In his 1961 farewell address, President Dwight D. Eisenhower warned against federal overreach during times of national crises.

“Whether foreign or domestic, great or small, there is a recurring temptation to feel that some spectacular and costly action could become the miraculous solution to all current difficulties,” he said.

“Today, the solitary inventor, tinkering in his shop, has been overshadowed by task forces of scientists in laboratories and testing fields…Partly because of the huge costs involved, a government contract becomes virtually a substitute for intellectual curiosity.”

In this video, we looked at how Eisenhower’s warnings can be applied to the government’s current response to COVID-19.

Music: “7” by Lex Villena; “Mareé” by Kai Engel, CC BY 4.0

Photos: Living room, smoggybeard; Eisenhower, akg-images/Newscom; Mask, Makidotvn/Dreamstime; DC archival footage, Throwback; Window, Daniel M. Cisilino/Dreamstime; NYC window, Joaquin Camejo/Dreamstime

from Latest – Reason.com https://ift.tt/2zZTk0s

via IFTTT

It is not every day that a cabinet secretary publicly attacks the decision of a federal agency, but this is 2020.

In today’s WSJ, Secretary of Defense Mark Esper criticizes the Federal Communications Commission for approving Ligado’s applicaiton to repurpose portions of radio spectrum for planned 5G services. According to the Secretary Esper, this plan will create interference for GPS services and compromise national security. Although the FCC imposed conditions, Secretary Esper maintains they are insufficient to prevent the compromise of GPS reliability and usability for both military and civilian uses.

I have no idea whether Secretary Esper’s claims have substantive merit. What interests me about Secretary Esper’s op-ed is the interagency conflict. Here we have a cabinet secretary—and presumably one of the more influential cabinet secretaries—publicly criticizing the actions of another federal agency on the op-ed page of a major newspaper.

Under normal circumstances, when two executive branch agencies disagree, the dispute is handled within the executive branch, sometimes with direct White House intervention. So, for instance, if the Environmental Protection Agency adopts rules that limit a fuel source the Department of Energy is trying to promote, the dispute will get resolved through various informal interagency processes. And, in the end, because both agencies are ultimately subject to presidential control, the White House typically has the ability to resolve the dispute in favor of one agency or the other.

In this case, however, we have an independent agency. The FCC is not subject to direct Presidential control and if the FCC votes unanimously to take a given course of action (as it did here) there is little the White House can do. So whereas the Defense Secretary could seek White House intervention to obtain relief from an EPA regulation, it is effectively powerless against the FCC. So, rather than call the Oval Office, Secretary Esper took his complaint to the WSJ, perhaps in the hope of encouraging intervention by Congress.

While public criticism of one agency by the head of another is rare, interagency litigation is even less common—but it does happen. See, for example, this litigation between the Tennessee Valley Authority and the EPA concerning TVA’s alleged Clean Air Act violations.

from Latest – Reason.com https://ift.tt/3dlhvoA

via IFTTT

In Jobaida v. Bd. of Elections, decided Monday by New York trial judge Leonard Livote, a woman whose official name (under which she was registered to vote) is Meherunnisa Jobaida sought to run in the Democratic Party primary for an Assembly seat under the name “Mary Jobaida” (apparently the name she had commonly used). She submitted the required nominating petition with voter signatures, but New York election officials rejected her petition because of the name difference:

A candidate seeking to be designated (or nominated) on a ballot is required to list her name on the petition pursuant to New York Election Law 6-134(1). The general rule is that one must petition under the name under which she is registered to vote.

“[T]he word ‘name’ as used in the Election Law should be afforded its plain, ordinary and usual sense.” (Lewis v New York State Board of Elections, 254 AD2d 568 [3rd Dept 1998].) Descriptive terms and nicknames are not permitted in the place of the candidate’s name on a petition. (Id.; [“Grandpa” Al Lewis’s name was struck from the ballot because the petition included a nickname which was impermissible].) While the use of descriptive terms and nicknames is impermissible, a candidate may use a familiar or diminutive form of her name. (See Gumbs v Board of Elections, 143 AD2d 235 [2nd Dept 1988] [candidate used the name “Marty” in place of “Martin”]; Matter of Abinanti v Duffy, 120 AD3d 669 [2d Dept 2014] (candidate used the name “Mike” in place of “Michael”)….

The Board determined that Mary is not a familiar or diminutive version of “Meherunnisa.” Accordingly, the Board determined that the Designation Petition was invalid and petitioner failed to qualify as a candidate ….

As a general rule, a petition should not be invalidated where “there is no proof of any intention on the part of the candidate or of those who have solicited on his (or her) behalf to mislead or confuse, and no evidence that the inaccuracy did or would lead or tend to lead to misidentification or confusion on the part of those invited to sign the petition.” For example, in Eisenberg v Strasser (100 NY2d 590 [2003]), the court affirmed the Second Department’s decision and agreed with the dissent stating “under these circumstances, there is no reason to disqualify the candidate for using the name ‘Tony Eisenberg’ rather than ‘Anatoly Eyzenberg,’ on his designating petition.” The petition in Eisenberg was, however, invalidated for other reasons.

Here, petitioner has sufficiently established that she held herself out both professionally and personally as “Mary” and that no intent existed to mislead signatories. Clearly, the differences in petitioner’s name in the Eisenberg case were far greater. In a county as diverse as Queens, with many exotic and unfamiliar names, an expansive view must be taken of what is familiar or diminutive. Thus, the position taken by the Board is impermissibly narrow. Accordingly, the petition is granted and … [Jobaida’s] Designating Petition … is declared valid, proper, sufficient and legally effective ….

from Latest – Reason.com https://ift.tt/3dkvtHg

via IFTTT

In Jobaida v. Bd. of Elections, decided Monday by New York trial judge Leonard Livote, a woman whose official name (under which she was registered to vote) is Meherunnisa Jobaida sought to run in the Democratic Party primary for an Assembly seat under the name “Mary Jobaida” (apparently the name she had commonly used). She submitted the required nominating petition with voter signatures, but New York election officials rejected her petition because of the name difference:

A candidate seeking to be designated (or nominated) on a ballot is required to list her name on the petition pursuant to New York Election Law 6-134(1). The general rule is that one must petition under the name under which she is registered to vote.

“[T]he word ‘name’ as used in the Election Law should be afforded its plain, ordinary and usual sense.” (Lewis v New York State Board of Elections, 254 AD2d 568 [3rd Dept 1998].) Descriptive terms and nicknames are not permitted in the place of the candidate’s name on a petition. (Id.; [“Grandpa” Al Lewis’s name was struck from the ballot because the petition included a nickname which was impermissible].) While the use of descriptive terms and nicknames is impermissible, a candidate may use a familiar or diminutive form of her name. (See Gumbs v Board of Elections, 143 AD2d 235 [2nd Dept 1988] [candidate used the name “Marty” in place of “Martin”]; Matter of Abinanti v Duffy, 120 AD3d 669 [2d Dept 2014] (candidate used the name “Mike” in place of “Michael”)….

The Board determined that Mary is not a familiar or diminutive version of “Meherunnisa.” Accordingly, the Board determined that the Designation Petition was invalid and petitioner failed to qualify as a candidate ….

As a general rule, a petition should not be invalidated where “there is no proof of any intention on the part of the candidate or of those who have solicited on his (or her) behalf to mislead or confuse, and no evidence that the inaccuracy did or would lead or tend to lead to misidentification or confusion on the part of those invited to sign the petition.” For example, in Eisenberg v Strasser (100 NY2d 590 [2003]), the court affirmed the Second Department’s decision and agreed with the dissent stating “under these circumstances, there is no reason to disqualify the candidate for using the name ‘Tony Eisenberg’ rather than ‘Anatoly Eyzenberg,’ on his designating petition.” The petition in Eisenberg was, however, invalidated for other reasons.

Here, petitioner has sufficiently established that she held herself out both professionally and personally as “Mary” and that no intent existed to mislead signatories. Clearly, the differences in petitioner’s name in the Eisenberg case were far greater. In a county as diverse as Queens, with many exotic and unfamiliar names, an expansive view must be taken of what is familiar or diminutive. Thus, the position taken by the Board is impermissibly narrow. Accordingly, the petition is granted and … [Jobaida’s] Designating Petition … is declared valid, proper, sufficient and legally effective ….

from Latest – Reason.com https://ift.tt/3dkvtHg

via IFTTT

Ukraine’s Ministry of Energy believes that using power plants for crypto mining could be one of the best ways to take advantage of a current energy glut.

Cryptocurrency mining is a contemporary and efficient way to use excess energy, Ukraine’s Ministry of Energy argued in a May 6 statement published on Facebook. According to the post, local nuclear plants have generated the surplus due to the COVID-19 lockdown.

The course toward digitalization

The bureau is now looking to apply progressive solutions to avoid wasting energy as part of the government’s course toward digitalization championed by president Volodymyr Zelensky. Leaving the situation unchanged might create “conditions for corruption offenses, which will ultimately be paid at Ukrainian citizens’ expense”, the ministry warns.

Crypto mining, in turn, could prove to be one of the efficient solutions, the post continues:

“There is a way to transfer this ‘liability’ into an ‘asset’. One of the modern approaches for using excess electricity is to devote it to cryptocurrency mining. That would not only allow to maintain the guaranteed load on the nuclear power plants, but also ensure that companies can attract extra funds. Therefore, it would open the way to a fundamentally new economy, new approaches, a new market model.”

As previously reported by a Russian-language crypto news outlet Forklog on May 5, the acting head of Ukraine’s Ministry of Energy requested the state-owned enterprise Energoatom to study potential ways to implement cryptocurrency mining at the country’s nuclear energy generating facilities by May 8.

A potentially profitable operation?

Power plants have been used for cryptocurrency mining before, although not on a government scale. As reported by Cointelegraph in March, a privately-owned power plant in New York’s Finger Lakes region turned to Bitcoin (BTC) mining, adding about $50,000 worth of BTC each day to daily revenues.

As The Gold Market Broke In March, HSBC Was Hit With A Record 12 VaR Breaches

Every quarter, banks proudly announce their VaR limits to demonstrate to the world just how overcapitalized they are for a worst case scenario. The only problem is that VaR calculations look at the past, not future, and when we get a forced global economic shutdown as a result of a viral pandemic which sends the VIX above 80, VaR models tend to… fail.

That’s what happened with the two largest European banks HSBC and BNP, whose risk limits were brutally and repeatedly violated in March as unprecedented market volatility made a mockery out of the banks’ estimates on how much they could lose or gain on their trading desks.

According to Bloomberg calcualtions, Europe’s two biggest banks exceeded their value-at-risk, or VaR limits, a measure of risk used to calculate how much capital they need to hold against potential losses, more times in March than over several years during calmer times.

In March alone, London-based HSBC’s trading models breached the daily expected profit-and-loss threshold 12 times, while French megabank BNP Paribas, which suffered hundreds of millions in losses on its various equity derivative products as discussed previously, reported nine such violations during the same quarter, close to a third of all such instances reported since 2007.

HSBC had 15 “back-testing exceptions” in January and March, when the firm was caught out by moves in the prices of precious metals. Europe’s biggest bank said it made two outsized profits and one loss in January that were driven largely by palladium volatility; subsequent problems were caused in part by “delivery disruptions in the gold market” which means that we now know which bank was on the other side of the gold spot-future trade.

While HSBC said it would normally only expect to record two to three breaches in an entire year, the pandemic “caused price disruptions that have not been observed in the past two years,” according to a filing, and in a statement to Bloomberg, the bank added that VAR “modelling forms just one part of our market risk management toolkit.” Hopefully the other “models” are more credible and don’t boil down to “beg central bank for bailout.”

At the same time, Germany’s Deutsche Bank reported several such “backtesting outliers” as well, while the largest Swiss bank, UBS, reported three “negative backtesting exceptions” in the quarter because of “unprecedented price moves in various asset classes,” filings show.

As Bloomberg notes, regulators have closely scrutinized banks that have problems gauging the risks their traders are taking ever since the huge losses racked up during the last financial crisis. While significant breaches usually lead to automatic penalties, regulators have naturally eased off when the breaches do occur, given how quickly trading models can become obsolete during such a virus pandemic, which begs the question: just what use are capital markets models, or stress tests for that matter? (Don’t answer, Nassim Taleb has written several books on the subject).

In March, the Bank of England said that it would temporarily allow banks to offset increases in value-at-risk calculations “through a commensurate reduction” in other risks they take. Which, considering the surge in loan standards, apparently means no longer offering loans or credit cards to ordinary peasants.

At BNP Paribas, the average daily value at risk soared to €35 million because of “the shock of volatility on equity markets,” mostly from mid-March onwards, according to a presentation Tuesday. That was the highest level in four years, and 49% above its quarterly average last year.

The surge in the VaR which caught the French bank unprepared, was reflected in BNP Paribas’ results. Its stock-trading business swung to a loss in the quarter, even as FICC climbed 35% as investors lifted their trading in interest rates, foreign exchange and corporate debt. Deutsche Bank has said the impact of the modeling breaches was mitigated because the European Central Bank relaxed its rules, and there was no overall impact on its capital requirements as a result.

[tl;dr] – High death tolls from the 1918 influenza pandemic likely helped the Nazis gain power in “crucial” German elections, according to new research from The Fed.

In a staff report published on Monday, researchers from the Federal Reserve Bank of New York found that German regions with higher mortality rates from the virus had a higher vote share for the Nazi Party in the elections of 1932 and 1933.

A new academic paper produced by the Federal Reserve Bank of New York concludes that deaths caused by the 1918 influenza pandemic “profoundly shaped German society” in subsequent years and contributed to the strengthening of the Nazi Party.

The paper, published this month and authored by New York Fed economist Kristian Blickle, examined municipal spending levels and voter extremism in Germany from the time of the initial influenza outbreak until 1933, and shows that “areas which experienced a greater relative population decline” due to the pandemic spent “less, per capita, on their inhabitants in the following decade.”

The paper also shows that “influenza deaths of 1918 are correlated with an increase in the share of votes won by right-wing extremists, such as the National Socialist Workers Party” in Germany’s 1932 and 1933 elections.

Together, the lower spending and flu-related deaths “had a strong effect on the share of votes won by extremists, specifically the extremist national socialist party” – the Nazis – the paper posits.

“This result is stronger for right-wing extremists, and largely non-existent for left-wing extremists.”

Perhaps Kristian Blickle, the author of the paper, should take a look closer to home – as in central bank money printing as a cause of social unrest.

The greatest inflation in the history of Germany occurred mainly from 1919-1923, but in fact it had already started in 1914, with the outbreak of WWI. When the war began, the German governments increased the money supply in order to cover the soaring costs, initially of the war itself, and afterwards, of the heavy reparations that the Allies had imposed on Germany in the Treaty of Versailles. One means of increasing the supply of money was the issue of war bonds purchased by many citizens. At the same time, it was decided to cut the linkage between the German mark and the price of gold, a connection that existed at the time in most advanced nations. The result was an expanding gap between the value of gold-based currency (the gold mark, which was actually in use until the end of the days of the German Empire) and paper currency, which could be printed in almost unlimited quantities. Flooding the market with printed money rapidly lowered its value, so that the prices rose disproportionately, while the real wage of salaried workers fell sharply.

At the same time, loans and debts lost their value by the same proportion…

This situation took its toll on the daily life of most citizens. The rise in prices that the consumer was required to pay was not matched by a rise in wages. Since wages rose more gradually, it was more difficult to keep up with the high prices…

In November 1923, the inflation reached a peak: one dollar was worth 4,200 billion German marks…Following this, the German economy recuperated over the coming years, but millions of citizens lost their capital, which had been deposited in savings plans.

Now which is more likely to spark social unrest and a dissonant desire for “someone to do something”? An extraneous flu pandemic or a government-enabled hyperinflation?

Of course, it didn’t take long for various establishment types to jump on these “findings”…

Research from British thinktank the Royal United Services Institute has warned that far-right groups and individuals are exploiting the Covid-19 crisis by “promoting disinformation and conspiracy theories to enhance their anti-immigrant or anti-government agendas and attract a new range of followers.”

Speaking to CNBC’s “Squawk Box Europe” in April, Tina Fordham, head of global political strategy at Avonhurst, said she was concerned that the pandemic could see a fresh emergence of support for extreme nationalist ideologies in Europe.

“The risk here is really a return to populism, which a few years ago was something we were all very concerned about,” she said.

“And that focus on a national self-interest is going to pave the way for the return of the (Matteo) Salvinis and others who are waiting in the wings for this.”

However, Pushan Dutt, professor of economics and political science at INSEAD, told CNBC in an interview that he did not believe the pandemic would push voters toward extreme politics.

“I think the first thing people thought about was technocratic and competent leadership,” he said.

“And I think they’re moving away from these populist politicians, whether they’re coming in from the left or coming in from the right.”

The Fed study finds that “a one std. deviation increase in the proportion of the population killed by influenza was associated with an up to 3% increase in the share of the vote won by the national socialist party,” but, as the above comments on soaring inflation (and inevitably hyperinflation) suggest the “Flu-Feeds-Nazis” theory collapses in a haze of correlation is not causation…

…but then again, bastardizing what Upton Sinclair is credited with saying “It is difficult to get a man [or woman] to understand something, when his salary [or her research grant] depends on his [her] not understanding it.”

Thousands Donate To GoFundMe For Jailed Salon Owner Who Stood Up To Judge In Viral Video

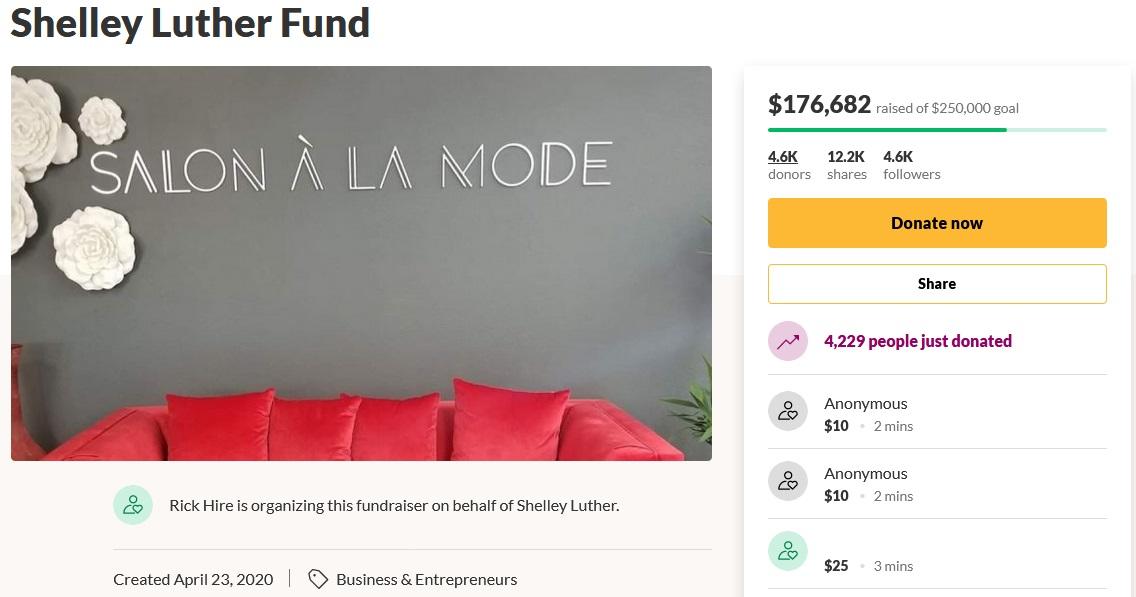

A GoFundMe account set up for a Texas salon owner who was sentenced to seven days in jail for denying Governor Greg Abbott’s stay-at-home rules has raised over $175,000 as of this writing.

Shelly Luther, owner of Salon À la Mode, found to be in criminal and civil contempt by Judge Eric V. Moyé of 14th Civil District Court in Dallas County, who also slapped her with a $7,000 fine, after she continued to operate in violation of the statewide order and a restraining order from the court.

Luther, 46, received a cease-and-desist letter from ordering her to close the salon. Instead, she made a public display of ripping it up – which gained attention among supporters, several of whom were at court.

Judge Moyé chastised Luther, saying she acted selfishly when she resumed operations – and called on her to apologize to elected officials whose orders she disobeyed. Moyé added that until a vaccine is found for COVID-19, citizens must obey emergency orders, according to the New York Times.

“Failure to do so will only have catastrophic consequences,” he said, adding “and those reach far beyond the exigencies of one family or one business.”

In response, Luther said in a now-viral video: “I have to disagree with you, sir, when you say that I’m selfish, because feeding my kids is not selfish,” adding “So, sir, if you think the law’s more important than kids getting fed, then please go ahead with your decision. But I am not going to shut the salon.“

Watch:

While criminals are being released into the streets, Shelley was sentenced to 7 days in jail.

Humans are inherently social creatures, and that is never going to change. Within each one of us there is a fundamental need for connection with others, but now these coronavirus lockdowns have separated us from one another like never before. Thankfully, many states are now starting to end their lockdowns, but unfortunately this is definitely not the end for “social distancing”. Just as 9/11 greatly altered our society on a permanent basis, many of our social engineers now intend to make “social distancing” a permanent part of our lives. If they have their way, there will be written or unwritten rules about how close you can get to other people virtually everywhere that you go.

Can you imagine a world where you have to constantly be concerned about walking, standing or sitting too close to someone else?

Already, there is talk of putting physical markings on sidewalks in order to constantly remind all of us not to walk too closely to one another…

Arrows on the ground, and other physical markers to encourage and enforce distance. Imagine sidewalks with scoring every 6 feet so those walking could make sure they’re the human equivalent of a few car lengths behind. Or large sculptures deployed to separate people.

We are being told that restaurants may have to start putting empty tables between customers, sports stadiums may have to keep at least half their seats empty, and churches may have to start holding services in shifts.

Just like in the days after 9/11, we will be told that the changes are just “temporary measures”, but once we accept “temporary measures” long enough they have a way of becoming permanent.

When I was much younger, I loved to attend concerts. And at first I was encouraged to hear that some states were going to start allowing live concerts once again, but then I learned about the new “fan pods”…

Travis McCready, the singer of the country-rock band Bishop Gunn, will be performing what’s billed as an “intimate acoustic set” in Fort Smith at the city’s TempleLive venue — but with social distancing measures in place. The show will take place on May 15, three days before the scheduled reopening.

According to Billboard, assigned seats for the show will be at least six feet apart per grouping in what Ticketmaster is calling “fan pods.” As fans enter the venue, they’ll be required to wear face masks (including the venue’s employees), have their temperatures taken at the door and capacity for the 1,100 person venue will be capped at 229.

Are you kidding me?

I understand that they are trying to prevent the spread of the virus, but it isn’t going to work.

Look, unless you plan on locking yourself in your own home for the next couple of years, you are almost certainly going to be exposed to the virus no matter how careful you are.

And once you are exposed to the virus, what is really going to matter is the strength of your immune system, and so that should be your focus instead of trying to maintain “proper social distancing” at all times.

To me, some of the “social distancing” measures that we are now seeing are completely and utterly ridiculous. For example, at one supermarket in Philadelphia cashiers are actually working in “tent-like” plastic enclosures…

At a Philadelphia supermarket, the cashier’s side of each checkout line has been outfitted with a tent-like plastic enclosure, keeping essential workers safe while on the job.

Alexander Tavares, 19, captured now-viral footage of the new working conditions, constructed to prevent the spread of the coronavirus, at a store on March 25.

Those enclosures may protect those workers for a short period of time, but it is inevitable that they will eventually be exposed to the virus.

This pandemic is never going to burn itself out until herd immunity is achieved, and herd immunity is never going to be achieved until about 70 percent of the population catches the virus.

Of course it would be wonderful if someone could actually find a way to keep 70 percent of the population from becoming infected, but because this virus spreads like wildfire that simply is not going to be possible.

In the end, “social distancing” can temporarily slow the transmission of the virus, but roughly the same proportion of the population will eventually catch it whether we have “social distancing” or not.

Thankfully, some industries are already starting to push back against “social distancing”. There has been an effort to require airlines to keep middle seats vacant on all flights from now on, and the airlines are fighting this really hard…

Airlines are pushing back on proposals to require social distancing onboard aircraft. During a press briefing today, airline industry group IATA argued that leaving the middle seat vacant would hurt airlines’ ability to recover from the coronavirus crisis and potentially cause a spike of up to 54% in airfares.

If you get on an airplane, you pretty much have to assume that you are going to be exposed to all sorts of nasty bugs. That has always been true, and there will never be a time when it isn’t true.

If you don’t want to be exposed to all sorts of nasty bugs, just don’t fly.

As far as COVID-19 is concerned, there are literally thousands of ways that you could potentially catch this virus, and anyone that believes that “proper social distancing” will keep people 100 percent safe is just being delusional.

Sadly, “social distancing” has been pounded into our heads so relentlessly in recent weeks that a big chunk of the population has become big believers in it.

On Wednesday, Education Secretary Betsy DeVos formally announced the new rules related to Title IX—the federal statute that governs sexual misconduct in schools—thus completing a process that began more than a year ago, when the government first unveiled its proposed changes.

The new rules aim to protect victims of sexual misconduct while also establishing fairer procedures for the accused. The department believes the new rules will “balance the scales of justice on campuses across America,” a Department of Education spokesperson said during today’s press briefing.

Justin Dillon, an attorney with the firm KaiserDillon who specializes in campus misconduct adjudication, hailed the new rules as tremendously well thought out.

“Nothing Betsy DeVos has done since she took office will have a more lasting effect on people’s lives than this,” Dillon tells Reason. “It’s frankly inspiring to see how hard she and her staff have worked to get these regulations done and get them right.”

The new rules are similar to what the Department of Education proposed in November 2018. Most notably, the government has abolished the single-investigator model, which previously permitted a sole university official to investigate an accusation of misconduct, decide which evidence to consider, and produce a report recommending an outcome. Under the new rules, the final decision maker must be a different person than the investigator, and a finding of responsibility can only be rendered after a hearing in which a representative for the accused is able to pose questions to the accuser—i.e., cross-examination.

Importantly, the new rules narrow the scope of actionable sexual harassment to exclude conduct that ought to be protected under the First Amendment. Obama-era guidance had defined sexual harassment as “any unwelcome conduct of a sexual nature.” The new rules keep this definition but add that the conduct must be offensive to a reasonable person, severe, and pervasive. In practice, this should mean that schools will no longer initiate Title IX investigations that impugn free speech.

“This new rule strikes a powerful blow against campus censorship,” said a Department of Education spokesperson. “Campus free speech must not be sacrificed in the misguided pursuit of any other value.”

The new rules will also end the pernicious practice of universities initiating Title IX investigations in cases where the alleged victims are not interested in this course of action. Under previous guidance, any university official who became aware of a potential Title IX issue had to report it, thus triggering an investigation. Under the new guidance, school employees should make the Title IX office aware of potential issues, which will prompt these officials to reach out and offer support to victims. But a formal complaint that results in adjudication can only be initiated by the victim or their parents/legal guardians. This approach gives agency to victims and prevents schools from taking actions contrary to their wishes.

Nevertheless, victims’ rights advocates intend to fight the new rules in court. Catherine Lhamon, current chair of the U.S. Commission on Civil Rights and the former Obama administration officialwho presided over the changes that compromised due process, slammed the reforms as “taking us back to the bad old days, that predate my birth, when it was permissible to rape and sexually harass students with impunity.” That’s a gross misrepresentation of what DeVos has done, though not an unexpected one, given how irresponsibly activists and members of the media have characterized DeVos’s work.

It remains to be seen whether colleges and universities will carefully follow the new rules—much is uncertain about the future of higher education right now. Nevertheless, today is a big day for the restoration of basic due process and free speech rights in schools.

The new rules, which take effect in August, are available here.

from Latest – Reason.com https://ift.tt/2Ww3fme

via IFTTT