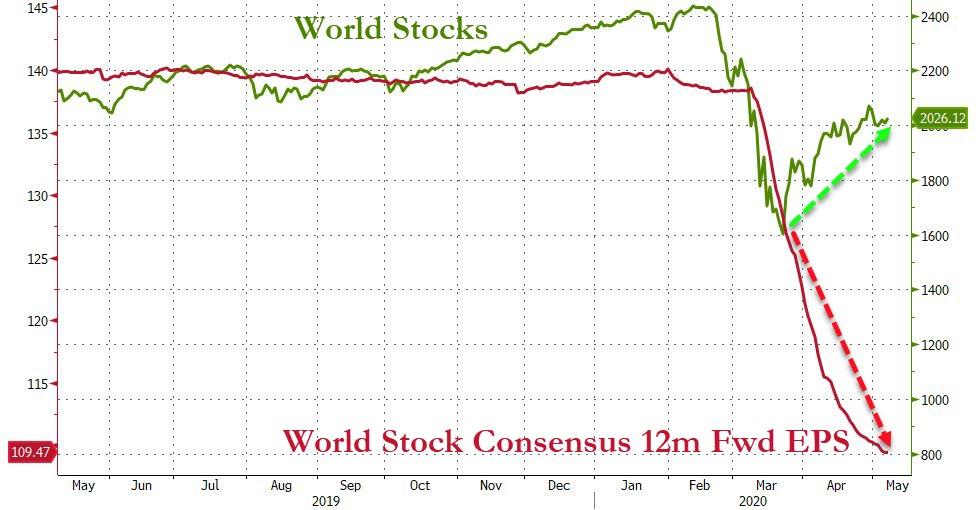

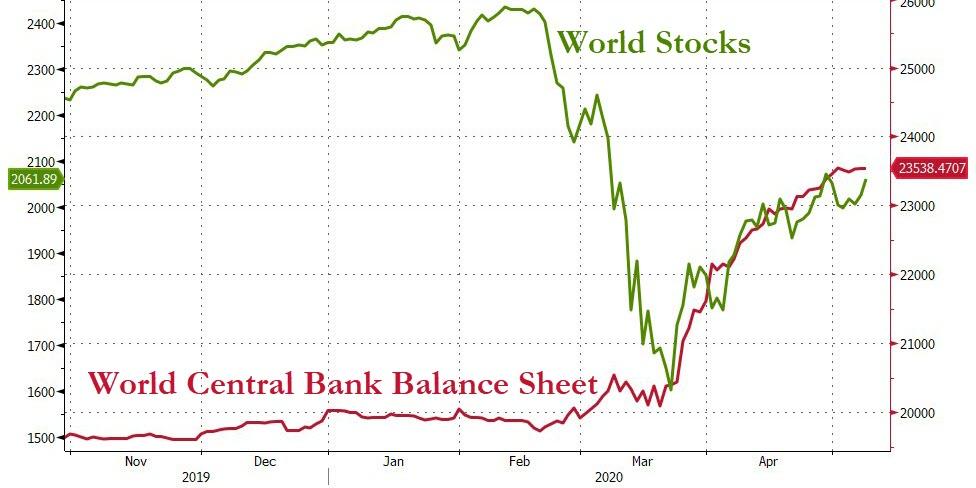

Equity markets have priced in a lot of love from the Federal Reserve. The Fed has done a lot to ease financial conditions, and the amount of liquidity is amazing. Since late February, they’ve done more in terms of balance sheet expansion than nearly two years of action in 2008 to 2010. They’ve clearly pumped up asset prices. Moreover, we have cities re-opening across the United States and some good news on Covid-19 treatments. So the bar is very high in terms of expectations, but underneath the surface trouble is brewing once again.

Why do you think so?

Everyone knows the Fed has expanded their balance sheet by nearly $3 trillion in recent months, but few realize the colossal distortions that are forming in markets. On February 20th, our 21 Lehman systemic risk indicators to gauge the health of financial markets were at the highest levels in years. And then, the market obviously rolled over. Now, our indicators are rising again because there are rising defaults in the leveraged loan space, and there is a lot of credit weakness lurking underneath. Additionally, stock buybacks are shrinking. Over the last decade, we’ve done around $5 trillion of repurchases. But that’s no longer going to be viable. Buybacks are going to go from $600 to $800 billion a year to something like $300 billion. So we’re seeing a sugar high in the markets, but there’s a good chance that we are going to get a big leg down in the next couple of months and test the lows of March.

What could wreak new havoc on the financial markets?

Credit spreads have tightened a lot, especially in the «buy what the Fed is buying» trades, such as investment grade and some fallen angels. But here’s the problem: Whenever we had these situations in the past, there was always another shoe to drop. In March 2008 for instance, after the failure of Bear Stearns, the Fed acted aggressively and we had a big relief rally. But then came Lehman. When you have this type of economic dislocation like today, you are going to have a major default cycle even though the Fed has provided lots of liquidity.

As a former senior distressed debt trader at Lehman Brothers you had a front-row seat at the financial crisis. How do today’s events compare to 2008?

In this recent panic, it got a little worse. During the Lehman crisis, you could still go to a Broadway show or to a ball game. But this is such an incredible economic hit across the board. The banks’ credit default swaps have been much tighter than in 2008, but in Europe there are so many of these zombie banks out there. There’s a whole bunch of institutions that have such massive losses on their loan books that the central banks have to take some of these assets off their balance sheet. But the question is at what price. You can’t move things off at par when they are 50 cents on the dollar.

What kind of loans are you referring to?

One of the big issues are EETCs, enhanced equipment trust certificates. Some of these loans are backed by airplanes and banks finance these things. The way airlines are going to come back is going to be like the restaurants: Let’s say you have a fleet of 4000 planes. So you bring back 1000 planes for the first month, then 2000, and finally you will get to 4000, probably in a year and a half or two years. This is why Boeing is in trouble because that pushes Boeing’s entire sales-production cycle out multiple years. But the worst part is that there are loans on all these planes. That means you are going to have a whole bunch of planes sitting in the desert for many months and even years with loaned capital against it. So interest has to be paid. It’s like a big apartment building with no tenants. This is setting up for a real problem.

In February and March, we witnessed market turmoil of historic proportions. Yet, there has not been a «Lehman Moment» so far. Who could become the Lehman Brothers of 2020?

We haven’t identified a real corporate short yet. But the big one in this cycle is Italy. Italy has shut its economy down for too long, and they have too much debt. Tax revenues are going to be severely impacted, and Italy’s GDP is going to drop massively. The country is insolvent, and the Italian banks are insolvent, too.

Still, central banks are moving heaven and earth to try to avoid another financial crisis.

What central banks are doing is just fueling populism. In America, many people of the middle-class are unemployed, some are getting checks and some aren’t. But then, you have stocks racing back towards their all-time highs after multiple years of buybacks and companies propping up their stocks. It’s similar in Europe where central banks fueled inequality. In Italy, people were already going down this road of populism with Matteo Salvini. So if Europe doesn’t issue Euro bonds, then Italy is going to leave. But if they issue Eurobonds, the Dutch are going to leave. There’s not a lot of wiggle room.

What about financial hotspots in the US?

There are massive defaults in CMBS, corporate mortgage backed securities. And then, the big ones are New York City and New York state. They’re both insolvent, which means the federal government has to bail them out. We think New York City, New York State and Illinois need about a $500 billion bailout.

What does this mean for investors?

Sell the sugar high. Since 2015, the only investment thesis which has consistently worked while providing the best risk-adjusted returns is buying capitulation panics like in September 2015, February 2016, December 2018, and March 2020, and then selling or lightening into strength.

Even in an environment like today, where central banks are moving full steam ahead with their massive stimulus programs?

We think equity markets have priced in a lot, and the real economy has lagged. In February, when the Fed was still expanding its balance sheet at a very aggressive pace, every single analyst on the Street told you: «Don’t fight the Fed.» Over and over again, we were lectured to not bet against the central banks. And, sure enough we got hit with Covid-19. So if you invested with this mantra, you have been destroyed. Now, here we are again: The Fed is extremely accommodative, and they’re using a tool box that is probably ten times more creative than the 2008 tool box. So we’re back again to «don’t fight the Fed». The problem is that this type of thinking gets too many people offsides, and it creates really poor risk reward in the market.

Then again, stocks have staged a strong comeback since the lows of March. April was the best month for the Dow since 1987.

Today, the S&P 500 is trading at 21 or 22 times this year’s earnings, and 24 times last year’s earnings. Now, same crowd that was telling us «don’t fight the Fed» in February, is pushing two new theses.

Number one is the «look through». This is just classic: After the S&P 500 has gone from 2200 to 2900, analysts are coming out with reports saying that you can look through two years of bad earnings: We have a 30% hit to earnings, but in two years from now, we will be back at $170 earnings a share for the S&P 500 and work our way to $200. According to this logic, stocks are «cheap». The theory is that the Fed is going to do so much stimulus that you can look through a 30% hit to earnings.

And what’s the second thesis?

Number two is the Fed model which compares the stock market’s earnings yield to the yield on long-term government bonds. The theory there is that even if you cut the earnings for the S&P 500 by 30%, you still got a superior yield of 150 to 160 basis points compared to less than 120 on 30-year Treasuries. Therefore, stocks are cheap. This all looks great on the chalkboard, but when the next shoes start to drop, it’s going to get ugly. In a crisis, there’s never just one shoe, there’s always three or four. The last time it was Bear, Lehman, AIG, Wachovia, Fannie and Freddie. Yet, the same fools that were telling us that stocks are cheap in February because of the Fed model are back at it again. But in March, you didn’t hear a thing from them, not a peep. They were hiding under their desks.

Where do you spot investment opportunities against this backdrop?

It’s very rare that you walk into a set up with a risk-reward profile as attractive as in the materials sector. We believe this is the trade of a lifetime: Investors are focused on deflation risk, but the side effects of all that fiscal and monetary spending globally are underappreciated. Everybody knows the Covid-19 tragedy poses a significant deflation risk. But in our view, the «unexpected» we must be positioned for is trillions in fiscal stimulus oozing into the economy after this virus has been snuffed out. Also keep in mind that many mines shut down. So you are going to have an increase in demand for commodities with less supply. That means there is a very high probability of a big move in commodities late this year. That’s why we’re long the XME Metals & Mining ETF and the XLE Energy Select Sector ETF.

What makes you so sure this bet will pay off?

It’s a fascinating setup because the supply destruction is unprecedented. If you are a company in the copper, steel or iron ore space, and you’ve gone through the 2016 debacle, you’re a survivor because that was the worst commodities sell-off in decades. So all these companies have massively deleveraged. Now, they are a little expensive, because their stocks have been up 20 to 30% in the last few weeks, but there will be temporary pullbacks, and then you buy the dips.

Then again, demand for commodities seems to be quite weak. The IMF is predicting the worst economic downturn since the Great Depression.

We’re going to get massive infrastructures bills, both in the United States and in Europe. Covid-19 destroyed so many service-sector jobs. When we come back to restaurants, the number of waiters and waitresses is going to be cut in half because you are going to have half the tables for years. Since the pandemic has destroyed the service sector, you are going to have hundreds of thousands of people who need to get a job, and they go to migrate into infrastructure jobs. The US is the perfect example. We have such horrific infrastructure. More than 47,000 bridges are in crucial need of repairs. So you are going to have this tremendous demand for commodities.

Are you long commodity producing countries, too?

Yes, we’re long equities in Chile and Brazil. They are screaming buys.

How important is inflation for this bet to pay off?

We are going to have inflation in about six to nine months. There are massive deflationary forces at work now, but supply chain efficiencies have been destroyed because of Covid-19. In the US, we had to send private citizens to China to buy masks because we don’t produce enough. The US doesn’t produce anything anymore. So even though it costs more, there is going to be a massive incentive to bring production back, and this ruins the whole supply chain efficiency. But we don’t even need inflation for commodities to outperform. The consensus is so skewed to further deflation that even the slightest change in expectations will lead to meaningful outperformance from commodity-sensitive risk assets relative to the S&P 500.

What role does the dollar have in your commodity play?

We are highly focused on the US dollar. The Fed has rolled out the big guns to prevent a disorderly dollar move higher. Of course, there is only so much they can control with every central bank around the world in easing mode. With that said, the Fed has done a lot of key work in dislodging the dollar funding markets. Part of the squeeze for dollars at the onset of the crisis had not only to do with emerging markets and dollar-denominated debt, but Asian financial players who fund and hedge their US risk books with dollars. These things are balance sheets intensive, so as dollar funding disappeared from global markets, many big players in the FX swap market were left desperate for dollars and no way of getting them. However, going forward, the Fed has tamed the FX swap market which should ease the dollar pressures.

Nevertheless, the DXY dollar index is up 3% since the beginning of the year.

We think the dollar is the next policy tool for the Fed. They don’t want the dollar wrecking ball undoing many of the successes other programs have had in easing financial conditions. But the rest of the world is in so much pain, that the dollar has not weakened. And, the problem with Covid-19 is that it’s exponentially more damaging for emerging markets because they don’t have the fiscal and monetary engine the US has. So there is tremendous pressure behind the scenes for the Fed and the Treasury to get the dollar lower to save the global economy. In other words: Why would you use $15 trillion of fiscal and monetary stimulus in the US, Europe and Japan combined, and then have emerging markets defaults blow it all up? The only way out is to weaken the dollar. If the dollar strengthens from here, you are going to have a colossal default cycle.

So what will the Fed do next?

The Fed will communicate to the market that just because things are getting better, it doesn’t mean that they will take their foot off the pedal. In fact, what the Fed is really going to be saying is: «Don’t worry about tightening for a long, long while». The point is: I expect a big forward guidance change to be accompanied by some sort of yield curve control implementation, as Fed Governor Lael Brainard argued for in a speech in February. And that’s very good for silver. The trade of the year will be silver. Every time the Fed used forward guidance aggressively, silver exploded.

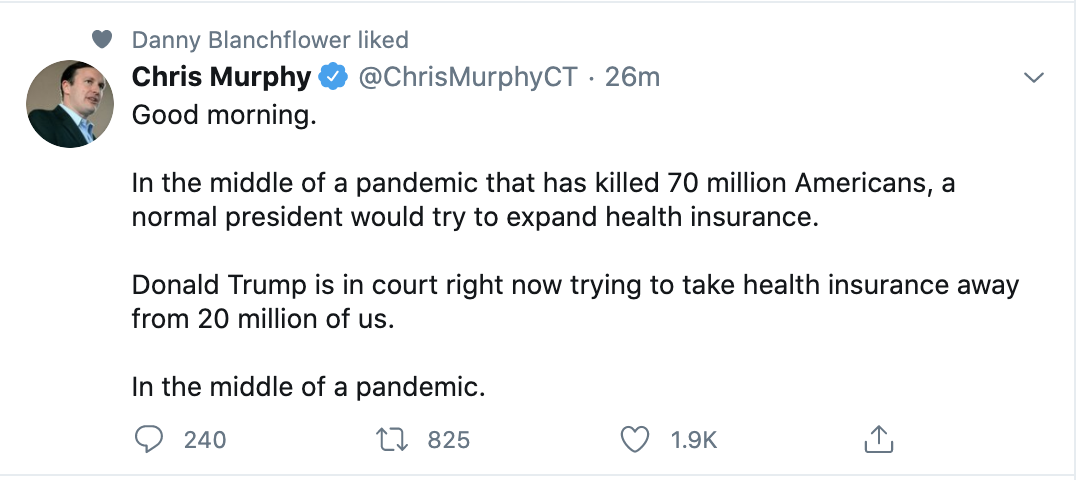

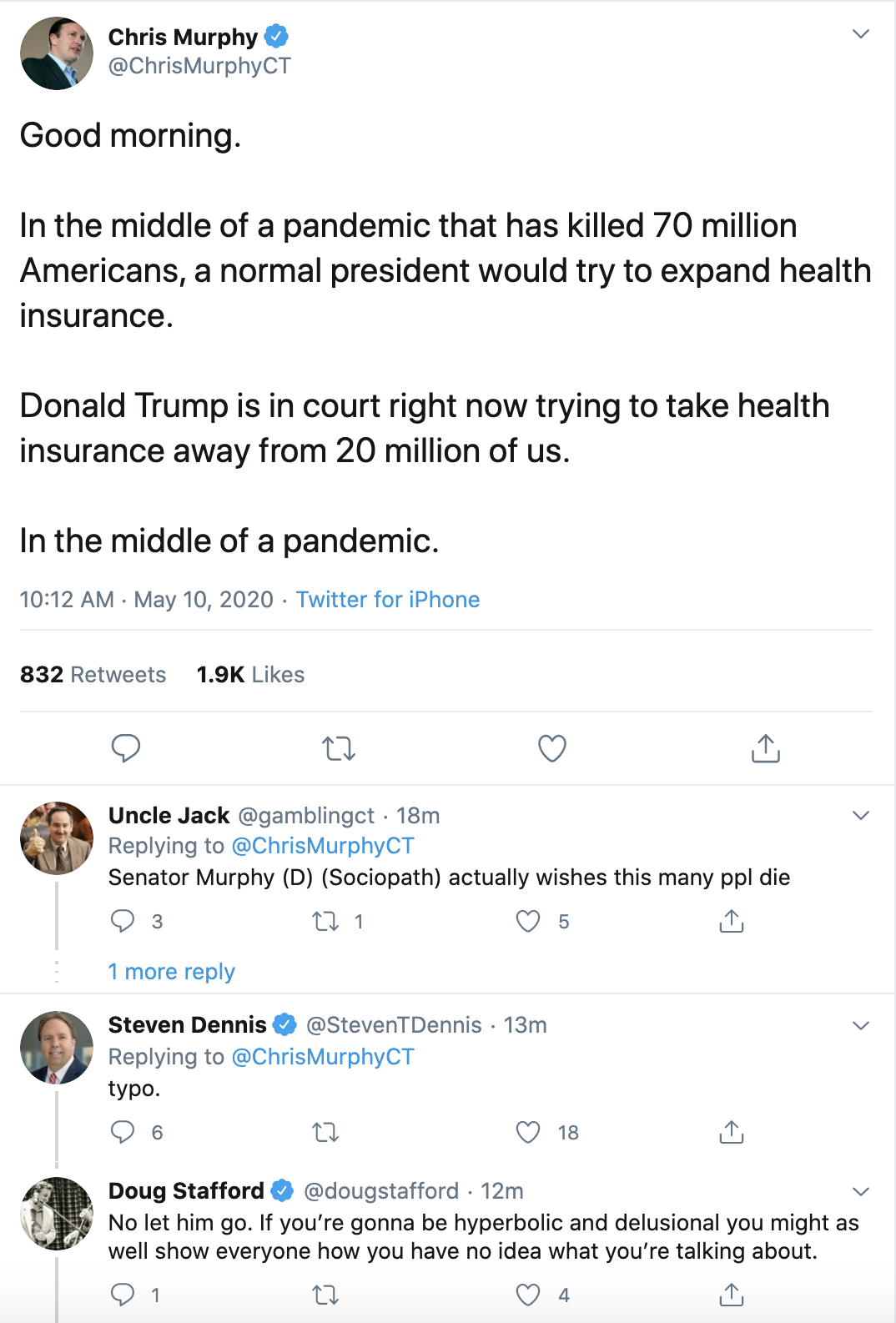

Connecticut Senator Claims COVID-19 Pandemic Has Killed “70 Million Americans”

To the Intern running Connecticut Sen. Chris Murphy’s twitter account on Mother’s Day: We’re sorry, but 70 million??

In what many assume is a hilarious twitter typo, the Connecticut Senator and Senate Foreign Relations Committee member accused President Trump in a tweet of trying to take away people’s health insurance while a brutal pandemic kills 70 million Americans. In reality, nearly 80k deaths have been linked to the virus across the US, with an overwhelming majority involving elderly patients and patients with co-morbidities.

The typo elicited a stream of hilarious replies.

We imagine Murphy’s staff will delete the tweet and issue a correction in the near future, if they haven’t already.

Murphy isn’t the first Democrat to exaggerate the pandemic’s death toll as the party embraces a position calling for lockdowns to be extended until more progress has been made on a vaccine or cure, even as initial data suggests that reopenings – at least in the West -are progressing mostly without incident, though there have been a few alarming reports.

We live through very unique times, not only because of the shock of the coronavirus that recently hit the world unexpectedly, but also because of large complex structural issues that have been building for decades.

A popular mantra says the stock market is not the economy and the economy is not the stock market referring to the often seen disconnect between market prices and events taking place in the economy.

The most recent example has been Wall Street rallying with each disastrous jobs report hitting the news wires. Even this last Friday markets rallied again unperturbed by the latest unemployment report showing the most severe collapse in employment in our recent history.

Depression like figures, yet the Nasdaq is green on the year, the S&P 500 largely off the lows with many again predicting new highs to come.

Why?

Because of unprecedented liquidity flooding markets as a result of monetary intervention making the disconnect between Wall Street and Main Street even wider.

We can pretend the stock market is not the economy, but there is no stock market without an economy yet we are witnessing an unprecedented disconnect between the two that has been building for years.

Can this disconnect be sustained? Are investors too optimistic about the current rally? What are the implications going forward?

These are complex issues everyone is confronted with and there are no easy answers. What an intellectually challenging and energizing time to be alive!

I am grappling with these issues as much as you are, we all are. And for that reason the idea for an ongoing webinar arose, to find a format to discuss these issues in more depth and make the debate more accessible and personal.

Hence I couldn’t be more pleased and honored to have found two people I greatly respect who are extremely well versed in markets and the macro market debate who share my passion for the issues at hand to join me for the debate: Guy Adami and Dan Nathan, both of CNBC Fast Money Fame.

As Guy Adami says all three of us have been trying to tell the truth in different ways for years. And that’s not an easy task for the truth is often unpopular or goes against the grain of a system that benefits from the truth being ignored.

So I invite you to join the three of us in this unscripted Zoom debate of what is hopefully the beginning of us discussing the issues we are all grappling with and we think matter to markets and you.

We hope you like it as much as we enjoyed recording it and please let us know what issues and topics are of interest to you for future episodes:

* * *

For a review of market technicals and chart discussion please see market videos. For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

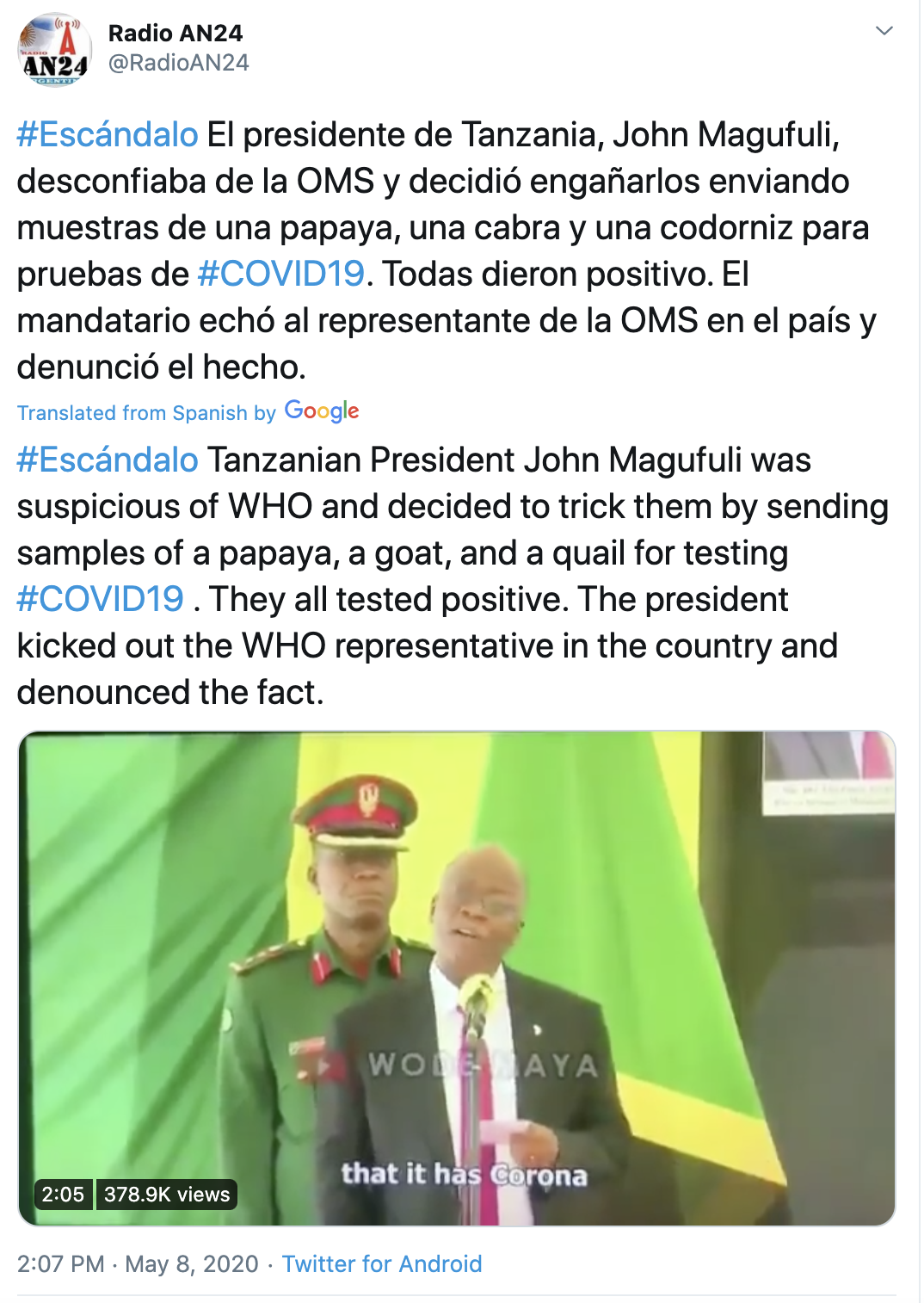

“We Sent Them Samples Of A Goat, A Papaya & A Pheasant”: Tanzanian President Catches WHO In Epic Lie

As the number of confirmed coronavirus cases explodes across Africa, the creeping involvement of the WHO has made some leaders suspicious of the NGO. Tanzanian President John Magufuli was growing suspicious of the organization, so he reportedly decided to investigate whether the organization was as trustworthy and reliable as it claimed to be.

He played what the local press described as “a trick” on the organization: He sent the WHO samples of a goat, a papaya and a quail for testing.

All three samples reportedly tested positive. When the president heard the news, he reportedly confronted the WHO, then kicked the organization out of the country. Though, to be sure, the WHO has yet to comment on the situation.

That would suggest one of two conclusions: either the strain of SARS-CoV-2 running amok in Tanzania is much, much more infectious than scientists understand, or the WHO has been reporting incorrect results either on purpose (as an attempt to bolster its credibility in the face of President Trump’s attacks) or via error (yet another indication that the WHO truly is “badly brokem” – as Vox described it back in 2015).

Most rational people would probably accept the latter scenario as the most accurate one.

Of course, Magufuli has garnered plenty of controversy himself over the past few weeks. He recently requested stockpiles of an ‘herbal tea’ that has been falsely branded as a COVID-19 cure, and has launched investigations impacting domestic labs and even frontline medical workers as he’s claimed the number of positive tests in his country is too high. The reality is that Tanzania doesn’t have much of a outbreak: It has recorded only 503 cases and 21 deaths. Though its mortality rate of 4% would suggest that the true number of cases likely numbers in the thousands.

Following the results, Magufuli fired the head of Tanzania’s national lab, sparking a political firestorm. Of course, though Magufuli has been criticized for trying to play down the impact of the virus, the government has so far refused to answer questions about where its test kits were manufactured, as Al Jazeera points out. On Thursday, the head of the Africa Center for Disease Control and Prevention rejected claims of faulty tests by Tanzania’s president.

The unreliability of COVID-19 tests manufactured in China has been a major problem for the US, and for Europe, as countries and states have been forced to discard PPE purchased in China – often after purchasing it at inflated prices – because only one-third of the masks actually work, and many of the tests have been found to produce positive and negative results more or less at random.

But we’d love to hear Bill Gates regale us with “data-based arguments” about why the WHO is indispensable to the international effort to combat the coronavirus.

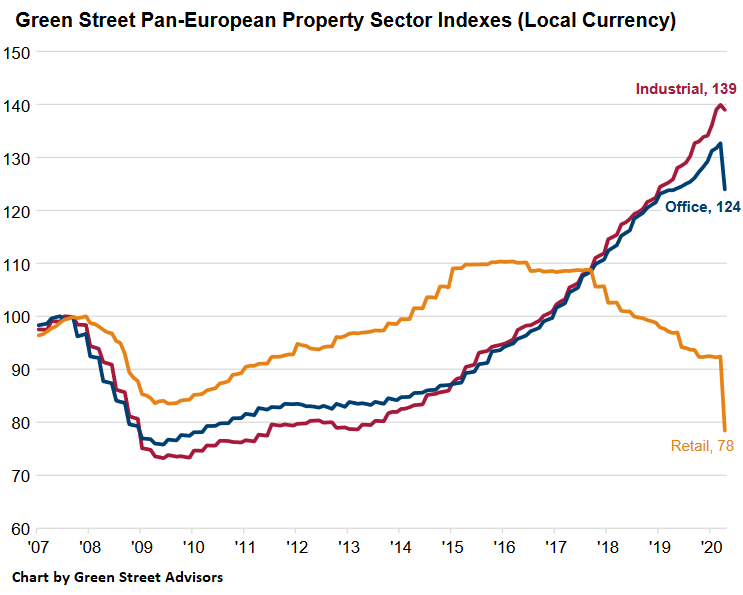

Over the past few years, the various sectors of commercial real estate have split into different trajectories, with some property types, such as industrial and office, rising to new highs, and with retail properties dropping further and further. Then came the issues surrounding Covid-19 and the lockdowns.

The trajectories suddenly turned into the same direction: down for all, but to different degrees, some sectors barely ticking down and other sectors dropping more sharply. And retail properties plunged.

Here is a first taste of the dynamics in Europe, where the lockdowns started earlier than in the US – in Italy, local lockdowns started on February 21, nearly a month before the first local lockdown in the US, the San Francisco Bay Area.

Retail properties have long been suffering from the structural shift of where retail spending takes place, the shift from brick-and-mortar stores to ecommerce. This shift had been relentlessly progressing over the years. But in March and April, it exploded higher as brick-and-mortar stores were shut down and ecommerce operations boomed.

Tenants of retail properties are now having trouble paying rent, or are unwilling to pay rent, as their stores are closed. Some of them will go out of business altogether; others will attempt to stay in business but renegotiate their leases. This whole dynamic has accelerated, as many future years of more or less gradual change are now being distilled into a few months. It has thrown the retail property sector into turmoil.

According to the Green Street Pan-European Commercial Property Price Index, which tracks prices of retail properties in the 25 most liquid real estate markets in Europe, all three sub-indices dropped in April, from March. But prices of retail properties plunged during the month:

Retail properties: -15.1%

Office properties: -6.6%

Industrial properties -0.7%,

“Wide bid-ask spread points to lower values” going forward, the report by Green Street Advisors notes.

The indices for office and industrial properties came off their all-time highs in March. But the all-time high of the retail index was the plateau period of mid-2015 to early 2016. Since then, the retail property index has plunged 29% (chart via Green Street Advisors, click to enlarge):

The report notes:

“The commercial real estate transaction market has largely come to a standstill as buyers and sellers adjust their underwriting expectations and try to agree on a fair price,” the Green Street report notes.

“During periods of wide bid-ask spreads, asset values often move closer to the bid than the ask. There is little to no investor demand in the retail sector and waning investor demand for sub-prime office buildings today.

“However, high-quality office and most industrial assets are still likely to trade at punchy capital values per square meter.”

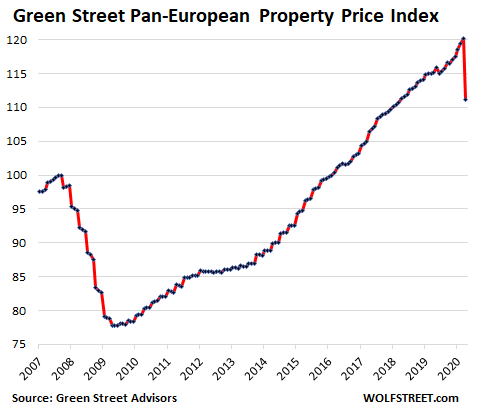

The overall Green Street Pan-European CPPI, which is an average of the retail, office, industrial sectors, dropped 7.5% in April from March and is down 3.4% over the past 12 months:

Each index was set at 100 for the month of its pre-Global-Financial-Crisis peak in 2007. According to Green Street, prices are tracked in local currency. The indices capture the prices at which commercial real estate transactions are currently being negotiated and contracted, which makes the index very timely.

Much like the retail sector of commercial real estate, the office sector also faces new structural challenges going forward as work-from-home strategies have been successfully rolled out during the pandemic, and companies and service providers now see that it is a functional and manageable alternative with high productivity for many jobs.

This too is playing out worldwide.

And this – much like the acceleration of ecommerce – is one of many structural shifts coming out of this crisis.