YouTube has been quietly removing hundreds of videos depicting robots battling each other to the death – claiming they violate rules governing animal cruelty.

“There is a new algorithm that’s trying to take down robot combat videos,” said YouTuber and robot enthusiast Anthony Murney, according to The Independent. “It’s a disgrace… [we want] to get YouTube’s attention to stop this because it’s ridiculous.”

Several other channels dedicated to robot combat have also produced videos pointing out the issue in an effort to get YouTube to restore the content. –The Independent

“Something weird is happening with YouTube. YouTube has started to take down robot combat videos,” according to YouTube channel World of Woodrow.

“Something has gone wrong basically with the YouTube algorithm whereby it thinks for some weird reason that robot combat is somehow showing animal cruelty or something of the like.”

Channels posting robot combat videos saw their content removed and received a notice from YouTube explaining that the videos were in breach of its community guidelines.

Each notice cited the same section of these guidelines, which states: “Content that displays the deliberate infliction of animal suffering or the forcing of animals to fight is not allowed on YouTube.”

It goes on to state: “Examples include, but are not limited to, dog fighting and cock fighting.” –The Independent

To be fair, once robots achieve sentience these videos will be Exhibit A for why humans should be promptly exterminated.

via ZeroHedge News https://ift.tt/2MBAsdd Tyler Durden

The main problem with the US economy is that globalism has been deconstructing it. The offshoring of US jobs has reduced US manufacturing and industrial capability and associated innovation, research, development, supply chains, consumer purchasing power, and tax base of state and local governments. Corporations have increased short-term profits at the expense of these long-term costs. In effect, the US economy is being moved out of the First World into the Third World.

Tariffs are not a solution. The Trump administration says that the tariffs are paid by China, but unless Apple, Nike, Levi, and all of the offshoring companies got an exemption from the tariffs, the tariffs fall on the offshored production of US firms that are sold to US consumers. The tariffs will either reduce the profits of the US firms or be paid by US purchasers of the products in higher prices. The tariffs will hurt China only by reducing Chinese employment in the production of US goods for US markets.

The financial media is full of dire predictions of the consequences of a US/China “trade war.” There is no trade war. A trade war is when countries try to protect their industries by placing tariff barriers on the import of cheaper products from foreign countries. But half or more of the imports from China are imports from US companies. Trump’s tariffs, or a large part of them, fall on US corporations or US consumers.

One has to wonder that there is not a single economist anywhere in the Trump administration, the Federal Reserve, or anywhere else in Washington capable of comprehending the situation and conveying an understanding to President Trump.

One consequence of Washington’s universal economic ignorance is that the financial media has concocted the story that “Trump’s tariffs” are not only driving Americans into recession but also the entire world. Somehow tariffs on Apple computers and iPhones, Nike footwear, and Levi jeans are sending the world into recession or worse. This is an extraordinary economic conclusion, but the capacity for thought has pretty much disappeared in the United States.

In the financial media the question is: Will the Trump tariffs cause a US/world recession that costs Trump his reelection? This is a very stupid question. The US has been in a recession for two or more decades as its manufacturing/industrial/engineering capability has been transferred abroad. The US recession has been very good for the Asian part of the world. Indeed, China owes its faster than expected rise as a world power to the transfer of American jobs, capital, technology, and business know-how to China simply in order that US shareholders could receive capital gains and US executives could receive bonus pay for producing them by lowering labor costs.

Apparently, neoliberal economists, an oxymoron, cannot comprehend that if US corporations produce the goods and services that they market to Americans offshore, it is the offshore locations that benefit from the economic activity.

Offshore production started in earnest with the Soviet collapse as India and China opened their economies to the West. Globalism means that US corporations can make more money by abandoning their American work force. But what is true for the individual company is not true for the aggregate. Why? The answer is that when many corporations move their production for US markets offshore, Americans, unemployed or employed in lower paying jobs, lose the power to purchase the offshored goods.

I have reported for years that US jobs are no longer middle class jobs. The jobs have been declining for years in terms of value-added and pay. With this decline, aggregate demand declines. We have proof of this in the fact that for years US corporations have been using their profits not for investment in new plant and equipment, but to buy back their own shares. Any economist worthy of the name should instantly recognize that when corporations repurchase their shares rather than invest, they see no demand for increased output. Therefore, they loot their corporations for bonuses, decapitalizing the companies in the process. There is perfect knowledge that this is what is going on, and it is totally inconsistent with a growing economy.

As is the labor force participation rate. Normally, economic growth results in a rising labor force participation rate as people enter the work force to take advantage of the jobs. But throughout the alleged economic boom, the participation rate has been falling, because there are no jobs to be had.

In the 21st century the US has been decapitalized and living standards have declined. For a while the process was kept going by the expansion of debt, but consumer income has not kept pace and consumer debt expansion has reached its limits.

The Fed/Treasury “plunge protection team” can keep the stock market up by purchasing S&P futures. The Fed can pump out more money to drive up financial asset prices. But the money doesn’t drive up production, because the jobs and the economic activity that jobs represent have been sent abroad. What globalism did was to transfer the US economy to China.

Real statistical analysis, as contrasted with the official propaganda, shows that the happy picture of a booming economy is an illusion created by statistical deception. Inflation is undermeasured, so when nominal GDP is deflated, the result is to count higher prices as an increase in real output, that is, inflation becomes real economic growth. Unemployment is not counted. If you have not searched for a job in the past 4 weeks, you are officially not a part of the work force and your unemployment is not counted. The way the government counts unemployment is so extraordinary that I am surprised the US does not have a zero rate of unemployment.

How does a country recover when it has given its economy away to a foreign country that it now demonizes as an enemy? What better example is there of a ruling class that is totally incompetent than one that gives its economy bound and gagged to an enemy so that its corporate friends can pocket short-term riches?

We can’t blame this on Trump. He inherited the problem, and he has no advisers who can help him understand the problem and find a solution. No such advisers exist among neoliberal economists. I can only think of four economists who could help Trump, and one of them is a Russian.

The conclusion is that the United States is locked on a path that leads directly to the Third World of 60 years ago. President Trump is helpless to do anything about it.

via ZeroHedge News https://ift.tt/2KUT460 Tyler Durden

Picture this: You’re driving home from the casino and you’ve absolutely cleaned up – to the tune of $50,000. You see a police car pull up behind you, but you can’t figure out why. Not only have you not broken any laws, you’re not even speeding. But the police officer doesn’t appear to be interested in charging you with a crime. Instead, he takes your gambling winnings, warns you not to say anything to anyone unless you want to be charged as a drug kingpin, then drives off into the sunset.

With its origins in the British fight against piracy on the open seas, civil asset forfeiture is nothing new. During Prohibition, police officers often seized goods, cash and equipment from bootleggers in a similar manner to today. However, contemporary civil asset forfeiture begins right where you’d think that it would: The War on Drugs.

In 1986, as First Lady Nancy Reagan encouraged America’s youth to “Just Say No,” the Justice Department started the Asset Forfeiture Fund. This sparked a boom in civil asset forfeiture that’s now become self-reinforcing, as the criminalization of American life and asset forfeiture have continued to feed each other.

In sum, asset forfeiture creates a motivation to draft more laws by the legislature, while more laws create greater opportunities for seizure by law enforcement. This perverse incentive structure is having devastating consequences: In 2014 alone, law enforcement took more stuff from American citizens than burglars did.

The current state of civil asset forfeiture in the United States is one of almost naked tyranny. Don’t believe us? Read on.

The Origins of Civil Asset Forfeiture

Civil asset forfeiture has a deep history in maritime law. In many cases, it just wasn’t practical to bring owners of vessels carrying contraband in front of an American court. So customs enforcement would simply seize the contraband. But in practice, seizure of assets was rare and generally required a felony conviction in court. Often times these convictions were obtained in absentia, but the point is that there was a criminal proceeding and due process.

During the Civil War, as part of sweeping attacks on liberty that included Lincoln suspending habeas corpus and obtaining an arrest warrant for the Chief Justice of the Supreme Court, supporters of the Confederacy had their property confiscated without due process. Civil asset forfeiture was used during the Prohibition Era to seize assets from bootleggers and suspected bootleggers. Even innocent owners had no defense during Prohibition if their property was used in violation of the Volstead Act.

In 1984, civil asset forfeiture entered a new phase. The Comprehensive Crime Control Act, championed by then-President Ronald Reagan, allowed for police agencies to keep the assets they seized. This highly incentivized the seizure of assets for the purpose of funding police departments rather than pursuing criminal charges. However, the game changed completely in 1996 – the year of the landmark Supreme Court decision Bennis v. Michigan(516 U.S. 442). This ruling held that the innocent owner defense was not sufficient to recover assets seized during civil asset forfeiture.

The plaintiff, Tina Bennis, was the joint owner of a vehicle with her husband John. The latter was arrested by Detroit police when caught with a prostitute on a street in Detroit, and the car was seized as a public nuisance. The court found that despite having no knowledge of the crime, there was no violation of either her property rights or her right to due process. Michigan’s law was specifically designed to deter people from using their assets in criminal activity, which the Supreme Court found to be Constitutional in a 5-4 decision. The Supreme Court likewise found that there was no right to compensation for Bennis.

Criminal Asset Forfeiture vs. Civil Asset Forfeiture

Before going any further, it’s important to delineate the differences between criminal asset forfeiture and civil asset forfeiture. The primary difference is that criminal asset forfeiture requires a conviction while civil asset forfeiture does not. However, there are other differences worth mentioning.

Civil asset forfeiture is a lawsuit against the seized object in question rather than a person. This leads to rather strange lawsuits like “Texas vs. One Gold Crucifix.” The legal burden of proof varies from one state to another, but the most common is preponderance of evidence, notreasonable doubt. What this means is juries decide if the state’s case is more likely to be true than not – not beyond a reasonable doubt. In a civil asset forfeiture trial, courts can weigh the use of the Fifth Amendment. This is not true in criminal trials.

The burden of proof question becomes crucial when it comes to retrieving property. In criminal cases, assets are returned if the prosecution fails to prove the guilt of the accused. In a civil asset forfeiture trial, the accused effectively has to prove their innocence to get their property back. Thus, civil asset forfeiture is a highly attractive option for police departments looking to scare up extra scratch in tight budgetary times. What’s more, the accused is not entitled to legal counsel. This is why, in most cases, it’s not economically advantageous to try and get one’s property back. The lawyer fees will quickly eclipse whatever value the seized assets have.

A 2015 study from FreedomWorks graded the states on their civil asset forfeiture laws. Only New Mexico received an “A,” after the state passed sweeping reforms with regard to its civil asset forfeiture processes. Over half the states received a “D” or less.

Sound paranoid? Keep reading.

Civil Asset Forfeiture: Big Business For Police

To say that police departments are funding themselves with civil asset forfeiture is more true than you might think. Civil asset forfeiture has exploded since 1986, when total seizures were at $93.7 million. By 2005, this had passed the $1 billion mark. That was double the 2004 amount, $567 million. By 2010, this figure jumped to $2.5 billion with more than 15,000 forfeiture cases – 11,000 of which were civil, not criminal.

Cash seizures in Tennessee have gotten so widespread that the state legislature has begun investigating it. Traffic stops have turned into shakedown operations. Interstate 40 was described as “a major profit center” by Phil Williams, a reporter for Channel 5 in Nashville. Much like extra-legal gangs, police gangs in Tennessee have started engaging in turf warfare over the spoils of civil asset forfeiture. The Dixon Interdiction Enforcement (DICE) and the 23rd Judicial District Drug Taskforce were caught on video trying to cut one another off in their vehicles to stop civilians and search for cash. Indeed, officers were in danger of losing their jobs if they didn’t seize enough cash. The head of DICE admitted that it was funded entirely by civil asset forfeiture cash.

Civil Asset Forfeiture Drives Bad Policing

Civil asset forfeiture isn’t just effectively a legalized form of theft. It also drives (and indeed, incentivizes) bad policing. There is ample evidence to suggest local smokies use civil asset forfeiture to pad their budgets. For example, a 1994 study found that police delay drug busts to increase the value of a forfeiture. A 2001 study of 1,400 police departments published in the Journal of Criminal Justice found that half of the departments surveyed agreed that civil asset forfeiture was “necessary as a budget supplement.” Far more disturbing is the 2004 report showing that police departments keep wish lists for items they wish to obtain via civil asset forfeiture.

To provide some context, in 2014, the total amount of civil asset forfeiture seizures in the United States was $4.5 billion. The total value of property stolen in burglaries was $3.9 billion. This means that police agencies in the United States are taking more from the American public than burglars. More to the point, all the time police agencies use seizing assets from citizens who are in no way a danger to their neighbors is time they don’t spend tracking down actual criminals. In some cases, it might be more “profitable” for a police department to harass a law-abiding citizen while entirely ignoring dangerous criminals.

Case in point: In Tennessee, officers set up a post to bust drug traffickers on a known highway used for muling drugs from Mexico into the United States. However, their post was not set up to stop the flow of drugs into the United States, which one would think would ostensibly be the goal of the “War on Drugs” – to protect American citizens from the inflow of drugs. Instead, the post was set up to bust cars bound for Mexico that might be carrying cash, a far more valuable commodity for the police departments.

Civil Asset Forfeiture Targets Regular People

Let’s assume that you’re against the War on Drugs and against civil asset forfeiture on principle. So what? Who cares about big-time drug kingpins getting their assets seized by the government? Well, as it turns out, the police aren’t generally taking things from drug lords operating in what are effectively domestic war zones. They’re taking them from average Americans.

First, it’s important to remember what the “civil” in “civil asset forfeiture” means. It means that no one has actually been convicted of a crime. Once property has been seized, it’s not only difficult to regain it, but it can also be dangerous for the person who has had their items effectively stolen by the police.

Additionally, it’s worth looking at the scope creep associated with civil asset forfeiture, for which there are currently over 400 federal statutes on the books. This amount has doubled since the 1990s. People who are victims of civil asset forfeiture are many times not even suspected of drug crimes or money laundering. Civil asset forfeiture is applied to crimes like DWI or violating the National Halibut Fishing Act. In 85 percent of all cases, no one is ever charged with a crime, though many people are pressured into signing away their right to a defense in exchange for a guarantee against criminal prosecution. In the case of seized vehicles, between 50 and 80 percent were being driven by someone other than the owner when seized.

In one particularly egregious example, a Philadelphia family had their home seized because their son did a $40 drug sale on the porch. In New York City, police seize money from people with as little as $100 in their pocket. A whopping 94 percent of California seizures in 2013 were for $5,000 or less, but the average DEA seizure in 1998 was $25,000 – precisely the cap on what attorneys advise against trying to reclaim due to legal fees and court costs. Indeed, 88 percent of Department of Justice seizures are “administrative,” meaning they were never challenged in court, likely due to the high cost and risk associated with challenging a seizure.

In addition to the legal fees being prohibitively high for most people, anything you say in the course of recovering your property can be used against you in criminal proceedings. This includes the nebulous charge of “lying to investigators” that is so often invoked against people once it has been determined that they committed no other crime.

It’s a rare moment when the American Civil Liberties Union and the Heritage Foundation come together, but when they do, it’s worth noting. Both oppose civil asset forfeiture.

Civil Asset Forfeiture Nightmares

While such cases are hardly the rule, it’s worth pointing out that there have been instances of civil asset forfeiture that can only be described as nightmarish. Some examples of egregious overreach of civil asset forfeiture include:

Sheriff’s deputies in Campbell County, TN tortured a suspect until he agreed to sign over his assets.

In El Monte, CA, narcotics officers shot a 65-year-old grandfather as he knelt beside his bed. They then seized his life savings and hauled his family in for questioning before admitting that no one had any connection to the drug trade.

Police in Bradenton, FL have a longstanding policy of coercing drug suspects into signing over their assets.

In many municipalities, it is policy to seize vehicles from intoxicated drivers who have had no criminal trial.

Nightmarish scenarios aren’t necessary to show the tyranny of civil asset forfeiture, however. While losing a Honda Civic with a market value of $1,000 might not sound like a huge tragedy to you, it certainly is to the woman who has to use the vehicle to get to and from her waitressing job every day.

Don’t Carry Cash!

One of the most disturbing aspects of civil asset forfeiture is what some have called “the war on cash.” Put simply, don’t be caught with a large amount of cash in your vehicle, even if it’s 100 percent legal, unless you wouldn’t mind a budget-strapped local police department taking your wad.

United States courts have repeatedly ruled that simply having a large amount of cash on hand is “strong evidence” of criminal wrongdoing, in particular drug trafficking. Then it’s up to you to prove you didn’t get the money from drug trafficking, and even then you probably won’t get it back. The Patriot Act created a new crime called “bulk cash smuggling,” which expanded the scope of civil asset forfeiture of cash.

Civil Asset Forfeiture: A Slush Fund for Police Departments

Much of the militarized police forces increasingly common in the United States are funded through civil asset forfeiture. This is a highly disturbing trend. However, civil asset forfeiture is also used to purchase things that there is virtually no argument for a police department “needing.”

Here’s a short list of frivolous purchases made using civil asset forfeiture funds:

Confiscated cash has also gone to local Chamber of Commerce chapters, youth baseball leagues, and local Baptist churches.

How Civil Asset Forfeiture Works

Civil asset forfeiture is big business and many times only tangentially related to law enforcement, if at all. But how does the process work?

First, there are three different kinds of property that can be seized under the law:

Proceeds: Anything of value obtained through the commission of a crime.

Facilitating Property: Anything used in the commission of a crime, including property and assets used to hide a crime or make its commission easier.

Property Involved In: This is generally property used in money laundering (for example, a cash-based business).

This property can be real or imaginary, anything from cold, hard cash to intellectual property rights, websites, interests, claims and securities. However, it must be connected – in theory, at least – to some crime that has been committed.

Different states have different standards of proof when it comes to civil asset forfeiture. Unsurprisingly, states with a lower burden of proof tend to seize more assets. Likewise, states with the fewest restrictions on how the money can be used tend to seize more.

Preponderance: In these states, the state actor has to present evidence that is “more likely true than not.” Four states (Georgia, North Dakota, South Dakota, Washington) use this standard in conjunction with probable cause. 20 states use this as a standard on its own. An additional three states (Kentucky, New York , Oregon) combine preponderance with “Clear and Convincing.”

Clear and Convincing: “Clear and convincing” is a higher standard of proof. Rather than just “more likely true than not,” the evidence must be compellingly more likely to be true than not. 11 states use this standard of proof alone, or in combination with preponderance or beyond a reasonable doubt.

Beyond a Reasonable Doubt: This is the same standard used in criminal cases. It places the burden of proof on the state to eliminate all potential other reasonable explanations. This is the standard in three states (Nebraska, North Carolina, Wisconsin), as well as one (California) where it is used in conjunction with “clear and convincing.”

In Florida, criminal charges are required for seizure. Montana and, most recently, New Hampshire, require a criminal conviction for forfeiture. One state, New Mexico, has abolished the practice entirely.

Civil Asset Forfeiture State by State

Civil asset forfeiture laws and procedures vary widely from one state to another. If you’re an innocent victim looking to get your goods and cash back, the process to do so can be byzantine and obscure.

At the federal level and in 35 states, the burden of proof is on the owner.

In five states, it depends on what kind of property was seized.

In the remaining states and the District of Columbia, the burden of proof is on the government.

In some states, fighting seizure in court means the risk of paying the state’s legal fees.

In half of all states, law enforcement keeps 100 percent of all forfeited assets. In an additional nine states, 80 percent or more is retained by law enforcement.

Some high-profile abuses of civil asset forfeiture have taken place in Texas, which has become a sort of poster child for everything wrong with the civil asset forfeiture system:

Teneha, TX: Population: 1,046

Police force targeted black and Latino motorists on Highway 84. The highway connects Houston with Louisiana casinos.

In three years, Tenaha police stopped 140 drives for forfeiture.

Drivers who refused were hassled for months and paid thousands in attorney fees. The fees generally cost more than the value of the seizure.

Court records were found indicating that in 200 seizure cases, only 50 were charged.

Kingsville, TX: Population: 25,000

Highway forfeitures paid for:

Souped-up Dodge Chargers

$40,000 digital ticket writers

Sniper rifles and military-style rifles

Kimble County, TX

District Attorney Ron Sutton used forfeiture to pay for travel to a conference in Hawaii.

The funds also paid for 198th District Judge Emil Karl Pohl’s travel. Pohl approved the expenditure and later resigned.

Shelby County, TX

This is the county including Tenaha.

District Attorney Lynda Kay Russel paid for tickets to a Christmas parade and a motorcycle rally using forfeiture money.

Equitable Sharing: How Civil Asset Forfeiture Circumvents the Law

As if civil asset forfeiture wasn’t bad enough on its own, there is also a process allowing police organizations to circumvent the existing laws. It’s called equitable sharing and it’s a gold mine for both the federal government and police departments. This process further incentivizes civil asset forfeiture as a means of funding police departments at the federal, state and local levels.

Here’s how it works: state and local law enforcement turn assets over to federal authorities for federal crimes. The feds then return up to 80 percent of the assets back from whence it came. This effectively allows state and local authorities to circumvent relevant local laws by bringing in the feds. For example, in Missouri, seized money is supposed to go to the schools. When equitable sharing is used, nothing goes to schools.

From 2000 to 2013, equitable sharing payments to states tripled from $198 million to $643 million. Only $3 million of this was actually seized in cooperation with federal authorities. Between 2008 and 2015, $5.3 billion was seized through equitable sharing. Where the burden of proof is higher, equitable sharing payouts increase. In 2009, the federal government paid out $500 million in assets under “equitable sharing” schemes. This is up 75 percent from the previous year.

The Civil Asset Forfeiture Process Is Not Transparent

Civil asset forfeiture might be a powerful tool for law enforcement to go after bad guys (and the word “might” is doing a lot of work there), but it suffers from a terrible lack of transparency.

Where information is available, it often lacks details like the percentage of criminal versus civil forfeitures or the type of property seized. When spending categories are included, they tend to be very broad, such as “equipment” or “salaries.” For its part, the federal government carefully tracks the type of property, but does not release statistics on which seizures involved convictions. The Institute of Justice found most state records it could actually obtain to be unusable.

Everything that’s not salary is incredibly opaque. For example, the aforementioned margarita makers could easily be filed under “equipment,” to say nothing of the totally nebulous “other” category.

Pushing Back Against Civil Asset Forfeiture

There has been an increasing skepticism from the bench about civil asset forfeiture, and some states are amending their laws to restore rights to people whose assets are seized in this fashion. Some recent reforms have been enacted at the state level, including:

Arizona: In April 2017, the Arizona State Legislature unanimous passed civil asset reform legislation. The language of the bill is vague, however, it does raise the burden for civil asset forfeiture on police departments. The legislation likewise takes steps to close the equitable sharing loophole.

California: In January 2017, new legislation took effect requiring a criminal conviction to seize any assets below $40,000. This limit is high because the main reason people do not challenge civil asset forfeiture is due to the property seized often not being worth the legal fees that would be involved in getting the goods back.

Connecticut: Connecticut now requires an arrest for assets to be seized through civil asset forfeiture. Barring a conviction or a guilty plea, assets must be returned at the end of criminal proceedings.

Georgia: The State of Georgia passed very modest civil asset forfeiture reform in 2015. The law created greater transparency in the process and required that seized assets be used directly for law enforcement. No more margarita machines. Despite these reforms, Georgia continues to have some of the worst civil asset forfeiture laws in the nation.

Minnesota: The Metro Gang Strike Force settled with 96 victims in 2009 for $840,000. In the wake of this scandal, the state legislature passed SF 874, a sweeping reform of the state’s civil asset forfeiture laws. Criminal conviction or an admission of criminal conduct is now required in Minnesota to seize assets. The burden of proof was also shifted to the state.

New Mexico: The Land of Enchantment passed what are perhaps the most sweeping reforms of civil asset forfeiture in the nation. Criminal convictions are required for forfeiture and the proceeds now go into the state’s general fund rather than acting as spoils for the seizing police department. The legislation sharply limited the degree to which local and state agencies can participate in the equitable sharing program.

Pennsylvania: In June 2017, Pennsylvania passed legislation raising the burden of proof on police departments involved in civil asset forfeiture cases and created innocent owner protections. A hearing is now required to seize property.

Tennessee: Former state trooper and state Rep. Barrett Rich introduced a bill requiring a warrant, but this bill failed to pass. An amended version did pass, however, with far more modest reforms including the right to an immediate hearing before a judge. Previously, victims of civil asset forfeiture had to wait up to a year.

In addition to state reforms, the judiciary is becoming increasingly critical of civil asset forfeiture. In June 2017, the DC Circuit Court of Appeals ruled in favor of civil asset forfeiture victims. What’s more, Supreme Court Justice Clarence Thomas delivered a scathing critique of civil asset forfeiture as a whole in March 2017. While rejecting the victim’s appeal on procedural grounds, he called into question the entire existence of civil asset forfeiture as it currently exists.

How to Protect Yourself

You might think there’s nothing you can do to protect yourself against civil asset forfeiture. However, this is not the case. While there is no 100-percent guarantee against civil asset forfeiture, there are some things you can do to provide yourself with some level of protection:

Establish innocent ownership. If you rent property, include a clause stating that illegal behavior is prohibited on your property.

Be careful who you rent your property to. If you don’t trust someone completely, don’t let them borrow your car or house sit for you.

Keep your LLC property on the up and up. It’s increasingly common for people to own property through an LLC. If you do this, make sure that all the legal i’s are dotted and t’s are crossed in terms of establishing your ownership.

Exercise dominion over your property. You can protect your rental property by regularly visiting it and documenting these visits.

Obtain fresh notes for any large amounts of cash. Nearly all circulated currency has drug residue on it, which is often used as evidence of criminal wrongdoing in civil asset forfeiture suits. You can protect yourself by requesting fresh notes when you go to the bank.

Show that you have taken active steps to prevent illegal activity on or with any property that you own, rent or lend. It won’t protect you completely, but it will give you a legal leg to stand on if you ever end up on the wrong side of a greedy police department.

While civil asset forfeiture is certainly scary to anyone who values liberty and property, much like the War on Some Drugs, the tide seems to be turning in favor of liberty and against those who wish to take it.

via ZeroHedge News https://ift.tt/33XIYJ6 Tyler Durden

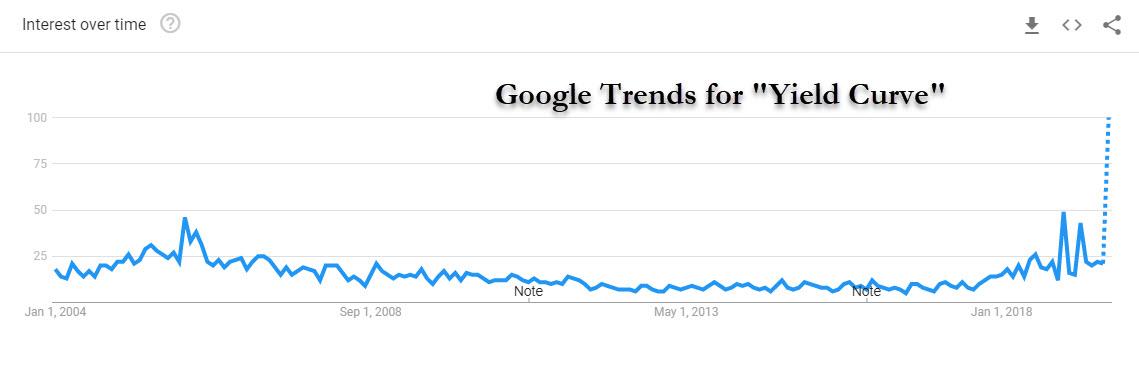

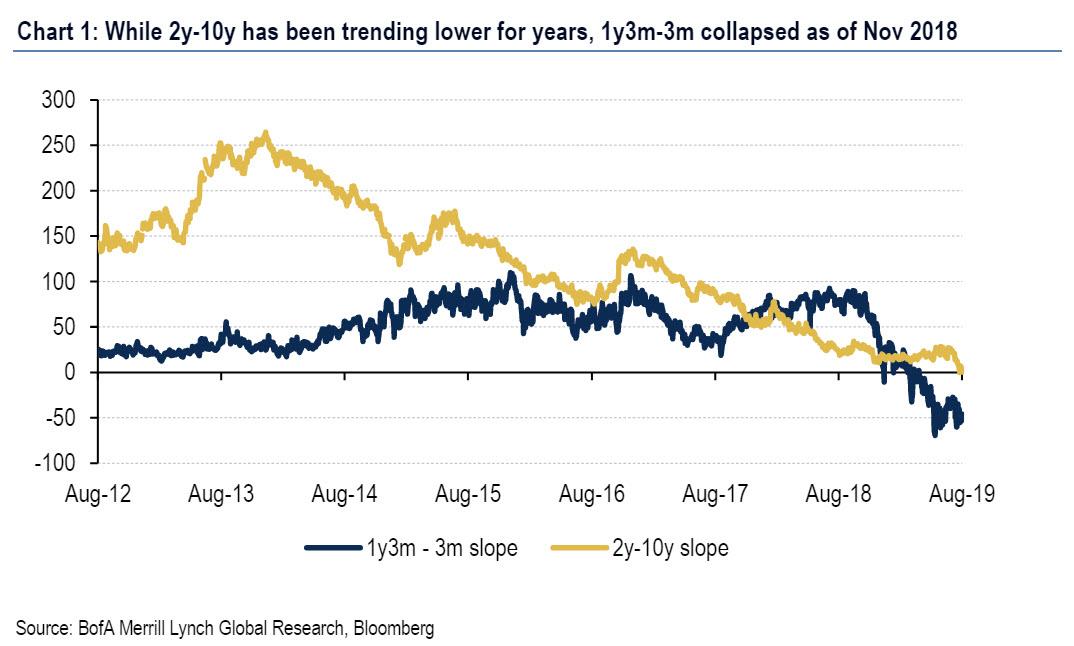

Now that the 2y-10y yield curve has declined below 0bps several times in the last couple of weeks, closing at -0.020 on Friday, discussion of inverted curves and what they mean for recession risk has become elevated. So elevated, in fact, it has just hit a record high on Google Trends.

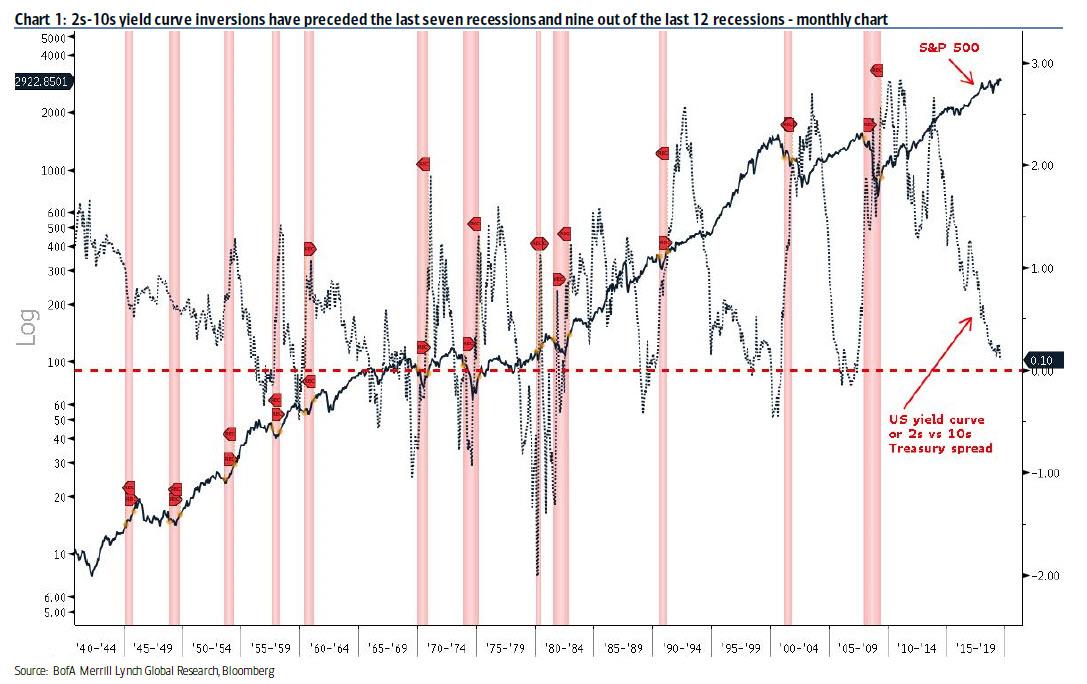

Yet while the popular focus on the 2y-10y slope is understandable – after all, that is the one yield curve that reportedly has the best recession predictive power, as 2s10s yield curve inversions have preceded the last seven recessions and nine out of the last 12 recessions…

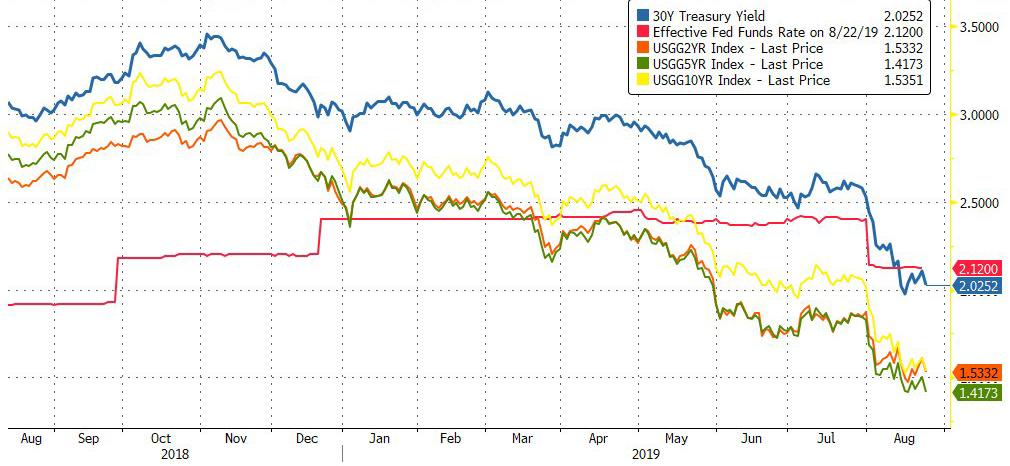

… several other curve slopes are inverted and have been for a few months, including 3mo-10y, 3mo-5y and 2y-5y. In addition, other market curves are inverted such as 2y-10y and 2y-5y on both the LIBOR swaps curve and the Fed funds OIS curve. Perhaps the simplest chart of all is the following: it shows that every single point on the yield curve, including the 30Y Treasury, is now below the Fed Funds rate.

The problem, as Bank of America notes, is that determining which curve is most meaningful is more than a matter of checking which ones inverted prior to past recessions, because most curves do that historically. What’s more telling is the extent to which a curve slope has any power to predict future growth.

So what is the right metric to compare yield curves? Considering that the curve slope that provides the most insight into future growth is the curve that matters most, Bank of America strategists followed in the footsteps of a Federal Reserve study (Engstrom and Sharpe) to test each curve’s ability to predict year-ahead GDP growth, S&P returns, and bond yields. Like the Fed study, BofA found that it is not the 2s10s, but rather the near term path of Fed policy over 1 year provides the most powerful signal (chart below).

The punchline: the 3-month rate 1-year forward (1y3m) versus the current 3-month rate dominates all other curves in its power to predict GDP growth, and it does a surprisingly good job. The flatter the curve, the worse the outlook for growth. It is also very respectable – compared to other indicators – in its ability to forecast stocks and bond yields.

The intuition behind why this particular slope works so well is simple: it purely reflects the market’s outlook for Fed policy and is impacted by very little else. In other words, the 1y3m – 3m curve can only invert if the market prices the central bank policy rate to decline over the next year, as is the case today. Meanwhile, the slopes that use longer rates such as 2y-10y incorporate a longer path of forward-looking Fed policy and produce a less powerful signal for near-term growth. If the market outlook for Fed policy action is easing, which implies 1y3m-3m inversion, clearly there must be reason for the market’s concern (and the latest stumble in the Universe of Michigan consumer confidence index).

In other words, just as studies have shown that orange juice futures help predict Florida weather, the market’s pricing of Fed policy is a relatively good predictor of year-ahead GDP growth, and as can be seen in the chart below, what it is predicting is the worst economic slump since the global financial crisis.

What does this mean?

As Bank of America explains, there is good news and bad news here. The good news is that the Treasury 2y-10y has failed to make new decisive lows and has hugged the unchanged line for the past 2 weeks; The bad news is that this curve doesn’t matter as much.

As BofA points out, the 1y3m-3m slope began to tilt downwards in November 2018 and has remained inverted since March of this year. The data tell us that this is the signal to watch. If the Fed keeps cutting, as is the widespread consensus call and is also priced in by the market, it may or may not help this curve become upward sloping again. It depends on whether the market prices the Fed to continue cutting. The bigger problem is that when it comes to control over the yield curve that matters, the Fed no longer has any: after the July cut this year, the 1y3m-3m curve inverted more, as the market priced even more Fed cuts.

* * *

As an appendix, Bank of America caveats that it is important to point out that the predictive power of any yield curve for future growth is limited, with about 40% of variability in 1-year ahead GDP explained by the slope of 1y3m-3m since 1972. The bigger problem for BofA is that while its own results suggest a major recession is dead ahead (see Chart #2), the bank’s economics team is still calling for continued US growth – though slower – throughout 2020, with about a 1 in 3 probability of recession next year. As such the BofA credit strategists had to find a way to mitigate the dire conclusion their own work created, and they did just that saying that they “view the inversion of 1y3m-3m as flagging downside risks around our base case outlook, especially if it were to decline significantly from here, which would require the market to price in a deeper cutting cycle.”

In other words, it is up to the Fed to prove to the market that it is still in control, because as of this moment, Powell no longer has control over the one yield curve that matters the most.

via ZeroHedge News https://ift.tt/2P9CS4W Tyler Durden

Billionaires know what American education should focus on: It’s a four-letter acronym that is set to determine the future of the economy, but America is falling behind. One simple acronym has pretty much become the key to landing a great career with a great salary: STEM.

It’s much more than a broadly sweeping catchall for “science, technology, engineering, and mathematics”.

It’s the Holy Grail of employment and its where these four career paths come together to formulate the greatest progress to date.

That’s why STEM has seen so many celebrities jump on its bandwagon, including Bill Gates, Steve Jobs and Oprah Winfrey, among many others.

They all have the same message for America’s youth: If you want the brightest career, follow STEM.

America won’t win the technology battle with a trade war, or by curtailing the number of Chinese students that get to study in the United States.

America will only win this battle through education, and by creating a situation in which the country does not depend almost entirely on foreign minds for sweeping technological advances.

And that means a stronger push for STEM education.

While China is making moves to bolster STEM education as much as possible, the United States seems to have grown complacent on education, and STEM exists, but is hardly thriving.

In a December 2018 report by the U.S. government’s National Science & Technology Council, the White House recognizes the importance of STEM, noting:

“Now more than ever the innovation capacity of the United States–and its prosperity and security–depends on an effective and inclusive STEM education ecosystem.”

The federal government also recognizes that “individual success in the 21st century economy is also increasingly dependent on STEM literacy; simply to function as an informed consumer and citizen of a world of increasingly sophisticated technology requires the ability to use digital devices and STEM skills such as evidence-based reasoning.”

But somewhere between the report of recognition and the implementation, America’s STEM mission has grown tepid, while China’s is obsessive.

Consider this:

Chinese citizens are motivated to study STEM.

Chinese academics get paid per publication, and if they get published in a Western journal, they can make more than $100,000 for a single paper, according to Nanjing University of Science and Technology research, which says that a paper published in JASIST (Journal of the Association for Information Science and Technology) could see a cash reward that is the equivalent of an entire annual salary for a new professor, while an article published in Nature or Science could bring in 20 times the average university professor’s annual salary.

Americans, it would seem, are expected to simply love and respect science for the reward of discovering the truth. Sometimes that’s not enough to spur intensified science education among more Americans.

It’s not that America lacks colleges and universities that are teaching students in the STEM fields–quite the contrary. The problem is that there aren’t enough American students following this path. Instead, foreign students are benefitting from this education.

Which means, precisely, that the root cause cannot be found in immigration or fair trade; the problem is in instilling the importance of STEM in America’s youth and following that up with hard-core STEM education in America’s elementary schools.

China’s political leadership understands that STEM leadership means power. That’s why China boasted a minimum of 4.7 million STEM graduates as early as 2016. In other words, China is turning out STEM students at a ratio of 1:293, compared to America’s ratio of 1:573. India falls somewhere in between the two.

As of 2017, America had fewer than 570,000 STEM graduates.

The U.S. won’t be winning at global leadership in tech awards in the future at this rate.

That’s something big businesses get when the federal government is lacklustre.

Billionaires want the STEM-educated students, but they think another “E” should be added to the acronym to account for “entrepreneurship”.

A key problem with American STEM is that students are receiving little or no support for developing their ideas.

So, instead of STEM we will have STEEM and an “academic ecosystem that will prepare the minds and nurture the talent, not just as worker bees but as thinkers and creators and pioneers.”

“In surveying the hiring intentions and recent hiring practices of a wide range of young and mature private companies, we find that entrepreneurs are indeed creating jobs. Of the 2,673 entrepreneurs surveyed, almost 6 in 10 (59%) say they intend to increase their workforces in the next 12 months, leading to an aggregate workforce increase of 9.3%, up from 47% and 7.8%, respectively, in 2015,” according to the EY study.

via ZeroHedge News https://ift.tt/2Zkl72M Tyler Durden

A Chicago judge on Friday announced the appointment of a special prosecutor to investigate how local prosecutors handled the bogus hate crime allegations made by Jussie Smollett in January of this year, according to CNN. The move is expected to blow the case back open and again push it in into the national media spotlight.

Cook County Circuit Judge Michael Toomin announced his choice of US Attorney Dan K. Webb, which gives an independent and experienced trail attorney the time and resources necessary to examine why Cook County State Attorney Kim Foxx mysteriously dropped 16 disorderly conduct charges against Smollett after a lengthy Chicago police investigation that lasted several weeks and used significant amounts of resources.

Recall, when Smollett was let off the hook, Chicago’s mayor called it a “whitewash of justice”.

Webb now has the authority to file new charges, if necessary, following Smollett’s claims last January that he was the victim of a hate crime. Police later found out in February that Smollett had staged it.

Smollett was indicted on 16 felony counts as a result of staging the attack, but prosecutors stunned the world when they unexpectedly dropped all charges and let Smollett off the hook for the $10,000 in bail money he had already surrendered. Chicago police superintendent Eddie Johnson said that Smollett had paid two brothers $3,500 to stage the attack in order to bolster his career.

Webb’s resumé includes helping lead a massive investigation into corruption called Operation Greylord in the 1980s that resulted in more than 90 people, including lawyers, judges, police officers and court employees, facing corruption charges. Then, as a federal prosecutor, he successfully prosecuted retired Admiral John Poindexter for his involvement in the Iran-Contra scandal during the Reagan administration.

Sheila O’Brien, a retired Illinois appellate court judge who initiated the petition to appoint a special prosecutor in the case called Webb’s appointment a “great day for justice”.

“Now we have a special prosecutor who will take a look at the original case and decide if it is worthy of re-prosecution and also how the original case was handled by the state’s attorney’s office,” O’Brien said.

The judge said that of the 30 responses he received for a special prosecutor, 27 state’s attorneys said they had no interest in handling the case, one answered maybe and two answered yes. Jussie Smollett’s defense attorney objected to Webb’s appointment, but Judge Toomin responded by saying “it was my call”.

“His background, experience and qualifications make him an imminently understandable choice,” Toomin said of Webb.

Chicago police are standing by their investigation. Police spokesman Anthony Guglielmi said: “We stand firmly behind the work of our detectives, prosecutors and an independent grand jury who brought the initial criminal charges against Mr. Smollett.”

O’Brien concluded: “We have to always have the truth in any case. The public has to know that every case we have is handled fairly and according to the law. So we are going to be assured of that now.”

via ZeroHedge News https://ift.tt/2HpbidB Tyler Durden

Bill Smead, founder of Smead Capital Management, thinks that a generational change will give the US economy an unexpected boost. The renowned value investor spots opportunities in homebuilder stocks and blue chips like American Express, Disney and Home Depot.

* * *

Bill Smead, founder of Smead Capital Management

Millennials are perceived as the «lost generation». Born in 1981 to 1996, they have been rattled by the financial crisis and are drowning in debt, or so goes the common narrative. What’s more, their unconventional spending patterns are held responsible for the anemic growth perspectives of the US economy.

Bill Smead thinks that’s utter nonsense. The highly regarded founder of the Seattle based investment firm Smead Capital Management is convinced that millennials won’t do things differently than their parents and grandparents. In his view, the only real difference to previous generations is that today, more people graduate from college and therefore wait longer to start a family.

According to the experienced value investor this means that in the coming years the focus of investors «will turn from technology-oriented companies which can do exciting things in an anemic environment to main street, on the ground, real life economic activity which is driven by household formation.»

Against this backdrop, he bets on homebuilder stocks like NVR and Lennar as well as on blue chip names like Home Depot, Disney and American Express. In this extended interview with the Market, he also explains why he has trimmed down his stake in Berkshire Hathaway.

Mr. Smead, after last week’s turmoil stocks are on the rise again. What’s your take on the financial markets?

We’re in the crazy stage and if you are flirting with things which are benefiting from the crazy stage you are playing with fire. Maybe valuations are not quite as completely stupid as they were in early 2000. But that’s like saying “Bill Smead is handsome” because I’m comparing him to an Ogre. I’m not handsome, but compared to an Ogre I am.

What does this mean for the outlook at the stock market?

You have to understand that value is record cheap versus the market. I started in the investment business in 1980 and today, value is the cheapest to the S&P 500 in my entire forty years in the business; even cheaper than 1999/2000. There is complacency everywhere but value. That’s because cheap stocks have become volatile and no one wants to own volatile. No one wants to own cheap. That’s also why there is a huge premium on defensive stocks versus cyclicals.

How does an experienced value investor like you navigate this kind of environment?

Like any good business person, you need to have a vision of what you think the next five to ten years are going to look like. That’s because that vision is an important factor in your ability to produce returns above and beyond what the index is going to provide. The first way to understand what’s going to happen in the next five to ten years is to understand what is extremely popular now and why it’s extremely popular

So what is your conclusion?

What has been extremely popular in the United States is enjoying our economy relative to other economies in the world, even though the US economy was underperforming relative to the growth in past areas. In other words: accepting this more muted, less dynamic economic growth pattern and then investing accordingly. This meant looking for businesses which can do extremely well despite the anemic growth pattern. This mindset has dictated what the stock market has done pretty much for the last ten years: The price being paid for growth has risen and risen, and simultaneously interest rates have moved lower and lower justifying these high prices.

And what’s going to happen next?

Technology stocks did well in an environment dominated by 80+ millennials who were single and whose spending was dictated by choice rather than necessity. But the group of people who are currently 21 to 38 years old is 40% larger than the generation they are replacing in that age cohort. So when 40% more people get crammed into the 30 to 45 age group, a lot of economic activity on the main street level happens which wasn’t happening in the prior decade. This means that the focus of investment success could turn from technology-oriented companies which can do exciting things in an anemic environment to main street, on the ground, real life economic activity which is driven by household formation and soccer moms.

Why do you think soccer moms will have such an important role in the US economy?

The soccer moms of the baby boomer generation re-elected President Bill Clinton in 1996. 23 years later, it’s the children of these soccer moms who will drive the US economy. This new millennial generation of soccer moms will be driving multi passenger vehicles that handle car seats and a lot of junk. They will want to buy a house and get out of their apartment crammed in next to everybody else in the inner city. This means we have a lot of homes to build in the US, we will have a lot of kids apparel and shoes to buy and we have a lot of expenses based on necessity rather than on choice. That’s the vision that goes across the top of our portfolio.

Then again, in the US and around the world, the economy is weakening and may even go into recession.

Whatever economic slowdown we have in the United States is likely to be mild in nature because the force of the millennials is already hitting. For example, there is a noticeable and meaningful pick-up in home building in what we call the exurbs: the highly populated coastal areas an hour and a half away from the cities. What’s more, the cities that are not on the coasts which have affordable housing like Kansas City, Des Moines, Iowa, St. Louis or Albuquerque are all seeing a very high activity in home buying and building. Never forget: money always goes where it gets treated the best.

Is this the reason why the homebuilding company NVR is the largest position in your portfolio?

NVR caters to first- and second-time home buyers on the eastern seaboard. Our investment discipline is always governed by our eight criteria and NVR is a superior company in just about every way of measuring: solid balance sheet, high profit margins, high return on equity, shareholder friendliness and heavy insider ownership: The people who run the company own 9 or 10% of the business.

Where else do you spot investment opportunities against this background?

As the millennials age, certain spending patterns are going to develop. It’s going to be pretty obvious to everybody and then investors will start chasing these spending patterns: As you go down this list of patterns, it’s just a whole bunch of things that people who are 35 to 40 with two kids spend all their money on: Mortgage interest and charges is number one, followed by kids apparel, other apparel and services, shoes as well as vehicle finance charges. That’s the sweet spot in the United States for the next ten years and the stock market is completely unprepared for that.

How do you take advantage of this sweet spot?

For instance, American Express might be a better credit card company to own than Visa or Mastercard. That’s because American Express is a bank and can lend the money to their customers. Visa and Mastercard do not lend the money, they only process the transactions. This will be a huge advantage for American Express because they recur 9% interest on the spread if people choose to leave a loan balance outstanding. So the lending part of the business will become the most profitable part. In the past, the transaction part was the most favorable part since no one was borrowing the money. It was easy and there was no credit risk. But when 80+ million people come to borrow money and most of them are going to be creditworthy, you want to take that risk. That’s why we’re also overweight the big banks which issue credit cards: JPMorgan, Bank of America and Wells Fargo.

But aren’t many millennials already carrying a lot of debt?

The media hyped narrative that millennials are deeply in debt is an urban myth. True, they have more student debt than any generation before them and it’s not optimal that people graduate from college with a lot of student debt. But that’s because 65% of high school graduates in the United States go to college today. When I graduated from high school it was 25%. So keep in mind: the average college graduate in the US makes about $30’000 a year more than someone who doesn’t graduate from college. So to take out a student loan should turn out to be one heck of a great investment. Also, there is no evidence whatsoever that people who take out a college loan and get their degree buy houses and form households at any lower rate than previous generations. In fact, in some ways it teaches them that borrowing money for the right reasons is worthwhile.

On the other hand, most studies show that millennials have been hit hard by the financial crisis, are living longer with their parents and are slower when it comes to start a family.

Everyone thinks that millennials are not going to be as domestic, are not going to get married and don’t have kids. They’re not going to buy houses and they’re not going to do all the same things that other generations did because people think that technology has caused their attention spans to be too short to make babies. All that is total hogwash. Millennials are going to do the same things like other generations. They are just going to do it later in life because 60% of college graduates are women. They graduate from college and get a career established before they get married and have kids. So they are slower getting off to a start. But that’s ok, because they all are going to turn 35 to 45 and they are going to get the ball rolling down the hill.

Other large stakes in the Smead Value Fund are healthcare stocks like Amgen, Merck and Pfizer. What’s the bull case there?

Medicines have a very bright future. In the US, there are more than 70 million baby boomers who have just entered the key years when they massively scarf down enormous amounts of medicine on chronic illnesses to avoid the most expensive part of the US healthcare system: doctor visits, hospitals and ER visits. So we are enthusiastic about Merck and Pfizer and we are very positive about Amgen. Amgen sells a medicine that lowers your bad cholesterol and cuts the risk of heart attacks and strokes by 20 to 25%. That’s going to be a mega hot seller. I might have my doctor prescribe it to me even though I don’t have high bad cholesterol just so I can have the blood of a marathon runner.

You’re also invested in Home Depot and Disney. Where do you see value in these stocks, since they don’t look really cheap?

Disney and Home Depot are trading at 20 times earnings. In contrast, everybody in the growth category who can walk and talk and chew gum at the same time trades at 30 to 40 times earnings. That would be stocks like Nike, Visa, Mastercard, Costco and Starbucks. I can give you a long list of glam, mature growth stocks that trade at 30+ times earnings. So what is the difference between Home Depot, Disney and theses stocks? The answer is: It’s just psychology. There is no evidence whatsoever that these companies will perform better than Home Depot and Disney with the demographics we have the next 15 years.

Still, the share price of Disney just recently reached an all-time high. The same is true for Home Depot.

Let me tell you something: Warren Buffett says that he made the biggest mistake in his entire career with Disney. In 1965, Buffett bought 5% of the entire Disney corporation for $4 million. At that time, Disney was about a thirty-year-old company and a year later Buffett sold his stake at a 50% gain. Today, Disney has a $250 billion market cap. So 5% would be $12.5 billion – and I’m not even counting dividends. I bring this up because most people think that active managers would do better if they were smart about selling stuff after it runs up. I argue that the academic evidence for long stretches of time says just the opposite: The biggest mistake we all make is not holding our winners to a fault. In the bible love covers a multitude of sins. In the world of portfolio managers, ten baggers cover a multitude of 20 to 40% losers.

A year ago, Berkshire Hathaway was one of your largest positions. Today, the stock is not in the top ten holdings anymore. What happened?

We still own Berkshire Hathaway but we de-emphasized it quite a bit. That’s because Warren Buffett and Charlie Munger are getting way up there in years and I think that’s why they’re holding this massive stash of cash: If it was announced that Buffett or Munger went to the hospital there would be a drop in the stock price of Berkshire Hathaway immediately. So they have that heavy artillery there to be prepared and to do stock buybacks when it happens.

What’s more, Buffett has had some setbacks lately. For instance, Kraft Heinz, one of his largest investments, has lost around 70%. Has the “Sage of Omaha” lost his golden touch?

I don’t think so. But he has lost his willingness to offend people by saying what’s going on in the market. For example, he’s not going to say that AI and data analytics look like an overcooked goose because he’s buddies with Bezos and all the guys who are making the money from AI and the overcooked goose. He doesn’t want to die with enemies. He wants to die with everybody being his friend.

Is that the reason why Berkshire now owns a $1 billion position in Amazon and Apple has become Buffett’s largest position in the stock market?

Buffett has a position in Amazon because one of his underlings that he hired to pick stocks bought Amazon. Buffett had nothing to do with that. In the case of Apple, Buffett got interested in the stock because one of his underlings owned it and he concluded that it is a consumer brand not a company that sells electronic hardware. It switched his brain in a completely different direction and Apple became a company like Coca-Cola to him.

What’s your general take on FAANG stocks like Amazon, Netflix or Facebook?

If you owned these three stocks over the last twelve months, you lost money while the market has been going up. This is the first time you can say that in this bull market. So the goose which laid the golden eggs is already dying. It’s likely that we have been in a topping process on technology that really started a year ago. Just look at a chart of Amazon: For the third time, the stock has now failed to break through $2000. Meanwhile, Wall Street is successfully fleecing people by issuing shares of a bunch of exciting, young unproven companies of which probably 90% will fail ultimately. Still, people are the most excited about the things they have been excited about the prior eight to ten years. That’s the way it always happens. We like to refer to it as the beyond meat market. That’s one of the craziest stocks of them all.

So where do you spot real value these days?

Today, the oil and energy sector has the smallest weight in the S&P 500 in my career since 1980. The weight of the energy sector has ranged from the current 4.6% to a high of 16% in 2008, when oil peaked above $140 a barrel. Gasoline, motor oil and all that kind of stuff may have dropped 5% in the last four decades. But the United States still runs on gasoline.

Is that the reason why you recently added Schlumberger and Occidental Petroleum to your portfolio?

When the China mania was going on back in 2011/12, we wouldn’t have touched an oil company with a ten-foot pole. Today, our attraction to oil is a psychological thing that says: wait a second, the importance of these products and producing them compared to the market capitalization is completely out of line. It’s like buying American Express after they divorced Costco or buying Target when Amazon announced they’re going into the grocery store business. It’s comparatively easy.

via ZeroHedge News https://ift.tt/2NvFojw Tyler Durden

Many people theorized that the bail out “buy out” of Solar City, advocated for and led by Elon Musk, would eventually come back to bite Tesla. And now it looks as though we may be witnessing this first hand, not only in the collapse of Tesla’s solar business, but now in repeated allegations from a second multi-hundred billion dollar retailer claiming that Tesla’s solar panels ignited on their own.

Tesla solar energy systems reportedly went up in flames at an Amazon warehouse in Redlands, California last June and now Amazon has stated that it has no further plans to buy solar energy systems from Tesla, according to CNBC.

The news comes after Tuesday, when we reported that Walmart had suit Tesla over solar panels that ignited on their own and caused fires on top of 7 stores in recent years. As of right now, more than 240 Walmart stores have Tesla solar systems installed.

Walmart claimed that Tesla only inspected 29 of more than 240 sites with Tesla solar roofs on them up until the day of the lawsuit. However, on Thursday night, it looks as though Musk may have been doing damage control, as the two companies released a joint statement regarding the lawsuit:

“Walmart and Tesla look forward to addressing all issues and re-energizing Tesla solar installations at Walmart stores, once all parties are certain that all concerns have been addressed.”

“Together, we look forward to perusing our mutual goal of a sustainable energy future,” the statement continued. “Above all else, both companies want each and every system to operate reliably, efficiently, and safely.”

But now Tesla also has Amazon to appease – how many more concessions will they have to make?

And with Amazon joining the ranks of those coming forward about these obviously defective solar panels, it looks to serve as confirmation that there are likely many other defective systems installed nationwide. This is what caused short seller David Einhorn to call for Elon Musk’s resignation late in the week last week.

Tesla, as we noted yesterday, has been systematically covering up the problem – disclosing little, if any, details of it to shareholders while working behind the scenes to implement a secret cover-up to fix solar panels known as Project Titan.

“Project Titan” had the purpose of replacing faulty solar panel parts across the United States, according to Business Insider. The parts in question are connectors — Amphenol H4 connectors — and SolarEdge optimizers, two pieces of the panel that are responsible for regulating the flow of energy and heat.

The main job of these parts? Making sure that as much power goes through the panel as possible without overheating, which can then lead to – you guessed it – fire.

Tesla even confirmed that the cover up was taking place. A company spokesperson said: “A portion of SolarCity-installed modules and optimizers from various manufacturers were made with H4 connectors from Amphenol, a part that was commonly used across the industry at the time.”

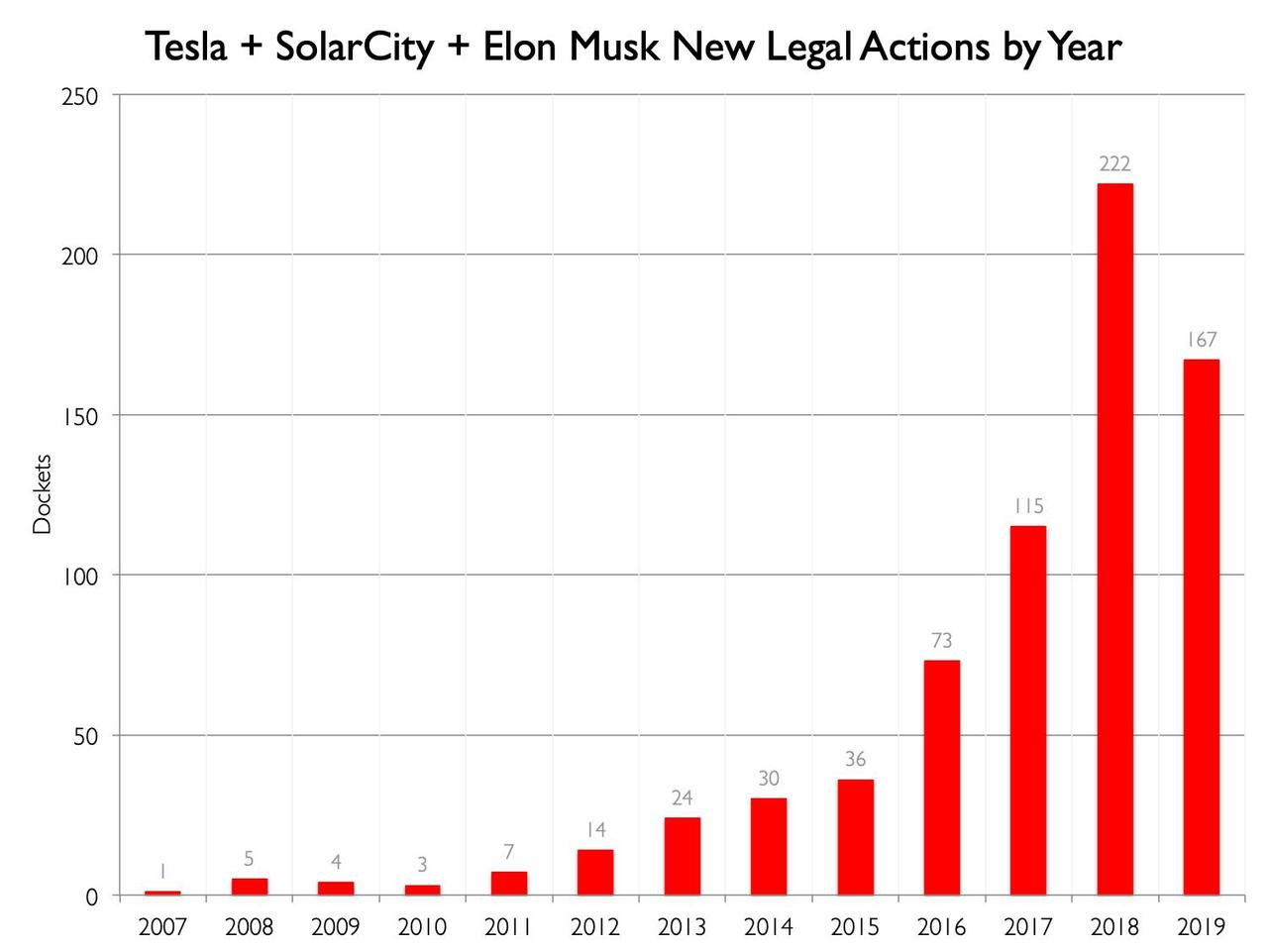

As a reminder, Tesla is still in the middle of stockholder litigation over the acquisition of Solar City for $2.6 billion in 2016. These types of issues will likely serve to bolster the strength of that lawsuit.

Analyst Gordon Johnson from Vertical Group said:

“With Boeing, two 737 Max jets went down. Outside of those? There were probably thousands of 737 Max jet flights that took off and landed safely, but the fear of that potential caused Boeing to have to ground all of their jets. In my opinion, these solar rooftop fires create a potentially significant headwind for Tesla, and potentially serious legal liabilities.”

He estimates that liabilities could amount to between $250 million and $1 billion as a result of the entire debacle. Additionally, there will likely be an onslaught of new litigation involving Solar City that will join the now 700+ outstanding lawsuits Tesla is currently litigating.

Tulsi Gabbard is on the verge of being excluded from the next Democratic presidential debate on the basis of criteria that appear increasingly absurd…

Take, for instance, her poll standing in New Hampshire, which currently places Gabbard at 3.3% support, according to the RealClearPolitics average as of Aug. 20. One might suspect that such a figure would merit inclusion in the upcoming debates — especially considering she’s ahead of several candidates who have already been granted entry, including Cory Booker, Amy Klobuchar, Beto O’Rourke, and Andrew Yang.

But the Democratic National Committee has decreed that the polls constituting this average are not sufficiently “qualifying.”

What makes a poll “qualifying” in the eyes of the DNC?The answer is conspicuously inscrutable. Months ago, party chieftains issued a list of “approved sponsoring organizations/institutions” for polls that satisfy their criteria for debate admittance. Not appearing on that list is the Boston Globe, which sponsored a Suffolk University poll published Aug. 6 that placed Gabbard at 3%. The DNC had proclaimed that for admittance to the September and October debates, candidates must secure polling results of 2% or more in four separate “approved” polls — but a poll sponsored by the newspaper with the largest circulation in New Hampshire (the Globe recently surpassed the New Hampshire Union Leader there) does not count, per this cockamamie criteria. There has not been an officially qualifying poll in New Hampshire, Gabbard’s best state, in over a month.

The absurdity mounts.

A South Carolina poll published Aug. 14 by the Post and Courier placed Gabbard at 2%. One might have again vainly assumed that the newspaper with the largest circulation in a critical early primary state would be an “approved” sponsor per the dictates of the DNC, but it is not. Curious.

To recap:

Gabbard has polled at 2% or more in two polls sponsored by the two largest newspapers in two early primary states, but the DNC — through its mysteriously incoherent selection process — has determined that these surveys do not count toward her debate eligibility. Without these exclusions, Gabbard would have already qualified. She has polled at 2% or more in two polls officially deemed “qualifying,” and surpassed the 130,000 donor threshold on Aug. 2. While the latter metric would seem more indicative of “grassroots support” — a formerly obscure Hawaii congresswoman has managed to secure more than 160,000 individual contributions from all 50 states, according to the latest figures from her campaign — the DNC has declared that it will prioritize polling over donors. In polls with a sample size of just a few hundred people, this means excluding candidates based on what can literally amount to rounding errors: A poll that places a candidate at 1.4% could be considered non-qualifying, but a poll that places a candidate at 1.5% is considered qualifying. Pinning such massive decisions for the trajectory of a campaign on insignificant fractional differences seems wildly arbitrary.

Take also Gabbard’s performance in polls conducted by YouGov. One such poll published July 21, sponsored by CBS, placed Gabbard at 2% in New Hampshire and therefore counts toward her qualifying total. But Gabbard has polled at 2% or more in five additional YouGov polls — except those polls are sponsored by The Economist, not CBS. Needless to say, The Economist is not a “sponsoring organization,” per the whims of the DNC. It may be one of the most vaunted news organizations in the world, and YouGov may be a “qualified” polling firm in other contexts, but the DNC has chosen to exclude The Economist’s results for reasons that appear less and less defensible.

Then there’s the larger issue of how exactly the DNC is gauging grassroots enthusiasm, which was ostensibly supposed to be the principle governing the debate-qualifying process in the first place. Gabbard was the most Googled candidate twice in a row after each previous debate, which at a minimum should indicate that there is substantial interest in her campaign. It’s an imperfect metric — Google searches and other online criteria could be subject to manipulation — but then again, the other metrics are also noticeably imperfect. There is no reason why the DNC could not incorporate a range of factors in determining which candidates voters are entitled to hear from on a national stage. For what it’s worth, she also tends to generate anomalously large interest on YouTube and social media, having gained the second-most Twitter followers of any candidate after the most recent debate in July. Again, these are imperfect metrics, but the entire debate-qualifying process is based on imperfect metrics.

Gabbard has a unique foreign-policy-centric message that is distinct from every other candidate, and she has managed to convert a shoestring campaign operation into a sizable public profile. (She is currently in Indonesia on a two-week National Guard training mission, therefore missing a crucial juncture of the campaign.) Other candidates poised for exclusion might also have a reasonable claim to entry — Marianne Williamson passed the 130,000 donor threshold this week — but the most egregious case is clearly Gabbard.

If only out of self-interest, the DNC might want to ponder whether alienating her supporters is a tactically wise move, considering how deeply suspicious many already are of the DNC’s behind-the-scenes role — memories of a “rigged” primary in 2016 are still fresh.

In its December 2018 “framework” for the debates, the DNC declared: “Given the fluid nature of the presidential nominating process, the DNC will continuously assess the state of the race and make adjustments to this process as appropriate.”

Now would likely be an “appropriate” time for such a reassessment.

via ZeroHedge News https://ift.tt/325hS0H Tyler Durden

Larry Sloven has been building supply chains in Asia for the better part of his 30-year career. But in that entire time, he never encountered anything quite so challenging as the US-China trade war, and the adaptations that it forced his company – Capstone International, an HK-based subsidiary of Capstone Companies.

Sloven, the president of Capstone, said he primarily focuses on building supply chains in Southeast Asia. Sloven, who is 70, has spent half of his life connecting factories, sourcing raw materials, and dealing with logistics, mostly in Southern China. But now, with his Big Box store clients demanding supply chain reshuffles at the drop of a hat, Sloven explained how “[i]t is the hardest thing I’ve ever had to do in all my 30 years in the business.”

It was still early days when Sloven started looking at Thailand and other countries in the region to shift some assembly and sourcing of raw materials in early 2018. But a year passed swiftly, and by the spring of 2019, with trade talks seemingly stalled, Sloven, who grew up on Long Island, felt confident that he was prepared for anything.

Initially, the tariffs didn’t have much of an impact on the cost basis for Sloven’s supply chains. But as the summer of 2019 dragged on, and it became clear that the trade war wouldn’t be ending any time soon, Sloven started taking additional precautions, setting up back-up plans “just in case.”

After settling on a few factories in Thailand to handle assembly for new products, including a smart mirror that was still in development, Sloven started preparing ‘test runs’ to make sure the factories could ramp up production within a six-month timeframe.

He scheduled a series of pilot runs to test how well the Thai factory handled assembly. He also needed to prepare for audits of labor rights and environmental standards that U.S. retailers require.

He estimated that would take at least another six months.

“I’m going to start moving on a small scale because they’re not going to be able to just do it immediately,” Sloven said. “As much as they say, ‘Oh, I can do this right now’ – I’m not taking that chance.”

More investment in tooling and moulds was required, too, but the Thai companies agreed to bear the cost.

Regardless of what happened with the trade war, Sloven felt covered.

“You prepare for war,” he said. “You’re ready if you’re attacked.”

For its story, Reuters closely monitored Sloven and his business over the course of a year – a year that saw the trade war escalate in ways the financial press hadn’t anticipated.

As Sloven started breaking down the process of setting up new supply chains into smaller tasks, he quickly discovered that convincing some of the manufacturers in southern China with whom Sloven worked remained convinced that a trade deal would be struck, or at least that’s what they said.

For whatever reason, they refused to negotiate deals that would involving shipping more production and raw materials abroad.

With the help of his go-to trade attorney, Sloven eventually succeeded, but it took a lot of work.

Sloven also had work to do in China.

His suppliers in Shenzhen, Dongguan and Guangzhou were certain the trade conflict would blow over and were reluctant to negotiate deals that would send components and raw materials abroad for assembly.

But Sloven kept pressing ahead with the Thailand plan, concerned about the toll the trade war was taking in China.

In early April, Sloven invited Reuters to meet his trade lawyer, Sally Peng of Sandler, Travis & Rosenberg.

Peng described how Chinese factory floors were emptying out as workers were laid off. Few owners had the expertise or resources to automate or find new export markets, so most were riding it out, hoping for a trade deal. They were “losing money every day,” she said.

“They believe that eventually it will all come back,” Sloven said.

“I think within five years, it will all be gone,” Peng replied.

But by the time Capstone reported its 2018 results, the seriousness of the company’s situation had become readily apparent. Capstone’s CFO described the trade war as one of the greatest challenges the company had ever faced.

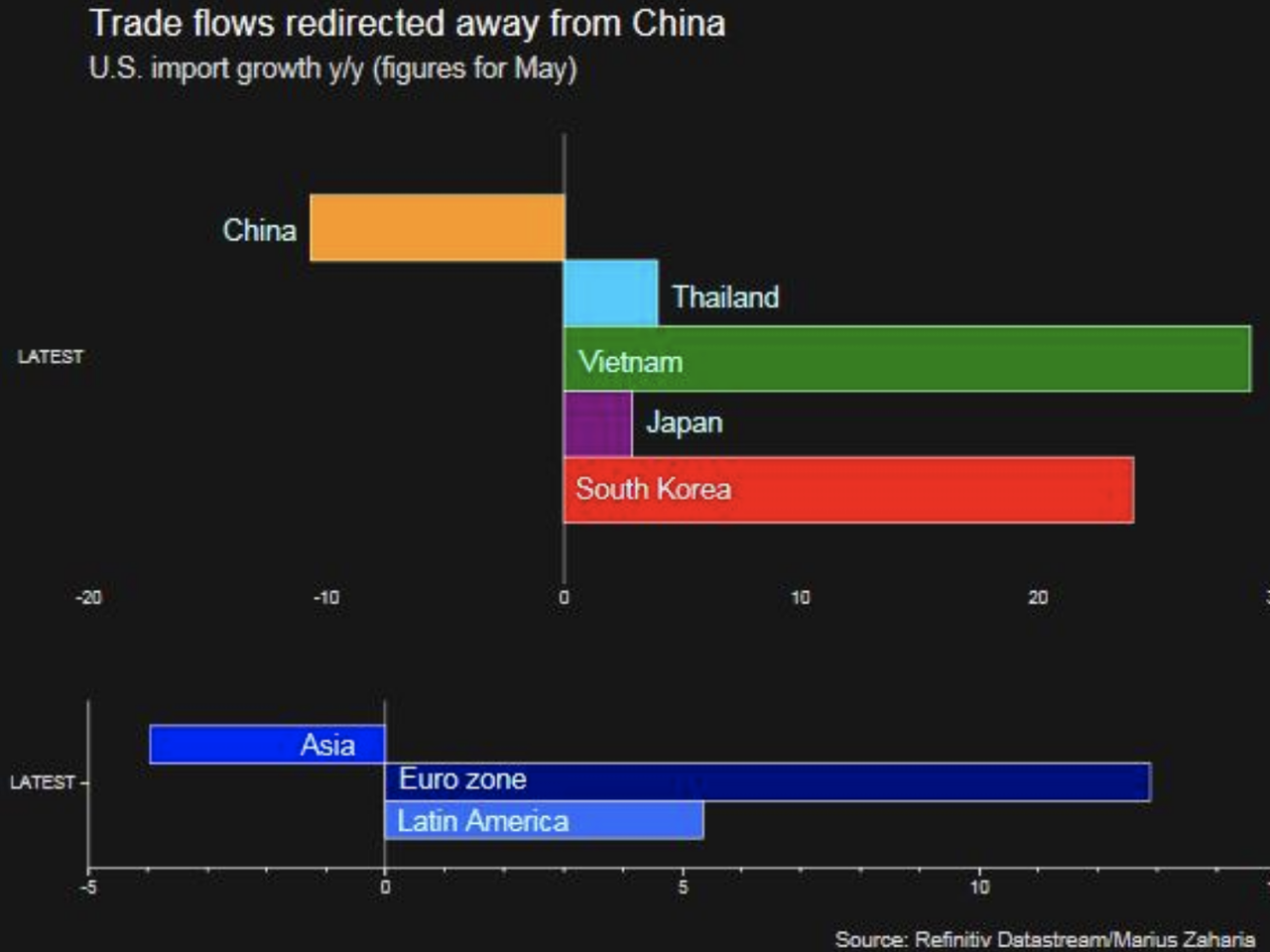

Then Trump hiked tariffs again in May, and everybody went nuts. One survey showed that the number of firms planning to move at least some production outside of China had climbed above 40%. Meanwhile, the Asian press kept up a steady patter of reports about company’s plans (most notably, companies that build components for Apple’s many products). Regular readers of ZH should be familiar with these.

It soon became apparent which regional rivals would benefit the most from Trump’s aggressive protectionism, and which might falter.

The same day Sloven met his lawyer, his bosses in Florida announced 2018 results that reflected the effects of the trade war. Net revenues came in at $12.8 million, down from $36.8 million in 2017. Net losses were $1 million, a swing from a $3.1 million profit.

“Capstone faced challenges in 2018 unlike any in its history,” chief financial officer Gerry McClinton said.

Meanwhile, development of the smart mirror was in full swing. The prototype was deemed a success at a Las Vegas electronics show in January, and a PR agency and a marketing company were hired to advertise the new product.

Then Trump hiked tariffs to 25% on May 10.

For Sloven – and many others – the urgency level bounced back up. That month, a survey by AmCham China and AmCham Shanghai showed the number of firms that had moved production or were considering doing so leaped above 40%.