If you watch CNBC long enough, you are bound to hear an investment professional urging viewers to buy stocks simply because of low yields in the bond markets. While the advice may seem logical given historically low yields in the U.S. and negative yields abroad, most of these professionals fail to provide viewers with a mathematically grounded analysis of their expected returns for the equity markets.

Mean reversion is an extremely important financial concept and it is the “reversion” part that is so powerful. The simple logic behind mean reversion is that market returns over long periods will fluctuate around their historical average. If you accept that a security or market tends to revolve around its mean or a trend line over time, then periods of above normal returns must be met with periods of below normal returns.

If the professionals on CNBC understood the power of mean reversion, they would likely be more enthusiastic about locking in a 2% bond yield for the next decade.

Expected Bond Returns

Expected return analysis is easy to calculate for bonds if one assumes a bond stays outstanding till its maturity (in other words it has no early redemption features such as a call option) and that the issuer can pay off the bond at maturity.

Let’s walk thought a simple example. Investor A and B each buy a two-year bond today priced at par with a 3% coupon and a yield to maturity of 3%. Investor A intends to hold the bond to maturity and is therefore guaranteed a 3% return. Investor B holds the bond for one year and decides to sell it because the bond’s yield fell and thus the bond’s price rose. In this case, investor B sold the bond to investor C at a price of 101. In doing so he earned a one year total return of 4%, consisting of a 3% coupon and 1% price return. Investor B’s outperformance versus the yield to maturity must be offset with investor C’s underperformance versus the yield to maturity of an equal amount. This is because investor C paid a 1% premium for the bond which must be deducted from his or her total return. In total, the aggregate performance of B and C must equal the original yield to maturity that investor A earned.

This example shows that periodic returns can exceed or fall short of the yield to maturity expected based on the price paid by each investor, but in sum all of the periodic returns will match the original yield to maturity to the penny. Replace the term yield to maturity with expected returns and you have a better understanding of mean reversion.

Equity Expected Returns

Stocks, unlike bonds, do not feature a set of contractual cash flows, defined maturity, or a perfect method of calculating expected returns. However, the same logic that dictates varying periodic returns versus forecasted returns described above for bonds influences the return profile for equities as well.

The price of a stock is, in theory, based on a series of expected cash flows. These cash flows do not accrue directly to the shareholder, with the sole exception of dividends. Regardless, valuations for equities are based on determining the appropriate premium or discount that investors are willing to pay for a company’s theoretical future cash flows, which ultimately hinge on net earnings growth.

The earnings trend growth rate for U.S. equities has been remarkably consistent over time and well correlated to GDP growth. Because the basis for pricing stocks, earnings, is a relatively fixed constant, we can use trend analysis to understand when market returns have been over and under the long-term expected return rate.

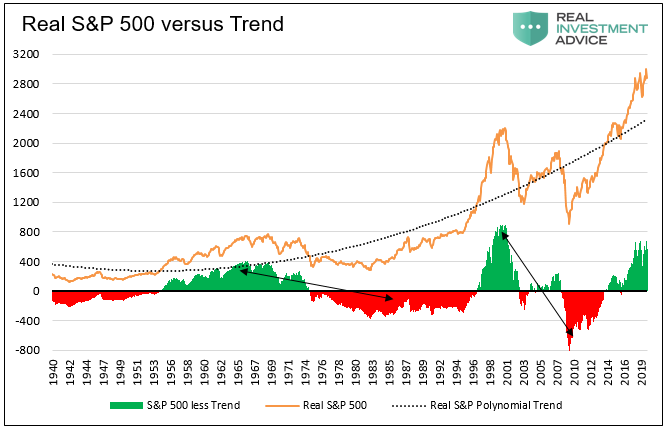

The graph below does this for the S&P 500. The orange line is the real price (inflation adjusted) of the S&P 500, the dotted line is the polynomial trend line for the index, and the green and red bars show the difference between the index and the trend.

Data Courtesy Shiller/Bloomberg

The green and red bars point to a definitive pattern of over and under performance. Periods of outperformance in green are met with periods of underperformance in red in a highly cyclical pattern. Further, the red and green periods tend to mirror each other in terms of duration and performance. We use black arrows to compare how the duration of such periods and the amount of over/under performance are similar.

If the current period of outperformance is once again offset with a period of underperformance, as we have seen over the last 80 years, than we should expect a ten year period of underperformance. If this mean reversion were to begin shortly, then expect the inflation adjusted S&P 500 to fall 600-700 points below the trend over the next ten years, meaning the real price of the S&P index could be anywhere from 1500-2300 depending on when the reversion occurs.

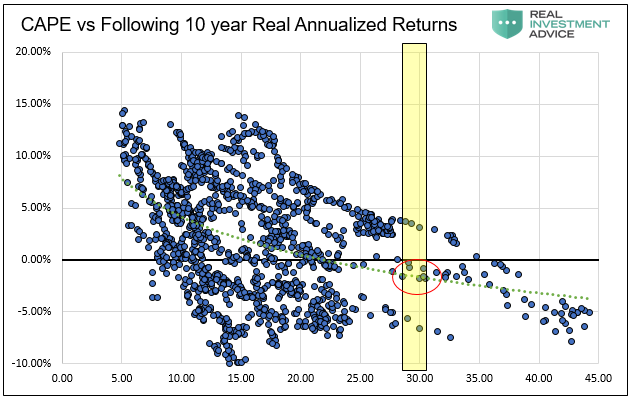

We now do similar mean reversion analysis based on valuations. The graph below compares monthly periods of Cyclically Adjusted Price to Earnings (CAPE) versus the following ten-year real returns. The yellow bar represents where valuations have been over the last year.

Data Courtesy Shiller/Bloomberg

Currently CAPE is near 30, or close to double the average of the last 100 years. If returns over the next ten years revert back to historic norms, than based on the green dotted regression trend line, we should expect annual returns of -2% for each of the next ten years. In other words, the analysis suggests the S&P 500 could be around 2300 in 2029. We caution however, valuations can slip well below historical means, thus producing further losses.

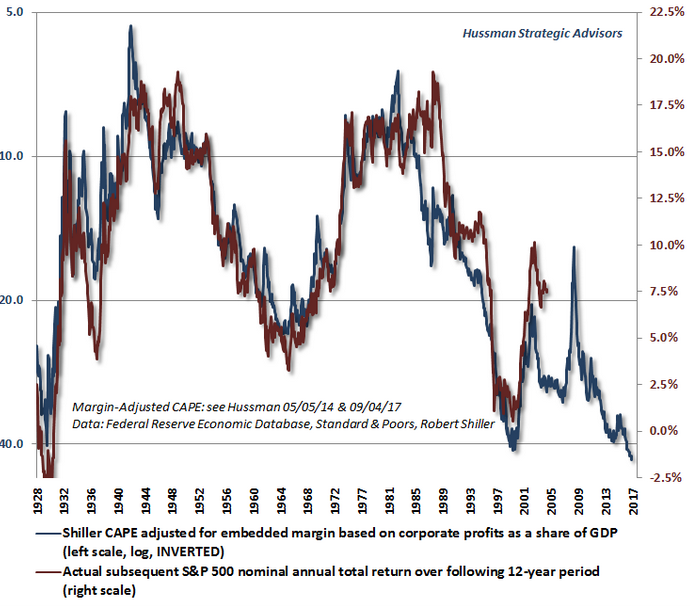

John Hussman, of Hussman Funds, takes a similar but more analytically rigorous approach. Instead of using a scatter plot as we did above, he plots his profit margin adjusted CAPE alongside the following twelve-year returns. In the chart below, note how closely forward twelve-year returns track his adjusted CAPE. The red circle highlights Hussman’s expected twelve-year annualized return.

If we expect this strong correlation to continue, his analysis suggests that annual returns of about negative 2% should be expected for the next twelve years. Again, if you discount the index by 2% a year for twelve years, you produce an estimate similar to the prior two estimates formed by our own analysis.

None of these methods are perfect, but the story they tell is eerily similar. If mean reversion occurs in price and valuations, our expectations should be for losses over the coming ten years.

Summary

As the saying goes, you can’t predict the future, but you can prepare for it. As investors, we can form expectations based on a number of factors and adjust our risk and investment thesis as we learn more.

Mean reversion promises a period of below average returns. Whether such an adjustment happens over a few months as occurred in 1987 or takes years, is debatable. It is also uncertain when that adjustment process will occur. What is not debatable is that those aware of this inevitability can be on the lookout for signs mean reversion is upon us and take appropriate action. The analysis above offers some substantial clues, as does the recent equity market return profile. In the 20 months from May 2016 to January 2018, the S&P 500 delivered annualized total returns of 21.9%. In the 20 months since January 2018, it has delivered annualized total returns of 5.5% with significantly higher volatility. That certainly does not inspire confidence in the outlook for equity market returns.

We remind you that a bond yielding 2% for the next ten years will produce a 40%+ outperformance versus a stock losing 2% for the next ten years. Low yields may be off-putting, but our expectations for returns should be greatly tempered given the outperformance of both bonds and stocks over the years past. Said differently, expect some lean years ahead.

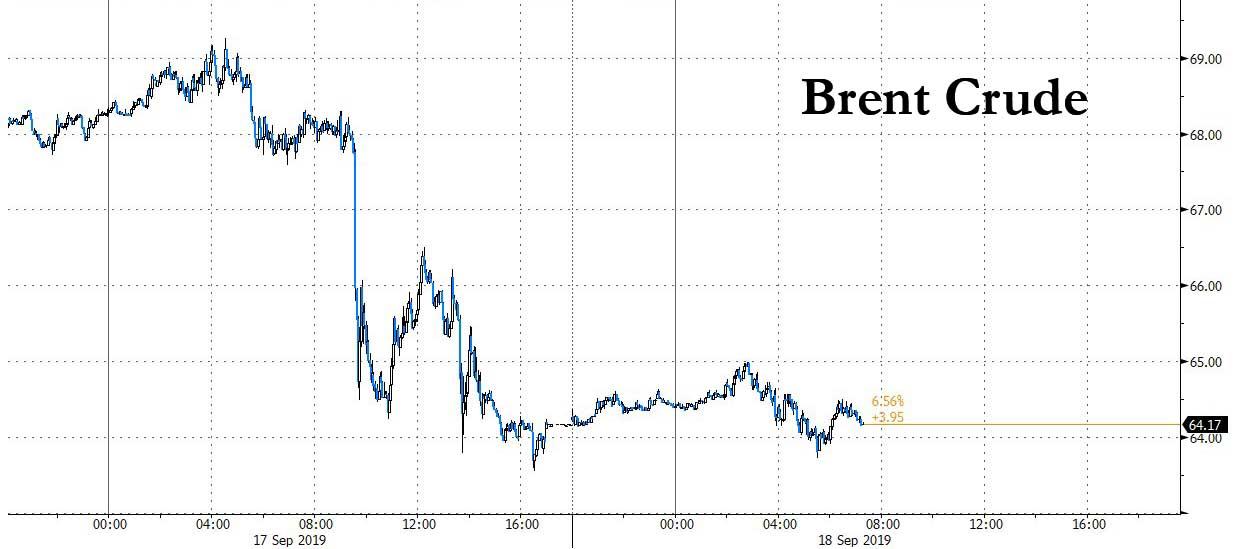

Soaring, then tumbling oil prices; soaring, then sliding repo rates; unprecedented factor volatility as crowded positions exploded – it sure has been quite a week headed into today’s Fed decision which quickly lost the top spot as the most market-moving event of the week amid a barrage of six sigma, exogenous shocks.

While everyone’s attention slowly turned to see how much the Fed would cut today, how Powell would justify easing even as the US economy is once again rebounding, and how the US central bank would respond to the unprecedented liquidity shortage in the repo market, traders were still on edge over this week’s record move in crude even as oil prices cooled further Wednesday after Saudi Arabia said full oil production would be restored by month’s end as it had already revived 41% of capacity. As a result, Brent futures dipped 0.28% to $64.34 a barrel, having conceded about 65% of its gains made after the weekend attack on Saudi Arabia’s oil facilities.

Saudi Energy Minister Prince Abdulaziz bin Salman on Tuesday sought to reassure markets, saying the kingdom would restore its lost oil production by month-end having recovered supplies to customers to the levels they were prior to weekend attacks. “I would think a spike in oil prices will likely prove to be short-term given that the global economy isn’t doing too well,” said Akira Takei, bond fund manager at Asset Management One.

Still, heightened geopolitical tensions underpinned oil as well as some safe-haven assets such as U.S. bonds. A U.S. official told Reuters on Tuesday the United States believes the attacks originated in southwestern Iran, an assessment that could further increase the rivalry between Tehran and Riyadh. Adding to uncertainties in the Middle East were exit polls from Israel’s election, which showed the race too close to call suggesting Prime Minister Benjamin Netanyahu’s fight for political survival could drag on.

At the same time, now that the record barrage of investment grade issuance is finally over, as are hedging rate locks, bonds rallied globally while stocks struggled for traction ahead of Wednesday’s Fed decision, as the dollar rose.

In equities, European stocks traded without direction, with the Stocks 600 index swinging from a loss to a modest gain, led by utilities and oil companies.

A similar drift was observed earlier, when Asian stocks traded little changed as investors awaited the Fed’s decision. Shares rose in China, but declined in Japan and Australia. The Topix dropped for the first time in nine days, ending its longest winning streak in almost two years. Electric appliance makers slid, with Sony Corp. being the biggest drag on the benchmark. Elsewhere, China’s Shanghai Composite Index gained as much as 0.6%, boosted by consumer stocks including Kweichow Moutai Co Ltd. and Foshan Haitian Flavouring & Food Company Ltd. India’s Sensex gained as much as 0.6% as market fears of higher oil prices were assuaged on signs Saudi Arabia is restoring production. The U.S. central bank is broadly expected to cut rates by 25 basis points Wednesday.

S&P 500 Index nudged lower, once again hugging the 3,000 line as Fedex shares plunged in pre-market trading after the company slashed its profit outlook, blaming a global economy weakened by trade tensions.

Looking at today’s main event, in which Fed officials are widely expected to cut their benchmark rate by a quarter-point, some investors such as DoubleLine Capital’s Jeffrey Gundlach are saying the central bank may also boost its balance sheet launching what we dubbed “QE Lite” to stabilize the volatile repo market. Traders also are keeping an eye on whether a potential oil shortage weighs on the global economy, and on preparations by the U.S. and China for top officials to meet on trade in October.

“Markets are currently almost pricing in three more rate cuts by the end of next year, including one by the end of this year, but the chances are that the Fed’s stance will be more hawkish than markets and we could see a rise in bond yields in the near term,” said Masahiko Loo, portfolio manager at Alliance Bernstein.

“Markets want to hear that the Fed is there if needed, the Fed is a backstop,” Alec Young, managing director for global markets research at FTSE Russell, told Bloomberg TV. “There is concern, obviously, from trade, manufacturing, and we’re seeing that bleed into some job-growth weakness, and these are all the big questions that Chairman Powell is going to be getting.”

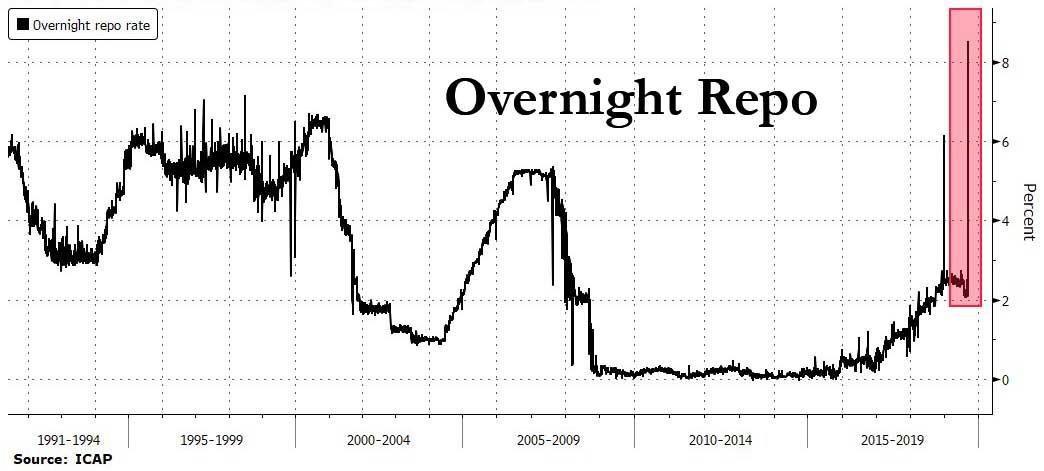

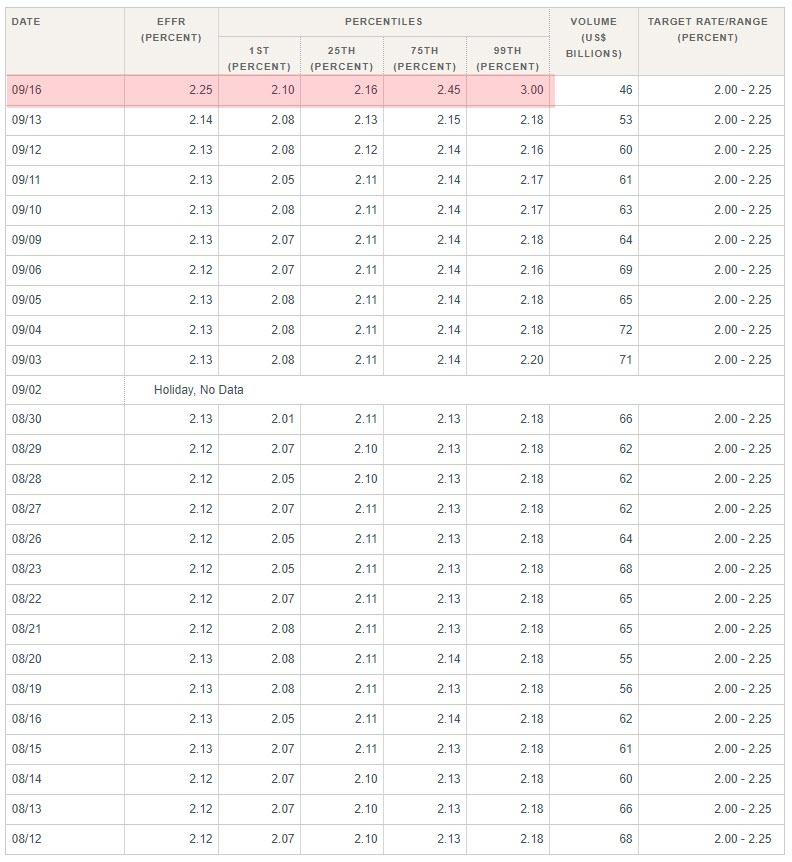

Further complicating the Fed’s discussions, short-term U.S. interest rates shot up this week, with overnight repo rates rising to 7%, due largely to seasonal factors such as huge payments for taxes and bond supply. That prompted the New York Fed to conduct its first repo operation in more than a decade to inject funds to stressed money markets.

The New York Federal Reserve said late Tuesday it would conduct a repurchase agreement operation early on Wednesday “in order to help maintain the federal funds rate within the target range of” 2.00% to 2.25%. Jeffrey Gundlach, chief executive of DoubleLine Capital, said on Tuesday that the repo market squeeze makes it more likely that the Federal Reserve will resume expansion of its balance sheet “pretty soon.”

In FX, the dollar gained against all peers, paring most of Tuesday’s losses, as money markets remained on edge and traders awaited Wednesday’s Federal Reserve policy decision. The pound retreated from the almost two- month high reached Tuesday; the currency was hit by inflation data and increasing pessimism of the Brexit deal being reached before the Oct. 31 deadline. The Norwegian krone was at the center of attention in the G-10, given that it risks volatility around its central bank decision on Thursday. Sterling traded at $1.2483, down 0.1% so far on the day, having hit a two-month high of $1.2528 as investors reversed their bets against the currency on fear of a no-deal Brexit at the end of next month.

Gold was mostly flat at $1,502.10, while the 10-year U.S. Treasuries yield fell to 1.799%, compared with Friday’s 1-1/2-month high of 1.908% ahead of the Fed’s policy announcement on Wednesday.

Expected data include mortgage applications and housing starts. General Mills will report earnings.

Market Snapshot

S&P 500 futures down 0.1% to 3,003.25

STOXX Europe 600 up 0.08% to 389.66

MXAP down 0.1% to 158.87

MXAPJ up 0.06% to 511.04

Nikkei down 0.2% to 21,960.71

Topix down 0.5% to 1,606.62

Hang Seng Index down 0.1% to 26,754.12

Shanghai Composite up 0.3% to 2,985.66

Sensex up 0.3% to 36,576.19

Australia S&P/ASX 200 down 0.2% to 6,681.59

Kospi up 0.4% to 2,070.73

German 10Y yield fell 2.2 bps to -0.496%

Euro down 0.2% to $1.1053

Italian 10Y yield rose 7.7 bps to 0.581%

Spanish 10Y yield fell 1.9 bps to 0.267%

Brent futures down 1% to $63.91/bbl

Gold spot little changed at $1,501.66

U.S. Dollar Index up 0.2% to 98.41

Top Overnight Headlines from Bloomberg

The Fed bought $53.2 billion of U.S. securities on Tuesday to quell a liquidity squeeze, and said it would conduct another overnight repo operation of up to $75 billion Wednesday morning; the moves had markets reeling and underscored just how deep the structural problems in U.S. money markets have become

Under pressure from Wall Street and President Donald Trump, the Fed is widely expected to reduce interest rates, but its sharply divided policy panel may be reluctant to forecast further cuts

Saudi Arabia reassured anxious customers that crude exports will keep flowing as normal and its industry can recover quickly from the worst attack in its history; the kingdom restored about half of pre-attack capacity at the crucial Abqaiq facility

European Commission President Jean-Claude Juncker said the risk of a no-deal Brexit on Oct. 31 is now “palpable,” sparking a drop in the pound; he said the main sticking point continued to be the so-called backstop to avoid a hard Irish border and demanded that the U.K. provide its proposals for an alternative in written form as soon as possible

Benjamin Netanyahu’s gamble to hold elections for a second time this year backfired after a stunning deadlock left Israel rudderless and convulsed by a new wave of political turmoil

Asian equity markets traded tentatively following the cautious gains on Wall St amid positioning heading into a flurry of central bank activity including the FOMC decision where the Fed are expected to deliver a consecutive 25bps cut. ASX 200 (-0.2%) and Nikkei 225 (-0.2%) were indecisive ahead of the looming risk events and with Australia subdued by losses in the energy sector after an aggressive pullback in oil prices due to reports Saudi oil output will return to normal levels quicker than initially anticipated, while the Japanese benchmark remained at the whim of a choppy currency amid somewhat inconclusive data which showed Exports contracted for a 9th consecutive month albeit at a narrower than expected decline. Hang Seng (-0.1%) and Shanghai Comp. (+0.3%) conformed to the holding pattern seen across regional and global counterparts after the PBoC opted for a net neutral position in its liquidity operations and after President Trump reverted back to a blasé approach on US-China trade in which he suggested a deal could come soon, possibly before the 2020 election or after. Finally, 10yr JGBs initially continued to oscillate around the 154.00 level as the BoJ kick-started its 2-day policy meeting, although prices eventually gained traction after tripping stops through this week’s resistance levels and largely ignored the mostly weaker 20yr JGB auction results.

Top Asian News

An Army of Japanese Salarymen Is Rocking Global Currency Markets

Vietnam Becomes a Victim of Its Own Success in Trade War

Profiting From Trade War, China Fund Jumps 54% in First Year

London Trading More Rupee Than India Shows What Modi Needs to Do

Thai Court Rejects Petition Seeking to Disqualify Prime Minister

Major European bourses are flat (Euro Stoxx 50 +0.1%), following on from a tentative AsiaPac session, amid cautious trade ahead of this evening’s FOMC meeting. IBEX 35 (+0.2%) was mildly softer after the open, although has since turned around, amid more political uncertainty, after the King stated there was no candidate for a parliament investiture vote; meaning Spaniards will return to the polls in November for the fourth time in four years. In terms of sector performance; Energy (+0.4%) has managed to shrug off yesterday’s fall in oil prices, while Telecoms (u/c), Consumer Discretionary (-0.4%), Consumer Staples (-0.2%) and Industrials (-0.1%) are the laggards. Luxury names, including Richemont (-4.1%) and Swatch Group (-2.6%), are under pressure after UBS downgraded the sector, with downside in Moncler (-4.5%) exacerbated by cautious comments from the co.’s CEO, who expressed concern about the situation in Hong Kong. In the lead are utilities (+0.4%), with gains in EDF (+3.7%) helping to prop up the sector (the Co. reported weld issues in six reactor units relating to 16 steam generators but does not believe they pose a significant adverse effect now), while materials (+0.2%) and Tech (+0.4%) are also higher. In terms of other notable individual movers; Kingfisher (-2.4%) is lower after sales disappointed (GBP 6.0bln vs. Exp. GBP 6.02bln and like-for-like sales down 1.8%). Elsewhere, Wirecard (+3.1%) took a leg higher on the news that the co. has signed a strategic co-operation agreement with Japan’s Softbank. Finally, Beiersdorf (-1.0%) is under pressure after being downgraded at Goldman Sachs.

Top European News

U.K. Inflation Rate Falls to Lowest Since 2016 on Games, Clothes

Comcast’s Sky Moves Beyond BT’s Network in U.K. with Fiber Deal

Cobham’s $5 Billion Sale to Advent Sparks U.K. Security Probe

EDF Rises on Belief That Reactor Weld Issues Don’t Need Fixing

In FX, the DXY seems to have established a firm base above 98.000 and Fib support just above the big figure, partly due to weakness in the Greenback’s G10 counterparts, but also on the back of recent firmer than forecast US data/surveys, increased demand for short term Usd funds and a marked change in Fed rate expectations going into September’s policy meeting (odds between another 25bp hike and no change much closer to even from around 90% for +1/4 point only a few days ago). The index is currently just shy of 98.500 and considerably closer to nearest resistance (98.744 yesterday) than the aforementioned downside chart retracement level (98.034).

GBP/NZD/AUD – The major underperformers, with Cable already retreating after another 1.2500+ sortie and failure to sustain gains above the 100 DMA (1.2501) amidst relatively negative Brexit remarks from EU’s Barnier and Juncker, but then extending its pull-back through 1.2450 at one stage in wake of significantly softer than expected UK CPI on the eve of retail sales and the BoE rate convene. Meanwhile, the Kiwi is back under pressure alongside the Aussie after overnight releases showing a decline in Westpac’s LEI and mixed NZ Q2 current account metrics, with Nzd/Usd under 0.6350 again and Aud/Usd sub-0.6850. Note, Aud/Nzd is still pivoting 1.0800 following this week’s dovish RBA minutes and eyeing NZ Q2 GDP later today, while Aud/Usd appears capped by decent upside option expiry interest at 0.6860-65 (1 bn) and 0.6895-0.6900 (2.6 bn).

JPY/CAD/CHF/EUR – Also weaker against their US peer, albeit on a sliding scale as the Yen contains losses over the 108.00 mark with the aid of a narrower than anticipated Japanese trade gap and with expiries also in close proximity (1.1 bn at 108.25-40 and then 1 bn at 108.75 if Tuesday’s multi-week peak and 108.50 are breached) ahead of the FOMC and BoJ tomorrow. Meanwhile, the Loonie has regained some poise and traction having held just above 1.3300 yesterday to meander around 1.3250 awaiting some independent impetus from Canadian CPI in advance of the Fed. Elsewhere, the Franc remains anchored near 0.9950, but has weakened vs the Euro to 1.1000 into the SNB on Thursday even though the single currency has lost momentum against the Buck following another approach towards 1.1100. Indeed, Eur/Usd has pulled back below 1.1050 amidst downbeat commentary from ECB’s de Guindos and the headline pair may gravitate further given more downside option expiry interest compared to upside (1.6 bn at the 1.1000 strike and 1 bn between 1.1020-30 vs 1.7 bn from 1.1100 to 1.1115).

EM – The Rand is also awaiting the Fed before turning attention to tomorrow’s SARB meet, and Usd/Zar has largely taken in stride slightly firmer than forecast SA CPI ahead of retail sales within a 14.7080-6325 band, though mostly trading near the base.

In commodities, the crude complex is largely in consolidation mode ahead of key risk events (FOMC) amid a lack of fresh catalysts and following yesterday’s declines, triggered by news that Saudi oil output will return to normal levels faster than originally assumed; Energy Minister Abdulaziz said oil supply is fully back online and resumed as before after more than half the oil output was resumed in the past few days and that it will keep full oil supply to its customers this month. Losses were later exacerbated by a surprise build in API inventories. Brent Nov’19 futures sit just above the USD 64/bbl handle, just above yesterday’s USD 63.50/bbl lows, with WTI similarly lacklustre just above the USD 59.0/bbl mark. In terms of geopolitical developments, the pace appears to have slowed somewhat; the Trump administration is reportedly considering a range of options to retaliate against Iran including cyberattack or physical strike on Iran’s oil facilities or Revolutionary Guards assets, meanwhile, the Saudis continue to point the finger at Iran, who have doubled down in denial. Looking ahead, IEA Birol will conduct a press conference today at 14.00BST alongside a press conference from the Saudis who are expected to show evidence of Iran’s involvement and that Iranian weapons were used in Aramco attacks. Separately, lacklustre trade in the metals complex reflects cautious sentiment, with gold holding on to the USD 1500/oz level for now and copper a touch lower.

US Event Calendar

7am: MBA Mortgage Applications, prior 2.0%

8:30am: Housing Starts, est. 1.25m, prior 1.19m; Housing Starts MoM, est. 4.95%, prior -4.0%

8:30am: Building Permits, est. 1.3m, prior 1.34m; Building Permits MoM, est. -1.29%, prior 8.4%

DB’s Jim Reid concludes the overnight wrap

I write this from Paris this morning but there’s only one place to start and that’s in Washington ahead of the Fed meeting this evening. Not long ago this FOMC was perhaps gearing up to be closer to a 50/50 call between a 25bp or 50bp cut however the latter looks a lot less likely now with markets only pricing in about a 15% chance of that happening. That fits with the view of our US economists who also expect a 25bp cut which mirrors the consensus.

The bigger focus will be on what the Fed signals about the expected policy trajectory in the coming months. Our US economists note that a continued dovish bias should be evident in the statement language, Summary of Economic Projections and Chair Powell’s press conference. The latter in particular should echo the narrative that, while the baseline outlook for the economy remains favorable, officials are attuned to significant risks emanating from softer global growth and elevated trade uncertainty. As in July, Powell should stop short of detailing the likelihood and timing of any future actions, but the signal should be that the bar is set relatively low for further rate reductions with the Committee intent to “act as appropriate to sustain the expansion”.

Our colleagues do not expect the September rate cut to be the last of this cycle though. With accumulating evidence that the economy is slowing amid greater sensitivity to the trade turmoil, they recently adjusted their call to reflect a further cumulative 75bps of rate cuts after this meeting, specifically at the October, December and January get togethers. All eyes on 7pm BST/2pm EST.

In an ideal world the Fed was probably hoping that markets would go into today in a relative state of calm however the mini sell-off across bond markets over the last couple of weeks and the biggest daily climb for oil in over a decade put an end to that. You can also add panic in the US funding market to that list after the overnight repo rate touched as high as 10% intraday yesterday and one of the highest levels on record. Notwithstanding a technical delay, the NY Fed did move to calm the market by conducting an overnight repo operation – the first in a decade – for $53bn which helped to push the rate back down however another operation is planned for today for up to $75bn.

There appeared to be various schools of thought on what caused the explosion in overnight funding rates with bulging treasury supply, a mismatch of cash liquidity tax payments, regulatory constraints, bloated dealer sheets, banking seasonals and investors selling bonds back to dealers all cited as possible reasons. We remained confused about the real cause!! Whatever created the tensions it’s not gone unnoticed that we’ve had two huge moves in different asset classes this week, in addition to the rates’ selloff of the prior two weeks.

Just on oil, WTI and Brent both sold-off around 6% yesterday – and thus gave up about half of Monday’s gains – after Reuters reported that Saudi Arabia is supposedly close to restarting 70% of the lost oil production following the weekend attack. The same story also suggested that output would be fully back online in the next couple of weeks, citing a “top Saudi source”. The Kingdom later confirmed that they will ensure this month’s supply by drawing on reserves. Aramco’s CEO also confirmed that the Abaqiq facility should be back to pre-attack levels of output by the end of September. Gasoline (-7.73%) and Heating Oil (-9.42%) also fell in tow however the end result for equities was fairly muted. Indeed the S&P 500 ended +0.26% while the DOW and NASDAQ ended +0.13% and +0.40% respectively. This was after the STOXX 600 had closed -0.05%. After the US bell, trade bellwether FedEx cut its 2020 profit outlook on a weaker global economy and trade tensions. The shares were down as much as 10% in after-hours trading potentially wiping out gains for the year.

Meanwhile US HY credit spreads finished little changed with energy spreads 4bps wider. As for bonds, 10y Treasuries finished -4.5bps lower with the 2s10s curve flattening 1bp to +7.2bps, while Bunds finished little changed. It was BTPs (+7.9bps) which stood out the most in Europe though following (an albeit expected) confirmation of the news we discussed yesterday morning that former PM Renzi was leaving the PD to form his own party, further complicating the political stability picture in Italy.

This morning in Asia, with the exception of Japan where the Nikkei (-0.13%) is a touch lower, most bourses are flat to slightly higher ahead of the Fed. That’s the case for the Hang Seng (+0.03%), Shanghai Comp (+0.39%) and Kospi (+0.44%). The yen is slightly weaker, following weak trade export data in Japan this morning (albeit not as weak as expected), and the news yesterday that South Korea had removed Japan from its list of most trusted trading partners.

In terms of the data yesterday, in the US the August industrial production print surprised to the upside at +0.6% mom (vs. +0.2% expected), as did manufacturing production (+0.5% mom vs. +0.2% expected). Given that Powell has previously flagged concerns about the manufacturing sector, this was a modest positive. The only other data release in the US was the September NAHB housing market index which rose 1pt to 68.

In Europe the only data worth noting was the September ZEW survey in Germany where the expectations component improved over 21pts to -22.5 (vs. -37.8 expected). That being said the current situation component did weaken over 6pts to -19.9 (vs. -15.0 expected). So a mixed survey.

In other news, it is worth flagging the unveiling of plans for a Dutch national investment fund for the economy. Finance Minister Hoekstra said in the budget that “we are going to investigate the possibilities for further investment in areas such as innovation, knowledge development and infrastructure” with details expected to be presented to parliament in early 2020. Various media reports in Holland suggested that the fund could be as much as €50bn (about 6% of GDP). As Mark Wall noted yesterday, this isn’t just a sign of follow through on Draghi’s plea for fiscal easing by those member states that can most afford it. With a public debt ratio close to 50% of GDP and a current account surplus of nearly 10%, the Netherlands would fit the bill. What’s more striking is that the Netherlands is one of the most fiscally conservative members of the Eurozone. So this could well put more pressure on Germany. Certainly one to watch.

Speaking of which, yesterday our economists in Germany published a report titled “A new ‘fiscal deal’ in Germany”. They note that there is talk that the climate package announced this Friday might amount to €40bn (until 2023 cumulatively). Technically, this might not be all additional spending but could also include higher climate related taxes and levies (possibly, it also includes expenditure items already earmarked elsewhere). Finally, implementation lags and bottlenecks lead the team to expect that expenditures will rise over time resulting in an amount likely below €10bn (at best 1/4 pp of GDP) for 2020. See their report here .

Looking at the day ahead, needless to say that all the focus will be on the Fed this evening. As for data, this morning the data includes August new car registrations for the Euro Area and final August CPI revisions for the UK and Euro Area. In the US the focus will be on the latest housing market data with August building permits and housing starts due. Away from that French President Macron is due to meet Italy’s Conte.

Blain: “Something Is Happening, And We Don’t Know What It Is”

Blain’s Morning Porridge, submitted by Bill Blain

Why so Calm?

Even as the Fed meeting pondered raising rates by a smidge, it had to intervene to pump money into the short-term US financial system for the first time since the 2008 crisis. That’s a clear sign of financial dislocation – but markets seem utterly unconcerned. (The wires all quote issues such as tax payments and an imbalance between new funding and low redemptions to explain the sudden lack of cash, but none of my money market chums are convinced. They fear something else, a big No-See-Em is underway.)

The last crisis started in money markets. Add that to the ongoing WTF-happened questions about the Saudi bombings, and there seems to be a curious sense of false calm in markets. No vol, no concern, and gold hardly moving. I can’t help but think of ducks; serenely floating upstream while their legs are furiously paddling below the surface. Something is happening, and we don’t know what it is.

Since I don’t know either, today is the day to take a pop at the Green Puritan movement:

There is a great comment from Bill Gates in the FT – Fossil fuel divestment has “zero” climate impact, says Bill Gates. Worth a read, and maybe get yourself thinking about what damage ESG/Green group-think nonsense is doing? Its distorting the global economy and voiding perfectly sane investment strategies. As regular readers will know, I absolutely believe Climate Change is The Big Threat – but I’m more and more convinced that much of the ESG / Green Investment bandwagon is utter bollchocks!

We are not going to solve Climate Change by going back to the Stone Age. It will require technological solutions. Yet, a whole green investment industry of advisors, influencers, and whatever the financial equivalent of an Instragram is, have taken over the agenda. They’ve become the market equivalent of whinny millennials, brutally offended by everything, but failing to realise how much they offend us and hold back solutions. They are fleas looking to feast. Every time I read some b*llsh*t about a wonderful and insightful Green Bond conference I reach for the barf bag. The organisers are fleas biting into bigger fleas.

The Gates article hits it squarely. Divesting from the oil majors will not change the world. Changing the world will change the world – Doh! And the best way to do that is to get everyone on the same side – understanding the problems and the costs of solving it.

Let me give you an example: we all accept renewable energies are critical to replace fossil fuels pumping Co2 into the atmosphere. It makes perfect sense to replace dirty coal fired power stations with sustainable solar, hydro and wind power (and I hope tidal soon).

But building a new Wind Generator, or an array of solar cells, or the turbines for a hydro scheme, requires high-grade steel. Steel is a wonderful material – you can recycle and reuse it. But you also need Carbon, from coking coal, to make it. A typical off-shore wind generator requires 250 tonnes of Met Coal to make. It’s a 1.8 bln tonne per annum market, and it’s in increasingly short supply. It’s known in the business as metallurgical coal – because that’s what its used for. Met Coal is a high value, clean commodity – but can you fund it?

Nope.

That’s because most fund managers have got ESG and Green guidelines that start and end with Coal is evil. They don’t want to propose it to investment committees as they might reject it for “reputational risk” reasons. As a result its bundled alongside dirty coal and cannibalism as too difficult to fund – meaning any smart investor should be taking notes on the basis Met Coal investments are cheap and rewarding. Making them attractive is a more difficult matter – but it has to happen.

And yes – I am working on such difficult deals. If your investment committee hasn’t already been taken over by the ESG pod-people or Green Puritans activists, and you want to make proper returns from real assets that are good for the planet – then give me a call…

Repeat the same exercise on anything that might be a wee bit polluting, environmentally challenging, squishes a few crested newts while saving the rest, and you rule out loads of perfectly good investments that are likely to be as environmentally sound as anything the Green lobby sticks a Green Finance label on.

If the default scenario is don’t do it – then we are missing opportunities. The right way to save the planet is to mitigate, solve, fund and finance things in such a way the environment is protected, the climate improved and things to solve the crisis get made. I believe Greta Thunberg is absolutely on the right track. It’s not her I’m mocking… it’s the lack of bravery by investment managers to do right thing in the face of misguided and ill-informed environmental populism led by Green Puritans!

If you want a decent omelette – you need to crack a few eggs.

Softbank going Flaccid?

Back on Planet reality… I’m struggling to find the time to do more in-depth digging on Softbank, but I’m more and more convinced we’re looking at a massive negative feedback loop. I won’t say its headed into a death-spiral.. (for that might get me a wrist-slapping), so I’ll let you draw your own conclusions.

What we do know is Softbank’s strategy of investing in disruptive tech to bring them to IPO is creaking. The plan looked brilliant – hype up disruptive tech opportunities and rewards, ignore the lack of profitability, talk up their own expertise to spot and fund opportunities, then pile millions into start-ups and reap billions from the ones it could quickly bring to market. It worked as long as hype preceded reality. Reality caught up as it became clear disruptive technologies are only unicorns if they work, are uniquely monopolistic and catch money. The ride-hailing market is awash with competitors. Streaming is something everyone wants a piece of.

The critical point is Softbank valued WeWork at nearly $50 bln a few weeks ago. Or think about it this way. Softbank pumped $100 bln into Tech Start Ups, creating its own market in its own holdings. What are they really worth?

Uber was a wake up moment. The embarrassment of the We-Work failed IPO demonstrates how far off kilter they now are. As a strategy, Tech Disruptive Hype has had its time. Sure, there are more Unicorns that will likely become multi-billion businesses to be snapped up, but how many has SoftBank got on its books? How much less hyped will prices be? How much less when you strip out Softbank and other Tech funds making their own prices on their own investments?

Softbank’s investors sound unhappy. Backers of Vision Fund 2 are pulling out. It’s clear the Saudi SWF Public Investment Fund and Abu Dhabi’s Mubadala are not best pleased. They invested $60bln into the $100bln fund. How much have they made? And will firms like Apple really want to put money into Vision 2 as the model creaks from the We-Work catastrophe?

Next couple of weeks are going to be very interesting. I’ll stick to my earlier thesis WeWork would be the IPO to break the Tech craze, but now I think it could bring down Softbank as well..

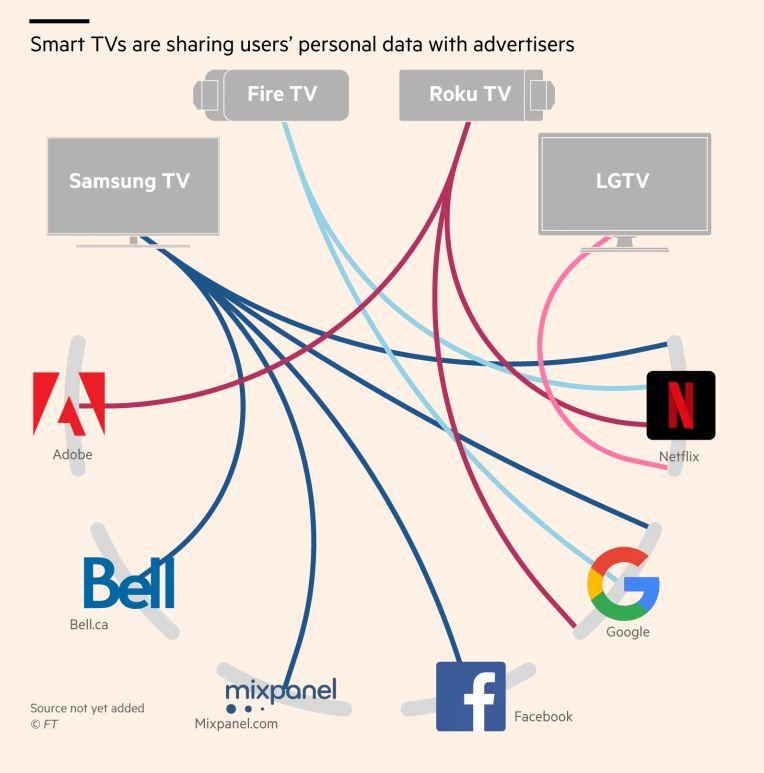

Smart TVs Caught Sending Sensitive User Data To Facebook And Netflix

A study by researchers from Northeastern University and Imperial College London found that many popular smart TV models, including models by Samsung and LG, as well as streaming dongles Roku and Amazon FireTV, are leaking sensitive user data to advertisers.

The models listed above would share data like location and IP address with Netflix, Facebook and third-party advertisers, according to the FT.

Just when social media companies were starting to modify their data collection practices to better respect user privacy, the next threat is coming from the Internet of Things (IoT). Smart TVs are becoming increasingly popular in the US.

In some cases, users’ data were being sent to Netflix even though they didn’t have an account. And it’s not just smart TVs: other smart devices from speakers to cameras have also been caught sending user data to third parties like Spotify.

Nearly 70% of Americans have a smart TV or a Roku or Apple TV. Nearly all of these devices have recognition technology that tracks what you watch, and sells data approximating your interests to advertisers.

In a separate study of smart TVs by Princeton University, researchers found that some apps supported by Roku and FireTV were sending data such as specific user identifiers to third parties including Google.

Amazon was one of the third-parties contacted by about half of the devices tested by researchers at Northeastern.

“Amazon is contacted by almost half the devices in our tests, which stands out because [this means] Amazon can infer a lot of information about what you’re doing with different devices in your home, including those they don’t manufacture,” said David Choffnes, computer scientist at Northeastern University and one of the paper’s authors. “They also can have a lot of visibility into what their competitors are doing.”

Since most of the data shared by the devices were encrypted, researchers couldn’t tell exactly what was being transmitted, in some cases.

“They can definitely see some [viewing] is taking place, but what they can exactly see depends on what the manufacturer is sending, which we have not made an attempt to re-engineer,” said Hamed Haddadi, computer scientist at Imperial College and another paper author.

But experts warn: There’s “minimal oversight” regarding these smart devices. As one analyst warned, “the situation is dire.”

$53.2 Billion In QE Lite: Fed Concludes First Repo In A Decade Amid Liquidity Panic

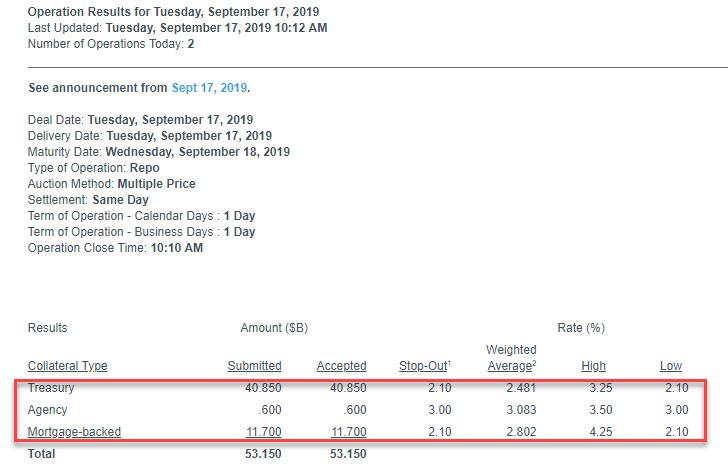

Update 4: It’s over: after a torrid 30 minutes in which the NY Fed first announced a repo operation, then announced the repo was canceled due to technical difficulties, then mysterious the difficulties went away just minutes later, at precisely 10:10am, the Fed concluded its first repo operation in a decade, which while not topping out at the $75 billion max, was nonetheless a significant $53.15 billion, split as follows:

$40.85BN with TSYs as collateral at a 2.1% stop out rate

$0.6BN with Agencies as collateral at a 3.0% stop out rate

$11.7BN with Mortgage-backed securities as collateral at a 2.1% stop out rate.

While the Fed did not disclose how many banks participated in the operation, it is safe to say it was a sizable number. Worse, the result from today’s unexpected repo operation, we can now conclude that in addition to $1.3 trillion in ‘excess reserves’, a Fed which is now cutting rates and will cut rates by 25bps tomorrow, the US financial system somehow found itself with a liquidity shortfall of $53 billion that almost paralyzed the interbank funding market.

Oh, and for those wondering why the Fed did a repo, the answer is simple: it did not want to launch QE just yet. But make no mistake, once repo is insufficient, the Fed will have no choice but to escalate to the next step which is open market purchases.

Which brings us to the bigger question of how long such overnight repos will satisfy the market, and how long before the next repo rate spike prompts the Fed to do the inevitable, and restart QE.

At least president Trump will be delighted.

* * *

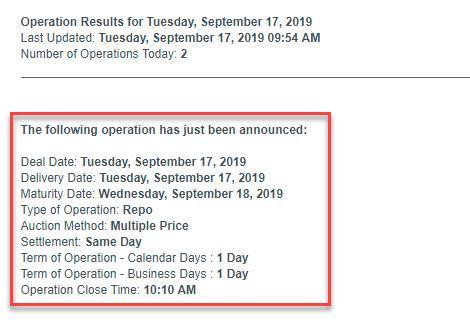

Update 3: The chaos is just getting worse, and minutes after the Fed announced that it would cancel today’s repo operation due to technical difficulties, it announced that it would hold a repo after all, with a closing time of 10:10am.

We now look forward to the results to see just how many counterparties were in desperate need of funding.

Which brings up an interest question: remember the discount window stigma? How many organizations will be willing to admit they were caught in a funding squeeze and needed repo access? We will find out in minutes.

* * *

Update 2: Total chaos – just 15 minutes after the Fed announced it would conduct the first repo in a decade to calm markets after overnight repo rates exploded, sending repo rates back to 0%, the Fed was forced to cancel the repo operation “due to technical difficulties.” This is taking place just a week after the Fed inexplicably suffered similar technical difficulties during a recent POMO operation, which forced only the second ever POMO delay in history.

And while it is unclear if the NY Fed’s infamous “interns” are now in charge of the Open Market Operations desk, and it is also unclear if the NY Fed’s incompetent academic head, John Williams – who recently fired former PPT head Simon Potter – will be fired with cause, it is certainly unclear what will happen to the repo rate which tumbled on the repo news, and will now likely surge higher as it is unknown if and when the Fed will be able to do the repo operation, and more importantly, just what the technical difficulties were that led to this failure.

* * *

Update: Not long after we hinted that today’s action in the US repo market is similar to what took place in 2013 China, when an explosion in funding rates nearly destroyed the local banking system before the PBOC intervened, the Fed has done just that, and as everyone – finally – began to realize this morning that something was very broken in the short-term liquidity markets, as overnight general collateral repo exploded to 10%…

… the New York Fed announced it will conduct its first overnight repo operation (for up to $75 billion) for the first time in a decade.

In accordance with the FOMC Directive issued July 31, 2019, the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York will conduct an overnight repurchase agreement (repo) operation from 9:30 AM ET to 9:45 AM ET today, September 17, 2019, in order to help maintain the federal funds rate within the target range of 2 to 2-1/4 percent.

This repo operation will be conducted with Primary Dealers for up to an aggregate amount of $75 billion. Securities eligible as collateral in the repo include Treasury, agency debt, and agency mortgage-backed securities. Primary Dealers will be permitted to submit up to two propositions per security type. There will be a limit of $10 billion per proposition submitted in this operation. Propositions will be awarded based on their attractiveness relative to a benchmark rate for each collateral type, and are subject to a minimum bid rate of 2.10 percent.

This is precisely what we said last Friday would be the Fed’s first line of defense, when we laid out what may happen after the dollar funding shortage arrives:

repos, i.e. temporary ad hoc reserve adding open market operations,

Treasury purchases, i.e. permanent open market operations, similar to outright UST QE only without a clear QE mandate (for now), and

standing repo facility (SRF), i.e. a new facility that could “automatically” add reserves to the banking system when GC or fed funds reaches a threshold above IOER.

We are now at 1. If and when repo rates continue to rise even with the Fed’s repos in market, the Fed will have no choice but to launch either QE or start a standing repo facility.

For those who may have forgotten how repos work – which is to be expected in a world where all the excess funding was provided by QE – here is the explainer we provided last week:

1. Old school funding pressure lessons: repos & outrights

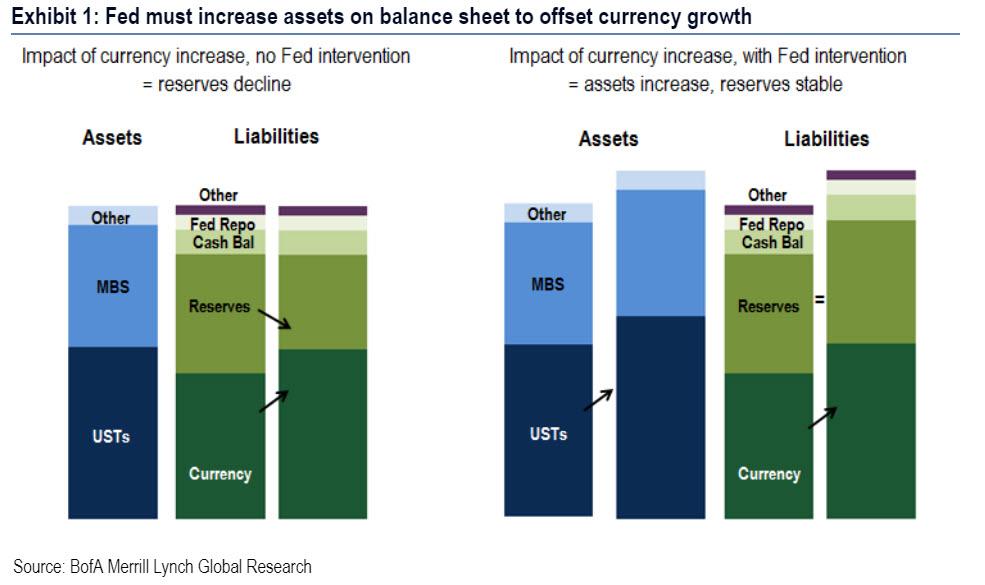

Pre-crisis the Fed relied on two types of open market operations to manage funding markets and their balance sheet: (1) temporary repo or reverse repo operations (2) outright UST purchases. Repo operations were used to “fine tune” the amount of reserves in the banking system to hit the fed funds target rate while outright UST purchases were used to offset currency in circulation growth. As a reminder, currency growth – of which we have seen a dramatic increase in recent years as the amount of $100 bills in circulation has soared – eats away at reserves in the banking system; this would pressure fed funds higher if the Fed did not growth their balance sheet to offset this (Exhibit 1).

Reserve adding operations: both repos and outright UST purchases have the same impact on the Fed’s balance sheet: on the asset side they increase SOMA holdings and on the liability side they increase reserves (Table 1). The only difference is that repos are relatively short-lived and unwind on an overnight or short-term basis; outright Treasury purchases have a permanent impact on the Fed’s balance sheet.

Reserve draining operations: pre-crisis the Fed only ever engaged in open market operations to drain reserves as a “fine tuning” fed funds management exercise. Prior to 2008 the Fed never engaged in any permanent open market operations to drain reserves (such as UST sales) since they only ever used this tool to offset currency growth.

Next, Cabana provides some historical perspective on each of the temporary repo and permanent UST purchase open market operations focuses on those operations that add reserves. As funding pressures begin to emerge and likely worsen in Q4, the BofA rates strategist expects the Fed to step in and use both sets of tools to contain these pressures and keep the fed funds in its target range.

Temporary repo operations

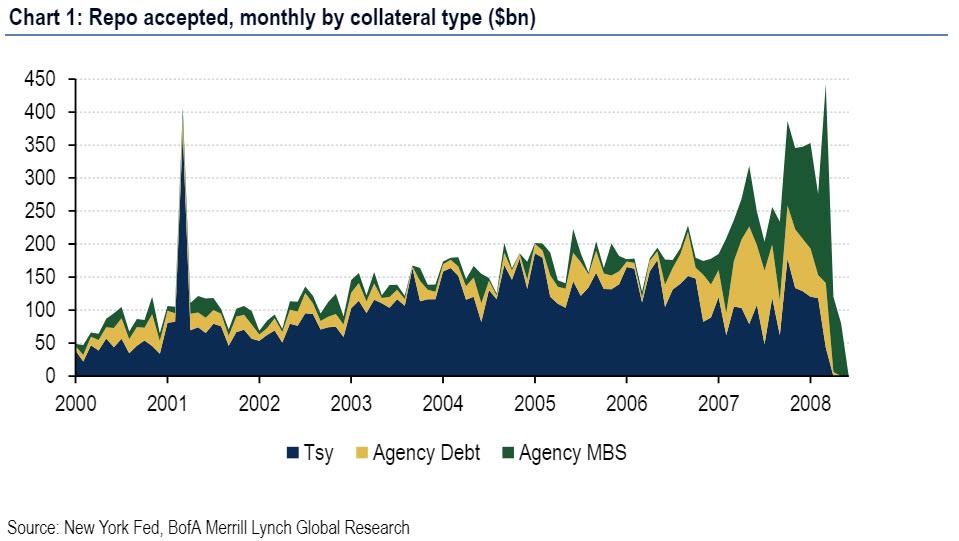

Temporary open market operations were a common practice prior to the crisis, when the Fed was in a scarce reserve regime. The New York Fed conducted frequent repo operations to fine tune the amount of reserves in the system and to ensure that the fed funds effective hit its target point. Below is a review of the mechanics of such repo operations as well as historical activity from 2000-2008. If the Fed conducts repo operations again to offset funding pressures, there will likely be parallels to their historical operations.

The mechanics

Temporary repo operations were executed in the tri-party market and were conducted only with primary dealers. Historically, repos were

multiple price and fixed amount

announced only at the outset of the open market operation

The Fed provides data on repo operations starting in July 2000. An increase in Fed repo operations corresponds to a similar increase in reserves, all else equal (Exhibit 1).

Historical repo operations

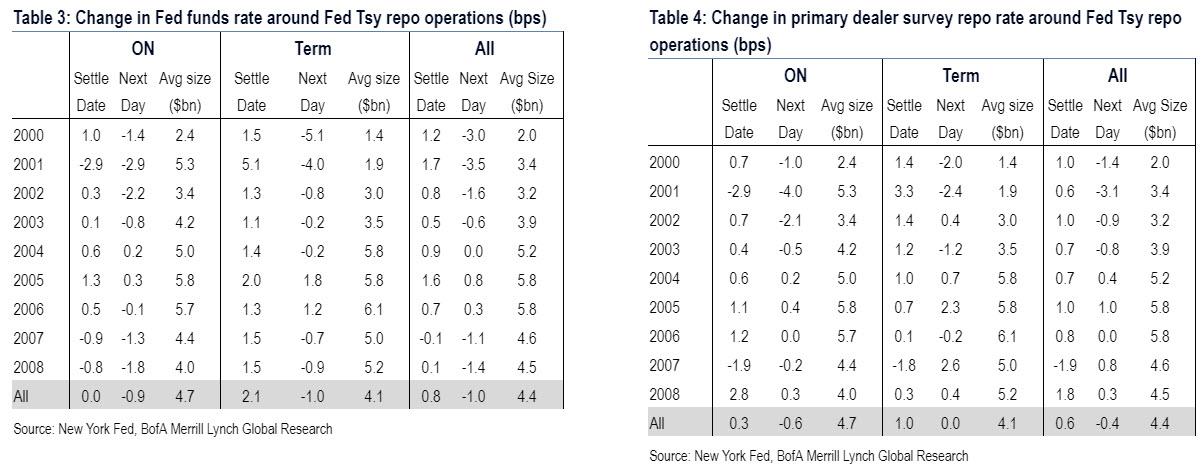

From mid-2000 to the end of 2008, the NY Fed conducted 5 UST repo operations on average each week. Overnight operations averaged around $5bn in size while term operations averaged around $4bn (Table 2). Fed repo operations were all fixed quantity and multiple price, which means that dealers were able to submit varying rates at which they would underwrite the repo operation. The Fed reports the high and low rate that dealers showed into the Fed: the range of rates averaged 13bps and was unsurprisingly wider for term rates. Operations were typically conducted between 8:30 and 10:00AM.

What to expect this time

If funding markets face stress in the next few months – which Bank of America expects will happen – the Fed could easily conduct repo operations to stem upward pressure. Since the recession, the NY Fed has periodically conducted small repo operations in order to “test operational readiness.” There have been 21 operations in total since 2012 – which is somewhat bizarre considering there are well over $1 trillion in reserves floating around the financial system – and the last set of Fed test repo operations was conducted in May. In the past few years the repo tests have been very small (around $23mn in size for USTs), were multiple price, and were overnight or matured in 2-3 business days. The tests have also been across UST, agency debt, & agency MBS collateral. The tests indicate that the NY Fed is prepared to conduct such repo operations at any time and that this is a readily available solution for any sharp increase in funding markets.

* * *

Earlier

Something critical is going on in overnight funding markets: ever since March 20, the Effective Fed Funds rate has been trading above the IOER. This is not supposed to happen, and it just got significantly worse.

As a reminder, ever since the financial crisis, in order to push the effective fed funds rate above zero at a time of trillions in excess reserves, the Fed was compelled to create a corridor system for the fed funds rate which was bound on the bottom and top by two specific rates controlled by the Federal Reserve: the “floor” for the corridor was the overnight reverse repurchase rate (ON-RRP) which usually coincides with the lower bound of the fed funds rate, while on top, the effective fed funds rate is bound by the rate the Fed pays on Excess Reserves (IOER), which served as the corridor “ceiling.”

Or at least that’s the theory. In practice, the effective FF tends to occasionally diverge from this corridor, and when it does, it prompts fears that the Fed is losing control over the most important instrument available to it: the price of money, which is set via the fed funds rate.

Ever since March 20, this fear is front and center because as shown in the chart below, starting on March 20, the effective Fed Funds rate rose above the IOER first by just 1 basis point. The Fed attempted to technically tamp this down.. and failed. But today the Effective Fed Funds Rate has exploded….

Smashing above the IOER…

Source: Bloomberg

As we noted earlier, no one is sure of what is driving this apparent liquidity shortage

elevated UST supply,

bloated dealer balance sheets and year-end regulatory constraints

a banking system near reserve scarcity,

investors selling bonds back to dealers, and

banks and money-market funds to make their quarterly tax payment.

The bottom line is simple – The Fed has lost control of its rate-control mechanism.

So what should the Fed do to regain control over interest rates?

According to Barclays to address the expected increase in fed funds volatility, the Fed, having ended the balance sheet runoff this summer instead of waiting until September, could create a standing repo facility – something which has been rumored for months – or conduct standard open market operations, injecting even more liquidity into the system.

But as we noted earlier, the problem for the Fed is that following today’s massive move in repo higher, it now appears that the Fed is once again behind the curve, and this time the funding squeeze could have dire consequences for not only the economy but the market, as the broken repo plumbing means that despite $1.4 trillion in excess reserves, one or more banks are suddenly left without liquidity, which as we explained over a month ago in “Forget China, The Fed Has A Much Bigger Problem On Its Hands”, the only alternative Powell may soon have is to restart QE.

Fun week so far:

Monday: biggest ever surge in oil

Tuesday: biggest ever surge in GC repo

But stocks are near record highs, because… The Fed.

New York Becomes 2nd State To Ban Flavored E-Cigarettes As ‘Vaping Illness’ Claims 7th Life

New York State has joined Michigan and become the second state to ban sales of most flavored e-cigarettes, CNN reports.

Just as the mysterious ‘vaping illness’ – which has been tied to black-market sales of marijuana vaping products – claimed its seventh life, New York Gov. Andrew Cuomo delivered an executive action to ban sales of flavored vape products that was upheld by state health officials in a late Tuesday vote.

The ban will initially stand for 90 days, but it can be renewed or extended.

Andrew Cuomo

The only two flavors that people will be able to buy are tobacco and menthol.

State Health Commissioner Dr. Howard Zucker said during the emergency meeting that officials would take a closer look at menthol to determine whether that should be banned as well.

Banning flavored products is aimed at reducing the number of teenagers and children who vape.

Zucker presented data to the state’s Public Health and Health Planning Council showing that New York state high school students’ use of tobacco products increased 160% from 2014 to 2018.

Meanwhile, across New York State, there have been 74 confirmed cases of people with fast-developing pneumonia, who developed symptoms after using black-market vaping products.

Of course, the vote at the planning council was hotly debated, with vape shop owners arguing that flavored products accounted for most of their sales, and that the ban would be devastating for their businesses. Others testified that the flavored products helped them quit smoking.

The state is also planning to slap a 20% tax on vaping products, Zucker said.

Cuomo’s ban follows the Trump administration’s new enforcement policy, which will require vaping companies to take all of their flavored products off the market.

Saudi Arabia Says It Has “Material Evidence” Tying Iran To Aramco Attack

Saudi Arabia revealed yesterday that, contrary to its initial estimates, Aramco should be able to restore oil production to 100% capacity by the end of the month. And on Wednesday morning, the kingdom’s Defense Ministry said it was planning a press conference to present “material evidence” purportedly linking Tehran to the unprecedented attack on the Kingdom’s oil infrastructure.

The country’s defense ministry will hold a news conference later in the day laying out new evidence. This follows reports from the US claiming that the roughly 20 missiles and drones used in the attack had been traced back to a ‘launch site’ in southern Iran.

Tehran has denied involvement in the Sept. 14 attacks, while the Houthi rebels in nearby Yemen have claimed credit. But Washington and Riyadh have adamantly blamed Iran, whom they have blamed for several ‘attacks’ in the region since the start of the year.

Of course, this attack would represent a serious escalation from the tanker bombings and the downing of an American drone. Some have speculated that Tehran has nothing to gain from attacks like this, which only serves to provoke the West and Saudi Arabia. The Houthis have carried out several attacks within Saudi Arabia, including the bombing of an airport earlier this year, but experts say the precision of the attack on Aramco’s Abqaiq plant was far more sophisticated than anything the armed movement has ever pulled off. Experts said cruise missiles were likely used to target critical components of the oil complex.

Secretary of State Mike Pompeo and several senior US officials are heading to Saudi Arabia on Wednesday, as are several UN experts responsible for monitoring sanctions on Iran and Yemen, and another team of investigators that will report to the Security Council, according to Reuters.

The Defense Ministry’s news conference will begin Wednesday at 10:30 am ET.

The Saudi Defense Ministry said it will hold a news conference on Wednesday at 1430 GMT to present “material evidence and Iranian weapons proving the Iranian regime’s involvement in the terrorist attack.” Riyadh has already said preliminary results showed the attack did not come from Yemen.

The Iranian leadership infamously threatened that if they couldn’t export crude oil, “no one would” shortly after Washington ended waivers for countries reliant on Iranian oil. The Iranian leadership has ruled out meeting with President Trump, arguing that this would only validate the administration’s strategy of maximum pressure.

Other countries, including Japan, have said they haven’t seen any intelligence linking the attacks to Iran. But that hasn’t deterred one senior US official from asking the UN Security Council to respond.

Several senior officials in the Trump Administration assured Reuters that the Saudi investigation would yield “compelling forensic evidence” showing the location of the attack’s origins.

Trump said Monday that there was “no rush” to retaliate, and that the US was working closely with Gulf states and its European allies. But the US and Saudi Arabia are pushing Iran to stop providing financial assistance to groups like the Houthis, who retain control of most of the territory in Yemen, despite years of fighting with supporters of the ousted government, which has Saudi Arabia’s backing.

While we read a great deal about the huge trade deficit America runs with China it is important to understand we are not the only one. Other countries also have this problem.

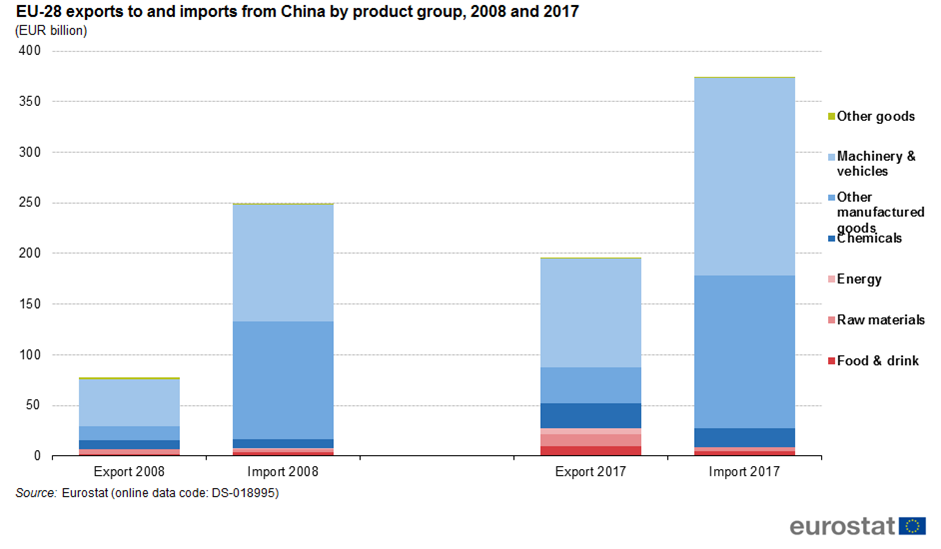

Europe as a whole runs a solid trade deficit with China. In some ways, this is balanced by the EU having a surplus with America. Still, in many ways, a growing trade deficit with China bodes poorly for the EU as they look down the road.

Europe Runs A Solid Trade Deficit With China (click to enlarge)

This brings up the importance of what countries buy and sell to each other. If a county’s exports are not centered around products where they have a core advantage over time they can see them erode. I contend part of the problem the EU has going forward is that much of the EU is simply uncompetitive. This means unless it takes strong action to halt the importation of cheap Chinese consumer goods it will be flooded with them in coming years. Since Europe does not sell China much in the way of “raw goods” it has little to balance this trade.

Simply put, the EU and the companies that call it home lag in both innovation and technology. The most innovative companies based on the number of patents they received in 2017 were IBM, Samsung Electronics, Canon, Intel, LG, Qualcomm, Google, and Microsoft, in that order. Note how European companies are absent from this list. Adding to their lack of industrial leadership is the matter of over-regulation that stifles EU companies from moving forward. When it comes to low-cost production they are also beaten by China and other Asian countries. This has caused Brussels to join Washington in complaining that China wants free trade but does not play fair.

The auto industry is just one example of the EU losing its ability to compete. A recent article titled, “European Carmakers Face Perfect Storm” delves into how European carmakers are facing what could turn out to be a major crisis. It is being created by EU regulators which are driving automakers to cut emissions at great cost. The EU has been enforcing emission caps on cars but beginning next year they will be reduced further to 95 grams of CO per km.This means a slew of electric vehicles will be rolled out but there are no guarantees that people will want to buy those cars. These cars will be much more expensive to build, estimates are each one will cost over $10,000 more to produce, so just because many people claim they are a greener alternative does not guarantee a market for them.

In future years the EU is expected to continue slipping further behind in many areas. Politico reports that Washington is preparing to announce tariffs on billions of goods from the European Union. This follows a decision by the WTO which has just ruled in favor of the US in a case against Airbus. This ends a multi-year transatlantic dispute between the world’s two largest aircraft manufacturers over whether Airbus had benefited from illegal state subsidies.Unfortunately, for both America and the EU the Chinese state-owned aviation manufacturer Commercial Aircraft Corp of China(COMAC), has been busy developing the C919, which is seen as China’s answer to the Boeing 737 and Airbus 320.

The C-919 hits right at the core market of both companies. COMAC is yet to release the price tag of the jet, but a report by China National Radio predicted that it would likely to be sold for around $43 million. This is much cheaper than a Boeing 737 or an Airbus 320 which each cost around $80 million $100 million respectively. It does not take a rocket scientist to calculate how rapidly China can ramp up production.

This is just the sort of thing that dooms the EU into an unwinnable position. The EU will be hard hit if America is successful in trimming its existing deficit with the region while its deficit with China widens.

With parliament suspended and the UK’s EU withdrawal process in enforced stasis, the next major stop on the Brexit road map is the EU summit in Brussels on 17 and 18 October. As we have become accustomed, no one knows what will happen now.

This flowchart though, based on analysis by The Independent’s John Rentoul, runs through the most likely scenarios, starting first with the question of whether the meeting bears fruit in the form of a new Brexit deal.

As Statista’s Martin Armstrong explains, the quickest, but let’s face it, most unlikely outcome, would be a new deal which gets approved by parliament, leading to the UK leaving the EU on the current Article 50 deadline of 31 October.

Going further down the Brexit rabbit hole, we could also see Boris Johnson refusing to request an extension and resigning, the Queen appointing Jeremy Corbyn to sort the mess out, only for a vote of no confidence motion to pass, placing the Father of the House, Ken Clarke, in temporary charge, leading to an Article 50 extension, a general election, and a possible second referendum in 2020.

Turkish President Recep Tayyip Erdogan announced after the first meeting at the Ankara peace talks that his country will not allow terrorists to appear in the area created on the border with Syria; instead, he has proposed to turn it into a refugee city.

“For the refugees there (on the Syrian border), it is necessary to create a city for them to participate in agriculture. I explained to my colleagues that it is necessary to build infrastructure for them,” Erdogan said.

Syrian refugees in Turkey. Image source: The New York Times

“It is necessary to prevent the formation of a terrorist corridor,” the Turkish president said after talks with Russian President Vladimir Putin and Iranian President Hassan Rouhani in Ankara on Monday.

The Turkish capital Ankara on Monday hosted the tripartite summit of the guarantors of the Astana process (Russia, Turkey and Iran) on the Syrian settlement.

During the meeting on Monday, the three presidents agreed to establish a constitutional committee to resolve future political disputes.

With refugees from Syria used in a negotiating tug-of-war between Turkey and the EU, the Balkan region might have to carry the brunt of any large numbers of people on the move trying to reach safety in Western Europe:https://t.co/CjGRSiyIEv

Furthermore, the three presidents discussed the future of the Idlib Governorate, but no official agreement was made to resolve their differences.

* * *

Syrian refugees in a Turkish camp. Image source: AP

Erdogan’s “refugee city” idea comes after earlier this month he issued a ‘with us or against us’ ultimatum to the world, promising that if he couldn’t have his Syria ‘safe zone’ (read: land grab to ethnically cleanse Syrian Kurds), he would flood Europe with one million refugees in response:

“You either support us to have a safe zone in Syria, or we will have to open the gates. Either you support us or no one should feel sorry. We would like to host 1 million refugees in the safe zone,” he said at the time.

It remains unclear, however, whether the so-called refugee city would be on Turkish soil or “newly acquired” Syrian territory occupied by the Turkish Army. Mostly likely in Erdogan’s mind it would be the former.

{kind=link}

{kind=link}

{kind=link}