Klobuchar’s prosecutorial past comes back to bite her (finally). But first: It’s Biden vs. Bernie again ahead of tomorrow’s Super Tuesday primaries. Former Vice President Biden took nearly half (48 percent) of the Democratic presidential primary votes in South Carolina, with Sen. Bernie Sanders (I–Vt.) earning 20 percent and former South Bend Mayor Pete Buttigieg getting just 8 percent.

Sen. Elizabeth Warren (D–Mass.) placed fifth in South Carolina, with just 7 percent of the vote, trailed by Sen. Amy Klobuchar (D–Minn.) with 3 percent and Rep. Tulsi Gabbard (D–Hawaii) with 1 percent. Former New York Mayor Michael Bloomberg wasn’t on the ballot.

Both Bloomberg and Klobuchar faced protests over the weekend, forcing Klobuchar to cancel her Sunday night campaign rally at a high school in Minnesota’s St. Louis Park.

Black Lives Matter protesters were there to call out Klobuchar for the incarceration of Myon Burrell, who as a 16-year-old was convicted of murder and sentenced to life in prison. Burrell maintains his innocence, and evidence suggests he may have been wrongfully convicted in the death of 11-year-old Tyesha Edwards, who was killed by a stray bullet in 2002.

“Sen. Klobuchar was the county attorney during Burrell’s first trial,” notes WCCO. And while campaigning for president, Klobuchar has repeatedly cited the story of how she helped put Burrell away.

The Klobuchar campaign released a statement saying that “the campaign offered a meeting with the Senator” if the protesters would leave. “After the group initially agreed, they backed out of the agreement and we are cancelling the event.”

In Alabama, protesters took a much different tack, silently standing and turning their backs toward Bloomberg as he spoke at a Selma church.

Some in the church in Selma, where Bloomberg is speaking are standing up with their backs toward him. pic.twitter.com/LUuvJeL2NZ

Bloomberg was invited to speak during Selma’s Jubilee, an annual event marking “Bloody Sunday” when hundreds of protesters were beaten and battered while marching across the Edmund Pettus Bridge in 1965.

Ryan Haygood, who turned his back on Bloomberg, told the paper:

I was sitting there really wrestling with the fact that 55 years ago 600 or more people assembled at this church and they prayed and prepared to be brutalized by Alabama state troopers about a half a mile up the bridge. Then comes Michael Bloomberg who when he was the mayor of New York City presided over those very kinds of police brutality practices and policies. So in my mind, I thought, though I was surprised to see him come through the doors, I thought he would use this space to atone for that….

And not only did he not do that, it was clear to me that he wasn’t even going to address the issue at all. And so I wrestled with it. So I felt like I had to do something to acknowledge that that’s not OK especially in this sacred space. This is a space that changed the world.

According to the Advertiser, around a dozen people “stood for about 30 seconds before Bloomberg realized what was happening. He paused, then stumbled over his words before picking back up with his speech”

Voters in 14 states and American Samoa will go to the polls tomorrow, with 1,357 delegates up for grabs. (To win the nomination, you need 1,991 delegates.) The states holding primaries will be Alabama, Arkansas, California, Colorado, Maine, Massachusetts, Minnesota, North Carolina, Oklahoma, Tennessee, Texas, Utah, Vermont, and Virginia.

QUICK HITS

The Trump administration is expanding a coronavirus-related travel ban “to include any foreign national who has visited Iran within the last 14 days,” Vice President Mike Pence said on Sunday. “The US is also increasing the travel advisory for Italy and South Korea to Level 4—the highest level—advising Americans not to travel to specific regions in those countries hit hardest by the virus,” reports CNN.

Two people in Washington state have died from the coronavirus. Ten cases have been confirmed there, all around the Seattle area in King County.

Yes, “2016 was the worst election ever,” writes Jonathan V. Last at The Bulwark. But what if “every subsequent election is worse?”

from Latest – Reason.com https://ift.tt/39fGeJr

via IFTTT

The markets’ reaction to the latest economic news is indeed odd. But entirely predictable. The Chinese PMIs were horrendous. How could that possibly have come as a shock? And on what basis should anyone have been relying on economist forecasts to decide whether it was a miss or a beat? Anyone surprised that China’s economy has taken a serious hit, is being delusional. Probably the same ones who where assuring us of the impending V-shaped recovery.

Perhaps less surprising was the immediate reaction to the 4 1/2-liner from Fed Chair Jerome Powell letting us know that he is “monitoring developments.” Isn’t that what he is meant to be doing? And is it a surprise that their reaction function is as predictable as it has always been? Blame it on risks or headwinds while keeping a vigilant eye on the level of the S&P 500. But, I guess that’s what it takes.

There is absolutely nothing wrong with cutting rates when appropriate. Nor are insurance cuts inappropriate.

But we were treated last week to a long litany of assurances:

that “the fundamentals of the U.S. economy remain strong” (Powell),

“I wouldn’t want to to prejudge the March meeting” (Bullard),

“there is some risk, but basically I think the U.S. outlook looks pretty good” (Yellen),

“I think it pays to be patient” (Kaplan).

At least Italy’s leaders weren’t assuring everyone that they feltsanguine before announcing yesterday emergency measures to combat the economic ill-effects they are experiencing. And to their credit, they are proposing to implement fiscal measures that are actually meant to reach businesses directly rather than relying on the old trickle-down method.

We’ve now moved to not merely assuming a March cut is baked in the cake — and maybe one bigger than 25 basis points– to debating if they can afford to wait that long and whether they should pull the trigger on an emergency basis.

And do so in tandem with the rest of the world’s central banks. We won’t be shocked and we won’t be awed. Cooperation is a good thing. Would that the powers-that-be could do it under more circumstances.

The Bank of Canada has its March meeting on Wednesday. Futures pricing has them going. Before Powell’s statement economists were undecided. Watch whether that changes rapidly. I suspect we move from talk of a tight housing market and financial stability considerations straight to discussions about not wanting to disappoint market expectations.

As far as U.S. numbers are concerned, it seems likely that any weakness will be taken as evidence that the economy is slowing and any strength as dated information. In reality, that isn’t necessarily true, but if rate cuts are on offer, that will have to be the interpretation. Especially, if ISM disappoints and no one wants to wait around for an expected robust non-farm payrolls to throw a spanner in the lower-rates works.

There is the usual long list of Fed speakers on the schedule this week. The extent to which they change their messaging will be well worth listening for. What a difference a week makes. This morning the OECD lowered its global growth forecast to what would be the lowest since 2009. The BOJ and BOE have waded in with pledges of support. A lot of people are relearning that globalization isn’t such a bad idea.

Jack Welch, a railroad conductor’s son who became chairman and CEO of General Electric and led it for two decades, growing its market value from $12 billion to $410 billion, has died. He was 84.

As CNBC reports,John Francis Welch Jr. was born Nov. 19, 1935, in Peabody, Massachusetts, to Irish American parents. His father was a conductor for the Boston & Maine Railroad and his mother was a homemaker. The younger Welch studied chemical engineering at the University of Massachusetts Amherst and received his Ph.D. from the University of Illinois in 1960.

Welch joined GE in 1960 as a chemical engineer in its plastics division in Pittsfield, Massachusetts. He became a vice president in 1972 and vice chairman seven years later. In April 1981, at age 45, he succeeded Reginald H. Jones as chairman and chief executive officer.

Welch insisted that all of GE’s divisions be market leaders. ″Fix it, close it or sell it,” he was fond of saying.

Fortune magazine dubbed him “manager of the century” in 1999.

“Though he acted with what seemed at the time like blitzkrieg aggressiveness, he regretted in later years that he hadn’t moved even faster,” Fortune editorial director Geoffrey Colvin wrote in explaining the title.

“Having been handed one of the treasures of American enterprise, he said, he was ‘afraid of breaking it.’ Not only did Welch not break it, but he transformed it as well and multiplied its value beyond anyone’s expectations.”

Welch retired from GE in September 2001, days before the 9/11 attacks. Upon his retirement, The New York Times published an editorial that gushed over his professional record.

“Mr. Welch was a white-collar revolutionary, bent throughout his career at G.E. on championing radical change and smashing the complacency of the established order,” the editorial said. “His legacy is not only a changed G.E., but a changed American corporate ethos, one that prizes nimbleness, speed and regeneration over older ideals like stability, loyalty and permanence.”

Survivors include his third wife, the former Suzy Wetlaufer, whom he married in 2004. He filed for divorce from his second wife, Jane, after reports surfaced that he was having an extramarital affair with journalist Wetlaufer. Four days before the divorce trial was to begin, Jack and Jane Beasley Welch reached a settlement that reports said was worth $180 million. He divorced his first wife, Carolyn, the mother of his four children, in 1987.

It was only a matter of time before smartphone and other electronic shortages from top brands, including Apple and Xiaomi, were seen in India amid supply chain disruptions in China. Many of these companies have production facilities in China, with factory output at half to idle speed because of the Covid-19 outbreak.

The Economic Times (ET) says supplies of made in China smartphones and electronics are dwindling at Indian shops. Suppliers told ET that in the last 7-10 days, only 10-20% of the average shipment had been sent to stores.

Supply disruptions have mainly hit iPhone X models, due mostly because iPhone XR and 7 are locally manufactured. Suppliers noted that TCL and Xiaomi smartphones and televisions from China are in short supply. Shenzhen-based Realme was another brand that was facing shipment delays to India.

ET said shortages of high-tech goods had forced many retailers to stop offering discounts in the last several weeks. There’s also reports that some prices of smartphones and TVs rose 10% last month due to manufacturers resourcing components, which has driven up overall costs.

“There are supply issues for several brands. There is no clarity when the situation will normalise,” said Nilesh Gupta, director at Vijay Sales, a top electronics retailer in Mumbai and New Delhi. “If it doesn’t get corrected fast, we may move into a stock-out situation from next month.”

A Xiaomi India spokesperson told ET that supply chain disruptions in China are expected in early March. “We are working towards balancing the demand in India, which should be met soon,” the spokesperson said.

Indian retailers have been building inventories of smartphones, television, air conditions, washing machines, and refrigerators since supply constraints developed in China last month.

A senior executive of an Apple exclusive store chain warned that supplies would normalize by April because much of the production is being routed to the US and Europe. “Business is down by 50% last week and March is looking bleak,” he said

The virus has gone global, now affecting South Korea and Japan, two top manufacturing hubs of electronic companies that have had some multinationals idle or close some plants because of the virus outbreak.

What’s coming down the pipe for the US is much of the same supply constraints seen in India at the moment. Major retailers, such as Target and Walmart, could experience shortages of products starting later this month or in April. Amazon has already warned several products could be “unavailable” in the weeks or months ahead.

Force cannot restore legitimacy, trust or confidence, nor can it magically erase the consequences of a still-unfolding national trauma.

The Chinese authorities threatening to punish workers who refuse to return to work are getting a lesson in the limits of force in an unprecedented national trauma: a bayonet in the back will not restore the legitimacy and confidence that have been lost.

There are two enormous blind spots in conventional media coverage of the pandemic:

1. The limits of force in restoring China’s economy to pre-pandemic levels.

2. The longer term (i.e. second-order) consequences of the immense trauma experienced by the Chinese people.

While the media focuses on questionable statistics and economic claims–factories are already back to 60% capacity, etc.– little attention has been paid to the tremendous losses. For me, a photo of a young woman weeping inconsolably as the body of her mother was unceremoniously hauled away to the crematorium crystallized the cost, the losses and the national trauma.

For this was not the first tragedy of the pandemic to befall this young person; her father had also died 20 days earlier of the coronavirus. This young person lost both parents in the space of a month to the pandemic.

Everyone knows the Chinese government uses statistics to fashion positive political optics of the Chinese Communist Party (CCP).

But for secrets and lies in service of political optics to have unleashed the virus on the entire nation–that is beyond the usual official rigging of statistics to serve Party optics. It is a complete betrayal of the Chinese people, and betrayal has long-lasting consequences.

Once trust, faith in institutions and confidence are lost, they cannot be recovered without much time and many small good faith steps; even one further betrayal will destroy whatever has been slowly regained.

Beneath the surface, confidence has been eroding for years. Despite the “permanently positive news” of bogus GDP statistics, China’s economy has been stagnating for the past few years, and the trade war was not the primary cause: unnoticed by a myopic Western financial media, China’s economy has shifted from a dependence on increasing production and direct foreign investment (FDI) to a largely hidden dependence on speculation.

Companies don’t have earnings from production, they have gains from speculating in debt and the stocks of other companies. Households aren’t getting wealthier because they’re producing more but because their real estate holding are rising in what’s been presented as a permanently expanding housing bubble.

This is one of the hidden costs of sacrificing reality to serve political optics: the average person has sensed the stagnation, but they’ve had little appreciation of the increasing fragility that left China’s pre-pandemic economy exquisitely vulnerable to an external shock.

The collapse of confidence has weakened the power of authorities’ threats. Trauma dulls the normal fear of punishment, as the pandemic’s punishments have stripped the traumatized of fear.

The limits of over-stretched authorities’ powers are also becoming visible. If 40% of a factory’s workforce doesn’t show up when ordered to do so, are there sufficient police to search for workers who returned to their home villages 1,000 kilometers away and put a bayonet in the back of each one? And then what? Will police officers be assigned to watch the workers 24/7 so they can’t escape? The practical limits on force are increasingly apparent.

And what about the borrowing and spending China’s economy has become dependent on for growth? Will bayonets be shoved in the backs of potential borrowers to make sure they sign loan documents? Will bayonets be shoved in the backs of potential buyers of empty flats in empty buildings in ghost cities?

Will a bayonet in the back of a flat-broke small business owner pay his overdue rent?

Force cannot restore legitimacy, trust or confidence, nor can it magically erase the consequences of a still-unfolding national trauma. The limits of force apply not just to China but to every national elite that reckons it can force the genie back in the bottle and magically restore legitimacy, trust and confidence to pre-pandemic levels.

Trauma has consequences, and they don’t disappear in a matter of days or weeks. Rather, these consequences unleash consequences of their own, i.e. second-order effects, that are beyond the reach of propaganda or force.

When force fails, threats lose their potency and whatever shreds of legitimacy, trust or confidence that survived the trauma evaporate.

A bayonet in the back doesn’t restore the confidence of the traumatized, especially when the pandemic is still expanding globally.

From Zeleny v. Newsom, decided Friday by Magistrate Judge Thomas S. Hixson (N.D. Cal.):

This case is about crusades. Plaintiff Michael Zeleny has been on a crusade to expose the wrongdoing of a prominent Silicon Valley executive, Min Zhu. From 2005 to 2012 Zeleny staged public protests of Zhu and his cohorts at New Enterprise Associates and WebEx. Zeleny’s protests took the form of in-person demonstrations, musical performances, and multimedia posts on YouTube. His protests were intended to be provocative. They included flyers and posters with graphic content that called out individuals by name. Zeleny eventually combined the First Amendment with the Second and started openly carrying and displaying unloaded firearms during his protests.

But Zeleny says the City of Menlo Park has been on a crusade too. Fed up with his loud and unwelcome message, the City allegedly entered into a conspiracy with NEA to stifle Zeleny and stop his protests. The conspiracy began in 2009, and the City’s part of it consisted of harassing Zeleny, with police constantly stopping and questioning him and his supporters without any reasonable suspicion of wrongdoing. Undercover officers in unmarked cars trailed him and his supporters, and followed him wherever he went. The police interfered with his protests, surveilled him, and falsely branded him a security risk.

In 2012 the City went so far as to frivolously refer Zeleny to the San Mateo County District Attorney’s Office for a sham prosecution for carrying a concealed weapon, which ended in an acquittal. Following the state’s adoption of new legislation regarding open carry, the City adopted a new municipal policy that requires Zeleny to obtain a permit if he is to carry an unloaded firearm during his protests. In furtherance of the conspiracy, the City has continuously denied Zeleny’s applications, all to stifle his free speech and Second Amendment rights.

Or, at least, that’s what he says. In an effort to obtain evidence to back up these accusations, Zeleny served document requests on the City for any documents relating to him or to any actual or contemplated arrest or criminal prosecution of him. The parties are now before the Court on a dispute concerning about 40 pages of responsive documents, over which the City claims the official information privilege.

Federal courts recognize a “qualified privilege” for official information. A governmental entity seeking to invoke the privilege must “make a substantial threshold showing.” It must, “through competent declarations,” “provide[ ] the court with specific information about how the disclosure of the subject material, in the situation presented by the case at hand, would harm significant law enforcement or privacy interests.” {The law enforcement investigatory privilege is similar and does not require separate analysis.} If it does so, the court must “conduct a case by case balancing analysis, in which the interests of the party seeking discovery are weighed against the interests of the governmental entity asserting the privilege.” The test is “moderately pre-weighted in favor of disclosure.”

Because this is a qualified privilege, we have to start with relevance. If a document is core to the case, a qualified privilege is easier to overcome. But if it’s collateral or unimportant, there’s less need to compromise the legitimate interests law enforcement may have in confidentiality. Here, the documents are clearly relevant to Zeleny’s conspiracy allegations. They are mostly dated 2012 and 2013 (with one in April 2011), during the most dangerous time in the conspiracy, when the police were harassing Zeleny and his supporters, and when the City was trying to have him imprisoned on a trumped up concealed-carry charge.

But a document has to be relevant to a “claim or defense,” not just to an allegation. So, we need to analyze the role the conspiracy plays in Zeleny’s claims against the City and its police chief.

Let’s start with the first claim for relief. Zeleny alleges that the City threatened him with criminal prosecution by claiming that some of his protest materials are obscene as to children and he seeks a declaration that they’re not obscene and, more generally, that his protests are protected First Amendment activity. The role of the conspiracy in this claim seems to depend on how the City responds to it. If the City says yes, it did make those threats and his posters are obscene as to children, the claim boils down to evaluating the obscenity status of some posters, which really has nothing to do with the City’s conduct. But if the City denies making the threats, or says the threats were because of neutral time, place and manner restrictions, then the City’s motives become important in deciding who to believe.

The conspiracy allegations function here mostly as evidence of motive and pretext. If they can be borne out by evidence, they would tend to show that the City’s actions were driven by bias against Zeleny and his message and that the City’s denials should be disbelieved.

In his second claim, Zeleny alleges that the City has wrongly interpreted the state open carry laws to create three problems (requirement for a permit, unfettered discretion, distinctions between forms of speech that are not meaningfully different) that give rise to a First Amendment violation. This claim raises factual questions about whether the City has done these things, but as pleaded, it doesn’t seem to turn on bias against Zeleny and his message. Of course, an unfettered discretion claim looks better to the trier of fact if the plaintiff can also show that the unfettered discretion was exercised with bias against him, so atmospherically the conspiracy allegations help here, even if they are not the essence of the claim.

But things come into sharper focus in the third claim. Here, Zeleny alleges that the City’s policy with respect to issuing permits for people to use unloaded firearms in various types of performances is unconstitutionally vague. But he also alleges in the alternative in paragraph 215 that the City singled him out to stifle his protests because of the content of his speech. Bias against Zeleny’s message is the core of that contention. And whatever evidence he is able to assemble of a years-long conspiracy against him is presumably how he would prove that contention.

Finally, any doubt about the relevance of the conspiracy is wiped away by the fourth claim for relief. Paragraphs 221 and 223 allege that the City threatened Zeleny with criminal prosecution to silence him and his message. So, while the role of bias against Zeleny’s message is not necessarily clear in the first and second claims for relief, it is an alternative liability theory in the third claim and the very essence of the fourth claim.

Accordingly, the documents at issue are relevant. And they are not just a little bit relevant. They date from the time Zeleny alleges the police were constantly harassing him and his supporters, so the police file is among the most important evidence necessary to evaluate the allegations at the heart of the fourth claim for relief. Thus, the qualified privilege starts out on shaky ground because these documents look like they’re core.

The City’s position is not helped by Police Chief Dave Bertini’s boilerplate declaration that is the opposite of substantial and specific. The first two paragraphs state his job title and that the declaration is based on personal knowledge. The next paragraph says that the police investigate things, sometimes working with other law enforcement agencies, and keep what they find confidential. The fourth paragraph appears to be the entire justification for the official information privilege, and it is so generic the police could use it in any lawsuit about anything:

“To disclose this official information to the general public, or even in the instant litigation pursuant to a protective order, would irreparably harm the ability of the Menlo Park Police Department and other law enforcement agencies (local, state and federal) to conduct criminal and/or public safety investigations. It is in the interest of justice to maintain the confidentiality of this material because its production would necessarily disclose how the Menlo Park Police Department and other law enforcement agencies obtain information and conduct their investigations and thus complicate their ability to conduct future investigations and irreparably damage any ongoing investigations. The production of this confidential official information would also disclose private and confidential information about third persons.”

The paragraph after that states that Zeleny’s document requests seek, in part, confidential police documents. And then Bertini swears the declaration under penalty of perjury. Bertini’s declaration is so lackluster, the Court could overrule the City’s privilege claim on this ground alone. Indeed, Kelly holds that the Court should do exactly that and not even bother with an in camera review if the defendant’s affidavit is insufficient.

But in an abundance of caution, the Court has conducted an in camera review of the documents at issue. They contain some information that was sensitive eight years ago, such as planned visits to the area by a presidential candidate and the Secretary of Defense. There are also law enforcement updates on then-recent events, suspicious activities, and assessments of security threats to the 2012 election. None of the documents are classified. These documents are so stale that their production will not in any way undermine legitimate law enforcement objectives. Because the documents have the names of specific people in them, including law enforcement officers and others, they should not be posted on the internet for the whole world to see, but there isn’t anything in them that justifies not giving them to Zeleny … subject to an appropriate protective order.

from Latest – Reason.com https://ift.tt/2Ic7xbK

via IFTTT

From Zeleny v. Newsom, decided Friday by Magistrate Judge Thomas S. Hixson (N.D. Cal.):

This case is about crusades. Plaintiff Michael Zeleny has been on a crusade to expose the wrongdoing of a prominent Silicon Valley executive, Min Zhu. From 2005 to 2012 Zeleny staged public protests of Zhu and his cohorts at New Enterprise Associates and WebEx. Zeleny’s protests took the form of in-person demonstrations, musical performances, and multimedia posts on YouTube. His protests were intended to be provocative. They included flyers and posters with graphic content that called out individuals by name. Zeleny eventually combined the First Amendment with the Second and started openly carrying and displaying unloaded firearms during his protests.

But Zeleny says the City of Menlo Park has been on a crusade too. Fed up with his loud and unwelcome message, the City allegedly entered into a conspiracy with NEA to stifle Zeleny and stop his protests. The conspiracy began in 2009, and the City’s part of it consisted of harassing Zeleny, with police constantly stopping and questioning him and his supporters without any reasonable suspicion of wrongdoing. Undercover officers in unmarked cars trailed him and his supporters, and followed him wherever he went. The police interfered with his protests, surveilled him, and falsely branded him a security risk.

In 2012 the City went so far as to frivolously refer Zeleny to the San Mateo County District Attorney’s Office for a sham prosecution for carrying a concealed weapon, which ended in an acquittal. Following the state’s adoption of new legislation regarding open carry, the City adopted a new municipal policy that requires Zeleny to obtain a permit if he is to carry an unloaded firearm during his protests. In furtherance of the conspiracy, the City has continuously denied Zeleny’s applications, all to stifle his free speech and Second Amendment rights.

Or, at least, that’s what he says. In an effort to obtain evidence to back up these accusations, Zeleny served document requests on the City for any documents relating to him or to any actual or contemplated arrest or criminal prosecution of him. The parties are now before the Court on a dispute concerning about 40 pages of responsive documents, over which the City claims the official information privilege.

Federal courts recognize a “qualified privilege” for official information. A governmental entity seeking to invoke the privilege must “make a substantial threshold showing.” It must, “through competent declarations,” “provide[ ] the court with specific information about how the disclosure of the subject material, in the situation presented by the case at hand, would harm significant law enforcement or privacy interests.” {The law enforcement investigatory privilege is similar and does not require separate analysis.} If it does so, the court must “conduct a case by case balancing analysis, in which the interests of the party seeking discovery are weighed against the interests of the governmental entity asserting the privilege.” The test is “moderately pre-weighted in favor of disclosure.”

Because this is a qualified privilege, we have to start with relevance. If a document is core to the case, a qualified privilege is easier to overcome. But if it’s collateral or unimportant, there’s less need to compromise the legitimate interests law enforcement may have in confidentiality. Here, the documents are clearly relevant to Zeleny’s conspiracy allegations. They are mostly dated 2012 and 2013 (with one in April 2011), during the most dangerous time in the conspiracy, when the police were harassing Zeleny and his supporters, and when the City was trying to have him imprisoned on a trumped up concealed-carry charge.

But a document has to be relevant to a “claim or defense,” not just to an allegation. So, we need to analyze the role the conspiracy plays in Zeleny’s claims against the City and its police chief.

Let’s start with the first claim for relief. Zeleny alleges that the City threatened him with criminal prosecution by claiming that some of his protest materials are obscene as to children and he seeks a declaration that they’re not obscene and, more generally, that his protests are protected First Amendment activity. The role of the conspiracy in this claim seems to depend on how the City responds to it. If the City says yes, it did make those threats and his posters are obscene as to children, the claim boils down to evaluating the obscenity status of some posters, which really has nothing to do with the City’s conduct. But if the City denies making the threats, or says the threats were because of neutral time, place and manner restrictions, then the City’s motives become important in deciding who to believe.

The conspiracy allegations function here mostly as evidence of motive and pretext. If they can be borne out by evidence, they would tend to show that the City’s actions were driven by bias against Zeleny and his message and that the City’s denials should be disbelieved.

In his second claim, Zeleny alleges that the City has wrongly interpreted the state open carry laws to create three problems (requirement for a permit, unfettered discretion, distinctions between forms of speech that are not meaningfully different) that give rise to a First Amendment violation. This claim raises factual questions about whether the City has done these things, but as pleaded, it doesn’t seem to turn on bias against Zeleny and his message. Of course, an unfettered discretion claim looks better to the trier of fact if the plaintiff can also show that the unfettered discretion was exercised with bias against him, so atmospherically the conspiracy allegations help here, even if they are not the essence of the claim.

But things come into sharper focus in the third claim. Here, Zeleny alleges that the City’s policy with respect to issuing permits for people to use unloaded firearms in various types of performances is unconstitutionally vague. But he also alleges in the alternative in paragraph 215 that the City singled him out to stifle his protests because of the content of his speech. Bias against Zeleny’s message is the core of that contention. And whatever evidence he is able to assemble of a years-long conspiracy against him is presumably how he would prove that contention.

Finally, any doubt about the relevance of the conspiracy is wiped away by the fourth claim for relief. Paragraphs 221 and 223 allege that the City threatened Zeleny with criminal prosecution to silence him and his message. So, while the role of bias against Zeleny’s message is not necessarily clear in the first and second claims for relief, it is an alternative liability theory in the third claim and the very essence of the fourth claim.

Accordingly, the documents at issue are relevant. And they are not just a little bit relevant. They date from the time Zeleny alleges the police were constantly harassing him and his supporters, so the police file is among the most important evidence necessary to evaluate the allegations at the heart of the fourth claim for relief. Thus, the qualified privilege starts out on shaky ground because these documents look like they’re core.

The City’s position is not helped by Police Chief Dave Bertini’s boilerplate declaration that is the opposite of substantial and specific. The first two paragraphs state his job title and that the declaration is based on personal knowledge. The next paragraph says that the police investigate things, sometimes working with other law enforcement agencies, and keep what they find confidential. The fourth paragraph appears to be the entire justification for the official information privilege, and it is so generic the police could use it in any lawsuit about anything:

“To disclose this official information to the general public, or even in the instant litigation pursuant to a protective order, would irreparably harm the ability of the Menlo Park Police Department and other law enforcement agencies (local, state and federal) to conduct criminal and/or public safety investigations. It is in the interest of justice to maintain the confidentiality of this material because its production would necessarily disclose how the Menlo Park Police Department and other law enforcement agencies obtain information and conduct their investigations and thus complicate their ability to conduct future investigations and irreparably damage any ongoing investigations. The production of this confidential official information would also disclose private and confidential information about third persons.”

The paragraph after that states that Zeleny’s document requests seek, in part, confidential police documents. And then Bertini swears the declaration under penalty of perjury. Bertini’s declaration is so lackluster, the Court could overrule the City’s privilege claim on this ground alone. Indeed, Kelly holds that the Court should do exactly that and not even bother with an in camera review if the defendant’s affidavit is insufficient.

But in an abundance of caution, the Court has conducted an in camera review of the documents at issue. They contain some information that was sensitive eight years ago, such as planned visits to the area by a presidential candidate and the Secretary of Defense. There are also law enforcement updates on then-recent events, suspicious activities, and assessments of security threats to the 2012 election. None of the documents are classified. These documents are so stale that their production will not in any way undermine legitimate law enforcement objectives. Because the documents have the names of specific people in them, including law enforcement officers and others, they should not be posted on the internet for the whole world to see, but there isn’t anything in them that justifies not giving them to Zeleny … subject to an appropriate protective order.

from Latest – Reason.com https://ift.tt/2Ic7xbK

via IFTTT

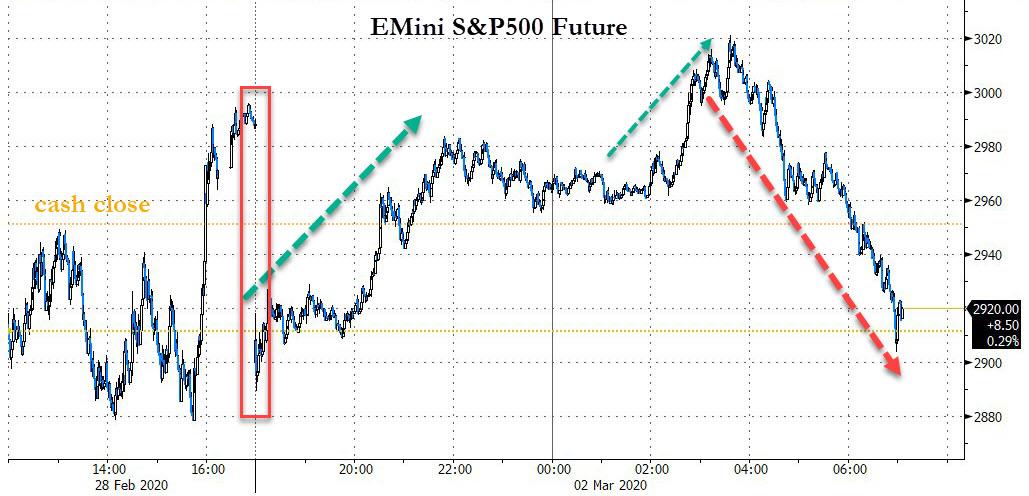

Market Mutates Into A Harrowing Rollercoaster As Futures Soar Then Tumble

A lot has happened since Friday’s cash close, which itself was a furious 600-Dow point squeeze on expectations of a coordinated central bank intervention… that never came.

On Sunday night, US equity futures initially tumbled after Powell failed to satisfy rumors that he would make an emergency rate cut announcement ahead of the 6pm trading open; however, subsequent jawboning attempts by the BOJ and BOE that they are ready to stabilize markets helped futures surge above 3,000.

“The market is coming back because there is perception that there will be a coordinated G7 policy response,” said BlueBay Asset Management’s head of credit strategy David Riley. “We have Fed and ECB meetings coming up in the next couple of weeks. The Fed is the key one and it will be very hard for them to hold off (from rate cuts) if we are in a situation where the economic downsides are becoming more prevalent.”

Alas, it wasn’t meant to last because once Europe opened, futures tumbled as much as 100 points in just over under three hours as traders felt compelled to make their case for 2 rate cuts to the Fed’s front door.

The failed attempt at a bounce followed a rare statement on Friday from the Federal Reserve that opened the door to a rate cut based on the “evolving risks” posed by the outbreak. Central banks in Japan and the U.K. followed suit with supportive messages. Investors weighed the comments against increasing pessimism from economists on global growth, with fears mounting that the virus will trigger more losses after the S&P 500 Index’s worst week since 2008. World growth will sink to levels not seen in over a decade as the outbreak hammers demand and supply, the OECD warned.

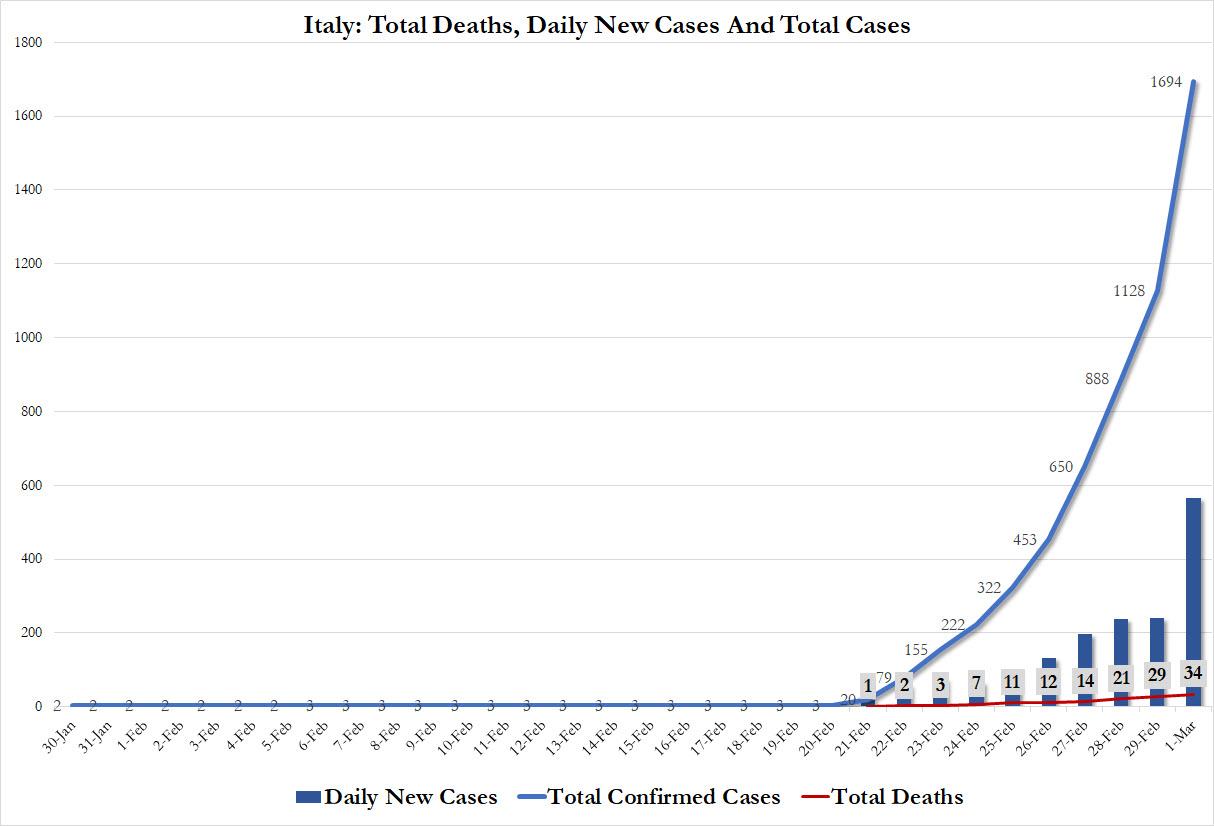

All this is happening as the global death toll from the virus has surpassed 3,000. U.S. cases climbed over the weekend, with the first infections appearing in New York City, Brussels and Berlin, while cases jumped in hot spots of Italy, South Korea and Iran as the US reported a second death and a case count which suggests several community outbreaks. Positive tests in Italy jumped by more than 500 to 1,694 on Sunday with 41 deaths. Lombardy, the region that includes the financial capital of Milan, accounted for almost 1,000 cases.

A weekend data release from China indicated contractionary activity levels – China’s official PMI plunged to a record low 35.7 – Asia trade was set for an ugly open. China’s worse than expected PMI decline will keep pressure on authorities to maintain liquidity and policy rate cuts this month, and more accommodation will be needed, particularly for exporters as the global disruptions from the COVID-19 outbreak escalate and China is now hit with the double-whammy of collapsing export demand from its trading partners.

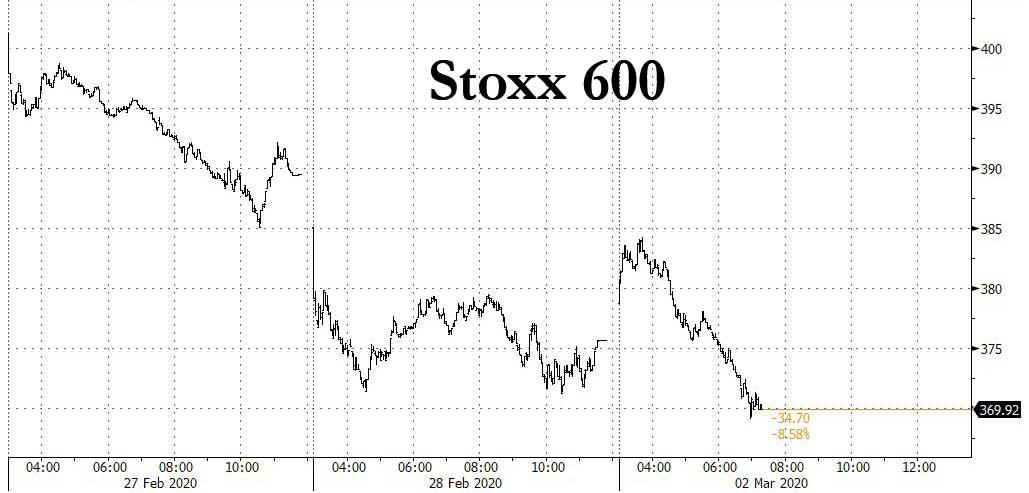

Back to stocks where after last week’s worst plunge for equities markets since the depths of the 2008 financial crisis, it was always going to be a wild ride. Asia had initially dived again after China reported a record slump in factory activity but the region rallied to finish higher as bond yields sunk and talk of OPEC supply cuts sent oil prices roaring up 3.5%. As a result, Asian stocks halted a seven-day losing streak, led by energy and tech companies, as global central banks advocated policy support to coronavirus-hit economies.

Markets in the Asian region were mixed, with the Shanghai Composite Index and India’s S&P BSE Sensex Index rising, while the Jakarta Composite and Taiwan’s Taiex fell. Trading volume for MSCI Asia Pacific Index members was 20% above the monthly average for this time of the day. Central banks sent the markets some supportive signals when the Bank of Japan said it will provide ample liquidity and ensure stability in the financial market, despite not actually doing anything, while the Federal Reserve said it is ready to reduce interest rates this month. Bank Indonesia cut banks’ reserve ratios and signaled it’s ready to add more measures to defend the nation’s battered currency and bonds. The Topix gained 1%, with CareerIndex and Land rising the most. The Shanghai Composite Index rose 3.1%, with Henan Huanghe Whirlwind and Longjian Road & Bridge posting the biggest advances.

After Asia’s torrid surge, Europe then made a blistering start. The Stoxx 600 initially jumped 1.5% putting it on course for its best day in well over a year and Wall Street S&P 500 and Dow futures were pointing to similar gains too. However, the overnight rally in European stocks evaporated with Italian stocks under the most pressure as the epicenter of the region’s virus cases.

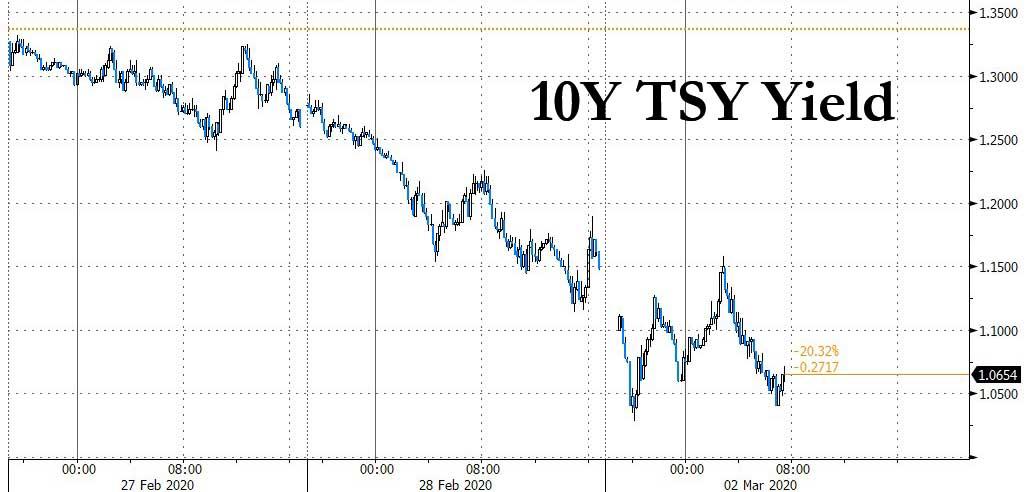

In rates, Treasuries surged, sending the 10-year rate closer to 1%, tumbling as low as 1.0283%.

Yields tumbled by up to 20bp across front-end of the curve, steepening 2s10s by 10.2bp; 10-year yields lower by an additional 10bp vs. Friday’s close around 1.05%. Sentiment soured as even more cases were reported around the world and the OECD cut its forecast for global growth. Most core European bonds gained, tracking Treasuries as they rallied for an eighth day.

Overnight index swaps now price in 50bp of rate cuts by April FOMC meeting, with the latest phase of the rally fueled by potential for a global economic slowdown was sparked by OECD cutting this year’s growth forecast as coronavirus spreads in the U.S. As treasuries continue to lead global flight-to-safety bid, bunds and gilts are relatively cheaper by 5.5bp and 5bp. Treasury 2-year yield dropped to 0.706%, breaching November 2016 low. 3-month dollar Libor -20.9bp at 1.25375%, biggest drop since 2008.

The dollar slipped against the euro and most major currencies on expectations of a Fed rate cut.

Commodity markets were part of Monday’s global rebound. Oil prices bounced $1.5 a barrel on hopes of a deeper cut in output by OPEC after earlier hitting multi-year lows. Brent crude last traded at $51.3 per barrel and WTI at $46.2 per barrel, while industrial metals copper and nickel were 2% and 3% higher respectively and gold jumped 1.4% too after a mild drop last week.

Looking at today’s events, expected data include PMIs and construction spending.

Market Snapshot

S&P 500 futures up 0.4% to 2,962.50

STOXX Europe 600 up 1.1% to 379.88

MXAP up 0.9% to 156.95

MXAPJ up 0.9% to 513.55

Nikkei up 1% to 21,344.08

Topix up 1% to 1,525.87

Hang Seng Index up 0.6% to 26,291.68

Shanghai Composite up 3.2% to 2,970.93

Sensex down 0.2% to 38,208.00

Australia S&P/ASX 200 down 0.8% to 6,391.52

Kospi up 0.8% to 2,002.51

Brent futures up 0.3% to $50.68/bbl

Gold spot up 1.5% to $1,609.16

U.S. Dollar Index down 0.4% to 97.78

German 10Y yield fell 2.6 bps to -0.633%

Euro up 0.5% to $1.1080

Italian 10Y yield rose 2.6 bps to 0.934%

Spanish 10Y yield fell 2.6 bps to 0.256%

Top Overnight News

New York state and California reported new coronavirus cases as Americans grappled with the prospect of a widening epidemic at home. The global death toll from the coronavirus outbreak surged past 3,000 as trading got underway Monday, after a weekend that saw cases in Italy surge 50% and France add 30 new infections

Bank of Japan Governor Haruhiko Kuroda issued an emergency statement after market jitters over over the economic implications of the coronavirus outbreak forced sharp drops in stocks and a strengthening of the yen

The Federal Reserve is now prepared to reduce interest rates this month even though it recognizes monetary policy cannot completely shelter a U.S. economy increasingly threatened by the coronavirus. Fed Chairman Jerome Powell opened the door to a rate-cut at the Fed’s March 17-18 meeting by issuing a rare statement Friday pledging to “act as appropriate” to support the economy.

Pete Buttigieg is ending his presidential campaign, people close to his campaign said Sunday. The decision to drop out just before Super Tuesday, when voters in 14 states to to the polls, is a potential boon for former Vice President Joe Biden, who’s looking for moderate and establishment Democrats to unite behind his campaign in an effort to blunt Sanders’ momentum from the party’s left wing. Michael Bloomberg says Super Tuesday won’t be end

The U.K. outlined its negotiating objectives for trade talks with the U.S., seeking a deal it hopes will deliver a 3.4 billion-pound ($4.4 billion) boost to the British economy.

After getting caught up in last week’s punishing virus-driven sell-off that hit everything from equities to commodities, gold rebounded on Monday to refresh its credentials as a haven in troubled times.

Expectations the OPEC+ alliance will deepen output cuts put a floor under last week’s 16% plunge in oil prices, with futures in New York rallying even as the coronavirus continued to spread rapidly.

Asian bourses and US equity futures began the week volatile with hefty losses seen at the reopen as markets reacted to the abysmal Chinese Manufacturing PMI data over the weekend which slumped to below GFC levels and its weakest on record. This saw US equity futures drop by as much as 3% although later recouped all their losses as markets found reprieve from the declining pace of China’s coronavirus cases and amid widespread anticipation of Central Bank measures including calls for the Fed to deliver a 50bps cut at this month’s meeting. ASX 200 (-0.8%) and Nikkei 225 (+1.0%) were mixed in which Australia suffered from its heavy exposure to China and with financials also weighed by expectations of a rate cut by the RBA tomorrow, while the Japanese benchmark staged a comeback helped by the BoJ which is to ensure liquidity through operations and offered to buy JPY 500bln of JGBs. Hang Seng (+0.6%) and Shanghai Comp. (+3.2%) were also positive despite the alarming Chinese PMI data in which both China’s Official and Caixin Manufacturing PMIs fell to record lows, as sentiment was underpinned by measures including China permitting SMEs to delay debt repayments and with construction stocks surging on anticipation of China rushing into infrastructure projects to offset the fallout to the economy from the outbreak. Finally, 10yr JGBs traded positive but were off their intraday highs as the turnaround in stocks eventually dampened safe-haven appetite, although JGBs still remained afloat after the BoJ declared it will ensure ample liquidity and received JPY 571bln of total bids for the aforementioned JPY 500bln offer.

Top Asian News

Indonesia Cuts Reserve Ratios After Virus Fears Spark Selloff

Member of Iran Advisory Body to Supreme Leader Dies From Virus

European stocks have given up their earlier gains [Eurostoxx 50 -1.3%] which initially emanated from Central Bank stimulus hopes given the concoction of dismal PMIs from China coupled with rising worldwide COVID19 cases. The European bellwether rose as much as 2.3% at the open before the optimistic sentiment faded during mid-trade with a lack of any fresh headlines to shadow the ongoing virus narrative. DAX 30 cash and futures briefly reclaimed 12k whilst the FTSE MIB (-3.1%) underperforms the region following another sharp rise in virus cases in the country alongside disappointing manufacturing PMI figures. Sector-wise, dropping yields see financials underperforming whilst defensives remain in firm positive territory amid the turnaround in sentiment. That said, energy and material names continue to benefit from the price action in the respective complexes. In terms of individual movers, Tesco (+2.0%) holds onto a bulk of its gains following a WSJ report that a Thai billionaire has secured USD 10bln in a bid to acquire Co’s Asian assets. SES (-17%) shares slumped to foot of the Stoxx 600 post-earnings despite noting that it sees no meaningful impact from coronavirus. Finally, Nokia (+1.6%) shares opened higher after Lundmark has been appointed as President and CEO of the Co.

Top European News

U.K. Mortgage Approvals Reach Highest Since Brexit Referendum

Deutsche Bank’s Controls Put Under Heightened Scrutiny in U.K.

Euro-Zone Factories Suffer Supply Disruptions From Coronavirus

Barclays Activist Pressures Board to Remove CEO Staley

In FX, the DXY has retreated even further amidst broad Greenback losses and growing speculation that the Fed will follow/front run other global Central Banks with decisive action to counter the nCoV epidemic. Indeed, expectations were stoked further by unexpected and unscheduled comments from Powell on Friday pledging to use ‘tools’ as required to support the US economy given risks posed by the aforementioned coronavirus outbreak. Rate cut pricing duly ramped up to 50 bp for the upcoming March FOMC and the index has now slipped below the 200 DMA (97.840) to a 97.693 low compared to 98.087 at best with little in the way left in terms of chart support ahead of 97.500.

AUD/EUR/CAD/CHF/NZD/JPY – Although the RBA is widely tipped to shave its OCR by ¼ point overnight, the Aussie is benefiting from US and NZ underperformance, while gleaning extra traction from relative Yuan strength on the premise that Chinese PMIs were so bad that more stimulus is almost certain to be forthcoming. Indeed, Aud/Usd has rebounded strongly from even deeper sub-0.6500 lows to 0.6550+ at one stage, while Usd/Cnh is back down around 9.9600 and Nzd/Usd is hovering just under 0.6275 as Aud/Nzd pivots 1.0450. Elsewhere, the Loonie has pared losses from circa 1.3445 to around 1.3340 ahead of Canada’s manufacturing PMI, the Franc is eyeing 0.9600, but waning against the Euro ahead of 1.0625 as the single currency forges more pronounced gains across the board, Eur/Usd towards 1.1100 and Eur/Gbp approaching 0.8700. Last, but by no means least the Yen is holding within a wide 107.00-108.57 range after the BoJ’s own considerable efforts to combat the adverse economic impact of COVID-19.

GBP/NOK/SEK – Sterling is bucking the overall trend, with Cable losing grip of another big figure handle at 1.2800 on the cusp of UK-EU trade talks that are not expected to go smoothly given well documented differences of opinion on key post-Brexit terms and conditions. However, a downgrade to the manufacturing PMI has also dented sentiment, in contrast to Norwegian and Swedish prints that both picked up pace from previous levels. Nevertheless, Eur/Nok and Eur/Sek are trading on a mixed footing circa 10.3800 and 10.5800 respectively.

EM – In keeping with the divergence noted above, regional currencies are somewhat betwixt and between as euphoria over the prospect of concerted and/or coordinated action to spur global growth fades, while the Lira is still anxiously eyeing events in Syria where Turkish President Erdogan renews calls for Government forces to withdraw or face more military attacks.

In commodities, WTI and Brent font-month futures have rebounded with a vengeance on the first trading session of the week as sentiment was bolstered amid hopes of monetary and fiscal intervention to deal with the fallout of the virus. Furthermore, OPEC will publish its latest output policy decision on March 6th as planned as per sources – with Russia seemingly on board for a unison response following comments from Russian President Putin. That being said, Putin caveated that the current oil prices are acceptable for Russia’s budget, whilst Kremlin stated the meeting with Russian oil companies were not aimed at taking any specific decision. Russia’s Energy Minister Novak stated that Russia did not get a proposal from OPEC to jointly cut production by 1mln BPD and are evaluating the earlier JTC proposal of 600k BPD cut. Futures opened lower to the tune of over 2.5% amid dismal Chinese PMI figures coupled by surging nCoV cases, in which WTI found a base at ~USD 44/bbl before recoiling to a high of USD 46.70/bbl, whilst the Brent contract bounces from an intraday low of around USD 49.50/bbl and tested USD 52/bbl to the upside, although the contracts encountered some selling pressure in recent trade but remain in solid positive territory thus far. Ahead of the OPEC confab, ING believes that “anything that falls short of the OPEC+ Joint Technical Committee recommendation of 600Mbbls/d of additional cuts over 2Q20, and extending the current deal through to year-end, will be taken as bearish.” Meanwhile, BofA Global Research lowered their 2020 WTI and Brent price forecasts by USD 8/bbl each to USD 49/bbl and USD 54/bbl respectively. Elsewhere spot gold drifts higher as the original optimism seen around the market-place fades, with the yellow metal back on a 1600/oz handle from an intraday low of ~1575/oz. Elsewhere copper initially spiked higher on further hopes of China stimulus, with prices briefly topping 2.60/lb before waning back below the figure.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 50.8, prior 50.8

10am: Construction Spending MoM, est. 0.6%, prior -0.2%

10am: ISM Manufacturing, est. 50.5, prior 50.9; New Orders, est. 51.8, prior 52; Prices Paid, est. 50.5, prior 53.3

DB’s Jim Reid concludes the overnight wrap

After a stunning rebound in the last 15 minutes of trading in the US session on Friday (up 2.5% in that time to close ‘only’ -0.82%) markets are holding on to these gains in Asia even after a bad weekend for newsflow. Asia risk kicked off slightly weaker but has rallied on hopes of co-ordinated action by global central banks. BoJ Governor Kuroda became the latest to signal potential action. He said overnight that the BOJ “will strive to provide ample liquidity and ensure stability in financial markets through appropriate market operations and asset purchases” and soon after the BoJ offered to buy JPY 500bn ($4.6 bn) of government bonds with repos. The Nikkei (+0.94%), Hang Seng (+0.77%), Shanghai Comp (+2.88%), CSI (+3.06%) and Kospi (+0.87%) are all up alongside most bourses in the region. As for fx the Japanese yen is down -0.25% and the US dollar index is down -0.15% overnight. Elsewhere, futures on the S&P 500 are also up +0.48% while 10yr USTs yields are down -5.8bps to 1.092 this morning. In, commodities brent crude oil prices are up +3.06% while gold is up +1.20%.

As discussed above the rally is in spite of negative news flow on the virus. In the US, New York City, California and the Seattle area all reported new coronavirus cases over the weekend. The US now has 88 cases with 2 deaths. In a sharp uptick of cases over the weekend, South Korea now has 4,212 cases (vs. 2,022 on Friday morning) with 22 deaths. Cases in Italy also more than doubled to 1694 (vs. 655 on Friday) with fatalities at 34. Similarly, Iran now has 978 confirmed cases up from 270 on Friday morning with 54 deaths up from 26 with most media reports suggesting this still understates the number. Elsewhere cases in Europe outside of Italy are starting to multiply.

The big thing for this week though is probably watching for the spread of cases in the US. There was a Bloomberg story on Friday suggesting there hadn’t been any tests for the virus in New York yet. Other anecdotal stories of late also suggest that testing elsewhere in the country is behind other countries. Indeed fewer than 2,000 had been tested in the US as of Thursday. Other large countries with much smaller populations have tested many more. The U.K. had tested 10,000 as of Saturday morning and South Korea are doing this number on a daily basis. So the US numbers could soar over the next couple of weeks as tests are in the process of moving to the jurisdiction of state and local health authorities from a centralised federal level. Bloomberg reported that 75,000 tests will be available in the US this week. There has even been talk of a severe flu season this year in the US, with cases at elevated levels. You can’t rule out the possibility that covid-19 has been spreading around the US for many weeks already now. Markets will likely take fright if these reported cases now soar.

Data is taking a back seat at the moment but one can’t ignore a truly shocking set of official Chinese PMI February numbers on Saturday with the manufacturing number falling from 50 to 35.7 (consensus 45). The non-manufacturing fell to an even more incredible 29.6 from 54.1. Both were their record ever lows and for perspective the lows for both in the GFC was 38.8 and 50.8 respectively. So the latter has never seen a reading below 50 before and now it’s below 30. Can you imagine the shock at being told at the start of the year that there would be a Chinese PMI with a 2-handle in your lifetime let alone 2 months later. Other global PMIs come out today but they’ll be very backward looking so will be of limited value. Markets will fear the Chinese print is the shape of things to come in Europe if we see anything like the kind of containment that China saw.

Some relief has come from China’s Caixin manufacturing PMI which came in better than the official number this morning at 40.3 (vs. 46.0 expected) but still its lowest reading since the series began in 2004. This reading is seen to be more export orientated than the more domestic based official one. Elsewhere South Korea’s PMI, a critical bellwether of global demand, dropped to a four-month low of 48.7 from 49.8 in January and Japan’s PMI declined to 47.8 (vs. 47.6 from the flash reading), the lowest reading since May 2016. Other PMI, in the region also slid to multi year lows.

Another story to watch is the potential migrant crisis in Turkey and hence the EU. The former has effectively now allowed passage through its country of tens of thousands of asylum seekers from Syria and elsewhere. EU leaders are already starting to condemn the action (fearing a populist backlash) and this is a headache they don’t need as they try to tackle the virus spread.

Recapping last week in markets, the S&P 500 fell -11.49% (-0.82% Friday) for the worst week since the GFC with the NASDAQ -10.54% (+0.01% Friday). Late in the trading session on Friday, Fed Chair Powell signalled that rate cuts may be needed if the market’s reaction to the virus tightens financial conditions, and risk markets did look to bounce on that announcement even if it faded out soon after. The huge rally in the last 15 minutes of trading was an hour or so after Powell’s statement and could have been more month-end index rebalancing between debt and equities given the abruptness of the move in the last minutes of the month. Before Powell’s statement our economists changed their Fed forecast and now expect two 25bps cuts. One this month and one next with the risks tilted to there being more needed. See their report here .

Staying on US equities you may remember we highlighted the work of our US equity analysts last month showing positioning in the 97th percentile and valuations not far behind. Well last week the former dropped from 95th to the 12th percentile in a week. So it’s probably fair that stretched positioning contributed to the scale of the sell-off last week. See their latest report here for more.

The STOXX 600 also saw its worst week since 2008, dropping -12.25% (-3.54% Friday) on the week. Asian markets actually declined less but did see large pullbacks late in the week, with the Nikkei down -9.59% (-3.67% Friday), the Kospi down -8.13% (-3.30% Friday), and the CSI 300 down -5.05% (-3.55% Friday). The VIX finished the week at 40.11 (highest since the China deval in August 2015), up from 17.08 a week ago but peaking at 49.48 intra-day Friday. Credit had an equally challenging week with Euro and US HY spreads +91bps (+31.5bps Friday) and +109bps (+28bps Friday) wider. The thing to watch going forward in credit is outflows and trader illiquidity. Companies are in decent shape but the illiquid market won’t be if you see consistent outflows.

With the large risk off move, sovereign debt continued to rally. The 30yr US Treasury yield has never been this low, finishing the week at 1.68%, down -24bps (-8.3bps Friday). 10yr US Treasury yields closed at 1.149% down 32.3bps (-11.2bp Friday) for the week, to also finish at record lows. Fed futures are now pricing in two cuts by the April Fed meeting and more than 1.5 cuts by March, indicating the belief among traders that there may be an emergency cut outside the regularly scheduled meetings. 10 year bund yields traded back to October levels, finishing the week at -0.607%, with yields falling -17.6bps (-6.4bps Friday). Not all haven assets performed well however, with Gold having a particularly bad close to the week, finishing down -3.51% (-3.61% Friday).

Its clear that not much else matters this week apart from the virus but there are other things to keep an eye on. The full day by day week ahead is at the end but we’ll expand on some of the main highlights below.

The main event will be from the Democratic primaries, with Super Tuesday tomorrow seeing primaries taking place across the US with 34% of total delegates being awarded on this single day. We’ll be publishing a primer on the whole primaries and US 2020 election later today so we’ll save our best material for that. Note that Joe Biden scored a substantial victory in South Carolina on Saturday with 48.4% of the vote vs Sanders 19.9%. He was expected to win but the margin was impressive and brings him back momentum into tomorrow. In other news Pete Buttigieg has pulled out of the race which might help the centrists gather some more momentum against Sanders.

In addition there are a number of usually important data releases out, particularly the PMIs (today and Wednesday) and Friday’s US jobs report. However they’ll be backward looking. Post-Brexit negotiations between the UK and the EU on their future relationship will begin, while central banks in Australia and Canada will be deciding on interest rates. There really isn’t much point in previewing much other data this week as it won’t be taken that seriously. You’ll see it all listed in the day by day week ahead below. If you really want to read about last Friday’s economic data we have a couple of paragraphs after this week ahead calendar. I’ll be impressed if anyone cares.

The deceased government advisor was named Mohammad Mir-Mohammadi. He is a member of Iran’s Expediency Council, a close circle of advisors responsible to the Ayatollah. Mir-Mohammadi reportedly died at a hospital in Tehran on Monday. He was 71.

Mir-Mohammadi

The sick Iranian officials include Vice President Masoumeh Ebtekar, better known to millions of older Americans as “Sister Mary,” the English-speaking spokeswoman for the students who seized the US Embassy in Tehran in 1979, sparking the 444-day hostage crisis. Also sick is Iraj Harirchi, the country’s deputy health minister and the head of an Iranian government task force on the coronavirus. That would be like if HHS Secretary Alex Azar got sick.

During a ‘teleconference’ press conference, Iranian government spokesman Ali Rabiei acknowledged that Iran has “two difficult weeks ahead.”

A separate news teleconference by the Iranian Foreign Ministry started with spokesman Abbas Mousavi dismissing an offer of help for Iran extended by President Trump and Secretary of State Mike Pompeo.

For the common Iranian, this refusal of the US’s offer is truly unfortunate. Because nothing says ‘we’ve got this’ like a rash of your most senior government officials falling ill.

Imagine what would happen to the market if the PM of Italy or President of South Korea got sick? Or even another important religious official like…say…the Pope?