Dr. Fauci Given Security Detail After Receiving Unspecified ‘Threats’

It sounds almost unimaginable that anybody in the country right now would wish harm on sweet, innocent Dr. Anthony Fauci, the gifted doctor whose pioneering work on HIV and AIDS has been credited with saving millions of lives, and whose work leading the federal COVID-19 response has been lauded as a “port in the storm” for millions of terrified Americans.

And yet, somebody somewhere apparently does.

The Hill reports that Dr. Fauci has been given a security detail after receiving threats, according to an anonymous “person familiar with the matter.”

Before taking his job as a top figure on the White House federal task force leading the government’s effort to suppress the outbreak, Dr. Fauci was the director of the National Institute of Allergy and Infectious Diseases, a position he has held since 1984.

Dr. Fauci

The doctor’s absence from two White House press briefings last week sparked rumors that Trump was sidelining him after he had “contradicted” the president (something the president has said he encourages his ‘expert’ advisors to do), and the PR hit was apparently enough of a concern that the doctor was swiftly returned to the lineup.

Asked whether he had been given security protection, Dr. Fauci refused to respond at Wednesday night’s briefing. But President Trump interjected, saying “everybody loves” Dr. Fauci, while noting that the good doctor was a formidable basketball player during his younger days.

“He doesn’t need security. Everybody loves him,” Trump said. “Besides that, they’d be in big trouble if they ever attacked him.”

Certainly, an attack on Fauci at such a sensitive time would garner very little sympathy, though there are some conservatives who have blamed the doctor for allegedly trying to undermine President Trump. As the Hill noted, Bill Mitchell and Tom Fitton are among those who have tweeted criticisms of Dr. Fauci recently. However, the motivations of those issuing the threats remain unclear, along with their identities.

COVID-19 ‘Miracle Drug’ Goes On FDA Shortage List After Study Confirms Efficacy

Days after the FDA approved the use of hydrochloroquine as a treatment for COVID-19, weekly prescriptions soard from 100k to 300k in one week.

Compounding the issue is a study, which shows that the commonly used treatment for lupus, arthritis and other disorders which was touted by President Trump has proven to be effective in a small study reported by The New York Times. As such, the drug has been placed on the FDA’s list of shortages – leaving those with the aforementioned afflictions at risk of not being able to refill their prescriptions, according to Bloomberg.

The news comes after Novartis AG’s Sandoz donated over 30 million doses of hydroxychloroquine, while Bayer AG donated 1 million doses of chloroquine to the national stockpile.

While we are still waiting on the results from clinical studies, compelling anecdotal evidence of the drug’s efficacy when combined with azithromycin (Z-Pac) and zinc sulfate has caused several countries to place them on their recommended treatment regemin for the disease.

Some of the nine companies on the FDA’s list that make hydroxychloroquine, including generic-drug giant Teva Pharmaceutical Industries Ltd., said there is a limited supply that is subject to allocation. 4

Others said the drug is available, particularly for existing customers. Increasingly larger shipments of chloroquine are scheduled over the next eight months, according to Natco Pharma Ltd., whose chloroquine is distributed by Rising Pharmaceuticals Inc. -Bloomberg

“The agency is working with manufacturers to assess their supplies and is actively evaluating market demand for patients dependent on hydroxychloroquine and chloroquine for treatment of malaria, lupus and rheumatoid arthritis,” the FDA said in a Tuesday evening statement, adding that all manufacturers are ramping up production.

Is Italy’s COVID-19 Mortality Rate Even Worse Than Officials Are Letting On?

As US intelligence agencies dispute China’s surprisingly low mortality stats, and as researchers ponder what’s causing Italy’s outrageous 10%+ mortality rate, one thing is indisputable: mortality rates are climbing even as the number of cases being reported in places like Italy are tapering off. And that is freaking out scientists, who are scrambling to find a cure.

As analysts at Commodore Research pointed out, the issue is not unique to Italy: Virtually every nation that has a large number of reported cases has continued to see mortality rates climb. In Spain, the mortality rate now stands at 8.7%. Ten days ago, it stood at 5.4%. In the Netherlands, the mortality rate stands at 8.3%. Ten days ago, it stood at 3.8%. In the United Kingdom, the mortality rate stands at 7.1%. Ten days ago, it stood at 4.6%. In France, the mortality rate stands at 6.7%. Ten days ago, it stood at 3.9%. In Belgium, the mortality rate stands at 5.5%. Ten days ago, it stood at 2.4%.

Even nations where the mortality rate has been relatively low have seen the rate climb: In Portugal, the mortality rate now stands at 2.2%. Ten days ago, it stood at 0.9%. In the US, the mortality rate stands at 2%, 10 days ago, it stood at 1.2%. In South Korea, the mortality rate stands at 1.7%. Ten days ago, it stood at 1.2%. In Austria, the mortality stands at 1.3%. Ten days ago, it stood at 0.4%. In Germany, the mortality rate stands at 1%. Ten days ago, it stood at 0.4%.

Italy’s more detailed breakdown of virus-related data and other mortality statistics have showed that virus-related deaths in Milan and the surrounding area, which has a population of 10 million, has caused the mortality rate to double from normal times.

According to AFP, the region registered 12,399 COVID-19 related deaths last month, thousands more than officially reported by any other country. Meanwhile, last Friday, the civil protection service disclosed a record 969 deaths.

Some have speculated that the death toll in Italy simply doesn’t add up, suggesting that Italy’s 10% reported death toll might be too low.

It might sound hard to believe, but AFP reports that by comparing data from 2018, its journalists determined that the average monthly deaths from 2018 in the same region was 8,300, and that March 2018 was likely a “statistically average” month. However, the city reported 7,176 coronavirus deaths in March, which is 15% below the average in normal times. Some say that this suggests local officials are deliberately misreporting the numbers.

Even some public officials are suspicious. Bergamo Mayor Giorgio Gori said Wednesday he does not trust the official figures and thinks the real toll for the region may be twice as high. The mayor tweeted a newspaper analysis suggesting that the COVID-19 toll in the Bergamo province was “between 4,500 and 5,000, and not the 2,060” officially reported.

One expert in Italy said that the data suggest Italy’s crisis has peaked, but that the peak in hospital deaths will arrive shortly, per the Hill.

“The data suggest that the increase in numbers of patients in intensive care in both the Lombardy region and Italy as a whole are likely to have peaked,” the report said.

But “”he numbers of deaths in hospital will continue to increase at the maximum rate for several days to come.”

To be sure, one new report published in the Lancet suggested that mortality rates might be smaller than initially suspected.

The study, published Monday in The Lancet Infectious Diseases medical journal, estimated that about 0.66% of patients who become infected with the virus will die. Previously, when undetected infections weren’t being taken into account, researchers found the coronavirus death rate was 1.38%. That’s still significantly deadlier than the seasonal flu.

“I’ve Never Seen Anything Like This”: Small Businesses Beg For ‘Speedy’ Stimulus Delivery

“I have never seen anything like this in my lifetime,” one small business owner was cited in Reuters as saying. The real question now is how long can small and family businesses — which account for some half of all US employment and are fast blowing through whatever cash remains (many say they’re good for no more than two weeks)— wait till they actually feel the effects of the $2 trillion stimulus package? After all it could take weeks to process checks and get loans out, and yet April remains essentially “cancelled”.

“Without something we wouldn’t be able to keep our employees,” another business owner with just five employees said. “My biggest goal is to keep them and of course make sure there’s a business for them to come back and work for.”

Congress’ $2 trillion includes $349 billion meant to rescue small firms through the Payroll Protection Program, intended for businesses to cover eight weeks of payroll and basic operating expenses via a forgivable loan of up to $10 million, which companies of up to 500 employees or fewer can access, available through June.

Via ABC News

This as 50,000 retail stores have already shuttered in just over a week nationwide with no clear re-opening date, resulting in over 600,000 workers on furlough, based on Bloomberg data — also as new soaring unemployment numbers come out weekly, with last week the Labor Department reporting a record 3.3 million people filing unemployment insurance claims in the week prior.

“Speed is the operative word,” spokesman for the specific Treasury Dept. agency (the Small Business Administration, SBA) which is to oversee getting the funds to businesses, Jovita Carranza, said. And CEO of the Bank Policy Institute, Greg Baer, pointed out that “This is the kind of program that in ordinary times would take a year to get started.”

Indeed as details and crucial processing elements on the rollout continue to come into focus, investors will remain wary of bottlenecks which would detract from the economic upside, given that ensuring as many firms as possible remain operating in the wake of the outbreak is vital to preserving as much of the previously robust employment market as possible.

We noted last week that now with the stimulus passed into law, it’s precisely this next hurdle of speed and timeliness which will be as great (if not greater) than the first and presents a significant degree of execution risk.There are several aspects of the proposed stimulus measures which have well-established distribution channels; unemployment benefits and the injection of cash directly to households. As for the corporate, small business, and state/local government allocations, this leg of the process presents a greater challenge.

“There’s a fair amount of money,” Yale University finance professor Andrew Metrick told Bloomberg this week:

“But ultimately we have capacity problems getting the money into the hands of the small businesses fast enough, without fraud or bad actors effectively figuring out how to siphon money off.”

Via National Restaurant Association

And Reuters adds further on the question of timing: “Banks have been telling customers to be patient and asking them to get relevant paperwork ready so that loans are processed quickly when it all comes together. Some expect cash to begin moving as soon as Friday.”

In short, there’s the classic question of speed vs. qualitative oversight.Either the government gives everyone what they want without checking — leaving the potential to unleash unprecedented fraud — or they do a meticulous check of everything and businesses fail during the long wait in limbo.

The White House is dispatching staff to the Small Business Administration as that agency struggles with a flood of requests for financial aid, according to people familiar with the matter. So many people tried to access one SBA loan program last week that the agency’s website failed repeatedly.

Mnuchin has vowed to have the small business loan program “up and running” by the end of the week.

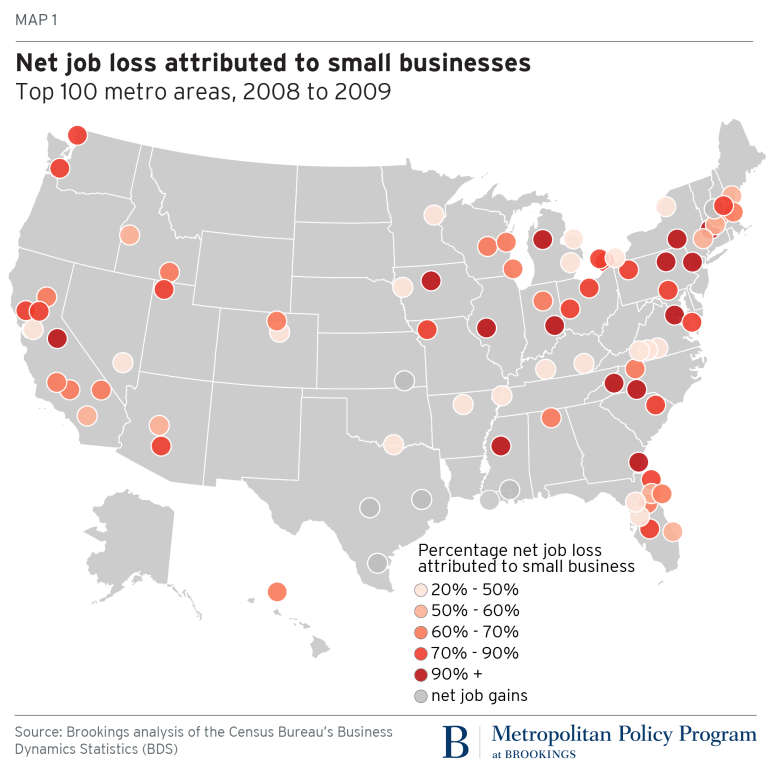

Via Brookings:Sifan Liu and Joseph Parilla observe that small business, particularly newer ones, were hit hardest during the 2007-09 recession. As the economy continues to suffer impacts from coronavirus-induced measures, they look back at what happened to such businesses then. In 16 of the largest metro areas, they find, small businesses were responsible for more than 90% of the net job loss:

But assuming we’re still having this discussion into next week, and possibly the next after, and as confused business owners struggle to fight through the red tape, it is sure to be too late for many who are still paying the bills today only on revenue from yesterday (or rather, from two weeks ago).

“This last week we’ve been working diligently with our banker to keep every single cash reserve dollar we’ve got to take care of things we absolutely have to pay until some of these loan programs become available and we can get cash out of them,” Jerry Akers, who co-owns over a couple dozen Great Clips hair salons locations in Iowa and Nebraska, told Bloomberg. “I’m not a big government-subsidy guy by nature, but right now, that’s our lifeline.”

Eight Registered Sex Offenders Released From NY Jail Due To Gov. Cuomo’s Statewide COVID-19 Orders

“We can’t let the cure be worse than the problem,” President Trump emphasized to the press several weeks ago when talking about coronavirus. Perhaps he should have been stressing that message to New York Governor Andrew Cuomo instead.

Eight registered sex offenders were among those recently released from Monroe County Jail in New York, according to WIVB, as part of statewide orders by Governor Andrew Cuomo to allow 1,100 parole violators out of prison due to concerns about the coronavirus.

“We’re releasing people who are in jails because they violated parole for non-serious reasons,” Cuomo told MSNBC last week.

More than 50 prisoners were released from the jail on Saturday. Among the inmates released, three of them are level 3 sex offenders and are deemed by NY courts as “likely to re-offend”. All three of the Level 3 offenders that were released have been convicted of the rape of minors.

Sadly, we’re not making this up. Instead of being in jail, the former prisoners are now being put up at the Holiday Inn Express in Greece, NY. Patrick Phelan, the Greece, NY Chief of Police, said:“It doesn’t make any sense. If you could present an argument to me that makes sense, I’m willing to listen. But this doesn’t make any sense.”

“So you have a violent criminal who’s done time in state prison who’s been given the chance of parole, and not followed the conditions of their parole. That’s who you’re talking about right now,” Phelan continued.

He also said that he wasn’t notified of the releases when they happened: “We weren’t told by anyone. I think good practice would be if you’re going to release convicted felons. Some of them very violent some of those level 3 sex offenders, You might want to give law enforcement the heads up.”

Meanwhile the Department of Corrections and Community Services, a statewide organization responsible for the releases, said in response: “This significant action is being taken in response to a growing number of COVID-19 cases in local jails over the past few days and weeks. Our top priority remains the public health and safety of New Yorkers during this global public health emergency and this measure will further protect a vulnerable population from contracting and transmitting this infectious disease.”

“That’s right at the edge of a neighborhood. It’s a couple hundred feet from a school,” Phelan said of where the convicted felons are being put up.

“Once again, it doesn’t make sense to me in a jail where you have no cases of the virus. There are zero cases. No one has it. No one is sick in the jail,” he concluded.

You can watch WIVB’s full report on the prisoners here:

The deputy prime minister of Japan says that the WHO should be renamed the ‘Chinese Health Organization’ for its role in helping Beijing cover-up the severity of the coronavirus outbreak.

Referring to a petition which now has almost 700,000 signatures calling on WHO Director-General Tedros Adhanom to resign, Taro Aso tore into the organization for conspiring with China and failing to stop a global pandemic that could have been prevented.

“People think the World Health Organization should change its name. It shouldn’t be called the WHO, it should be renamed the Chinese Health Organization (CHO). This appeal is truly resonating with the people,” said Aso.

“Early on, if the WHO had not insisted to the world that China had no pneumonia epidemic, then everybody would have taken precautions,” he added, noting that Taiwan had to face coronavirus on its own because it was excluded from the WHO.

Indeed, as we have highlighted, the World Health Organization repeatedly amplified Chinese propaganda that the coronavirus outbreak was under control, including a January 14th tweet which falsely claimed there was no human to human transmission of the disease, despite this having occurred in December.

Throughout January, the WHO praised China for its open and “speedy” response to COVID-19, even as Beijing authorities were silencing and disappearing doctors like Ai Fen who tried to warn the world that China was engaged in a cover-up.

The global health body also repeatedly told countries not to enforce border controls that could have stopped the spread of the virus, instead placing more importance on avoiding the “stigmatization” of Chinese people.

Daily reminder that China is to blame for coronavirus.

It originated in China.

China lied about human to human transmission.

The WHO amplified this lie.

China disappeared doctors who tried to warn the world.

Yet our media still suggests it’s racist to talk about any of this.

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Chinese whistleblowing Wuhan doctor Ai Fen, who claimed Beijing prevented her from warning the world about COVID-19, has mysteriously disappeared, according to an investigation by 60 Minutes, Australia.

Besides Chinese doctor Li Wenliang, Fen was one of the first to notice a steady stream of patients with pneumonia-like symptoms in Wuhan before Beijing declared the COVID-19 outbreak. Fen is the Director of the emergency department at Wuhan Central Hospital, told a Chinese media outlet in February that the government silenced her for bringing awareness to the localized virus outbreak that would eventually spread across the world.

Doctor Ai Fen

Wuhan hospital officials punished Fen after she posted test results of a patient that was suffering from Severe Acute Respiratory Syndrome (SARS)-like coronavirus on WeChat before COVID-19 was declared. That image went viral in China.

“Just two weeks ago the head of Emergency at Wuhan Central Hospital went public, saying authorities had stopped her and her colleagues from warning the world,” 60 Minutes Australia reported on Sunday.

Just two weeks ago the head of Emergency at Wuhan Central hospital went public, saying authorities had stopped her and her colleagues from warning the world. She has now disappeared, her whereabouts unknown. #60Minspic.twitter.com/3Jt2qbLKUb

After the 60 Minutes episode aired, Radio Free Asia (RFA) said a cryptic message was published on Fen’s Weibo account. It consisted of a picture overlooking Wuhan, with text that read:

“A river, A bridge. A clock chime.”

Fen’s Weibo post

RFA notes that it was Fen’s “first since March 16, when the account posted to thank everyone for their concern about Ai and to reassure them that she was back at work as usual.”

Concerns over Fen’s whereabouts were sparked after she wrote a now-deleted essay in February tilted “The one who supplied the whistle” in China’s People (Renwu) magazine, describing how the government silenced her after she raised awareness of the “SARS coronavirus” before Beijing declared an outbreak.

“The one who supplied the whistle” in China’s People (Renwu) magazine front page

RFA could not “verify Ai’s whereabouts independently.” There are concerns that the doctor has been detained by the government for speaking out about the virus:

“Detainees in police or other official custody have been known to have their social media accounts updated, either by themselves acting under orders from the authorities, or after police gain access to their devices.”

And it hasn’t been just Beijing trying to keep virus developments under wraps, Fox News’ Tucker Carlson blamed the World Health Organization on Tuesday night for aiding China in the cover-up.

The oil-bears continue their romp across the energy markets with various grades of crude reaching lows not seen in almost twenty years. There will come a point where I can sit down and pen the following words, “We’ve reached bottom, and this is as bad as it gets.” There is a ways to go before it will be possible to make that statement. We are writing off the notion of any recovery in the broad oil and gas market for the next couple of quarters, and probably the rest of 2020. The situation will likely get worse before it gets better, very rapidly. 2021…who knows… things might begin to improve. We will discuss the mechanics of a possible recovery early next year.

The world is awash in cheap oil right now. Goldman Sachs is calling for a final demand decline in March (now) of ~10.5 mm bod, and a projected demand decline of 18.5 million bpd for April. Folks that’s ~20% of total EIA projected global demand.

As discussed in prior OilPrice articles, OPEC and the Russians have drawn a bead on U.S. shale production as the world’s marginal producer. We are beginning to see how rapidly this status may be stripped away as these low cost producers strive to regain their market share lost to American shale production.

In this article we will run down the early indicators the market is sending on where the tipping point will be for shale production. Finally we will include an early estimate for the decline in U.S. shale production by year’s end.

Quick status check for shale

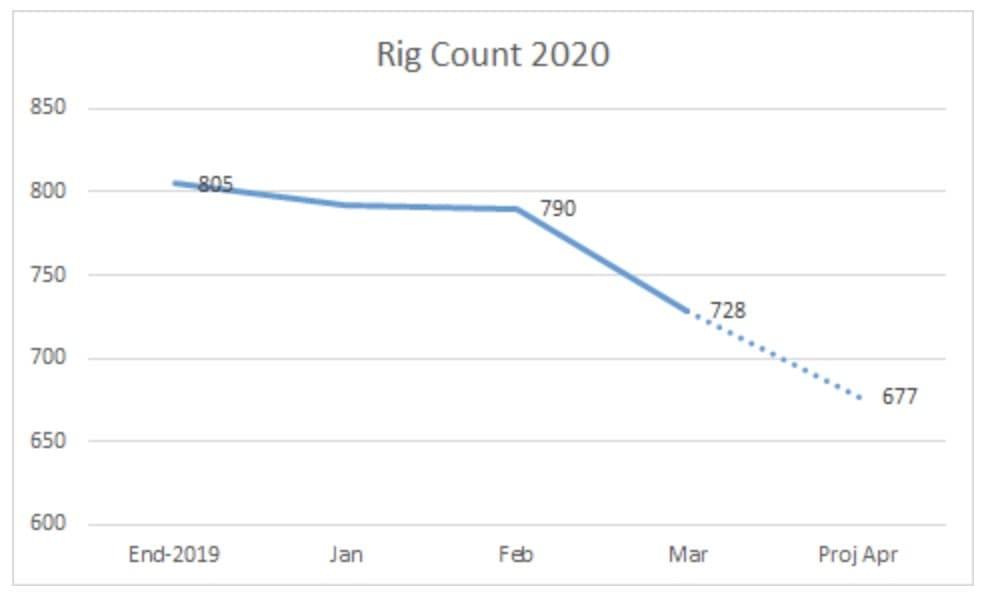

In an OilPrice article last week, I argued that a few things would need to happen before we saw any potential improvement in the market for the oil price. One of them was a reduction in capex across the board for shale. This metric is starting to manifest itself in a couple of ways.

The dotted line is a conservative estimate for the slope of the continued decline as operators tighten their belts.

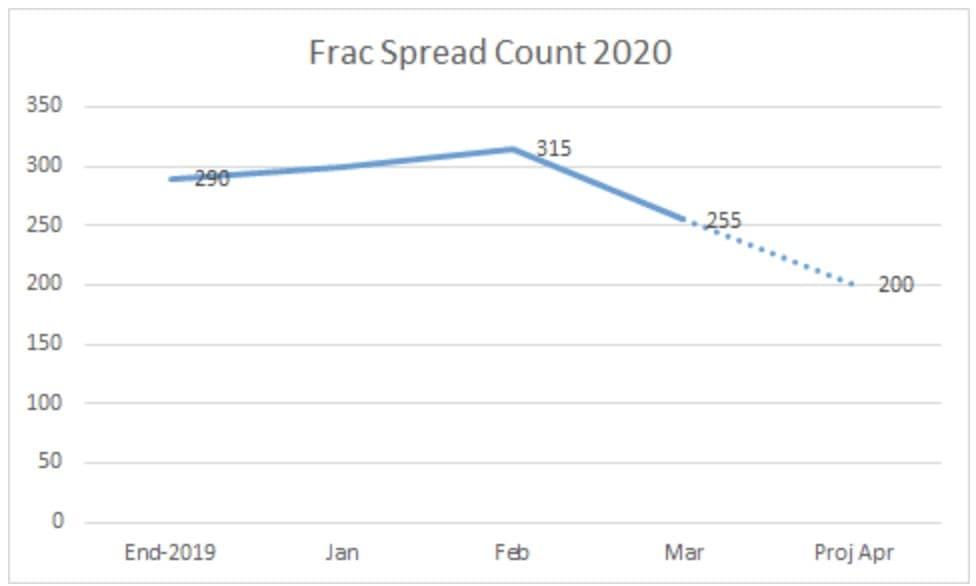

I’ve pointed out that while the rig count has been declining for the past couple of years, Drilled but Uncompleted- DUC, wells withdrawal has helped production to continue its almost inexorable climb. That’s coming to an end as noted by Primary Vision, publishing a drop in Frac Spreads to 255 as of Friday.

I think the rate of decline in Frac Spreads-equipment used to fracture the reservoir, will accelerate in the month of April reaching ~200 by months end.

My analysis of the upward trend in the Frac Spread line to February was that prices…in the mid-$40s through Feb, were still attractive for DUC withdrawal to March 6th. I’ve been thinking for some time that the next logical step would be for uneconomic producers to….BEGIN SHUTTING IN WELLS ALREADY ON PRODUCTION.

I actually put forward this notion in an Oilprice article on the Marcellus gas play. That article focused on the gas glut that led Chevron,to write down its assets in the Marcellus to focus on the Permian. The Permian is more oil-prone, and is part of the reason operators have focused on it so intensively.

Now this idea is becoming mainstream with analysts putting out estimates for how much shale oil might have to be shut in. Here’s a quote from one of these analysts from a recent article in JPT.

“Uday Turaga, the chief executive officer of oil and gas consultancy ADI Analytics, offered two reasons. The first is that many shale players have hedged large volumes of oil sales in the $50-range through 2020. The other is that shale producers remain too optimistic on the chances of a price recovery coming by year’s end

“We don’t see prices and demand rising before 2021,” shared Turaga. “So this approach of cutting just drilling and not completion of wells in inventory is insufficient—they need to go beyond and have a material impact on production volumes.

ADI Analytics is running several forward-looking models, including one that suggests US shale players need to cut as deep as 2 million B/D from year-over-year production. Such a dramatic reduction would be needed to keep oil prices from remaining locked at marginal cash costs. “We could potentially get there just with capex declines,” said Uday, “but not all operators will cut capex, so a little bit of shut in will be necessary.”

Hopefully you caught the line I bolded about shale producer’s optimism.

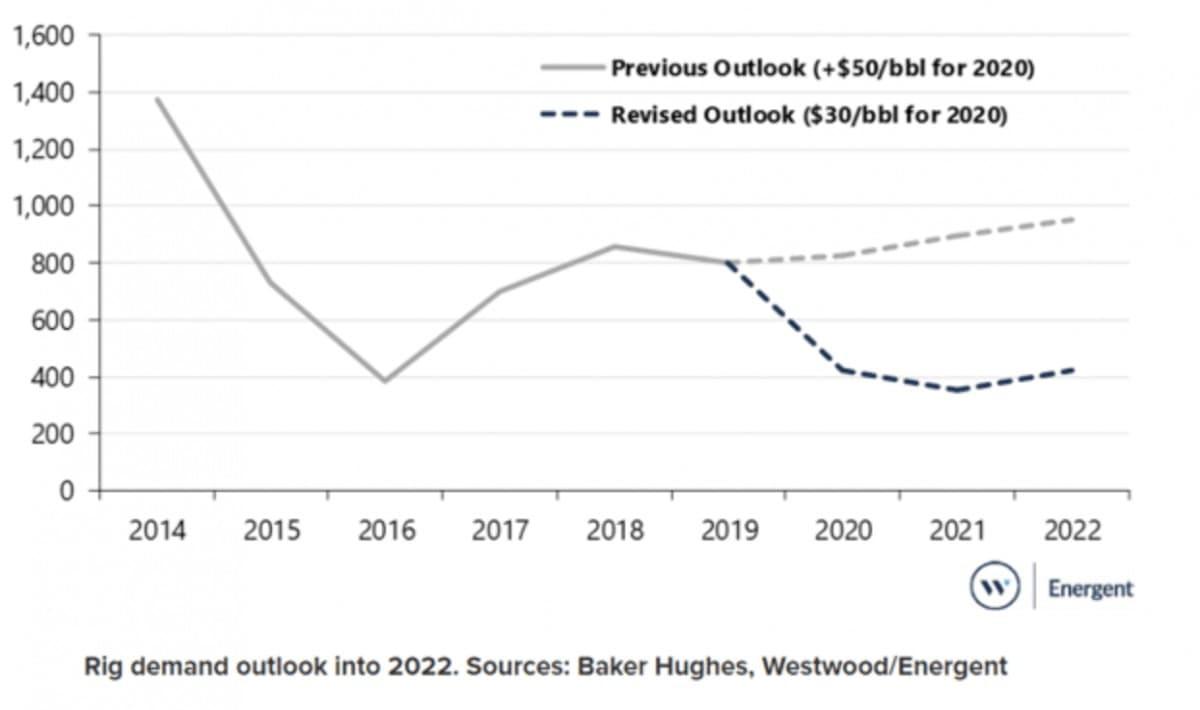

To close this section out here is another graphic from Baker Hughes and Westwood Energent regarding the outlook for the rig count at year end.

Baker Hughes/Westwood Energent

Let’s do some ciphering

Here’s the number you read this article to get.

According to the EIA the incremental new oil per rig is 856 BOPD (the relationship between drilling rigs and daily production is purely statistical, I am just using the EIA’s number to make a guess.) With 728 rigs turning to the right as of March, that works out to…623K BOPD. Reduce the rigs to the high 380’s by late 2020, early 2021 as in the graphic above and you only get…~325K BOPD new incremental production from shale.

Now take the natural decline rate of (again using simple arithmetic here), ~6% per month for shale wells on the average and you get (~9mm Bpd x 540K Bpd. In other words we will be producing about 215 K Bpd below the shale replacement rate as the year closes out. Extending those daily declines to a 30 day period, shale production will be 6 million Bpd LOWER.

That’s an extreme decline I will admit, and you should be reminded I haven’t used any sophisticated analysis to reach this number. A number of factors can and will influence the final amount of the decline. Among them actual new well productivity, and the length of the interval as examples. A higher oil price, responding ironically to the decline in shale production, could actually spur a pickup in new drilling. We will monitor this in future articles and make adjustments to this estimate as production waypoints are passed.

Your takeaway

Game, set, and match to OPEC and the Russians if the scenario I’ve outlined in this article even comes close to playing out. If U.S. production declines to that level, and we return to 2012 in terms of our production. OPEC+ should be happy.

Capturing breaking news in this article it should be noted that President Trump and President Putin have had a chat on the emerging energy depression. I honestly don’t put much store in this having any effect on oil prices in the short-run, even if you assume Putin would have any actual sympathy for the plight of U.S. shale producers. Remember…this debacle started only last month when they ruined the OPEC+ party in Vienna by not agreeing to more cuts to shore up prices.

What’s changed since? Nothing really in terms of their original objective. The Russians have the cash reserves to see this collapse of American shale for at least another couple of quarters, and the collapse in demand due to the Corona virus is going to play out no matter what they do. Basically Putin has no incentive to change course, save as a bargaining chip for sanctions relief. Something that is politically unacceptable in this country as elections draw nearer. This leaves with the status quo firmly in place.

Bottom-line, U.S. shale appears to be on an unavoidable rapid decline. That is bad news for a lot of companies that depend on this activity for their daily bread. The good news is this will inevitably drive higher prices and the growth cycle for energy will begin again.

Study Finds That Trump’s ‘Miracle Drug’ Helps Fight COVID-19

The New York Times and Washington Post aren’t going to enjoy reporting this.

A relatively small study involving coronavirus patients in China has determined that the malaria drugs that President Trump has been pushing as potential coronavirus ‘miracle cures’ actually do seem to work in preventing COVID-19, the disease caused by the novel coronavirus, from progressing into its most lethal stage.

The news will send “a ripple of excitement” through the medical community, one doctor said.

The malaria drug hydroxychloroquine helped to speed the recovery of a small number of patients who were mildly ill from the coronavirus, doctors in China reported this week.

Cough, fever and pneumonia went away faster, and the disease seemed less likely to turn severe in people who received hydroxychloroquine than in a comparison group not given the drug. The authors of the report said that the medication was promising, but that more research was needed to clarify how it might work in treating coronavirus disease and to determine the best way to use it.

“It’s going to send a ripple of excitement out through the treating community,” said Dr. William Schaffner, an infectious disease expert at Vanderbilt University.

Though NYT, WaPo, and most of the left-wing press has sought to focus on the “unproven” nature of hydroxychloroquine and its analogue chloroquine, as well as the fact that Trump’s remarks have purportedly spurred harmful hoarding (which has deprived some regular patients of their medication) and at least one man’s decision to try a harmful COVID-19 “home remedy” with the same active ingredient in the medication (spoiler alert: that man poisoned himself, and the mainstream press swiftly declared it to be Trump’s fault), some professionals have backed Trump.

Writing in WSJ last week, a pair of doctors reviewed the evidence at hand and recounted their clinical experience saying they had seen the drug effectively treat COVID-19.

Fortunately, as the NYT noted in this latest article, the drugs are cheap, relatively plentiful, and mostly harmless.

Now that the FDA has granted the drug emergency approval, part of a plan to allow its use in New York in particular, doctors suspect more patients will begin asking for the drug.

“I think it will reinforce the inclination of many people across the country who are not in a position to enter their patients into clinical trials but have already begun using hydroxychloroquine,” he said.

And now, doctors have every reason to give it a shot.

Hawaii Lt. Governor: Everyone Should Wear A Mask When Leaving Home

Everyone should wear a mask when they’re leaving their home during the CCP virus pandemic, according to Hawaii’s Lieutenant Gov. Josh Green, a physician.

The statement comes, as The Epoch Times’ Zachary Stieber reports, as experts across the United States are increasingly recommending the same while warning people to leave N95 masks for healthcare workers, a request Green also made.

Most other masks don’t provide the same level of protection but can still protect against the CCP (Communist Chinese Party) virus, commonly known as the novel coronavirus. Any mask, Green told KHON-2, “is better than nothing.”

“We are all doing what we can by staying home but a lot of people are still having to to go out to run a few errands or go out and provide health care. When you do, wear a mask, cover up. And if you’re in the hospital of course wear an N95,” Green said.

People wearing masks should still follow social distancing measures, including staying at least 6 feet from other people. Mask wearers should take the time to learn how to properly wear them. Most surgical masks were designed for one-time use but masks made at home may be able to be washed and used again.

“I want to go on record, I’m recommending anyone who’s out there in line, any line whatsoever, please keep 6 feet social distance, that’s totally critical, and have a mask of some sort if you have it,” Green said.

Green’s recommendation was one of the first made by a state official as federal officials consider advising everyone to wear masks after recent data shows asymptomatic patients, or people with the CCP virus who aren’t showing symptoms, can easily pass on the virus.

We all remember this – when Surgeon General Jerome Adams tweet said it all “Stop Buying Masks!”:

Seriously people- STOP BUYING MASKS!

They are NOT effective in preventing general public from catching #Coronavirus, but if healthcare providers can’t get them to care for sick patients, it puts them and our communities at risk! https://t.co/UxZRwxxKL9

“There is no specific evidence to suggest that the wearing of masks by the mass population has any potential benefit. In fact, there’s some evidence to suggest the opposite in the misuse of wearing a mask properly or fitting it properly,” Dr. Mike Ryan, executive director of the WHO health emergencies program, said at a media briefing in Geneva, Switzerland, on Monday.

“There also is the issue that we have a massive global shortage,” Ryan said about masks and other medical supplies.

“Right now the people most at risk from this virus are frontline health workers who are exposed to the virus every second of every day. The thought of them not having masks is horrific.”

We were told that face masks weren’t effective at preventing a coronavirus infection unless we are a healthcare worker, but now the CDC is saying otherwise.

There’s still no consensus (meaning someone from the government hasn’t made a decision yet) on whether widespread use of facial coverings would make a significant difference, and some infectious disease experts worry that masks could lull people into a false sense of security and make them less disciplined about social distancing, according to a report by The Washington Post.

But studies done by doctors in the medical field have shown properly fitting N95 face masks to be about 80% effective.

Dr. Deborah Birx, response coordinator for the White House Coronavirus Task Force, told reporters at the White House on Tuesday that the matter was still under discussion.

President Donald Trump said that people can use scarves to cover their mouth.

“I think some people disagree with the mask, for various reasons, and some people don’t. But you can wear a scarf. You can do the masks if it makes you feel better. We have no objection to it, and some people recommend it,” the president said. The CDC has recommended health workers who can’t obtain masks wear scarves.

Officials have expressed concern about potential shortages of masks in hospitals, he noted.

“We don’t want everybody competing with the hospitals. So you can use scarves. You can use something else over your face. Doesn’t have to be a mask,” Trump added.

However, as South Korea’s top COVID doctor explained, “during the SARS and MERS outbreaks, masks were proven to work [to slow the infection rates].”

Nassim Taleb had strong feelings about the bullshit…

This is the strongest statistical association I’ve seen w/ respect to the virus. Wear a mask, mandate others to wear masks, & remember that @WHO is criminally incompetent. To repeat:@WHO is criminally incompetent.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}