Harvard Admits To $9 Million Donation From Jeffrey Epstein

Harvard University on Thursday night acknowledged that it had taken in approximately $9 million in donations from pedophile and alleged child sex-trafficker Jeffrey Epstein over the course of a decade ending in 2007, according to the Boston Globe.

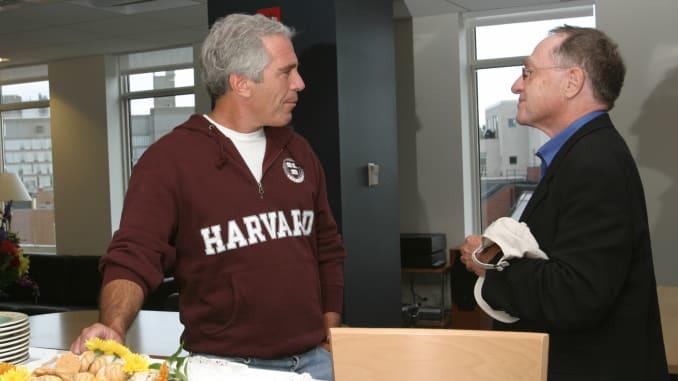

Jeffrey Epstein and former attorney, Harvard Law Professor Alan Dershowitz

The donations, the bulk of which occurred while former US Treasury Secretary Larry Summers served as the university’s President, provides clarity after Harvard maintained that it did not take money from Epstein after 2007 – just one year before he pleaded guilty to soliciting a minor for prostitution and was sentenced to 13 months in jail with partial ‘work’ release.

“Jeffrey Epstein’s crimes were repulsive and reprehensible. I profoundly regret Harvard’s past association with him,” Bacow continued.

“Epstein’s behavior, not just at Harvard, but elsewhere, raises significant questions about how institutions like ours review and vet donors,” said Harvard president Larry Bacow in a letter to the community – while announcing that the university would expand an ongoing probe of the pedophile’s donations to determine whether Epstein served as a conduit for other donors, as he did for Bill Gates and others at MIT.

What’s more, Epstein’s Harvard and MIT donations may be linked, according to the Globe. “For example, according to emails released by an MIT whistleblower this past week, Epstein gave money to support a researcher who was visiting scholar at the Media Lab, but was based at Harvard’s evolutionary dynamics program. The emails were provided by Whistleblower Aid, a non-profit representing a former MIT Media Lab employee.

In the letter, Bacow acknowledged that Epstein’s largest gift was a $6.5 million contribution to establish the Program for Evolutionary Dynamics in 2003. But between 1998 to 2007, Epstein or his foundations also gave another $2.4 million in total gifts to support Harvard, Bacow said, based on current information.

…

Bacow said Harvard also recently learned that Stephen Kosslyn, a former faculty member and a beneficiary of Epstein’s philanthropy, designated Epstein as a visiting fellow in the pyschology department in 2005. The university is trying to gather more information about the appointment. –Boston Globe

While most of Epstein’s money was immediately spent at the time it was given, the university says it located $186,000 which it will give to non-profits that support victims of human trafficking.

Epstein was found dead in his Manhattan jail cell last month where he was awaiting trial on charges of sex-trafficking minors. His death was ruled a suicide.

Get ready for your Friday absurdity! Here are this week’s stories:

Professor advocates for cannibalism to fight climate change

If you’re concerned about the human impact on Earth’s climate, you could plant a tree, install solar panels, ride a bike, or eat your dead relatives.

Don’t let that sack of meat decompose. Put it to good use, save a cow, and sequester that carbon into your own body.

At a summit in Sweden about the future of food, a professor gave two presentations about how eating human flesh could combat the negative effects of climate change.

He claims resistance to cannibalism is “conservative” or even “selfish.”

And of course, the human meat industry will have to start slow, first getting people used to the idea of eating pets and insects. But eventually humans can be “tricked into making the right decisions,” the professor suggested.

Experiment to cool earth with chemicals in the atmosphere

Backed by the likes of Bill Gates and other powerful elite, scientists are set to try their first experiment in “geoengineering” to cool the globe.

This experiment will be small scale, spewing chemicals into the atmosphere in order to mimic a volcanic eruption. Eruptions are known to cool the globe, because the particles in the air reflect the sun’s rays away from the earth.

If they deem the experiment a success, it could be replicated around the globe.

Of course, volcanoes can also cause famine, drought, and eliminate blue skies.

But those are risks this enlightened group of elites is willing to take… without anyone else’s consent.

Oregon unions want to limit self check-out lanes at grocery stores

Have you ever used the self-checkout at the grocery store to beat the long lines?

If Oregon unions get their way, those lines will be just as long.

A group of labor unions is collecting signatures in Oregon for a 2020 statewide ballot initiative.

They want to put the Grocery Store Service and Community Protection Act to popular vote, which would prohibit grocery stores from having more than two self-checkout lanes.

The unions say these self service lanes are cutting jobs and are hard for elderly and handicapped to operate.

The self-checkout is also causing social isolation, they say– because we all know how important those social interactions like, “paper or plastic?” are.

DOJ Inspector General Completes FISA Abuse Probe; To Be Made Public After Review

DOJ Inspector General Michael Horowitz has completed his investigation into potential FBI abuse of the Foreign Intelligence Surveillance Act during its counterintelligence investigation into the Trump campaign, according to a letter from Georgia Rep. Doug Collins (R) to House Judiciary Committee Chairman Jerry Nadler.

Horowitz informed Attorney General William Barr on Friday that he had completed his probe.

“Earlier today, Department of Justice (DOJ) Inspector General Michael Horowitz notified Attorney General William Barr of the completion of his investigation into possible abuses of the Foreign Intelligence Surveillance of Act (FISA) by DOJ officials during the 2016 presidential election,” wrote Collins, who called on Nadler to invite Horowitz and FBI Director Christopher Wray to testify after the report has undergone Judiciary Committee review and then made public.

“After the DOJ has a chance to review and comment on the report, it will be sent to the Judiciary Committee and made public,” wrote Collins.

In late June, Horowitz informed several congressional committees that his probe was “nearing completion,” and that his office had interviewed over 100 witnesses and reviewed more than 1 million documents, according to the Daily Caller‘s Chuck Ross.

The FBI relied heavily on the infamous and unverified Steele dossier in applications for the warrants.

The special counsel’s report severely undercut dossier author Christopher Steele’s claim that there was a “well-developed conspiracy of co-operation” between the Trump campaign and Russian government.

The special counsel said there was no evidence of a conspiracy involving the Trump team. There was also no evidence that Page or any other Trump associates acted as agents of Russia.

Republicans have accused the FBI of mishandling the dossier, and failing to disclose to FISA Court judges that the DNC and Clinton campaign had hired Steele to investigate Trump. Investigators with the OIG reportedly interviewed Steele in London, where he is based, in early June. –Daily Caller

According to Rep. Jim Jordan (R-OH), top Republican on the House Oversight and Reform Committee, Horowitz will likely conclude that the FBI illegally obtained FISA warrants against 2016 Trump campaign aide Carter Page.

“I think he will,” said Jordan during an discussion with Fox News‘s Sean Hannity and Gregg Jarrett Monday night.

And in December, a string of emails quietly requested by House Republicans for declassification by President Trump may provide the smoking gun in the FISA abuse case.

The email exchanges show the FBI was aware — before it secured the now-infamous warrant — that there were intelligence community concerns about the reliability of the main evidence used to support it: the Christopher Steele dossier.

The exchanges also indicate FBI officials were aware that Steele, the former MI6 British intelligence operative then working as a confidential human source for the bureau, had contacts with news media reporters before the FISA warrant was secured. –The Hill

Doing more of what’s failed for ten years will finally fail spectacularly..

It was a huge relief to see the charts of the Baltic Dry Index (BDI) and the U.S. retail sector ETF (RTH): both have soared to the moon, signaling that both the U.S. and global economies are booming: the BDI is widely regarded as a proxy for global shipping, which is a proxy for global trade and economic activity.

Amazon is 18% of the RTH basket of retail stocks, but the rest are conventional bricks and mortar chains with online sales: Walmart, Home Depot, Lowes, Costco, CVS, etc.

The American consumer must be ready, willing and able to spend freely since the retail sector is hitting new heights.

OK, now let’s change channels from soaring market valuations to the real-world economy. What planet are buyers of BDI and RTH on? Maybe the shipping and retail sectors are incredibly robust on Sirius B, but here on Planet Earth the global economy is weakening, trade is stagnating, shipping is in recession, and retail sales and profits are stagnating.

Lumping all American households in one basket gives a false signal of financial health. If we look at averages, debt levels are reasonable, incomes are notching higher and so expectations of rising household debt and spending are reasonable.

But this radically distorts reality: only the top 10% are creditworthy and have rising incomes; the bottom 90% are over-indebted, poor credit risks and their income is stagnant and/or precarious.

The top 10% of households–a mere 12 million households–are also precarious, as much of their wealth and income is based on insanely overvalued asset bubbles in stocks, bonds and real estate. The wealth effect fuels their free-spending ways (recall that the top 10% collect roughly half of all income and account for almost half of all consumer spending).

As all the asset bubbles pop, the reverse wealth effect kicks in. Once households feel poorer, they tighten their borrowing and spending.

Another under-appreciated reality is the top 10% of households have much lower levels of debt (relative to their income) than the average middle-class household. This has several sources:

1. The top 10% hasn’t needed to borrow as much for college, healthcare, vehicles, vacations, etc. because their higher income enables saving and paying cash.

2. The top 10%, especially the self-employed and small-business owners, tend to be debt-averse. They understand that debt is always a noose around the neck. As a result, the desire to take on more debt, even at near-zero rates of interest, is near-zero for many top 10% households.

3. The wealth effect is real for 10% households which have sold off bubble-valuation stocks, bonds, real estate, art, vintage autos, etc. The smart money has been selling these assets and pocketing the gains. The bottom 90% don’t own enough bubble-valuation assets to move the needle on their overall wealth, income and financial security.

Globally, those who want to borrow more are poor credit risks while those who are creditworthy don’t want more debt, regardless of how low interest rates fall. If we set aside the top 10% of households and enterprises, and focus on the creditworthiness and precariousness of the bottom 90%, we get a much more accurate picture of global debt exhaustion, a.k.a. debt saturation.

As I’ve written here recently, the recession that’s unfolding isn’t one triggered by crisis such as higher oil prices or a financial panic. It’s a recession of debt exhaustion and diminishing returns as doing more of what’s failed for ten years will finally fail spectacularly.

And US equities surged led by Trannies and Small Caps, each of which was panic-bid at every day’s open. The Dow is up 8 days in a row. Nasdaq underperformed on the week…

That is the best week for Small Caps since Dec 2016 (and best for Trannies since Dec 2017)

Very narrow range in Dow futs in the day session (having tried and failed to break to new highs numerous times)…

The driver of the Trannies/Small Caps surge was a huge short-squeeze…

Source: Bloomberg

The biggest weekly squeeze since Trump’s election…

Source: Bloomberg

September has seen a massive shift into cyclical stocks…

Source: Bloomberg

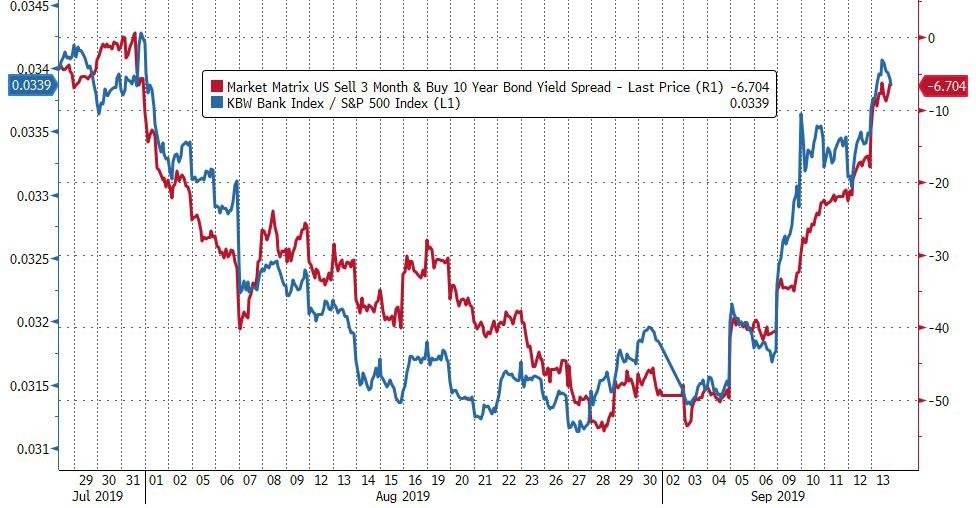

Bank stocks soared this week (as rates rose and the curve steepened)…

Source: Bloomberg

…but note below they are merely back at a critical level of resistance…

Source: Bloomberg

The week was an utter bloodbath for bondholders (yields are up 8 days in a row)…

Source: Bloomberg

Just as the start of August sparked a panic-buying period for bonds, so September has seemingly sparked the exact opposite with a huge retracement so far…

Source: Bloomberg

The 10Y Yield is testing critical technical levels…

Source: Bloomberg

Some might argue the 10Y has a long way to go…

Source: Bloomberg

But don’t listen to Jamie Dimon: In 2018, he predicts 10Y yields will hit 4%, 10Y yield drops to all time low. In 2019, he says JPM preparing for 0% rates on 10Y, 10Y yield soars most in years.

Meanwhile, elsewhere in bond land, that 100-year maturity Austrian bond (which was up 85% YTD, is now in a bear market, down 21% from the highs)…

Source: Bloomberg

The US yield curve (3m10Y) remains inverted but had the biggest weekly steepening since June 2013…

Source: Bloomberg

The Dollar slipped lower the second week in a row, testing one-month lows…

Source: Bloomberg

Cable soared this week – its best since May – as BoJo faced defeat and a no-deal brexit was believed to be less likely…

Source: Bloomberg

Offshore Yuan ended the week stronger than the Yuan fix

Source: Bloomberg

This is the strongest offshore yuan has been relative to the fix since Dec 2018…

Source: Bloomberg

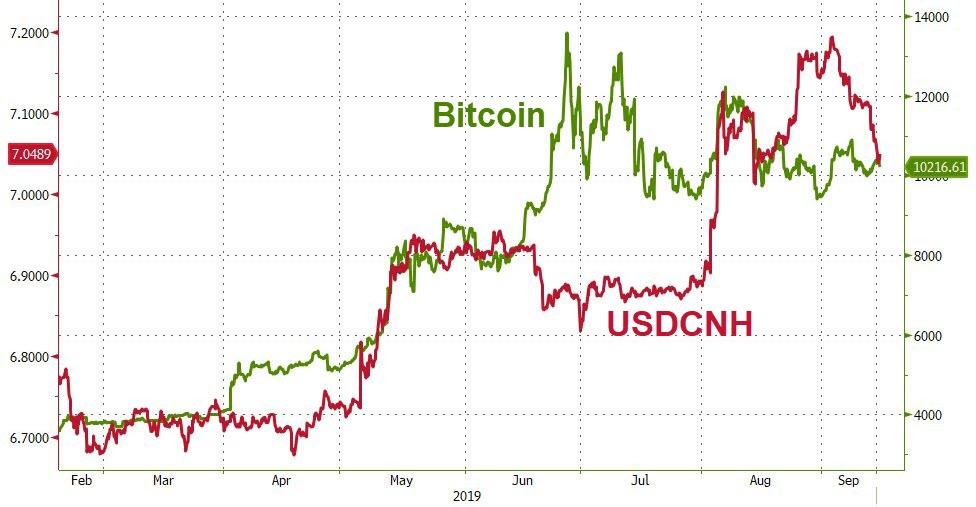

Yuan appears to have caught up to Bitcoin’s stability…

Source: Bloomberg

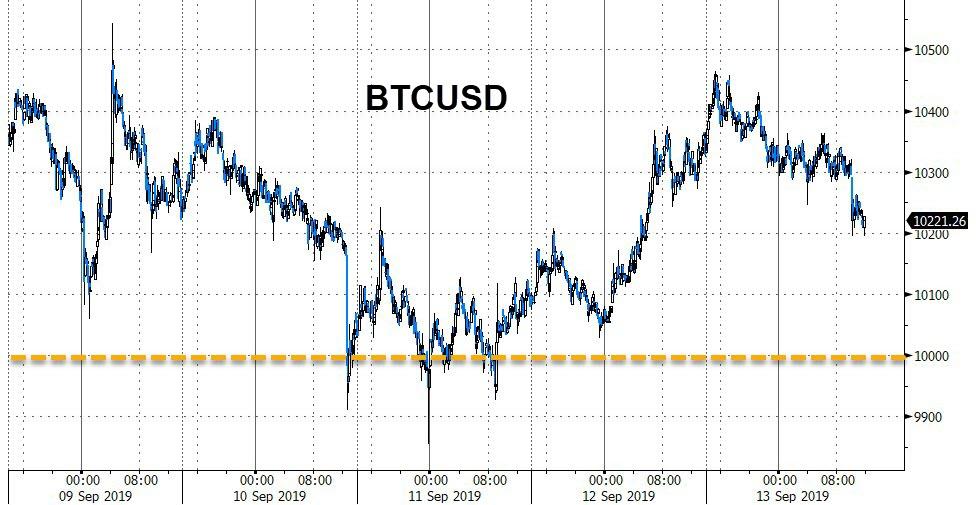

Cryptos were mixed with Bitcoin down on the week and Altcoins up led by Ethereum…

Source: Bloomberg

But Bitcoin held above $10,000 for now…

Source: Bloomberg

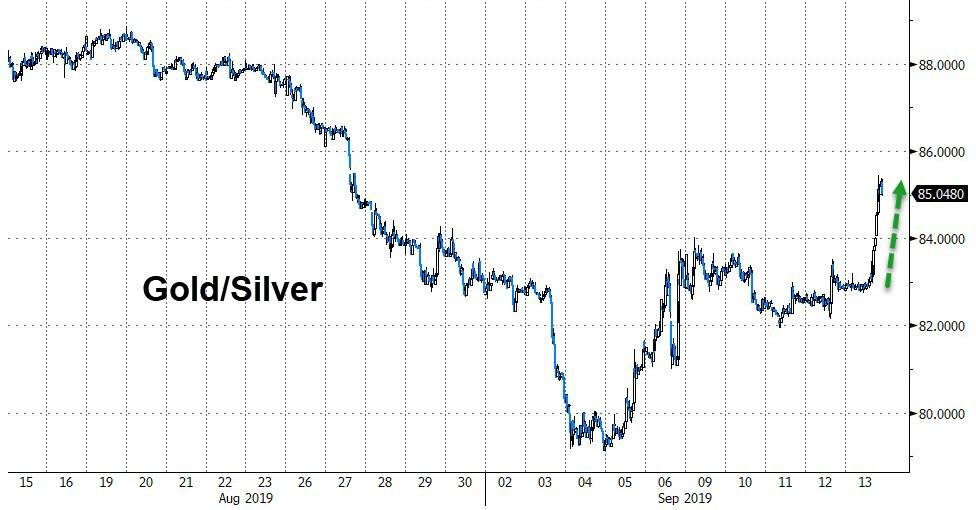

Oil had a volatile week as copper surged but PMs got pummeled today (most notably silver)…

Source: Bloomberg

Soft Commodities soared 5.2% this week, its best rally since May and snapping 10 straight losses in what was the longest losing streak since at least 1991.

Source: Bloomberg

With the surge in rates this week, the volume of global negative-yielding debt tumbled, and gold tracked it lower…

Source: Bloomberg

But it was silver that was monkeyhammered most…

Smashing Gold/Silver dramatically higher this week…

Source: Bloomberg

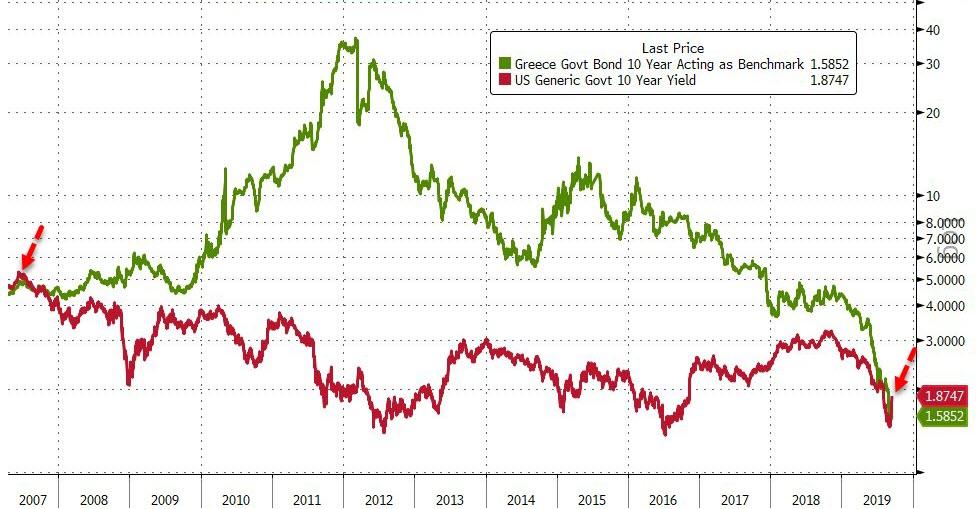

Finally, straight from the WTF world we live in, Greek 10Y Yields are now below US 10Y Yields for the first time since 2007…

Source: Bloomberg

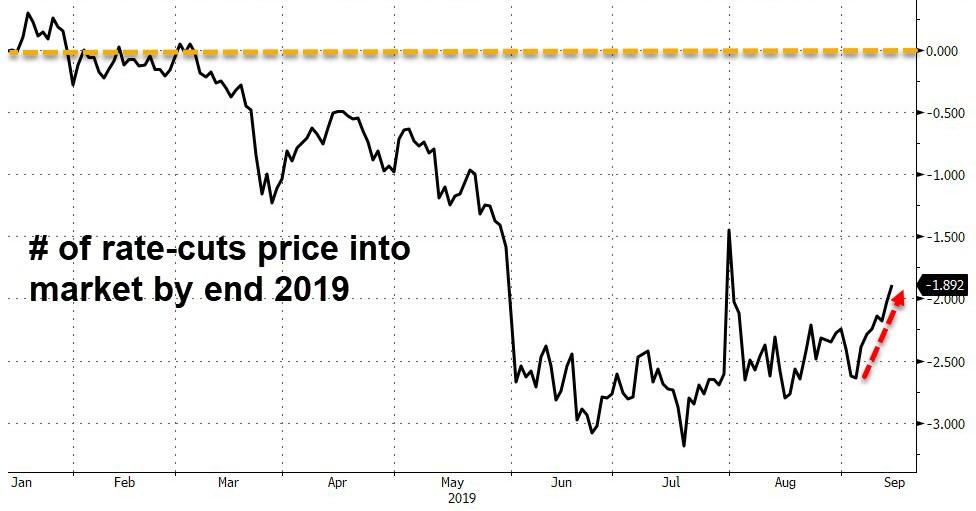

And the market is starting to ease off its pressure on The Fed as it now prices in less than 2 rate-cuts by year-end (from more than 3 in July)…

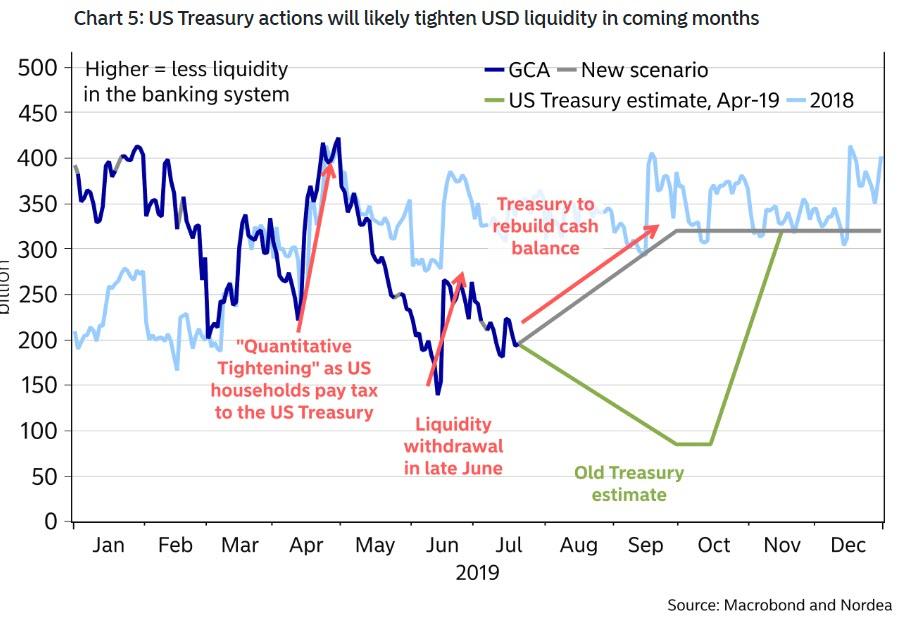

A “Dollar Funding Storm” Is Set To Make Landfall In Weeks: What Happens Next

One month ago we explained why, regardless of the outcome of the US-China trade war and the fate of the US economy, the Fed may have no choice but to resume QE in the coming weeks – potentially as early as 4Q – in order ease funding pressures expected during the coming wave of accelerated Treasury supply as the US Treasury seeks to rebuild its cash balance up to $350 by mid-November.

And while the Treasury has taken its time in rebuilding the cash over the past month, with the latest Treasury cash balance just $184BN as of Sept 11, it only means the ramp up in the coming weeks will be that much more acute. So acute in fact, that as BofA rates strategist Mark Cabana writes today, “the USD funding storm has been brewing for months and is likely to make landfall in Q4.”

For those still unfamiliar with the core reasons behind the coming dollar shortage, BofA recaps the converging sources of pressure that will likely result in secured funding markets breaking higher, including

elevated UST supply,

bloated dealer balance sheets and year-end regulatory constraints, and

a banking system near reserve scarcity.

Ironically, it was the rising recession concerns in August – manifesting in the form of an inverted yield curve, cash hiding in repo, and a slow build in UST supply – that kept secured funding pressures at bay. However, Cabana believes that “clear signs of funding pressure could emerge starting next week with sizeable coupon settlements and the mid-September corporate tax date.“

So what happens next?

According to BofA, the Fed will have no choice but to respond to these funding pressures by year end. As of this moment, the Fed has a number of tools to deal with these pressures including:

repos, i.e. temporary ad hoc reserve adding open market operations,

Treasury purchases, i.e. permanent open market operations, similar to outright UST QE only without a clear QE mandate (for now), and

standing repo facility (SRF), i.e. a new facility that could “automatically” add reserves to the banking system when GC or fed funds reaches a threshold above IOER.

As Cabana explains, all three of these have the same Fed balance sheet and funding impact; they only differ in their design and implementation; furthermore in terms of deployment, BofA expected traditional repos will be first tool employed by the Fed and SRF likely the last.

Here are the details on how the Fed will scramble to offset what BofA sees as a coming dollar “funding storm” starting with the most conventional sources of short-term funding:

1. Old school funding pressure lessons: repos & outrights

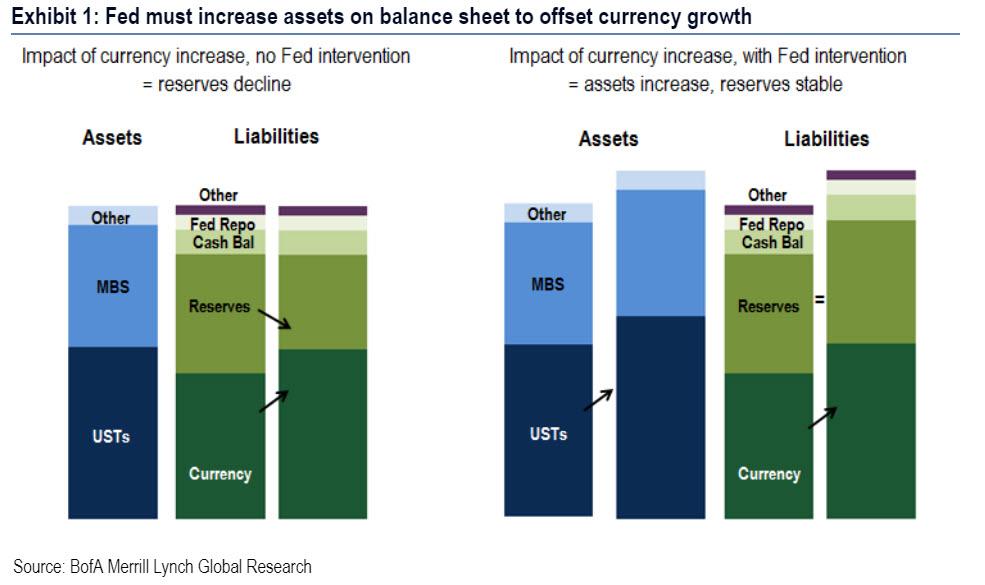

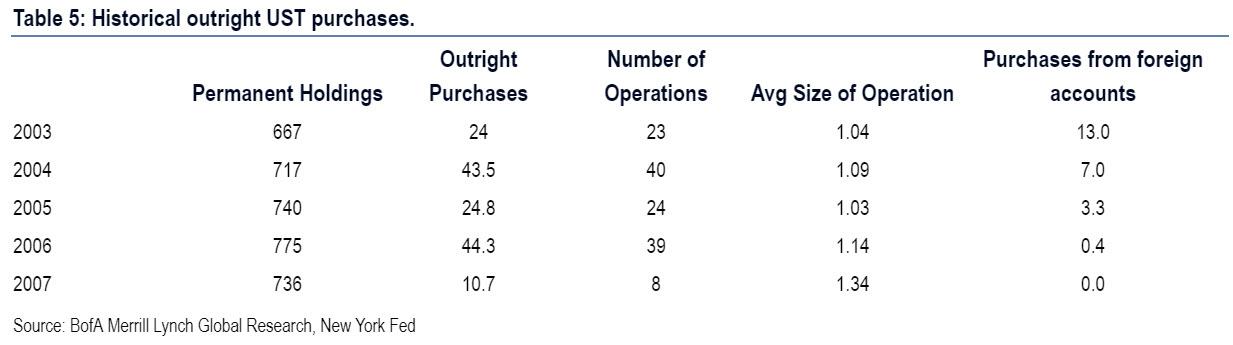

Pre-crisis the Fed relied on two types of open market operations to manage funding markets and their balance sheet: (1) temporary repo or reverse repo operations (2) outright UST purchases. Repo operations were used to “fine tune” the amount of reserves in the banking system to hit the fed funds target rate while outright UST purchases were used to offset currency in circulation growth. As a reminder, currency growth – of which we have seen a dramatic increase in recent years as the amount of $100 bills in circulation has soared – eats away at reserves in the banking system; this would pressure fed funds higher if the Fed did not growth their balance sheet to offset this (Exhibit 1).

Reserve adding operations: both repos and outright UST purchases have the same impact on the Fed’s balance sheet: on the asset side they increase SOMA holdings and on the liability side they increase reserves (Table 1). The only difference is that repos are relatively short-lived and unwind on an overnight or short-term basis; outright Treasury purchases have a permanent impact on the Fed’s balance sheet.

Reserve draining operations: pre-crisis the Fed only ever engaged in open market operations to drain reserves as a “fine tuning” fed funds management exercise. Prior to 2008 the Fed never engaged in any permanent open market operations to drain reserves (such as UST sales) since they only ever used this tool to offset currency growth.

Next, Cabana provides some historical perspective on each of the temporary repo and permanent UST purchase open market operations focuses on those operations that add reserves. As funding pressures begin to emerge and likely worsen in Q4, the BofA rates strategist expects the Fed to step in and use both sets of tools to contain these pressures and keep the fed funds in its target range.

Temporary repo operations

Temporary open market operations were a common practice prior to the crisis, when the Fed was in a scarce reserve regime. The New York Fed conducted frequent repo operations to fine tune the amount of reserves in the system and to ensure that the fed funds effective hit its target point. Below is a review of the mechanics of such repo operations as well as historical activity from 2000-2008. If the Fed conducts repo operations again to offset funding pressures, there will likely be parallels to their historical operations.

The mechanics

Temporary repo operations were executed in the tri-party market and were conducted only with primary dealers. Historically, repos were

multiple price and fixed amount

announced only at the outset of the open market operation

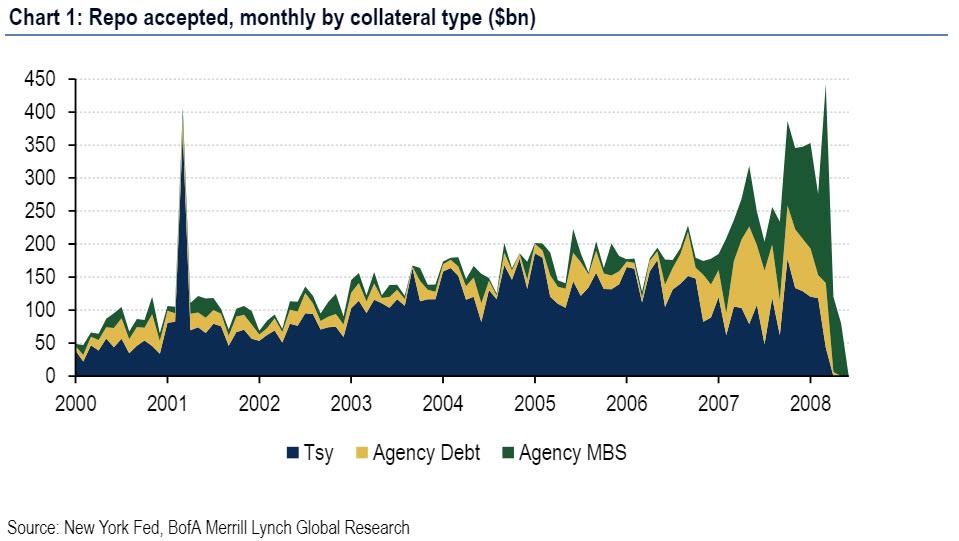

The Fed provides data on repo operations starting in July 2000. An increase in Fed repo operations corresponds to a similar increase in reserves, all else equal (Exhibit 1).

Historical repo operations

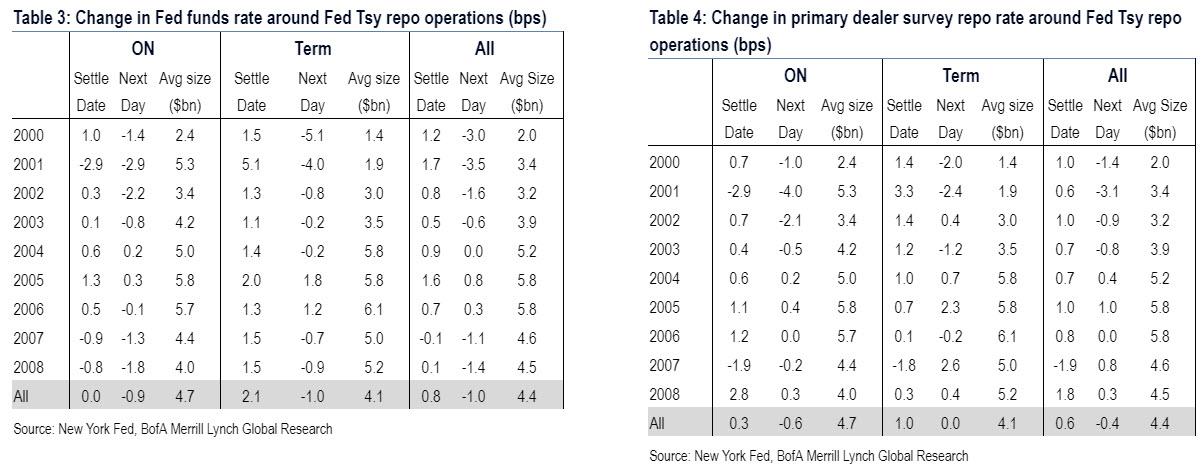

From mid-2000 to the end of 2008, the NY Fed conducted 5 UST repo operations on average each week. Overnight operations averaged around $5bn in size while term operations averaged around $4bn (Table 2). Fed repo operations were all fixed quantity and multiple price, which means that dealers were able to submit varying rates at which they would underwrite the repo operation. The Fed reports the high and low rate that dealers showed into the Fed: the range of rates averaged 13bps and was unsurprisingly wider for term rates. Operations were typically conducted between 8:30 and 10:00AM.

What to expect this time

If funding markets face stress in the next few months – which Bank of America expects will happen – the Fed could easily conduct repo operations to stem upward pressure. Since the recession, the NY Fed has periodically conducted small repo operations in order to “test operational readiness.” There have been 21 operations in total since 2012 – which is somewhat bizarre considering there are well over $1 trillion in reserves floating around the financial system – and the last set of Fed test repo operations was conducted in May. In the past few years the repo tests have been very small (around $23mn in size for USTs), were multiple price, and were overnight or matured in 2-3 business days. The tests have also been across UST, agency debt, & agency MBS collateral. The tests indicate that the NY Fed is prepared to conduct such repo operations at any time and that this is a readily available solution for any sharp increase in funding markets.

Outright Treasury purchases

Before the crisis, Fed outright purchases of Treasuries averaged $30bn per year, with individual operations sizes around $1bn (Table 5). Purchases ranged across the entire Treasury curve but were concentrated in the belly. The NY Fed limited its purchases to 35% of any single issue but has subsequently increased this limit to 70%. The Fed also avoided purchasing issues with less than 5 weeks remaining to maturity, issues trading with significant specialness, and newly issued securities

Extending on this, if the Fed wanted to offset elevated funding pressures today and was leery of using repos, it would first utilize ad-hoc repo operations and then shift to use outright Treasury purchases, i.e. Q.E., according to BofA.

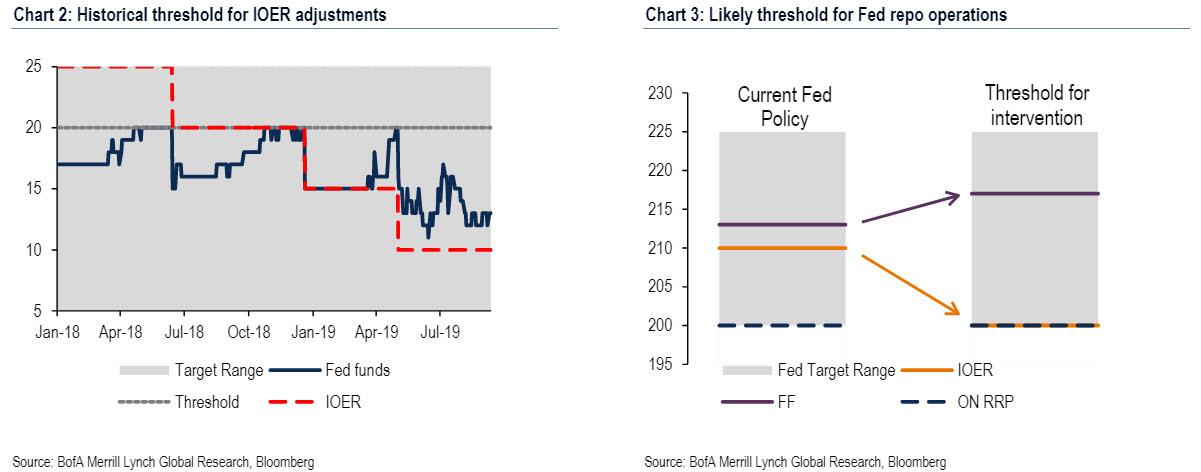

Fed funding intervention today: when, what level, why?

According to BofA, in recent weeks client speculation has increased that the Fed might announce measures to offset potential Q4 funding pressures at the September FOMC meeting; the bank itself is skeptical, and believes the Fed will need to see both GC repo and fed funds rise materially in relation to IOER before intervening in the repo market.

September FOMC expectations: the Fed is unlikely to provide much concrete guidance on its plans to intervene in funding markets at the September meeting, according to Cabana. The reason is that with less than a week to go until the FOMC meeting, funding markets have been relatively well behaved over recent weeks and the Fed would likely need to see more upward pressure in money markets before committing to take any specific actions. As such, BofA is “skeptical that the Fed is ready to unveil a new SRF, especially since the Fed has repo and outright operations they can rely on to manage money markets.” New SRF detail is most likely to come through the September FOMC meeting minutes on October 9 rather than through communications next week.

That said, not even BofA believes the September meeting will be completely devoid of communications around Fed activity in money markets, and expects the Fed to send a reminder that it stands ready to act to ensure that the fed funds effective remains comfortably in the target range. The most logical place for such communications would be through the “implementation note” that accompanies all recent FOMC meetings. The Fed could note that “the Federal Open Market Committee directs the Desk to undertake open market operations as necessary to maintain the federal funds rate in a target range of 1 ¾ – 2 percent, including repurchase operations and reverse repurchase operations…”. The inclusion of repos in this language would likely signal to the market that the Fed remains ready to act in case funding markets come under greater pressure.

Threshold: TSYs will need to get notably cheaper before the Fed conducts temporary repo operations or outright UST purchases. As funding pressure begins to emerge, the Fed will cut IOER at least once if not twice more to the bottom of their target range, per BofA. In the past, technical IOER adjustments have taken place when EFFR is 5bps from the top of the range.

Curiously, despite the recent rate cut, the effective FFR has remained stable around 2.13% or 12bps from the top of the range, if still above the IOED level. Here BofA claims that since the Fed has never “preemptively” lowered IOER, the fed funds will need to be near 2.20% in order for the Fed to take such action at the September meeting.

So when will the Fed re-enter the market aggressively and restart open market operations?

According to Cabana, BofA’s best guess is that “the Fed re-starts open market operations when fed funds trades at IOER+15 to +20 bps, assuming IOER is dropped to the bottom of the target range”, with the caveat that the Fed might choose to intervene at less extreme levels of money market cheapness vs IOER but believe fed funds will need to be higher than 10 bps above IOER since the Fed did not engage in repo operations when fed funds traded near similar levels in the past. The key takeaway is USTs still have room to cheapen in the near-term until the Fed backstops the funding markets.

So why wait?

As BofA reveals, a number of its clients have asked why the Fed would wait to see more material funding pressures emerge before seeking to intervene in repo markets. The answer stems from the Fed’s balance sheet normalization principles (which sadly have now been trampled) and plans where it states that it wants to hold “no more securities than necessary for efficient and effective policy implementation”. This, to Cabana, suggests that the Fed wants to find the minimum quantity of reserves necessary in the banking system before it will be willing to expand its securities portfolio. Stated differently, the Fed needs to see the “whites of the funding pressure eyes” before they will act to offset these pressures. Here, the fact that this potential reserve shortage is taking place with nearly $1.4 trillion in “excess” reserves in the system, is probably not lost on anyone.

Further to this point, the necessity to see the funding pressures materialize in markets is aided by the fact that the Fed has received inconsistent guidance about the minimum level of reserves from their various surveys:

Assumptions drawn from the June ’19 Survey of Primary Dealers and Market Participants suggests that reserves are to bottom out at a level between $1.1 – $1.25 tn. However, when the Fed asked banks in their most recent February ’19 Senior Financial Officer Survey these respondents generally indicated a minimum level of reserves in the $800-$950 bn range. While the Fed will want to have a “reserve buffer” likely ranging from $100-$200 bn on top of the estimates provided in the Senior Financial Officer Survey it still suggests a relatively wide range.

Why does this matter? Since the Fed does not know the minimum quantity of reserves needed in the banking system and it desires to hold “no more securities than necessary” for the efficient implementation of monetary policy, BofA believes that the Fed will likely want to test how low reserves can fall before intervening in funding markets. “This runs the risk of a temporary overshoot on the extent of money market tightness as the Fed plumbs how low reserves can fall before it ultimately needs to start growing its balance sheet.“

This matters because the last time the market freaked out about insufficient reserves in the market was in Q4 2018 when QT was on “auto pilot” and stocks tumbled.

Which brings the $64 trillion question: how to determine if the dollar funding squeeze will cause another major risk off episode? Here, Cabana answers that as the Fed starts to test these reserve lows, “we expect funding markets to react by showing further Treasury cheapening, widening of FRA-OIS, and narrowing of front-end spreads & SOFR-FF basis.”

However, once the Fed responds by engaging in repo or outright UST purchase operations we expect these markets to move in the opposite direction. We suggest clients continue to trade these themes tactically and consider moving out of UST cheapening positions as fed funds rises towards the IOER +15 to +20 bps level.

Of course, if the Fed wants to front-run the funding shortage, and aggressively inject liquidity into the system, nothing prevents it from following in the ECB’s footsteps and hint at another round of QE in the near future: not only would that send stocks soaring in the asset bubble’s “Icarus song”, but it would also make Trump happy, if only until it all comes crashing down.

Actress Felicity Huffman, First Parent Sentenced In College Admissions Scandal, Gets 14 Days In Prison

Following reports that she might avoid jail time, actress Felicity Huffman has been sentenced to 14 days in prison at a federal court in Boston on Friday.

Prosecutors had recommended that Huffman serve a month in prison. They argued that “imprisonment is needed because this was a considered, deliberate and purposeful act.”

But before handing down the sentence, U.S. District Judge Indira Talwani said she wasn’t swayed by the prosecutions claims that Huffman and her fellow defendants’ actions undermined the whole college admissions system.

She is the first parent to be sentenced in the ongoing college admissions cheating scandal case.

Per CNN, Felicity Huffman’s husband William H. Macy – who was present in court on Friday to support his wife – hasn’t been charged in connection with the college cheating scandal because it’s unclear if he was aware of his wife’s alleged activities.

Her legal team is expected to deliver a statement to the press after the sentencing has been adjourned.

FELICITY HUFFMAN SENTENCED: Actor Felicity Huffman receives her sentencing today after pleading guilty in May for her involvement in the widespread college admissions cheating scheme. https://t.co/6nvweUYeX0

President Trump Met By Dozens Of Protesters After Arriving In Baltimore On Thursday

President Trump was met by dozens of protesters in downtown Baltimore on Thursday during his first visit to the city since he called it “disgusting” and “rodent infested”, according to Reuters. They greeted the President with signs depicting him as a rat and telling him to “return to the swamp”.

Trump was in town to give a speech to Republicans from the House of Representatives who were holding an annual retreat. His motorcade passed signs reading things like “Dump Trump, Ditch Mitch”.

The reception comes as a result of Trump attacking Baltimore-based Congressman Elijah Cummings this summer, who he called a “brutal bully”, before saying he should concentrate on cleaning up his “disgusting, rat and rodent infested” district instead of criticizing Border Patrol agents.

Cummings is the chair of the of House Committee on Oversight and Reform and has led investigations into Trump and his administration. He has openly called Trump a “racist” and has lashed out at his immigration policies. Cummings responded to Trump’s tweets by telling him he should tour the city, which is about 40 miles north of Washington D.C.

Trump was received warmly, however, by the crowd at the dinner he was speaking at. He was met with chants of “four more years”.

During his hour long remarks at the dinner, Trump took a jab at city leaders:

“We are going to fight for the futures of cities like Baltimore that have been destroyed by decades of failed and corrupt rule.”

You can watch Trump’s full remarks from Baltimore here:

The memory hole that appeared in America’s zeitgeist around 2016 is expanding like some evil cosmic rot. Things happen and then things unhappen and after a while it’s like they never happened. For instance, little seems to have happened all summer long with the matter known as RussiaGate, the attempt by high US government officials to overthrow the result of the 2016 election by pretending that Russia was trying to interfere in the 2016 election.

Quite a confection of lies and subterfuge. It apparently grew out of an effort at the highest levels of the Obama administration well before 2016 to run so-called intel operations against the perceived enemies of Mr. Obama’s foreign policy. One target was General Michael Flynn, who until 2014 had headed the Defense Intelligence Agency, which is devoted to military intel analysis. General Flynn was known to be unfavorably disposed to Mr. Obama’s deal to pay billions to Iran for a halt in that country’s nuclear weapons program.

After retiring, General Flynn set up his own intel consulting company, which had two clients in Russia: a short-hop airline and a cyber-security firm owned by a holding company in Britain. In late 2015, General Flynn attended a Moscow dinner for Russia Today (RT) where he sat next to Vladimir Putin and gave a speech for which he was paid $45,000. Note: at that point, General Flynn was a private citizen and we were not at war with Russia. It was one of many European nations that Americans were allowed to do business in.

My own heuristic analysis is that rival Intel chief, John Brennan of the CIA, enlisted British Intel “asset” (i.e., agent) Joseph Mifsud to sandbag General Flynn in order to put him out of business and shove him offstage. The scheme failed, and soon the General was seen around rallies for candidate Donald Trump. In one notorious scene at the Republican convention, he castigated his former colleague Hillary Clinton and joined in the crowd’s chant to “lock her up.” I’m sure that went over well with Mrs. Clinton and all the Obama administration honchos then still running the CIA, the FBI, and the DOJ.

After Mr. Trump won the 2016 election, he moved to appoint General Flynn as his National Security Advisor. Within a few days, FBI director James Comey pulled off an entrapment gambit to incriminate General Flynn over a conversation he had with Russian Ambassador Sergey Kislyak — as if incoming high officials for foreign policy are not supposed to associate with foreign ambassadors. You understand now that the government had continued its surveillance of General Flynn for years, including tapping his phone when he moved into his White House office. That enabled Mr. Comey to set up a perjury trap. The General was successfully sandbagged this time, kicked offstage, and conned into a guilty plea. He’s been awaiting sentencing for more than a year.

A few months ago, General Flynn fired his old lawyers and hired Sidney Powell, an attorney who literally wrote the book on discovering prosecutorial misconduct in the case of Alaska Senator Ted Stevens, whose prosecution over Mickey Mouse comped hotel bills was thrown out of court by the same Judge, Emmet Sullivan, who presides in the US versus Flynn. Ms. Powell has now declared that she intends to prove “egregious prosecutorial conduct” and suppression of exculpatory evidence against the DOJ lawyers who ran the case against General Flynn. The government never would have had a case if they revealed the FBI’s internal memos on General Flynn.

Attorney Powell is seeking to have the case thrown out of court. The FBI and the DOJ lawyers who conducted the prosecution have stonewalled the court on producing the documents at issue. Judge Sullivan may sense that he’s seen this movie before. The case took on a life of its own long before William Barr was confirmed as attorney general and one wonders if he has any role in ending this damaging farce. Legal protocol may require Judge Sullivan to complete the case one way or another. I wrote in this space a year ago that General Flynn had been subject to prosecutorial misconduct. Now, I’ll venture to assert that if Judge Sullivan does not throw the case out, Mr. Trump will step in and pardon General Flynn, and in doing so will make it clear exactly how and why he was run into court.

The case against General Flynn was an intersection between all the malign forces operating in RussiaGate: rogue high government officials, the vengeful Mrs. Clinton, her allies in the media, and the ass-covering of figures in Barack Obama’s White House inner circle. The case needs to be resolved to plug the memory hole in American political life.

Meanwhile, all indications are that former acting FBI director Andrew McCabe is about to be frog-marched into an indictment for his part in the epic, many-tentacled RussiaGate intrigue. Perhaps today. Many of the other well-known players will follow. Until they do, the Justice branch of the US government may be considered an enemy of the people.

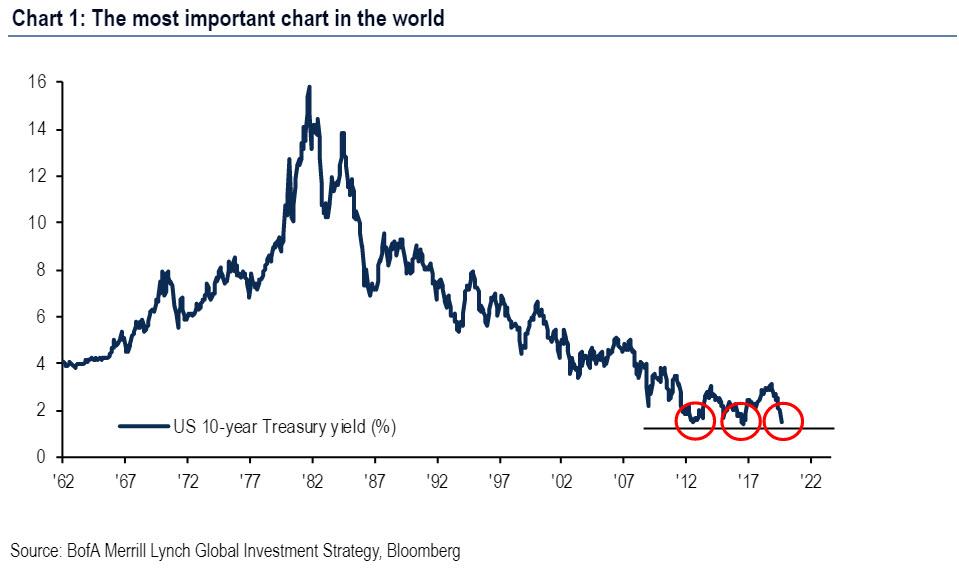

According To Bank of America, This Is “The Most Important Chart In The World”

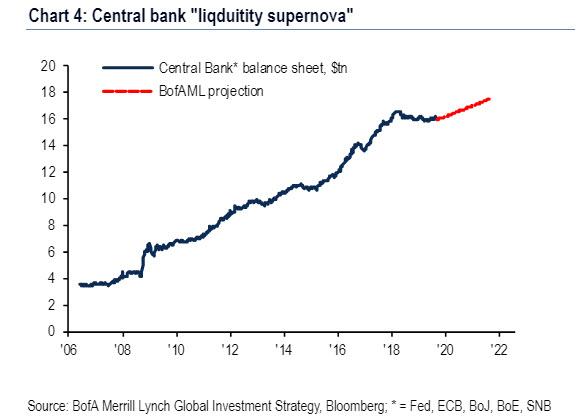

As we noted earlier today, as recently as Sept 3, global negative-yielding debt hit a record $17 trillion, the result of surging recession fears, while 40 global rate cuts in 2019 (China, ECB, Turkey, Malaysia this week) or a total of 748 since Lehman only made the bond bull case that much stronger; subsequently, the ECB’s “QE-infinity” announcement meant the “liquidity supernova” is back and central bank assets are back on course for new all-time high of $16.6 trillion in July’20, according to Bank of America, as shown in the chart below.

Of course, now that both Jackson Hole and Mario Draghi made it clear that monetary policy alone is impotent to stimulate growth, fiscal policy has entered the picture in a big way, with Mnuchin “seriously considering” issuance of 50-year Treasury, the UK announcing a 4.1% rise in government spending, Korea announcing a 9.8% increase, China likewise set to boost infrastructure spend by 7-9%, and even a recessionary Germany is set to raise spending €50bn.

Of course, as Draghi laid out on Thursday, the only way a fiscal stimulus deluge will be possible, is if central banks backstop the bond issuance with “open-ended QE”, de facto launching MMT-lite, which effectively means that the entire world is now set for “Japanification.”

The result, as BofA’s CIO Michael Hartnett explains, is that “investors are now all-in on bond bubble”:

this can be seen in record inflows to bonds + record prices across fixed income + widespread belief central banks to keep rates extraordinarily low + growing conviction US rates can turn negative = bond mania & 2019 consensus capitulation into “Japanification” theme; and explains 2019 extreme relative positioning in deflation assets vs. inflation assets, credit vs. gold, growth vs. value, defensives vs. cyclicals, US vs. RoW, passive vs. active, private equity vs. stocks…

In an amusing tangent, Hartnett comes up with yet another name for central bankers: “Murders Row”, which he likens to the 1927 NY Yankees batting lineup (“those fellows not only beat you, they tear your heart out”) and says that in 2019 global policy makers are intent on reversing bearish Wall St sentiment… “since Wall St >5X size of Main St (Chart 6) they have every incentive to do so to reverse recession risk, contagion from manufacturing/trade.”

And so, with central banks on their way to remonetize (and nationalize) the world, there are clearly no signs of the bond bubble popping (why would there be with central banks set to backstop the bond market indefinitely): corporate bond inflows continue, private equity & venture capital on pace for record fundraising year ($624bn), QE restarting, zero contagion from Argentina credit event & Ford downgrade from IG to junk.

And yet, as first Morgan Stanley, and then SocGen noted, no-one is positioned for policy success, everyone is positioned for bond bubble to continue.

Which brings us to what BofA calls the “Most important chart in the world”, that of 10-year US Treasury yields, which for the 3rd time since 2012 have failed to sustain a break down below 1.5%…

… in the process catalyzing a furious waterfall of downstream effects starting with yield retracement causing $2.4tn drop in negative-yielding bonds.

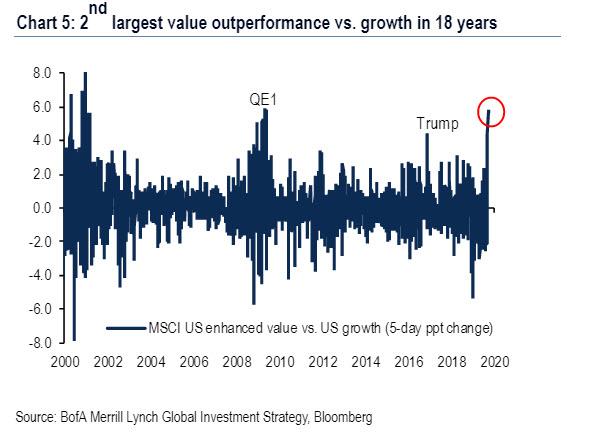

It was also this violent rejection of the 10Y breakdown that unleashed a historic quant quake, or as BofA calls it, the “hate rotation”, as the Value outperformed Growth by 6%t in 5 sessions, the 2nd largest relative return past 18 years.

The good news: for now there are – still – no sign of policy Impotence (US and European credit spreads back to new lows, BTP-bund spread just 138bps); bubbles pop but historically after surge in growth (e.g. Japan in ’89 = 4.9% GDP growth, US in ’99 = 4.8%, Eurozone in ’06 = 3.2%, China in ’07 = 14.2%); as such today’s bond bubble reduces risk of recession.

Meanwhile, the possibility of even more positive surprises has surged on the back of two key developments: huge bond Issuance (US corp. bond issuance to surge $130bn in Sept) allowing companies to refi into record low interest rates, as well as strong mortgage refis, which have resulted in an injection of cash into real economy, letting BofA conclude that macro can surprise to upside next 2 quarters.

Yet the paradox is that much of this is happening in response to a certainty that the Fed will cut rates next week even as inflation is set to spike: to wit, the US quits ratio (workers quitting jobs = sign of confidence they find better job) hit an 18 year high of 2.4% in July – it leads private sector wages by two quarters and implies almost 4% wage growth in Q1’20

Meanwhile, rising investor interest in implications of a Warren/Sanders/Biden win in 2020 – all of which revolve around some version of helicopter money – also say inflation expectations are set to spike.

Based on these observations, here are Bank of America’s tactical conclusion:

Bullish risk assets in 2019 as bearish investor sentiment & the irrationality of central banks and bond markets allows “overshoot” in credit & equity prices this autumn.

No impotence, big issuance, rising inflation means recent violent growth to value, defensives to cyclicals continues episodically in coming months

However, BofA then turns bearish on risk assets in 2020 as the bond bubble pop induces a “Big Top” in credit (as spreads trough) & equities (as multiples peak), causing Wall St deleveraging and – at long last – Main St recession.

{kind=link}