“Contagion Runs The Risk Of Spreading” In India’s Financial Sector, Rating Agency

India, one of the largest emerging markets in the world, is at serious risk of widespread contagion ripping through its banking sector as many large financial companies have already seen their equity value halved over the last 12 months, S&P Global Ratings said in a report on Wednesday, also reported by Bloomberg.

India’s shadow lenders, also called non-banking finance companies, have been under severe pressure since the collapse of Infrastructure Leasing and Financial Services (IL&FS) last Sept., which was on the 10th anniversary of the bankruptcy of Lehman Brothers.

“India’s finance companies are among the country’s largest borrowers. A substantial part of this funding comes from banks. The failure of any large non-banking financial company or housing finance company may deliver a solvency shock to lenders,” said S&P Global Ratings credit analyst Geeta Chugh.

According to the report, the next big banking failure in India could run the risk of disrupting local credit markets, interbank markets, payments, and even damage economic growth.

“This contagion runs the risk of spreading to real estate companies too. Finance companies are the largest lenders to this segment and any failure among such institutions could jeopardize credit flows to developers,” Chugh said.

“The credit profile of a bank could deteriorate sharply due to outsized exposure to weak entities, huge market or operational losses, or significant deposit withdrawals if the depositors lost confidence in the bank,” Chugh added. “A governance deficit could also quickly turn to a trust deficit, hurting the stability of a bank.”

It’s likely that if one Indian bank fell, “the contagion could spread to other banks perceived to be struggling with the same problems as the failing bank,” S&P warned.

S&P’s report comes several weeks after Punjab Maharashtra Co-operative Bank (PMC) collapsed, while contagion at the moment is unknown, thousands of depositors have been locked out of their accounts, likely to never see their savings again.

Customers of PMC Bank prepare for a dark Diwali as their Laxmi is locked away by those in power. Their cries for help fall on deaf ears as the BJP-Sena govts. at state and centre seem to believe that Sab Achha Hai.

S&P says if the banking crisis widens in India, the Indian government will act “swift and orderly” to limit the contagion — but with a synchronized global slowdown, and emerging markets getting slammed the hardest — it’s likely that a large banking crisis is brewing in India.

The National Development and Reform Commission (NDRC) has approved 21 projects, worth at least 764.3 billion yuan (US$107.8 billion), according to South China Morning Post calculations based on the state planner’s approval statements released between January and October this year.

The amount is more than double the size of last year’s 374.3 billion yuan (US$52.8 billion) in approvals recorded over the same period, which included 11 projects such as railways, roads and airports.

Local governments have been under increasing pressure from Beijing to support the economy, but they have less budget room due to lower tax revenues after the central government over the past year ordered individual and business tax cuts.

To fill the gap, Beijing has allowing local governments to sell more special purpose bonds, whose proceeds can only be used to fund infrastructure projects. At the beginning of this year, the Ministry of Finance raised the quota for special bonds to 2.15 trillion (US$302 billion) from 1.35 trillion (US$190 billion) last year. And when local governments came close to exhausting their annual quota set this autumn, the central government brought forward a portion of their 2020 quota so they could continue to raise funding for new projects.

Infrastructure Urgency

Michael Pettis, Finance Professor, Peking University, and author of the China Financial Markets website has an interesting take infrastructure projects.

Analysts had expected China to announce more policy easing measures soon as the world’s second-largest economy comes under growing pressure from escalating U.S. tariffs and sluggish domestic demand.

The People’s Bank of China (PBOC) said it would cut the reserve requirement ratio (RRR) by 50 basis points (bps) for all banks, with an additional 100 bps cut for qualified city commercial banks. The RRR for large banks will be lowered to 13.0%. The PBOC has now slashed the ratio seven times since early 2018. The size of the latest move was at the upper end of market expectations, and the amount of funds released will be the largest so far in the current easing cycle.

The broad-based cut, which will release 800 billion yuan in liquidity, is effective Sept. 16. The additional targeted cut will release 100 billion yuan, in two phases effective Oct. 15 and Nov. 15.

Real Growth

With real growth at probably half reported levels – which measure growth in activity, whether or not it is wealth enhancing – lower-than-expected growth rates are not a bad thing: they mean credit growth, while still too high, is slowing.https://t.co/s8aCyK2SOQ via @scmpnews

World Bank has just cut its GDP forecast for China to 6.1% in 2019, 5.9% in 2020, 5.8% in 2021. For this to happen, debt-to-GDP ratios would have to rise by at least 12-15 percentage points, which I think is very unlikely. I’ll bet 2021 growth is below 5% (still way too high). https://t.co/1M5ljprfJW

I suspect that the only thing driving “substantial progress” is election pressures in the US. I don’t think any agreement between Washington and Beijing will matter for more than few months.https://t.co/aRFimMFljZ

“There are not many economically viable projects for us to take on,” an official at Sichuan Development told the FT.

“We have plenty of bridges and roads already.”

GDP Formula

GDP = C + I + G + (X – M)

GDP = private consumption + gross investment + government investment + government spending + (exports – imports).

Whether or not the projects are viable, government spending adds to nominal GDP.

If the government paid people to spit at the moon it would add to GDP.

Arguably, that’s a far better use than dropping bombs and making enemies in the process.

Not Writing Down Losses

I suspect that the only thing driving “substantial progress” is election pressures in the US. I don’t think any agreement between Washington and Beijing will matter for more than few months.https://t.co/aRFimMFljZ

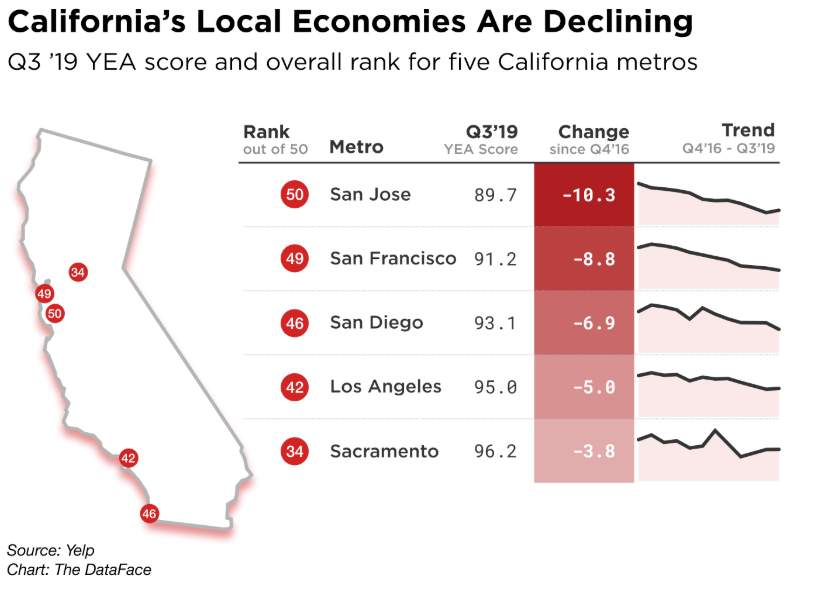

Consumer Activity Falters In California’s Largest Metros, Yelp Warns

The US economy is rapidly decelerating into year-end. Inflation, industrial, and employment down cycles are well underway, which is expected to deepen in the near term. This fall, the economy experienced a rare transmission of weakness from manufacturing into services and the consumer. Contagion is here — and there are minimal measures the government and central banks, at the moment, can do to prevent the slowdown from broadening.

To get a more precise picture of consumer health, which powers about 70% of the economy. We turn to new alternative data from Yelp, that is showing, economic stagnation across major metropolitan areas in California, the country’s most populous state and largest economy.

The report is intriguing because it indicates that California’s massive economy and all the hot money from the tech boom is cooling — an ominous sign that suggests a countrywide consumer slowdown is imminent. And to make matters worse — the slowdown in consumer activity is happening right before the holiday season.

Yelp data from 3Q19 shows the brunt of the consumer activity slowdown is in San Jose, San Francisco, San Diego, and Los Angeles. These four cities had the weakest consumer activity not seen since 4Q16.

“California’s biggest local economies are continuing to struggle,” Carl Bialik, Yelp’s data science editor, told Bloomberg.

“Construction limits and increasing rent are pushing consumers and workers farther from businesses, contributing to continued quarterly declines in some of the state’s biggest metro areas, with retail and restaurants taking the biggest hits.”

Yelp tracks over 100 million users across the US and can track users in specific regions and metro areas. Researchers track users based on their activity in various sectors of the local economy, including shopping, automotive, local services, home services, professional services, restaurants, food, and nightlife.

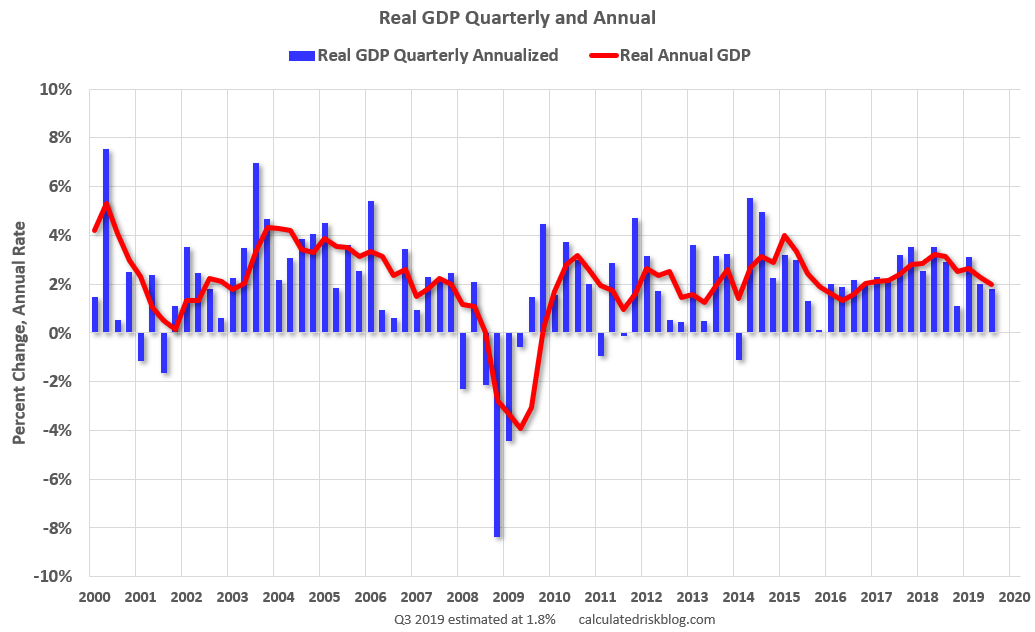

Yelp’s consumer data shows that it’s likely inline with declining 3Q19 GDP figures, expected to print at an annualized pace of 1.8%.

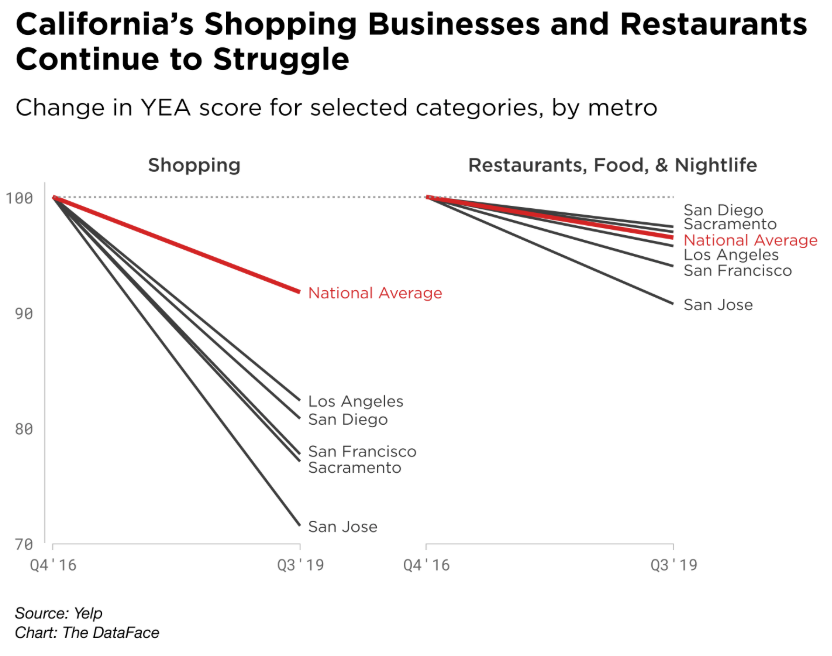

Yelp said, “California’s shopping businesses have been hit the hardest. Shopping ranks at the bottom in each of the five Golden State metros we track, among the six major sectors of the local economy included in YEA (the other sectors are auto; restaurants, food, and nightlife; professional services; home services; and local services). Stores selling shoes, cellphones, and women’s clothing have fallen sharply in all five California metros. Retail rents in San Jose and San Francisco have surged in the last decade. The fate of retail and restaurants is intertwined: Retail stores attract foot traffic which benefits nearby restaurants, and restaurants similarly bring business to neighboring stores. The rise of food-delivery services can separate restaurant customers from after-dinner shopping. And our data bears this out, with restaurants, food, and nightlife categories struggling in all five California cities. The declines range from 2.6% in San Diego to 9.3% in San Jose, with San Francisco near the upper end at 6%.”

It’s believed that California consumer activity is a lead on the rest of the country.

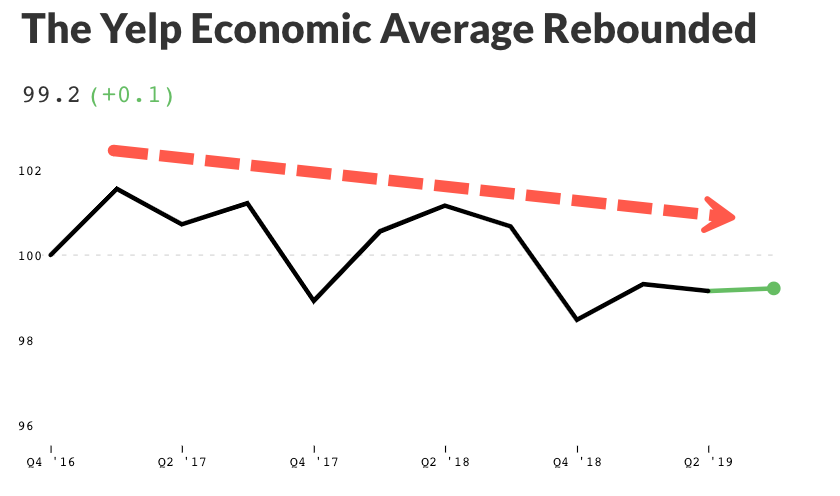

Yelp Economic Average (YEA), a benchmark of consumer strength countrywide, barely rose in 3Q, up .07% above 2Q levels. Yelp blames the trade war, recession fears, impeachment fears, out of control rents, and surging health care costs on a weakening consumer.

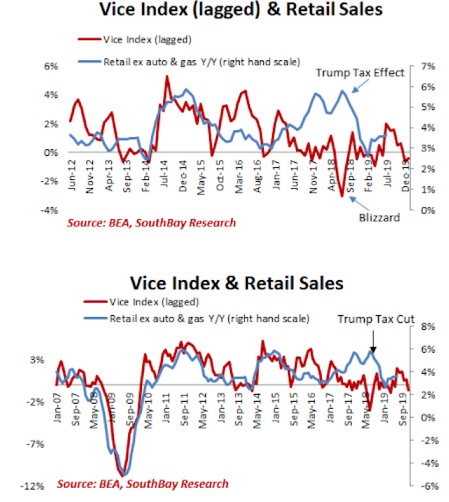

For more color on the overall US consumer health, SouthBay Research has a “Vice Index” that tracks spending on gambling, alcohol, drugs, and prostitution. The index shows the consumer has been weakening for nearly a year thanks to a hangover after President Trump’s tax cut.

Shown below is SouthBay’s proprietary Vice Index (lagged by six months), which dropped to its weakest level since February of this year. Might indicate that retail sales for the final stretch of this year will remain weak through the holiday season.

Alternative data, if it’s from Yelp or SouthBay, is showing that consumer weakness could persist through year-end. This could undoubtedly spoil the hopes for stock market bulls who now suggest that consumers will power the economy through 2020. Betting on the consumer this late in the cycle could be dangerous.

Since 2013 the real government whistleblower, Edward Snowden, has been in political asylum in Russia, where he continues to write books and tell his story of how as an employee of the NSA he discovered that the government was breaking the law in constructing a massive surveillance state. Today, the surveillance is such a ubiquitous par of our lives, that people have come to see it as a normal part of everyday life, and hardly any politician bothers to work against it. It’s here to stay, sadly.

Recently, Snowden published a book entitled Permanent Record, which was immediately attacked by the US government, prompting them to sue Snowden for all of the profits related to the book. The government does not want you to hear his message. Ironically, though, Permanent Record became an instant bestseller, and Snowden’s popularity has only increased in recent years.

In a newly released podcast by Joe Rogan, Snowden calls in from Russia, talking about his understanding of how corruption from within has led the permanent establishment of the massive and highly profitable surveillance state which has filled the coffers of defense contractors and corrupt politicians. Snowden discusses the fact that all three branches of the U.S government are corrupt and that for admirable government employees who witness government agencies breaking the law have no available channels to blow the whistle and get the truth out to the American people.

Interestingly, in the podcast Snowden also talks about his experience on 9/11 when he was working for a small business out of a house on Fort Meade near the DC metro area. He describes how the base, which is home to a vast portion of the U.S. Military’s intelligence apparatus, was immediately dispatched and the base cleared as soon as the events of the day began to unfold.

Snowden points out how strange this was, considering that all of the personnel on the base would have been more than willing to take the risk of being attacked in order to fulfill the duty they has all signed up for, that of protecting the American people. Snowden’s point here is that the intelligence agencies were essentially taken off-line at the most critical moment in the entire history of their existence.

So, why did the directors of these agencies send all of these resources home on 9/11?

Snowden continues…

“It says so much about the bureaucratic character of how the government works. The people who rise to the top of these governments. It’s about risk management for them. It’s about never being criticized for something…

Everybody wants to believe in conspiracy theories because it helps life make sense. It helps us believe that somebody is in control… that somebody is calling the shots, that these things all happen for a reason. There are real conspiracies… but when you look back at the 9/11 report and when you look back at the history of what actually happened, what we can prove. Not on what we can speculate on, but what are at least are the commonly agreed facts… it’s very clear to me, as someone who worked in the intelligence community… that these attacks could have been prevented.”

He goes on to explain that the government’s excuse for not preventing the attacks was essentially due to the fact that the various intelligence agencies were unable to effectively share information, coordinate investigations, and work together. Snowden is implying that 9/11 was essentially allowed to happen so that the mass surveillance state, which is insanely profitable to certain people, could be created. And it has since been created.

Considering that the Patriot Act soon followed 9/11, and in the nearly two decades since, the massive warfare and surveillance state continues to balloon and spread its reach into American citizen’s lives and around the globe, Snowden’s assessment seems rather accurate.

NBC Refutes Its Own ‘Trump Is In Trouble Due To Manufacturing Recession’ Narrative

Readers should know by now that President Trump’s aggressive trade war with China didn’t start the synchronized global slowdown, but his trade policies have certainly amplified it.

So NBC News, like many other media outlets and even global leaders today, are laying the groundwork, or economic narrative, pinning the slowdown, or manufacturing recession, and or even next financial crash on the president.

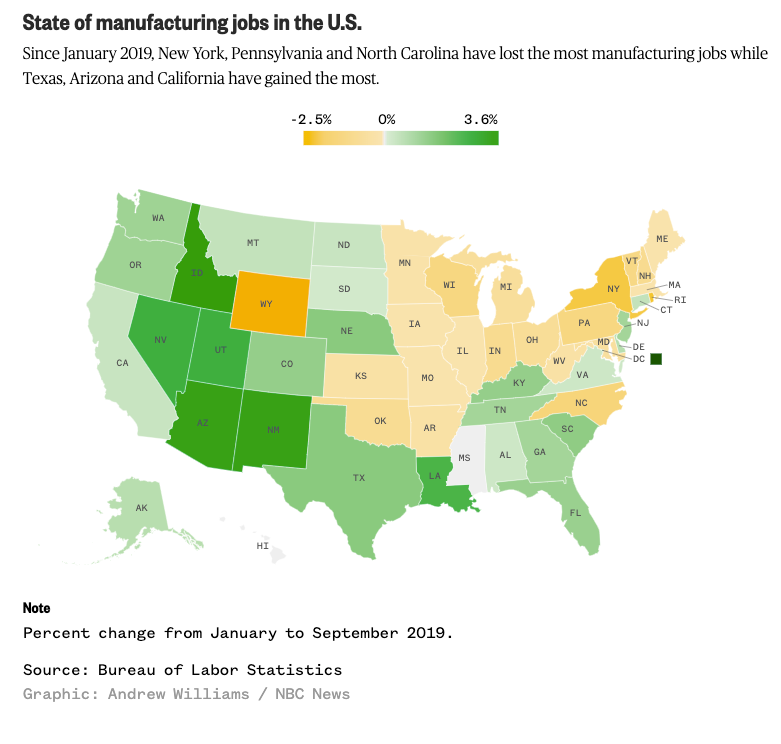

NBC’s latest report on the manufacturing recession ripping through Pennsylvania, North Carolina, and Wisconsin, outlines how a “protracted and chaotic trade war” led to the downfall of a seven-decade-old factory in rural Kreamer, Pennsylvania, called Wood-Mode, who recently laid off 900 blue-collar workers.

NBC interviews several former employees of Wood-Mode, who gave their sad stories about how the company struggled to make a profit amid “Trump’s protectionist measures and bruising trade war.”

At the end of the article, so far down where most people wouldn’t read, the author chose to lay out the facts from one former employee, destroying the original narrative pinning the company’s financial woes on President Trump’s trade policies. By saying:

“Wood-Mode was having troubles before Trump took office,” said former employee Michele Sanders.

“I don’t think he had anything to do with it [trade war], but I don’t know that he’s helping matters,” she said.

So it wasn’t President Trump’s trade policies that were responsible for Wood-Mode’s demise but rather company mismanagement, competition, and or macroeconomic headwinds that were present before the president took office.

As we’ve noticed recently, corporate leaders, management teams, government officials, and monetary authorities across the world are quickly scapegoating the president’s trade war for their failures. Why not, right?

The ability of the president to regain the economic narrative and correctly place the blame of the manufacturing slowdown and upcoming financial crash on the Fed has yet remained to be seen. It’s unlikely that the president could win such a battle at the moment since everyone and their mother is blaming their issues on the trade war — not the Fed. Tell a big enough lie, and everyone will eventually believe it…

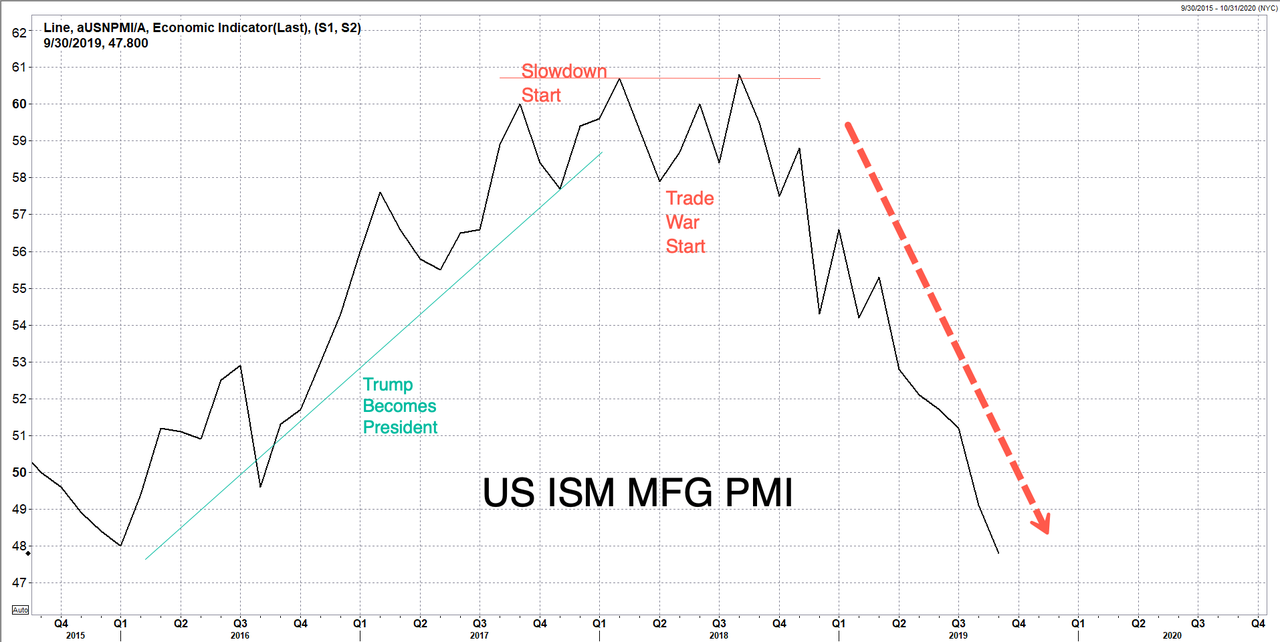

As shown below, growth rates in US manufacturing slowed several quarters before the trade war began.

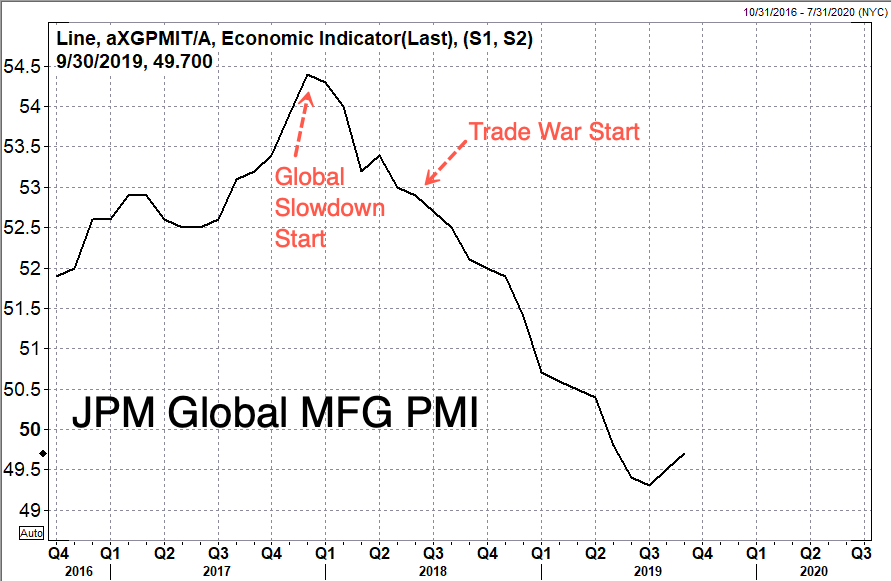

Also seen in the JPMorgan Global Manufacturing PMI, the world’s manufacturing sector slowed before the trade war started — a common miss by many economists who conveniently blame the trade disputes on the downturn.

So it’s hilarious how NBC criticizes the president for the death of Wood-Mode due to the trade war, but then at the end of the article indicates via a quote from a former employee that the company was already on shaky grounds before the president entered the office.

This type of bias reporting is everywhere — and by the way, it’s creating an economic narrative that is overpowering the Trump administration. It’s likely that the president will get the blame for the next crash — and the Fed will say, “I told you so.”

Abnormal circumstances oblige people to be creative and innovative.

The hyperinflation in Venezuela made wages a complete joke. We’re talking about the equivalent of $3 USD per month. The inability of the government (by far the largest employer in Venezuela) to provide raises as this hyperinflation destroyed the remaining acquisitive power people once had and condemned millions of people to misery, hunger, and deprivation.

This has originated a myriad of protests and demonstrations all over the country. Entirely useless, as the country is not a democracy nor there are any high-level functionaries that are going to do something. They’re too busy trying to evade the sanctioning of other countries while looting whatever is left of the national treasure.

The few actions taken are just for propaganda, the most powerful tool of the communist world. That’s why a highly educated population will never be subject to such a level of manipulation.

The problem is so complex, that it´s going to be impossible to explain in such limited space. I have been trained (mostly because of my line of work and my studies) to think logically and to expand my field of vision to notice some aspects that normally people without so much training don´t see. Those who know me personally know that I don´t talk too much about stuff I am not sure of.

Here’s why the collapse of Venezuela was engineered.

In this instance, I will allow myself to make an assumption because there are strong indicators that can support my theory. Our collapse was engineered. There is no simple reason to have committed suicide by condemning our main income source, the oil industry, to oblivion.

This is not a political article by any means. This is an article written by the request of one of my readers of the Prep Club Facebook group.

This being said, this collapse was generated to bring instability to the entire Latin America region as you´re already aware. The main reason, I think, was to kick Venezuela out of the oil producer countries to take over their quotas in the OPEC that were expected to be close to 3 million barrels per day, a substantial amount of money. Screwing us 30 millions of Venezuelans in the process, of course.

Wages are obscenely low

Small change for the billions of dollars involved. There is no reason to keep minimum wages under $3 monthly when a kilo of ground meat costs that much. It´s simply not logical. The State that once was the biggest employer is broken and looted. They are not doing other jobs but trying to keep people quiet, by coercion and food blackmail, deceiving propaganda, and whatever other means they have. This way, the looting can continue “unnoticed”.

The oil industry in my area used to provide lunch at cheap prices for employees. Our laws dictate that if the work area is over one hour away from the employee´s residence, lunch must be provided. This is no longer happening in that area, and the work schedule, as a result, was cut by half. People work until 11:00 AM because the company can´t provide lunch.

Those relying solely on a wage don´t survive. It´s this simple. Those with a parallel income source (like myself back in the day) survived and could keep getting the needed equipment to keep prepping. Those with a business non-related to essentials, like clothing/shoes, water, hygiene items and/or food, have it rough because there is not too much market nor liquidity to keep them in an economy based on survival.

Some with jobs like plumbing, building/repairing, and electrician technics, have been able to keep in business, although barely. There are some interesting exceptions, though. Some companies have been able to export what they produce, at least partially, and this is a huge oxygen injection for them because they don´t have to depend on a corrupted currency exchange system to buy dollars and pay their providers. Most of these companies pay their employees in two currencies: the national, devalued worthless Bolivar, mostly to avoid being sued by lack of payment and comply with the local laws (it´s illegal to pay workers in foreign currency) and euros or dollars.

Scammers and organized criminals are profiting.

However, there are unscrupulous patrons that pay their workers in Bolivares, even though when they export and receive dollars. These receive a huge profit, something incredibly high in margin…exploiting their workers.

There is a similar system to the food stamps, called the “Cesta tickets” (“Basket” tickets). This was created to provide means to get food without inflating the final salary and the patron can avoid paying at the end of the year the amount corresponding according to our laws, which obliges them to pay a monthly percentage of the perceived salary.

Of course, the mafias soon took advantage of this system: they bought the tickets, exchange them per cash (banknotes very hard to find in the proper amounts) at 70% of their value. This seemed to work because many food providers did not want to accept the tickets…surely they were as well part of the mafia.

Meanwhile, hyperinflation continues.

I´m not by any means economist, but the destruction of the economy is so vast, that there is even more hyperinflation now…even with the dollars. An air conditioner can cost 550$ one week, and the next one 600$. That´s entirely unacceptable. This kind of speculation is deeply embedded in the psyche of the Venezuelan merchants.

Oh and not just Venezuelans. Most of the white line merchants are Lebanese, or Syrians, even Chinese. There is an interesting anecdotic data about this. I found the other day in a national wide-spread chain store like Home Depot, a nationally produced electric fan. It´s not rocket science to produce a fan, after all, isn´t it? Interestingly, I asked for that very same brand in another shop, owned by some middle-eastern family. They said that they did not have that brand, but some others that they claimed to be “better”. I ask how do they know it is better if they don´t even know the national brand.

I ended scolding them for not supporting the national production, but instead to make profits bleeding the money out of the country that received them with open arms, in detriment of their own citizens. I never bought equipment nor furniture again from anyone similar to them. I decided to buy my own tools, and start building my own furniture company…back then in 2014, when the entire system started to crumble and almost crushed me and my family.

It´s one of the goals of my life, indeed. Entire forests are disappearing in humongous factories to manufacture cheap, poorly made (by semi-slaves workers) furniture that in a few years is going to fall apart, to end in landfills all over the planet. Or we stop that now, or our grandsons will have to pay premium money (very likely to the insanely rich descendants of foreign companies who devastated the world in the first place) to be able to walk in a park and see how the forest looked like.

I grew up running in a tropical forest. I never was so happy in my entire life. I want my descendants to be able to do it, too.

Latin America is corrupted beyond repair.

For those who don´t know Latin America, this can look like an entire corrupted land. Maybe you´re right. There is an entire mountain of things we have to fix.

I am sure now, that the only way to fix is to destroy it, and then rebuild. The structure is entirely rotten and you can´t get anything good with those foundations. In order to make a decent living in Caracas, the capital city, you need 300$. That is, assuming you are the owner of your home. Most people survive with much less than that. By decent I mean well-fed, and some entertainment. This is not the case for many of them. There´s plenty of people surviving because of their relatives abroad pumping money into their accounts, just like Cubans.

Cuba has always been a parasitic society. They don´t produce, and ship overseas fake medical personnel (desperate to escape of that jail of an island) charging the governments stupid enough to accept them absurd amounts of money…money that is not enjoyed by the so-called “doctors” entirely but a small fraction. It´s a modern slavery system that the world accepted as “normal”. It´s a real shame for the rest of the world that this situation is happening in our supposedly modern world.

Coming back to Venezuela, the economy is so distorted because of the elimination of 95% of the country´s income, the oil production. The only way to reactivate it, is to reset it. A full halt, and to make mandatory the use of a foreign currency already solid and established.

I hope this is enough to provide a more complete overview of how things are in Venezuela these days and the paramount importance of prepping. I´ve mentioned in other articles how easy we had it compared to this fellow in the picture. No coat, keeping warm with old blankets. No shoes, lots of people walking with sandals and socks.

I had an emergency fund, and even with this, I had to ask assistance to get my family out. Thanks to you, readers. And I will never have enough words to thank you for that.

The Next Big Seller Are Chinese Firms, Looking To Offload Western Companies

Before the next recession strikes and valuations reset, who around the world will be the next bagholder? The Chinese have understood in the last several years, it could be them. Their recent acquisitions of foreign companies were paid at hefty premiums, and now, it seems that with an imminent global trade recession, these folks are ready to dump.

Bloomberg outlines a significant problem. Since the Chinese overpaid for many foreign companies in the last several years, volatile markets across the world have made it impossible at the moment to sell for the right price.

Since the ability to offload some of these companies through public markets has shut in 2019, one needs to look at the IPO implosion in the US, as these companies are now trying to reduce their debt piles, which is an acknowledgment that bad times are ahead.

Ferretti SpA, an Italian superyacht maker, owned by China’s SHIG–Weichai Group, shelved its IPO last week. Ferretti blamed macroeconomic headwinds for the dealy, as the IPO was seen as a way for SHIG–Weichai Group’s to cash out of its position in the company.

Since the trade war began a little over 15 months ago between the US and China, the Chinese have been selling assets across the world to build liquidity as domestic capital controls become tighter.

The global IPO and M&A markets are slowing, something we recently highlighted, has made it much more difficult for Chinese firms to sell foreign companies and assets in 2H19.

“It’s a big process of adjustment,” Mark Webster, managing director at BDA Partners in Shanghai, told Bloomberg in a phone interview. “Some Chinese companies made overseas acquisitions at the top of the cycle and ended up overpaying for assets that did not make a lot of strategic sense. They are now finding it challenging to offload those businesses at fair values.”

Another example of Chinese firms attempting to liquidate companies is PizzaExpress Ltd., a UK casual dining chain acquired by Chinese private equity firm Hony Capital in 2014.

Sources told Bloomberg that PizzaExpress had hired a financial adviser to prepare debt talks with creditors. There’s also a possibility that advisors are preparing the company for a sale.

China’s HNA Group Co. recently attempted to dump its stake in Avolon Holdings Ltd. for $8.5 billion, a deal that has yet to close.

Data compiled by Bloomberg shows the volume of Chinese outbound deals dropped to $59 billion so far this year, down 13% over last year, and well off 2016 high.

It’s only a matter of time before Chinese firms become forced sellers of Western companies, only to realize that there will be no buyers at the valuations they paid several years ago, as forced selling will then crush valuations.

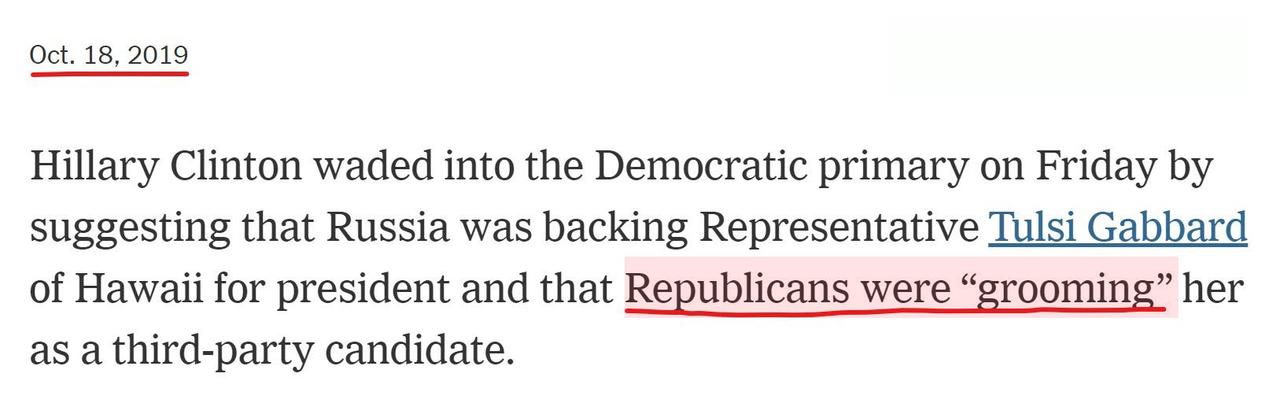

The New York Times stealth edited a story to hide Hillary Clinton’s claim that Tulsi Gabbard was being groomed by Russia, instead making it appear as though Clinton had said Republicans were grooming Gabbard.

Last week, Clinton told David Plouffe, “I’m not making any predictions but I think they’ve got their eye on somebody who is currently in the Democratic primary and are grooming her to be the third-party candidate. She’s the favorite of the Russians.”

The context of the conversation was Russian election meddling.

BEFORE

The New York Times initially reported Clinton’s comments accurately, writing that Hillary said “Russia was “grooming” Representative Tulsi Gabbard of Hawaii as a third-party candidate for president.”

NYT just stealth edited the original story about Hillary Clinton to claim that she didnt say the Russians were grooming Tulsi But that Republicans were

There is no correction, no notice, this was done quietly

However, this line was subsequently changed with no notice that the edit had been made to say that Clinton said “Republicans were “grooming her as a third-party candidate for president.”

AFTER

“NYT just stealth edited the original story about Hillary Clinton to claim that she didnt say the Russians were grooming Tulsi But that Republicans were. There is no correction, no notice, this was done quietly,” tweeted Tim Pool.

It appears as though the NY Times is literally trying to change history to cover for Clinton given the massive backlash she received for falsely claiming Gabbard was a Russian asset.

NY Times caught lying to cover up what Hillary said! Won’t Work!

“Hillary accuses Tulsi Gabbard of being a Russian asset”

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

Iraq Urges UN To Kick “Unauthorized” US Forces From Country

The Iraqi government’s efforts to expel what it increasingly considers an ‘unauthorized’ American occupation have just escalated dramatically, as Baghdad is now urging the United Nations to expel US troops from sovereign Iraqi territory.

As we noted previously, Baghdad officials rejected a Pentagon plan to relocate some 1,000 US troops now exiting Syria to US bases in western Iraq, saying the additional troops had “no approval to stay”.

On Wednesday Prime Minister Adel Abdul Mahdi announced he’s taking “all international legal measures” over the entry of U.S. troops from neighboring Syria, again underscoring the Pentagon had no authorization for such a move, and that the troops are “not allowed” to remain in the country, but only “transition” on their way to other US bases in Kuwait and Qatar.

US exiting Syria, via Getty/Al Jazeera

“We have (already) issued an official statement saying that and are taking all international legal measures. We ask the international community and the United Nations to perform their roles in this matter,” Abdul Mahdi’ said.

He said that any American forces coming from Syria have four weeks to leave Iraq, as reported by the AP.

The firm ‘red line’ assertion came immediately after the prime minister met with US Defense Secretary Mark Esper, who arrived earlier in the day on an unannounced visit, apparently to negotiate a compromise. Without Iraq’s cooperation, the White House’s Syria exit strategy and its logistics are in question.

On Tuesday, Defense Secretary Mark Esper in a likely attempt to placate growing Iraqi anger, said, “The aim isn’t to stay in Iraq interminably. The aim is to pull our soldiers out and eventually get them back home.”

Currently there are more than 5,000 American forces stationed in the country as part of a prior controversial agreement with Baghdad. One senior Pentagon official noted to Reuters this week that the situation remains “fluid and plans could change”.

There’s growing popular anger at the continued US presence largely due to a spate of Israeli drone strikes over the past few months on Iran-backed Iraqi paramilitary bases, mostly in and around Baghdad.

Washington’s priorities in the country have generally been expressed by defense officials as countering the threat of any resurgent ISIS , and preventing Iranian entrenchment and expansion in the region.

Establishment Democrats are becoming extremely nervous, because they are starting to realize that the field of candidates currently running for the Democratic nomination is exceedingly weak.

The campaign is nearly a year old, there have been nationally televised debates month after month, and at this point only three candidates in the field have any chance of winning. All of the other candidates have completely flopped, and establishment Democrats are deeply concerned about the weaknesses of the three candidates that are still standing. Elizabeth Warren and Bernie Sanders are considered to be way too liberal to win a general election, and Joe Biden has been slipping in the polls and his fundraising numbers have been absolutely terrible.

With just a few months left until voting begins, many establishment Democrats are now desperate for a “savior” to come along and bail them out, and that could potentially result in a very familiar name entering the race.

This cycle, more Democrats have run for president than ever before, and at first it seemed like at least a few of them would generate a significant level of enthusiasm. But now that it is clear that it is a three way race between Biden, Warren and Sanders, key Democratic operatives all over the country are evaluating whether there are other options. The following originally comes from the New York Times…

When a half-dozen Democratic donors gathered at the Whitby Hotel in Manhattan last week, the dinner began with a discussion of which presidential candidates the contributors liked. But as conversations among influential Democrats often go these days, the meeting quickly evolved into a discussion of who was not in the race – but could be lured in.

What Democrats care about more than anything else is beating Donald Trump in November 2020, and right now there are serious doubts about those that are leading the race.

“With Trump looming, there is genuine concern that the horse many have bet on may be pulling up lame and the horse who has sprinted out front may not be able to win,” said David Axelrod, a former adviser to President Barack Obama.

Of course the horse that is “pulling up lame” is Joe Biden. For most of the race he was leading in the polls, but recently his numbers have been falling and his fundraising has been abysmal. The following comes from Vanity Fair…

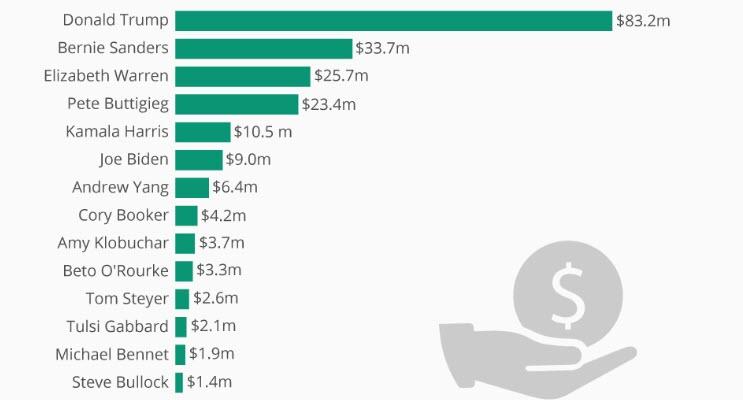

While Vice President Joe Biden may still be the front-runner in the 2020 polls, he’s falling woefully behind when it comes to campaign cash. New campaign finance filings released Tuesday reveal that while the 2020 candidate took in $15.7 million in the third quarter, Biden’s campaign only has $8.9 million on hand going into the fourth quarter. And with the Iowa caucuses rapidly approaching in February, his donors are reportedly starting to get nervous about Uncle Joe making it to the finish line.

Biden’s third quarter cash haul falls far behind his fellow top-tier 2020 candidates. Senator Bernie Sanders took in $25.3 million and has $33.7 million cash on hand, while Sen. Elizabeth Warren, Biden’s closest rival in the polls, took in $24.7 million and has $25.7 million on hand. Though slightly further down in the polls, Mayor Pete Buttigieg was one of the top third-quarter fundraisers with $19.2 million and $23.4 million on hand.

Biden’s pitiful fundraising haul is yet another indication of the lack of enthusiasm surrounding his campaign.

People that give money to campaigns generally do so because they truly believe in the candidate that they are giving money to.

But throughout his political career, Biden has never been able to generate much national enthusiasm, and the same thing is true today.

And if Biden is really struggling to raise money now, how in the world is he going to compete with Trump’s fundraising machine in the general election?

Top Democrats all over the nation are talking about these things, and many of them are intent on finding a “savior” that can rescue them from the potential disaster that they see looming in November 2020.

Mrs. Clinton and Mr. Bloomberg have both told people privately in recent weeks that if they thought they could win, they would consider entering the primary — but that they were skeptical there would be an opening, according to Democrats who have spoken with them.

Bloomberg is an interesting figure, but the Democrats are simply not going to nominate a rich, white billionaire, and so he might as well forget it.

Hillary Clinton, on the other hand, would instantly become the front runner if she were to enter the race, and according to the Stamford Advocate she thinks about it “all the time”…

Those close to Clinton, speaking on the condition of anonymity because they were not authorized to comment on her behalf, say she has felt vindicated over the past few weeks as Trump’s political difficulties have deepened. That sentiment was reinforced this week when the State Department announced its probe into emails sent to a private server, a major complication of her 2016 campaign, found no evidence of deliberate mishandling of classified information by department employees.

“Ultimately, it’s unlikely she would do it,” said one person who has spoken with her. “But put it this way: It ain’t zero. And does she think about it all the time? Absolutely.”

This month, Hillary Clinton has been all over the mainstream media, and she has been frequently asked about the 2020 race.

In response, she has repeatedly stated that she is not endorsing any of the current candidates, and she has refused to shoot down the persistent rumors that she may enter the race herself.

For example, at the latest stop on her “book tour” she had every opportunity to say that she was not running, but instead she seemed to welcome the speculation…

“All that matters is that we win,” Clinton told Strayed. “I hate to be so, you know, simplistic about it. We have to nominate (cough) … the best …

“You!” someone shouted from the audience, drawing a big smile and laugh from Clinton.

She didn’t disavow the idea.

“Oh, my. Well, thank you,” Clinton said. “I just feel so strongly that, look, I just want to say a little bit more about this, because what’s going on now with the impeachment inquiry is not a choice it was an obligation under the Constitution.”

You can watch her making these remarks on video right here.

And then on Tuesday, Clinton sparked even more speculation when she shared a very cryptic quote from Beyonce on Instagram…

Hillary Clinton on Tuesday kicked up more 2020 buzz after posting a quote from pop megastar Beyoncé about the need to take power, praising the sentiment and adding, “Beyoncé speaks the truth.”

The failed presidential candidate posted the quote from the “Halo” singer on Instagram on Tuesday. It read, “Power’s not given to you. You have to take it.”

Clinton’s post has received more than 58,000 likes so far, and most of the candidates currently in the Democratic field would kill for that sort of enthusiasm.

Of course that could only happen if Trump actually makes it to the 2020 election. After the Democrat-controlled House impeaches Trump, there will be a trial in the U.S. Senate, and many experts are assuming that the Republican-controlled Senate will protect Trump and keep him in office.

But when the Daily Caller recently contacted every Republican in the Senate, only 7 of them said that they have ruled out voting to remove President Trump from office.

Only 7 out of 53.

I am extremely concerned about what is going to happen in the Senate, because removing Trump from office would throw our entire country into a state of chaos.

And with our nation in a state of chaos, it would be the perfect opportunity for the most evil politician of our generation to step forward and pick up the pieces.

{kind=link}