Maddow Meltdown: In Defense To OAN Lawsuit, Host Argues Her Words Are Not Facts

Back in September, we reported that TV network OAN had filed a lawsuit against Rachel Maddow for the time the host said that OAN “really, literally is paid Russian propaganda.”

Now, Maddow finds herself having to come up with a defense for her statement in court. And she has also apparently hired Lionel Hutz as her legal adviser.

According to Culttture, her lawyers argued in a recent motion that “…the liberal host was clearly offering up her ‘own unique expression’ of her views to capture what she saw as the ‘ridiculous’ nature of the undisputed facts. Her comment, therefore, is a quintessential statement ‘of rhetorical hyperbole, incapable of being proved true or false.”

Oh, it’s capable of being proved false, alright. Maddow had previously claimed, on air, about one of OAN’s reporters:

“In this case, the most obsequiously pro-Trump right wing news outlet in America is really literally is paid Russian propaganda,” and added, “Their on-air politics reporter (Kristian Rouz) is paid by the Russian government to produce propaganda for that government.”

The testimony of UC Santa Barbara linguistics professor Stefan Thomas Gries, however, stands at odds with Maddow’s defense. Gries said: “It is very unlikely that an average or reasonable/ordinary viewer would consider the sentence in question to be a statement of opinion.”

Gries continued: “I am the second most widely-cited cognitive linguist and sixth most widely-cited living corpus linguist. The field of cognitive linguistics draws from both linguistics and psychology and studies how language interacts with cognition.”

OAN had filed the defamation suit in federal court in San Diego, according to AP. OAN is a small, family owned conservative network that is based in San Diego and has received favorable Tweets from the President. It is seen as a competitor to Fox News.

OAN’s lawsuit claims that Maddow’s comments were retaliation after OAN President Charles Herring accused Comcast of censorship. The suit said that Comcast refuses to carry its channel because “counters the liberal politics of Comcast’s own news channel, MSNBC.”

It was about a week after Herring e-mailed a Comcast executive when Maddow opened her show by referring to a Daily Beast report that claimed an OAN employee also worked for Sputnik News, which has ties to the Russian government.

Maddow said: “In this case, the most obsequiously pro-Trump right-wing news outlet in America really literally is paid Russian propaganda. Their on-air U.S. politics reporter is paid by the Russian government to produce propaganda for that government.”

Except Maddow, likely still upset from spending 3 years trying to promulgate a Russian hoax that didn’t exist, didn’t quite get her facts straight.Big surprise.

Poor Bill Gates. He’s very much dedicated to philanthropy and giving away all his vast wealth, yet he can’t help getting richer every day and is once again the richest person in the world gaining over $22B in personal wealth in just 2019. Not bad for a retired guy. I guess it’s hard to give all your money away when the functionings of modern day capitalism make it seemingly impossible to do so. A key driver of Bill Gates’s vast wealth expansion being the same as always: The ongoing meteoric rise of Microsoft stock. Maybe one day the Fed will figure out the causes of vast wealth inequality, but for now they’re too busy grappling with their own system failure turbo charging wealth inequality across the globe.

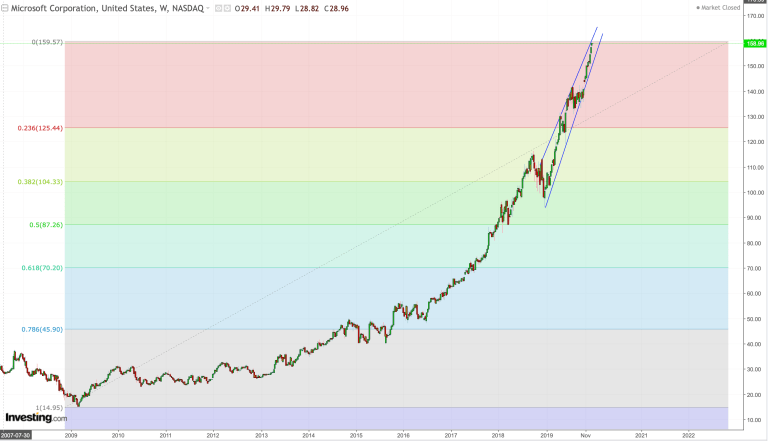

But I digress, back to $MSFT: The stock has been an absolute beast with one of the strongest trends out there. No down year since 2011, massive growth for a company so large, well executed, strong business model, with a booming cloud business that got the additional benefit of a US government cloud contract this year. And like $AAPL discussed yesterday $MSFT is a big beast in the $NDX contributing vastly to the index gain.

And like the rest of the market $MSFT has seen a vast expansion in multiples and market cap this year.

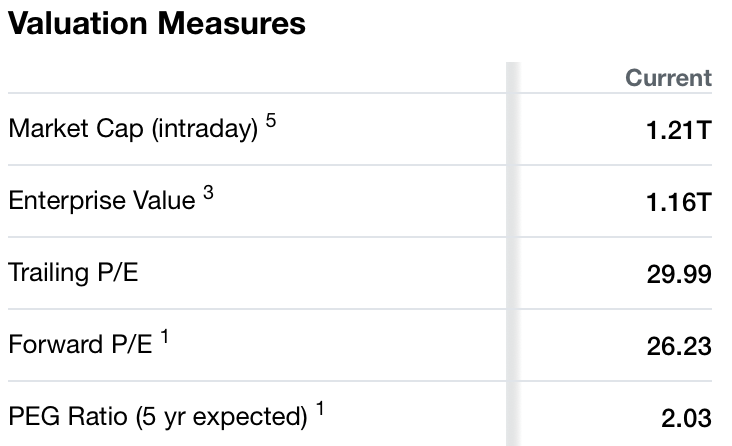

This puppy ain’t cheap, especially for a company this size:

Trailing P/E of 30 for a company with a market cap of $1.2 trillion. Oh kay then.

But these are risk free markets so why worry? Well I, for one, try to keep a sense of perspective on risk/reward through a technical lens. So, as with $AAPL, let’s have a look at charts.

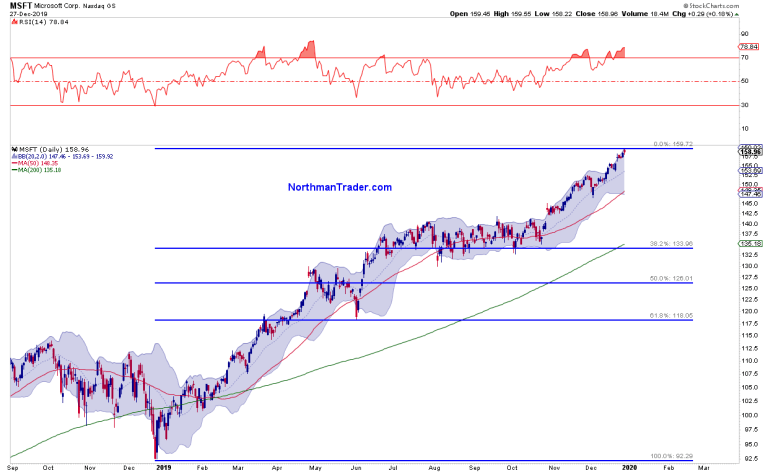

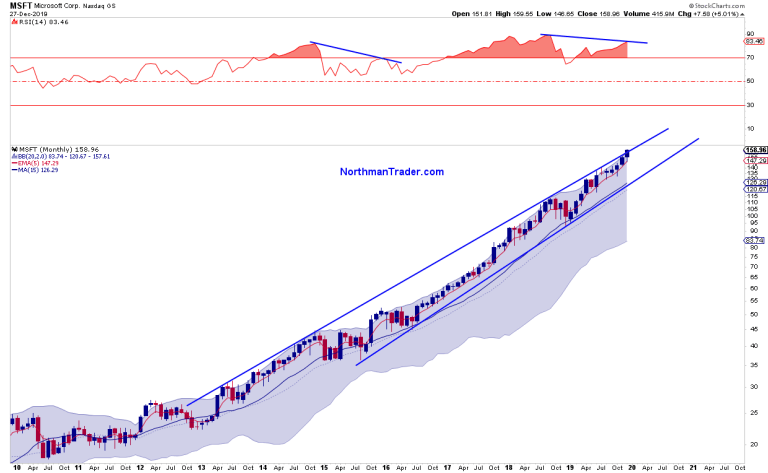

A basic daily chart:

Like the rest of the market $MSFT recovered fiercely following the 2018 correction, but then based in range all summer long despite the Fed rate cuts. And like the rest of the market it didn’t really take off until the Fed’s balance sheet and repo interventions went full blast in October:

This run has brought the daily RSIs to very overbought readings. Yet overbought readings alone are not a sell signal. The stock, on a daily chart, is extended, but absolutely nothing is broken, no MA breakdowns not even a negative divergence on the daily chart. What can be said is that the stock is far extended above its 200MA suggesting reversion risk as we can observe in the larger market.

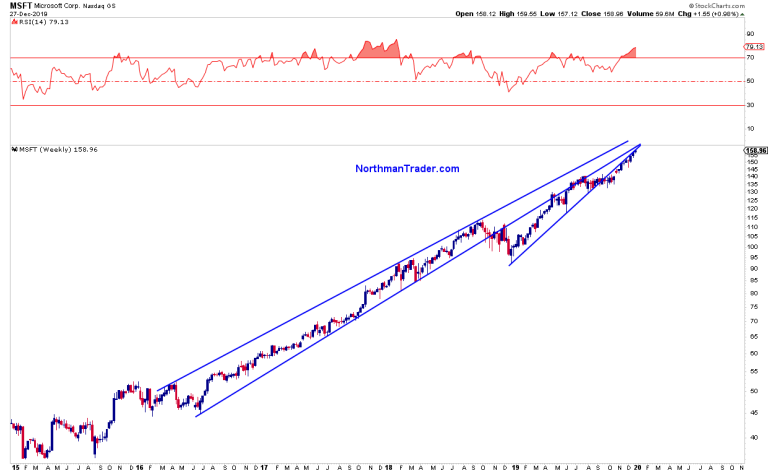

The weekly chart gives a bit more nuanced perspective:

A trend break in 2018 and a furious rally below that broken trend, a secondary trend that was also broken, and then a Q4 rally that has brought price to a point of confluence of resistance that the stock may find difficult to exceed from here. The weekly RSI also being highly overbought.

On a monthly chart however we see that the larger trend remains fully intact:

As with $AAPL we see the stock pressing against a larger upper trend and the stock exceeding the upper monthly Bollinger band with a notable negative monthly divergence.

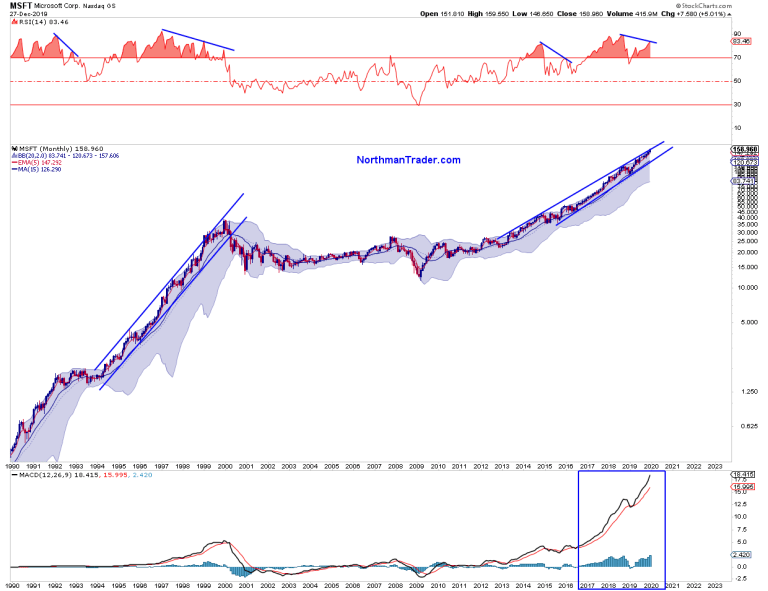

How one sided has $MSFT’s ascent been over the past few years? Only a broader timeline perspective can reveal an appreciation for how outsized the bull move in $MSFT is.

For giggles check the monthly MACD:

Parabolic much? Sustainable? Historic precedence for such a move to be sustainable is precisely zero.

And so the technical argument becomes one of reversion risk.

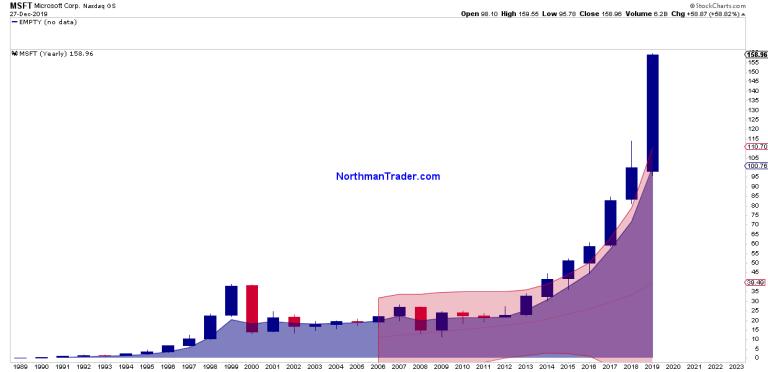

Here’s a chart I’ve shown a few times this year and its value is the yearly 5 EMA disconnect and the extension above the upper Bollinger band, but one can also appreciate the parabolic nature of this linear chart:

There is no history in the stock remaining entirely disconnected above the yearly Bollinger band. Each year it finds a way to reconnect. Currently the upper Bollinger band is at $110, the 5 EMA at $100. Both will be higher in 2020, but represent reversion risk targets rooted in history, both suggesting massive downside risk in 2020.

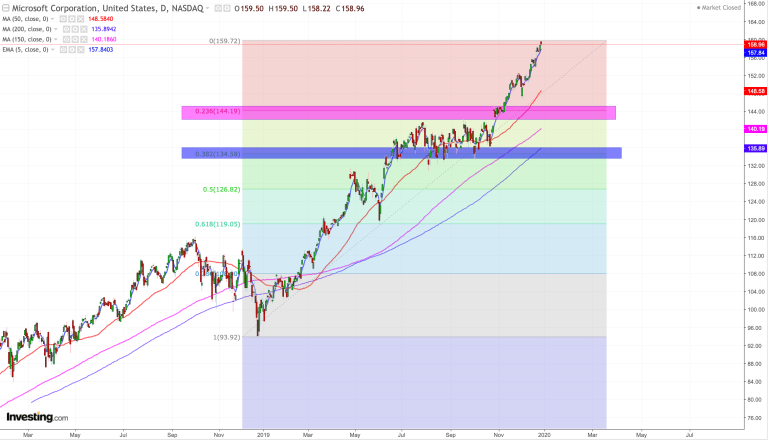

The rally in 2019 has been so furious that fib levels and MAs give a sense as to the scope of even basic reversion risk:

A basic .236 fib retrace offers a target of $144, the .382 fib targeting $134 an area which would be met with strong support as it was the consolidation phase in the summer of 2019. The zone between $134 and $144 also showing key MAs racing higher.

Such a corrective move would not present reasons alone to constitute the end of the bull run in $MSFT, but without new highs following such a correction they may well signal an impending shift.

See, the run in $MSFT has been so vast that not even the 2018 correction shows as a corrective year in $MSFT. The last red candle down year in $MSFT was in 2011.

And again we find ourselves asking: Given high valuations, massive market cap, disproportionate influence on index weightings and so many index funds and hedge funds all owning the same stock an end to a bull market in this stock would present systemic risk for the larger market.

I showed you fib levels for the 2019 rally as benchmarks for a basic correction.

What about going back to 2009?

Yea. Nothing parabolic and excessive about that. It’s only a $1.2 trillion company with a 30 trailing P/E.

Is this sustainable? According to bulls anything is sustainable. The Fed’s got this. Party like it’s 1999.

From my perch this market is reliant on mega cap stocks such as $AAPL and $MSFT to stay on historic unprecedented chart and valuation runs. Trends that are extremely steep, narrow, and vastly disconnected and hence in my view: Dangerous.

I’m not saying these companies won’t continue to grow, or don’t have winning business models. What I am saying is that there is massive corrective technical risk in all of them and given their size and dominance these companies also contain the elements of systemic risk as so many own the same few stocks that dominate everything. For now buying begets buying as all sellers have all but disappeared, but know the exit door is thin on the way out. Should these companies priced to perfection for years to come disappoint these steep channels are easily broken with technical consequences.

As with $AAPL $MSFT is a key stock to watch in 2020. Bulls can’t afford to lose either one of these and their trajectory in price is in my view unsustainable.

Once we see corrective activity in $MSFT and $AAPL we will need to asses any chart damage. Remember tops are processes, but correction risk is vast. As we saw in 1999: Stocks go up forever until they don’t and then everything can change. Fast.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

I want to start with the quote from last week’s missive only because it is so apropos:

“We are so overbought, and this is feeling like a panicky-just-get-me-in buy day. Be careful about being impressed.” – Kevin Muir

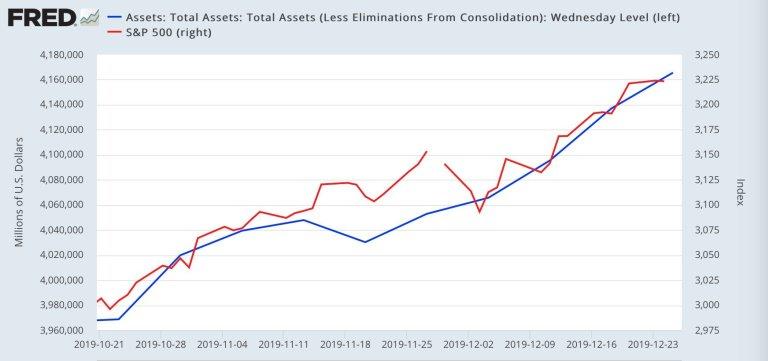

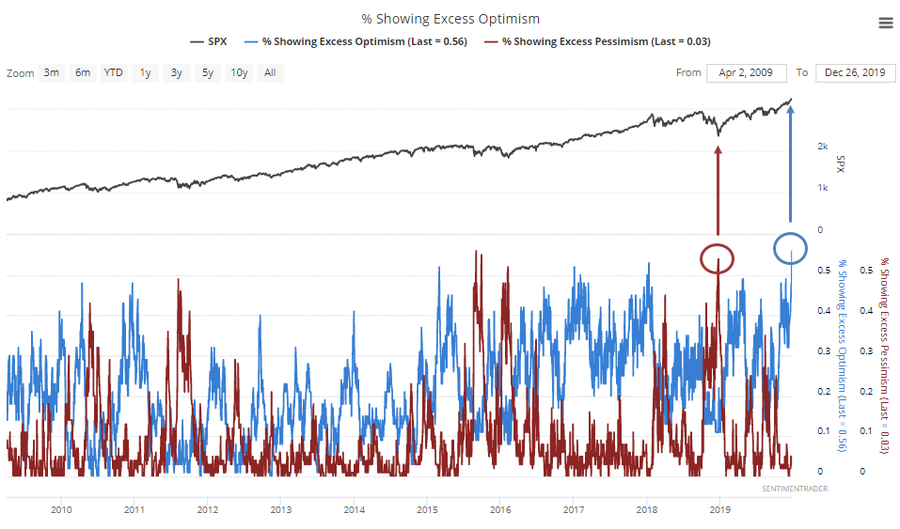

That remains the case again this week as investor optimism has surged to record highs. As noted by Sentiment Trader, this is a marked reversal from just 1-year ago as sentiment plumbed more extreme lows.

Of course, this reversal in optimism should not be a surprise. My pal Victor Adair at Polar Futures group explains this well.

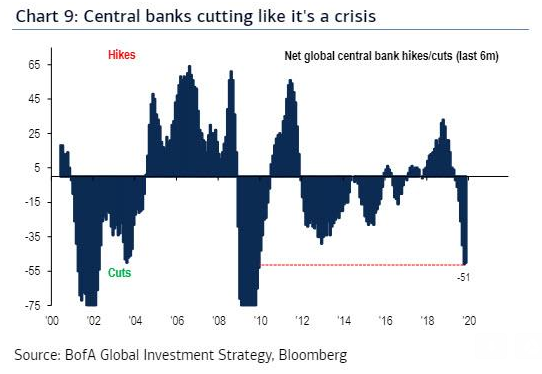

“The most important message from the financial markets in 2019 was, ‘Don’t Fight The Fed.’ The 180 degree turn in Federal Reserve policy…the Powell Pivot…caused markets to realized that it was, once again, ‘All About The Central Banks.’

In December 2018 the Fed raised interest rates and indicated that they expected to be raising rates in 2019…but instead of raising rates they cut rates three times…stopped their quantitative tightening policies and wrapped up 2019 by pumping vast amounts of liquidity into the market.

The Fed’s policy reversal inspired Central Banks around the world to step up their own monetary stimulus programs. That global shift to easier monetary policy may or may not have kept the world economy from slipping into recession in 2019…but it certainly helped drive global stock and bond markets to big gains. Bond yields hit All Time Lows, the ‘stack’ of negative yielding bonds soared to a high of ~$17 Trillion and major stock indices kept making ‘New All Time Highs.’”

As I penned last week:

“This stimulus is the largest ever outside of a ‘recession’ or ‘financial crisis,’ which should lead to the obvious question of ‘what exactly is going on we don’t know about?’”

This surge of liquidity is the reason for the markets surge over the last 3-months and was the crux of Friday’s “Morning Market Commentary” which was provided to our RIAPRO subscribers:

“While the media has continued to use the same straw man of trade optimism to justify the rally whatever trade agreement there may actually be was priced in long ago.

The reality is that the Fed’s $500 billion flush of liquidity into year-end to meet short-term funding needs has been interpreted by the markets at “QE.” This interpretation, and subsequent F.O.M.O, led to a rush by managers to benchmark performance and push equity allocations, and subsequently investor optimism, toward record highs.”

This message hasn’t changed over the last week:

“While the Federal Reserve accurately states this is NOT ‘Quantitative Easing,’ apparently market participants didn’t get the memo. The market has risen in every single week the Fed has been active, despite collapsing fundamentals. (h/t ZeroHedge)”

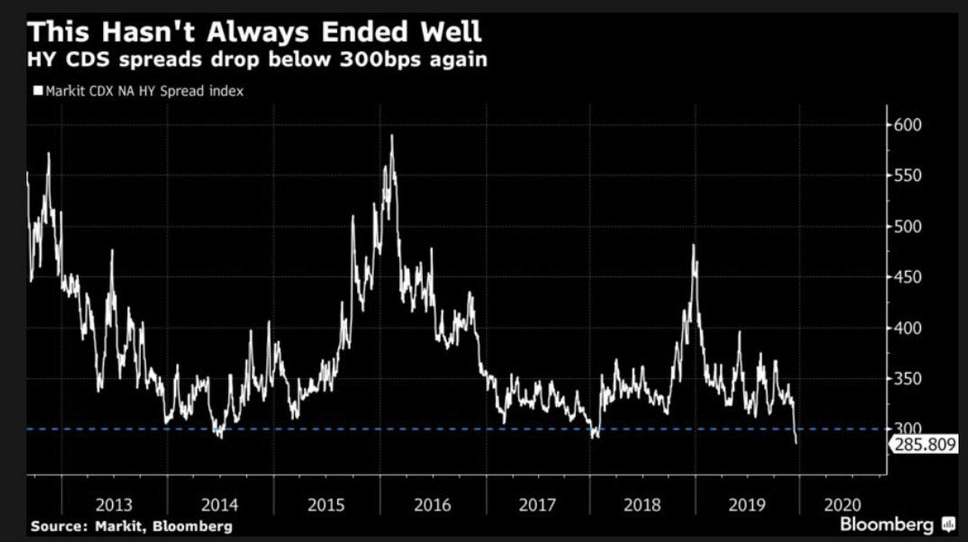

Speaking of optimism, and outright complacency, the difference (spread) between the high yield (junk debt) CDX index and U.S. Treasury yields has fallen back below 300 basis points. The index measures the cost of insuring high yield debt against default. This extremely low cost of insurance, especially this far into an economic expansion, reeks of complacency and a chase for extra yield as we are seeing in other asset markets.

Four Charts That Will Define The Next Decade

The following four charts were tweeted out by my partner Jack Scott (@jackpscott) which will literally define the next decade.

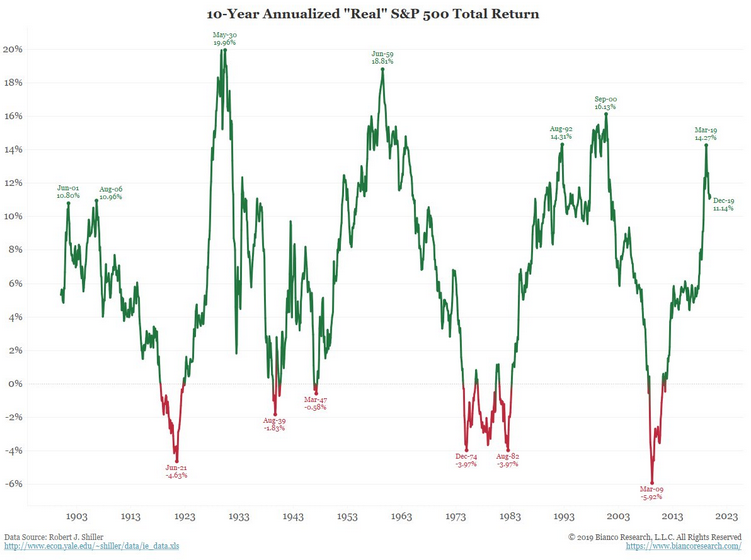

1 – Annualized Returns are one of the more “mean reverting” series in the financial markets. Decades of high returns are inevitability followed by a subsequent low, and even negative, returns. (If you are close to retirement this is an extremely critical point to understand when it comes to your financial planning.)

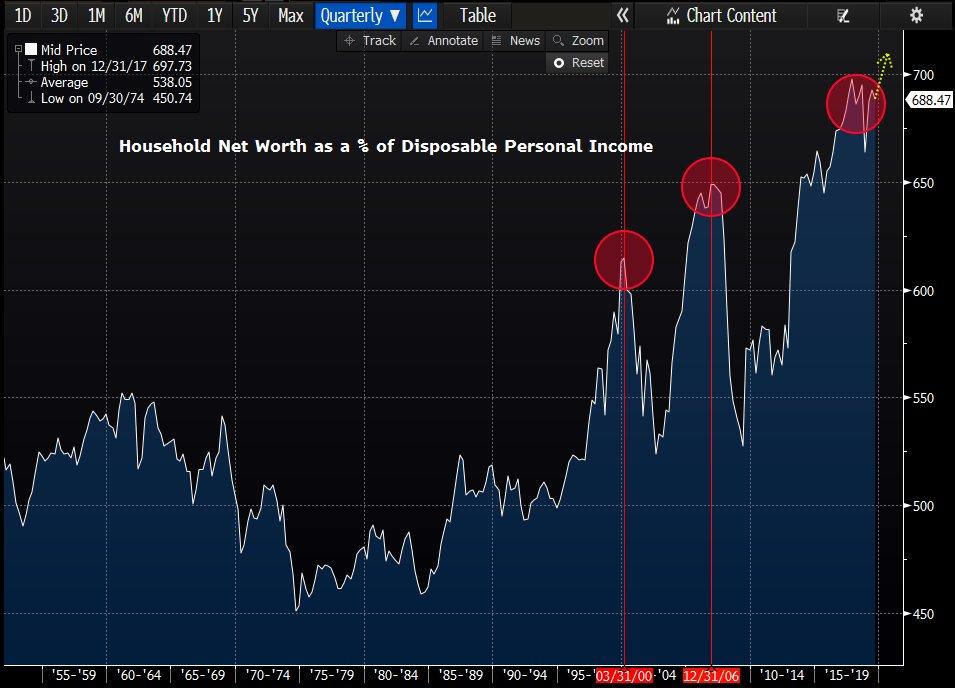

2 – Household Net Worth as a Percentage of GDP is pushing record levels. While not in itself a “bad thing,” the benefit has been confined to the top-20% income earners. Importantly, asset growth has far outstripped economic growth which is unsustainable long-term. This series too, will mean revert.

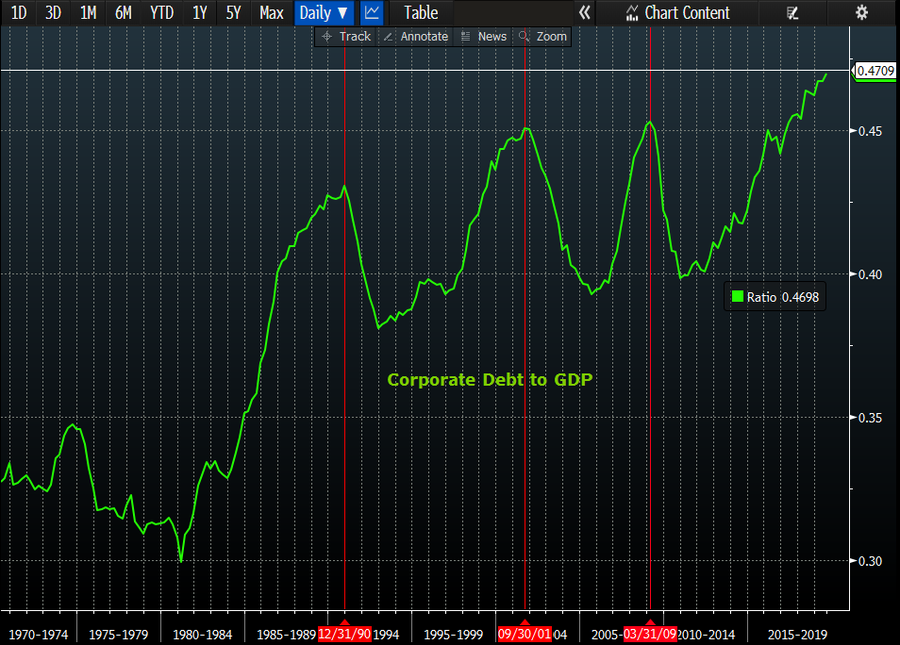

3 – Corporate Debt To GDP is also pushing unsustainable levels. Debt ultimately has to be “cleared” before the system can re-leverage for the next growth cycle. The next reversion cycle will be brutal on a large number of publicly traded companies which have relied on “cheap debt” to sustain poor fundamental business models. Be careful what you own.

4 – Melt-Ups In Markets Can Seem Rational in the heat of the moment. However, when “reality” inserts itself, the eventual reversion tends to be brutal.

What you do with the data is up to you. All I am suggesting is that it took a decade of “fiscal largess” by Central Banks globally to create these extremes. It will likely take a decade to complete a reversion.

Portfolio Positioning

From last week:

“As we have noted over the past year, we have remained primarily allocated toward equity exposure, but have also worked around the edges hedging risk, raising stop levels, and remaining primarily domestic-focused. Given our outlook for a steeper yield curve earlier this year, we also shorted duration in our bond allocations, increased credit quality, and carried a slightly higher than normal level of cash.”

Currently, that remains the case again this week.

In September, we added exposure to Amazon (AMZN) and the Discretionary Sector (XLY) to participate with a “better than expected retail shopping season.”

Not surprisingly, this past week both surged on headlines from the media that retail sales were strong for the Christmas shopping season. However, this is probably not actually the case judging from real “retail sales” which were weak in November and will likely be weak in December. Nonetheless, the positions have performed well and will take profits as the decade ends.

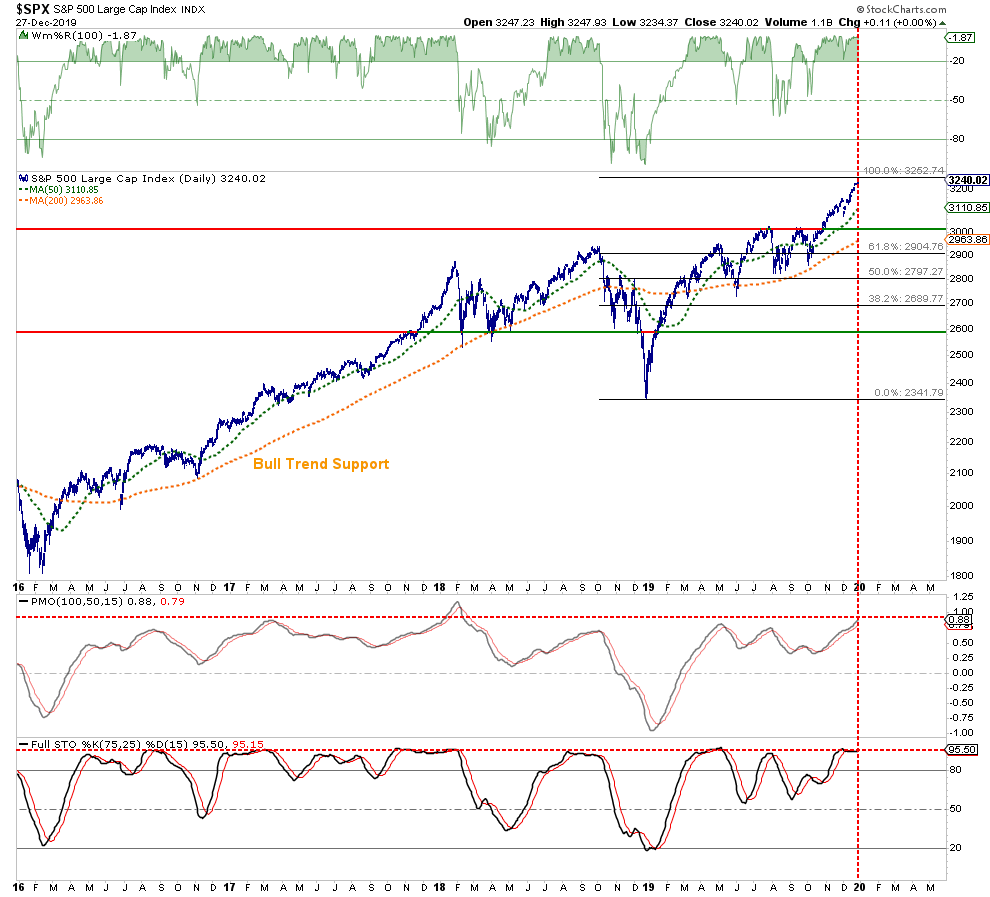

As noted last week, the markets are now even more extremely deviated from long-term trends. Combined with the extreme complacency and excess bullishness (as noted above), the risk of a correction remains high as we move into January or February. (More on this in our MacroView)

As noted below, the market has not been this overbought, extended, and deviated from long-term trends since the peak of the market in 2018. This isn’t necessarily a “bearish” note, but does suggest that the bulk of the gains are currently built into portfolios.

While none of this means the next “bear market” is lurking, it does suggest that a fairly decent 5-10% correction is likely over the next couple of months.

As we head into the final few trading days of the year, it is worth reminding you of “the rules” we penned in last week’s missive.These processes follow our basic rules of portfolio management, which you can apply to your portfolio as well to reduce overall volatility risk.

Tighten up stop-loss levels to current support levels for each position.

Hedge portfolios against major market declines.

Take profits in positions that have been big winners

Sell laggards and losers

Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says, “sell everything and go to cash.”

Remember, our job as investors is pretty simple – protect our investment capital from short-term destruction, so we can play the long-term investment game.

Of course, if the Fed fails to “extinguish” whatever “blaze” they are currently battling, then we will begin to have a very different conversation about risk, positioning, and liquidity.

Cracks Are Showing On The Surface Of Once “Safe” Top Tier Malls

For a while, it looked as though top tier malls may be able to narrowly avoid the ugly fate that was facing most malls around the country in the wake of the Amazon revolution.

But this holiday season, it looks like that’s not going to be the case. Some landlords of the most highly trafficked malls across the country are issuing warnings about slowing income growth as they try to continue to target new ways to get feet in the door, according to the Wall Street Journal.

Simon Property Group said during its most recent earnings call that retail bankruptcies “negatively impacted” net operating income in the quarter. It also lowered its 2019 guidance to a range of $6.76 to $6.81 from $7.04 to $7.14 due to a one time cost associated with an early debt repayment.

Taubman Centers, owner of The Mall at Short Hills in New Jersey and Beverly Center in Los Angeles, also lowered its 2019 guidance for same property net operating income growth to a range of 0% to 1%, from 2%. The company’s COO blamed the lowering partially on the bankruptcy of Forever 21.

William Taubman, chief operating officer said: “Forever 21’s bankruptcy has disproportionately impacted ‘A-malls’ and Taubman Centers specifically.”

These higher end malls were among 260 top tier malls in the U.S. that many analysts thought were protected from store closings and bankruptcies. But bankruptcies of large name retailers are starting to create aftershocks, even in these once “protected” malls. And even when malls are fall, revenue can still be falling, as landlords have to cut rent to entice stores to stay.

Forever 21 has started closing 87 of its stores, which is actually an improvement after planning on closing 178, before securing rent reductions from landlords. Landlords, of course, had to lower their earnings projections as a result.

Average occupancy of top malls is still in the 90% range – for now. Some analysts are concerned about the higher costs landlords face to replace departing tenants. They are also expressing concern about the “sales per square foot” metric that is often touted by landlords in the business. Malls usually only need one very productive tenant – like a Tesla store – to skew this metric higher.

Vince Tibone, an analyst at Green Street Advisors said: “All it tells me is that you added a Tesla into your mall. It tells me nothing about how the mall is doing.”

And while the market has roared in 2019, investors have punished top mall owners. Shares of Taubman and Macerich are down by about 33% each and Simon is down about 14%. Dividend yields currently hover around 10% for some names.

Bill Smead, chief executive of Smead Capital Management has started to invest in Macerich because Macerich executives have been buying their own shares.

Still, some analysts are cautious. A recent Morgan Stanley note warned: “They may not be as attractive as they look, especially since the dividends for some REITs are not fully covered and require cash flow growth.”

Landlords point out that they continue to invest in new entertainment options and retail strategies that combine online shopping with traditional brick and mortar retail. They are also spending to give older malls face-lifts.

Ali Slocum, a Simon spokeswoman said: “Our company continues to be well-positioned, prosperous and dynamic.”

Something odd is happening with Brexit. It looks like Prime Minister Boris Johnson is pushing for a hard Brexit much to my surprise.

Johnson’s strong showing in the recent election which secured the Tories its biggest majority since the days of Margaret Thatcher should have set the stage for the great Brexit bait and switch.

This has been my argument for months since Johnson became the front-runner to replace Theresa May. All Johnson had to do was manipulate events to get a majority which marginalizes the hard Brexiteers of the European Research Group (ERG).

Then he could undermine Brexit by giving back all the concessions during his subsequent negotiations with the EU over a trade deal.

This analysis should have been the correct one given the staunch opposition by the political elite in the U.K. to Brexit.

But something has changed.

Johnson is practically channeling Nigel Farage in his stance to trade negotiations with the European Union. The modified Withdrawal Bill that passed Parliament with six Labour defectors significantly strengthens Johnson’s hand in trade negotiations by removing any potential extension beyond the end of 2020. There are a ton of changes the Guardian article linked above covers.

The two year transition period EU Chief Negotiator Michel Barnier was planning on using to bully Johnson around with is dead. January 31st Brexit happens.

And if no trade deal happens between then and the end of 2020, the U.K. leaves on WTO terms and the so-called Hard Brexit happens. Hard Brexit is back on the table and Parliament has been sidelined.

While this isn’t news anymore what it means is.

Given the context of his negotiations with French President Emmanuel Macron in October which secured the current Withdrawal Treaty, I think the way forward is clearer now.

The Macron Gambit

The key to understanding what’s happening is the ever-shifting dynamic between France, Germany and the U.K. in relation to their relationship with the United States.

Macron is pushing France to unseat Germany as the de facto rule-setter for the EU. He wants more integration at every level, but most importantly fiscally.

Macron understands that the euro is flawed because of a lack of fiscal integration. For the euro to survive at least three major things need to happen.

There needs to be a single entity capable of issuing and retiring Euro-zone sovereign debt. The ECB and the EU fiscal authorities need to have a relationship similar to that of the Federal Reserve and the U.S. Treasury Dept.

The euro has to weaken considerably to remove the garrote around the necks of countries like Spain, Portugal, Italy, Greece and even France.

Much of the existing sovereign debt needs to be converted into a Eurobond, doing away with much of the stock of debt as liabilities for member states like Italy and Spain. The ECB can lead the way with its $3 trillion it’s holding on its balance sheet.

In my podcast with Yra Harris from a few weeks ago, Yra made the point that the ECB has an enormous pile of gold it can use to back its new Eurobonds to sell this plan to skeptical markets.

So all the pieces are in place. But opposition to Brexit was actually undermining it.

Macron realized that the Brits would never accept betraying Brexit the way it had been planned. He saw the opportunity to cut the Gordian knot of Brexit and screw Germany at the same time.

Germany is dead set against any of these things occurring. It wants to continue with using the euro to underwrite its mercantilism to leverage its industrial prowess. It has benefited handsomely at the hollowing out of member states economies through internal trade advantages. And then, once they were broke used debt restructuring as a bludgeon to buy up their assets at pennies on the euro, c.f. Greece.

Italy was to be next on the block.

This is fundamentally why the euro is designed the way it currently is. It wasn’t a mistake, rather it was the plan. I know that sentiment will rankle my German readers, but that’s my take on the history.

They may have had their reasons for this, but this is classic colonialism.

But, what does this have to do with Brexit?

The Double Cross

Everything.

Macron installed Christine Lagarde as head of the ECB to push for fiscal integration and to politically blackmail the Germans into going along with it.

How? By threatening to write down or allowing default on the massive $850 billion in TARGET 2 liabilities German banks have in euro-zone sovereign debt on their balance sheets.

But there’s no way City of London and the crown would survive the British people’s anger at underwriting the costs of this shakedown and subsequent debt crisis.

Nigel Farage and the other hard Brexiteers understood that this was a key issue, but one that didn’t resonate with voters. Fishing rights and immigration get people to the polls, not bailing out German banks.

But, make no mistake, Farage, the old commodities trader, knows that breaking the British banking system free from the EU’s and put up a hard border, as it were, between them is the key to a successful Brexit.

And I suspect, after it was clear they couldn’t convince the British people otherwise, that City of London and the Crown saw this as well.

So, Macron and Johnson looked at the landscape clearly and with the blessing of the British political class negotiated a settlement.

By allowing Johnson and the U.K. to get clear of the fiscal and political storm, Macron gets even more leverage over Germany whose economy is the one hurt most by a hard Brexit.

The Germans run a huge trade surplus with the U.K. Cutting that down weakens the euro and Germany at the same time.

Germany will insist on bail-ins of depositors versus bailing out the Italian government. But Macron realizes the only way for the EU to survive the coming debt crisis is to over-ride Germany’s deflationary attitudes. They are going to have to print euros like no tomorrow.

He may throw Merkel a bone in the negotiations but it won’t be much. She lost the power struggle over the new European Commission.

Macron is many things, but he’s not stupid. He knows the Euroskeptic populists will eventually rise to power in Italy, Spain, Portugal and potentially even Germany. He knows he’s in trouble in France.

The miserable polling data is a reflection of the economic misery of German austerity taken too far.

The only way to placate them and keep them in the euro-zone and, ultimately, the EU is to give them debt relief and a bigger seat at the monetary policy table.

Matteo Salvini understands this. Viktor Orban understands this.

The Special Relationship

So the deal is pretty simple in the end. The collapse of Project Fear to dissuade the British people against Brexit forced a reconsideration on the ruling elite who finally felt a real threat to their power. Because if they betrayed Brexit one of either Farage or Jeremy Corbyn could have entered 10 Downing St. giving real voice to political change in the U.K.

I’m sure Prince Andrew’s relationship with Jeffrey Epstein didn’t help matters one whit.

This forced Macron and Johnson to make a deal which gave Johnson just enough room to win the election and blame the Remainers. This ends the stalling and Macron can use Brexit to his advantage within the EU to get what he wants.

No one gets everything they want here, but this is the best of a bad situation for everyone.

He’ll likely win re-election in November unless something profound changes. British neoconservatives, which Johnson represent, want to continue fighting against a resurgent Russia.

Macron and Merkel want rapprochement.

Brexit, in the end, may be more about the return of the special relationship between the U.S. and the U.K. while Europe splits itself off as an independent beast.

But with the euro being systemically destroyed by the ECB’s poisonous negative interest rates, I still don’t see a path forward even if Macron gets what he wants.

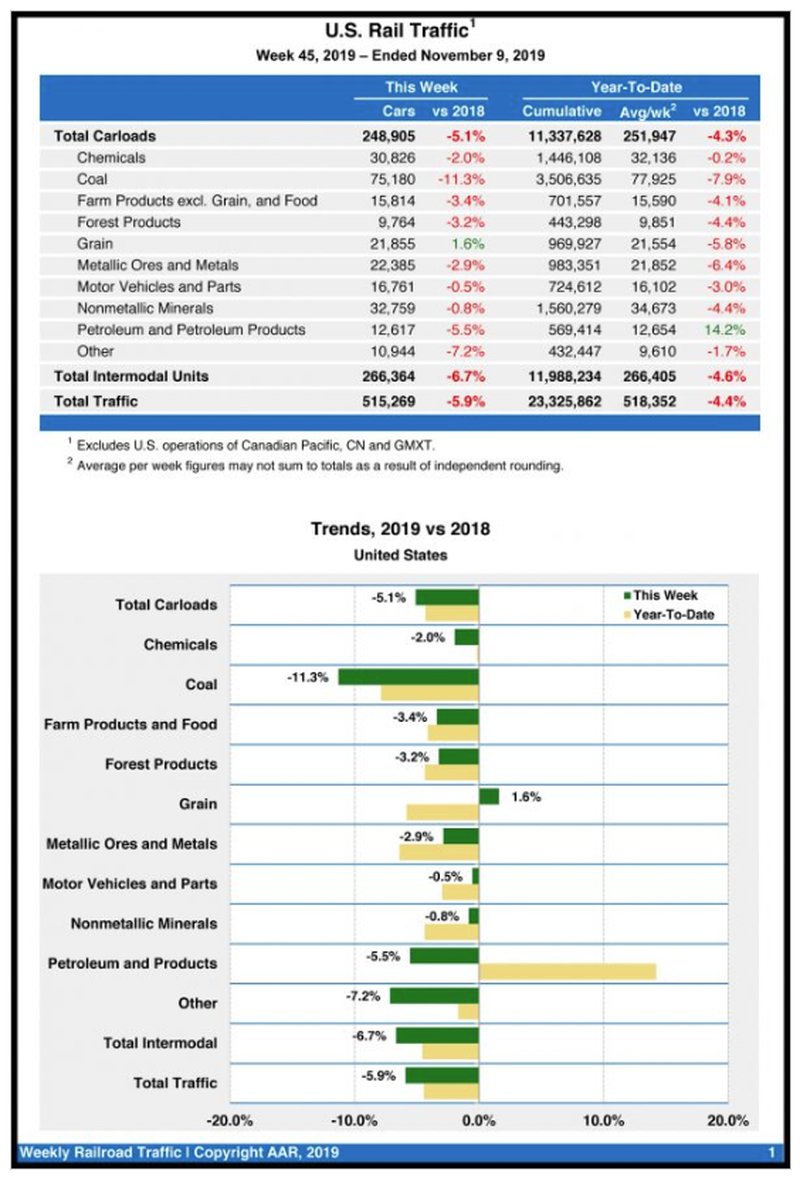

“Worst Market In 30 Years” – 400,000 Commodity Railcars Sit Idle Amid Industrial Recession

Wells Fargo, Citigroup, PNC Financial Service Group, and CIT Group accumulated hundreds of thousands of commodity hauling railcars in North America over the last decade. These banks believed railcars carrying coal, grain, and other commodities were going to be highly profitable but have recently turned out to be a major headache as many cars are now in storage because of new regulations and demand woes brought on by fluctuating commodity markets.

David Nahass, president of Railroad Financial Corp., which provides advisory services to railroad firms, told The Wall Street Journal that “the industry is suffering, there are no two ways about it. Lease rates are down, and there’s not a source of hope about when it will start to improve.”

The Journal, citing the Association of American Railroads (AAR), said about 400,000 railcars currently sit in storage with no use at all, and many are bank-owned.

CIT estimated railcar lease rates fell 10% to 15% in 2019 over the prior year. GATX Corp., a nonbank lessor, said specific car lease rates crashed 20% in 3Q Y/Y as an industrial recession worsened.

Wells Fargo is the largest railcar lessor in the US, with 175,000 total cars under management. The Journal provided no details on how many railcars from the bank were sitting idle.

The railroad crisis has hit certain types of railcars the hardest. For instance, coal shipments have plunged since 2011, which diminished the demand for coal hopper cars.

“It’s the worst market I’ve seen in my 30-plus years in the industry,” railcar appraiser Patrick Mazzanti told the Journal.

Mazzanti said new regulations have also been the reasoning behind many oil cars sitting idle, as these cars must be retrofitted with modern technology to meet new federal requirements.

Rail-leasing units at major banks are a tiny fraction of their overall balance sheets and won’t make or break the banks.

AAR’s report last month of plunging rail traffic and intermodal container usage could be a sign that the slowing industrial economy will continue to weigh on the rail industry and force banks to idle more cars in 2020.

Transportation is a barometer of how well the real economy is doing. And it just keeps getting worse as investors hope for “green shoots” next quarter.

France, already in the midst of a 4-week transportation strike has a new activist complaint against Sunday shopping.

Sacred Sundays

Besieged by online rivals, retailers are staying open Sunday afternoons with automated cashiers. Critics see an invasion of American-style consumerism.

French labor rules prohibit most shops from employing workers past 1 p.m. on Sundays. But as e-commerce and online giants like Amazon usher in an era of round-the-clock spending, retailers are amping up the use of automated cashiers to help them compete.

The move has caused an outcry in France, where Sundays are traditionally a rest day for workers and families. While self-checkout machines are often used alongside cashiers, labor unions say that tilting toward fully cashierless operations threatens the French way of life by encouraging American-style consumerism and automation, putting thousands of jobs at risk.

“Sundays are sacred,” said Patrice Auvinet, the head of the General Confederation of Labor union in Angers, a midsize city in western France. “If they change that, it will change French society. And if automated cashiers become normalized, it will have a catastrophic impact on workers.”

At the Angers store, which employs 115 in a working-class neighborhood, Groupe Casino is having salaried employees clock out as usual at 12:30 p.m. on Sundays, then bringing in security guards, hired through another company, to keep the store open through evening. Groupe Casino had been operating 130 smaller stores in Paris and other cities using self-checkout machines to let consumers shop until midnight or even around the clock.

Chaos mounted when the protesters were joined by local members of the Yellow Vest movement, which arose last year to protest stagnating wages and declining living standards. Denouncing what they said was an erosion of workers’ living standards, they charged through the store, dumping produce in the aisles and heckling customers who were using the automatic checkout machines.

Travelers in France faced frustrations on Wednesday, as the transport strike extended into its fourth week and coincided with the Christmas holiday.

Thousands of trains were cancelled or delayed, while taxis, ride-sharing services and car rental agencies were overwhelmed by demand. The underground metro in Paris was shut down, except for two lines.

At the center of the labor dispute, which sparked widespread protest and strikes lasting over two weeks, are reforms that would do away with 42 different pension schemes and replace them with a points-based system.

Additionally, the reforms seek to set 64 as the age until which people must work to earn a full pension. That is two years beyond the current official retirement age in France.

Even Paris Opera workers, who can retire at 42, joined the strike. On Tuesday, some 40 dancers performed Swan Lake to passers-by on the steps outside the opera house with banners warning: “Culture in danger.”

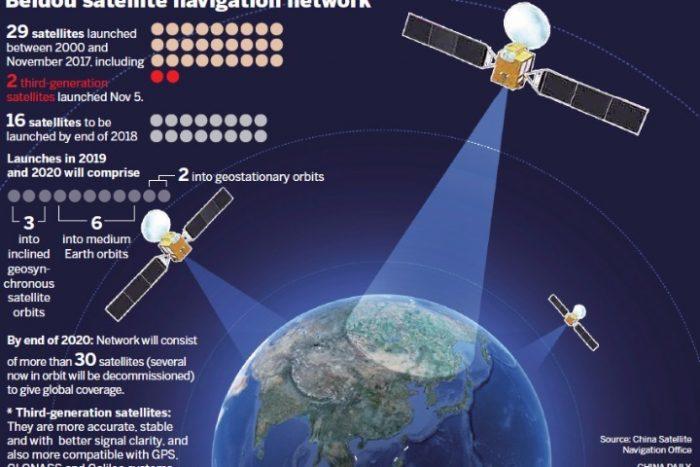

China announced Friday that it was nearing completion of its new global positioning system (GPS) network as it prepares to dominate the world’s next generation of telecommunications services and further decouple from the US’ GPS network, reported Nikkei Asian Review.

China’s Beidou network of satellites is expected to be completed at the end of 1H20 when the last two of 35-satellites will be launched.

The Beidou GPS network will be 17% larger than the current 30 satellites operated by the US-owned GPS.

The strategic purpose of China’s new GPS is to decouple from the West’s GPS and provide service to Southeast Asia, South Asia, Africa, and Eastern Europe.

China’s rapid advances in fifth-generation wireless communications (5G) and satellite technology present a significant challenge to the US hegemony over the global telecommunications infrastructure.

News of GPS decoupling between China and the US comes as tensions ease over trade. Still, it seems the world’s two largest economies have entered a new period of sustained competition that will result in further decoupling.

China’s Beidou network of satellites will be able to support 70% of all Chinese smartphones.

Ran Chengqi, a spokesperson for the Beidou Navigation Satellite System, said the Beidou network plays a vital role in 5G, an area where Huawei Technologies is the world’s leader in development.

“The integration of Beidou and 5G is an important sign on the path toward China’s development of information technology,” Chengqi said.

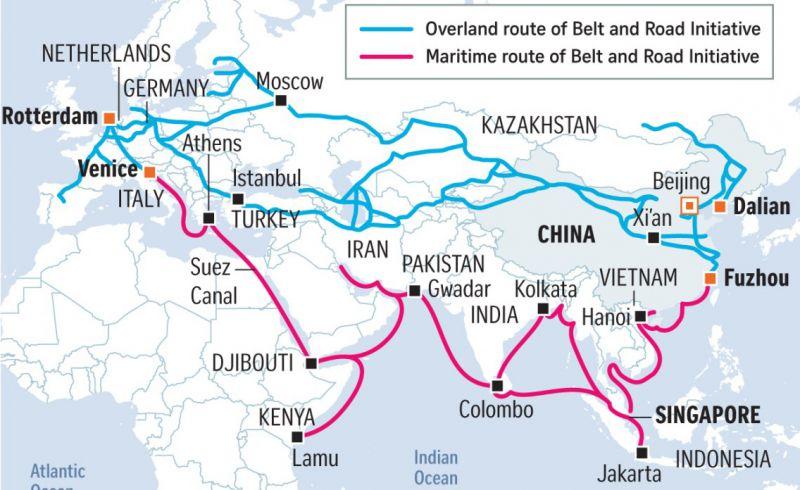

Beidou’s network coverage is expected to span across countries where the Chinese have developed Belt and Road infrastructure initiative projects.

Beidou “has entered into a new era of global service,” he said, “benefiting ASEAN, South Asia, Eastern Europe, West Asia, and Africa in precision farming, digital construction, and smart port construction.”

Beidou and 5G will help China usher in self-driving vehicle development, a sector funded and supported by Beijing.

The Beidou GPS network will be essential for achieving Beijing’s “Made in China 2025” plan to transition the country from the world’s factory to produce higher-value products and services.

It will also allow China to expand its global influence without relying on another country to provide satellite service. This will be crucial in times of conflict, where the US will no longer be able to shutdown down GPS to China.

The rush to decouple is occurring as a great power competition between both countries has sparked Cold War 2.0.

“At least since the events at the Cologne cathedral square on New Year’s Eve in 2015 people apparently feel more and more unsafe,”said Oliver Malchow, the chairman of one of Germany’s two largest police unions. He was referring to the mass sexual assaults committed mainly by Arab and North African men at the Cologne cathedral square on New Year’s Eve more than four years ago. Malchow was also referring to new statistics, which show that approximately 640,000 Germans now have licenses for gas pistols — a large increase since 2014, when around 260,000 people had such a license. A gas pistol fires loud blanks or tear gas cartridges and is only potentially lethal at extremely close range.

The new statistics, according to Malchow, showed a “latent sense of insecurity” in the population. The number of real firearms owned privately also reportedly increased in 2018 — by 27,000 over the previous year. In Germany now, 5.4 million firearms are privately owned, most of them rifles.

A recent annual poll, conducted in September, confirms Malchow’s estimate: Every year since 1992, R+V, Germany’s largest insurance firm, has been asking Germans what they fear most. “This year, for the first time,” according to a report in Deutsche Welle, “a majority said they were most afraid that the country would be unable to deal with the aftermath of the migrant influx of 2015”. Fifty-six percent of those polled said they were scared that the country would not be able to deal with the number of migrants. This September marked exactly four years since Chancellor Angela Merkel opened Germany’s borders and allowed in almost a million migrants. However, Ulrich Wagner, professor of social psychology at the University of Marburg toldDeutsche Welle:

“It’s really got more to do with the fact that politicians and media discuss this issue a great deal — which triggers fear… For example, in the latest study, fear of terrorism has clearly gone down. We simply don’t discuss this issue as much as we used to, and that means that people feel safer.”

What the professor appears to imply is that you can solve a crucial societal issue, not by debating its ramifications and publicly seeking to find solutions to it, but by not talking about it, thereby lulling the public into a false sense of security by pretending that the problem does not exist.

The terror threat in Germany has not, in fact, disappeared. Just this March, 11 men were arrested on suspicion of planning a terrorist attack in Germany. Police told the media that the goal of the attack had been “to kill as many infidels as possible” by using firearms and vehicles. According to police, the Islamist group had already organized the rental of a large vehicle: money had been raised and weapons dealers had been approached. “The terror threat in Germany remains high,” the media reported in April. “According to security authorities, there is currently no concrete risk of an attack. But officials are prepared for any development”.

German media also reported in April that German authorities have prevented 13 terrorist attacks in Germany since 2010 and that, according to the Federal Criminal Police Office, all of them were “linked to Islamic extremism”. As recently as October, a Syrian man plowed a stolen truck into the back of a line of traffic, ramming eight cars together and injuring seven people.

Professor Wagner does have a point, however — people do talk a lot less publicly about crucial societal issues: As previously reported by Gatestone Institute, a May 2019 survey, conducted by Institut für Demoskopie Allensbach for the newspaper Frankfurter Allgemeine Zeitung, showed that discussing certain issues in Germany has become taboo. While the survey did not specifically mention terrorism, it concluded that “The refugee issue is one of the most sensitive topics for the vast majority of respondents, followed by statements of opinion on Muslims and Islam”. As an example, 71% of Germans say, according to the survey, that one can only comment on the refugee issue “with caution”.

Also, according to the annual poll on what Germans fear most, mentioned above, the level of fear in the former East Germany is more than 10% higher than in the West. According to Deutsche Welle:

“The paradox is that fewer migrants and fewer refugees actually live in the east than in the west, and yet the levels of fear are higher,” says psychologist Ulrich Wagner. He explains that people who have had personal interactions with foreigners are less likely to believe unfounded horror stories about criminal refugees. “And in the east of Germany, people simply have fewer opportunities to meet refugees and debunk those myths.”

As for that hypothesis, it may be more likely, not that fear is higher, but that people in the former East Germany are less afraid of telling pollsters how they really feel. As the survey on German self-censorship has shown, 57 % of Germans say that “increasingly being told what to say and how to behave” is getting on their nerves. Germans from the formerly communist East complain more about this than the average German, as they have “fresh historical memories of regulation and constriction”.

August Hanning, a former president of Germany’s Federal Intelligence Service, recently confirmed that the “latent sense of insecurity” is not due to public fear-mongering. During a visit to the UK, Hanning said that Chancellor Angela Merkel had endangered security in Germany with her historic decision to allow virtually unrestricted immigration into the country by creating a “security crisis” for Germany and the other member states of the European Union.

“We have seen the consequences of this decision in terms of German public opinion and internal security – we experience problems every day.

“We have criminals, terrorist suspects and people who use multiple identities…

“While things are tighter today, we still have 300,000 people in Germany of whose identities we cannot be sure. That’s a massive security risk.

“Moreover, that decision led to the rise of the extremist right, and that’s another security risk, too…”

While Germans are afraid to speak publicly about migrants, refugees and Islam, a recent study conducted by Bertelsmann Stiftung showed that roughly every second German considers Islam to be a threat. Professor Wagner’s theory above, that not talking about certain issues makes fears go away, is, apparently, false. According to the study:

“Overall, about half of those surveyed perceive Islam as a threat. This proportion is higher in eastern Germany, at 57 percent, than in western Germany (50 percent). These findings, recorded in spring 2019, are largely similar to the results of previous Religion Monitor surveys taken in 2013, 2015, and 2017.”

According to Yasemin El-Menouar, Bertelsmann Stiftung’s expert on religion, according to the organization’s website, “Evidently, many people nowadays view Islam more as a political ideology and less as a religion and therefore not deserving of religious tolerance.”

‘Mass Stabbing’ At Jewish Hannukah Celebration In New York, At Least 5 Injured

At least 5 people have been stabbed after a black male entered Rabbi Rottenburg’s Shul, located in the Forshay neighborhood in Monsey, New York, and pulled out a machete.

As VosIzNeias.com reports, the alleged assailant pulled off the cover and stabbed at least 3 people. One of the victims was stabbed in the chest.

The perpetrator then ran out and escaped in a vehicle. His plates were spotted before he left, and the police are currently searching for him.

Videos of the stabbing attack began disseminating on social media.

Motti Seligson, director of media for Chabad.org, told The Jerusalem Post that the congregants, Hassidim, were gathered for a Hanukkah party and confirmed the preliminary details of the event.

Video from the scene of the stabbings at a synagogue in Monsey where Chassidim were gathered for a Hanukkah celebration. pic.twitter.com/wQhWp9SrdA

The Orthodox Jewish Public Affairs Council said five people, all Hasidic, were transported to local hospitals with stab wounds.

At 9:50 this eve, a call came in about a mass stabbing at 47 Forshay Road in Monsey (Rockland County; 30 miles North of NYC). It’s the house of a Hasidic Rabbi. 5 patients with stab wounds, all Hasidic, were transported to local hospitals.

“We are closely monitoring the reports of multiple people stabbed at a synagogue in Monsey, NY (Rockland County),” a representative of the New York City Police Department Counterterrorism Bureau tweeted.

Hatzalah emergency response team is on scene and victims have been transferred to the hospital.

As JPost.com notes,this is the second stabbing attack in Monsey in the last two months. In November, a man jumped out of his car in stabbed a father on his way to synagogue, gauging his eye. In the last week, a spate of antisemitic crimes has swept the city.