Congress has proposeda $25 billion bailout for the U.S. Postal Service (USPS) as part of the latest COVID-19 stimulus bill, but it’s unlikely that any amount of cash will be enough to stabilize the agency’s finances. Postmaster General Megan Brennan told the House Oversight Committee in April that the postal service stands to lose $13 billion this year. That’s an acceleration of an ongoing trend, not a new problem created by the coronavirus pandemic; the post office has lost $69 billion since 2007.

In May, a report from the Government Accountability Office called the agency’s business model “not financially sustainable”—a conclusion it had reached before the impact of the coronavirus was factored in. The report called for Congress to make changes to “critical foundational elements” of how USPS operates. In other words, COVID-19 might be an easy scapegoat to justify a federal bailout, but the pandemic is not the main problem, and a bailout would not be a permanent solution.

Thanks to congressional mandates, the USPS has been unable to adapt to a changing marketplace. First-class mail has declined 44 percent since 2006, but Congress has rejected proposals that would free the postal service to operate more like a business, instead requiring the agency to deliver mail everywhere six days per week regardless of cost efficiency.

Second, like many government entities, the USPS has overpromised and undersaved when it comes to employee retirement benefits. At the end of 2019, the postal workers’ pension fund had $50 billion in unfunded liabilities—the gap between what the fund expects to owe beneficiaries over the long term and the revenue it expects to collect from paychecks and investment earnings. Meanwhile, the fund that covers health care expenses for retired postal workers is facing a $69 billion unfunded liability. The pandemic’s economic impact has made both situations worse.

President Donald Trump has called for the USPS to raise prices, particularly on packages. He believes the agency is giving a free ride to Amazon and other online retailers. USPS has already tried that—the shipping price for the agency’s largest flat-rate box has gone from $14.50 in 2010 to $21.10 this year, for example—but price increases are limited by market conditions (since the USPS does not have a monopoly on package shipments) and congressional mandates.

Rather than more bailouts or slightly different mandates, Congress should set the postal service free. Privatizing it in whole or in part would allow the USPS to make smart changes to its business model while guaranteeing that taxpayers aren’t on the hook for yet another massive bailout in a year or two.

from Latest – Reason.com https://ift.tt/2PYPYzF

via IFTTT

Congress has proposeda $25 billion bailout for the U.S. Postal Service (USPS) as part of the latest COVID-19 stimulus bill, but it’s unlikely that any amount of cash will be enough to stabilize the agency’s finances. Postmaster General Megan Brennan told the House Oversight Committee in April that the postal service stands to lose $13 billion this year. That’s an acceleration of an ongoing trend, not a new problem created by the coronavirus pandemic; the post office has lost $69 billion since 2007.

In May, a report from the Government Accountability Office called the agency’s business model “not financially sustainable”—a conclusion it had reached before the impact of the coronavirus was factored in. The report called for Congress to make changes to “critical foundational elements” of how USPS operates. In other words, COVID-19 might be an easy scapegoat to justify a federal bailout, but the pandemic is not the main problem, and a bailout would not be a permanent solution.

Thanks to congressional mandates, the USPS has been unable to adapt to a changing marketplace. First-class mail has declined 44 percent since 2006, but Congress has rejected proposals that would free the postal service to operate more like a business, instead requiring the agency to deliver mail everywhere six days per week regardless of cost efficiency.

Second, like many government entities, the USPS has overpromised and undersaved when it comes to employee retirement benefits. At the end of 2019, the postal workers’ pension fund had $50 billion in unfunded liabilities—the gap between what the fund expects to owe beneficiaries over the long term and the revenue it expects to collect from paychecks and investment earnings. Meanwhile, the fund that covers health care expenses for retired postal workers is facing a $69 billion unfunded liability. The pandemic’s economic impact has made both situations worse.

President Donald Trump has called for the USPS to raise prices, particularly on packages. He believes the agency is giving a free ride to Amazon and other online retailers. USPS has already tried that—the shipping price for the agency’s largest flat-rate box has gone from $14.50 in 2010 to $21.10 this year, for example—but price increases are limited by market conditions (since the USPS does not have a monopoly on package shipments) and congressional mandates.

Rather than more bailouts or slightly different mandates, Congress should set the postal service free. Privatizing it in whole or in part would allow the USPS to make smart changes to its business model while guaranteeing that taxpayers aren’t on the hook for yet another massive bailout in a year or two.

from Latest – Reason.com https://ift.tt/2PYPYzF

via IFTTT

Shares of Alibaba trading on the NYSE during Monday’s premarket session slumped 120bps to $251 following President Trump’s comments on Saturday about exerting more pressure on Chinese-owned companies.

During the Saturday press conference in Bedminster, New Jersey, the president said he would increase pressure on Chinese-owned companies, such as Alibaba, along with a move to ban TikTok.

“Well, we’re looking at other things, yes,” President Trump said without providing additional details.

Reuters explained how Trump has been heaping more pressure on Chinese-owned tech companies as ByteDance supplants Huawei as President Trump’s Chinese corporate villain No. 1.

“Trump has been piling pressure on Chinese-owned companies, such as by vowing to ban short-video app TikTok from the United States. The United States ordered its Chinese owner ByteDance on Friday to divest the U.S. operations of TikTok within 90 days, the latest effort to ramp up pressure over concerns about the safety of the personal data it handles,” Reuters said.

U.S.-China tensions are mounting ahead of the U.S. presidential elections this fall. President Trump has made his tough stance on China a central theme of his presidency.

via ZeroHedge News https://ift.tt/3aAGVyf Tyler Durden

In The “Everything Rally”, ‘Diversification’ Is The New Four-Letter-Word Tyler Durden

Mon, 08/17/2020 – 05:30

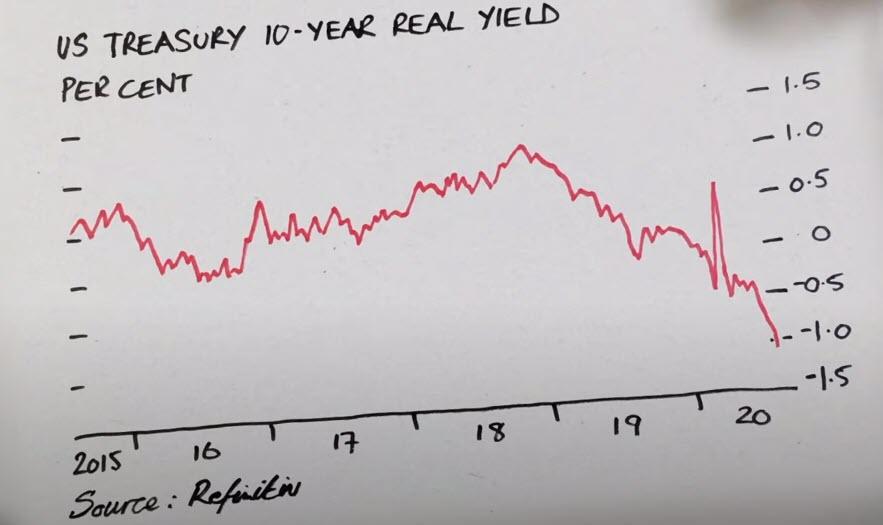

“The price of just about every financial asset is heading up… and they are heading up in unison,” is the ominous warning that The FT’s Robert Armstrong begins the brief clip below as he

From stocks to bonds to commodities – everything is levitating on a bed of ultra-low (if not negative) rates and as more excess liquidity than the world has ever seen.

This “sychronized exuberance” is being driven by a collapse of real yields into negative territory for the first time…

Or, as Armstrong notes “money is free… and under those conditions, no asset price can be too high!” and this low or negative real rate environment is expected (by the market) to be around for a really, really long time.

But Armstrong’s ultimate warning comes as he point out that “what is especially worrisome now is that in a downturn, it used to be that investors’ best defense was diversification… which means that when the next downturn comes, there will be no place to hide!“

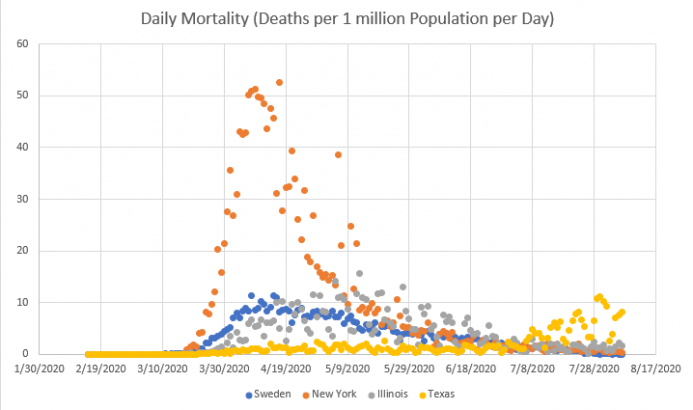

Figure 1 illustrates the daily mortality attributed to covid-19 in Sweden, New York, Illinois, and Texas. The figure plots the daily number of deaths per million population. This figure illustrates the rise and fall of deaths from covid-19 in four different policy environments. The data were obtained from Worldometer.

Sweden: The Control Group

Sweden (blue dots) has served as a control group to compare policies intended to decrease deaths from covid-19. Sweden has been unfairly criticized for its policy despite having an outcome more favorable than places with authoritarian lockdown policies. Sweden did not close its schools. Other than stopping gatherings of more than fifty people, the Swedish government left decisions of closing businesses, using masks, and social distancing to the Swedish people. The government encouraged the use of masks and social distancing, but there were no requirements and there were no penalties for those who declined to follow the advice. Mortality attributed to covid-19 hit a peak value of 11.38 deaths per day per million population on April 8, 2020. This mortality was matched on April 15, and mortality has decreased since then. Daily mortality has been less than one death per day per million population for the previous eighteen days. Cases are very low. For all practical purposes, the covid-19 epidemic is over in Sweden. Almost certainly herd immunity has been achieved in Sweden irrespective of any antibody test results. Testing is usually only for IgG antibody and the herd can become immune via IgA antibody or cellular mechanisms that are not detected by the usual testing. Whether covid-19 will reappear this next fall or winter remains to be seen.

New York: Locking the Barn Door Shut after the Horse Has Already Left

New York (brown dots) has been a catastrophe. On March 20, 2020, a full lockdown was implemented. Nonessential businesses were ordered to close. Workers in nonessential businesses were ordered to work only from home. Pharmacies, grocery stores, liquor stores, and wine stores were deemed to be essential and allowed to remain open. Restaurants and bars could only deliver to homes. In addition to the lockdown, nursing homes were ordered on March 25, 2020, to accept patients positive for the covid-19 virus in transfer from hospitals. On May 10, this order was changed such that patients had to test negative for the virus before being transferred to nursing homes, but the damage had already been done. By April 7, 2020, within three weeks of the nursing home order, a daily mortality of over fifty deaths per day per million population had been reached. This daily mortality rate was almost five times the peak rate observed in Sweden, where no lockdown was implemented.

The New York policy assumed that all human interactions carry the same risk of death by covid-19. The New York data clearly shows that interactions among young and healthy people have a much different risk than interactions between the young and elderly and interactions among the elderly. By facilitating the transmission of the virus from hospitals to nursing homes, the rate of spread within the elderly population was maximized, and any possible benefit from lockdown of the young and healthy population was rendered moot. The general population was kept locked down after the virus had been broadly disseminated among the elderly population. The decline of deaths from the peak levels in New York, with its harsh lockdown, has followed roughly the same time course as what has been observed in Sweden without any lockdown. It is unclear whether the lockdown interfered with herd immunity or not. This will not be known until after the economy and schools are completely reopened for at least a month.

Illinois: A Flattened Curve Led to More Deaths

Illinois (gray dots) has more subtle differences from Sweden than does New York. Illinois also implemented a harsh lockdown on March 20, 2020. There was no nursing home order as in New York. The daily mortality rate increased more slowly than it did in New York and Sweden, reaching a peak of over fifteen deaths per day per million population on May 17, 2020. The daily mortality has declined more slowly than it did in New York and Sweden, and it remains significantly higher than the rates in those places. The most likely explanation for the Illinois data is that the lockdown did indeed slow the rate of transmission among the young and healthy but also allowed a longer time for transmission from young people to elderly people. The lockdown appears to have made more deaths from covid-19 in Illinois than would have occurred without it. Almost certainly herd immunity has not been achieved and will not be achieved until the schools and economy are reopened.

Texas: The Ox Is Slow, but the Earth Is Patient

Texas (gold dots) had very few deaths following a less harsh lockdown than was implemented in New York and Illinois. Nonessential businesses were closed on March 31. Outdoor activities were permitted. Social distancing was advised but not required. Governor Abbott was criticized for not squeezing hard enough, but predictions that Texas health care would be overwhelmed by late April failed to materialize. Texas appeared to be a success story, with a much lower mortality, and the state began a phased reopening of the economy on May 1, 2020. By late June, however, cases of covid-19 were increasing and the daily mortality rate was creeping up. The general reopening was paused, and some relaxations of measures were rescinded on June 26, 2020. The Texas daily mortality rate hit a peak of over ten deaths per day per million population on July 31, 2020. The Texas mortality peak is almost bad as the peak rate seen in Sweden, but Texas still has a largely closed economy. Texans are debating whether schools should be reopened or not. Sweden does not have to worry about its schools, because it never closed its schools. Texas will eventually have to reopen its schools and economy. It would appear that covid-19 deaths were deferred rather than prevented by the lockdown. Although the overall covid-19 mortality is lower in Texas (293 deaths per million population) than in Sweden (570), the current daily mortality in Texas is much higher than in Sweden, so covid-19 mortality in Texas may catch up to Sweden over the next 30–60 days. Furthermore, the situation in Texas will likely get worse when the schools and economy are reopened, as they eventually must be. Like the ox and the Earth, the lockdown slowed the transmission of the virus among the young and healthy, but the virus appears to be very patient and will spread when it is able to.

Conclusions

The data suggest that lockdowns have not prevented any deaths from covid-19. At best, lockdowns have deferred death for a short time, but they cannot possibly be continued for the long term. It seems likely that one will not have to even compare economic deprivation with loss of life, as the final death toll following authoritarian lockdowns will most likely exceed the deaths from letting people choose how to manage their own risk. After taking the unprecedented economic depression into account, history will likely judge these lockdowns to be the greatest policy error of this generation. Covid-19 is not going to be defeated; we will have to learn how to coexist with it. The only way we can learn how best to cope with covid-19 is to let individuals manage their own risk, observe the outcomes, and learn from mistakes. The world owes a great debt to Sweden for setting an example that the rest of us can follow.

via ZeroHedge News https://ift.tt/31ZJ8iT Tyler Durden

When a mob of radical Hindus attacked several Christian families in the Latehar district of Jharkand state in India, the Christians went to the police. But instead of arresting the attackers, cops told the Christians they should either convert to Hinduism or move. The Evangelical Fellowship of India reports there were 135 cases of persecution against Christians in India in the first half of 2020.

from Latest – Reason.com https://ift.tt/3audzSl

via IFTTT

When a mob of radical Hindus attacked several Christian families in the Latehar district of Jharkand state in India, the Christians went to the police. But instead of arresting the attackers, cops told the Christians they should either convert to Hinduism or move. The Evangelical Fellowship of India reports there were 135 cases of persecution against Christians in India in the first half of 2020.

from Latest – Reason.com https://ift.tt/3audzSl

via IFTTT

Banker Bonus Cap “Curbs” Excessive Risk-Taking Tyler Durden

Mon, 08/17/2020 – 04:15

The Bank of England (BoE) published a new study Friday (Aug. 14) to examine whether a cap on banker bonuses rolled out a decade ago post-financial crisis can thwart excessive risk-taking.

The working paper titled “Does bonus cap curb risk-taking? An experimental study of relative performance pay and bonus regulation” found that higher risk-taking was associated when bonuses were linked to how well an individual, or team, preformed.

“Despite the modest stakes offered to the participants, our study demonstrates that bonus schemes may affect risk choices, and certain restrictions on bonus payments might reduce risktaking,” said BoE staff.

The survey of 253 participants found “in the absence of relative performance pay, bonus cap, and malus reduced risk-taking. With relative performance pay, the risk-mitigating effects of bonus cap and malus were significantly weakened; but participants took less risk when the bonus was made conditional on their team avoiding a loss.”

“This finding supports the view that some appropriately designed restrictions on bonus payments could mitigate excessive risk-taking. However, our findings suggest that commonly used bonus practices – such as relative performance benchmarking – might undermine the risk-mitigating effects of regulatory bonus restrictions,” said BoE staff.

The publication of the study comes as bankers in London are hoping the European Union’s cap on banker bonuses can be discarded now the country has exited the EU, noted Reuters.

And while UK bankers push for higher bonuses this year, Wall Street is about to get “shafted” come bonus season despite the Fed pumping an endless flood of liquidity into markets.

via ZeroHedge News https://ift.tt/31Tg5O0 Tyler Durden

The ECB balance sheet has risen to 53.9% of GDP in July 2020. This compares to a 32% of the Federal Reserve and 33% of the Bank of England. This means a 1.78 trillion euro increase year-to-date. Furthermore, excess liquidity has soared to 2.9 trillion euro, a 1.2 trillion increase since January. Added to this unprecedented monetary stimulus, the Eurozone has included a record-high 10% of GDP in various fiscal stimulus programmes. None of it has prevented the economy from showing signs of slowing down in August.

After a strong bounce in May and June, coming from the re-opening of most economies and the base effect, high frequency data compiled by Bloomberg Economics shows an evident slowdown in July and August. All economists that follow the eurozone economy are warning about the worrying weakening of leading indicators. The OECD has also published its July 2020 Leading Indicator Index which shows that economies like Spain are not just showing signs of weaker growth, but contraction. Italy continues to improve but at a slow pace, while France and Germany post declining growth levels.

The reason is evident. All the Eurozone monster stimulus is focused on perpetuating bloated government budgets and incentivising non-economic return or subsidized spending. The entire European Recovery Fund is clearly aimed at promoting white elephants disguised as green projects, but what is more concerning is that the Eurozone green deal includes more taxes and measures to prevent demand growth than productivity-enhancing plans.

This lesson should have been learnt in 2009. The European Union launched its massive Growth and Jobs Plan, which rose to more than 1.5% of the EU GDP, and the economy did not improve, while more than 4.5 million jobs were lost.

The problem of these massive stimulus is that they benefit the wrong parts of the economy. Current government spending in entitlements and subsidies, massive deficits and the corporations that take advantage of the massive private bond purchases and liquidity injections are the large multinationals and national champions that did not have any problem accessing markets in the past.

While the eurozone is raising “environmental” taxes to citizens and promoting subsidized spending in “the new green deal”, the biggest beneficiaries of the ECB corporate bond purchase programme are large automotive companies, oil and gas multinationals and big multi-utilities. The ECB has bought bonds from Shell, Eni, Repsol, OMV, Total, Siemens, Daimler AG, BMW, Volkswagen, Renault etc. None of these companies had any difficulty accessing capital markets or issuing debt at low rates, and their bonds could not be categorized in any way as cheap considering the yields and spreads. Most of these companies have established and mature businesses in sectors where overcapacity and margin challenges existed way before the previous and current crisis, so they will not increase hiring or capital spending due to the monetary stimulus.

Meanwhile, thousands of start-ups and small businesses with no access to credit because they have no hard assets are collapsing every month. The monster credit support coming from the transmission mechanism of monetary policy is hoarded by governments and multinationals. It is a massive incentive to overspend and malinvest. Governments feel happy adding more current spending and entitlements with no real economic return and traditional multinationals that were in slowdown phase years ago are zombified by low rates.

The ECB and Eurozone stimulus plans end up as massive subsidies to low productivity with collateral damages to high productivity sectors in the shape of higher taxes.

The reader may think that the same can be said about the United States and what the Federal Reserve does. Yes, to a certain extent. The main -and vital- difference is that the United States monetary policy transmission mechanism does not depend on the commercial bank channel. Less than 15% of the United States’ real economy is financed by the banking sector thanks to a diversified and flexible private credit system. In the Eurozone it is more than 80%, similar to Japan.

This path to long-term stagnation should serve as a reminder for the United States, again, of why it is not advisable to follow the eurozone policies. The results are invariably disastrous.

via ZeroHedge News https://ift.tt/3iKphuQ Tyler Durden

Countries On The UK’s “High Risk” Travel List Tyler Durden

Mon, 08/17/2020 – 02:45

In a blow for many UK holidaymakers, France was added to the list of ‘high risk’ countries from 4am on Saturday 15 August. The announcement, made late last week, means that all but essential travel is now advised against and returning travellers will have to quarantine for 14 days.

As Statista’s Martin Armstrong notes, France had previously been on the UK’s list of ‘travel corridors’, allowing unrestricted travel, but is now joined by the Netherlands, Malta, Monaco, the Turks & Caicos islands, and Aruba as one of the latest places to have this exemption removed.