Pentagon Confirms Over 1,000 COVID-19 Cases Among Military, Orders Bases To Stop Public Reporting

The Department of Defense (DoD) announced a grim milestone Monday — it’s total number of COVID-19 cases among US service members, civilian contractors, on-base civilian staff, and family dependents of troops has surpassed 1,000.

“Total DoD Cases (current, recovered and deaths) is 1,087,” according to DoD fact sheet released on Monday. The numbers are as follow:

569 military cases

220 civilian cases

190 dependent cases

64 contractor cases

Defense Secretary Mark Esper, via Reuters.

The Pentagon said 569 service members have been infected, among these 26 hospitalizations, and 34 have recovered.

The remainder of total cases involve civilian contractors working on military bases and/or at the Pentagon, as well as dependents. This number is up significantly from Friday’s total DoD number of 600.

But it appears we are fast heading toward a near total reporting blockage in terms of DoD-wide cases, and specifically where they originate, and in what branches of the US armed services. As Stars & Stripes reports:

The Defense Department has ordered commanders at all of its installations worldwide to stop announcing publicly new coronavirus cases among their personnel, as the Pentagon said Monday that more than 1,000 U.S. military-linked people had been sickened by the virus.

The order issued by Defense Secretary Mark Esper on Friday is meant to protect operational security at the Defense Department’s global installations, Jonathan Hoffman, the Pentagon’s chief spokesman, said in a statement Monday. He said Defense Department leaders worried adversaries could exploit such information, especially if the data showed the outbreak impacted U.S. nuclear forces or other critical units.

This constitutes perhaps the clearest admission thus far throughout the crisis that the coronavirus pandemic is a serious threat to US defense readiness and national security.

USS Theodore Roosevelt, via US Navy

Currently at least two aircraft carriers are battling outbreaks in their midst – both are in the Pacific Ocean and likely have seen their operational readiness deeply compromised as commanders try to contain the spread, with the USS Theodore Roosevelt already being diverted to Guam days ago.

The US 2020 Fiscal Deficit Will Explode To 18%, Unseen Since World War II

Authored by Chetan Ahya, Morgan Stanley chief economist

A Full-Court Policy Press

I hope that you and your families are well. The past few weeks have been challenging both personally and professionally. Covid-19 is at once a human tragedy and unparalleled synchronous shock, affecting both the demand and supply sides of the global economy.

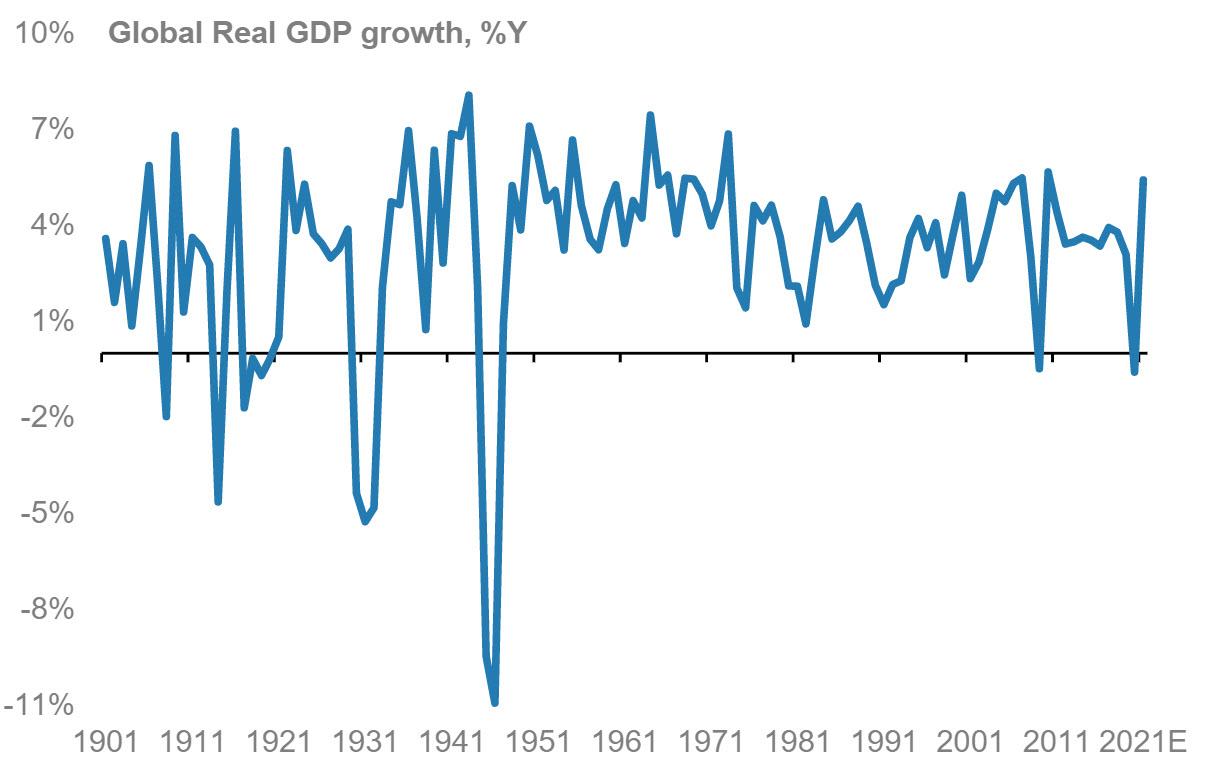

Given the scale of disruption to economic activity, we expect a deep global recession in 1H20, with growth contracting by 2.3%Y in 1H20. Assuming the outbreak peaks by April/May, this will likely set the stage for a recovery in 2H20, to 1.5%Y by 4Q20. For the US, we expect an unprecedented drop of 30.1%Q SAAR in 2Q20 with the unemployment rate also rising to a record 12.8% (since data collection began in the 1940s) before we see it bouncing back at a 29.2%Q SAAR pace in 3Q20. However, global growth for full-year 2020 will still see a decline of 0.6%Y, past the 0.5%Y rate of contraction we saw during 2008 and, on our estimates, the weakest pace of growth during peacetime since the 1930s.

Even before the coronavirus outbreak, the post-GFC global economy had been facing the triple challenge of demographics, debt and disinflation (the 3D Challenge we have written about previously), which the world last faced in the 1930s. At its core, the outbreak represents a substantial shock to incomes, and the impact on aggregate demand will ultimately create renewed disinflationary pressures. The debt challenge will also become more pronounced in the near term as nominal GDP growth weakens and nations, households and corporates face rising levels of indebtedness. Taken together, we expect these forces to bring the 3D Challenge back to the fore.

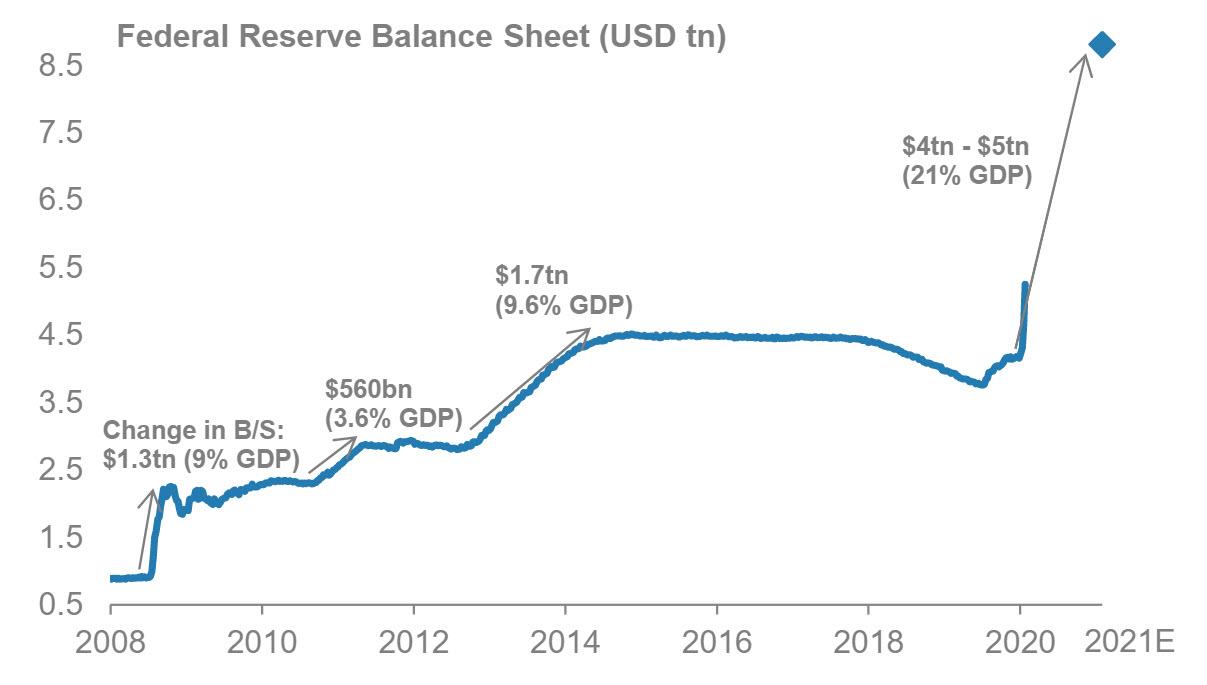

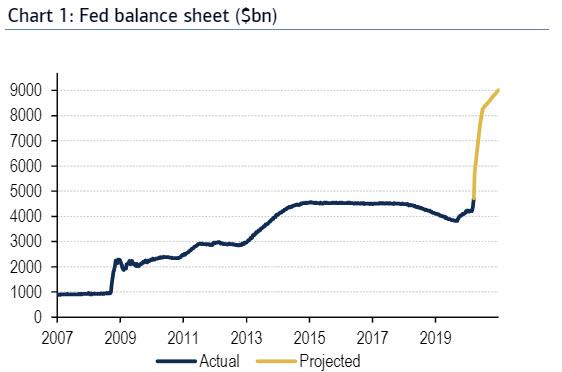

The silver lining is that the coronavirus has elicited a strong coordinated monetary and fiscal response. The pace and magnitude at which these policies have been implemented are also unprecedented. Since mid-January, 23 of the 30 central banks we cover have eased monetary policy. The global weighted average policy rate has declined to below post-GFC lows. All the G4 central banks have now announced aggressive quantitative easing programmes. We estimate that these central banks will make asset purchases of ~US$6.5 trillion in this easing cycle, with cumulative asset purchases of US$4-5 trillion by the Fed alone.

Over the last few days, the pace of fiscal action has also picked up significantly. We now expect that in the G4 plus China, the combined primary fiscal balance will rise by 440bp (~US$2.8 trillion) in 2020. As a percentage of GDP, the G4+China cyclically adjusted primary deficit will rise to 8.5% of GDP in 2020, significantly higher than the 6.5% in 2009 immediately after the GFC.

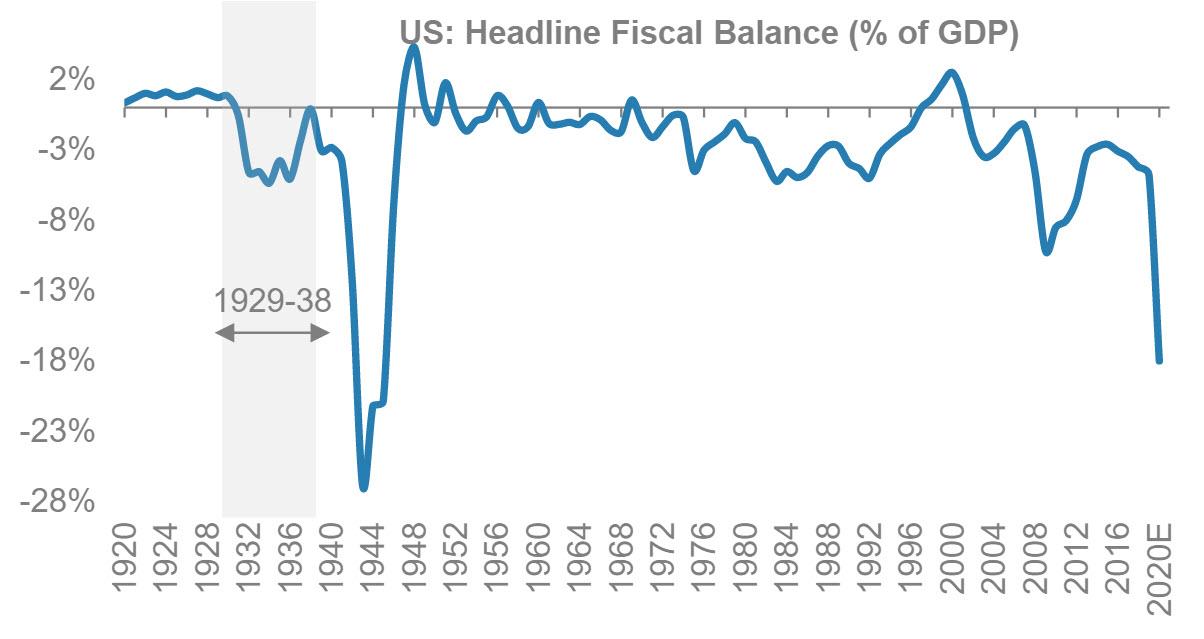

In the US, the speed and magnitude of the policy response have been truly remarkable. The Fed has cut rates to zero and put QE and other lending facilities in place much faster than during the GFC. A fiscal stimulus package has been assembled in a little over a week, compared with two months for the 2008-09 package. In terms of magnitude, we expect the cyclically adjusted primary fiscal deficit to rise to 14% of GDP in 2020 (assuming stimulus of US$2.0 trillion) compared with 7% of GDP in 2009 – the highest level since the 1930s. The headline fiscal deficit will rise to around 18% of GDP in 2020.

Based on the experience of the 1930s and of Japan since the 1990s, this aggressive, coordinated fiscal and monetary easing will be critical in addressing the 3D Challenge. With the help of this extraordinary policy action, and assuming an April/May Covid-19 peak, we expect the global economy to be on the mend from 3Q20 onwards.

However, based on the experience in China, we foresee a tepid pace of recovery initially, and it won’t be until 3Q21 that output reaches pre-Covid-19 levels in the US and euro area.

Hawks will undoubtedly argue (and we’ve already heard murmurings) that these expansionary policies bring the risks of rising inflation and deficits and risks to debt sustainability. However, we take the opposing view and argue that these policies need to remain in place for longer until inflation expectations have systematically risen closer to the central banks’ goals. Again, the 1930s offer a cautionary tale. Because expansionary policies were terminated prematurely in 1936-37, the US economy suffered a double dip in 1937-38 (see Global Macro Briefing: 1937-38 Redux?). Hence, policy-makers must not be too quick to sound the all-clear.

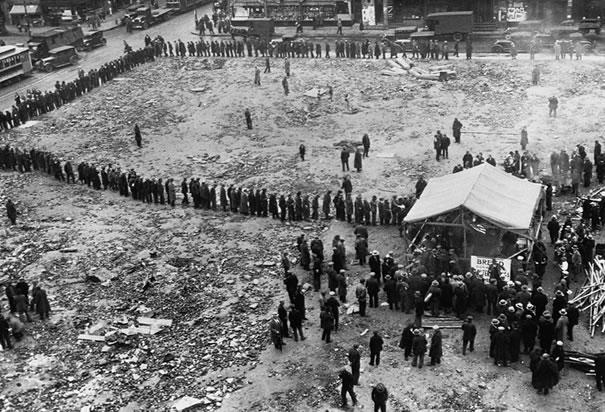

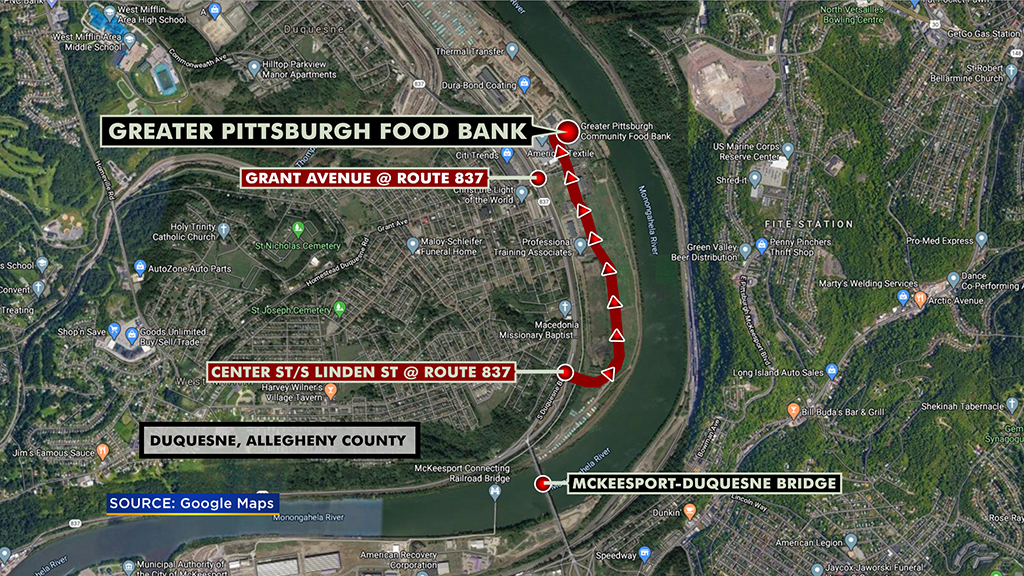

Greater Depression? Shocking Images Show Horror Of America’s New ‘Breadlines’

“It could never happen again…”

A quick Google search shows the horrific scenes from the 1930s as Americans lined up by the thousands for food as The Great Depression struck fast, hard, and deep…

And here is today’s shocking ‘breadlines’ – This video shows hundreds of cars waiting to receive food from the Greater Community Food Bank in Duquesne, near Pittsburgh…

The last two food bank giveaways drew massive crowds and caused major delays on Route 837. When they had one at Kennywood last week, it drew over 800 cars and backed up for miles.

How did America go from “greatest economy ever” to “Greater Depression” so fast?

For years regulatory agencies like the FDA have subtly targeted the use of such things as intravenous vitamins.

One method they use to target the fabric of culture in which people utilize simple, naturopathic remedies is the stringent enforcement of any regulation they can think of. It seems that the FDA targets regulatory violations supposedly committed by those who deal in naturopathic medicine far more than violations from Big Pharma.

Almost 10 years ago, in 2011 it was reported that the FDA sent out a warning letter to a small pharmacy, urging them not to stock intravenous vitamin C. In Australia, the mainstream media has consistently inundated the discussion surrounding health with propaganda over the last 10 years, and vitamin C has been specifically scoffed at.

Despite an observable urge for the regulatory agencies to crush the culture of vitamins and erase their history, it’s leaking out into the mainstream that intravenous (IV) vitamin C in high doses is effective against COVID-19.

Now New York’s largest hospital system is using Vitamin C for Covid-19

In New York’s largest hospital system, urgently ill COVID-19 patients are now being given large doses of IV vitamin C, an article from the New York Post reported a couple of days ago.

Dr. Andrew G. Weber, a pulmonologist and critical-care specialist affiliated with two Northwell Health facilities on Long Island, said his intensive-care patients with the coronavirus immediately receive 1,500 milligrams of intravenous vitamin C.

Identical amounts of the powerful antioxidant are then readministered three or four times a day, he said.

Each dose is more than 16 times the National Institutes of Health’s daily recommended dietary allowance of vitamin C, which is just 90 milligrams for adult men and 75 milligrams for adult women.

The regimen is based on experimental treatments administered to people with the coronavirus in Shanghai, China, Weber said.

“The patients who received vitamin C did significantly better than those who did not get vitamin C,” he said.

“It helps a tremendous amount, but it is not highlighted because it’s not a sexy drug.” (source)

They say the decision to use IV C in New York was based on reports of its effectiveness in China, but vitamin C’s reputation in America far predates that info, although not specifically in response to this virus.

Intensive-care patients who tested positive for the virus immediately receive a dose of intravenous vitamin C measuring 1,500 milligrams, says pulmonologist Dr. Andrew G. Weber, a Long Island, New York critical-care specialist affiliated with two Northwell Health facilities in the area.

Up to 4 times a day, the same dose is re-administered. It was not specified what form of IV C was used, but it is likely to be either Ascorbic Acid (what you typically buy at the store) or Sodium Ascorbate (a popular form intended to be easier on the stomach or the body’s acidity).

Some vitamins, originally derived from the phrase “vital amines,” have different, beneficial effects at much higher doses. At the same time, some minerals or vitamins can throw bodily processes into a state of imbalance with doses too high.

Vitamin C seems to be one of those vitamins that is potent and extremely beneficial at high doses.

Vitamin C is being “widely used” to treat this virus “throughout the system,” a spokesman for Northwell confirmed, the institution that operates 23 hospitals including Lenox Hill Hospital in Manhattan.

This may be a better choice than the more pharmaceutical option.

On a different note, a pharmaceutical combination consisting of malaria drugs known for horrific side-effects, mixed with antibiotics that are known to have no ability to kill viruses (hydroxychloroquine and azithromycin) was promoted by Donald Trump recently.

Nevada recently banned the use of hydroxychloroquine and chloroquine to treat the virus. For someone who believes in freedom, any sort of ban would seem like a step in the wrong direction, but the side effects of hydroxychloroquine and related compounds are well documented.

This 2018 paper published in the Journal of Thoracic Disease examined “HCQ-induced cardiotoxicity,” and heart failure in twins born to a mother who took the drug.

Another paper published in the European Heart Journal of Acute Cardiovascular Care said cardiotoxicity is a “rare but serious complication of hydroxychloroquine.”

Not only that but as of March 24, some kind of federal permission was granted to New York hospitals to dose patients with a “cocktail” of hydroxychloroquine and azithromycin to patients who were considered desperately ill, “on a ‘compassionate care’ basis.”

Hopefully, this compassionate care mentality can be directed toward the firm belief in voluntary treatment, of whatever a hospital has, wherever in the world the person is, rather than involuntary treatment with whatever a hospital chooses to give.

NY is ahead of the curve

In contrast to what is happening in other places, the NY Post reported the Vitamin C is being “administered in addition to such medicines as the anti-malaria drug hydroxychloroquine, the antibiotic azithromycin, various biologics, and blood thinners.”

So why Vitamin C?

Weber, 34, said vitamin C levels in coronavirus patients drop dramatically when they suffer sepsis, an inflammatory response that occurs when their bodies overreact to the infection.

“It makes all the sense in the world to try and maintain this level of vitamin C,” he said.

A clinical trial on the effectiveness of intravenous vitamin C on coronavirus patients began Feb. 14 at Zhongnan Hospital in Wuhan, China, the epicenter of the pandemic. (source)

Let’s hope we see more hospitals using IV Vitamin C in the fight against Covid-19.

“This Will Be A Tsunami” – America Has A New Problem: How To Give Away $2 Trillion In 2 Weeks

Markets have rejoiced over the prospect of an unprecedented stimulus bill, which was passed by unanimous vote in the Senate earlier this week, and is awaiting passage in the House on Friday. But as BMO rates strategist Ian Lyngen argued in a note published earlier this week, passing the stimulus bill into law is merely the first hurdle.

After that, bureaucrats will need to figure out how to get the money to the people, while individuals and small/medium business owners pray that the money finds its way into their hands before they’re driven into bankruptcy or starvation (or both). The quest to distribute the money will require cooperation between various state and federal systems on a level that’s unprecedented, while states make adjustments to their unemployment systems and other processes to disburse the federal grant money in ways that have never been done before.

Douglas Holtz-Eakin, who was on President George W. Bush’s economic team during the 2001 recession, said he’s “cautiously optimistic” about the package, but worries about the money getting where it needs to go, while also worrying that it won’t prevent a dramatic economic contraction.

“I hope it works. It’s designed sensibly on paper. Now we have to get the money out the door,” Holtz-Eakin said. Even still, “we’re probably going to have a second quarter growth rate that is double-digit negative.”

Barack Obama’s $800 billion stimulus bill was literally the first major policy accomplishment of his administration, undertaken almost immediately after his inauguration as most of the country was still wrapped up in the aftermath of the crisis. In March, Obama would remark that stocks looked ‘cheap’, effectively calling the bottom. And over the following years, the money slowly trickled out of federal departments and state grants.

Just as the selloff and economic hit seem more concentrated this time around, so is the government stimulus package meant to effectuate a powerful jolt to economic growth – something strong enough to resuscitate an economy that’s bleeding more than 3 million jobs a week, a number that was effectively curbed by our country’s ability to process the claims (remember, most state governments are still running on massive mainframe computers from the 1980s).

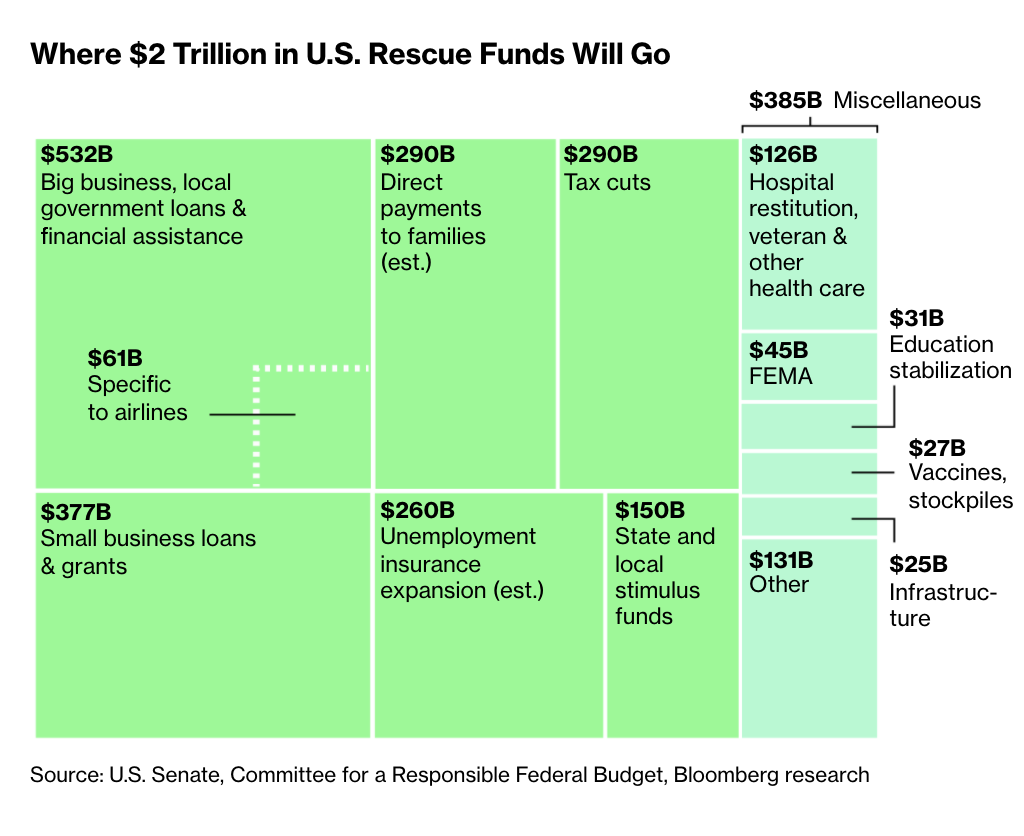

As Bloomberg explains, new programs like the $377 billion subsidy for small businesses via loans that will become “grants” if the businesses simply choose to retain all of their pre-crisis employees for the next few years are intended to get moving quickly, with the money being ladled out in weeks, not months.

Remember last week when President Trump first said he wanted checks in mailboxes in two weeks? That deadline is probably impossible. But if that money isn’t there in a month or two, people are really going to start to feel it. As one reporter explained via twitter earlier, the financial system isn’t really set up for the mass forbearance of payments.

The financial system is just not set up for a temporary forbearance on payments. If someone doesn’t pay for something, then someone else is owed something. (Buyers of credit protection *will* ask for money due).

In other words, the government, the banks, the Fed and everyone else involved is racing against the clock. Both the Treasury, the banks, the various state agencies that administer the welfare and unemployment insurance programs that have just been given a shot of “steroids”, as Chuck Schumer put it – basically everybody involved in making sure this money gets to where it was intended to go – is now scrambling to compete in a sack race that will test the capacity of their systems to work together and also process the sheer volume of payments and disbursements necessary for this program to work.

Remember how state websites around the country crashed last week as millions of Americans tried to file for unemployment insurance? That was just a glimpse of the mayhem to come. The technological pandemonium will be tantamount to a mass marketing opportunity for Amazon, Microsoft and Google as they battle for the lucrative state and federal contracts to transition these systems off the old mainframes and on to the cloud.

But technological limitations aren’t the only potential roadblocks. The bill was written in a hurry, and some legal definitions and processes remain vague, opening the door to lawsuits and injunctions and other potential disagreements intended to tie up the payments and divert money as everybody scrambles to get a piece.

The biggest single portion of the stimulus is the billions earmarked for large companies and state and local governments. But the rules for deciding who is entitled to that money, and how it will be distributed, are still being worked out.

According to the legislation, the Treasury has 10 days from the date Trump signs it into law to come up with a set of guidelines governing who will qualify for the loans and how the application process will be regulated.

One of the biggest components of the legislation is the $600 billion earmarked for states to dole out via beefed up unemployment benefits through July 31. Maximum state benefits range from $235 in Mississippi to $823 in Massacjusetts, and the number will range depending on income.

Though the government wants individuals to take advantage of the programs “quickly”, at best, the money will take a few days to become available, and the checks won’t start to flow for a week or two, probably longer.

The added boost would be four months for those laid off now, but less time for those losing their jobs closer to July 31. And with so many different state agencies administering their own programs, there’s plenty of room for some stated to stand out as successes, and others to stand out as failures.

“We want people to take advantage of all of this quickly,” Pelosi said Thursday. Some of that will “depend on how the states do it, and they are not all uniform.”

As one Obama-era official said to Bloomberg, compensating contractors and the self-employed gig economy workers could be a challenge for some states.

Seth Harris, who was deputy secretary of labor in the Obama administration, said the expanded coverage in the legislation, especially to contractors and those employed in the gig economy, may be a logistics challenge for some states.

“These under-resourced, strapped, stressed systems in many cases do not have the latest technology or data systems,” he said. “Now they’re being hit by the largest tsunami of unemployment claims in the history of those data being collected. Now Congress is asking them to change the way they do things.”

One Kentucky Republican is threatening to throw up roadblocks for the bill by essentially showing up and demanding an in-person roll call vote, while Speaker Pelosi tries to push through a voice vote to expedite the vote and avoid individuals coming close to one another after at least 2 Congressmen have tested positive for COVID-19.

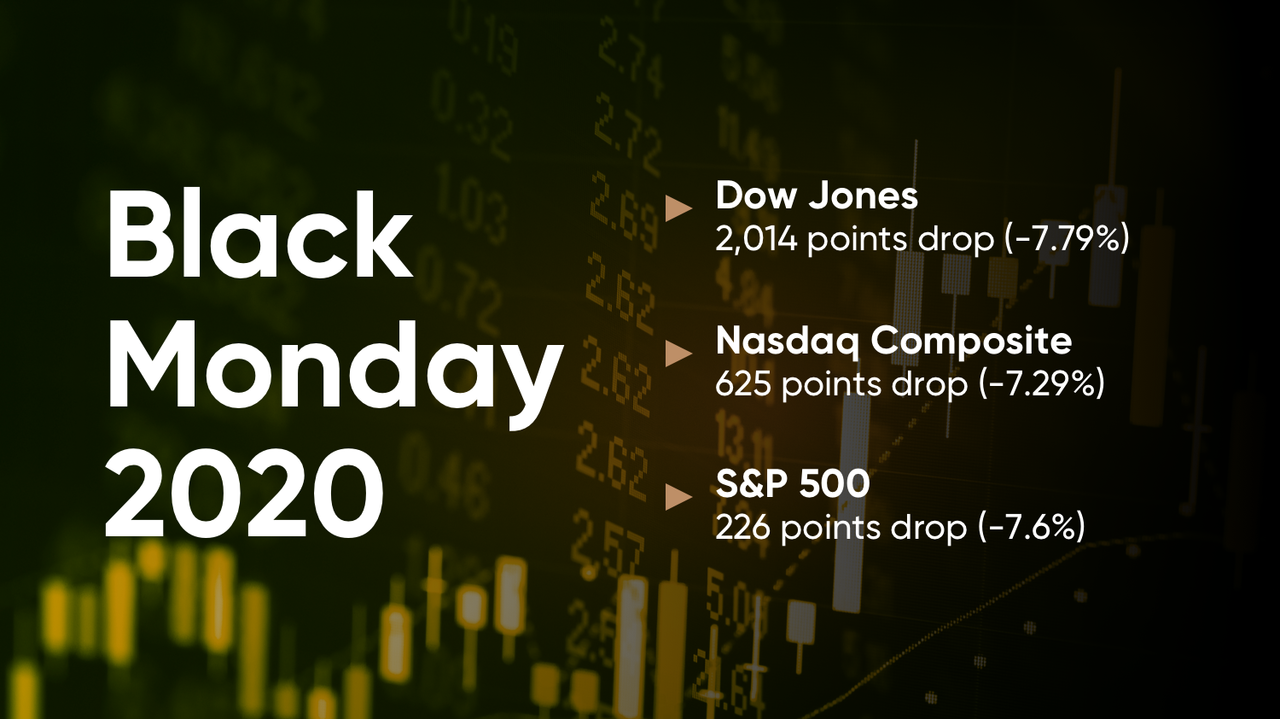

Now that almost a month has passed since a meteor (metaphorically… for now) slammed the US stock market, unleashing the fastest bear and bull markets in history, a global economy that has ground to a halt as over 2 billion people now live under lockdown conditions, and an unprecedented response that includes $7 trillion in monetary and $5 trillion in fiscal stimulus (and counting), which will explode the US budget deficit to at least $2.4 trillion in 2020…

… it is allowing analysts to present a more nuanced take on if not where we are headed, then where we have been.

One such take was performed by BMO’s FICC strategist Daniel Krieter who looked at the recent move in fixed income markets and credit spreads to determine if the current crisis is better, worse or in line with the global financial crisis of 2008.

Comparing the current crisis to his previous assessment of the US economy in 2020 that framed the backbone of his full year outlook, Krieter writes that rather than a modest drop, consumer spending is likely to reach all-time lows in short order and bring about a far more severe recession than he was originally projecting. Therefore, spreads moving wider than any non-crisis period on record makes sense. But do the peaks of 2008/09 represent fair targets for the peaks in credit spreads this time around? To answer this question, the BMO analyst looks at a few factors to determine if the increasingly common comparisons between the current economic downturn and the global financial crisis are justified.

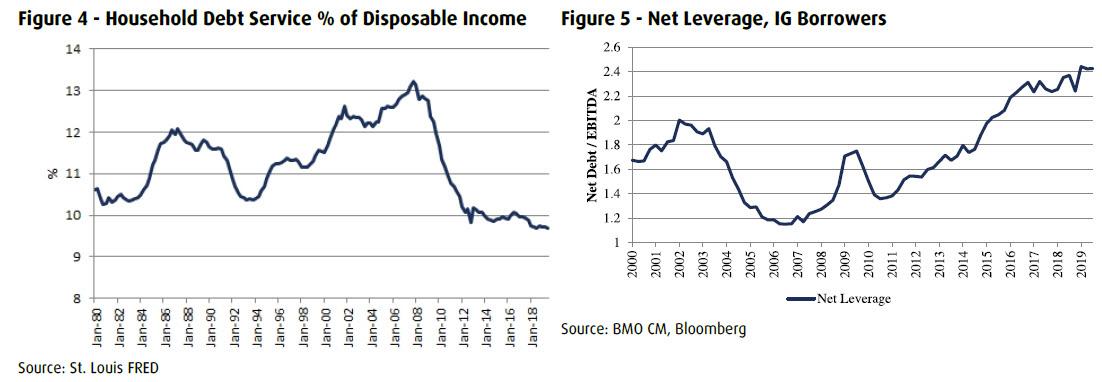

Household vulnerability: Figure 4 shows the ratio of household debt service expense to total disposable income reached a 40-year peak in 2008, just ahead of the financial crisis. In the current cycle, the consumer is in much better shape according to this and other metrics of consumer leverage. We simply display debt service expense to total disposable income because of superior historical data availability. Despite increasing concerns of rising non-mortgage debt on consumer balance sheets, the consumer appears far more able to handle an economic downturn now than during 2008. Comparison: Better than 2008

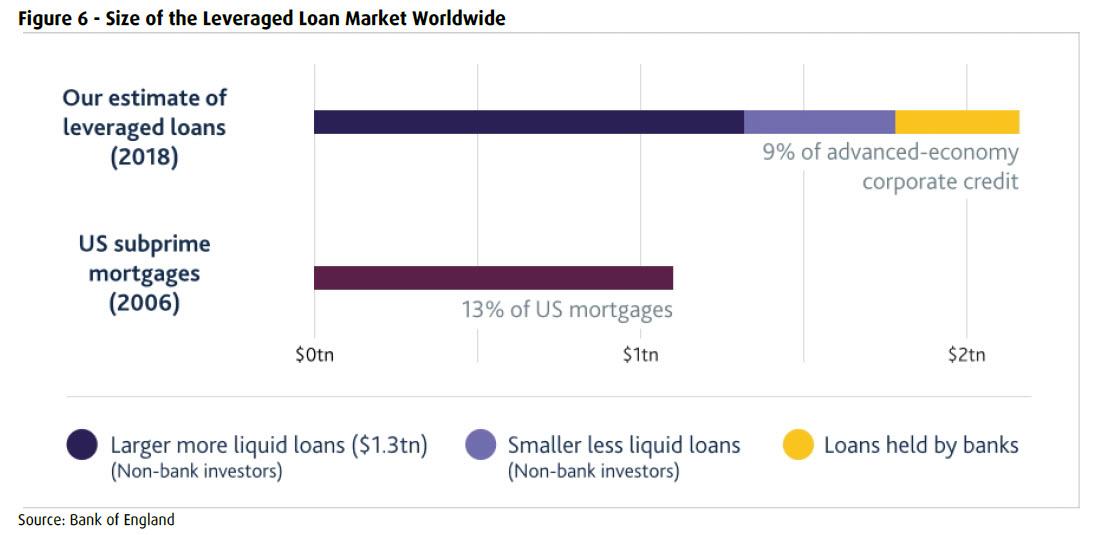

Business vulnerability: The same cannot be said for the business sector. Figure 5 shows leverage in the business sector currently sits near all-time highs, well in excess of the previous peaks realized during the 2001 cycle. (There is an extended discussion of the business sector in more detail below). Comparison: Worse than 2008

Consumer confidence/spending: BMO breaks this important factor down into three sub-categories.

Wealth effect: In 2008, the stock market sold off more than 55% with a drastic impact on savings, particularly retirement saving. In addition, the housing market fell precipitously, causing many people to either lose their home or go underwater on their mortgages. This phenomenon was not limited to just the bad borrowers that turned in their keys. Good borrowers who simply bought their house at the wrong time lost a significant portion of the equity in their house and, in many cases, all of it. The massive hit to wealth is what slowed down consumer spending and brought on recession. The housing market will not repeat its decline this time around, even if a slow spring moving season will very likely be reflected in housing prices. Still, the expected temporary nature of the virus means that housing prices are extremely unlikely to experience drops similar to the financial crisis. In addition, the stock market was down as much as 30% since reaching all-time highs on February 20th. Though downward momentum remains, the hit to 401k is nowhere near as drastic as the 2008 experience (at least so far). Comparison: Better than 2008

Exogenous shock: Naturally, there were many ingredients in the 2008 recession, but if one event were to meet the definition of “catalyst” it would without doubt be the failure of Lehman Brothers in September 2008. Lehman’s collapse set in motion the chain of events that led to the worst economic downturn since the Great Depression, but, in isolation, the Lehman collapse had very little impact on the economy. On the other hand, the economic consequences of self-quarantine brought on by COVID-19 are arguably the most difficult exogenous shock that financial markets have ever dealt with. Comparison: Worse than 2008

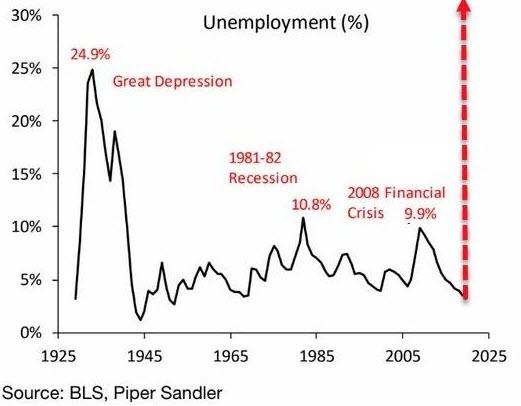

Unemployment: The official U3 unemployment rate peaked at 10% during the 2008 recession compared to today’s unemployment rate of 3.5%. The loss of jobs during the financial crises was the second most severe in the history of the data series. In this cycle, the severity of the projected drop in consumer spending as a result of quarantine is likely to send unemployment significantly higher, and there is concern that the unemployment rate could surpass 2008 levels in a worst case scenario. In fact, during a behind closed doors meeting with Congress during the past week, Treasury Secretary Mnuchin reportedly used estimates of unemployment as high as 20% unless Congress intervened with fiscal stimulus considering the outsized impact the virus has on the service sector and the disproportionally high number of service sector employees. Fortunately, a $2.2 tn dollar stimulus package has passed. Nevertheless, unemployment is going to rise, the only question is how much. Consider the loans being made available to small business through stimulus. As currently proposed, the loans stipulate that employees must be kept on payroll for the next six weeks and the loan covers wages paid. The cash doesn’t help with anything else, it just covers the wages of employees that you are now required to keep employed. Following the six-week period, the small business must then pay all of its employees and a new loan out of future earnings. This means that stimulus loans have very little or no benefit for companies that won’t realize significant pent-up demand once the virus is contained. For these companies, a more appealing option may be to simply reduce headcount now and try to weather the storm until demand comes back. Next, consider that the majority of employees in the United States work for companies with more than 500 employees and are thus ineligible for small business loans (even if some work in distressed sectors that will receive stimulus funds). The coming fiscal package likely ensures that unemployment won’t reach the worst case scenario projected by Secretary Mnuchin, but an increase to 2008 levels is likely well within in reach. In a worst case scenario where the virus lingers longer than currently expected, unemployment could easily surpass the highs of the financial crisis. Comparison: Unknown.

Government/Central Bank Response: In response to the current economic downturn, the Fed and U.S. government have already deployed essentially the same relief package that was deployed in response to the 2008 financial crisis. The Fed has slashed rates to zero and committed to unlimited QE. In addition, the central bank has deployed a number of non-traditional monetary policy tools to help aid the functioning of financial markets through this difficult time. These tools designed to boost liquidity are very similar to the “alphabet soup” facilities deployed during the financial crisis. For its part, the government has enacted a $2.2 tn stimulus package, very similar in terms of financial commitment to the ARRA act of 2009. As part of the stimulus, most Americans will get checks of at least $1,200 dollars in April and May to help smooth the fall in consumer spending. In 2008, Americans got a check for $600, followed by a tax credit of $400 in 2009 for a total fiscal stimulus of $1,000. Importantly, this is just the extent of measures deployed so far. Further stimulus in the form of delayed mortgage payments are on the table, and have already been deployed in certain circumstances alongside a 60-day suspension in student loan payments. The Fed is also buying corporate bonds for the first time. Comparison: Better than 2008

Timing of government/central bank response: In 2008, it took months for rates to reach to the effective lower bound, enact QE, and for large scale fiscal stimulus to be deployed. In 2020, this process took just weeks. Comparison: Better than 2008

GDP: The reality that the U.S. is now in recession has officially taken root, and evidence of that is beginning to show up in economic projections. Updated economist expectations for Q1 GDP range from -4% to 1%, while Q2 projections are looking very dire. In fact, economists are expecting the second quarter to potentially be the worst quarter of GDP growth since at least the Great Depression, with estimates as low as -24%. If realized, these estimates suggest GDP growth of -2.5% for 2020, which is likely a good starting point for a base case. By comparison, the worst annual GDP growth realized during the financial crisis came during the four quarters ending June 2009 at -3.9%. Unfortunately, estimates of the COVID-19 impact on GDP continue to worsen, exemplified by a projection of -24% annualized GDP contraction in Q2 from Goldman Sachs. If second quarter GDP actually turns out that bad, GDP contraction in 2020 could easily rival or surpass 2008. In addition, most economists currently project a swift rebound in the third and fourth quarters, presumably once virus concerns fade with the arrival of higher temperatures in summer. But what if summer fails to stem the spread of the virus? Or even if it does, what if virus fears return during the fourth quarter with temperatures dropping again and no vaccine in place? In this case, any growth in the third quarter is unlikely to be sustained in the fourth quarter with the return of quarantine fears. Comparison: Unknown.

In conclusion, Krieter writes that after analyzing a variety of factors in both the current environment and the financial crisis of 2008, comparisons between the two are indeed justified. A few factors suggest that the current recession may not be as bad as the financial crisis, chief among these the strength and timing of government/central bank intervention. On the other hand, there are other factors to suggest that the current downturn will be just as bad as the financial crisis, and potentially worse. Much remains uncertain and dependent upon the path of the virus. In a worst case scenario where virus spread and ensuing quarantine lasts longer than the market currently expects, some of the factors discussed above that we determined were better than or similar to 2008 could easily flip to being worse (unemployment, contagion, and GDP). In this case, the current economic downturn is likely to be worse than the financial crisis. There is no potential for the factors determined to be worse than 2008 to flip to being better.

Arrest Warrant Issued For Florida Pastor Who Defied Order To Suspend Church Service

As governors around the country begin enforcing their lockdown orders or other closure requests and restrictions, a small but vocal alliance of individuals who are opposing the lockdowns is growing. And in what’s likely going to be remembered as a watershed moment for the individualist movement opposing the lockdowns, a Florida pastor is now facing an arrest warrant after holding two church services on Sunday in defiance of the governor’s “safer at home” order.

Tampa-area pastor Rodney Howard-Browne “intentionally and repeatedly chose to disregard the order set in place by our president, our governor, the CDC, and the Hillsborough County Emergency Policy Group,” Hillsborough County Sheriff Chad Chronister said during a press briefing on Monday.

Apparently, this decision to prosecute the pastor is becoming a big deal. The warrant is for unlawful assembly in violation of a public health emergency order. Chronister said the pastor’s “reckless disregard for human life put hundreds” of congregants and thousands of residents at risk. Rumor has it that Howard-Browne scoffed when he was informed about the order and insisted he wouldn’t follow it no matter what the county said or did, ABC News reports.

Well, that apparently got their attention, because since Friday, the sheriff’s office has been in contact with The River at Tampa Bay Church and has received an anonymous tip that Howard-Browne has refused to stop large gatherings in accordance with the order.

The pastor has refused several attempts by the police to go and speak with him.

Not only did the church choose to deliberately defy the stay at home order when it could have held digital sermons, but it even sent out buses to bus in the faithful to attend church that Sunday.

Howard-Browne apparently took umbrage at the notion of being labeled a “nonessential service.”

Howard-Browne told congregants Sunday, “I know they’re trying to beat me up about having the church operational, but we are not a nonessential service.”

This is the same pastor who made headlines a few weeks ago by declaring that he would “cure” COVID-19 in the US, just like he promised to do with Zika.

The Flood Begins: Treasury To Sell Over A Quarter Trillion Bills In 48 Hours

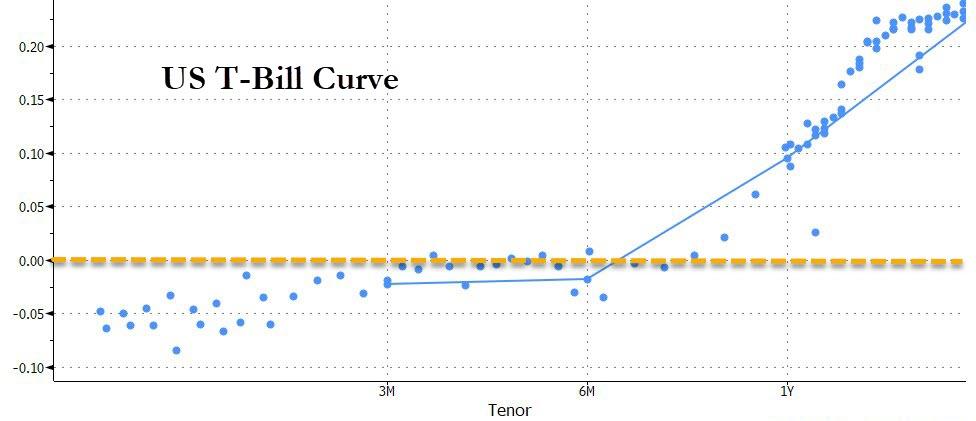

Having noticed the Treasury shortage forming in the bond market, which as we observed emerged both across the broader curve as manifested by the surging demand for the Fed’s reverse repo…

… as well as the unprecedented demand for “cash-like” T-Bills resulting in negative yields for all paper through 3 months…

… which has gifted bond traders with an arb that literally prints free money as described in “Here Is The Treasury’s (Not So) Secret Trade Printing Millions In Guaranteed, Risk-Free Profits Every Day“, the Treasury has taken decisive action and in order to prevent the Fed from becoming the money market fund of last resort, is literally flooding the market with T-Bills to satisfy the market’s panicked need for cash-equivalent paper by announcing an additional two cash management bills today in addition to the one that was revealed last week.

Starting tomorrow, the Treasury will sell just over $100 billion in Cash Management Bill, including a $60BN 42-day CMB and a $45BN 69-day security at 11:30am ET on Tuesday. This follows the sale of $60BN of 37-day CMBs at 0.025% Monday, which saw Indirects awarded 60.6% of the issue.

There’s more: the Treasury also sold $51BN of three-month bills at 0.085% (tailing the When-issued bid of 0.040%), and $42BN of six-month Bills which also tailed at 0.100% versus the WI bid of 0.085%. Why the tails? According to Jefferies economists Thomas Simons and Ward McCarthy, the morning announcement of a second $60BN CMB auction this week, plus quarter-end balance sheet pressure “necessitated some concession for the auctions.” Also, while the 4.5bps tail can be considered a bad thing, the market is “just starting to back off zero or negative yields” so the auctions are still coming in at “very, very low outright yield levels” according to the Jefferies duo.

In other words, inside of 48 hours we are looking at a gross deluge of $258BN gross in Bills and Cash Management Bills to satisfy what seems to be unprecedented demand for short-term paper. On a net basis, between Monday’s regularly schedule auctions, Tuesday’s four- and eight- week settlements and cash management bill sales, the Treasury will raise about $194BN of new cash this week, according to Bloomberg calculations.

And that’s just the beginning, as the Treasury does everything it can to alleviate the Treasury shortage. Considering it has a few trillion in stimulus payments it has to fund, we are confident the shortage won’t last too long.

I voted for you and I’m voting for you again. I like what you’re doing with our country. I like too that you like me. I say that because I’m a fracker and you seem to like frackers. We like you too. Because of our solid relationship, I feel I can be impertinent, even obnoxious, and suggest that you take a few moments out of your extremely tight schedule and entirely remake the oil world at your earliest possible convenience.

Please keep applying all your efforts to the Coronavirus. Don’t stop any of your momentum there. The oil and gas industry can wait. We’re used to supply and demand-side disruptions. We’ve grown accustomed to working without a net. In fact, it’s no secret that we are masters of pandemics—at creating our own that is. But once you are ready for us, we will be unconditionally ready for you.

The demand side destruction now taking place is huge, bigger I think than what most analysts are forecasting; maybe something as high as 20 to 25 million barrels of oil a day in a previously balanced 100 million a day market. The supply-side destruction about to take place is going to add to the problem, but it will be small relative to the demand side. The Saudi’s are thumping their chests but the truth is they can only add a few million barrels of oil per day. Under normal circumstances, that’s a market changer. But these days, when compared to the demand destruction, it’s only a drop in the bucket. Collectively, though, we are in for a real stomping. Inventories are going to spill over into unheard of prices. We’re going to wish for those halcyon days of $25 oil. It’s coming. There’s no stopping it, and with it will come the unraveling of one of the centerpieces of your platform, sir, an energy-independent America. Many in your administration will ask you to appeal to the reasonable side of the Saudi’s. They will tell you to make a deal, give something away, turn your head. Please don’t. If you must, sneak off for a well-deserved round of golf when them Ivy Leaguers who have been writing US policy for the last few centuries start lining up with advice. They will be in smart suits carrying satchels filled with mission statements on how to preserve our relationship with the Middle East. Let’s duck those meetings.

Rather, obnoxiously, I would suggest, you give some consideration to the possibility that there is no reasonable side to the Saudi’s—not as it would pertain to our interests. There’s no talking to the Russians either, but their excess capacity is measly when put up against the Saudi’s, so why bother? Backchannel negotiations aren’t going to do much either. You’ll just be breathing life into dead and outdated ideas, like the foreign policy of countless administrations before yours. Instead, why don’t you reinvent American’s energy policy and its relationship with all of the oil-exporting countries? I ask you to do something completely different because you are completely different. You do the unthought of. I like that about you. A lot of people do.

As a fellow free-market advocate, what I’m suggesting may sound treasonous, but only because it is. What I’m saying is you need to fix the price of oil, maybe basin by basin, or one price for all. Set it at $62/bbl if one price for all. All imported oil would be subject to a tariff. This includes all the Sulphur-rich, low-quality oil the Saudi’s are sending into their state-owned Motiva refinery in Port Arthur, Texas, along with all the other heavy crudes shipped into our ports. Of course, they’re going to cry and moan, but so do my kids when I tell them no more TV.

Now, this is putting a simpleton’s spin on it, but no bailout money would be required for the US oil and gas sector, plus you’d be sitting on those tariff dollars. Use them as you see fit, but I would argue against stuffing oil tariffs into a general fund. My treasonous thinking has you allocating some of it to wind and solar development. I would also push some into nuclear and would rewrite the rules there so plants can be built quickly, efficiently and safely. Oil and gas alone cannot meet all of our needs, not with decline curves and high-graded shale getting in the way, not to mention the time to bring on new offshore development. So, include renewables.

Odd things may happen to your presidency when embracing all forms of energy. You may find some of the green energy crowd coming along with you. But you won’t get them all; not the militants anyways. They tend to be a strong-willed, loud-mouthed bunch not fond of compromise. Nevertheless, with such an all-encompassing, all of the above approach—heavy on natural gas—and light on stupidity (think farting cows)—you just might win over enough of them to win over the House.

To clean up our air, I would also create tax incentives for refiners along the Gulf Coast to retool for lighter grades of shale oil. It’s cleaner and it’s right there, not half a world away. That way, we won’t have to overlook the heavy Venezuelan crudes shipped to Citgo’s three Gulf Coast refineries. Citgo is owned by Venezuela. Their refineries would have to retool as well (hello, EPA!) and start running lighter, cleaner crudes. Venezuela doesn’t have lighter cleaner crudes, but we do.

Think of it, you’d be able to kiss off the dictators long on self-interest and short on tolerable human rights records. I don’t know about you, but it sounds like fun to me.

As to what to do with the Saudi’s, I would say be their friends, but with limits (see Khashoggi). Don’t expect much in return for your friendship. It will be lopsided as some friendships can be. As to geopolitics and a presence in the Middle East; you can have that. We just won’t need their oil. The Russians don’t either, so that makes us kind of even with them, doesn’t it? And all those policy folks, screaming about diplomacy and normalizing relationships, remind them of Russia’s seventeen years in Afghanistan until we took our turn. Where did that get them? Remind them too of the decades we’ve toiled in the Persian Gulf. Where did that get us?

I can answer that.

The Saudi’s are now, in the midst of the Coronavirus pandemic, opening up their spigots as a direct strike at American’s energy independence. But they always do that, regardless of how many of our troops have been killed and maimed defending order in their area of the world. Billions and billions and billions of dollars have been spent too, dollars they do not payback. It really is time to go. It’s over. They’ve moved on. So should we. Think of it like a divorce. You have the moral high ground so no one can blame you.

Another thing. Turning our back on MBS’s misdeeds just doesn’t cut it anymore. Who’s going to be his next Jamal Khashoggi, when does he next fill up the Riyadh Ritz Carlton, who is the next cousin to be detained as he consolidates power? You are the friends you keep, sir. This is a simple and homey kind of thing to say—which makes it true. So, let’s dump this guy. But be nice about it. After all, we still want him to buy our stuff, but not with the currency we just handed to him.

If the Coronavirus has taught us anything, it’s that supply chains essential to life in America should not be outsourced. Move energy and pharmaceuticals and all other essentials back home. We’re safer that way. You’ll be creating homegrown jobs and we won’t have to kiss anyone’s backside. No longer is there any need for that. We have it all; shale, wind, solar, nuclear and enormous offshore potential.

One last point worth mentioning is that energy independence was about to fall apart anyway. The present structure of shale wasn’t working—“present” meaning two months ago. Producers can’t generate free cash flow, pay off ridiculously (and irresponsibly) large amounts of debt, and grow reserves at the same time, at least not if they want to stay listed on the NYSE. The industry was already struggling at $55 oil and $1.80 gas. Everyone was hedging every time there was a little bounce. Service companies in the shale sector were being squeezed into unprofitability. Leave natural gas alone for now but fix the cost of oil. If too much is produced, it can be sold and exported at whatever the going rate is.

Should there be naysayers, those that say this is nothing more than a bailout request, I say so what. It is and it isn’t. Prices will be low, but that will fix things and then there will be another mad rush to produce because prices will be high. Trust me. It happens every time. Boom and bust. Go to an energy conference and you will find all the producers talking about their humongous acreage position, and all the frackers talking about their humongous horsepower. Margins and profits won’t come up. Trust me. We can’t help ourselves.

In closing, Mr. President, we finally need to go it alone. Shale has proven that we can. No wars, no backroom deals, no dictators. Remaking the oil world could be an absolute boon for the US economy, a cleaner environment and a guarantee at the energy independence you have touted. It’s time to adjust to the new world order and you are the only president I have known that would have the cajones to do it.

“People should not be afraid of their governments. Governments should be afraid of their people.”

– Alan Moore – V for Vendetta

“Authority, when first detecting chaos at its heels, will entertain the vilest schemes to save its orderly facade.”

–Alan Moore – V for Vendetta

I wrote an article called V for Vendetta – 2011 just over nine years ago on the day after the Tucson shooting where congresswoman Gabrielle Giffords and eighteen others were shot by a psychologically disturbed lunatic, with six dying. At the time, I thought of the scene from the V for Vendetta movie where someone did something stupid and all hell broke loose. I expected a similar result from this act, but those in control of our society were successfully able to put a cork in the bottle, preserving their façade of order.

We learned shortly thereafter, through the patriotic efforts of Edward Snowden and Julian Assange, how the government was using the vilest of schemes to surveil every American through their abuse of the Patriot Act. The government has become and enemy of the people.

It is interesting to go back and view my conclusion from nine years ago and assess its accuracy as of today:

“This country has not reached the level of control and fear seen in Orwell’s 1984 and V for Vendetta, yet. We are moving relentlessly in that direction. Surveillance, monitoring, spying, censorship, secret prisons, predator drones, and conforming to state rules and regulations put citizens further under the thumb of an all-powerful state. The freedom to dissent, the freedom to be left alone, the freedom to speak out against injustice, the freedom to disagree with your government, and the freedom to present your ideas without fear of retribution or penalty are essential in a democratic society.

The next phase of this Fourth Turning will surely include another downward spiral in financial markets as un-payable debts accumulate to a tipping point level. When ATM machines stop spitting out twenties, food shelves are bare and gas stations are shuttered, social chaos will ensue. The government will react with further command and control measures. In V For Vendetta, the government creates a terrorist incident in order to gain unquestioned control over the population. Americans will need to be more vigilant than they have been over the last ten years in keeping an eye on their government.”

In light of what has happened in 2020 thus far, I’d say my fears have been realized, with more downside to come. I was deeply concerned about the surveillance state, on par with Orwell’s 1984, two years before Snowden made his revelations public. The country has been in a downward spiral since the government used the 9/11 fear and panic to ram through a 300-page pre-written piece of legislation to further take away our Constitutional rights and put vastly more power and control into the hands of uncontrolled psychopaths operating in the shadows of government halls.

Those in charge never let a crisis go to waste. 9/11 was used to pass the Patriot Act and initiate nineteen years of declared and undeclared wars in the Middle East to create chaos, empower Israel, and abscond with the oil of sovereign countries.

The 2008/2009 crisis, created by the Fed and their Wall Street banker proprietors, was used by the powers that be to abscond with trillions in national wealth, while further enslaving senior citizens in poverty and forcing the working middle class further into debt servitude. Bernanke, Yellen, Geithner and a myriad of other banker flunkies have been richly rewarded for their traitorous actions by their Wall Street brethren, with tens of millions in compensation for their duty and honor to the cabal.

The men who created the 2008/2009 global financial collapse through their mortgage fraud scheme, used fear and panic in the markets to force the feckless pathetic bought off congress apparatchiks to pass TARP and dozens of other ridiculous “bailout bankers” schemes to provide a façade of recovery. There was never a recovery. The unpayable debt was papered over with trillions more of unpayable debt, until something snapped in September 2019.

The first half of this twenty year, or so, Fourth Turning was ushered in by the 2008/2009 financial collapse and the subsequent disastrous solutions implemented by the ruling class in order to preserve their wealth, power and control. The taxpayer bailout of Wall Street should have been called NO BANKER LEFT BEHIND. The mind-boggling amount of debt issued over the last decade in order to rectify a problem created by issuing a previously mind-boggling amount of unpayable debt over the previous decade has become so large, the average person can’t comprehend the implications or consequences.

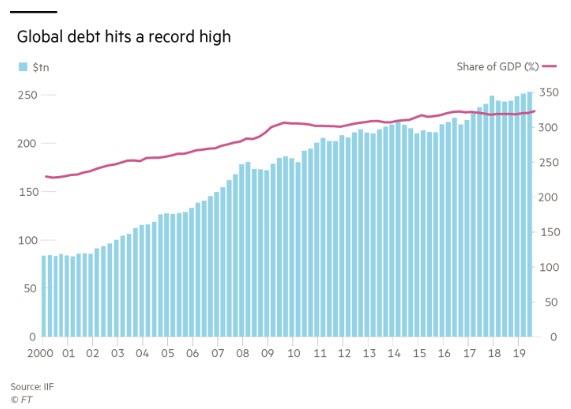

The masses have been indoctrinated through government schools and propagandized by the captured corporate media to such an extent, they have been convinced abnormality and pillaging by the ruling class are both normal and acceptable. The world added $90 trillion of debt between 2000 and 2008, over a 100% increase. Bernanke, Yellen, Powell and their other central bank co-conspirators said hold my beer and added another $90 trillion since the first debt created crisis. The Himalayan mountain of debt now stands at $253 trillion, or 322% of global GDP. Rogoff and Reinhart proved countries whose debt surpass 90% of GDP always proceed towards crisis and currency debasement.

Even John Maynard Keynes knew countries should run surpluses during good times, so they could run deficits during the bad times. Our glorious financial and political leaders seemed to have skipped that chapter in their economics textbooks. So, under the tutelage of Bernanke, Yellen, Powell, Bush, Obama, and Trump the country has added $12 trillion to the national debt, $3 trillion of corporate (junk) debt to buy back stock, a few trillion in credit card, auto, mortgage and student loan debt, all while the Fed was feeding the Wall Street parasites with zero interest rates and buying $4 trillion of their worthless assets (aka QE). This was all done while we were supposedly experiencing the longest economic boom in history and the stock market confirmed the boom by rising 400% to all-time highs in February of 2020. All’s well that ends well. Right?

It seems debt can’t buy happiness in the long run. This economy and stock market have been bugs in search of a windshield for a long time. Longer than I ever thought possible. But, as some bright financial minds have said, that which is unsustainable will not be sustained. The critical thinking financial people I trust knew something went screwy deep in the recesses of the opaque banking system sometime in September when the overnight repo rates soared to 10%.

I know 99.99% of Americans have no idea what an overnight repo is, let alone care about them. But Wall Street bankers and connected billionaire hedge fund managers cared, because Powell and his flunkies bailed them out every night from their bad trades and extreme risk taking. As we entered the fateful year of 2020, years of poisonous sludge was clogging the gears, and another financial collapse was imminent. What a fortuitous time for a global pandemic.

This is when things began to get interesting. There have been so many earth shattering events in the last two months it’s almost impossible to assess the current situation with any semblance of certitude. I believe I’m being lied to by virtually everyone. I know for a fact I’m being lied to by the Fed, Wall Street billionaire titans, the fake news media, corrupt politicians, the Chinese dictator, most people on social media and the blithering idiot talking heads on CNBC.

If almost everyone is lying, how can someone decipher the truth? The best way to untangle falsehood from truth is to follow the money. Just as the monied interests and Deep State didn’t let a crisis go to waste after 9/11 and the 2008/2009 Wall Street created collapse, they are again taking advantage of the distress and panic caused by the Chinese coronavirus to once again plunder the American public while assuring them it’s in their best interest.

“When the institutions of money rule the world, it is perhaps inevitable that the interests of money will take precedence over the interests of people. What we are experiencing might best be described as a case of money colonizing life. To accept this absurd distortion of human institutions and purpose should be considered nothing less than an act of collective, suicidal insanity.”

– David Korten

Collective suicidal insanity is the perfect description for what has happened in the last two weeks. There is no doubt the world is experiencing a health crisis not seen since the 1918 Spanish Flu pandemic. It is estimated 20 to 50 million people died during that pandemic, with approximately 600,000 succumbing in the U.S., or .57% of the population. A similar death rate from this pandemic would total 1.9 million people in the U.S.

As of today, there have been 140,000 confirmed cases and approximately 2,400 deaths. Over the coming weeks there will be hundreds of thousands more cases and thousands of additional deaths. That is a depressing and sorrowful fact. But the death count is going to be drastically lower than the 1918 total, during which the country continued to function and slog forward.

A judicious thinking individual might wonder why the Swine Flu epidemic of 2009, which is estimated to have infected 61 million Americans and killed 12,000 to 18,000, did not require a countrywide lockdown resulting in a second Great Depression. Maybe it was because the ruling class already had the ongoing financial crisis as their logic to use panic and fear in achieving their plundering objectives. Did anyone really notice we experienced a global pandemic in 2009?

Our very own CDC “experts” tell us the country has already experienced 38 to 54 million flu infections since October, with a half million hospitalizations, and at least 24,000 deaths, so why weren’t our hospitals overwhelmed? I know this is a serious virus, but the scare tactics being utilized by our overseers, corrupt politicians and their corporate media propaganda outlets is beyond excessive, and reveals a far more nefarious purpose.

Did we need to purposely create a global depression in order to defeat this virus? Will the benefits outweigh the cost? Is this health crisis being used by the monied interest swine to again gorge themselves at the taxpayer trough, robbing the public, while persuading them it’s for their advantage? The “conspiracy theorists” among us, who have been proven correct time after time over the last decade, know the answers to these questions. This is a controlled demolition by the powers that be as cover for their fraud, criminal schemes, and looting of the national treasure.

“To rob the public, we must first deceive it. The trick consists in persuading the public that the theft is for its advantage; and by this means inducing it to accept, in exchange for its property, services which are fictitious, and often worse.”

– Frederic Bastiat

Only in a suicide cult, which our country has become, would the majority support and cheer for a corporate lobbyist written $2.2 trillion 873-page windfall to bankers, connected mega-corporations, and every special interest imaginable. This doesn’t even account for the $4 trillion of secret payoffs and behind the scenes shenanigans of the Federal Reserve, as they do their part to support their banker owners once again. And just to make sure none of their despicable acts will see the light of day, the ruling class slipped in little clause titled:

SEC. 4009. TEMPORARY GOVERNMENT IN THE SUNSHINE ACT RELIEF.

The provision authorizes the Federal Reserve Board and other such officials to meet in secret without any oversight constraints. Who needs transparency from the privately owned organization who controls our currency, interest rates, banking regulation and is most responsible for the third financial collapse in the last two decades? And why should we worry that Goldman alum Mnuchin was given a $500 billion slush fund to use as he wishes? I’m sure he’s going to use it to help the local restaurant owner down the block.

I’m outraged we’ve let this happen again. All they needed to do was crash the stock market by 32% in a few weeks, while having their propaganda machine media predicting millions of deaths, and scaring the nation into shuttering our entire economy. The oppressors once again have succeeded in convincing us they know best and are working for our best interests.

We’ve shirked responsibility for our own lives by believing the very same people who didn’t see the crisis coming, weren’t prepared, and have failed miserably to centrally control the situation. We’ve given them the power over our lives and we are being led towards the slaughterhouse. It was our choice. We let fear overcome reason and courage.

“Since mankind’s dawn, a handful of oppressors have accepted the responsibility over our lives that we should have accepted for ourselves. By doing so, they took our power. By doing nothing, we gave it away. We’ve seen where their way leads, through camps and wars, towards the slaughterhouse.”

– Alan Moore, V for Vendetta

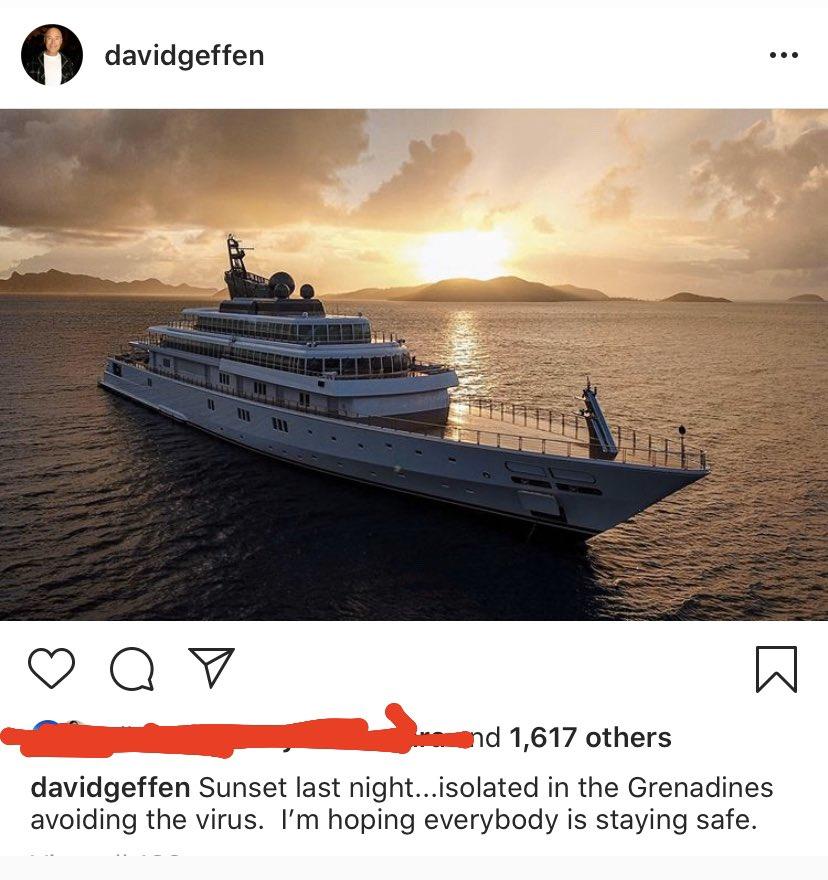

The egotism and hubris of the ruling class has no limits, as they quarantine themselves in one of their six mansions or on one of their yachts, eating caviar and drinking champagne, paying their lobbyists to ensure they get a big hunk of the $2.2 trillion stimulus pie, while the average Joe and Jane get a couple thousand bucks to pay one month’s rent and buy some ramen noodles to sustain themselves through the coming military lockdown.

Don’t look now but you’ve been screwed again. The Wall Street bankers are again able to borrow at 0%, while charging you 17% on your ever-increasing credit card balance. Why aren’t these scumbag bankers announcing a three-month moratorium on credit card and mortgage payments, with no interest accruing? Because their goal is to further enslave you in debt, while enriching themselves. They will run patriotic commercials, while sticking a red white and blue dildo up your ass.

In Part Two of this article I will examine the parallels between our current situation and the favorite anarchist/libertarian film V for Vendetta. I address both the disturbing aspects and the hopeful aspects of the film in relation to what the future holds.

{kind=link}

{kind=link}