From an opinion by Judge Katherine Polk Failla in Doe v. Indyke (S.D.N.Y.), decided in late June, but just mentioned in the Westlaw Bulletin:

To begin, Defendants seek dismissal of Plaintiff’s punitive damages claim on the ground that New York law bars such claims in personal injury suits against representatives of a decedent’s estate. The statute in question, § 11-3.2(a)(1) of New York’s Estates, Powers and Trusts Law (“EPTL”), provides:

“No cause of action for injury to person or property is lost because of the death of the person liable for the injury. For any injury, an action may be brought or continued against the personal representative of the decedent, but punitive damages shall not be awarded nor penalties adjudged in any such action brought to recover damages for personal injury.”

As three recent cases in this District, presenting similar claims against the same Defendants, have recognized, this provision clearly prohibits the award of punitive damages in the situation at hand. See Mary Doe v. Indyke, 2020 WL 2036707 (S.D.N.Y. Apr. 28, 2020); Lisa Doe v. Indyke, 2020 WL 3073219 (S.D.N.Y. June 9, 2020); Doe 15 v. Indyke, 2020 WL 2086194 (S.D.N.Y. Apr. 30, 2020) (“New Mexico common law as announced by the state supreme court, like EPTL § 11-3.2(a)(1), bars punitive damages in a personal injury action against a tortfeasor’s estate.”). Both federal courts addressing constitutional-tort claims under New York law, and state courts in personal injury actions governed by New York law, have concluded similarly. See Mary Doe, 2020 WL 2036707, at *2 (collecting New York federal and state cases).

This position is also reflected in the majority of United States jurisdictions, as the Restatement (Second) of Torts indicates. See Restatement (Second) of Torts § 908 cmt. a (Am. Law Inst. 1979) (“Punitive damages are not awarded against the representatives of a deceased tortfeasor.”). The common justification for the majority rule is that “punishment and deterrence—the recognized bases for imposing punitive damages on a tortfeasor—are not advanced by imposing punitive damages on his or her estate.” Mary Doe, 2020 WL 2036707, at *3; see also Blissett v. Eisensmidt, 940 F. Supp. 449, 457 (N.D.N.Y. 1996) (brackets and citation omitted) (“There is a strong policy against the assessment of punitive damages against an estate on account of wrongful conduct of the decedent.”).

The court also held, consistently with past decisions, that New York law applied, because

Plaintiff was domiciled in New York. All of the alleged torts took place in the home Epstein maintained in New York. Further, Plaintiff chose to sue in New York, where her causes of action are timely pursuant to the New York Child Victims Act…. These facts, taken together, demonstrate that New York’s interest in applying its punitive damages rules to this case outweighs the USVI’s interest, which exists only because of Epstein’s decision to probate his estate there. If anything, it is the USVI, and not New York, that has a “merely fortuitous relationship with the case,” minimizing its interest in governing punitive damages.

(The court also concluded that Virgin Islands law would likely also preclude punitive damages against dead tortfeasors, but in any event New York law definitely precluded such damages, and it was New York law that applied.)

from Latest – Reason.com https://ift.tt/3bxpyyK

via IFTTT

Kamala Gets Conspiratorial: Says Russians May Cost Biden Election, Won’t Trust Trump On COVID-19 Vaccine Tyler Durden

Sun, 09/06/2020 – 14:25

Kamala Harris has gone full Schiff – suggesting in an interview that she thinks Russian interference could cost Joe Biden the election.

Speaking with CNN, Harris said that Russia will be at the “front of the line” when it comes to election interference, according to the Washington Times.

“Could it cost you the White House?” asked CNN‘s Dana Bash.

“Theoretically of course,” replied Harris. “Yes.”

Harris, providing no evidence, continued, “We have classic voter suppression, we have what happened in 2016, which is foreign interference, we have a president who is trying to convince the American people not to believe in the integrity of our election system and compromise their belief that their vote might actually count.”

“These things are all at play and I am very realistic, Joe is very realistic, that until we can win…that there will be many obstacles that people are intentionally placing in front of Americans’ ability to vote.”

Sen. Kamala Harris (D-CA): “Theoretically, of course” Russian interference could cost Biden the election pic.twitter.com/uIA54jIOhz

In July, Harris said without evidence that she was being targeted on Twitter by “Russian bots” (she also blamed said ‘bots’ for whipping up national outrage over Colin Kaepernick kneeling during the National Anthem).

Going further down the rabbit hole, Harris also said that she wouldn’t trust President Trump when it comes to a COVID-19 vaccine.

When asked if she would personally take any vaccine approved before November, she replied: “I will say that I would not trust Donald Trump and it would have to be a credible source of information that talks about the efficacy and the reliability of whatever he’s talking about. I will not take his word for it.”

She then suggested that Trump would somehow interfere with medical experts and overrule them.

“They’ll be muzzled, they’ll be suppressed, they will be sidelined,” Harris said – parroting a Biden talking point. “Because he’s looking at an election coming up in less than 60 days and he’s grasping to get whatever he can to pretend he has been a leader on this issue when he is not.”

Meanwhile, Dr. Anthony Fauci – Trump’s top COVID-19 adviser, says that the president has “never” gone against science-based advice he’s provided.

Dr. Fauci says President Trump has “never” gone against the science-based advice he provided.

“When he suggests, ‘why don’t we do this?’ And I say, ‘no, that’s really not a good idea from a scientific standpoint’ – he has never overruled me.” pic.twitter.com/2VLwgkR7K5

— Trump War Room – Text TRUMP to 88022 (@TrumpWarRoom) March 26, 2020

Perhaps Russia simply hacked Biden’s brain?

via ZeroHedge News https://ift.tt/3bJz2Y9 Tyler Durden

UK Reports Most New COVID-19 Cases Since May; India Sees New Record Surge: Live Updates Tyler Durden

Sun, 09/06/2020 – 14:00

Summary:

India reports new global recod

UK sees highest case tally since May

Jakarta graveyard overflowing with COVID dead

France expands COVID warnings

Victoria extends lockdown

* * *

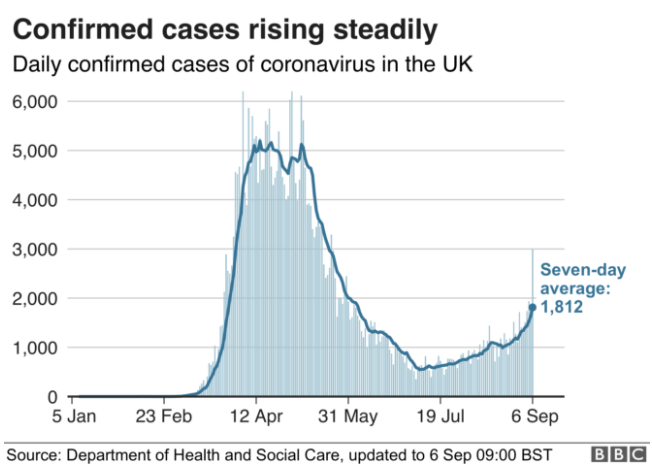

While the holiday weekend leads to a drop off in activity in the US, including a decline in COVID-19 testing rates, the UK just reported the highest number of new cases in a single day since May (the latest sign of a coronavirus comeback in Europe) while India cemented a new global daily record after reporting more than 90k new cases.

Britain reported nearly 3,000 new cases, – 2,988 to be exact – on Sunday, its largest daily tally since May 23. The country also saw 2 new deaths, bringing Britain’s death toll to 41,551, and its confirmed case total to 347,152.

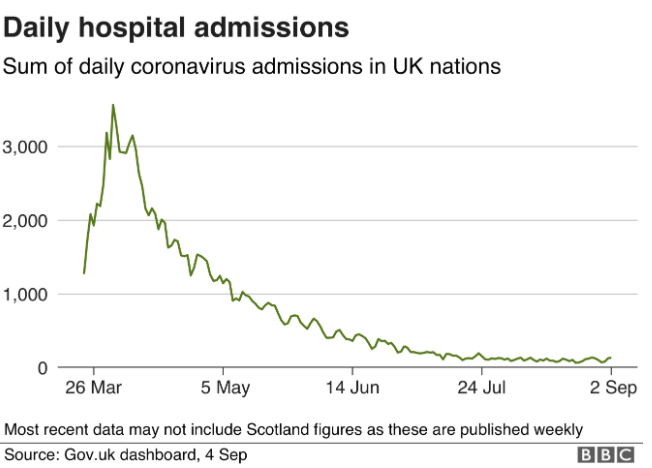

A day earlier, the UK reported just 1,813 cases. Daily hospitalizations, meanwhile, have hardly budged from their lows.

Elsewhere in Europe, France placed seven more departments covering major cities including Lille, Strasbourg and Dijon on high alert as the country’s latest outbreaks accelerate. Of France’s 101 mainaland and overseas “departments”, 28 are now considered “red zones.” This comes amid a surge in new cases seen over the past week, but especially over the past 2 days.

On Sunday, India topped its own world record when it reported 90,632 daily new cases, the largest daily tally reported anywhere in the world. The new cases brought India’s total confirmed caseload to 4.11 million.

Meanwhile, the number of deaths in the world’s second-most-populous country rose by 1,065 to 70,626.

India is set to pass Brazil on Monday as the second-most affected country by total infections. After that, it will be behind only the US in terms of total cases.

While a recent testing campaign has been blamed for the country’s record-beating numbers, testing isn’t the only issue. India is in second place worldwide when it comes to overall tests administered, with 47,831,145, behind the US, with 86,763,797. But its rate is 35,322 per million compared with the global average of 69,512, the US with 261,844 and Brazil with 67,696.

Despite fervent protests that led to hundreds of arrests the other day, Australia’s coronavirus hotspot state of Victoria on Sunday extended its “hard” lockdown once again, adding another two weeks, which extends it until the end of September as infection rates have declined more slowly than hoped.

State Premier Daniel Andrews on Sunday extended the hard lockdown, in place since August 2, to September 28 with a slight relaxation, and explained how restrictions would gradually decline over the coming two months. The extension comes after Australia slumped into its first recession in decades.

Victoria, Australia’s second-most populous state, has been the epicentre of a second wave of the novel coronavirus, now accounting for roughly 75% of the country’s 26,282 cases and 90% of its 753 deaths.

The state on Sunday reported 63 new COVID-19 infections and five deaths, down from a peak of 725 new cases reported on Aug. 5.

Finally, as Philippines and Indonesia cement their status as the worst outbreaks in Southeast Asia, Al Jazeera reports that a cemetery in the Indonesian capital of Jakarta is reportedly running out of space as the number of deaths linked to the coronavirus continues to rise. Unfortunately, in swampy Jakarta, using portable refrigeration trucks might not be feasible, like it was in New York. Indonesia has reported roughly 190,000 cases, and roughly 8,000 dead.

via ZeroHedge News https://ift.tt/2EUIBHH Tyler Durden

Connecting The Dots: How SoftBank Made Billions Using The Biggest “Gamma Squeeze” In History Tyler Durden

Sun, 09/06/2020 – 13:35

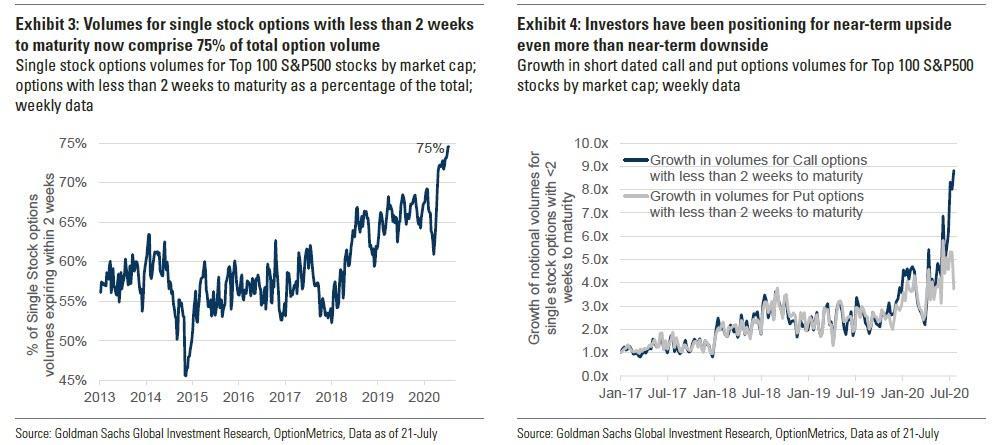

It was back in July when we first reported that Goldman had observed a “historic inversion” in the stock market: for the first time ever, the average daily value of options traded has exceeded shares for the first time, with July single stock options volumes hitting 114% of shares volumes.

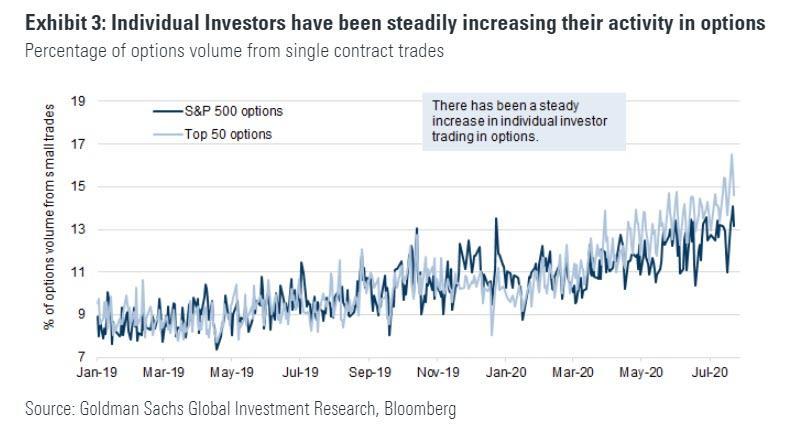

This followed a May report in which we discussed “how retail investors took over the stock market”, pointing out the “recent surge in options trading – which has far more impact on market flows due to embedded leverage” and cited Goldman data which showed that “individual investor active trading is playing an increased role in market volatility, particularly in select stocks. In the shares market, 2.3% of all volume is made up of trades for $2,000 or less. The increase in small trades has been even more notable in the options market, where 13% of all trades are for 1 contract.”

We also pointed out that “a significant portion of this increase has been driven by higher volumes in short dated contracts, as investors are literally using massive leverage to wager on near-term momentum moves such as those often highlighted OTM calls traded in Tesla stock.”

The last clue that an entire generation of investors were flooding into options (read calls) was the surge in individual investor option activity in both the top 50 and the top 500 US names, which has continued a steady climb since the start of the year.

To be sure, this option frenzy was a goldmine for retail brokerages such as Robinhood, Schwab and Etrade, which reported options trading activity surging 129% YTD (up 35% from June levels), which helped explain why various HFT outfits are paying so much to frontrun Robinhood option trades.

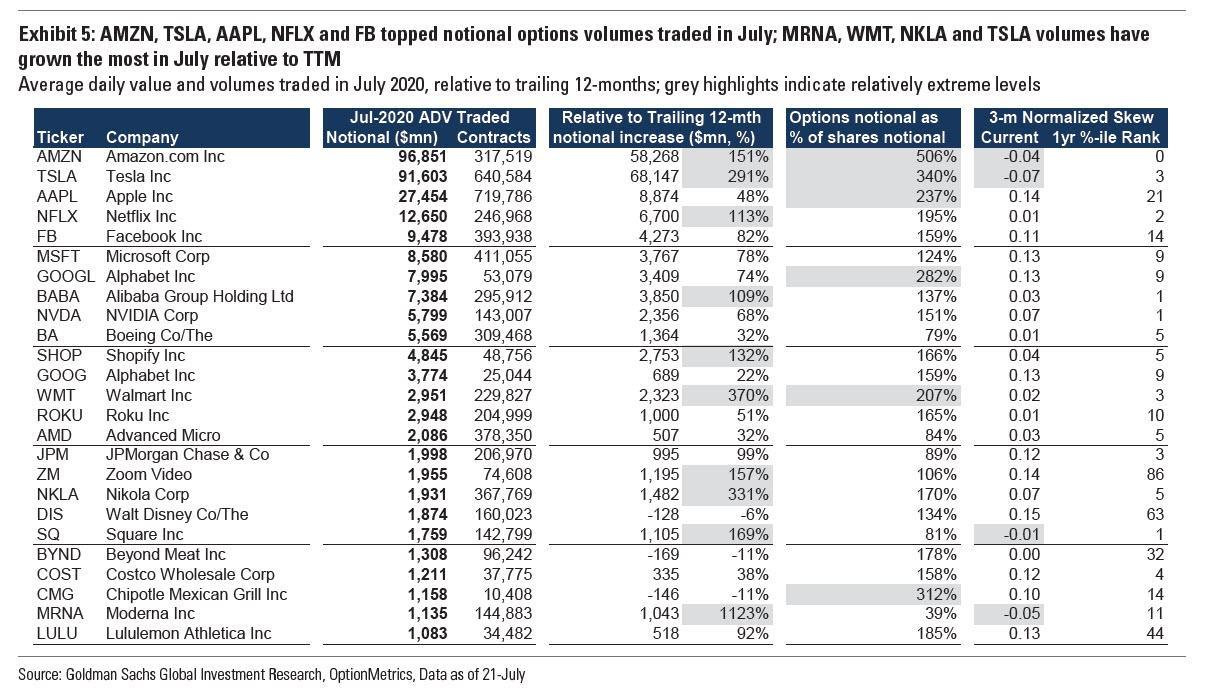

Finally, we also pointed out where the option trading footprint was largest, and not surprisingly we showed that options volumes had been driven higher by an increase in trading in many of the large market cap names. AMZN, TSLA, AAPL, NFLX and FB had the highest volumes in July. Among the top 25 underliers with high notional volumes, MRNA, WMT, NKLA and TSLA saw the biggest jump relative to the prior 12-months.

Also of note, bullish sentiment in a number of names as indicated by options market skew, was at extremely high levels. Three-month normalized put-call skew in AMZN, TSLA, SQ and MRNA had declined to below 0 as of two months ago, a striking development because as Goldman notes, “negative skew is a relatively rare statistic for large cap names such as AMZN (where three month skew is currently at all-time lows), implying crowding in long AMZN calls.”

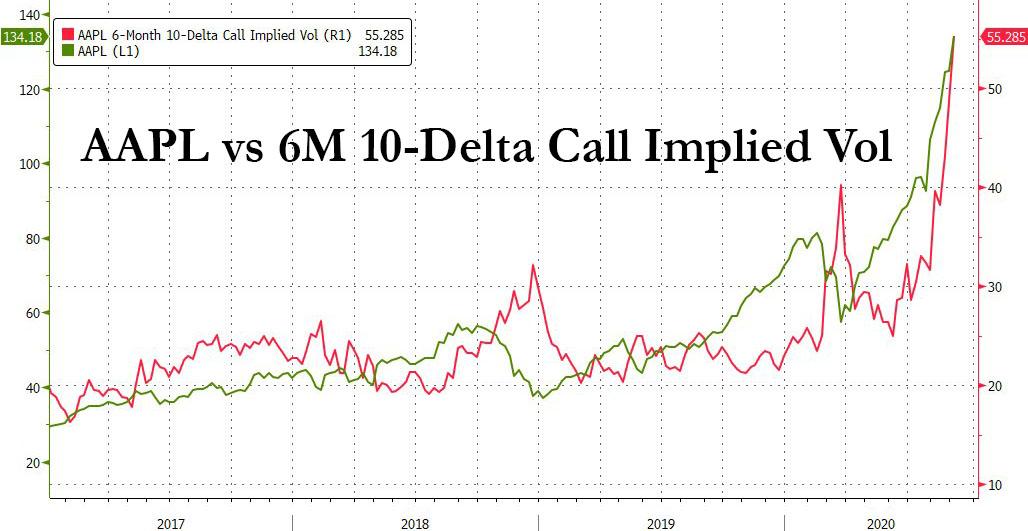

Fast forward to last week when we first showed that these trends had accelerated to an unprecedented degree, and the implied vol among some of the giga-cap names had exploded to insane levels even as the stock was trading at all time highs with a market cap of $2.2 trillion…

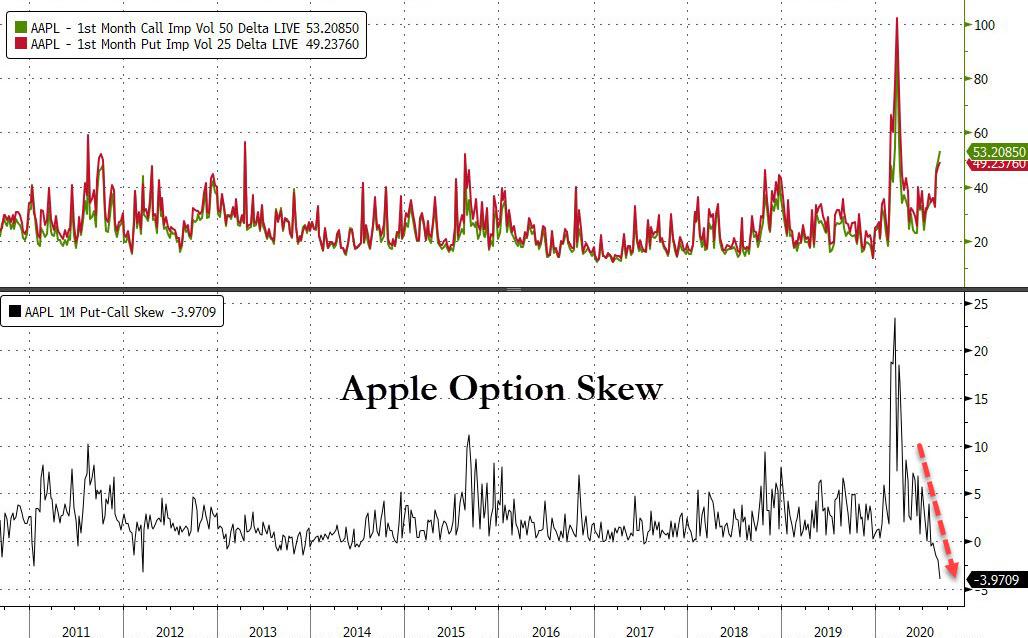

… while the plunge in option skew, first highlighted in July, had also hit unprecedented levels.

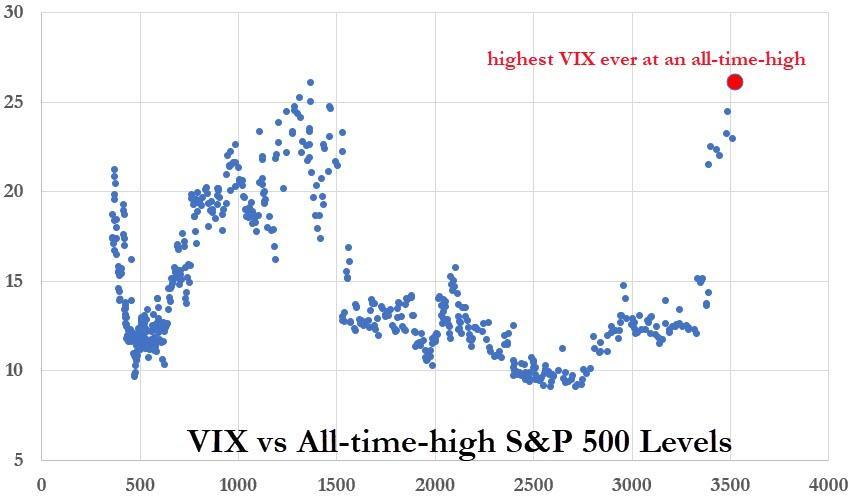

These bizarre trends, where one or more players where furiously buying calls and pushing both the implied vol and gamma (in both single stocks and the broader market) ever higher even while dealers were caught short gamma and were forced to chase stock price to obscene levels, creating a feedback loop where the more calls were bought, the higher the underlying stock price surged, leading to even more call buying and the paradox of a record high vix at an all time high in the S&P500 (in fact the last time we had observed such a confluence was the day the dot com bubble burst)…

… led us to explain last Wednesday that “an epic battle was raging beneath the market surface” where as Nomura’s Charlie McElligott said that “street-wide, Dealers are short Gamma / short Calls off the back of the MASSIVE upside premium buyer (as in BILLIONS spent) who has been in the market over the past month or so in a number of mega-cap single-name Tech cos.”

Putting it all together, we said that “a combination of market euphoria, free options trading, and most importantly, few market-makers have sparked the fire” indicating that a key player in all this was indeed retail investors. We then added that it also meant that “a few large funds understood this and have added fuel to the fire by pushing implied higher and higher and putting further pressure on the likes of Citadel and Goldman. With this process helping drive names like Apple and Tesla, this also makes sense why Breadth has been so terrible.”

The punchline, for all those who had been looking at the market action in recent weeks in stunned silence, was that “while most of the market is fading lower we are seeing a battle between a few big hedge funds and banks who are getting shorter and shorter gamma.“

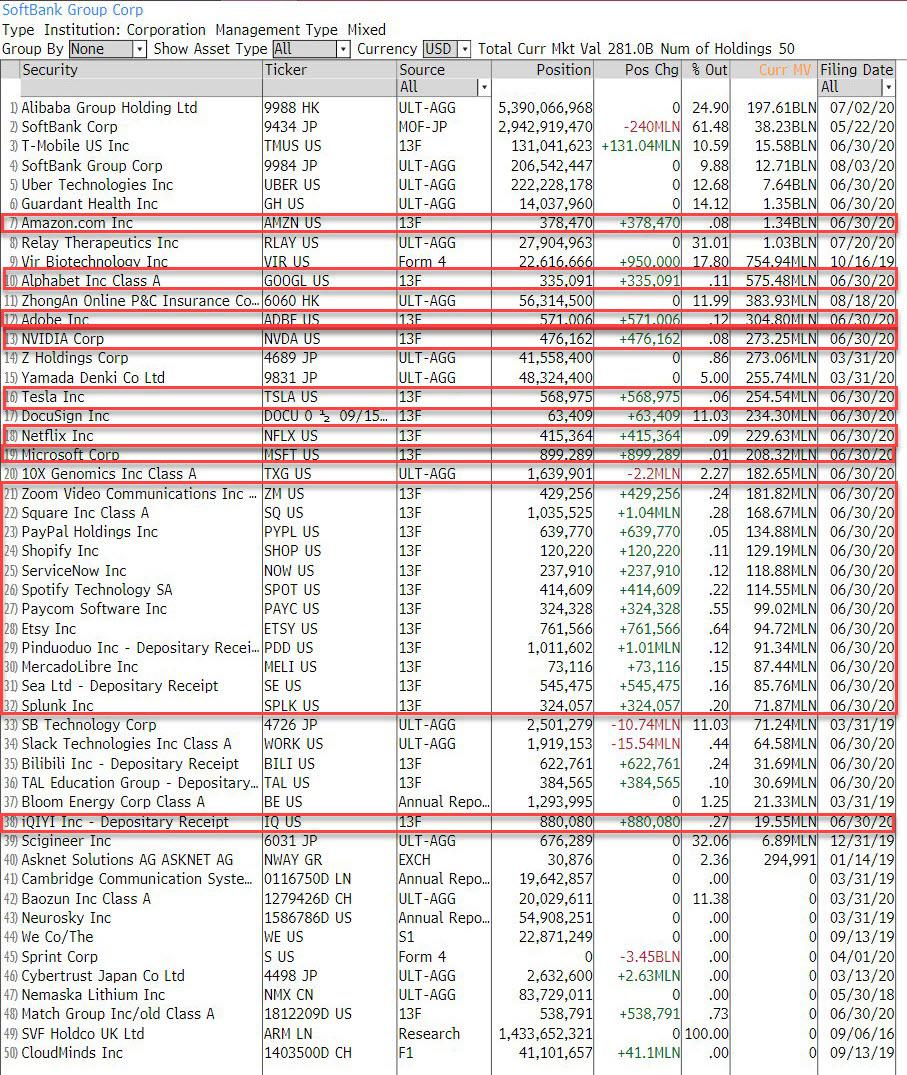

It all came into place on Thursday when we first reported that contrary to expectations that the furious melt up of July and August was solely due to a buying frenzy among retail speculators, the identity of the “mystery marketwide call buyer” – or “nasdaq whale” as he was later dubbed – was none other than SoftBank and its founder, Masa Son. This is what we said:

It is hardly unreasonable to imagine SoftBank, the “brains” behind such catastrophic investments as WeWork, WireFraud WireCard, and countless other failed “unicorns” would desperately try to Volkswagen not just a handful of tech names, but the entire market in the process. After all, Masa Son is desperate to deflect attention from the fact that as we put it last October, ” SoftBank is the Bubble Era’s “Short Of The Century.” And if there is one thing that can salvage the Japanese VC titan’s reputation it is a second tech bubble which blows out the valuation of his countless (otherwise worthless) investments…

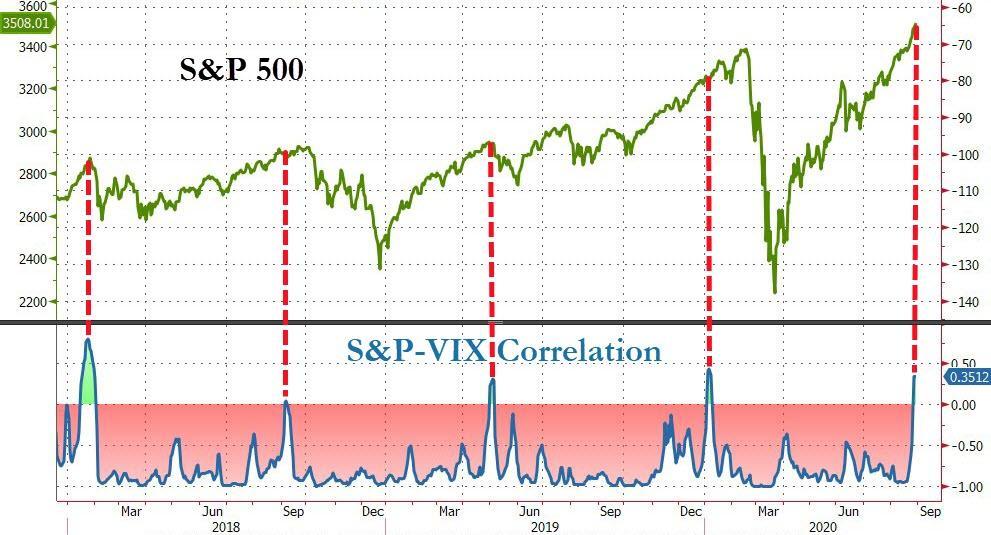

One day later both the FT and the WSJ confirmed that it was indeed SoftBank which was using a “positive gamma” strategy of buying up single name stocks, which it then propelled higher by buying calls in the same stock, if not sparking then certainly accelerating the gamma feedback loop which we first described last Tuesday before the SoftBank presence was reported in “A Classic Feedback Loop”: Why Everyone Is Chasing The “Gamma Crash Up” as both single name implied vol and the overall VIX surged alongside stocks (resulting in a historic inversion in the S&P-VIX correlation)…

… sending both the FAAMGs, the Nasdaq and the S&P500 to all time highs.

In retrospect it should have been obvious not just to us but everyone what was going on.

After all, it was in early August that we first learned that for the first time SoftBank was targeting investments of more than $10 billion in public stocks as part of a new asset management arm, far exceeding the initial holdings that founder Masayoshi Son outlined to shareholders in the company’s latest earnings call, and a break from the company’s strategy of investing in private names.

None of this was a secret, because on Aug 11, Son said SoftBank had acquired major holdings in not only the FAAMG stocks but some of the highest beta, “story” tech names.

Of course, the biggest hint was Bloomberg’s report in mid-August that SoftBank’s “investments were made using financing structures that can prevent SoftBank from showing up in public records as a direct shareholder.” Because why hide its footprints if it wasn’t engaging in a trade that would spark a historic surge in the very same public names it had just purchased, and which would gradually seep over to the broader market, sending the S&P to a record high of 3,580 just a few days ago.

There was also another reason why Masa Son desperately felt the need to spark a massive ramp in public stocks (conveniently taking place at a time in the year when markets were especially sleepy, during the vacation breaks of August): having seen his reputation and credibility crushed after the WeWork and WireFraud fiascos, the new unit reflected Son’s revived ambitions to secure tens of billions in fresh outside capital after the bombing of the second Vision Fund. And what better way to do it than to show a remarkable return on his brand, spanking new investments in public FAAMG stocks:

The founder had said in May that SoftBank was unlikely to secure outside investors for a second Vision Fund after problems with the first. But in the upbeat financial results Tuesday, Son expressed readiness to accelerate a companywide shift from telecom to investing. “Our strategy hasn’t changed,” Son said. “We still plan on unicorn hunting with Vision Fund two, three and so on.”

Which brings us to the “brains” behind the strategy, which we now know is Akshay Naheta, a SoftBank senior vice president in Abu Dhabi, who is the head of SoftBank’s new asset management team (i.e., the brand new team investing in public companies) and who was hired in Jan 2017 from the London-based Knight Assets which he founded, and where he focused on “arbitrage and value investing.”

Remarkably, Knight’s investments had generated a staggering IRRs of 112.5% annually since its 2011 launch, and one wonders just how much of the fund’s impressive performance was the result of similar gamma loops. One also wonders why Akshay would leave what was arguably one of the best performing buyside platforms last decade?

And where did Akshay learn the tools of the trade? Why at that “pristine” bank which has “never” had any legal issues or record criminal and civil settlements: Deutsche Bank, where Naheta was Head of Principal Strategies, “responsible for proprietary trading and structured deals, managing risk across various asset classes globally.”

Surely this financial wizard is a Wharton grad – after all for him to have such phenomenal “deep value” investing acumen, he must have learned from the best. Wrong: the SoftBank gamma guru graduated from MIT with an M.Sc in Electrical Engineering and Computer Science in 2004, following an undergrad from the University of Illinois at Urbana-Champaign where he graduated with a B.S., highest honors, in, drumroll, Electrical Engineering.

If JPM’s Bruno Iskil was the London whale, perhaps we should now call Askhay the “Gamma whale.”

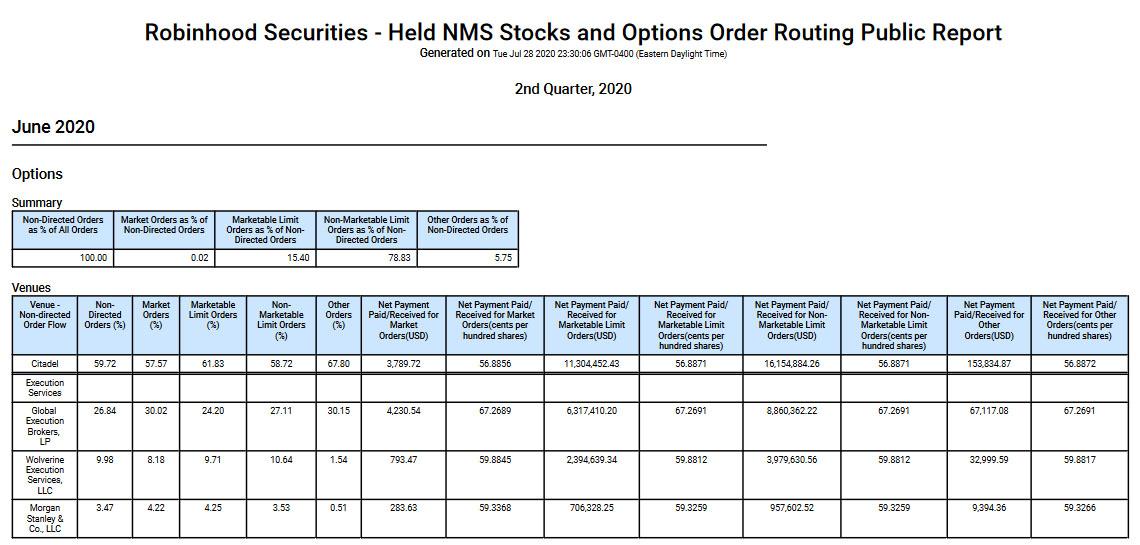

One almost wonders how much of a role in the marketwide gamma that flooded across markets in the past month did this computer science expert relegate to HFTs, whose momentum buying he knew would be sparked the moment SoftBank indicated it was splurging on calls across the most popular tech names, especially with HFTs frontrunning similar call buying over at retail frenzy ground zero, Robinhood, which made a killing in option trading payment for orderflow in June according to its 606 Report. We can only imagine what July and August will look like.

Conveniently, Askhay had Robinhood to help him, because having observed the furious retail call buying which we described from May across July (see above), Askhay realized that all he needs to do is pour a little extra gasoline on the fire, show a few outsized trades to the HFTs which would then unleash a cascade of call buying on their own, resulting in massive – and free – leverage of SoftBank’s own call buying trade.

As an aside, we find it rather remarkable that some of the most prominent Deutsche Bank traders are now at SoftBank. Yes, there’s Akshay triggering the biggest gamma squeeze in history, but we learned in 2018 that Colin Fan, former co-head of Deutsche’s investment bank who made MD at 28, and one-time head of Deutsche’s trading business had also joined SoftBank, where he was reunited with Rajeev Misra, Deutsche’s former head of global credit trading, and the current head of Softbank’s $100BN Vision Fund.

Other Deutsche Bank alumni, Nizar Al-Bassam, Michele Faissola (who was implicated in the death of DB’s senior risk manager, William S. Broeksmit, who was found dead in 2014 after committing a still unexplained suicide) and Wayne Grigull, work for or advise (Faissola is an advisor) Centricus Advisors (formerly known as F.A.B. Partners) and helped the Vision Fund raise its Saudi money. Many worked together at Merrill Lynch before joining Deutsche Bank. As EFC noted some time ago, “they have history.”

Keeping a close eye on these former Deutsche Bankers, now at SoftBank, is imperative.

* * *

Which brings us to what is perhaps the last loose end: how much money did Akshay – and SoftBank – make using this strategy? Aaccording to some original (for a change) reporting by the FT, SoftBank is currently sitting on unbooked profits of about $4 billion. This is roughly the same amount as SoftBank has spent on call premiums over the past few months – as it built up a massive position equivalent to roughly $30 billion in notional exposure – meaning it has essentially generated a 100% IRR.

Of course, as we noted yesterday, despite being exposed as the fund behind the market’s bizarre August moves, implied vol has yet to drop which means that SoftBank is likely still in the trade and has yet to take a profit…

… or that dealers have not yet figured out a proper strategy to hammer implied vol. One thing that is certain is that it is only a matter of time before dealers, who were counterparties to the SoftBank trade and are likely nursing billions in losses (assuming they didn’t delta-hedge all of their exposure) will do everything in their power to punish the Japanese conglomerate. And even if they did fully delta-hedge their outlier gamma exposure, now that the FAAMG rally has broken, the precipitous ramp observed on the way up is about to reverse as dealers start dumping the stocks they had to buy as gamma spiked, leading to a mirror image of the melt up trade. In short, while SoftBank may have made a 100% profit, unless it somehow unwinds this trade asap, it risks losing not only all of its gains but also suffer material losses that would eat into the option premium and would then also hammer the value of its underlying stock investments.

The bottom line is that as one unnamed trader quoted by the FT said, “it’s just a levered punt on the market. The whole strategy is just momentum buying.“

Well of course it is, but it had not only the benefit of massive leverage, but also timing, striking just as there was virtually nobody in the market to take the opposite side of the trade while piggybacking on a call-buying frenzy among the retail community, something any trader with a background in HFT/market structure inefficiencies such as a Akhsay would be well aware of.

The only question we have now is what happens to SoftBank – whose reputation for foolhardy leeroy jenkins-tyle investments with little to no diligence but merely seeking to manipulate the market with its size and scope precedes it, once the momentum reverses, and after hunting dealers with a max painful gamma squeeze, dealers now return the favor.

The answer: probably not much – recall that the BOJ is now the biggest investor in Japan’s ETFs, and with SoftBank widely held not only by Japan-focused ETFs but also by Trust banks through which the BOJ operates, it is safe to say that the Japanese central bank is one of the top investors in SoftBank, if not bigger even than Masa Son himself with his 21% holding.

Add the fact that Japan’s pensioners via the GPIF are among the top investors in SoftBank (which among other thing, means that the fate of Japan’s pension funds is now directly tied to the performance of AAPL and TSLA calls), not to mention that the world’s largest sovereign wealth fund, the Norges Bank is also a top 15 investors…

… and it is clear that nothing bad can ever happen to SoftBank – even if this particular momentum trade were to crash and burn – simply because a failure of this particular “Nasdaq whale” would be far too systemic, causing massive losses among both sovereign wealth fund and central banks, and it would promptly receive a bailout from the BOJ, something we first suggested last year.

In fact, the fact that SoftBank is now too big to fail is – in our view – the true reason behind Masa Son’s unprecedented gamma gamble: after all if the trade succeeds Masa wins, if the trade loses it is the merely taxpayers that lose (as they always do in the end)… something which apparently was not lost on Akshay himself:

This is why capitalism is breaking down! Our future includes a significant increase in taxes to counter these government-backed bailout policies at any sign of “trouble”. The Fed’s policies have exacerbated inequality and tensions in the social fabric. https://t.co/H8UmloRhhK

Trump Tweets: “Baltimore’s Poverty & Crime Will Only Get Worse Unless You Elect Kim Klasick” Tyler Durden

Sun, 09/06/2020 – 13:14

Baltimore-based GOP Congressional candidate Kim Klasick gained a national media profile thanks to a viral campaign ad accusing Democrats of failing to revive Baltimore, and encouraging blacks in the city and some surrounding suburbs to try voting Republican for a change.

Now, President Trump has endorsed Klasick with one of his typical endorsements via tweet, while urging Baltimore to “be smart” and reject the pandering Democrats who are unwilling to make the necessary changes to save the city from the twin scourges of crime and drugs.

Be smart Baltimore! You have been ripped off for years by the Democrats, & gotten nothing but poverty & crime. It will only get worse UNLESS YOU ELECT KIMBERLY KLACIK TO CONGRESS. She brings with her the power & ECONOMIC STRENGTH OF THE REPUBLICAN PARTY. She works sooo hard….

….Baltimore will turn around, and I will help. Crime will go way down, money and jobs will pour in. Life will be MUCH better because Kimberly really cares. The Dems have had 100 years and they gave you nothing but heartache. Baltimore is the WORST IN NATION, Kimberly will..

….fix it, and fast. The current recipient has no chance, and won’t even try. As I have often said, Baltimore is last in everything, WHAT THE HELL DO YOU HAVE TO LOSE! Kimberly is fully Endorsed by me, something I do not do lightly. Take advantage of it and MAKE BALTIMORE GREAT!

Trump insisted that “Baltimore will turn around, and I will help. Crime will go way down, money and jobs will pour in. Life will be MUCH better because Kimberly really cares. The Dems have had 100 years and they gave you nothing but heartache. Baltimore is the WORST IN NATION, Kimberly will fix it, and fast!”

Maryland is a reliably Democratic state, and Baltimore a solidly Democratic city, with more than 5x the number of registered Dems as registered GOP. Trump initially praised Klasick after her convention speech, so his endorsement is hardly a shock.

But maybe with the aid of a national media profile, Klasick might have a shot to fill the seat – representing Maryland’s 7th District – once held by Elijah Cummings, a seat which has been held by Democrats for nearly 70 years.

via ZeroHedge News https://ift.tt/35bt5Sv Tyler Durden

Former NYT Reporter Challenges Dr. Fauci’s Climate Change “Mission Creep” Tyler Durden

Sun, 09/06/2020 – 12:45

For anybody who isn’t already suspicious of Dr. Anthony Fauci’s self-aggrandizing ways, former NYT reporter Alex Berenson has called the “bureaucrat” out for trying to overstep his authority by proposing nothing short of a radical restructuring of society to ensure humanity’s survival during the “pandemic era”.

It might sound far-fetched, but in a paper recently published in the journal Cell, Dr. Fauci claimed that the world had entered a new “pandemic era”, and claimed that an onslaught of infectious diseases is already transitioning from animals to humans via ‘zoonotic transmission’. Going off on a seemingly absurd, pseudo-scientific, tangent, Dr. Fauci claimed that “industrialization” is to blame for infectious diseases like COVID-19, and the only remedy is to live “in harmony with nature”.

We suspect the good doctor is a fan of Greta Thunburg and her fellow “climate activists”.

Of course, who benefits from this level of conjecture? Only Dr. Fauci, as he begins selling his vaguely progressive sound “solution” to humanity’s newest problem. “There are many examples where disease emergences reflect our increasing inability to live in harmony with nature,” Dr. Fauci wrote.

But in a twitter thread that went viral, Berenson takes Dr, Fauci to task for “mission creep”.

1/ Hoo boy. Dr. Anthony Fauci has some advice for us.#Sars-Cov-2 is just the beginning. We’re in a “pandemic era” now, friends.

2/ “Living in greater harmony with nature will require changes in human behavior as well as other radical changes that may take decades to achieve: rebuilding the infrastructures of human existence, from cities to homes to workplaces… to recreational and gatherings venues.”

3/ “In a human-dominated world, in which our human activities represent aggressive, damaging, and unbalanced interactions with nature, we will increasingly provoke new disease emergence.”

Huh. Sounds like human domination is the real problem here?

5/ But, see, if #COVID-19 turns out to be a testing-driven lil-bit-worse-than-a-bad-flu year, what then? Maybe we WON’T need to redesign all of human existence because some 79-year-old bureaucrat wants us to?

Others who commented on Berenson’s tweets pointed out how the “Green New Deal” and the climate extinction movement loomed large in Dr. Fauci’s new “pseudo-science” based anti-human ideology.

I sense a Green Nude Eel lurking there somewhere.

— Archibald Heatherington Nastyface (@ArchibaldHeath1) September 4, 2020

Because once COVID-19 is finally under control, pandemics will join wildfires and hurricanes as one more natural ill that can potentially be tamed via the “Green New Deal” and other radical proposals to fight “climate change.”

via ZeroHedge News https://ift.tt/35dfp9E Tyler Durden

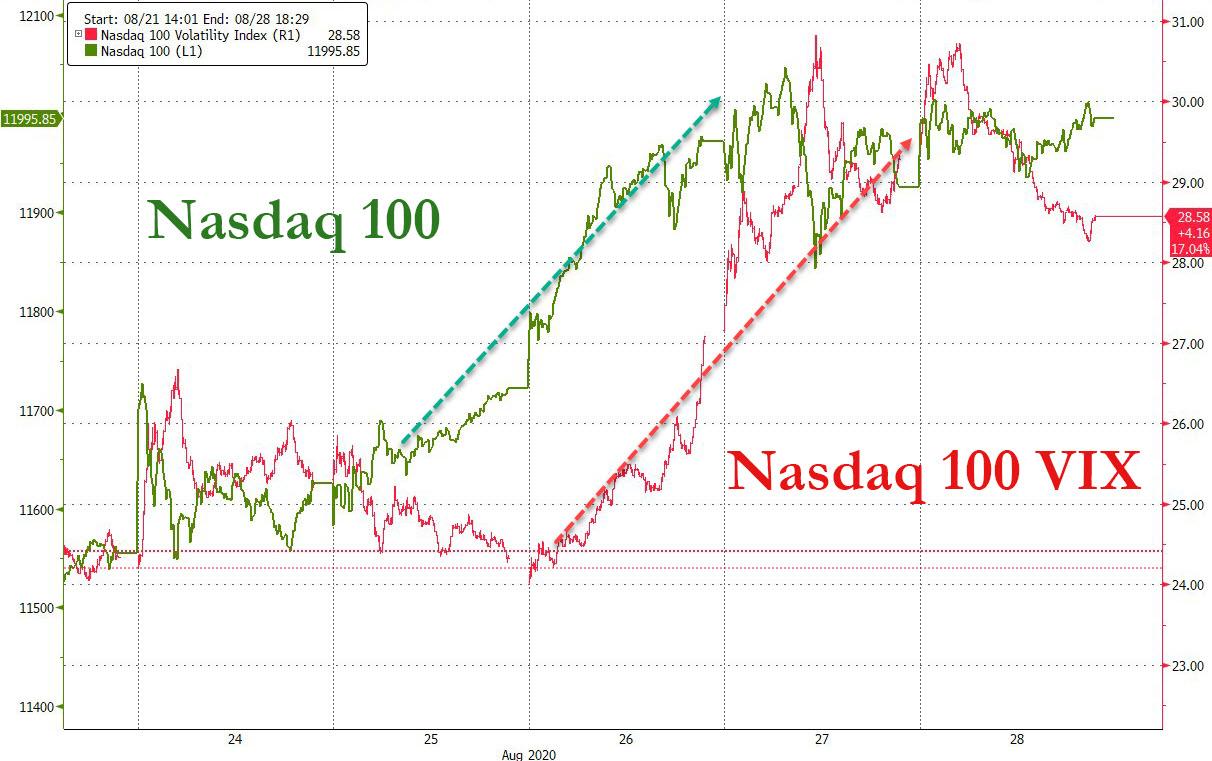

Last week, I noted here that a relatively rare condition had arisen in which stocks and expected volatility had risen at the same time. Last week, I noted on twitter that the Nasdaq Composite and its volatility index (VXN) had never been more positively correlated than they have over the past 10 days. This week, I’d like to briefly put forth my best guess as to why this is happening.

As noted by Jason Goepfert, speculative call buying has recently surged to levels never seen before.

Speculative options trading reached the equivalent of 12% of NYSE volume last week.

Like some combustible combo of musical chairs, Russian roulette, and five finger fillet.

At the same time, market makers selling all those call options to the traders buying them are forced to hedge by buying the underlying stocks.

‘If short gamma hedging lifted stocks, logically it should also be capable of exacerbating moves the other way. When shares fall, market makers are likely to unwind hedges at an increasing speed, spurring more losses.’ https://t.co/ojNZvf97WD

DHS Leaker Who Sabotaged ICE Raids Strikes Again With Memos Declaring White Supremacists “Greatest Terror Threat” Tyler Durden

Sun, 09/06/2020 – 11:55

Politico managed to find several draft copies of an annual threat assessment prepared by the Department of Homeland Security, all of which used “similar” language to describe white supremacists as “the deadliest domestic terror threat facing the US”. Unsurprisingly, the reporters later explained that all three drafts stemmed from an order given by former acting secretary Kevin McAleenan during the brief period before he was ousted in favor of Chad Wolf, nominated by Trump to drop the “acting” from his title of “Acting Homeland Security Secretary”.

McAleenan

For those who don’t remember McAleenan, he was pushed out like his predecessor, Secretary Kirstjen Nielson, after he was caught leaking details of upcoming ‘ICE Raids’ to the Washington Post, as we reported during June 2019. The Washington Examiner, which initially outed McAleenan as the leaker, reportedly did so “deliberately” in an attempt to stymie the raids, a central tenant of his boss’s immigration policy.

Like many other former Trump Administration officials (most notably, former chief of staff John Kelly and secretary of defense Gen. James Mattis), McAleenan has apparently found a way to keep attacking and undermining the administration. Releasing damaging documents and other stories from theit time in the administration has become one popular method of doing – as James Comey calls it – “one’s civic duty” to “protect democracy” from the first Republican president to win the electoral college, but not the popular vote, since – checks notes – George W Bush.

McAleenan didn’t act alone. He apparently had help from notorious James Comey crony and “LawFare” blogger Ben Wittes, a notable voice in the anti-Trump movement. Politico identified him as the source of the leaked memos. We feel it’s safe to assume Wittes obtained the memos from McAleenan.

Notably, none of the documents reviewed by Politico referenced any threat posed by Antifa, which President Trump back in May labeled a “Domestic Terrorist Organization”. However, two of the drafts, which – keep in mind, were probably written some time early last year – did refer to the possibility of extremist groups hijacking peaceful protests by exploiting “social grievances”.

We must concede, McAlennan was pretty much spot on with that last one.

via ZeroHedge News https://ift.tt/2QXt503 Tyler Durden

As it turns out, there actually was a Murphy. His now ubiquitous American idiom, Murphy’s Law, is well-known to everyone: whatever can go wrong, will go wrong. The reason it has proliferated and penetrated to every corner of our modern society is the embedded truth sprinkled with just a kiss of post-modern ironic fatalism.

As a result, it doesn’t quite mean what the original version did. I think you, as I, will prefer the first one.

That Murphy was Air Force Captain Edward A. Murphy, Jr. Around the time Chuck Yeager was out at Edwards Air Force Base in California breaking the sound barrier, in 1947, another less well-known figure, John Paul Stapp, was in the same place at the same time trying not to kill himself by testing the limits of the forces that would otherwise kill him.

In addition to being military, Captain Stapp was also a medical doctor. He was often rumored to be the physician who signed off on Yeager’s famously broken ribs so that the latter pilot would be able to make history the very next day by becoming the first human to ever break the sound barrier. That didn’t actually happen but the truth, as is often the case, was more interesting as filmmaker (and author of “A History of Murphy’s Law”) Nick Spark discovered. Yeager related to Spark that it was actually a vet in Rosamund, California who fixed up his ribs, not Stapp.

But Stapp did make significant contributions to history. More important than any footnote to Yeager’s accomplishments was his other incredibly dangerous work, where the good doctor would repeatedly and voluntarily strap himself into a rocket-powered sled in order to examine the potentially catastrophic effects of massive physical forces on the human body.

In one of his more famous runs, Capt. Stapp climbed aboard the apparatus, nicknamed Gee Wiz, blasting down the test track wearing no helmet and on his body nothing more than shorts and a thin T-shirt. The idea was pretty simple: accelerate the machine to the limits of speed, which were closing in on the sound barrier for these sledges, and then decelerate in the least amount of time mechanically possible.

The tested forces and impacts impacted much more than military jet designs. Everyone riding around in an automobile today, meaning everyone, owes some significant gratitude to Dr. Stapp’s amazingly selfless investigations. After doing things to himself hardly any person alive can have imagined, Stapp also worked tirelessly to share what was learned with the auto industry, the safety of everyday folks becoming more and more the embodiment of what he was doing and why.

And because he was out there in the scorching California desert pushing right to the edge of the envelope, his equipment needed to perform flawlessly. If it hadn’t, not only would Capt. Stapp have been killed, how many multitudes of others would’ve needlessly followed?

Enter Capt. Murphy. The story that was told by direct witnesses to Nick Spark was that Murphy’s role was pretty minor in it. He had come to the base for only a very short time, overseeing one small technical aspect of Gee Wiz’s operation. The couple of technicians he brought along apparently screwed up the installation of a pair of transducers which were expected to more accurately measure acceleration forces (G forces).

Running the sled with a chimp aboard to test and calibrate what was a new setup, they were all stunned when the gauges showed zero. Whichever mechanic had installed them with electrical bridges wired backwards, the readings for one canceling out the readings for its opposite. A relatively minor mistake.

When informed the next morning of the snafu, an ornery Murphy allegedly snapped back, “If that guy has any way of making a mistake, he will.” It wasn’t clear which guy, exactly, had aroused his officer’s ire. Either way, the legend was born.

Murphy’s Law, however, didn’t take full shape until a few days later, after Capt. Murphy had faded back into the obscurity of the vast military bureaucracy. Capt. Stapp, on the other hand, had been tasked with handling a press conference where he was asked hard questions about the nature of his business.

What they were all doing was dangerous stuff, putting not just his own life at risk but of those around him. And what about the downstream consequences? Even more lives at stake; far more than any of them could’ve known in those early days of advanced scientific study.

Answering the reporter’s question, Stapp said the guys working on the project adhered to principles only recently dedicated locally as this Murphy’s Law: if it can happen, it will happen.

They had to think ahead, think on their feet, all the while trying to worry about every little thing and all pushing the very edges of survival. They couldn’t afford indulgences, what-ifs designed to save a reputation or adhere needlessly to a religious-like doctrine.

Maybe the original is only a slight change in slant to the wording before the current version, but there’s a world of difference in it. These people weren’t expecting failure to plague and harass them, as the current iteration makes it seem, rather they were anticipating even welcoming breakdowns which would demand their own ingenuity to overcome.

Everyone realized the complexity, therefore they were looking ahead for problems so that the way forward, because there would be a way forward, could be achieved with as little risk and maximum efficiency as possible.

The original Murphy’s Law was a hope-filled expression of harsh reality being surmounted by retail-level human genius. Simple. Elegant. Devastatingly powerful because it was small “s” science practiced in another one of those beautifully informal settings.

No wonder it was corrupted.

Capt. Stapp, in addition to being a tough son-of-a-bitch as well as a doctor, he was also known to be something of a wit and wordsmith, too. Crafting this first version of Murphy’s Law for the cameras, he also put together several others including one he called his Ironical Paradox: the universal aptitude for ineptitude makes any human accomplishment an incredible miracle.

The sentiment embodied within it undoubtedly contributed to the perversion of its more famous cousin. History, or at the very least progress, is never smooth and linear. It comes in fits and starts, big leaps and then prolonged periods of nothing but intellectual stagnation. And the reason is no more difficult to understand than these clichés.

People aren’t perfect, nor perfectible.

All of which brings us to the cool mountains of Wyoming in the year 2020.

What everyone heard from the last week’s media summations of Jay Powell’s virtual address to the virtual conference was “lower rates for longer.” Massive “dovish” “accommodation” for as long into the future as it is possible to look toward. Pure Japanese (oops, no one said that).

Specifically, he referred to this as changing monetary policy focus from merely a symmetrical one to an average inflation target (if you’re trying to figure out the difference, you’re not alone).

What you didn’t hear was all the analysis and scholarship that went into this Grand New Strategy. The reasoning behind what they are telling you is a huge deal.

It’s not just that the economy is in bad shape right now and policymakers decided on a whim to do something (they’ve already done plenty of that). Chairman Jay Powell’s overhaul was begun all the way back in November 2018, which already implies there must’ve been some reason to spur on such big changes. Here we’ll take them at their word; if this is a big deal, then how unsatisfactory might it have been to shove even the most stubborn among policymakers towards one?

We’d already heard rumblings before. For quite a few years now, researchers and Economists driven by the work of FRBNY’s John Williams have been playing around with R* theories. The natural interest rate, therefore the neutral interest rate, has fallen, they claim. What that might mean insofar as monetary policy has been concerned is that maybe it was less powerful than they once thought.

Yeah, I know. It’s not what central bank chief after central bank chief has told the public. Each new QE was always the biggest, baddest, most guaranteed successful program Ivy League Economists could have ever come up with. Now, R*?

And it only got worse – mostly for us, but also for their QE’s. The one thing that could have possibly restored the honor of Ben Bernanke and his successors was the unemployment rate. The lower it went, the more it suggested the economy had reached full employment. At full employment, QE is a complete success.

However, as you’re no doubt aware, the unemployment rate kept going lower and lower and lower. By 2019, it had fallen to a 50-year low – at the same time the US and global economy was beset by an “unexpected” downturn.

It’s not as if questions haven’t plagued the unemployment rate from the very end of the last “great recession.” The participation problem is well-known, too, but Economists have sought excuse after excuse to write it off as a statistically insignificant quirk, or to blame the American worker for it.

But, and there was always this “but”, the main labor market ratio required corroboration no matter how outwardly goading. It’s one thing to say the number must have dropped low enough to be at or even past full employment; it’s quite another for full employment to show itself in the real economy, which it would’ve done had it been real.

Inflation, in other words. AW Phillips’ updated relationship between employment and consumer prices, all of which traverses directly through economic slack and wage rates. If the unemployment rate had been correct, well below all prior estimates of full employment, wage rates would’ve accelerated sharply setting off sustained, broad consumer price increases as company after company desperately competing for the allegedly scarce marginal worker passed along the increased costs to their customer bases.

Implicit in the Fed’s Grand Strategy Review, therefore, is a full-blown admission that this never happened. Fed officials like Powell who charged into office as a hawk kept saying that it was going to happen, that it was beginning to happen, now years later to quietly, meekly accept the reality that it never once did.

But why?

The most obvious answer is that the participation problem was a real factor, that sizable, verifiable economic slack must still remain behind even after the passage of a dozen years, and that monetary policy fell way, way short of every single one of its goals – therefore both statutory mandates.

Oh no, cried the Fed’s vast teams of researchers! No, no, no. The Phillips Curve itself must’ve shifted, flattening out to something more like the yield curve, so low and flat as to be nearly unrecognizable as one. But whereas the latter has been evidence directly contradicting the mainstream story, the flat Phillips Curve offers it a way out. Tempting, no?

At nearly a level horizontal line, this would say no matter how large the increase in expectations for growth the result in inflation would be exceedingly small.

Like R*, though, this requires a fundamental rewriting and reordering of basic economic processes to get there. What would those have to be in order to flatten Dr. Phillips’ great legacy to such a huge degree that the 50-year low in unemployment couldn’t muster the slightest sustained elevation in consumer price advances?

Well, you see, they don’t really know. Several crude theories abound, of course, but what’s going on here is about as unscientific as it gets. The theory of monetary policy, that it led to robust economic circumstances, fitted to the data and evidence piled up against it.

Money printing always leads to inflation, yet the reckless money printing the Federal Reserve and other modern central banks are alleged to have conducted never leads to any. Have the most basic and fundamental of economic properties and relationships so drastically changed, and that drastic change just coincidentally timed to a global monetary crisis twelve years ago, or are central bankers and Economists bending over backwards bending curves, openly trying too hard to evade recognition of the most logical and straightforward explanation?

The answer is obvious.

We need not search for an explanation, either. As Dr. Stapp put it, progress is quite often a miracle itself. Humans are as hardwired to cover for their failures, to any dubious lengths, as they are to honestly move forward toward the light of truth. In one of man’s greatest ironies, you almost have to add the pain of death to make it possible.

The original failure, the Fed’s modern original sin it must forever cover up, is money itself. When central bankers and Economists realized they could no longer define it, and this was more than a half century ago, they came up with what they believed was progress. The post-Great Inflation Fed, the Volcker era, was one in which policymakers supposed they’d never have to figure out the monetary details.

The dirty work would be left to the banks. The only act the central “bank” needed, then, was to signal to the banks what it wanted them to do and let the banking system sort out the particulars. Simple. Elegant. And dangerous.

Not only were central bankers warned when this shift took place that it would be irresponsible, and the likely consequences of such dereliction potentially momentous, some of the most famous proponents like Alan Greenspan worried how they’d not only end up fooling the public but themselves along with every layperson (his famous 1996 “irrational exuberance” speech a perfect example of the “maestro’s” gross monetary concerns).

August 2007 and thereafter was simply those consequences finally arriving. Contradicting also Keynes, in the long run someone really would have to pay for a system in which central banks are not central and don’t do money. As it turns out, the costs have been born by the whole global economy as it has been deprived for thirteen years of enough necessary monetary oxygen to make things work.

Including the lack of inflationary success at each central bank target, no matter each central bank “money printing” session.

Central banks don’t do money. They are not central. This fact, yes fact, has dawned on broad swaths of the financial markets, which explains why for all the hoopla and hype surrounding the Jackson Hole reveal of the Grand Strategy Update, and its gigantic inflationary commitment we were told it represented, the spectacle went off with less than a whimper. Even in stocks.

Like their view of the Phillips Curve, you could honestly say it fell flat. I smile only briefly for such true progress.

Worst of all, though, the great Americans who toiled at the California test tracks suffering under the most brutal conditions for the benefit of humankind did so without any need nor expectation of ever being hailed as the heroes they really were. They remained honest, as honest as they could, and pushed forward knowing the consequences of even the smallest setbacks would be felt very near and dear.

Success was big, and hard-won, because no matter what, if it could happen, they were already thinking about it no matter how uncomfortable it might make them, no matter how much it harmed their personal views and reputations. These scientists didn’t wear white lab coats and sit under academic instruction, they wore blood and pain conducting their work in the gritty trenches of the real world.

Nowadays, detached entirely from any accountability whatsoever, we are supposed to call Ben Bernanke, Janet Yellen, and Jay Powell heroes. For what? From the very start, these are all acts of intellectual cowardice, a bankrupt foundation so perverse it is an embarrassment to science itself; becoming ever more so with each additional stab at everything but the truth. Anything other than that.

They’ve perverted Murphy’s Law into a third version, a specific version. Fed’s Law is now this: monetary policy will never go wrong, so everything else will.

As it has. And it is.

via ZeroHedge News https://ift.tt/3bx7lBo Tyler Durden

Outrage After University Suspends 11 Students For “Party” But Keeps $36,500 Tuition Tyler Durden

Sun, 09/06/2020 – 11:00

It’s been no secret that only a couple weeks into the start of the fall semester, colleges across the US are struggling to keep COVID-19 numbers down, with some schools already reporting hundreds of confirmed cases, and others quickly shutting down in-person classes a mere days after starting back up, when numbers merely reached 130 infected, as recently happened with University of North Carolina Chapel Hill.

Schools have imposed strict measures while threatening severe punishments for hosting or even attending parties on or off campus, as they’re considered potential “super spreader” events. In some instances schools are actually threatening expulsion. But there’s rising tensions given students are complaining their high price tag college experiences are turning into “isolation prisons” – as we detailed earlier, yet schools in many cases are collecting full tuition and fees.

But now one major university is driving headlines after making good on its ‘max punishment’ threat, and all the while pocketing students’ full tuition after they were accused of “violating social distancing protocols”.

Northeastern University, file image

Apparently they were caught in a gathering deemed a “party” by the staff members who discovered them. Again the “party” apparently consisted of eleven people total in the room, and they happened to be housed in the same building:

“Northeastern has dismissed 11 first-year students after they were discovered together in a room at the Westin Hotel in Boston on Wednesday night, in violation of university and public health protocols that prohibit crowded gatherings,” the college website News@Northeastern writes.

The students along with their families were notified Friday that they’ve been suspended from the school effective immediately, and have further been ordered to vacate the hotel within 24 hours. The Westin, which lies less than a mile from campus, was reportedly being used to house over 800 students who stayed two to a room.

In particular it’s part of a program called N.U.in Program, described as a “study-abroad experience for first-year students”.

Critics of the school’s harsh punishment say the international students’ actions can’t even be deemed as part of an ‘off campus party’ – but instead it’s tantamount to students simply being gathered in a dorm room.

Northeastern excessively punishes 18 year olds for acting like 18 year olds and steals their money. Is Northeastern run by cops? https://t.co/atZLcfyS7T

Senior vice chancellor for student affairs at Northeastern, Madeleine Estabrook, issued a statement underscoring there’s a zero tolerance policy for protocol violators:

“Cooperation and compliance with public health guidelines is absolutely essential. Those people who do not follow the guidelines—including wearing masks, avoiding parties and other gatherings, practicing healthy distancing, washing your hands, and getting tested—are putting everyone else at risk,” according to the school publication.

Among other things the school’s new COVID-19 social distancing policy spells out in the updated N.U. handbook that “there will be no guests, visitors, or additional occupants” in student residential rooms.

Particularly outrageous and perhaps why the story is going viral online, is that the school is keeping the now expelled students’ full tuition, despite the program of all international newcomers being a mere week or so in session.

According to The Boston Globe, that means the school has pocketed each student’s $36,500 they already forked over. N.U. officials have confirmed and emphasized to local media there will be no refunds.

Northeastern University risks student and faculty lives by reopening prematurely during deadly pandemic and then steals over $400,000 from 11 students. https://t.co/RxGx6qkxeI

That is indeed over $400,000 in total that the university is keeping from the “busted” students, who merely made the mistake of momentarily emerging from the school-imposed isolation of their cells rooms in order have actual human-to-human contact.

Meanwhile, out of 36,000 coronavirus tests conducted so far, there’s only been 20 positive cases on the campus.

via ZeroHedge News https://ift.tt/2Z8XIDZ Tyler Durden

{kind=link}

{kind=link}