Yesterday I highlighted former judge Michael Luttig’s critique of Judge Emmet Sullivan’s handling of the Department of Justice’s motion to dismiss the charges against former National Security Advisor Michael Flynn.

Stuart Gerson, who served as Assistant Attorney General in the George H.W. Bush Administration and briefly as Acting Attorney General, has a response to Luttig’s op-ed in today’s Washington Post. Here’s a taste:

Luttig argues in his op-ed that the appeals court should step in to replace the advisory counsel that Sullivan selected to argue against the motion to dismiss, block the receipt of briefs from friends of the court (including one in which I participated), and name a new trial court judge to oversee the case. With due respect, he is wrong on all counts. . . .

This would be unwarranted, unfair and an inefficient use of judicial resources. Sullivan has overseen the Flynn case, has accepted his guilty plea and is well-versed in the facts. He has done nothing improper in dealing with the extraordinary move by the government, at the 11th hour, to abandon its own case. He is an independent thinker who has stood up to the Justice Department before, most notably in using an outside counsel to uncover the tarnished prosecution of the late Sen. Ted Stevens (R-Alaska.) In this situation, that is an asset, not a demerit.

Sullivan’s concern about the gravity and complexity of the issue before him is understandable, as is his effort to establish mechanisms to help ensure that he has the benefit of a competing view now that the government has aligned itself with the defense’s effort to end the case. The D.C. Circuit should let him proceed.

from Latest – Reason.com https://ift.tt/3ccd52i

via IFTTT

Less than a day after two members of the House of Representatives salvaged an amendment to block federal law enforcement from secretly accessing Americans’ private web and browser search histories, the proposal has lost support and faces an unclear future.

Reps. Zoe Lofgren (D–Calif.) and Warren Davidson (R–Ohio) announced on Tuesday that they had successfully revived a Senate amendment to the USA Freedom Reauthorization Act (H.R. 6172) that would stop the FBI and other federal agencies from using the Foreign Intelligence Surveillance Act (FISA) court to secretly obtain Americans’ online records from third parties, such as internet service providers.

Initially introduced by Sens. Ron Wyden (D–Ore.) and Steve Daines (R–Mont.), the amendment died in the Senate by a single vote earlier in March due to the absence of several senators, some of whom may have voted in favor had they been present. This past weekend, Lofgren and Davidson coordinated a plan to revive the amendment for reconsideration in the House.

But cracks developed Tuesday evening within the bipartisan coalition, and now it appears Wyden is withdrawing his support for Lofgren and Davidson’s adaptation of his amendment. The New York Timesreports that House Intelligence Committee Chair Rep. Adam Schiff (D–Calif.) suggested that the bill doesn’t protect Americans as thoroughly as Wyden and Lofgren say it does. Charlie Savage at The New York Times reports that:

Mr. Schiff put forward a narrower emphasis. Stressing the continued need to investigate foreign threats, he described the compromise as banning the use of such orders “to seek to obtain” an American’s internet information.

That formulation left open the possibility of interpreting the potential new law as banning only deliberate attempts to collect an American’s data, leaving the F.B.I. free to ask for lists of all visitors to websites despite the risk that the list may turn out to incidentally include some Americans.

One traditional means by which courts interpret ambiguously written statutes is by looking at evidence of legislative intent—like statements by lawmakers explaining what they believed a bill would do before a vote—so such statements may in part be an attempt to create fodder to argue about what the compromise language means in future litigation.

Because Schiff suggested that the amendment could be interpreted by law enforcement to allow for the incidental collection of Americans’ browser and search records, Wyden subsequently pulled his support for Lofgren’s and Davidson’s version and suggested that his original version be reconsidered. Progressive tech privacy group Demand Progress put out a statement Tuesday night in which it opposed Lofgren’s and Davidson’s amendment and encouraged representatives to vote against the Lofgren-Davidson amendment and the underlying USA Freedom Reauthorization Act, to which their amendment (or Wyden’s) would be attached.

This morning, Lofgren and Davidson defended their amendment at a House Rules Committee hearing that seemed mostly supportive, though some committee members echoed concerns that the House version did not adequately shield Americans from secret surveillance or preserve Fourth Amendment due process protections.

At the hearing, Lofgren said she didn’t believe there was any ambiguity in her amendment (read it here), but that if there were any doubts, she’d be happy to support an amendment that more precisely mirrored the Wyden-Daines Senate amendment (read it at the top of the first page here), which bluntly forbids the feds from any order calling for the collection of “internet website browsing information or internet search history information.”

Lofgren was polite about Schiff’s comments but insisted there was really no ambiguity in the wording of her amendment. She also noted that the Senate passed another amendment to the bill that requires the FISA court to consult with an independent adviser should government officials attempt a “novel” interpretation of the law that would grant them access to the private records of Americans or people legally in the United States.

Davidson, as a Republican, was much blunter.

“Schiff has attempted to fracture the coalition by saying things he’s known to be false,” Davidson said. Schiff, along with Rep. Jerry Nadler (D–N.Y.), is a cosponsor of the USA Freedom Reauthorization Act. As I’ve noted previously, their proposed reforms to the surveillance law, while welcome, are very mild. The reauthorization formally eliminates the mass metadata collection program revealed by National Security Agency (NSA) whistleblower Edward Snowden. But the NSA had already abandoned this program because it consistently violated Americans’ privacy while not actually helping catch terrorists.

Amendments like those from Wyden and Lofgren are intended to shore up the rather limp reforms offered by Schiff. Despite criticisms that the bill is not protective enough, the Senate’s edition of the FISA advisor amendment cited by Lofgren and the House’s consideration of the Wyden-Daines amendment led the Justice Department to revoke its support. Assistant Attorney General Stephen E. Boyd put out a statement this morning opposing the amended renewal bill as well as Lofgren’s proposed amendment, claiming the bill will damage the Justice Department’s ability “to identify and track terrorists and spies.” The DOJ is recommending that Trump veto the legislation.

Trump tweeted out last night that he hoped House Republicans would vote against reauthorization, perhaps because no one told him that House Republicans already voted in favor of the weaker reforms before they were sent to the Senate:

I hope all Republican House Members vote NO on FISA until such time as our Country is able to determine how and why the greatest political, criminal, and subversive scandal in USA history took place!

In March, House Republicans voted in favor of the bill 126-60. Democrats voted in favor 152-75, so neither side proved particularly heroic in fighting for Americans’ data privacy.

The Rules Committee has not yet voted on the Lofgren-Davidson amendment but is expected to do so today. The House may take up the bill as soon as this evening.

Rep. Tulsi Gabbard (D–Hawaii) and Rep. Louis Gohmert (R–Texas) independently introduced amendments that, like the one proposed in the Senate by Sen. Rand Paul (R–Ky.), would prohibit the FISA Court from authorizing surveillance of U.S. citizens entirely. Paul’s amendment went down in flames in the Senate, and the Gabbard and Gohmert amendments are expected to fare similarly in the House.

from Latest – Reason.com https://ift.tt/36ASH9M

via IFTTT

Community platform Nextdoor is going to great lengths to become the go-to app to snitch on your neighbors.

According to a CityLab article, Nextdoor is showering law enforcement with all-expenses paid vacations to their headquarters in San Francisco, California all in an effort to gain law enforcement acceptance and put police on Public Agency Advisory Councils.

Charles Husted, the chief of police in Sedona, Arizona, couldn’t contain his excitement. He had just been accepted into the Public Agencies Advisory Council for Nextdoor, the neighborhood social networking app.

At a time when most Americans are concerned with just surviving the COVID-19 pandemic, Nextdoor views it as an opportunity to influence law enforcement and local politics.

As part of the chosen group, he would be flown to San Francisco on President’s Day, along with seven other community engagement staffers from police departments and city offices across the country. Over two days, they’d meet at Nextdoor’s headquarters to discuss the social network’s public agency strategy. Together, the plan was, they’d stay at the Hilton Union Square, eat and drink at Cultivar, share a tour of Chinatown, and receive matching Uniqlo jackets. All costs — a projected $16,900 for the group, according to a schedule sent to participants — were covered by Nextdoor.

Exactly what Nextdoor includes in their law enforcement paid vacations is protected by a corporate non-disclosure agreement. But you can be sure it isn’t just a trip to their headquarters.

Nextdoor’s excuse for influencing law enforcement and advisory councils is to allegedly “help [public agency] partners to share their expertise and experiences with each other and our product development team.”

If you look past Nextdoor’s lame excuse to shower law enforcement with gifts, you see the real reason behind what they are doing.

Since the Covid-19 crisis began in the U.S. at the beginning of March, Nextdoor says the volume of posts by public agencies has tripled. Along with his daily press conferences, New York Governor Andrew Cuomo has been posting occasionally on the site as part of Nextdoor’s new partnership with the National Governors Association.

The article goes on to say that Nextdoor’s plan is to shamelessly follow in Amazon Ring’s footsteps by cozing up to law enforcement and influencing government officials. Nextdoors goal is “to earn the trust of more public agencies, and to eventually pitch a paid version of the app.”

The real reason Nextdoor is schmoozing with law enforcement and influencing advisory councils is to make them more profitable than the $2.1 billion dollars they are currently worth.

As Slate revealed, Nextdoor is more than happy Americans are using their platform to snitch on each other for not social distancing.

“If there are kids outside, getting more than adequate exercise time, and basically goofing around,” a concerned Nextdoor user in Cherry Hill Village, Michigan, asked in a recent post on the hyperlocal social network, “is there something that can be done?”

Social distancing complaints on the rise during pandemic

A recent WCPO 9 article revealed that since the COVID-19 outbreak, social distancing complaints on Nextdoor and to the police have skyrocketed.

“I wish I could say everything was warm and fuzzy, but that would be lying,” Jenn Takahashi, the proprietor of the Twitter account @BestofNextdoor said. It’s not so much that people are being better or worse than usual; it’s more that human nature is to judge and police others, and so this persists even—especially?—in times of crisis.

The Chicago Tribunereports that neighbors are using Nextdoor to snitch on each other “with a sense of duty.” Rewire.org said, the snitch or “call-out culture is based in rage and there is no empathy involved.”

The article further explained that neighbors attempted to justify snitching on each other by saying they are the call-in culture.

“Calling-in is when you express concern about what someone is saying but you do it in as respectful a fashion as you can,” activist Loretta Tomes said.

It does not matter what people refer to it by. Snitching, calling out your neighbor or calling-in only sows distrust in our communities, while Big Tech worries about who will become the next multi-billion dollar company.

Finding a cure for COVID-19 should not be entrusted to Apple-Google, Amazon, Nextdoor, DoorDash, Clear Biometrics, or any other Big Tech corporations whose only interest lies in making their shareholders more money.

via ZeroHedge News https://ift.tt/2LZXlVA Tyler Durden

In Landmark Decision, Pompeo Tells Congress Hong Kong No Longer Independent From China Tyler Durden

Wed, 05/27/2020 – 11:46

In what appears to be a preview of the at-this-point inevitable White House decision to strip Hong Kong of its preferred trading status over the new National Security law imposed by Beijing, Secretary of State Mike Pompeo tweeted on Wednesday that he has “reported to Congress that Hong Kong is no longer autonomous from China.”

Congress now has the power to strip Hong Kong of its “special status” under the United States-Hong Kong Policy Act of 1992, which has allowed for the city-state to be treated more favorably than the rest of China by the US.

The status is part of what’s allowed Hong Kong to develop as a ‘gateway to the West’, a key part of its appeal as an international city. Without the US ‘special status’, HK might lose its international cachet as well, and eventually become just another Chinese city.

Indeed, without such easy access to the global economy, Hong Kong will become just an extension of Shenzen, which lies just across the border on the mainland.

Today, I reported to Congress that Hong Kong is no longer autonomous from China, given facts on the ground. The United States stands with the people of Hong Kong.

In a story published just minutes before Pompeo’s tweet, the Washington Post explains that “a US law passed last year requires the secretary of state to certify – as part of an annual report to Congress – whether Hong Kong remains ‘sufficiently autonomous’ from Beijing to justify its unique treatment. That includes assessing the degree to which Hong Kong’s autonomy had been eroded by the government of China. (Hong Kong is part of China but has a different legal and economic system, a holdover from its time as a British colony.) The law also provides for sanctions against officials deemed responsible for human rights abuses or undermining the city’s autonomy. Such sanctions were also said to be under consideration at the White House in the wake of the Chinese government’s decision in May to impose new national security laws on the city.”

Stocks have shown a surprising degree of resilience, though the offshore yuan – a key barometer of China-related risks – skidded lower.

Aside from the fact that the decision – which was widely anticipated – marks another milestone in the deterioration in Washington-Beijing relations, as police in HK have already begun arresting protesters brave enough to take the streets in the face of an unprecedented police crackdown, it also jeopardizes nearly $40 billion in bilateral trade, as WaPo explains.

“Longer term, people might have a second thought about raising money or doing business in Hong Kong,” said Kevin Lai, chief economist for Asia excluding Japan at Daiwa Capital Markets. Another expert described revoking HK’s special status as “the nuclear option” for the US, and “the beginning of the death of Hong Kong as we know it”.

For the last day or so, the editor of China’s Global Times has been taunting the US in a series of tweets, daring it to use its navy and come save the protesting Hong Kongers, some of whom have written messages begging Trump to interfere.

Will you really send US troops to land on Hong Kong? If you don’t’, your “powerful” response is nothing but bluffing, isn’t it? Canceling Hong Kong’s separate customs territory status is not “powerful,” and China has long been prepared for that. pic.twitter.com/WhMNCP5HAs

Senior administration officials have insisted that this likely won’t be the end of Trump’s aggression toward China. Earlier on Wednesday, Commerce Secretary Wilbur Ross, who leads the department in charge of Washington’s crackdown on Huawei, said the president has more in store.

While there’s no question rescinding HK’s special status will be interpreted as another economy attack by Washington. But there’s something else even more alarming possibly lying in wait: The law passed last year in the US also requires the president to freeze US-based assets and bar entry to anyone who helps China repress Hong Kong.

It’s this possibility – which we could hear more about in the coming days – that should really stick in investors’ minds.

via ZeroHedge News https://ift.tt/2X8oMCI Tyler Durden

Rabobank: “A Few Months Ago, Any One Of These Stories Would Have Been Front-Page News And Market-Moving” Tyler Durden

Wed, 05/27/2020 – 11:45

Submitted by Michael Every of Rabobank

Equity markets (and EM FX) are still trying to rally in line with an epic central bank liquidity injection and the underlying plan that if we keep them up until the economy recovers, a recovered economy will then ultimately justify them. There has also been a boost from the fact that we are indeed now reopening in many locations.

What we now see is the relief when the cast around a broken bone comes off.Aah! The itching and constriction is gone! Fantastic! Cheer-leading from an FOMC member and someone who was publicly calling for a 4% US 10-year yield relatively recently aside, the problem is that we did not set the bone in question before we put the cast on. Yes, the leg is now out of plaster: but can you actually walk on it like before – or will you fall flat on your face? Doubly so as while the cast comes off, so do the gloves.

Central Hong Kong today is filled with police (and protestors) as legislation is being passed to criminalise insulting the Chinese national anthem or burning the Chinese flag. This is a warm up for the national security law that will soon be put in place by Beijing, and which yesterday was revealed to: 1) ban foreign judges from sitting on cases related to national security; and 2) ban not just “acts” against national security, but “activities” that can “seriously undermine” it. That is a very broad brush to be painting with in that geography, allege critics.

Meanwhile, in Washington DC we have heard US President Trump promise “interesting action” on China / HK by the end of the week. More importantly, the White House press secretary underlined that Trump is considering sanctions on a range of Chinese officials, businesses, and financial institutions: the Treasury department could impose controls on USD transactions and/or freeze assets of those targeted. The White House also reportedly does not see how Hong Kong can continue to operate as a global financial centre if China passes the national security laws, underlining its own threat. It is also looking at a sanctions bill targeting China’s alleged human rights abuses against the Uighur minority; and the State Department has just released a statement bringing up Tibetan rights. This is full-court US pressure.

Optimists point out that the US might be bluffing: really? Or that China can just do the same kind of financial business elsewhere. Pessimists might ask why other jurisdictions won’t be subject to the same US sanctions. Even Europe. The same top diplomat who on Memorial Day spoke of the end of US dominance in Asia, shrugged, and noted the EU’s reluctance to take its side, yesterday stated the EU is not considering any sanctions of its own against China because they are “not helpful.” The US will almost certainly make Europe comply anyway, as it has on Iran for the most part.

But there is more. White House Economic Advisor Larry Kudlow has openly stated that Trump is so “miffed” with China that he may walk away from the phase one trade deal, and that the US is prepared to pay the relocation costs for firms wishing to return to the US from China. We’ve heard it before, but this time it was black and white on red, white, and blue Fox News….where host Lou Dobbs recently eviscerated White House China-trade hawk Peter Navarro for going soft on Beijing and needing to far more.

Meanwhile, China’s gloves are also off – and not just against the US.

The People’s Daily has threatened the UK economically if it decides to drop Huawei from 5G, which seems inevitable after PM Johnson’s latest stumble leaves his backbenchers feeling empowered. Which makes US-UK trade talks all the easier, one would imagine, to the EU’s chagrin.

The Global Times has implicitly threatened Canada over today’s critical court decision on whether to proceed with the extradition proceedings of “hostage” Meng Wanzhou, Huawei CFO and daughter of its founder: does PM Trudeau have the ability to lean on judges? Despite tensions, this is likely to push Canada back closer to the US (and CAD lower?)

This week the same state-run paper has already stated that if Australia sides with the US vs. China in geopolitics then Australia-China economic relations will be hugely damaged. Won’t Australia diversify exports, for example to India, and move even closer to the US in logical response (as AUD moves lower)?

The stand-off on the India-China border continues, with the world showing more interest. An Indian academic interviewed on Al Jazeera on the matter yesterday stated that this was being seen in New Delhi as a clear Beijing warning not to sidle up to the US ahead. Which will probably create the opposite response.

Vietnam has just released footage of a Chinese ship chasing, ramming, and sinking one of its fishing vessels in the disputed (by China) South China Sea, which occurred yesterday. Which will again push Vietnam closer to the US.

Xinhua reports that Xi Jinping yesterday ordered the PLA to “scale-up” training and preparedness for war, and to be ready for worst-case scenarios. True, he said the same in early 2019 – but against the current backdrop it is worth noting.

The FT has reported that China is expected to promote the use of domestic coal by tightening import rules, starting with shipments from Australia. After imports to the world’s second-biggest economy jumped in the first four months of the year, market participants said it was likely Beijing would impose restrictions that made it more difficult or expensive for coastal utilities to bring in thermal coal from overseas.

A few years ago, or even a few months ago, any one of these stories would have been front-page news and potentially market-moving. The fact that we can have all of them happen in the same week –alongside the US decoupling/sanctions headlines– and markets still hardly move says a lot about how successfully central banks have detached them from reality.

However, we are now starting to see USD/CNH move higher. At time of writing it stood at 7.1720 when it was as low as 6.8672 on 20 January following the ‘phase one trade deal’. If we break above 7.20 then things get interesting as we are in uncharted waters. Except they aren’t really uncharted – charts show we can easily head back to the 8+ level where the Chinese currency was pegged for years: it all depends on the politics. And on that front we are also not in uncharted waters either. We can all hope the above is just ‘noise’. Yet we have clear heuristics of where these kind of trends can lead if not well managed: more than the broken bones markets are trying to celebrate the ‘end of.’

via ZeroHedge News https://ift.tt/2TKEv93 Tyler Durden

Boeing Slashes 6,770 US Workers, Sees No Recovery In Air Travel For “Years” Tyler Durden

Wed, 05/27/2020 – 11:43

Update (11:40 ET): Boeing CEO Dave Calhoun has just released an update on this week’s layoffs. He said involuntary layoffs have begun, a total of 6,770 US workers will be cut this week, adding that work reduction programs have already gone into effect for the company’s international facilities.

“Following the reduction-in-force announcement we made last month, we have concluded our voluntary layoff (VLO) program. And now we have come to the unfortunate moment of having to start involuntary layoffs (ILO). We’re notifying the first 6,770 of our U.S. team members this week that they will be affected. We will provide all the support we can to those of you impacted by the ILOs — including severance pay, COBRA health care coverage for U.S. employees and career transition services,” the statement read.

“Our international locations also are working through workforce reductions that will be communicated locally on their own timelines in accordance with local laws and benefit terms,” the statement continued.

Calhoun also gave an update on the 737 Max program. He said production is set to restart at its Renton, Washington facility in the near term.

“We’re moving forward with our plan to restart 737 MAX production in Renton, Washington, as our return-to-service efforts continue. And our Global Services team is changing its organization to ensure it is lean and focused on the post-COVID needs of its customers.”

He reiterated that the commercial airliner industry “will come back, but it will take some years to return to what it was just two months ago.” Further signaling, the travel and tourism industry remains doomed through 2021.

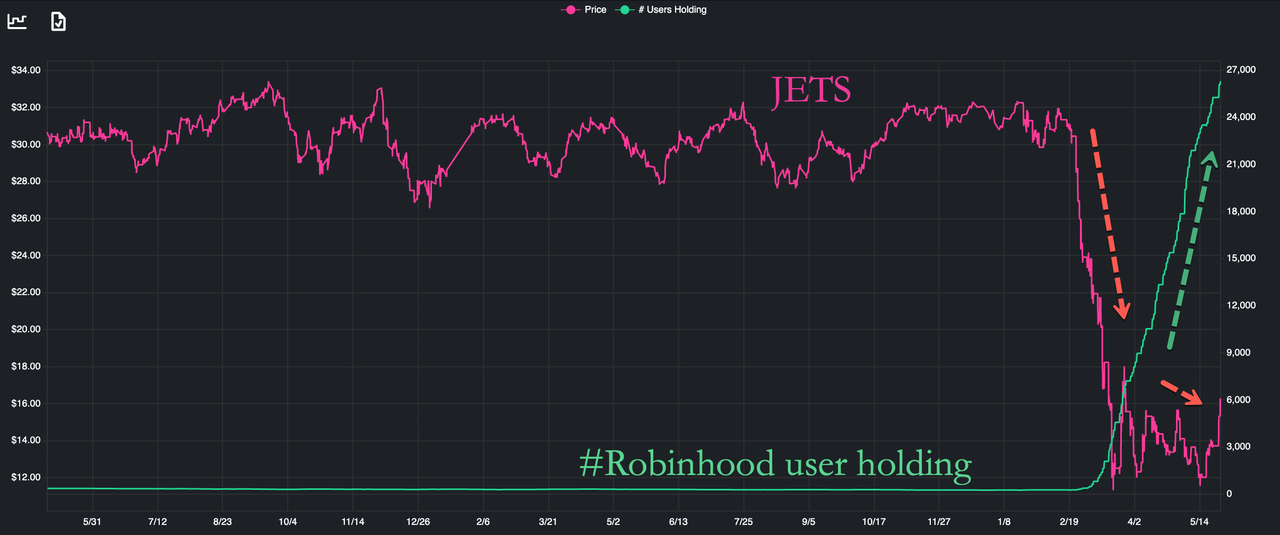

Robinhood users are also piling into JETS ETF — hoping for a massive recovery – but according to Calhoun, it could take several years for a recovery to unfold…

So does that mean Robinhood users will be left holding the bag?

* * *

Boeing has notified union officials that it will cut workers this week, reported Bloomberg. Demand for air travel has collapsed during the COVID-19 outbreak, and the aerospace company continues to reel from the 737 Max grounding.

We noted in early May, Boeing announced a 10% cut of its jobs, or about 16,000 positions, with many of the reductions focused in the commercial airplane unit.

“The demand for commercial airline travel has fallen off a cliff,” Boeing CEO Dave Calhoun said earlier this month. “The pandemic is also delivering a body blow to our business.”

Society of Professional Engineering Employees in Aerospace (SPEEA), which represents about 18,000 engineers in the Puget Sound region, has already told employees that they will lose their jobs as soon as this week. SPEEA spokesman told Bloomberg that 1,300 workers were willing to accept buyouts.

Puget Sound Business Journal said Boeing had told SPEEA that cuts between 15% and 20% of white-collar workers in the Seattle area and Southern California are expected. The planemaker has already cut jobs in Australia and Canada.

Calhoun recently said it had offered 70,000 of its employees a voluntary layoff package. He warned that it could take upwards of three years to return sales back to 2019 levels.

And that is precisely why Warren Buffett dumped his stake in U.S. airlines because the recovery will take years.

via ZeroHedge News https://ift.tt/2TJ8xKe Tyler Durden

For years, I have been warning that during the age of permanent stimulus (which began in earnest with the Federal Reserve’s reaction to the dotcom crash of 2000), each successive economic contraction would have to be met with ever larger, increasingly ineffective, doses of monetary and fiscal stimulus to keep the economy from spiraling into depression. I have also said that the enormity of the asset price gains over the last 10 years had increased the danger because reflating the bloated stock, real estate, and public and private debt markets would bring on doses of stimulus that could prove lethal for the economy. But even though I expected that the next financial crisis would be catastrophic, I thought that it would come into the world in the usual way, as a credit crisis triggered by over-leverage. But the Coronavirus ripped up those stage notes, and instead ushered in a threat that is faster and deeper than I imagined, and I imagined a lot. It’s a perfect storm, a black swan with teeth.

Even in my most pessimistic assessments, I did not expect that so many seemingly distant sectors of the economy would simultaneously evaporate, almost overnight, or that government deficits would expand to nearly $4 trillion in the first wave of the crisis, or that the Federal Reserve would so suddenly launch its largest-ever experiment in quantitative easing, (with almost none of the forward guidance they have used to telegraph lesser moves), which would expand its balance sheet by more than $3 trillion in a matter of just a few months. Nor did I expect that at its outset the Fed’s new buying plan would include, for the first time, corporate bonds and high yield debt ETFs. (I thought those expansions would come eventually, not immediately.)

To make matters even worse, the crisis has struck in the midst of a presidential election year, which guarantees that every policy decision has been made through a political prism. Democrats are seizing on the crisis to paint the Trump Administration as incompetent, ineffective and uncaring, often twisting themselves into knots to do so. (Trump has done himself no favors by using his daily briefings to showcase his inconsistent policy positions, combative political style, and his tenuous grasp of medical concepts.) So, in contrast to prior national crises that had tended to pull the country together (think 9/11), this event is tearing us apart.

But there is one thing upon which both sides seem to agree:the need for the Federal government to shower the economy with newly created money, bail out everyone who can claim that the virus “was not their fault,” and to fully liquefy the financial markets. The result has been an increase in government spending that dwarfs everything we have ever seen in the past, including the government’s response to the 2008 financial crisis. The $3 trillion increase in Federal debt accumulated this spring may just be the beginning.

The major political differences now center on matters of degree, particularly how long the economy should remain closed and how many jobs, businesses, and family financial plans should be exchanged for each life that may be saved through extended lockdowns. This is where it gets ugly.

Most Democrats, claiming that they are solely motivated by a desire to save as many lives as possible, are pushing for extended lockdowns. But given the economic and scientific idiocy of their proposals (for instance, the failure to differentiate between relative risk levels across society), you can forgive those who conclude that they are at least partially interested in enacting the sorts of radical economic transformations that would have been impossible to push through in normal circumstances.

Republicans are leaning in the other direction, with many favoring the Swedish approach to the pandemic, which looks to quarantine the most vulnerable (the elderly and immuno-compromised) while seeking to build “herd immunity” among the majority of healthy citizens. This idea avoids lockdowns and social distancing (and tolerates elevated infection rates among the healthy) in order to suppress future infection waves, and more importantly, to prevent economic catastrophe.

Of course, the Swedish government, knowing that it alone would have to bear the cost of its decisions, did a rational cost/benefit analysis on its options. U.S. governors, who are relying on the Federal government to support the unemployed and to bail out state deficits, have been spared these hard choices. With costs shifted to the Federal government, states have underplayed economic considerations in their public health plans. No doubt many states have seized on the crisis as an opportunity to be bailed out of financial problems that predated the current crisis.

From his basement-based presidential campaign, Joe Biden has repeatedly asserted that trade-offs between safety and economic activity are a “false choice,” and that any policies that may just prevent “one more death” should be implemented, no matter the costs. Such claims are symptomatic of a politician who prefers cheap posturing to reality.

The insanity of this idea can be seen in California, a state under total control of the Democrats.

Despite a per capita death rate that is less than 30% of the national average, based on current data from Wolrldometer, the state seems to be prepared to commit economic suicide. In Los Angeles County, home to more than 10 million people as of 2018, the County Public Health Director just recommended that lockdown orders stay in place until August. On May 8 The Mercury News reported that California guidelines now dictate that counties remain closed until there are no COVID deaths, and no more than one new case per 10,000 residents, in the last 2 weeks. That bar is set so high that it seems designed never to be cleared.

Democrats’ preferred approach seems to be: Test everyone in the country for the disease, contact trace the tens of millions who are likely to test positive (even though that accomplishes nothing), lockdown until a vaccine is developed, and pass the costs on to the Federal Government. They seem to prefer this to a world in which Americans are empowered to make choices regarding their own health risks and economic imperatives. In so doing, some have equated calls for “liberty” with racism and greed.

Some of the government’s immediate responses have been laughably inept. Take the Paycheck Protection Program (PPP), which provides direct payments to workers who have lost jobs due to forced shutdowns. The problem is that the payments are often significantly higher than the former wages earned by many workers. That means that even when companies are allowed to open and rehire, many employees may not want to come back to work, at least not until their new unemployment checks run out. And based on the current drift in Washington and the stakes created by the election, there is a high likelihood that the generous payments will be renewed before the program expires in late summer. (Democrats want to extend the higher payments until January).

This is dangerous territory. As former Libertarian leader Harry Browne once said:

Government breaks your leg, and then hands you a crutch and says, “See, if it weren’t for us, you wouldn’t be able to walk.”

That is precisely what is happening here.

For countries that issue currencies that are not the world’s reserve (that is every country but the U.S.) the playbook is radically different. Down in the cheap seats, politicians are aware that the costs of trying to print your way out of a financial dead-end are likely to be higher than the temporary gain of immediate liquidity injections. Blatant “debt monetization,” whereby a government sells newly-created bonds to its central bank, usually ends in rampant, or even hyper, inflation, which wipes out the savings and the economic viability of the nation. But the dollar sits at the center of the global financial system, creating a built-in demand, as most cross-border transactions need dollars to execute. This advantage allows Washington to consider policy options that would be too risky for other countries.

And so while we can clearly see this new wave of debt forming on the horizon, few fear any real damage when it finally crashes onto shore. The fact that we have yet to pay a high price for our prior accumulation of debt, in terms of inflation and high interest rates, gives politicians and Wall Street cheerleaders room to suggest that there is no downside to the “government pays for everything” approach.

With this trump card tucked into our sleeve, the United States will now engage in the biggest experiment in money creation the world has ever seen. The hubris of American monetary exceptionalism may mean that no plan will be devised to steer us out of the dead-end of zero, or negative interest rates, no plan to confront our massive fiscal structural deficits, and no plan to create an economy that can survive without government life support.

But maybe the experiment in money creation can succeed in getting us through the COVID Depression without causing consumer prices to surge and cutting the legs out under the dollar? Maybe everything I have ever learned, or felt, about economics is wrong? Maybe money can grow on trees? I’m betting it can’t.

But this crisis will present different math than what we have seen over the last 20 years. We will be showering the country with money at a time when the supply of goods and services is diminishing due to work stoppages, production declines, distribution bottlenecks, and import restrictions.

Even if all restaurant and retail employees were to ignore the incentives and return to work, there is no certainty that customers will follow as fears of contagion will remain long after the economy reopens, and social distancing procedures will reduce the quality of the experience while increasing its cost. There are also no legal protections currently on the books to shield employers from lawsuits brought by workers or customers who may contract the virus on their premises. Under these circumstances, wide swaths of business sectors may just cease to be. In sum, there are many reasons to suspect that a very deep recession, or even a depression, will remain even after the disease subsides. All this means that the economic rebound may be much softer than expected.

So, we will have more money chasing fewer goods and services. This is a recipe for stagflation, whereby prices go up even while the economy contracts, creating a horrible economic situation for those at the bottom of the economic pyramid. Most dangerously, we see this happening now in the food supply, with meat processors and farmers facing difficulties in getting products to market. If you think social cohesion is breaking down now, wait until people have problems feeding their families.

When you get down to it, this crisis exposes just how deeply the decay of debt has undermined the economy. The forced shutdowns and social distancing would have been a serious blow to a very robust economy, but not likely fatal. In a healthy economy, individuals, businesses, and even governments, may have had the savings to draw on in case everything went wrong. Savings could have allowed us to freeze economic activity for a time, and survive to see it restart. But credit has become so cheap and so freely given in recent decades that the incentive to save has never been lower. Knowing that credit cards are handed out like lollipops, consumers have learned to live paycheck-to-paycheck. With interest rates near zero, small businesses have learned to rely on business lines of credit to pay current bills, and mega-cap corporations borrow to buy back shares, trading long-term stability for a short-term share price appreciation. In such an environment, any economic interruptions that constrain short-term revenues create an immediate crisis. Without the life support of savings, everyone immediately calls on the government to ride to the rescue. The problem is the politicians show up with the economic equivalent of pep pills and leeches.

So, we can see where this is going. Debt and monetary expansion look almost certain to increase. The dollar may eventually buckle under the weight, dragging the bond market down with it. It’s hard to say what the economy will look like once the bill comes due, but investors have plenty of warning. They should use the current period, where the dollar has yet to fall, to consider holdings that may provide real protection.

via ZeroHedge News https://ift.tt/2Xz3YUa Tyler Durden

If there was ever a time in history to pay attention, it’s now. It’s now obvious that we all need to keep our eyes and ears open to that which Big Tech and the government continue to censor to “save us” from “misinformation.” Google Drive, at the request of The Washington Post, has taken down a user’s personal copy of the movie “Plandemic.”

Ever since Big Tech platforms started cracking down on what they deem to be “coronavirus misinformation” (information they don’t want you to know about), the media has been willfully flagging alleged violations to social media companies and getting content taken down, reported News Break.

In other words, they want us to remain in a panic-induced state of fear and only listen to the mainstream media’s official Operation Mockingbird narrative about the entire Plandemic. And because you are not supposed to know anything else, Google drive has removed a user’s personal copy of Dr. Judy Mikovitz’s “Plandemic” after it was flagged by the Washington Post.

It doesn’t get more blatant than this, folks. We are being lied to and expected to stay fearful and obey the ruling class at all costs. It’s going to get ugly by the end of this year if tyrants don’t release their grip on power…and we know they won’t let go easily.

In an article reporting on the takedown, The Washington Post’s Silicon Valley Correspondent Elizabeth Dwoskin complained that after the coronavirus documentary Plandemic was censored on social media, some YouTube clips were telling users how to access “banned footage” from the documentary via Google Drive. She then notes that after The Washington Post contacted Google, Google Drive took down a file featuring the trailer for the Plandemic documentary.

As Big Tech ramps up censorship, we need to ramp up our exit and cease to use their products. We said last month that the mainstream media was going to continue a smear campaign against anyone who stands up to the elitists and this tyrannical takeover and economic terrorism while using a virus as an excuse.

The mainstream media is going to continue its smear campaign against anyone who dares to believe they have the right to live freely so long as they aren’t harming others and take life’s risk upon themselves. But as fewer people tune in to listen to their propaganda, fewer people will be brainwashed by it. –SHTFplan

And that’s exactly what the Washington Post did. Dwoskin frames users sharing files containing the Plandemic trailer with each other as:

“A wave of seemingly countless workarounds employed by people motivated to spread misinformation about the virus — efforts that continue to thwart social media companies’ attempts at preventing hoaxes and conspiracy theories from spreading amid the greatest public health crisis in decades.”

There is good news though. We now know that the mainstream media is struggling to maintain their grip on the official narrative, and for all intents and purposes, they’ve already failed. Too many have awoken to the lies and propaganda designed to keep a ruling class in place, and the rest of us subjugated. But that’s all ending and they will not go down without a fight. Expect more censorship as they desperately try to cling to their mind control and social engineering schemes in the coming months.

[1.] But such labeling by Twitter isn’t stifling free speech—it’s Twitter management exercising their own free speech: They are letting him speak, but responding to the speech with their own. That’s their First Amendment right, just as it’s his First Amendment right to criticize them.

Now if they did take down his post, then one could argue that would be stifling free speech. It wouldn’t be a violation of the Free Speech Clause, because Twitter is a private company. But free speech is a broader idea than just the freedom from government suppression; one could sensibly say that a private entity is undermining free speech in various ways, especially when the entity promotes itself as a forum for public discourse.

If Twitter, for instance, started taking down pro-animal-rights statements or anti-war speech or anti-transgender-rights advocacy or criticism of the Chinese government, I think it would be reasonable to label that as stifling free speech. One can still say that it’s defensible for various reasons (perhaps some speech should be stifled, at least by private entities, some might argue), but “stifling free speech” would at least be a plausible label.

Likewise if Google were to close the Gmail accounts of people who publicly expressed such views, or if Hollywood studios set up a blacklist of screenwriters and others who had supposedly expressed, say, Communist views or racist views or what have you. Twitter’s decision to block certain posts might be seen as the exercise of its own First Amendment rights as editors (a plausible argument, though not a fully settled one, see Turner Broadcasting System v. FCC); still, it could still be properly labeled as stifling free speech.

But that label doesn’t apply to simply responding to speech with speech of one’s own. Rather, such labeling (and linking to a response) is the very sort of “counterspeech” that the Supreme Court has (rightly) said is the proper response for speech with which one disagrees.

[2.] The President, of course, has no power to stop Twitter from doing this, partly because he can’t create new laws and partly because Twitter’s speech is constitutionally protected.

Congress could, as some people have argued, limit 47 U.S.C. § 230, which gives Twitter immunity from liability for posts by its users. In particular, some have argued that platforms should only be immune if they allow all speech by their users (setting aside constitutionally unprotected speech, such as true threats of violence or child pornography), or perhaps only if any restrictions they impose are viewpoint-neutral. Once platforms start excluding certain material based on content or viewpoint, the theory goes, they should become potentially liable (perhaps on some notice-and-takedown basis). I on balance don’t buy that argument, but it’s worth debating, and it would indeed be in some ways a return to a traditional approach to liability, under which there were some platforms were indeed immune from speech by their users but only when they were legally prohibited from controlling such speech.

But this is beside the point here, since the President’s objection here isn’t that Twitter is excluding speech—it’s that Twitter is including its own speech. And Twitter can’t be penalized for such speech of its own.

[3.] Finally, there is a separate objection here: that Twitter is “interfering” in the election by throwing its massive weight behind one particular position. But the First Amendment protects our right to speak, at least under Citizens United v. FEC; nor is there anything improper or unethical in a business expressing its views on something that’s being said using its services, and trying to prevent what it sees as a misleading use of its services.

In any event, though, even if one concludes that speech by rich and powerful institutions or individuals that may influence elections is “interference” that should be condemned, it is still not “stifling FREE SPEECH.”

(By the way, tt’s not clear where the Citizens United dissenters would have drawn the line between newspaper corporations, which they said do have a First Amendment right to speak about candidates, and other corporations, which they said don’t have such a right. It’s therefore not clear which side of the line Twitter would fall on—recall that Citizens United was a video production company, and the dissenters would have ruled against it. But their position didn’t prevail.)

from Latest – Reason.com https://ift.tt/3eu2t0p

via IFTTT

[1.] But such labeling by Twitter isn’t stifling free speech—it’s Twitter management exercising their own free speech: They are letting him speak, but responding to the speech with their own. That’s their First Amendment right, just as it’s his First Amendment right to criticize them.

Now if they did take down his post, then one could argue that would be stifling free speech. It wouldn’t be a violation of the Free Speech Clause, because Twitter is a private company. But free speech is a broader idea than just the freedom from government suppression; one could sensibly say that a private entity is undermining free speech in various ways, especially when the entity promotes itself as a forum for public discourse.

If Twitter, for instance, started taking down pro-animal-rights statements or anti-war speech or anti-transgender-rights advocacy or criticism of the Chinese government, I think it would be reasonable to label that as stifling free speech. One can still say that it’s defensible for various reasons (perhaps some speech should be stifled, at least by private entities, some might argue), but “stifling free speech” would at least be a plausible label.

Likewise if Google were to close the Gmail accounts of people who publicly expressed such views, or if Hollywood studios set up a blacklist of screenwriters and others who had supposedly expressed, say, Communist views or racist views or what have you. Twitter’s decision to block certain posts might be seen as the exercise of its own First Amendment rights as editors (a plausible argument, though not a fully settled one, see Turner Broadcasting System v. FCC); still, it could still be properly labeled as stifling free speech.

But that label doesn’t apply to simply responding to speech with speech of one’s own. Rather, such labeling (and linking to a response) is the very sort of “counterspeech” that the Supreme Court has (rightly) said is the proper response for speech with which one disagrees.

[2.] The President, of course, has no power to stop Twitter from doing this, partly because he can’t create new laws and partly because Twitter’s speech is constitutionally protected.

Congress could, as some people have argued, limit 47 U.S.C. § 230, which gives Twitter immunity from liability for posts by its users. In particular, some have argued that platforms should only be immune if they allow all speech by their users (setting aside constitutionally unprotected speech, such as true threats of violence or child pornography), or perhaps only if any restrictions they impose are viewpoint-neutral. Once platforms start excluding certain material based on content or viewpoint, the theory goes, they should become potentially liable (perhaps on some notice-and-takedown basis). I on balance don’t buy that argument, but it’s worth debating, and it would indeed be in some ways a return to a traditional approach to liability, under which there were some platforms were indeed immune from speech by their users but only when they were legally prohibited from controlling such speech.

But this is beside the point here, since the President’s objection here isn’t that Twitter is excluding speech—it’s that Twitter is including its own speech. And Twitter can’t be penalized for such speech of its own.

[3.] Finally, there is a separate objection here: that Twitter is “interfering” in the election by throwing its massive weight behind one particular position. But the First Amendment protects our right to speak, at least under Citizens United v. FEC; nor is there anything improper or unethical in a business expressing its views on something that’s being said using its services, and trying to prevent what it sees as a misleading use of its services.

In any event, though, even if one concludes that speech by rich and powerful institutions or individuals that may influence elections is “interference” that should be condemned, it is still not “stifling FREE SPEECH.”

(By the way, tt’s not clear where the Citizens United dissenters would have drawn the line between newspaper corporations, which they said do have a First Amendment right to speak about candidates, and other corporations, which they said don’t have such a right. It’s therefore not clear which side of the line Twitter would fall on—recall that Citizens United was a video production company, and the dissenters would have ruled against it. But their position didn’t prevail.)

from Latest – Reason.com https://ift.tt/3eu2t0p

via IFTTT