Chinese Warplanes Advance On Taiwan As Tensions Soar Tyler Durden

Mon, 06/22/2020 – 08:40

For the seventh time this month, Chinese warplanes approached Taiwan’s air defense identification zone (ADIZ) on Monday in what could be a deepening phase of geopolitical turmoil between Beijing and Taipei, reported Reuters.

The People’s Liberation Army Air Force (PLAAF) flew at least one H-6 bomber and J-10 fighter jet into the ADIZ at the island’s southwest territory.

Taiwan’s air force responded by issuing verbal warnings to the PLAAF aircraft and dispatched aerial reconnaissance and fighter jets to intercept the Chinese jets.

Taiwan’s Ministry of National Defense (MND) said Taiwanese fighters “proactively drove off” the PLAAF aircraft. The incident marks the seventh time, last seen on June 9, 12, 16, 17, 18, and 19, that Chinese military aircraft have violated the country’s ADIZ.

The H-6 is a nuclear-capable bomber, used by China in “island encirclement” war exercises around the Chinese claimed-island.

Beijing insists Taiwan is part of China, and the war drills around the island, if that is in the air or by sea, act as a routine reminder that China has plans for unification.

The sudden spike in Chinese warplane sightings comes weeks after Taiwan’s President Tsai Ing-wen was sworn in for a second presidential term in late May.

US Secretary of State Michael Pompeo congratulated Tsai and said Taiwan is a “force for good in the world and a reliable partner.”

Usually, the US has refrained from recognizing Taipei’s government in the past. This certainly angered China – and probably why PLAAF aircraft have been flying around the island.

With cross-strait and Sino-US diplomatic relations quickly deteriorating – Beijing will likely continue its aggressive stance in the region.

via ZeroHedge News https://ift.tt/3hPKNi2 Tyler Durden

I’ve written a new book about language (you can see it here), and Eugene and friends have kindly consented to let me discuss it this week (thanks, Eugene!). The book talks about why the prose of Lincoln, Churchill, Holmes, and other greats is so compelling, and asks what we can learn from them about how to write better ourselves. The book is part of a series on rhetoric—a sequel to this one and this one (which will be reprinted later this summer).

The new book’s general claim is that our culture of advice about good writing doesn’t explain the power that Lincoln achieved with his words. The usual story is that the best writing is the most efficient—that clarity and concision are everything. It’s hard to argue with this; who doesn’t want to be clear? But writing can be clear and powerful, clear and memorable, clear and full of fire, or clear without any of those things. The book argues that rhetorical force isn’t created by efficiency alone. It’s created by the use of contrasts.

Consciously or not, Lincoln understood this. It’s how he wrote. Here I will talk about one example: contrast in the kinds of words you use.

English is a language built mostly out of two others. Much of it was created out of the language of invaders who came to Britain around 450 ad from Anglia and Saxony (in what we’d now call northern Germany). About 600 years later the French invaded and brought their language with them, too; it was derived from Latin. The new French competed with Old English, and the outcome was a language—modern English—built out of both.

Often words with similar meanings from the two languages were both turned into English words, such as make (Saxon) and create (from French), or need (Saxon) and require (from French). So in English you can say almost anything with two kinds of words: short, simple ones with Saxon origins, or fancier ones that come from Latin.

It’s a fun parlor game to name a Latinate equivalent for every Saxon word you can think of. If a word ends with –tion or similar suffix, or if it could be made into a similar word that does, then it’s usually derived from Latin. Thus the Latinate word acquire can become acquisition or acquisitive; but the equivalent Germanic word get doesn’t take endings in that way.

In any event: advisers on English style have long said that it’s best to use Saxon words when you can, because those words are most clear and forceful. If you need a single rule, that’s as good as any. But Lincoln didn’t create his great effects by sticking to one kind of word or another. He created them by skillfully mixing the two kinds of words, and doing the same with other aspects of his language.

For example, Lincoln especially liked to start a sentence with Latinate words and then end with a Saxon finish. Look at this famous passage from his “House Divided” speech in 1858:

Either the opponents of slavery will arrest the further spread of it, and place it where the public mind shall rest in the belief that it is in the course of ultimate extinction; or its advocates will push it forward till it shall become alike lawful in all the States, old as well as new, North as well as South.

The first half of the sentence has lots of Latinate words: opponents, slavery, arrest, course, ultimate, extinction, advocates. Then it ends with 14 words of one syllable in a row, all of them Saxon except “States” (which might as well be). He expresses the hope in large, uplifting words, and the threat in words that are short and simple. The first round sets up the second.

Another example, this from Lincoln’s Second Inaugural Address:

Both parties deprecated war, but one of them would make war rather than let the nation survive, and the other would accept war rather than let it perish, and the war came. —Lincoln, Second Inaugural Address (1865).

This is another good case of a simple finish used for the sake of contrast. The opinions and purposes of the parties are put in Latinate words (deprecate, nation, survive, accept, perish). The fact of what happened next is stated in solemn words of one syllable. Large words for complex intentions, plain words for plain truths.

The point: Lincoln is well-known for his love of simple language, but he was also at home with Latinate words and mixed the two types to strong effect. He especially liked to circle with larger words early in a sentence and then finish it simply. This pattern let him offer intellectual or idealistic substance and then tie it to a stake in the ground.

If you want to experiment with this idea, try finishing your arguments with words that are simpler and shorter than the ones you’ve recently been using—in other words, with a Saxon clincher.

If you’d like to read more about these ideas, you can find the book here.

from Latest – Reason.com https://ift.tt/2V5asto

via IFTTT

I’ve written a new book about language (you can see it here), and Eugene and friends have kindly consented to let me discuss it this week (thanks, Eugene!). The book talks about why the prose of Lincoln, Churchill, Holmes, and other greats is so compelling, and asks what we can learn from them about how to write better ourselves. The book is part of a series on rhetoric—a sequel to this one and this one (which will be reprinted later this summer).

The new book’s general claim is that our culture of advice about good writing doesn’t explain the power that Lincoln achieved with his words. The usual story is that the best writing is the most efficient—that clarity and concision are everything. It’s hard to argue with this; who doesn’t want to be clear? But writing can be clear and powerful, clear and memorable, clear and full of fire, or clear without any of those things. The book argues that rhetorical force isn’t created by efficiency alone. It’s created by the use of contrasts.

Consciously or not, Lincoln understood this. It’s how he wrote. Here I will talk about one example: contrast in the kinds of words you use.

English is a language built mostly out of two others. Much of it was created out of the language of invaders who came to Britain around 450 ad from Anglia and Saxony (in what we’d now call northern Germany). About 600 years later the French invaded and brought their language with them, too; it was derived from Latin. The new French competed with Old English, and the outcome was a language—modern English—built out of both.

Often words with similar meanings from the two languages were both turned into English words, such as make (Saxon) and create (from French), or need (Saxon) and require (from French). So in English you can say almost anything with two kinds of words: short, simple ones with Saxon origins, or fancier ones that come from Latin.

It’s a fun parlor game to name a Latinate equivalent for every Saxon word you can think of. If a word ends with –tion or similar suffix, or if it could be made into a similar word that does, then it’s usually derived from Latin. Thus the Latinate word acquire can become acquisition or acquisitive; but the equivalent Germanic word get doesn’t take endings in that way.

In any event: advisers on English style have long said that it’s best to use Saxon words when you can, because those words are most clear and forceful. If you need a single rule, that’s as good as any. But Lincoln didn’t create his great effects by sticking to one kind of word or another. He created them by skillfully mixing the two kinds of words, and doing the same with other aspects of his language.

For example, Lincoln especially liked to start a sentence with Latinate words and then end with a Saxon finish. Look at this famous passage from his “House Divided” speech in 1858:

Either the opponents of slavery will arrest the further spread of it, and place it where the public mind shall rest in the belief that it is in the course of ultimate extinction; or its advocates will push it forward till it shall become alike lawful in all the States, old as well as new, North as well as South.

The first half of the sentence has lots of Latinate words: opponents, slavery, arrest, course, ultimate, extinction, advocates. Then it ends with 14 words of one syllable in a row, all of them Saxon except “States” (which might as well be). He expresses the hope in large, uplifting words, and the threat in words that are short and simple. The first round sets up the second.

Another example, this from Lincoln’s Second Inaugural Address:

Both parties deprecated war, but one of them would make war rather than let the nation survive, and the other would accept war rather than let it perish, and the war came. —Lincoln, Second Inaugural Address (1865).

This is another good case of a simple finish used for the sake of contrast. The opinions and purposes of the parties are put in Latinate words (deprecate, nation, survive, accept, perish). The fact of what happened next is stated in solemn words of one syllable. Large words for complex intentions, plain words for plain truths.

The point: Lincoln is well-known for his love of simple language, but he was also at home with Latinate words and mixed the two types to strong effect. He especially liked to circle with larger words early in a sentence and then finish it simply. This pattern let him offer intellectual or idealistic substance and then tie it to a stake in the ground.

If you want to experiment with this idea, try finishing your arguments with words that are simpler and shorter than the ones you’ve recently been using—in other words, with a Saxon clincher.

If you’d like to read more about these ideas, you can find the book here.

from Latest – Reason.com https://ift.tt/2V5asto

via IFTTT

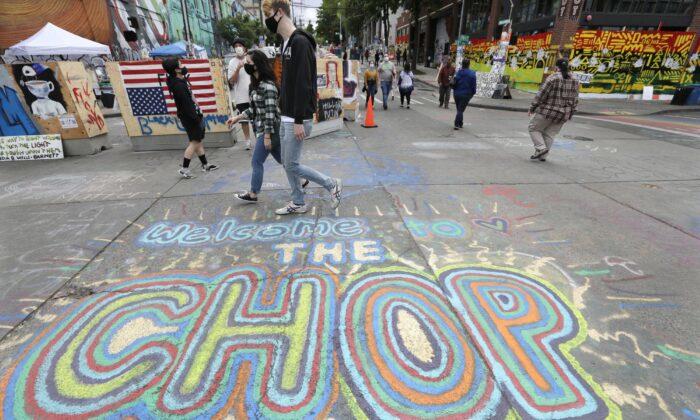

One person was wounded in what was the second shooting in Seattle’s protest zone in less than 48 hours, police said.

The shooting happened late Sunday night in the area near Seattle’s downtown that is known as CHOP, for “Capitol Hill Occupied Protest,” police tweeted, adding that one person was at a hospital with a gunshot wound.

The person arrived in a private vehicle and was in serious condition, Harborview Medical Center spokesperson Susan Gregg said in a statement.

The zone evolved after weeks of protests in the city over police brutality and racism, sparked by the police killing of George Floyd, a black man, in Minneapolis.

The Sunday shooting followed a pre-dawn shooting on Saturday in a park within the zone that left a 19-year-old man dead and a 33-year-old man critically injured. The suspect or suspects in that first shooting fled the scene, and no arrests had been made as of Sunday, Detective Mark Jamieson had said.

A sign welcomes visitors on East Pine Street during ongoing Black Lives Matter events at the so-called “Capitol Hill Organized Protest” in Seattle, Wash., on June 14, 2020. (David Ryder/Getty Images)

It wasn’t immediately clear where within the zone Sunday night’s shooting took place. The Seattle Fire Department arrived at the scene at 10:46 p.m. and went to a staging area near the zone’s perimeter, fire department spokesperson David Cuerpo told The Seattle Times.

The fire department was soon notified that the injured person has already been taken away. Both victims in Saturday’s shooting—whose identities hadn’t yet been released—were also transported to the same hospital via private car.

Seattle police tweeted that they had heard of a second shooting that they were unable to verify, given “conflicting reports.”

Further details about what transpired Sunday night weren’t immediately available. It wasn’t clear whether anyone was in custody.

The CHOP zone is a several-block area cordoned off by protesters near a police station in the city’s Capitol Hill neighborhood. President Donald Trump, a Republican, has criticized Seattle Mayor Jenny Durkan and Gov. Jay Inslee, both Democrats, for allowing the zone.

Response to Deadly ‘CHOP’ Shooting

Seattle police released the body camera footage of officers responding to the fatal shooting in the CHOP zone over the weekend.

“This is inside the area referred to as the Capitol Hill Organized Protest (CHOP),” the department wrote in a statement. “Officers attempted to locate a shooting victim but were met by a violent crowd that prevented officers’ safe access to the victims.”

The body camera footage showed officers arriving before heading through the zone with guns drawn as angry occupiers yelled profanities and approached the officers.

An officer in the video can be heard yelling: “Please move out of the way so we can get to the victim! All we want to do is get to the victim and provide them aid!”

Protesters are then heard telling the police to “put your guns down.”

“Homicide detectives responded and are conducting a thorough investigation, despite the challenges presented by the circumstances,” the department said.

The president of the union representing a Seattle police union told Fox News that “violence has now besieged the area known as CHOP, and it is no longer the summer of love, it’s the summer of chaos.” He was referring to the flowery “summer of love” comment made by Seattle Mayor Jenny Durkan earlier this month when she described the autonomous zone.

A 1970s-era poster of activist Angela Davis hangs at a boarded up and closed Seattle police precinct on June 21, 2020. (Elaine Thompson/AP Photo)

Washington state Gov. Jay Inslee told reporters in response to the shooting:

“I certainly believe we have to find a way to simultaneously have the community a chance to speak and for police services and importantly fire services to people to be able to be provided. Clearly we need to have a way to provide adequate police and fire protection everywhere in the state of WA including in that area.”

Over the weekend, the New York Post published a written, first-hand account from journalist Andy Ngo, who has long documented the far-left militant group Antifa throughout the Pacific Northwest, about CHOP. Because of a lack of “agreed-upon leadership,” he wrote, “those who have naturally risen to the top have done so with force or intimidation.”

“Though CHAZ claims to have no rules, it quickly developed a complex code of conduct that varied from zone to zone and even the time of the day. For example, those in the garden area, who are mostly white, need to make sure they do not ‘recolonize’ the space,” Ngo wrote, as he detailed random acts of violence in the zone.

via ZeroHedge News https://ift.tt/3hQnQLW Tyler Durden

Futures Swing In Slowmotion Overnight Rollercoaster Tyler Durden

Mon, 06/22/2020 – 08:08

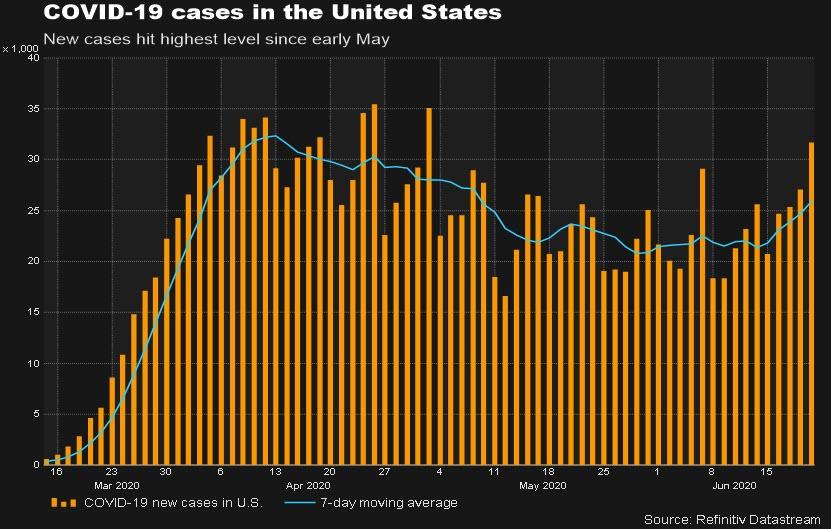

Welcome to a new week, and a new rollercoaster in illiquid overnight futures trading, which saw spoos start off sharply lower on fresh coronavirus concerns after new cases in California rose by a record (4,515) and Florida infections up 3.7% from a day earlier, compared with an average increase of 3.5% in the previous seven days, while the German R-naught surged almost 3x to 2.88 in three days. As a reminder, on Friday stocks slumped late in the day after Apple said that it will again close almost a dozen stores in the US because of a recent rise in coronavirus infections in the South and West, denting the optimism that the US recovery is in full swing.

However, sentiment reversed sharply around 9pm ET when China reported that Beijing saw only 9 new cases suggesting that the latest breakout in the capital had been contained while South Korea saw the smallest daily increase in about a month, prompting renewed optimism that everything is once again under control. Futures then continued their ascent into the early European open, when Eminis rose as high as 3,097 before once again hitting the brakes and reversing modestly lower. Despite the rise in virus cases in Germany and the U.S. states of Florida, California and Texas.

Sentiment was also lifted by the same old news, that there’s growing speculation that politicians will be unwilling to put cities back on lockdown because of the economic toll. Historical stimulus programs by the major central banks are also supporting the sentiment.

European shares also opened lower as much as 1.1% but then quickly staged a sharp rally and nudged into positive territory as a jump in Germany’s coronavirus reproduction rate over the weekend was seen as unlikely to trigger a massive second wave or new lockdowns. Germany’s coronavirus reproduction rate jumped to 2.88 on Sunday from 1.06 on Friday, health authorities said. The spike in infections was mainly related to local outbreaks including in North Rhine-Westphalia.

“I regard the German R statistic as a bit of a red herring or more of a statistical quirk,” said Chris Bailey, Raymond James European strategist. “Coronavirus at-the-margin remains an overhang but the opening up of Europe still looks on much more solid foundations than the US/Americas.”

Meanwhile Germany’s mega-fraud WireCard shed another 50% of its market cap after the company admitted $2.1 billion in cash will never be found. The plunge assured that CEO Braun is facing financial ruins as he no longer has enough shares to cover his €150MM margin loan.

Asian stocks were little changed, with communications rising and industrials falling, after rising in the last session. Markets in the region were mixed, with Thailand’s SET and South Korea’s Kospi Index falling, and India’s S&P BSE Sensex Index and Singapore’s Straits Times Index rising. The Topix declined 0.2%, with Olympic and Land Co falling the most. The Shanghai Composite Index was little changed, with Ningxia Xinri Hengli Steel Wire advancing and Guangdong Songyang declining the most.

Investors are also wary of developments in Hong Kong after details of a new security law for the territory showed Beijing will have overarching powers on its enforcement. China’s top legislative body, the National People’s Congress Standing Committee, will meet on June 28, and the Global Times reported it was likely to enact the Hong Kong security law by July 1.

Hong Kong’s Hang Seng .HSI fell 0.5%, underperforming regional markets.

Torn between record stimulus and growing fears of a second wave of infections, global stocks have been moving sideways in recent weeks after rising more than 40% from March lows on hopes the worst of the pandemic was over.

“Markets have climbed back … with stocks proving the doubter wrong yet again as a world of stimulus trumps the reality of economic and health struggles,” said Joshua Mahony, senior market analyst at IG.

In rates, the 10Y TSY yield dropped to 0.685%, trading around its 50DMA, and back in sideways trading range after false breakout beginning of June. The yield on Germany’s 30-year government debt fell below zero for the first time since May. Crude oil hovered below $40 a barrel in New York. Bunds bull flattened, breaching Friday’s highs and outperforming Treasuries by ~1bp. Gilts bull steepen slightly in a subdued reaction to comments from BOE’s Bailey.

In FX, the U.S. dollar meanwhile slipped from two-and-a-half-week highs as risk appetite remained alive in a world awash with cheap money after credit rating agency Moody’s warned that the stimulus measures will leave advanced economies with much higher debt than they accumulated during the last financial crisis. “Government debt/GDP ratios will rise by around 19 percentage points, nearly twice as much as in 2009 during the GFC … the rise in debt burdens will be more immediate and pervasive, reflecting the acuteness and breadth of the shock posed by the coronavirus.” Moody’s said.

The pound rose for the first time in five days against the dollar after Governor Andrew Bailey indicated that the Bank of England would reduce the size of its balance sheet before considering interest-rate increases. The euro also headed for the first gain since June 15. New Zealand’s dollar and the Swedish krona led G-10 currency gains. U.S. stock futures dictated the market’s mood after a record increase in California’s new virus cases was followed by news that China was containing a resurgence of infections, prompting a rally.

As central banks continued their unprecedented liquidity firehose, gold finally appeared reach to breach $1,750, nearing a seven-year high.

Elsewhere in commodities, oil prices steadied on tighter supplies from major producers, but concerns that the rising coronavirus cases could curb demand checked gains. Brent rose 0.2% to $42.25 a barrel, while WTI fell slightly to $39.65 a barrel.

Market Snapshot

S&P 500 futures up 0.7% to 3,082.25

STOXX Europe 600 down 0.2% to 364.83

MXAP down 0.09% to 159.14

MXAPJ down 0.06% to 513.47

Nikkei down 0.2% to 22,437.27

Topix down 0.2% to 1,579.09

Hang Seng Index down 0.5% to 24,511.34

Shanghai Composite down 0.08% to 2,965.27

Sensex up 1.2% to 35,159.56

Australia S&P/ASX 200 up 0.03% to 5,944.54

Kospi down 0.7% to 2,126.73

German 10Y yield fell 1.7 bps to -0.432%

Euro up 0.3% to $1.1209

Brent Futures up 0.02% to $42.20/bbl

Italian 10Y yield fell 2.2 bps to 1.229%

Spanish 10Y yield fell 1.9 bps to 0.474%

Brent Futures up 0.02% to $42.20/bbl

Gold spot up 0.2% to $1,747.44

U.S. Dollar Index down 0.2% to 97.41

Top Overnight News from Bloomberg

Germany’s coronavirus infection rate rose for a third day, lifted by local outbreaks including in the region of North Rhine-Westphalia, where more than 1,300 people working at a slaughterhouse tested positive.

Beijing reported only nine new infections, a sign that a recent outbreak is under control. China blocked poultry from a Tyson Foods plant where many workers tested positive

The European Central Bank’s most determined attempt yet to confront the German legal headache bedeviling its quantitative easing policy may emerge as soon as this week.

Bank of England Governor Andrew Bailey signaled a major shift in the central bank’s strategy for removing emergency stimulus, stressing the need to reduce the institution’s balance sheet before hiking interest rates.

Asian equity markets began the week cautiously as sentiment was clouded by reports of increasing COVID-19 infections rates globally in which the World Health Organization reported a record daily increase of 183k cases, while new cases in the US topped the 7-day average and Germany’s reproduction rate surged to 2.88 from 1.79. This initially pressured US equity futures at the open and also weighed on ASX 200 (U/C) and Nikkei 225 (-0.2%), although US index futures have since fully recovered and Asia-Pac bourses also retraced their early declines with outperformance seen in commodity-related sectors, in particular Australia’s gold miners after the precious metal resumed its rally and broke above the USD 1750/oz level. Hang Seng (-0.5%) and Shanghai Comp. (-0.1%) were mixed with price action rangebound after the PBoC maintained its 1-year and 5-year Loan Prime Rates at 3.85% and 4.65% respectively as expected, while it also conducted a CNY 120bln net liquidity injection which was welcomed by mainland bourses. Furthermore, there were reports that China is planning to step up purchases of US farm goods following recent discussions and that President Trump deferred sanctions on Chinese officials related to Uighur minorities as it may impact the US-China trade deal, although Hong Kong lagged after the release of the draft Hong Kong National Security Law which the Standing Committee of the NPC is speculated to enact when it meets on June 28th-30th. Finally, 10yr JGB traded subdued as the intraday recovery in Japanese stocks weighed on bond prices but with downside also cushioned by the BoJ’s presence in the market for over JPY 1tln of JGBs with 1yr-10yr maturities and with the Japan Securities Dealers Association noting regional banks bought a record amount of ultra-long JGBs last month.

Top Asian News

Hong Kong Central Office Vacancies Reach 12-Year High: JLL

Japan Industry Group May Penalize Banks Breaking Debt Sale Rules

Virus- Drug Nod Spurs Record Rally in India’s Glenmark Pharma

The Most Popular U.S. Bond Market Trade Has Now Gone Global

Europe kicked the week off on the back-foot but have since nursed a bulk of its losses [Euro Stoxx 50 -0.4%] as initial downside stemmed from second wave woes amid record daily increases recorded by the WHO, Germany’s R-number jumping amid cluster outbreaks and with the US cases rising above its key 7-day level. Nonetheless, stock markets continued on its upwards trajectory since the cash open despite light fundamental news-flow. Note, the EU-China summit is underway but with expectations low. Sources noted there will be no joint communique between the sides this year – but, the meeting with Germany could prove to be interesting as the country will be taking the baton of rotating EU presidency in H2 2020; note, Germany has previously signalled a tougher EU line towards China. Nonetheless, bourses regain earlier lost ground alongside sectors – now mixed following an all-negative open – but still fail to indicate a clear risk tone. The sectorial breakdown also provides little clarity on this front as Oil & Gas, Travel & Leisure and telecoms remain the laggards. In terms of individual movers, Wirecard (-36%) shares continue to suffer after the group announced the missing EUR 1.9bln likely never existed, whilst it withdrew its prelim FY19 and Q1-2020 results. Separately, former CEO Braun – who was the largest individual shareholder – is reportedly unloading a large amount of his 7% stake in the Co. Elsewhere, Lufthansa (-6%) shares are weighed on after its CEO stated that the EUR 9bln state-backed aid is at risk of not passing the upcoming shareholder vote as only around 40% of shareholders have registered to vote at the EGM thus far vs. required 2/3 majority for it to pass. On the flip side, BT (+1.9%) remains supported by reports that the Saudi Public Investment Fund is said to have been acquiring a stake in the Co. through open-market purchases over the last few weeks, according to sources.

Top European News

Lufthansa Braces for Portentous Week With Future on the Line

Turkish Stocks Erase 2020 Losses After Wave of Local Buying

Halkbank, Involved in U.S. Case, Jumps After Berman Resigns

In FX, the Greenback is weaker across the G10 board with only the Yen underperforming, and then only marginally vs the scale of recovery gains forged by other majors. Further increases in coronavirus infections and fatalities appear to be weighing on the Buck even though the US is far from alone in terms of suffering fresh outbreaks. Indeed, the KCDC is reportedly classifying the situation in South Korea as a 2nd wave as the global tally hit the highest level so far for a single day, according to the WHO and Germany’s R value rebounds to 2.88. However, the DXY has slipped back below 97.500 to a 97.287 low from last Friday’s 97.727 high ahead of May’s national activity index, existing home sales and a late speech from Fed’s Kashkari.

AUD/NZD/GBP/SEK/EUR – The Aussie is back within striking distance of 0.6900 vs its US counterpart and not too unsettled by comments from RBA Governor Lowe overnight reiterating that rates are likely to remain at current levels for years, as he also seemed unfazed by the Aud’s present valuation. Meanwhile, the Kiwi has reclaimed 0.6400+ status ahead of the RBNZ policy meeting with markets all but ruling out any chance of a change in rates, but Sterling’s comeback from the low 1.2300 area towards 1.2435 is somewhat less easy to reconcile and may have more to do with Eur/Gbp flows/direction as the cross pulls back from 0.9065 to test bids said to be sitting at 0.9025. Note also, 1.85 bn option expiries at 0.9060 may be capping the cross ahead of the NY cut after Sterling shrugged off an improvement in CBI trends. Elsewhere, the Swedish Crown is also perky against the single currency and perhaps drawing some traction from the latest Riksbank business survey revealing stabilisation in May and June, though the Euro has clawed back gains vs the Dollar from circa 1.1168 to hover between decent expiry interest at 1.1200-05 (1.9 bn) and 1.1245-50 (1.24 bn) ahead of flash Eurozone consumer confidence and ECB speeches via de Guindos and Lane.

CAD/CHF/NOK – Also on a firmer footing to at least start the new week, with the Loonie nearer the top of a 1.3560-1.3630 range vs its US peer awaiting comments from BoC Governor Macklem, the Franc back above 0.9500 in wake of latest weekly Swiss bank sight deposits showing a dip in both domestic and total balances and the Norwegian Krona consolidating post-Norges Bank advances either side of 10.8000 against the Euro.

JPY/XAU – As noted above, the Yen is bucking the broad trend, but still keeping its head over 107.00 and Gold has lost some steam after surging above Usd 1750/oz and stalling ahead of the next major bullish technical target around Usd 1765 from May 18.

In commodities, WTI and Brent August contracts remain choppy and reside within a tight range, albeit the benchmarkes have nursed opening losses of around 1%, which originally emanated from COVID-19 second wave woes as the WHO reported a record daily increase of 183k cases, while new cases in the US topped the 7-day average and Germany’s R-rate spiked to 2.88 from 1.79. Meanwhile, Nigeria and Angola will be presenting their respective over-compliance plans today after failing to do so last week – with a presser expected following a review of the strategy – albeit, this has not been confirmed. Meanwhile, a new study shows that US shale companies could be forced into writing down at least USD 300bln of assets in Q2 as producers account for the oil price collapse earlier this year on balance sheets, which will be based on an oil price around USD 35/bbl according to the FT. WTI August fluctuates on either side of USD 40/bbl (vs. 39/bbl low) whilst its Brent counterpart tested resistance at USD 42.50 (vs. 41.58/bbl low) earlier in the session. Elsewhere, spot gold has given up some recent gains amid the recovery in stocks, but nonetheless currently remains underpinned by a weaker USD – with the yellow metal trading on either side of USD 1750/oz early-doors before printing a marginal new session low at USD 1741.90/oz. Copper prices are supported by the softer Buck and continues to trend higher amid support from draws in LME and China inventories. In terms of bank commentary, Citi sees gold prices at an average of USD 1702/oz this year and USD 1761/oz next year, whilst the bank forecasts copper at USD 5654/t in 2020 and 5850/t in 2021.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, prior -16.7

10am: Existing Home Sales, est. 4.09m, prior 4.33m; Existing Home Sales MoM, est. -5.59%, prior -17.8%

DB’s Jim Reid concludes the overnight wrap

Hard to believe we’re now going to have to deal with the nights slowly getting darker again here in the northern hemisphere. We spent the longest day yesterday at the beach and I think we’ll be discovering sand in various places across the house, car and bodies for the next week. It’s a horrendously messy thing to do, especially when the showers were closed for social distancing reasons. It is amazing what the bracing sea air does though as bed time went without incident last night, which is a rarity. They were all shattered.

It was amazing how busy the beach was but people generally practiced social distancing unless they were just deliberately keeping out the way of my horrors. It’s a strange period where life is getting slowly back to some kind of normality, but with major constraints and with everyone waiting to see what happens next. Indeed the virus spread continues to create a lot of uncertainty in markets. For example, does it matter that the troublesome US states are continuing to see case numbers increase or does it provide some good news that economies can stay open as cases rumble on? It’s possible that with more knowledge on the virus, the vulnerable are now being better protected which will dramatically reduce the fatalities if successful.

Even in countries that are perceived to have had a good response to the crisis are having issues. Last week we highlighted the reports out of Germany of a meat factory closing due to a rash of infections. Over the weekend, the Robert Koch Institute estimated that the effective reproduction factor of the virus was now 1.79 in the country after being 1.06 on Friday, and below 1.0 earlier in June. Yesterday there were over 600 new cases in the country, with the 7 day average of new cases over 500 for the first time in 5 weeks. It will be interesting to see how they deal with this small uptick that has shades of a second wave. China is also seeing a mini second wave with the country now having averaged around 40 new cases per day for the last week, after seeing low single-digit new cases per day all through May and early June. Beijing has closed schools and asked those who can to work from home when possible. In a positive sign, Beijing reported only 9 new cases overnight.

Elsewhere Brazil is still engulfed in their first wave passing 1 million total cases over the weekend, and registering 54,711 new cases on Friday, the most new cases in one day for any country in the world. They did have a small reporting backlog though. Nevertheless cases have risen by 3.3% per day over the last 7 days, in line with the 7 day period prior at 3.4%. The other virus hotspot is the US. After registering multiple days with daily case growth under 1.0% in the early part of June, cases have been rising at 1.5% per day on average over the last week, higher than the 1.2% average for the period previous. The majority of these cases are in large Southern states like Texas, Florida, and Arizona, but California continues to have similar problems. All four states currently have a 7-day average of new cases higher than the period prior, implying that the virus spread is accelerating and no longer even flat.

Using rtlive’s estimates, whose underlying methodology was updated over the weekend, 24 of the 50 US states now have effective transmission rates over 1.0. Of the main focus states, California has been trending higher for the last month and after falling back below 1.0, it is now at 1.05. Florida is at 1.39 and Texas at 1.16.

So plenty of worrying news on the virus at a global level but there are still signs that technicals in the market look supportive. Doing my weekend reading of DB research it was interesting to read our equity strategist Binky Chadha’s latest view where he suggested positioning in US equities has dipped again to the 5th percentile. He suggested that such low positioning is historically associated with strong performance of the market 1 week and 1 month forward. See here for more. A reminder that when Binky discussed the low positioning a few weeks ago one of the main justifications for that during a big rally was the emergence of new retail investors into the market with institutional investors remaining relatively on the sidelines.

A quick check on markets this morning now where broadly speaking most Asian bourses have pared a weak open. The Nikkei (+0.31%), Shanghai Comp (+0.28%) and ASX (+0.47%) are now showing modest gains while the Kospi is flat and the Hang Seng down -0.32%, likely not helped by news over the weekend that China has proposed a national security law that would allow the Beijing to override Hong Kong’s independent legal system. Elsewhere, futures on the S&P 500 are trading up +0.65% after erasing losses at the open of c. -1%.

In other weekend news, a Bloomberg story has argued that a change in the composition of Germany’s Constitutional Court has the potential to be less confrontational towards the ECB. Astrid Wallrabenstein, seen as more EU friendly, will replace Andreas Vosskuhle, president of the court whose term has expired and made the May 5 ruling on the ECB bond purchases while, Stephan Harbarth, a conservative lawmaker from 2009-2018, will become the new president. German daily Frankfurter Allgemeine Sonntagszeitung has already reported Wallrabenstein saying that it could be in the interest of the court to take an easier stand if the “demands are being taken seriously” and the actions taken by politicians, the German central bank and ECB “go into the right direction.” This comes on the back of Friday’s news that the ECB is preparing papers on proportionality of the PSPP to satisfy the GCC.

Staying with Europe, Italian PM Conte has indicated that his government would likely seek a wider budget gap as the government will focus on infrastructure projects including high-speed railways and may approve a value-added tax cut to stem the coronavirus’s impact. He said, “We will probably need to intervene for a further widening of the budget gap because the resources are not enough to cope with the impact of a horrible year both economically and socially,” while, adding that the government will present its reform plan in September. The reform plan is in response to lobby for the country’s share of a proposed EUR 750bn recovery fund.

The main highlight this week is likely to be the flash PMIs for June tomorrow, with manufacturing, services and composite PMIs coming out from around the world. Back in May, the PMIs rebounded from April’s rock-bottom prints. For example, the Euro Area composite PMI rose to 31.9 from 13.6, while in the US the composite PMI recovered to 37.0 from 27.0. For June the range of expectations across Europe/US are generally in the 40s with U.K. at the lower end and the US manufacturing possibly scraping to just over 50. Given these are diffusion indices and simply reflect whether conditions are getting better or worse then surely at some point soon these numbers are going to massively spike up regardless of the actual level of growth.

There are various other data releases but it’s not a big week for data. See the day by day calendar at the end for the full slate. Note that the IMF’s latest economic forecasts are released this Wednesday. In a website blogpost last week, their Chief Economist Gita Gopinath said that the update “is likely to show negative growth rates even worse than previously estimated.”

Looking back at last week now, Global equities finished higher but there feels like there is a bit more two way tension in asset markets now. Nevertheless, the significant amount of liquidity in the financial system and a steady drip of improving data outweighed concerns of a rise of covid-19 cases in China and Germany (albeit from low levels) as well as in the largest US states. The S&P 500 rose +1.86% (-0.56% Friday as Apple reversed a decision to reopen some stores in high case states). The index is now down -4.12% YTD. The last two weeks have seen growth stocks go back to outperforming in the US, with the tech-focused Nasdaq finishing this past week up +3.73% (+0.03% Friday). European equities also outperformed the S&P, with the Stoxx 600 rallying +3.22% (+0.56% Friday) over the five days. The rally was widespread with the DAX (+3.19%), FTSE MIB (+3.87%), FTSE 100 (+3.07%), and CAC (+2.90%) all gaining on the week. Asian indices also rose but to a lesser degree. The Nikkei rose +0.78% over the week (+0.55% Friday) while the CSI 300 was up +2.39% (+1.34% Friday), and the Kospi rose +0.42% (+0.37% Friday). The CSI 300 joined the NASDAQ as one of the few equity indices in the world that is up on the year, closing Friday +0.05% YTD.

Oil prices rallied for a 7th week out of the last 8 as OPEC+ gave reassurances on output cuts on Thursday. Expectations for demand also continues to slowly improve. WTI futures rose +9.62% (+2.34% Friday) to $39.75/barrel and Brent crude rose +8.93% on the week (+1.64% Friday) to $42.19/barrel. With risk assets rising and sentiment staying generally constructive, HY credit spreads on both sides of the Atlantic tightened on the week. European HY cash spreads were -15bps tighter on the week (+2bps Friday), while US HY cash spreads were -26bps tighter (+1bp Friday). Euro IG and US IG cash spreads were -3bps (+1bp Friday) and -12bps (-1bp Friday) tighter, respectively.

Peripheral debt tightened, with Spanish 10yr yields -12.6bps tighter to German bunds over the 5 days, while Italian BTPs were -11.4bps tighter, and Portuguese bonds tightened -8.5bps. Core sovereign bonds were little changed on the week as US 10yr Treasury yields fell -1.0bps (-1.5bps Friday) to finish at 0.694%, while 10yr Bund yields rose +2.4bps over the course of the week (-0.8bps Friday) to -0.42%.

The main highlight from last Friday was the European Council meeting where leaders were cautious, but still constructive on a Recovery Fund agreement. German Chancellor Merkel mentioned that an agreement had been reached on the mixture of grants and loans, while Austrian Chancellor Kurz said that grants would be possible, with conditionality. It feels like compromise is slowly building even if we’re not yet there. On the data front, the main two headlines were out of the UK. Public finance data for May showed the government’s debt-to-GDP ratio rose above 100% for the first time since 1963. Retail sales in the UK rose +12.0% MoM during May, well above the expected rise of 6.3% and recovering from last month’s revised -18.0% fall.

via ZeroHedge News https://ift.tt/311Ifrj Tyler Durden

Nearly 9 Million Infected As WHO Says Outbreak Still “Accelerating” Following Largest Daily Jump: Live Updates Tyler Durden

Mon, 06/22/2020 – 07:52

The international community kicked off the summer with some disturbing news from the WHO: the NGO’s tally of newly reported cases showed that Sunday marked the biggest single-day jump in new cases since the outbreak began, with most of these cases coming from North and South America.

As the WHO insisted that the virus is still “accelerating” which it warned about last week, Brazil reported more than 50k new cases in a single day – a record unmatched even by the US – while the worsening outbreaks along the American Sun Belt (which encompasses parts of the South and West) contributed more than 30k cases, nearly half the international daily total.

As Florida and Texas officially surpass NYC as the virus epicenter of the US, the country’s largest city on Monday entered the official start of ‘Phase 2’ of its reopening plan.

The US hasn’t reported more than 31k cases in a day since May 1.

As the number of new cases in the US, Mexico, Brazil and India spirals out of control, a growing body of research suggests the virus likely started to circulate in and around Wuhan, and even in some areas in Europe and the US, as early as October or September. Now, according to a report in the LAT, California officials are slowly reexamining deaths in cases of unexplained respiratory failure or inflation to see if a mysterious syndrome impacting children might have caused any of the deaths.

The deaths date back as early as November, more than two months before the first documented coronavirus death in the US was confirmed on Feb. 6. China’s first “confirmed” case was identified in Wuhan on Dec. 8, with the onset of symptoms believed to have occurred around Dec. 1.

As Spain enters the last phase of its reopening plan, which includes reopening the country’s tourism industry for the first time in more than 3 months, Dubai authorities announced late Sunday that the country would once again be allowing in tourists starting on July 7, while allowing locals to begin traveling again as early as Monday. Travelers visiting the country will however need a clean bill of health.

Spain will decide this week which visitors from outside Europe can enter as it welcomes back travellers from neighbouring nations in an effort to revive a tourism industry hammered by the coronavirus lockdown, a minister said.

While the US death toll topped 120k and the Brazilian death toll topped 50k over the weekend, worldwide, at least 8.9 million people have been confirmed to be infected. At least 4.4 million have recovered, while more than 467,000 people have died, according to Johns Hopkins data.

A growing list of US states and countries, from California to Bulgaria, have been mandating that masks be worn indoors, while Kazakhstan plans to impose a two-day lockdown in the northern city of Kostanay, along with four nearby towns next weekend after a jump in fresh COVID-19 cases.

As India continues to report record numbers of new cases, the outbreak in neighboring Pakistan continued in the top 10 countries for daily coronavirus-case increases, with 4,471 new cases on Sunday, bringing its tally to 181,088 to date, according to government data. At least 89 people died of the virus on Sunday, taking its death toll to 3,661.

After a handful of American MLB players tested positive over the weekend, Serbia just announced that five players on the champion Serbian football squad Red Star Belgrade have tested positive for the coronavirus.

In the UK, officials are finally moving away from uncomfortable swab tests to “no-swab” saliva tests, which are being trialed in Southampton, southern England, and could result in a simpler and quicker way to detect outbreaks of the virus, the UK government said.

Meanwhile, Johnson on Monday is set to unveil his government’s latest lockdown easing plan and the results of a review of the “2-meter rule” on Tuesday, with rumors about the possibility that the gov’t will swap this out for a “one-meter rule”.

Furthermore, UK Health Secretary Hancock suggested customers may need to register when visiting pubs and restaurants, while it was separately reported that the UK government may announce foreign travel could resume from July 4.

The mayor of Seoul said Monday that he fears the country is losing control over the virus, and will reimpose stronger social-distancing measures if the daily jump in infections does not come below an average of 30 cases over the next three days, which is lower than the most recent daily numbers reported.

“If Seoul gets penetrated (by the virus), the entire Republic of Korea gets penetrated,” Park Won-soon said in a televised briefing. He also lamented what he described as complacency of citizens in social distancing, citing an increase in public transportation usage that he says has been approaching last year’s levels in recent weeks.

Russia reported 7,600 new cases on Monday (remember, cases are reported with a 24-hour delay), pushing its nationwide case total to 592,280, the world’s third-largest tally.

Hong Kong recorded around 30 new imported COVID-19 cases on Monday, marking the largest daily jump in two months, per the SCMP. Officials in Beijing, meanwhile, touting a “cliff-like” drop in new cases by the end of this week with efforts to control the spread of infections in the Chinese capital underway, said an “expert” from China’s national health authority. The city of more than 20 million people reported its first case linked to a wholesale food market on June 11. So far, 236 people have been infected in the worst outbreak in Beijing since COVID-19 was identified. Beijing reported just nine new cases for Monday so far, a sharp drop from 22 a day earlier.

via ZeroHedge News https://ift.tt/2AXFlJv Tyler Durden

Wirecard Shares Down 50% As Company Admits Missing Cash Won’t Ever Be Found Tyler Durden

Mon, 06/22/2020 – 07:04

Germany’s once-prized fintech giant Wirecard is teetering on the brink of bankruptcy now that both the disgraced company and its “Big Four” auditors have finally acknowledged that €1.9 billion euros ($2.1 billion) of cash missing from its reserves will probably never be found.

The acknowledgement, confirmed Monday by a flurry of press reports, caused the price of Wirecard shares to halve once again, falling by 45% at its peak, before bouncing slightly.

Per CNBC, the search for the missing cash hit a dead-end after two Asian banks, the Philippines-based BDO and BPI, both denied having Wirecard as a client. Furthermore, the Philippines’ central bank said Sunday that the money hadn’t even entered the country’s financial system, exposing yet another one of Wirecard’s probably-improvised lies as just that.

“The initial report is that no money entered the Philippines,” Bangko Sentral ng Pilipinas Governor Benjamin Diokno said Sunday, adding the names of BDO and BPI were used “in an attempt to cover the perpetrators’ track.” Both banks claimed rogue employees falsified documents to indicate the existence of the funds, suggesting that whistleblowers’ claims that the money never existed are probably true.

Wirecard CEO Markus Braun quit on Friday one day after the company said EY had refused to sign off on WC’s 2019 accounts. Before leaving, the CEO claimed the company had been the victim of “considerable fraud” (whistleblowers, on the other hand, have described a culture where accounting fraud like this was encouraged to pacify regulators and overhype investors).

According to Bloomberg sources, Braun is facing a massive margin call as Deutsche Bank has issued a margin call on a €150MM loan pledged by shares that have lost 72% of their value following news that billions in company cash have gone missing. Braun, who holds 7% of Wirecard’s shares and is the company’s biggest shareholder, did what so many CEOs have done, and funded a €150 million margin loan that was secured by the value of the underlying stock. However, last week’s plunge has triggering a margin call liquidation of these shares which no longer cover the full value of the loan.

In 2017, Braun – who has invested tens of millions of euros of his own funds into the firm and owned 8.7 million shares of Wirecard as of June 19 – secured the loan from Deutsche Bank (there’s that name again) by pledging 4.2 million shares, or just under half of his personal stake. When the stock was trading above €100/share the overcollaterialization cushin was generous, giving the loan an LTV of well below 50%. However, with the stock now trading at €25, there is a €50MM shortfall in the loan and DB is rushing to collect on whatever it can.

At one point, BaFin, the German regulator, even barred short-selling in Wirecard’s shares, an extremely unusual action that was widely criticized at the time, and only looks worse in retrospect.

Braun

As expected, it has been rough going for Wirecard shares since they gapped lower at the open in Frankfurt.

With no outright buyers waiting in the wings, an analyst from Citi declared that this is the end of the road for Wirecard, thought not exactly in those words. “The KPMG/E&Y audits and this morning’s announcement lead to such uncertainty over the financials that we are unable to quantify the true profile of the business with conviction. If the company can navigate through the current turmoil, we believe it will still be hard to restore confidence in WDI itself,” Citi analyst Robert Lamb said.

What’s the next shoe: WireCard is funding a meth empire in New Mexico?

President Donald Trump’s “America First” agenda has reignited conservatives’ love affair with nationalism, with National Review‘s Rich Lowry (a onetime NeverTrumper) and Israeli political theorist Yoram Hazony publishing books in the last few years arguing that America needs a nationalist revival to rebuild fraying social cohesion.

The truth is the opposite: Cultural nationalism will dissolve the glue that binds Americans—namely, their commitment to the founding principles of equality, individual rights, and human dignity.

When I came to America 30 years ago, it was obvious to me—as it was to French philosopher Alexis de Tocqueville 200 years earlier—that Americans not only love but also like their country. American patriotism, Tocqueville observed, is very different from the Old World variety that regarded the nation as the father and citizens as his offspring. Americans see their country as their offspring and themselves as its creator. It’s the result of their actions if not their designs, as the economist F.A. Hayek might have put it.

Americans believe in spontaneous and uncoerced expressions of patriotism, such as displaying the American flag outside their homes and beginning sporting events with a heartfelt rendition of the national anthem. That’s not the case in my native India, where Republic Day celebrations involve a massive parade by various military divisions. Four years ago, after India came to blows with Pakistan, the Indian Supreme Court briefly ordered not only that movie theaters play the national anthem but that viewers stand up for it.

That’s hard to imagine in America. In fact, precisely because the country exists for the sake of individuals and not vice versa, the First Amendment protects the right to use national symbols for protests, such as taking a knee during the anthem. This makes it more apparent when a course correction by the government is needed, making the country more worthy of affection.

The other striking thing about the American identity is that it does not define itself as against something else. If Pakistan and Islam were to disappear from the face of the Earth, there would be nothing left to sustain Indian nationalism. But America’s ideals anchor it. The demise of communism didn’t diminish America’s self-conception. It vindicated it.

Hazony claims in The Virtue of Nationalism (Basic Books) that America’s classical liberalism is fundamentally imperialistic because its political principles are deduced from Lockean notions of universal human nature. He thinks that leads to a crusading moral universalism that denies the validity of alternative principles of national self-determination. But America doesn’t have to try to universalize its ideals; the universe embraces them on its own, as the post–Cold War wave of democratization demonstrated.

Pre-Trump America wasn’t immune from the “us vs. them” mentality, and Trump isn’t the first person to campaign on it. He is, however, the first president in living memory to win America’s highest office by characterizing Mexican immigrants as “rapists and criminals” and Mexico’s failure to stop unauthorized border crossers as a threat to American sovereignty. Instead of rejecting this kind of nationalism, conservatives are putting a respectable intellectual foundation beneath it, as if borrowing German philosopher Carl Schmitt’s notion that the core of political life requires a cultural enemy.

And what is this new enemy? Mass immigration from non-Western countries, primarily. In The Case for Nationalism (Broadside Books), Lowry attempts to sanitize the case for blood-and-soil nativism, arguing that “an exclusively idealistic account of America is a mistake” and “the criterion for citizenship in the United States is not attachment to a set of ideas but birth within our borders.” He castigates President George W. Bush’s statement that “our identity as a nation, unlike other nations, is not determined by geography or ethnicity or soil or blood” as “willful ignorance.” He claims it denies “the contribution of geography or land to our identity.” Lowry insists that celebrating the “beauty and bounty of our land in the most exalted terms” ought to inform our understanding as Americans, along with the fact that our ancestors are buried here.

The most charitable explanation for Lowry’s project is that he is trying to articulate a nonracial, nonreligious criterion in which to anchor a thick understanding of American nationalism. He wants America to remain broadly inclusive of those whose families have been here for a long time but not so inclusive that relative newbies can waltz into the club at will. But if America’s principles are not enough to anchor a robust nationalism, and if race and religion are off the table, then ancestry and geography—blood and soil—are the only candidates left. To that end, Lowry wants to radically slash immigration, and National Review writers including Reihan Salam have advocated scrapping birthright citizenship. Meanwhile, NationalReview.com Editor Charles C.W. Cooke wants more stringent criteria for judging who is worthy of naturalization.

But that would make America less—not more—patriotic, because it’ll sever it from a great source of patriotism: immigrants. Most immigrants, even more than many natives, viscerally appreciate America, because they know what it’s like to live in an unfree country.

Lowry’s deification of land and ancestry doesn’t just work against immigrants. Once a criterion to judge “outsiders” is established, it’ll inevitably be applied to “insiders” as well. Hindus, Muslims, Jews, and other religious minorities without the very deepest roots might easily be viewed as lesser Americans. Regardless of his intention, Lowry’s scheme would establish a test that many citizens of this country simply couldn’t pass. By declaring that there is only one way to be an American, he denies many individuals and communities the chance to define their own relationship with the United States and formulate their own reasons to love it.

What’s more, if the nationalist project is serious, it will require state aggression. This is precisely what’s happening in India, where Prime Minister Narendra Modi is demonstrating what it takes to convert a liberal democracy into a robustly nationalistic one. Hindu extremists have long touted a full-throated blood-and-soil nationalism called “Hindutva,” which says the only true Indians are those whose holy sites sit on hallowed Indian soil. This definition includes Hinduism and its offshoots: Buddhism, Jainism, and Sikhism; it excludes India’s 140 million Muslims and 30 million Christians, whose holy lands lie in the Middle East.

Hindutva’s goal is to purge India of these “foreign” religions and return to the halcyon days when only true Indians roamed the subcontinent. To that end, Modi’s home minister announced plans to create a national registry of citizens, allowing the government to distinguish unauthorized residents in the country. Only those among India’s 1.3 billion residents who produce papers showing that they have ancestors dating back to some cutoff year will be included on this list.

This is an impossible task for millions of Indians, especially poor ones: Many of them don’t even know their own birth dates, let alone have their grandfathers’ birth certificates. So Modi ramrodded through parliament a law that non-Muslims who can’t produce documents will be granted expedited citizenship. But paperless Muslims will be out of luck even if they have ancestors going back generations.

The Indian experience shows that a program of nationalism does not enhance “mutual loyalty” among citizens, as Hazony wants. That’s because it empowers the state to judge citizens not by their loyalty to each other but by their loyalty to the state’s aims and methods. In Modi’s India, it is not just Muslims and Christians who are considered less Indian. Hindus who don’t dutifully line up behind Hindutva’s ideas are attacked as anti-nationals. Predictably, this project has made the population more polarized.

A program of nationalism that empowers the government to slice and dice people into an in-group and an out-group will backfire badly. It will be simultaneously oppressive and divisive, sundering—not soldering—the country.

from Latest – Reason.com https://ift.tt/2BxQvEw

via IFTTT