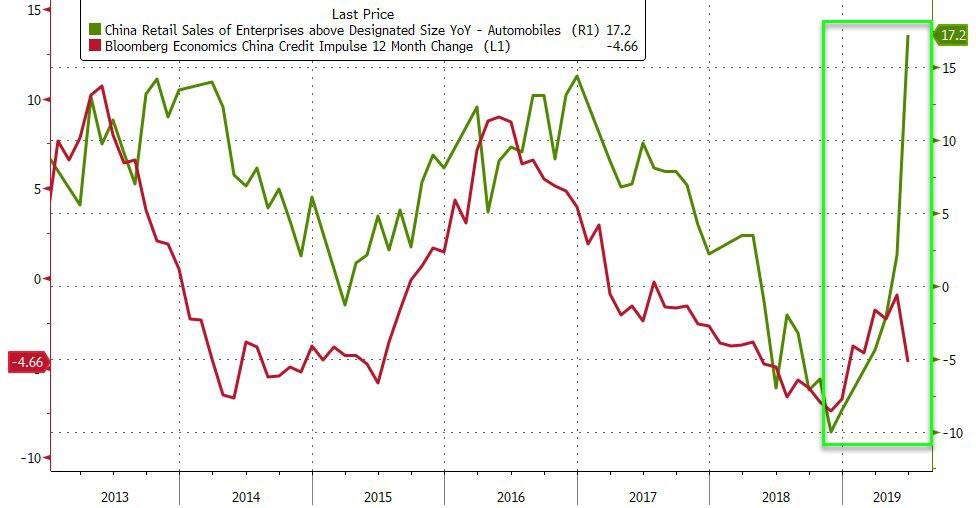

And, as we pointed out earlier this week, this month was no exception, when following China GDP’s dramatic slowing to just 6.2% YoY – the slowest since record began – there was a delightful surprise to appease those who are wondering whether record credit injections and more easing measures than during the financial crisis had any effect at all. To wit, China retail sales and industrial production rebounded handsomely with the former spiking 9.8% YoY – the most since March 2018.

There’s just one thing though – the entire surge in retail sales (and industrial production) seems to have been triggered by an almost unprecedented sudden surge in auto sales to – who else – the government itself, in the form large, state-owned enterprises. Think Cash for Clunkers on steroids – if the clunkers belonged to the Federal Government, and the new cars purchased were made by the Government.

Yet there was one critical data set in China’s manipulated economic data spreadsheet, which failed to get the royal goalseek treatment, one with dramatic implications for the broader market.

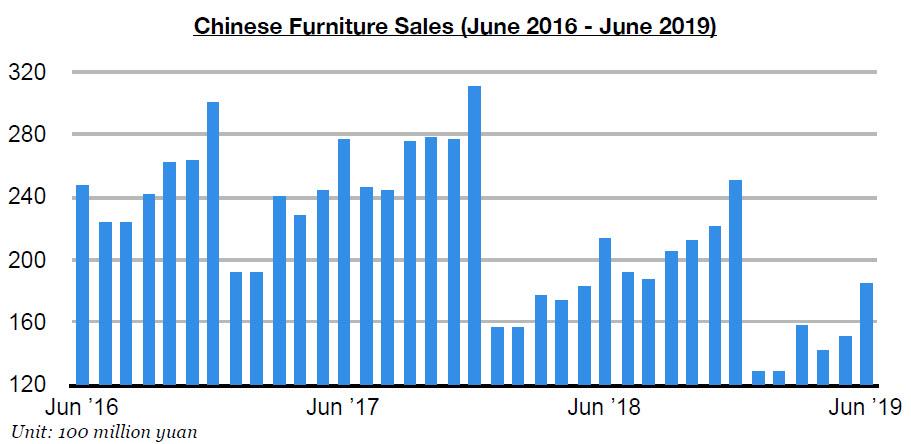

According to Commodore Research, Chinese June data showed that furniture sales in China totaled only 18.4 billion yuan last month. This marks a year-on-year decline of 14% from the 21.3 billion yuan in sales that was reported last year for June 2018’s furniture sales.

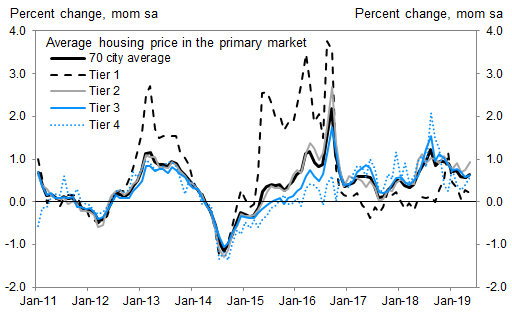

This is puzzling in light of the official Chinese data according to which the local housing market continues to hum along, firing on all cylinders, with the average, 70-city primary market property price rising 10.5% Y/Y in May.

Alas, that does not seem feasible when one considers that furniture sales in China have now contracted on a year-on-year basis for eighteen straight months.

What does this mean? As Commodore Research concludes, “we continue to believe that there is a good chance that the ongoing plummet in furniture sales in China is pointing to much greater weakness existing in the Chinese housing market than is generally being recognized.“

This could potentially be very bad news not only for China, but the entire world because as we explained all the way back in March 2017, “The Fate Of The World Economy Is In The Hands Of China’s Housing Bubble“, and if China’s biggest, and most resilient bubble has now indeed burst, the not only is Trump about to steamroll China in the trade war, but the resulting deflationary shock wave is about to send every bond around the world deep into sub-zero territory.

via ZeroHedge News https://ift.tt/2LtoWA1 Tyler Durden

When meeting some clients a few weeks ago in Amsterdam, I made my usual remark about the stupidity of running negative interest rates.

In response my host told me a sobering story.

He manages a pension fund and had recently started to build large cash positions. One day he was called by a pension regulator at the central bank and reminded of a rule that says funds should not hold too much cash because it’s risky; they should instead buy more long-dated bonds.

His retort was that most eurozone long bonds had negative yields and so he was sure to lose money.

“It doesn’t matter,” came the regulator’s reply: “A rule is a rule, and you must apply it.”

Thus, to “reduce” risk the manager had to buy assets that were 100% sure to lose the pensioners money.

A long time ago, I taught accounting and have always been fascinated by the brilliance of double entry accounting systems.

This approach got me thinking where those losses would be booked in the case of pension funds, insurance companies and banks? And what would be the long term effects?

To this end, consider the following example:

Back in May 2016, an institutional investor bought a five-year zero coupon bund at €103. Five years on, the bond will be repaid at €100, generating a loss of €3. How this loss appears will depend on the type of investor in question:

Pension fund. The €3 loss will reduce the market value of assets by €3. Holland also has a rule that pension funds must buy more government bonds the closer they get to being underfunded. Yet buying such negative-yielding bonds and keeping them to maturity ensures losses, making it more likely the fund will be underfunded, and so forced to buy more loss-making bonds (spot the feedback loop). Soon the fund will be distributing returns from capital, rather than returns on capital. Hence, it is not inflation that will destroy pension funds, but the mix of negative rates and rules that stop managers from deploying capital as they see fit. These protect governments, not pensioners who are forced to buy bad paper.

Bank. As a leveraged player, let’s assume it lends a fairly standard 12 times its capital. This capital has to be invested in “riskless” assets that are always liquid. In the old days, this would have been gold or central bank paper exchangeable into gold. Today, the government bond market plays the role of “riskless” (you have to laugh) asset, which has no reserve requirement. As a result, banks are loaded up with bonds issued by the local state. Now let us assume that a bank has just lost €3 on the zerocoupon bond mentioned above. The bank’s capital base will be reduced by €3. Based on the 12x banking multiplier, the bank will have to reduce its loans by a whopping €36 to keep its leverage ratio at 12. Hence, the effect of managing negative rates while also respecting bank capital adequacy rules means that the capital base can only shrink.

Insurance company. These institutions have two centers of profits. First is the core business of assuming risk on behalf of clients. Second, they manage premiums paid by the clients in a way that aims for a profit over the present value of the risks covered. A standard solution is to cover the maximum amount of risk with a government bond of similar duration to the client’s contract period, and then put the remainder into equities or real estate to help build up the firm’s capital base. This gets very difficult when government bonds offer negative yields. The insurance company could raise its premium by the amount of the expected loss from holding the bond (not very commercial), or it could just underwrite less business. Either way, it will have less money to invest in equities and real estate. Simply put, either the insurance company’s clients will pay the negative rates, or the company itself will do so by increasing its risks without raising returns. This means that either the client pays more for insurance, and so becomes less profitable, or the insurance company takes a hit to its bottom line.

The conclusion is that negative rates must eventually destroy the longterm savings industry run by pension funds, banks and insurance firms.

As Peter Bernstein showed in Against the Gods: The Remarkable Story of Risk, financial institutions can bet against the gods and win if they compute the odds intelligently. If those odds are 100% you lose, then betting is just stupid.

via ZeroHedge News https://ift.tt/2O5ds83 Tyler Durden

FaceApp, the popular application that has become a viral trend for showing what people would look like after they age 30 years, isn’t well known to be a Russia-based piece of software. Its even lesser known that the terms and conditions of the app grant it ‘perpetual, irrevocable’ rights to your content, according to a new report from Fox 29.

The app has skyrocketed in popularity over the last couple of weeks because it allows users to digitally alter their age. Many celebrities have even joined in and posted photographs of what their elder selves may look like. More than 1 million users have downloaded the app from Google and it is now the number one app in the Apple store.

But, what most users don’t know, is that the terms and conditions of the software “allow it to access to use, modify, adapt and publish any images that a user offers up in exchange for its free artificial intelligence service.”

This prompted Senate Minority leader Chuck Schumer to play the “Russia, Russia, Russia” card, sending a letter to the FBI and FTC requesting them to conduct an investigation into the app. He wrote that the app “could pose national security and privacy risks for millions of U.S. citizens.” Schumer’s main concerns were:

In order to operate the application, users must provide the company full and irrevocable access to their personal photos and data. According to its privacy policy, users grant FaceApp license to use or publish content shared with the application, including their username or even their real name, without notifying them or providing compensation.

Furthermore, it is unclear how long FaceApp retains a user’s data or how a user may ensure their data is deleted after usage. These forms of “dark patterns,” which manifest in opaque disclosures and broader user authorizations, can be misleading to consumers and may even constitute a deceptive trade practices. Thus, I have serious concerns regarding both the protection of the data that is being aggregated as well as whether users are aware of who may have access to it.

In particular, FaceApp’s location in Russia raises questions regarding how and when the company provides access to the data of U.S. citizens to third parties, including potentially foreign governments.

A similar ‘Reds-under-the-bed’ alarm was sounded by Bob Lord, a former Yahoo! executive and current chief security officer for the Democratic National Convention (DNC), who told Democratic campaign staff not to use the app, because it “was developed by Russians.”

And small business lawyer Elizabeth Potts Weinstein also warned about the app’s terms, stating “if you use #FaceApp you are giving them a license to use your photos, your name, your username and your likeness for any purpose including commercial purposes (like on a billboard or internet ad).”

The app’s terms read:

“You grant FaceApp a perpetual, irrevocable, nonexclusive, royalty-free, worldwide, fully-paid, transferable sub-licensable license to use, reproduce, modify, adapt, publish, translate… distribute, publicly perform and display your User Content.”

Former marketing manager for Google and security expert Ariel Hochstadt said:

“Hackers many time[s] are able to record the websites that people visit, and the activities they perform in those websites, but they don’t always know who are those users. Imagine now they used the phone’s camera to secretly record a young gay person, that visits gay sites, but didn’t yet go public with that, and they connect his face with the websites he is using.”

He continued:

“They also know who this image is, with the huge DB they created of Facebook accounts and faces, and the data they have on that person is both private and accurate to the name, city and other details found on Facebook. With so many breaches, they can get information and hack cameras that are out there, and be able to create a database of people all over the world, with information these people didn’t imagine is collected on them.”

The app was been around since 2017, when it was created by Wireless Lab in St. Petersburg, Russia. In case you wondered, IT experts are yet to catch FaceApp doing anything nefarious, or at least more nefarious than what other apps out there do. The company has provided assurance that it doesn’t get access to all camera photos, contrary to what some people have claimed, and that the servers used for its AI magic are owned by Amazon and Google.

via ZeroHedge News https://ift.tt/2XZO9Us Tyler Durden

In reality, there are a number of things employers can do in response to a minimum wage hike that don’t involve laying off employees…

Most of you will be familiar with a supply and demand graph. This shows a demand curve, which graphs the relationship between the price of something and the quantity demanded of that something, as well as a supply curve, which graphs the relationship between the price of something and the quantity supplied of that something. It is probably the most basic—and useful—model in economics.

Whether the something in question is a good or a service, shoes or labor, the basic supply and demand model predicts that, ceteris paribus, an increase/fall in the price of something will lead to a fall/increase in the quantity demanded of that something—this is Econ 101.

In the context of minimum wage laws, this model predicts that setting a minimum wage above the equilibrium level or raising it will lead to a lower quantity of labor demanded. Often, people think this means fewer workers employed. So, when minimum wage hikes aren’t followed by increases in unemployment, people cite this as evidence that minimum wage hikes don’t reduce employment.

But a model is an abstraction from reality. In that messy reality, there are a number of things employers can do in response to a minimum wage hike that don’t involve laying off employees.

Cut Hours Rather Than Workers

Remember, the simple supply and demand model says that increasing the price of labor leads to a lower quantity of labor demanded. But an employer doesn’t need to cut workers to achieve that. They can cut their hours instead.

Research from Seattle illustrates this. In 2014, the city council there passed an ordinance that raised the minimum wage in stages from $9.47 to $15.45 for large employers in 2018 and $16 in 2019. In 2017, research from the University of Washington examining the effects of the increases from $9.47 to as much as $11 in 2015 and to as much as $13 in 2016, found:

…the second wage increase to $13 reduced hours worked in low-wage jobs by around 9 percent, while hourly wages in such jobs increased by around 3 percent. Consequently, total payroll fell for such jobs, implying that the minimum wage ordinance lowered low-wage employees’ earnings by an average of $125 per month in 2016. [This was later revised to $74]

As the model predicts, the price of labor increased, and the quantity of labor demanded fell.

A follow-up paper looked at the impact on workers who were employed at the time of the wage hike, splitting them into experienced and inexperienced workers. It found that, on average, experienced workers earned $84 a month more, but about a quarter of their increase in pay came from taking additional work outside Seattle to make up for lost hours. Inexperienced workers, on the other hand, got no real earnings boost—they just worked fewer hours. Again, as the model predicts, the price of labor increased and the quantity of labor demanded fell. Instead of more money, they got more free time.

Make Employees Work Harder

An employer could try to raise worker productivity to match the new minimum wage. One way to do this is simply to work their employees harder.

One paper by Hyejin Ku of University College London looks at the response of effort from piece-rate workers who hand-harvest tomatoes in the field to the increase in Florida’s minimum wage from $6.79 to $7.21 on January 1, 2009. It found that worker productivity (i.e., output per hour) in the bottom 40th percentile of the worker fixed effects distribution increases by about 3 percent relative to that in the higher percentiles. The author concludes:

These findings suggest that while an exogenously higher minimum wage implies a higher labor cost for the firm, the rising cost can be partly offset by the increased effort and productivity of below minimum wage workers.

Another recent study by economists Decio Coviello, Erika Deserranno, and Nicola Persico looks at the impact of a minimum wage hike on output per hour among salespeople from a large US retailer. “We find that a $1 increase in the minimum wage (1.5 standard deviations) causes individual productivity (sales per hour) to increase by 4.5%,” they note.

Importantly, tomato harvesting and sales are labor-intensive work. Any increase in output per hour can be assumed to come from increased physical effort.

Cut Other Elements of Remuneration

Supporters of higher minimum wages talk almost exclusively about wages. But this is only one part of a worker’s total remuneration. The cost of an employee to the employer is not just the wage but total remuneration, including benefits such as health insurance. If legislation increases the wage, the employer can keep overall remuneration the same by reducing other elements.

A new paper from economists Jeffrey Clemens, Lisa B. Kahn, and Jonathan Meer finds that this is what happens in practice. The authors “explore the theoretical and empirical relationship between the minimum wage and fringe benefits, with a focus on employer-sponsored health insurance.” They find:

[There is] robust evidence that state-level minimum wage changes decreased the likelihood that individuals report having employer-sponsored health insurance. Effects are largest among workers in very low-paying occupations, for whom coverage declines offset 9 percent of the wage gains associated with minimum wage hikes. We find evidence that both insurance coverage and wage effects exhibit spillovers into occupations moderately higher up the wage distribution. For these groups, reductions in coverage offset a more substantial share of the wage gains we estimate.

Simply put, as the minimum wage rises, other elements of worker compensation fall.

Hire Fewer People, More Robots

If a business that plans to add 10 jobs over a year cancels these plans on the passage of a minimum wage hike, those 10 jobs have been destroyed without ever showing up in the data.

Economists from Washington University in St. Louis use wage data on one million hourly wage employees from over 300 firms spread across 23 two-digit NAICS industries to estimate the effect of six state minimum wage changes on employment. They find “…that firms are more likely to reduce hiring rather than increase turnover, reduce hours, or close locations in order to rebalance their workforce.”

As we look at responses over time, we also see the possibility that employers can substitute capital inputs for labor inputs.

Economists Grace Lordan and David Neumark analyze how changes to the minimum wage from 1980 to 2015 affected low-skill jobs in various sectors of the US economy, focusing particularly on “automatable jobs – jobs in which employers may find it easier to substitute machines for people,” such as packing boxes or operating a sewing machine. They find that across all industries they measured, raising the minimum wage by $1 equates to a decline in “automatable” jobs of 0.43 percent, with manufacturing even harder hit.

They conclude that

groups often ignored in the minimum wage literature are in fact quite vulnerable to employment changes and job loss because of automation following a minimum wage increase.

Minimum wage hikes are bad public policy. Economics, like all social sciences, has difficulty testing its models against data, but even where we can, the evidence bears this out.

via ZeroHedge News https://ift.tt/32zNUD7 Tyler Durden

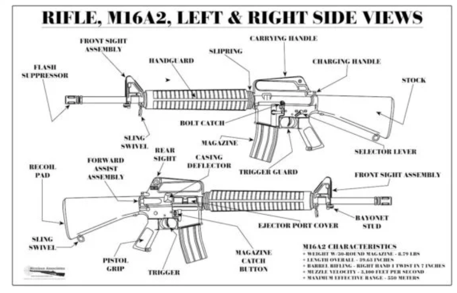

Philippine Foreign Secretary Teodoro Locsin said on Tuesday that the Philippine Army wants to buy 74,000 M-16 assault rifles with accessories from the US, following President Duterte’s 180-degree stance about not purchasing defense equipment from the West.

Locsin made the request to US Assistant Secretary of State for East Asian and Pacific Affairs David Stilwell on Tuesday who was in Manila for the 8th US-Philippines Bilateral Strategic Dialogue, reported Philstar Global.

“I told him that to concretize words of US-Phl amity into action is to sell us what Pompeo was told we need and want to buy 74,000 brand new M16s – w/3 clips each. And Duterte will finish all security threats to our democracy. Not a gift; we will pay. We’re waiting,” Locsin said on Twitter.

This was Stilwell’s first trip to the region since becoming Assistant Secretary of State for East Asian and Pacific Affairs last month. He discussed strengthening the two countries’ economic and defensive ties and promoting regional stability in the Indo-Pacific region, including free and unobstructed access to waters in the South China Sea.

“As a treaty ally, our partnership with the Philippines is critical for realizing our shared vision for a free and open Indo-Pacific, with sovereign thriving nations,” Stilwell said in a statement, adding that a strong bilateral alliance “deters aggression and promotes regional stability.”

Last month Duterte had a change of heart in purchasing American defense equipment since he said he now likes President Trump.

A falling out between Duterte and the Trump administration occurred last summer when the Philippines bought grenade launchers from a blacklisted Russian firm, a deal that almost resulted in sanctions.

Both sides acknowledged the significance of a robust Philippines-US alliance in improving security cooperation and promoting regional stability.

Stilwell referenced US State Secretary Michael Pompeo’s March statements on the 1951 Mutual Defense Treaty, explaining that if any Philippine vessels or aircraft in the South China Sea are attacked will trigger Article IV of the Mutual Defense Treaty.

“Noting this, senior officials discussed a wide variety of issues of mutual interest and reaffirmed their commitment to deepening the alliance and expanding areas of cooperation,” the Philippines-United States Eighth Bilateral Strategic Review Joint Statement said.

Both sides are committed to starting new activities to enhance maritime awareness, would probably result in an increase of joint military exercises in the South China Sea. They also agreed on upholding freedom of navigation through the South China Sea, especially around China’s militarized islands.

The war hawks in the Trump administration are doing everything in their power to squeeze China, the rising power of the world, the 2019 theme seems to be restoring the Philippines-US relationship, to eventually ramp up joint-military exercises in the South China Sea to continue pressure on China.

via ZeroHedge News https://ift.tt/30yS3pg Tyler Durden

On a day that’s witnessed serious escalation amid already soaring tensions in the Persian Gulf, Iran has confirmed the vessel it earlier said its IRGC forces seized for “smuggling” oil is in fact Panamanian-flagged oil tanker MT Riah which had disappeared near Iranian waters starting last weekend. State TV aired dramatic footage showing multiple IRGC fast-boats swarming the clearly marked vessel in the Strait of Hormuz.

On Tuesday international reports described the Riah as a tanker based in the United Arab Emirates and cited US intelligence officials to say Iran’s navy had forced the vessel into waters near Iran’s coast starting late Saturday night. Iran had initially denied the accusations that it had detained the vessel.

“We do this (inspecting ships) every day. These are people who smuggle our oil,” Iran’s Press TV quoted Iranian Foreign Minister Mohammad Javad Zarif as saying, adding: “It was a small ship used to smuggle 1 million litres – not 1 million barrels – of crude oil.”

It’s clear that Tehran is attempting to ramp up the pressure on Washington and drive up global oil prices, while also potentially in the beginning phase of making good on its long time threat to cut off global shipping through the vital oil passageway.

State run ISNA had earlier in the day described, “A foreign vessel smuggling one million liters of fuel in the Lark Island of the Persian Gulf has been seized,” and said its navy detained it starting Sunday.

Iran’s Press TV had previously issued the following details:

The incident took place to the south of the Iranian Lark Island on Sunday.

IRGC naval forces, which were patrolling the waters on an anti-smuggling mission, acted against the vessel in a “surprise” operation upon ascertaining the nature of its cargo and securing the required legal approval from Iranian authorities.

The ship had loaded the fuel from Iranian dhows and was about to hand it over to other foreign vessels in farther waters. The vessel, which had 12 foreign crewmembers aboard at the time of the mission, is capable of carrying two million liters of fuel.

The statement hailed the naval forces’ “perceptiveness” in frustrating the smuggling effort. It added that the crime had invoked due legal proceedings.

Days ago Iran vowed to “answer” the UK’s seizure and detention of the ‘Grace 1’ which had been transporting 2 million barrels of Iranian oil to Syria. The Royal Marines had boarded it in the Strait of Gibraltar and arrested its crew.

Tehran condemned it as an act of “piracy” and warned the UK it would respond in kind. Thursday’s so far mysterious vessel seizure announced by the IRGC could be the start of the promised coming retribution.

Meanwhile, late in the day Thursday President Trump announced that the amphibious assault ship, the USS Boxer, shot down an Iranian drone in the Strait of Hormuz in a defensive action.

But strangely, Iran’s FM Zarif claimed not be aware of any drone downing following Trump’s announcement, according to Reuters. “We have no information about losing a drone today,” Zarif told reporters at the United Nations.

via ZeroHedge News https://ift.tt/2xW8dN0 Tyler Durden

Grant’s Almost Daily, submitted by Grant’s Interest Rate Observer

On Tuesday, California governor Gavin Newsom signed Assembly Bill 1054, establishing a $21.5 billion wildfire relief fund and setting a June 30, 2020 deadline for fallen utility PG&E Corp. (PCG on the NYSE) to emerge from bankruptcy in order to participate. PG&E, which was found liable for a series of 2017 and 2018 blazes including the Camp Fire (which killed 85 people and destroyed the town of Paradise), entered Chapter 11 on Jan. 29. Investors have kept their hopes up for a swift return to business as usual, as the company still commands a $9.8 billion market cap.

There is reason for that optimism. The new legislation will allow utilities to choose between accessing designated liquidity and insurance funds which allow for fire cost coverage. While PG&E cannot participate in the scheme until it emerges from bankruptcy, analysts at Bloomberg Intelligence note today that PG&E shareholders “would face significantly less downside” if the company can achieve various safety certifications and make the necessary payments to buy in to the insurance fund post-bankruptcy.

As noted by The Mercury News yesterday, “as much as some legislators may have wanted to roundly punish bad actors among California’s electricity providers, they were mindful that even a slap on the wrist to utilities could have the unintended impact of a punch in the nose to consumers.”

But will PG&E investors avoid the proverbial knuckle sandwich? In its most recent 10-Q filing on March 31, the company disclosed $14.2 billion in existing wildfire-related liabilities. In testimony concurrent with the filing, CFO Jason Wells estimated that figure could end up topping $30 billion.

The clock is ticking for future liabilities, as claims from any new wildfire damages would take precedence over existing liabilities. A study released Sunday by the journal Earth’s Future finds that: “During 1972–2018, California experienced a five-fold increase in annual burned area, mainly due to more than an eight-fold increase in summer forest-fire extent.”

Media scrutiny continues apace. Last Wednesday, The Wall Street Journal reported that company executives were aware of problems with transmission lines that were eventually responsible for the Camp Fire, yet “repeatedly failed to perform the necessary upgrades.” In addition, PCG estimated in 2017 that its transmission towers were 68 years old on average (already above the mean life expectancy of 65 years), with some as old as 108.

The company is no stranger to bad press surrounding environmental disaster and big payouts. In 1996, PG&E was forced to pay $333 million to settle claims it dumped more than 350 gallons of chemically-poisoned water into ponds near Hinkley, Calif., an episode memorialized in the 2000 film Erin Brockovich.

It might be harder to shake the wildfire legacy costs than the bulls reckon. In a bearish analysis of PG&E in the Feb. 22 edition of Grant’s, Angelo Thalassinos, the deputy managing editor at Reorg Research, Inc., noted that the Camp Fire may act as a millstone around PCG for years to come.

The thing that jumps out at me, and the distinction here from other mega cases, is the damages and liabilities from the wildfires. It most harkens back to old Chapter 11 cases that had asbestos liabilities. . . . There is potential for continuing damages from that respect throughout the bankruptcy case and even post-emergence.

In the five months since our report, PCG shares have treaded water, lagging the 8.3% total return from the S&P 500 Utilities Index over that period. But the company’s debt has fared well, with the senior unsecured 6.05% notes of 2034 rallying to 111 cents on the dollar (from 93 in February), for a 283 basis point pickup over Treasurys.

That performance disparity seemingly reflects the unfolding political situation. On Friday, The Journal reported that creditors led by Elliott Management Corp. petitioned California lawmakers for bondholder-friendly tweaks to the bill, including allowing PG&E to issue debt to pay future wildfire claims but not existing liabilities, such as from the Camp Fire. As noted by the WSJ: “Legislators ultimately sided with bondholders on the issue.”

Victory in court for that Elliott-led bondholder group would likewise spell trouble for shareholders. Creditors have proposed injecting up to $18 billion into PCG, in return for control of the company. A court hearing at which Elliott et al. will present their arguments is scheduled for July 23.

With PCG continuing to sport a substantial market cap, investors may be underestimating the risks. That Feb. 22 Grant’s analysis broke down the pertinent numbers, concluding:

To the equity holders, it’s a daunting figure. Wildfire claims of just $10 billion (around a third of the CFO’s estimate) would impair the equity— assuming that PG&E’s asset base is not overstated through overly long depreciation schedules.

Even prior to the recent disaster, PCG’s shareholder economics looked less than compelling. From 2013 to 2018, the company generated $25.5 billion in operating cash flow, well shy of the $31.9 billion in capital expenditures over that period. In his Jan. 31 affidavit, CFO Wells forecast that cash from operations will lag capex by an additional $1.6 billion per year in 2019 and 2020. Even after suspending its dividend in December 2017, post-2013 disbursements to shareholders foot to $4.4 billion, a sum which PCG borrowed to pay.

The utility increased operating earnings to $3 billion in 2017 from $2.3 billion in 2008, while capital employed jumped to $62 billion in 2018 from $30 billion in 2008. James S. Chanos, founder and managing partner of Kynikos Associates L.P. and a PG&E bear, noted to Grant’s in February:

It’s a 2% return on incremental capital. That is below their cost of capital. They are liquidating. The utility is in effect liquidating before your eyes before any wildfire liability.

via ZeroHedge News https://ift.tt/2O1Ibmp Tyler Durden

In a long-overdue step that suggests Boeing is eager to put the 737 MAX debacle behind it, the Seattle airplane company announced it would take a $4.9 billion charge in Q2 related to the grounding of the 737 Max aircraft, which represents that troubled aircraft maker’s first estimate of the cost of compensating airlines for schedule disruptions and delays in aircraft deliveries. The charge will result in a $5.6 billion hit to pre-tax earnings when the company reports earnings on July 24, the company said in a statement issued on Thursday.

There is just one problem: there is no assurance Boeing’s 737 MAX woes will end in Q2, with media reports suggesting the grounding of the jet may last into 2020. That scenario is not being contemplated by the world’s largest commercial aircraft manufacturer, which said it assumes regulatory approval will be granted for the Max to return to global skies in the fourth quarter of this year.

“This assumption reflects the company’s best estimate at this time, but actual timing of return to service could differ from this estimate,” the company said.

To address the possibility of an extended grounding, Boeing said that although the charge equal to $8.74 per share, would be taken in the second quarter, the company said it expects “potential concessions or other considerations” would come “over a number of years”. As the FT notes, “concessions in such circumstances often take the form of price cuts on aircraft orders rather than cash payments.”

More importantly, and the reason why the company finds itself in this spot, Boeing said it is raising its estimated costs to produce the aircraft by $1.7bn in the second quarter, primarily due to higher costs associated with a reduced production rate (and hopefully with safety equipment that is sold as standard instead of options). While Boeing cut production to 42 per month in April from 52 per month, and is parking the grounded plane in car-lots…

… Boeing said it expects to ramp up to 57 a month in 2020.

Addressing Boeing’s shareholders, CEO Dennis Muilenburg said that “we remain focused on safely returning the 737 Max to service. This is a defining moment for Boeing.”

Boeing chief financial officer Greg Smith added: “We are taking appropriate steps to manage our liquidity and increase our balance sheet flexibility the best way possible as we are working through these challenges. Our multiyear efforts on disciplined cash management and maintaining a strong balance sheet, in addition to our strong and broad portfolio offerings, are helping us navigate the current environment.”

Boeing suspended financial guidance after the grounding and said it will issue new guidance in future, but for now investors liked the fact that over half a billion dollars would be paid out, sending Boeing stock higher after hours.

via ZeroHedge News https://ift.tt/2JTX4lB Tyler Durden

Today in “the entire world is steadily losing its mind” news, there will no longer be terms like “manhole”, “policeman” or “chairman” in Berkeley, California city codes, according to CNN.

Words that “imply a gender preference” will soon be removed from the city’s codes and replaced with gender-neutral terms, according to recently adopted ordinances. Berkeley voted on Tuesday to replace “gendered” terms in its municipal codes.

Words like “manhole” will be replaced with words like “maintenance hole”.

“Manpower” will be replaced with “human effort”.

The item passed without comment or discussion and wasn’t controversial, according to Berkeley City Council member Rigel Robinson, the bill’s primary author.

Robinson said:

“There’s power in language. This is a small move, but it matters”.

Gendered pronouns like “he” and “she” will also be replaced with words like “they”. The office of the city manager said that the city’s municipal codes currently “contain mostly masculine pronouns”.

Robinson concluded:

“Having a male-centric municipal code is inaccurate and not reflective of our reality. Women and non-binary individuals are just as entitled to accurate representation. Our laws are for everyone, and our municipal code should reflect that.”

When will this idiocy end?

via ZeroHedge News https://ift.tt/2JSx4a4 Tyler Durden

You have to wonder whether Chicago Mayor Lori Lightfoot really thought she could get away with it.

Just three weeks ago, she was demanding a state taxpayer bailout of her city’s nearly bankrupt pension funds. The problem was so big, she said, she’d risk her “re-election” over it. Eventually, Gov. J.B. Pritzker denied her bailout request for obvious reasons – the state is just one notch from a junk rating.

Now news reports confirm that Lightfoot has offered the Chicago Teachers’ Union a five-year contract that will cost taxpayers another $325 million. That includes guaranteed raises of more than 14 percent over the life of the contract. And that, of course, turns into more pension benefits and an even bigger pension hole for CPS.

That’s an expensive gift for a city that Lightfoot claims is in need of a multi-billion dollar bailout.

That about-face should infuriate every downstate Illinoisan. If the bailout had gone through, here’s what all Illinoisans would have been paying for:

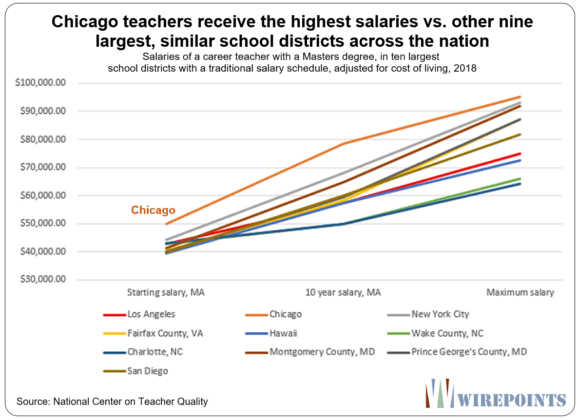

1. Chicago teachers are already highest paid vs. teachers in similar districts.

Chicago teachers are the nation’s highest paid when compared to the largest school districts with traditional salary schedules, according to data from the National Center on Teacher Quality.

For example, a Chicago teacher with a master’s degree receives $80,000 a year after ten years of work. In contrast, an equivalent teacher in New York City makes $70,000 and a Los Angeles teacher makes $60,000.

A big reason for that is due to how fast Chicago teacher salaries grow. The average new teacher with one to four years under her belt starts out with a salary just above $50,000. By the time that teacher reaches 10 to 14 years of service, her salary grows to more than $85,000 annually.

2. The average career Chicago teacher will get $2 million in total pension benefits, far more than ordinary Illinoisans.

High salaries translate into big pension benefits for career teachers. The average CPS teacher who retired in 2018 with 30-34 years of service had a final average salary of nearly $98,000 and a starting pension of over $70,000. Their average retirement age was 61.

That pension will increase automatically by 3 percent each year and by year 25 of retirement, the pension will be double its starting amount. In all, the average retired career Chicago teacher will collect over $2.1 million in benefits over the course of her retirement.

In contrast, an ordinary Illinoisan at retirement would need to have around $1.5 million in his or her account at retirement to collect the same amount of benefits as a career Chicago teacher. Most Illinoisans will never save that amount of money.

3. Taxpayers still “pick up” a majority of Chicago teacher pension contributions.

Not only do Chicago teachers receive millions in pension benefits, they contribute almost nothing towards them over the course of their careers.

Chicago teachers are supposed to contribute 9 percent of their salary every year towards their pensions. But every year since 1981, CPS has paid for, or “picked up” 7 of that 9 percent.

That means Chicago teachers only have to pay 2 percent of their salary towards their own pensions every year. That costs Chicagoans over $100 million a year.

Rahm tried to reform pickups in 2016, but he was rebuffed by the union. Only new workers lost the pickup. And even then, the district gave out extra 3.5 percent raises in exchange.

4. CPS is losing students but spending more on them than ever before.

One of the CTU’s contract demands calls on CPS to spend money to hire more teachers and even more support staff. That might make sense in a dynamic, rapidly growing city with a growing school population.

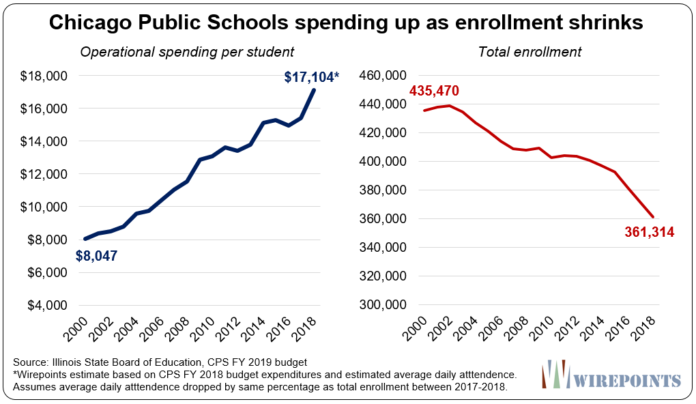

But CPS is losing students and has been for nearly 20 years. At the same time, the district’s spending per student has jumped.

In all, CPS’ per student spending has doubled since 2000 according to ISBE, even as the district’s enrollment has fallen by nearly 75,000 students, or 17 percent, over the same time period.

5. Near empty, failing schools should be closed and their resources redirected.

Declining enrollment is hitting some Chicago schools particularly hard.

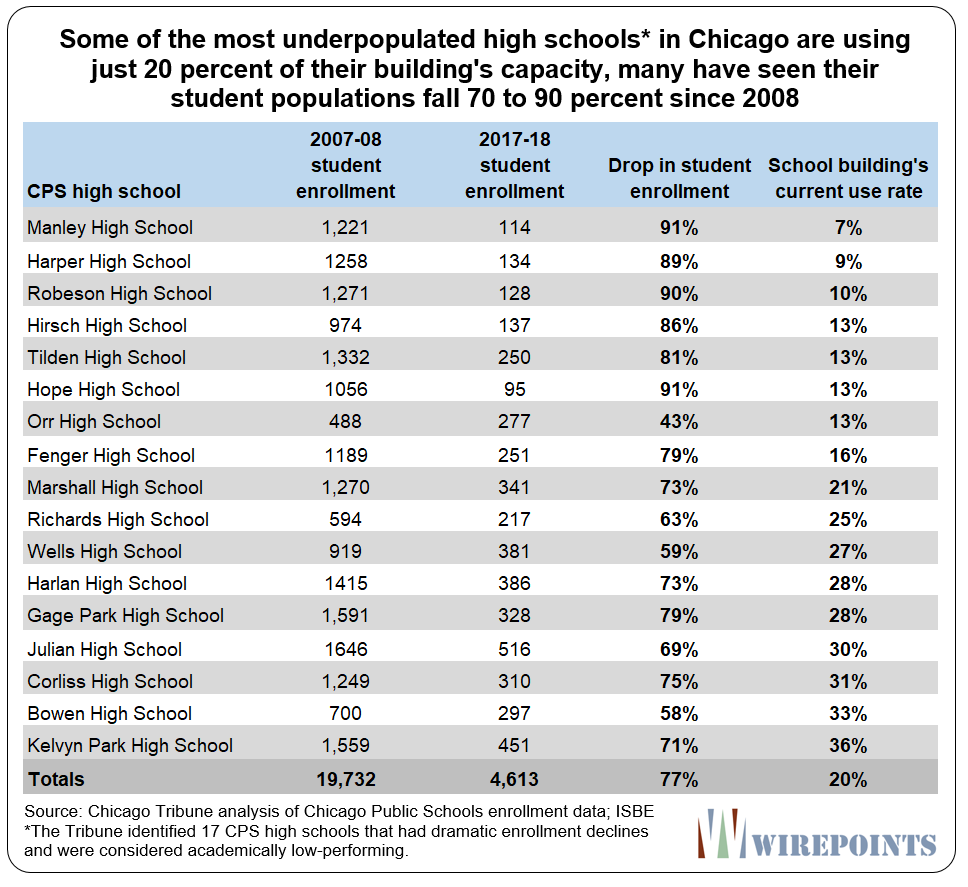

In 2017, the Chicago Tribune examined the demographics of some of the most underpopulated schools in Chicago. It found the enrollment of the 17 worst schools has dropped from nearly 20,000 in 2008 to just over 4,600 today. Their buildings are, on average, filled to just 20 percent capacity.

And the few students that do attend aren’t getting a good education. In those schools, no more than 8 percent of students are ready for college. Despite that, the CPS hasn’t closed the nearly-empty, failing schools.

* * *

Lightfoot has landed some great punches when taking on corruption in City Hall, but when it comes to finances, she’s acting just like any other Chicago politician.

She said she’d “risk her political career” to tackle pensions. Making downstate taxpayers foot the city’s pension bills is hardly a “risk.”

via ZeroHedge News https://ift.tt/2JNcRTc Tyler Durden

{kind=link}