Harvey Weinstein was convicted of third degree rape and a criminal sexual act by a New York jury of seven men and five women, who took five days to reach their verdict. He faces up to 25 years in prison.

Weinstein was acquitted of predatory sexual assault, the most serious charge, and first degree rape.

The jury was deadlocked on the charge of predatory sexual assault, the most serious accusation against the disgraced 67-year-old Hollywood mogul, offering a glimpse into disagreements between jurors who had been deliberating in New York City over four days.

Jurors had told Judge James Burke in a note, “We the jury request to understand if we can be hung on 1 and or 3 but unanimous on the others.”

Counts 1 and 3 are charges of predatory sexual assault.

Count 2 is criminal sexual act in the first degree, count 4 is rape in the first degree, and count 5 is rape in the third degree.

Burke told jurors that any verdict that they returned must be unanimous and that if they cannot be unanimous on a specific criminal count then they cannot return a verdict for that count. –CNBC

According to the Wall Street Journal, “Predatory sexual assault requires jurors to agree that Mr. Weinstein carried out more than one sex crime and carries a sentence of up to life in prison.”

Weinstein was charged with one count of criminal sex act for allegedly forcible performing oral sex on former film-production assistant Miriam Haley in 2006, as well as first and third degree rape charges for allegedly forcing himself upon aspiring actress Jessica Mann in a Manhattan hotel room in 2013.

With Sen. Bernie Sanders now the clear frontrunner for the Democratic nomination for president, even some on the left have expressed worry over what a self-described Democratic Socialist on the ticket in November could mean not only for Democrats’ chances of taking back the White House but also for their down-ballot odds, namely, control of the U.S. House of Representatives and Senate.

Among Sanders’ most ardent supporters are college-aged voters, who favor the Democratic Socialist far more overwhelmingly than the broader electorate. However, from liberal MSNBC commentators Chris Matthews and Joy Reid to former Clinton campaign manager James Carville, a growing number of voices on the left are sounding the alarm, joining those with whom Campus Reform spoke more than a year ago.

At a Washington, D.C. protest, Campus Reform‘s Cabot Phillips spoke with individuals who escaped socialism in Venezuela to come to America.

WATCH:

“You do not ever want anyone, not even close, to socialism to come to this country,” one person said.

The same person specifically invoked Sanders’ name.

“Bernie Sanders is your enemy. Do not ever get involved with this individual or any of the other socialists,” he said.

“It is not the route to go. It is not possible. It is not feasible. Don’t fall for it,” another said.

“We also thought that this could never happen in our country,” one victim of socialism said about the economic system’s perils.

“We had a balance of powers. We had democracy and we elected our leaders.”

One person who said that he was born and raised in Venezuela said that he has seen the country “deteriorate” under socialism.

On Saturday, Sanders won the Nevada Democratic caucuses. The win follows his victory in the New Hampshire primary and his virtual tie for first place with former South Bend, Indiana Mayor Pete Buttigieg in Iowa.

Sanders’ wins in the first three contest states pave a clearer path for him to the Democratic nomination than for any other Democratic presidential candidate, although the South Carolina primary is just one week away, with Super Tuesday also quickly approaching.

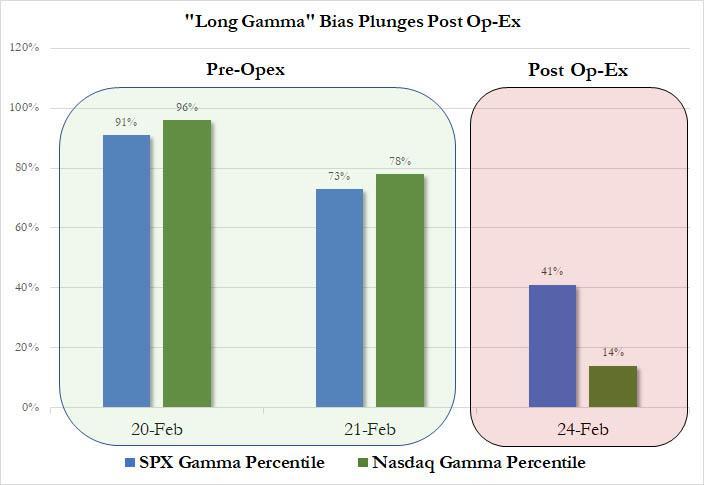

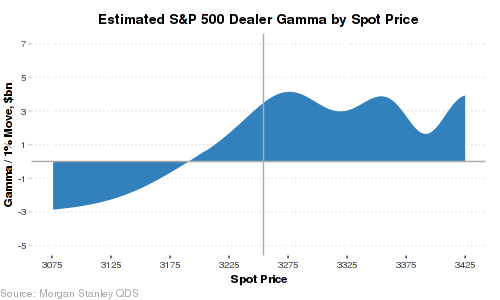

Morgan Stanley: If We Close Below 3,235, Systematic Selling Will Become “Self-Fulfilling”

Earlier today we noted that according to Nomura’s Charlie McElligott, the biggest risk facing the market was a “shock down” as dealer gamma bias had evaporated following Friday’s Op-Ex (especially in the Qs)…

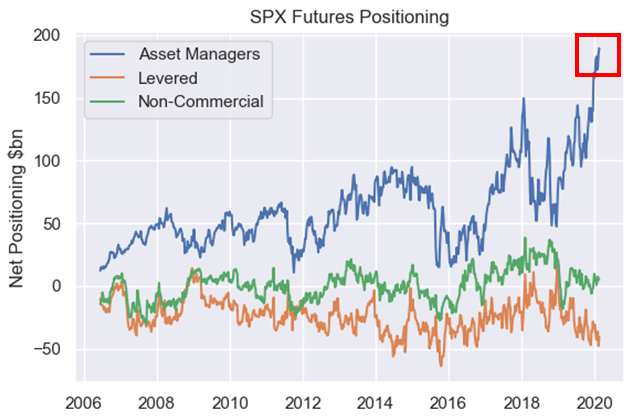

… which meant that instead of providing a natural buffer to any selling (“buy weakness/sell strength”), dealers are now procyclically positioned, and any accelerated selling would only lead to more selling, resulting in even lower gamma, even more selling, and so on, in a typical gamma feedback loop. A separate, and just as tangible risk according to McElligott, was the record positioning (100%ile) across asset managers, whose net long exposure across SPX futures hit a record $190BN.

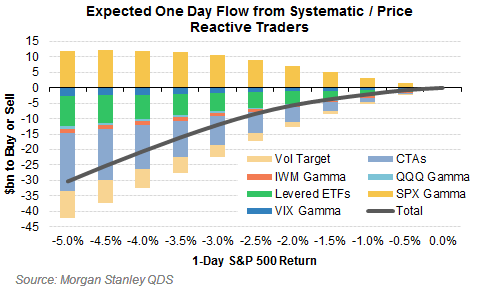

At roughly the same time, Morgan Stanley’s Christopher Metli, executive director in the bank’s QDS division, looked at selling pressure from another source, and calculated that while there is up to $10BN in notional selling pressure today from “systematic and price reactive traders”, this liquidation amount could soar to $60BN which would “generate a self-fulfilling downward move in QDS’ view” if the S&P closes below 3,235 or just a handful of points from here.

As Metli writes, “on the worst pre-open selloff since June 24th 2016″…

… QDS estimates $5 to $10bn in equity needs to be sold today with an additional $20bn over the rest of the week from systematic and price reactive traders.

As MS further notes, this number would be a lot higher except dealers are long $3 to $4bn of SPX gamma per 1% move here…

… which cuts today’s number in half (i.e. option rebalancing is about $9bn to buy, offsetting other drivers of supply), and the rally in bonds cushions some of the blow as well.

That said, for every extra 50 bps selloff here QDS models roughly $20bn in more supply this week, and a close below ~3235 (-3%) on the SPX threatens to bring in enough supply ($60bn+ total) this week to generate a self-fulfilling downward move in QDS’ view.

The silver lining: some of this supply should be offset by pension demand – Metli has previously estimated (when stocks were at all time highs) a US equity-for-sale imbalance for asset allocators this month, but today’s selloff, which has sent yields to record lows, flips that number to $7BN to buy over the next two weeks (and $15bn ex-US). Yet even so, while this demand is an “offset”, the MS quant warns that “it should come through more slowly than the supply.”

* * *

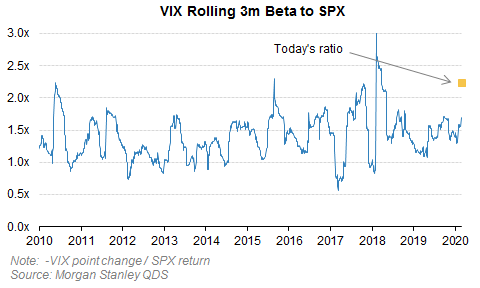

We doubt that a blind liquidation panic causing even more selling, is news to any trader. However, what is notable is that the pace of the selloff (i.e. volatility) is the key driver of how much needs to be sold, according to MS, which echoes McElligott in observing that CTA triggers / moving average crossovers “are far away for US futures so most of the likely supply comes from deleveraging on the back of higher volatility.”

So what does volatility tell us? Consider that the VIX surged to the low 20s (yet another confirmation of the prescience of “50 cent” who was buying deep OTM VIX calls over the past two weeks), moving 2.3 points for every 1% of S&P 500 decline…

… which according to Morgan Stanley is a bigger move than normal beta would suggest, but isn’t a massive overreaction (over 3x ratio on a daily basis it starts to get extreme).

In other words, despite the frenzied liquidation at the start of trading, for now at least the volatility market is showing relatively ‘normal’ behavior for this size selloff.

US Intel Briefer Who Gave Overblown Russian Interference Assessment Has Reputation For Hyperbole

The US intelligence community’s top election security official who appears to have overstated Russian interference in the 2020 election has a history of hyperbole – described by the Wall Street Journal as “a reputation for being injudicious with her words.”

The official, Shelby Pierson, “appears to have overstated the intelligence community’s formal assessment of Russian interference in the 2020 election, omitting important nuance during a briefing with lawmakers earlier this month,” according to CNN.

The official, Shelby Pierson, told lawmakers on the House Intelligence Committee that Russia is interfering in the 2020 election with the goal of helping President Donald Trump get reelected.

The US intelligence community has assessed that Russia is interfering in the 2020 election and has separately assessed that Russia views Trump as a leader they can work with. But the US does not have evidence that Russia’s interference this cycle is aimed at reelecting Trump, the officials said.

“The intelligence doesn’t say that,” one senior national security official told CNN. “A more reasonable interpretation of the intelligence is not that they have a preference, it’s a step short of that. It’s more that they understand the President is someone they can work with, he’s a dealmaker.” –CNN

Pierson was reportedly peppered with questions from the House Intelligence Committee, which ’caused her to overstep and assert that Russia has a preference for Trump to be reelected,’ according to the report. CNN notes that one intelligence official said that her characterization was “misleading,” while a national security official said she failed to provide the “nuance” required to put the US intelligence conclusions in proper context.

To recap – Pierson told the House Intelligence Committeea lie, which was promptly leaked to the press – ostensibly by Democrats on the committee, and it’s just now getting walked back with far less attention than the original ‘bombshell’ headline received.

Sound familiar?

No biggie… the media just ran with hysteria for 3 years as gospel accusing people of treason

Well guess what? It turns out the media and the DNC were the ones working for Russia, executing their long standing goal to create chaos better than Russia could have ever dreamed of. https://t.co/PhrJiES9ui

Brace! Brace! Brace! Have we arrived at the moment when the global economy and markets tumble into a proverbial hole?

Relax! Markets always overreact, and things are never as bad as the papers say, but the bad news Virus narrative is gaining momentum with extraordinary speed…. Venice Carnival and sports events cancelled. Italy Lockdown and Korean red alerts. Apparently, its running unchecked in Iran – the ultimate WHO nightmare. Breathe deep.

The reality is the Coronavirus Covid19 remains primarily an economic event. Global authorities are struggling with containment policies in the face of the massive unknowns still surrounding the virus. Its likely mistakes have been made, but they were probably right to err on the side of over-reaction. The effect of underestimating the virus could be even worse. If we are going to be hit with a global Coronavirus pandemic, and mortality rates rise above 2% – similar to 1918/19 – then it’s tragic and has massive implications which we can analyse. Heaven forbid it ever comes to that stage.

But the reality for markets is to answer the question: Which way will the massive economic shock the Covid19 virus has triggered push markets? (Assume the Real and Present Economic damage and a Snap Recession is the direct result of the Authorities policy decisions to contain the virus, and were unavoidable.)

The economic damage in terms of cancelled tourist trips to Asia and vice-versa, empty container ships, global supply chain breakdown shuttering factories across the globe, commodities tumbling, rising fears of mass defaults as just-in-time manufacturers fail to make interest payments is clear. There are any number of articles in the press with the time and space to describe the damage in detail.

Markets feel properly nervous this morning. After another record high last week, the 3% plus subsequent slide in stocks, plus the news, has scared the punters. Treasuries hit a record low yield.

Check out any Chartist, and they will be telling you the runes, pentograms, and discarded chicken livers used to make their market prognostications all scream the same thing: Sell Stocks, Buy Treasuries, Sell Corporate Bonds, Sell Oil and Buy Gold. Generally, they are unconvinced on a positive market outcome.

Could the Covid19 virus crisis have come at a worse time? There is never a convenient time for the end of the world.

This crisis comes at the top of massive bubbles in stocks and bonds, fuelled by 10-years of accommodative monetary experimentation – just at a time when the global monetary authorities are increasingly understanding the urgent need undo the unintended negative consequences, end QE, to normalise interest rates and take the pressure out of asset bubbles. It doesn’t help the dollar is going stratospheric – a natural safe-haven shift, helped by Japan’s massive 6.7% slide in annualised GDP on the back of another VAT hike. That looks increasingly ill-considered as Chinese spenders stay home and fail to sustain Japan’s retail sector. There are a lot of painful wake up and feel the pain moments coming.

Q1 economic and company reporting is going to be brutal.

So……. Buy or sell the market?

Your call boils down to: do you believe central banks can continue to pull it out the hat? Yes/No? Do you keep buying this market on the mounting calls for central banks to ease and provide further accommodative policy support will happen? Will the virus give investors yet another free put on markets?

35 years of markets has taught me a number of lessons – now formalised as Blain’s Market Mantra’s. These include: 1) “The Market has but one objective; to inflict the maximum amount of pain on the maximum amount of participants”, 3) “The Market has no memory”, and, one I borrowed: 26) “The Market can remain irrational longer than you can remain solvent”. I think the one that applies best may be: 8) “Markets are about emotion, never be emotional in the way you play them”.

Think about this market in unemotional terms. What choice do Central Banks have? It strikes me this could become a “Draghi Moment”: that critical singularity when global central banks have no alternative but to do “whatever” it takes to avoid economic meltdown.

The last thing Central Banks can allow is a market collapse alongside the snap Virus recession – the long term damage to economic activity would be brutal, and unnecessary. Could we even see Occidental Central Banks step into buy equities “to support market confidence through the economic consequences of the virus”?

What else could they do? Massive and unlimited lending/giveaways to banks to support and maintain struggling corporates? State support for populations to stay home? The news out of China is the banks have been told to lend and support firms getting perilously close to default as industry and towns remain shuttered. Companies have been banned from laying off workers. I suspect where China goes, other economies may follow.

Or maybe time to get even more imaginative. How about a real fiscal kick? The crisis facing the planet is about distribution – broken global supply chains on the back of the policy response to the Virus. At some stage, and I suspect fairly soon, these will be restored (although I doubt the Chinese swift V shaped recovery). The issue might be a broken global economy by the time it happens…

What about driving demand through variations on Helicopter money? What about massive tax cuts for consumers, VAT holidays, debt forgiveness for students etc. The idea would be to drive the economy into recovery through a demand side boost – which would be inflationary if its enacted too early, but massively pro-cyclical if it was to drive a massive demand led boost to supply chains as the story behind the virus becomes clearer?

While markets start to worry that a couple of days of lower markets means the imminent end of everything, and wonder what lower bond yields means – the reality is global supply chains from just-in-time tech, autos, tourism and commodities have all been hit for 6. There will be a massive Q1 shock. Some sales will simply be delayed – like an iPhone not purchased in Feb will probably be bought in May, but a holiday next week cancelled is gone for ever. Choosing stocks is a tactical call for investors – which firms take real damage, and which might just slow.

The strategic call is one for Central banks. Just how much will they have to juice the COVID Recession?

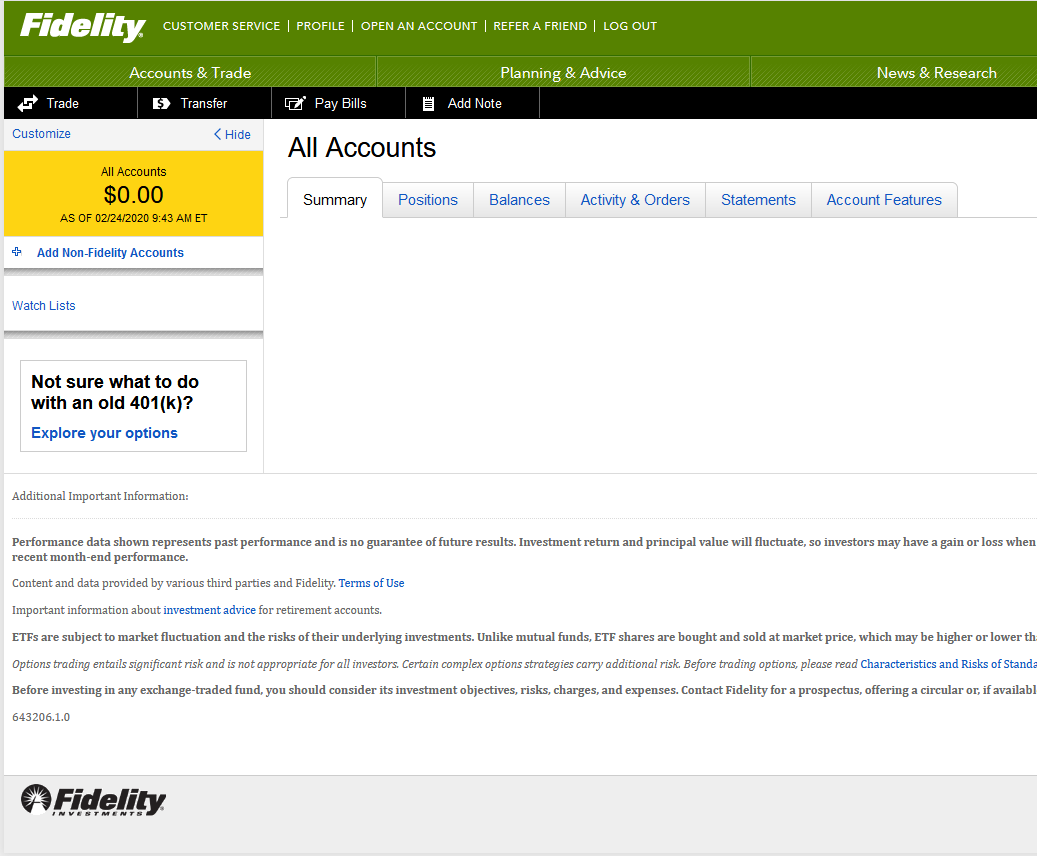

Fidelity Breaks For 2nd Time In A Week: Countless Accounts Showing Zero Balance

One week ago, when stocks were hitting all time highs as traders were blissfully ignoring all the same news that are sending markets crashing today, we reported that online brokerage Fidelity was true to its name and, well, broke, showing zero balances on countless accounts. At the time we said that “while we assume this pesky “glitch” will be resolved promptly, we should point out that if the market were to ever again suffer a down day and should investors wish to sell some/all of their holdings, this would be a convenient way to quickly and efficiently prevent that from ever happening.“

Little did we know that this hypothesis would be test just three days later, because as of Monday morning, with stocks crashing and the Dow on pace to wipe out all gains for 2020, Fidelity has once again gone dark with the website barely working, and with countless clients eager to put on some “hedging trades” or at least get the hell out of Dodge, unable to do so because as Fidelity helpfully informs them, they suddenly have zero assets in their possession.

Needless to say, Fidelity’s (rapidly declining) clients are not too happy but this repeat fiasco, and are aggressively considering some rather flagrant Infidelity vis-a-vis their online broker in light of what has become an almost daily farce on high vol days:

Looks like @Fidelity is trying to protect investors from themselves?

Or I just lost all my monies already today. @Fidelity it would be great on a day like today if your site worked. pic.twitter.com/hSXFsZwnMH

Hey @Fidelity why does your app and website consistently just crap out during high volatility days? Also what is the point of a brokerage if you can’t trade during high volatility days? Took so long to get an order in by the time I got an order fill I was down 10%. Thanks.

How does this happen on a day like today? @Fidelity is this intentional to control trading and volatility? My IRA and HRA accounts are gone from the website… pic.twitter.com/p37TAAz7lE

@Fidelity AGAIN?! The company needs to put out a statement about these problems besides, “we are experiencing problems”. What is the real problem and what are you doing to fix it? I don’t want to change brokerages, but I’m real close. Please give me a reason not to. pic.twitter.com/Q6lHwR9eFU

@fidelity my accounts are now showing a zero balance. I know I’m not the only customer experiencing this. Fidelity needs to be prepared for days like this.

Judge In Roger Stone Case Refuses To Bow Out Of Retrial Decision Over Accusations Of Bias

The judge in Roger Stone’s trial who sentenced the longtime Trump adviser to more than three years in prison last week has shut down Stone’s request that she exit the case before ruling on whether he should get a new trial over a controversial juror.

US District Court Amy Berman Jackson issued a harsh rebuke to Stone’s legal team, who accused her of bias when she said the jury in his case served with “integrity,” despite the fact that the forewoman – a former Democratic political candidate who despises President Trump – may have lied when asked if she knew who Roger Stone is during jury selection.

“At bottom, given the absence of any factual or legal support for the motion for disqualification, the pleading appears to be nothing more than an attempt to use the Court’s docket to disseminate a statement for public consumption that has the words ‘judge’ and ‘biased’ in it,” Jackson wrote on Sunday, according to Politico.

The jury took about a day to unanimously find Stone guilty on all seven counts he faced related to impeding Congressional and Justice Department investigations into Russian interference in the 2016 presidential election.

The recusal motion argued that Jackson evinced bias because during the sentencing hearing Thursday she said the jurors in the case “served with integrity.” But in a six-page order released Sunday evening, the Obama-appointed judge said her remark fell well short of the kind of evidence of bias that would require a judge to step aside. –Politico

“Judges cannot be ‘biased’ and need not be disqualified if the views they express are based on what they learned while doing the job they were appointed to do,” Jackson continued, noting that recusal for bias typically applies to statements judges make outside of court in unofficial settings.

“The defendant has not suggested that the Court said one word about him outside of the courtroom, or to anyone other than the parties, at any time. Its characterization of the jurors’ service was voiced on the record, and it was entirely and fairly based on the Court’s observations of the jurors in the courthouse; through the nine days of voir dire and trial, when they were uniformly punctual and attentive, and through their thoughtful communications with the Court during deliberation … and the delivery of the verdict,” Jackson wrote.

She added that she wasn’t referring to the jury-related comment during her Thursday remark about “integrity,” but that even if she was, she was free to comment or rule on it regardless.

“If parties could move to disqualify every judge who furrows his brow at one side or the other before ruling, the entire court system would come to a standstill,” warned Berman Jackson.

The order contains more indications that Jackson has grown frustrated with and irritated by Stone’s defense team. During the sentencing Thursday, she excoriated the defense over its closing argument, riffing on the refrain of “So what?” that the defense used in its unsuccessful bid to get jurors to acquit Stone. –Politico

“So what? So what? Of all the circumstances in this case, that may be the most pernicious,” said Berman Jackson during her almost 45-minute statement last week to the packed D.C. courtroom. “The truth still exists. The truth still matters. Roger Stone’s insistence that it doesn’t, his belligerence, his pride in his own lies are a threat to our most fundamental institutions, to the very foundation of our democracy.”

The truth may still exist, and it may matter – but allowing clearly biased jurors to serve on the trial of a guy you hate is nothing short of a miscarriage of justice.

Rabobank: Our Coronavirus Base Case Is Rapidly Shifting From “Bad” To “Ugly”

Submitted by Michael Every of Rabobank

Regular readers will know that our four projected COVID-19 scenarios were “Bad, Worse, Ugly, and Unthinkable”. Current news today suggests risks that the base case is rapidly shifting from “Bad”, meaning only China is impacted, to “Ugly”, where both emerging Asia and developed economies see soaring infection rates and deaths.

After all, following Vietnam, Iran now has eight deaths and an uncertain number of cases, prompting schools and universities to closed and the borders with Afghanistan and Pakistan to be sealed from the other side. For an economy already being crushed by sanctions, this is all that it needed. More worrying for markets, South Korea (with a GDP of over USD1 trillion) has also been swamped by hundreds of new cases, a 20-fold leap in just five days, and, as in China, is seeing the highest-level emergency declared, cities on lock-down, gatherings and travel bans in place, and the national assembly additionally suspended. Samsung has had to shutter at least one factory, in the city of Gumi. The Asian economy, already reeling, it about to suffer another major kick.

Worse, in Europe there also are over 160 cases in a cluster in northern Italy, with three deaths so far, and the regions of Lombardy and Veneto, the industrial and financial heartlands, in both panic and lockdown. Venice’s Carnival has been cancelled, and so was a recent fashion show. Italy is 11% of Eurozone GDP, and those two regions are 30% of Italy’s GDP. For a Eurozone already close to recession, that shock could well be more than enough to generate a downturn. Once again, we also see what we said we would in our recent virus special report: a “China-style” response: yesterday a train from Venice to Munich was stopped at the Austrian border because of fears that two passengers on board may have had the virus. So much for Schengen? Recall that the origins of the world “quarantine” come from Venice in an earlier phase of globalisation, and refer to the *40* days sailors had to stay on a visiting ship to prove they were not carrying an infectious disease. No just-in-time supply chains in those days though.

Meanwhile, China is saying the virus may not have started in the seafood market; hot-headed Chinese social media is saying it might have been America who started it; experts are saying COVID-19 can linger on surfaces for nine days, and is airborne, and can be passively carried with no symptoms for up to *27* days, nearly double the 14 days previously thought; and other reports show that false negative tests are a serious issue, with at least one confirmed case of a patient being tested negative twice and then switching to positive. As the WHO, which has urged us all to travel as normal until now, “because markets”, wails, the window to stop this becoming a global pandemic is closing.

By contrast, China is doing its best to say that all is well. Unsurprisingly, since Party Chairman Xi Jinping placed his hand-picked people in charge, new cases have dropped sharply. Optimists see this means the lockdowns have worked – which means more global lockdowns must now be priced in, however; pessimists suggest data goal-seeking is playing a role here. However, deaths have not fallen yet, with another 97 yesterday raising the overall fatality rate worryingly (and one study of 53 Wuhan patients suggests a 61.5% fatality rate for those with any co-morbidity factor such as diabetes and/or heart or lung disease).

Just as unsurprisingly, Xi has publicly promised China will have beaten the virus by the end of March, and that the overall economic goals for 2020 are still in place, even as right now we are still basically flat-lining as shown by traffic congestion, pollution, and property sales. As we have already covered in recent weeks, the only way for BAU to return ASAP is for everyone to start travelling and gathering and working again: which is exactly how the virus will spread, especially after we have been told there is a 27-day latent period, as well as a clear tendency of asymptomatic carriers, and even more so now it has legs outside China too. Even so, people are being urged back to work as eagerly as they were being told to lock themselves in at home just two weeks ago.

Equally unsurprisingly, the PBOC, who have already lowered rates 10bp, are making clear that COVID-19 “will be short-lived and will not change the country’s sound economic fundamentals”. With several reports suggesting up to 85% of China’s small business are going to run out of cash within three months, and many within weeks, its banks riddled with bad loans and already under-capitalised, and the state clearly about to embark on another massive debt-splurge to build more infrastructure to keep to a set GDP number regardless, even when China does re-emerge from COVID-19 it will be sagging under an even more unsustainable debt load, and the state will be playing an even larger economic role. It’s also unclear if foreign firms will be as willing to be embedded in a long, China-centric supply chain regardless, making USD inflows less likely; and all of those issues above will mean the weaker CNY we have referred to for years. It is no surprise we are through 7 again; the larger surprise is that we are not closer to 7.20.

More broadly, of course, the “Ugly” scenario is seeing US Treasury yields test critical support levels. The 10-year is now at 1.47% and another leg down will see us in whole new territory. Likewise, the USD is on a roll upwards and threatening to push higher: imagine if European virus cases spread, the same happens in Japan, and China cannot reopen as planned. And imagine what a stronger USD on top of this virus backdrop will mean for emerging-market USD borrowers. Ugly indeed.

Such is the news-flow that I hardly have time to relate that Bernie Sanders handily won the Nevada Democratic caucus, leaving Joe “White Walker” Biden in a poor second place and Mike Bloomberg looking as user-friendly as his terminals are. That makes Bernie the clear presidential nominee front-runner at this stage – and makes many Never-Trumpers into Rather-Trumpers, I would imagine. And imagine if Bernie’s plans for free healthcare for all intersect with a virus outbreak in the US….(on which note, please see our recent Through The Looking Glass report imagining a Sanders presidency).

Last night, when the implied 10Y yield (Japan was closed) dropped to just 1 basis point above 1.40%, we said that we are literally this close from BofA’s “tipping point” for the 10Y Treasury, below which a recession is virtually assured according to the NY Fed’s recession probability indicator, and which also triggers a 12-18 month countdown to 0% rates.

Well, this morning, with risk assets crashing, the yield on the 10Y has sliced below the 1.40% “tipping point” like a hot knife through butter…

… and is now less than 1 basis point away from the all time low of 1.3579% hit on July 8, 2016.

Why does 1.40% matter again?

Because, as we explained yesterday, breaking below this “tipping point” level requires more than 50% probability priced for the Fed cutting rates back to 0%! This means that breaking 1.4% in an on-hold context for the Fed creates a significant inversion of the curve, pushes recession signals higher, and pressures a further inversion of the FF1/FF6 spread which we found in Pricing cuts ahead of the Fed to have no false positives for Fed cuts following a -30bp inversion (currently -16bp).

What this means in practical terms from a duration perspective is that “the market may gap lower on a break below 1.4% for the 10Y Treasury”, as this corresponds to phase transition higher in recession probabilities and a clear challenge to the on-hold Fed stance, “particularly as convexity flows add to what would likely be a broader risk-off move. “

Finally, while the threshold for cuts is high – especially if a slowdown is driven by pandemic fears – and considering the Fed’s recent rhetoric which has sought to allay expectations of a rate cut as soon as June, once the Fed commits to cuts, BofA finds it unlikely that they will be the insurance style of 2019, and instead the Fed will proceed to cut all the way to zero to avert the coming recession. For the curve, this implies some scope for further bull flattening, but limited beyond 1.4% in the 10Y, as the Fed is likely to be more significantly priced in beyond this level.

And with the 10Y now at 1.3655%, this means that trapdoors to both a recession and the Zero Lower Bound – if not outright negative rates – are now open.