African COVID-19 Cases Hit 1.2 Million As Dr. Fauci Urges FDA To ‘Carefully Vet’ Vaccines: Live Updates Tyler Durden

Tue, 08/25/2020 – 08:46

Summary:

Africa COVID cases near 1.2 million

Deaths in England + Wales hit 20-week low

Germany to extend benefit program

German infections remain close to 4-month high

Russia reported 4,696 new cases

Usain Bolt tests positive

Dr. Fauci warns FDA must thoroughly vet COVID vaccines

Dr. Hahn walks back endorsement of FDA-approved plasma treatment

* * *

President Trump and the RNC placed the GOP president’s response to the coronavirus pandemic front-and-center during last night’s opening salvo for what’s set to be a scaled down version of the quadrenniel Republican Convention, as Trump and his supporters praised Trump’s travel restrictions, “Project Warp Speed” and other measures for helping the US fight off the virus.

But on Tuesday morning, the focus shifts back to Europe and Asia, as yet another case of COVID-19 reinfection has been confirmed – this time, in Belgium, making it the first such case in Europe, following yesterday’s confirmed case of reinfection documented in Hong Kong.

The disheartening discovery comes as Belgium grapples with one of the Continent’s worst active outbreaks.

In the UK, deaths in England and Wales fell to a 21 week-low after reporting just 139 virus-linked fatalities during the week ended Aug. 14. That’s jus 1.5% of the region’s total fatalities, the Office for National Statistics said on Tuesday.

Germany, which has seen new case numbers climb in recent weeks, will likely extend a state wage-support program, according to Carsten Schneider, a caucus manager for the Social Democratic Party, who made the claim during an interview with Deutschlandfunk radio.

German Finance Minister Olaf Scholz proposed extending the job-preserving subsidies to 24 months last week, arguing that the measure would cost the government an extra €10 billion euros ($11.8 billion).

Meanwhile, Germany’s new coronavirus cases increased at a pace close, but just below, Sunday’s 4-month high, while its closely watched infection rate dropped back below 1, indicting that the pandemic has shifted back into “contraction” territory.

The Robert Koch Institute reported 1,628 new infections in the 24 hours through Tuesday morning, raising its total to 236,122. The daily gain compared with 633 on Monday and 1,737 on Saturday. That marked the highest number since April. One death was also reported, lifting the overall number of deaths to 9,276.

Officials from Chancellor Angela Merkel’s coalition, expected to meet later on Tuesday in Berlin, have “always taken the sensible path in the end on labor-market and social policy,” he said.

Bavarian Premier Markus Soeder warned Tuesday that Germany risks a return to the peak levels of daily new cases close to 7,000 seen at the end of March and beginning of April, and ruled out easing restrictions on movement and social gatherings.

After the Oxford/AstraZeneca vaccine project released some more optimistic sounding updates touting the possibility of winning approval for the experimental vaccine by the end of the year, AstraZeneca announced that its first participants have been dosed in a Phase 1 trial of AZD7442, a COVID-19 drug created by combining two monoclonal antibodies harvested from sick patients.

As infection rates fall in Hong Kong…

…the special administrative region said it would allow dining-in until 9 pm, while cinemas, beauty parlors and outdoors sports venues will start reopening Friday, according to Secretary for Food and Health Sophia Chan.

The government will also allow residents to go maskless in parks and while exercising outdoors. The present suite of social distancing measures will be extended to Aug. 27, per Bloomberg.

Elsewhere, while the outbreak across the world’s poorest continent hasn’t been nearly as severe as many feared the, Coronavirus outbreak in Africa is closing in on 1.2 million cases and 30,000 deaths ((with nearly 28,000 confirmed so far), according to the Africa Centres for Disease Control and Prevention. The total number of infections stands at 1,195,297, including 27,783 fatalities and 921,783 recoveries, according to the latest update. Southern Africa is the continent’s worst-hit regio, with 652,400 cases and 14,100 deaths, and South Africa is the worst hit country. But even countries that demonstrated a surprisingly robust response, like Uganda, are starting to see problems, according to Al Jazeera.

In sports news, Champion sprinter Usain Bolt tested positive for coronavirus just days after hosting a ‘mask-less’ 34th birthday bash.

Russia, meanwhile, reported 4,696 new cases on Tuesday, pushing its national total to 966,189, the world’s 4th-largest, cementing its lead over South Africa (which currently holds the No. 5 spot). 120 Russians died, pushing the death toll to 16,568.

Finally, while millions of Americans were focused on the RNC last night, FDA Director Stephen Hahn took to twitter to recant a statement he made late Sunday evening, when he parroted President Trump’s claim that treatments based on survivor plasma had already proven to reduce mortality by 35%, which Trump used to justify pressuring the FDA for its emergency approval.

Not only did Hahn walk back these claims…

Media coverage of FDA’s decision to issue emergency authorization for convalescent plasma has questioned whether this was a politically motivated decision. The decision was made by FDA career scientists based on data submitted a few weeks ago.

We at FDA do not permit politics to enter into our scientific decisions. This happens to be a political season but FDA will remain data driven. On behalf of FDA‘s 18,000 career employees, I want to reassure the American public about this commitment.

I have been criticized for remarks I made Sunday night about the benefits of convalescent plasma. The criticism is entirely justified. What I should have said better is that the data show a relative risk reduction not an absolute risk reduction.

…but Dr. Hahn’s decision to acquiesce to Trump’s demands has even prompted other national health-care figures, like National Institute of Allergy and Infectious Diseases head Dr. Fauci, to issue warnings about the FDA’s credibility. Dr. Fauci said the agency must thoroughly vet all vaccine candidates, since a rushed job could risk doing even more damage, and destroying the agency’s credibility in the eyes of the public. He told Reuters giving approval to one potential vaccine would make it “difficult, if not impossible for other vaccines to enroll people in their trials.”

via ZeroHedge News https://ift.tt/31wbzpT Tyler Durden

Mortgage Delinquencies Soar To Decade High Tyler Durden

Tue, 08/25/2020 – 08:35

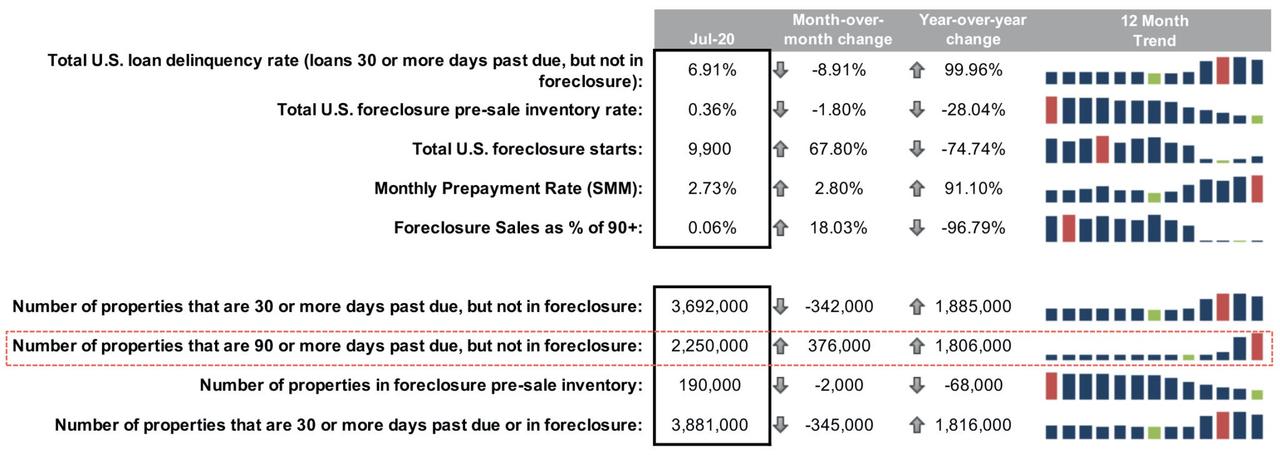

Readers may recall last week we outlined the dam of pent up mortgage delinquencies continued to crack, with the share of delinquent Federal Housing Administration’s loans hitting a record high in the second quarter.

With millions of Americans out of work due to the virus-induced recession, their personal income has become overly reliant on Trump stimulus checks, as we’ve outlined, a quarter of all personal income now comes from the government.

A fiscal cliff hit the economy on August 01, when the program to distribute stimulus checks to tens of millions of broke Americans ran out of funds. Even though President Trump signed an executive order to fund additional rounds of checks, only one state, as of August 21, has paid out new jobless benefits and paused evictions as stimulus talks in Washington have failed to materialize into a deal.

Leading up to the fiscal cliff in July, financial data firm Black Knight reported the number of serious mortgage delinquencies catapulted to a ten-year high.

The number of homes with mortgage payments past due by 90 days or more rose by 376,000 in July to a total of 2.25 million. Serious mortgage delinquencies have jumped by 1.8 million since July 2019, a decade high, not seen since the last financial crisis.

Black Knight’s July 2020 Month-End Mortgage Performance Statistics:

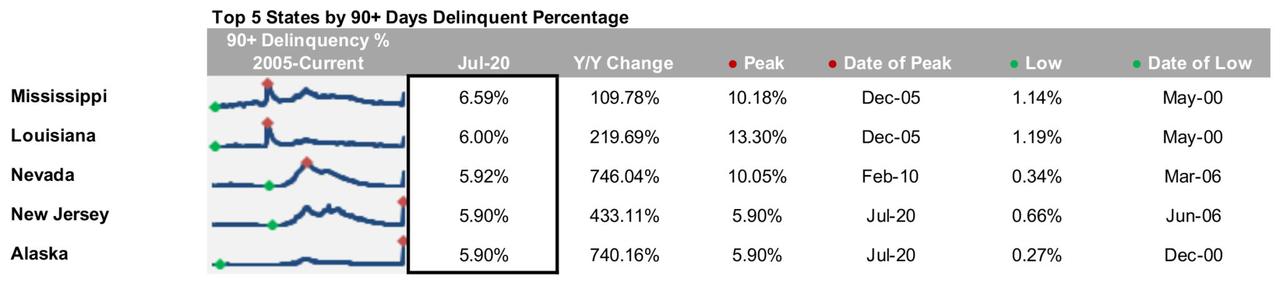

Top 5 States By 90+ Days Delinquent Percentage:

Black Knight said, “foreclosure activity continues to remain muted due to widespread moratoriums; though starts rose for the month, overall activity remains near record lows.”

Cracks in the dam of pent up mortgage delinquencies are becoming larger as the presidential election nears. Still, millions of folks are unable to service mortgages, remain protected from foreclosure by the federal forbearance program, in which borrowers with pandemic-related hardships can delay payments for as much as a year without penalty. What happens when the program finally ends, and all the payments that were deferred come due could result in housing market weakness.

The prospect of a tidal wave of foreclosures could be ahead as the mortgage industry and government’s policies were merely short-term measures to push a housing crisis off until after the election.

If homeowners still can’t find jobs as the labor market recovery falters, then their ability to service future mortgage becomes impossible. At the same time, deep economic scarring is being realized, resulting in the shape of the economic recovery transforming from a “V” to a “Nike Swoosh.”

Even with part of the housing market booming, that is primarily due to folks ditching metro areas for suburbia and ultra-low mortgage rates pulling demand forward in such a massive way that today’s boom will lead to much lower activity in the future.

Think about it, millions of folks still can’t pay their mortgage, and many of them still can’t find jobs. But, of course, none of that matters as President Trump distracts the sheep and points to how well the Nasdaq is doing.

via ZeroHedge News https://ift.tt/3lfMjvz Tyler Durden

Yesterday’s Fourth Circuit decision in U.S. v. Miselis, written by Judge Robert King and joined by Judges Albert Diaz and Allison Jones Rushing considered a facial First Amendment challenge to the Anti-Riot Act:

Whoever travels in interstate or foreign commerce or uses any facility of interstate or foreign commerce, including, but not limited to, the mail, telegraph, telephone, radio, or television, with intent—

(1) to incite a riot; or

(2) to organize, promote, encourage, participate in, or carry on a riot; or

(3) to commit any act of violence in furtherance of a riot; or

(4) to aid or abet any person in inciting or participating in or carrying on a riot or committing any act of violence in furtherance of a riot;

and who either during the course of any such travel or use or thereafter performs or attempts to perform any other overt act for any purpose specified [above] … [s]hall be fined … or imprisoned not more than five years ….

“[T]o incite a riot”, or “to organize, promote, encourage, participate in, or carry on a riot”, includes, but is not limited to, urging or instigating other persons to riot, but shall not be deemed to mean the mere oral or written (1) advocacy of ideas or (2) expression of belief, not involving advocacy of any act or acts of violence or assertion of the rightness of, or the right to commit, any such act or acts.

“Riot” is defined as a public disturbance involving “an act or acts of violence by one or more persons part of an assemblage of three or more persons, which act or acts shall constitute a clear and present danger of, or shall result in, damage or injury to the property of any other person or to the person of any other individual,” or involving threats of such violence.

The court held (to oversimplify):

[A.] The “incite” prohibition (item 1) constitutionally applies when people travel or communicate with the intent to engage in constitutionally unprotected incitement, defined by Brandenburg v. Ohio (1969) to mean advocacy intended to and likely to promote an imminent riot. This covers things such as traveling to engage in actual incitement (e.g., going to some place with the plan to egg on a violent crowd), whether the incitement takes place or the plan is foiled before such incitement (in which case the behavior is constitutionally unprotected attempted incitement). The “instigating” provision is likewise valid, as a synonym for inciting.

[B.] The “organize” prohibition in item 2 is constitutional because it involves not just abstract advocacy but concrete orchestrating of criminal rioting. The best way of understanding this ruling, I think, is by analogy to U.S. v. Williams (2008), which held that specific solicitation of crime (as opposed to abstract advocacy) is constitutionally unprotected as speech integral to the underlying criminal conduct.

[C.] The “aid or abet” prohibition (item 4) is constitutional because it likewise involves not just abstract advocacy but concrete assistance (even if the assistance comes through speech) to criminal rioters. Here too U.S. v. Williams (2008) would be a good analogy. (The “commit any act of violence” provision wasn’t challenged, but that’s clearly constitutional).

But the court held other parts of the statute were unconstitutional:

[i.] The “promote” and “encourage” prohibition (item 2) and the “urging” provision are unconstitutional because they can extend to abstract advocacy of crime.

[ii.] Likewise, the “not involving advocacy of any act or acts of violence or assertion of the rightness of, or the right to commit, any such act or acts” provision suggests that advocacy of violence and assertion of the rightness of violence are prohibited, and that too is unconstitutional.

[iii.] The court also held that the words “promote,” “encourage,” “urging or,” and “not involving advocacy of any act or acts of violence or assertion of the rightness of, or the right to commit, any such act or acts” should therefore be in effect deleted from the statute—something courts often do, under the name of “severing” unconstitutional provisions—and the remainder of the statute would be upheld.

The analysis generally seems right to me. The decision came in the prosecution of white supremacists, but of course the same reasoning (both as to the partial validity of the statute and the partial invalidity) would equally apply to people connected to any other kinds of riots, whether antifa or anti-globalization or anything else.

from Latest – Reason.com https://ift.tt/3aWPt2x

via IFTTT

Yesterday’s Fourth Circuit decision in U.S. v. Miselis, written by Judge Robert King and joined by Judges Albert Diaz and Allison Jones Rushing considered a facial First Amendment challenge to the Anti-Riot Act:

Whoever travels in interstate or foreign commerce or uses any facility of interstate or foreign commerce, including, but not limited to, the mail, telegraph, telephone, radio, or television, with intent—

(1) to incite a riot; or

(2) to organize, promote, encourage, participate in, or carry on a riot; or

(3) to commit any act of violence in furtherance of a riot; or

(4) to aid or abet any person in inciting or participating in or carrying on a riot or committing any act of violence in furtherance of a riot;

and who either during the course of any such travel or use or thereafter performs or attempts to perform any other overt act for any purpose specified [above] … [s]hall be fined … or imprisoned not more than five years ….

“[T]o incite a riot”, or “to organize, promote, encourage, participate in, or carry on a riot”, includes, but is not limited to, urging or instigating other persons to riot, but shall not be deemed to mean the mere oral or written (1) advocacy of ideas or (2) expression of belief, not involving advocacy of any act or acts of violence or assertion of the rightness of, or the right to commit, any such act or acts.

“Riot” is defined as a public disturbance involving “an act or acts of violence by one or more persons part of an assemblage of three or more persons, which act or acts shall constitute a clear and present danger of, or shall result in, damage or injury to the property of any other person or to the person of any other individual,” or involving threats of such violence.

The court held (to oversimplify):

[A.] The “incite” prohibition (item 1) constitutionally applies when people travel or communicate with the intent to engage in constitutionally unprotected incitement, defined by Brandenburg v. Ohio (1969) to mean advocacy intended to and likely to promote an imminent riot. This covers things such as traveling to engage in actual incitement (e.g., going to some place with the plan to egg on a violent crowd), whether the incitement takes place or the plan is foiled before such incitement (in which case the behavior is constitutionally unprotected attempted incitement). The “instigating” provision is likewise valid, as a synonym for inciting.

[B.] The “organize” prohibition in item 2 is constitutional because it involves not just abstract advocacy but concrete orchestrating of criminal rioting. The best way of understanding this ruling, I think, is by analogy to U.S. v. Williams (2008), which held that specific solicitation of crime (as opposed to abstract advocacy) is constitutionally unprotected as speech integral to the underlying criminal conduct.

[C.] The “aid or abet” prohibition (item 4) is constitutional because it likewise involves not just abstract advocacy but concrete assistance (even if the assistance comes through speech) to criminal rioters. Here too U.S. v. Williams (2008) would be a good analogy. (The “commit any act of violence” provision wasn’t challenged, but that’s clearly constitutional).

But the court held other parts of the statute were unconstitutional:

[i.] The “promote” and “encourage” prohibition (item 2) and the “urging” provision are unconstitutional because they can extend to abstract advocacy of crime.

[ii.] Likewise, the “not involving advocacy of any act or acts of violence or assertion of the rightness of, or the right to commit, any such act or acts” provision suggests that advocacy of violence and assertion of the rightness of violence are prohibited, and that too is unconstitutional.

[iii.] The court also held that the words “promote,” “encourage,” “urging or,” and “not involving advocacy of any act or acts of violence or assertion of the rightness of, or the right to commit, any such act or acts” should therefore be in effect deleted from the statute—something courts often do, under the name of “severing” unconstitutional provisions—and the remainder of the statute would be upheld.

The analysis generally seems right to me. The decision came in the prosecution of white supremacists, but of course the same reasoning (both as to the partial validity of the statute and the partial invalidity) would equally apply to people connected to any other kinds of riots, whether antifa or anti-globalization or anything else.

from Latest – Reason.com https://ift.tt/3aWPt2x

via IFTTT

“ There are three ways to make a living on Wall Street; be first, be smarter, or cheat.”

As yet another storm batters the UK, I drove she-who-is-Mrs-Blain to the station early this morning. The brave little soldier is going up to her office in London today for the first time since March!

The S&P hits another record high, but headlines this morning include the first documented case of reinfection with COVID 19. Some 5 months after suffering the virus, a Hong Kong chap has contracted a different strain of the virus while in Europe.

Apparently, its “nothing to worry about”, as the fellow “might’ have had very low antibody levels from the first mild infection, and the vaccines being developed “shouldn’t” be rendered ineffective because virus mutations won’t change the way it binds to cells and triggers an immune response.

Hmm.. Trying to cut through the noise… It sounds like COVID is going to be just like flu – immunologists guessing which strain to immunise against each year. Maybe that’s a good thing – the market has so priced in Vaccine expectations it was increasingly looking a “sell-the-fact” moment when/if it actually ever happens..

Meanwhile.. Good News is Bad.

Great news in UK as Tesco announces 16,000 new jobs for its internet delivery service – which has doubled in volume during the pandemic. That’s another nail for the high-street; an example of how COVID has accelerated the evolution of retail away from high-streets and malls towards internet delivery. In the states, Lumber prices have doubled on the back of the Pandemic construction boom, holding back new builds, pushing prices higher, eat, sleep, repeat. What you win on the swings, you lose on the roundabouts…

Inflation Averaging?

And then there is this week’s big event to look forward to; Fed Chair Jerome Powell will use the virtual Jacksons Hole conference to announce “average inflation” targeting. Whoop Whoop Whoopedy-do… All the Fed Watchers think this is going to be profoundly significant – a historic moment as the Fed will continue with a 2% inflation target, but instead of worrying if it goes above, it will allow inflation to remain higher for longer, ie “averaging” for the periods when it’s been sub-target.

These are just words. Meaning is more important.

What it actually means is the Fed will simply ignore inflation, and won’t hike interest rates if/when the economy is overheating and inflation rises.

The market will love it.

Inflation averaging means – “don’t worry about rate hikes, or normalising rates, we are so desperate for inflation we’re going to encourage it.” It’s a way of reassuring the market there won’t be interest rates rises for ever and ever… and magics away the fear of a market taper-tantrum if inflation were to rise. It completely resets the game of Fed Watching – you don’t have to worry about interest hikes ever again.. (or at least in the medium term..)

This confirms what we’ve come to understand.

In the battle against deflation the Fed, and I guess the other central banks, see markets as the major weak spot. The are managing markets to avoid a global market meltdown occurring, which would further drive chronic economic weakness across the whole global economy.

Economically, the effects of pandering to markets are proving disasterous – inflated assets bubbles and a massive debt anchor tied around our feet. The result is we are stuck “In Irons”. Let me explain.

“In Irons” is a sailing term. It’s a crisis which can occur when a sailing ship has to turn through the wind. Yachts can’t sail directly into the wind. At best they can sail upwind at an angle, say 45 degrees either side of the direction the wind is coming from. (Sailors call sailing close to the wind “close-hauled” – it’s when the boat leans over at a frightening angle.) Because you can’t sail directly into the wind, there is a 90 degree “no-go zone” centred on the direction the wind is coming from.

If a boat has to “tack” through the wind, and its going too slowly, doesn’t have enough momentum or something goes wrong as the manoever is happening, the boat can get stuck in the wind: its bows pointing directly into the wind, and the sails flapping uselessly. We say the boat is “In Irons” – as in handcuffed. It’s extremely difficult to get the boat the boat back on the wind.

It happened to us over the weekend when I was helming a friend’s beautiful 1888 Pilot Cutter in the Hamble Classics Regatta. We tacked too slowly with too little momentum, and got caught In Irons. It took ages to get out. What saved us was a swiftly running tide that pulled us back into the wind.

I reckon “In Irons” is a pretty good allusion to the current economic crisis.

The Pandemic has simply catalysed an economic crisis that’s been brewing since 2008. It’s a culmination of over-regulation in the wake of the 2008 crisis, a transfer of risk from banks to the asset management sector, distortions from artificially-low interest rates creating massive price bubbles across all financial assets, soaring debt levels, and deflation rather than inflation becoming the major threat.

It’s happened at a time of enormous technical innovation, which has rather hidden the reality of a growing deflationary threat as Western economies choke on debt and companies increasingly become debt-encumbered zombies. We haven’t learnt much from the 30 year Japanese deflationary death spiral because we’ve been so excited about the potential of internet shopping, the connected economy and smart-phones, soaring property values, and the consumption led economy.

Now that economy is wobbling and is increasingly unbalanced. It feels like large parts of the global economy are flapping uselessly in the wind. Getting the economy back on track after the sudden turn forced upon us by the Pandemic is proving much tougher than Central Banks expected. They know that QE failed to stimulate growth by much after 2008, but it did avoid a succession of embarrassing market collapses by bailing out banks (by making the bond holdings look attractive) and supporting jobs by stopping insolvent companies going bust.

The newest buzz-expression in markets is a “K-shaped recovery” – explaining why the big five Tech stocks have done so extraordinarily well, while the rest of the market are laggards. The real pain is still to come. Banks are simply not lending at present, concerned about their rising NPLs while keeping capital ratios high so they don’t upset shareholders or trigger CoCo capital instruments (which governments might just do anyway). That means SMEs too small to feast at the burgeoning new issue debt markets are likely to find themselves starved of new capital as this recession really bites. It’s therefore likely the underperformance between the Tech Haves and SME Have-Nots is going to accelerate.

The right strategy is to keep arbitraging the increasingly convoluted mess the Central Banks have created and are walking us all into. The Central Banks are trapped in promises to do “whatever it takes”, and low interest rates forever (whatever inflation does). The problem for investors is where to find returns – the only answer to take on more and more risk for lower and lower returns.

(And buy gold for when it inevitably all goes wrong…)

via ZeroHedge News https://ift.tt/3htE78G Tyler Durden

Futures Punch To New Record High After US-China Reaffirm Committment To Trade Deal Tyler Durden

Tue, 08/25/2020 – 07:59

Three things send the market higher these days: i) optimism that Congress will finally renew the fiscal stimulus which expired on July 31; ii) optimism that a covid vaccine will miraculously fix the global economy, and iii) in a throwback to 2019 optimism on the US-China trade deal. We got a dose of iii) late on Monday when the USTR reported that top U.S. and Chinese trade officials reaffirmed their commitment to a Phase 1 trade deal which has seen China lagging on its obligations to buy American goods, with a call (originally scheduled for Aug 15) in which both sides saw “progress and are committed to taking the steps necessary to ensure the success of the agreement”, and demonstrating a willingness to cooperate even as tensions rise over issues ranging from data security to democracy in Hong Kong.

Given the exchanges between the U.S. and China recently “have been negative, any small bit of positivity is seen as a big step forward, even when it isn’t,” said David Madden, market analyst at CMC Markets UK. It was certainly enough to push US equity futures higher for a fourth straight session, with the Emini punching to a new all time of 3,448.75 during the Asian session which saw shares rise throughout most of Asia, before trimming gains to around 3,440 after the European open.

The S&P 500 and Nasdaq both clocked new record highs on Monday, with the benchmark index surpassing its pre-pandemic high last week even as recent economic data pointed to a wobbly recovery from the virus-led downturn. However, even as the ES was up some 0.3%, Nasdaq futures were shockingly in the red sparking panic and hysteria among a generation of retail daytraders who have never seen a red open in a centrally-planned market.

Salesforce.com, Amgen and Honeywell climbed between 3.6% and 4% premarket on news they would join the blue-chip Dow Jones Industrial Average index on Aug. 31. This came at the expense of three companies that are getting kicked out of the DJIA including E&P titan and formerly world’s most valuable company Exxon Mobil, Pfizer and Raytheon Technologies which were down between 1.5% and 2.4%. Best Buy dropped despite reporting earnings that beat on the top and bottom line; Folgers coffee maker JM Smucker medical device maker Medtronic are also due to report quarterly results before the opening bell.

Investors also remain focused on vaccine progress as global economies reopen. Moderna said it’s near a deal to supply at least 80 million vaccine doses to the European Union.

“A steady flow of progress with Covid-19 treatments/vaccines is delivering the latest boost to risk appetite,” said Oanda senior market analyst Edward Moya, but just like Morgan Stanley, he cautioned that “market breadth however does not support the surge to record high territory for U.S. indexes.”

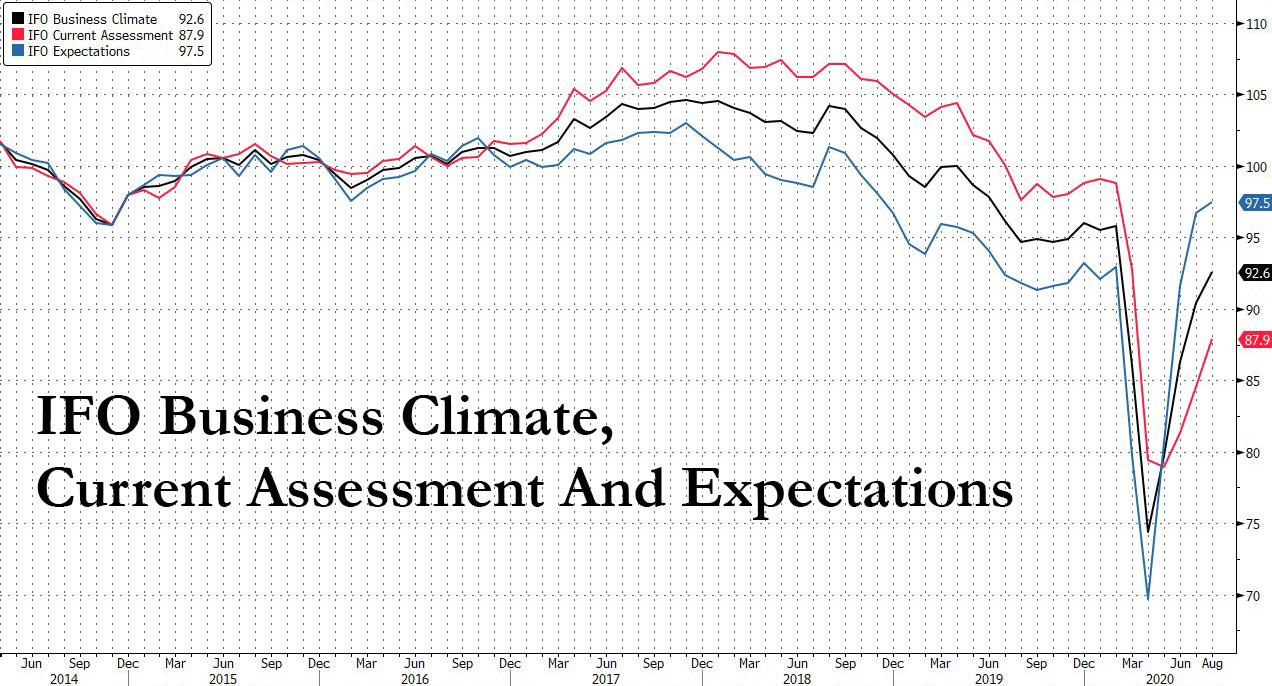

European stocks advanced for a second day after the latest IFO surveys showed German companies turning slightly more optimistic on the economic recovery despite missing expectations on, well, expectations:

Ifo Expectations 97.5 vs. Exp. 98.0 (Prev. 96.7)

Ifo Current Conditions 87.9 vs. Exp. 87.0 (Prev. 84.5)

Ifo Business Climate 92.6 vs. Exp. 92.1 (Prev. 90.4)

The current assessment continues to lag expectations about the future, a reversal to pre-covid days.

The Stoxx Europe 600 Index climbed 0.4% as of 10:28 a.m. in London, with travel stocks advancing more than 2% and leading gains among sectors.

In Asia, markets were broadly higher, with Tokyo, Taipei, Seoul and Sydney all in the green while peers in Hong Kong and Shanghai slipped. South Korea’s Kospi Index gained 1.6% and Jakarta Composite rising 1.2%, while Shanghai Composite dropped 0.4%. Japan’s Topix gained 1.1%, with Globeride and Land Co rising the most. The Shanghai Composite Index retreated 0.4%, with Jiangxi Hongdu Aviation Industry and Dalian Bio-Chem posting the biggest slides.

In rates, treasuries traded heavy into early U.S. session with yields cheaper by 1bp-4bp across the curve in bear-steepening move. Treasury 10-year yields close to cheapest level of the day at 0.684%, highest in several days; long-end-led losses steepen 2s10s, 5s30s by ~2bp. Factors weighing on the curve include IG credit issuance, start of Treasury auction cycle and grind higher in S&P 500 futures. In Europe, Bunds lag Treasuries by 2bp while gilts trade broadly in line. As Bloomberg notes, concession starts to build into front-end also with $50b 2-year note sale at 1pm ET, ahead of $51b 5-year Wednesday and $47b 7-year Thursday.

In FX, the dollar and yen have softened against most currencies, while the euro has been topping the top-performing list as Action Economics recaps. This dynamic has come amid risk-on positioning in global markets. EUR-USD lifted to the mid 1.1800s, posting an intraday peak at 1.1843, which is 60 pips up on Monday’s New York closing level. The euro has also rallied against the yen, which is the day’s biggest loser, and most other currencies. While a bout of general dollar selling has helped to lift EUR-USD, there have concurrently been a couple of cues to buy euros, including August German Ifo business climate indicator, which beat forecasts in rising to a headline reading of 92.6, and remarks from German finance minister Scholz, who said there are signs that the German economy is developing above forecasts. USD-JPY, meanwhile, posted an eight-day high at 106.38, which is a gain of just over 40 pips on yesterday’s closing level. The biggest mover out of the main currency pairings and crosses was EUR-JPY, which was showing over a 0.8% gain. The cross printed a six-day high at 125.97. GBP-JPY was not far behind, while AUD-JPY was showing a near 0.5% upward advance. Cable pegged an intraday high at 1.3126. USD-CAD posted a five-day peak at 1.3240 in pre-London trading, subsequently settling lower.

In commodities, oil was slightly higher as traders kept a watchful eye on Tropical Storm Laura, which is expected to strengthen into a hurricane before making landfall later this week. U.S. gasoline futures rose to the highest level since March on concern over possible fuel shortages. Elsewhere, gold dipped as low as $1,922 an ounce trading in a narrow range.

Looking at today’s calendar, we’ll get the FHFA house price index for June, new home sales or July, as well as the Conference Board’s consumer confidence reading and the Richmond Fed manufacturing index for August. The Conference Board is expected to show U.S. consumer confidence improved slightly in August after falling more than expected in July amid a flare up in coronavirus cases. Otherwise, San Francisco Fed President Daly will be speaking, and earnings releases include Salesforce, Medtronic, Intuit and Autodesk. Investors also await Federal Reserve Chairman Jerome Powell’s address on Thursday for hints on the central bank’s next steps to support an economic recovery.

Market Snapshot

S&P 500 futures up 0.3% to 3,439.25

STOXX Europe 600 up 0.4% to 372.29

MXAP up 0.3% to 172.99

MXAPJ up 0.2% to 572.19

Nikkei up 1.4% to 23,296.77

Topix up 1.1% to 1,625.23

Hang Seng Index down 0.3% to 25,486.22

Shanghai Composite down 0.4% to 3,373.58

Sensex up 0.06% to 38,824.20

Australia S&P/ASX 200 up 0.5% to 6,161.39

Kospi up 1.6% to 2,366.73

German 10Y yield rose 2.1 bps to -0.47%

Euro up 0.3% to $1.1817

Italian 10Y yield unchanged at 0.819%

Spanish 10Y yield rose 3.3 bps to 0.36%

Brent futures up 0.3% to $45.28/bbl

Gold spot down 0.1% to $1,926.57

U.S. Dollar Index down 0.3% to 93.06

Top Overnight News from Bloomberg

The U.S. and China reaffirmed their commitment to the phase-one trade deal in a biannual review, demonstrating a willingness to cooperate even as tensions rise over issues ranging from data security to democracy in Hong Kong

Germany’s coronavirus daily new cases increased at a pace not seen for almost four months

Moderna Inc. has announced it is close to a deal with the EU to provide at least 80 million vaccine doses

Storm Laura is expected to be upgraded to a hurricane when it makes landfall on the American gulf coast in the next few days, leading U.S. gasoline futures to rise to their highest since the start of the pandemic on fears over potential fuel shortages

Courtesy of NewsSquawk, here is a quick recap of global markets:

Asian equity markets were mixed after trading mostly higher as the region initially took impetus from the fresh record highs on Wall St where cyclicals outperformed and with risk appetite also spurred by COVID-19 plasma treatment hopes, as well as reports US and China’s top trade negotiators held a constructive conversation on the Phase 1 agreement. ASX 200 (+0.5%) was led by tech and financials although gains in the benchmark index were capped by resistance at the 6200 level and amid headwinds from a deluge of earnings, while Nikkei 225 (+1.4%) outperformed as exporters cheered recent currency weakness and with the government to ease the ban on foreign residents returning to the country. Hang Seng (-0.3%) and Shanghai Comp. (-0.4%) also began higher after the PBoC boosted its liquidity efforts with a total CNY 300bln of reverse repo operations and following talks between USTR Lighthizer, Treasury Secretary Mnuchin and China’s Vice Premier Liu He in which both sides saw progress and were committed to taking the next steps required to ensure the success of the deal. However, gains later faded given that discussions were not much of a surprise and with the PBoC distancing itself from lowering capital requirements for bank, while Hong Kong was also cautious ahead of Chief Executive Lam’s announcement on social distancing arrangements later today as the current restrictions which limits public gatherings to two people are set to expire. Finally, 10yr JGBs were lacklustre with price action contained below the 152.00 level after weakness in T-notes and demand sapped by the gains in stocks, with the 20yr JGB auction doing little to spur prices despite printing improved results.

Top Asian News

U.S., China Signal Progress on Trade Deal as Relations Fray

Hong Kong to Relax Social Distancing Rules as Virus Cases Drop

Credit Suisse’s Head of Asia Technology to Join Xiaomi as CFO

Thai Cabinet Approves Extension of Emergency for Another Month

Stocks in Europe trade with modest gains (Euro Stoxx 50 +0.6%) albeit off highs, as sentiment somewhat improved following the mixed APAC lead. Some suggest that the “constructive” US-Sino trade call is spurring risk assets. However, it is worth remembering that there has been no new progress/developments in terms of trade, and in the grand scheme of things, US-Sino relations remain at all-time-lows on a number of fronts – e.g. geopolitics, capital markets and technology. On the data front – the German Ifo survey showed optimism in the country has increased, but economists noted that the German recovery is fragile and stocks were largely unfazed by the release. Sectors are mostly in the green, although the cyclical tilt seen at the open has somewhat faded, but nonetheless, financials and travel & leisure hold their top positions in the region, whilst materials and energy lag amid the price action in their respective complexes. In terms of individual movers, Aveva (+3.9%) holds onto gains after announcing a proposed acquisition of Osisoft for an enterprise value of USD 5bln. Nokia (+0.5%) and Ericsson (+1.2%) remain firm after reports noted that the Indian government is looking to phase out equipment from Chinese companies including Huawei from its telecoms network amid border tensions – with Nokia and Ericsson potentially to gain from this. On the flip side, Swisscom (-1.0%) is subdued after Swiss competition watchdog opened a probe into the Co. amid suspected abuse of market position within the broadband sector.

Top European News

German Businesses Signal Optimism Recovery Is on Track; Germany Closes In on Agreement to Extend Job-Preserving Aid

Credit Suisse to Cut Branches, Staff by Merging Swiss Unit

Vanishing Jobs and Empty Offices Plague Britain’s Retailers

Italy Clashes With Ex- Monopoly Over Future of Phone Network

In FX, as the DXY hovers just above the 93.000 level within a confined 93.012-351 band, major Dollar counterparts are also sitting close to big figures awaiting firm breaks or clearer direction, like the Euro in wake of an encouraging German Ifo survey on balance. To recap, 2 out of the 3 metrics exceeded expectations, but the more forward looking outlook reading missed consensus remains the institute was reserved in describing the economic recovery as fragile. Hence, Eur/Usd was toppy ahead of yesterday’s peak and hefty option expiry interest close by at 1.1850 in 1 bn. Meanwhile, Cable continues to pivot 1.3100 ahead of CBI trades and amidst the ongoing threat of Britain leaving transition without a Brexit trade deal, and the Franc is still tethered to 0.9100 after a dip in Swiss Q2 payrolls was largely nullified by an upward revision to the previous quarter. However, the Yen has retreated through 106.00 and into a lower range on a loss of safe-haven premium and with US Treasury yields backing up before this week’s auctions amidst curve re-steepening.

NZD/AUD/CAD – The Kiwi is holding above 0.6500 in advance of NZ trade data and the Aussie has gleaned more indirect support from another firm PBoC CNY fix that in turn has given the CNH fresh impetus to test 6.9000 vs the Greenback. Aud/Usd is meandering between 0.7152-82 following mixed independent impulses overnight via an improvement in ANZ weekly consumer confidence in contrast to labour data revealing a 1% decline in jobs for the month to August 8 and 2.8% drop in the state of Victoria for a national fall of 4.9% relative to mid-March (pre-pandemic or the ‘first’ wave as such). Conversely, the Loonie is licking wounds beneath 1.3200 and detached from choppy oil prices following Canada’s appeal to the WTO against US soft lumber levies.

SCANDI/EM – Marginal Nok outperformance even though Norwegian GDP was a bit weaker than forecast in Q2, but the Try has not derived much traction on the back of a rise in Turkish manufacturing sentiment and the Rub is not tracking the firm tone in Brent against the backdrop of ongoing geopolitical/diplomatic tensions that are also weighing on the Lira.

In commodities, WTI and Brent front month futures remain relatively flat in early European trade, with the benchmark only some USD 0.2-0.3/bbl off overnight lows. Traders are keeping a keen eye on the developments in the Gulf of Mexico as Tropical Storm Laura is forecast to evolve into a major hurricane before making landfall late-Wednesday, whilst Marco was downgraded to a Tropical Depression. On that front, the latest update from the Search Results Bureau of Safety and Environmental Enforcement (BSEE) estimates around 82.4% of current oil production shuttered – with the next release scheduled for 1400ET/1900BST. WTI Oct resides around USD 42.50/bbl (vs. low ~42.30/bbl), whilst its Brent counterpart trades around USD 45.25/bbl (vs. low USD 45.08/bbl). Traders will now be eyeing the weekly release of the Private Inventories in the absence of macro headlines – albeit price action could be muted as hurricane developments are timelier. Elsewhere, spot gold trades choppy within a tight range on either side of USD 1930/oz whilst spot silver sees similar action around 26.50/oz – both moving in tandem with the Buck ahead of Fed Chair Powell’s speech on Thursday. In terms of base metals, Dalian iron ore prices fell some 3.5% whilst Shanghai steel rebar edged lower as downstream demand recovery missed market forecasts. Conversely, Shanghai nickel prices rose almost 2% at one point amid dwindling Chinese port inventories.

US Event Calendar

9am: FHFA House Price Index MoM, est. 0.3%, prior -0.3%; House Price Purchase Index QoQ, prior 1.7%

9am: S&P CoreLogic CS 20-City MoM SA, est. 0.1%, prior 0.04%; YoY NSA, est. 3.6%, prior 3.69%

10am: New Home Sales, est. 790,000, prior 776,000; MoM, est. 1.8%, prior 13.8%

10am: Richmond Fed Manufact. Index, est. 10, prior 10

DB’s Jim Reid, freshly back from vacation, concludes the overnight wrap

If you’d have told me at the start of the year that at the end of August I’d be quarantining with my family and not allowed to leave the perimeter of my garden then I’d have been extremely worried and assumed that one of my children had dug up the bubonic plague. Thankfully it’s less worrisome than that and instead because I was on holiday in the French Alps and new travel rules now apply back to the U.K from France. Ironically the French Alps have hardly seen new cases rise even if they have in say Paris and parts of the South of France. So if you’d have got back two days before me from Paris you wouldn’t have to quarantine but I do from the Alps. We still had to cut our holiday short by a week to ensure the children didn’t miss their first days at school next week. Elite athletes are exempt from these rules but after trying to show the customs officer at the Channel Tunnel my golf swing I wasn’t given special dispensation.

So we’ve been looking after three young terrors at home over the last week and it’s been painful with nothing to do or nowhere to go. Bronte also doesn’t understand why she doesn’t get walked. All first world problems admittedly but I really don’t understand those that say the best thing about Covid is that you get to spend more time with your family. I love them all dearly but an hour or two a day is ideal (that doesn’t include my wife by the way).

So I actually mean it when I say it’s good to be back in my home office mentally and physically quarantining from the kids. Over the holiday I’ve been thinking a lot about the virus and the way forward and I continue to scratch my head about the end game. Within the next few weeks we should know much more about the state of play with regards to the leaders in the vaccine race (supportive news yesterday for the AstraZeneca/Oxford Uni version as we’ll see below). That’s probably going to be the most important newsflow of the next month or so. We’re trying to collate as much info as possible on the current state of play with vaccines and will try to put out a piece next week on where we are at. Obviously if a vaccine gets approved in the coming weeks then we’ll likely have a realistic end game within months as I’m sure we’ll go into mass production very quickly.

However without a vaccine it feels like global strategies are very difficult to decipher. When lockdowns started back in March the main rational was to ensure health services did not get overrun. Five months on, the number of Covid cases in hospitals are relatively low in many areas and yet many countries seem to be trying to keep cases as low as possible as a badge of honour and the world has got so scared that such a strategy seems to meet high approval. Countries that are seeing cases rise are looked at with great suspicion even if hospitalisations are still relatively low. However is such suppression a sustainable strategy? Given this is happening in the northern hemisphere summer I can’t help wondering where we’ll be in two or three months time and what the reaction will be from the authorities.

The good news is that there continues to be plenty of evidence that those catching the virus seem to be from younger, less vulnerable cohorts and this seems to be contributing to a lower and lower case fatality rate across the globe alongside better treatment and possibly the virus mutating. To be fair listening to politicians the bar to renewed full lockdowns seems to be high around the world, but equally the bar to getting to anything resembling normality also seems very high. So we are in Covid limbo until a vaccine or a yet unidentified master plan materialises. All ahead of a northern hemisphere autumn and winter when life will naturally move more indoors.

To be fair all of this continues to be a passing curiosity to the US equity market which continues to hit new highs even if the breadth of the winners has narrowed further in recent weeks. Yesterday showed some signs of rotation and catch up from the laggards though, which helped push the S&P 500 up a further +1.00%, having already risen for 7 of the last 8 weeks. The move took the index to another record high and puts it +6.03% on a YTD basis. The airline industry led the S&P yesterday, gaining +8.23% as optimism on a possible vaccine buoyed the beaten down industry higher. In fact American Airlines (+10.53%), Carnival (+10.17%), United (+9.93%), Delta (+9.28%) and Norwegian Cruise Line (+7.58%) were five of the seven best performing stocks in the index. Elsewhere, tech stocks underperformed as there was some rotation out of biotechs (-0.47%) in particular. The Nasdaq closed +0.60% higher yesterday (also to a new record) with the tech-dominated index now standing at an astonishing +26.83% higher YTD.

On the vaccine news, AstraZeneca shares were up +2.06% following the FT report that the Trump administration could bypass normal regulatory standards for the Oxford vaccine. As the election approaches it seems inevitable that Mr Trump will want to encourage as much positivity on the virus as is in his power. So one to watch.

Oil prices were buoyant as well yesterday, with Brent crude up +1.76% to $45.13/bbl in a move that wiped out all of last week’s declines and helped energy stocks lead the equity advance on both sides of the Atlantic. Over in Europe, equities saw even bigger moves higher, with the STOXX 600 up +1.58% and the DAX up +2.36%.

The rotation into risk assets saw sovereign bonds lose ground somewhat yesterday, and yields on 10yr Treasuries were up +2.6bps by the close. With market participants awaiting Fed Chair Powell’s speech at Jackson Hole for any policy hints, our global head of rates research Francis Yared wrote a blog post yesterday (link here) in which he says that a lot of the expected dovishness is already priced into markets. As a result, only a material upsizing in QE should have a material market impact. There was a similar pattern for European rates too yesterday, where yields on 10yr bunds (+1.6bps), OATs (+0.9bps) and gilts (+0.7bps) all rose. And in line with this retreat from safe assets, gold extended its falls from the previous week with a further -0.60% decline. It’s now -6.53% off its highs 3 weeks ago.

Overnight the key news has been that the US and China’s top trade negotiators discussed the Phase 1 trade deal last night and the US concluded that both sides saw progress and are committed to its success. The US statement said that “The parties also discussed the significant increases in purchases of US products by China as well as future actions needed to implement the agreement,” while adding that China has made progress on other commitments like taking steps to ensure greater protection for intellectual property rights and removing impediments to American companies in the areas of financial services.

Asian markets are mostly positive this morning outside of China and HK which are seeing the Hang Seng (-0.53%) and Shanghai Comp (-0.19%) both down. The Nikkei (+1.84%), Kospi (+1.44%) and Asx (+0.42%) are up though alongside futures on the S&P 500 (+0.46%). Elsewhere, gold and silver prices are also up +0.39% and +0.49% and in agriculture commodities, CBT soybeans and corn future prices are up +1.10% and +1.52% respectively.

On the coronavirus and as alluded to at the top, countries around the world continue to re-implement restrictions at the first uptick in cases. Zurich has announced new limits on social gatherings of up to 100 unless masks are worn and have mandated that masks must be worn within shops. This followed news that the Netherlands have issued 10-day quarantine measures on all travelers from Spain, as well as the majority of travelers from France. This comes as Spain posted four month highs in cases last week. In what may be a harbinger for the colder month’s ahead, Germany is planning to stop testing people returning from hotspots, citing a lack of testing capacity for the virus. Those travelers will still have to undergo quarantine measures and will have to get tested themselves in order to exit their quarantine early. These measures weighed on the STOXX 600 Travel and Leisure stocks (-0.09%), which did not see the same performance as their American counterparts on the upbeat vaccine news.

We did get further signs of stabilisation in new cases in the United States though, with Florida reporting the lowest number of new cases since mid-June yesterday, while New York state saw their infection rate fall to 0.66%, the lowest since the beginning of the pandemic. In a sign of further normalization following the recent uptick in cases, Apple announced plans to reopen some of the over 120 stores that they had reclosed during the summer outbreak. This could happen as soon as the end of this month. Across the other side of world, Singapore has identified a total of 58 cases in the country’s largest foreign workers dormitory which houses c. 16,000 people and as a precaution has placed another 4,800 workers from the same dormitory on stay-home notices. Meanwhile, South Korea added a further 280 cases in the past 24 hours up from 266 a day earlier and also ordered kindergarten, elementary, middle and high schools in the greater Seoul area to shift to online classes from partial attendance. Elsewhere, Qantas Airways said overnight that it will cut an additional 2,500 jobs due to the COVID impact on top of the earlier announced plans to eliminate 6,000 jobs or 20% of the workforce.

To the day ahead now, and data highlights from Germany include the Ifo business climate indicator for August along with the final reading of Q2’s GDP. Meanwhile in the US, we’ll get the FHFA house price index for June, new home sales or July, as well as the Conference Board’s consumer confidence reading and the Richmond Fed manufacturing index for August. Otherwise, San Francisco Fed President Daly will be speaking, and earnings releases include Salesforce, Medtronic, Intuit and Autodesk.

via ZeroHedge News https://ift.tt/2Ysbt0r Tyler Durden

“From Cotton To Congress In 1 Generation” – Black Republicans Back Trump During RNC Night 1 Tyler Durden

Tue, 08/25/2020 – 06:33

Republicans wasted no time during the first night of the Republican National Convention from laying out their vision for America, a vision that rests on the spirit of national revival and unity, standing in contrast to the hysterical warnings about “the fate of our democracy” and the bankrupt ideology of identity politics.

Keynote speaker Tim Scott, the only black male Republican in all of Congress, topped a diverse bill of speakers that underscored the fact that Republicans under Trump haven’t given up on courting minority votes, even as Democrats have declared themselves the ‘saviors’ of minority groups – so long as they don’t accumulate too much wealth and power.

Speaking of his humble upbringing in South Carolina, Scott recounted how a mentor taught him the life-changing power of building companies and creating jobs.

The senator shared an incredibly moving tale about how his grandfather had been forced to leave school in the third grade to pick cotton. But he still lived long enough to see his grandson become the first Black American elected to both the House and the Senate.

“Our family went from cotton to Congress in one lifetime,” Scott said.

Scott wasn’t the only black male politician to speak. Vernon Jones, a lifelong Democrat who served in the Georgia General Assembly before resigning and announcing his support for Trump, criticized Democratic leaders tone deaf attempts at ‘connecting’ with minorities – like the infamous “kente clothe” incident.

Remember when Trump “sought to earn the Black vote, the Democratic Party leaders went crazy! Nancy Pelosi and Chuck Schumer literally started wearing Kente cloth scarves around the Capitol!”

As far as Dems pandering attacks on police go, Jones pointed out the irony in them walking around with their police escorts. “Isn’t it ironic that the Democrat politicians never leave home without security to protect them at all times? Why don’t they forgo their security and replace them with social workers, since that’s what they want for us?”

Football legend Herschel Walker shared stories from his 37-year friendship with Donald Trump, sharing a touching story about how Trump once joined Walker and their kids at Disney World, wearing his business suit in the sweltering heat as they waited in line for rides.

Then he landed one of his most powerful lines: “I take it as a personal insult that people would think I would have a 37-year friendship with a racist,” Walker said. “Growing up in the Deep South, I have seen racism up close. I know what it is. And it isn’t Donald Trump.”

One of the breakout stars of the evening was Kim Klacik, a young Republican woman and Congressional candidate running for the late Elijah Cummings’ congressional seat situated in the heart of Baltimore. “The Democrats have controlled my city, Charm City, for over 50 years,” she began in a powerful pre-recorded segment “And they have run this beautiful place into the ground. Abandoned buildings, liquor stores on every corner, drug addicts and guns on the street — that is now the norm in many neighborhoods,” she said.

And with their “de-fund the police” policies, Democrats risk making the situation in Baltimore worse, not better.

Other speakers on the slate from last night included the President’s son Donald Trump Jr., one of his most popular surrogates.

Kimberley Guilfoyle, “a Latina and a proud American”, also shared her support for Trump and how his policies have enabled “strivers” from the middle class and the working class to succeed.

Nikki Haley, former South Carolina Governor and until recently Trump’s ambassador to the UN, also spoke, adding one more minority voice to the Republican slate.

Trump kicked off one of his first appearances by lambasting the Democrats’ mail-in ballot efforts by sending out ballots to people who haven’t requested them.

“This is the most important election in the history of our country,” Trump said. “2016 – how special was that evening. But we have to be very, very careful…and we have to win.”

“Our country can go in a horrible horrible direction…or an even greater direction…and before the plague came in from China, we were going in a direction that we have never seen,” Trump said.

While the mainstream press loves to tout its flawed opinion polling, even the NYT was forced to admit yesterday that Trump’s ratings on the economy remain much higher than Joe Biden’s.

“The Nasdaq has broken the record 16 times already…but Biden, he said he’d shut it down,” Trump said.

via ZeroHedge News https://ift.tt/3lqV1rc Tyler Durden

In this blog, we present the anatomy of a financial crisis. A characteristic feature of a banking crisis is that it tends to follow, more-or-less, the same path regardless of the ‘shock’ or ‘trigger’ that initiates it.

The next phase of the crisis is likely to be a global financial crisis, as we have been anticipating for quite some time (see, e.g., Q-Review 4/2017). However, few understand what a financial crisis is, though it is probably among the most feared economic phenomena of mankind.

So, let’s dive in.

The initiation

If a banking system is sound and robust, it can usually withstand financial and economic shocks.

But a banking system may be fragile. Usually this is due to high leverage levels, where banks have either lent aggressively or carry risky financial investments on their balance sheets—usually both. Banks can also have a weak financial position, with chronically low profitability and insufficient reserves. As we have explained earlier, this is exactly the state the European banking sector finds itself in.

The onset of a financial crisis requires a trigger. The most common is a recession or the expectation of recession among consumers and investors.

Recession leads to diminished income and defaults by both corporations and households. This increases the share of non-performing loans in bank loan portfolios, reducing the value of loan collateral and increasing bank risks and capital needs. As write-downs and losses increase, mistrust among other banks and depositors and investors does as well. The bank’s share price will usually start to reflect this.

A ‘bank run’

If suspicion spreads, banks will be apprehensive about counterparty risk and will be unwilling to lend to one another even on an overnight basis. If allowed to continue, this will have a calamitous impact on liquidity in money markets.

In the worst case, possibly fueled by rumors and insider information, a ‘bank run’ will ensue, where depositors try to withdraw their money suddenly and simultaneously. In years past, depositors would queue outside of bank offices to obtain cash. Now withdrawals are largely electronic.

At the same time, the bank’s investors and institutional counterparties rush to lower their exposure by frantically selling its stocks and bonds as well as derivatives and other interbank liabilities. If this continues, trust in the bank is broken, and it fails. Growing speculation about the financial health of both sound and unsound banks, combined with funding issues, eventually triggers a system-wide banking crisis.

In history, there have been many different triggers for financial calamity. The trigger for the Great Depression of the 1930s was a recession, which first crashed the U.S. stock market in October 1929 and then started the banking crisis in October 1930. The financial crisis of Japan in the 1990s started from an asset market crash in 1990. The recent Global Financial Crisis had several triggers including the collapse of the “High-Grade Structured Credit Strategies Enhanced Leverage Fund” sponsored by investment bank Bear Stearns in June 2007, and ultimately the collapse of the venerable investment bank Lehman Brothers on 14th October 2008.

The response

What follows the initiation of a banking crisis—which often starts with just one bank—is dependent on the general condition of the banking sector and the response of authorities.

Bank regulators can take over the failing bank, ensure the payment of deposit guarantees, and arrange for the merger or acquisition of the ailing bank by a stronger financial institution. This well-established process provides that bank customers—depositors and borrowers—are protected while equity owners, management, and some, or even all, creditors rightly bear the losses. A central bank will usually provide liquidity to facilitate this. If the problems in the banking sector are limited to one bank, such measures may be sufficient to stem the panic.

However, if the banking sector as a whole is compromised or suffering from a significant enough economic shock, even sound policies may not be enough to cover losses of banks and depositors leading to sector-wide bank runs.

The implications

In a banking crisis, credit will become restricted and credit lines are likely to be withdrawn—especially those to enterprises. In the worst case, authorities will be able to rescue only certain banks or only save depositors, which occurred in Iceland in 2008/2009. When the banking sector collapses, it means that the economy faces a serious credit depression, where the availability of credit become diminished to a significant degree.

When the banking crisis is global, as it will be this time around, access to credit will be restricted globally, with hedging activity sharply curtailed as a result. For example, from 2007 to 2008, global gross capital flows plunged by 90 percent.

The availability of so-called “freight derivatives”, which are used by end-users (e.g., ship owners and grain houses) and suppliers (e.g., international trading companies) to mitigate the risk of shipments, may face a collapse. This would mean a serious reduction in, or even a complete halt to global freight activity. While it’s impossible to evaluate, precisely, how serious the impact of a collapse in the availability of these derivatives would have on global freight, we have to assume that it would be large, because manufacturers will not ship without adequate insurance.

In the case of a global financial crisis we therefore have to be prepared for:

Collapse of asset markets.

Collapse in global availability of credit and banking services.

Collapse in global demand.

Collapse of global freight.

In the worst case, the collapse of the global financial system (a global “systemic crisis”).

The coming crisis

The European banking crisis has been brewing for some time. It is also likely to go global, as Europe holds the largest concentration of global, systemically important banks (G-SIBs). Italy and Spain, but also Germany (Deutsche Bank), are the countries to keep a close eye on.

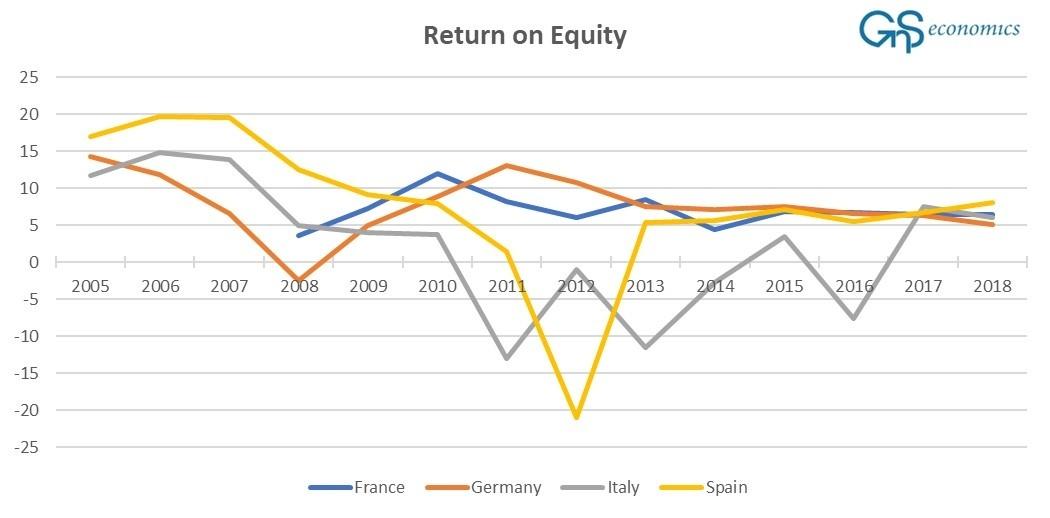

Return on Equity (RoE) of the European banks has been dismal since the GFC (see Figure 1). This is mostly for two reasons. First, the toxic assets, like CDOs, were allowed to remain and compromise the balance sheets of European banks after the GFC. Secondly, the misguided policies of the ECB (OMT, negative interest rates and QE) led to the deterioration of the profitability of the European banking sector.

Figure 1. Return on Equity (RoE, net income minus shareholders’ equity). Source: GnS Economics, IMF

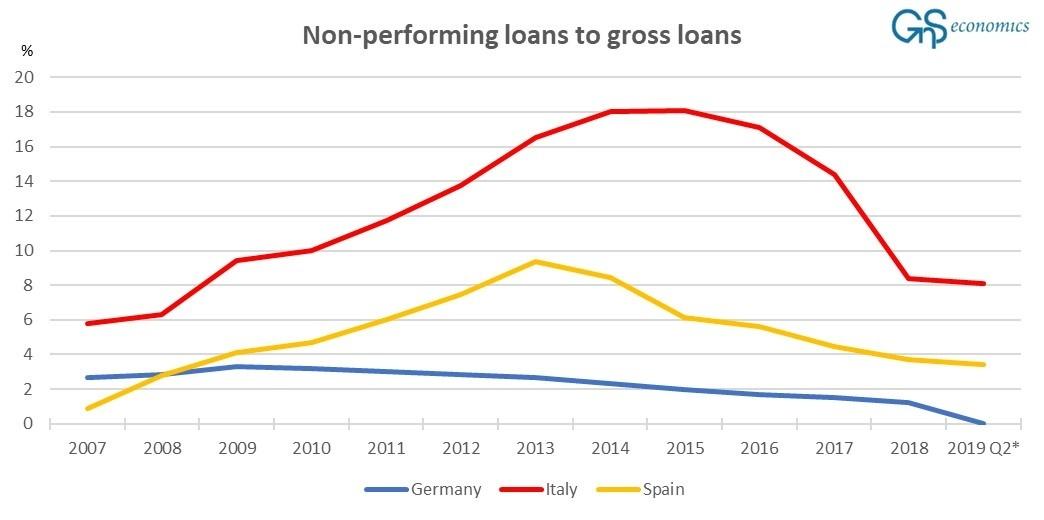

Now, due to the recession, which started in the Eurozone in Q4 2019, and the severe economic impact of the coronavirus, the non-performing (bad) loans of Italian and Spanish banks are expected to skyrocket from a level that was already considerably higher than pre-GFC (see Figure 2).

Figure 2. The share of non-performing loans to gross loans. Source: GnS Economics, IMF

There is practically no way that the Italian and—likely—Spanish banks can remain standing against the hurricane-force of these accumulated economic losses.

The onset of a European banking crisis is close, and it should worry us all.