Emerging market investors appear to be the most sensitive canaries in the global investing coalmine as they abandon ‘high growth’ opportunities in favor of safe-havens, sending broad-based emerging market currencies to record lows…

JPMorgan’s Emerging Market FX index just hit a new record low…

Source: Bloomberg

The various “pesos” are leading the most recent collapse…

Source: Bloomberg

Today sees new record lows for the Colombian Peso…

Source: Bloomberg

And fears that Argentine net foreign currency reserves are in a more dire situation than many people assume from looking at the gross figure, sent the peso plummeting back towards record lows…

“We think that the gross FX reserve figure overstates the BCRA’s ability to prop up the peso,” economist Edward Glossop writes in a note.

Capital Economics estimates the BCRA’s net FX reserves have fallen from $30 billion in mid-April to just $19 billion now

Source: Bloomberg

Where investors have stayed local, they have dramatically shifted to investment grade EM debt and away from high yield EM debt:

Source: Bloomberg

“Credit quality will matter, and I strongly prefer investment grade over high yield in emerging-market debt,” said Sergey Dergachev, senior portfolio manager at Union Investment in Frankfurt, who favors Indonesia, India, Egypt and Croatia. “I definitely see more volatility to come.”

But it seems the flood of capital is flowing from EM FX into dollars and from there into US Treasuries, as the long-end of the curve hits new record low yields.

In developing nations, “the balance of risks are skewed to the downside in the near-term,” said Patrick Wacker, a fund manager for emerging-market fixed income at UOB Asset Management Ltd. in Singapore.

via ZeroHedge News https://ift.tt/2L40rIx Tyler Durden

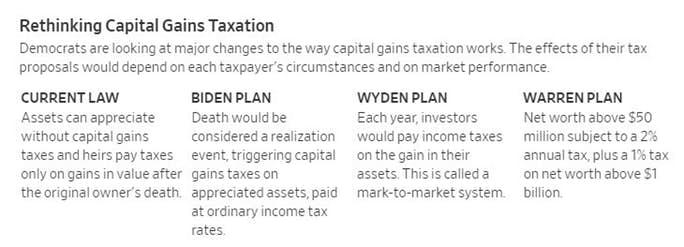

Former Vice President Joe Biden, the candidate most prominently picking up where Mr. Obama left off, has proposed repealing stepped-up basis. Taxing unrealized gains at death could let Congress raise the capital gains rate to 50% before revenue from it would start to drop, according to the Tax Policy Center, because investors would no longer delay sales in hopes of a zero tax bill when they die.

And indeed, Mr. Biden has proposed doubling the income-tax rate to 40% on capital gains for taxpayers with incomes of $1 million or more.

But for Democrats, repealing stepped-up basis has drawbacks. Much of the money wouldn’t come in for years, until people died. The Treasury Department estimated a plan Mr. Obama put out in 2016 would generate $235 billion over a decade, less than 10% of what advisers to Sen. Warren’s campaign say her tax plan would raise.

That lag raises another risk. Wealthy taxpayers would have incentives to get Congress to reverse the tax before their heirs face it.

Wyden Plan

Instead of attacking favorable treatment of inherited assets, Mr. Wyden goes after the other main principle of capital-gains taxation—that gains must be realized before taxes are imposed.

The Oregon senator is designing a “mark-to-market” system. Annual increases in the value of people’s assets would be taxed as income, even if the assets aren’t sold. Someone who owned stock that was worth $400 million on Jan. 1 but $500 million on Dec. 31 would add $100 million to income on his or her tax return.

For the government, money would start flowing in immediately. The tax would hit every year, not just when an asset-holder died. Mr. Wyden would apply this regime to just the top 0.3% of taxpayers, said spokeswoman Ashley Schapitl.

There are serious challenges. Revenue could be volatile as markets rise and fall. Also, the IRS would determine asset increases annually, requiring baseline values and ways to measure change. That’s easy for stocks and bonds but far more complicated for private businesses or artwork.

The rules would have to address how to treat assets that lose instead of gain value in a year, and how taxpayers would raise cash to pay taxes on assets they didn’t sell. Under Mr. Castro’s proposal, losses could be used to offset other taxes or carried forward to future years.

Warren Plan

The most ambitious plan comes from Sen. Warren of Massachusetts, whose annual wealth tax would fund spending proposals such as universal child care and student-loan forgiveness.

The ultra-rich would pay whether they make money or not, whether they sell assets or not and whether their assets are growing or shrinking.

Ms. Warren, who draws cheers at campaign events when she mentions the tax, would impose a 2% tax each year on individuals’ assets above $50 million and a further 1% on assets above $1 billion. Fellow candidate Beto O’Rourke has also backed a wealth tax, and it is one of Vermont Sen. Bernie Sanders ’ options for financing Medicare-for-All.

Won’t Stop There

Expect more and more radical ideas to pay for nonsense like the “Green New Deal”, an idea that will cost an estimated $51 to $93 trillion.

Elizabeth Warren backs the Green New Deal so she is the most desperate to raise the most money the fastest.

They claim this a tax only on the wealthiest citizens. It won’t stop there. It never does.

via ZeroHedge News https://ift.tt/32dFd0C Tyler Durden

A strange series of blasts at Gaza police checkpoints that rocked Gaza City Tuesday evening has resulted in a rare admission by the Hamas-run Palestinian territory’s health ministry that a prior statement blaming Israel for the new attacks was inaccurate. It now says Islamic State cells active in the strip are responsible.

On Wednesday morning Hamas declared a ‘state of emergency’ amid a crackdown on both Islamic State supporters and renegade Salafist organizations after at least three Gazan police officers were reported killed in twin suicide explosions on separate checkpoints after motorcycles detonated at the sites. A handful of others were wounded in the attacks from the rival Islamist outlawed group.

ISIS in Sinai previously threatened to overthrow “apostate” Hamas leaders in Gaza. Image via AMN news.

Currently “mass arrests” are underway according to local reports, yet Hamas officials are calling for calm while describing the attacks as an isolated incident.

An Interior Ministry spokesman described that, “Mobilization of all police and security forces has been declared to follow-up on security developments in the aftermath of the two explosions.”

This comes at a moment of continued heightened tensions between Hamas and Israel after last May hundreds of rockets were launched from Gaza into Israel, with corresponding IDF retaliatory strikes, and as deadly incidents involving Palestinian clashes with Israeli security forces along the border increased.

Starting in 2018 the Islamic State’s so-called “Sinai branch” declared war on Hamas, describing the Palestinian militant organization as “apostates”.

And now with a state of emergency declared, we could be witnessing the start of a low-grade civil war in Gaza as Hamas roots out more rival extremist elements.

via ZeroHedge News https://ift.tt/3269UEA Tyler Durden

In the July 31 Democratic presidential debate, former Vice President Joe Biden gave this reponse to a question about whether he would continue to support the production of domestic coal, oil and natural gas resources: “No. We would work it out. We would make sure it’s eliminated, and no more subsidies for either one of those, period.” Note the word “eliminated.” Not limited, not regulated, not discouraged – eliminated.

In a speech on August 22, fellow candidate Bernie Sanders had this to say: “Fossil fuel executives should be criminally prosecuted for the destruction they have knowingly caused.” Sanders could have said those executives “should” be prosecuted. He could have said they “might” be prosecuted. Instead, reading from a pre-written script, he said they “should” be prosecuted. And not in a civil case, mind you, but “criminally” prosecuted.

These two blanket, pointed, unqualified statements by the two leading candidates for the 2020 Democratic presidential nomination raise the specter of an all-out war on the oil and gas industry during the next Democratic presidential administration, regardless of who that Democrat happens to be. This is especially true since every other candidate for the nomination has issued similar statements of hostility directed at fossil fuels.

Given the party’s near-unanimous adoption of various climate change plans based off of the “Green New Deal” proposed by Alexandria Ocasio Cortez, this really should come as no surprise to those who pay close attention to national politics.

But you can bet many industry executives, most of whom don’t pay close attention to national politics but pay employees whose job it is to do so, were somewhat taken aback by the Biden and Sanders statements. This would be especially true since industry executives as a class overwhelmingly supported Hillary Clinton in the 2016 race based largely on the advice given to them by those employees.

The fact that neither Biden nor Sanders has made any effort to walk their comments back as of this writing raises a legitimate question about which party’s candidate these executives will support with hundreds of thousands of their personal dollars next year. In 2016, most were glad to support the Democrat nominee for a variety of reasons: Many did not approve of candidate Trump’s personal behavior in the past and present; many didn’t like his Tweets, a Trump practice that has only become amplified with time; and pretty much none of them believed Trump had any chance of winning, in part because that was what they were being advised by those employees they paid to pay attention to such things.

Luckily for them and their companies, President Trump didn’t hold a grudge. The Trump plan for “Energy Dominance” was and has continued to be a key centerpiece of his economic and international policy agenda, an agenda that he has aggressively implemented. Through a series of executive orders and regulatory actions too numerous to detail here, the Trump Administration done much to enable the ongoing domestic oil and natural gas boom, despite the industry’s failure to support his 2016 campaign in any meaningful way.

Now comes the 2020 campaign and another choice:

Will these executives throw their support to the incumbent who has done so much to stimulate their industry even though they disapprove of his personality and tweets?

Or will they once again pour large parts of their personal fortunes into the campaign of the nominee of a political party that seems to be hell-bent on putting their companies out of business?

An equally interesting question is what will the government affairs employees advise them to do this time around? From a logical standpoint, this would not seem to be a very difficult choice.

But hey, when has logic ever been determinative in the world of U.S. politics?

via ZeroHedge News https://ift.tt/2Ua27mH Tyler Durden

After more than a week of increasingly fraught negotiations that nearly blossomed into a full-blown political crisis, the Five Star Movement (M5S) and the Democratic Party (PD) have reportedly struck a deal to form a new coalition government with Giuseppe Conte as prime minister, according to Italian newswire ANSA.

Earlier this month, League leader Matteo Salvini tried to dissolve the government by withdrawing his support for the coalition in an effort to try and call for new elections. However, he was thwarted when his former coalition partner, M5S leader Luigi di Maio, and his party engaged in negotiations with the centrist Democratic Party. On Wednesday night, the two parties finally reached an agreement to form a new coalition, with Conte – who had quit the government last week – returning to reprise his role as prime minister.

Salvini’s hope was that the country would hold new elections in which he would likely be named prime minister, at the head of a hard-right coalition.

The coalition will now be tasked with the responsibility for leading Italy through what’s expected to be difficult budget negotiations with the EU.

Meanwhile, the Telegraph reports that the League, Salvini’s party, is furious, pointing out that his party wont 34% of the national vote in May’s European parliament elections, and that it was polling as high as 39% as recently as earlier this month. Salvini affirmed that he would stay on as Interior Minister and Deputy PM in the lame duck government – members of his party urged supporters to take to the streets to protest the party. Salvini held back from calling for his people to march in the streets, saying he was “not interest” in “popular insurrections.” “Those happened back in 1848,” he quipped.

“Let’s hope that if a Democratic Party-Five Star government is formed, the people will rise up as soon as possible,” said Alessandra Locatelli, a League minister.

“They’re stealing the government by preventing Italians from going to a vote,” she said.

Salvini was similarly critical.

“A government made up of Five Star and the Democrats will not correspond to the sentiment of the people,” Salvini said. “If you make deals that are against nature, in the end the people will kick you out. Sooner or later, the judgement of the people will be heard.”

Since the new coalition has been formed, Italy will manage to avoid heading to new elections in the fall. Italian President Sergio Mattarella gave the coalition the mandate to former the new government.

via ZeroHedge News https://ift.tt/2Pn2USq Tyler Durden

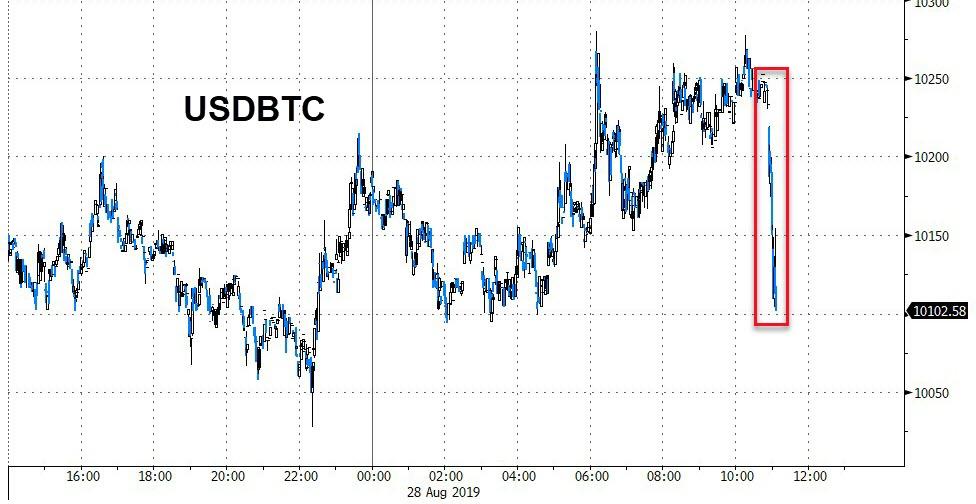

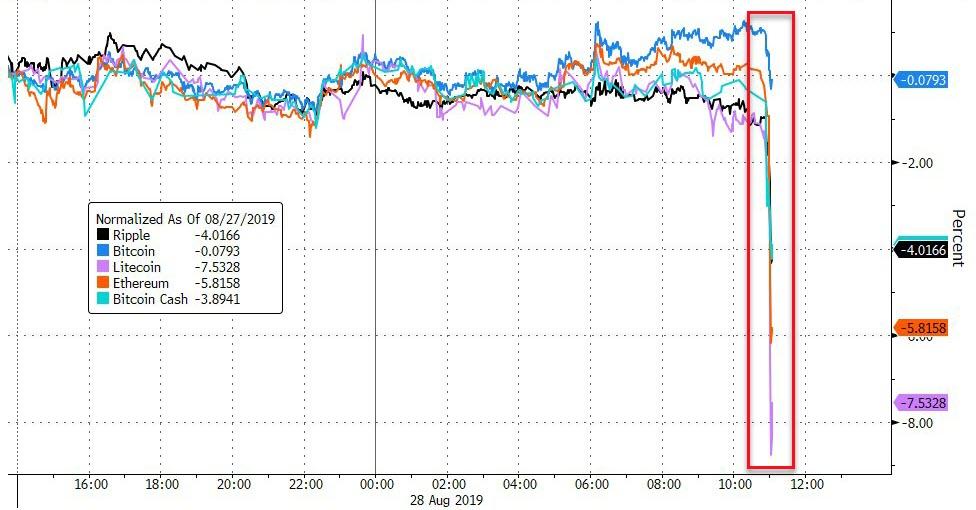

But it is the rest of the crypto-space that is really getting hit hard…

Source: Bloomberg

Interestingly this sudden plunge occurs as CoinTelegraph reports that the pro-democracy, anti-government protest movement in Hong Kong is spurring wider adoption of cryptocurrencies such as Bitcoin.

Yahoo! Finance reported on Aug. 28 that the political upheaval in the city — which has now entered its 12th week — is prompting several local businesses and individuals to switch to using non-sovereign and decentralized digital currencies.

Apolitical, borderless money for the pro-democracy movement

On Aug. 26, Hong Kong department store Pricerite announced it would begin accepting Bitcoin, Litecoin (LTC) and Ether (ETH) at its fourteen locations in Hong Kong.

Yahoo Finance! notes that the store has indicated it will be able to swiftly convert the crypto into Hong Kong dollars using the Bitcoin network’s scalability layer, Lightning Network.

Alongside traditional retailers, cryptocurrency firm Genesis Block has been operating 14 crypto ATMs across the city.

In July, Genesis Block — which trades under the name “CoinHere” — distributed water to protestors that had been paid for using international donations in Bitcoin Cash (BCH), as well as umbrellas — a symbolic reference to the city’s 2014 Umbrella Revolution.

The surge in interest in cryptocurrencies comes against a backdrop of other forms of economic activism. Earlier this month, protestors initiated an action to withdraw as much money as possible from their bank accounts, or convert their local currency into US dollars.

This had a twofold purpose, serving both as preemptive protection of their personal assets and sending a sharp warning to Chinese authorities.

As early as June, moreover, it was reported that a numver of Hong Kong’s tycoons — a city which counts 853 individuals worth more than $100 million — had begun to move their wealth offshore.

Bitcoin trades at a premium in Hong Kong

Should the protest movement fail to prevent China’s controversial extradition bill from becoming law, mainland Chinese authorities will have the right to demand that Hong Kong courts freeze and confiscate assets related to crimes perpetrated on the mainland.

Bitcoin trading volumes in Hong Kong soared in June amidst the turmoil, and the coin continues to trade locally at a several hundred dollar premium on peer-to-peer exchange LocalBitcoins.

* * *

One can’t help but wonder what Chinese authorities will do to prevent Honkers citizens from getting their cash out of dodge.

via ZeroHedge News https://ift.tt/2LkilFU Tyler Durden

President Trump has made it less and less a secret that he is pushing for new talks with Iran to “negotiate a better deal” after previously pulling out of the JCPOA. He and French President Emmanuel Macron at the close of the G7 on Monday actually spoke as if a potential meeting with Iran’s President Hassan Rouhani would be “soon” in the works.

Though The Washington Post hours after those statements cited a source saying Rouhani was “open” to such renewed talks, Tehran hours later poured cold water over the prospect by saying its ballistic missile program is “non-negotiable” and that face-to-face talks are conditioned on the White House biding by its prior commitments under the 2015 nuclear deal; however, Iranian officials were said to have reacted positively to Macron’s idea of a $15BN credit line should Iran refrain from breaching uranium enrichment caps under the prior terms of the JCPOA.

Now with media speculation rampant that Rouhani and Trump might sit down at the same table, both Israel and Saudi Arabia are reportedly stepping up efforts to preempt such a dialogue.

Trump said at the close of the G7 summit in France that he doesn’t want regime change and is “open” to meeting with Iran’s Rouhani, via LA Times.

Israeli press and officials are expressing extreme concern, per a recent Haaretz article:

The fears in Israel, which for now are only being expressed in completely off-the-record conversations, are that Trump, eager to make his mark on world affairs and prove he can achieve a better deal than his predecessor, will find himself in a room with negotiators much wilier and more knowledgeable on the issues than he is. Convinced that he is the grand master of the art of the deal, Trump could swiftly come to an agreement with the Iranians that may sound preferable to him, but in reality will be much worse.

Israel’s intelligence and defense community are said to be strongly lobbying against such a renewed Trump engagement with Tehran after the president told reporters there’s “a really good chance” the meeting would happen.

It’s not the first time the White House has hesitantly invited Iran to the table following a summer of escalating “tanker wars” and boiling point tensions in the Persian Gulf, and amid a US military build-up in the region.

It was recently revealed that last month Iran’s Foreign Minister Javad Zarif had rebuffed a secret invitation to meet with President Trump in the oval office, which involved the mediation of Rand Paul. Just days following this, the US Treasury announced unprecedented sanctions against the Iranian top diplomat.

NEW: Pres. Trump says he would meet with Iranian Pres. Rouhani “if the circumstances were correct.”

Currently, the Saudis are also jumping into the fray increasingly as Israel’s unlikely junior lobbying partner on all things “countering Iran”.

It’s been no secret that Riyadh and Tel Aviv, despite never having official diplomatic relations, have developed an intelligence sharing relationship as a result of the common cause to oust Assad in the years-long Syrian proxy war.

This week Riyadh dispatched Deputy Defense Minister Khalid bin Salman – the younger brother of Saudi Crown Prince Mohammed bin Salman – to Washington to specifically express “common concerns” over Iran. Khalid is scheduled to meet with Secretary of State Mike Pompeo Wednesday afternoon where he’s expected to argue against any US engagement with Rouhani.

Deputy Defense Minister Khalid bin Salman and younger brother of MbS, via Saudi embassy in the US.

Given that by all appearances the Saudis and Israelis are doing everything in their power to stymie direct US-Iran talks, the fact that Israel just conducted airstrikes on multiple Arab countries within 24 hours over the weekend in a dramatic escalation is deeply significant, given the curious timing for such brazen aggression.

Could it have been a desperate Netanyahu bid to ensure tensions with Iran and its proxies remain as high and “on the brink” as possible?

If the attacks – one of which was on a Hezbollah site in Beirut for the first time since 2006 – was toward telegraphing and provoking an Iranian response, Israel can then present the case to Washington that Iran is “on the offensive” and therefore cannot be engaged diplomatically.

via ZeroHedge News https://ift.tt/2Zy3j4i Tyler Durden

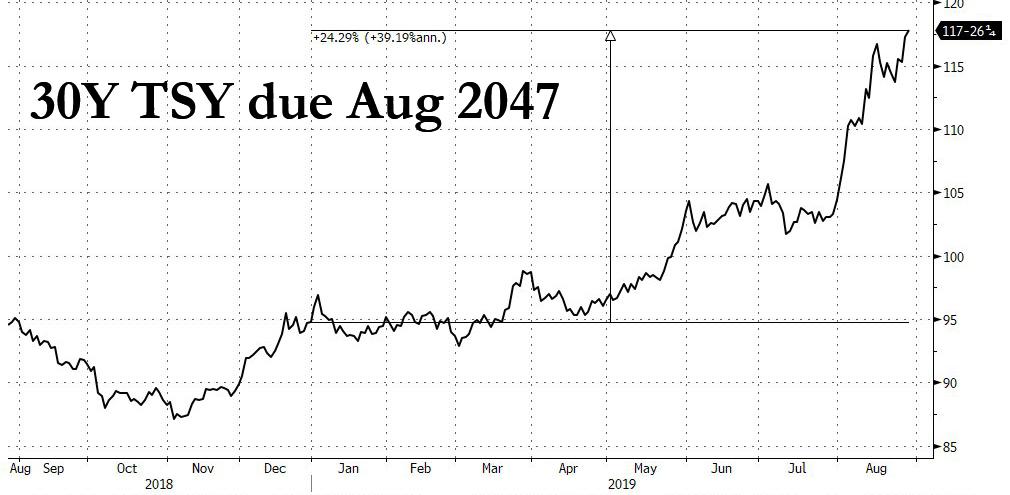

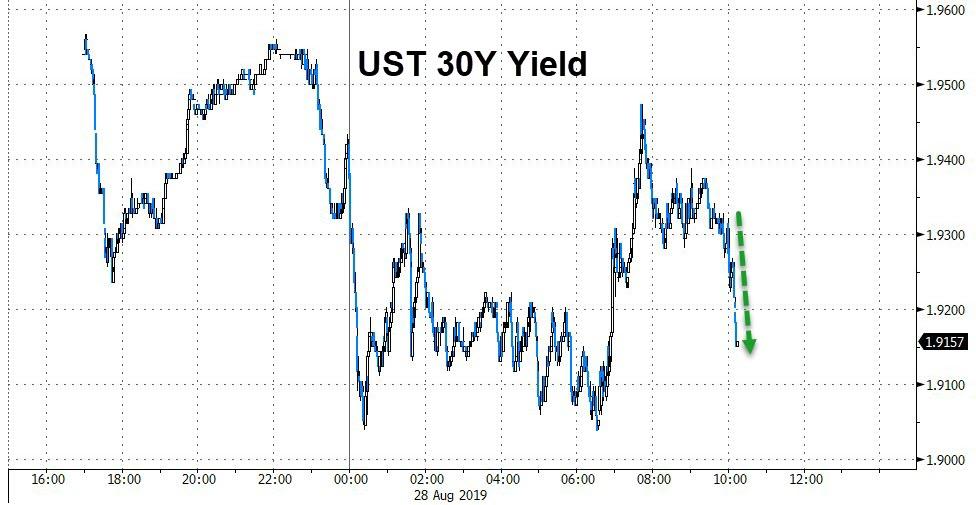

While most US traders were deep in REM sleep, at precisely 3:30am ET, we noted yet another historic moment for the US yield curve: the yield on the 30Y Treasury dropped to an all time low.

U.S. 30-YEAR BOND YIELD FALLS TO NEW RECORD LOW OF 1.90%

And indeed, as BMO’s rates strategy duo of Ian Lyngen and Jon Hill notes, an extension of the grinding bid for duration was the primary development during the overnight session and it was one which has brought 30-year yields to new record lows.

With 1.907% now representing the lowest rate ever for the long bond, we remain biased for a break even lower as the final week of August continues to unfold. Similarly, the local low in 10s at 1.444% is likely to be challenged given the bullish backdrop that remains well in place for Treasuries.

This, as BMO notes, bodes well for an ongoing flattening of the yield curve, which was further observed after today’s very strong 5Y auction.

But back to the outperformance of the long bond, which as Lyngen points out “has been remarkable on a number of levels and the overnight move adds even more to the bullishness.” Additionally, as has been the case for much of the past month, the strong bid emerged in Asia – as Japanese and Taiwan lifers rushed to bid up the paper – and was then extended in London, suggesting a variety of pockets of demand for 30-year Treasury yields below 2.0%.

And here an important aside: as the BMO analysts point out, the 30s are now yielding less than the S&P500’s dividend yield of 1.98% – for first time since 2009 and represents “yet another potential recessionary indicator, as if more were needed to stoke concerns of a meaningful slowdown.”

And while the move in yield may not sound like much, as a result of the convexity of the ultra long-dated paper and the massive duration, the move means that a typical 30Y bond has now returned 25% in cash terms YTD, making it one of the best performing assets in the world.

Returning to the most recent leg, BMO notes that “the bid has been accompanied by a constructive cross in stochastics which indicates there remains ample room to press the move. In addition, with overnight volumes at 1.4x the norms and an impressive 8% marketshare for 30s, we’ll suggest a 1-handle is more sustainable than a late-summer’s bounce might imply.”

So does the Canadian bank think that more gains are on deck? You bet. First, it’s the fact that the rally took place without any actual catalyst:

We’re certainly cognizant that today’s absolute dearth of economic data doesn’t offer much in the way of incremental trading direction; this is in part supportive of our logic for an extension of the flattening bid for Treasuries. Call it the path of least resistance and a world of yield inertia.

Then, there are the seasonals:

Given the relevance of the constructive seasonals thus far this summer, we’re content to anticipate the rally continues as the real challenge to this historical pattern doesn’t materialize until late-September when higher yields become the norm.

Also notable, the month-end moves, which were expected to be bond bearish, did not materialize; quite the contrary:

Let us not forget the month-end considerations; after all August did see new 10s and 30s and despite the Fed’s return to outright purchases in the Treasury market there are plenty of natural buyers needing to simply stay neutral to the benchmark.

Meanwhile, growing geopolitical concerns will only make the flight to safety more acute (even as stocks inexplicably ramp higher on what appears to be pension month end rebalancing and/or a last gasp of stock buybacks before the buyback blackout window closes):

The British question continues to plague the global economic outlook; to put it mildly. PM Johnson’s attempt have parliament prorogued (aka suspended, who knew?) from mid-Sept to mid-Oct has been seen as an overt effort to orchestrate a no-deal Brexit and was yet another reason to chase the flight-to-quality that has rebased all US rates well below 2.0% at this stage. With limited insight into the inner workings of the UK political machine; the October 31st deadline does point toward an entirely different character of our annual Día de Muertos celebration.

It’s not just Brexit: Italian politics, the trade war, a stumbling global economy, and the Fed’s ‘uncertainties’ all remain essential to the bullish underpinnings in the Treasury market, according to Lyngen/Hill.

And while the duo would like to assume there will be a resolution on one or all of these issues in the near- or medium-term, the trajectory evident in the current environment would suggest otherwise.

With this in mind, we remain very much in the buy-the-dip mode ahead of the looming month-end and suspect this proves prudent even as September gets underway.

But the biggest reason why yields are likely to keep drifting lower is that virtually all experts are either pressing their shorts, or convinced that any minute now will be the “right time to short”, which simply means that wave after wave of shorts will continue to get stopped out.

via ZeroHedge News https://ift.tt/2PjeP3J Tyler Durden

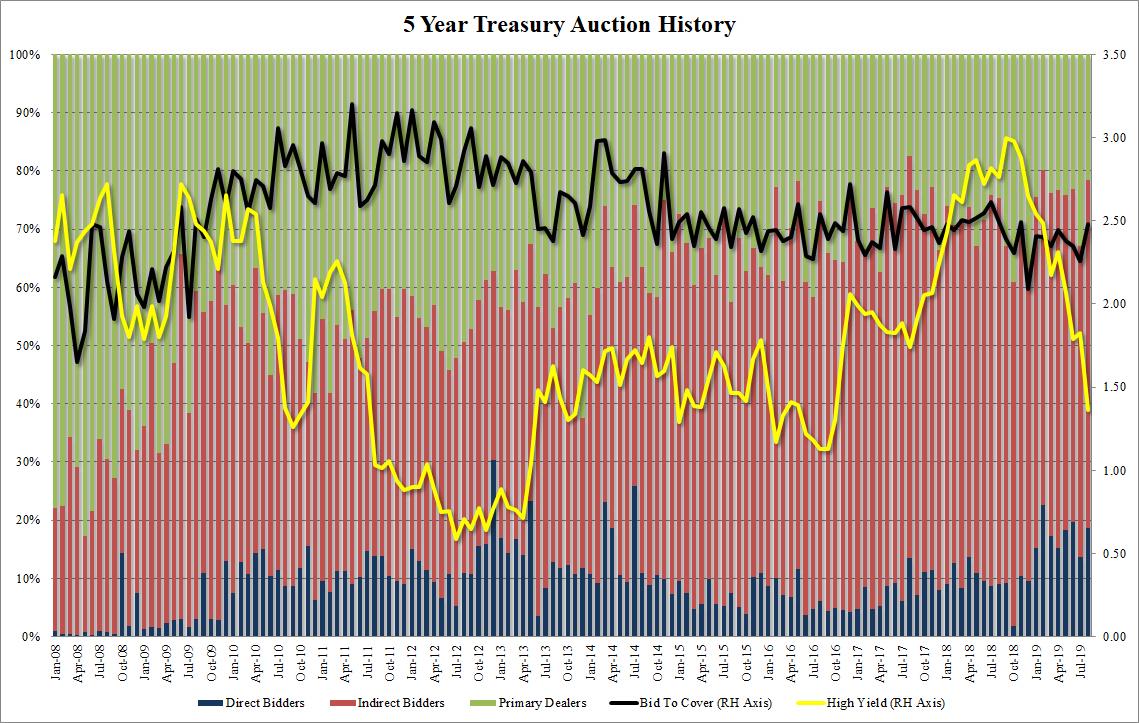

One day after the US sold 2Y Treasurys at a yield that was higher than the market yield on 10Y paper, i.e., the 2s10s yield curve inverted, for the first time since the financial crisis, the Treasury sold $41 billion in 5 Year paper, and if yesterday’s 2Y auction was a small tail, today’s 5Y auction was remarkably strong because despite the lowest yield since October 2016, at 1.365%, the demand was so acute the auction stopped 1 basis point through the When Issued of 1.375%.

The strong metric continued with the bid to cover, which rebounded from 2.26 to 2.48, the highest since August 2018, and well above the 6 auction average of 2.36. Meanwhile, the internals were sterling as well, with Indirects taking down 59.7%, a jump from last month’s 53.4%, the highest since April and above the recent average of 57.7%, leaving Directs with 18.7%, above the 17.8% six auction average, and finally Dealers left holding just 21.6%, the lowest since February.

Overall, a very strong auction, with the market surprised by just how impressive demand was, in turn sending 10Y yields sliding from 1.465% before the auction some 2bps lower after, to 1.446% after, with the 30Y enjoying a similar rally, and also hitting stocks which today are trading inversely to Tsys.

via ZeroHedge News https://ift.tt/32bi7aS Tyler Durden

{kind=link}

{kind=link}

{kind=link}