Watch Live: White House Task Force Holds Monday Briefing

With the chaos in the oil market Monday, we imagine President Trump will have something to say about the state of the economy and the US energy industry during tonight’s task force press briefing.

It’s slated to start at 5pmET…but we wouldn’t be surprised to see it start closer to 530…

From California to New Jersey, Americans are protesting in the streets. They are demanding an end to house arrest orders given by government officials over a virus outbreak that even according to the latest US government numbers will claim fewer lives than the seasonal flu outbreak of 2017-2018.

Across the US, millions of businesses have been shut down by “executive order” and the unemployment rate has skyrocketed to levels not seen since the Great Depression. Americans, who have seen their real wages decline thanks to Federal Reserve monetary malpractice, are finding themselves thrust into poverty and standing in breadlines. It is like a horror movie, but it’s real.

Last week the UN Secretary General warned that a global recession resulting from the worldwide coronavirus lockdown could cause “hundreds of thousands of additional child deaths per year.” As of this writing, less than 170,000 have been reported to have died from the coronavirus worldwide.

Many Americans have also died this past month because they were not able to get the medical care they needed. Cancer treatments have been indefinitely postponed. Life-saving surgeries have been put off to make room for coronavirus cases. Meanwhile hospitals are laying off thousands because the expected coronavirus cases have not come and the hospitals are partially empty.

What if the “cure” is worse than the disease?

Countries like Sweden that did not lock down their economy and place the population under house arrest are faring no worse than countries that did. Sweden’s deaths-per-million from coronavirus is lower than in many lockdown countries.

Likewise, US states that did not arrest citizens for merely walking on the beach are not doing worse than those that did. South Dakota governor Kristi Noem said last week, “we’ve been able to keep our businesses open and allow people to take on some personal responsibility.” South Dakota has recorded a total of seven coronavirus deaths.

Kentucky, a strict lockdown state, is five times more populated than South Dakota, yet it has some 20 times more coronavirus deaths. If lockdown and house arrest are the answer, shouldn’t those numbers be reversed, with South Dakota seeing mass death while Kentucky dodges the coronavirus bullet?

When Anthony Fauci first warned that two million would die, there was a race among federal, state, and local officials to see who could rip up the Constitution fastest. Then Fauci told us if we do what he says only a quarter of a million would die. They locked America down even harder. Then, with little more than a shrug of the shoulders, they announced that a maximum of 60,000 would die, but maybe less. That is certainly terrible, but it’s just a high-average flu season.

Imagine if we had used even a fraction of the resources spent to lock down the entire population and focused on providing assistance and protection to the most vulnerable – the elderly and those with serious medical conditions. We could have protected these people and still had an economy to go back to when the virus had run its course. And it wouldn’t have cost us six trillion dollars either.

Governments have no right or authority to tell us what business or other activity is “essential.” Only in totalitarian states does the government claim this authority. We should encourage all those who are standing up peacefully and demanding an accounting from their elected leaders. They should not be able to get away with this.

IBM Reports Lowest Revenue This Century And Grotesque EPS Fudge; Pulls Guidance But Keeps Dividend

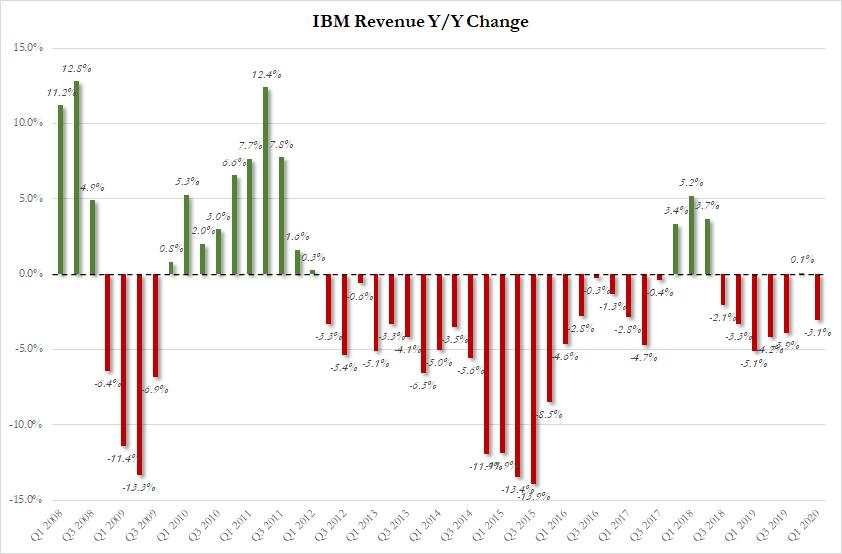

There was some hope last quarter that IBM was finally turning things around: after all, after 5 consecutive quarters of declining revenues, the company had just managed to grow its top-line for the first time since Q2 2018, and only for the 4th time in the past 8 years. Alas it was not meant to be, and moments ago IBM revealed that revenue once again declined in the first quarter, down 3.1%, amid the spread of COVID-19, even as Red Hat sales boosted its cloud business.

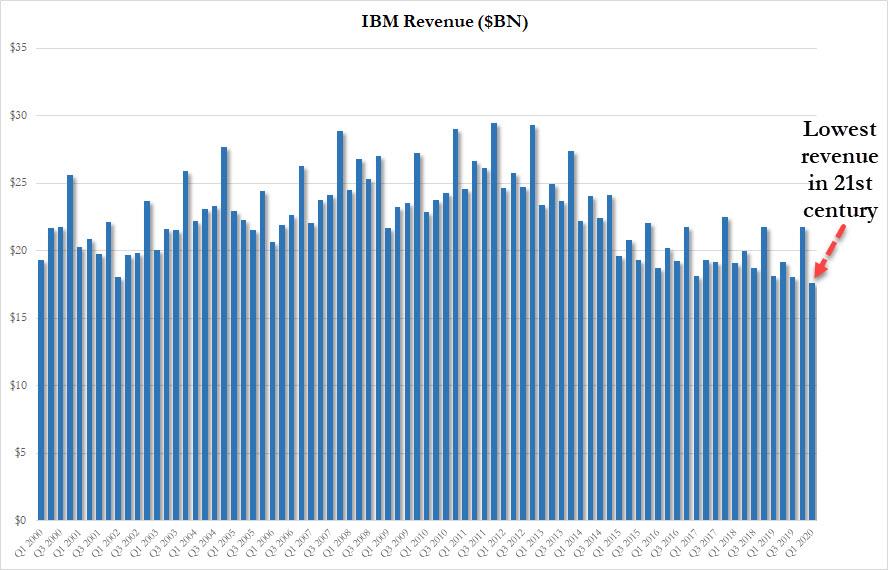

Then again “boosted” may be using the term loosely: at $17.6BN in total revenue, and missing consensus expectations of a $17.7BN print, IBM’s Q1 2020 was its worst quarter for sales this century.

Some more details:

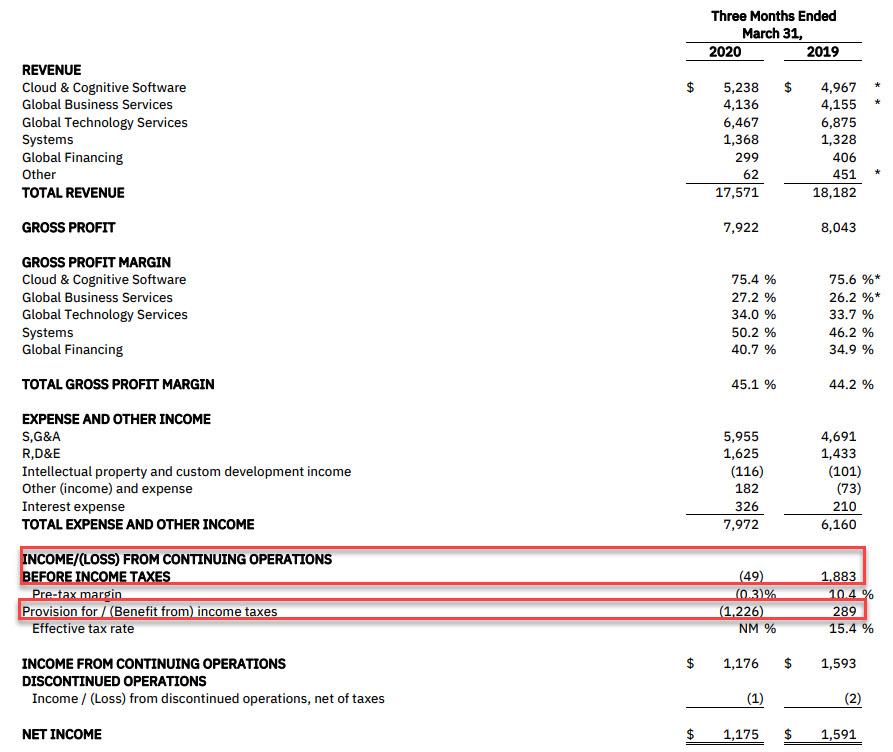

Cloud and cognitive software sales, which includes the recently acquired Red Hat, came in at $5.24 billion, missing analysts estimates of $5.3 billion.

Systems revenue, which includes mainframes, was $1.37 billion also missing the $1.42 billion consensus .

Global technology services revenue came in at $6.47 billion which completed the revenue miss trifecta (the Street expected $6.51 billion)

Global business services revenue was the only beat, coming in at $4.14 billion and above the $3.91 billion forecast.

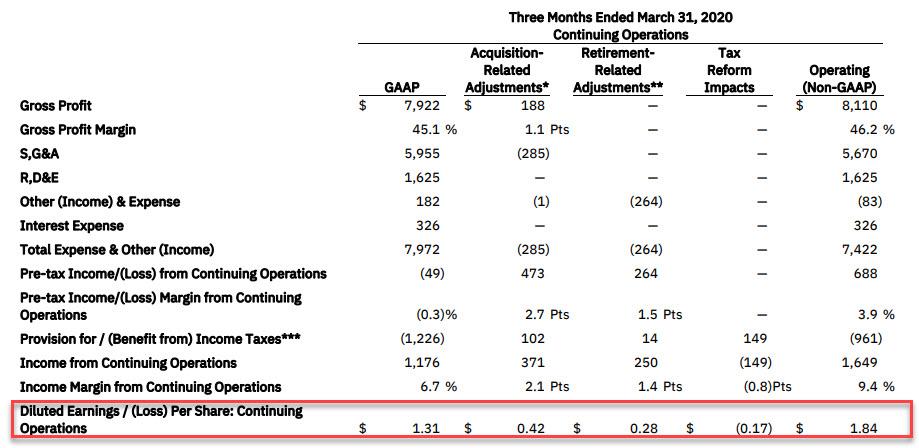

Hilariously, even with revenue missing and sliding, and the world around it burning, IBM still felt compelled to “beat” sellside EPS estimates which were $1.80, reporting $1.84 in adjusted EPS (down from $2.25 a year ago).

As usual, this number was total garbage for two reasons:

First, the unadjusted EPS was $1.31, or 40% below the adjusted number. The GAAP to non-GAAP bridge was, as usual, absolutely ridiculous and a continuation of an “one-time, non-recurring” addback trend that started so many years ago we can’t even remember when, but one thing is certain: none of IBM’s multiple-time, recurring charges are either one-time, or non-recurring.

Second, and as has become an IBM habit in recent years, the company’s entire net income was thanks to a tax benefit, because whereas per-tax net “income” was a loss of $49MM, the company added a $1.2BN benefit from taxes to get an after tax “Net Income” number of $1.175BN. The fudge was so grotesque, IBM was even embarrassed to point out what the effective tax rate was and simply said “Not Meaningful”, when it clearly is meaningful for anyone who believes foolishly that the company beat earnings.

Of course, none of this matters as the only thing investors care about is the future in a post-corona world, and here IBM had nothing to say, as it pulled its profit forecast for the year, signaling that the Covid-19 pandemic has become another hurdle for the company in its transition to cloud computing.

IBM is withdrawing its full-year 2020 guidance in light of the current COVID-19 crisis. The company will reassess this position based on the clarity of the macroeconomic recovery at the end of the second quarter.

As Bloomberg notes, IBM’s new CEO Arvind Krishna, who took the reins from Ginni Rometty earlier this month, has the challenge of leading the 108-year-old tech giant through the economic shocks stemming from the coronavirus. Many organizations have delayed major information technology purchases to avoid projects that are expensive, complex and sometimes disruptive to existing business processes. Even before the coronavirus emerged, IBM had struggled to increase sales on a consistent basis.

The company has been trying to boost its share of revenue from hybrid-cloud software and services, which lets customers store data in private servers and on multiple public clouds, including those of IBM rivals Amazon and Microsoft. IBM bought RedHat for a massively overvalued $34 billion in 2018 (the price represented more than 30x EBITDA) to boost this effort.

“IBM remains focused on helping our clients adapt to the immediate challenges of the Covid-19 pandemic, while we continue to enable them to shift their mission-critical workloads to hybrid cloud and expand their use of AI to help transform their operations,” Krishna said in the statement.

And while IBM has no idea what the future holds, it was confident enough to keep its dividend. In fact, in Q1 every dollar IBM made was returned to shareholders, to wit: “IBM’s free cash flow was $1.4 billion. The company returned $1.4 billion to shareholders in dividends.”

Here Is The Full Explanation Behind Today’s Unprecedented Negative Oil Price

Courtesy of IHSMarkit’s energy vice president Roger Diwan

How did you end up with negative oil prices today? This happens when a physical futures contract find no buyers close to or at expiry.

Let me explain what that means:

A physical contract such as the NYMEX WTI has a delivery point at Cushing, OK, & date, in this occurrence May. So people who hold the contract at the end of the trading window have to take physical delivery of the oil they bought on the futures market. This is very rare.

It means that in the last few days of the futures trading cycle, (which is tomorrow for this one) speculative or paper futures positions start rolling over to the next contract. This is normally a pretty undramatic affair.

What is happening today is trades or speculators who had bought the contract are finding themselves unable to resell it, and have no storage booked to get delivered the crude in Cushing, OK, where the delivery is specified in the contract.

This means that all the storage in Cushing is booked, and there is no price they can pay to store it, or they are totally inexperienced in this game and are caught holding a contract they did not understand the full physical aspect of as the time clock expires.

The contract roll and liquidity crunch that made the extreme sell-off today possible but it DOESN’T necessarily represent futures market conditions: NYMEX June settled today at $21.13.

The June contract is not out of the woods either: today’s action indicate that physical oil markets at Cushing are not in good shape and that storage is getting very full.

A decline of over 15% in the June contract price points to real worries that the physical stress will continue to reverberate, and will force a lot more production shutdowns during May than the ones announced so far.

So today negative prices are the reflection of dire market conditions for producers, with the hope that demand restart before the middle of May and that the June contract does not face the same fate.

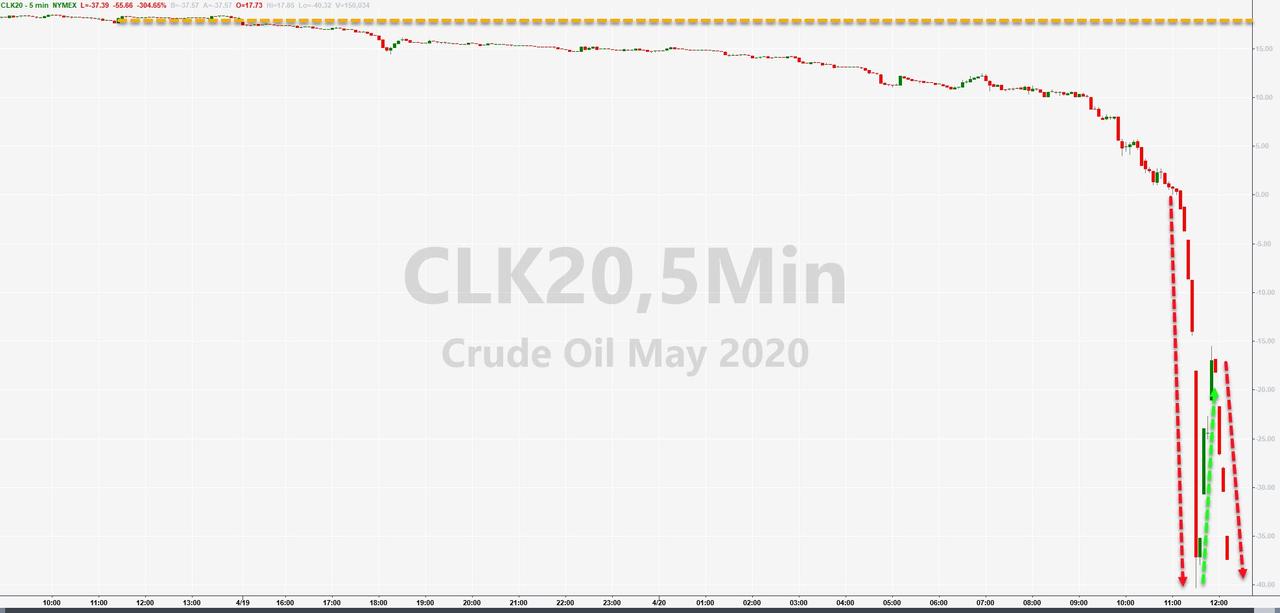

1) Front-month oil traded at an utterly irrational and unprecedented negative $43 intraday (this was not about storage into settlement, this was forced selling into settlement, then notice the bounce, and then later more selling.)

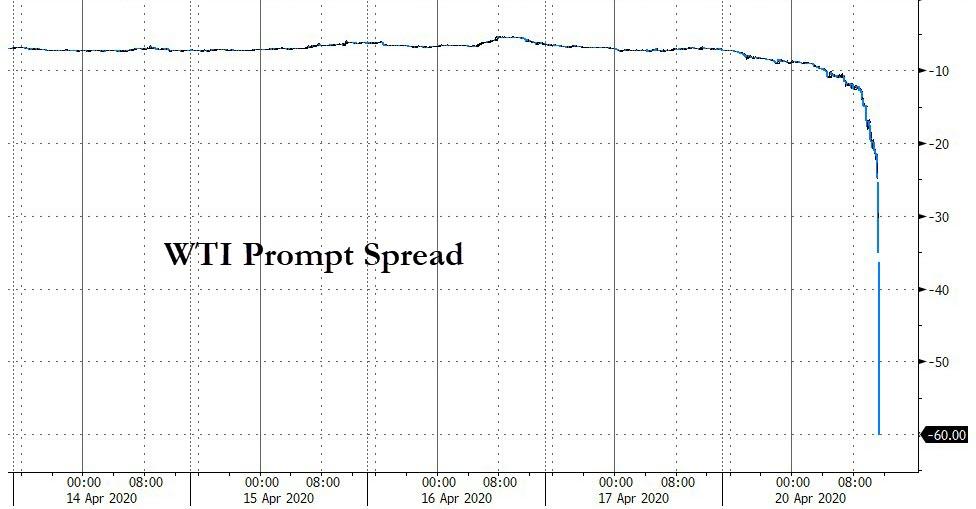

2) Oil’s prompt-spread exploded to a record negative $60 (smells like at least one fund was carried out on an arb)

Source: Bloomberg

3) Oil ‘VIX’ exploded today to record highs…

Source: Bloomberg

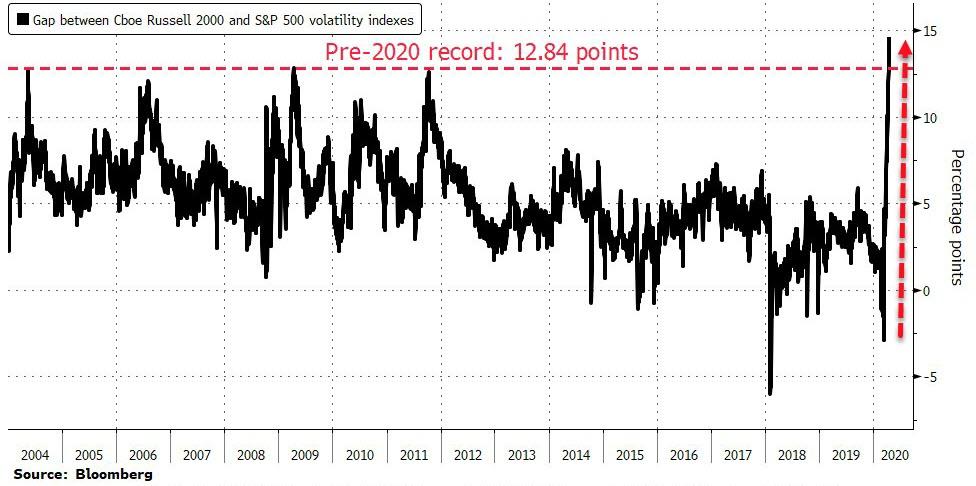

4) Russell 2000 ‘VIX’ has never been higher relative to Nasdaq ‘VIX’ than today (The widening gap reflects the damage being done to smaller companies by the coronavirus, Julian Emanuel, head of equity and derivatives strategy at BTIG LLC, wrote in a report.)…

Source: Bloomberg

5) A AAA CLO tranche failed its O/C test(this is a major liquidity problem – it means that a key pillar of the credit market will be crushed for years: CLOs have been the biggest buyers in the $1.2 trillion leveraged loan market, helping fuel a surge in debt-fueled buyouts and other transactions.)

6) Liquidity shortages reappeared as the 3m FRA-OIS Spread blew out once again… despite the massive injections of cash from The Fed…

Source: Bloomberg

7) US Macro-economic data crashed at a record pace back to the worst levels since the peak of the 2008 financial crisis…

Source: Bloomberg

* * *

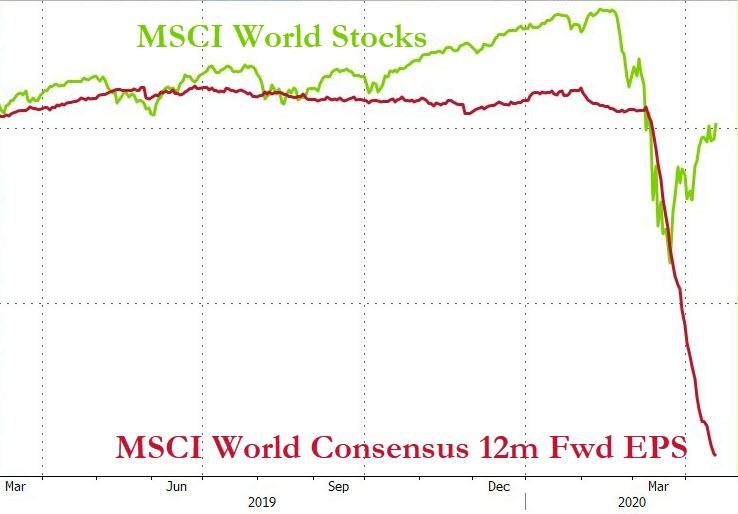

World stocks continue to make a mockery of every rational investor…

Source: Bloomberg

Chinese markets were a shitshow overnight when the CSI-300 Healthcare Index crashed 17% for no good reason, hung around there for hours and then spiked back to the green…

Source: Bloomberg

European stocks roundtripped from ugliness overnight to end mixed but all eyes were on Italian credit markets which were once again starting to signal redenomination risk…

Source: Bloomberg

US equity markets were in the red on the day with Nasdaq relatively outperforming once again and Trannies weakest (odd given the huuuge benefits from oil’s collapse)…NOTE the red rectangle shows the drop in all stocks as oil crashed into settlement…

Remember the last few minutes on Friday where The Dow shot up almost 400 points… well that’s all gone now…

The Dow was unable to hold above the 50% retrace level…

The dollar trod water today for a second day, ending slightly higher…

Source: Bloomberg

Cryptos had an ugly day today, erasing gains from the weekend…

Source: Bloomberg

Gold prices rallied on the day (spot and futures) and compressed the premium modestly…

Source: Bloomberg

Finally, the price of a barrel of oil has traded generally between 2.5oz and 5oz of silver for over 40 years… until today – using the June contract, it now costs just 1.3oz of silver to buy a barrel of oil – the cheapest ever.

With the global economy in freefall as worldwide COVID-19 cases surpass 2 million this week, officials in hard-hit countries are suggesting that so-called ‘immunity passports’ may be a path back to economic stability, according to France 24.

The way it would work is that those who have already had the disease would be assumed to be immune, and would be given permits to conduct their lives like they did before the pandemic.

Shortly after emerging from self-isolation after testing positive for Covid-19, the UK’s Health Secretary Matt Hancock announced in early April that the British government was considering an “immunity certificate” system to allow those who qualify to “get back as much as possible to normal life”.

Paris Mayor Anne Hidalgo has also given the idea her backing – putting it in a list of proposals for returning to business as usual in the City of Lights that she sent to the French government. On the other side of the Atlantic, Anthony Fauci, the director of the US National Institute of Allergy and Infectious Diseases, told CNN that immunity passports are “being discussed” in the Trump administration. “It might actually have some merit under some circumstances,” he added. –France 24

Thereare a few problems with this idea. For starters, nobody knows how long immunity lasts.

“At this point, the virus has been widely circulating in Europe and North America only for a couple of months, and so that is all the information we have – we will know in a year if immunity lasts a year; we will know in two years if immunity lasts two years,” said Abram Wagner, an assistant professor of epidemiology at the University of Michigan. “From past research into other coronaviruses, immunity was not long lasting, and I would not be surprised if, for most people, immunity lasted less than one year.“

Second, antibody tests are not ‘sufficiently accurate’ at this point, according to Georgetown University Center for Global Health Science and Security assistant professor Claire Standley, so added “we are still a long way off it being useful to test individuals with these methods.”

A major reason why such tests look likely to be ineffective, Standley explained, is that they do not seem specific enough to avoid mistaking a similar virus for Covid-19: “There may be cross-reactivity between the antibodies for SARS-CoV-2 [Covid-19] and other circulating coronaviruses – including those that cause common colds – meaning a positive result might not indicate past exposure to SARS-CoV-2 but maybe another coronavirus instead.”

Standley also warned that the tests can fail to detect those who have experienced a minor case of COVID-19, noting that “High false negative rates (lack of sensitivity) of the test mean that those currently available are not recommended for patient-level clinical diagnosis; unless the sensitivity improves, these tests may also not be effective in identifying people who have recovered from mild cases of Covid-19, and thus may have lower levels of antibodies in their blood.”

A third issue is concerns over the social implications of immunity passports.

“I suspect many people will be resentful if others were able to return to work and make money because they had an immunity passport,” said Standley, adding “I have grave concerns about how these types of schemes could be implemented equitably and fairly, even assuming a reliable antibody test were available, and more known about the length of immunity and how protective it is.”

“If the tests need to be purchased, this could further exacerbate disparities between those who can afford the tests (and who may already have been able to work from home/maintain an income during lockdown) versus those who cannot, and thus would be further barred from re-entering the workforce.,” added Standley.

Lastly, Standley suggested that immunity passports would create a perverse incentive to contract the disease.

“In an effort to return to work, or allow their children back to school, will the promise of an immunity passport make people behave less responsibly, and risk infection, in order to end up with a positive antibody test?” Therefore “The scheme would potentially punish those citizens who have behaved responsibly and tried their best to reduce their own risk of exposure and that of transmission within their communities.“

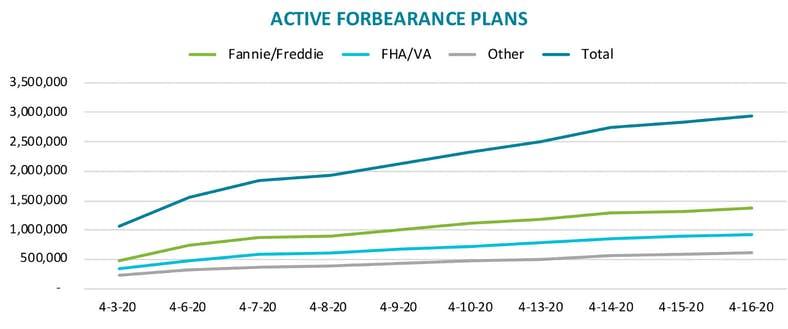

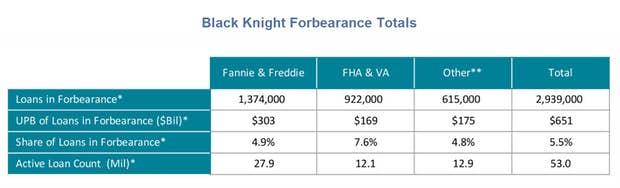

As of April 16, more than 2.9 million homeowners – or 5.5% of all mortgages – have entered into COVID-19 mortgage forbearance plans

This population represents $651 billion in unpaid principal and includes 4.9% of all GSE-backed loans and 7.6% of FHA/VA loans

At today’s level, mortgage servicers would be bound to advance $2.3 billion of principal and interest payments per month to holders of government-backed mortgage securities on COVID-19-related forbearances

Another $1.1 billion per month in lost funds will be faced by those with portfolio-held or privately securitized mortgages

Forbearance Totals

Payment Forbearance Under Cares Act

On March 27, 2020, President Donald Trump signed the Coronavirus Aid, Relief, and Economic Security Act (also known as the CARES Act) into law. A provision of the CARES Act allows borrowers with federally backed mortgages to request temporary loan forbearance for up to 180 days. Borrowers also have the right to apply for an extension of another 180 days of forbearance.

Once a borrower requests hardship forbearance due to the COVID-19 pandemic, the act requires the servicer to offer a CARES Act forbearance.

John Ulzheimer, an Atlanta-based credit expert formerly of FICO and Equifax, warns of a potential balloon payment.

“If the lender or servicer demands that you pay back the deferred amount all at once or in an otherwise expedited manner, that could be impossible for the borrower.”

Unfortunately, having a mortgage servicer ask for a “balloon” payment once your forbearance period ends is a very real possibility. Borrowers from multiple national banks have reportedly been informed of the need to repay any delayed payments in a lump sum at a future date.

Three Things Not to Do

Don’t apply for forbearance if you don’t need to.

Make sure you understand the terms being offered. A huge balloon payment at the end could do you in.

Don’t pay your mortgage with a credit card. The interest rates are outrageous.

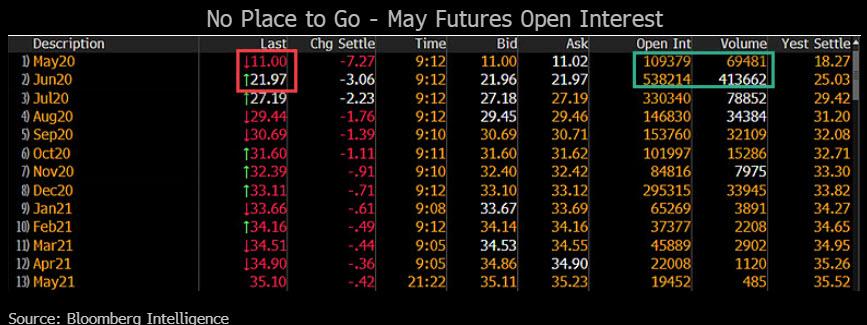

Here’s The Next Problem: Where Do 100 Million Oil Barrels Get Delivered… And What Happens Next Month?

The entire financial world is watching in stunned amazement as the May WTI contract crashed as low as -$40, an unprecedented – until today – event, and one which is sparking frenzied speculation who will be oil’s “Amaranth”, the nat-gas trader which remains the best example of how futures-spread positions can go wrong.

But sooner or later, investors will ask themselves the next question: where will roughly 100 million barrels of oil be delivered. That is roughly the equivalent of the outstanding May WTI open interest of some 109 thousand contracts.

As Bloomberg’s Mike McGlone writes, “the greater-than-normal level of open interest in May futures has no place to go but is likely to mark an extreme, if history is a guide.”

As of April 17, there were over 100,000 open positions in the May contract, well above the five-year average of about 60,000. What is more striking is that while the May position stops trading at 230pm tomorrow, April 21, only about 2,000 contracts are usually delivered. This time we are looking at 100,000 contracts, or about 100 million barrels of oil. The question, of course, is where does all this oil get delivered in a world where commercial storage is expected to run out as soon as next month?

And let’s say the May contract somehow finds enough space – this brings up the June contract, which is trading at around $21.51 because somehow traders believe that some magical solution will present itself in the next 4 weeks (spoiler alert: it won’t). The open interest for June is 538K contract, or the equivalent of over half a billion barrels of. While much of this will be rolled up the contago-ing curve, this still means that the world is looking at hundreds of thousands of oil barrels to be delivered next month, and the question again: where will all this oil be delivered, and what happens to the price of WTI next month?

And what about July… and August… And September? As prominent squawker Yogi Chan put it best, “Back of the fag box: Take all WTI contracts from May 2020 through to Dec 2021 (covers 93% of all OI). Average price weighted by open interest? $43.48/bbl” (editor’s note: in the UK “fag” means cigarette)

Back of the fag box: Take all WTI contracts from May 2020 through to Dec 2021 (covers 93% of all OI). Average price weighted by open interest? $43.48/bbl #oott

The unfortunate answer: oil producers will have to eat the billions of dollars in foregone production even as they shut down and keep oil in the ground, suffering unprecedented losses by “selling” oil at negative prices.

To be sure, some had creative solutions, such as airplane guru and Editor in chief of the Air Current, Jon Ostrower:

I mean it’s no better or worse than handing every adult $1,200 one time.

Which brings us to the tragic, if accurate, conclusion from the FT’s energy director: “this is a colossal economic tragedy in the making right now.”

This crash is going to destroy so many livelihoods and so many jobs. Whatever anyone thinks about the oil sector — and there many obvious reasons why the world needs to reduce oil use — this is a colossal economic tragedy in the making right now. #oott

These are strange days, indeed. But in what alternative universe can anyone imagine Joe Biden actually making it through a presidential election campaign? The party he supposedly leads stuffed him into a broom closet last week after he gibbered through a session with CNN’s leading light Anderson Cooper. They can’t just hide the poor fellow there until November 3.

Asked about reopening everyday life in America, Mr. Biden said, “You know, there’s a… uh, during World War II, uh… you know, where Roosevelt came up with… a thing, uh, that, uh… you know, was totally different than a… than the… the, it’s called… he called it the… you know, the World War II… he had the war… the War Production Board….”

Everybody knows he’s dimmer than a night-lite, and everybody’s pretending it’s okay. There’s no analog in history for any faction putting up such an empty vessel for high office. Granted, the Democratic Party has trafficked in unreality for years, from Crossfire Hurricane through UkraineGate — with side-trips like trannies in women’s sports — but those capers were just old-fashioned scams. Joe Biden for President is Emperor’s-New-Clothes caliber deceit, requiring a rank-and-file so marinated in falsehood they couldn’t tell you the difference between a red light and a green light.

So, you have to ask: what is their game? In the weeks that led up to the blossoming of Covid 19, the game was apparently to bump off Bernie Sanders to satisfy the party’s corporate sponsors, who were not so eager to back someone that promised to confiscate their wealth. Ironically, Covid 19 only fortified Bernie’s case that the nation’s obscenely crooked health care system demands drastic reform. Now, you could easily construct a scenario in which ol’ Bernie would have glided to victory in November on the basis of that, combined with unemployment figures that make the Great Depression look like a job fair.

Picking Joe Biden as the instrument to block Bernie seemed especially dumb just weeks after the Democrat’s impeachment gambit blew up in their faces by shining a fiercely revealing light on Joe and Hunter’s adventures in international grift. One can easily discern Mr. Biden’s motive for remaining in the race after that because sheltering in candidacy seemed to inoculate him from any criminal investigation. But, did the whole party want to go all-in on that?

Maybe so, because the doings in Ukraine circa 2014 included a large cast of characters in Barack Obama’s state department – not least, Secretary of State John Kerry – plus the entire George Soros network of international backstage finaglers, with tendrils to Jeffrey Epstein’s nefarious operations – in short, a can of worms so slithery and disgusting they make the Democratic Party look like a primordial sink of species dumped into Mother Nature’s discontinued merchandise bin. Note: none of that has been adjudicated yet and don’t assume they’ll get off scot-free.

Then there is the sexual molestation charge against Mr. Biden by ex-staffer Tara Reade, who claims the then-Senator violated her manually in 1993. The New York Times editors sang la-la-la-la-la-la-kittens-and-puppies for two weeks before they even acknowledged the accusation, only to dismiss it because, well, it was like… you know, where Roosevelt came up with… a thing, uh, that, uh… you know, was totally different than a….

There really are only two plausible game plans for the Dems with Joe Biden.

One is that he’s a mere placeholder until the convention – assuming it can even be held — where party bigwigs are forced to un-do their Biden blunder by some legerdemain of rules-fudging, and cram in a last-minute replacement. The putative savior would be none other than She-Whose-Turn-Was-Thwarted in 2016, on the grounds that she at least knows how to run for president, even if she isn’t very good at it. They might as well hand every delegate a dixie-cup of cyanide-enhanced kool-aid as they cast that fateful vote.

The other pretty obvious scheme, seemingly underway now, is to fix up Mr. Biden with a running-mate who can take over his duties twenty-three minutes after the inauguration ceremony. Stacey Abrams, the self-proclaimed “real governor of Georgia” who, in fact, lost that election but has made out nicely hustling her delusions, is campaigning arduously for the VP appointment. Wouldn’t that make a heck of an appealing ticket?

Apparently, that’s one more memo the Democratic Party did not get: America no longer has time for identity politics. There are more important things to attend to, like whether large numbers of people go to bed hungry, get cast out of their homes, live or die. Things like that. For the moment, the USA doesn’t have an economy. Nor does much of the rest of the world. Believe me, that’s a problem. And unlike Mr. Biden’s dementia, there’s no pretense about not noticing it.

Something Impossible Just Happened: A CLO Just Failed Its AAA Overcollateralization Test

Over the weekend, we reported that in its quest to bailout the richest Americans and the country’s financial system, the Fed unleashed an unprecedented array of actions meant to backstop capital markets, going so far as buying investment grade, high yield bonds and even AAA-rated CLO bonds.

However, as we warned, it won’t be enough, for two reasons: first, recall that the expanded Term Asset-Backed Securities Loan Facility (TALF) announced by the Fed last Thursday only buys AAA-rated bonds of CLOs, which after the coming tsunami of CLO downgrades is complete, will not only collapse in nominal size but will mean that any further attempts to stabilize the CLO space will require yet another Fed backstop of even riskier – i.e., rated AA and lower – structured products.

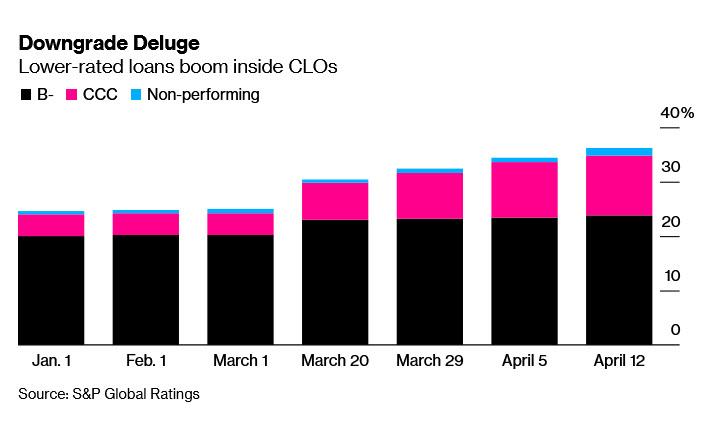

The second reason – one which Bloomberg called a “bigger and more ominous force at work that has investors bracing for the kind of pain they’ve never experienced in the decades that the [CLO] market has existed” – is that late on Friday, in the most draconian and widespread ratings action since the financial crisis, Moody’s warned it may cut the ratings on $22 billion of U.S. collateralized loan obligations – a fifth of all such bonds it grades – as a result of the collapse in cash flows due to the Covid-19 pandemic.

The ratings agency took action on 859 bonds from 358 CLOs that package leveraged loans into securities of varying degrees of risk and return. The step – which according to Bloomberg affects about 19% of Moody’s-rated CLOs that purchase broadly syndicated loans – comes as the underlying debt gets downgraded at a record pace.

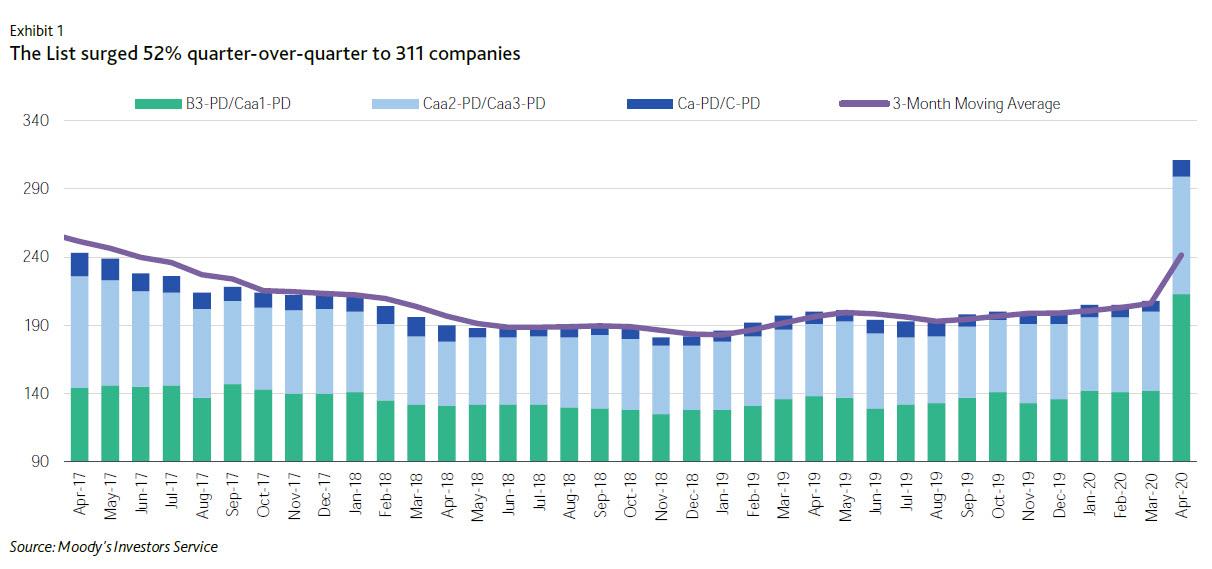

The action followed a report by Moodys earlier in the week in which it reported that its “B3 Negative and lower list” soared to its highest tally ever — 311 companies. That tops a former peak of 291 companies, reached during the credit crisis of 2009 and the commodity-related downturn in April 2016. At 20.7% of the total rated spec-grade population, the list also shot up above its long-term average of 14.8%, and closing in on its all-time high of 26.1%. This spike is the result of the confluence of a coronavirus outbreak, plunging oil prices, and mounting recessionary conditions, which created severe and extensive credit shocks across many sectors, regions and markets, the effects of which are unprecedented.

And with the underlying bonds set to suffer an unprecedented collapse in solvency, it is only a matter of time before the products where they are packaged are also hammered. Products such as CLOs.

Today, picking up on this growing risk of widespread impairments across the CLO deal stack, Bloomberg echoes what we said, namely that credit ratings on risky corporate loans that were stuffed into the CLOs “are being downgraded at a pace so frenetic that it threatens to overwhelm safeguards that were put in place to ensure the securities’ financial strength.”

And “if that happens” Bloomberg continues, “the firms that manage the CLOs will be forced to dump under-performing debt at fire-sale prices or suspend the cash payments they hand over to their investors.”

It just happened.

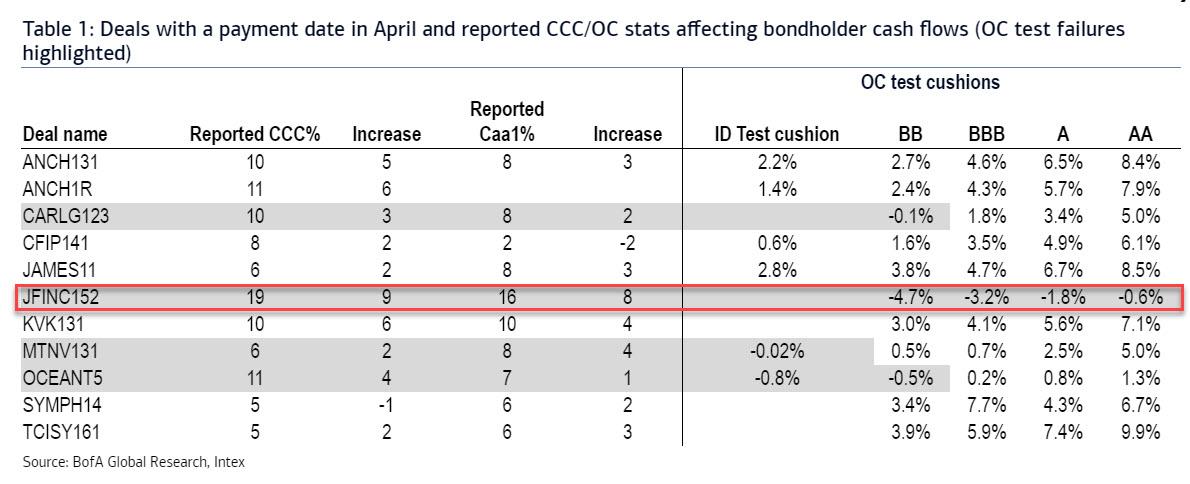

In yet another case of something that was previously deemed impossible becoming reality thanks to the Coronavirus depression – like oil trading at a negative $14 per barrel – Bank of America’s Chris Flanagan writes that with some deals already reporting late March/early April data, we find that some deals are failing, not just the junior overcollateralization (OC) test but in one case, even the AAA/AA OC test!

According to Flanagan, this will be the likely be the first “CLO 2.0” deal failing the senior most OC test; as a reminder, not even during the financial crisis were the supersafe AAA tranches impaired. This time it took just a few weeks for the cash flow collapse to impair the very top of the stack!

The CLO deal in question is JFINC152, where downgrades have sent the reported CCC percentage to 19%, up 9%, and the result is that every single test cushion is now showing impaired results, from BB (-4.7%) all the way to AA (-0.6%).

Those seeking the reason for this unprecedented development will find it in the dramatic deterioration of CLO credit ratings: for the deals that failed any one of the tests, the increase in CCC is almost 2x over the past month, BofA notes adding that the lack of reinvestment flexibility for some of the transactions as the deals were post the RP period implied managers could not take advantage of the volatile loan market condition in March.

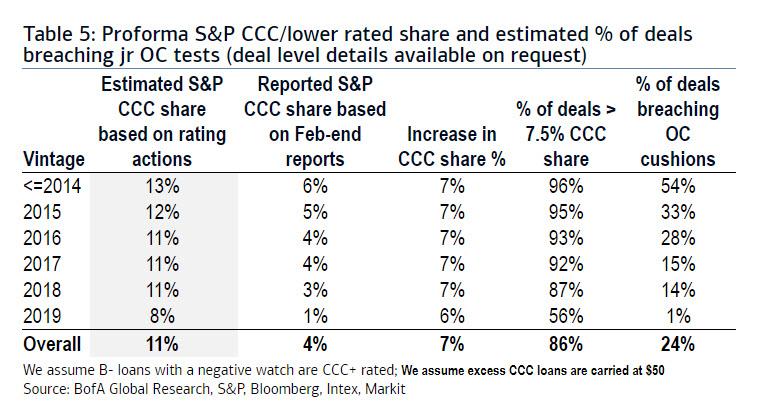

Looking at the past month, since March, S&P and Fitch have placed around 100 tranches on negative watch. The vast majority of these deals were initially rated BB/B and there are 8 IG-rated tranches (mostly BBB). BBB bonds continue to face a high risk of downgrade in the near term considering the increasing CCC share and the recent uptick in defaults. According to an analysis by S&P, should CCC’s increase to 18%, defaults to 5% and OC declines of 2pts, around 46% of BBB bonds could be downgraded to Non-IG.

This has important ramifications for both bondholders and investors as many deal documents initiate a restricted trading condition if any IG-rated bond is downgraded. This will further limit manager’s ability to trade in/out of loans.

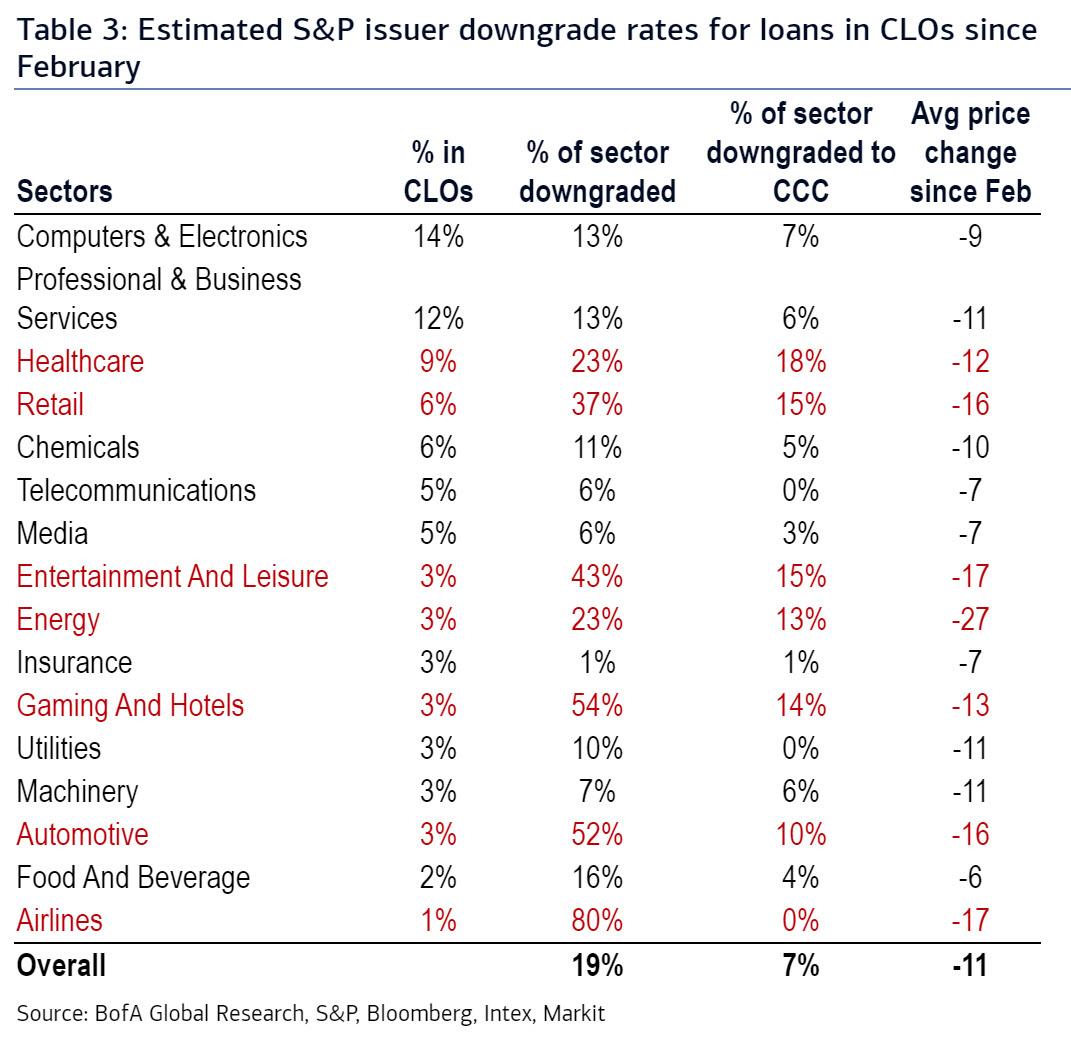

Additionally, the surging share of CCC downgrades has caused many deals to have lower OC ratios as a result of CCC excess and/or par burn as managers traded out of lower priced/lower rated loans. BofA currently estimates that around 17-19% (and counting) of loans in CLOs have been downgraded by both Moody’s and S&P since February, and many more downgrades are coming. Currently, the share of CCC+/lower rated issuers is estimated to be 10.5% and the share of Caa1/lower rated loans is estimated to be around 8.5% across CLO portfolios (assuming loans with a negative watch have been downgraded by a notch lower).

BofA also highlights the average price across each rating cohort currently (after adjusting for downgrades). There has been an increased dispersion between high/low quality names with B+/BB issuers trading around $90 and CCC issuers, around $60. As a result, to swap from a CCC name into a B or higher rated asset still implies taking a $25 hit to par.

Next, looking at updated CCC concentrations, BofA estimates that as many as 20-30% of deals are now potentially breaching their OC tests (assuming a $40-50 price for excess CCC assets and based off March portfolios). In some cases, the BB bonds may PIK as well. With April determination dates beginning and around the corner, managers have very less room/time to trade out of loans and cure these breaches.

Looking ahead, BofA thinks further OC breaches are likely to occur as more deals that make their payment in April report. With the estimated CCC share reaching 10.5%, roughly 20-30% of deals could breach their junior OC tests, and increasingly more deals will likely impair the AAA tranche as well – that’s where Japanese pensioners’ money is currently allocated – an outcome that until just a few weeks ago was inconceivable.

* * *

With the safest tranches facing impairments, the riskiest – or equity – tranches are set for a historic wipeout. According to Bloomberg, analysts expect as many as one in three CLOs may soon have to limit payouts to holders of the equity portion.

The loan downgrades have come so fast that Stephen Ketchum of Sound Point Capital Management compared it to a spill “at the Daytona 500, where the cars are crashing into each other.” It’s a lot different, he said, than the 2008 financial crisis, which “was a slow-moving train wreck.”

Another major difference between the financial crisis and now is that back in 2008, the CLO market emerged largely unscathed – especially the AAA tranches – an outcome which we now know will not happen. Corporate loans were far enough removed from the epicenter of the 2008 crisis – a housing bubble – to avoid much of the collateral damage and, besides, the CLO market back then was a fraction of its size today.

Ironically, the strong track record, the lack of major CLO impairments, along with the fact that the securities provided juicy returns in an era of near-zero global rates; fueled a boom in demand over the past decade. The same boom will now lead to hundreds of billions in losses.

Worse, it means that a key pillar of the credit market will be crushed for years: CLOs have been the biggest buyers in the $1.2 trillion leveraged loan market, helping fuel a surge in debt-fueled buyouts and other transactions.

In sympathy with the broader market, prices on CLOs have recovered some in recent days with AAA securities recouping most of their declines since the selloff began largely thanks to the Fed’s promise to backstop the supersafe tranche. However, as cash flows plunge and as a flood of downgrades hit the underlying loans which then leads to even more AAA tests being missed, the entire CLO space is in for a very violent repricing and unless the Fed is prepared to backstop the entire $1.2 trillion market, the consequences – for both the loan and broader bond market – will be catastrophic, while the Fed ends up holding paper that in a few months will be insolvent, at which point the Congressional hearings why Powell bought worthless securities with freshly printed dollars will be the hottest thing on TV.

{kind=link}