Central banks continued their gold-buying spree in February, although the pace of gold purchases has slowed compared to last year’s near-record purchases.

On net, central banks globally added another 36 tons of gold to their reserves in February, according to the latest data released by the World Gold Council. That was about 33% higher than January’s total.

On the year, central banks have bought 64.5 tons of gold. That compares to 116 tons through the first two months of 2019.

Central bank demand came in at 650.3 tons in 2019. That was the second-highest level of annual purchases for 50 years, just slightly below the 2018 net purchases of 656.2 tons. According to the WGC, 2018 marked the highest level of annual net central bank gold purchases since the suspension of dollar convertibility into gold in 1971, and the second-highest annual total on record.

The World Gold Council bases its data on information submitted to the International Monetary Fund.

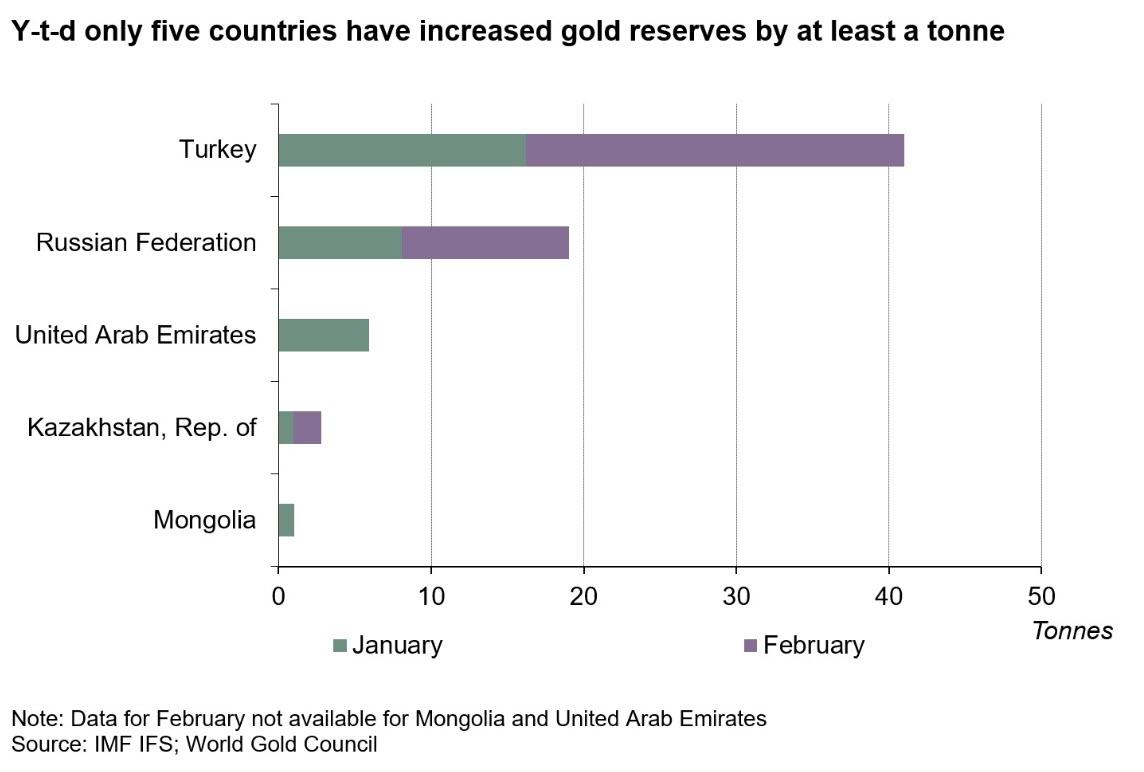

Turkey continued to be the biggest gold-buyer. The Turks added another 24.8 tons to their reserves in February.

Russia further increased its stockpile of yellow metal, adding another 10.9 tons to their hoard.

The Russians have been buying gold for the last several years in an effort to diversify away from the US dollar. Russian gold reserves increased 274.3 tons in 2018, marking the fourth consecutive year of plus-200 ton growth. Meanwhile, the Russians sold off nearly all of its US Treasury holdings. According to Bank of America analysts, the amount of US dollars in Russian reserves fell from 46% to 22% in 2018.

Last month, the Central Bank of Russia announced it planned to suspend gold-purchases for the time being, effective April 1. But in the first week of April, Russian banks were already asking the central bank to restart gold purchases. They expressed concern over gold exports amid disruptions in the transportation industry due to the coronavirus pandemic. National Finance Association head Vasily Zablotsky told Reuters that banks are “facing problems” exporting gold as there are also fewer cargo flights and transportation costs have doubled.

Other buyers of gold in February included:

Bulgaria – 0.3 tons

Greece – 0.1 tons

Kazakhstan – 1.8 tons

Qatar – 1.6 tons

The only major seller was Uzbekistan at 3.1 tons.

The People’s Bank of China did not report any gold purchases for the fifth straight month. It’s not uncommon for China to go silent and then suddenly announce a large increase in reserves.

Many analysts believe China holds far more gold than it officially reveals. As Jim Rickards pointed out on Mises Daily back in 2015, many people speculate that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE). Given the political dynamics and the ongoing trade war, it seems unlikely the Chinese suddenly stopped increasing their gold reserves in 2016.

The WGC said it expects central banks to remain net-buyers of gold in 2020, but likely at a slower pace than the record levels we’ve seen over the past two years.

“We often get asked if central bank demand will be sustained. The past two months clearly suggest gold continues to be an important component of foreign reserves despite heightened levels of demand in recent years. But like everyone else, the recent market instability and uncertainty will be at the forefront of central bankers’ mind.”

Of course, it is difficult to tell how the economic impacts of the coronavirus pandemic will impact things down the road. It is possible that a rapid devaluation of the dollar due to Federal Reserve quantitative easing could drive central banks to dump dollars in exchange for gold.

Earlier this year, World Gold Council director of market intelligence Alistair Hewitt said there are two major factors driving central banks to buy gold – geopolitical instability and extraordinarily loose monetary policy.

Central banks are looking toward gold to balance some of that risk. We’ve also got negative rates and yields for a large number of sovereign bonds.”

Central bank policy has become significantly looser since Hewitt made that observation.

The days where the dollar is the reserve currency are numbered and we’re going back to basics. You know, everything old is new again. Gold was money in the past and it will be money again in the future, and central banks that are smart enough to read that writing on the wall are increasing their gold reserves now.”

We simply can’t expect people to stay cooped up for a year or longer, as some have suggested. And there are reasons for cautious optimism anyway: Although the data are hazy and ever-changing, decreasing rates of infection and death in parts of Asia, Europe, and the United States suggest that non-pharmaceutical interventions like better hygiene and social distancing have indeed made COVID-19 more manageable.

But we can’t just blindly open the gates and infect vulnerable populations that overwhelm the healthcare supply, either. Not only could that scenario increase the threats to healthcare workers and first responders, it could compel people to stay home more often anyway for fear of the virus, which would create the same economic problem that the re-opening was trying to fix.

The challenge is how to intelligently get closer to normal without letting COVID-19 transmissions get out of control. The specific pathway to open the United States back up is still unclear, but we’ll probably need at least three things to do so: near-universal mask-wearing, targeted mass testing, and a virus-tracing surveillance system.

The first two conditions should find few dissenters. We should make sure that our essential workers have enough personal protective equipment, but in the meantime, pandemic civilians can dramatically cut down on the viral spread by simply wearing a good homemade mask. Strategically testing to determine where the virus has spread is similarly a no-brainer, since it allows us to separate virus-free “green zones” that can be loosened up from beleaguered “red zones” that need to continue control measures.

But when you start talking about “surveillance,” many may understandably chafe. In our age, the word is synonymous with rights-defying government snooping, and so it immediately smacks of a conspiracy to spy.

But surveillance has a more innocuous meaning in the context of public health. The official definition is the “ongoing, systematic collection, analysis, and interpretation of health-related data essential to planning, implementation, and evaluation of public health practice, closely integrated with the timely dissemination of these data to those responsible for prevention and control.” Less spying on your Facebook messages to see whether you’re up to no good, more looking at seasonal influenza trends to determine which vaccine to recommend this year.

For the COVID-19 pandemic, public health surveillance mostly means contact tracing. When an infectious disease is in a manageable state, outbreaks can be contained by identifying who is sick and “tracing” the other people with whom they have made “contact.” Those sick patients can then be surgically quarantined to stop the spread while their contacts are monitored to see whether they too develop symptoms. Meanwhile, those who are healthy or who have immunities can continue on mostly unimpeded.

In the past, contact tracing took a lot of public health officials’ shoe leather. To beat back the 2014-2016 Ebola outbreak in Africa, for instance, officials asked patients to physically write out a list of people they remembered seeing recently. Faulty memory and insufficient resources meant that some cases could go undiscovered, and public health surveillance was not as effective as it might have been.

Today, we have technology to help. We can devise applications and wearables to help us see how diseases are spreading by monitoring with whom we come into contact. If one of us falls sick, we can review whom we’ve been around to hopefully catch new outbreaks before they spiral out of control.

And this is where the typical definition of surveillance can rear its ugly head. Many worry that such technology-enabled contact tracing can indeed become a tool for state control. After all, what government wouldn’t want to get its greedy paws on such a God View of society? (Setting aside the question of whether it already has one.)

The governments of South Korea and China have rolled out mandatory apps that capture and share people’s full location and identification data. This may have helped to spread to tide of COVID-19, but at a great cost to privacy. In China’s case, the data are already being shared with law enforcement. Perhaps it will continue being collected long after the pandemic passes.

But as Peter Van Valkenburgh of Coin Center points out, there is no need to sacrifice either public health or privacy.

Here’s an example from Singapore: The country’s Government Technology Agency developed an app called TraceTogether that takes note of each user’s SARS-CoV-2 (the virus that causes COVID-19) status and which other app users each person comes into contact with using Bluetooth signals. If a person tests positive, they update their status on the app, which triggers a notification to others that someone they recently saw tested positive. This not only helps individuals know when they should be limiting social interactions and monitoring their symptoms, it also gives epidemiologists an easy way to trace contacts and determine how the virus is spreading.

Singapore’s system is better and less intrusive because it is voluntary (each user can choose whether to download the app or share with health officials or both), anonymizes the data before sharing, and does not track GPS data (because it relies on Bluetooth, it merely senses other nearby phones). You will know that you came into contact with someone with COVID-19, but you won’t necessarily know who or where.

But we can do even better than that. As Van Valkenburgh notes, some TraceTogether data are still stored in a central location and tied to a person’s phone number, which is less than ideal. By borrowing some tools from cryptography, we can design a system that not only uses Bluetooth to track possible infections, but we can do in a way that conceals our phone numbers and does not require storage on a central server managed by a government or corporation. The ZCash Foundation has already put forth a proposal to build such a system, and similar projects are in development across the world.

The race to develop privacy-preserving contact tracing technologies stepped up in a big way last week when Apple and Google announced a joint partnership to develop APIs and tracing systems that can assist the applications that government bodies eventually roll out. The companies report that their tracing tech will use anonymized encrypted Bluetooth sensing like Singapore. But we’ll want to scrutinize their offerings and any other private- or government- developed applications to ensure that they are as privacy-preserving as possible.

Emergencies are precisely the times when powerful groups seek to expand their control. The promises and perils of new public health surveillance technologies are no exception to that trend.

In the American context, scrutiny is particularly prudent. At the same time that encryption technologies are proving more critical than ever, an effort to kneecap safe computing techniques is snaking its way through the halls of Congress in the form of the EARN IT Act.

Officials may say that their apps and offerings protect privacy. Yet at the same time, many of them defend privacy-killing measures like the EARN IT Act. We cannot just take their word. To ensure that any contact tracing applications are truly privacy-preserving, we must be able to take a look under the hood and verify that they are designed in a way like Van Valkenburgh describes. Anything else is just too risky.

from Latest – Reason.com https://ift.tt/2XC7wGK

via IFTTT

From Thursday’s N.Y. appellate decision in Cohen v. Cohen:

We agree with the father that, by directing him to comply with the “cultural norms” of Hasidic Judaism [which were practiced by the parties during the marriage] during his periods of parental access, the Supreme Court ran afoul of constitutional limitations by compelling the father to himself practice a religion, rather than merely directing him to provide the children [age about 5 and 7 at the time of the order] with a religious upbringing (see Cohen v. Cohen, 177 AD3d at 852; Weisberger v. Weisberger, 154 AD3d at 53). While the court referred to the “cultural norms” by which the children were raised, the testimony at the hearing made clear that the “cultural norms” referenced were that each parent would comply with the religious requirements of Hasidic Judaism. Under this Court’s decisions in Weisberger and on the prior appeal, the court’s directive that the father himself comply with these religious practices was an unconstitutional modification of the religious upbringing provision in the judgment of divorce, which must be reversed (see Cohen v. Cohen, 177 AD3d at 852; Weisberger v. Weisberger, 154 AD3d at 53).

I think this is right, though I disagreed with the appellate court’s earlier decision upholding an earlier trial court order in the same case, in which “the father was directed to provide the children with exclusively kosher food and to make ‘all reasonable efforts to ensure that the children’s appearance and conduct comply with the Hasidic’ religious requirements of the [mother] and of the children’s schools as they were raised while the children are in [his] physical custody.'” For more on that, see this post.

from Latest – Reason.com https://ift.tt/3a8JgPc

via IFTTT

From Thursday’s N.Y. appellate decision in Cohen v. Cohen:

We agree with the father that, by directing him to comply with the “cultural norms” of Hasidic Judaism [which were practiced by the parties during the marriage] during his periods of parental access, the Supreme Court ran afoul of constitutional limitations by compelling the father to himself practice a religion, rather than merely directing him to provide the children [age about 5 and 7 at the time of the order] with a religious upbringing (see Cohen v. Cohen, 177 AD3d at 852; Weisberger v. Weisberger, 154 AD3d at 53). While the court referred to the “cultural norms” by which the children were raised, the testimony at the hearing made clear that the “cultural norms” referenced were that each parent would comply with the religious requirements of Hasidic Judaism. Under this Court’s decisions in Weisberger and on the prior appeal, the court’s directive that the father himself comply with these religious practices was an unconstitutional modification of the religious upbringing provision in the judgment of divorce, which must be reversed (see Cohen v. Cohen, 177 AD3d at 852; Weisberger v. Weisberger, 154 AD3d at 53).

I think this is right, though I disagreed with the appellate court’s earlier decision upholding an earlier trial court order in the same case, in which “the father was directed to provide the children with exclusively kosher food and to make ‘all reasonable efforts to ensure that the children’s appearance and conduct comply with the Hasidic’ religious requirements of the [mother] and of the children’s schools as they were raised while the children are in [his] physical custody.'” For more on that, see this post.

from Latest – Reason.com https://ift.tt/3a8JgPc

via IFTTT

Dimon Warns Of “Severe Recession” As JPM Profit Plunge To 7 Year Low On Billions In Covid-Linked Credit Losses

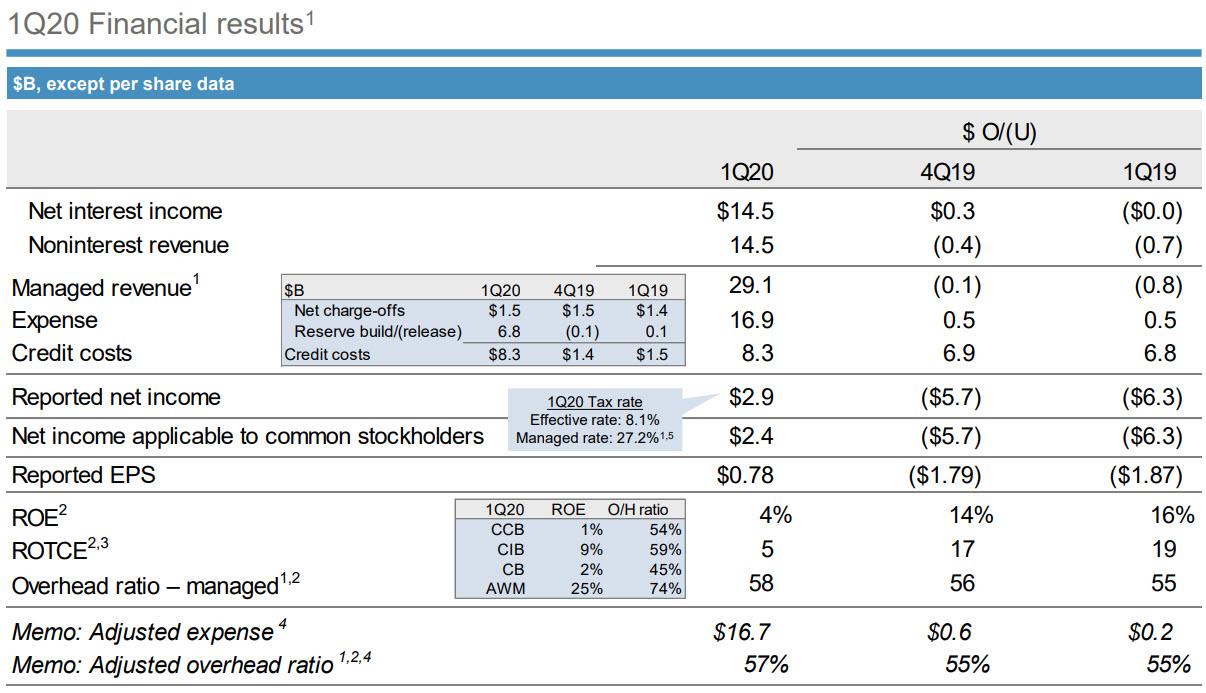

And so the worst quarterly earnings season since the financial crisis (at least until the catastrophic Q2 earnings) is off, when moments ago JPMorgan reported that it missed expectations, with earnings plunging from a year ago, reporting Q1 adjusted revenue of $29.07 billion, which was -2.6% y/y, and missed the estimate of $29.52 billion, while Q1 EPS was 78c, down 71% from the $2.65 reported a year ago.

Breaking these down, net interest income was $14.5 billion, flat versus the prior-year, with the impact of lower rates offset by balance sheet growth and mix as well as higher net interest income in CIB Markets. Noninterest revenue was $14.5 billion, down 5%, and included a $951 million loss in Credit Adjustments & Other in CIB driven by what the bank said was “funding spread widening on derivatives and $896 million of markdowns on held-for-sale positions in the bridge book”. Noninterest expense was $16.9 billion, up 3%, driven by higher volume- and revenue-related expense and investments, as well as higher legal expense, partially offset by lower structural expense.

As a result, JPM recorded profits of just $2.865BN, down 69% Y/Y, and the lowest since 2013 as the largest US bank recorded a surge in credit losses to $8.3BN, up from $1.5 billion a year ago, mostly in the form of a reserve build as JPM braced for a surge in defaults linked to the coronavirus crisis.

Before we dig into the rest of the results, here is what everyone was looking for: the bank announced that it had added a whopping $6.8 billion in reserves this quarter, while keeping its net charge offs flat on Q/Q and Y/Y. The total provision for credit losses was $8.3 billion, “driven by reserve builds which reflect deterioration in the macro-economic environment as a result of the impact of COVID-19 and continued pressure on oil prices.”

Separately, JPM also reported that the impact of CECL adoption lifted reserves by $4.3 billion, which together with the $6.8 billion Covid-19 related reserve build, took the firmwide total of $14.3BN at the end of 2019 and almost doubled it to $25.4 billion.

Detailing the breakdown, JPM said that the Consumer reserve build was $4.4 billion, predominantly in Card, and the Wholesale reserve build was $2.4 billion across multiple sectors, with the largest impacts in the Oil & Gas, Real Estate, and Consumer & Retail industries.

And this is just the start: looking ahead, JPM said that expects more net reserve builds in Q2 2020.

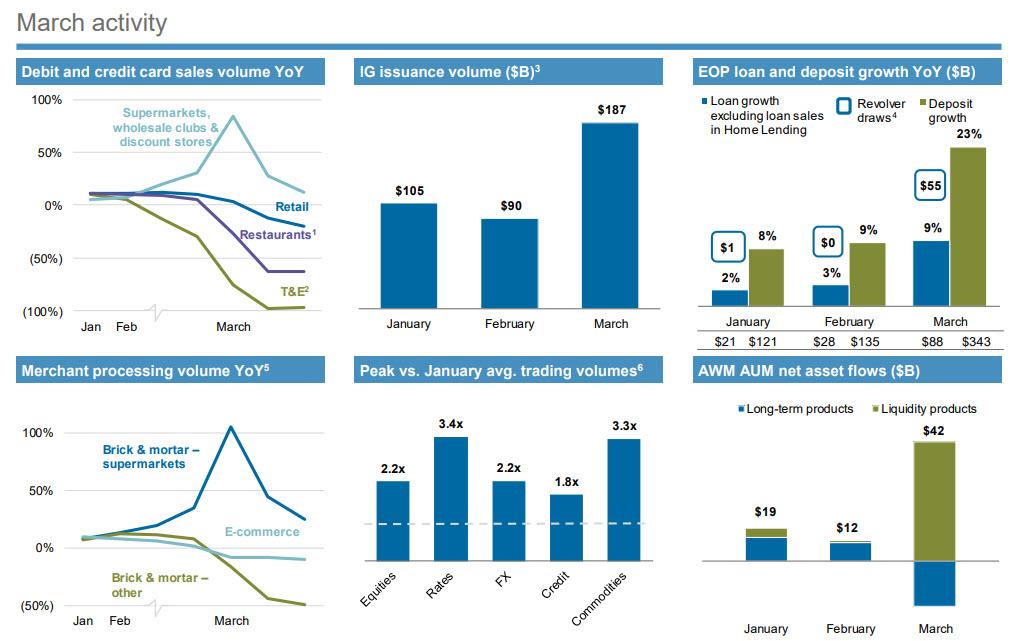

To demonstrate just how major the impact from Covid-19 – for which the bank had reserved $6.8 billion – was, the bank showed a chart detailing the changes in March activity.

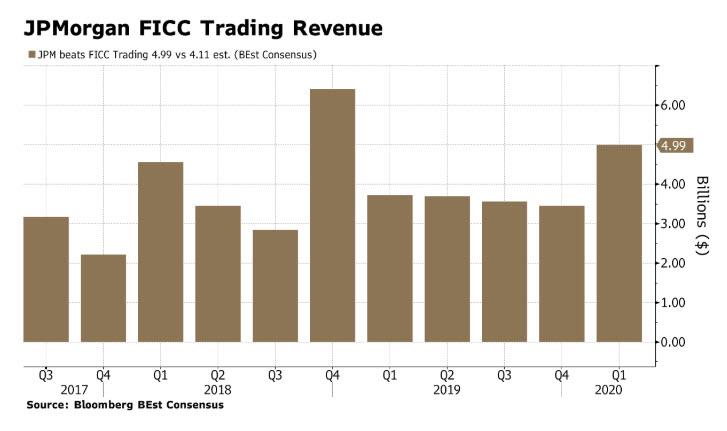

We’ll get back to the bank’s balance sheet shortly, but first let’s look at the rest of the company’s operations, starting with investment banking and trading, where we saw an impressive surge in results with JPM reporting FICC sales & trading revenue of $4.99 billion, a whopping +34% increase and far better than the estimate of $4.11 billion “driven by strong client activity across products”

And while Q1 equities sales & trading revenue also surged on the March market chaos, rising to $2.24 billion, or up +28% y/y, high above the estimate of $2.05 billion “predominantly driven by higher revenue in derivatives“, investment banking revenue collapsed nearly in half, and at just $886 million it was down 49% y/y, missing badly the estimate of $1.79 billion. And even as IB fees were up 3%, reflecting higher debt and equity underwriting fees, largely offset by lower advisory fees, JPM reported that it recorded $820mm of markdowns on HFS positions in the “bridge book.” What is the bridge book? “The bridge book consists of certain held-for-sale positions, including unfunded commitments, in CIB and CB.” Expect manyu questions on the earnings call for more details on these markdowns.

Stepping away from FICC, JPM reported that its Q1 net yield on interest-earning assets was 2.37%, sharply below the 2.56% last year y/y, but above the estimate of 2.34%.

Jamie Dimon also said that the bank’s clients drew over $50 billion on their existing lines, and that the bank provided over $25 billion of new credit extensions in March for companies most impacted by the crisis and helped our clients execute record Investment Grade bond issuances this quarter

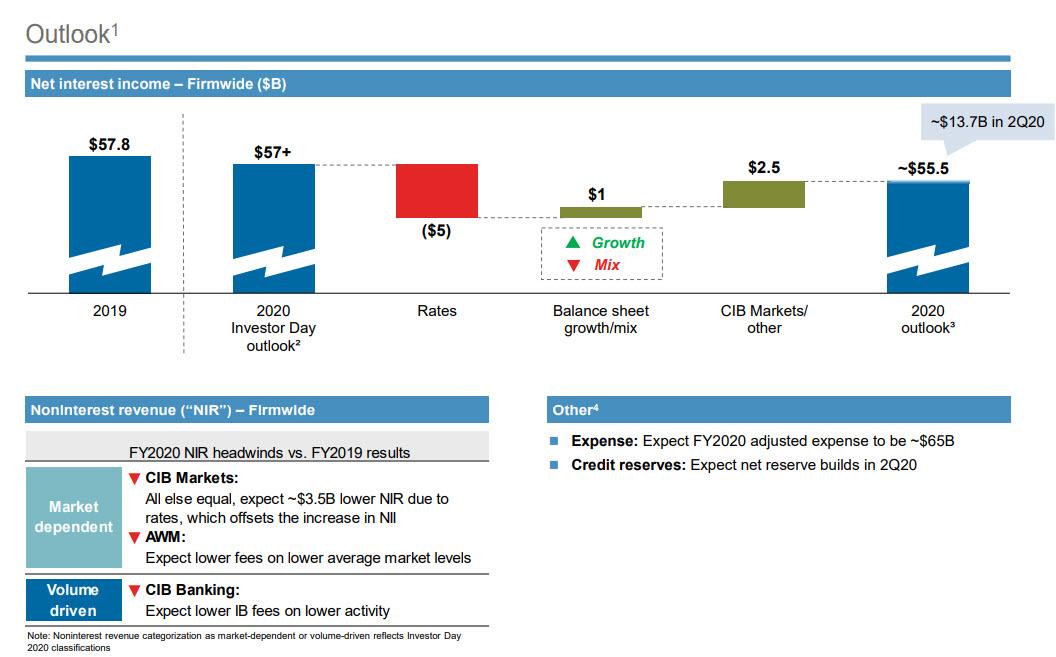

The outlook was cloud: looking ahead, JPM cut its 2020 Net Interest Income forecast, and now sees $55.5BN for the full year, down from $57BN guided in its investor day, and down from $57.8BN for the full year 2019. JPM also sees FY 2020 adjusted expense of $65B.Up

The Q1 letter was notable for a lengthy letter and comments from CEO Jamie Dimon.

Jamie Dimon, Chairman and CEO, commented: “My heart goes out to the communities and individuals, including healthcare workers and first responders, most deeply hit by the COVID-19 crisis. Throughout our history, JPMorgan Chase has built its reputation on being there for clients, customers and communities in the most critical times. This unprecedented environment is no different. We will do everything in our power to help the world recover from this global crisis.”

Dimon added: “The company entered this crisis in a position of strength, and we remain well capitalized and highly liquid – with a CET1 ratio of 11.5% and total liquidity resources of over $1 trillion. And JPMorgan Chase performed well in what was a very tough and unique operating environment – growing deposits in every line of business and providing loans as we extended credit and served as a port in the storm for our clients and customers. In the first quarter, the underlying results of the company were extremely good, however given the likelihood of a fairly severe recession, it was necessary to build credit reserves of $6.8B, resulting in total credit costs of $8.3B for the quarter.”

Dimon commented on the results: “The first quarter delivered some unprecedented challenges and required us to focus on what we as a bank could do – outside of our ordinary course of business – to remain strong, resilient and well-positioned to support all of our stakeholders. In Consumer & Community Banking, we have remained focused on meeting our customers’ needs. Approximately three quarters of our 5,000 branches have been open – all with heightened safety procedures and many with drive-through options – and the vast majority of our over 16,000 ATMs remain open. In March alone, we opened half a million new accounts for our card customers and extended over $6 billion of new and increased credit lines, and we were active in Home Lending and Auto. We lent over $500 million to small businesses in the month and we’re now actively supporting the SBA’s Paycheck Protection Program. For the quarter, we continued to see flows into both client investment assets and deposits.”

Dimon continued: “We continued to support our wholesale clients throughout this challenging period, as they drew over $50 billion on their existing lines. We also provided over $25 billion of new credit extensions in March for companies most impacted by the crisis and helped our clients execute record Investment Grade bond issuances this quarter. In Commercial Banking, we partnered closely with clients on their liquidity needs, increasing loans $25 billion and deposits $40 billion in the quarter. The Corporate & Investment Bank turned in another solid quarter with record Markets revenue, as we helped clients navigate extremely tough and volatile market conditions, and we maintained our #1 rank in Global IB fees as clients turned to us for financing and advice. And in Asset & Wealth Management, we saw strong growth in both loans and deposits, we took in $75 billion in liquidity flows, and more importantly we proactively reached out and helped clients manage their risk. In addition, JPMorgan Chase made a $50 million commitment to help address the immediate humanitarian crisis, as well as the long-term economic challenges that the most vulnerable people face. And the firm announced a $150 million loan program to help community partners get capital to underserved small businesses and nonprofits, particularly in the hardest hit communities.”

Dimon concluded: “I want to thank our more than 250,000 employees for remaining steadfast in helping our clients, customers, communities and governments and continuing to operate with the highest standards every day. I’m proud of the extraordinary effort by our call center employees, traders, bankers, portfolio managers, technology and operations teams across the globe. I also want to thank Daniel Pinto, Gordon Smith, our Operating Committee and our senior leaders for the exceptional leadership they have shown under the most difficult of circumstances. Finally, the countries and citizens of the global community will get through this unprecedented situation, undoubtedly stronger for it. Together, we will rise to the challenge.”

US Coronavirus Death Toll Nears 25k As European Slowdown Continues: Live Updates

As groups of states on the West and East Coast promised to release plans for reopening the economy in the coming days, while President Trump continued to insist that the decision of when to reopen the economy rests with him alone. Last night, we shared a detailed timeline developed by Morgan Stanley illustrating how the bank’s analysts expect the reopening will unfold.

Tensions between the President and the press reached a new breaking point last night, as Trump jousted with a CBS News reporter and insisted that “everything we did was perfect” and that he had “total authority” over when to reopen the economy, which he said would happen “ahead of schedule.” Meanwhile, Dr. Fauci insisted he didn’t mean to imply that the administration should have ordered a lockdown in mid- or late-February, a time when even Dr. Fauci was cautioning the public that the most strict measures weren’t necessary – at least not yet.

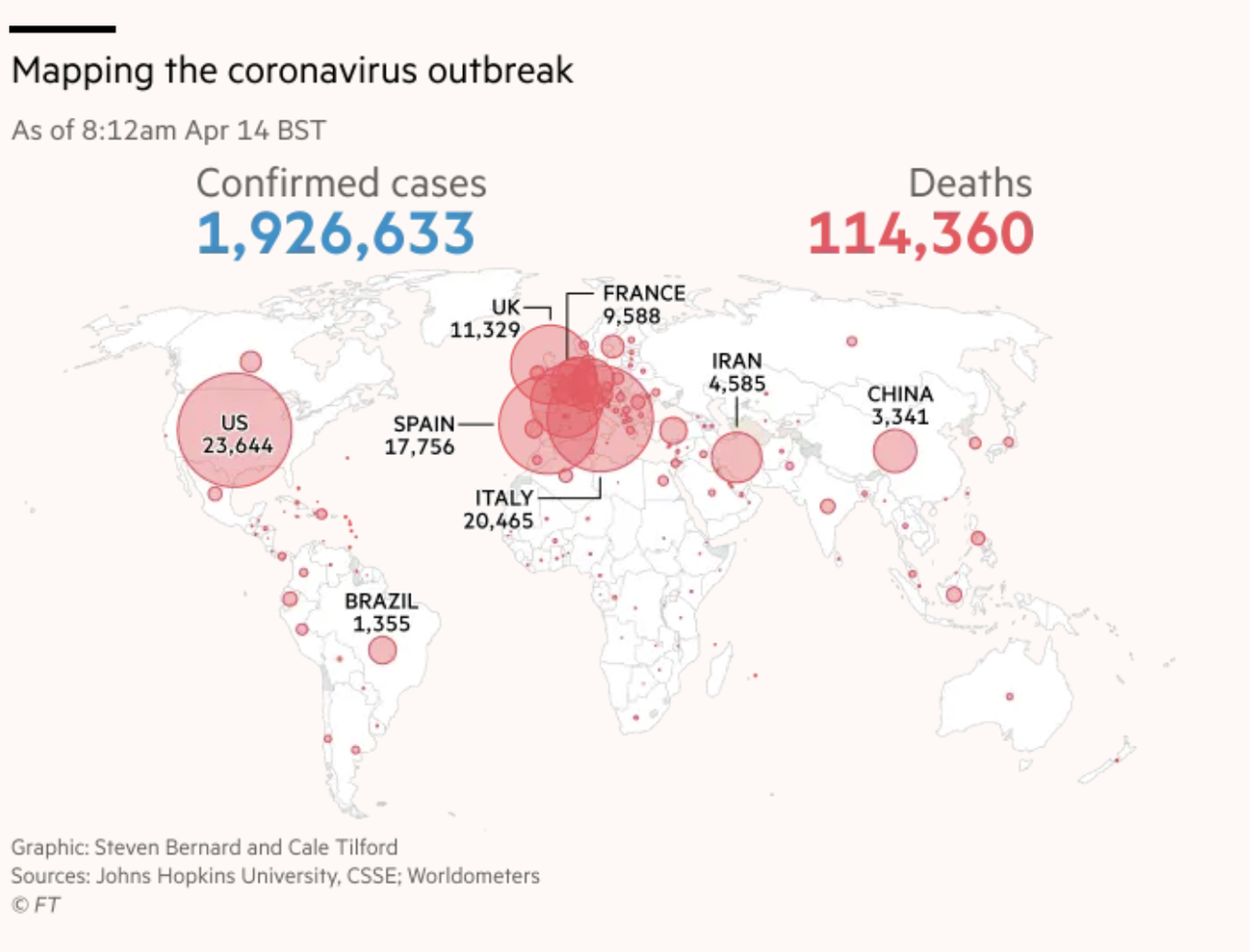

All the while, US deaths are nearing 25,000, as the total number of confirmed cases in the country near 600k.

Meanwhile, over in Europe, Italy and Spain are beginning to let more workers return to their shops and worksites while French President Emmanuel Macron last night warned that France still had a long way to go, before extending the French lockdown until mid-May while acknowledging that “we weren’t prepared”.

This week’s Bank of America fund manager survey discovered that fund managers are sitting on more cash right now than at any time since 9/11.

As millions of Americans clamor for bringing more of the medical supply chain back under the control of the US, now that the world has seen what relying too heavily on China-based supply chains can lead to, NATO Secretary General Jens Stoltenberg said Tuesday that there would be a meeting of alliance members to discuss moving more production of critical medical supplies out of “non-member” countries.

“We have to look into issues like supplies of medical equipment, protective suits, medicines…and also ask questions about whether we are too dependent on production coming from outside, whether we need to produce more of this equipment from our own countries,” he told reporters on Tuesday.

In the UK, the FT reported that more deaths were recorded in England and Wales during the week ending on April 3 than in any week since comparable estimates started 15 years ago, the Office for National Statistics said on Tuesday.

Global cases of the virus increased by 71,572 yesterday, the 4th day in a row that the number of newly infected around the world has fallen. Still, the pace of increases brought the total number north of 1.9 million.

Meanwhile, with the IMF and World Bank annual meetings slated to begin later this week, the IMF has said it would supply grants to some of the poorest nations in Africa and Asia.

Vladimir Putin now officially has reason to panic as Russia records 2,774 new coronavirus cases on Tuesday, a third consecutive record daily increase. Russia now has 21,102 cases of the virus, and 170 people have died from the disease. Russia’s outbreak has soared over the past 2 weeks, as numbers have doubled roughly every 4 days. China, meanwhile, reported 89 new cases, a slight drop.

Following warnings that first emerged late last week, Iran is set to kick off its privatization push to save its economy from the coronavirus: To accomplish this, Iran will sell off 10% of Shasta, the investment arm of the Social Security Organization of Iran – which is one of the state’s crown-jewel assets.

As cases in Europe continued to slow, Germany reported 2,082 new coronavirus cases on Tuesday, the lowest number in more than three weeks, and an increase of under 2%. Germany has confirmed 125,098 cases so far, according to official data from the Robert Koch Institute in Berlin. Spain also reported a less-than-2% (1.8%) jump in new cases, its slowest rate since the beginning of the outbreak, according to the Washington Post.

In the US, the US Department of Ag will reportedly unveil as much as $15.5 billion as part of the first phase of coronavirus aid to the farming industry on Tuesday. Meanwhile, late yesterday, Florida’s surgeon general reportedly said that social distancing should continue until a vaccine has been developed. The Trump administration, meanwhile, has requested a roughly 3-month delay on all US census field operations. The administration also asked Congress to postpone the deadline for delivering key data that will affect redistricting.

As millions of religious Americans continue to skip worship-related gatherings like Church, several pastors in California are suing the state and local officials over their stay-at-home edicts prohibiting in-person services, claiming these rules violate the 1st Amendment. And finally, more than 2,100 US cities are bracing for serious budget shortfalls.

Futures Jump As Chinese Trade Data Unexpectedly Outperforms; All Eyes On Bank Earnings

Global stocks jumped and US equity futures traded just around 2,800 on Tuesday after Chinese trade data came in better than expected and some countries tried to restart their economy by partly lifting restrictions aimed at containing the coronavirus outbreak.

Wall Street indexes ended mixed on Monday. The Dow and S&P 500 fell, but a 6.2% gain in Amazon shares helped the Nasdaq end higher.

“The pullback in US equities should come as no surprise in light of last week’s historic rally,” said Mark Haefele, chief investment officer at UBS Wealth Management, noting the S&P 500 posting its best weekly performance since 1974. “Sentiment will zigzag until there is more clarity on formal measures to reopen major economies. More broadly, even though global markets have rebounded, it is difficult to say with any certainty whether the bottom has been reached.”

European stock markets opened stronger, with the pan-European STOXX 600 index rising 0.6% to its highest since March 11, with Spanish shares gaining 1.5% as some businesses re-opened, although shops, bars and public spaces were set to stay closed until at least April 26. Market sentiment was boosted by data showing China’s exports fell only 6.6% in March from a year ago, less than the expected 14% plunge. Imports fell 0.9% compared with expectations for a 9.5% drop.

The gains in Europe took MSCI’s All-Country World Index .MIWD00000PUS, which tracks shares across 49 countries, up 0.5%.

The Stoxx Europe 600 Basic Resources index is among leading sector gainers after China disclosed numbers showing trade performed better than expected in March, with China exports declining 6.6% in dollar terms in March from a year earlier (exp.-13.9%) while imports fell 0.9% (exp. -9.8%), the customs administration said Tuesday, indicating that supply chains may be adapting better than thought. Specifically, this is the data that China reported:

Exports: -6.6% yoy in March vs Bloomberg consensus -13.9%. January-February: -17.2% yoy. Month-over-month export growth: +5.4% non-annualized in March vs. -7.8% in January-February.

Imports: -0.9% yoy in March vs consensus: -9.5%. January-February: -4.0% yoy. Month-over-month imports growth: +0.8% non-annualized in March vs. -2.6% in January-February.

Trade balance: US$+19.9bn NSA vs consensus US$+20.0bn in March. January-February: US$-7.1bn.

“Although further slowdown in the pandemic’s spreading may keep sentiment supported, we are still reluctant to trust a long-lasting recovery, and we prefer to take things day by day,” said Charalambos Pissouros, analyst at JFD Group.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares excluding Japan rose 1.3% to its highest in a month, up 20% from a four-year low on March 19. Chinese shares gained, with the blue-chip index up 1.2%. Australian shares were up 1.7% and Japan’s Nikkei rose 2.8%. Hong Kong’s Hang Seng was up 0.9%.

Earnings season kicks off this week with some of the world’s biggest banks reporting, giving investors their first glimpse of how bad the hit to global profits will be. Fidelity International analysts expect earnings to almost halve at companies globally this year. While Goldman Sachs Group forecasts advanced economies will shrink about 35% this quarter, investors are focusing on whether trillions of dollars in stimulus and rescue plans will fuel a rally in risk assets when the infections curve flattens.

In addition to the start of earnings season which begins with JPM reporting today, investors are also eyeing the easing of virus-related restrictions in some regions for further trading cues. In Europe, thousands of shops across Austria are set to re-open on Tuesday. Spain recorded its smallest proportional daily rise in the number of deaths and new infections since early March and let some businesses return to work on Monday.

In the United States, which has recorded the highest number of casualties from the virus in the world, President Donald Trump said on Monday his administration was close to completing a plan to re-open the U.S. economy. However, some state governors say the decision to restart businesses lies with them.In the latest developments, India and France extended their lockdowns and the British government is weighing similar steps.

In rates, 10Y yields dipped modestly to 0.75%, while Italian bonds fell after a report that the government is set to seek a significant deficit deviation. Bunds dropped as markets rose.

In commodities crude was up 0.85% at $22.55 a barrel, compared with a January peak of $63.27. Brent rose 1.3% to $32.16 a barrel. Oil prices rose around 1% after the U.S. Energy Information Administration (EIA) predicted shale output in the world’s biggest crude producer would fall by a record amount in April, adding to cuts from other major producers. Gold prices clung to highs not seen in more than seven years at $1,720.1 an ounce.

In currencies, the dollar extended losses on the back of the U.S. Federal Reserve’s massive new lending program. It weakened against the Japanese yen to 107.7. The euro was up 0.2% at $1.0929. The risk-sensitive Australian dollar jumped 0.6% to $0.6420.

Expected data include import and export prices. Fastenal, J&J, JPMorgan and Wells Fargo are among companies reporting results.

Market Snapshot

S&P 500 futures up 1.3% to 2,793.75

MXAP up 1.6% to 143.26

MXAPJ up 1.3% to 461.49

Nikkei up 3.1% to 19,638.81

Topix up 2% to 1,433.51

Hang Seng Index up 0.6% to 24,435.40

Shanghai Composite up 1.6% to 2,827.28

Sensex down 1.5% to 30,690.02

Australia S&P/ASX 200 up 1.9% to 5,488.11

Kospi up 1.7% to 1,857.08

STOXX Europe 600 up 0.9% to 334.66

German 10Y yield fell 0.3 bps to -0.35%

Euro up 0.04% to $1.0918

Italian 10Y yield fell 6.0 bps to 1.419%

Spanish 10Y yield rose 3.2 bps to 0.814%

Brent futures down 0.3% to $31.64/bbl

Gold spot up 0.3% to $1,720.80

U.S. Dollar Index down 0.1% to 99.21

Top Overnight News from Bloomberg

Bloomberg’s monthly survey puts contraction in the euro area at more than 10% in the January-June period, with most of the hit – – 8.3% — in the second quarter. Even with an expected rebound later in the year, the bloc’s output will still decline more than 5% in 2020

U.K. Foreign Secretary Dominic Raab told reporters it was likely to carry on and the government’s chief scientific adviser saying he expects the daily rate of deaths to continue to rise

The Federal Reserve will start buying commercial paper on Tuesday, just as Wall Street braces for an earnings season likely blighted by the coronavirus outbreak

Japanese Prime Minister Shinzo Abe said he wanted to start cash handouts for individuals and businesses hurt by the coronavirus pandemic as soon as May

China has started the process of potentially merging its two biggest brokerage firms to create a company that can better compete with the global investment banks as the country opens up its financial markets, according to people familiar with the matter

Asian equity markets were positive across the board as sentiment picked up from the holiday lull and as the region digested the mostly better than expected Chinese trade data, but with some of the gains capped heading into the start of US earnings season and as participants pondered how soon the US will reopen its economy. ASX 200 (+1.9%) was led by strength in gold miners after the precious metal surged above the USD 1700/oz level to its highest in more than 7 years, while Nikkei 225 (+3.1%) outperformance was fuelled by favourable currency moves with SoftBank shares also reversing the initial glut of sell orders that followed its preliminary results that showed the first loss in 15 years. Hang Seng (+0.6%) and Shanghai Comp. (+1.6%) conformed to the regional optimism after the latest trade figures showed a much narrower than expected contraction in Exports and a surprise expansion to CNY-denominated Imports, although there were mixed comments from the customs bureau which noted there are signs of recovery for China’s foreign trade which is resilient but also warned of increasing uncertainties and that trade is encountering larger difficulties which cannot be underestimated. On the coronavirus front, China recently approved 2 experimental coronavirus vaccines to enter clinical trials and Beijing was said to have resumed all of the city’s 2130 major construction projects. Finally, 10yr JGBs were subdued in tandem with the downside in T-notes amid gains in riskier assets, but with losses stemmed after somewhat improved demand at the enhanced liquidity auction for long to super-long JGBs.

Top Asian News

China’s Trade Fell Less Than Expected Even as Virus Spread

India’s Modi Says Nationwide Lockdown Extended Through May 3

Indonesia Surprises by Holding Key Rate, Cuts Reserve Ratio

Air Arabia Is Said to Seek State Aid and Delay New Venture

World’s Most Battered Corners in Bull Zone on Newfound Optimism

European equities remain mostly firm following a broad pickup in sentiment across APAC and US regions, with the former also aided by better-than-forecast Chinese trade data overnight. That being said, eyes turn to the resumption of earning season to gauge the initial impact of the virus outbreak on large-cap businesses. For reference, states-side earnings today include Johnson & Johnson (4.1% weighting in DJIA), JP Morgan (2.9% weighting in DJIA) and Wells Fargo. Back to Europe, UK’s FTSE 100 (-0.4%) lags regional peers as a firmer Sterling weighs on exporters, whilst reports also noted that the UK gov’t is poised to extend its lockdown to May 7th, although some reports over the weekend touted May 25th. Other European bourses see broad-based gains, with some possibly underpinned by comments from EU’s Competition Chief Vestager, who said member countries should purchase stakes in companies to repel the threat of Chinese takeovers. Broader sectors are somewhat mixed with underperformance in the Energy Sector, whilst Healthcare names lead the gains thus far. The sector breakdown does not give much by way of additional colour, although Travel & Leisure resume its downbeat performance as the sectors see no reprieve for the near future, whilst Carnival (-7.0%) sees pressure after the group is to extend its suspension on North American cruises. In terms of individual movers; AstraZeneca (+6.0%) props up the healthcare sector as shares were bolstered at the open after the Co. said its Tagrisso Adjuvant trial has been overwhelmingly positive. Separately, Co’s Koselugo has been approved in the US for paediatric patients with a rare genetic condition. Finally, the Co. has also initiated the Calavi clinical trials with Calquence against COVID-19. Renault (+3.0%) remains firm despite a cancellation to FY19 dividend after the Co. is to transfer its 50% stake in Dongfeng Renault to Dongfeng in a non-binding memorandum. Publicis (-0.3%) saw losses at the open after reporting that organic revenue dell 2.9% YY, although the Co. launched a EUR 500mln cost reduction plan. Accor (-2%) saw early-morning pressure after French Finance Minister Le Maire said he cannot say when hotels and restaurants will reopen. Note: Eurex and Deutsche Boerse have been experiencing technical problems that are being investigated.

Top European News

Austria Tests Easing Lockdown With Some Stores Reopening Tuesday

GAM Accelerates Cuts as Assets Plunge by $13 Billion in Quarter

Norwegian Air Plunges 63% on Plan to Convert Debt to Equity

Crisis in Russia Puts $13 Billion of Remittances at Risk

Crisis Gives Germany Sense of Vindication for ‘Black Zero’

In FX, the Dollar remains depressed after last Thursday’s mega Fed stimulus package and ramp up in Gold through the Usd1700/oz threshold to fresh 7 year peaks, with the DXY unable to regain a foothold above 99.500 within a 99.432-121 range amidst selective risk-on flows in wake of latest COVID-19 updates, the eventual OPEC+ crude output accord and Eurozone Finance Ministers finally agreeing on a substantial fiscal stimulus package. Ahead, US import export prices are scheduled, but unlikely to prompt much, if any reaction, but Wednesday’s data releases are top tier.

GBP – The Pound is off best levels, but still the best performing G10 currency after UK PM Johnson’s discharge from hospital. Cable remains comfortably above the 1.2500 handle and briefly crossed the 50 DMA at 1.2568 to print a fresh 1.2575 recovery high before reports from the ONS emerged raising the number of fatalities in England and Wales by 15% vs NHS figures published to April 3rd, while Eur/Gbp is back above 0.8700 from circa 0.8784 at one stage awaiting revised GDP and deficit estimates from the OBR under various coronavirus scenarios due at 12.00BST.

ZAR – In contrast to Sterling, Rand gains against the Buck were initially reversed from 18.0000+ to just shy of 18.2000 in wake of an unexpected 100 bp SARB rate cut that was announced via social media and came after May’s scheduled policy meeting was brought forward. However, Usd/Zar subsequently soared beyond 18.3300 as Central Bank Governor Kganyago

JPY/EUR/CHF/AUD/NZD – All firmer vs the Greenback, as the Yen defies improved risk sentiment to hold at the upper end of 107.79-39 parameters, but not quite close enough to disturb decent option expiry interest protecting 107.00 at 107.05 (1.1 bn). Note, no real rection to latest BoJ source talk about increased and wider QE remits at this month’s meeting that might include expanding the range of assets accepted for collateral. Similarly, the Euro is hovering closer to the top of 1.0957-06 confines and the Franc nearer 0.9637 than 0.9679 even though latest weekly Swiss sight deposits indicate significantly more intervention by domestic banks on behalf of the SNB. Elsewhere, some loss of overnight momentum forged on the back of Chinese trade revealing a surprise rise in Yuan denominated imports for the Aussie and Kiwi, but both retaining sight of big figure/psychological resistance marks at 0.6400 and 0.6100 respectively.

CAD/NOK/SEK – In keeping with the rather muted response following knee-jerk relief in oil on the aforementioned OPEC+ pact, the Loonie is paring advances from around 1.3863 to sub-1.3900 as attention switches towards tomorrow’s BoC meeting and the prospect of downbeat/dovish guidance, assuming no further action. Meanwhile, the Norwegian Krona has also retreated from almost 11.1700 vs the Euro to 11.2800, but its Swedish peer showing a bit more resilience above 10.9000 due to signs of the case and death count from nCoV flattening.

EM – The Lira is struggling to contain losses below 5.7900 amidst heightened coronavirus contagion and the Turkish banking regulator slashing FX swap and derivative limits, while the already unstable political backdrop has been rocked by the resignation of the country’s Interior Minister.

In commodities, WTI and Brent front-month futures reverse course after initially eking mild gains following the fallout of the OPEC+ and G20 ad-hoc meetings which failed to spur a rally but more-so stemmed declines in the complex (in the short-term at least). As a recap for European players, OPEC+ agreed to cut joint output by 9.7mln BPD, starting on 1 May 2020, for an initial period of two months that concludes on 30 June 2020. For the subsequent period of 6 months, from 1 July 2020 to 31 December 2020, the total adjustment agreed will be 7.7mln BPD. It will be followed by a 5.8mln BPD cut from 1 January 2021 to 30 April 2022. The baseline for the calculation of the adjustments is the oil production of October 2018, except for the Kingdom of Saudi Arabia and Russia, both with the same baseline level of 11.0mln BPD. The agreement will be valid until 30 April 2022; however, the extension of this agreement will be reviewed during December 2021. Saudi, UAE and Kuwait all pledged voluntary over-compliance, whilst G20 is to curtail output by some 3.7mln BPD. Yesterday, Saudi Aramco cut their OSPs for several grades for the second month in a row despite the output cut deal; albeit, OSPs for all grades to the US were raised. The Arab Light discount to Asia reflects the supply glut. Furthermore, Russian Energy Minister Novak said he met with domestic oil producers and they supported the OPEC+ deal, while he added that total oil output cuts in May-June will total between 15-20mln BPD. WTI straddled around USD 22.50/bbl in early trade before briefly dipping below USD 22/bbl, whilst Brent meanders just below USD 31.50/bbl, having confirmed to the modest sell-off during the session The difference between the contracts meanwhile remains wider to the tune of around USD 9.50/bbl vs. a pre-OPEC sub-5/bbl number. Elsewhere, spot gold holds onto a bulk of yesterday’s gains and remains north of USD 1700/oz and near recently-set 7yr highs given USD weakness and as investors stock up on the yellow metal following the liquidity-induced declines last month. Copper meanwhile has given up the gains seen during the APAC session after Freeport-McMoRan said it will temporarily shut its Chino copper mine (produced 88k tons of copper in 2019) due to the virus outbreak, albeit the red metal remains caged in a narrow 2.3250-2.3480 band.

US Event Calendar

8:30am: Import Price Index MoM, est. -3.2%, prior -0.5%; Import Price Index YoY, est. -5.0%, prior -1.2%

8:30am: Export Price Index MoM, est. -1.9%, prior -1.1%; Export Price Index YoY, prior -1.3%

DB’s Jim Reid concludes the overnight wrap

I hope you all had a relaxing if probably a little strange Easter. Today is actually 10 years to the day that the second more dramatic eruption of Icelandic volcano Eyjafjallajökull occurred. The following day all European air travel was shut down for a week. Imagine if you’d had a big trip planned for your 40th or 50th birthday that week, saw it cancelled and vowed that in 10 years’ time you’d celebrate your next major landmark with an even bigger trip to make up for it. I feel for you this week it’s that’s you!! I certainly won’t be arranging a big trip for mid-April 2030!

So strange times indeed and we come back from Easter still reflecting on two big events that occurred late on Thursday. Although this crisis is unique in its making and is clearly not the fault of anyone in financial markets, it is clearly exposing two of the biggest fault lines in the financial system over the last two decades. Firstly, Thursday saw the latest instalment of a 20- to 25-year super cycle where the authorities have been so reluctant to see the creative destruction that’s so important to successful capitalism that they had to make another stunning major intervention, and secondly, we saw the latest evidence that a European monetary union without fiscal union was always going to involve sporadic but hugely existential risks to the EU and help to create ever more fraught politics.

On the first one, ever since the Fed of the late 1990s decided to bail out the financial system post the LTCM collapse, we’ve had rolling state sponsored capitalism and large moral hazard. This has meant that each subsequent default cycle (or mini market cycle) has been less severe than the free market parallel universe version would have been and has left increasingly more debt in the system as a result and meant that the intervention necessary to protect the system has got greater and greater. In my opinion, it also helps lock in lower productivity as you keep more low/no growth entities alive.

On Thursday, the Fed announced the details of their $2.3 trillion to support the US economy. The main additional features within credit was the buying of any eligible corporates that were IG rated before March 22nd and also HY ETFs. For fallen angels this is huge moral hazard as a lot of BBB-rated companies have seen their ratings downgraded in recent years due to: 1) central bank inspired ultra-low interest rates encouraging them to lever up, and 2) a related desire to return value to shareholders, especially through share buybacks. In terms of buying HY ETFs while this is planned to be small in terms of size, it is the first time a major central bank has purchased HY corps and therefore opens the door for more aggressive interventions in lower rated credits going forward. As an example of the impact, Ford which became the 2nd largest fallen angel in history in late March, saw its 5.875% August 2021 bond yields fall from 8.8% to 4.9% on Thursday on a YTM basis after the announcement (closed 5.6% yesterday). US HY and IG tightened -85bps and -22bps on Thursday and then a further -26bps and -15bps, respectively, yesterday. For those looking for more details on the Fed announcement, Craig has published a couple of reports with the first (link here) providing details on the facilities and the second (link here ) details on the eligible universe.

While I would stress that in the face of a global pandemic, there has to be some sympathies with these policies, had markets not been repeatedly bailed out over the last 20-25 years the authorities wouldn’t have needed to be as aggressive. It also makes me wonder what could ever allow us to see free market creative destruction again in my lifetime. When we see the subsequent recession after this one you’ll again start from even higher debt and the same issues will come up albeit with a much less severe economic scenario than the covid-19 one.

I can hear the refrain from investors in say 2025 when credit looks too tight for the late cycle risks. They’ll say that it’s impossible not to be long as the Fed has their back and they’ll miss out if they are not fully invested. Understandable but a very bad way of ensuring capital is allocated in the most growth enhancing manner. I’ll be coming back to talk much more about this in the weeks ahead so I’ll leave it there for now.

Sticking with the Fed, yesterday the NY Fed announced that from May 4 onwards it will conduct one rather than two overnight repo operations each day, a step that will halve the amount available to $500bn. It also plans to halve the frequency of its three-month repo operations, which also have a maximum size of $500bn apiece, to once every two weeks, although it will continue to do one-month actions every week. The accompanying statement read that the decision was taken “in light of more stable repo market conditions.”

As for Europe in terms of what has been agreed, best to read Mark Wall’s blog here from Thursday night. As he discusses, there is much ambiguity in the plan. Perhaps most ambiguity exists around whether the ESM is accessed by a number of countries and thus removing the stigma for Italy where it’s a politically sensitive issue to access it and accept conditionality. In these circumstances if it unlocks the ECB to buy short-term government debt via the OMT program it could take some pressure off the capital keys question within the PEPP. However, at this point we don’t know whether this form of the ESM unlocks OMT, which is part of the ambiguity. In speaking to Mark last night it seems Italy don’t plan to use the ESM and will focus attention on the leaders’ meeting on 23 April and making sure that the recovery fund is as good as it can be.

The summit closed the door on Eurobonds and my thoughts on this is that if they are not going to be seriously considered in such a catastrophe then it’s pretty hard to imagine the scenario we get them in the future or see meaningful steps towards fiscal union. To be fair this was never going to happen in this response after all the northern countries’ negativity towards it but it’s now inevitable that non-core country debt is going to go up at an even faster pace due to Covid-19 (and it’s after effects) than it is in core countries. The politics of this will resonate and it will be worth watching in Italy especially. Regardless of the short-term impact, the fault-lines in the European construct are being exposed again by this crisis. This will have ramifications further down the line.

Turning to markets now. Yesterday in the US, the S&P 500 retreated -1.01% ahead of earnings season and following its 8th best week on record, but did close off intra-day lows of c.-2.5%. Technology and Consumer Discretionary (led by stay-at home-stocks Amazon and Netflix) outperformed on the day, with the NASDAQ up +0.48%. Possibly showing some nerves ahead of earnings, Bank stocks, which are early reporters, were the second worst performing sector in the S&P 500, down -4.13%. As risk fell, fixed income was relatively quiet until a small sell-off at the end of the day. US 10yr Treasury yields rose 5.2bps to 0.77% and longer dated 30yr yields climbed 6.4bps to 1.41%. Elsewhere, Gold reached its highest closing level since November 2012, gaining 1.10% on the day to finish at $1715/oz.

After nearly a week of negotiations between OPEC+ and G20 oil ministers, we got a late Sunday resolution from the oil producing nations to end the price war and cut production by 9.7million barrels a day based on headline numbers. This compared with reports out last week suggesting a 10 million barrels. However, as our colleague Michael Hsueh noted yesterday, given a creative baseline level, the actual cut from March levels will be roughly -8.4million barrels a day at most and there are reasons to expect not all of the cut will happen immediately in May. The expected demand decline continues to dwarf the reduction in supply at least in April and perhaps in all of Q2. Michael sees pressure on oil prices remaining to the downside in the near term. See the link to his full note here. Brent futures had gapped over 6 % higher in early trading, before quickly falling and then retracing the entirety of that move to close just +0.83% higher.

Moving onto the virus, full details will be in our sister daily the Corona Crisis Daily. In brief global cases have risen to nearly 2 million over the holiday weekend from 1,518,719 on Thursday. The weekend saw a massive amount of slowing of new cases growth in the US and Europe though. However, will the recent pattern of lower Weekend/Monday rates of increases in cases/mortality for the US, UK, Germany and France be even worse over Easter? We won’t know until the reporting catches up later in the week.

A quick refresh of our screens shows that most major markets in Asia are up this morning. The Nikkei (+2.19%), Hang Seng (+0.62%), Shanghai Comp (+0.68%) and Kospi (+1.68%) in particular have posted gains. In FX, the US dollar index is trading down -0.17% while the Norwegian krone is up +0.95% leading the advance amongst G-10 currencies. Elsewhere, futures on the S&P 500 are up +1.20% this morning ahead of the start of earnings season. In commodities, Brent crude oil prices are up +1.54% while most base metals are also trading up with iron ore up +1.08%. Gold is also trading up +0.18% this morning.

Contributing to the stronger tone this morning was China’s March export data, which showed exports declining -3.5% yoy (vs. -12.8% yoy expected) and imports rising +2.4% yoy (vs. -7.0% yoy expected) in local currency terms. In USD terms, exports were down -6.6% yoy (vs. -13.9% expected) while imports were down -0.9% yoy (vs. -13.9% yoy expected). Our Asia strategists make argument that the better-than-expected numbers could be due to the fact that as labor mobility increased in China in March as lockdowns got lifted it helped the country to clear the backlog of export orders. A word of caution though that the improvement in exports could be temporary as the majority of the world went on lockdown in April and Chinese authorities are continuing to highlight that the export headwind China is facing remains strong. Another detail worth attention from the release is that the China’s imports of pork and soybeans from the US rose 6.6 times and 2.1 times, respectively, in Q1 2020. Overall, China’s agriculture imports from the US rose 110% in 1Q. This could be a sign that China is trying hard to stick to its commitment under Phase 1 of the trade deal with the US.

As for the rest of this week the main highlights are the start of US Q1 earnings today and China Q1 GDP on Friday. In addition every week initial jobless claims are now going to be a big event. With regards to earnings, 33 companies in the S&P 500 report including many financials. A number of firms have already withdrawn their guidance as a result of the coronavirus, but it’ll be interesting to see the first impact of the shutdowns in March and what companies say about any visibility they have. In terms of the highlights, today we’ll hear from Johnson & Johnson, JPMorgan Chase and Wells Fargo. Then tomorrow reports come from UnitedHealth Group, Bank of America, ASML, Citigroup and Goldman Sachs. Thursday sees Abbott Laboratories, BlackRock and BNY Mellon report, before Friday sees releases from Danaher, Honeywell and Morgan Stanley. Bank earnings will be fascinating as the surge in volatility will help trading revenues but the loan losses won’t have come through yet. Will they make big provisions or will they see all the schemes in place to stop companies going bust and be relatively sanguine about this.

For China’s Q1 GDP figures on Friday, the consensus expectation on Bloomberg is for a year-on-year decline of -6.0% in Q1, down from a 6.0% year-on-year expansion in the last quarter of 2019. This would represent an astonishing deterioration without precedent in the quarterly data we have going back to 1992.

Other data to look for in the US are the start of some March hard data, which will capture the initial part of the slump. These include retail sales, industrial production and capacity utilisation tomorrow, followed by building permits and housing starts on Thursday.

In addition to data one thing that’s always closely watched is the release of the IMF’s semi-annual World Economic Outlook, which is coming out today. To be fair it will probably just catch up with the consensus huge declines expected from all economists but it will no doubt capture some headlines.

Before the day-by-day rest of the week ahead calendar let’s briefly review last week. It was a week that saw some equity markets enter technical bull market territory after virus curves flattened and the Fed deployed further aggressive interventions in the US. The S&P 500 rose +12.10% on the week (+1.45% Thursday), the best week since October 1974 and the 8th best week out of 4,184 weeks on record since January 1928. The index also entered a bull market, rising +24.69% from the index’s closing lows on March 23rd. European equities rose slightly less than the US, with the Stoxx 600 up +7.36% over the 4 day week (+2.24% Thursday), and is now up +18.64% off the March lows. The DAX rose +10.91% (+2.92% Thursday) to rise +25.15% from lows to finish the week in bull market territory itself. Asian equities also rallied last week, though on a full 5 days basis. The Nikkei rose +9.42% (+0.79% Friday), while the CSI was up a more moderate +1.51% (-0.62% Friday) and the Kospi gained +7.84% (+1.33% Friday) on the week. As risk sentiment improved and global equities rose, the VIX fell -5.1pts over the course of the week to finish at 41.7, the lowest closing level in over a month. Further highlighting the effects of the Fed’s actions late in the week and the improvement in risk sentiment, credit spreads tightened significantly over the week. US HY cash spreads were -147bps tighter on the week (-85bps Thursday), while IG tightened -47bps on the week (-22bps Thursday). In Europe, HY cash spreads were -89bps tighter over the 4 days (-37bps tighter Thursday), while IG was -29bps tighter on the week (-14bps Thursday).

Ahead of the OPEC+ and the separate, but interwoven G20 oil minister meetings this past weekend, crude failed to maintain the extreme rally of the prior week. Brent fell -7.71% (-4.14% Thursday) while WTI fell -19.69% (-9.29% Thursday) as sentiment toward a broad based deal started to sour. Elsewhere in commodities, even as risk rallied, gold rose +4.68% over the week (+0.77% Friday) on the back of further monetary stimulus and a -1.64% weekly drop in the Bloomberg dollar index.

With equity prices improving globally, sovereign bond yields rose on the week in both Europe and the US even as the stimulus measures on Thursday saw bonds rally with risk assets. US 10yr Treasury yields rose +12.4bps (-5.3bps Thursday) to finish at 0.72%, while 10yr Bund yields increased +9.4bps (-4.1bps Thursday) to -0.35%. Even prior to the deal being reached by the European commission peripherals spreads started tightening. Italian yields tightened -5.4bps over the 4 days (-2.0bps Thursday), and Spanish 10yr bonds tightened -5.3bps (-1.8bps Thursday).

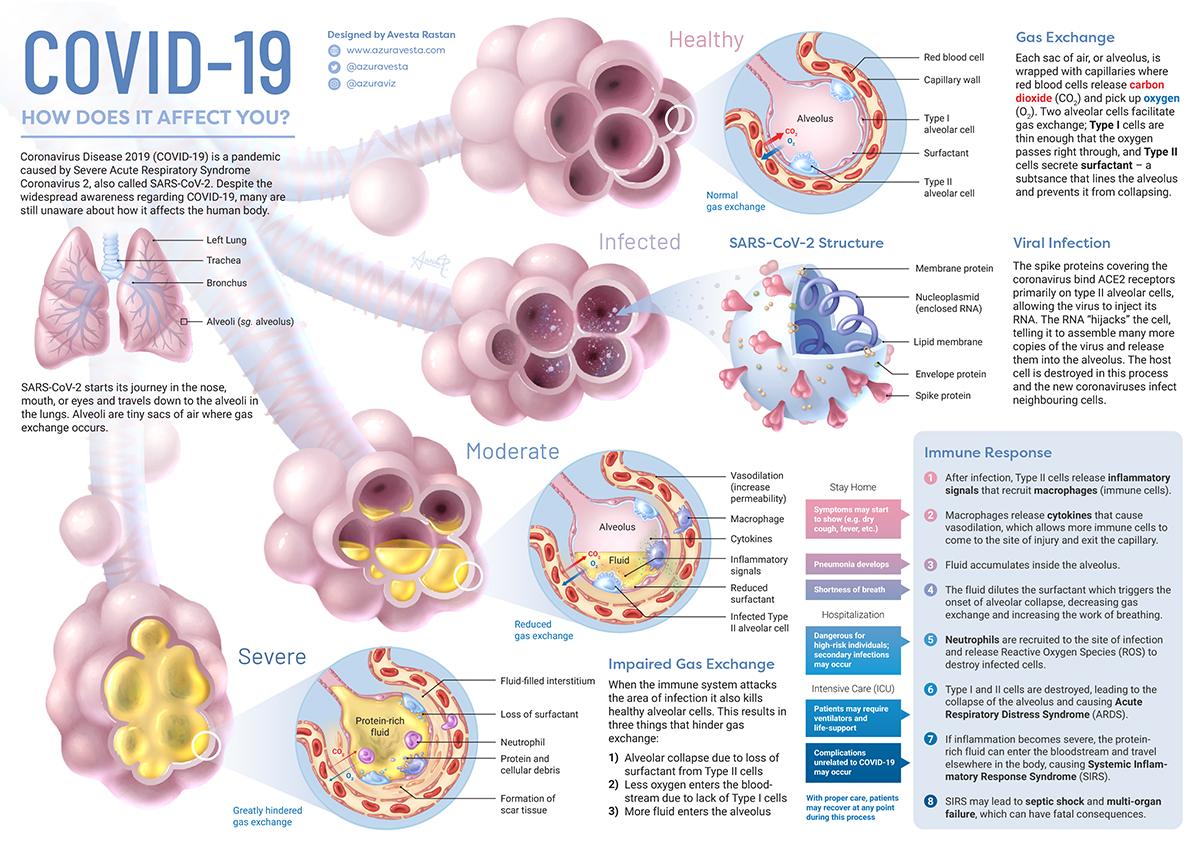

By now, researchers and health experts have gained a better understanding of the range of symptoms caused by COVID-19, which include fever, a dry cough, and of course, the dangerous inflammation of the respiratory system. Most of us know that COVID-19 can be much more severe than a typical flu, but, as Visual Capitalist’s Nick Routley explains below, lesser known are the mechanics behind how the virus causes pneumonia in its victims.

Today’s informative illustration, by scientific designer and animator Avesta Rastan, details the effects COVID-19 has on our lungs, from moderate to severe cases.

According to the World Health Organization (WHO), most people who contract COVID-19 only experience mild flu-like symptoms. Occasionally though, the infection can cascade into a severe case of pneumonia that can be lethal, especially for older people and those with underlying medical conditions.

Here’s what COVID-19 does to your body.

Infection

The virus, officially named SARS-CoV-2, enters the body – generally through the mouth or nose. From there, the virus makes its way down into the air sacs inside your lungs, known as alveoli.

Once in the alveoli, the virus uses its distinctive spike proteins to “hijack” cells. The primary genetic programming of any virus is to make copies of itself, and COVID-19 is no exception. Once the virus’ RNA has entered a cell, new copies are made and the cell is killed in the process, releasing new viruses to infect neighboring cells in the alveolus.

This process can occur initially without a person being aware of the infection, which is one of the reasons COVID-19 has been able to spread so effectively.

Immune Response

The process of hijacking cells to reproduce causes inflammation in the lungs, which triggers an immune response. As this process unfolds, fluid begins to accumulate in the alveoli, causing a dry cough and making breathing difficult.

For 80-85% of people infected by COVID-19, these symptoms will run their course much as they would with a case of the flu.

Severe Symptoms

In 15-20% cases, the immune system’s response to inflammation in the lungs can cause what’s known as a “cytokine storm”. This runaway response can cause more damage to the body’s own cells than to the virus it’s trying to defeat, and is thought to be the main reason for why the conditions of young, otherwise healthy individuals can rapidly deteriorate.

If enough alveoli collapse, acute respiratory distress syndrome (ARDS) can occur, requiring a patient to be placed on a ventilator for breathing assistance.

At this stage, the surfactant that helps keep alveoli from collapsing has been diluted, and fluid containing cellular debris is impairing the gas exchange process that supplies oxygen to our bloodstream.

In the most severe cases, systemic inflammatory response syndrome (SIRS) occurs as the protein-rich fluid from the lungs enters the bloodstream, resulting in septic shock and multi-organ failure. This is often the cause of death for people who have succumbed to a COVID-19 infection.

The Best Protection

Thankfully, COVID-19 isn’t a death sentence for most people who become infected, but the symptoms described above are not pleasant. Until a vaccine is developed, the best defense is avoiding infection altogether through frequent, thorough hand washing, and physical distancing as recommended by health authorities.

To see the full set of graphics, as well as other health and science related illustrations, visit Avesta Rastan’s website.