5/27/1935: Schechter Poultry Corp. v. U.S. decided.

from Latest – Reason.com https://ift.tt/2AgaaIQ

via IFTTT

another site

5/27/1935: Schechter Poultry Corp. v. U.S. decided.

from Latest – Reason.com https://ift.tt/2AgaaIQ

via IFTTT

COVID-19 Spreads To Brazil’s Offshore Oilfields

Tyler Durden

Wed, 05/27/2020 – 06:00

Authored by Tsvetana Paraskova via OilPrice.com,

At least five oil producers offshore Brazil, including international oil majors and state oil firm Petrobras, have seen COVID-19 infections among offshore workers spike in recent weeks, industry and government sources told Reuters on Tuesday.

Brazil’s Petrobras and Enauta Participacoes, as well as Shell, Equinor, and Perenco have registered cases of coronavirus infections among workers or contractors who are sharing confined areas on offshore oil rigs.

At the same time, Brazil surpassed Russia last week to become the country with the second-largest number of COVID-19 infections behind the United States. The U.S. moved to ban as of Tuesday the travel of foreign nationals from Brazil into the United States in a temporary move to prevent the spread of COVID-19 from Brazil.

According to sources and data from regulators compiled by Reuters, Norwegian major Equinor had around 60 coronavirus cases as of last week, most of which at the Peregrino oilfield, Perenco had 40 cases, while Petrobras had more than 300 workers among staff and contractors with COVID-19.

Shell and Enauta had one coronavirus case each, the two companies told Reuters.

Petrobras says that it is taking every person’s temperature upon boarding offshore units and has adopted work-from-home as much as possible.

Days before the production cuts at the OPEC+ group formally began on May 1, Petrobras of Brazil – which is not part of that group – said that it had reversed the cuts it had announced in early April, opting for “the gradual return to an average oil production level of 2.26 MMbpd in April alongside an increase in the utilization factor of our refineries,” due to better than expected demand for its products.

Yet, the coronavirus pandemic spiraling out of control in Brazil could crush its oil industry, analysts say. Apart from the health of the offshore oil workers, Brazil’s oil sector is threatened by the low oil prices and the economic downturn in the country and in the world. Being state-held, Petrobras’s ratings are closely related to the credit rating of Brazil.

via ZeroHedge News https://ift.tt/2THSuwt Tyler Durden

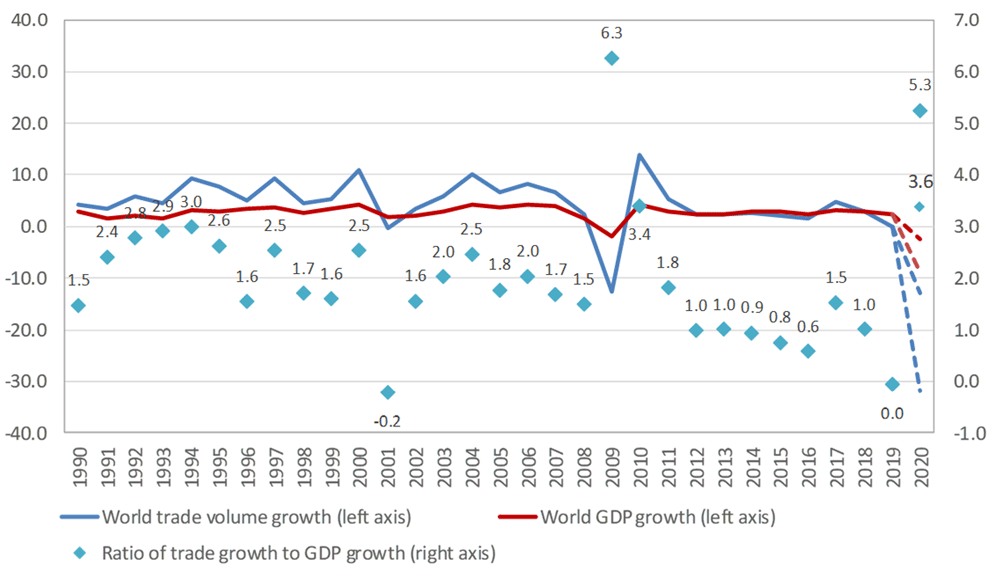

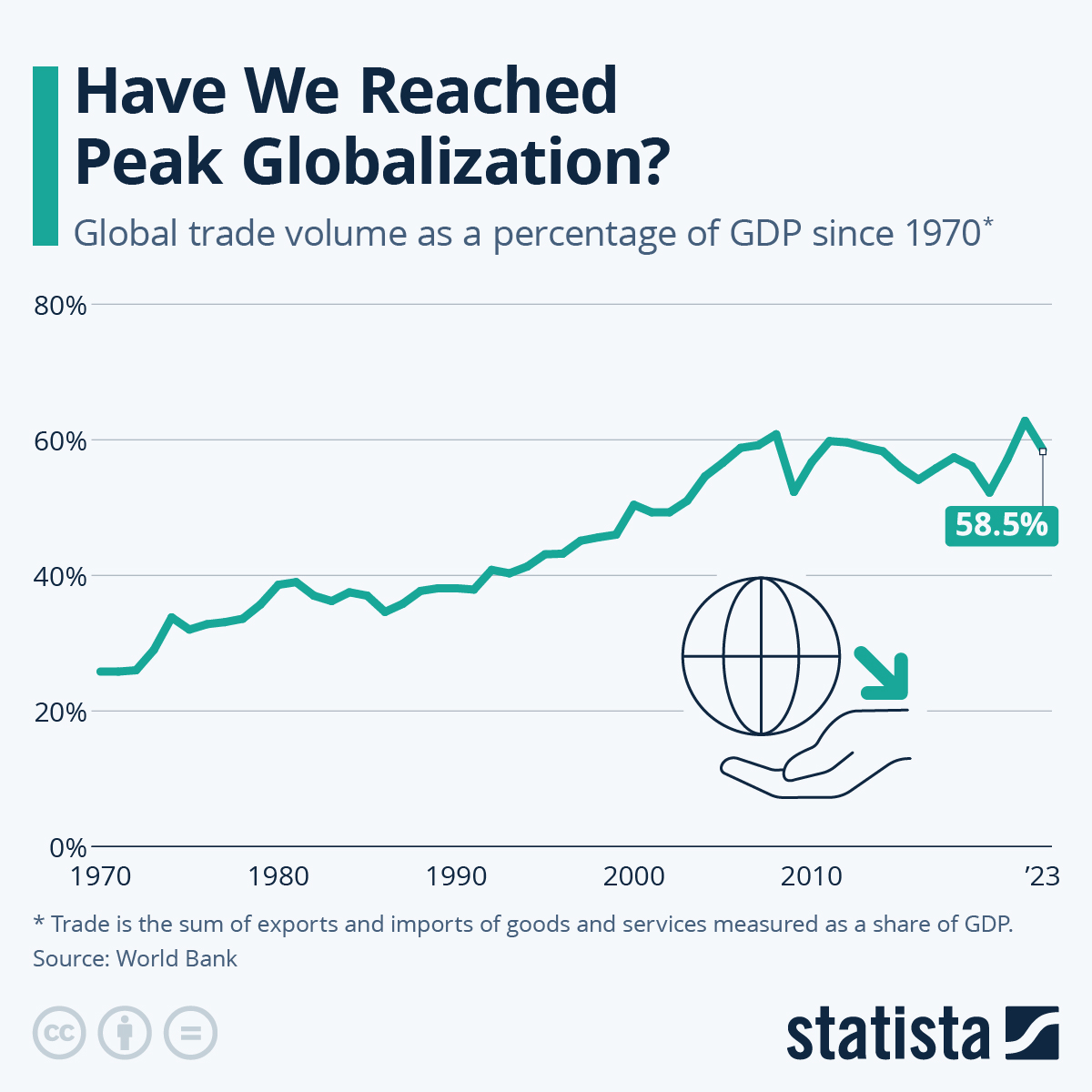

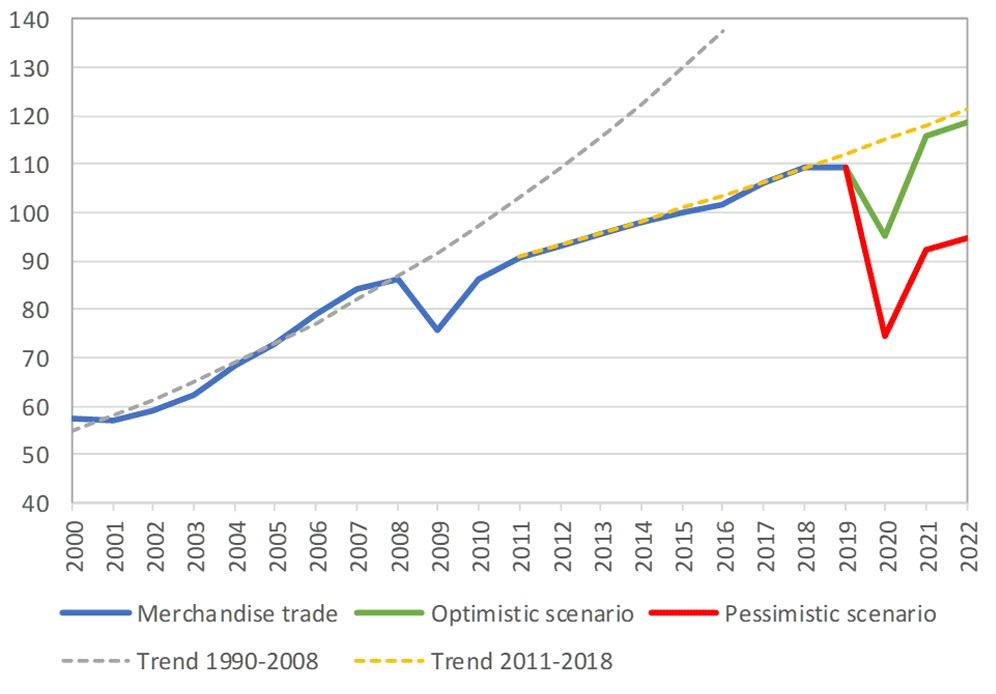

Has Globalization Passed Its Peak?

Tyler Durden

Wed, 05/27/2020 – 05:30

After decades of growth for world trade, global tourism and international cooperation, globalization hit a couple of roadblocks in recent years, as the reemergence of nationalism and protectionism have undone some of the progress made in the past. After global trade growth slowed significantly in 2019, due in large part to trade tensions between the United States and China, the COVID-19 pandemic is expected to cause an unprecedented fall in world trade.

According to estimates from the World Trade Organization, world merchandise trade is set to plummet between 13 and 32 percent this year, depending on how quickly the coronavirus is contained and trade can return to pre-crisis levels.

“These numbers are ugly – there is no getting around that. But a rapid, vigorous rebound is possible,” WTO Director-General Roberto Azevêdo said in a press release on the matter, while emphasizing the role of free trade on the road to recovery.

“Keeping markets open and predictable, as well as fostering a more generally favourable business environment, will be critical to spur the renewed investment we will need. And if countries work together, we will see a much faster recovery than if each country acts alone.”

As the following chart based on World Bank data shows, global trade volume – measured here as a percentage of global GDP – has been relatively stagnant for years, after several decades of uninterrupted growth.

You will find more infographics at Statista

Following the trade decline caused by the global financial crisis in 2009, world trade never returned to its previous growth trajectory and many are expecting a similar long-term effect of the current crisis.

Having reminded many companies of the vulnerabilities of global supply chains, both the pandemic and the trade war between the U.S. and China could lead companies towards a more domestic approach to production and sourcing, which might result in a sustained reduction of global trade.

via ZeroHedge News https://ift.tt/2X6l3FP Tyler Durden

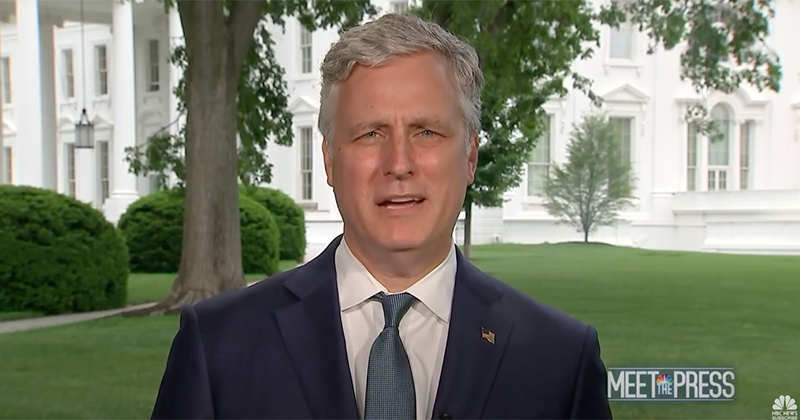

Coronavirus “Cover-Up” Is China’s Chernobyl: White House National Security Adviser

Tyler Durden

Wed, 05/27/2020 – 05:00

Authored by Steve Watson via Summit News,

The White House national security advisor Robert O’Brien has compared China’s response to the coronavirus outbreak to the Soviet Union’s cover-up of the meltdown at the Chernobyl nuclear power plant.

“They unleashed a virus on the world that’s destroyed trillions of dollars in American economic wealth that we’re having to spend to keep our economy alive, to keep Americans afloat during this virus,” O’Brien said in an NBC interview.

“The cover-up that they did of the virus is going to go down in history, along with Chernobyl.” O’Brien added.

“We’ll see an HBO special about it 10 or 15 years from now.” he urged, referring to the recent award winning dramatisation of the 1986 disaster.

“This is a real problem and it cost many, many thousands of lives in America and around the world because the real information was not allowed to get out,” O’Brien further proclaimed.

“It was a cover-up. And we’ll get to the bottom of it eventually.” O’Brien asserted.

O’Brien’s comments come as Shi Zhengli, the the deputy director of the Wuhan Institute of Virology, warned that COVID-19 is ‘just the tip of the iceberg’ of unknown deadly viruses, while again denying that her lab had anything to do with the outbreak.

“If we want to prevent human beings from suffering from the next infectious disease outbreak, we must go in advance to learn of these unknown viruses carried by wild animals in nature and give early warnings.” Shi said, adding “If we don’t study them there will possibly be another outbreak.”

As details continue to emerge, China admitted recently that it did order laboratories to destroy samples of the new coronavirus in the early stage of the outbreak.

The destruction of the samples was first noted back in February. It was also noted that the Wuhan Institute of Virology, which was conducting controversial experiments into animal-to-human transmission of bat coronaviruses, altered their database in an apparent attempt to distance the lab from the outbreak.

The alteration was carried out just two days before a gene sequencing lab was ordered by the Health and Medical Commission of Hubei Province to destroy it’s coronavirus samples.

In addition, a scientific study in Austria has found that SARS-CoV-2 was likely created in a lab, barring some “remarkable coincidence” that led to the virus naturally evolving to be optimised to attack human cells.

The authors of the study believe this means that the virus “became specialized for human cell penetration by living previously in human cells, quite possibly in a laboratory.”

via ZeroHedge News https://ift.tt/2AcdVyV Tyler Durden

New York City building inspectors are staking out intersections trying to spot contractors performing “non-essential” construction and remodeling work, in violation of Gov. Andrew Cuomo’s executive order. Contractors caught violating the order as well as their clients face fines of up to $10,000 each.

from Latest – Reason.com https://ift.tt/2X4p2Tf

via IFTTT

New York City building inspectors are staking out intersections trying to spot contractors performing “non-essential” construction and remodeling work, in violation of Gov. Andrew Cuomo’s executive order. Contractors caught violating the order as well as their clients face fines of up to $10,000 each.

from Latest – Reason.com https://ift.tt/2X4p2Tf

via IFTTT

France’s Determination To End Free Speech Knows No Limits

Tyler Durden

Wed, 05/27/2020 – 03:30

Authored by Judith Bergman via The Gatestone Institute,

On May 13, the French parliament adopted a law that requires online platforms such as Facebook, Google, Twitter, YouTube, Instagram and Snapchat to remove reported “hateful content” within 24 hours and “terrorist content” within one hour. Failure to do so could result in exorbitant fines of up to €1.25 million or 4% of the platform’s global revenue in cases of repeated failure to remove the content.

The scope of online content deemed “hateful” under what is known as the “Avia law” (after the lawmaker who proposed it) is, as is common in European hate speech laws, very broadly demarcated and includes “incitement to hatred, or discriminatory insult, on the grounds of race, religion, ethnicity, gender, sexual orientation or disability”.

The French law was directly inspired by Germany’s controversial NetzDG law, adopted in in October 2017, and it is explicitly mentioned in the introduction to the Avia law.

“This law proposal aims to combat the spread of hate speech on the internet,” it is stated in the introduction to the Avia law.

“No one can dispute the exacerbation of hate speech in our society… the attack[s] on others for what they are, because of their origins, their religion, their sex or their sexual orientation… hints… [at] the darkest hours in our history… the fight against hatred, racism and anti-Semitism on the Internet is an objective of public interest that justifies…strong and effective provisions… this tool of openness [the internet] to the world, of access to information, to culture, to communication, can become a real hell for those who become the target of ‘haters’ or harassers hidden behind screens and pseudonyms. According to a survey carried out in May 2016, 58% of our fellow citizens consider the internet to be the main locus of hate speech. More than 70% say they have already been confronted with hate speech on social networks. For younger people in particular, cyber-harassment can be devastating…However… Few complaints are filed, few investigations are successful, few convictions are handed down – this creates a vicious circle…”

Having acknowledged that online “hatred” is tricky to prosecute under the existing laws because “few complaints are filed and few investigations are successful, few convictions are handed down”, but nevertheless determined that censorship is the panacea to the perceived problems, the French government decided to delegate the task of state censorship to the online platforms themselves. Private companies will now be obliged to act as thought police on behalf of the French state or face heavy fines. As in Germany, such legislation is bound to lead to online platforms exhibiting overzealousness in the removal or blocking of anything that might conceivably be perceived as “hateful” to avoid being fined.

The purpose of the law appears to have been twofold — not only to achieve the actual censorship of speech by the removal or blocking of online posts, but also the (inevitably) chilling effects of censorship on online debate in general. “People will think twice before crossing the red line if they know that there is a high likelihood that they will be held to account,” French Minister of Justice Nicole Belloubet said in what sounded ominous for a government representative to say in a country that still claims to be democratic.

From the beginning, when French President Emmanuel Macron first tasked the group led by Laetitia Avia with preparing the law, the proposal was met with criticism from a number of groups and organizations. France’s National Consultative Commission on Human Rights criticized the law proposal for increasing the risk of censorship, and La Quadrature du Net, an organization that works against censorship and surveillance online, warned that, “Short removal times and large fines for non-compliance further incentivize platforms to over-remove content”. The London-based free speech organization Article 19 commented that the law threatened free speech in France. According to Gabrielle Guillemin, Senior Legal Officer at Article 19:

“The Avia Law will effectively enable the French state to devolve online censorship to the dominant tech companies, who will be expected to act as judge and jury in determining what is ‘manifestly illegal’ content. The Law covers a wide range of content so this is not always going to be a straightforward decision.

“Given the timeframes by which companies have to respond, we can expect them to err on the side of caution when it comes to deciding whether content is legal or not. They will also have to resort to using filters that will inevitably lead to the over-removal of content.

“The French government has ignored the concerns raised by digital rights and free speech groups, and the result will be a chilling effect on online freedom of expression in France”.

The passed law was also met with disapproval in France. On May 22, Guillaume Roquette, editorial director of Le Figaro Magazine, wrote:

“Under the pretext of fighting ‘hateful’ content on the Internet, it [the Avia law] is setting up a system of censorship that is as effective as it is dangerous… ‘hate’ is the pretext systematically used by those who want to silence dissenting opinions.

“This text [law] is dangerous because, according to lawyer François Sureau, ‘it introduces criminal punishment… of the conscience’. It is dangerous…because it delegates the regulation of public debate… on the internet to American multinationals… A democracy worthy of its name should accept freedom of expression”.

Jean Yves Camus. from Charlie Hebdo, called the law “a placebo for fighting hate” and pointed out that the “hyper-focus on online hate” masks the real danger:

“It is not online hatred that killed Ilan Halimi, Sarah Halimi, Mireille Knoll, the victims of the Bataclan, Hyper Cacher and Charlie; it is an ideology called anti-Semitism and/or Islamism… Who determines what hatred is and its [distinction from] criticism? A Pandora’s box has just been opened… There is a risk of a slow but inexorable march towards a digital language hyper-normativized by political correctness, as defined by active minorities”.

“What is hate?” asked French writer Éric Zemmour rhetorically. “We do not know! You have the right not to love… you have the right to love, you have the right to hate. It’s a feeling… It cannot be judicialized, legislated.”

Nevertheless, that is what hate speech laws do, whether in the digital or the non-digital sphere. Asking private companies — or the government — to act as thought police does not belong in a state that claims to follow a democratic rule of law.

Unfortunately, the question is not whether France will be the last European country to introduce such censorship laws, but what other countries are next in line.

via ZeroHedge News https://ift.tt/3ekQsu3 Tyler Durden

Over 40% Of Brits Claim They’ve “Changed For The Better” During Lockdowns

Tyler Durden

Wed, 05/27/2020 – 02:45

A new study revealed that 43% of people feel they’ve “changed their ways for the better” as a result of the extra time they had during coronavirus lockdowns. Many found new habits and activities — including creating podcasts, learning to code, and exercising.

The study, commissioned by LG Electronics, polled nearly 2,000 British adults of how their daily lives were transformed because of the lockdowns. About half of the respondents said they would maintain the newly acquired hobbies, skills, and daily habits in a post-corona world.

Learning new computer skills, creating podcasts, participating in online fitness classes, and walking outside were some of the top activities people turned to during lockdowns. It was increasingly evident that technology played a significant role in occupying people’s time: 54% said they couldn’t function without a computer, 64% said smartphones were critical, and 57% couldn’t do without television.

“The fact that many people are forming productive and healthy new habits is testament to the nation’s ability to adjust,” Hanju Kim, IT product director at LG UK, said in a statement.

“The nation is working from home and has an appetite to continue working flexibly even after offices reopen. A big part of this can be attributed to technology keeping us connected,” said Kim.

Around 20% of respondents said they slept more during lockdowns, while 10% said they learned new things from YouTube tutorials.

Two-fifths of respondents believe these new habits and activities will increase their wellbeing, while one in four noticed a more comfortable life that allowed for a better routine in daily activities. About a quarter found new ways of making money during the lockdowns.

The research found that social distancing led to an increase in video conference calls among respondents, who used the software to connect with friends, family, and work. Roughly half said they conducted video calls more than they did before lockdowns.

And 48% plan to keep this up in a post-corona world, or even increase this new lifestyle, suggesting how people’s daily lives will forever change and could soon result in huge economic impacts.

Regardless of how long the current public health crisis lasts, people working at home will result in forcing huge changes and ultimately restructuring the old economy. This could have profound impacts on corporate real estate, transportation, energy, restaurants, and many other industries. With the economy crashed, the restructuring phase has just begun, it will take several years for the recovery to play out.

via ZeroHedge News https://ift.tt/2THkAYG Tyler Durden

Trump Slams Libya “Foreign Interference” & Urges “Rapid De-escalation” In Erdogan Call

Tyler Durden

Wed, 05/27/2020 – 02:00

Authored by Jason Ditz via AntiWar.com,

After weeks of military gains by Libya’s Government of National Accord (GNA), President Trump has called for a deescalation during his phone call with Turkey’s President Erdogan. Turkey is the GNA’s only foreign ally.

This is bound to once again raise questions about the US position. Nominally the US is backing the GNA, but at times Trump has expressed support for their enemy, the Libyan National Army (LNA). The deescalation would be seen as bailing out the LNA from recent losses.

“President Trump reiterated concern over worsening foreign interference in Libya and the need for rapid de-escalation,” White House spokesman Judd Deere said in a statement.

The LNA has a lot of foreign allies, from France and Russia to virtually the whole list of Gulf Arab states. LNA leader Khalifa Hafter, was a CIA asset in the past, and the US has criticized Russia for being too close with him, despite their own long history of backing him.

Reuters reports:

As the LNA has promised to respond with a massive air campaign, diplomats have warned of the risk of a new round of escalation with the warring sides’ external backers pouring in new weaponry.

Turkey “will not bow to threats by Haftar or anyone else,” Turkey’s presidential spokesman Ibrahim Kalin said separately in an interview on NTV.

LNA General Commander Field Marshal Khalifa Haftar: Every Turkish solider, mercenary sent by Erdogan to Libya and every traitor who has allowed the occupier to return is a target of our armed forces. Do not show them any mercy. #Libya #LibyaReview pic.twitter.com/ywJNeGfvkx

— Libya Review (@LibyaReview) May 23, 2020

It’s not clear where Turkey is going with this, as they mostly want maritime rights and a military base.

Those are likely secured already, but the GNA probably feels very little need to step down in the face of recent gains.

via ZeroHedge News https://ift.tt/2ZH13LU Tyler Durden

We have a choice!

Next presidential election, we don’t have to decide between two big-spending candidates, neither of whom has expressed much interest in limited government.

Now, we have a third serious choice. This week, Jo Jorgensen, a psychology lecturer at Clemson University, won the Libertarian Party’s presidential nomination.

OK, I won’t delude myself—a libertarian is unlikely to become president. But Jorgensen’s platform is a refreshing change.

She correctly points out that government “is too big, too bossy, too nosy, and way too intrusive.”

Of course, many candidates say that when running for office.

President Donald Trump said it, but once he was elected, he increased spending by half a trillion dollars, created a new military branch designed to protect U.S. interests in space, imposed tariffs, and demanded more funds for “infrastructure” and “building a giant wall.”

Joe Biden wants to spend $532 billion more, increasing spending on things like education, climate, and health care.

By contrast, Jorgensen says government should do less and spend less.

She’s right. The founders’ insistence on limited government is what made America prosperous.

Jorgensen noticed how our big and cumbersome government slowed our response to the coronavirus.

“We had about 60 American companies making testing kits and the FDA only approved two,” she said in the final Libertarian Party debate. “What the president should have done was use the Emergency Powers Act and say, ‘FDA, you only have to prove safety, not efficacy. Get these kits out there.'”

If some tests don’t work, the free market will weed that out, says Jorgensen. “If you are a large drug company, you don’t want to put out a drug or testing kit that doesn’t work—you’ll go bankrupt.”

Trump supported the latest multitrillion-dollar stimulus bill, saying, it “will deliver urgently needed relief to our nation’s families and workers.” Biden called for another stimulus—”a hell of a lot bigger.”

Jorgensen wouldn’t sign either bill. “Let the people keep their money,” she says. “Let them decide who should stay in business and who shouldn’t.”

She points out that government is not as good as individuals at deciding where money should go. “Government money usually goes to their friends and special interests and lobbyists.”

America’s most popular government program is probably Social Security. Created to help the minority of Americans who lived past age 65 at that time, it’s now an unsustainable handout to most older people. Social Security is going broke because people my age just keep living longer. Sorry. We won’t volunteer to die.

Jorgensen would save social security by offering everyone “an immediate opt-out,” something like the Cato Institute’s 6.2 percent solution, which would let individuals invest 6.2 percent of their payroll tax into a private retirement account.

While phasing the program out, she says seniors would be paid back what they’ve put in. “Sell those government assets, mineral rights, water rights, buildings downtown,” she says. “Give that money to seniors.”

Finally, Jorgensen would end “these needless wars that caused the injuries or deaths of hundreds of thousands of American soldiers…and the waste of trillions of tax dollars.” She’d “make America one giant Switzerland, armed and neutral…no American military personnel stationed in foreign countries. No foreign aid. No loan guarantees.”

This is not pacificism, she says, “I am proposing an American military force ready and able to defend the continental United States, Alaska, Hawaii, and all U.S. territories against foreign attackers.”

But like most libertarians, she doesn’t want America involved in foreign wars.

As the Libertarian Party’s presidential candidate, Jorgensen will be on the ballot in most states. Voters will have a real choice this November.

Libertarian ideas are very different from those held by today’s Democrats and Republicans. Instead of lusting for more money and power, her party proposes a government that keeps the peace and, mostly, leaves people alone.

Sounds good to me.

COPYRIGHT 2020 BY JFS PRODUCTIONS INC.

DISTRIBUTED BY CREATORS.COM

from Latest – Reason.com https://ift.tt/2Xx2cCV

via IFTTT

{kind=link}